Abstract

The purpose of the study is to examine the impact of agency issues such as free cash flow, empire-building, managerial risk aversion, and private benefit of control on post-merger financial performance in the context of emerging markets of SAARC and ASEAN regions. The sampling period for the study is from 2000 to 2017, limited to M&A deals where at least three years of pre- and post-merger data is available. A total of 184 M&A deals were analyzed from SAARC and ASEAN regions. Financial performance is measured through operating profit returns and cash returns, while the explanatory variables are free cash flow, firms’ size, industry relatedness, and block holding. Two-sample t-test is used for univariate analysis, and OLS regression is used for multivariate analysis. Results reveal that post-mergers and acquisition (M&A) financial performance declined as compared to pre-M&A financial performance over three (−3, +3) years window. Opposite to the free cash flow hypothesis, this study found that free cash flows are beneficial for acquirers in the context of emerging markets. Furthermore, acquirers’ size has either no impact or a significantly positive impact in robustness check on post-M&A performance, which rejects the empire-building motive. Unrelated mergers cause a decline in post-M&A performance, and large block holding enhances post-M&A performance. The findings of the study are helpful for managers, shareholders, and the board’s members to ensure that the free cash flow before the M&A transaction is positive and consistent also conscious of the nature of the target and avoid unrelated M&A deals.

1. Introduction

Mergers and acquisitions (M&A) is growth strategy employed by firms across the globe. Research also increased proportionately with increasing trend in M&A (Boateng et al., Citation2011). Gao and Kling (Citation2008) states that reorganization, particularly M&A, is vital to firm’s development. Large numbers of M&A transaction are incurred every year in corporate world and at the same time the success of mergers deals are always under discussion. Mergers and acquisitions (M&A) influence by different financial and strategic objectives (Kalra et al., Citation2013). Motive behind the M&A deals influence the post-M&A financial performance and the motives are synergy, market share and rapid growth (Ladha, Citation2017). But there are motives that arise from agency conflicts such as empire building, managerial risk aversion and private benefits of conflict.

Motive behind M&A deals could be any, but it is important to measure the impact of such on post-M&A financial performance of the acquirers firms. The impact on post-financial performance communicate about the success or failure of M&A transaction. Mergers and acquisitions (M&A) are not spontaneous event but it took time and involves huge cost and efforts. Management and shareholders are interested in success of M&A deals due to substantial cost incurred by acquirers and success or failure of M&A deals is a topic of debate for researchers as well as for practitioner (Bhaskar et al., Citation2012).

Mergers and acquisitions (M&A) deals are frequently happening phenomena in the corporate landscape worldwide. Research on mergers and acquisition (M&A) is deemed important as it involves a considerable amount of wealth, and an increasing number of M&A deals are witnessed happening, generally, around the globe and, particularly, in SAARC and ASEAN regions.Footnote1 Mergers and acquisitions (M&A) have an irrevocable impact on target and acquirer firms, employees of firms involved, competitors, and the complete supply chain. Thus, the topic received attention in economic and finance literature and public news. Consequently, different aspects of M&A have been studied and investigated by researchers across the globe.

Research on M&A is highly skewed towards developed market and developing market received little attention in this regards (Mehrotra & Sahay, Citation2018). Developing markets have family business & concentrated ownership, weak regulatory authority, political instability and weak judicial system (Jackling & Johl, Citation2009; Sun et al., Citation2017).

The obvious motive of mergers and acquisitions (M&A) is to gain synergistic benefits that arise from combining two firms (Nguyen et al., Citation2012), but research shows agency and hubris motives behind M&As. Synergy then appears in enhanced profitability, cost reductions, growth, and market share. The impact of mergers and acquisitions (M&A) deals on firms’ post-M&A performance is a highly investigated area with inconsistent results. Inconsistent results of empirical studies showed that the synergy motive is not achieved in the post-M&A period. Therefore, the discussion further extended to examine other motives behind M&A activities such as empire building, managerial risk aversion, private benefits of control, managerial hubris, and regret avoidance. Post-M&A performance is not only affected by the M&A event but also influenced by other factors such as free cash flow (Jensen, Citation1986), firm size (Sharma & Ho, Citation2002), related versus unrelated target (Chatterjee & Lubatkin, Citation1990), acquirers past performance, and ownership concentration (Chen & Young, Citation2010). Research is not unequivocal on factors that affect post-M&A performance and lead to an intriguing question “What is the motive behind mergers and acquisition? Synergy or Too big to fail.”

Empire building motive of managers refers to working in large organizations and enjoying more perks and privileges rather than increasing shareholders’ wealth. Managers desire to achieve the status of “Too big to fail” and consume free cash flow for less profitable M&As, engage in unrelated M&As and enlarge the size of the organization. However, emerging markets are characterized by high ownership concentration, and block holders actively monitor the firms that consequently reduce type-1 agency problems (Gregory & Wang, Citation2013). It is justifiable to investigate synergistic benefits that arise due to M&As and also examine agency issues such as empire building, managerial risk aversion and private benefit of control in emerging markets of SAARC and ASEAN regions.

The question is unanswered, and there is no clear stance in the literature to resolve the quandary of factors affecting post-M&A performance. This study examined synergy motive by comparing pre- and post-M&A performance and also investigated the motive of “Too big to fail” by assessing the impact of free cash flow, acquirers size, relatedness of target and block holding on post-M&A financial performance. The scope of the study covered emerging markets of SAARC and ASEAN regions which includes India, Pakistan, Malaysia, Indonesia, Thailand and the Philippines.

Motivation for this study is to examine that whether agency issue such as empire building and risk aversion exist in the presence of concentrated ownership in developing markets (SAARC & ASEAN regions). In addition to that, possibility of private benefits of control will also be investigated in the presence of concentrated of ownership, business group and family businesses.

2. Literature review & hypothesis development

Empirical studies on M&A examined the financial performance of a firm in the post-M&A period, and the literature is inconsistent in its findings. To investigate post-M&A financial performance, research is categorized into two streams based on financial performance measurement. Studies that use stock prices to measure financial performance are termed as event studies, while the second stream of studies uses accounting measures, and the current study lies in the second stream. Reasons behind choosing accounting-based measures are market’s under or over reaction to merger announcement (Aggarwal & Garg, Citation2022; Gregory & Wang, Citation2013), and announcement period returns are less likely to capture long-term synergistic benefits (Schoenberg, Citation2006).

2.1. Pre- and post-merger performance

Ubiquitous studies reported a positive effect of M&A on the post-M&As financial performance of acquirers firms. Post-mergers cash flows, profits and leverage are higher than pre-merger period (Lau et al., Citation2008) and cash returns (Linn & Switzer, Citation2001; Rahman & Limmack, Citation2004; Ramaswamy & Waegelein, Citation2003), profitability and liquidity (Aggarwal & Garg, Citation2022; Alhenawi & Stilwell, Citation2017; Heron & Lie, Citation2002; Kalra, Citation2013) improved in the post-mergers period.

The opposite opinion also exists in the literature that revealed poor performance after M&A transactions. Post-M&A financial performance, measured in accounting ratios, decrease in UK firms (Ravenscraft & Scherer, Citation1987). Ghosh (Citation2001) found similar results and reported that cash returns declined after M&A, and Kumar (Citation2009) concluded that asset turnover and solvency ratios of acquirers declined in the post-mergers period. Acquirer firms experienced higher return on assets (ROA), return on equity (ROE) and profit margin in post-M&A period in comparison with pre-M&A period (Akben-Selcuk & Altiok-Yilmaz, Citation2011; Cabanda & Pajara-Pascual, Citation2007; Yeh & Hoshino, Citation2002).

Literature is inconsistent in consensus on post-M&A performance (Ismail et al., Citation2011). Some studies revealed that M&A does not lead to synergy, and on average, M&A is unable to maximize the wealth of shareholders. Other streams of researchers reported positive returns after M&As. While another stream of studies showed no impact on returns as a result of M&A. Hence, below hypothesis are deduced.

H1: Financial performance of the firms is significantly different between the pre-M&A period and the post-M&A period.

2.2. Empire building and free cash flow hypothesis

The free cash flow hypothesis posits that firms with unconsumed debt capacity and a substantial amount of free cash flows are likely to engage in poor performing or even value-destroying mergers and acquisitions (Jensen, Citation1986). Firms with ample free cash flows are subject to conflict of interest between managers and shareholders on the payout of free cash flows (Harford et al., Citation2012). M&A is one of the suitable avenues where managers invest cash rather than distribute it among the shareholders. Managers overinvest (Officer, Citation2011) and undertake value-destroying M&As (Schmidt & Fowler, Citation1990) to enhance their compensation and prestige irrespective of the Net Present Value (NPV) of the project.

Corporate finance theories such as agency theory advocate that free cash flows, industry type, and growth opportunities influence the post-M&A value of firms (Denis & Sibilkov, Citation2010; Dogru, Citation2017). Firms possessing high free cash flows are engaged in value-destroying acquisitions as compared to firms having a low level of free cash flow (Dogru et al., Citation2020; Harford et al., Citation2012; Masulis et al., Citation2007; Oler, Citation2008). In the absence of free cash flows, firms borrowed to finance mergers deals, and strict debt covenants worked as a monitoring tool for managers, which restricted spending of free cash flows to pursue their empire-building motives (Servaes, Citation1991).

The free cash flow hypothesis supports agency theory and conflicts with financial synergy theories and the pecking order hypothesis. The free cash flow hypothesis is developed in U.S. markets where firms have diverse ownership and a robust regulatory environment (Gregory & Wang, Citation2013). The possibility exists that free cash flow becomes less relevant in emerging markets characterized by concentrated ownership and a weak regulatory framework. Concentrated ownership mitigates the traditional agency issues, and it is argued that the free cash hypothesis needs to be investigated in the emerging market of SAARC and ASEAN regions.

H2: Post-M&A financial performance is negatively affected by the acquirer’s free cash flow before the acquisition.

Empire building motive of managers is manifested by working in a large organization, and managers pursue it through undertaking underperforming M&As. Small firms are involved in value-creating M&As as compared to large firms (Moeller et al., Citation2004; Nguyen et al., Citation2012; Sharma & Ho, Citation2002). The acquirer size effect exists in developed markets where large acquirer firms experience lower acquisition returns than smaller acquirers firms (Yaghoubi et al., Citation2016).

Large firms are less likely to be acquired and are less likely to be exposed to the disciplinary actions of the market for corporate control (Offenberg, Citation2009). Masulis et al. (Citation2007) posited that large firms are more likely to be engaged in empire-building as compared to small firms.

Large corporate firms in emerging economies have more market power and stronger political connections to safeguard shareholder wealth and consequently led to higher performance in the post-M&A period (Brockman et al., Citation2013; Humphery-Jenner & Powell, Citation2014; Kinateder et al., Citation2017; Yang & Zhang, Citation2015; Zhao et al., Citation2019). While opposite opinion also exists, which state that weak regulatory authority and weak corporate governance mechanism can exacerbate the empire-building motive of managers (Chen et al., Citation2011).

It is still debatable whether large acquirers indulge in empire-building or large acquirers have more resources and management skills to increase post-M&A performance. Therefore it is justifiable to examine the impact of the acquirer’s size (empire-building motive) on post-M&As performance in emerging markets of SAARC and ASEAN regions. The literature is unable to solve the M&As performance quandary and lead to the below hypothesis;

H3: Post-M&A financial performance is negatively affected by firm size before the acquisition.

2.3. Managerial risk aversion

Managers employed in the stand-alone company are vulnerable to business risk in case of recession. Such firms are prey to the acquisition, and managers are no more required or may face dismissal due to poor performance. Shareholders diversify their risk quickly by diversifying their portfolio in an open market, but managers tend to diversify their risk at the firm level. So, M&As transactions are motivated by risk reduction strategy. Firms with diverse shareholding (Amihud & Lev, Citation1981) and CEOs’ investment in ownership (May, Citation1995) are likely to be involved in conglomerate mergers, and managers are in a suitable position to pursue personal motives of risk aversion.

Related M&A negatively influences total risk measured by volatility of ROA, whereas unrelated M&A decreases the systematic risk of a firm measured by beta (Wu & Chiang, Citation2019). Similarly, Chatterjee and Lubatkin (Citation1990) also confirmed that related mergers reduce the variability of stock returns and unrelated mergers reduce business risk. Acquiring in related industry decrease risk and enhance the performance of acquirer firms (Zhang et al., Citation2020; Zhou et al., Citation2020).

Managers’ self-serving motives led to bad acquisitions, and unrelated mergers were penalized by the stock market (Morck et al., Citation1990). Related M&As lead to synergistic benefits and operational efficiency rather than diversifying acquisitions (Lin & Chou, Citation2016), but concentrated ownership minimizes the losses of unrelated mergers (Doukas et al., Citation2001).

Nonetheless, diversifying M&A deals caused improved long-run post-M&A financial performance (Kruse et al., Citation2002). Still, there is no clear stance of literature on the impact of related/unrelated mergers on post-M&A performance.

H4: Related M&A and Unrelated M&A have a significant difference in post-Merger and acquisitions (M&A) financial performance.

2.4. Principal-principal conflict

The classical principal-agent conflict has received much attention in academic research, but managers are nothing more than a tool used and controlled by controlling shareholders. Majority shareholders that influence decisions of firms give rise to other types of agency issues called principal-principal conflict. This issue occurs when controlling shareholders (family, institutional investors) get private benefits of control, called financial gain, which is not available to minority shareholders (Dyck & Zingales, Citation2004; Young et al., Citation2008). Although block holders decreased monitoring cost and increased value but exceeded from an optimal level, concentrated ownership generates agency problems (Demsetz, Citation1983) and lead to expropriation of wealth from minority shareholders.

Majority shareholders (block holders, founder family, and institutional shareholders) pay a high premium to acquire a target in which they receive high cash flows right and shift wealth from minority shareholders to controlling shareholders (Albuquerque & Schroth, Citation2010). Higher private benefit of control prevailed in less developed countries where concentrated ownership exists, and privatization is let to happen through private negotiation (Dyck & Zingales, Citation2004). After a survey of the literature, Holderness (Citation2003) concluded that block holders have incentives and opportunities to gain private benefits from corporate affairs while excluding non-controlling (minority) shareholders.

Chinese firms engaged in cross-border M&As with large government ownership experienced low cumulative abnormal returns (Chen & Young, Citation2010), revealing that minority shareholders doubt government interference and the situation due to principal-principal conflicts. High ownership concentration negatively influences post-M&A long term performance (Yaacob & Alias, Citation2018). While literature also supports the opposite opinion that block holders actively monitor the managers and achieve high post-M&As performance (Boateng et al., Citation2017; Shleifer & Vishny, Citation1997).

In emerging markets, business group affiliated firms achieved better long term post-M&A performance than stand-alone companies because business groups capitalized on resources to achieve post-merger performance (Popli et al., Citation2017). Institutional ownership in acquirers and target increased synergistic benefits and enhanced post-M&A long-term performance (Brooks et al., Citation2018).

Block holding effect on post-M&A performance is a less examined area and needs further investigation. Therefore, the below hypothesis is formulated in the light of the above literature;

H5: Post-M&A financial performance is negatively affected by the percentage of block-holding.

3. Methodology

The post-M&A financial performance is assessed through event study methodology or through accounting based measures for (−3, +3) windows around mergers deals. This study used accounting based measure in order to examine the impact of agency issues on post-M&A financial performance. In event study approach, the abnormal returns are measured around the announcement of M&A deals. Another approach is to assess the success of M&A deals through accounting based measure for a longer period of time.

Rationale behind the using accounting based measured is that M&A deals are strategic decisions and need to be examine in longer period of time. Contrary to it, event study methodology is biased towards investor’s expectations and perception about the potential synergy from M&A deals which might not reflect the real economic value added (Kar et al., Citation2021)..

3.1. Population

All M&A deals occurred and completed in SAARC and ASEAN regions constitute population for this study. Mergers and acquisitions (M&A), for this study, mean those mergers or acquisitions deals in which merged firm or target firm ceases to exist after the M&A transaction.

3.2. Sampling

Multilevel mixed method of sampling is used in this study (Teddlie & Yu, Citation2007) and in the first level, the study selected SAARC and ASEAN regions from the globe. The second level extends it scope to emerging markets of SAARC and ASEAN regions. According to MSCI Inc. (formerly Morgan Stanley Capital International and MSCI Barra), Pakistan and India from the SAARC region, and Malaysia, Thailand, Indonesia, and the Philippines from the ASEAN region qualified as emerging economies. These six emerging economies were selected as the sample.

At the 3rd level, a purposive sampling technique is used to select firms involved in M&As. So, the selection criteria for the firms to be included in the sample is as follow:

Those M&A transactions are included in the sample, which took place from 2000 to 2017.

Only non-financial firms are selected for this study.

Financial information of acquirer and target firm for three years before M&A and three years after the M&A deal is available.

Both acquirer firms and target (acquired) firms must be listed on respective stock exchanges of Pakistan, India, Malaysia, Thailand, Indonesia, and the Philippines.

The deal has to be a type of merger or acquisition.

The sample includes 70 M&A deals from India, 29 deals from Pakistan, 32 deals from Malaysia, 20 deals from Indonesia, 19 deals from Thailand and 14 deals from the Philippines.

3.3. Data collection

The study used three years (−3,+3) window before and after M&As for the analysis as the method is used in earlier research (Linn & Switzer, Citation2001; Sharma & Ho, Citation2002).

Firm-specific variables such as return on assets (ROA), return on equity (ROE), total assets, profit margin (PM), Tobin’s Q, free cash flow (FCF) and relative target size are computed from annual reports of respective firms.

Deal specific variables such as related vs unrelated mergers type, and method of payment (cash vs stock) are gathered from the Bursa Malaysia library, from websites of the acquirer or target firms, and news archives.

Country specific variables (GDP, Ease of doing business) of the sample countries are extracted from the World Bank database.

3.4. Statistical technique

Below statistical analyses are employed to test the above-formulated hypotheses.

3.4.1. Change model or univariate analysis

The change model is based on the univariate analysis in which the mean difference between the two variables is compared. The group will be made based on (1) pre-M&As and Post-M&As period, (2) free cash flow, (3) size of the firm, and (4) related and unrelated mergers. This model tests whether the change between the two groups is significantly different from zero or not.

Nonetheless, the change model has limitations but has been extensively used in the literature (Healy et al., Citation1992; Kalra, Citation2013; Kumar, Citation2009; Linn & Switzer, Citation2001).

3.4.2. Regression (Multivariate) analysis

The change model provides insights only into the changes of means of variables between groups and informs about the existence of a phenomenon but cannot elucidate the reasons and causes of such changes. In multivariate analysis, the cause and effects of variables are studied.

In this study, multiple regression models are employed to capture the impact of empire building (free cash flows & total assets), risk aversion (related/unrelated) and principal-principal conflicts (block holding) on post-M&As performance.

Prior studies have also used multiple regression models to investigate the effect of explanatory variables on dependent variables in the context of mergers and acquisitions deals (Agrawal et al., Citation1992; Ghosh, Citation2001; Heron & Lie, Citation2002; Powell & Stark, Citation2005; Sharma & Ho, Citation2002; Shim, Citation2011).

The following linear equations are used to approximate a relationship that is based on the principle of least squares method.

3.5. Measurement of variables

The dependent variable is measured through return on assets (RoA), return on equity (ROE), operating cash flow return on both asset & equity (OCFret) and profit margin. These measures used in this study are consistent with earlier studies that have used operating profit returns on asset and equity (Ghosh, Citation2001; Healy et al., Citation1992; Linn & Switzer, Citation2001; Powell & Stark, Citation2005; Sharma & Ho, Citation2002; Switzer, Citation1996;) and operating cash flow returns (Fu et al., Citation2016; Hauser, Citation2018; Shim, Citation2011).

Financial performance is measured through return on asset and return on equity and these dependent variables. Free cash flow, merger type (related/unrelated), size of acquirer firm (natural log of assets) are block holding are explanatory variables (independent variables) while method of payment (cash/Stock), target firms relative size, board size, board independence, audit committee size, audit committee independence, GDP, and ease of doing business are control variables as shown in the Table . The Table summarized the regression models use to examine the impact of free cash flow, firm’s size, mergers types and block holding on post-M&A financial performance.

Table 1. Regression model for each hypothesis

Table 2. Shows dependent and independent variables and proxies that measure the variables for this study

4. Analysis

To examine whether M&A increase financial performance and create synergy, pre- and post-mergers performance are compared as shown in Table .

Table 3. Mean comparison for 184 merger & acquisition in SAARC & AEASN

Accounting measures of financial performance shows a significant decrease during the post-M&A period except for cash returns on asset, as evident from the mean comparison using two-sample t-test is shown in Table .

This study’s findings are supported by earlier researchers from the developed markets (Ghosh, Citation2001; Sharma & Ho, Citation2002) and from emerging markets (Ferrer, Citation2012; Kar et al., Citation2021; Mantravadi & Reddy, Citation2007; Syukur & Bungkilo, Citation2020; Zuhri et al., Citation2020; Mantravadi, Citation2020a). Earlier studies have also provided opposite evidence on post-M&A performance (Aggarwal & Garg, Citation2022; Healy et al., Citation1992; Heron & Lie, Citation2002; Linn & Switzer, Citation2001; Powell & Stark, Citation2005;). Contrary to the findings of this study, Indian construction and real estate industry improved financial performance in post-M&A period (Gupta, Raman, Tripathy et al., Citation2021b).

The reasons for conflicting results are the use of different proxies for measuring financial performance, market context and deals specific variables.

The increase in firm size and block holding during the post-M&A period is statistically significant at a 1% level, which reveals that firm size increased as a result of mergers and acquisitions. Similarly, block holding also increased by 4.44% (statistically significant at 1%) due to mergers deals in the SAARC and ASEAN region.

4.1. Univariate analysis

Univariate analysis categorizes the data into a group or subset of variables. The current study analyzed financial performance of acquirers firms on the basis of free cash flow, size of firm and related & unrelated mergers deals as used as categorical variables.

4.1.1. Empire building and free cash flow hypothesis

Firms’ free cash flow is categorized into two groups based on the mean value (above mean & below mean) to assess the impact of free cash flow on post-M&A performance. Results in Table show that acquirers firms with free cash flow above means show higher financial performance as compared to firms having free cash flow below mean, and the mean difference is statistically significant for all performance variables at 1% level except for ROE and Tobin’s Q which is significant at 5% level.

Table 4. Free Cash flow and Post-M&A performance for 184 Mergers & Acquisitions in SAARC & AEASN

It is evident from the results that acquirer firms with more free cash flows outperform the acquirer firms with less amount of free cash flow. This study’s results do not support Jensen’s (Citation1986) free cash flow hypothesis.

In the context of the emerging market of SAARC and ASEAN region characterized by high ownership concentration, it is argued that concentrated ownership provides sufficient monitoring and hence, consequently, reduce agency issues arising from the presence of free cash flows. Thus free cash flow hypothesis has become less relevant in the emerging markets characterized by high ownership concentration, and our results are consistent with earlier studies (Cremers & Nair, Citation2005; Gregory & Wang, Citation2013).

4.1.2. Empire building and acquirers size

Firms’ size is used as a proxy to examine the empire-building motive, and firms are categorized into large and small groups based on the mean value. Two-sample t-test is used to examine empire building motives in emerging markets of SAARC and ASEAN regions.

Large acquirer firms produce higher ROE but the mean difference is statistically significant at 10% level as shown in Table . Return on equity (RoE) shows that large firms perform better in operating results which reveals that empire-building motive is less likely to prevail in the emerging market of SAARC and ASEAN regions. Similar findings are confirmed in weak governance countries (Humphery-Jenner & Powell, Citation2014) and in BRICS countries (Kinateder et al., Citation2017).

Table 5. Acquirers Size and Post-M&A performance for 184 Mergers & Acquisitions in SAARC & AEASN

4.1.3. Related versus unrelated mergers

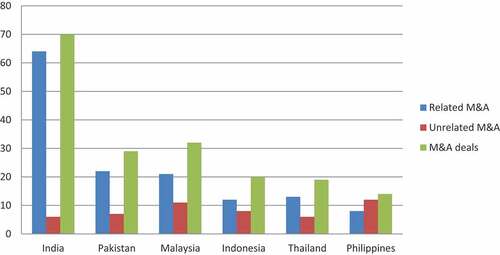

Figure reveals that 91.42% (64 out of 70) of the M&A sample in India is related M&A deals in which targets and acquirers firms are from related (common) industries. Similarly 75.86% (7 out of 29) in Pakistan, 65.63% (21 out of 32) in Malaysia, 60% (12 out of 20) in Indonesian and 68.42% (13 out of 19) in Thailand are related M&A deals. While in the Philippines the related M&A deals are 14.29% (2 out of 14) only of the total Thai’s M&A deal sample. Overall SAARC and ASEAN have 134 related M&A deals out of 184 M&A deals which constitute 72.83% of the total sample. The sample has more related M&A than unrelated M&A deals.

Figure 1. M&A Deals in SAARC & ASEAN

It is summarized that related M&A deals, where target and acquirers firms have common industry, are more than unrelated M&A deals in all countries except for the Philippines. Conglomerate mergers are dominant in the Philippines while the Indian market is dominant by related mergers.

Two-sample t-test is used to capture the impact of related and unrelated mergers on post-M&A performance. Results in Table reveal that related mergers outperform unrelated mergers in terms of ROA, ROE, cash return on equity, and the mean difference is statistically significant at a 5% level.

Table 6. Related versus Unrelated Mergers and Post-M&A performance for 184 Mergers & Acquisitions deals in SAARC & AEASN

Related mergers create synergy more than unrelated mergers, as evident from operating results. Results do not confirm managers’ risk avoidance motives in the emerging markets of the SAARC and ASEAN region. Similar results are produced by earlier researchers, such as industry commonality positively affects post-M&A performance (Lin & Chou, Citation2016) and related industry enhance post-M&A performance (Cui & Leung, Citation2020; Gupta, Raman, Tripathy et al., Citation2021a; Zhang et al., Citation2020; Zhou et al., Citation2020;). There is also opposite finding that horizontal mergers in same industry (related merger) cause to decline post-M&A financial performance in Indian acquirers (Mantravadi, Citation2020b).

4.2. Multivariate analysis

In univariate analysis, only variable of interest is used as the sole factor which influences the dependent variable, but post-M&A performance is not influenced by single variable. Other variables also influence post-M&A performance of acquirers firms. The multivariate analysis incorporates simultaneously multiple variables for hypothesis testing.

4.2.1. Free cash flow hypothesis

Pre-M&A free cash flow of the acquirers firm has a positive impact on post-M&A performance, and the impact is statistically significant at 1% level for all measures of performance except for EBITROEpost, as shown in Table . Our results contrast with Jensen’s (Citation1986) free cash flow hypothesis and other studies in the developed markets (Doukas, Citation1995; Gregory, Citation2005; Lang et al., Citation1991). This study’s findings suggest that the free cash flow hypothesis is less relevant in the emerging markets of SAARC and ASEAN regions due to high ownership concentration, which reduces agency issues. Gregory and Wang (Citation2013) also reported that free cash flow enhances performance provided institutional shareholders’ monitoring is sufficient. Similarly, Tarigan et al. (Citation2018) examine Indonesian firms and found that M&A are motivated by synergy motives instead of agency motives.

Table 7. Regression Analysis estimates for Free Cash Flow and Post-M&A performance for 184 Mergers & Acquisitions deals in SAARC & AEASN

Other possible reasons for the difference of our results with earlier studies and established literature are the measurement of financial performance and the difference of market characteristics of developed and emerging economies.

Board size of acquirers firms has positive and significant impact on cash return on asset and cash return on equity in the post-M&A financial period while board audit committee size of acquirer firms positively affected operating profit return on equity as shown in Table . Findings of the study is consistent with resource dependence theory that posit that large board is helpful in arranging the resources. The study is also consistent with earlier research such as Mohapatra (Citation2017) examined Indian firms and concluded that firms with large board experience higher financial performance. In similar study, Abdullah (Citation2022) concluded that board size has positive and significant impact on firm performance in Malaysia market.

Board independence negatively affect the operating profit return on asset and cash return on asset and results are statistically significant. The possible reason for the negative impact is inefficient role of independent director in post-M&A integration (Liu & Wang, Citation2013). The cost of large number of outside directors on board exceed the benefits (Kor, Citation2006) and proved free rider. While the impact of outside directors on post-M&A financial performance is positively recorded in developed market such as the USA (Dahya et al., Citation2019).

4.2.2. Empire building motive and acquirer’s size

Firms size of acquirers before mergers and acquisitions has a positive impact except for return on equity but statistically insignificant, as shown in Table . The study’s findings are not consistent with the empire-building motive of agency theory. The plausible arguments for this inconsistency are that large and small firms are controlled by major block shareholders in SAARC and ASEAN regions. Emerging markets are characterize by family ownership, state ownership and weak regulatory environment that consequently lessen the agency conflicts (Claessens & Yurtoglu, Citation2013). The mean block holding for sample firms is 58% and 62.45% in pre- and post-M&A period, respectively, as shown in Table which may lead minimizing traditional agency issues.

Table 8. Regression Analysis estimates for Acquirer’s Size and Post-M&A performance for 184 Mergers & Acquisitions deals in SAARC & AEASN

Firms size of acquirers does not matter in determining post-M&A performance in the context of the emerging market of SAARC and ASEAN regions, and the results are consistent with earlier studies (Humphery-Jenner & Powell, Citation2014; Kinateder et al., Citation2017).

4.2.3. Related versus unrelated mergers

Unrelated mergers have negative impact post-M&A performance, and it is statistically insignificant for all models of Table except for the results are statistically significant at 5% level for operating profit return on equity (EBOTROEpost) as shown in Table . It is evident from the results that acquirers who engage in unrelated mergers are unable to reap synergistic benefits from the acquisition in the post-M&A period. When the results are assessed jointly with univariate analysis results, it becomes obvious that firms that engage in related mergers perform better in the post-M&A period in comparison to firms involved in unrelated mergers.

Table 9. Regression Analysis estimates for Related & Unrelated Mergers and Post-M&A performance for 184 Mergers & Acquisitions deals in SAARC & AEASN

Notwithstanding, findings of the study support managerial risk aversion motive where managers of acquirers firms undertake mergers for diversifying their risk instead of post-M&A performance, yet in the presence of high block holding, such motives are less likely to be achieved.

Our results are consistent with the earlier studies (Doukas et al., Citation2001; Lin & Chou, Citation2016; Mantravadi, Citation2020a).

The impact of mergers type (related/unrelated) on post-M&A financial performance is not change by including corporate governance variables. The post-M&A financial performance (cash returns on asset & cash returns on equity) is positively influenced by board size while operating profit returns on equity and cash returns on assert is negatively affect by board independence. The study is also consistent with earlier research such as Mohapatra (Citation2017) examined Indian firms and concluded that firms with large board experience higher financial performance. In similar study, Abdullah et al. (Citation2022) concluded that board size has positive and significant impact on firm performance in Malaysian market.

The plausible explanation for the negative impact is negligent of independent director in post-M&A period (Liu & Wang, Citation2013). The cost of large number of outside directors on board exceed the benefits (Kor, Citation2006) and proved free rider. While the impact of outside directors on post-M&A financial performance is positively recorded in developed market such as USA (Dahya et al., Citation2019).

4.2.4. Block holding and post-M&A performance

Acquirers with high block holding in the pre-M&A period experience high operating profit ROA and ROE as shown in Table . The impact is statistically significant at 1% in Model 1& 2 and 5% level in Model 3.

Table 10. Regression Analysis estimates for Block holding and Post-M&A performance for 184 Mergers & Acquisitions deals in SAARC & AEASN

Results reveal that large shareholders of acquirers are actively involved in monitoring the mergers and acquisitions process and also involved in disciplining managers that, consequently, lead to enhanced post-M&A performance.

Agency problems between majority and minority shareholders become apparent in mergers & acquisitions deals in which majority shareholders pay a high premium for the target firm to get the private benefit of control instead of enhanced financial performance. However, our results do not support this principal-principal conflict of majority and monitory shareholders.

Similar findings are found in earlier literature (Boateng et al., Citation2017; Brooks et al., Citation2018; Shleifer & Vishny, Citation1997), while opposite findings also exist in earlier finance scholarship (Chen & Young, Citation2010; Yaacob & Alias, Citation2018). The firms owned by family outer perform the firms without the family ownership (Tarigan et al., Citation2022). Malaysian acquirers firms with high Institutional ownership perform better in post-M&A period than acquirers firms influence by agency cost (Ibrahim et al., Citation2019). Consistent with the study, research also confirms that active institutional investors experience less value destruction in M&A deal as compare to acquirers without active institutional investor (Ishak et al., Citation2020). In a similar study from Philippines, it is confirmed that inside ownership is an obvious factor for higher post-M&A financial performance (Popairoj, Citation2019).

5. Robustness check

The first reason for the robustness check is to investigate the phenomena with different proxies for financial performance. The second reason is to examine the impact of block holding on financial performance in the form of quartile rather than a linear relationship.

The study used operating profit returns on asset (EBITROA), operating profit returns on Equity (EBITROE), cash flow returns on asset (OCFROA) and cash flow returns on equity (OCFROE) which is meant to calibrate operating performance and ignore firms with other incomes, interest expenses and taxes. Similarly, these proxies also ignore market-based measures of financial performance. Net profit margin accounts for other income, interest expenses and taxes, and Tobin’s Q is a market-based financial performance measure. Therefore, net profit margin and Tobin’s Q are used as alternative proxies for financial performance.

5.1. Net profit margin as a proxy for financial performance

Table shows those firms with large free cash flow and firms controlled by block holders in the pre-M&A period experienced a high-profit margin (PMpost), and the results are statistically significant at the 1% level as depicted in Model 1&4. Earlier results are generally maintained in the case of free cash flows and block holding.

Table 11. Regression Analysis estimates for Profit Margin for 184 Mergers & Acquisitions deals in SAARC & AEASN

However, firms’ size of acquirers positively affects profit margin in the post-M&A period, and the result is statistically significant at a 1% level as depicted in Model 2. The relationship turns from insignificant to significant with the proxy change for financial performance. The nearest plausible argument for the change in relationship is that large acquirer firms better manage taxation and financial cost than small firms after mergers and acquisitions.

Although the impact of mergers types (related/unrelated) is negative, as observed with earlier proxies, the results turn insignificant for the impact of related versus unrelated mergers on post-M&A performance when profit margin (PMpost) is used as a proxy of financial performance.

5.2. Tobin’s Q as measure as a proxy for financial performance

The market measure of financial performance (Tobin’s Q) is not affected by acquirer firms’ free cash flow, acquirers’ size, related & unrelated mergers and block holding, as shown in Table . It is evident from the results that financial markets do not maintain long term memory of events such as mergers and acquisitions.

Table 12. Regression Analysis estimates for Tobin’s Q for 184 Mergers & Acquisitions deals in SAARC & AEASN

5.3. Quartile of block holding

In the previous analysis, block holding (BHpre) is a continuous variable, and the relationship of block holding (BHpre) with post-M&A performance was assumed to be linear. Nevertheless, the effect of block holding (BHpre) on post-M&A performance may vary with the level of ownership concentration. We re-estimate the regression for four levels (quartile) of block holdings (BHpre).

Table shows that variation from the first quartile (base) to the second quartile has no statistically significant impact on post-M&A performance. However, the impact of block holding in 3rd and 4th quartile causes to increase the post-M&A performance and the results are statistically significant except for Model 4. Similarly, block holding in the 3rd and 4th quartile positively affected operating profit returns on asset (EBITROApost) and operating profit returns on equity (EBITROEpost), and results are statistically significant at the 1% level.

Table 13. Regression Analysis estimates for quartile of Block holding (BHpost) and Post-M&A performance for 184 Mergers & Acquisitions deals in SAARC & AEASN

Generally, previous results are maintained with additional insights that changes in the lower quarter do not affect post-M&A performance, which reveals that firms with higher block holding are better positioned to monitor M&A deals and post-M&A integration process, which consequently enhance post-M&A performance.

6. Sub sample (SAARC & ASEAN) analysis of pre- and post-M&A financial performance

Univariate analysis of sub sample (SAARC & ASEAN) is based on comparing the mean of variables for (−3,+3) years windows before and after M&A deals. Paired sample t test is used to obtained the mean difference as shown in Table . While summary of results of whoel sample is reported in the Table for comparison with sub sample results.

Table 14. Summary of results

Table 15. Mean Comparison of Sub-sample (SAARC & ASEAN)

Sub sample analysis reveals that financial performance decline after mergers and acquisitions (M&A) in both SAARC and ASEAN regions. The mean difference of operating profit returns on asset (ROA), operating profit returns on equity (ROE), operating cash flow returns (OCF-ROE) and net profit Margin (PM) is negative and statistically significant at 5% level in SAARC region while the mean difference of Tobin’s Q is positive and statistically significant at 5% level. Similar, results are obtained for ASEAN region and Table shows that operating profit returns on asset (ROA), operating profit returns on equity (ROE), operating cash flow returns on asset (OCF-ROA) and net profit Margin (PM) is negative and statistically significant at 5% level. The mean difference of Tobin’s Q is negative but the result is statistically insignificant. The study is unable to report any significant difference in the impact of M&A on post-M&A financial performance.

The mean difference of free cash flow is positive and statistically significant at 5% level in ASEAN region while the difference is insignificant in SAARC region. The Debt to equity ratio decrease in SAARC region while increase in ASEAN region in post-M&A period. Size of the acquirers increase as a result of M&A deals in both SAARC & ASEAN region as shown in Table . The M&A deals consequently diluted shareholding of block holders in SAARC region while insufficient consequences on block holding in ASEAN region.

7. Conclusions

Using data of 184 M&A deals from six emerging economies of SAARC and ASEAN regions, it is found that post-M&A performance declined for the sample firms. Based on univariate and multivariate analysis, we conclude that the free cash flow hypothesis of Jensen (Citation1986) is irrelevant in emerging markets of SAARC and ASEAN regions. It is contended that these emerging markets characterized by high block holding (ownership concentration) minimized the agency issues, and hence free cash flow helps reduce post-M&A financial distress. Free cash flow enhances the post-M&A performance of acquirers in the emerging markets instead of declining post-M&A performance as promulgated by the free cash flow hypothesis. Our results are consistent with the alternative hypothesis, which posited that the combination of strong shareholder rights and sufficient monitoring by institutional shareholders diminish any agency issues that arise from the presence of free cash flows (Cremers & Nair, Citation2005; Gompers et al., Citation2003; Gregory & Wang, Citation2013).

This study did not find any support for acquirers’ size effect on post-M&A performance in emerging markets of SAARC and ASEAN regions except for the positive and significant impact of large acquirers on profit margin. The study’s finding is contrary to prior research from developed countries which generally reported that large acquirers gain lesser returns than small acquirers due to empire building motives of the managers. Therefore, this study found no evidence of empire-building motive in the M&A deals of firms from emerging economies.

Mergers with matched firms create more synergy, resulting in higher post-M&A performance. Although unrelated mergers decline post-M&A performance yet, we are unable to support managerial risk aversion motives arising from agency conflict in the context of emerging economies such as India, Pakistan, Malaysia, Indonesia, Thailand and the Philippines. Univariate analysis suggested that industry relatedness creates higher returns in the post-M&A period than unrelated firms.

Acquirers with high ownership concentration experience high post-M&A financial performance, and the study’s findings provide no evidence to support principal-principal conflict amongst the majority and minority shareholders. The impact of block holding on post-M&A performance become more prominent in the upper quartile, which provides evidence that changes in block holding in non-controlling ranges do not make any difference. Finally, it is also concluded that block holding reduces agency issues and firms are closely monitored and controlled by majority shareholders.

Although, corporate governance variables such as board size, board independence, audit committee size and audit committee independence are control variables in the study. Board size has positive impact on post-M&A financial performance and the results are consistent with resource dependence theory in emerging markets of SAARC and ASEAN regions. The study reports that the board independence has negative impact on post-M&A financial performance. In emerging markets, independent directors are appointed on the board to comply with code or regulatory requirements instead of their vigilant role in monitoring the firms.

Overall, the findings of this study provide no evidence that mergers and acquisitions create synergy in the emerging markets of SAARC and ASEAN regions, as evident from the decline in accounting base measure of financial performance after M&A. At the same time, this study did not find any evidence of the managerial motive of “Too big to fail” because agency issues such as empire building, managerial risk aversion and principal-principal conflict are not found in the emerging markets of SAARC and ASEAN regions. The study provides interesting insights on free cash flow and post-M&A performance. It concludes that free cash flows are beneficial for acquirers in emerging markets of SAARC and ASEAN regions.

8. Practical implication

The findings of the study has practical implications for managers, shareholders and board members. The shareholders, both current and potential, need to focus on the free cash flow of acquirers because free cash flow has long term positive impact on post-M&A financial performance in emerging market of SAARC and ASEAN regions. In case of stock acquisition, the target shareholders need to approve mergers with firms experience higher free cash flow to become shareholders of profitable organization. Findings of study suggest that the board is required to proactively engage in related mergers and avoid unrelated mergers as evident from the results that unrelated mergers negatively affect post-M&A financial performance. Managers of acquirers with high free cash flow are suggested to engage in M&A instead of organic growth in the sample emerging markets of SAARC and ASEAN regions.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Majeed Ullah Khan

Majeed Ullah Khan Department of Management Sciences, COMSATS University Islamabad, Abbottabad Campus, Abbottabad 22060, Pakistan

Yasir Bin Tariq

Yasir Bin Tariq Department of Management Sciences, COMSATS University Islamabad, Abbottabad Campus, Abbottabad 22060, Pakistan

Notes

1. During 2019, there are 21 M&A deals worth 0.13 billion US$ in Pakistan, 483 deals worth 31.61 billion US$ in Malaysia, 208 deals worth 8.72 billion US$ in Indonesia, 165 deals worth 6.80 US$ in Philippines, 202 M&A deals with value 15.62 billion US$ in Thailand and 1684 M&A deals with value 75.53 billion US$ in India (https://imaa-institute.org).

References

- Abdullah, S. N., Aziz, A., & Azani, A. (2022). The effect of board independence, gender diversity and board size on firm performance in Malaysia. Journal of Social Economics Research, 9(4), 179–28.

- Aggarwal, P., & Garg, S. (2022). Impact of mergers and acquisitions on accounting-based performance of acquiring firms in India. Global Business Review, 23(1), 218–236.

- Agrawal, A., Jaffe, J. F., & Mandelker, G. N. (1992). The post‐merger performance of acquiring firms: A re‐examination of an anomaly. The Journal of Finance, 47(4), 1605–1621.

- Akben-Selcuk, E., & Altiok-Yilmaz, A. (2011). The impact of mergers and acquisitions on acquirer performance: Evidence from Turkey. Business and Economics Journal, 22, 1–8.

- Albuquerque, R., & Schroth, E. (2010). Quantifying private benefits of control from a structural model of block trades. Journal of Financial Economics, 96(1), 33–55.

- Alhenawi, Y., & Stilwell, M. (2017). Value creation and the probability of success in merger and acquisition transactions. Review of Quantitative Finance and Accounting, 49(4), 1041–1085.

- Amihud, Y., & Lev, B. (1981). Risk reduction as a managerial motive for conglomerate mergers. The Bell Journal of Economics, 605–617.

- Bhaskar, A. U., Bhal, K. T., & Mishra, B. (2012). Strategic HR integration and proactive communication during M&A: A study of Indian bank mergers. Global Business Review, 13(3), 407–419.

- Boateng, A., Bi, X., & Brahma, S. (2017). The impact of firm ownership, board monitoring on operating performance of Chinese mergers and acquisitions. Review of Quantitative Finance and Accounting, 49(4), 925–948.

- Boateng, A., Naraidoo, R., & Uddin, M. (2011). An analysis of the inward cross‐border mergers and acquisitions in the UK: A macroeconomic perspective. Journal of International Financial Management & Accounting, 22(2), 91–113.

- Brockman, P., Rui, O. M., & Zou, H. (2013). Institutions and the performance of politically connected M&As. Journal of International Business Studies, 44(8), 833–852.

- Brooks, C., Chen, Z., & Zeng, Y. (2018). Institutional cross-ownership and corporate strategy: The case of mergers and acquisitions. Journal of Corporate Finance, 48, 187–216.

- Cabanda, E., & Pajara-Pascual, M. (2007). Merger in the Philippines: Evidence in the corporate performance of William, Gothong, and Aboitiz (WG&A) shipping companies. Journal of Business Case Studies (JBCS), 3(4), 87–100.

- Chatterjee, S., & Lubatkin, M. (1990). Corporate mergers, stockholder diversification, and changes in systematic risk. Strategic Management Journal, 11(4), 255–268. https://doi.org/10.1002/smj.4250110402

- Chen, S., Sun, Z., Tang, S., & Wu, D. (2011). Government intervention and investment efficiency: Evidence from China. Journal of Corporate Finance, 17(2), 259–271.

- Chen, Y. Y., & Young, M. N. (2010). Cross-border mergers and acquisitions by Chinese listed companies: A principal–principal perspective. Asia Pacific Journal of Management, 27(3), 523–539.

- Claessens, S., & Yurtoglu, B. B. (2013). Corporate governance in emerging markets: A survey. Emerging Markets Review, 15, 1–33.

- Cremers, K. M., & Nair, V. B. (2005). Governance mechanisms and equity prices. The Journal of Finance, 60(6), 2859–2894. https://doi.org/10.1111/j.1540-6261.2005.00819.x

- Cui, H., & Leung, S. C. M. (2020). The long-run performance of acquiring firms in mergers and acquisitions: Does managerial ability matter? Journal of Contemporary Accounting & Economics, 16, 1. https://doi.org/10.1016/j.jcae.2020.100185

- Dahya, J., Golubov, A., Petmezas, D., & Travlos, N. G. (2019). Governance mandates, outside directors, and acquirer performance. Journal of Corporate Finance, 59, 218–238. https://doi.org/10.1016/j.jcorpfin.2016.11.005

- Demsetz, H. (1983). The structure of ownership and the theory of the firm. The Journal of Law and Economics, 26(2), 375–390.

- Denis, D. J., & Sibilkov, V. (2010). Financial constraints, investment, and the value of cash holdings. The Review of Financial Studies, 23(1), 247–269. https://doi.org/10.1093/rfs/hhp031

- Dogru, T. (2017). Under-vs over-investment: Hotel firms’ value around acquisitions. International Journal of Contemporary Hospitality Management, 29(8), 2050–2069.

- Dogru, T., Kizildag, M., Ozdemir, O., & Erdogan, A. (2020). Acquisitions and shareholders’ returns in restaurant firms: The effects of free cash flow, growth opportunities, and franchising. International Journal of Hospitality Management, 84, 102327. https://doi.org/10.1016/j.ijhm.2019.102327

- Doukas, J. (1995). Overinvestment, Tobin’s q and gains from foreign acquisitions. Journal of Banking & Finance, 19(7), 1285–1303.

- Doukas, J. A., Travlos, N. G., & Holmen, M. (2001). Corporate diversification and firm performance: Evidence from Swedish acquisitions

- Dyck, A., & Zingales, L. (2004). Control premiums and the effectiveness of corporate governance systems. Journal of Applied Corporate Finance, 16(2‐3), 51–72.

- Ferrer, R. C. (2012). An Empirical Investigation of the Impact of Merger and Acquisition on the Firm’s Activity Ratios. Journal of International Management Studies, 12(2), 68–73. https://web.p.ebscohost.com/76384964

- Fu, F., Guay, W. R., & Zhang, W. (2016). Costly Corporate Governance: Evidence from Shareholder Approval in Mergers and Acquisitions. Finance Down Under 2018 Building on the Best from the Cellars of Finance Paper. http://cc.iift.ac.in/research/docs/extract/204.pdf

- Gao, L., & Kling, G. (2008). Corporate governance and tunneling: Empirical evidence from China. Pacific-Basin Finance Journal, 16(5), 591–605. https://doi.org/10.1016/j.pacfin.2007.09.001

- Ghosh, A. (2001). Does operating performance really improve following corporate acquisitions? Journal of Corporate Finance, 7(2), 151–178. https://doi.org/10.1016/S0929-1199(01)00018-9

- Gompers, P., Ishii, J., & Metrick, A. (2003). Corporate governance and equity prices. The Quarterly Journal of Economics, 118(1), 107–156.

- Gregory, A. (2005). The long run abnormal performance of UK acquirers and the free cash flow hypothesis. Journal of Business Finance & Accounting, 32(5‐6), 777–814.

- Gregory, A., & Wang, Y. H. (2013). Cash acquirers: Can free cash flow, debt and institutional ownership explain long‐run performance? Review of Behavioural Finance, 5(1), 35–57. https://doi.org/10.1108/RBF-02-2013-0010

- Gupta, I., Raman, T. V., & Tripathy, N. (2021a). Creating Value Through Related and Unrelated Merger and Acquisition: Empirical Evidence. Corporate Ownership and Control, 18(4), 67–76. https://doi.org/10.22495/cocv18i4art5

- Gupta, I., Raman, T. V., & Tripathy, N. (2021b). Impact of Merger and Acquisition on Financial Performance: Evidence from Construction and Real Estate Industry of India. FIIB Business Review, https://doi.org/10.1177/23197145211053400

- Harford, J., Humphery-Jenner, M., & Powell, R. (2012). The sources of value destruction in acquisitions by entrenched managers. Journal of Financial Economics, 106(2), 247–261.

- Hauser, R. (2018). Busy directors and firm performance: Evidence from mergers. Journal of Financial Economics, 128(1), 16–37. https://doi.org/10.1016/j.jfineco.2018.01.009

- Healy, P. M., Palepu, K. G., & Ruback, R. S. (1992). Does corporate performance improve after mergers? Journal of Financial Economics, 31(2), 135–175.

- Heron, R., & Lie, E. (2002). Operating performance and the method of payment in Takeovers. Journal of Financial and Quantitative Analysis, 37(1), 137–155.

- Holderness, C. G. (2003). A survey of blockholders and corporate control. Economic Policy Review, 9(1), 1–14. http://dx.doi.org/10.2139/ssrn.281952

- Humphery-Jenner, M., & Powell, R. (2014). Firm size, sovereign governance, and value creation: Evidence from the acquirer size effect. Journal of Corporate Finance, 26, 57–77. https://doi.org/10.1016/j.jcorpfin.2014.02.009

- Ibrahim, Y., Minai, M. S., Hasan, M. M., & Raji, J. O. (2019). Agency costs and post cross border acquisition performance of Malaysian acquirers. International Journal of Business and Society, 20(3), 870–887.

- Ishak, N., Taufil Mohd, K. N., & Shahar, H. K. (2020). Does investors react in long-term? The case of Malaysian acquisition. Cogent Business & Management, 7, 1. https://doi.org/10.1080/23311975.2020.1857593

- Ismail, T. H., Abdou, A. A., & Annis, R. M. (2011). Exploring Improvements of Post-Merger Corporate Performance: The Case of Egypt. IUP Journal of Business Strategy, 8(1), 7–24. https://www.academia.edu/1893816

- Jackling, B., & Johl, S. (2009). Board structure and firm performance: Evidence from India’s top companies. Corporate Governance: An International Review, 17(4), 492–509.

- Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review, 76(2), 323–329. http://www.jstor.org/stable/1818789

- Kalra, R. (2013). Mergers and acquisitions: An empirical study on the post-merger performance of selected corporate firms in India. IUP Journal of Business Strategy, 10(4), 7–67. https://ssrn.com/abstract=2466887

- Kalra, N., Gupta, S., & Bagga, R. (2013). A wave of mergers and acquisitions: Are Indian banks going up a blind alley? Global Business Review, 14(2), 263–282.

- Kar, R. N., Bhasin, N., & Soni, A. (2021). Role of mergers and acquisitions on corporate performance: Emerging perspectives from Indian IT sector. Transnational Corporations Review, 13(3), 307–320.

- Kinateder, H., Fabich, M., & Wagner, N. (2017). Domestic mergers and acquisitions in BRICS countries: Acquirers and targets. Emerging Markets Review, 32, 190–199.

- Kor, Y. Y. (2006). Direct and interaction effects of top management team and board compositions on R&D investment strategy. Strategic Management Journal, 27(11), 1081–1099. https://doi.org/10.1002/smj.554

- Kruse, T. A., Park, H. Y., Park, K., & Suzuki, K. (2002). Post-Merger Corporate Performance in Japan. 302341. http://dx.doi.org/10.2139/ssrn.302341

- Kumar, R. (2009). Post-merger corporate performance: An Indian perspective. Management Research News, 32(2), 145–157.

- Ladha, R. S. (2017). Merger of public sector banks in India under the rule of reason. Journal of Emerging Market Finance, 16(3), 259–273.

- Lang, L. H., Stulz, R., & Walkling, R. A. (1991). A test of the free cash flow hypothesis: The case of bidder returns. Journal of Financial Economics, 29(2), 315–335.

- Lau, B., Proimos, A., & Wright, S. (2008). Accounting measures of operating performance outcomes for Australian mergers. Journal of Applied Accounting Research, 9(3), 168–180.

- Lin, H. C., & Chou, Y. Y. (2016). The impact of industry commonality on post-merger performance. Advances in Economics and Business, 4(6), 297–305.

- Linn, S. C., & Switzer, J. A. (2001). Are cash acquisitions associated with better post combination operating performance than stock acquisitions? Journal of Banking & Finance, 25(6), 1113–1138.

- Liu, Y., & Wang, Y. (2013). Performance of mergers and acquisitions under corporate governance perspective. Open Journal of Social Sciences, 1(6), 17–25.

- Mantravadi, M. P. (2020a). Does merger type or industry affect operating performance of acquiring firms? A long-term merger performance study in India. Theoretical Economics Letters, 10(3), 696–717. https://doi.org/10.4236/tel.2020.103043

- Mantravadi, M. P. (2020b). Does Time-Period of Occurrence, or Firm-Relatedness, Impact Operating Performance of Acquiring Firms Differently? Evidence from Mergers in the New Millennium in Indian Industry. Open Journal of Business and Management, 9(1), 74–90. https://doi.org/10.4236/ojbm.2021.91004

- Mantravadi, P., & Reddy, A. V. (2007). Relative size in mergers and operating performance: Indian experience. Economic and Political Weekly, 42(39), 3936–3942. http://www.jstor.org/stable/40276470

- Masulis, R. W., Wang, C., & Xie, F. (2007). Corporate governance and acquirer returns. The Journal of Finance, 62(4), 1851–1889.

- May, D. O. (1995). Do managerial motives influence firm risk reduction strategies? The Journal of Finance, 50(4), 1291–1308. https://doi.org/10.1111/j.1540-6261.1995.tb04059.x

- Mehrotra, A., & Sahay, A. (2018). Systematic review on financial performance of mergers and acquisitions in India. Vision, 22(2), 211–221. https://doi.org/10.1177/0972262918766137

- Moeller, S. B., Schlingemann, F. P., & Stulz, R. M. (2004). Firm size and the gains from acquisitions. Journal of Financial Economics, 73(2), 201–228. https://doi.org/10.1016/j.jfineco.2003.07.002

- Mohapatra, P. (2017). Board Size and Firm Performance in India. International Journal of Management Practice, 9(3), 317–332. https://doi.org/10.1504/IJMP.2016.077834

- Morck, R., Shleifer, A., & Vishny, R. W. (1990). Do managerial objectives drive bad acquisitions? The Journal of Finance, 45(1), 31–48. https://doi.org/10.1111/j.1540-6261.1990.tb05079.x

- Nguyen, H. T., Yung, K., & Sun, Q. (2012). Motives for mergers and acquisitions: Ex‐post market evidence from the US. Journal of Business Finance & Accounting, 39(9‐10), 1357–1375. https://doi.org/10.1111/jbfa.12000

- Offenberg, D. (2009). Firm size and the effectiveness of the market for corporate control. Journal of Corporate Finance, 15(1), 66–79. https://doi.org/10.1016/j.jcorpfin.2008.09.006

- Officer, M. S. (2011). Overinvestment, corporate governance, and dividend initiations. Journal of Corporate Finance, 17(3), 710–724. https://doi.org/10.1016/j.jcorpfin.2010.06.004

- Oler, D. K. (2008). Does acquirer cash level predict post-acquisition returns? Review of Accounting Studies, 13(4), 479–511.

- Popairoj, J. (2019). Mergers and Acquisitions and Success Factors in Thailand. ASEAN Journal of Management & Innovation,6, (2), 41–57.

- Popli, M., Ladkani, R. M., & Gaur, A. S. (2017). Business group affiliation and post-acquisition performance: An extended resource-based view. Journal of Business Research, 81, 21–30. https://doi.org/10.1016/j.jbusres.2017.08.003

- Powell, R. G., & Stark, A. W. (2005). Does operating performance increase post-takeover for UK takeovers? A comparison of performance measures and benchmarks. Journal of Corporate Finance, 11(1), 293–317.

- Rahman, R. A., & Limmack, R. J. (2004). Corporate acquisitions and the operating performance of Malaysian companies. Journal of Business Finance & Accounting, 31(3‐4), 359–400. https://doi.org/10.1111/j.0306-686X.2004.00543.x

- Ramaswamy, K. P., & Waegelein, J. F. (2003). Firm financial performance following mergers. Review of Quantitative Finance and Accounting, 20(2), 115–126.

- Ravenscraft, D. J., & Scherer, F. M. (1987). Life after takeover. The Journal of Industrial Economics, 36(2), 147–156.

- Schmidt, D. R., & Fowler, K. L. (1990). Post‐acquisition financial performance and executive compensation. Strategic Management Journal, 11(7), 559–569.

- Schoenberg, R. (2006). Measuring the performance of corporate acquisitions: An empirical comparison of alternative metrics. British Journal of Management, 17(4), 361–370.

- Servaes, H. (1991). Tobin’s Q and the Gains from Takeovers. The Journal of Finance, 46(1), 409–419. https://doi.org/10.1111/j.1540-6261.1991.tb03758.x

- Sharma, D. S., & Ho, J. (2002). The impact of acquisitions on operating performance: Some Australian evidence. Journal of Business Finance & Accounting, 29(1‐2), 155–200.

- Shim, J. (2011). Mergers & acquisitions, diversification and performance in the US property-liability insurance industry. Journal of Financial Services Research, 39(3), 119–144. https://doi.org/10.1007/s10693-010-0094-3

- Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance. The Journal of Finance, 52(2), 737–783.

- Sun, J., Yuan, R., Cao, F., & Wang, B. (2017). Principal–principal agency problems and stock price crash risk: Evidence from the split‐share structure reform in China. Corporate Governance: An International Review, 25(3), 186–199.

- Switzer, J. A. (1996). Evidence on real gains in corporate acquisitions. Journal of Economics and Business, 48(5), 443–460. https://doi.org/10.1016/S0148-6195(96)00033-1

- Syukur, M., & Bungkilo, D. A. (2020). The aftermaths of acquisition in Indonesia. International Journal of Monetary Economics and Finance, 13(1), 16–33.

- Tarigan, J., Claresta, A., & Hatane, S. E. (2018). Analysis of merger & acquisition motives in Indonesian listed companies through financial performance perspective. Kinerja, 22(1), 95–112. http://repository.petra.ac.id/18002/

- Tarigan, J., Evania, J., Devie, D., & Hatane, S. E. (2022). The long-term performance of post-merger and acquisition: Evidence from Indonesia’s stock market. Afro-Asian Journal of Finance and Accounting, 12(3), 399–412.

- Teddlie, C., & Yu, F. (2007). Mixed methods sampling: A typology with examples. Journal of Mixed Methods Research, 1(1), 77–100.

- Wu, C. H., & Chiang, H. E. (2019). Impact of Diversified Mergers and Acquisitions on Corporate Risk. Journal of Economics, 15(1), 93–115.

- Yaacob, M. H., & Alias, N. (2018). Ownership Structure, Types of M&A and Long-Term Performance. Jurnal Pengurusan (UKM Journal of Management), 52, 235–244. https://doi.org/10.17576/PENGURUSAN-2018-52-19

- Yaghoubi, R., Yaghoubi, M., Locke, S., & Gibb, J. (2016). Mergers and acquisitions: A review (part 2). Studies in Economics and Finance, 33(3), 437–464.

- Yang, L., & Zhang, J. (2015). Political connections, government intervention and acquirer performance in cross‐border mergers and acquisitions: An empirical analysis based on Chinese acquirers. The World Economy, 38(10), 1505–1525. https://doi.org/10.1111/twec.12190

- Yeh, T. M., & Hoshino, Y. (2002). Productivity and operating performance of Japanese merging firms: Keiretsu-related and independent mergers. Japan and the World Economy, 14(3), 347–366.

- Young, C. S., Tsai, L. C., & Hsu, H. W. (2008). The effect of controlling shareholders’ excess board seats control on financial restatements: Evidence from Taiwan. Review of Quantitative Finance and Accounting, 30(3), 297–314.

- Zhang, Z., Lyles, M. A., & Wu, C. (2020). The stock market performance of exploration-oriented and exploitation-oriented cross-border mergers and acquisitions: Evidence from emerging market enterprises. International Business Review, 29(4), 2–15.

- Zhao, X., Ma, H., & Hao, T. (2019). Acquirer size, political connections and mergers and acquisitions performance. Studies in Economics and Finance, 36(2), 311–332.

- Zhou, B., Dutta, S., & Zhu, P. (2020). CEO tenure and mergers and acquisitions. Finance Research Letters 34, 101277.

- Zuhri, S., Fahlevi, M., Abdi, M. N., Irma, D., & Maemunah, S. (2020). The impact of merger and acquisition on financial performance in Indonesia. Journal of Research in Business, Economics, and Education, 2(1), 326–338.