Abstract

This study investigates the extent to which tax literacy, power, and trust strengthen tax attitudes in Indonesian micro, small, and medium enterprises. To meet this objective, this study analyzes (1) the effect of tax literacy on trust and power, (2) the effect of trust and power on voluntary compliance and tax avoidance, and (3) the direct and indirect effects of tax literacy on voluntary compliance and tax avoidance through trust and authority. The findings indicate that tax literacy is very important in determining trust and power. Further, trust and tax authority are important to create a synergistic climate that encourages increased voluntary compliance. Despite evidence that trust in tax authorities is likely to reduce tax evasion, the power of tax authorities had no significance in determining tax evasion. In this case, power was present solely because of the tax obligations imposed through tax regulations rather than legitimacy. Additionally, this study found that trust in authority and the power of authority mediate the relationship between tax literacy and voluntary compliance. Hence, it demonstrates that voluntary compliance depends on whether or not trust and power create legitimacy in the view of taxpayers. A stronger perception of trust and power can ultimately increase tax compliance. For SMEs, the role of tax literacy is crucial, as it helps SMEs understand the facilities provided by the government in the form of tax privileges or facilities. This research uncovered the importance of tax knowledge and its benefits for SMEs in terms of understanding their situation regarding tax. Further, SMEs would be better placed to understand the privileges provided by the government if tax administration principles were simplified.

1. Introduction

Tax attitude is an important issue in tax psychology research because it can indicate the behavior of taxpayers (Kirchler et al., Citation2008). Taxpayers’ attitudes may be positive or negative (Damayanti et al., Citation2020). A positive (negative) attitude indicates an individual’s positive (negative) evaluation of an object. Taxpayers whose attitude toward tax compliance is positive are more compliant than those whose attitude is negative. On the other hand, taxpayers who have a positive attitude toward tax evasion are less compliant than those with a negative attitude (Kirchler et al., Citation2008).

Tax compliance research has evolved over time. The Slippery Slope Framework underlies modern tax compliance studies. The framework shows that trust in authorities (trust) and perceived power of authorities (power) are relevant dimensions in determining tax compliance (Kastlunger et al., Citation2013; Kirchler et al., Citation2008; Muehlbacher & Kirchler, Citation2010). The Slippery Slope Framework distinguishes an antagonistic climate from a synergistic climate, with both of these potentially creating maximum tax compliance (Iqbal & Sholihin, Citation2019; Kirchler et al., Citation2008). In an antagonistic climate, taxpayers and tax authorities work in opposite directions so that the social distance between the two parties becomes wide. In contrast, in a synergistic climate, both parties work cooperatively, narrowing their social distance (Kirchler et al., Citation2008).

The individual factors of taxpayers, including literacy and knowledge (Kirchler et al., Citation2008), determine trust and power. Better tax knowledge is associated with increased trust, while weak knowledge will lead to distrust because of a lack of awareness and understanding of tax law. On the other hand, a good understanding of efforts to enforce tax obligations and the effectiveness of these efforts will determine power.

Scholars have begun to research tax literacy. Tax literacy is seen as crucial to overcoming the tax system’s complexity to increase tax compliance (T. Brackin, Citation2014; Freudenberg et al., Citation2017; Nichita et al., Citation2019; Pham et al., Citation2021; Toni Brackin, Citation2007). The complexity and uncertainty of the tax system often mean taxpayers do not know what to pay in taxes (Musimenta & Ntim, Citation2020). However, knowledge about taxation is also needed in carrying out tax avoidance (Cechovsky, Citation2018). Various studies that have been conducted have not shown solid empirical evidence regarding the role of tax literacy in determining tax attitude. Tax literacy is considered to have the ability to determine trust and power (Kirchler et al., Citation2008), while trust and power have an influence on tax attitude (Batrancea et al., Citation2019; Hofmann et al., Citation2008; Inasius et al., Citation2020; Kogler et al., Citation2013; Muehlbacher et al., Citation2011).

Currently, no empirical research has identified the impact of tax literacy, trust, and power on voluntary tax compliance and tax evasion in micro, small, and medium enterprises (MSMEs), especially in the context of an emerging economy. MSMEs have contributed to the Indonesian economy by absorbing 96.92% of the workforce and accounted for an astonishing 60.51% of Indonesia’s total GDP in 2019. Although the role of SMEs in Indonesia’s economic development is highly significant, their contribution to total tax revenue is meager. Based on data from the Directorate General of Taxes in 2019, the ratio of MSME tax revenue to total tax revenue is 0.36%. Therefore, there is a critical need to improve tax literacy in SMEs. This study seeks to fill this gap by determining the impact of tax literacy, trust, and power of tax authorities on voluntary tax compliance and tax evasion, and further investigates the mediating role of trust and power.

2. Literature review and hypotheses development

2.1. Relevance of Trust and Power with Tax Literacy

Tax literacy is a fundamental concept in the taxation literature and is closely related to financial literacy (T. Brackin, Citation2014; Cvrlje, Citation2015). From a resource-based theory perspective, financial literacy, which includes knowledge, skills, experience, and reputation, is a form of intangible asset that organizations must own to survive (Mutamimah et al., Citation2021). Financial literacy can be viewed through the lens of the consumer behavior model framework, which provides a more comprehensive perspective, focusing on information and knowledge, and is expected to encourage an individual’s behavioral change (T. Brackin, Citation2014).

According to Nichita et al. (Citation2019), tax literacy is a taxpayer’s ability to understand their rights and obligation to utilize tax knowledge and expertise to determine appropriate reporting to bolster the effect this has on tax regulation compliance. It is also described as a person’s knowledge that enables effective management of tax matters (Puneet Bhushan, Citation2013). Tax literacy represents a higher understanding, and its effect on tax compliance has been proven (Freudenberg et al., Citation2017; Nichita et al., Citation2019). Thus, tax literacy can counter the problematic aspects of the tax system, which is often criticized for being too complex and difficult to understand (Kirchler et al., Citation2008; Toni Brackin, Citation2007).

Taxpayer literacy is an individual aspect that determines trust and power (Kirchler et al., Citation2008). Trust can arise from a sufficient knowledge of regulatory frameworks and consequences; conversely, insufficient knowledge can trigger distrust. Increased taxpayer literacy is believed to increase trust in tax authorities since good knowledge can simplify complex tax systems. In addition, tax knowledge enhances the power (of tax authorities). Understanding efforts to enforce tax regulations through tax audits and their effectiveness also strengthens power (Kirchler et al., Citation2008). Based on these arguments, the relevant hypotheses as formulated (see ) in this study are:

Hypothesis 1: Tax literacy has a positive influence on trust.

Hypothesis 2: Tax literacy has a positive influence on power.

Figure 1. Conceptual framework.

2.2. Relevance of trust and power to tax attitude

The Slippery Slope Framework describes the role of the trust–power dyad as an interaction between government and society. These interactions move between synergistic and antagonistic climates (Kirchler et al., Citation2008; Muehlbacher & Kirchler, Citation2010). A synergistic climate is based on the notion that tax authorities provide services to the community and should, therefore, be aimed at diminishing the social distance between both. This encourages the emergence of voluntary compliance. In a synergistic climate, taxes paid by the community contribute economic value to the state as a form of obligation. On the contrary, there is a vast social distance between tax authorities and taxpayers under an antagonistic climate because of different perceptions of tax authorities (Kirchler et al., Citation2008).

Trust and power have become the focus of current tax compliance research and have been shown to determine tax compliance behavior (Kastlunger et al., Citation2013; Kirchler et al., Citation2008). Trust and power are closely related to the psychology of taxpayers. Trust describes the opinion of individuals and social groups that tax authorities have a benevolent nature and work for the common good (Kirchler et al., Citation2008). Taxpayers who do not trust the government are dubious as to how the taxes collected by the government will be spent (Aktaş Güzel et al., Citation2019). The trust that taxpayers have in tax authorities is related to respect and commitment, and motivates voluntary tax compliance. Power is defined as the taxpayer’s perception of the potential of tax officials to detect illegal tax evasion by, among others, conducting tax audits and enforcing penalties for evaders. The power dimension relates to taxpayers’ knowledge and attitude (Kirchler et al., Citation2008). The power of authorities to protect cooperative citizens is considered more efficient than coercive and punitive power (Kastlunger et al., Citation2013). Kastlunger et al. (Citation2013) distinguish power into coercive and legitimate, where coercive power is based on the expectation that authorities will punish non-compliance and legitimate power is related to the authority’s ability to ensure that taxpayers act cooperatively.

The interaction between trust and power is illustrated in the Slippery Slope Framework. Voluntary compliance can occur when trust in authority is high (Kirchler et al., Citation2008) and when people can accept the power shown by the authority (Kastlunger et al., Citation2013). Taxpayers are assumed to have the intention to withhold tax contributions that would be paid if the trust held is low. Tax compliance can be enforced when taxpayers have low trust, but authorities have substantial power to audit effectively and provide sanctions for wrong behavior. If trust and power are low, taxpayers will tend to violate the law and evade taxes (Kirchler & Wahl, Citation2010). Therefore, the research hypotheses are:

Hypothesis 3: Trust has a positive influence on voluntary compliance.

Hypothesis 4: Power has a positive influence on voluntary compliance.

Hypothesis 5: Trust has a negative influence on tax evasion.

Hypothesis 6: Power has a negative influence on tax evasion.

2.3. Relevance of tax literacy to tax attitude

Research on tax behavior reveals that the tendency of individuals to obey and cooperate with the government and tax authorities, in particular, is determined by economic and psychological aspects. The relevant economic aspects as determinants of tax compliance are tax rate, probability of audits, fines, and income (Alm et al., Citation2012; Hofmann et al., Citation2008). Nonetheless, the results of research on the economic aspect as a determinant of tax compliance show mixed evidence, indicated by psychological variables that moderate the inconsistent findings (Hofmann et al., Citation2008). In the absence of a consensus regarding economic determinants of tax behavior, the psychological perspective provides an alternative. The psychological determinants of tax compliance noted in the literature include tax literacy, taxpayers’ knowledge of tax law, attitudes toward the government, and taxation together with norms and justices (Alm et al., Citation2012; Hofmann et al., Citation2008; Nichita et al., Citation2019).

Various perspectives underlie the arguments and perspectives of researchers in considering what influences people to pay taxes. The notion that compliance is a decision taken by individuals under risk was a breakthrough in the study of tax compliance. The underlying idea is that taxpayers can declare their taxes honestly or choose a riskier option to engage in tax fraud (Alm, Citation2019; Alm et al., Citation2012). The economics-of-crime perspectives in the general economic theory of criminal behavior underscore the deterrent effect of government punishment if criminal acts are discovered, such as tax evasion (Allingham & Sandmo, Citation1972; Alm, Citation2019). This framework considers individuals as rational beings who are outcome-oriented, selfish, egoistic, and maximize personal gain, whose compliance is based on enforcement (Alm, Citation2019; Alm et al., Citation2012).

The behavior of taxpayers is divided into compliant and non-compliant. Tax compliance refers to the extent to which taxpayers comply with tax regulations. In contrast, tax non-compliance refers to the failure of taxpayers to fulfill their tax obligations, either intentionally or unintentionally (Randlane, Citation2016). Specifically, tax compliance is grouped into voluntary and enforced tax compliance (Kirchler et al., Citation2008; Muehlbacher & Kirchler, Citation2010; Randlane, Citation2016). Voluntary compliance means taxpayers voluntarily fulfill their obligations exclusive of tax authorities’ involvement, while enforced tax compliance means that tax compliance is achieved through the intervention of tax authorities. While non-compliant behavior is often associated with tax evasion and tax avoidance, the latter takes advantage of loopholes in the current legal boundaries (Muehlbacher & Kirchler, Citation2010), whereas tax evasion is considered illegal behavior. Tax non-compliance can be influenced by direct factors (non-compliance opportunity, tax system/structure, and attitude and perception) or indirect factors (demography and culture; Nuryanah et al., Citation2022).

Tax literacy motivates tax compliance actions, especially voluntary compliance (Kirchler et al., Citation2008; Nichita et al., Citation2019). The decision to comply with or avoid taxes is not only related to economic factors, it also arises from the taxpayer’s perception of the tax system (Fatas et al., Citation2021). The complexity of the taxation system can be overcome by increasing tax literacy (Toni Brackin, Citation2007), with improved knowledge also providing insight into the importance of taxes as a source of state revenue. In addition, good literacy will provide an understanding of tax law, reducing the tendency to undertake tax evasion actions (Cechovsky, Citation2018). Based on these thoughts, the relevant hypotheses are:

Hypothesis 7. Tax literacy has a positive influence on voluntary compliance.

Hypothesis 8. Tax literacy has a negative influence on tax evasion.

2.4. Relevance of trust and power to tax literacy and tax attitude

Research on attitude is important in studying tax behavior because attitude can indicate behavior. Attitude reflects positive and negative self-evaluation of certain objects. Thus, the assumption is that individual actions are driven by attitudes (Kirchler et al., Citation2008). Tax attitudes and compliance behavior are closely related to interactions with tax administrators (Kastlunger et al., Citation2013; Rashid et al., Citation2021a). Several studies have attempted to identify variables that shape taxpayer attitudes, including benefit fraud (Moro-Egido & Solano-García, Citation2020), threat of punishment (Mohdali et al., Citation2014), religiosity (Khalil & Sidani, Citation2020), perceived uncertainty and self-interest (Umit & Schaffer, Citation2020), and political ideology (Lozza et al., Citation2013). However, knowledge and literacy are implicitly mentioned as factors that can increase trust and power and shape tax compliance, especially voluntary compliance (Kirchler et al., Citation2008).

Based on the Slippery Slope Framework, trust and power have a role in determining tax compliance and non-compliance. Voluntary tax compliance is related to willingness to pay taxes as a form of citizen compliance. The Slippery Slope Framework explains that encouraging trust can increase voluntary compliance (Gangl et al., Citation2015; Kastlunger et al., Citation2013; Lozza et al., Citation2013). In addition, the voluntary cooperation of taxpayers can be determined by legitimate power based on legitimacy, knowledge, ability, and identification with those in power (Kastlunger et al., Citation2013). Tax authorities and taxpayers are the two dominant players in tax evasion (Nurkholis et al., Citation2020), defined as engagement in activities classified as unlawful. Increased trust will reduce the tendency toward tax evasion. Meanwhile, the authorities’ power plays a role in combating law violations to reduce tax evasion (Kastlunger et al., Citation2013). According to Kirchler et al. (Citation2008), both trust and power are determined by the literacy level of the taxpayers. Based on this logic, the hypotheses formulated to test the mediating role of trust and power in this study are:

Hypothesis 9. Trust mediates the influence of tax literacy on voluntary compliance.

Hypothesis 10. Power mediates the influence of tax literacy on voluntary compliance.

Hypothesis 11. Trust mediates the influence of tax literacy on tax evasion.

Hypothesis 12. Power mediates the influence of tax literacy on tax evasion.

3. Research method

This study is explanatory in nature and aims to test relevant hypotheses in the context of tax behavior. Tax literacy (Resmi et al., Citation2021) is employed as an exogenous variable in this study. Further, tax attitudes represented by voluntary compliance and tax evasion (Kirchler & Wahl, Citation2010) were employed as endogenous variables. In addition, the intervening variables utilized are perceived trust in authorities and perceived power of authorities (Kirchler et al., Citation2008).

This study employs established scales from previous studies. The tax literacy construct, derived from Resmi et al.’s (Citation2019, Citation2021) research, consists of nine items. Further, a three-item scale of trust (in authorities) and power (of authorities; Kirchler et al., Citation2008) was utilized. Finally, a 10-item voluntary compliance scale and a nine-item tax evasion scale were derived from Kirchler and Wahl (Citation2010). All scales were measured with a five-point Likert-type scale that aims to determine an individual’s degree of agreement with a given statement in the survey instruments.

In terms of sampling technique, this study employed a sampling frame for MSMEs in East Java, Indonesia, with a total n = 9,782,262 as the population. In determining the appropriate sample size, this study uses Slovin’s approach via an online sample size calculator, which determines the minimum sample size at a 95% confidence level. This approach shows that the minimum sample size representing appropriate statistical power is n = 385 (https://qualtrics.com). In addition, MSMEs were assigned as the unit of analysis since the owner/manager is a representative of a business unit or an organization.

Online and offline survey questionnaires were distributed as a means of data collection. This study obtained a total sample of n = 561, surpassing the minimum threshold (n = 385) to achieve adequate statistical power.

In terms of the analytical approach, this study utilized three statistical approaches: confirmatory factor analysis, descriptive statistical analysis, and inferential statistical analysis. Descriptive statistical analysis was conducted to determine the respondents’ demographic profile (frequency and percentage). Further, inferential statistical analysis was performed to test the relationship between the hypothesized variables via PLS-SEM as an inferential statistical analysis tool. In addition, this study tested validity and reliability assumptions. The validity test of the research instrument was carried out by assessing the Average Variance Extracted (AVE), with the provisions of construct validity being met if the AVE value was more than 0.50 (Hair et al., Citation2019, p. 687). The reliability test was carried out using Cronbach’s alpha, with a good reliability provision of more than 0.80 (Bougie & Sekaran, Citation2020, p. 271). In general, statistical “rules of thumb” suggested by prominent authors (Hair et al., Citation2019, p. 687; Bougie & Sekaran, Citation2020, p. 271) were employed to ensure that no statistical assumptions were violated.

4. Results and discussion

4.1. Descriptive statistics: SMEs’ demography

In total, 561 questionnaires could be used for data analysis. The statistical analyses describing the respondents’ demographics are shown in Table . The data indicate that SMEs in East Java comprised 545 micro-enterprises (82.35%), 12 small enterprises (2.14%), and four medium enterprises (0.71%). Of the total sample, 318 were male (56.68%) and 243 were female (43.32%). Respondents with a high school education numbered 389 (69.34%), while 139 respondents had a diploma/bachelor degree (24.78%), 23 respondents had completed junior high school education (4.1%), seven were elementary school graduates (1.25%), and three had completed a postgraduate program (0.53%). Of the total, 250 had been in business 5–9 years (44.56), 163 had been in business for 1–4 years (29.06%), 97 had been in business for more than 10 years (17.29%), and 51 had been in business for less than 1 year (9.09%). Most of the respondents (462 or 82.35%) were registered as taxpayers, while 99 (17.65%) were not.

Table 1. Respondent’s demographic characteristics (n = 561)

4.2. Construct measurement

Before conducting inferential analysis, reliability tests were performed to determine the consistency of the measurement items. Reliability testing was done by observing the value of Cronbach’s alpha. In general, reliability is considered weak if Cronbach’s alpha is less than 0.60; reliability with a value of 0.70 is acceptable, and a value of more than 0.80 indicates good reliability (Bougie & Sekaran, Citation2020, p. 271). Table shows the value of Cronbach’s alpha and AVE for each variable. Each variable has a Cronbach’s alpha value of more than 0.80, which means it has good reliability. Thus, in this study, all variables meet the criteria for reliability testing.

Table 2. Reliability and validity test

4.3. Hypothesis testing

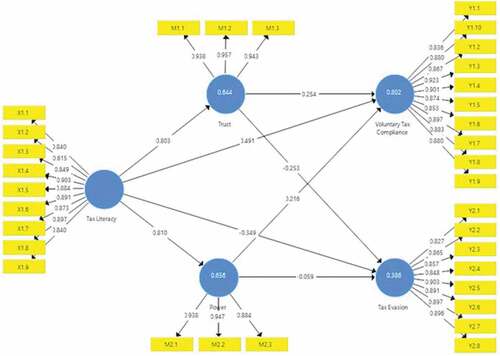

In this study, 12 hypotheses were tested using a statistical approach. PLS-SEM was used to determine the model-fit and path coefficients in determining each variable relationship in the model. Based on the test results of the model, the coefficient of determination (R2) is 0.644 for trust and 0.656 for power. These results indicate tax literacy’s ability to explain trust and power as mediating variables used in the study.

4.4. Tax literacy, trust, and power

Table shows the statistical results of the hypotheses testing to examine the effect of tax literacy on trust and power. Tax literacy was proven to be statistically significant on trust (p < 0.01) and power (p < 0.01). Tax literacy positively affects trust (0.803) as well as power (0.810). Therefore, hypothesis 1 and hypothesis 2 are accepted. This means that the higher the perceived tax literacy, the higher the perceived trust in authorities. Likewise, the increase in perceived tax literacy affects the perceived power of tax authorities. This is consistent with the view that literacy determines perceptions of trust and power (Kirchler et al., Citation2008). The better individuals’ literacy about taxes, the better their ability to understand complex tax systems (Toni Brackin, Citation2007). Therefore, trust in tax authorities will also increase. Further, good tax literacy enables individuals to perceive the effectiveness of tax law enforcement carried out by the authorities. Taxpayers will understand the ability of tax authorities to audit and detect tax fraud as a representation of power. Thus, the more literate individuals are, the higher their perception of the power of authorities (Kirchler et al., Citation2008).

Table 3. Statistical effect and hypotheses test

4.5. Trust, power, and voluntary compliance

The results of the analysis examining the influence of trust and power toward voluntary compliance are shown in Table . Trust is statistically proven to significantly affect voluntary tax compliance (p < 0.01). Likewise, power is proven to significantly influence voluntary compliance (p < 0.01). Voluntary compliance is positively influenced by trust and power (0.254 for trust) and (0.216 for power). Therefore, hypothesis 3 and hypothesis 4 are accepted. These results show that the higher the perceived trust in tax authorities, the higher taxpayers’ voluntary compliance. In addition, evidence supports the argument that an increase in the perceived power of tax authorities will improve perceived voluntary compliance. These results are consistent with the predictions of the Slippery Slope Framework (Kirchler et al., Citation2008), which argues that the interaction of perceived trust in authorities and the perceived power of authorities forms voluntary compliance. Perceived trust in authorities is related to respect for the government. Tax compliance is carried out as a voluntary obligation if the individual has high trust. On the other hand, an increase in the perceived power of tax authorities causes perceived voluntary compliance to increase. Individual perceptions of the authority’s ability to implement tax regulations effectively encourage compliance. High compliance can occur under two conditions: strong trust in authorities (Kirchler et al., Citation2008) or strong power of authorities, especially legitimate power (Kastlunger et al., Citation2013). Therefore, the results of this study are consistent with the Slippery Slope Framework and support previous research (Benk, Citation2012; Muehlbacher et al., Citation2011).

4.6. Trust, power, and tax evasion

The results of the statistical analysis for hypothesis 5 and hypothesis 6 are shown in Table , which shows that the effect of trust and power on tax evasion is not entirely in accordance with the predictions. Trust is statistically proven to have a significant negative effect on tax evasion (p < 0.01); however, power was not proven to significantly affect tax evasion (p > 0.01). Trust and power have a negative relationship with tax evasion, with each effect of −0.253 (trust) and −0.059 (power). Therefore, based on the analysis results, hypothesis 5 is accepted, but hypothesis 6 is not. Trust is described as an individual’s respect and positive feelings toward tax authorities. On the other hand, tax evasion is a form of non-compliance that arises from law violations and disobedience (Kirchler & Wahl, Citation2010). Therefore, the higher the trust in tax authorities, the lower the perceived tax evasion.

4.7. Tax literacy, voluntary compliance, and tax evasion

Table shows the analysis results examining the effect of tax literacy on voluntary compliance and tax evasion. Tax literacy is proven to have a significant effect on voluntary compliance (p < 0.01). In addition, tax literacy also has a significant effect on tax evasion (p > 0.01). Tax literacy positively affects voluntary compliance (0.491), while the effect of tax literacy on tax evasion is negative (−0.349). Therefore, hypothesis 7 and hypothesis 8 are accepted.

The results show that the higher the perceived tax literacy, the higher the voluntary compliance. On the other hand, an increase in perceived tax literacy will reduce perceived tax evasion. Tax literacy shows not only knowledge but also understanding of the tax system and law. The complexity of the tax system can be parsed and overcome by tax literacy (Toni Brackin, Citation2007). Therefore, the more literate an individual is, the greater his or her ability to understand the role and contribution of taxes as a source of state revenue and as a form of voluntary civic responsibility (Kirchler et al., Citation2008).

The results of this study also demonstrate the role of tax literacy in reducing tax evasion. Tax literacy will provide individual insights about tax law and the possibility of examination as well as sanctions and fines that can be imposed for violations of the law. Therefore, the better the individual understands the risk of non-compliance, the less perceived tax evasion there will be.

4.8. Mediating role of trust and power

Table shows the mediating effect of trust and power. The results of the analysis show that the coefficient of the direct influence of tax literacy on voluntary compliance (0.491) has decreased compared with the indirect effect of tax literacy on voluntary compliance through trust (0.204) and power (0.175). Thus, the data show that trust and power mediate the effect of tax literacy on voluntary tax compliance. Therefore, hypothesis 9 and hypothesis 10 are supported. Further, a mediating role of trust and power on the relationship between tax literacy and tax evasion is not fully supported by the data. Trust is proven to mediate the relationship between tax literacy and tax evasion, but power is not statistically significant in mediating the effect of tax literacy on tax evasion. Therefore, based on Table , hypothesis 11 is accepted, but hypothesis 12 is not.

The results of the analysis show that tax literacy can increase trust and power. Thus, trust and power lead to higher voluntary compliance. Therefore, trust and power are proven to be mediators between tax literacy and voluntary compliance. These results are in accordance with the explanation of Kirchler et al. (Citation2008) about how literacy skills encourage the role of trust and power, which then determine the voluntary compliance of individuals. In addition, trust is proven to negatively mediate tax literacy and tax evasion. These results indicate that the existence of trust can encourage the influence of tax literacy in reducing tax evasion. Meanwhile, the role of power in mediating tax literacy and tax evasion is not proven.

4.9. Inner and outer model

Figure describes the overall model tested in this study. The explained variance (R2) in the equation with the endogenous voluntary compliance variable is 0.802. Meanwhile, R2 in the equation with tax evasion as an endogenous variable is 0.386. These values indicate that tax literacy explains voluntary compliance better than tax evasion.

Figure 2. Structural model output.

5. Additional analysis

This study formulated and statistically analyzed hypotheses on the relationships between tax literacy, trust, power, voluntary tax compliance, and tax evasion. In addition, it performed additional analysis to determine differences in tax attitudes in the form of voluntary tax compliance and tax evasion based on business scale and status as taxpayers.

5.1. ANOVA test based on business scale

This study examined the effect of business scale on the perception of business actors regarding attitude toward tax compliance. A different test aimed to assess the differences in perceptions of business actors regarding voluntary compliance and tax evasion in MSMEs. The results of the analysis are shown in Table . Additional test results show a significance level of more than 0.05 for voluntary compliance (0.125) and tax evasion (0.179), proving that the business scale of respondents did not influence tax attitude. MSMEs have the same perception of voluntary compliance and tax evasion.

Table 4. ANOVA test

5.2. Independent t-test based on tax registered and tax non-registered

The next test sought to analyze the effect of registration as a taxpayer on the perception of business actors regarding tax attitude, as represented by both voluntary tax compliance and tax evasion. A different test aims to assess the difference in perceptions of business actors regarding voluntary compliance and tax evasion in businesses that have been registered and have not been registered as taxpayers. The results of the analysis are shown in Table .

Table 5. Independent t-test results

Additional test results show a significance level of more than 0.05 for voluntary compliance (0.115) and tax evasion (0.570). This proves that tax attitude (voluntary tax compliance and tax evasion) is not significantly different between respondents who have been registered as taxpayers and those have not. MSMEs registered or not registered as taxpayers have the same perception of voluntary compliance and tax evasion.

6. Conclusions and limitations

The research aimed to analyze the relationship between perceptions of tax literacy, perceived power, and perceived trust toward voluntary compliance and tax evasion based on the Slippery Slope Framework, which underpinned the research model development and underscored the determinants of voluntary tax compliance based on the role of perceived trust and power (Batrancea et al., Citation2019; Kirchler et al., Citation2008; Kogler et al., Citation2013).

This study revealed several findings. First, the analysis results show the important role of tax literacy in positively influencing trust in and the power of authorities. Second, the hypothesis testing proves that trust in authorities and the power of tax authorities significantly improve voluntary tax compliance. Third, the results of statistical tests show that trust significantly negatively affects tax evasion, but that power does not. Fourth, the evidence shows that tax literacy significantly affects voluntary compliance (positively) and tax evasion (negatively). Further, evidence supports that trust and power have a role in mediating the indirect effect of tax literacy on voluntary compliance. However, only trust was proven to mediate the indirect effect of tax literacy on tax evasion, while power did not mediate this relationship.

The study results provide empirical evidence of the alleged role of literacy in determining trust and power, as stated by Kirchler et al. (Citation2008). As one of the individual factors that determine perceived trust and power, tax literacy is proven to have the ability to increase trust and power. Literacy provides a good understanding for the public about tax regulations and can minimize the tax system’s complexity (Toni Brackin, Citation2007). Therefore, good tax literacy can encourage trust from the public in the government and increase the perceived power of the tax authorities.

The perception of MSMEs regarding trust in the government have been proven to increase tax compliance, especially voluntary tax compliance. Further, high public trust can reduce tax evasion. The research findings prove that taxpayers will be more voluntarily obedient if the tax authorities treat taxpayers well and have the power to enforce tax regulations for the community. Cooperative actions between tax authorities and taxpayers will create a synergistic climate with narrow social distance between the two. A synergistic climate that encourages the emergence of trust will reduce the tendency to violate the law in the form of tax evasion.

When there is an increase in taxpayers’ perceptions of the power possessed by tax authorities, the next set of statistical tests prove that this can elevate voluntary compliance. Voluntary compliance can be created if there is a climate of synergy between taxpayers and tax authorities. Legitimate power can form trust in the government, thus encouraging voluntary tax compliance (Kastlunger et al., Citation2013). Therefore, people who view authorities as having legitimacy in terms of their power to enforce tax regulations will increase voluntary compliance. In this study, the role of trust and power is underlined by examining their ability to mediate the effect of tax literacy on voluntary compliance and tax evasion. The research findings show that trust mediates the effect of tax literacy on voluntary tax compliance. In addition, trust plays an important role in mediating the indirect effect of tax literacy on tax evasion. Power can mediate the indirect effect of tax literacy on voluntary tax compliance. However, power mediating the effect of tax literacy on tax avoidance is not supported by the evidence. These results provide a more straightforward explanation that literacy helps the community better understand the government’s efforts in building a tax climate and strengthens evidence on the role of trust in shaping tax attitudes.

Based on the results of this study, to increase the voluntary compliance of SMEs, the government should not limit its focus to solely exercising its authority and power. Rather, it should continuously increase its trust by providing and enhancing the level of tax literacy and knowledge to raise SMEs’ awareness of taxation issues. SMEs must prioritize their tax awareness to obtain substantial benefits and privileges from the government. By opening up the views on taxation, SMEs have the possibility to obtain financial access or external capital funding from other financial sources (i.e., access to capital or credit).

Despite these results, this research has some limitations. There are several aspects of the study that could be improved. First, the role of perceived power in determining perceived tax evasion and mediating the indirect effect of tax literacy on tax evasion is not yet clear. In addition to the measures used in this study, other indicators (Rashid et al., Citation2021b) may be useful in providing a more holistic view to explain power. Second, the sample of this study is limited to MSMEs in East Java, Indonesia. This study has not explored the perceptions of other groups of taxpayers, such as individual taxpayers. In addition, most of the respondents in this study are micro-scale business actors. Thus, it would be beneficial to determine other respondents’ perceptions of tax attitudes such as corporate taxpayers.

Disclosure statement

The authors declare that there is no financial, professional, or personal competition interest with other parties.

Additional information

Funding

References

- Aktaş Güzel, S., Özer, G., & Özcan, M. (2019). The effect of the variables of tax justice perception and trust in government on tax compliance: The case of Turkey. Journal of Behavioral and Experimental Economics, 78, 80–15. February 2019 https://doi.org/10.1016/j.socec.2018.12.006

- Allingham, M. G., & Sandmo, A. (1972). Income tax evasion: A theoretical analysis. Journal of Public Economics, 1(1972), 323–338. https://doi.org/10.1016/0047-2727(72)90010-2

- Alm, J. (2019). What motivates tax compliance? Journal of Economic Surveys, 33(2), 353–388. https://doi.org/10.1111/joes.12272

- Alm, J., Kirchler, E., & Muehlbacher, S. (2012). Combining psychology and economics in the analysis of compliance: From enforcement to cooperation. Economic Analysis and Policy, 42(2), 133–151. https://doi.org/10.1016/S0313-5926(12)50016-0

- Batrancea, L., Nichita, A., Olsen, J., Kogler, C., Kirchler, E., Hoelzl, E., Weiss, A., Torgler, B., Fooken, J., Fuller, J., Schaffner, M., Banuri, S., Hassanein, M., Alarcón-García, G., Aldemir, C., Apostol, O., Bank Weinberg, D., Batrancea, I., Belianin, A., & Zukauskas, S. (2019). Trust and power as determinants of tax compliance across 44 nations. Journal of Economic Psychology, 74(July), 102191. https://doi.org/10.1016/j.joep.2019.102191

- Benk, S. (2012). Power and trust as determinants of voluntary versus enforced tax compliance: Empirical evidence for the slippery slope framework from Turkey. African Journal of Business Management, 6(4), 1499–1505. https://doi.org/10.5897/ajbm11.2157

- Bougie, R., & Sekaran, U. (2020). Research method for business: A skill building approach (8th) ed.). Wiley.

- Brackin, T. (2007). Overcoming tax complexity through tax literacy – An analysis of financial literacy research in the context of the taxation system. In: 2007 Australasian Taxation Teachers Association Conference, 22-24 Jan. Brisbane, Australia. https://research.usq.edu.au/item/9y0q0/overcoming-tax-complexity-through-tax-literacy-an-analysis-of-financial-literary-research-in-the-context-of-the-taxation-system

- Brackin, T. (2014). Taxation as a component of financial literacy–How literate are Australians in relation to taxation? [ Unpublished doctoral dissertation]. Griffith Business School. http://hdl.handle.net/10072/367027

- Cechovsky, N. (2018). The importance of tax knowledge for tax compliance: A study on the tax literacy of vocational business students. In C. Nägele & B. E. Stalder (Eds.), Trends in vocational education and training research. Proceedings of the European Conference on Educational Research (ECER), Vocational Education and Training Network (VETNET) (pp. 113–121). https://doi.org/10.5281/zenodo.1319646

- Cvrlje, D. (2015). Synthesis and evaluation in the C-cubed system: Custom coprocessor compilations. The Macrotheme Review, 4(3), 156–165. http://macrotheme.com/yahoo_site_admin/assets/docs/13MR43Cv.804829.pdf

- Damayanti, T. W., Nastiti, P. K. Y., Supramono, S., Allingham, M. G., & Sandmo, A. (2020). Does tax amnesty influence intention to comply?: If students are taxpayers already. Business Management and Education, 18(1), 1–13. https://doi.org/10.3846/bme.2020.10292

- Fatas, E., Nosenzo, D., Sefton, M., & Zizzo, D. J. (2021). A self-funding reward mechanism for tax compliance. Journal of Economic Psychology, 86, 102421. October, 2021 https://doi.org/10.1016/j.joep.2021.102421

- Freudenberg, B., Chardon, T., Brimble, M., & Belle Isle, M. (2017). Tax literacy of Australian small businesses. Journal of Australian Taxation, 18(2), 21–61. https://www.jausttax.com.au/Articles_Free/JAT%20Volume%2019%20Issue%202%20-%20Freudenberg.pdf

- Gangl, K., Hofmann, E., & Kirchler, E. (2015). Tax authorities’ interaction with taxpayers: A conception of compliance in social dilemmas by power and trust. New Ideas in Psychology, 37, 13–23. https://doi.org/10.1016/j.newideapsych.2014.12.001

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2019). Multivariate data analysis (Eight) ed.). Cengage.

- Hofmann, E., Hoelzl, E., & Kirchler, E. (2008). Preconditions of voluntary tax compliance: Knowledge and evaluation of taxation, norms, fairness, and motivation to cooperate. Journal of Psychology, 216(4), 209–217. https://doi.org/10.1027/0044-3409.216.4.209

- Inasius, F., Darijanto, G., Gani, E., & Soepriyanto, G. (2020). Tax compliance after the implementation of tax amnesty in Indonesia. SAGE Open, 1–10. October-December 2020 https://doi.org/10.1177/2158244020968793

- Iqbal, S., & Sholihin, M. (2019). The role of cognitive moral development in tax compliance decision making: An analysis of the synergistic and antagonistic tax climates. International Journal of Ethics and Systems, 35(2), 227–241. https://doi.org/10.1108/IJOES-10-2018-0152

- Kastlunger, B., Lozza, E., Kirchler, E., & Schabmann, A. (2013). Powerful authorities and trusting citizens: The slippery slope framework and tax compliance in Italy. Journal of Economic Psychology, 34, 36–45. https://doi.org/10.1016/j.joep.2012.11.007

- Khalil, S., & Sidani, Y. (2020). The influence of religiosity on tax evasion attitudes in Lebanon. Journal of International Accounting, Auditing and Taxation, 40, 100335. https://doi.org/10.1016/j.intaccaudtax.2020.100335

- Kirchler, E., Hoelzl, E., & Wahl, I. (2008). Enforced versus voluntary tax compliance: The “slippery slope” framework. Journal of Economic Psychology, 29(2), 210–225. https://doi.org/10.1016/j.joep.2007.05.004

- Kirchler, E., & Wahl, I. (2010). Tax compliance inventory TAX-I: Designing an inventory for surveys of tax compliance. Journal of Economic Psychology, 31(3), 331–346. https://doi.org/10.1016/j.joep.2010.01.002

- Kogler, C., Batrancea, L., Nichita, A., Pantya, J., Belianin, A., & Kirchler, E. (2013). Trust and power as determinants of tax compliance: Testing the assumptions of the slippery slope framework in Austria, Hungary, Romania and Russia. Journal of Economic Psychology, 34, 169–180. https://doi.org/10.1016/j.joep.2012.09.010

- Lozza, E., Kastlunger, B., Tagliabue, S., & Kirchler, E. (2013). The relationship between political ideology and attitudes toward tax compliance: The case of Italian taxpayers. Journal of Social and Political Psychology, 1(1), 51–73. https://doi.org/10.5964/jspp.v1i1.108

- Mohdali, R., Isa, K., & Yusoff, S. H. (2014). The impact of threat of punishment on tax compliance and non-compliance attitudes in Malaysia. Procedia–Social and Behavioral Sciences, 164(August), 291–297. https://doi.org/10.1016/j.sbspro.2014.11.079

- Moro-Egido, A. I., & Solano-García, Á. (2020). Does the perception of benefit fraud shape tax attitudes in Europe? Journal of Policy Modeling, 42(5), 1085–1105. https://doi.org/10.1016/j.jpolmod.2020.01.008

- Muehlbacher, S., & Kirchler, E. (2010). Tax compliance by trust and power of authorities. International Economic Journal, 24(4), 607–610. https://doi.org/10.1080/10168737.2010.526005

- Muehlbacher, S., Kirchler, E., & Schwarzenberger, H. (2011). Voluntary versus enforced tax compliance: Empirical evidence for the “slippery slope” framework. European Journal of Law and Economics, 32(1), 89–97. https://doi.org/10.1007/s10657-011-9236-9

- Musimenta, D., & Ntim, C. G. (2020). Knowledge requirements, tax complexity, compliance costs and tax compliance in Uganda. Cogent Business & Management, 7(1), 1812220. https://doi.org/10.1080/23311975.2020.1812220

- Mutamimah, M., Tholib, M., & Robiyanto, R. (2021). Corporate governance, credit risk, and financial literacy for small medium enterprise in Indonesia. Business: Theory and Practice, 22(2), 406–413. https://doi.org/10.3846/btp.2021.13063

- Nichita, A., Batrancea, L., Marcel Pop, C., Batrancea, I., Morar, I. D., Masca, E., Roux-Cesar, A. M., Forte, D., Formigoni, H., & da Silva, A. A. (2019). We learn not for school but for life: Empirical evidence of the impact of tax literacy on tax compliance. Eastern European Economics, 57(5), 397–429. https://doi.org/10.1080/00128775.2019.1621183

- Nurkholis, N., Dularif, M., Rustiarini, N. W., & Ntim, C. G. (2020). Tax evasion and service-trust paradigm: A meta-analysis. Cogent Business & Management, 7(1), 1827699. https://doi.org/10.1080/23311975.2020.1827699

- Nuryanah, S., Gunawan, G., & McMillan, D. (2022). Tax amnesty and taxpayers’ noncompliant behaviour: Evidence from Indonesia. Cogent Business & Management, 9(1), 2111844. https://doi.org/10.1080/23311975.2022.2111844

- Pham, A., Genest-Grégoire, A., Godbout, L., & Guay, J.-H. (2021). Tax literacy: A Canadian perspective. Canadian Tax Journal/Revue Fiscale Canadienne, 68(4), 987–1007. https://doi.org/10.32721/ctj.2020.68.4.pham

- Puneet Bhushan, P. B. (2013). Determining tax literacy of salaried individuals–An empirical analysis. IOSR Journal of Business and Management, 10(6), 67–71 .

- Randlane, K. (2016). Tax compliance as a system: Mapping the field. International Journal of Public Administration, 39(7), 515–525. https://doi.org/10.1080/01900692.2015.1028636

- Rashid, S. F. A., Ramli, R., Palil, M. R., & Amir, A. M. (2021a). Improving voluntary compliance using power of tax administrators: The mediating role of trust. Asian Journal of Business and Accounting, 14(2), 101–136. https://doi.org/10.22452/ajba.vol14no2.4

- Rashid, S. F. A., Ramli, R., Palil, M. R., & Amir, A. M. (2021b). The influence of power and trust on tax compliance: Motivation in Malaysia. International Journal of Economics and Management, 15(1), 133–148. http://www.ijem.upm.edu.my/vol15no1/9.%20The%20Influence%20of%20Power%20and%20Trust.pdf

- Resmi, S., Pahlevi, R. W., & Sayekti, F. (2019). Is there a pattern of relationship between financial literacy, tax literacy, business growth, and competitive advantage on creative MSMEs in Yogyakarta. Journal of Advance Management Science, 7(4). https://doi.org/10.13106/jafeb.2021.vol8.no2.0963

- Resmi, S., Pahlevi, R. W., & Sayekti, F. (2021). The effect of financial and taxation literation on competitive advantages and business performance: A case study in Indonesia. Journal of Asian Finance, Economics and Business, 2, 963–971. https://doi.org/10.13106/jafeb.2021.vol8.no2.0963

- Umit, R., & Schaffer, L. M. (2020). Attitudes towards carbon taxes across Europe: The role of perceived uncertainty and self-interest. Energy Policy, 140(March), 111385. https://doi.org/10.1016/j.enpol.2020.111385