?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

An empirical study was conducted with the aim of testing and analyzing the relationship between the variables of financial literacy, morality, organizational culture, and preventing financial mismanagement. The originality of this research lies in the integration of cultural factors in the organizational context and efforts to prevent financial mismanagement, which are rarely given the attention of researchers. Research design with survey techniques based on quantitative philosophy. The sample chosen to represent the population uses a proportionate random sampling technique. Data collection techniques using a structured questionnaire. Also, the collected data were analyzed using multiple linear regression models and moderation analysis. The results obtained from this study are based on the results of the analysis that financial literacy and morality have a significant effect on preventing financial mismanagement. Other empirical results find that organizational culture is able to moderate the relationship between financial literacy and morality towards preventing financial mismanagement. The contribution of this research is theoretically providing a theoretical phenomenon to the theory of reasoned action in terms of mismanagement behavior and the morale of government employees in the economic development sector of government. Practical contributions are given to village administration so that they consider the determinants of individual behavior in preventing financial mismanagement by increasing good organizational governance. The implication of this research is to provide a reference for village administration to reinforce rules to place more emphasis on individual and organizational behavioral factors.

PUBLIC INTEREST STATEMENT

The organization always tries to maintain its sustainability. For this reason, organizations must be able to carry out sustainable management. One of the efforts is to control or prevent the occurrence of financial mismanagement which can trigger fraudulent practices within the organization, especially in financial management. Every main and supporting activity that does not provide added value must be identified and eliminated, so that employee morality needs to be improved. In addition, employees and all levels of the organization need to have financial knowledge or literacy in order to understand the process of entering and exiting finances or managing finances. Therefore, it is not only financial literacy and morality that can increase the prevention of financial mismanagement, but also an organizational culture adopted from local wisdom which in turn increases the overall prevention of financial mismanagement. Findings from research on local government leaders in Tabanan Regency, Bali, Indonesia as respondents indicate that by increasing financial literacy and morality, they are able to do better in preventing financial mismanagement. In addition, organizational culture can strengthen the relationship between financial literacy and morality towards preventing financial mismanagement. Thus, financial literacy, morality, and organizational culture contribute to preventing financial mismanagement.

1. Introduction

Many fraud cases are related to village financial management in Indonesia. According to data from the Indonesian Corruption Watch in 2018, the most corruption occurred in villages related to village finances. Out of the 454 cases of financial fraud that were prosecuted, 96 were cases of village financial fraud that cost the state a total of 37.2 billion rupiahs. As actors who perpetrate financial fraud, there are 102 village heads and 22 village officials. The data states that although it is relatively new, village finances implemented in 2017 have a very high level of fraud (Majid et al., Citation2014; Saputra et al., Citation2020). It indicates that the village head concerned lacks knowledge of financial literacy and morality, thus committing fraud (Popoola et al., Citation2016). Village finances must be managed by prioritizing the principle of prudence, so stricter supervision must be carried out to prevent deviant behavior through financial literacy. Financial literacy in village government is undoubtedly very dependent on solid knowledge of financial principles and concepts (Fernandes et al., Citation2014). These are financial planning, compound interest, debt management, good savings techniques, and insight into the ever-changing value of money (Morgan & Long, Citation2020; Stolper & Walter, Citation2017; Taft et al., Citation2013).

Needs are the key component behind someone’s motivation to make mistakes. (Groen et al., Citation2017; Suebvises, Citation2018). Everyone has material needs that can be a driving force for mistakes (Ekayani et al., Citation2020; Saputra et al., Citation2020).People are willing to engage in fraud to fulfill these needs if it means getting what they want. Individual characteristics are connected to the behavior that each person has inherently. These individual factors will be related to a person’s morale to make mistakes (Ariall & Crumbley, Citation2016; Saputra, Mu’ah et al., Citation2022). Financial illiteracy and dishonesty are two factors that can lead to wrongdoing in an organization. Building ethical behavior and a strong organizational culture requires positive workplace concern and financial literacy (Knechel, Citation2007; Sujana & Saputra, Citation2020). Low morale and a lack of financial literacy will encourage dishonest behavior, which will ultimately harm and possibly destroy the organization (Jones, Citation2003; Uzun & Kilis, Citation2020).

The Theory of Reasoned Action can explain financial literacy and morality. Within the framework of the Theory of Reasoned Action theory, the stability of intentions is essential for this theory, because intentions can change from time to time (Nezakati et al., Citation2015). Moreover, it is often impossible or impractical to gauge a person’s intentions as soon as possible before the behavior occurs. So, when there is a significant time gap to realize the intention into behavior, then the intention can change. For example, in the context of planning in organizations, intentions are indicated by financial literacy planning. Intentions in this organizational context are usually related more to individual segments or populations within the organization, not at the individual level. Therefore, in the organizational context, an individual control system mechanism is needed or called morality, that can be used to control and ensure that these intentions can be realized into behavior (Horomnea & Pașcu, Citation2012).

Several research results provide the same definition of fraud and error. Meanwhile, based on the behavioral context, cheating is done intentionally and motivated. However, ignorance or a lack of information can lead to unintentionally wrong behavior (Ghazali et al., Citation2014; Majid et al., Citation2014). Inconsistent findings have been found in research on financial mismanagement in villages. Lidyah (Citation2018) found that the occurrence of village financial mismanagement was positively influenced by financial literacy knowledge. However, Morgan and Long (Citation2020) stated that financial literacy is not important in preventing financial fraud. The differences in the results of previous studies have become a gap for the latest research in the field of finance by presenting new aspects or re-examining the same variables to answer inconsistencies in the results of previous research. Based on the results of previous studies measuring financial mismanagement using fraud indicators (Ekayani et al., Citation2020). Research on financial mismanagement has only ever been studied using qualitative methods so far. However, this study attempts to investigate using quantitative methods by creating indicators based on the concept of misbehavior in financial management.

Research on the effect of morality on preventing village financial mismanagement has reported varying results. Morality has a significant influence on the prevention of financial fraud (Balan & Knack, Citation2012). At the same time, Hodges and Sulmasy (Citation2013) state that morality has nothing to do with cheating, as long as morality does not affect a well-managed life. However, in research Starr (Citation2005) get the result that morality has nothing to do with someone’s mistake in managing government finances. The results of previous studies still leave gaps for further research by re-testing the same variables in different populations. In previous studies, morality and financial fraud investigations focused on the context of state institutions, banks and other profit organizations (Maria & Bleotu, Citation2014; Phornlaphatrachakorn & Peemanee, Citation2020). This study explores different populations, namely the village government, which is important to study, because the village government distributes large funds to villages with the hope that development starts from the village for advanced Indonesia. Contrary to the government’s expectations, it turns out that the resources in the village are still not qualified to manage finances in a professional and accountable manner.

Mismanagement that occurs in village government will disrupt the intermediary function of the organization, so that the goals of achieving its performance will be difficult to achieve. In preventing mismanagement to improve bank performance, protect the interests of stakeholders and increase compliance with laws and regulations and ethical values (code of conduct) that apply in general to village government, it is mandatory to carry out organizational culture improvements (Phornlaphatrachakorn & Peemanee, Citation2020). Village government is one of the public sector organizations that provide services, so that in its operations, organizational culture is very important to consider as preventing mismanagement towards good governance (Saputra et al., Citation2021). Organizational culture in this discussion is more directed towards a culture that can prevent mismanagement. In contrast to previous research that occurred at central level government organizations and large private institutions, this analysis explores the smallest level of government institutions, namely villages. Because villages in Indonesia receive large amounts of funds to manage, and village administrations still have a shortage of qualified personnel to manage finances, it is suspected that high financial management violations have occurred. In addition, this study has an originality that raises the mismanagement variable. Previously, only the level of financial fraud was considered. Also, organizational culture variables adopted from Balinese local wisdom to become work guidelines for workers or employees in Bali. This becomes universal because the teachings of this culture are in synergy with international culture.

This research was conducted in Tabanan Regency because it is one of the largest areas and has the most villages, so that it automatically manages the most village funds in the Province of Bali. In addition, in this district, based on data from the media in Bali (bali.antaranews, Bali post, and the ombudsman) there have been the most cases of mismanagement of village funds based on management errors. However, not all cases are criminal cases, there are also civil cases and some cases are resolved amicably. Tabanan Regency is currently also experiencing a leadership and management crisis because the former district head for two terms and his assistants in the field of finance and village management were involved in corruption cases and have been sentenced to prison. This shows that Tabanan currently needs a solution for better management of village funds. For this reason, this research was conducted in order to be able to contribute to the transparent management of village funds.

The contribution of this research is theoretically providing a theoretical phenomenon to the theory of reasoned action in terms of mismanagement behavior and the morale of government employees in the economic development sector of government. Practical contributions are given to village administration so that they consider the determinants of individual behavior in preventing financial mismanagement by increasing good organizational governance. The implication of this research is to provide a reference for village administration to reinforce rules to place more emphasis on individual and organizational behavioral factors. More will be discussed in the next sub-discussion.

2. Literature review and hypothesis

2.1. Theory of reasoned action

Attitudes and subjective norms are determinants of the intention to behave in a certain way so that a person will intend to behave in a certain way if his assessment of the behavior is positive and he has the perception that those who are important to him want him to behave in such a way. In determining intentions, the two determinants have different weight combinations for different behaviors and individuals. What is meant by the attitude in this context is an attitude towards a particular behavior, namely the opinion of a person that carrying out behavior is good or bad, that he supports or opposes performing a particular behavior. Attitude is a function of belief. Someone who believes that a particular behavior will positively impact others will have a positive attitude towards that behavior. On the other hand, people who believe that the impact produced by behavior is negative will also have a negative attitude towards that behavior. Beliefs that underlie one’s attitude towards a behavior are referred to as behavioral beliefs (Afdalia et al., Citation2014).

3. Financial literacy and prevention of financial mismanagement

A growing number of financial instruments have gained importance, including alternative financial services such as payday loans, pawnshops, and rent to own stores that charge very high interest rates (Moure, Citation2016). Simultaneously, in the changing economic landscape, people are increasingly responsible for personal financial planning and for investing and spending their resources throughout their lifetime. We have witnessed changes not only in the asset side of household balance sheets but also in the liability side. For example, in the USA, many people arrive close to retirement carrying a lot more debt than previous generations did (Lusardi et al., Citation2018). Overall, individuals are making substantially more financial decisions over their lifetime, living longer, and gaining access to a range of new financial products. These trends, combined with low financial literacy levels around the world and, particularly, among vulnerable population groups, indicate that elevating financial literacy must become a priority for policy makers (Moure, Citation2016).

Financial literacy is knowledge of basic financial concepts, including compound interest, the difference between nominal and honest values, basic knowledge of risk diversification, the time value of money and others. Financial literacy indicators are general knowledge about finance, loans and savings, investment and insurance (Arianti, Citation2018; Lin et al., Citation2017). Previous research from Lin et al. (Citation2017) finds that financial literacy significantly affects financial management behavior. There is a significant influence between financial literacy and financial fraud prevention behavior (Haque & Zulfiqar, Citation2016; Marcolin & Abraham, Citation2006). Based on previous research investigations, the following hypotheses can be formulated:

H1: Financial Literacy has a significant effect on Preventing Financial Mismanagement

4. Morality and prevention of financial mismanagement

Management morality significantly negatively affects the tendency of fraudulent financial management. Haque and Zulfiqar (Citation2016) get results that the higher the morality of management, the lower the tendency of financial fraud or the higher the level of management morality, the more management pays attention to broader and universal interests than the interests of the company alone, especially personal interests (Stets & Carter, Citation2011; Wong & Lui, Citation2007). Horomnea and Pașcu (Citation2012) stated that morality is a guideline that individuals or groups have regarding what is right and wrong based on moral standards. Morality can come from traditional or customary sources, religion or ideology or a combination of several sources (Euchner et al., Citation2013). Morality is measured by intrinsic and extrinsic indicators (Bromley & Orchard, Citation2015). Based on previous research, the following hypotheses can be formulated:

H2: Morality has a significant effect on preventing Financial Mismanagement

5. Financial literacy, morality, organizational culture and prevention of financial mismanagement

By using organizational culture, work behavior can be seen through employee evaluation of their results when controlled internally or externally (Saputra, Mu’ah et al., Citation2022). Employees/managers who understand the culture of the organization feel that they can personally influence results through their abilities, skills or their own efforts. If a worker/manager is committed to the organizational culture so that he is confident in his ability to solve a problem, then this will lead to preventive behavior against mismanagement and is expected to improve work performance/achievement (Saputra et al., Citation2021). However, if an employee has a tendency to believe in factors outside of himself as a determinant of his success, and ignores organizational culture, this will actually lead to mismanagement at work (Saputra, Mu’ah et al., Citation2022). Related to the moderating variable of organizational culture, Bromley and Orchard (Citation2015) states that organizational culture has a positive and significant effect on performance. Furthermore, according to Moure (Citation2016) this condition shows that the values contained in the organizational culture in this study are able to reduce mismanagement. From the explanation above regarding the results of previous research, the following hypotheses can be obtained:

H3: Organizational culture moderates the effect of financial literacy and morality on mismanagement behavior.

6. Method

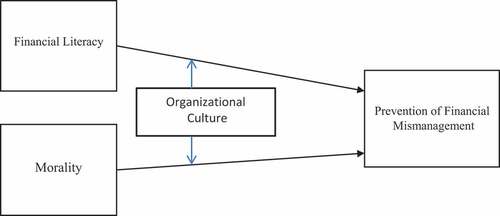

This study examines the effect of financial literacy and morality on preventing mismanagement of village financial management. Therefore, the conceptual framework of the research can be described as follows shown in :

Figure 1. Research model.

The research design used in this study is a survey research design conducted on village heads in Tabanan Regency, Bali-Indonesia Province. The population in this study were village heads in Tabanan Regency, with a total of 133 villages. To get a sample that can describe and reflect the population in this study which amounted to 133 villages, the calculations using the Slovin formula used a sample of 100 village heads in Tabanan Regency. The sampling technique used in this study uses proportionate random sampling, which is selecting samples by taking sample members from the population proportionally by taking into account the strata that exist in a population. From the number of questionnaires that were distributed, 87 of the results of the questionnaires were analyzed. Data analysis technique using multiple linear regression (Atmadja et al., Citation2021). Research data were analyzed with multiple regression models and moderated regression analysis.

The financial literacy variable consists of indicators of basic knowledge of financial management, savings education, and investment management (Warmath & Zimmerman, Citation2019). Morality indicators based on Sayans‐Jiménez et al. (Citation2017) consists of politeness and adherence to organizational culture, social and environmental concerns, honesty at work, and compliance with rules and responsibilities. The prevention of financial mismanagement variable adopts indicators of fraud prevention and is adjusted based on research objectives, which have indicators namely pattern of good organizational structure, management mindedness, uniformity regarding work methods and procedures between divisions or sections, effective implementation of supervision, effective coordination, and equation of vision and mission (Zeng & Yang, Citation2020, December). The organizational culture variable adopts indicators from Saputra, Mu’ah et al. (Citation2022) which consists of integrity, work ethics, and environmental sustainability.

This study adds a moderating variable, namely organizational culture. The organizational culture referred to here is a local culture based on Balinese local wisdom which is adopted in the organization to be used as the main guideline in organizing for Balinese people (Saputra, Mu’ah et al., Citation2022). This culture is based on three things, namely respecting God, fellow human beings, and the universe (Saputra et al., Citation2021). These three things are universal teachings that are in line with today’s international human culture. Both belief in God, respect for fellow human beings, and glorify the universe. Organizational culture as a moderating variable is important to prevent mistakes in village financial management.

Questionnaire statements are arranged with a Likert scale of 1 to 5, which states that they strongly agree with the highest score and strongly agree with the lowest score. Variable measurement indicators conform to previous studies which are modified and adapted to research needs and the context of field research. Survey research techniques allow the researcher to play a major role when explaining the research objectives and detailing the content and intent of the questionnaire. The researcher also made an ethical agreement with the respondent, because the respondent was a village government official. The questionnaire prepared has gone through a pilot study process (conducted with university lecturers throughout Bali), because researchers assume that lecturers have experience dealing with village administration in terms of research or community service. Lecturers have qualified government knowledge so that they can be used in pilot studies. After a pilot test was carried out, and it was declared valid and reliable, the questionnaire was then given to the real respondents.

7. Results and discussion

The implementation of this research was carried out first by testing the validity and reliability of the instrument. The validity test uses the product moment Pearson correlation test by connecting each item score with the total score obtained in the study. The instrument reliability test is measured based on Cronbach’s alpha value.

The profiles of respondents in this study were grouped by age, education, and years of service. The characteristics of respondents based on age showed that they were at the age of 30–39 years as much as 20%, respondents were at the age of 40–49 years as many as 41.76%, and at the age of 50–59 years as many as 38.24%. Most of the respondents had a high school education background, as many as 82.35%, with a bachelor’s degree as many as 17.65%. Based on the years of service of the respondents, as many as 88.24% of respondents had a working period of 1–5 years, and 11.76% had a service period of > 5 years. The results of testing the validity and reliability of the instrument indicate that the instrument used in this study is valid and reliable, as indicated by the value of the item-total variable correlation coefficient greater than 0.3 and significantly less than 0.05. The reliability test results showed that the Cronbach alpha value for all variables used in this study was more significant than 0.70. The multiple linear regression analysis results explain the effect of financial literacy and morality variables on preventing village financial mismanagement. The results of these calculations are shown in the following table:

Based on the test results, the influence of financial literacy and morality on the prevention of financial mismanagement can be interpreted as follows:

= 0.340; means that if the morality variable (X2) is considered constant, then increasing the implementation of financial literacy (X1) by one unit will be followed by the prevention of financial mismanagement (Y), an average of 0.340

= 0.729; means that if financial literacy (X1) is considered constant, then it increases morality (X2) by one unit and will be followed by an increase in the prevention of financial mismanagement (Y) by an average of 0.729

From the regression analysis above, it can be seen that the variables that have a significant effect on preventing mismanagement are financial literacy () and morality with significance values () of 0.000 and 0.018. The FL*OC variable is 0.024 and ML*OC is 0.025. Age variable (AGE) as a control variable has a significance of 0.022. This shows a significance value of less than 0.05, which means that the relationship between variables has a significant effect. FL, ML, FL*OC and ML*OC variables have a significant effect on preventing mismanagement behavior through interaction tests. Financial literacy and morality variables are proven to have an impact on preventing mismanagement with organizational culture variables as moderating variables as shown in . The interaction test results above are complemented by an additional residual test method because they do not fulfill one regression assumption, namely the assumption of multicollinearity as shown in . This is overcome by developing a residual test method as shown in . Residual test results by regressing the absolute residuals of organizational culture regression results on financial literacy and morality with the dependent variable. The residual test results are presented in Table .

Table 1. Financial literacy model indicators and measurements

Table 2. Morality model indicators and measurements

Table 3. Prevention of financial mismanagement model indicators and measurements

Table 4. Organizational culture model indicators and measurements

Table 5. Multiple linear regression test results

Table 6. Results of moderation analysis with the Interaction test

Table 7. Residual test results

From Table it can be seen that the variable preventing of financial mismanagement has a significant effect on the absolute residual results of the regression model between organizational culture and financial literacy and morality, and the coefficient obtained is negative, namely −0.95, so it can be said that financial literacy and morality has a significant effect on preventing of financial mismanagement with organizational culture as a moderating variable. Therefore, according to the results obtained, hypothesis three (H3) can be accepted. The results of the interaction test include control variables. The following table compares the value of the goodness of the regression model using R2 before entering the control variable and after entering the control variable for each response variable preventing of financial mismanagement.

The goodness-of-fit value of the regression model (R2) is the coefficient of determination whose function is to find out how much the diversity of the response variables can be explained by the explanatory variables, so that in the regression analysis the higher the R squared value, the better the regression model will be. Based on Table . it can be seen that R squared has increased after the regression is given the addition of control variables. The increase in R squared in the regression with the response variable prevention of financial mismanagement tends to be high, which is around 10%. This is because there is a control variable that has a significant effect on performance and job satisfaction, namely the age variable.

Table 8. Value of the goodness of the regression model (R2)

Based on the results of data analysis that has been carried out regarding the effect of financial literacy and morality on preventing financial mismanagement, it is found that financial literacy has a positive effect on preventing village financial mismanagement. The hypothesis is accepted based on the t-count for the financial literacy variable of 2.738 and the t-test significance value of 0.008, which is smaller than = 0.05 and the regression coefficient value of 0.340. These results indicate that financial literacy positively prevents financial mismanagement (Fernandes et al., Citation2014). The results of this study are supported by the main principle of behavioral theory, namely the relationship between individual knowledge related to finance and financial behavior (Balushi et al., Citation2018). Problems will occur when financial employees with inadequate financial literacy knowledge are asked to prepare and plan village finances as outlined in the village government budget according to applicable standards and regulations, the results will lead to budget errors (Saputra et al., Citation2019, Citation2020). This assumption emphasizes that if individuals act without maximizing their financial literacy knowledge, then good governance will not be achieved in the process of implementing good governance (Fernandes et al., Citation2014). It can cause the creation of a control or prevention of fraudulent village financial management (Lusardi et al., Citation2010; Osman et al., Citation2018). However, if the financial literacy possessed by individuals has quality, the organizational control system will be better and build confidence to manage mismanagement (Earl et al., Citation2015; Garg & Singh, Citation2018; Potrich et al., Citation2016). The results of this study agree with previous research from Saputra et al. (Citation2019) and Osman et al. (Citation2018).

An essential indicator of people’s ability to make financial decisions is their level of financial literacy (Lusardi et al., Citation2018). The Organisation for Economic Co-operation and Development (OECD) aptly defines financial literacy as not only the knowledge and understanding of financial concepts and risks but also the skills, motivation, and confidence to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, to improve the financial well-being of individuals and society, and to enable participation in economic life (Moure, Citation2016).

In the context of rapid changes and constant developments in the financial sector and the broader economy, it is important to understand whether people are equipped to effectively navigate the maze of financial decisions that they face every day (Lusardi et al., Citation2018). To provide the tools for better financial decision-making, one must assess not only what people know but also what they need to know, and then evaluate the gap between those things (Moure, Citation2016). There are a few fundamental concepts at the basis of most financial decision-making (Klapper et al., Citation2015). These concepts are universal, applying to every context and economic environment. Three such concepts are (1) numeracy as it relates to the capacity to do interest rate calculations and understand interest compounding; (2) understanding of inflation; and (3) understanding of risk diversification (Van Prooijen & Ellemers, Citation2015).

These findings are supported by many other surveys. For example, the 2014 Standard and Poor’s Global Financial Literacy Survey shows that, around the world, people know the least about risk and risk diversification (Klapper et al., Citation2015). Similarly, results from the 2016 Allianz survey, which collected evidence from ten European countries on money, financial literacy, and risk in the digital age, show very low-risk literacy in all countries covered by the survey. In Austria, Germany, and Switzerland, which are the three top-performing nations in term of financial knowledge, less than 20% of respondents can answer three questions related to knowledge of risk and risk diversification (Allianz, Citation2017). To summarize, financial literacy is low across the world and higher national income levels do not equate to a more financially literate population. This enhances the measure’s utility because it helps to identify general and specific vulnerabilities across countries and within population subgroups, as will be explained in the next section (Moure, Citation2016). The results of this study agree with previous research from Klapper et al. (Citation2015) and Allianz (Citation2017).

Morality has a positive effect on preventing village financial mismanagement. The second hypothesis is accepted based on the tcount value for the morality variable of 7.091 and the t-test significance value of 0.000, which is smaller than = 0.05 and the regression coefficient value of 0.729. The results of this study are supported by the main principle of interaction theory, namely, an open system in a company closely related to interaction for adjustment and control of the environment to maintain good governance (Fernandhytia et al., Citation2020; Saputra et al., Citation2020). It shows that good governance morality will result in effective and efficient error prevention. In addition, positive individual morality possessed by government leaders will result in better public trust in the government (Bromley & Orchard, Citation2015; Kurniawan & Azmi, Citation2019). Therefore, there is a balanced correlation between morality and public trust so that synergy can be established to jointly supervise the running of the government, especially in managing village finances for community welfare and increasing village independence (Saputra et al., Citation2020). The results of this study agree with previous research from Saputra et al. (Citation2020); Fernandhytia et al. (Citation2020); and Kurniawan and Azmi (Citation2019).

In this study it can be interpreted that morality plays an important role in preventing financial mismanagement, especially within the scope of village government which only has limited human resources in financial management. In addition, the capacity of village officials who still need to be increased makes the role of morality significant in realizing clean village governance (Bromley & Orchard, Citation2015; Kurniawan & Azmi, Citation2019). This is related to the relationship between the village leadership or head and apparatus and apparatus to establish harmonious and synergistic relationships with other communities to supervise and participate in village financial management, especially in preparing the village budget (Saputra et al., Citation2019). Everyone who deals with village finances within the scope of village administration, either directly or indirectly, must have a good mentality or morals so as not to get caught up in corruption which ultimately leads to legal action. Morality is more controlled by each individual (Saputra et al., Citation2020). There is no system that can control morality so that the behavior of everyone in the village government must work together to create a government that is transparent, accountable and participatory (Fernandhytia et al., Citation2020; Saputra et al., Citation2020). Therefore, in essence, the morals of the village apparatus are very important in preventing financial mismanagement in any form that exists in the administration of village governance, especially in financial management. This research is in line with previous research from Saputra et al. (Citation2020), and researchers agree with the results of previous studies.

This research is in line with research conducted by Saputra, Mu’ah et al. (Citation2022) which states that organizational culture has a significant effect on fraud prevention. In addition, the results of this study support research conducted by Saputra et al. (Citation2021), Sujana and Saputra (Citation2020), and Saputra et al. (Citation2019) who in their research stated that organizational culture variables had a positive and significant effect on preventing management errors. An explanation that can be given from the results of the third hypothesis test is that financial literacy, morality and organizational culture can influence the prevention of mismanagement in village government in Bali (Saputra, Jayawarsa et al., Citation2022). Therefore, conditions like this show that the values contained in organizational culture can and are important to be applied in a government. Financial literacy and morality which are individual controls, can be strengthened by anti-corruption values contained in the organizational culture to prevent acts of mismanagement in village government (Saputra et al., Citation2019). In the context of preventing mismanagement including control variables, according to the results of the analysis, empirically found that age determines employees to engage in deviant behavior. This means that, the older the age, the need will increase, so the need for money also increases. If not limited by good governance and financial literacy, morality education, and a strong organizational culture, fraud or mismanagement will occur (Sujana & Saputra, Citation2020). Therefore, it is necessary to consider the age factor in the context of preventing financial mismanagement. The results of this study support previous research from Sujana and Saputra (Citation2020); Saputra et al. (Citation2021); and Saputra, Jayawarsa et al. (Citation2022).

8. Conclusion

Based on the study’s results, it can be concluded that financial literacy and morality significantly positively affect preventing village financial m. It can indicate that in organizationally managing village finances, applying an excellent financial literacy mechanism is necessary to avoid fraud. In addition, the morality of the village government apparatus needs to be improved either through training or awareness of local wisdom which can be believed to be capable of being an internal controller for each individual. Therefore, further research can link local wisdom variables such as internal control of the village apparatus and re-explore financial factors such as financial performance, financial development, and public finance theory, which is the government domain.

Financial education can also be efficiently provided in workplaces. An effective financial education program targeted to adults recognizes the socioeconomic context of employees and offers interventions tailored to their specific needs. Finally, it is important to provide financial education in society, in places where people go to study. A recent example is the international finance federation public sector, an innovative global collaboration promote financial knowledge through outreach and meetings in the public sector and exchange of resources. Village Government Organizations can become places where to provide good financial literacy among young and old. There are various other ways in which finance education can be offered as well as targeted to specific group, namely the village government apparatus. However, there are few evaluations of effectiveness such initiatives and this is an area where more research is urgently needed, given the statistics reported in the first part of this paper.

One of the things that mismanagement perpetrators do is think outside the box. When an actor learns the mechanism of work, control weaknesses and controls so that he becomes innovative in exploring gaps to gain profits. This will be difficult to detect, if the functions within the organization are not aware and ignore the organizational culture in carrying out operational activities. Sometimes gaps have been identified but seem to be insensitive and become an acute disease within the organization which is then only realized after the loss has actually occurred. This of course requires an organizational culture that is integrated with the government’s internal control system. Financial mismanagement is only one of the many threats faced by village governments. Perpetrators have many ways of committing intentional fraud making it difficult to detect. This is when organizational culture needs to strengthen the influence of financial literacy and increase morality in preventing financial mismanagement.

The implication for research, practice, or society is that research implies that this research is important to be carried out to provide up-to-date solutions for the high level of management errors in village financial management. The social implications are in terms of implementing research results in organizations that have a positive impact on village communities to get their rights to enjoy and manage village funds with the aim of welfare. The results of this research also have an impact on business, the economy and public policy. In the business sector, this study has an impact on the sustainability of local community businesses that expect assistance from village funds. In the economic sector, of course, the misuse of village funds has an impact on community creativity, because the allocation of village funds is prioritized for the economic welfare of the community, not for government operations. And in the policy sector, based on the results of this research, regional and village governments should make firm policies regarding the guidelines for good village financial governance based on financial regulation and transparency and accountability.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

I Made Sara

I Made Sara is Associate Professor, Dean of the Faculty of Economics and Business, Warmadewa University, Bali, Indonesia. His main research focuses on development economics, governance, corporate governance, entrepreneurship, government finance, organizational management, and banking.

Ida Bagus Udayana Putra

Ida Bagus Udayana Putra is a lecturer in the Department of Management, Faculty of Economics and Business, Warmadewa University, Bali, Indonesia. His main research focuses on corporate governance, intellectual capital, financial reporting, financial management, strategic management, and human resource management.

Komang Adi Kurniawan Saputra

Komang Adi Kurniawan Saputra is a lecturer in the Department of Accounting, Faculty of Economics and Business, Warmadewa University, Bali, Indonesia. His main research focuses on Corporate Governance, government accounting, public sector accounting, Organizational Behaviors and Management Accounting such as environmental management accounting, sustainability performance, and corporate accountability.

I Wayan Kartika Jaya Utama

I Wayan Kartika Jaya Utama is a lecturer in the Department of Law, Faculty of Law, Warmadewa University, Bali, Indonesia. His main research focus is land law, government regulations, criminal and civil law, organizational governance, organizational law, finance and engagement law.

References

- Afdalia, N., Pontoh, G. T., & Kartini, K. (2014). The theory of planned behavior and readiness for change in predicting the intention to implement government regulations. nomor 71 Tahun 2010. Jurnal Akuntansi & Auditing Indonesia, 18(2), 110–15. https://doi.org/10.20885/jaai.vol18.iss2.art3

- Allianz. (2017). When will the penny drop? Money, financial literacy and risk in the digital age. http://gflec.org/initiatives/money-finlit-risk/. Accessed 1 June 2022

- Ariall, D. L., & Crumbley, D. L. (2016). Fraud triangle and ethical leadership perspective on detecting and preventing academic research misconduct. Journal of Forensic and Investigative Accounting, 8(3), 480–500. https://s3.amazonaws.com/web.nacva.com/JFIA/Issues/JFIA-2016-No3-6.pdf

- Arianti, B. F. (2018). The influence of financial literacy, financial behavior and income on investment decisions. EAJ (Economic and Accounting Journal), 1(1), 1–10. https://core.ac.uk/download/pdf/337610685.pdf

- Atmadja, A. T., Saputra, K. A. K., Tama, G. M., & Paranoan, S. (2021). Influence of human resources, financial attitudes, and coordination on cooperative financial management. Journal of Asian Finance, Economics and Business, 8(2), 563–570. https://doi.org/10.13106/jafeb.2021.vol8.no2.0563

- Balan, D. J., & Knack, S. (2012). The correlation between human capital and morality and its effect on economic performance : theory and evidence. Journal of Comparative Economics, 40(3), 457–475. https://doi.org/10.1016/j.jce.2011.12.005

- Balushi, Y. A., Locke, S., & Boulanouar, Z. (2018). Islamic financial decision-making among SMEs in the sultanate of Oman: an adaption of the theory of planned behavior. Journal of Behavioral and Experimental Finance, 20, 30–38. https://doi.org/10.1016/j.jbef.2018.06.001

- Bromley, P., & Orchard, C. D. (2015). Managed morality : The rise of professional codes of conduct in the U S . Nonprofit Sector. Nonprofit and Voluntary Sector Quarterly, 30(November), 1–24. https://doi.org/10.1177/0899764015584062

- Earl, J. K., Gerrans, P., Asher, A., & Woodside, J. (2015). Financial literacy, financial judgment, and retirement self-efficacy of older trustees of self-managed superannuation funds. Australian Journal of Management, 40(3), 435–458. https://doi.org/10.1177/0312896215572155

- Ekayani, N. N. S., Sara, I. M., Sariani, N. K., Jayawarsa, A. A. K., & Saputra, K. A. K. (2020). Implementation of good corporate governance and regulation of the performance of micro-financial institutions in the village. Journal of Advanced Research in Dynamical and Control Systems, 12(7), 1–7. https://doi.org/10.5373/JARDCS/V12I7/20201977

- Euchner, E., Heichel, S., Nebel, K., & Raschzok, A. (2013). From ‘ morality ’ policy to ‘ normal ’ policy : Framing of drug consumption and gambling in Germany and the Netherlands and their regulatory consequences. Journal of European Public Policy, 20(3), 372–389. https://doi.org/10.1080/13501763.2013.761506

- Fernandes, D., Lynch, J. G., Jr, & Netemeyer, R. G. (2014). Financial literacy, financial education, and downstream financial behaviors. Management Science, 60(8), 1861–1883. https://doi.org/10.1287/mnsc.2013.1849

- Fernandhytia, F., Muslichah, & Muslichah, M. (2020). The effect of internal control, individual morality and ethical value on accounting fraud tendency. Media Ekonomi Dan Manajemen, 35(1), 112–127. https://doi.org/10.24856/mem.v35i1.1343

- Garg, N., & Singh, S. (2018). Financial literacy among youth. International Journal of Social Economics, 45(1), 173–186. https://doi.org/10.1108/IJSE-11-2016-0303

- Ghazali, M. Z., Rahim, M. S., Ali, A., & Abidin, S. (2014). A preliminary study on fraud prevention and detection at the state and local government entities in Malaysia. Procedia - Social and Behavioral Sciences, 164(August), 437–444. https://doi.org/10.1016/j.sbspro.2014.11.100

- Groen, B. A. C., Wouters, M. J. F., & Wilderom, C. P. M. (2017). Employee participation, performance metrics, and job performance: A survey study based on self-determination theory. Management Accounting Research, 36, 51–66. https://doi.org/10.1016/j.mar.2016.10.001

- Haque, A., & Zulfiqar, M. (2016). Women’s economic empowerment through financial literacy, financial attitude and financial wellbeing. International Journal of Business and Social Science, 7(3), 78–88. https://iiste.org/Journals/index.php/RJFA/article/view/26911

- Hodges, K. E., & Sulmasy, D. P. (2013). Moral Status, Justice, and the Common Morality: Challenges for the Principlist Account of Moral Change. Kennedy Institute of Ethics Journal, 23(3), 275–296. https://doi.org/10.1353/ken.2013.0011

- Horomnea, E., & Pașcu, A. (2012). Ethical and morality in accounting epistemological approach. Journal of Eastern Europe Research in Business & Economics, 2012, 1–11. https://doi.org/10.5171/2012.405721

- Jones, C. (2003). Theory after the Postmodern Condition. Organization, 10(3), 503–525. https://doi.org/10.1177/13505084030103009

- Klapper, L., Lusardi, A., & Van Oudheusden, P. (2015). Financial Literacy Worldwide: Insights from the Standard & Poor’s Rating Services Global Financial Literacy Survey. International Bank for Reconstruction and Development & World Bank. Available online: https://gflec.org/wp-content/uploads/2015/11/3313

- Knechel, W. R. (2007). The business risk audit: Origins, obstacles and opportunities. Accounting, Organizations and Society, 32(4–5), 383–408. https://doi.org/10.1016/j.aos.2006.09.005

- Kurniawan, P. C., & Azmi, F. (2019). The effect of management morality on accounting fraud with internal control as a moderating variable (study in pemalang regency). Jurnal Riset Akuntansi Dan Keuangan Indonesia, 4(2), 177–185. https://doi.org/10.23917/reaksi.v4i2.8552

- Lidyah, R. (2018). Islamic corporate governance, IslamiCity financial performance index and fraud at Islamic Bank. Jurnal Akuntansi, 22(3), 437. https://doi.org/10.24912/ja.v22i3.398

- Lin, C., Hsiao, Y.-J., & Yeh, C.-Y. (2017). Financial Literacy, Financial Advisors, and Information Sources on Demand for Life Insurance. Pacific-Basin Finance Journal, 43, 218–237. https://doi.org/10.1016/j.pacfin.2017.04.002

- Lusardi, A., de Bassa Scheresberg, C., & Avery, M. (2018). Millennial mobile payment users: A look into their personal finances and financial behaviors. GFLEC Insights Report https://gflec.org/wp-content/uploads/2018/04/GFLEC-Insight-Report-Millennial-Mobile-Payment-Users-Final.pdf

- Lusardi, A., Mitchell, O. S., & Curto, V. (2010). Financial Literacy among the Young. Journal of Consumer Affairs, 44(2), 358–380. https://doi.org/10.1111/j.1745-6606.2010.01173.x

- Majid, R. A., Mohamed, N., Haron, R., Omar, N. B., & Jomitin, B. (2014). Misappropriation of assets in local authorities : A challenge to good governance. Procedia - Social and Behavioral Sciences, 164(August), 345–350. https://www.sciencedirect.com/science/article/pii/S1877042814059060

- Marcolin, S., & Abraham, A. (2006). Financial literacy research: Current literature and future opportunities. https://ro.uow.edu.au/commpapers/223/

- Maria, T. D., & Bleotu, V. (2014). Modern trends in higher education funding. Procedia - Social and Behavioral Sciences, 116, 2226–2230. https://doi.org/10.1016/j.sbspro.2014.01.548

- Morgan, P. J., & Long, T. Q. (2020). Financial literacy, financial inclusion, and savings behavior in laos. Journal of Asian Economics, 68, 101197. https://doi.org/10.1016/j.asieco.2020.101197

- Moure, N. G. (2016). Financial literacy and retirement planning in Chile. Journal of Pension Economics & Finance, 15(2), 203–223. https://doi.org/10.1017/S1474747215000049

- Nezakati, H., Moghadas, S., Aziz, Y. A., Amidi, A., Sohrabinezhadtalemi, R., & Jusoh, Y. Y. (2015). Effect of behavioral intention toward choosing green hotels in Malaysia – preliminary study. Procedia - Social and Behavioral Sciences, 172, 57–62. https://doi.org/10.1016/j.sbspro.2015.01.335

- Osman, Z., Madzlan, E. M., & Ing, P. (2018). In pursuit of financial well-being: The effects of financial literacy, financial behaviour and financial stress on employees in labuan. International Journal of Service Management and Sustainability, 3(1), 55–94. https://ir.uitm.edu.my/id/eprint/33618/1/33618.pdf

- Phornlaphatrachakorn, K., & Peemanee, J. (2020). Integrated performance measurement as a strategic management accounting approach: A case of beverage businesses in Thailand. The Journal of Asian Finance, Economics and Business, 7(8), 247–257. https://doi.org/10.13106/JAFEB.2020.VOL7.NO8.247

- Popoola, O. M. J., Che-Ahmad, A. B., Samsudin, R. S., Salleh, K., & Babatunde, D. A. (2016). Accountants ’ Capability Requirements for Fraud Prevention and Detection in Nigeria. International Journal of Economics and Financial Issues, 6(4), 1–10. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2807837

- Potrich, A. C. G., Vieira, K. M., & Mendes-Da-Silva, W. (2016). Development of a Financial Literacy Model for University Students. Management Research Review, 39(3), 356–376. https://doi.org/10.1108/MRR-06-2014-0143.

- Saputra, K. A. K., Jayawarsa, A. A. K., & Atmadja, A. T. (2019). Resurrection as a Fading Implication of Accountability in Financial Management for Village Credit Institution. International Journal of Business, Economics and Law, 19(5), 258–268. https://www.ijbel.com/wp-content/uploads/2019/11/K19_263.pdf

- Saputra, K. A. K., Jayawarsa, A. A. K., & Priliandani, N. M. I. (2022). Antonio Gramsci Hegemonical Theory Critical Study : Accounting Fraud Of Hindu - Bali. International Journal of Business, 27(2), 1–11. https://doi.org/10.55802/IJB.027(2).001

- Saputra, K. A. K., Manurung, D. T., Rachmawati, L., Siskawati, E., & Genta, F. K. (2021). Combining the Concept of Green Accounting with the Regulation of Prohibition of Disposable Plastic Use. International Journal of Energy Economics and Policy, 11(4), 84–89. https://doi.org/10.32479/ijeep.10087

- Saputra, K. A. K., Mu’ah, M., Jurana, J., Korompis, C. W. M., & Manurung, D. T. (2022). Fraud Prevention Determinants: A Balinese Cultural Overview. Australasian Accounting, Business and Finance Journal, 16(3), 167–181. https://doi.org/10.14453/aabfj.v16i3.11

- Saputra, K. A. K., Subroto, B., Rahman, A. F., & Saraswati, E. (2020). Issues of Morality and Whistleblowing in Short Prevention Accounting. International Journal of Innovation, Creativity and Change, 12(3), 77–88. https://ijicc.net/images/vol12/iss3/12314_Saputra_2020_E_R.pdf

- Sayans‐Jiménez, P., Rojas Tejada, A. J., & Cuadrado Guirado, I. (2017). Is it advisable to include negative attributes to assess the stereotype content? Yes, but only in the morality dimension. Scandinavian Journal of Psychology, 58(2), 170–178. https://doi.org/10.1111/sjop.12346

- Starr, K. W. (2005). Morality, Community, and the Legal Profession. Wyoming Law Review, 5(2), 403–415. https://heinonline.org/HOL/LandingPage?handle=hein.journals/wylr5&div=18&id=&page=

- Stets, J. E., & Carter, M. J. (2011). A Theory of the Self for the Sociology of Morality. American Sociological Review, Xx(x), 1–21. https://doi.org/10.1177/0003122411433762

- Stolper, O. A., & Walter, A. (2017). Financial Literacy, Financial Advice, and Financial Behavior. Journal of Business Economics, 87(5), 581–643. https://doi.org/10.1007/s11573-017-0853-9

- Suebvises, P. (2018). Social Capital, Citizen Participation in Public Administration, and Public Sector Performance in Thailand. World Development, 109, 236–248. https://doi.org/10.1016/j.worlddev.2018.05.007

- Sujana, E., & Saputra, K. A. K. (2020). Fraud Detection and Prevention Methods : Inspector ’ s Auditor ’ s Perception in Bali. Journal of Advance Research in Dynamical and Control System, 12(4), 8–16. https://doi.org/10.5373/JARDCS/V12I4/20201413

- Taft, M. K., Hosein, Z. Z., Mehrizi, S. M. T., & Roshan, A. (2013). The Relation between Financial Literacy, Financial Wellbeing and Financial Concerns. International Journal of Business and Management, 8(11), 63. https://doi.org/10.5539/ijbm.v8n11p63

- Uzun, A. M., & Kilis, S. (2020). Investigating Antecedents of Plagiarism using Extended Theory of Planned Behavior. Computers and Education, 144(January), 103700. https://doi.org/10.1016/j.compedu.2019.103700

- Van Prooijen, A. M., & Ellemers, N. (2015). Does it pay to be moral? How indicators of morality and competence enhance organizational and work team attractiveness. British Journal of Management, 26(2), 225–236. https://doi.org/10.1111/1467-8551.12055

- Warmath, D., & Zimmerman, D. (2019). Financial literacy as more than knowledge: The development of a formative scale through the lens of Bloom’s domains of knowledge. Journal of Consumer Affairs, 53(4), 1602–1629. https://doi.org/10.1111/joca.12286

- Wong, O. W. B., & Lui, M. C. G. (2007). Culture, Implicit Theories and the Attribution of Morality. Behavioral Research in Accounting, 19(1), 231–246. https://doi.org/10.2308/bria.2007.19.1.231

- Zeng, S., & Yang, W. (2020, December). Selection Of Variables And Indicators In Financial Distress Prediction Model-Svm Method Based On Sparse Principal Component Analysis. In 2020 International Conference on Wavelet Analysis and Pattern Recognition (ICWAPR) (pp. 26–30). IEEE.