?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Owing to the significant role of financial sector reforms in economic growth, several studies have examined its transmission channels. This paper focuses on the stock market channel by investigating the impact of financial sector reforms on stock market growth in Ghana from 1990 to 2019. A multidimensional index was constructed to measure the financial sector reforms. Employing fully modified least squares (FMOLS) and error-correction models, the findings reveal that financial sector reforms promote stock market growth in Ghana in the long run. By disaggregating the financial sector reforms, the findings reveal that competitive reform has the highest impact followed by behavioural and privatisation reforms respectively. Finally, the findings reveal a bi-causal relationship between financial sector reforms and stock market growth. The paper thus implores the Securities and Exchange Commission (SEC) to reinforce its supervisory role, policy implementation, and investor protection laws to ensure greater compliance with the reforms. In addition, macroeconomic policies that are helpful to the growth of the capital market must be deepened to stimulate expected growth in the Ghanaian stock market.

PUBLIC INTEREST STATEMENT

Given the significant role played by financial sector reforms on economic growth, this paper sought to analyse the effect of financial sector reforms on stock market growth in Ghana. The paper constructed a multidimensional index to measure the financial sector reforms. The findings reveal that financial sector reforms promote stock market growth in Ghana. It was also revealed that although all three categories of financial sector reform index promote stock market growth, competitive reforms had the highest impact, followed by behavioural and privatisation reforms respectively. Lastly, the findings revealed there exist a bi-causal relationship between financial sector reforms and stock market growth. Thus, the paper recommends that the Bank of Ghana reinforce its supervisory role, policy implementations and investor protection laws to ensure greater compliance with the reforms. In addition, inflation and interest rate policies that are helpful to the growth of the capital market must be deepened (by the Bank of Ghana) to stimulate the expected growth on the Ghana Stock Exchange.

1. Introduction

Financial markets and financial intermediaries have been evidenced to play a key role in economic growth (see Athari et al., Citation2021a; Kirikkaleli & Athari, Citation2020). Stock markets facilitate trading of bonds, stocks, and other long-term financial instruments raised by corporate institutions. Theoretically, stock markets contribute to economic development by enabling entrepreneurs with viable projects to access capital required to grow their businesses. In practice, the activities of stock market permit businesses, corporate bodies, and subdivisions of the economy to acquire long-term funding to facilitate productive investment ventures and increase production, which results in economic growth (Abu, Citation2009). Therefore, although stock markets perform other functions, UNCTAD (Citation2015) notes that access to finance by firms and liquidity for investors is the core reason for establishment of stock exchanges.

Growth in the African stock market has been based on domestic financial liberalisation and reform programmes specific to member countries and global integration (Yartey & Adjasi, Citation2007). Ghana, pursuant to its growth strategy, has seen major financial sector reform programs implemented in the 1980s, which involved institutional reforms as well as financial sector reforms and liberalisation. Owusu-Antwi (Citation2009) noted that “these reforms became unavoidable when the pre-reform strategies of the government of Ghana for financial markets, coupled with a severe and long-lasting economic crisis seriously impaired the financial system, resulting to financial capriciousness and bank distress”. Thus, financial sector reforms are seen as a means used by governments to bring efficiency to the mobilization and allocation of capital to ensure stability and confidence in the financial sector. The underlying objectives are to relax external constraints in financial market operations; remove financial repression to provide operational autonomy to institutions; create an efficient, competitive, and stable sector; and increase transparency through deregulated interest and credit rates (Mohan, Citation2013).

Beyond 1988, two major reform programmes were implemented in Ghana, the first being the Financial Sector Adjustment Programme (FINSAP) within the period 1988 to 2000, driven by the World Bank to tackle institutional insufficiencies by restructuring troubled banks, reforming prudential legislation and supervisory systems, permitting new entrants into the financial markets, and developing money and capital markets. The second was the Financial Sector Strategic Plan (FINSSP), which was spearheaded by the government from 2001 to 2008 with the objective of consolidating gains made under FINSAP and to further improve financial service delivery. Some of the reform policies included the Bank of Ghana Act 2002, Banking Amendment Act 2007, Foreign Exchange Act 2007, Credit Reporting Act 2008, and Lender and Borrowers Act 2008, among others.

Subsequent to the implementation of financial sector reforms in Ghana, several studies have been undertaken on financial sector reforms and their impacts on various economic outcomes. These include economic growth (Owusu & Odhiambo, Citation2015), foreign direct investment (Kamasa et al., Citation2020), private sector investment (Ofori-Abebrese & Kamasa, Citation2013), and bank performance and systems (Antwi-Asare & Addison, Citation2000; Owusu-Antwi, Citation2009). However, one key transmission channel that is yet to be explored is the stock market channel. In addition, most studies on financial sector reforms fail to account for the gradual changes in the reforms by simply using proxies such as broad money supply, credit to private sector, and real interest rate, among others. This paper seeks to bridge these gaps by addressing three specific objectives. First, it measures the impact of financial sector reforms on stock market growth in Ghana by constructing a composite reform index that takes into account the changes that occur in the sector’s reforms. Second, this paper decomposes the composite reform index into behavioural, privatization, and competitive reform indexes to ascertain the category of reforms that are most relevant in achieving stock market growth in Ghana. Third, this paper assesses the causal relationship between stock market growth and financial sector reforms. Given the role of the stock market in economic growth, this paper’s findings have policy implications for deepening the financial sector, ultimately making it possible to reap the benefits associated with stock market growth.

The remainder of the paper is outlined as follows. Section 2 deals with brief review of the literature. Section 3 describes the construction of the financial sector reform index. Issues regarding data, model specification, and estimation techniques are laid out in Section 4. Section 5 deals with presentation and analysis of empirical results. Finally, Section 6 concludes the paper with policy implications and recommendations.

2. Review of related literature

Calderon-Rossell (Citation1991) developed a partial equilibrium framework that laid the foundation for financial theory on stock market growth. El-Wassal (Citation2013) presented a theoretical framework to clarify the channels for stock market growth and found that policies geared toward financial sector liberalisation have a direct and positive influence on stock market growth. This theory supports the financial liberalisation hypothesis advocated by McKinnon (Citation1973) and Shaw (Citation1973), who emphasized the need for a liberalised financial sector. Theoretically, financial sector reforms through financial deepening can increase the ratio of money supply to GDP via increased access to investible funds. The increase in liquidity makes it possible for investment and growth opportunities in the stock market. Moreover, a well-developed financial sector enhances the efficiency and strengthen the stability of the financial system through investor confidence and uncertainty alleviation, which goes a long a way in affecting investment decisions. On the contrary, when the financial system is not well developed, it limits access to investment funds and tends to reduce the incentive to invest. Again, with a poor financial system, there is little control over investor behavior, which can lead to irrational herd behavior with its negative impacts. For instance, irrational herd behavior produces rapid increases in asset values, lax lending and over-borrowing, excessive risk-taking, and outsized profits, followed by crash asset values, rapid deleveraging, risk aversion, and huge losses (Rivlin, Citation2009).

From the standpoint of stock market, the current empirical literature outlines two sets of factors that influence its growth—macroeconomics and institutional, of which macroeconomic factors have received much attention. Khan et al. (Citation2021) investigated the impact of macroeconomic variables on Shanghai stock exchange returns. The results indicate that oil and gold prices have a positive effect on stock returns in the short and long run, while the exchange rate exhibits a negative effect in both the short and long run. Kumar et al., Citation2020) studied the causal relationship between international prices of crude oil, gold, exchange rate, and the Indian stock market and found evidence that crude oil prices positively affect the Indian stock market, whereas exchange rate negatively affect the stock market in the short run. However, gold prices do not affect the stock market. He et al. (Citation2021) also assesses the causal relationship between Turkish stock market returns and foreign exchange rates. They found, among others, that there is a negative correlation between the Turkish stock market and foreign exchange rates at different frequencies. Athari et al. (Citation2022) on their part examined the impact of the global pandemic uncertainty index on the German stock market index and found that in both high- and low-volatility regimes, the global pandemic uncertainty index negatively affects the German stock market index. Jelilov et al. (Citation2020) investigated the stock market returns–inflation nexus by controlling for the effect of the COVID-19 pandemic in Nigeria. Their results show that COVID-19 increases volatility and distorts the positive relationship between inflation and stock market return. Kirikkaleli (Citation2020) investigated the effects of economic, financial, and political risk and global economic policy uncertainty on the stock market index in Taiwan. The findings reveal that declining economic, political, and financial risk are associated with an increasing stock market index. With respect to Ghana, Asravor and Fonu (Citation2020) examine the long- and short-term relationship between macroeconomic variables and stock market returns and development and find that money supply, inflation rate, and human capital have a negative impact on stock market development, whereas the foreign direct investment and interest rate have a positive impact on stock market development.

For studies that have centered on institutions and financial sector reforms, the emphasis has been largely limited to a few areas, one of which is the banking system. For instance, Moyo et al. (Citation2014) used a duration model to study the connection between competition, banking systems, and financial sector reform stability in sub-Saharan Africa (SSA). The findings establish that macroeconomic, bank-specific, and institutional factors are vital in foretelling bank distress occurrences. Similarly, Bhaumik et al. (Citation2017) study the success of banking reforms in the Indian economy in the 1990s. The study was premised on the fact that a well-functioning credit market indicates effective monetary policy works through credit channels. According to the findings, private firms are most susceptible to monetary strategy changes during tight policy governance (i.e., their bank credit is highly sensitive to changes in interest rates). In the case of Ghana, Owusu-Antwi (Citation2009) assessed the impact of financial sector reforms on banking systems using the pre- and post-reform policy eras and found that the financial sector had been ample and healthy since the implementation of the reforms and that the financial liberation approach pursued by Ghana has been helpful to general economic growth.

Another area that has received attention in relation to financial sector reform is investment. Zhang (Citation2016) investigated financial sector reforms in emerging economies from a micro-sector perspective using data from listed companies in China and found evidence that financial flexibility has a positive influence on investment and firm performance, although investment scale, and not investment efficacy, drove firm performance. As with regard to Africa, Agbloyor et al. (Citation2014) investigated the causality between FDI and financial sector development and found evidence of a bi-causal relationship between FDI and financial sector development. Similarly, Sghaier and Abida (Citation2013) found evidence that the degree to which economic growth was enhanced via FDI improves with the development of the financial sector. Kamasa et al. (Citation2020) established a positive effect of financial sector reforms on FDI in Ghana. In a related study, Ofori-Abebrese and Kamasa (Citation2013) established that financial sector reforms enhanced private investment in Ghana.

In terms of economic growth and development, empirical studies demonstrate that stock market promotes economic development (see Seven & Yetkiner, Citation2016; Wong & Zhou, Citation2011). Manasseh et al. (Citation2018) examined the causality between stock market development, financial sector reforms, and economic growth in Nigeria. They observed bidirectional causality between stock market development and economic growth, along with financial sector reforms and economic growth. In addition, their study revealed unidirectional causality, from financial sector reforms to stock market development. In a recent study, Dabwor et al. (Citation2020) assessed the effect of stock market volatility on economic growth in Nigeria, accounting for the moderating role globalization. Their findings reveal a positive, inelastic but statistically insignificant effect of stock market returns on economic growth in Nigeria. Adu et al. (Citation2013) on their part studied the effect of financial development on economic growth in Ghana and found that the effect depends on the choice of proxy used to measure financial development, such that credit to the private sector and total domestic credit proxies positively affect economic growth, whereas broad money proxy affects growth negatively.

Despite a host of studies on the impact of financial reforms on variables discussed above, those relating to stock market growth are limited. Schäfer et al. (Citation2013) used four regulatory reforms to analyse the responses of stock market returns and Credit Derivative Swap (CDS) spreads of banks in Europe and the United States. The event study analysis found that not only did financial markets respond to the structural reforms implemented at the national level but also reduced the bail-out expectations of systemic banks and lowered equity returns in most cases. Li et al. (Citation2022) on their part evaluated the effect of stock market liberalisation on stock price synchronicity and found evidence to suggest that the implementation of the Shanghai-Hong Kong Stock Connect significantly reduces stock price synchronicity of eligible firms listed in the Shanghai Stock Exchange, and that this effect mainly exists in listed firms with a lower degree of openness. In the case of Ghana, the review indicates a lacuna. At best, the reviewed identified Barnor and Wiafe (Citation2015) who examined the impact that financial sector openness has on stock market performance in Ghana and found a positive relationship between stock market performance and financial openness. Even with their study, they proxied financial openness with the Chinn-Ito index (KAOPEN), an index that measures a country’s degree of capital account openness. As such, they did not measure financial sector reforms because there are multifaceted items that come into play when dealing with reforms. Having noted the role of the stock market, this paper adds to the growing literature by investigating the impact of financial sector reforms on stock market growth in Ghana by constructing a multidimensional index to measure changes in financial sector reforms. This study goes a step further to assess the various dimensions of the reforms to identify which matters most in terms of stock market growth.

3. Construction of financial sector reforms index

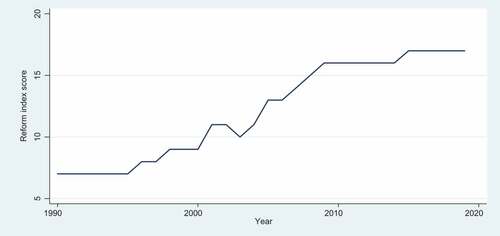

Several measures have been proposed to measure reforms in the financial sector (see, for instance, Abiad & Mody, Citation2005; Arestis et al., Citation2002; Bandiera et al., Citation2000; Laeven, Citation2000). For this paper, we adopt and extend the financial reform index constructed by Kamasa et al. (Citation2020) who applied a method proposed by Abiad et al. (Citation2010) to construct an index spanning 1987–2016. This paper extends to construct index for 2017–2019. Financial sector reform is multidimensional. To this regard, seven dimensions of policy changes were used in the development of the index, which includes financial account restrictions, security markets, state ownership, banking regulations, interest rate controls, credit controls, and barriers to entry (Abiad et al., Citation2010).

As explained by Kamasa et al. (Citation2020), a scaler score is assigned to range between zero (0) and three (3) for each dimension. If the outcome score assigned is zero (0), it represents full repression in that particular dimension. A score of one (1) represents partial repression while scores of two (2) and three (3) represents partial liberalisation and full liberalisation respectively. This culminates in a matrix of seven variables, with each representing a particular reform dimension of which a summation is obtained and used as a reform index for a particular year. It must be noted that changes in policies brings about changes in the scores for a particular year. For example, when there is a complete removal of restrictions on the securities markets, this policy reform will correspond to a jump of the score with respect to the dimension in question. Likewise, restrictions and impositions in a particular policy dimension will result in a reduction in the score for a particular year. With this approach, Kamasa et al. (Citation2020) argue that index constructed presents a more reliable measure of the reform changes as compared to existing measures such as Bandiera et al. (Citation2000) and (Laeven, Citation2000), where binary dummy variables are coded to denote financial liberalisation

The financial sector reform index constructed for the study period is illustrated in Figure , where it can be noted that there is a general deepening of reforms over time.

Figure 1. Composite reform index scores.

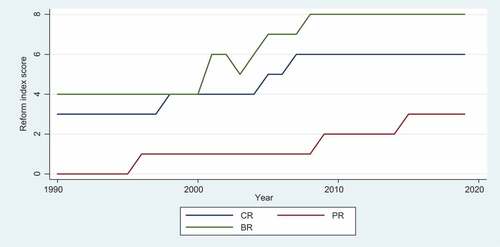

In order to assess the impacts of the various types of financial sector reforms on private sector investment, the reforms index developed is categorised into three main types (of behavioural reforms (credit and interest rate liberalisation), competitive reforms (banking sector entry, financial account transactions and security market reforms), and privatization reforms) following Angkinand et al. (Citation2010). They argue that controls on credit and interest rate to a large extent are almost equal or comparable. This is because if financial institutions are allowed to give credit facilities but are not granted the freedom to set rates of interest on credit they give out, it will imply that the credit allocation is going to be affected by the structure of the prevailing interest rate. It can be argued that interest rate and credit controls of all forms may be seen as a restriction on the behaviour and actions of financial institutions. Therefore, reforms to abolish interest rate as well as credit controls are combined into what is to be called Behavioural Reforms (BR). Again, equity market restrictions as well as international capital transactions would mean that banks are restricted with respect to the use of funds, the number of available sources of funding, foreign entry and competition from non-bank financial institutions. The effect of these restrictions on entry and banks transactions has comparable consequences with respect to the competitive position of institutions in the financial system. Thus, reforms for banking sector entry, financial account transactions, and securities market are combined into Competitive Reforms (CR). Finally, government ownership is argued to be a restriction of a different form. Thus, reforms in respect to government ownership is categorized as Privatization Reforms (PR). Figure shows the index with respect to the categorization. The full data for the index constructed is shown in Table in the appendix.

Figure 2. Reform index for sub-categories.

4. Empirical strategy and data

4.1. Model specification

This paper tests the hypothesis that financial sector reforms enhance stock market growth in Ghana. Accordingly, the paper employed a linear model specification following Caporale et al. (Citation2005) as shown in EquationEquation (1)(1)

(1) :

where; LNMCAP is the natural log of stock market growth (proxied by market capitalization), LNFRIN is log of Financial Sector Reform Index, LNINFL is log of Inflation Rate, LNFDI is log of Foreign Direct Investment, LNINT is log of Interest Rate and LNTR is log of Trade Openness. The paper took natural log of the variables to reduce the problem of heteroscedasticity and make all values be at the same unit or level.

Further, the effects of the various types of reforms on stock market growth were assessed using EquationEquation (2)(2)

(2) :

where LNCR is the log of competitive reform, LNBR is log of behavioural reform and PR is privatisation reform. The definitions for the other variables are same as defined in EquationEquation 1(1)

(1) . To avoid multicollinearity-related issues, each reform was estimated in a separate model.

4.2. Estimation strategy

The use of ordinary least squares (OLS) estimations to estimate Equationequations (1)(1)

(1) and (Equation2

(2)

(2) ) is reliable but is not designed to take into account long-run endogeneities in the regressors and the presence of such endogeneities produces biased results. In other to obtain reliable long-run estimates and check for robustness of results, this paper employed the fully modified least squares (FMOLS) estimator. The FMOLS regression was originally developed to make available optimal estimates of co-integrating regressions. The method adopts the semi-parametric approach in estimating the long-run parameters (Adom et al., Citation2015; Fereidouni et al., Citation2014) and also uses the Kernel estimators of the nuisance parameters which affect the asymptotic delivery of the OLS estimator. In order to attain asymptotic efficiency, the FMOLS method modifies least squares to account for serial correlation impact and test for the endogeneity in the regressors. In addition, this technique gives consistent parameters even in small sample size and allows for the heterogeneity in the long-run parameters (Bashier & Siam, Citation2014; Fereidouni et al., Citation2014). Other studies too have used FMOLS include Merlin and Chen (Citation2021), and Kirikkalel et al. (2018). FMOLS is expressed in Equationequation (3)

(3)

(3) as follows:

where:

and

are covariance matrices,

is residuals,

is lower triangular matrix.

and

represent dependent and independent variables respectively.

and

addresses serial correlation and endogeneity issues.

The short-run adjustment of stock market growth to changes in the financial sector reforms and other covariates are analysed through the error-correction method given that the variables as stated in Equationequation (1)(1)

(1) establishes cointegration. With that, the paper estimates an error-correction model as stated in equation (6):

where ,

,

,

,

,

are the short-run coefficients for the lag of stock market growth, financial sector reforms, inflation, foreign direct investment, interest rate, and trade openness respectively.

represents the first difference operator, while

represents the error correction term. Most significantly,

is the lag of the error-correction term, computed from the long-run cointegrated relationship equation in Equationequation (1)

(1)

(1) and

is the coefficient of the error-correction term, which measures the speed of adjustment from short-run disequilibrium. Theoretically,

must be negative and statistically significant.

4.3. Data and descriptive statistics

This paper used annual times series data spanning 1990 to 2019 for its analysis. Data sources include the Ghana Stock Exchange (GSE), Bank of Ghana bulletins, and World Bank’s World Development Indicators (World Bank, Citation2021).

4.4. Dependent variable

Market capitalization is the combined value of all listed company’s total shares outstanding and current share price on a national stock exchange. In this paper and several empirical studies, it is used as a proxy for stock market (see, for instance, Niroomand et at., 2014; Acheampong & Wiafe, Citation2013; Anokye & Tweneboah, Citation2009).

4.5. Independent variable

Financial sector reform index is the main independent variable for this study. It measures changes in reforms which has taken place in the financial sector over the study period. The index used was of two kinds. The first entails the composite index made up of all the seven dimensions while the second deals with the disaggregated along the kinds of reforms as explained in detail in Section 3.

4.6. Controlled variables

In estimating the stock market, the literature has shown other important covariates that must be controlled to avoid the problem of omission variable bias. Foreign direct investment refers to direct investment equity flows in the reporting economy. FDI can stimulate stock market growth through different channels. First, FDI has a positive influence on the number of firms participating in capital markets because foreign investors might want to finance part of their investment with external capital or might want to recover their investment by selling equity in capital markets (see Acheampong & Wiafe, Citation2013; Anokye & Tweneboah, Citation2009). In addition, given that foreign investors partly invest by purchasing existing equity, the liquidity of stock markets increases. Inflation is a sustained rise in the general prices of goods and services. A high inflation rate is an indication of economic uncertainty, which leads to low investor confidence. Additionally, an increase in the inflation rate reduces the real rate of return on money and all other assets. Therefore, there is a negative relationship between stock market growth and the inflation rate (Khan, Citation2004). Another covariate is interest rate, which refers to the cost of capital. Higher interest rates tend to negatively affect earnings and stock prices in the long run (Panda, Citation2008). The final covariate is trade openness. According to Niroomand et al. (Citation2014), “trade openness benefits financial market development in two different ways: supply side and demand-side roles”. Rajan and Zingales (Citation2003) also note that “trade openness weakens the incentives of incumbent financial intermediaries or interest groups to slow down financial market development to reduce entry and competition. As a result, trade openness tends to induce investment and bank lending, and hence fosters the general development of financial markets”. Formal definition, measurement, and sources of all variables used in this paper are displayed in Table of the appendix.

4.7. Descriptive statistics of variables

With respect to descriptive statistics, all variables were normally distributed. Stock market growth (LNMCAP) has a mean of 21.48 and standard deviation of 3.27. Financial sector reform index (LNFRIN) has a mean of 2.44 and standard deviation of 0.35. Inflation (LNINFL) has a mean of 2.80 and standard deviation of 0.54. Foreign direct investment (LNFDI) has a mean of 1.02 and standard deviation of 1.01. Interest rate (LNINT) has a mean of 3.40 and standard deviation of 0.20. Finally, trade openness (LNTR) has a mean of 4.29 and standard deviation of 0.25. Details of variable statistics are displayed in Table .

Table 1. Descriptive statistics of variables

5. Results and discussions

5.1. Preliminary results

The Phillip-Perron (PP) unit root test together with the Augmented Dickey-Fuller (ADF) test was used to test for unit root and stationarity at level and at first difference for all the variables. Results for the PP test are shown in column 1 of Table with the Newey-West bandwidth automatically selected using Bartlett kernel, while results for ADF test are shown in column 2 with the lag length automatically selected using AIC. The null hypothesis that variables are not stationary was not rejected at levels for all variables. However, it was rejected at first difference, which means that all variables are integrated of order one I(1).

Table 2. PP and ADF unit root test results

After the unit root test, Hansen parameter instability cointegration test together with the bounds test procedure for cointegration by Pesaran et al. (Citation2001) was used to test for long-run relationship amongst stock market growth (MCAP) and the other independent variables employed in the paper. As revealed in Table , there is the existence of co-integration amongst the variables given an Lc statistic of 0.542 and p-value of >0.2 on a test statistic whose null hypothesis states that “series are cointegrated”. Similarly, given that the F-Statistic of 6.02 is higher than the upper bounds critical value of 5% (3.79), it implies that the null hypothesis of no long-run relationship is rejected as displayed in Table . This suggests that a long-run relationship exist between stock market growth and the independent variables.

Table 3a. Hansen parameter instability cointegration test results

Table 3b. Bound test for cointegration results

5.2. Main results

5.2.1. Effect of composite financial sector reforms on stock market growth

Having established cointegration, the paper went on to employ the FMOLS method to examine the long-run relationship between stock market growth and financial sector reforms with results displayed in Table .

Table 4. Long-run results

Results as reported in Table reveal a positive and significant effect of financial sector reform (LNFRIN) on stock market growth (LNMCAP). In particular, a 1% improvement in the financial sector reforms (LNFRIN) increases stock market growth by 5.68%. This finding is consistent with financial liberalisation hypothesis which supports financial sector reforms to promote growth and investment. The positive impact is as a result of the fact that financial sector reforms lead to reduction in the cost of capital as well as the elimination of rigidities that hampers the development of the stock market. Also, financial sector reforms increase information efficiency (Chinn & Ito, Citation2006; Claessens et al., Citation2001), which helps to boost the confidence of investors with its eventual improvement in stock returns. This ends up in the reduction of losses and an increase in market capitalization (Barnor & Wiafe, Citation2015). Again, financial sector reforms through financial deepening can increase the ratio of money supply to GDP via increased access to investible funds. The increase in liquidity makes it possible for investment and growth opportunities in the stock market. Empirically, this paper’s finding is corroborated by Atsin and Ocran (Citation2017), who found that financial sector reforms promote capital market development. Kamasa et al. (Citation2020), and Ofori-Abebrese and Kamasa (Citation2013) also found positive impacts of financial sector reforms on FDI and private investment, respectively.

As far as the covariates are concerned, FDI positively impacts stock market growth. That is, a 1% increase in FDI increases stock market growth by 0.96%. This result is justified in theory. FDI has a positive effect because foreign investors might want to finance part of their investment with external capital or might want to recover their investment by selling equity in capital markets (see Acheampong & Wiafe, Citation2013; Anokye & Tweneboah, Citation2009). Also, given that foreign investors partly invest through purchasing existing equity, the liquidity of stock markets increases. Empirically, this result is in line with Malik and Amjad (Citation2013), Acheampong and Wiafe (Citation2013), Walsh and Yu (Citation2010) as well as Adam and Tweneboah (Citation2009) whose findings support the positive role played by FDI in boosting stock market growth in the long run. Furthermore, the findings reveal that trade openness has a positive impact stock market growth whereby a 1% increase in trade openness leads to stock market growth by 3.33%. As noted by Rajan and Zingales (Citation2003), trade openness weakens the incentives of incumbent financial intermediaries to slow down financial market development to reduce entry and competition. As a result, trade openness tends to induce investment and bank lending, and hence foster the general development of financial markets. This result is supported empirically by Awiagah and Choi (Citation2018), Keho (Citation2017), and Law and Habibullah (Citation2009), whose findings also revealed that trade openness plays a prominent role in promoting capital market development. Again, the paper reveals a negative and significant effect of interest rate on stock market growth, where a percentage increase in interest rate is associated with a 3.922% decrease in stock market growth. In theory, the rationale for the negative relationship between interest rates and stock prices is that higher interest rates reduce the value of stocks as shown by the dividend discount model, making fixed income securities more attractive to investors than stocks. A similar argument is that an increase in the interest rate reduces the present value of future dividend incomes, which then depresses stock prices. Moreover, higher interest rates may reduce the propensity of investors to borrow and invest in the stock market. Finally, there is a positive, albeit insignificant, effect of inflation on stock market growth in the long run. Theoretically, there is an expected negative relationship between stock market growth and inflation rate because an increase in the inflation rate reduces real rate of return on money and all other assets. So, it is not surprising that although the result indicates positive relationship, it is statistically not significant.

The short-run error-correction results are displayed in Table . Most worthy of note is the coefficient of the error-correction term ECT (−1), which is negative and highly significant. This indicates that there is a long-run adjustment to any deviation in the short-run and thus corroborates the existence of cointegration already established. With a coefficient of −0.354, it means that long-run equilibrium from short-run deviations are restored at a speed of approximately 35%. The findings reveal a positive and significant relationship between the lag and current stock market growth. Interestingly, both the current and first lag of financial sector reforms did not have significant effect on stock market growth in the short-run, albeit with a negative coefficient. This finding is not surprising given that investors normally would want to be very sure about the nature and how any reforms could affect their investments and thus may be skeptical and cautious with their investment in the short-run until they have acquired enough knowledge and information. For the covariates, foreign direct investment and interest rate continued to have a significant positive and negative effect respectively on the stock market growth in the short run. Although the current period inflation had a negative insignificant effect, its lag had a positive and significant effect in the short run. Also, despite a positive coefficient, trade openness did not have a significant effect in the short run.

Table 5. Short-run error-correction results

5.2.2. Effect of the types of financial sector reforms on stock market growth

In evaluating the long-run effects of the various types of financial sector reforms on stock market growth, reforms were grouped into privatization, competitive, and behavioral. The results are reported in Table . Results from column (1) of Table show positive and significant effect of competitive reforms on stock market growth with a 1% increase in competitive reforms resulting in a 6.09% increase in stock market growth. With the exception of inflation (LNINFL) which is insignificant, foreign direct investment (LNFDI), interest rate (LNINT), and trade openness (LNTR) are all statistically significant.

Table 6. Results of the various types of reforms on stock market growth

Results from column (1) of Table show positive and significant effect of competitive reforms on stock market growth with 1% increase in competitive reforms resulting in 6.09% increase in stock market growth. With the exception of inflation (LNINFL) which is insignificant, foreign direct investment (LNFDI), interest rate (LNINT), and trade openness (LNTR) are all statistically significant as shown in column 1. Also, column 2 reveals a positive and significant effect of behavioural reforms on stock market growth. 1% increase in behavioural reforms improves stock market growth by 5.465%. With the exception of inflation (LNINFL) and interest rate (LNINT) which are insignificant, foreign direct investment (LNFDI) and trade openness (LNTR) are statistically significant in affecting stock market growth. Finally, column 3 shows that an increase in privatisation reform by 1% improves stock market growth by 1.152% and with the exception of inflation (LNINFL) which is insignificant, foreign direct investment (LNFDI, interest rate (LNINT), and trade openness (LNTR) are all statistically significant in affecting stock market growth. These results are consistent with the results reported in Table on the relationship between financial sector reform (LNFRIN) (that is, the composite index of all the other reforms) and stock market growth. The results, however, indicate that competitive reforms have the highest impact on stock market growth, followed by behavioural and privatisation reforms respectively.

5.3. Granger causality test

Table presents the results for the pairwise Granger causality between financial sector reforms and stock market growth.

Table 7. Pairwise granger causality test

Per the results, the null hypothesis that stock market growth (LNMCAP) does not Granger causes financial sector reform (LNFRIN) is rejected due to the significant p-value (0.016). Also, the null hypothesis that financial sector reforms do not Granger causes stock market growth is weakly rejected at 10% level of significance. Therefore, it can be said that there exists a bi-causal relationship between financial sector reforms and stock market growth, although the relationship which runs from financial sector reforms to stock market development is of a weak one.

5.4. Robustness and diagnostic test

Aside the FMOLS, this paper also employed alternative cointegration models including dynamic least squares (DOLS) and canonical cointegrating regression (CCR) models to check the robustness of its findings. Studies in Ghana that also employed DOLS include Tetteh et al. (Citation2022) and Amoah et al. (Citation2020). Table displays the results for DOLS (column 1) and CCR (column 2) respectively. It is to be noted that these tests were performed only on Equationequation (4)(4)

(4) , which captures the composite reform index and also the long-run relationship (due to limits on words and space). As shown in Table , both the DOLS and CCR results do not differ in both significance and sign (relationship) from that of the FMOLS in Table , except for marginal differences in the coefficients and thus indicates the robustness of the paper’s results. Both DOLS and CCR results show positive and significant effect of financial sector reforms on stock market growth in the long run. Likewise, for the covariates, both estimators reveal positive and significant effects of foreign direct investment and trade openness on stock market growth while interest rate impacted negatively on the stock market growth. Inflation, although positive, had no significant effect in both estimators.

Table 8. Robustness checks

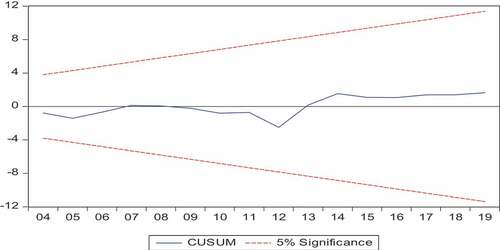

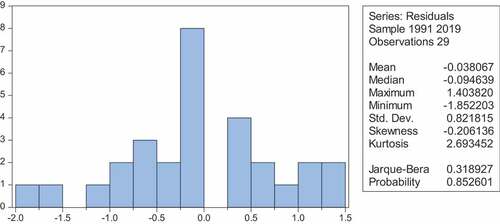

The paper further conducted series of diagnostic checks in ascertaining the reliability and robustness of its results. The key regression statistics associated with the FMOLS estimator as well as the error-correction model indicates a goodness of fit. Results from normality test performed using histogram, skewness, kurtosis, and Jaque-Bera test (see in the appendix) show that residuals are normally distributed. Furthermore, results from the CUSUM graph (see in the appendix) indicate the stability of variables. Moreover, the test statistic with its associated p-values for serial correlation, heteroskedasticity, and specification tests as shown in Table demonstrates the robustness of results.

Table 9. Model diagnostics

6. Conclusion and policy implication

On one hand, stock markets contribute to economic development by enabling entrepreneurs with viable projects to access capital required to grow their businesses. On the other hand, financial sector reforms are seen as a means used by governments to bring efficiency in the mobilization and allocation of capital to ensure stability and confidence in the financial sector. To this end, Ghana, pursuant to its growth agenda, has implemented several reforms in the financial sector since the late 1980s. Although several studies have been conducted since the inception of financial sector reforms, one important area is yet to be explored is the impact of financial sector reforms on stock market growth. Therefore, this paper sought to address that gap by constructing a multidimensional composite and disaggregated financial sector reforms index and assess its impact on stock market growth in Ghana. Employing fully modified least squares (FMOLS) and error-correction models the findings reveal that financial sector reforms promote stock market growth in Ghana in the long run. By disaggregating the financial sector reforms, the findings reveal that competitive reform has the highest impact followed by behavioural and privatisation reforms respectively. Furthermore, the findings revealed the existence of a bi-causal relationship between financial sector reforms and stock market growth. Finally, FDI and trade openness are identified to have a positive and significant impact while interest rate impacts negatively on stock market growth in Ghana.

Therefore, as a recommendation, this paper thus implores the SEC, which is the main regulatory body for the GSE market, to reinforce its supervisory role, policy implementations, and investor protection laws to ensure greater compliance with the reforms. Also, it is recommended that the Bank of Ghana take the needed steps to strengthen supervision and compliance across the financial sector with its regulatory measures, especially those related to capital requirements and transparency in financial statement practices to consolidate and sustain the gains made so far in stabilising the financial sector. Furthermore, policies that remove or limit restrictions on cross-border trade and financial flows, and thus foster integration into the global economy, should be promoted. This is because increased trade openness has the potential to increase efficiency in the allocation of capital through diversification of investments across local and international markets; improve market liquidity due to inflow of external capital; improve financial stability by lowering the likelihood of asymmetric shocks; and enhance the capacity of the entire financial system to absorb shocks. Finally, interest rate policies that are helpful to the growth of the capital market must be deepened by the Bank of Ghana to stimulate the expected growth on the Ghana stock exchange.

As a suggestion for further studies, consideration should be given towards using wavelet coherence analysis methods (see, for instance, Athari & Hung, Citation2022; Athari et al., Citation2021b; Kondoz et al., Citation2021), which can then make it possible to deal with time and frequency co-movement causality between financial sector reforms and stock market growth.

Disclosure statement

The authors report there are no competing interests to declare.

Additional information

Funding

Notes on contributors

Kofi Kamasa

Kofi Kamasa is an Economist, Researcher and Senior Lecturer at the Department of Management Studies, University of Mines and Technology, Tarkwa. He holds both Ph.D. and MPhil in Economics from the Kwame Nkrumah University of Science and Technology, Kumasi. His research areas include Monetary & Financial Economics; Economic Growth; International Trade & Finance and Public Finance.

Linda Owusu

Linda Owusu holds Master of Science degree in Industrial Finance and Investment from the Kwame Nkrumah University of Science and Technology, Ghana. She is a Benefit Advisor and also an Investment Analyst. She is also interested in researching into Change Management, Sustainability Management, Organizational Development, Business and Consulting.

Grace Nkansah Asante

Grace Nkansah Asante Asante is an Associate Professor of Economics at the Department of Economics of the Kwame Nkrumah University of Science and Technology (KNUST) Kumasi Ghana. She holds a PhD in Economics from Kwame Nkrumah University of Science and Technology (KNUST). Her research interest is in economic policy issues, finance and monetary issues. She is also a Priest in the Anglican Communion.

References

- Abiad, A., Detragiache, E., & Tressel, T. (2010). A new database of financial reforms. IMF Staff Papers, 57(2), 281–21. https://doi.org/10.1057/imfsp.2009.23

- Abiad, A., & Mody, A. (2005). Financial reform: What shakes it? What shapes it? American Economic Review, 95(1), 66–88. https://doi.org/10.1257/0002828053828699

- Abu, N. (2009). Does stock market development raise economic growth: Evidence from Nigeria. The Review of Finance and Banking, 1(1), 15–26.

- Acheampong, I. K., & Wiafe, E. A. (2013). Foreign direct investment and stock market development: Evidence from Ghana. International Journal of Finance and Policy Analysis, 5(1), 3–15.

- Adam, A. M., & Tweneboah, G. (2009). Foreign direct investment (FDI) and stock market development: Ghana evidence. International Research Journal of Finance and Economics, 26, 178–185.

- Adom, P. K., Amakye, K., Barnor, C., & Quartey, G. (2015). The long-run impact of idiosyncratic and common shocks on industry output in Ghana. OPEC Energy Review, 39(1), 17–52. https://doi.org/10.1111/opec.12039

- Adu, G., Mensah, J. T., & Mensah, J. T. (2013). Financial development and economic growth in Ghana: Does the measure of financial development matter? Review of Development Finance, 3(4), 192–203. https://doi.org/10.1016/j.rdf.2013.11.001

- Agbloyor, E. K., Abor, J. Y., Adjasi, C. K. D., & Yawson, A. (2014). Private capital flows and economic growth in Africa: The role of domestic financial markets. Journal of International Financial Markets, Institutions and Money, 30(C), 137–152. https://doi.org/10.1016/j.intfin.2014.02.003

- Amoah, A., Kwablah, E., Korle, K., & Offei, D. (2020). Renewable energy consumption in Africa: The role of economic well-being and economic freedom. Energy, Sustainability & Society, 10(1), 32. https://doi.org/10.1186/s13705-020-00264-3

- Angkinand, A. P., Sawangngoenyuang, W., & Wihlborg, C. (2010). Financial liberalisation and banking crises: A cross-country analysis. International Review of Finance, 10(2), 263–292. https://doi.org/10.1111/j.1468-2443.2010.01114.x

- Anokye, A. M., & Tweneboah, G. (2009). Foreign direct investment and stock market development: Ghana’s evidence. International Research Journal of Finance and Economics, 26, 179–185.

- Antwi-Asare, T. O., & Addison, E. K. Y. (2000). Financial sector reforms and bank performance in Ghana (pp. 106). Overseas Development Institute.

- Arestis, P., Demetriades, P., Fattouh, B., & Mouratidis, K. (2002). The impact of financial liberalisation policies on financial development: Evidence from developing economies. International Journal of Finance and Economics, 7(2), 109–121. https://doi.org/10.1002/ijfe.181

- Asravor, R. K., & Fonu, P. D. (2020). Dynamic relation between macroeconomic variable, stock market returns and stock market development in Ghana. International Journal of Finance and Economics, 26(2), 2637–2646. https://doi.org/10.1002/ijfe.1925

- Athari, S. A., & Hung, N. T. (2022). Time–frequency return co-movement among asset classes around the COVID-19 outbreak: Portfolio implications. Journal of Economics and Finance, 46(4), 736–756. https://doi.org/10.1007/s12197-022-09594-8

- Athari, S. A., Kirikkaleli, D., & Adebayo, T. S. (2022). World pandemic uncertainty and German stock market: Evidence from Markov regime-switching and Fourier based approaches. Quality and Quantity. https://doi.org/10.1007/s11135-022-01435-4

- Athari, S. A., Kirikkaleli, D., Wada, I., & Adebayo, T. S. (2021a). Examining the sectoral credit-growth nexus in Australia: A time and frequency dynamic analysis. Economic Computation & Economic Cybernetics Studies & Research, 55(4), 69–84. https://doi.org/10.24818/18423264/55.4.21.05

- Athari, S. A., Kirikkaleli, D., Yousaf, I., & Ali, S. (2021b). Time and frequency co‐movement between economic policy uncertainty and inflation: Evidence from Japan. Journal of Public Affairs, e2779. https://doi.org/10.1002/pa.2779

- Atsin, J. A., & Ocran, M. K. (2017). Financial liberalisation and the development of stock markets in Sub-Saharan Africa. MPRA Paper 87580, University Library of Munich, Germany.

- Awiagah, R., & Choi, S. B. (2018). Stock market development in Ghana: Whither trade openness. International Journal of Trade, Economics and Finance, 9(4), 135–141. https://doi.org/10.18178/ijtef.2018.9.4.603

- Bandiera, O., Caprio, G., Honohan, P., & Schiantarelli, F. (2000). Does financial reform raise or reduce saving? The Review of Economics and Statistics, 82(2), 239–263. https://doi.org/10.1162/003465300558768

- Barnor, C., & Wiafe, E. A. (2015). Financial sector openness and stock market development in Ghana. Research Journal of Finance and Accounting, 6(24), 80–88.

- Bashier, A. A., & Siam, A. J. (2014). Immigration and economic growth in Jordan: FMOLS approach. International Journal of Humanities Social Sciences and Education, 1(9), 85–92.

- Bhaumik, S. K., Kutan, A. M., & Majumdar, S. (2017). How successful are banking sector reforms in emerging market economies? Evidence from impact of monetary policy on levels and structures of firm debt in India. The European Journal of Finance, 24(12), 1047–1062. https://doi.org/10.1080/1351847X.2017.1391857

- Calderon-Rossell, R. J. (1991). The determinants of stock market growth, in S. G. Rhee & P. C. Rosita (Eds), Pacific basin capital markets research proceeding of the second annual pacific basin finance conference , Vol. II, Bangkok, Thailand, 4–6 June 1991.

- Caporale, G. M., Howells, P., & Soliman, A. M. (2005). Endogenous growth models and stock market development: Evidence from four countries. Review of Development Economics, 9(2), 166–176. https://doi.org/10.1111/j.1467-9361.2005.00270.x

- Chinn, M. D., & Ito, H. (2006). What matters for financial development? Capital controls, institutions, and interactions. Journal of Development Economics, 81(1), 163–192. https://doi.org/10.1016/j.jdeveco.2005.05.010

- Claessens, S., Djankov, S., & Klingebiel, D. (2001). Stock markets in transition economies. In Financial sector discussion paper No. 5. World Bank.

- Dabwor, D. T., Iorember, P. T., & Danjuma, S. Y. (2020). Stock market returns, globalization and economic growth in Nigeria: Evidence from volatility and cointegrating analyses. Journal of Public Affairs. https://doi.org/10.1002/pa.2393

- El-Wassal, K. A. (2013). The development of stock markets: In search of a theory. International Journal of Economics and Financial Issues, 3(3), 606–624.

- Fereidouni, H. G., Al-mulalia, U., & Mohammed, M. A. H. (2014). Wealth effect from real estate and outbound travel demand: The Malaysian case. Current Issues in Tourism, 20(1), 68–79. https://doi.org/10.1080/13683500.2014.882886

- He, X., Gokmenoglu, K. K., Kirikkaleli, D., & Rizvi, S. K. A. (2021). Co-movement of foreign exchange rate returns and stock market returns in an emerging market: Evidence from the wavelet coherence approach. International Journal of Finance and Economics. https://doi.org/10.1002/ijfe.2522

- Jelilov, G., Iorember, P. T., Usman, O., & Yua, P. M. (2020). Testing the nexus between stock market returns and inflation in Nigeria: Does the effect of COVID-19 pandemic matter? Journal of Public Affairs, 20(4). https://doi.org/10.1002/pa.2289

- Kamasa, K., Mochiah, I., Doku, A. K., & Forson, P. (2020). The impact of financial sector reforms on foreign direct investment in an emerging economy: Empirical evidence from Ghana. Journal of Humanities and Applied Social Sciences, 2(4), 271–284. https://doi.org/10.1108/JHASS-11-2019-0077

- Keho, Y. . (2017). The impact of trade openness on economic growth: The case of Cote d’Ivoire. Cogent Economics and Finance, 5(1), 1332820. https://doi.org/10.1080/23322039.2017.1332820

- Khan, K. N. (2004). Inflation and stock market performance: A case study for Pakistan. Savings and Development, 28(1), 87–101.

- Khan, M. K., Teng, J., Khan, M. I., & Khan, M. F. (2021). Stock market reaction to macroeconomic variables: An assessment with dynamic autoregressive distributed lag simulations. International Journal of Finance and Economics. https://doi.org/10.1002/ijfe.2543

- Kirikkaleli, D. (2020). The effect of domestic and foreign risks on an emerging stock market: A time series analysis. The North American Journal of Economics and Finance, 51, 100876. https://doi.org/10.1016/j.najef.2018.11.005

- Kirikkaleli, D., & Athari, S. A. (2020). Time-frequency co-movements between bank credit supply and economic growth in an emerging market: Does the bank ownership structure matter? The North American Journal of Economics and Finance, 54, 101239. https://doi.org/10.1016/j.najef.2020.101239

- Kondoz, M., Kirikkaleli, D., & Athari, S. A. (2021). Time-frequency dependencies of financial and economic risks in South American countries. The Quarterly Review of Economics and Finance, 79, 170–181. https://doi.org/10.1016/j.qref.2020.05.014

- Kumar, S., Kumar, A., & Singh, G. (2020). Causal relationship among international crude oil, gold, exchange rate, and stock market: Fresh evidence from NARDL testing approach. International Journal of Finance and Economics. https://doi.org/10.1002/ijfe.2404

- Laeven, L. (2000). Does financial liberalisation relax financing constraints on firms? World Bank Policy Research Working Paper No. 2467, World Bank, Washington D.C.

- Law, S. H., & Habibullah, M. S. (2009). The determinants of financial development: Institutions, openness and financial liberalisation. South African Journal of Economics, 77(1), 45–58. https://doi.org/10.1111/j.1813-6982.2009.01201.x

- Li, Q., Liu, X., Chen, J., & Wang, H. (2022). Does stock market liberalisation reduce stock price synchronicity? —Evidence from the Shanghai-Hong Kong Stock Connect. International Review of Economics & Finance, 77, 25–38. https://doi.org/10.1016/j.iref.2021.09.004

- Malik, I. A., & Amjad, S. (2013). Foreign direct investment and stock market development in Pakistan. Journal of International Trade Law and Policy, 12(3), 226–242. https://doi.org/10.1108/JITLP-02-2013-0002

- Manasseh, C. O., Ogbuabor, J. E., Anumudu, C. N., Abada, F. C., Okolie, M. A., & Okoro, O. E. (2018). The causal effect of stock market development, financial sector reforms and economic growth; the application of Vector autoregressive and error correction model. International Journal of Economics and Financial Issues, 8(2), 357–369.

- McKinnon, R. I. (1973). Money and capital in economic development. Brookings Institution.

- Merlin, M. L., & Chen, Y. (2021). Analysis of the factors affecting electricity consumption in DR Congo using fully modified ordinary least square (FMOLS), dynamic ordinary least square (DOLS) and canonical cointegrating regression (CCR) estimation approach. Energy, 232, 121025. https://doi.org/10.1016/j.energy.2021.121025

- Mohan, R. (2013). Financial sector reforms and monetary policy. In N. Hope, A. Kochar, R. Noll, & T. Srinivasan (Eds.), Economic reform in India: Challenges, prospects, and lessons (pp. 139–186). Cambridge University Press.

- Moyo, J., Nandwa, B., Oduor, J., & Simpasa, A. (2014). Financial sector reforms, competition and banking system stability in sub-Sahara Africa. https://www.imf.org/external/np/seminars/eng/2014/lic/pdf/Moyo.pdf.

- Niroomand, F., Hajilee, M., & Al Nasser, O. M. (2014). Financial market development and trade openness: Evidence from emerging economies. Applied Economics, 46(13), 1490–1498. https://doi.org/10.1080/00036846.2013.866207

- Ofori-Abebrese, G., & Kamasa, K. (2013). Do financial sector reforms promote private sector investment? The case of Ghana. International Journal of Research in Commerce, Economics and Management, 3(9), 129–136.

- Owusu-Antwi, G. (2009). Impact of financial reforms: On the banking system in Ghana. International Business and Economics Research Journal, 8(3), 77–99.

- Owusu, E. L., & Odhiambo, N. M. (2015). Financial sector reforms and economic growth in Ghana: A dynamic ARDL model. Contemporary Economics, 9(2), 181–192. https://doi.org/10.5709/ce.1897-9254.166

- Panda, C. (2008). Do interest rates matter for stock markets? Economic and Political Weekly, 43(17), 107–115.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Rajan, R. G., & Zingales, L. (2003). The great reversals: The politics of financial development in the twentieth century. Journal of Financial Economics, 69(1), 5–50. https://doi.org/10.1016/S0304-405X(03)00125-9

- Rivlin, A. (2009). Systemic risk and the role of the federal reserve. Financial reform project, briefing paper No. 2, The PEW economic policy department. https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.580.4348&rep=rep1&type=pdf

- Schäfer, A., Schnabel, I., & Weder Di Mauro, B. (2013). Financial sector reform after the crisis: Has anything happened?, CEPR discussion paper No. 9502.

- Seven, Ü., & Yetkiner, H. (2016). Financial intermediation and economic growth: Does income matter? Economic Systems, 40(1), 39–58. https://doi.org/10.1016/j.ecosys.2015.09.004

- Sghaier, I. M., & Abida, Z. (2013). Foreign direct investment, financial development and economic growth: Empirical evidence from North African countries. Journal of International and Global Economic Studies, 6(1), 1–13.

- Shaw, E. S. (1973). Financial deepening in economic development. Oxford University Press.

- Tetteh, J. E., Amoah, A., Ofori-Boateng, K., & Hughes, G. (2022). Stock market response to COVID-19 pandemic: A comparative evidence from two emerging markets. Scientific African, 17, e01300. https://doi.org/10.1016/j.sciaf.2022.e01300

- UNCTAD. (2015). Investment Policy Framework for Sustainable Development. https://unctad.org/en/PublicationsLibrary/diaepcb2015d5_en.pdf. Accessed: Feb 3, 2022

- Walsh, J. P., & Yu, J. (2010). Determinants of foreign direct investment: A sectoral and institutional approach, IMF Working Paper, 10 (187).

- Wong, A., & Zhou, X. (2011). Development of financial markets and economic growth: Review of Hong Kong, China, Japan, United States and United Kingdom. International Journal of Economics and Finance, 3(2), 11–15. https://doi.org/10.5539/ijef.v3n2p111

- World Bank. (2021), World development indicators, world bank group database, https://databank.worldbank.org. Accessed: June 6, 2021.

- Yartey, C. A., & Adjasi, C. K. (2007). Stock market development in Sub Saharan Africa: Critical issues and challenges. IMF Working Paper, 7, 209.

- Zhang, C. (2016). Financial reforms and performance in emerging market economies: An introduction. Emerging Markets Finance and Trade, 52(9), 1967–1969. https://doi.org/10.1080/1540496X.2016.1221627

Appendix

Table A1. Financial sector reform index (author’s constructs)

Appendix

Table A2. Definition of variable and data sources

Appendix

Figure A1. Normality Test.

Appendix

Figure A2. CUSUM test on residuals.