Abstract

Taxation is a fundamental source of revenue for governments. However, globally tax revenue performance has continuously been poor. This has been attributed largely to poor tax compliance behaviour. Theoretical arguments from Pecking Order Theory (POT) and the Extended Parallel Process Model (EPPM) suggest that financial constraints and tax risk assessment could explain the dynamics of tax compliance. Motivated by these grounds, this paper seeks to explore the extent to which prior research efforts have been directed toward tax risk assessment, financial constraints and tax compliance. This paper employs bibliometric analytical procedures to interrogate the existing empirical literature from 1981 to 2022. This paper uses the Scopus database to conduct the bibliometric analysis using “bibliometrix” package. It was evident through the analyses that emerging studies have explored these variables: tax risk assessment, financial constraints and tax compliance. However, joint search criteria were introduced; it was found that the empirical literature has largely not considered the interconnectedness of these variables. When two variables mapping search criteria were used, it was observed that apart from financial constraints and tax compliance, these variables have virtually not been investigated. Given these empirical gaps coupled with the theoretical justification of the connectedness of these variables, it is recommended that future studies should extend the literature to contribute to filling the gap. Evidence of such analyses could also shape tax policy and practice and therefore government and tax authorities should sponsor studies in this area.

1. Introduction

Globally, the principal source of government revenue comes from taxation. It is through taxes that almost all governments are able to finance their activities, implement policies and support projects that otherwise are only provided by the state (Seidu et al., Citation2021). Effective tax compliance by individuals and corporations is the panacea to boost proper functioning government (Imam & Jacobs, Citation2014; Lee & Yoon, Citation2020; Litina & Palivos, Citation2016). Failure on the part of corporations and taxable people to comply with taxes could destabilise government and economy (Hanlon et al., Citation2007). Tax non-compliance could lead to a reduction in tax revenue, an increase in unemployment due to inadequate provision of jobs and a complete scramble in government operations (Carsamer, & Abbam, Citation2020; Hanlon & Heitzman, Citation2010). Across the globe, tax authorities' attempts to meet their tax revenue targets have not been successful. Even though developed countries have a better tax compliance tax-to-gross domestic product (GDP) ratio, no country has been able to cross 50% tax-to-GDP mark (Seidu et al., Citation2021). This tax revenue mobilisation challenge affects all economies (i.e. developed and developing).

New OECD data in the Annual Revenue Statistics (2021) reveal that, on average, tax revenue as a percentage to GDP has increased by 0.1% to 33.5% in 2020 from 2019. Even though there is a small increase from the prior year, it is inadequate and fell short of expectations. In Europe, Denmark with the highest tax-to-GDP ratio mobilised 46.5% in 2020. It is important to acknowledge that with the exceptions of 2017 and 2018, in which France was higher, Denmark had the highest tax-to-GDP ratio among the OECD countries since 2002. France had the second highest tax-to-GDP ratio in 2020 (45.4%). Mexico had the lowest tax-to-GDP ratio (17.9%) in Europe. Of the 36 OECD countries for which data for 2020 are available, the ratio of tax revenues to GDP compared to 2019 rose in 2020 and fell in 2016. In Africa, the average tax-to-GDP ratio for 30 countries increased by 1.8% to 16.6% in 2019 from 14.8% in 2018.

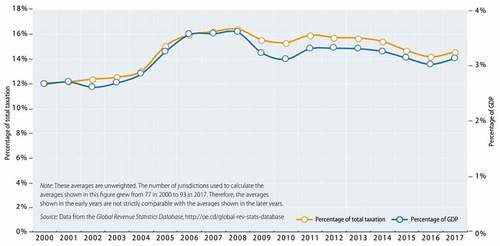

Tax revenues could originate from several sources such as corporate tax, personal income tax, social security contribution, value added tax, and others. Corporate tax revenue is a vital source and forms an important share of the overall tax revenues of many economies. Corporate revenue performance may predict tax compliance from other elements as poor corporate tax compliance may suggest firms may also not declare the right to withhold taxes. This makes corporate tax revenue an important path for tax compliance. OECD Corporate Tax Statistics () reports that there was a minor upsurge in both the average corporate income tax revenues as a share of GDP and as a share of total tax revenues between 2000 and 2018 across 105 countries. Figure indicates that average corporate income tax revenues as a share of GDP surged from 2.7% in 2000 to 3.2% in 2018 and average corporate tax revenues as a percentage of total tax revenues went up from 12.3% in 2000 to 15.3% in 2018.

Figure 1. Average Corporate Tax Revenue Performance.

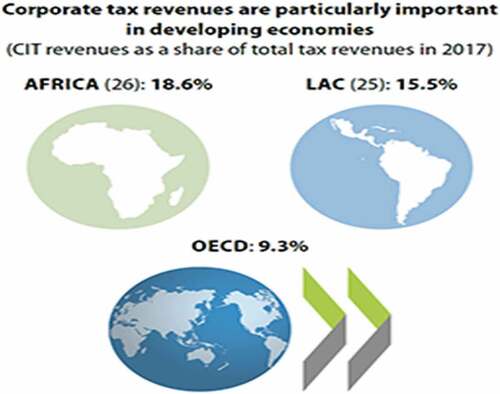

Corporate tax revenues are predominantly vital in developing countries. For instance, as exhibited in Figure , data from Corporate Tax Statistics (2021) show that CIT revenues as a percentage of total tax revenues in 2018 were 19.2% for Africa, 15.6% for Latin America and the Caribbean (LAC) and 10.0% for the OECD.

Figure 2. CIT Analysis.

These analyses show that corporate income tax revenue though important especially for developing economies, it is still low as compared to other forms of tax revenues. Whilst corporate income tax revenue forms as high as 19.2% for Africa and 10.0% for OECD, there is high corporate tax non-compliance. Corporate tax non-compliance is believed to premise on two main grounds: tax risk assessment and financial constraints.

Tax and revenue authorities worldwide have established that the assessment of tax risks by corporate organisations plays an important role in tax compliance (Lavermicocca, Citation2011). In spite of countries’ diverse regulatory and business environments, generally, it is understood that an effective tax risk assessment is central to both revenue authorities and corporate taxpayers (Amanamah, Citation2016; Devos, Citation2014; Dowling, Citation2014; Hapsoro & Suryanto, Citation2017; Keen, Citation2013; Liapis et al., Citation2013; Nechaev & Antipina, Citation2016; Ogbonna & Appah, Citation2016). Revenue authorities have to deal with more complex tax risks due to globalisation and sophisticated financial markets. In Africa and other developing economies, tax risk assessment has taken the central stage due to double-edged situations where governments need to simultaneously strengthen fiscal power through taxation and offer tax privileges and concessions for new and prospective businesses.

Tax risk burdens make corporate businesses more vulnerable to failure. In a healthy and highly competitive business environment, tax risk burdens become the key problem and a common factor for bankruptcy in a short period. Even when the tax burden is optimal, inappropriate responses to tax risks and early warning signals of existing risks could cause corporate organisations not to be tax compliant (Cai et al., Citation2015; Lavermicocca, Citation2011). Therefore, an improved tax compliance requires an understanding of the tax risk dynamics. In addition to tax risk, financial constraint has also been identified as an antecedent for tax compliance of both large and small corporate businesses (Seidu et al., Citation2021). Corporate businesses' inability to comply with tax obligation could partly be due to financial constraints resulting from solvency and liquidity. Financial constraints can be likened to a two-edged sword: damning to the business operations and detrimental to government tax revenue (Agyei & Yankey, Citation2019; Seidu et al., Citation2021).

It has been argued that when corporate organisations are beleaguered with financial constraints, there is a probability to maximise operating financial capacities through practical firm-level management including tax planning (Kinda, Citation2018; Seidu et al., Citation2021; Yorke et al., Citation2016). Firm is financially constrained when it faces a high cost of accessing external financing or an increasing challenge in obtaining the required levels of external funds (Haselip et al., Citation2015; Olaleye, Citation2016; Seidu et al., Citation2021). Constraint is also evident when a firm is unable to fund all lucrative investment opportunities or a firm is financially afflicted and cannot fund cover for short-term working cash flow obligations. It is believed that financial constraints lead firms to an increasing propensity to engage in tax noncompliance.

The critical role of tax risk and financial constraints in explaining tax compliance dynamics is also grounded in theories such as extended parallel process model and pecking order theory. Extended parallel process model (EPPM) is one of the fundamental theories underpinning the tax compliance. This framework was developed by Witte et al. (Citation1994). The extended parallel process model establishes a relationship between tax risk, financial constraints and tax compliance. This extended parallel process theory opines that an individual, firm-level or management decision is influenced by the risk profile through the analysis of the likelihood of occurrence and the severe of the consequence of occurrence. This framework attempts to predict how individuals and firms react when confronted with fear-inducing stimuli. “Messages which are fear appealing have been effective in behavioural change since they draw attention to the risk(s) a person faces for performing or not performing a particular action” (Murray-Johnson et al., Citation2004). The outcome of a corporate assessment of tax risk could determine the nature and extent of tax compliance, an assertion that is deeply rooted in the EPPM.

According to the proponents of EPPM, when firms assess their risk severity profile and realise that the risk is high and the probability of occurrence is also high, it generates fear among management and could cause management to take a decision out of danger control in line with the severity profile. Relatedly, when tax risks and sanctions are viewed as highly punitive and the probability of such sanctions is not remote, tax compliance may be high. Similarly, when tax risks and sanctions are viewed as not punitive enough and the probability of such sanctions is too remote, tax compliance may be weak. Moreover, following the assumptions of EPPM, when firms are experiencing financial constraints either liquidity or solvency, this may be fear evoking and may cause management to take swift action including engaging in aggressive tax planning (Kinda, Citation2018; Yorke et al., Citation2016). The response to financial constraints may primarily be to generate and use more internal source of funding including minimising cash flow (Ghazouani, Citation2013; Serrasqueiro & Caetano, Citation2015) such as tax payments. This argument is also supported by the pecking order theory (POT; Myers, Citation1984; Queku, Citation2018; Seidu et al., Citation2021). This may be more pronounced especially firms in the financial sector such as banks.

Given these theoretical insights coupled with the struggle to contain weaknesses in tax revenue performance, it is important to determine the extent of empirical understanding of these dynamics and their interplay. Although some studies have reported a dearth of the literature in this area (Agyei & Yankey, Citation2019; Edward et al., Citation2016; Seidu et al., Citation2021) such conclusions become comprehensive when centered on a thorough analysis and interrogation of the existing literature that is virtually absent. This paper seeks to explore the extent of empirical studies and current development in tax risk, financial constraints and tax compliance literature. This is considered as the foundational study that has concurrently interrogated these related constructs.

Over the years, scholars have traditionally employed two methods in determining the extent of studies and current development: the qualitative approach (structured literature review) and the quantitative approach (meta-analysis; Schmidt et al., Citation2008; Zupic & Carter, Citation2015). This paper, however, follows an emerging approach popularised as science mapping. Science mapping uses bibliometric methods to examine how disciplines, fields, specialties, and individual papers are related to one another (Zupic et al., 2015). Unlike the manual searches, which lean credence to prejudice by the researcher and most of the time lack rigor (Tranfield et al., Citation2003; Zupic et al., 2015), science mapping follows a system-based literature review. This makes the choice of science mapping more suitable and appropriate. Nevertheless, since not all databases support the system-based review, an integrated approach (manual and science mapping) would be followed.

Even though bibliometric analysis is not new (cf., Kessler, Citation1963; Small, Citation1973), it only started to attract widespread attention with the proliferation of easily accessible online databases with citation data (e.g., Thomson Reuters Web of Science [WOS] and Scopus). The method is mainly used in the field of sciences. However, it is getting much attention, with evidence emerging in the other fields such as strategic management (Nerur et al., Citation2008; Ramos‐Rodríguez & Ruíz‐Navarro, Citation2004; Di Stefano et al., Citation2010), entrepreneurship (Gartner et al., Citation2006; Landstro ̈m, Harirchi, & A ° stro ̈m, 2012; Schildt et al., Citation2006), innovation (Fagerberg et al., Citation2012), and others. Some research fields (innovation, entrepreneurship and strategy) have more rapidly embraced bibliometric analysis, while others such as accounting have been slower.

This paper makes fundamental contributions to the literature. Firstly, the paper complements the efforts of extending the science mapping approach to review studies in accounting (taxation). Following this approach would not only provide a window to address the main issue of consideration: empirical diversity and current development in the literature of tax risk assessment, financial constraints, and tax compliance, it would also contribute to extending science mapping approach to the accounting (tax) literature. Secondly, the theoretical assumptions from extended parallel process model and pecking order theory and some empirical assertions suggest possible link among tax risk, financial constraints and tax compliance (Kinda, Citation2018; Murray-Johnson et al., Citation2004; Queku, Citation2018; Seidu et al., Citation2021; Yorke et al., Citation2016). This study seeks to explore the integrated empirical evidence of these theoretical relationships through a systematic review.

Thirdly, although there has been growing interest and studies on tax compliance, less has been documented in aggregating and integrating the empirical findings of these studies. This paper seeks to complement prior research efforts by comprehensively consolidating the depth of existing evidence on the subject and determining the trend, current development and the aspects of these relationships, which have been explored over time. Finally, the evidence from this review would also reveal further propositions about the interconnectedness of tax risk assessment, financial constraints and tax compliance for further empirical analyses.

2. Literature selection criteria and analytical framework

This paper relies on Google Scholar, General Google Search and Scopus database for the literature selection and review. Google Scholar and Google search are fundamental search engines for search validation, and they are connected to almost all databases including Web of Science and Scopus (Aiello, Citation2022). Therefore, search results from these search engines could be conclusive (Seidu et al., Citation2022). The challenge with Google Scholar and Google search is that they currently do not support Biblioshiny” function in the “bibliometrix” package. Therefore, the paper conducted a search on the subjects of review on Google Scholar and the main Google search engine manually. Although the search generated several studies on tax compliance, constraints and tax risk, there was virtually no study connecting these constructs (see, Altman et al., Citation2017; Beck & Lisowsky, Citation2014; Chen et al., Citation2010; Dan, &Tran , Citation2021; Dyreng et al., Citation2008; Eberhartinger & Zieser, Citation2021; Rego & Wilson, Citation2012; Richardson et al., Citation2015; Seidu et al., Citation2021). The keywords in those studies include bankruptcy, financial distress, risk, risk management in tax, tax aggressiveness, tax avoidance, tax compliance, tax evasion and tax uncertainty (Altman et al., Citation2017; Beck & Lisowsky, Citation2014; Chen et al., Citation2010; Dyreng et al., Citation2008; Eberhartinger & Zieser, Citation2021; Rego & Wilson, Citation2012; Richardson et al., Citation2015).

The paper followed these baseline results to conduct further analyses using the “Biblioshiny” function in the “bibliometrix” package. This study uses the Scopus database as the source for material collection for the bibliometric analysis. The Scopus database is selected for its reputation as the “major single abstract and indexing database ever built” (Adamu et al., Citation2021) and for its integration and consistency with the “bibliometrix” package. It has more than 50,000 records of published and proceeding journals, books, conference papers and others. To retrieve the relevant articles from the Scopus database, a combination of three sets of keywords with the logic term “OR” is employed. The set includes tax risk assessment, financial constraints and tax compliance keywords. The search for combinations of keywords was conducted in the following fields: article title, abstract and keywords. The search used was as follows: TITLE-ABS-KEY (((((“tax risk assessment” OR ”financial constraints” OR ”tax compliance”))))).

The initial search yields 8,684 document results. These documents were filtered by the following conditions: title-abs-key (((((“tax risk assessment” or ”financial constraints” or ”tax

compliance”))))) and (limit to (language, ”english”)) and (limit-to (oa, ”all”)) and (limit-to (doctype, ”ar”)) and (limitto (subjarea, ”econ”) or limitto (subjarea, ”busi”)) and (exclude (language, ”portuguese”)) and (exclude (srctype, ”k”)) and (limit to (pubstage, ”final”)).

Articles with no bearing on two of the keywords are excluded.

Surveys and review works are not included.

Only articles in the English Language are included.

Article in Press and are not included

All Open Access documents and final stage publications are included

The remaining documents were manually reviewed and the final set of dataset consists of 1002 papers. After reviewing the 1002 papers at first glance, it shows the majority of the papers relate to financial constraints and tax compliance and only 15 papers in the dataset cover tax risk assessment: financial constraints (Aiello, Citation2022; Du & Nguyen, Citation2022; De Guevara et al., Citation2022; Hai et al., Citation2022; Ma & Hao, Citation2022; Malika et al., Citation2022; Nicolas, Citation2022; Zhang & Lucey, Citation2022), tax compliance (Bellon et al., Citation2022; Delgado-Rodríguez & Lucas-Santos, Citation2022; Kasper & Alm, Citation2022; Morrow et al., Citation2022; Sunardi et al., Citation2022) and tax risk assessment (Chyz et al., Citation2021). This shows that concepts such as financial constraints and tax compliance dominate research fields and fewer tax risk assessment literature exist.

3. Bibliometric analysis

Bibliometrics is the use of quantitative tools to study science (Kaffash et al., Citation2021; Pritchard, Citation1969). Many fields in the literature have employed the use of bibliometric analysis (Kaffash et al., Citation2021). In the past years, a sizeable number of indicators and tools have been developed to analyse and measure the research performance and contribution of journals, authors, institutions, states and countries. Bibliometric analysis is employed to monitor scientific contributions and visualise scientific knowledge from the context of concept, intellect and social structures (Seidu et al., Citation2022). In this study, bibliometric analysis is used with the help of “Biblioshiny” function in the “bibliometrix” package (Aria et al., Citation2017; Kaffash et al., Citation2021).

This paper contributes to the literature by providing a comprehensive bibliometric analysis of published papers in the field of tax risk assessment, financial constraints and tax compliance. This dataset consists of 1002 papers in journal articles. Table illustrates the main information about the dataset. Like Gautam (Citation2017) and Kaffash et al. (Citation2021), the study uses two measures: Publication numbers and Average citations per year to show the research performance in the study. Details of the dataset are reported in Table .

Table 1. Main information about the dataset

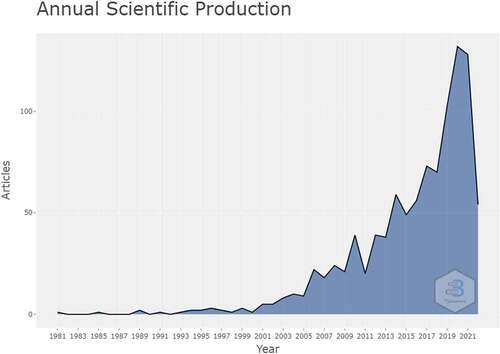

The number of documents in the literature indicates the level of research output. The annual growth rate of the number of publications is one relevant measure. Figure shows the annual growth rate of papers published from the period 1981 to May 2022. It is evident that there is an increase in documents published beginning from 2014. This indicates a sharp rise in research publications for tax risk assessment, financial constraints and tax compliance. It is instructive to note that this figure is obtained with 7 months left in 2022.

Figure 3. Annual growth rate.

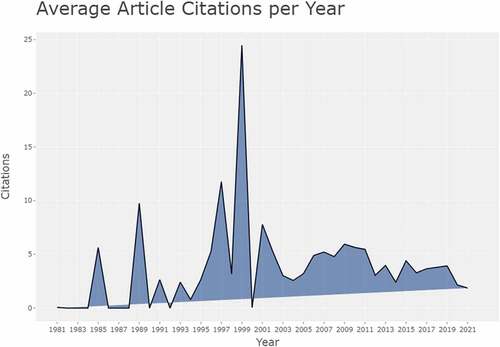

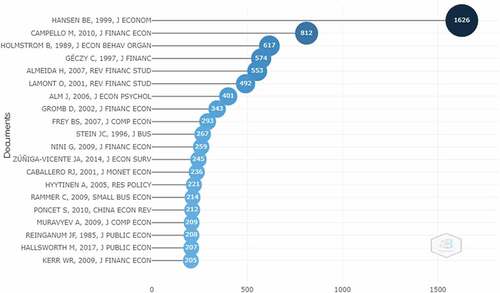

The average citation per year within the study frame is also captured in Figure . This measures the influence of documents published. It can be seen that average number of citation per year peaked at 1999 with 1626 citations followed by 2010 and 1989 with 812 and 617 citations, respectively. The peak in 1999 is the result of one highly cited paper. The paper, “Threshold effects in non-dynamic panels: Estimation, testing, and inference” by Hansen (Citation1999) discusses whether financial constraints affect investment decisions using data from 565 US firms. This was the most frequently cited paper in the dataset. In 2010, “The real effects of financial constraints: Evidence from a financial crisis” by Campello et al. (Citation2010) became the dominant paper. This paper discusses whether corporate spending plans differ conditionally on survey-based measure of financial constraints. The result indicates that financial constrained firms planned deeper cuts in tech spending, employment and capital spending. In 1989, a publication “Agency cost and innovation” by Holmstrom (Citation1989) attracted 617 citations from scholars. Finally, a paper “why firms use derivatives” by Geczy, Minton and Schrand received 574 citations. Together, the four published articles were cited 3629 times by scholars in the field.

Figure 4. Average citation per year.

The first paper to be published in the literature from the dataset was in 1985. Reinganum and Wilde (Citation1985) published the paper “Income tax compliance in a principal-agent framework” in the Journal of Public Economics: ScienceDirect. The paper modeled income tax evasion as a “portfolio problem” deriving the optimal consumption of the “risky asset” assuming a fixed probability of detection. The study finds that random audit rules are weakly dominated by audit cutoff rules.

3.1. Top relevant sources, authors and highly cited works

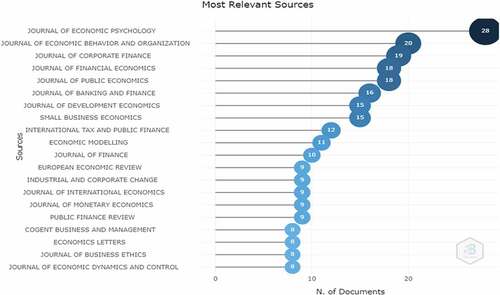

This section focuses on the most relevant authors, sources and largely cited papers. On a whole, 1002 articles from various journals form the dataset for the analysis. These published papers appeared in 411 different sources. Figure shows the distribution of the top 20 most relevant sources. As evident, the Journal of Economic Psychology is ranked first with 28 papers, and second place occupied by the Journal of Economic Behaviour and Organisation with 20 papers.

Figure 5. Most relevant sources.

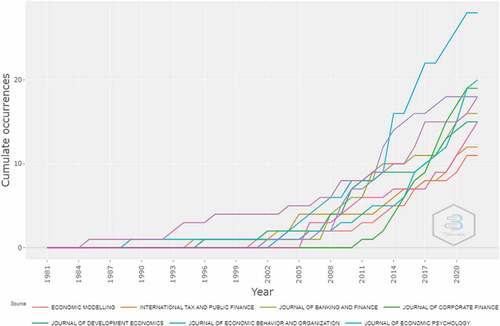

Further analysis was conducted on the contribution of the top 10 ten sources over the period of 1981 to 2022. The results are captured in Figure . It reveals the top 10 sources with the highest number of documents published and the pattern of growth of publishing more papers over time. The graph depicts that after 2011, there is an upswing in the number of published articles in the Journal of Economic Psychology.

Figure 6. Contribution of the top ten sources 1981–2022.

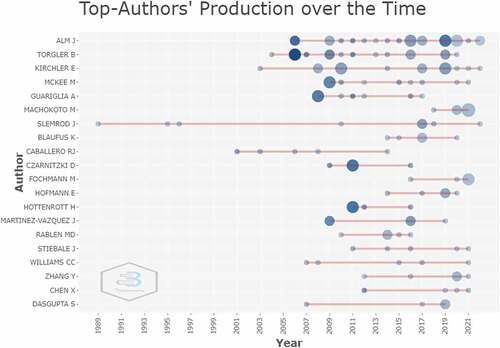

The paper also analysed the most relevant authors and their respective annual outputs over the years in the study span. Figure presents the results of the analyses. From Figure , Alm Justice and Torgler Burn are the two leading authors with the highest period of contribution to the field.

Figure 7. Most relevant authors and production over the years.

Figure reports the analysis of the most cited articles, over the period of 1981 to 2022. The topmost paper cited is the “Threshold effects in non-dynamic panels: Estimation, testing and inference” by Hansen (Citation1999) with average citation being 67.75 per year.

Figure 8. Most cited articles.

3.2. Keyword analysis

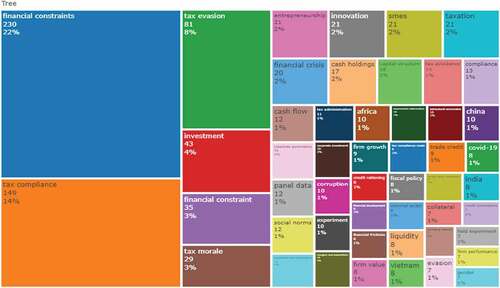

Analysis of keywords in these selected papers, and the tree mapping also showed relevant evidence as reported in Figure . Figure illustrates the Treemap of the top 50 authors’ keywords. The map reveals that the keyword financial constraints are the most frequently appearing keywords. Overall, this keyword appeared 230 times in the dataset. The second and third keywords frequently used by scholars are tax compliance and tax evasion.

Figure 9. Treemap of top 50 authors’ keywords.

3.3. Conceptual, intellectual and social structure

This section of the paper presents an analysis of science mapping, which is employed to map three different aspects of scientific knowledge: conceptual structure, intellectual structure and social structure. Science mapping helps to reveal the hidden patterns of these structures. Conceptual structure illustrates what science talks about and the main theme and trends, whereas intellectual structure maps the way authors’ work impacts a particular scientific community (Kaffash et al., Citation2021). The social structure discloses how authors, institutions and countries interact with each other. The results of this analysis are depicted in Figure . Figure shows a total picture of the evolution of topics in tax risk assessment, financial constraints and tax compliance from 1981 to 2022.

Figure 10. Thematic evolution of authors’ keywords.

For the period 1981 to 2022, “tax compliance” keyword started as a unique theme. This is divided into various branches: “tax morale,” “tax evasion,” “social norms,” entrepreneurship” and “taxation.” In the next time slice (1997), they merge into “financial constraints.” Considering the keywords “financial constraints” and “tax compliance,” it is not surprising that these keywords have become major topics from 2010 onwards. The keyword “tax compliance” keeps featuring in authors’ publications into the next slice, indicating that more recent research studies are not only interested in tax compliance and financial constraints but also other aspects of taxations such as tax morale, tax evasion and tax avoidance. For the time slice 2017–2022, the thematic map reveals “financial constraints” and “tax compliance” as the two main topics that have taken the center stage of scholars’ output.

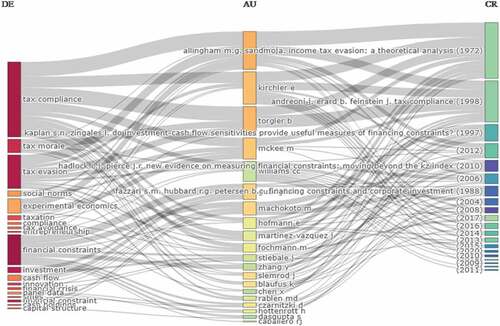

Figure presents the historic direct citation network for the top 20 authors. The network uncovers the first most important articles on the topic of research and track the historical development of core authors and papers. The direction of arrows illustrates the persistent change of research learning for the first top 20 papers. For example, it reveals that Erel et al. (Citation2015), the first author of the article “Do acquisitions relieve target firms’ financial constraints?” has cited two out of the 20 most often cited articles in the dataset (Gromb & Vayanos, Citation2018; De Neve et al., Citation2021). After reviewing the title of the 20 papers, it is observed that all these papers are focused on financial constraints and tax compliance.

Figure 11. Historic direct citation network for the top 20 authors.

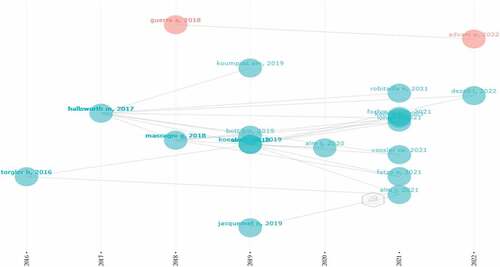

To comprehend how countries, institutions and authors researching tax risk assessment, financial constraints and tax compliance are linked and connected, an assessment of international collaboration based on co-authorship is carried out with the results in Figures . In total, there were 95 pairs of country collaboration. From Figure , the thickness of the link between countries indicates the level of collaboration (co-authorship). The figure shows that the link of international research collaboration between the USA and the United Kingdom is relatively higher compared to other countries. Figure backs this by showing a thicker link between these two countries. According to each country’s contribution, the United Kingdom, USA, South Africa and China are the leading countries with 385, 287, 40 and 34 publications out of 1002 papers.

Figure 12. Country collaboration.

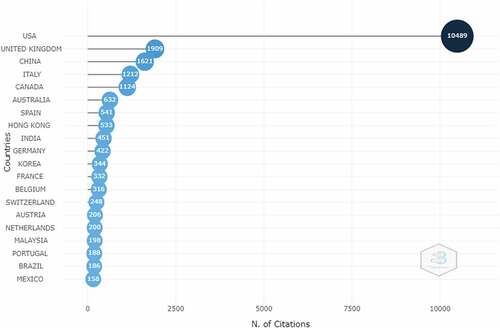

Figure 13. Most cited countries.

In Figure , it is interesting to note that the finding shows that the USA, the United Kingdom, China, Italy and Canada are the first five countries to have the highest total citations of papers. For the U.S.-published papers, American scholars have been cited 10,489 times in the literature. The United Kingdom, China, Italy and Canada have 1909, 1621, 1212 and 1124 citations, respectively.

4. Top relevant application of tax risk assessment, financial constraints and tax compliance

This section evaluates the most significant applications of financial constraints, tax risk assessment and tax compliance. Authors, year of publication, title of paper, contribution, and direction of further studies. The literature is well-off when it comes to financial constraints and tax compliance. The two “financial constraints” and “tax compliance” appear in the titles of 414 out of 1002 journal articles from the dataset. Another word that is dominant in the literature that has attracted scholars’ attention is “tax evasion” and “investment.” In the section below, a review of the most frequently cited papers in the literature is carried out for each application.

4.1. Financial constraints

Financial constraints have been a predicament for the smooth running of businesses across the world. Due to the critical role it plays in the going-concern of entities both public and private, it has become an attractive topic for many researchers in the fields of finance, accounting, economics, public sector, investment, private sector, financial institutions and banking sectors. Financial constraint is one of the antecedents of tax compliance (Seidu et al., Citation2021). Financial constraint may relate either to solvency or liquidity or both. Regardless of the nature or the cause of the financial constraint, a firm could suffer from bankruptcy or complete collapse when faced with such constraints and the rippling effect of tax compliance could not be overstated. Having many of the research being conducted in the subject of finance, accounting and taxation related to modelling and proposing relationships among the variables, scholars use different analytical methods and models to address financial constraints and tax compliance dynamics.

There are some review papers in the literature that specifically relate to financial constraints. Holmstrom (Citation1989) reviews agency cost and innovation and its association with financial constraints on small and large firms. Our findings show that optimal organisational responses to coordination and control could lead to bureaucratisation within the firm and to financial constraints by capital markets, both of which may be unfriendly to innovation. Hansen (Citation1999) explores threshold effects on non-dynamic panels: estimation, testing, and inference. Recently, Campello et al. (Citation2010) review the real effects of financial constraints from a financial crisis perspective. This sub-section further reviews some highly cited articles.

Erel et al. (Citation2014) explore if acquisitions relieve target firms’ financial constraints. They used a large sample of European acquisitions to test the level of cash that target firms hold, the sensitivity of cash and investments to cash flow. The finding suggests that acquisitions relieve financial frictions in target firms when the target firm is small. Li and Zhang (Citation2021) examine the relationship between disclosure policy and investment due to changes in regulation. The finding reveals a stronger association for ex ante financially constrained firms and firms with difficulty in accessing the debt market.

4.2. Tax compliance

Tax compliance is defined as the extent to which a person and/or a firm comply with tax regulations and laws (Musimenta et al., Citation2019; Young et al., Citation2016). Following this, Reinganum and Wilde (Citation1985) argue that the existing system of income tax is based on the principle of voluntary compliance as individual taxpayers choose to declare their incomes, but this might not necessarily reflect their true income. Erard and Feinstein (Citation1994) came through with a different route in examining moral elements in tax compliance. They discovered shame and guilt in the utility of individual taxpayers and hypothesised that individual taxpayers will feel guilty and shameful if they under-reported taxable income and are subsequently caught for non-tax-compliance. Andreoni (Citation1998) states that the economics of tax compliance can be viewed in light of certain factors, either separately or in combination, including problems of public finance, organization structure, enforcement of laws and regulations, supply of labour and ethics. Understanding tax compliance amid financial constraints and tax risk assessment can help improve liquidity buffers for organisations. Several studies in the literature examine tax compliance from various perspectives.

Reinganum and Wilde (Citation1985) review income tax compliance in a principal–agent framework. The study focused on audit cut-off policy. It finds that audit cut-off rules are the least cost policies, which induce truthful income reporting. De Neve et al. (Citation2021) review tax compliance from the perspective of simplification, deterrence and tax morale. They ran four natural fields of experiments varying the communication of the tax administration with income taxpayers in Belgium throughout the tax process. They find that simplification is far more cost-effective, making room for savings on enforcement costs.

5. Tax risk assessment, financial constraints and tax compliance: analysis of interconnectedness

Having explored the studies emanating from these individual variables of interest, the paper further analyzes their joint investigation in the empirical literature. When the three variables are jointly explored, the search yielded no output. The paper therefore revised the search criteria into two variables mapping as follows:

5.1. Financial constraints and tax compliance

Literature linking financial constraints to tax compliance was very few. The study used the search: TITLE-ABS-KEY (((“financial constraints”) AND (“tax compliance”))) to explore the prior studies on financial constraints and tax compliance from Scopus database. The search yields a total output of four papers (Alasfour et al., Citation2016; Engida & Baisa, Citation2014; Palil & Mustapha, Citation2011; Yu & Fang, Citation2022). The paper by Alasfour et al. (Citation2016) is the most cited paper with 25 citations, followed by Engida and Baisa (Citation2014) with 11 citations and Palil and Mustapha (Citation2011) with 10 citations. These analyses have been summarised in Table .

Table 2. Search Results on Financial Constraints and Tax Compliance

A critical consideration of the search results and their output titles shows that although the two terms appeared in keywords, the joint investigation is virtually absent. Thus, prior studies have largely not interrogated the connectedness between financial constraints and tax compliance. Given the fact that financial constraints could limit firms’ financial capacity to honour their tax obligations, it is a useful research area for future studies. Extending the literature in this area would not only contribute to theory but could also shape policy and practice of taxation.

5.2. Tax risk assessment and financial constraints

Based on the Scopus database, literature on tax risk assessment and financial constraints was also explored using the search: TITLE-ABS-KEY (((“financial constraints”) AND (“tax risk assessment”))). This search yielded no output. This suggests that the area is a fertile ground for future studies.

5.3. Tax risk assessment and tax compliance

Attempts to draw prior studies on tax risk assessment and tax compliance using search: TITLE-ABS-KEY (“tax risk assessment” AND ”tax compliance”) returned an output of one document. The paper by Ovcharova, Tasalov and Osina (Citation2019) “Tax compliance in the Russian Federation, the United Kingdom of Great Britain and Northern Ireland, and the United States of America: Forcing and encouraging lawful conduct of taxpayers” has been cited twice. This paper was published in the Russian Law Journal.

6. Research gaps and directions for future studies

This paper emphasises the need for some future empirical studies in the field of taxation and emerging antecedents of tax risk and financial constraint. Firstly, it is of great importance for the current literature on taxation to be extended to integrate the dynamics of financial constraints at both firm and individual taxpayers’ level. Payment of tax is based on the strength of taxpayers’ cash flow and therefore those experiencing or likely to experience financial constraints are likely to alter their tax compliance behaviour. Although this assertion is grounded in theory, empirical studies to shape our understanding are virtually absent, as evident in both the manual review and the bibliometric analysis. This could undermine the comprehensiveness of interventions to address tax compliance challenges globally. It is therefore recommended that future studies on antecedents of tax compliance should explore the dynamics of firm level financial constraints and corporate tax compliance.

Secondly, as evident in this paper, there is a scarcity of literature on how tax risk assessment affects tax compliance behaviour. Researchers could build on the assumptions of the Extended Parallel Process Model (EPPM) to focus and direct their future empirical studies to fill this gap. Evidence from such an investigation would not only contribute to the theory but also provide a framework to evaluate tax payers’ risk profile and the implication on tax compliance behaviour.

This further study is critical as tax risk becomes more complex with the ascendency of globalisation and integration.

Thirdly, following the assumptions of EPPM and POT, even a risk-aversed firm may still be exploring avenues to outwit the tax system when it is financially constrained. This suggests that financial constraints could moderate the tax risk-tax compliance nexus. Surprisingly, there is a paucity of empirical evidence to corroborate with these theoretical postulations. Future studies could focus on these dynamics.

7. Conclusion and implication

This paper conducted manual and bibliometric analyses on tax risk assessment, financial constraints and tax compliance. The paper was conceived on the fact that although tax revenue is a fundamental source of revenue for governments, globally tax revenue performance has continuously been poor. This has been attributed largely to poor tax compliance behaviour. Theoretical arguments from Pecking Order Theory (POT) and Extended Parallel Process Model (EPPM) suggest that financial constraints and tax risk assessment could explain the dynamics of tax compliance. Motivated by these grounds, this paper seeks to explore the extent to which prior research efforts have investigated the interconnectedness of tax risk assessment, financial constraints and tax compliance

The paper relied on Google Scholar, general Google search and Scopus database for the literature selection and review. Google Scholar and Google search are fundamental search engines for search validation, and they are connected to almost all databases including Web of Science and Scopus. The paper conducted a manual search about the subjects of review on Google Scholar and the main Google. It was found that although there are several studies on tax compliance, constraints and tax risk, there has been virtually no study connecting these constructs. The keywords in those studies in Google Scholar and Google database include bankruptcy, financial distress, risk, risk management in tax, tax aggressiveness, tax avoidance, tax compliance, tax evasion and tax uncertainty.

The paper followed these baseline results to conduct further analyses using the “Biblioshiny” function in the “bibliometrix” package. To retrieve the relevant articles from the Scopus database, a combination of three sets of keywords with the logic term “OR” was employed. The set included tax risk assessment, financial constraints and tax compliance keywords. The search for combinations of keywords was conducted in the following fields: article title, abstract and keywords. The search used was as follows: TITLE-ABS-KEY (((((“tax risk assessment” OR ”financial constraints” OR ”tax compliance”))))). This paper interrogated the existing empirical literature from 1981 to 2022.

Key research themes, players, cross country collaboration and research gaps for future studies were identified. It was evident through the analyses that emerging studies have explored these variables: tax risk assessment, financial constraints and tax compliance. However, when joint search criteria were introduced; it was found that the empirical literature has largely not considered the interconnectedness of these variables. From two variables mapping search criteria, it was observed that apart from financial constraints and tax compliance, these variables have virtually not been investigated. The implication of the findings is that empirical evidence of the consequence of tax risk on tax compliance is still in its infancy. The paucity of empirical evidence despite the sound theoretical bases of such relationship could create policy burden for tax authorities.

This implication becomes more challenging with the ascendency of globalisation and financial integration. Revenue authorities have to deal with more complex tax risks due to globalisation and sophisticated financial markets. In Africa and other developing economies where they are in the period of transition to market relations and private sector expansion, tax risk assessment has taken the central stage due to the double-edged situation of developing public need for strengthening fiscal power and offering tax privileges for new and prospective. Therefore, the lack of sufficient empirical evidence about the tax risk-tax compliance nexus could worsen the already troubling tax compliance gap.

A further implication of the findings is that there is a dearth of evidence on financial constraints-tax compliance. This makes it not only difficult to streamline firm-level tax policy but also in affirming or disaffirming theoretical assumptions of EPPM and POT within the tax compliance framework. It is asserted that corporate businesses' inability to comply with tax obligations could partly be due to financial constraints resulting from solvency and liquidity. Financial constraints are likened to a two-edged sword: damning to the business operations and detrimental to government tax revenue. It has been argued that when corporate organisations are beleaguered with financial constraints, there is a probability to maximise operating financial capacities through practical firm-level management including tax planning. There are relatively few studies to support these assertions and virtually no study for the interaction effect of financial constraints on the tax risk-tax compliance nexus.

Overall, more empirical studies are needed to shape our understanding of the interconnectedness of tax risk assessment, financial constraint and tax compliance. The evidence from such an investigation would not only explore the practicality of related theoretical assumptions and assertions but also provide directions for improving tax compliance through the integration of tax risk and financial constraints in firm-level tax policy. Given these empirical gaps coupled with theoretical justifications for the connectedness of these variables, it is recommended that future studies should extend the literature to contribute to filling the gap. Evidence of such analyses could also shape tax policy and practice and therefore government and tax authorities should sponsor studies in this area.

8. Limitation

Despite the sound contribution of this bibliometric paper, there are also some limitations, which should be considered when relying on the findings. Although the paper expanded the search for paper selection through Google Scholar, Google and Scopus, the search in Google Scholar and Google was conducted manually. It is therefore possible that some papers might have been ignored. Moreover, manual literature reviews most of the time lack rigor.

The bibliometric analysis through “bibliometrix” package was also limited to those retrieved from journals that are indexed in Scopus. The search criteria also excluded journals from non-English papers. This could have consequences on the top papers, institutions, authors and active countries.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- . (1997). . , (), . https://doi.org/10.1111/j.1540-6261.1997.tb01112.x

- Adamu, M., Ibrahim, Y. E., Al-Atroush, M. E., & Alanazi, H. (2021). Mechanical properties and durability performance of concrete containing calcium carbide residue and nano silica. Materials, 14(22), 6960. https://doi.org/10.3390/ma14226960

- Agyei, S. K., & Yankey, B. (2019). Environmental reporting practices and performance of timber firms in Ghana: Perceptions of practitioners. Journal of Accounting in Emerging Economies, 9(2), 268–21. https://doi.org/10.1108/JAEE-12-2017-0127

- Aiello, D. J. (2022). Financially constrained mortgage servicers. Journal of Financial Economics, 144(2), 590–610. https://doi.org/10.1016/j.jfineco.2021.09.026

- Alasfour, F., Samy, M., & Bampton, R. (2016). The determinants of tax morale and tax compliance: Evidence from Jordan. In Advances in taxation (pp.125-171). Emerald Group Publishing Limited.

- Altman, E. I., Iwanicz-Drozdowska, M., Laitinen, E. K., & Suvas, A. (2017). Financial Distress prediction in an international context: a review and empirical analysis of Altman’s Z- score model. Journal of International Financial Management & Accounting, 281, 131–171. 131–171. https://doi.org/10.1111/jifm.12053

- Amanamah, R. B. (2016). Tax compliance among small and medium scale enterprises in Kumasi metropolis, Ghana. Journal of Economics and Sustainable Development, 7(16), 5–16.

- Andreoni, J. (1998). Toward a theory of charitable fund-raising. Journal of Political Economy, 106(6), 1186–1213. https://doi.org/10.1086/250044

- Aria, M., Cuccurullo, C., & Aria, M. M. (2017). Package ‘bibliometrix’.

- Beck, P. J., & Lisowsky, P. (2014). Tax uncertainty and voluntary real-time taxaudits. The Accounting Review, 89(3), 867–901. https://doi.org/10.2308/accr-50677

- Bellon, M., Dabla-Norris, E., Khalid, S., & Lima, F. (2022). Digitalization to improve tax compliance: Evidence from VAT e-Invoicing in Peru. Journal of Public Economics, 210, 104661. https://doi.org/10.1016/j.jpubeco.2022.104661

- Cai, D. F., Ni, N. N., & Cai, J. (2015). Big enterprise tax risk management: Warning, simulation and application. International Journal of u-and e-Service, Science and Technology, 8(4), 135–146. https://doi.org/10.14257/ijunesst.2015.8.4.14

- Campello, M., Graham, J. R., & Harvey, C. R. (2010). The real effects of financial constraints: Evidence from a financial crisis. Journal of Financial Economics, 97(3), 470–487. https://doi.org/10.1016/j.jfineco.2010.02.009

- Carsamer, E. & Abbam, A (2020) Religion and tax compliance among SMEs in Ghana. Journal of Financial Crime, 01(2020),1–17 DOI 10.1108/JFC-01-2020-0007

- Chen, S., Chen, X., Cheng, Q., & Shevlin, T. (2010). Are family firms more tax aggressive than non-family firms? Journal of Financial Economics, 95(1), 41–61. https://doi.org/10.1016/j.jfineco.2009.02.003

- Chyz, J. A., Gal-Or, R., Naiker, V., & Sharma, D. S. (2021). The association between auditor provided tax planning and tax compliance services and tax avoidance and tax risk. Journal of the American Taxation Association, 43(2), 7–36. https://doi.org/10.2308/JATA-19-041

- Dang, V. C, Hang Tran, X., & McMillan, D. (2021). The impact of financial distress on tax avoidance:An empirical analysis of the Vietnamese listed companies. Cogent Business & Management, 8(1), 1953678.

- Dang, V. C., & Tran, X. H. (2021). The impact of financial distress on tax avoidance: An empirical analysis of the Vietnamese listed companies. Cogent Business & Management. https://doi.org/10.1080/23311975.2021.1953678

- de Guevara, J. F., Maudos, J., & Salvador, C. (2022). Firms’ investment, indebtedness and financial constraints: Size does matter. Finance Research Letters, 46, 102240. https://doi.org/10.1016/j.frl.2021.102240

- Delgado-Rodríguez, M. J., & Lucas-Santos, D. (2022). Synchronization and cyclicality of social spending in economic crises. Empirica, 1–35. https://doi.org/10.1007/s10663-022-09554-9

- De Neve, J. E., Imbert, C., Spinnewijn, J., Tsankova, T., & Luts, M. (2021). How to improve tax compliance? Evidence from population-wide experiments in Belgium. Journal of Political Economy, 129(5), 1425–1463. https://doi.org/10.1086/713096

- Devos, K. (2014). Tax compliance theory and the literature. In Factors influencing individual taxpayer compliance behaviour (pp. 13–65). Springer.

- Di Stefano, G., Peteraf, M., & Verona, G. (2010). Dynamic capabilities deconstructed: A bibliographic investigation into the origins, development, and future directions of the research domain. Industrial and Corporate Change, 19(4), 1187–1204. https://doi.org/10.1093/icc/dtq027

- Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially irresponsible? Journal of Business Ethics, 124(1), 173–184. https://doi.org/10.1007/s10551-013-1862-4

- Du, J., & Nguyen, B. (2022). Cognitive financial constraints and firm growth. Small Business Economics, 58(4), 2109–2137. https://doi.org/10.1007/s11187-021-00503-7

- Dyreng, S. D., Hanlon, M., & Maydew, E. L. (2008). Long-run corporate tax avoidance. The Accounting Review, 83(1), 61–82. https://doi.org/10.2308/accr.2008.83.1.61

- Eberhartinger, E., & Zieser, M. (2021). The effects of cooperative compliance on firms’ tax. Schmalenbach J Bus Res, 73(1), 125–178. https://doi.org/10.1007/s41471-021-00108-6

- Edwards, A., Schwab, C., & Shevlin, T. (2016). Financial constraints and cash tax savings. The Accounting Review, 91(3), 859–881.

- Elena, O., Kirill, T., & Dina, O. (2019). Tax compliance in the Russian federation, the United Kingdom of Great Britain and Northern Ireland, and the United States of America: Forcing and encouraging lawful conduct of taxpayers. Russian Law Journal, 7(1), 4–54.

- Engida, T. G., & Baisa, G. A. (2014). Factors influencing taxpayers’ compliance with the tax system: An empirical study in Mekelle city, Ethiopia. eJTR, 12, 433.

- Erard, B., & Feinstein, J. S. (1994). Honesty and evasion in the tax compliance game. The RAND Journal of Economics, 25(1), 1–19. https://doi.org/10.2307/2555850

- Erel, I., Jang, Y., & Weisbach, M. S. (2015). Do acquisitions relieve target firms’ financial constraints? The Journal of Finance, 70(1), 289–328. https://doi.org/10.1111/jofi.12155

- Erel, I., Jang, Y., & Weisbach, M. S. (2015). Do acquisitions relieve target firms’ financial constraints?. The Journal of Finance, 70(1), 289–328.

- Fagerberg, J., Fosaas, M., & Sapprasert, K. (2012). Innovation: Exploring the knowledge base. Research Policy, 41(7), 1132–1153. https://doi.org/10.1016/j.respol.2012.03.008

- Gartner, W. B., Davidsson, P., & Zahra, S. A. (2006). Are you talking to me? The nature of community in entrepreneurship scholarship. Entrepreneurship Theory and Practice, 30(3), 321–331. https://doi.org/10.1111/j.1540-6520.2006.00123.x

- Gautam, I. (2017). Cashless economy: A step towards green economy. Mangalmay Journal of Management & Technology, 7(2), 61–71.

- Ghazouani, T. (2013). The capital structure through the trade-off theory: Evidence from tunisian firm. International Journal of Economics and Financial Issues, 3(3), 625–636.

- Gromb, D., & Vayanos, D. (2018). The dynamics of financially constrained arbitrage. The Journal of Finance, 73(4), 1713–1750. https://doi.org/10.1111/jofi.12689

- Hai, B., Yin, X., Xiong, J., & Chen, J. (2022). Could more innovation output bring better financial performance? The role of financial constraints. Financial Innovation, 8(1), 1–26. https://doi.org/10.1186/s40854-021-00309-2

- Hanlon, M., & Heitzman, S. (2010). A review of tax research. Journal of Accounting and Economics, 50(3), 127–178.

- Hanlon, M., Mills, L., & Slemrod, J. (2007). An empirical examination of corporate tax noncompliance, in taxing corporate income in the 21st century (pp. 171–210). (A. Auerbach, J. R. Hines Jr., & J. Slemrod, eds.). Cambridge University Press.

- Hansen, B. E. (1999). Threshold effects in non-dynamic panels: Estimation, testing, and inference. Journal of Econometrics, 93(2), 345–368. https://doi.org/10.1016/S0304-4076(99)00025-1

- Hapsoro, D., & Suryanto, T. (2017). Consequences of going concern opinion for financial reports of business firms and capital markets with auditor reputation as a moderation variable: An experimental study. European Research Studies Journal, 20(2A), 197–223. https://doi.org/10.35808/ersj/637

- Haselip, J., Desgain, D., & Mackenzie, G. (2015). Non-financial constraints to scaling-up small and medium-sized energy enterprises: Findings from field research in Ghana, Senegal, Tanzania and Zambia. Energy Research & Social Science, 5, 78–89. https://doi.org/10.1016/j.erss.2014.12.016

- Holmstrom, B. (1989). Agency costs and innovation. Journal of Economic Behavior & Organization, 12(3), 305–327. https://doi.org/10.1016/0167-2681(89)90025-5

- Imam, P. A., & Jacobs, D. (2014). Effect of corruption on tax revenues in the Middle East. Review of Middle East Economics and Finance Rev. Middle East Econ. Fin, 10(1), 24.

- Kaffash, S., Nguyen, A. T., & Zhu, J. (2021). Big data algorithms and applications in intelligent transportation system: A review and bibliometric analysis. International Journal of Production Economics, 231, 107868. https://doi.org/10.1016/j.ijpe.2020.107868

- Kasper, M., & Alm, J. (2022). Audits, audit effectiveness, and post-audit tax compliance. Journal of Economic Behavior & Organization, 195, 87–102. https://doi.org/10.1016/j.jebo.2022.01.003

- Keen, M. (2013). The Anatomy of the VAT. National Tax Journal, 66(2), 423–446. https://doi.org/10.17310/ntj.2013.2.06

- Kessler, C. F. (1963). Charlotte Perkins Gilman: Her progress toward utopia, with selected writings. Syracuse University Press.

- Kinda, M. T. (2014). The quest for non-resource-based FDI: Do taxes matter? International Monetary Fund.

- Kinda, T. (2018). The quest for non-resource-based FDI: Do taxes matter?. Macroeconomics and Finance in Emerging Market Economies, 11(1), 1–18.

- Lavermicocca, C. (2011). Tax risk management practices and their impact on tax compliance behaviour-the views of tax executrices from large Australian companies. eJTR, 9, 89.

- Lee, K., & Yoon, S. (2020). Managerial ability and tax planning: Trade-off between tax and nontax costs. Sustainability, 12(1), 370–383. https://doi.org/10.3390/su12010370

- Liapis, K. J., Rovolis, A., Galanos, C., & Thalassinos, E. (2013). The clusters of economic similarities between EU countries: A view under recent financial and debt crisis. EUROPEAN RESEARCH STUDIES JOURNAL, XVI(1), 41–66. https://doi.org/10.35808/ersj/380

- Litina, A., & Palivos, T. (2016). Corruption, tax evasion and social values. Journal of Economic Behavior and Organisation, 124, 164–177. https://doi.org/10.1016/j.jebo.2015.09.017

- Li, W., & Zhang, Y. (2021). Firms’ Disclosure Policies and Capital Investment: Evidence from Regulation Fair Disclosure. Journal of Accounting, Auditing & Finance, 36(2), 379–404.

- Ma, H., & Hao, D. (2022). Economic policy uncertainty, financial development, and financial constraints: Evidence from China. International Review of Economics & Finance, 79, 368–386. https://doi.org/10.1016/j.iref.2022.02.027

- Malika, M., Maheswaran, D., & Jain, S. P. (2022). Perceived financial constraints and normative influence: Discretionary purchase decisions across cultures. Journal of the Academy of Marketing Science, 50(2), 252–271. https://doi.org/10.1007/s11747-021-00814-x

- Morrow, P., Smart, M., & Swistak, A. (2022). VAT compliance, trade, and institutions. Journal of Public Economics, 208, 104634. https://doi.org/10.1016/j.jpubeco.2022.104634

- Murray-Johnson, L., Witte, K., Patel, D., Orrego, V., Zuckerman, C., Maxfield, A. M., & Thimons, E. D. (2004). Using the extended parallel process model to prevent noise-induced hearing loss among coal miners in Appalachia. Health Education & Behaviour, 31(6), 741–755. https://doi.org/10.1177/1090198104263396

- Musimenta, D., Naigaga, S., Bananuka, J., & Najjuma, M. S. (2019). Tax compliance of financial services firms: A developing economy perspective. Journal of Money Laundering Control, 22(1), 14–31. https://doi.org/10.1108/JMLC-01-2018-0007

- Myers, S. C. (1984). Finance theory and financial strategy. Interfaces, 14(1), 126–137. https://doi.org/10.1287/inte.14.1.126

- Nechaev, A., & Antipina, O. (2016). Analysis of the impact of taxation of business entities on the innovative development of the country. EUROPEAN RESEARCH STUDIES JOURNAL, XIX(1), 71–83. https://doi.org/10.35808/ersj/507

- Nerur, S. P., Rasheed, A. A., & Natarajan, V. (2008). The intellectual structure of the strategic management field: An author co‐citation analysis. Strategic Management Journal, 29(3), 319–336. https://doi.org/10.1002/smj.659

- Nicolas, T. (2022). Short-term financial constraints and SMEs’ investment decision: Evidence from the working capital channel. Small Business Economics, 58(4), 1885–1914. https://doi.org/10.1007/s11187-021-00488-3

- Ogbonna, G. N., & Appah, E. (2016). Effect of tax administration and revenue on economic growth in Nigeria. Research Journal of Finance and Accounting, 7(13), 49–58.

- Olaleye, M. O. (2016). Effect of tax incentives on foreign direct investment in listed Nigerian manufacturing companies (Doctoral dissertation, coherd, Jkuat).

- Palil, M. R., & Mustapha, A. F. (2011). Determinants of tax compliance in Asia: A case of Malaysia. European Journal of Social Sciences, 24(1), 7–32.

- Pritchard, R. D. (1969). Equity theory: A review and critique. Organizational Behavior and Human Performance, 4(2), 176–211. https://doi.org/10.1016/0030-5073(69)90005-1

- Queku, I. C. (2018). International financial reporting standards (IFRS) compliance and earning predictability: Evidence from banks in Ghana. International Journal of Innovative Research and Advanced Studies, 4(8), 102–111.

- Ramos‐Rodríguez, A. R., & Ruíz‐Navarro, J. (2004). Changes in the intellectual structure of strategic management research: A bibliometric study of the strategic management journal, 1980–2000. Strategic Management Journal, 25(10), 981–1004. https://doi.org/10.1002/smj.397

- Rego, S. O., & Wilson, R. (2012). Equity risk incentives and corporate tax aggressiveness. Journal of Accounting Research, 50(3), 775–810. https://doi.org/10.1111/j.1475-679X.2012.00438.x

- Reinganum, J. F., & Wilde, L. L. (1985). Income tax compliance in a principal-agent framework. Journal of Public Economics, 26(1), 1–18. https://doi.org/10.1016/0047-2727(85)90035-0

- Richardson, G., Lanis, R., & Taylor, G. (2015). Financial distress, outside directors and corporate tax aggressiveness spanning the global financial crisis: An empirical Analysis Journal of Banking & Finance 52 112–129 .

- Schildt, H. A., Zahra, S. A., & Sillanpää, A. (2006). Scholarly communities in entrepreneurship research: A co–citation analysis. Entrepreneurship Theory and Practice, 30(3), 399–415. https://doi.org/10.1111/j.1540-6520.2006.00126.x

- Schmidt, S., Schmidt, A., & Seetharaman, A. (2008). The effects of standardized tax rates, average tax rates, and the distribution of income on tax progressivity. Journal of Accounting and Public Policy, 27(1), 88–96. https://doi.org/10.1016/j.jaccpubpol.2007.11.006

- Seidu, B. A., Opoku-Boahen, E., Queku, Y. N., Boateng, K., & Opoku-Boahen, G. (2022). A critical review of antecedents of unauthorised extra-budgetary expenditure: Application of fraud triangle theory. African Journal of Business and Economic Research (AJBER), 17(4), 311–341. https://doi.org/10.31920/1750-4562/2022/v17n4a14

- Seidu, B. A., Opoku-Boahen, E., Queku, Y. N., Boateng, K., & Opoku-Boahen, G. (2022). A Critical Review of Antecedents of Unauthorised Extra-Budgetary Expenditure: Application of Fraud Triangle Theory. African Journal of Business and Economic Research (AJBER), 17(4), 311–341.

- Seidu, B. A., Queku, Y. N., & Carsamer, E. (2021). Financial constraints and tax planning activity: Empirical evidence from Ghanaian banking sector. Journal of Economic and Administrative Sciences. https://doi.org/10.1108/JEAS-12-2020-0199

- Serrasqueiro, Z., & Caetano, A. (2015). Trade-off theory versus pecking order theory: Capital structure decisions in a peripheral region of Portugal. Journal of Business Economics and Management, 16(2), 445–466. https://doi.org/10.3846/16111699.2012.744344

- Small, H. (1973). Co-citation in the scientific literature: A new measure of the relationship between two documents. Journal of the American Society for Information Science, 24(4), 265–269. https://doi.org/10.1002/asi.4630240406

- Sunardi, S., Damayanti, T. W., Supramono, S., & Hermanto, Y. B. (2022). Gender, perception of audits, access to finance, and self-assessed corporate tax compliance. Economies, 10(3), 65. https://doi.org/10.3390/economies10030065

- Tranfield, D., Denyer, D., & Smart, P. (2003). Towards a methodology for developing evidence‐informed management knowledge by means of systematic review. British Journal of Management, 14(3), 207–222. https://doi.org/10.1111/1467-8551.00375

- Witte, J. F., Fitzmartin, R., Slywka, J., Buckley, B. J., Kaiko, R., Goldenheim, P. D., Mooar, P., Witte, J. F., & Hersh, E. V. (1994). Successful tax reform: Lessons from an analysis of tax reform in six countries. Advances in Therapy, 11(5), 213–227.

- Yorke, S. M., Amidu, M., & Agyemin-Boateng, C. (2016). The effects of earnings management and corporate tax avoidance on firm value. International Journal of Management Practice, 9(2), 112–131. https://doi.org/10.1504/IJMP.2016.076741

- Young, A., Lei, L., Wong, B., & Kwok, B. (2016). Individual tax compliance in China: A review. International Journal of Law and Management, 58(5), 562–574. https://doi.org/10.1108/IJLMA-12-2015-0063

- Yu, X., & Fang, J. (2022). Tax credit rating and corporate innovation decisions. China Journal of Accounting Research, 15(1), 100222. https://doi.org/10.1016/j.cjar.2022.100222

- Zhang, D., & Lucey, B. M. (2022). Sustainable behaviors and firm performance: The role of financial constraints’ alleviation. Economic Analysis and Policy, 74, 220–233. https://doi.org/10.1016/j.eap.2022.02.003

- Zupic, I., & Cater, T. (2015). Bibliometric methods in management and organization.Organizational Research Methods. 18(3), 429–472.