Abstract

One of the main tasks of the accounting information systems is to provide information users at all levels with reliable and easy-to-understand information to be used in planning and auditing activities at the required time and place. Changing conditions lead accounting information systems to renew and contribute more to business management. In this study, the article studies related to the accounting information system in the world under this subject were examined with the bibliometric analysis method, and the 20 most cited and the most recent 40 studies among these studies were evaluated in terms of subject, method, and result. Within the scope of the study, it is seen that the most publications were made in 2020, according to the results of the searches carried out on the subject of “accounting information system” in the Web of Science database between 1985 and 2022. When the examined publications were evaluated in terms of countries, it was determined that the only country that exceeded the limit of 100 publications was the USA, which was far ahead of other countries in the number of citations of these publications. In the distribution of the reviewed publications by universities, Iowa State University from the USA is at the top of the list with seven publications. Among the authors, it was revealed that Diane J. Janvrin had the highest number of publications with 7 articles. Finally, by including the 20 most cited studies and the 40most recent studies, their methods and results, a map of the most used publications from the past to the present has been made, and it has been tried to reveal which topics and their results are currently discussed.

1. Introduction

In an increasingly competitive environment with globalization, accounting information has become very important for companies in order to stay strong and maintain business activities. This information, which the decision makers need in the decision-making processes, is produced by the accounting information system.

Accounting information system (AIS) is an important subsystem within an organization’s general information system in relation to accounting practices. AIS is perceived as critical in establishing “solid ground” in the business realm (Allah et al., Citation2013, p. 263). One manner in which economic factors can be properly managed is by means of using accounting information systems. Fundamentally accounting information systems can be described as those logical systems where numerical information is accumulated, evaluated and analysed with the main intent to provide financial and accounting information pertaining to a business entity which, in turn, allow management to make sound business decisions which may impact on the operations of a business (Bruwer et al., Citation2018, p. 107).

The aim of this study is to guide the studies to be prepared by revealing the appearance of the studies carried out within the scope of AIS in the Web of Science database. Questions such as who has worked on the work to be done before, the scope, method, and findings of these studies, which countries stand out on these issues and which channels can be broadcast after the preparation of the publication, can be answered with such studies. In this study, which was put forward for these purposes; The publications under the subject of accounting information system were examined with the bibliometric analysis method and a literature review was made regarding the studies carried out, the scope of the publications was determined and the orientation of the studies in this field was determined.

2. Accounting information system

Information systems, which enable the acquisition, recording, processing, and transmission of information, have always existed in businesses for the purpose of communication, decision-making, and use as a competitive tool in competitive markets (İbrahim et al., Citation2020, p. 52). The information system is a set of methods that processes data and transforms it into computable, comparable, presentable, and interpretable information (Stair & Reynolds, Citation2012, p. 11). AIS, which is a part of the management information system, collects, processes, and stores financial data of businesses, including raw data or information, and transforms them into financial data, which is a very important factor that decision makers can use in the decision-making process (Nguyen et al., Citation2021, p. 3). Perceptions of the role of accounting systems in the academic accounting literature are based mainly on economic theories originating in liberal market economies (Shareia, Citation2016, p. 55).

Managers are faced with various problems related to business activities almost every day during the period, and they take decisions and implement them to solve these problems. A large part of the data that forms the basis of the decisions taken is obtained from the accounting information system of the enterprise. One of the main tasks of the modern accounting information system, which has emerged as a result of the developments in the technologies in the field of information and production today, is to provide information users at all levels; is to provide reliable and easy-to-understand information, which will be used in planning and auditing activities, at the required time and place. Changing conditions lead accounting information systems to renew and contribute more to business management. Accordingly, it is clear that the accounting system will be one of the most important assistants of the managers in the dynamic environmental conditions of today and the future.

3. Method and data

In this study, firstly, the publications under the subject of accounting information system were examined by bibliometric analysis method. Bibliometric analysis is a method that examines the characteristics of scientific studies written on the relevant subject, such as the author, institution and country of the author, and citation links. In the first stage of the study, a search was made based on the keyword “accounting information system” in the journals scanned in the Web of Science database, and publications related to this subject were compiled. The results obtained from this scan were classified and the data obtained by using the VOSviewer program, which is one of the many software developed for scientific mapping analysis, was presented in a certain order with the visual mapping method. It is necessary to identify research areas in order to monitor a scientific field and determine its structure and development. In this study, the scanning of the accounting information system word was carried out with the subject (topic) limitation in order to make the evaluation comprehensively. The studies used in the research were obtained from articles that were visible in the Web of Science database as of August 2022. The literature review carried out in the second stage of the study was carried out on two criteria. While one of them was the citation criterion, the other was determined as the time of publication. In the study, first of all, the literature of the 20 most cited studies was carried out, and the research topics of the most used articles by the researchers, as well as their methods and results were included. Thus, a map of the most used publications from the past to the present has been drawn up. At the time of publication, which was determined as the second criterion, the evaluations of the 20 most recently published publications were shared, and it was tried to reveal which topics and their results are currently discussed.

Literature review was preferred as the method of the study. In the first stage of this study, a search was made based on the keyword “accounting information system” in the journals scanned in the Web of Science database, and publications related to this subject were compiled. The main reason for choosing this database is that the data required for analysis can be easily compiled and it is the most widely accepted and frequently used database in the scientific literature. In addition, since Web of Science contains many journals in the field of accounting, it is possible to reach a sufficient number of articles to be used in the study. It is necessary to identify research areas in order to monitor a scientific field and determine its structure and development. In this study, the scanning of the accounting information system word was carried out with the subject limitation in order to make the evaluation comprehensively. The studies used in the research were obtained from articles that were visible in the Web of Science database as of August 2022. The literature review carried out within the scope of the study was carried out on two criteria. While one of them was the citation criterion, the other was determined as the time of publication. In the study, first of all, the literature of the 40 most cited studies was carried out, and the research topics of the most used articles by the researchers and their methods and results were included. Thus, a map of the most used publications from the past to the present has been drawn up. At the time of publication, which was determined as the second criterion, the evaluations of the 40 most recently published publications were shared, and it was tried to reveal which topics and their results are currently discussed.

4. Findings

In the study, firstly, search records were compiled in the Web of Science database between the years 1985–2022 regarding the subject of “accounting information system”. The information obtained from this survey was first evaluated in terms of distribution over the years and then analyzed within the scope of other headings such as country, institution, author, journal, keyword, and bibliography.

4.1. Distribution of studies published on accounting information system by years

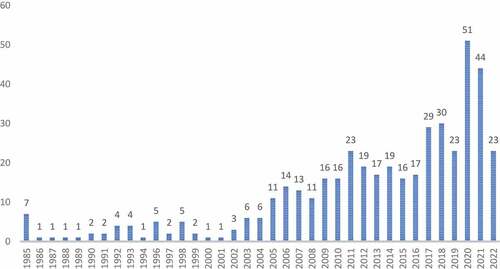

First of all, when we look at the distribution of publications on the accounting information system by years, it was determined that the first study was published in 1985. This publication is the article “Structuring an undergraduate accounting information systems course: Alternate strategies” by Michael J. Cerullo, H. Perrin Garsombke, and Lawrence A. Klein.

Graphic 1. Distribution of Studies Published on Accounting Information System by Years

The most publications on the accounting information system were made in 2020. 2020 is followed by 2021, 2018, and 2017, respectively. Especially since 2005, it is seen that the publications related to the accounting information system have gained momentum and exceeded the average of 15 publications annually since 2009, and this acceleration became more evident in 2017 and was based on 30 publications. Since the study was conducted in the middle of 2022, the number of publications for this year was less.

4.2. Distribution of examined publications by country

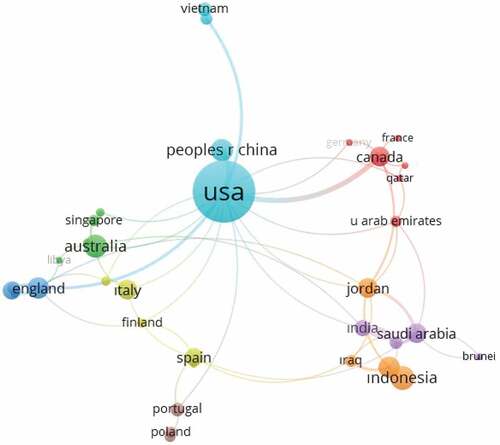

When we look at the distribution of the publications examined within the scope of the study by countries, it is seen that the status of multi-authorship and the fact that the same publication is written to each country household because a publication has multiple authors, and the authors are from different countries affects the country information.

In Table , there are countries that have six or more publications on the accounting information system. When the table is examined, it is seen that most of the published studies are from the USA, followed by Indonesia, Australia, and China, respectively. However, although these countries are above the ranking, the number of publications was far below the USA. Here are 10 publications and over 13 countries.

Table 1. Publications by Countries and Number of Citations

As can be seen from the table, there is a large difference between the USA and its followers in the number of citations. Here, it emerges from the average number of citations that the most influential publications are based in Taiwan and South Korea.

When we look at the mapping image of the links related to the citations in terms of countries (), the countries with a high number of citations also appear here. In particular, the strength of the USA’s connection with Canada is evident.

Figure 1. Linkage Map of Citations by Country.

4.3. Distribution of examined publications by universities

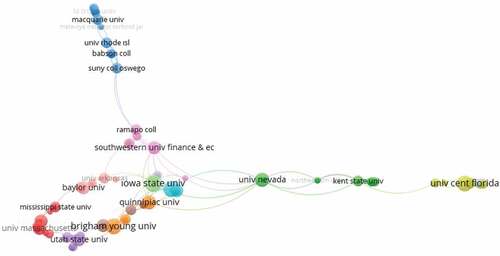

Considering the universities with four or more studies published under the subject of accounting information system in the Web of Science database, 20 universities are listed in ; it is seen that the maximum number of publications is 7.

Table 2. Distribution of Examined Publications by Universities

When the table is examined, it is seen that there is no prominent institution in which universities have publications close to each other. While Iowa State University from the USA is at the top of the list with seven publications, it is followed by five universities with six publications. While three of these universities are still operating in the USA, the other two have been identified as DrBabasaheb Ambedkar Marathwada University from India and Hodeidah University from Yemen as shown in .

Figure 2. Connection Map of Universities with the Most Publications.

4.4. Distribution of examined publications by authors

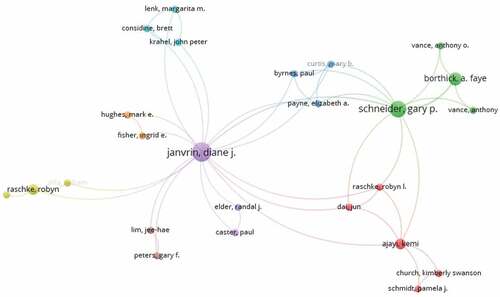

Considering who wrote the reviewed publications, the authors with at least three publications are listed in Table .

Table 3. Distribution of Examined Publications by Authors

According to the table, the highest number of publications was made by Diane J. Janvrin with seven copies. It is followed by Gary P. Schneider, Jong-min Choe, and Daniel E. O’leary with five publications, respectively. The number of authors who have three or more publications in the Web of Science database is 20.

Considering the connections of the authors with the highest number of publications in , it is seen that although many authors have weak connections with each other, the connection network is a little more concentrated around the authors with a large number of publications.

Figure 3. Link Map of Authors with the Most Publications.

4.5. Distribution of examined publications by sources

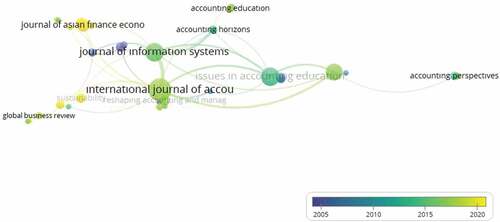

When we look at the distribution of the publications covered in the study to the journals in , it is seen that 20 journals with at least 4 publications emerge, while three of these journals (International Journal of Accounting Information Systems, Issues in Accounting Education and Journal of Information Systems) host more than 20 publications.

Table 4. Distribution of Examined Publications by Sources and Number of Citations

When the map in , which includes the links of the journals in which the studies are published within the scope of the accounting information system, is examined, it is seen that the three journals that stand out with the most publications, namely International Journal of Accounting Information Systems, Issues in Accounting Education and Journal of Information Systems, also have links with other sources. It is also noteworthy that the strongest connection is between the International Journal of Accounting Information Systems and the Journal of Information Systems.

Figure 4. Link Map of Journals with the Most Publications.

4.6. Keywords used in reviewed publications

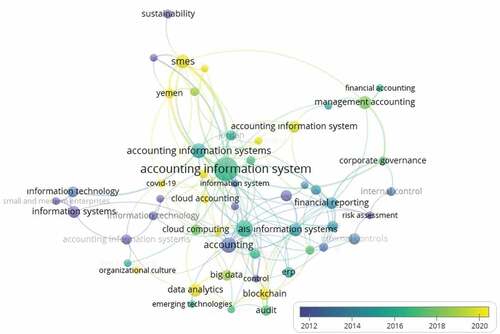

When the studies published on the accounting information system are examined in the context of the keywords used, Table is formed. Keywords mentioned at least 7 times here are used as constraints.

Table 5. Keywords Used in Reviewed Publications

When Table is examined, it is seen that the accounting information system keyword is incomparably dominant with its four different forms in the table due to spelling differences; it is seen that it is followed by words such as accounting (accounting), SME (Smes), information systems (information systems), data analysis (data analytics), and management accounting.

Looking at the keyword map in , it is seen that both the number of usage of the accounting information system statement and the strength of the connection are seen. It turns out that the strongest ties of the word accounting information system are with the words SME and Yemen. The reason for these connections is the increase in publications originating from Yemen in recent years and that they are mostly related to SMEs in that country. As a matter of fact, the strongest link of the word Kobi is with Yemen. In the context of the year, it is seen that the accounting information system keyword is concentrated in the years 2015–2018, and concepts such as data analytics, blockchain, and cloud accounting are used more up-to-date.

Figure 5. Keyword Link Map.

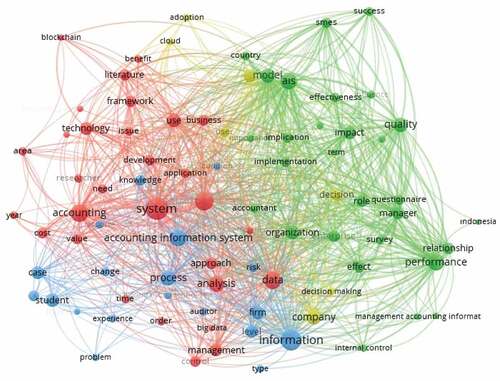

When the connection of the concepts in the abstracts of the examined publications is examined, a more complex and intertwined structure is formed.

It is seen that the word system is the most used concept in the connection map () of the concepts used in the abstracts, followed by the word informationand accounting, respectively. These concepts also have strong connections with other words. Although the number of uses is less, it is noteworthy that the concepts of performance, quality, and aims have very strong ties. The concept of accounting information system, which is used as a whole, is among the most used and strongly connected concepts.

Figure 6. Connection Map of the Concepts in the Abstracts of the Reviewed Publications.

4.7. Most cited and most recent from reviewed publications

Table contains data on the 20 most cited studies among the reviewed publications. The aims, methods, and results of the article regarding the publications included here are summarized below.

Table 6. The Most Cited Publications and the Number of Citations in the Examined Publications

Wilson et al. (Citation2006): They refer to the role of accounting information systems in controlling waste management in the informal sectors in developing countries. In this study, a qualitative research method was used as the research method. In the results of working, it has been stated that many people in developing countries are dependent on recycling materials from waste to make a living, and it has been emphasized that the role of accounting information system is important in controlling this area.

Pacini et al. (Citation2003): They consider the financial and environmental aspects of the sustainability of organic, integrated, and traditional farming systems at the farm level and at more detailed spatial scales. The study is supported by the case study method, and the data is measured with the accounting information system application. The study discusses the results of the case study farms and compares them with environmental sustainability thresholds reported in the literature and EU Directives on nitrates and pesticides in groundwater.

Abernethy and Vagnoni (Citation2004): They empirically examine the impact of authority structures on the use of accounting information systems (AISs) for decision control and decision management. The study is based on data collected from physician managers in major public teaching hospitals in Italy. The results support the hypotheses and show the consequences of power on organizational functioning. As a result of the study, it is determined that the transfer of official authority to physician managers does not have a direct effect on the use of accounting for decision control and decision management, but also has a significant effect on cost awareness.

Kobelsky et al. (Citation2008): It examines the extent to which the budgets of information technologies are affected by environmental, organizational, and technological conditions. The study also examines the extent to which IT budget levels relate to future firm performance, as measured using broad financial accounting metrics such as both operating margins and return on assets and market returns.

Kelton et al. (Citation2010): They present the role of accounting information system in individual decision-making in a conceptual framework. In addition to this in the study, it is stated that an integrated information presentation research model based on cognitive adaptation theory has been developed and it is stated that this model is used to summarize previous literature and provide recommendations for future research.

Dilla et al. (Citation2010): They determine that enterprises use interactive data visualization to present their accounting information to external users on investor relations websites and to internal users in applications such as enterprise resource planning, Balanced Scorecard, network security, and fraud detection systems. Within the scope of the study, a classification method is developed to examine the current state of interactive data visualization research related to accounting decision-making. At this point, three main topics were determined in the study: the relationship between task characteristics and interactive data visualization techniques, the relationship between decision-maker features and interactive data visualization techniques, and the impact of interactive data visualization techniques on decision processes and results.

Wiersma (Citation2009) conducts an empirical study on the purposes for which business managers use balance scorecards. In this context, a survey was conducted for 19 Dutch companies that were determined to use balance scorecards. In the results of working, the main purposes of managers’ use of accounting information systems are decision-making, coordination, and self-monitoring.

Corcoles et al. (Citation2011): They conducted a study on the necessity of including intellectual capital information in the accounting information systems of public universities in Spain. An empirical study has been carried out to reveal the extent to which university accounting information demands intellectual capital-related information in order to make the right decisions from different users who need this information. For this purpose, a questionnaire was designed and sent to all members of the Social Councils of public universities in Spain. The results of this research show what intangibles universities should provide to meet the new information demands of their users.

In the studies of Ruivo et al. (Citation2014) it is stated that there is a great interest among researchers and practitioners in accounting information systems (AIS), and it is stated that this is especially important in systems such as enterprise resource planning (ERP). The determinants of ERP use and value are empirically measured and analyzed in a single framework, and empirical evidence from Portuguese small and medium enterprises (SMEs) is presented. In the study, a dataset consisting of 134 web surveyed firms was used to test hypotheses through structural equation modeling.

J.L. Worrell et al. (Citation2013): They examine the use of Delphi Method, one of the methodologies used in the research of accounting information systems, in accounting information system research. At this point, an application example for the use of Delphi technique is given in the study. Within the scope of this example, the adequacy and limitations of the method on accounting information systems are also revealed.

In the studies of Schneider et al. (Citation2015), since the business use of data analytics is developing rapidly in the accounting environment, it is stated that data analytics fundamentally changes task processes, especially tasks that provide inference, prediction, and assurance to decision makers, similar to many new systems containing accounting information. For this reason, it is stated in the study that accounting researchers and practitioners should consider data analytics and its impact on accounting practice in their studies. In the study, Mauldin and Ruchala’s (Citation1999) organizing principles in accounting information systems (AIS) meta theory are used to identify current data analytics use, examine how data analytics impact the accounting environment and discuss challenges and research opportunities.

Brazel and Agoglia (Citation2007) examine the importance of the accounting information system in auditing studies and deal with the margins of error that may occur in audit judgments as a result of a complex accounting information system.

The study of Barton (Citation2005) deals with TAS 29 and TAS 31 standards regarding the application of accounting standards in Australian public administrations. In the study, it is stated that the working styles of the public and private sectors are very different from each other and it is stated that accounting standards should be shaped to suit the specific information needs of each sector in order for accounting information systems to provide the necessary information.

The studies of Al-Htaybat and von Alberti-Alhtaybat (Citation2017) explore the phenomenon of big data and corporate reporting and reveal the impact of big data and the current big data mindset on corporate reporting, and what are the perceptions of accountant and non-accountant participants. The study is a qualitative study, and the interview data of 25 participants are taken into account. Data are analyzed according to open and selective coding stages. Data collection and analysis is carried out in two stages, in 2014 and 2016.

Ezzamel and Bourn (Citation1990); The role of accounting information system in a business experiencing financial crisis is mentioned. In the study, it is stated that there is important but insufficient information about the roles of accounting information system in businesses. It is observed that the accounting information system does not have the necessary qualifications for effective pro-active or crisis management in the first stages of crises in businesses. As a result of the research, the necessity of applying more experimental and practical models regarding the accounting information system is emphasized.

Choe (Citation2004a) study: It is seen that this is done on the necessity of considering cultural differences in the design of information systems. In the study, cultural differences in the amount of information provided by management accounting information systems (MAIS) are examined empirically. In order to demonstrate these differences, data were collected from samples of Australian and Korean companies. In the results of working, it is stated that much more flexible performance information is provided by Korean firms, while Australian firms provide more quality performance and traditional cost control information (TCCI).

The study of Choe (Citation2004b) deals with the relationship and effects between management accounting, organizational learning and production performance. In the study, the relationship between the level of use of advanced production technology and the amount of information provided by the management is investigated. As a result of the study, it is stated that there is a positive relationship between the level of advanced production technology and the amount of management accounting information. The study also empirically examines the learning-promoting effects of organizational facilitators supported and complemented by information technology. Empirical results show that organizational learning facilitators have a moderator effect on the relationship between knowledge provision and performance improvement.

Choe (Citation1998) examines the effects of accounting information system users’ contributions to the system, influencing accounting information system design. Questionnaire method is used in the study.

Looking at the most cited publications, it is seen that the most recent publication belongs to 2017 and was generally published between the years 2000–2010. For this reason, the evaluations of the 40 most recently published publications on the accounting information system have been shared below. It has been attempted to reveal which topics and their results are currently discussed.

The study prepared by Gazi et al. (Citation2022) examined the evaluation of internal indicators related to the Northern Cyprus banking system with the balanced scorecard, which is one of the sustainable performance evaluation methods. In this study, limited sections of the balanced scorecard method were used, and a survey was conducted to collect data from 350 employees and managers of 21 banks in Northern Cyprus. Structural equation modeling was used in the analysis of the collected data. According to the results obtained from the research, while the positive effects of organizational culture, intrapreneurship, and accounting information system effectiveness on the balanced scorecard and its dimensions were revealed, it was seen that innovation performance had no effect.

Lutfi, Al-Okaily et al. (Citation2022) discussed the accounting information system in their study and evaluated it in terms of De Lone and Mc Lean’s Information System Success Model. The study was carried out using structural equation modeling with a quantitative approach, using a questionnaire applied to 101 decision makers who are familiar with the use of the accounting information system within the organizations in Jordan. Based on the results obtained, it has been revealed that while system quality and information quality significantly affect the use of accounting information system, service quality has no effect. On the other hand, accounting information system has a significant effect on user satisfaction; Again, it has been determined that the use of accounting information system and user satisfaction affect the sustainability of decision-making.

Chen et al. (Citation2022) analyzed the complex networked accounting cloud service in their study. As a result of the study, it has been determined that the current accounting cloud service network density is low and this has a great impact on the integration of accounting cloud services. At the end of the article, it was mentioned that integration is also the main reliability feature of accounting cloud services and it is very important, and it is recommended that accounting cloud service providers develop more integrated new accounting cloud services.

The study prepared by Monteiro et al. (Citation2022), in contrast to the studies that focus primarily on financial information quality and financial performance, shows that accounting information system quality, internal control system quality, and non-financial information quality are related to decision-making success and non-financial performance. They aimed to develop and evaluate a model that aims to measure its impact on company success. The model created in the study was tested empirically with the data obtained from the managers of 381 Portuguese companies and structural equation modeling was used to analyze the causal relationships between different structures. The results showed that the quality of information and control systems (accounting and internal control) has a direct effect on non-financial information quality and an indirect effect on decision-making success. In addition, it was concluded that quality non-financial information does not directly contribute to non-financial performance, but indirectly through decision-making success.

Al-Hattami et al. (Citation2022) examined the effect of the success of the accounting information system on the efficiency of the planning process in small and medium-sized enterprises (SMEs) in Yemen, an underdeveloped country. Within the scope of the study, a theoretical model based on the information system success model (DMISS2003) was developed and the components of this model were tested using structural equation modeling on a sample of 325 SMEs. The results showed that if SMEs focus on the information quality, system quality, user satisfaction, and use of the accounting information system, the success of the accounting information system positively affects the efficiency of the planning process.

Li and Fang (Citation2022) introduced the business process management system, analyzed the accounting information system based on business process management, and stated that process perception can support accounting information system research with the help of case studies. According to the study, with the continuous development of economy and technology, it was stated that the business process should be constantly optimized, and finance personnel should master more information technology knowledge. In addition, business management should maintain its sensitivity to policies and the economy, evaluate the opportunities it encounters, and encourage its personnel in this regard.

Wang et al. (Citation2022), in their study on the risk assessment method, state that traditional risk assessment methods yield results with less data output and are insufficient in system risk assessment. Experimental results show that the proposed method has a larger data output and a wider range of risk indicators when compared to the traditional risk estimation method.

Lutfi, Al-Khasawneh et al. (Citation2022) aimed to investigate the effects of accounting information system applications on sustainable business performance among Jordanian SMEs in this study, which deals with the sustainability of Small and Medium Enterprises during the COVID-19 pandemic. Data were collected from 194 participants among Jordanian SMEs through a survey study, and these data were evaluated using structural equation modeling. According to the results of the study, it has been determined that the demand of external stakeholders, compliance, financial support, and senior management support significantly affect the accounting information system applications, which in turn affects sustainable business performance. From this point of view, it was concluded in the study that SMEs should develop effective accounting information system applications in order to achieve their sustainability goals.

Al-Matari et al. (Citation2022) investigated the effect of accounting information system on organizational resilience and included 144 large companies from various sectors in Malaysia. Based on the results obtained from the survey data evaluated with the structural equation model, the hypothesis that dynamic accounting information system capability has a positive effect on organizational resilience and that business process capabilities mediate the relationship between dynamic accounting information system capability and organizational resilience is confirmed.

Thuan et al. (Citation2022), in their study to determine the factors affecting the application of accounting information systems in small and medium-sized enterprises (SMEs) in Vietnam, conducted an online survey with 132 people working in these enterprises. The survey data were evaluated using the structural equation model, and the hypotheses put forward were tested. First, the factors that had a significant impact on the use of the accounting information system were as follows: relative advantage, owner/manager commitment, and the impact of COVID-19. Organizational preparation and government support, on the other hand, did not have a positive effect on the use of accounting information system. Research results show that there is a positive relationship between the use of accounting information system and the effectiveness of accounting information system. It also confirms that accounting information system performance has a positive effect on business performance.

The main purpose of the study, written by Lutfi (Citation2022), is stated as explaining the factors that affect accountants’ intention to continue using the accounting information system in the context of Jordanian small and medium-sized enterprises (SMEs). This study was carried out with a survey on SMEs that fully implement an accounting information system and the data were analyzed with a structural equation model. The results revealed that the variables examined, namely achievement expectation, performance expectation, and social influence, have a positive effect on accountants’ intention to continue using the accounting information system, while facilitating influence and senior management support do not have a significant and positive effect on such use intention.

Fitrios et al. (Citation2022), p. 60 financial units from accredited higher education institutions in Riau Province and Riau Islands were included in this study, in which they aimed to examine the impact of information technology and user competence on the quality of accounting information systems and accounting information. As a result of the study, it was concluded that information technology and user competence have an impact on the quality of accounting information system for the higher education institutions where the study was conducted. Another result is that the quality of the accounting information system also affects the quality of accounting information needed by decision makers.

Guo (Citation2022), in his study emphasizing the importance of management accounting practices, states that the incentive mechanism can be used in the development of this field. Because, according to the author, the approaches of the employees are a determinant of the spread of management accounting in the enterprise, and the resistance on this subject can be eliminated with the incentive mechanism. This study argues that management accounting informatics lays the groundwork for achieving corporate strategic goals and that an accounting decision support system can significantly improve decision-making efficiency and effectiveness.

Li (Citation2022) aimed to reveal the view of the financial accounting personnel in smart cities to continuous optimization from the perspective of smart sensor technology. Three hundred and ten questionnaires were distributed to the accounting personnel of the enterprises located in the modeled smart cities, and healthy feedback was received in 248 of them. The results show that approximately 40%–60% of corporate finance accountants believe that data integration and sharing, data governance and data operations management systems should be continuously optimized and upgraded. Applying IoT technology and intelligent sensing technology to the optimization of corporate financial accounting information system not only improves the accuracy of financial data processing but also ensures that the required results are obtained efficiently and in real time.

Lu (Citation2022), unlike other authors, emphasized the security of accounting data created through the accounting information system. The use of information technologies not only brings convenient and efficient services to businesses but also has a great impact on the internal control of the business. However, the system in which this data is kept is vulnerable to illegal intrusions and viruses. This study aimed to evaluate the application of DES encryption technology to accounting data processing and finally concluded that it can realize secure management of accounting data.

Astuty et al. (Citation2022) stated that the purpose of their study was to examine the role of enterprise resource planning in the quality of management accounting information systems. Management accounting information system is followed and evaluated under three dimensions: reliability, efficiency, and flexibility. Within the scope of the study, a survey of 180 valid answers was conducted among public-owned enterprises in Indonesia, and the results were analyzed using least square structural equation modeling. The results of the study revealed that enterprise resource planning has an important role in the quality of the management accounting information system. According to the data obtained, it is stated that enterprise resource planning has the potential to increase the three dimensions of the management accounting information system, reliability, efficiency, and flexibility among public-owned enterprises in Indonesia.

Singh and Singh (Citation2022), in their study, which aimed to investigate the awareness of the extensible business reporting language (XBRL) and perceptions of certified public accountants in India about the barriers to XBRL adoption, also perceived problems related to XBRL adoption and individual characteristics (education and age). They also examined the relationship between gender and professional experience. Certified public accountants registered with the Institute of Chartered Accountants of India (ICAI) were sent an internet-based survey via e-mail, and data from 233 chartered accountants who responded to the survey were analyzed using reliability statistics and multivariate regression analyses. The results show that accountants perceive environmental, organizational, and innovative factors to be compelling in adopting XBRL; education and experience were also identified as important factors in explaining the perceptions of the participants.

Malitha and Nadarajah (Citation2022) aimed to evaluate the impact of the quality of accounting information systems on organizational effectiveness in automobile companies in Sri Lanka, a developing country. While organizational effectiveness was determined as the dependent variable in the research, system quality, information quality, and service quality were the independent variables of the study. The findings obtained as a result of the analysis showed that the quality of the accounting information system significantly and positively affects the organizational effectiveness of automobile companies. In addition, when viewed in detail, it has been determined that the system quality and service quality dimensions of the accounting information system affect the organizational effectiveness more than the information quality of the accounting information system.

Hamundu et al. (Citation2021) examined the factors affecting the intention to adopt cloud accounting among micro-small and medium-sized enterprises. According to the results of the research conducted on Indonesian micro-small and medium-sized enterprises, cloud computing features, organizational readiness, government intervention, and counterfeit pressure were found to be directly related to technology acceptance while indirectly related to cloud accounting adoption intention.

Hladika and Žmuk (Citation2021) aimed to investigate the structure of management accounting information system in Croatian companies. To collect data for analysis, an online survey was conducted on a representative sample of Croatian companies and 225 firms from the real sector overall participated. The results showed that managers viewed management reports as an important basis for decision-making. In addition, the findings of the study showed that managers in large companies use management reports more in decision-making than managers in micro, small, and medium companies.

Monteiro et al. (Citation2021) empirically examined the effect of the quality of the information and control system (internal control system, accounting information system, financial information, and non-financial information) on decision-making success and business performance. An online survey was conducted with the managers of Portuguese companies, and 381 responses were received. Evaluation of the data was carried out using AMOS statistical software and applying the structural equation modeling technique. The results support the hypothesis that the quality of the internal control system has a positive effect on the quality of the accounting information system. Another inference from the results is that the quality of the internal control system has a significant and positive effect on the quality of financial information; It does not have a significant effect on the quality of non-financial information. In addition, it has been revealed that while the quality of accounting information system has a positive effect on the quality of financial information, it has no effect on the quality of non-financial information.

Liu et al. (Citation2021), in their study in which they conducted a bibliometric analysis, aimed to help educators improve the integration of scientific data analytic knowledge by using technology tools that emerged in accounting throughout the curriculum and thus contribute to teaching for future applications. Within the scope of the study, an analysis of 215 peer-reviewed data analytics contributions, including 16 classroom applications, published from 2004 to 2018 in six journals, commonly referred to as accounting information system journals, is presented.

Kareem, Dauwed et al. (Citation2021) investigated the role of accounting information system and information management based on the low performance of Small and Medium Enterprises in Iraq due to limited use of accounting information systems and inability to benefit from information management capabilities. As the target audience, managers and business owners in SMEs using accounting information systems in Iraqi cities were determined, and the least square structural equation model was used by making 236 questionnaires for analysis. The results of the analysis showed that the accounting information system and information management capabilities have a positive and important role in increasing corporate performance. The study also revealed that knowledge management capabilities partially mediate between the accounting information system and organizational performance. Starting from here, it was concluded that SME managers and owners should focus on the accounting information system and pay more attention to information management capabilities in order to improve corporate performance.

Carrasco and Romi (Citation2021) explored the use of blockchain technology, the development and use of which they consider as a tool that can democratize competitive markets for vulnerable populations, supporting contentious entrepreneurs while “cooling” moral strife against the market. As a result, it has been mentioned that it demonstrates that blockchain has the potential to create reach, trust, and representation, especially in an age where trust is declining as it relates to a digital, globalized market.

Anggraeni and Winarningsih (Citation2021) aimed to determine the impact of the organizational framework on the quality of accounting information systems and its effects on the financial situation. The study included 72 participants in the positions of general manager, accounting and finance manager, and accounting and finance staff from a 24-star hotel in Bandung, Indonesia. As a result of the analysis using structural equation modeling, it has been determined that the overall institutional framework has a dominant effect on the implementation of quality accounting information systems and directly and indirectly supports the production of quality accounting information.

Ngo et al. (Citation2021) analyzed the impact of internal control on the quality of accounting information in paper manufacturing businesses in Vietnam. Research data were collected through emails and face-to-face interviews with managers, employees, and accountants of 56 paper manufacturing businesses in Vietnam. The research results show that the control environment in Vietnamese paper manufacturing enterprises has a positive effect on the quality of accounting information, including the accounting information system and internal control procedures.

The study, built on adaptive structuring theory by Nguyen et al. (Citation2021), investigated how regulatory changes in accounting, especially international financial reporting standards, affect the use of accounting information system and thus affect the performance of the accounting process. The data analyzed within the scope of the research were collected through a survey study involving 250 accountants from 36 countries who currently use international financial reporting standards as accounting standards. Evaluation results show that perceived system constraint, IT professional support, and accountant self-efficacy significantly explain loyalty of allocation (FOA), but not the perceived effectiveness of controls over IT use.

Singh et al. (Citation2021) developed a problem-solving approach to improve applied learning in database design, considering that significant changes in accounting information systems in modern businesses necessitate revisions in accounting curricula. The current industry prefers students who are equipped with hands-on learning projects that involve solving problems in real-life situations rather than following them. In the developed teaching module, students not only gain confidence in working by correcting a partially completed database with flaws deliberately placed by the instructor but also learn valuable concepts in database design.

Monteiro and Cepêda (Citation2021), with their bibliometric study, aimed to provide a state-of-the-art overview in accounting information systems research, analyzing scientific production characteristics and determining research trends in this regard. Within the scope of the study, they conducted a bibliometric analysis on 144 articles published in journals indexed in the Web of Science database, focusing especially on accounting information systems. While the first article on this field was published in 1973, the year with the highest number of accounting information systems studies was 2020. In addition to these results, the authors, journals, organizations, and countries/regions that contributed the most to the development of accounting information system research are among the results obtained as a result of the analysis.

The case study developed by Sledgianowski et al. (Citation2021) to analyze a large dataset of simulated US federal individual income tax returns of students of taxation and accounting information systems to determine the potential effects of tax changes on different individual taxpayers. It allows them to use data analysis software for the student outcomes that are thought to emerge after this application are stated as follows: (1) developing basic knowledge and skills about data analytics and how these skills can be used to visualize data to make it more meaningful, (2) demonstrating an understanding of the law regarding individual taxation, and (3) demonstrating information on how the law affects different types of filers.

Faccia and Petratos (Citation2021) conducted a literature study on the continuous development and applications of blockchain or the broader distributed ledger technology (DLT), which can overcome and improve some limitations of centralized systems today, especially security and privacy. Considering the results of the investigation, it is demonstrated that blockchain applications can have significant benefits and that Blockchain can facilitate integration at multiple levels and better serve a variety of purposes such as auditing compliance.

Shi (Citation2021) states in their studies that e-commerce affects many areas as well as the environmental structure of the traditional accounting industry and this causes the digitalization of accounting and the expansion of the economic environment of the new accounting industry. Due to the rapid development of e-commerce, traditional internal audit plans of enterprises cannot keep up with accounting and digitalization, which limits further development of e-commerce. In the study, the effect of the digitalization of accounting on the internal audit part of e-commerce was analyzed and internal audit was examined based on the example of an H firm.

Murad et al. (Citation2021) aimed to investigate the factors affecting the management decisions of manufacturing enterprises in Ethiopia. By including 140 manufacturing companies in the analysis, the effects of accounting information system, manager experience, manager education level, environmental factors, and organization size on management decisions were evaluated with the help of multiple regression analysis. It has been revealed that there is a significant and positive relationship between accounting information systems, manager experience, manager education level, environmental factors, and management decisions. In addition, it has been determined that there is a negative and insignificant relationship between management decisions and the size of the organization.

Zada et al. (Citation2021) analyzed the impact of financial management practices on small and medium-sized forest enterprises in Pakistan’s emerging economy. The research focuses on five financial management practices: working capital management, financial reporting, accounting information systems, investment decisions, and financing. For the analysis, data were collected from the owners, finance managers, and other finance personnel of 260 small and medium-sized forest enterprises and regression analysis was applied. The results obtained from the analyzes; demonstrated that higher levels of working capital management, financial reporting, accounting information systems, investment decisions, and financing practices are positively associated with financial performance and firm growth. The results also revealed a significantly strong positive correlation between financial management practice and firm growth.

The study by Tingey-Holyoak et al. (Citation2021) investigated the failure of integrating accounting information systems with agricultural data in detail and developed an integrated accounting and agricultural information system model by setting goals for the solution. Using data from a case study on a potato farm in Murraylands, South Australia, it integrated accounting data with soil moisture and climate data to monitor, alert, and inform irrigation decisions. Thus, the development of model-based preliminary digital software by tracking cost information has demonstrated how alerts and forecasts can be supported by combining accounting information systems and sensing technology.

The case study by Cheng and Varadharajan (Citation2021) was developed using US Revenue Service Revenue Statistics Program (IRS SOI) data to help students understand the power of data analysis in identifying potential policy issues facing state governments. The learning objectives set by the authors for this case study post are as follows: (1) improving students’ extraction, transformation, and loading (ETL) skills; (2) improve students’ data visualization skills; (3) to develop students’ critical thinking skills; and (4) to develop students’ effective oral and written communication skills. The pre- and post-learning assessment questionnaires and answers to open-ended questions within the scope of the study show that the case met these learning objectives.

Banker et al. (Citation2021) evaluated the effects of technical debt, which means that the software is not developed with the desired quality and quality deficiencies during software development, on the performance of the firm knowingly or unknowingly. In this study, they examined the economic effects of technical debt accumulated over an 11-year period in the customer relationship management (CRM) systems of 26 companies. In the study, it has been determined that firms operating in sectors with higher competitive threats tend to accumulate more technical debt. The analysis reveals that the technical debt accumulated in the customer relations methods systems negatively affects the performance of the firms, which is measured by the ratio of gross profit to total assets. It is estimated that a 10% increase in technical debt reduces the return on assets by an average of 16%. According to the authors, the negative impact of technical debt on return on assets increases throughout the life cycle of systems and significantly reduces the long-term operating value of these systems.

Kareem, Aziz, et al. (Citation2021), in order to examine small and medium enterprises (SMEs) in Iraq in terms of the relationship between innovation-mediated accounting information systems (AIS) use, knowledge management capabilities (KMC), and organizational performance (OP), have done the work. Within the scope of the study, 312 questionnaires were made and the structural equation model was used for analysis. From the results obtained from the analysis, it has been shown that the use of accounting information system and knowledge management capabilities has a positive and significant effect on innovation, while all three structures have a positive and significant effect on the organizational performance of SMEs. In addition, all dimensions of accounting information system use (decision-making, control process, operational efficiency, planning process, and financial reporting, etc.) and all dimensions of information management capabilities (information acquisition, information sharing, and information use) have a positive effect on organizational performance.

Huy and Phuc (Citation2021) conducted this research to examine the link between emotional intelligence (EI), blockchain technology application (BLO), and the effectiveness of the accounting information system (AIS). Structural equation modeling was applied to the survey-based data obtained from 412 participants to validate the model hypotheses. The results of the analysis revealed the impact of emotional intelligence on the application of blockchain technology. In addition, according to the findings of the study, it has been determined that the application of blockchain technology is also important on the efficiency of the accounting information system.

Søgaard (Citation2021), with this study based on the participation of the Danish Trade Authority and following a design science research (DSR) approach, value added tax (VAT) settlement, and DLT enabled by DLT and design principles, developed a platform prototype to design platforms. The prototype and design principles proposed in the study show how accounting information systems, DLT, and public administration can be interrelated to increase social welfare.

5. Conclusion

In today’s global competitive environment, it is possible for businesses to compete with their competitors and gain competitive advantage against their competitors by using accounting information systems effectively and efficiently. One of the main tasks of the accounting information system is to provide information users at all levels; is to provide reliable and easy-to-understand information to be used in planning and auditing activities at the required time and place. Changing conditions lead accounting information systems to renew and contribute more to business management. Accounting information systems are becoming one of the most important tools for businesses to gain competitive advantage over their competitors. Businesses that use the accounting information system accurately and reliably can provide cost control. This situation increases the capacity of enterprises to compete in international markets with their competitors at the right price.

In this study, a literature review was conducted within the scope of studies on accounting information system. Literature review was preferred as the method of the study. In the first stage of this study, a search was made based on the keyword “accounting information system” in the journals scanned in the Web of Science database, and publications related to this subject were compiled. The biggest reason for choosing this database is that the data required for analysis can be easily compiled and it is the most widely accepted and frequently used database in the scientific literature. In addition, since Web of Science includes many journals in the field of accounting, it is possible to reach a sufficient number of articles to be used in the study.

In this study, the article studies related to the accounting information system in the world under this subject were examined with the bibliometric analysis method, and the 20 most cited and the most recent 40 studies among these studies were evaluated in terms of subject, method, and result.

Within the scope of the study, when we look at the results of the searches carried out in the Web of Science database between 1985 and 2022 regarding the subject of “accounting information system”, the first studies were in 1985. It was determined that the most publications were made in 2020. When the examined publications are evaluated in terms of countries, it is revealed that the only country that exceeds the limit of 100 publications is the USA, followed by Indonesia, Australia, and China, respectively. While there is a big difference between the USA and its followers in the citation numbers of these publications, it is seen that the most active publications are based in Taiwan and South Korea.

In the distribution of the examined publications by universities, 20 universities with 4 or more publications were identified. It is seen that there is no prominent institution in which universities have publications close to each other. Iowa State University from the USA is at the top of the list with seven publications.

When the authors of the publications identified under the accounting information system are examined, it was found that while the number of authors who have three or more publications in the Web of Science database is 20, it has been determined that Diane J. Janvrin has the most publications with 7 publications. When we look at the distribution of the publications covered in the study to the journals, it is seen that 20 journals with at least 4 publications emerge, while three of these journals (International Journal of Accounting Information Systems, Issues in Accounting Education and Journal of Information Systems) host more than 20 publications.

Finally, when the publications discussed are evaluated in terms of keywords, the accounting information system keyword is incomparably dominant with its four different forms in the table due to spelling differences. It is seen that it is followed by words such as accounting (accounting), SME (Smes), information systems (information systems), data analysis (data analytics), and management accounting.

In the last part of the study, which was carried out on the criteria of citation and actuality, first of all, the literature of the 20 most cited studies was carried out, and the research topics of the articles most used by the researchers and their methods and results were included. Thus, a map of the most used publications from the past to the present has been drawn up. At the time of publication, which was determined as the second criterion, the evaluations of the 40 most recently published publications were shared, and it was tried to reveal which topics and their results are currently discussed.

With these results, it is thought that the aim of being a guide for new studies to be prepared by revealing the appearance of publications made under the subject of accounting information system has been achieved. In future studies, in light of these data, it will be possible to collaborate with which authors, in which channels to publish, and so on. Considering the issues, a plan can be created accordingly.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Abernethy, M. A., & Vagnoni, E. (2004). Power, organization design and managerial behaviour. Accounting Organization and Behaviour, 29(3–4), 207–25. https://doi.org/10.1016/S0361-3682(03)00049-7

- Al-Hattami, H., Abdullah, A., Kabra, J., Alsoufi, M., Gaber, M., & Shuraim, A. (2022). Effect of AIS on planning process effectiveness: A case of SMEs in A less developed nation. The Bottom Line, 35(2/3), 33–52. https://doi.org/10.1108/BL-01-2022-0001

- Al-Htaybat, K., & von Alberti-Alhtaybat, L. (2017). Big data and corporate reporting: Impacts and paradoxes. Accounting Auditing Journal, 30(4), 850–873. https://doi.org/10.1108/AAAJ-07-2015-2139

- Allah, T., August, P., Bhaza, S., Chigovanyika, T., Dyan, U., Muteweye, T., Ngcoza, M., Tshiwula, N., Qambela, V., Vooi, Y., & Bruwer, J. P. (2013). Accounting information systems in the fast food industry: A valuable tool for small business survival. African Journal of Business Management, 7(4), 260–264. https://doi.org/10.5897/AJBM12.1307

- Al-Matari, A., Amiruddin, R., Aziz, K., & Al-Sharafi, M. (2022). The impact of dynamic accounting information system on organizational resilience: The mediating role of business processes capabilities. Sustainability, 14(9), 1–22. https://doi.org/10.3390/su14094967

- Anggraeni, A., & Winarningsih, S. (2021). The effects of accounting information system quality on financial performance. Economic Annals-ХХI, 193(9–10), 128–133. https://doi.org/10.21003/ea.V193-16

- Astuty, W., Pratama, I., Basir, I., & Harahap, J. (2022). Does enterprise resource planning lead to the quality of the management accounting information system? Polish Journal of Management Studies, 25(2), 93–107. https://doi.org/10.17512/pjms.2022.25.2.06

- Banker, R., Liang, Y., & Ramasubbu, N. (2021). Technical Debt and Firm Performance. Management Science, 67(5), 3174–3194. https://doi.org/10.1287/mnsc.2019.3542

- Barton, A. (2005). Professional accounting standards and the public sector - a mismatch. Abacus, 41(2), 138–158. https://doi.org/10.1111/j.1467-6281.2005.00173.x

- Brazel, J. F., & Agoglia, C. R. (2007). An examination of auditor planning judgements in a complex accounting information system environment. Contemporary Accounting Research, 24(4), 1059. https://doi.org/10.1506/car.24.4.1

- Bruwer, J. P., Le Roux, S., & Smit, Y. (2018). The effectiveness of financial and accounting information systems used in South African SMMEs as decision-making tools. Southern African accounting association (SAAA) national teaching and learning and regional conference proceedings, 105–124. https://www.academia.edu/38272227/The_Effectiveness_of_Financial_and_Accounting_Information_Systems_Used_in_South_African_SMMEs_as_Decision_making_Tools

- Carrasco, H., & Romi, A. (2021). Toward an omniopticon: The potential of blockchain technology toward influencing vulnerable populations in contested markets. Accounting, Auditing & Accountability Journal, 35(7), 1685–1713. https://doi.org/10.1108/AAAJ-08-2020-4732

- Chen, X., Guang, C., & Hua, D. (2022). Credibility analysis of accounting cloud service based on complex network. Journal of Sensors, 2022, 1–11. https://doi.org/10.1155/2022/5420772

- Cheng C and Varadharajan A. (2021). Using Data Analytics to Evaluate Policy Implications of Migration Patterns: Application for Analytics, AIS, and Tax Classes. Issues in Accounting Education, 36(2), 111–128. https://doi.org/10.2308/ISSUES-19-09810.2308/iace-52952.s01

- Choe, J. M. (1998). The effects of user participation on the design of accounting information systems. Information&Management, 34(3), 185–198. https://doi.org/10.1016/S0378-7206(98)00055-X

- Choe, J. M. (2004a). The relationships among management accounting information, organizational learning and production performance. Journal of Strategic Information Systems, 13(1), 61–85. https://doi.org/10.1016/j.jsis.2004.01.001

- Choe, J. M. (2004b). The consideration of cultural differences in the design of information systems. Information&Management, 41(5), 669–684. https://doi.org/10.1016/j.im.2003.08.003

- Corcoles, Y. R., Penalver, J. F. S., & Ponce, A. T. (2011). Intellectual capital in Spanish public universities: Stakeholders’ information needs. Journal of Intellectual Capital, 12(3), 356. https://doi.org/10.1108/14691931111154689

- Coyne J G, Summers S L, Williams B and Wood D A. (2010). Accounting Program Research Rankings by Topical Area and Methodology. Issues in Accounting Education, 25(4), 631–654. https://doi.org/10.2308/iace.2010.25.4.631

- Dilla, W., Janvrin, D. J., & Raschke, R. (2010). Interactive data visualization: New directions for accounting information systems research. Journal of Information Systems, 24(2), 1–37. https://doi.org/10.2308/jis.2010.24.2.1

- Ezzamel, M., & Bourn, M. (1990). The roles of accounting information-systems in an organization experiencing financial crisis, 15 (5). Accounting Organizations and Society.

- Faccia, A., & Petratos, P. (2021). Blockchain, enterprise resource planning (ERP) and accounting information systems (AIS): Research on e-procurement and system integration. Applied Sciences, 11(15), 1–17. https://doi.org/10.3390/app11156792

- Fitrios, R., Nur, E., & Zakya, I. (2022). How information technology and user competence affect the quality of accounting information through the quality of AIS. Quality Access to Success, 23(187), 109–118. https://doi.org/10.47750/QAS/23.187.13

- Gazi, F., Atan, T., & Kılıç, M. (2022). The assessment of internal indicators on the balanced scorecard measures of sustainability. Sustainability, 14(14), 1–19. https://doi.org/10.3390/su14148595

- Guo, Y. (2022). Data source analysis of computerized management accounting based on data warehouse and mobile edge computing. Wireless Communications and Mobile Computing, 2022, 1–11. https://doi.org/10.1155/2022/3216180

- Hamundu, F., Husin, M., & Baharudin, A. (2021). Accounting information system adoption among Indonesian msmes: A conceptual model for cloud computing. Journal of Engineering Science and Technology, 16(6), 4438–4451. https://jestec.taylors.edu.my/Vol%2016%20Issue%206%20December%20%202021/16_6_6.pdf

- Hladika, M., & Žmuk, B. (2021). Exploring the level of utilizing management reports in decision-making in Croatian companies. Management: Journal of Contemporary Management Issues, 26(2), 63–78. https://doi.org/10.30924/mjcmi.26.2.4

- Huy, P., & Phuc, V. (2021). Accounting information systems in public sector towards blockchain technology application: The role of accountants’ emotional intelligence in the digital age. Asian Journal of Law and Economics, 12(1), 73–94. https://doi.org/10.1515/ajle-2020-0052

- İbrahim, F., Ali, D. N. H., & Besar, N. S. A. (2020). Accounting information systems (AIS) in SMEs: Towards an integrated framework. International Journal of Asian Business and Information Management, 11(2), 51–67. https://doi.org/10.4018/IJABIM.2020040104

- Kareem, H., Aziz, K., Maelah, R., Yunus, Y., Alsheikh, A., & Alsheikh, W. (2021). The influence of accounting information systems, knowledge management capabilities, and innovation on organizational performance in Iraqi SMEs. International Journal of Knowledge Management, 17(2), 72–103. https://doi.org/10.4018/IJKM.2021040104

- Kareem, H., Dauwed, M., Meri, A., Jarrar, M., Al-Bsheish, M., & Aldujaili, A. (2021). The role of accounting information system and knowledge management to enhancing organizational performance in Iraqi SMEs. Sustainability, 13(22), 1–13. https://doi.org/10.3390/su132212706

- Kelton, A. S., Pennington, R. R., & Tuttle, B. M. (2010). The effects of information presentation format on judgment and decision making: A review of the information systems research. Journal of Information Systems, 24(2), 79–105. https://doi.org/10.2308/jis.2010.24.2.79

- Kile C O and Phillips M E. (2009). Using Industry Classification Codes to Sample High-Technology Firms: Analysis and Recommendations. Journal of Accounting, Auditing & Finance, 24(1), 35–58. https://doi.org/10.1177/0148558X0902400104

- Kobelsky, K. W., Vernon, J. R., Rodney, E. S., & Ve Robert, W. Z. (2008). Determinants and consequences of firm information technology budgets. Accounting Rewiev, 83(4), 957–995. https://doi.org/10.2308/accr.2008.83.4.957

- Li, X. (2022). Optimization of accounting information system for enterprises in smart city by intelligent sensor under the internet of things. Wireless Communications and Mobile Computing, 2022, 1–11. https://doi.org/10.1155/2022/6205940

- Li, F., & Fang, G. (2022). Process-aware accounting information system based on business process management. Wireless Communications and Mobile Computing, 2022, 1–15. https://doi.org/10.1155/2022/7266164

- Liu, Q., Chiu, V., Muehlmann, B., & Baldwin, A. (2021). Bringing scholarly data analytics knowledge using emerging technology tools in accounting into classrooms: A bibliometric approach. Issues in Accounting Education, 36(4), 153–181. https://doi.org/10.2308/ISSUES-19-079

- Lu, Z. (2022). Encryption management of accounting data based on DES algorithm of wireless sensor network. Wireless Communications and Mobile Computing, 2022, 1–14. https://doi.org/10.1155/2022/7203237

- Lutfi, A. (2022). Factors influencing the continuance intention to use accounting information system in Jordanian SMEs from the perspectives of UTAUT: Top management support and self-efficacy as predictor factors. Economies, 10(4), 1–17. https://doi.org/10.3390/economies10040075

- Lutfi, A., Al-Khasawneh, A., Almaiah, M., Alsyouf, A., & Alrawad, M. (2022). Business Sustainability of Small and Medium Enterprises during the COVID-19 Pandemic: The Role of AIS Implementation. Sustainability, 14(9), 1–20. https://doi.org/10.3390/su14095362

- Lutfi, A., Al-Okaily, M., Alsyouf, A., & Alrawad, M. (2022). Evaluating the D&M IS success model in the context of accounting information system and sustainable decision making. Sustainability, 14(13), 1–17. https://doi.org/10.3390/su14138120

- Malitha, R., & Nadarajah, R. (2022). Quality of accounting information systems and organizational effectiveness in an emerging country. SMART Journal of Business Management Studies, 18(1), 22–29. https://doi.org/10.5958/2321-2012.2022.00003.3

- Mauldin E G and Ruchala L V. (1999). Towards a meta-theory of accounting information systems. Accounting, Organizations and Society, 24(4), 317–331. https://doi.org/10.1016/S0361-3682(99)00006-9

- Monteiro, A., & Cepêda, C. (2021). Accounting Information Systems: Scientific Production and Trends in Research. Systems, 9(3), 1–25. https://doi.org/10.3390/systems9030067

- Monteiro, A., Vale, J., Leite, E., Lis, M., & Kurowska-Pysz, J. (2022). The impact of information systems and non-financial information on company success. International Journal of Accounting, 45, 1–14. https://doi.org/10.1016/j.accinf.2022.100557

- Monteiro, A., Vale, J., & Silva, A. (2021). Factors determining the success of decision making and performance of Portuguese companies. Administrative Sciences, 11(4), 1–24. https://doi.org/10.3390/admsci11040108

- Murad, T., Tamiru, B., Saleh, A., Elliam, A., Ahmed, H., & Hamed, M. (2021). Factors influencing management decisions of manufacturing companies in Ethiopia. SMART Journal of Business Management Studies, 17(2), 86–93. https://doi.org/10.5958/2321-2012.2021.00020.8

- Ngo, H., Luu, D., & Truong, T. (2021). The relationship between internal control and accounting information quality: Empirical evidence from manufacturing sector in Vietnam. The Journal of Asian Finance, Economics and Business, 8(10), 353–359. https://doi.org/10.13106/jafeb.2021.vol8.no10.0353

- Nguyen, T., Chen, J., & Nguyen, T. (2021). Appropriation of accounting information system use under the new IFRS: Impacts on accounting process performance. Information & Management, 58(8), 1–15. https://doi.org/10.1016/j.im.2021.103534

- Pacini, C., Wossink, A., Giesen, G., Vazzana, C., & Ve R, H. (2003). Evaluation of sustainability of organic, integrated and conventional farming systems: A farm and field-scale analysis. Agriculture Ecosystems, 95(1), 273–288. https://doi.org/10.1016/S0167-8809(02)00091-9

- Ruivo, P., Oliveira, T., & Neto, M. (2014). Examine ERP post-implementation stages of use and value: Empirical evidence from Portuguese SMEs. International Journal of Accounting Information Systems, 15(2), 166–184. https://doi.org/10.1016/j.accinf.2014.01.002

- Schneider, G. P., Dai, J., Janvrin, D. J., Ajayi, K., & Raschke, R. L. (2015). Infer, predict, and assure: Accounting opportunities in data analytics. Accounting Horizons, 29(3), 719–742. https://doi.org/10.2308/acch-51140

- Shareia, B. (2016). Accounting information systems in developing countries. Journal of Business & Economic Policy, 3(1), 46–57. https://www.jbepnet.com/journals/Vol_3_No_1_March_2016/5.pdf

- Shi, W. (2021). Research on the influence of accounting computerization and networking on E-commerce. EURASIP Journal on Wireless Communications and Networking, 1–12. https://doi.org/10.1186/s13638-021-02024-z

- Singh, A., Bhadauria, V., & Gurung, A. (2021). A problem-solving-based teaching approach to database design. Journal of Emerging Technologies in Accounting, 18(2), 149–155. https://doi.org/10.2308/JETA-19-10-13–41

- Singh, H., & Singh, A. (2022). Understanding Inhibitors to XBRL Adoption: An Empirical Investigation. Accounting Research Journal, 35(5), 598–615. https://doi.org/10.1108/ARJ-05-2021-0144

- Sledgianowski, D., Petra, S., Pelaez, A., & Zhu, J. (2021). Using Tableau to analyze the effects of tax code changes: A teaching case for tax and AIS courses. Issues in Accounting Education, 36(3), 117–133. https://doi.org/10.2308/ISSUES-19-127

- Søgaard, J. (2021). A Blockchain-Enabled Platform for VAT Settlement. International Journal of Accounting Information Systems, 40, 1–18. https://doi.org/10.1016/j.accinf.2021.100502

- Stair, R. M., & Reynolds, G. W. (2012). Principles of Information Systems (Tenth) ed.). Course Technology Inc.

- Thuan, P., Khuong, N., Anh, N., Hanh, N., Thi, V., Tram, T., & Han, C. (2022). The determinants of the usage of accounting information systems toward operational efficiency in industrial revolution 4.0: Evidence from an emerging economy. Economies, 10(4), 1–19. https://doi.org/10.3390/economies10040083

- Tingey-Holyoak, J., Pisaniello, J., Buss, P., & Mayer, W. (2021). The importance of accounting-integrated information systems for realising productivity and sustainability in the agricultural sector. International Journal of Accounting Information Systems, 41, 1–19. https://doi.org/10.1016/j.accinf.2021.100512

- Wang, Y., Wang, T., Zhao, R., & Lun, X. (2022). Research on the construction of accounting informatics system and risk assessment method in big data’s Era. Discrete Dynamics in Nature and Society, 2022, 1–9. https://doi.org/10.1155/2022/7673807

- Wiersma, E. (2009). For which purposes do managers use balanced scorecards? An Empirical Study, Management Accounting Research, 20(4), 239–251. https://doi.org/10.1016/j.mar.2009.06.001

- Wilson, D. C., Velis, C., & Cheeseman, C. (2006). Role of informal sector recycling in waste management in developing countries. Habitat International, 30(4), 797–808. https://doi.org/10.1016/j.habitatint.2005.09.005

- Worrell, J. L., Di Gangi, P. M., & Bush, A. A. (2013). Exploring the use of the Delphi method in accounting information systems research. International Journal of Accounting Information Systems, 14(3), 193–208. https://doi.org/10.1016/j.accinf.2012.03.003

- Worrell, J., Wasko, M., & Johnston, A. (2013). Social network analysis in accounting information systems research. International Journal of Accounting Systems, 14(2), 127–137. https://doi.org/10.1016/j.accinf.2011.06.002