?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to scrutinize the impact of the independent variables, i.e., budget participation and leadership style, on managerial performance mediated by organizational commitment. For this reason, the quantitative research approach was utilized to examine the hypotheses, and such an approach is considered appropriate for this study. This study adopted to cover the field side by using the questionnaires; thus, the total population was 42 people with a saturated sample, which means that all population members were involved as research samples, and the analysis of the data employed statistical tests and the coefficient of determination and path analysis. In brief, the findings revealed that budget participation had a positive but not significant effect on managerial performance at the Public Works and Public Housing Office of Wonogiri Regency, and Tax Service Office, Wonogiri Regency, Indonesia. Thus, the variable of leadership style had a positive and significant effect on managerial performance. Besides, the organizational commitment had a positive but not significant effect on managerial performance. Furthermore, organizational commitment did not mediate the significance of the effect of budgetary participation and leadership style on managerial performance. In addition, leadership style is the dominant factor influencing managerial performance and is explained by budget participation and leadership style with intervening organizational commitment.

1. Introduction

The success or failure of an organization can be seen from the exposure of the resulting performance. This performance is a form or embodiment of the vision and mission of the organization concerned. Gibson discusses in (Gibson et al., Citation2012) conveys that performance is a highly desirable result of organizational behavior. Hasibuan and Malayu (Citation2015) also states that performance is the end outcome of a worker completing duties based on expertise, sincerity, and experience. Meanwhile, social responsibility in the organization lies with the manager. For the accomplishment of the organization’s goals and objectives with success, it can be realized if the manager performs all the duties and obligations properly. Based on contingency theory, assumes that leadership exerts its influence depending on the situation to produce managerial performance. In this study, the contingency theory is related to the results of uncertainty from various previous studies, which showed the impact of uncertainty on managerial performance through organizational commitment.

The evidence is that the Department of Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency for the implementation of good governance could not be separated from the role played by the apparatus as state servants and public servants. The reason to choose and focus Department of Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency is because the researchers observed revealed that managerial performance within the Department of Public Works and Public Housing Office and Tax Service Office in the areas of Wonogiri Regency has not been maximized. One of the causes was the lack of communication between the Operator Officer and the Government Office regarding the budget. Supposedly, every government must practice excellent governance to fulfill the expectations of the populace and accomplish the state and nation’s objectives and ideals. Yet, the phenomena in the Department of Public Works and Public Housing Office and Tax Service Office in Wonogiri Regency were the infrequent evaluation of operating officers and the limited resources and sources of funds they have. Thus, the annual performance assessment, in its implementation, has not been in accordance with the regulations of Regulation of the Head of the State Civil Service Agency No. 01 of 2013 and Government Regulation No. 46 of 2011. In addition, the employee work targets, and work performance assessment were not based on the results of existing reports. Thus, Concerning managerial performance, there is a critical requirement for a management control system that guarantees the effective and efficient execution of corporate goals. In this case, the Wonogiri Regency Office is one of the government institutions for public services, and it is very important to control its management. The importance of evaluating performance as a reference for empowerment is useful for assessing how far an institution is supported by the strength of existing resources. According to Ermawati (Citation2017), managerial performance is nothing but the work of public service organizations in carrying out their activities in serving the community, and good managerial performance can be seen as an indicator of how managers carry out management functions. Individual employees’ performance in managerial tasks such as staffing, planning, investigating, coordinating, and negotiating are also referred to as managerial performance.

Furthermore, one of the elements that might impact managerial performance is participation in budgeting. In the Wonogiri Regency, participation in budgeting requires subordinate involvement in assisting superiors during the process of budgeting to achieve budget targets. Here, the contribution of lower-level managers in supporting level managers is carried out through coordination between management, to create a budget according to managerial needs. It indicates that there is communication between top managers and subordinate managers, which in turn improves organizational performance. Therefore, lower-level managers will find it easier to carry out targeted activities, so they can contribute optimally. In this regard, a budget is a management tool for allocating limited resources and sources of funds owned by the organization in achieving goals. Budget is also financial planning tool for managers (it is a managerial tool in the form of finance; Syahputra, Citation2014). The definition of budgeting participation is a form of approach in budgeting with the participation of subordinate managers. Participation will enable managers to contribute to budget development and encourage creativity. Again, Indarto and Ayu (Citation2011) state that participation in the budgeting process shows respect or concern for subordinates for work and company responsibilities. Budget participation is also defined by WiseGEEK (Citation2012) as “A type of financial planning strategy that involves the active involvement of a broader range of employees in the process of creating a viable budget for a department or even the entire organization. So participation plays a very important role in Management efficiency. Budget participation has also become the most comprehensive study in the investigation of behavior in management accounting.

Likewise, Indarto and Ayu (Citation2011) state that an increase in managerial performance can be demonstrated through accuracy in budgeting. Thus, budget participation has an important role in the delivery of public services, and participation is the involvement of subordinates and superiors in coordinating activities in the preparation process within the framework of realizing better performance, according to the set targets. Through participation in budgeting, it is easier for superior managers to communicate the activities carried out by subordinates in achieving the targets that have been agreed upon in the budget preparation. Budgetary participation is also a form of a general approach to enhance performance to increase the effectiveness of organizational activities. Brownell (Citation1982 in Lina and Stella, Citation2013), and Sari and Abdullah (Citation2017) define participation as a process of evaluating the performance of individuals and setting rewards based on the budget targets achieved and the involvement and influence of individuals on budgeting.

Nevertheless, various empirical evidence shows the resulting discrepancy in the influence of budgetary participation on managerial performance. Research related to the influence of budget participation on managerial performance with significant positive results was conducted by Indarto and Ayu (Citation2011), Putri and Adiguna (Citation2014), Abata (Citation2014), and Moheri and Arifah (Citation2015); Tarigan and Devie (Citation2015); Manica and Hanny (Citation2016); Ermawati (Citation2017); Sari and Abdullah (Citation2017). Meanwhile, Syahputra (Citation2014); Yulianingsih (Citation2017); Andison (Citation2017) concluded that budgetary participation had no impact on managerial performance. Then, studies by Suharman, Citation2012) and Noor and Othman (Citation2012) revealed a negative correlation between budget participation and managerial performance. The existence of a research gap in previous studies related to the influence of budgetary participation on managerial performance indicates uncertainty, and a variable that may affect managerial performance other than budgetary participation is leadership style.

In this case, budgets can be effective if managers have good predictive abilities, with considerations such as participation factors and appropriate leadership styles. Leadership style is a form of leadership in organizational management. Success in managing an organization cannot be separated from the leadership factor and the subordinates’ attitude in executing the tasks to accomplish organizational goals. Therefore, effective leadership should direct efforts in accomplishing organizational goals (Putri & Adiguna, Citation2014). Leadership style is also a manager’s behavior in managing and interacting. Alternatively stated, good or bad organizational performance is affected by leadership style. Moreover, the contingency approach emphasizes the possibility of other variables as moderating or mediating (Brownell, Citation1982; Jannah & Rahayu, Citation2015). Thus, this study used the organizational commitment variable as a mediator. As such, employee commitment to the organization’s beliefs and objectives is known as organizational commitment. Here, a positive view for the sake of the organization is shown by managers who have high commitment. Conversely, employees who are poorly committed will reduce their performance if they are involved in budgeting. As a mediator in the process of budgeting participation, organizational commitment is assumed that a leader will be able to achieve the set budget goals if there is an encouragement of employee engagement in doing the best for the organization above personal interests. Therefore, organizational commitment has a very important influence on work to create conducive working conditions so that the organization can run effectively and efficiently. Commitment is also described as a willingness to work hard and with all efforts directed at improving the organization. Research by Jannah and Rahayu (Citation2015) has shown that commitment significantly and positively impacted managerial performance.

Based on the description above, the author takes the title “The Impact of Budget Participations and Leadership Style on Managerial Performance by Organizational Commitment as Intervening Variable” (A Study at Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency, Indonesia).”

2. Literature review and hypotheses development

Managers have a social responsibility in achieving organizational goals. Managers in carrying out their duties well will then encourage the achievement of the goals and objectives set. According to Gibson et al. (Citation2012, p. 70) describes performance as a behavior’s result, or elucidates that performance is a person’s capability to achieve good results or stand out towards the achievement of an organizational goal. Hasibuan and Malayu (Citation2015, p. 105) also suggests that performance is the outcome a person achieves in completing the duties given to him based on his abilities, sincerity, and experience. Departing from the description above, it can be interpreted that the definition of performance is the work of individual or group behavior according to the respective authorities and responsibilities both in quality and quantity.

Meanwhile, managerial performance is a manager’s achievement to accomplish the goals of the organization. Moreover, managerial performance refers to organizational success based on an organization’s vision and goal. In other words, management performance is the result of working in accordance with the rules and norms set out by the company. Thus, managerial performance is the achievement of managers or employees in work to attain the organization’s vision, mission, and goals. In addition, as Giri and Wiguna (Citation2014) stated, managerial performance can be seen through indicators of how managers perform management functions.

From the preliminary description above, there is a research gap that comes from research by Indarto and Ayu (Citation2011), Putri and Adiguna (Citation2014), Abata (Citation2014), and Moheri and Arifah (Citation2015); Tarigan and Devie (Citation2015); Manica and Hanny (Citation2016); Ermawati (Citation2017); Sari and Abdullah (Citation2017), revealing a significant positive correlation between budget participation and managerial performance. Meanwhile, Syahputra (Citation2014); Jannah and Rahayu (Citation2015); Andison (Citation2017); Elwisa (Citation2017); Yulianingsih (Citation2017) uncovered that budgeting participation was not significant in managerial performance. Moreover, Suharman, Citation2012) and Noor and Othman (Citation2012) showed a negative relationship. These empirical results are inconsistent. Therefore, further research is needed in the hope of confirming the correlation between budget participation and managerial performance.

Furthermore, before, Melek Eker’s (Citation2009) research entitled “The Impact of Budget Participation on Managerial Performance via Organizational Commitment: A Study on the Top 500 Firms in Turkey” has been published in the journal Ankara Üniversitesi SBF Dergisi pages 118–136. Then, this current research is a development of Eker’s (Citation2009) research. Eker (Citation2009) used budgetary participation as an independent variable with organizational commitment as an intervening variable and managerial performance as the dependent variable. Therefore, this research was developed by including the leadership variable as an independent variable. The difference is that in Eker’s (Citation2009) research, the research location was in Turkey with the object of research being 500 companies in Turkey, while this research was conducted at the Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency, Indonesia. Further, the researchers formulated five hypotheses prepared based on existing theories and the results of previous research. According to Sugiyono (Citation2013, p. 51), the hypothesis shows a temporary answer. Therefore, empirical evidence is needed to test the research assumptions.

2.1. 1- The impact of budgetary participation on managerial performance

Budget is a component in management control that has planning and control functions so that activities run effectively and efficiently. Obviously, the budget is a plan of activity for the execution of a sequence of future activities. According to Siegel (in Indarto & Ayu, Citation2011), the budget had a direct impact on those involved in its preparation. During the budgeting process, participation is a form of respect for subordinates (Indarto & Ayu, Citation2011). According to Baiman (1982 in Indarto & Ayu, Citation2011), the involvement of subordinates will help superiors so that the budget can be arranged accurately. Indarto and Ayu (Citation2011) also stated that budget accuracy can result in better managerial performance. Research by Indarto and Ayu (Citation2011); Eker (Citation2009); Putri and Adiguna (Citation2014), Abata (Citation2014), Kholidah and Murtini (Citation2014), and Moheri and Arifah (Citation2015); Tarigan and Devie (Citation2015); Manica and Hanny (Citation2016); Ermawati (Citation2017); Sari and Abdullah (Citation2017), Sari and Abdullah (Citation2017), showed positive and significant results between budget participation and managerial performance. Based on the description above, the following hypothesis could be made:

H1: Budget participation has a significant positive impact on managerial performance at the Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency, Indonesia

2.2. 2- The impact of leadership style on managerial performance

Leadership is a process that results in individual tenacity, focus, and intensity in pursuit of a goal. According to Robbins & Judge, Citation2019, p. 208), to be able to provide intensity, the right direction, and perseverance to individuals, a leader must understand and master the organization’s vision and mission, be able to socialize and communicate and demonstrate behavior that is imitated by others. Syukri and Surasni, Ni & Furkan, Lalu (Citation2019) with research entitled “The Influence of Budget Participation and Leadership Style on Managerial Performance with Job Relevant Information as Moderator” demonstrated that leadership style was significant in managerial performance. Arfan et al’s (2017) research entitled “The Effect of Budgetary Participation, Leadership Style, and Organizational Commitment on the Managerial Performance at Universitas Muhammadiyah Aceh, Indonesia” also showed the results that budgetary participation, leadership style, and organizational commitment had a significant impact on managerial performance. In addition, studies by Sari and Abdullah (Citation2017); Elwisa (Citation2017); Syukri and Surasni, Ni & Furkan, Lalu (Citation2019) concluded that leadership style significantly affected managerial performance. The description allows for the following supposition to be made:

H2: Leadership style has a significant positive effect on managerial performance at the Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency, Indonesia.

2.3. 3- The impact of organizational commitment on managerial performance

Organizational commitment is the attachment, involvement, and bond of an employee to the organization. Andre and Hermanto (Citation2021) suggest that organizational commitment is a promise that is reflected in the actions or behavior carried out in the organization. This action fosters trust or confidence that drives all activities and participation within the group. The better a person’s commitment, the higher his performance. Syakieb et al.’s (Citation2018) research entitled “Effect of Participative Budgeting, Organizational Commitment, and Work Motivation on Managerial Performance (Survey of Motor Vehicle Dealers in Bandung)” concluded that organizational commitment significantly and positively impacted managerial performance. In line with the research of Syakieb et al. (Citation2018), the research found that organizational commitment significantly and positively influenced managerial performance. According to Brownell (Citation1982 in Gamayuni and Suryani, Citation2019), employees committed to the organization will be more driven to perform well and help the company reach its objectives. Studies by Jannah and Rahayu (Citation2015); Manica and Hanny (Citation2016); Sari and Abdullah (Citation2017), Giusti et al. (Citation2018), Syakieb et al. (Citation2018), and Gamayuni et al. (Citation2019) revealed that organizational commitment had a significant positive impact on managerial performance. From the above description, the following hypothesis could be made:

H3: Organizational commitment has a significant positive effect on managerial performance at the Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency, Indonesia.

2.4. 4- The impact of budget participation on managerial performance mediated by organizational commitment

Managerial performance is the result of the actions and behavior of a person or group within the organization (Giri & Wiguna, Citation2014). The budget is a management control system component that serves as a tool for planning and controlling organizational operations so that managers may do so more successfully and effectively. The subordinate managers’ budgeting participation is a form of contribution of subordinate managers (respect) to the work that is their responsibility and the organization (Indarto & Ayu, Citation2011). This attitude of respect is a form of commitment given by employees to the organization which is their involvement in the progress of the organization. Participation given by subordinates will help the results of budgeting more accurately in Indarto & Ayu, Citation2011). Furthermore, Indarto and Ayu (Citation2011) stated that budget accuracy can be expected in improving managerial performance. Indarto and Ayu (Citation2011), Giri and Wiguna (Citation2014), Kholidah and Murtini (Citation2014), Jannah and Rahayu (Citation2015), and Giusti et al. (Citation2018) showed that budget participation significantly and positively influenced managerial performance mediated by organizational commitment. From the description above, the hypothesis could be made below:

H4: Budget participation has a significant positive effect on managerial performance through the mediation of organizational commitment at the Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency, Indonesia.

2.5. 5- The impact of leadership style on managerial performance mediated by organizational commitment

In achieving good performance, employee commitment is needed in an organization. Organizational commitment is something essential, and it cannot be separated from the leadership of an organizational leader, because a leader will direct employees to work to accomplish the mission and vision of the organization. Organizational commitment is also the attachment, involvement, and bond of employees to the organization. In addition, it can create the maximum implementation of work tasks. High organizational commitment is expected so that employees can work professionally. Meanwhile, managerial performance is the manager’s achievement of organizational goals. According to Elwisa (Citation2017), managerial performance is an organization’s accomplishment of the organization’s vision and mission. The achievement of this vision and mission cannot be separated from the leadership in managing the organization. However, maximum performance will not be achieved without organizational commitment in the efforts of the organization’s vision and mission. Research by Fabio and Puspitawati (Citation2016);Elwisa (Citation2017) indicated that leadership significantly and positively affected managerial performance mediated by organizational commitment. From the description before, the below hypothesis could be made:

H5: Leadership style has a significant positive effect on managerial performance through the mediation of organizational commitment at the Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency, Indonesia.

2.6. Research model and research method

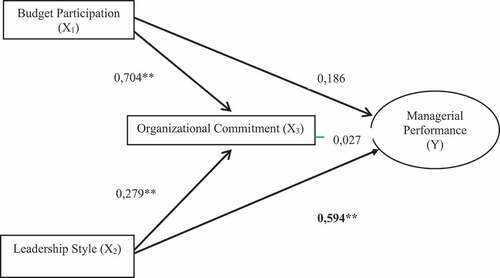

This study’s research model was based on several variables: budget participation and leadership style on managerial performance, with organizational commitment as an intervening variable. Therefore, the model of this research can be described as follows as shown in Figure :

Figure 1. Research model.

The object of this research was Wonogiri Regency in Indonesia, while the subjects in this study were employees, especially the Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency, Indonesia. This current study applied a quantitative exploratory approach, and hypothesis testing explains the connections between and among the variables. Then, a survey was used to obtain the information. The purpose of the study was to examine the correlations between independent and dependent variables. This type of research data was included in primary data. Primary data are those whose sources are attained directly from the field. According to Sugiyono (Citation2013, p. 129), primary data sources are those that provide data directly to the collectors of data. The data sources were respondents, namely employees of Wonogiri Regency who answered statements formulated by researchers regarding budget participation, leadership style, organizational commitment, and managerial performance. As stated by Sugiyono (Citation2013, p. 73), “the sample is part of the number and characteristics possessed by the population.” Sampling is based on research subjects. If it is less than 100, it is better to make all samples, so this research is called the total population (Arikunto, Citation2014, p. 120). The total population was 42 employees. The sample of this study was taken utilizing a census, where all population members were taken as samples. Thus, the number of samples was 42 people. Sugiyono (Citation2013, p. 135) also stated that the questionnaire is a way of getting data by providing a set of statements to get a response; hence, this research used a questionnaire method. Another expert asserted that a list of statements or questionnaires is several statements employed to get information from respondents in terms of reports about themselves or things they know (Arikunto, Citation2014, p. 229). this study used Path analysis because path analysis can be used to analyze models that are more complex (and realistic) than multiple regression. It can compare different models to determine which one best fits the data. Path analysis can disprove a model that postulates causal relations among variables. In addition, Path analysis assist the researchers measure which of the possible relationships matter the most, and which might turn out to be not important at all. Determining what variables to include in the model is job as a researcher. Since path analysis is also a kind of statistical analysis, it also comes with several assumptions. In path analysis, the association among the model should be linear in nature. The associations among the models should be additive in nature. In path analysis, the association among the model should be causal in nature. Therefore, The researchers used regression analysis in measuring the causality relationship between predetermined variables, which is intended to find out the impact of significance between the independent and the dependent variables together. And regression analysis is that it can be used to understand all kinds of patterns that occur in data. This study then used a Likert scale. The Likert scale is useful for measuring respondents’ attitudes, opinions, and perceptions of social phenomena. The answers to the instrument indicators were given the following scores (values): Strongly agree = 5, Agree = 4, Neutral = 3, Disagree = 2, and strongly disagree = 1.

3. Variable operational definition

Managerial Performance (Y2) The outcome of an efficient management activity process, which begins with the planning and budgeting process, administration, reporting, accountability, and supervision, is managerial performance. The degree of management performance is determined by measuring this variable using a questionnaire with an interval scale. This research questionnaire was adapted from Mahoney (Citation1963) & Syakieb et al. (Citation2018) Managerial performance measurement in this study is indicated by indicators of planning, investigation, coordination, evaluation, staffing, negotiation, supervision, then representation. Thus, Budget Participation (X1) Participation is the participation of the work unit manager in the process of budgeting, for instance, a subordinate manager’s participation program in determining targets and budgets and activities to be carried out. To determine this variable, an interval scale was employed and demonstrated the participation level of the apparatus in budgeting. Some indicators utilized from the research conducted by Hidrayadi (Citation2015) are: 1) Involvement of managers and employees in budget preparation, 2) Influence in budget formulation, 3) Influence in setting goals and budgeting, 4) Providing opportunities to subordinates in the budget, 5) Control over setting budget targets, and 6) Frequency of submission of suggestions and opinion. And Leadership Style (X2) Leadership style is the leaders’ ability to impact the actions of employees, in this study, the Public Housing and Settlement Areas of Wonogiri Regency. Leadership style also describes the behavior of leaders in the Public Housing and Settlement Areas of Wonogiri Regency in dealing with or interacting with situations. The indicators in this study modified the instrument developed by the Hersey & Blanchard Model as cited in Hakim et al. (Citation2021), including 1) Instruction Style, 2) Consultation Style, 3) Participation Style, and 4) Delegation Style. Organizational Commitment (X3/Y1) Organizational commitment is attachment, involvement, and bond to the organization and is experienced. The indicators used were the modifications of Hakim (Citation2015), namely: 1) Feelings of belonging, 2) Emotional attachment, 3) Feelings of meaning, 4) Being part of the organization, 5) Participating in the success of the organization’s goals, 6) Feeling the organization as a second home, and 7) Participating.

4. Results and discussion

This section contains a descriptive analysis that describes the classification of respondents from the data obtained from as many as 42 from distributing questionnaires to respondents. Based on the respondents’ characteristics, the following can be elucidated:

4.1. Classification of respondents by age

Based on the respondents’ age in this study, the distribution of grouping based on age is shown in the classification of respondents in Table in the appendix. It describes the number of employees who became respondents aged 20–39 years as many as 19 employees (45.23%), ages 40–49 years amounting to nine (21.42%), and ages over 50 years totaling 14 (33.35%). From the classification results, most respondents were over 20–30 years old.

4.2. Classification of respondents by gender

Based on gender, respondents can be grouped as shown in Table in the appendix, revealing that male respondents 19 (45.23%), and female respondents 23 (54.77%). From the classification results, most respondents were female.

4.3. Classification of respondents by marital status

The respondents based on marital status can be classified in Table in the appendix. It displays that respondents with married marital status were 27 (64.29%), and those with unmarried marital status were 15 (35.71%). This classification’s results indicate that the married respondents were more dominant.

4.4. Classification of respondents by the level of education

As presented in Table in the appendix, the classification based on the level of education uncovered that 11 or 26.20% of the employees became respondents with high school education. A total of five (11.90%) had a Diploma III education. A total of 17 (40.48%) had undergraduate education (S1). A total of nine (21.41%) had master’s degrees. This classification indicates that the most dominant were those with undergraduate education (S1) as many as 17 (40.48%).

4.5. Classification of respondents by years of service

The classification of respondents by years of service can be observed in Table in the appendix, showing that the Public Works and Public Housing Office and Tax Service Office employees in Wonogiri Regency who worked between 0–10 years were 17 people (40.48%). The number of employees who had worked 10–15 years was six (14.29%), for 15–20 years was five (11.90%), and over 20 years was 14 (33.33%). These results illustrate that the most dominant respondents were those who had worked 0–10 years

4.6. Instrument tests (validity and reliability)

The validity of six budget participation statements on the budget participation variable (X1) were all valid as in Table in the appendix.

The validity test results of the budget participation uncovered the highest values for statements 4, 2, and 3. It signifies that the forming indicators for the highest budget participation behavior were in the statements of items 4, 2, and 3. In addition, for the validity of the statement items for the leadership style variable (X2), all 35 leadership style statements were tested. The validity test of 35 leadership style statements was all valid, completely shown in Table in the appendix.

The validity test results of the leadership style revealed the highest values for statements 17, 6, and 7. It means that the indicators for forming leadership style behavior were the highest in items 17, 6, and 7. Likewise, the validity of the statement item variable for organizational commitment (X3) tested seven statements, where all were valid, completely presented in Table in the appendix.

Table 1. Correlation of organizational commitment statement items (X3)

The validity test results of organizational commitment showed the highest values of the 5th, 4th, and 3rd statements. It means that the forming indicators of the highest organizational commitment behavior were in the statements of items 5, 4, and 3. Thus, the validity of the statement items for the managerial performance variable (Y) tested the eight statements, which were all valid. Details are displayed in Table .

Table 2. Correlation of managerial performance statement items (Y)

The validity test results of the managerial performance uncovered the highest values for statements 7, 3, and 4. It means that the indicators for forming managerial performance behavior were the highest in the statements of items 7, 3, and 4.

Moreover, a way to assess a questionnaire’s reliability is to consider it as an indication of a variable or construct. In this study, each statement’s reliability was carried out utilizing Cronbach’s Alpha. Nunnally Han & Cao, (Citation2022) states that reliability testing can be done in one way one shot or measurement. A variable is said to be reliable if it has a Cronbach Alpha (α) > 0.60. If a variable’s Cronbach Alpha (α) value is greater than 0.60, it is deemed reliable. The reliability test results as in the attachment of the data processing are shown in Table . The reliability test results showed that the statement items for all variables may be deemed to be reliable since the Cronbach alpha count exceeds the necessary threshold or the crucial value (rule of thumb) of 0.60.

Table 3. Reliability Test Results

Table 4. Equation 1 path analysis results

5. Path equation results

Path analysis is an extended regression analysis in measuring the causality relationship between predetermined variables, which is intended to find out the impact of significance between the independent and the dependent variables together.

Equation I: Y = β1Y1+ β2Х1+ β3Х2 + еEquation I: X3= β4 Х1+ β5 Х2 + е

5.1. Results of path analysis for equation 1

Obtained the equation:

Y2 = 0.182 X1 + 0.541 X2 + 0.063 Y1 + є1Sig (0.378) (0.001)** (0.781)

Description:Y2 = Managerial performanceX1 = Budget participationX2 = Leadership styleY1 = Organizational commitmentЄ1 = Residual** = 5% significance level

The regression coefficient of the budget participation variable was 0.186. It signifies that if there is no leadership style and organizational commitment, managerial performance increases constant and with the addition of 0.186. Meanwhile, the regression coefficient of leadership style was −0.541. It denotes that if budget participation and organizational commitment do not exist, managerial performance increases constant and with the addition of 0.541. In addition, the regression coefficient of the organizational commitment variable was 0.063. It demonstrates that if there is no budgetary participation and leadership style, managerial performance increases constant and with the addition of 0.063.

5.2. Results of path analysis for equation 2

Obtained the equation:

Y1 = 0.703 X1 + 0.278 X2 + є2Sig (0.000)** (0.004)**Y2 = Managerial performanceX1 = Budget participationX2 = Leadership styleY1 = Organizational commitmentЄ1 = Residual** = 5% significance level

The budget participation variable’s regression coefficient was 0.703. It suggests that if there is no leadership style, organizational commitment will increase by a constant plus 0.703. On the other hand, the leadership style variable’s regression coefficient was 0.278. It indicates that if there is no budget participation, organizational commitment will increase by a constant plus 0.278.

6. Hypothesis test

6.1. T-test

The significance of the partial effect of the independent variables on the dependent was assessed using the t-test. The partial regression coefficient test is concluded through the p-value, i.e., if the significant value of the study shows ≤ 0.05, independent variables significantly affect the dependent variable partially. Besides, the data calculation was done by utilizing SPSS

6.2. Budget participation on managerial performance

The second equation regression results revealed that the budgetary participation variable’s t-count was 0.891, with a significant value of 0.378 > 0.05. In other words, the budget participation had a positive but not significant impact on managerial performance so hypothesis 1 was not supported.

6.3. Leadership style on managerial performance

The second equation regression results uncovered that the leadership style variable’s t-count was 3.781, with a significant value of 0.001 < 0.05, meaning that the leadership style variable positively and significantly impacted managerial performance so hypothesis 2 was supported.

6.4. Organizational commitment on managerial performance

The second equation regression results showed that the organizational commitment variable’s t-count was 0.280, with a significant value of 0.781 > 0.05. It signifies that the organizational commitment positively but insignificantly impacted managerial performance so hypothesis 3 was not supported.

6.5. Budget participation on organizational commitment

The second equation regression results displayed that the budget participation variable’s t-count was 7.668, with a significant value of 0.000 < 0.05. It denotes that budget participation significantly impacted organizational commitment.

6.6. Leadership style on organizational commitment

The second equation regression results showed that the leadership style variable’s t-count was 3.036, with a significant value of 0.004 < 0.05. It signifies that leadership style significantly impacted organizational commitment.

7. Sobel test

To ascertain the function as a mediator on the impact of the independent variable on the dependent variable, the Sobel test was used. The formula is as follows.

The significance test used the following formula: calculate = A mediating effect occurs when the value of the t-count exceeds that of the t.

7.1. Budget participation on managerial performance mediated by organizational commitment

Based on Tables , , the impact of budget participation on managerial performance mediated by organizational commitment was calculated as follows.

Table 5. Equation 2 path analysis results

Table 6. T-test coefficient

Table 7. T-test coefficient analysis

Sab = 0.169669

The magnitude of t-table of 42 data with df = 39 obtained t-table = 2.023.

t-count = 0.279969 < t-table (2.023)

It is concluded that budget participation had no mediation impact on management effectiveness. The fourth hypothesis, according to which organizational commitment mediated the positive impact of budgetary participation on management performance, was not confirmed.

7.2. Budgetary participation on managerial performance mediated by organizational commitment

Based on Tables , , the impact of budgetary participation on managerial performance mediated by organizational commitment was determined as follows.

Table 8. First equation F-test results

Sab = 0.013874

The magnitude of t-count is sought as follows:

Thus, t-count = 0.267909 < t-table (2.023)

It is concluded that there was no mediating effect of leadership style on managerial performance. The fifth hypothesis, stating that leadership style positively affected managerial performance mediated by organizational commitment, was not verified. (See Table )

Table 9. The second equation F-test results

Table 10. The results of the coefficient of determination of equation 1

Table 11. The results of the coefficient of determination of equation 2

7.3. F-test

7.4. First equation F-test results

The simultaneous test results (F-test) in the first equation revealed the value of F = 10.777, with a significance of 0.000 < 0.05. Thus, it can be concluded that jointly, the independent variables affected managerial performance.

7.5. Second equation F-test results

Since F-value = 49.885 with a significance value = 0.000 < 0.05, simultaneously, the independent variables of budget participation and leadership style affected organizational commitment.

7.6. Determination Test (R2)

7.7. Coefficient of determination equation 1

e12 = 1—R12= 1–0.460= 0.540e1 = 0.7348

7.8. Coefficient of determination equation 2

e22 = 1—R22 = 1–0.719= 0.281e2 = 0.5301

7.9. Total coefficient of determination

From equations 1 and 2, the value of the coefficient of total determination was obtained (R2 total) as follows:R2 total = 1- (e12 x e22)= 1—(0.540 x0.281)= 1–0.1517= 0.8483

Because R2 total = 0.8483, managerial performance could be explained by budget participation, leadership style, and organizational commitment by 84.83%. On the other hand, the residual value of 15.17% can be obtained from other variables outside the model, such as communication, discipline, and others.

8. Path analysis

Based on the outcomes of several tests, the following recapitulation may be made:

8.1. Direct effect

In this study, the direct effect is the impact of one independent variable on the dependent variable without other variables.

1) Budget participation on Managerial Performance

Tables present that budget participation positively but insignificantly impacted on performance. The path coefficient was 0.182, with a sig. of 0.352.

Table 12. Results of path analysis recapitulation

Table 13. Results of direct, indirect, and total effects

2) Leadership Style on Managerial Performance

Tables show that managerial performance was positively and significantly influenced by leadership style, with path coefficient = 0.541 and sig 0.000.

8.2. Indirect Influence

1) Budget Participation on Performance through Organizational Commitment

Table shows that organizational commitment could be significantly affected by budget participation. Managerial performance would be affected by organizational commitment although it was not significant, and the coefficient value was 0.019.

2) Leadership Style on Performance through Organizational Commitment

Table displays that leadership style significantly and positively impacted organizational commitment. In other words, the organizational commitment was positively significant in improving managerial performance, with a coefficient value of 0.008.

8.3. Total effect

1) Table shows that the total impact of budget participation on managerial performance through organizational commitment was 0.205.

2) Table indicates that the total impact of leadership style on managerial performance through organizational commitment was 0.602. (See Figure )

Figure 2. Path analysis results.

8.4. Summary of path analysis results

9. Discussion

9.1. Budget participation on managerial performance

The results revealed that the direct influence of the budget participation variable on performance was 0.182 but not significant because the significant value was 0.352 > α = 0.05. The insignificance of budget participation on managerial performance is possible because subordinate managers, who should work hard and find solutions if there are obstacles in achieving the budget that has been set together, do not conduct it. It denotes that in the budget preparation at the Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency, it was not too strict with the emphasis on managerial performance carried out by the budget makers. Budgeting was also only considered a routine that must be followed. Therefore, subordinate managers did not follow the success of the targets that have been set. In contrast to private organizations, wherein the preparation of the budget for private companies, it is necessary to emphasize a significant increase in performance

The findings of this study support the previous research results conducted by Syahputra (Citation2014); Yulianingsih (Citation2017); Andison (Citation2017), who concluded that budgetary participation did not impact managerial performance.

Yet, these results do not support the research conducted by Indarto and Ayu (Citation2011), Putri and Adiguna (Citation2014), Abata (Citation2014), and Moheri and Arifah (Citation2015); Tarigan and Devie (Citation2015); Manica and Hanny (Citation2016); Ermawati (Citation2017); Sari and Abdullah (Citation2017), which showed a positive influence. The current study also does not support the research of Suharman, Citation2012) and Noor and Othman (Citation2012), which uncovered a negative relationship between budget participation and managerial performance.

Based on the discussion above, the effect of budget participation in efforts to improve performance is not effective because it is not significant. Since it is not effective (not significant) to improve performance, efforts should be made to maintain the behavior of budget participation on managerial performance behavior. It can be done by paying attention to the validity test value of the budget participation indicator located in the 4th, 2nd, and 3rd statement items. It means that those statement items form the behavior of budget participation. The steps that can be taken are:

a. Leaders maintain ways of providing opportunities for subordinates to take part in the budget process.

b. The leadership maintains ways of providing opportunities to formulate budgets in the Public Housing and Settlement Areas and Housing Offices with subordinates.

c. Leaders maintain ways of providing opportunities for subordinates to participate in setting goals and setting budgets.

9.2. Leadership style on managerial performance in the public works and public housing office and tax service office, wonogiri

The findings uncovered that the influence of the leadership style variable on managerial performance was 0.541 and was significant. It signifies that if the leadership style is improved, the managerial performance at the Department of Public Housing and Settlement and Housing in Wonogiri Regency will increase significantly. This study’s findings support the previous research results conducted by Sari and Abdullah (Citation2017), Elwisa (Citation2017); concluding that leadership style had a significant positive impact on managerial performance.

Based on the above discussion, the effect is effective in improving managerial performance. Because it is effective (significant) to improve managerial performance, efforts should also be made to maintain leadership style on managerial performance behavior directly. It can be performed by paying attention to the validity test indicator value of the leadership style variable located in statement items 17, 6, and 7. It indicates that these statement items are from the behavior of the leadership style. The steps that can be taken are:

a. Managers tend to get out of hand in dealing with work problems; for example, the leader encourages subordinates to be responsible for a job that has been done.

b. The supervisor always plans clear and firm steps in carrying out work supervision, such as the leader has anticipatory steps in supervising the work of subordinates.

c. Superiors always monitor the actions of subordinates in completing work tasks, e.g., leaders always pay attention to the progress of the work of subordinates.

9.3. Organizational commitment on managerial performance

The results showed that the organizational commitment’s impact on performance was 0.063 but not significant. It can be observed from the results of the significance of 0.903 ≥ 0.05. The insignificant impact of organizational commitment on managerial performance is caused, among others, by most of the employees who think that commitment to the organization is an obligation in carrying out their duties and is considered to have a meaning to perform better. Based on the respondent’s age, the most dominant were young people, namely 20–39 years (45.23%) with a few years of service, i.e., 0–10 years, as many as 17 employees (45.23%). Therefore, the probability of being committed to the organization was also very low. In addition, employees considered commitment not very important. This study’s findings do not reinforce the previous research conducted by Jannah and Rahayu (Citation2015); Manica and Hanny (Citation2016); Sari and Abdullah (Citation2017), Giusti et al. (Citation2018), Hartini (2018), Syakieb et al. (Citation2018), Gamayuni et al. (Citation2019), denoting that organizational commitment significantly impacted managerial performance.

Based on the discussion above, the impact of organizational commitment in improving performance is not effective because it is not significant. Since it is not effective (not significant) to improve managerial performance, efforts should be made to maintain organizational commitment behavior toward managerial performance behavior. It can be done by paying attention to the value of the validity test indicator for the organizational commitment variable located in the 5th, 4th, and 3rd statement items. It means that these statement items form organizational commitment behavior. The steps that can be taken are:

a. The leadership maintains the participation and efforts of subordinates to make the agency’s program a success if there are obstacles in the implementation of the budget.

b. Leaders maintain a sense of meaning as employees by being involved in the budgeting process

c. The leadership maintains a sense of employee engagement in the success of the budget goals that have been set together.

9.4. Budgeting participation on managerial performance mediated by organizational commitment

This study’s results indicate that the regression coefficient of budgetary participation on organizational commitment was 0.278, with a significance value of 0.004 < 0.05, and the impact of organizational commitment on managerial performance was 0.063, with a significance value of 0.781 > 0.05. It demonstrates that budgeting participation positively and significantly impacted organizational commitment, and organizational commitment positively but insignificantly impacted managerial performance. Through organizational commitment, the indirect influence results of budgetary participation on managerial performance are shown by obtaining an indirect effect coefficient, which is the multiplication of the regression coefficient of budgetary participation on organizational commitment and the regression coefficient of organizational commitment on managerial performance. It was 0.018, smaller than the direct impact of the budget preparation participation on the managerial performance of 0.182. This result is known through the Sobel test, which shows t-count = 0.2799769 < t-table = 2.023. It denotes that the mediating role of organizational commitment in the significance of the influence of budgetary participation on managerial performance is known through the Sobel test. It signifies that organizational commitment was not effective as a mediator of the significance of budgetary participation’s influence on managerial performance.

Its ineffectiveness as a mediator is because organizational commitment is considered a mere obligation by employees in doing their tasks. The lack of a sense of attachment to the organization is one of the reasons that organizational commitment becomes a process that must be followed as an employee and does not foster enthusiasm in achieving organizational goals. As stated by Han & Cao, (Citation2022) a variable is referred to as an intervening variable if it affects how the predictor variable (which is independent) and the criterion variable relate to one another (dependent). The t-count value of the Sobel test results is 0.279969 compared to the t-table value of 42 data with df = 39 (t-table = 2.023). The t-count value is smaller than the t-table value, so it can be concluded that there is no mediating effect of the participation variable. budgeting on managerial performance. The results of this study do not support research from Indarto and Ayu (Citation2011), Kholidah and Murtini (Citation2014), Jannah and Rahayu (Citation2015), and Giusti et al. (Citation2018), showing that budget participation significantly and positively impacted managerial performance, with the mediation of organizational commitment. Hence, the fourth hypothesis, stating that budgetary participation had a positive effect on managerial performance mediated by organizational commitment, was not supported.

9.5. Leadership style on managerial performance mediated by organizational commitment

This study’s findings demonstrate that the leadership style’s regression coefficient on organizational commitment was 0.703, with a significance value of 0.000 < 0.05 and the impact of organizational commitment on employee performance was 0.063, with a significance value of 0.781 > 0.05. It means that leadership style positively and significantly impacted organizational commitment, and organizational commitment positively but insignificantly impacted managerial performance. Then, through organizational commitment, the indirect influence results of leadership style on managerial performance are shown by obtaining an indirect effect coefficient, which is the multiplication of the regression coefficient of leadership style on organizational commitment. The regression coefficient of organizational commitment on managerial performance was 0.044, smaller than the direct effect of leadership style on the managerial performance of 0.541. It denotes that organizational commitment was not effective as a mediator of the significance of the leadership style’s influence on managerial performance.

To prove and find out the mediating role of organizational commitment in the significance of the leadership style’s influence on managerial performance, it was supported through the Sobel test, which obtained t-count <t-table. Moreover, the ineffectiveness of organizational commitment as a mediator of the relationship of leadership style to managerial performance is because organizational commitment has not become an inner bond for employees to continuously work hard to support managerial performance achievement, which should be supported together. An existing commitment also did not foster enthusiasm for hard work even though it was driven by the existing leadership.

10. Conclusion and recommendations

Departing from the research results and discussion presented before, several conclusions can be drawn. First, budget participation had a positive but not significant impact on managerial performance. It indicates that if budget participation is increased, the managerial performance at the Public Works and Public Housing Office of Wonogiri Regency, and Tax Service Office, of Wonogiri Regency, Indonesia does not follow directly; there will be an increase but not significant. Therefore, the leadership can take concrete steps as follows: 1) Leaders maintain ways of providing opportunities for subordinates to take part in the budget process; 2) Leaders maintain ways of providing opportunities to formulate a budget at the Public Works and Public Housing Office of Wonogiri Regency, and Tax Service Office, Wonogiri Regency, Indonesia with subordinates; 3) Leaders maintain ways of providing opportunities for subordinates to participate in setting goals and setting budgets.

Second, leadership style positively and significantly impacted managerial performance. It denotes that if the leadership style is improved, the managerial performance will increase at the Public Works and Public Housing Office of Wonogiri Regency, and Tax Service Office. Therefore, the leadership can take concrete steps as follows: 1) Supervisors have a tendency to get out of hand in dealing with work problems, e.g., the leader encourages subordinates to be responsible for a job that has been done; 2) The supervisor always plans clear and firm steps in carrying out work supervision, such as the leader has anticipatory steps in supervising the work of subordinates; 3) Superiors always monitor the actions of subordinates in completing work tasks, i.e., leaders always pay attention to the progress of the work of subordinates.

Third, organizational commitment had a positive but significant impact on managerial performance. Fourth, organizational commitment was not a mediator in the significance of budget participation’s influence on managerial performance. Finally, organizational commitment did not mediate the significance of the leadership style’s influence on managerial performance at the Public Works and Public Housing Office and Tax Service Office of Wonogiri Regency, Indonesia. In future research, the researchers suggest taking a broader sample so that a more real and representative overview of the population can be obtained. Likewise, the researchers can develop other variables so that they do not only use budgetary participation, leadership style, and organizational commitment variables, but can use variables of competence, compensation, communication, loyalty, and others. The contribution of this study attempts to offer new insights into the impact of budget participation and leadership Style on managerial performance with organizational commitment as the intervening variable for more internal control and organizational commitment for improving managerial performance in terms of the work of public service organizations in carrying out their activities in serving the community by managers carry out management functioning state-owned organizations and governmental services office. Moreover, the novelty of this study uses organizational commitment as a mediating variable. Organizational commitment is an employee’s attachment to organizational values and goals. A positive view of the benefit of the organization is shown by managers who have a high commitment. Therefore, Organizational commitment as a mediator in the budgeting participation process assumes that a leader will be able to achieve the set budgetary goals if there is encouragement for employee engagement in doing the best for the organization above personal interests. Organizational commitment has a very important influence on work to create conducive working conditions so that the organization can run effectively and efficiently. Commitment is described as an attitude of willingness to work hard and with all efforts for the progress of the organization.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abata, M. A. (2014). Participative budgeting and managerial performance in the Nigerian food products sector. Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA) an Online International Research Journal, 1(3), (2311-3162). https://nanopdf.com/download/file-global-business-research-journals_pdf

- Andison, Y. A. (2017). Budget participation, job satisfaction, and managerial performance: A study on the pempek family business in palembang city. Journal of Business and Management, 7(1), 73–25.

- Andre, M., & Hermanto, A. (2021). The effect of organizational commitment and organizational culture on employee performance Pt. Citra Mandiri Cemerlang Prima. Krisnadwipayana Business Management Journal, 9.2. http://dx.doi.org/10.35137/jmbk.v9i2.578

- Arikunto, S. Research Procedure A Practical Approach. Jakarta: Rineka Copyright 2014.

- Brownell, P. (1982). The role of accounting data in performance evaluation, budgetary participation, and organizational effectiveness. Journal of Accounting Research, 20(1), 12. https://doi.org/10.2307/2490760

- Eker, M. (2009). The impact of budget participation on managerial performance via organizational commitment: A study on the top 500 firms in Turkey. e-Journal Ankara Univesitesi SBF Derg, 64(4), 118–136. https://dergipark.org.tr/tr/download/article-file/35937

- Elwisa, J. (2017). Effect of budget participation, work motivation, work environment, and compensation on managerial performance in local government agencies in Bintan Regency. Thesis. Accounting Study Program, Faculty of Economics, Universitas Maritim Raja Ali Haji

- Ermawati, N. (2017, July). Effect of budget participation on managerial performance with work motivation as moderating variable case study of local government agencies in Pati Regency. Indonesian Journal of Accounting, 6(2), 141–156.

- Fabio, H., & Puspitawati. (2016). Effect of leadership style, work motivation on organizational commitment with implications for employee performance. Journal of Business and Management Applications, 2(1), 91–104. https://doi.org/10.17358/jabm.2.1.91

- Gamayuni, Gamayuni, R. R., & Suryani. (2019). The effects of budgetary participation, budgetary slack, authority delegation, and organizational commitment on managerial performance on local government in Lampung, Indonesia. Journal of Administrative and Business Studies, 5(6), 330–338. https://doi.org/10.20474/jabs-5.6.4

- Gibson, J. L., Ivancevich, J. M., Donnelly Jr, J. H., & Konopaske, R. (2012). Organizations: Behavior, structure, processes (14th edition) ed.). McGraw-Hill.

- Giri, M., & Wiguna, D. B. (2014). Effect of budgetary participation on managerial performance through distributive justice, procedural fairness, and commitment to budget goals as mediating variables. Thesis, Universitas Udayana. Denpasar.

- Giusti, G., Kustono, A. S., & Effendi, R. (2018). Effect of budget participation on managerial performance with organizational commitment and motivation as intervening variables. E-Journal of Business Economics and Accounting, 2, 121–128.

- Hakim, A. (2015). Effect of organizational culture, organizational commitment to performance: Study in hospital of district South Konawe of Southeast Sulawesi. The International Journal Of Engineering And Science (IJES), 4(5), 33–41. https://doi.org/10.22146/jlo.64390

- Hakim, A. L., Faizah, E. N., & Mas’adah, N. (2021). Analysis of leadership style by using the model of hersey and blanchard. Journal of Leadership in Organizations, 3(2), 138–148. https://doi.org/10.22146/jlo.64390

- Han, X., & Cao, N. (2022). Application of multivariate statistical analysis based on the random matrix in the study of Chinese cultural symbols. Mathematical Problems in Engineering, 2022(9717752), pp, 8. https://doi.org/10.1155/2022/9717752

- Hasibuan, S., & Malayu, P. (2015). Human resource management. Jakarta. PT. Bumi Aksara.

- Hidrayadi, R. (2015). The effect of decentralization, budget participation, organizational commitment, and work motivation on performance of SKPD managerial pekanbaru city. Student Online Journal (JOM) in Economics, 2(2), 15.

- Indarto, & Ayu, S. D. (2011). The influence of participation in budgeting on company managerial performance through budget adequacy, organizational commitment, commitment to budget objectives, and Job Relevant Information (JRI)]. Scientific Studies Series, 14(1), 1–44.

- Jannah, & Rahayu. (2015, October-December). The influence of budgetary participation on local government agency managerial performance with clarity of budget goals, commitment to budget goals, distributive justice, and internal control as intervening variables. Journal of Regional Development and Financing Perspective, 3(2).

- Kholidah, L., & Murtini, H. (2014). Budget participation in managerial performance: organizational commitment and task information as mediators. Accounting Analysis Journal, 3, 2. https://doi.org/10.15294/aaj.v3i2.4186

- Lina, & Stella. (2013). Effect of budgeting participation on managerial performance: Job satisfaction and job relevant information as intervening variables. Journal of Business and Accounting, 15(1), 37–56.

- Mahoney. (1963) “Development of Managerial Performance: A Research Approach”. Cincinnati: South-western Pub. Co., Cincinnati

- Manica, & Hanny. (2016). Effect of budget participation on managerial performance through job satisfaction, commitment to budget goals, and job relevant information. Journal of Administrative Sciences, 8(1), 77–92.

- Moheri, & Arifah. (2015, January). Effect of budget participation on managerial performance. EKOBIS, 16(1), 86–93.

- Noor, I. H. B. M., & Othman, R. (2012). Budgetary participation: How it affects performance and commitment. Accountancy Business and the Public Interest, 1, 53–73.

- Putri, & Adiguna. (2014). Effect of budget participation, organizational commitment, and leadership style on managerial performance. Esensi, 4(3), 137–160.

- Robbins, & Judge. (2019). Organizational behavior. Salemba empat.

- Sari, A., & Abdullah. (2017). The influence of participation in budgeting, job satisfaction, job relevant information, and work motivation on the managerial performance of the public prosecutor’s office in the aceh region. Journal of Masters in Accounting, 20–31.

- Sugiyono. (2013). Qualitative Quantitative Research Methods and R&D. Alphabeta.

- Suharman, H. (2012). The influence of corporate social performance, budget emphasis, participative budget on job related tension. World Journal of Social Sciences, 2(7), 48–63.

- Syahputra, Z. (2014). Budget Participation on Managerial Performance: Related Factors in that influenced to Government’s Employee (Study of Indonesian Local Government). Journal of Economics and Sustainable Development, 5(21), 2222-1700 (Paper) 2222-2855 (Online).

- Syakieb, A., Mohd Saudi, M. H., Rini, S., & Adison, A. (2018). Effect of participative budgeting, organizational commitment, and work motivation on managerial performance (survey of motor vehicle dealers in Bandung). International Journal of Engineering & Technology, 7 /4(34), 240–244.

- Syukri, M., Surasni, Ni & Furkan, Lalu. (2019). The influence of budget participation and leadership style on managerial performance with job relevant information as moderator. E-Journal of Accounting, 29(987). https://doi.org/10.24843/EJA.2019.v29.i03.p06

- Tarigan, & Devie. (2015). The influence of budgeting participation on managerial performance in service companies: An evidence from Indonesia. Journal of Accounting and Finance, 15(8), 95–105.

- WiseGEEK. 2012. Clear Answers for common Questions www.wisegeek.com

- Yulianingsih, Y. (2017). The effect of budget participation on managerial performance with motivation and organizational culture as moderating variables (Case Study at the Center for Community Lung Health (BBKPM) in Surakarta). Thesis. Faculty of Economics & Business, Accounting Economics Study Program, Universitas Muhammadiyah Surakarta.

Appendix

Table A1. Description of respondents by age

Appendix

Table A2. Classification of respondents by gender

Appendix

Table A3. Description of respondents by marital status

Appendix

Table A4. Classification of respondents by education level

Appendix

Table A5. Classification of respondents by years of service

Appendix

Table A6. Correlation of Statement Items for Budget participation (X1)

Appendix

Table A7. Correlation of Leadership Style Statement Items (X2)