?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The present paper provides new empirical evidence on the relationship between CEO facial masculinity and tax avoidance. We use data from non-financial companies listed on the Indonesia Stock Exchange during the period 2010–2019. The findings suggest that the CEO facial masculinity is positively associated with tax avoidance, which is one of the risky financial decisions. We also conducted a battery of robustness tests, including testing the sample of companies with/without a risk management committee, the interaction with CEO age and big 4 audit firm, the implementation of the tax amnesty in Indonesia, and addressing endogeneity using the propensity score matching. The current measurement of CEO masculinity, which is based on the fWHR of the CEO’s photo, could be further developed by future studies using artificial intelligence (AI) technology. This study contributes to the literature on CEO characteristics by filling in the gaps of biological characteristics associated with tax avoidance decisions. This is the first study investigating the relationship between CEO biological characteristics and tax avoidance.

Keywords:

1. Introduction

The Chief Executive Officer (CEO) has an important role and significantly influences an organisation’s financial and non-financial decisions (Bouaziz et al., Citation2020). In Indonesia, the position of CEO is the same as the president director who serves in a company. Based on the upper-echelon theory, company performance and strategic decisions taken by company leaders are influenced by the characteristics and conditions of each CEO (Hambrick & Mason, Citation1984). Therefore, it can be concluded that the characteristics of the CEO have a very important role in organisational outcomes.

The masculinity of the CEO’s face is one of the factors from within the manager that is thought to influence his behavior. A person’s facial masculinity is directly influenced by the hormone testosterone, which is a steroid hormone that encourages a person to take more risks to occupy a dominant position in a competition (Kamiya et al., Citation2019). The level of testosterone in humans is thought to have a relationship with a person’s behavior through neural mechanisms (Dabbs & Mallinger, Citation1999; Mehta & Beer, Citation2010). Several previous studies have found that the biological characteristics of a CEO, especially the masculinity of the CEO’s face, are related to the company’s financial policies and performance (Hambrick & Mason, Citation1984). Wong et al. (Citation2011) found that male CEOs with high fWHR achieved better financial performance than male CEOs with low fWHR.

The characteristics that exist in a CEO become an important factor in every strategic decision of the company. One of the resulting strategic decisions is related to the decision to avoid corporate tax. Corporate tax avoidance includes legal tax planning and illegal tax evasion aimed at reducing the corporate tax burden through investing and structuring business activities within the scope of tax laws or violating tax laws and related regulations (Dyreng et al., Citation2019). Due to the complexity and ambiguity in tax laws, tax authorities may have difficulty determining the taxes that companies must pay, especially when the company aggressively avoids taxes (Hanlon et al., Citation2017).

This research takes the setting of Indonesia because several previous studies have documented how CEO facial masculinity relates to earning management (Prasetyo et al., Citation2022) and leverage (Tjaraka et al., Citation2022). The findings explain that the decrease and increase in research and development practices impact increasing and decreasing the value of CEO masculinity and the growth and reduction in the value of research & development companies (Prasetyo et al., Citation2022). Besides that, the other findings explain that the decline and increase in earnings management practices impact increasing and decreasing the value of the masculinity face of male CEOs and increasing and decreasing the importance of corporate leverage (Tjaraka et al., Citation2022).

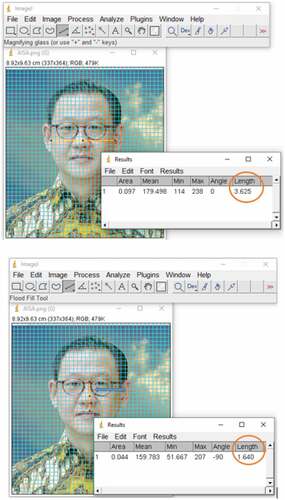

This study aims to analyze the relationship between CEO facial masculinity and tax avoidance in non-financial companies listed on the Indonesia Stock Exchange in 2010–2019. The data is obtained from the company’s annual report, Google Images, the company’s website, and the Osiris database. illustrates how bizygomatic width and upper face height were calculated from two-dimensional image. Hypothesis testing is done by using least square regression. The results of this study indicate that the masculinity-faced CEO has a significant positive relationship with tax avoidance. Furthermore, this indicates that the higher the CEO’s facial width-height ratio (fWHR), the higher the tendency to do tax avoidance. In addition, this research also performs various kinds of additional analysis to enrich the main analysis, and robustness to strengthen the results.

Figure 1. Illustration of measuring bizygomatic width and upper facial height (Hengky Koestanto, CEO of PT FKS Food Sejahtera Tbk)

This study contributes to the growing literature on the relationship between CEO facial masculinity and tax avoidance, especially in the context of developing countries with a high dependence on tax revenues. To the best of our knowledge, this study provides the first statistical panel evidence of this relationship from Indonesian public companies. The results of this study will be of interest to policymakers and regulators in choosing a company CEO. Stakeholders can give them consideration in making decisions. This is because the characteristics of the CEO as measured by the level of masculinity have a relationship with tax avoidance.

The structure of the paper is as follows: Section 2 discusses the Literature review and hypothesis development. Section 3 discusses the research methods. Section 4 presents result and discussion. Section 5 concludes the study.

2. Literature review and hypothesis development

The CEO has an important role and significantly influences financial and non-financial decisions in an organization (Bouaziz et al., Citation2020). Upper echelon theory states that CEO’s personality influences their prediction of choice (decision) in leading the company, which in turn will have an impact on organizational output, such as performance, investment in research and development (R&D), and tax payments (Hambrick & Mason, Citation1984). Previous researchers have widely studied the relationship between CEO characteristics (such as financial expertise, narcissistic, overconfidence, CEO hometown ties, CEO political connections, and others) and tax avoidance. Huang and Zhang (Citation2020) found that CEOs with financial expertise tend to choose more aggressive tax avoidance policies. On the other hand, Araújo et al. (Citation2021) prove a positive correlation between narcissistic CEOs and tax avoidance. Executives with this personality trait appear bold or aggressive, making them more prone to adopting tax avoidance strategies. Research Chyz et al. (Citation2019) shows empirical evidence that there is a positive relationship between a proxy for corporate tax avoidance and CEO overconfidence. Our study uses different proxies as a novelty in the corporate tax avoidance research literature. We use CEO facial masculinity as a proxy for CEO characteristics.

The masculinity of the CEO’s face is thought to be able to influence the company’s tax policy. CEO facial masculinity is an internal factor associated with complex masculine behaviours (including aggression, egocentrism, risk-seeking, and maintenance of social status) in men (Jia et al., Citation2014). The masculinity of the CEO’s face can encourage CEOs to implement tax strategies in the form of deferred payments or use legal and illegal mechanisms to reduce the company’s tax burden (Araújo et al., Citation2021). Generally, this action is called tax avoidance. Interestingly, research conducted by Kim et al. (Citation2022) elucidates the dark side of masculine-faced CEOs by empirically examining the relationship between masculine-faced CEOs and corporate fraud. And the results show that CEOs with high fWHR are more likely to commit fraud than CEOs with low fWHR. This positive association is consistent for each type of fraud: embezzlement, collusion, and tax evasion.

Previous research in the field of neuroendocrinology determined that facial width-height ratio (fWHR) as a proxy for facial masculinity can predict masculine social behaviour associated with occupying a dominant position in a competition (Kamiya et al., Citation2019; Kim et al., Citation2022). In addition, a series of characteristics of human behaviour is also related to testosterone levels. Lefevre et al. (Citation2013) have shown that men with high levels of facial width-to-height ratio (masculine) tend to have high testosterone levels. Previous research has also shown CEO facial masculinity’s effect on managerial preferences. Mills and Hogan (Citation2020) proves that high levels of fWHR are associated with more aggressive financial manager decisions. Apicella et al. (Citation2008) in their research showed that men with a higher masculine face tend to make risky financial decisions.

Tax avoidance can be one of the risky financial decisions chosen by masculine-looking CEOs. This action is taken to reduce the tax burden paid, and the company’s profit will increase. This relates to the CEO’s responsibility to develop, approve, and oversee the tax planning strategy of the companies they lead. The leadership style of each CEO is different and basically more sensitive to tax avoidance (Araújo et al., Citation2021). Wong et al. (Citation2011) documented that the CEO’s fWHR is positively related to firm profitability, especially in less cognitively complex firms. In addition, a more masculine CEO will try to occupy a dominant position in a competition (Kamiya et al., Citation2019), one of which is to generate high profits. This is done in order to attract investors to invest their funds in the company, which can then be used to finance the company’s activities. Therefore, a CEO with a masculine face will do everything he can to win the competition.

H1: There is a relationship between CEO facial masculinity and tax avoidance

3. Research methods

3.1. Samples and data sources

This study uses archival data from all non-financial companies listed on the Indonesia Stock Exchange from 2010–2019. The sample selection technique used is purposive sampling using specific criteria. In addition, this study uses secondary data obtained from the company’s annual report, Google Images, the company’s website, and the Osiris database. After eliminating some missing variables, we get a total sample of 1,529 firm-year observations. In Table Panel A, it can be seen how the distribution of the sample is based on the year of observation. From the table, at the distribution, more than half of the observations (50.62%) indicate more masculine-faced CEOs. Meanwhile, the distribution of samples by industry in Panel B is reported. The highest number of samples is in companies with SIC 2 (Construction Industries), as many as 422, and the least is in SIC 8 (Health, Legal, and Educational Services and Consulting). And after being divided based on the more masculine-faced CEO, the results are also the same, namely in SIC 2 as many as 212 or 50.24% including the more masculine-faced CEO. We resized all continuous variables at the 1st and 99th percentiles to reduce the effect of unwanted outliers. The distribution of data from all samples has been summarized in Table .

Table 1. Sample distribution

3.2. Variable definition and measurement

CEO facial masculinity (MASCULINITY) was the independent variable in this study, which was proxied by a dummy of facial width-to-height ratio (fWHR; Hambrick & Mason, Citation1984; Jia et al., Citation2014). A value of 1 is given if fWHR shows a value above the median of all samples and 0 otherwise. fWHR is the distance between the left and right zygion (cheekbones) (bizygomatic width) divided by the distance between the upper lip and the midpoint of the inner end of the eyebrow (upper facial height; Hambrick & Mason, Citation1984). This measurement uses ImageJ software, also used by several previous studies (Hambrick & Mason, Citation1984; Jia et al., Citation2014).

This study measures corporate tax avoidance using ETR, which is measured as the ratio of corporate tax expense to before-tax operating income (Panda & Nanda, Citation2020). A high ETR indicates that the company has paid or imposed a fairly large tax on its income (Mohanadas et al., Citation2019), thus indicating a low tax aggressiveness of the company (Noor et al., Citation2010). ETR is often used as a proxy for corporate tax avoidance because it reflects book-tax differences resulting from tax-aggressive (Lanis & Richardson, Citation2012). The required measurement data is also available from financial reports (Hanlon & Heitzman, Citation2010).

We also add some control variables that can influence the outcomes. First, related to other CEO characteristics, CEO age (CEOAGE), CEO busyness as measured by the number of positions held (CEOBUSY), CEO expertise in finance (CEOFIN), and previous CEO experience working as an auditor (CEOAUD). Second, we consider company characteristics such as whether the company has ever been audited by a big 4 company (BIG4), the size of the board in the company (BOARDSIZE), the number of audit committees in the company (AUCOM), consider whether there is a risk management committee (RMC), firm size (FIRMSIZE) and firm age (FIRMAGE). Third, we also add important financial ratios such as return on assets (ROA), debt to total assets (LEV) ratio, and company losses (LOSS). All variables used in this study are summarized in Appendix 1.

3.3. Research design

We use cluster regression with year and industry-fixed effects of testing the hypothesis using STATA 17.0 software. The results of data collection will be processed using statistical descriptive, Pearson correlation, two-sample independent t-test, regression testing for the primary analysis, and additional analysis. Furthermore, we also add regression using propensity score matching (PSM) to test the robustness of the model. The following is the regression equation model in this study:

4. Result and discussion

4.1. Descriptive statistics and univariate analysis

Table summarises the statistics of the variables used in this study. It can be seen that GAAP_ETR shows an average of 0.252 with a standard deviation of 0.176, and the maximum and minimum values are 0.886 and −0.327, respectively. For the MASCULINITY variable, the average is 0.506. This shows that more than half of the sample companies used in this study have a more masculine-faced CEO. Furthermore, the average age of the CEO is 53,213, with a maximum and minimum value of 86 and 30, respectively. Meanwhile, BIG4 shows an average of 0.427, meaning that the companies audited by BIG4 are less than half of the sample or around 42.7%. This average value is also similar to other CEO characteristics, such as CEOBUSY and CEOFIN.

Table 2. Descriptive statistics

Furthermore, in Table , Pearson correlation is shown to see how the correlation of one variable with one variable is univariate. It can be seen that the relationship between GAAP_ETR and MASCULINITY has a value of 0.043, while for CEOAGE and BIG4, it is 0.006 and 0.055, respectively. Meanwhile, the univariate relationship between MASCULINITY with CEOAGE and BIG4 is −0.130 and −0.004, respectively.

Table 3. Pearson correlation

4.2. Independent t-test

We conducted an independent t-test to find out whether there were differences in the research variables in the sample with CEO masculinity or not. In Table it is reported that GAAP_ETR shows a higher average of 0.0259 compared to 0.0244 in companies with CEO masculinity, with a coefficient value of 0.015 and a t-value of 1.664. CEOAGE shows a significant negative relationship with a coefficient of −2.354 and a t-value of −5.121, which indicates that the average age of CEOs in companies with high masculinity scores has lower age. Significant variables in the independent t-test were CEOBUSY, BOARDSIZE, RMC, LEV, FIRMSIZE, and FIRMAGE.

Table 4. Independent t-test of CEO masculinity

4.3. Regression result CEO masculinity with tax avoidance

Table shows our main regression analysis. The results of our study showed that CEO masculinity had a significant positive relationship with GAAP_ETR (coeff = 0.014, t = 1.84). In specification 1 main analysis, we report this significant positive relationship followed by several variables such as BIG4, CEOBUSY, RMC, ROA, FIRMSIZE, and FIRMAGE. Finally, we perform cluster regression by controlling for fixed effect variables for industry and year. From 1529 samples, we get an R2 value of 11.6%.

Table 5. Main regression and PSM analysis of CEO masculinity with tax avoidance

We conducted a robustness test in specification 2 in Table using propensity score matching (PSM) to strengthen the study’s results. The results show that with PSM testing, our main analysis is strengthened. In addition, the relationship between CEO masculinity and GAAP_ETR showed a significant relationship at the 1% level (coeff = 0.033, t = 3.69), which strengthens the study’s results. With a sample of 1084 after matching the score, we get a higher R2 value than the main analysis, which is 14.6%. Several control variables also showed significant results in the model, including BIG4, CEOAUD, BOARDSIZE, RMC, ROA, and FIRMAGE.

This study shows that CEO masculinity related to avoid taxes. This result support the upper echelon theory (Hambrick & Mason, Citation1984), which explains how a CEO’s personality can influence his decisions. Especially in the context of corporate taxation. The CEO’s facial masculinity is one of the proxies that can explain the biological characteristics of the CEO. This result captures how facial masculinity, measured by face width-to-height ratio (fWHR), can represent social behaviour associated with position dominance and competition. Research (Mills & Hogan, Citation2020) also explains how high fWHR is associated with more aggressive financial managers’ decisions. Therefore, our study supports the theory and hypotheses throughout the article.

Tax avoidance carried out by companies can reflect the aggressiveness of managers in making decisions. Moreover, research by (Amin et al., Citation2022) explains that CEOs’ facial masculinity is associated with less conservative accounting. Indeed, several CEO characteristics can influence how tax decisions, especially tax avoidance, are carried out (Duan et al., Citation2018; Elsheikh et al., Citation2022; Hsieh et al., Citation2018; Shin et al., Citation2022). Therefore, this study can complement previous research regarding CEO characteristics by providing empirical evidence from a characteristic biological perspective associated with tax avoidance decisions (Wang et al., Citation2020). This captures that tax avoidance is an important behavior that occurs in companies (Firmansyah et al., Citation2022; Machdar, Citation2022; Masri et al., Citation2019; Ngelo et al., Citation2022; Rahmayanti et al., Citation2022; Sudibyo & Jianfu, Citation2016; Sutrisno et al., Citation2022).

4.4. Additional analysis

4.4.1. Subsample firm with risk management committee (RMC) vs. without RMC

In addition to the main test, we have carried out to confirm the hypothesis, we also conducted several additional analyses. Table reports the additional analysis using a subsample of companies with RMC with companies with our RMC. The results show that the relationship between CEO masculinity and GAAP_ETR shows a positive significance in the subsample of firms without RMC (coeff = 0.015, t = 1.83). This can explain that the role of the risk management committee is very important in the organization. Furthermore, when companies have RMC, masculine CEOs tend not to do tax avoidance. Therefore, the risks that may arise when CEO masculinity and tax avoidance may have been considered by RMC so that the relationship becomes insignificant when the company has RMC.

Table 6. Additional analysis—sub sample RMC vs without RMC

4.4.2. Interaction with age of CEO and BIG4 firms

Next, we consider the role of CEO age and external auditors of BIG4 companies. In Table specification 1 shows the results of the interaction between CEO masculinity and CEO age, the results are significantly positive (coeff = 0.002, t = 1.68). Meanwhile, specification 2 shows the results of the interaction of CEO masculinity with BIG4 (coeff = 0.044, t = 2.49). These results indicate that the relationship between CEO masculinity and tax avoidance strengthens when the CEO’s age increases and BIG4 audits the company.

Table 7. Additional Analysis—Interaction CEO AGE & BIG4

4.4.3. Tax amnesty in Indonesia (Pre, Current, and Post)

We also divide the sample period based on the tax amnesty event in Indonesia Volume I in late 2016. We divide this research sample into three specifications: specification 1 pre-period, specification 2 current period, and specification 3 on post-period tax amnesty. The regression estimates are reported in . It can be seen from the three specifications only in specification 1, namely the pre-period tax amnesty which showed significant positive results at the 10% level (coeff = 0.016, t = 1.72). This means that the relationship between CEO masculinity and tax avoidance only occurs when the tax amnesty has yet to be enacted. This result can happen because companies tend to disclose their tax expense when the government implements a tax amnesty.

Table 8. Additional Analysis—Pre, Current, and Post Tax Amnesty in Indonesia

Tax amnesty in Indonesia was a very important event at that time (Hajawiyah et al., Citation2021; Nuryanah & Gunawan, Citation2022; Tiurmauli et al., Citation2018; Waluyo, Citation2017). With the amnesty of this tax, it is hoped to help increase state revenues and economic growth. Furthermore, it is expected to foster public awareness and compliance in carrying out the obligation to pay taxes. In addition, with the tax amnesty event, many companies report their taxes. So that companies will tend to reduce tax avoidance. This result captured the significant returns in the pre-period tax amnesty, while the other periods did not (Huda & Hernoko, Citation2017; Inasius et al., Citation2020; Said, Citation2017).

5. Conclusion

This study examines the relationship between CEO faced masculinity and tax avoidance. Using data from non-financial companies listed on the Indonesia Stock Exchange for 2010–2019, this study shows that CEOs with a higher FWHR tend to do tax avoidance. We also conducted a robustness test with a propensity score matching (PSM) test, and the results supported our main test. In addition, we also carried out several additional analyses, such as the presence of the company’s risk management committee (RMC), the age of the CEO, the company’s BIG4 external auditor, and the incidence of the tax amnesty in Indonesia.

Next, we also review how the role of the risk management committee is very important in the organization. The existence of this RMC can make the relationship between CEO masculinity and tax avoidance insignificant. Furthermore, we also find that the relationship between CEO masculinity and tax avoidance is strengthened when the CEO’s age is more senior and a Big 4 external auditor audits the company. Finally, we also tested the tax amnesty event in Indonesia by dividing the sample based on pre, current, and post. The results show a significant relationship that only occurs in the pre-period tax amnesty.

This research provides theoretical and practical implications. First, theoretically, this research has implications for developing literature related to CEO biological characteristics, especially fWHR, which represents CEO masculinity. In addition, this study also provides empirical evidence of the phenomenon of tax avoidance in Indonesia, specifically when a tax amnesty occurs. This can capture how CEO masculinity responds to tax avoidance when a tax amnesty occurs in Indonesia. Second, practically, this research will attract a lot of attention for stakeholders and regulators in making a policy by looking at it in the context of corporate governance.

This research has limitations that can be developed for future research. The independent variables of this study were measured using facial width-to-height ratio using ImageJ software and performed manually. So, there may be bias when calculating the fWHR value. Future research can use artificial intelligence (AI) software to measure facial width-to-height ratio for more precision.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Amin, K., Feng, C., Guo, P., & You, H. (2022). CEO Facial masculinity and accounting conservatism. Accounting and Business Research, 1–18. https://doi.org/10.1080/00014788.2022.2116384

- Apicella, C. L., Dreber, A., Campbell, B., Gray, P. B., Hoffman, M., & Little, A. C. (2008). Testosterone and financial risk preferences. Evolution and Human Behavior, 29(6), 384–390. https://doi.org/10.1016/j.evolhumbehav.2008.07.001

- Araújo, V. C., Góis, A. D., DeLuca, M. M. M., & De lima, G. A. S. F. (2021). CEO narcissism and corporate tax avoidance. Revista Contabilidade & Finanças, 32(85), 80–94. https://doi.org/10.1590/1808-057x202009800

- Bouaziz, D., Salhi, B., & Jarboui, A. (2020). CEO characteristics and earnings management: Empirical evidence from France. Journal of Financial Reporting and Accounting, 18(1), 77–110. https://doi.org/10.1108/JFRA-01-2019-0008

- Chyz, J. A., Gaertner, F. B., Kausar, A., & Watson, L. (2019). Overconfidence and corporate tax policy. Review of Accounting Studies, 24(3), 1114–1145. https://doi.org/10.1007/s11142-019-09494-z

- Dabbs, J. M., & Mallinger, A. (1999). High testosterone levels predict low voice pitch among men. Personality and Individual Differences, 27(4), 801–804. https://doi.org/10.1016/S0191-8869(98)00272-4

- Duan, T., Ding, R., Hou, W., & Zhang, J. Z. (2018). The burden of attention: CEO publicity and tax avoidance. Journal of Business Research, 87(February), 90–101. https://doi.org/10.1016/j.jbusres.2018.02.010

- Dyreng, S. D., Hanlon, M., & Maydew, E. L. (2019). When does tax avoidance result in tax uncertainty? The Accounting Review, 94(2), 179–203. https://doi.org/10.2308/accr-52198

- Elsheikh, T., Hashim, H. A., Mohamad, N. R., Almaqtari, F. A., & Ettish, A. A. (2022). CEO facial masculinity, characteristics and earnings management. Management and Accounting Review, December. https://doi.org/10.24191/MAR.V21i03-11

- Firmansyah, A., Arham, A., Qadri, R. A., Wibowo, P., Irawan, F., Kustiani, N. A., Wijaya, S., Andriani, A. F., Arfiansyah, Z., Kurniawati, L., Mabrur, A., Dinarjito, A., Kusumawati, R., & Mahrus, M. L. (2022). Political connections, investment opportunity sets, tax avoidance: Does corporate social responsibility disclosure in Indonesia have a role? Heliyon, 8(8), e10155. https://doi.org/10.1016/j.heliyon.2022.e10155

- Hajawiyah, A., Suryarini, T. K., & Tarmudji, T. (2021). Analysis of a tax amnesty’s effectiveness in Indonesia. Journal of International Accounting, Auditing and Taxation, 44, 100415. https://doi.org/10.1016/j.intaccaudtax.2021.100415

- Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top managers. Academy of Management Review, 9(2), 193–206. https://doi.org/10.2307/258434

- Hanlon, M., & Heitzman, S. (2010). A review of tax research. Journal of Accounting and Economics, 50(2–3), 127–178. https://doi.org/10.1016/j.jacceco.2010.09.002

- Hanlon, M., Maydew, E. L., & Saavedra, D. (2017). The taxman cometh: Does tax uncertainty affect corporate cash holdings? Review of Accounting Studies, 22(3), 1198–1228. https://doi.org/10.1007/s11142-017-9398-y

- Hsieh, T. S., Wang, Z., & Demirkan, S. (2018). Overconfidence and tax avoidance: The role of CEO and CFO interaction. Journal of Accounting and Public Policy, 37(3), 241–253. https://doi.org/10.1016/j.jaccpubpol.2018.04.004

- Huang, H., & Zhang, W. (2020). Financial expertise and corporate tax avoidance. Asia-Pacific Journal of Accounting & Economics, 27(3), 312–326. https://doi.org/10.1080/16081625.2019.1566008

- Huda, M. K., & Hernoko, A. Y. (2017). Tax amnesties in Indonesia and other countries: Opportunities and challenges. Asian Social Science, 13(7), 52–61. https://doi.org/10.5539/ass.v13n7p52

- Inasius, F., Darijanto, G., Gani, E., & Soepriyanto, G. (2020). Tax compliance after the implementation of tax amnesty in Indonesia. SAGE Open, 10(4), 2158244020968793. https://doi.org/10.1177/2158244020968793

- Jia, Y., Van, L. L., & Zeng, Y. (2014). Masculinity, testosterone, and financial misreporting: Masculinity, testosterone, and financial misreporting. Journal of Accounting Research, 52(5), 1195–1246. https://doi.org/10.1111/1475-679X.12065

- Kamiya, S., Kim, Y. H., Park, Andy, S., & Park, S. (2019). The face of risk: CEO facial masculinity and firm risk. European Financial Management, 25(2), 239–270. https://doi.org/10.1111/eufm.12175

- Kim, Y. H., Park, Andy, H., Park, J., & Shin, H. (2022). CEO facial masculinity, fraud, and ESG: Evidence from South Korea. Emerging Markets Review, 53, 100917. https://doi.org/10.1016/j.ememar.2022.100917

- Lanis, R., & Richardson, G. (2012). Corporate social responsibility and tax aggressiveness: An empirical analysis. Journal of Accounting and Public Policy, 31(1), 86–108. https://doi.org/10.1016/j.jaccpubpol.2011.10.006

- Lefevre, C. E., Lewis, G. J., Perrett, D. I., & Penke, L. (2013). Telling facial metrics: Facial width is associated with testosterone levels in men. Evolution and Human Behavior, 34(4), 273–279. https://doi.org/10.1016/j.evolhumbehav.2013.03.005

- Machdar, N. M. (2022). Does tax avoidance, deferred tax expenses and deferred tax liabilities affect real earnings management? Evidence from Indonesia. Journal Institutions and Economies, 14(2), 117–148. https://doi.org/10.22452/IJIE.vol14no2.5

- Masri, I., Syakhroza, A., Wardhani, R., & Samingun, N. A. (2019). The role of tax risk management in international tax avoidance practices: Evidence from Indonesia and Malaysia. International Journal of Trade and Global Markets, 12(3/4), 311. https://doi.org/10.1504/IJTGM.2019.101561

- Mehta, P. H., & Beer, J. (2010). Neural mechanisms of the testosterone–aggression relation: The role of orbitofrontal cortex. Journal of Cognitive Neuroscience, 22(10), 2357–2368. https://doi.org/10.1162/jocn.2009.21389

- Mills, J., & Hogan, K. M. (2020). CEO facial masculinity and firm financial outcomes. Corporate Board: Role, Duties and Composition, 16(1), 39–46. https://doi.org/10.22495/cbv16i1art4

- Mohanadas, N. D., Abdullah Salim, A. S., & Pheng, L. K. (2019). CSR and tax aggressiveness of Malaysian listed companies: Evidence from an emerging economy. Social Responsibility Journal, 16(5), 597–612. https://doi.org/10.1108/SRJ-01-2019-0021

- Ngelo, A. A., Permatasari, Y., Harymawan, I., Anridho, N., & Kamarudin, K. A. (2022). Corporate tax avoidance and investment efficiency: evidence from the enforcement of tax amnesty in Indonesia. Economies, 10(10), 251. https://doi.org/10.3390/economies10100251

- Noor, R. M., Fadzillah, N. S. M., & Mastuki, N. (2010). Corporate tax planning: A study on corporate effective tax rates of Malaysian listed companies. International Journal of Trade, Economics and Finance, 1(2), 189. https://doi.org/10.7763/IJTEF.2010.V1.34

- Nuryanah, S., & Gunawan, G. (2022). Tax amnesty and taxpayers’ noncompliant behaviour: Evidence from Indonesia. Cogent Business & Management, 9(1), 2111844. https://doi.org/10.1080/23311975.2022.2111844

- Panda, A. K., & Nanda, S. (2020). Receptiveness of effective tax rate to firm characteristics: An empirical analysis on Indian listed firms. Journal of Asia Business Studies, 15(1), 198–214. https://doi.org/10.1108/JABS-11-2018-0304

- Prasetyo, I., Aliyyah, N., Endarti, E. W., Rusdiyanto, R., & Rahmawati, A. (2022). The role of research & development as mediating the effect of male CEO masculinity face on earnings management: Evidence from Indonesia. Cogent Business & Management, 9(1), 1. https://doi.org/10.1080/23311975.2022.2140491

- Rahmayanti, E. A. N., Maryasih, L., & Achyar, D. H. (2022). No woman, no tax avoidance? A study on CEO gender in Indonesia. 2022 International Conference on Sustainable Islamic Business and Finance (SIBF), 25–29. https://doi.org/10.1109/SIBF56821.2022.9939674

- Said, E. W. (2017). Tax policy in action: 2016 tax amnesty experience of the Republic of Indonesia. Laws, 6(4), 16. https://doi.org/10.3390/laws6040016

- Shin, H., Park, J., Kim, Y. H., & Andy. (2022, April). CEO facial masculinity, fraud, and ESG: Evidence from South Korea. Emerging Markets Review, 53, 100917. https://doi.org/10.1016/j.ememar.2022.100917

- Sudibyo, Y. A., & Jianfu, S. (2016). Political connections, state owned enterprises and tax avoidance: An evidence from Indonesia. Corporate Ownership and Control, 13(3), 279–283. https://doi.org/10.22495/cocv13i3c2p2

- Sutrisno, P., Utama, S., Anitawati Hermawan, A., & Fatima, E. (2022). Founder and descendant vs. professional CEO: Does CEO overconfidence affect tax avoidance in the Indonesia Case? Economies, 10(12), 327. https://doi.org/10.3390/economies10120327

- Tiurmauli, K., Pasu, R., Fauziah, F., Halawa, S. D., & Rahayu, C. A. (2018). The impact of tax amnesty policy influence the investment decision and profitability in stock prices the best 45 companies in Indonesia. IOP Conference Series: Earth and Environmental Science, 175, 12038. https://doi.org/10.1088/1755-1315/175/1/012038

- Tjaraka, H., Hidayat, W., & Rusdiyanto, R. (2022). The role of earning management as a mediator of the effect of the facial width to height ratio CEOs on leverage. Cogent Business & Management, 9(1), 2115733. https://doi.org/10.1080/23311975.2022.2115733

- Waluyo. (2017). Tax amnesty and tax administration system: An empirical study in Indonesia. EUROPEAN RESEARCH STUDIES JOURNAL, XX(Issue 4B, 20, 548–556. https://doi.org/10.35808/ersj/910

- Wang, F., Xu, S., Sun, J., & Cullinan, C. P. (2020). Corporate tax avoidance: A literature review and research Agenda. Journal of Economic Surveys, 34(4), 793–811. https://doi.org/10.1111/joes.12347

- Wong, E. M., Ormiston, M. E., & Haselhuhn, M. P. (2011). A face only an investor could love: CEOs’ facial structure predicts their firms’ financial performance. Psychological Science, 22(12), 1478–1483. https://doi.org/10.1177/0956797611418838

Appendix 1

List of Variable Definition

Appendix 2.

CEO Facial Masculinity Measurement

CEO facial masculinity (MASCULINITY) was proxied by a dummy of facial width-to-height ratio (fWHR; Jia et al., Citation2014; Kamiya et al., Citation2019). A value of 1 is given if fWHR shows a value above the median of all samples and 0 otherwise. fWHR is the distance between the left and right zygion (cheekbones) (bizygomatic width) divided by the distance between the upper lip and the midpoint of the inner end of the eyebrow (upper facial height; Kamiya et al., Citation2019). This measurement uses ImageJ software used by several previous studies (Jia et al., Citation2014; Kamiya et al., Citation2019).

Measuring the masculinity of the CEO’s face is carried out in several steps. First, collect photos or pictures of the CEO of each firm obtained from the annual report, firm website, or Google image. The second step is to exclude female CEOs because, according to research by Jia et al. (Citation2014), this measurement can only be used on CEOs of the male gender. The third step is to measure the width and height of the face. Finally, divide the width (bizygomatic width) by the upper facial height to determine the fWHR value. There are several provisions in selecting CEO photos that will be used to measure the CEO’s facial masculinity. First, the CEO must face straight ahead with the boundary between the ear and cheek clearly visible. Second, the CEO’s photo quality is good and not too small.