?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Even though Environmental tax policy impacts inequality theoretically, empirical studies remain scanty not only in the context of volumes and the estimation approaches but are also focused on selected advanced countries, communities, households, and emerging countries, the neglect of the global or big picture effect, which is essential for measuring the overall effect of the collective and individual country-concerted efforts in addressing this global cancer. We provide empirical evidence in the global context using the novel method of moments quantile regression. We found that Income Inequality across the globe is sharply reduced by restrictive environmental tax policy, a finding that has ramifications for global sustainable development, particularly in dealing with the ravaging effects of Covid-19.

PUBLIC INTEREST STATEMENT

This paper assesses the impact of environmental tax on income inequality at the global level, continental level, and on income levels. We used the Method of Moments quantile regression and found that globally, environmental tax policies can be used as policy strategies to reduce income inequality. A further analysis at the continental level shows that in Africa environmental tax is more effective in reducing income inequality in countries with medium inequalities, but in Asia in countries with higher levels of income inequality. In Europe, environmental taxes rather increase income inequalities, and in particular widen the inequalities in countries with smaller inequalities. A mixed result was found for America where for the countries with higher inequalities, the gap is reduced, but for those with smaller inequalities the gap is widened. A sub-analysis of the nexus based on income levels verifies that environmental tax indeed reduces income inequalities across all income levels.

1. Introduction

The effect of climate change on global inequality among countries has been recognized in the literature (Fremstad & Paul, Citation2020; Gmbh, Citation2014; Grottera & Olimpio, Citation2017; James et al., Citation2012; Joumard et al., Citation2012; Klenert et al., Citation2018; Kuo, Citation2021a; Markkanen & Anger-kraavi, Citation2019; Oueslati et al., Citation2017; Qiao & Dowell, Citation2022; Roberts, Citation2010; Säll, Citation2018; Shan et al., Citation2018; Wang et al., Citation2019; S. S. Zhao et al., Citation2022; Y. Zhao et al., Citation2021). This is on the backdrop of ravaging consequences climate change has exerted on countries, communities, businesses, economies, and individual lives, and even more worrying is the fact that global statistics project that given the current trend of events in emissions of greenhouse gases, by the end of this century the global temperature is projected to exceed 1.5°C, a historically alarming level (Zhao et al., Citation2021).

Furthermore, the latest World Inequality Report (2022) produced by the World Inequality Lab indicates that Global Inequality is more pronounced in view of the ravaging effects of the Covid-19 pandemic, which has exacerbated the inequality between the very rich and the rest of the population including the vulnerable(Antosiewicz et al., Citation2022). The startling statistics depict that the richest 10% of the global population currently take home 52% of the income whilst the poorest half of the global population earn just 8%. Also, in terms of wealth, half of the poorest global population owns just 2% of the total global wealth, while the 10% of the richest own 76% of all total global wealth (Chancel et al., Citation2022). A compelling fact that leads to the conclusions in the report that the challenges of the twenty-first century cannot be tackled well, without significant redistribution of wealth and income inequality.

Meanwhile, concerns have been raised in the literature about how potentially, policy options to deal with climate change by reducing greenhouse gas emissions can magnify the global inequalities among countries (Fremstad & Paul, Citation2020). Therefore, even though environmental tax policy has gained notoriety both in the literature and policy stands as the dominant policy instrument for reducing greenhouse gas emissions and economic growth and welfare, however, issues have been raised regarding the burden it can exert on the poor and vulnerable populations (Klenert et al., Citation2018; Patriarca & Vona, Citation2012; Säll, Citation2018). This study posits that on the strength of the double dividend effects of environmental tax policy, the revenues generated from these taxes can be redistributed and targeted towards interventions to ameliorate global inequality and other socioeconomic benefits (Antosiewicz et al., Citation2022; Peichl & Wissenschaftskolleg, Citation2017).

Despite the commendable efforts in the literature to unravel the nexus between environmental tax policy and Inequality theoretically, empirical studies remain scanty not only in the context of volumes and the estimation approaches but are focused on selected advanced countries, and a few emerging countries, community and, household levels to the neglect of the global or big picture effect, which is essential for measuring the overall effect of the collective and individual country’s concerted efforts in addressing this global cancer. These studies have also failed to account for the heterogeneous, distributional, and asymmetric incidence of environmental tax policies, and this partly explains the lack of clarity and consensus on interventions for the effective redistribution of revenues from environmental tax. Again, prior literature has failed to reveal if the environmental tax-inequality nexus varies across the groupings of countries per income levels and continents.

This study thus seeks to address these limitations in literature by examining the asymmetric impact of environmental tax on global inequality.

The study contributes to the literature in three folds. First, employing global panel data of 92 countries with the currency of data spanning 1994 to 2020 gives a more comprehensive insight into the big-picture effect using the global context. Second, the study breaks the global analysis into the various income levels and continents analysis. This provides insight into policy prescriptions and interventions to undertake in addressing the menace not only at the global but sub-global levels as well. Third, we provide empirical evidence by using the novel method of moments quantile regression, which is most appropriate for dealing with distributions and asymmetric effects of environmental tax—inequality nexus. We found that Income Inequality across the globe is sharply reduced by restrictive environmental tax policy, a finding that has ramifications for global sustainable development, particularly after recovering from the ravaging effects of Covid-19.

2. Literature Review

The call for more ambitious efforts toward achieving the below 2 °C global temperature targets set in the Paris Agreement is more deafening than ever before, and this comes in the wake of the latest emission gap report, which clearly depicts the insufficiency of the combined global mitigation pledges and efforts (Bruckner et al., Citation2022; Mor & Ghimire, Citation2022; UnitedNtions Environmental Programme, Citation2021). Consequently, several countries across the globe have continued to rally around the United Nations Framework Convention on Climate Change (UNFCCC) and proceeded to develop and entrench policies to mitigate greenhouse gas emissions.

An important consensus that has been achieved in the literature is the resounding acceptance of environmental tax as the most cost-effective policy prescription that addresses the mitigation of greenhouse gas emissions (UNFCCC, Citation2018). Indeed, the theoretical foundation for this position can be traced to mechanisms of the double dividend hypothesis, propounded by Pearce (Citation1991) in advancing the Pigouvian tax position, which posits that environmental taxes can be employed to yield two dividends, firstly, improve environmental quality by taxing pollutant behavior so as to increase the cost of pollution to the polluter, hence discourage the pollution behavior in order to shield the environment, which represents the green dividend. Secondly, revenues generated from environmental taxes can be redistributed using various strategies including tax cuts to shift the tax burden from labor tax (income tax), and capital (corporate tax) to environmentally degrading activities, directly paying lump-sum to vulnerable and poor populations, and so on, and this has the potential to yield increased employment and other welfare issues as well as economic growth. This makes up the second dividend titled the blue dividend. Goulder (Citation1995) further advanced the double dividend hypothesis into “weak” and “strong” dividends. The difference between the two dividends is represented by an environmental tax yielding cost savings to the economy being the “weak” dividend but when it yields no cost at all leading to welfare maximization, it represents the “strong” dividend.

Meanwhile, increasing global inequality is an urgent global issue as captured under the sustainable development goals 10, and particularly in the aftermath of Covid-19, inequality within and among countries have become a persistent cause for concern, this is against the backdrop of increased global unemployment, weaker health systems, increase in migrants and refugees, rising humanitarian crises, among others (Hoffmann et al., 2020; Vincens et al., 2018; Ratnawati, 2020; Darvas, 2019; Breunig and Majeed, 2020; Huang, 2019; Hu, 2021). These concerns are justified because of the rippling effect of inequality on health, quality of the environment, quality of education, human capital, economic growth, and ultimately human happiness. According to Aiyar and Ebeke, Citation2020, these disparities in opportunities continue to expand and could be passed on as a generational legacy.

The nexus between environmental tax and inequality is well acknowledged in literature (Caillavet et al.,Citation2019Citation2019; Chen, Citation2022; Antosiewicz et al., Citation2022; Dissou & Siddiqui, Citation2014a; Fremstad & Paul, Citation2020; Grottera & Olimpio, Citation2017; Joumard et al., Citation2012; Kuo, Citation2021b, Citation2021a; Mamoon & Murshed, Citation2013; Oueslati et al., Citation2017, Säll, Citation2018; Wang et al., Citation2019; Yan & Yang, Citation2021).

The empirical literature on the environmental tax-inequality nexus thus far has mainly focused on addressing the question of whether or not environmental tax policy prescriptions are progressive or regressive to deliver equitable welfare maximization, particularly taking account of the poor and vulnerable populations who conversely remain the most disproportionately affected directly by the ravaging effects of climate change and indirectly via environmental taxes even though scholarly evidence pontificate they are the least emitters (Althor et al., Citation2016; Burgess & Whitehead, Citation2020; Cuomo, Citation2011). Two strands of literature explain the regressive or progressive character of environmental taxes on inequality, depending on two channels, i.e., the commodity channel(use-side) and the income channel (source-side). The use-side channel views the distributional effects of environmental taxes on welfare from the standpoint that the taxes have incremental effects on the comparative prices of the goods and services, which are greenhouse gas emissions based and also represent the very commodities the vulnerable and the poor generally spend a chunk of their incomes on. Hence, the findings of this strand of studies normally depict environmental tax as being regressive because the poor and the vulnerable have their purchasing power or incomes disproportionately affected. For example, Fremstad and Paul (Citation2020) in an empirical study of the distributional effects of carbon pricing using the use-side approach and comprehensively considering the cost–benefit analysis of the effect show that the double dividend of carbon pricing is insufficient to protect the purchasing power of the majority of the American population, hence regressive. Similarly, S. Zhao et al. (Citation2022) also investigated the incidence of environmental tax in China, using a newly developed integrated assessment model revealed that environmental tax is regressive mainly due to price increases in food and energy goods. This is in tandem with the earlier evidence presented in Canada (Hamilton & Cameron, Citation1994); and in Denmark (Wier et al., Citation2005) as well as in the Netherlands (Kerkhof et al., Citation2008). It is also in sync with the current evidence revealed in Spain (Tomás et al., Citation2020) and in Germany (Hardadi et al., Citation2021).

A counterargument in the literature is premised on the source-side by Dissou & Siddiqui (Citation2014b) who argue that these industries that produce carbon and energy-intensive goods and services are mostly capital intensive and are funded by the rich or upper-income class, whose capitals are also burdened by the implementation of environmental taxes, thus progressive. Again, Yan and Yang (Citation2021), undertook a study to address the same research question using a comparative setting between rural and urban inequality and between varied income groups and concluded that the implementation of environmental taxes in China is progressive. In fact, a finding contrary to similar studies done in the same China. Chepeliev et al. (Citation2021) using a microsimulation model and taking account of policies in the Nationally Determined Contribution (NDC) depict that environmental taxes have been progressive at the global level mainly due to lower relative prices of food as compared to non-food commodities and also due to a reduction in the incomes of the rich or upper-income class.

Even though there is a surge in research interest on the distributional effect of environmental taxes on inequality, studies thus far have largely focused on micro-level analysis and have also been predominantly simulation-based backed by several assumptions, as well as country-specific (Bosquet, Citation2000; Cao et al., Citation2021; Devi & Gupta, Citation2019; Freire-González, Citation2018; Goulder, Citation1995; Kirchner et al., Citation2019; Kou et al., Citation2021; Labeaga et al., Citation2021; Maxim, Citation2020; Patuelli et al., Citation2005; Peng et al., Citation2019; Raza Abbasi et al., Citation2021; Roosen et al., Citation2022; Säll, Citation2018; Silva et al., Citation2021; Zhou et al., Citation2020). Many of the empirical studies have also used calibrated and stylized data, which can yield unrealistic results. Therefore, a macro-econometric analysis of the distributional effect of environmental taxes on inequality at the global and continental levels is a departure in the literature to entrench the theoretical analysis of the double-dividend hypothesis. This study, therefore, complements the stream of the literature by providing evidence at the global, continental, and cross-country macro-level econometric research.

3. Methodology

3.1. Data and Sources

This paper uses panel data on 92 countries across the globe to examine the effects of environmental taxes on global inequality. The period for the study spans from 1994 to 2020. The focus on the number of countries and the period of the study was strictly due to the availability of data on all variables, especially on environmental tax. The data on environmental tax is obtained from the OECD database (Bashir et al., Citation2021; Wolde-Rufael & Mulat-Weldemeskel, Citation2022a; Zahid et al., Citation2022). We gathered the income inequality data from the World Bank. The remaining variables, which represent the control variables, i.e., gross domestic product, trade, population density, and urbanization, were all gathered from the world development indicators of the World Bank in accordance with many (see, Abdullah & Morley, Citation2014; Khoso et al., Citation2021; Liya et al., Citation2021; Rahman & Alam, Citation2021).

3.2. Variables Definition

The Gini represents the main dependent variable for this study in line with the scan of the literature (Álvarez-verdejo et al., Citation2021; Candeira & Winter, Citation2021; Hardardottir & Erik, Citation2021). The environmental tax variable has also been used as the main independent variable. GDP, urbanization, trade, and globalization have been employed as control variables after a cursory scan of the literature (Khoso et al., Citation2021; Rahman & Alam, Citation2021; Wan et al., Citation2022; Abdullah & Morley, Citation2014; Liya et al., Citation2021; Immurana et al. Citation2020). See Table for the details of the variables, in terms of definitions, sources, and the expected signs.

Table 1. Variable description

3.3. Theoretical Framework and Model

Regarding the expected impact of environmental taxes on income inequality, the theory decomposes the impact as positive or negative depending on two channels. The first channel, which is the user-side (commodity) channel, is of the basic claim that an imposition or increase in environmental taxes increases the prices of these environmentally degrading commodities, the very commodities the vulnerable and poor usually spend a chunk of their incomes on because they relate to food, transportation, electricity, gas, and other basic requirements for survival. Therefore, these usually low-income earners are disproportionately affected by ceteris paribus. Making the environmental taxes regressive, hence, has negative effects, because it widens the income inequality gap. Studies that have confirmed this claim include Cao et al. (Citation2021), and Säll (Citation2018). The second channel, which is the source-side, also claim the production of these greenhouse gas emission commodities usually entail huge capital investments, which are naturally funded by the rich or high-income earners, thus environmental taxes place a strain on the capitals of the rich class, termed as progressive because it reduces income inequality as evidenced by some studies (see, McLaughlin et al., Citation2019; Nguyen & Song, Citation2021). Again, the other macroeconomic variables per theory can be negatively or positively depending on the effect accruing through the user-side or source-side. Economic growth, trade, population density, and urbanization are all expected to generate the active production and consumption of the pollutant goods and services, hence are expected to result in an asymmetric or non-linear effect. We also expect to have some tail dynamics in the relationship between the variables under investigation, because like many economic variables, the impact at early stages of implementation might differ across the various implementation paths.

On the strength of the above theoretical underpinning, even though the purpose of this study is to investigate the nexus between environmental tax and income inequality, hence entails two variables. However, modeling such a nexus demands a multivariate framework because income inequality can be determined by technical, economic, and social variables. Thus, there is a need to capture the key determinant variables in the model. Another reason for the addition of control variables in the model is to address the issue of omitted variable bias, which can lead to an invalid estimation result. This is also in sync with the studies of (Adebola et al., Citation2022; Adeleye et al., Citation2021; Anser et al., Citation2021; Mdaghri & Oubdi, Citation2022; Sun, Citation2022; Wolde-Rufael & Mulat-Weldemeskel, Citation2022a; Xie & Jamaani, Citation2022; Xin & Xie, Citation2022) which provide grounds for the inclusion of these control variables. We therefore employ the following basic model in our empirical analysis:

Thus, Inequality (Inequality) is expressed as a function of environmental tax (Tax) and a vector of control variables represented by M. Meanwhile, ɛ represents the disturbance term and i and t represent country and time, respectively. For the purpose of estimation, we re-specify EquationEq. 1(1)

(1) as follows:

where et is environmental tax, gdp is gross domestic product, trade is trade, popudense stands for population density and urb is urbanization. The intercept of the regression equation is represented by β0 and the coefficients of the explanatory variables are represented by β1− β5. Moreover, i (i = 1, 2 … 5) represents each country or panel member across the time frame of t (t = 1, 2 … 26). ɛ is the residual and is assumed to meet the classical criteria of independent as well as identically distributed with a zero mean as well as constant variance. Further, we employ logarithms (log) of variables in our regressions provided they do not have negative or zero values (thus, we do not take logarithms of environmental taxes and urbanization because they have negative values). The use of logarithms is to allow the data to be more normally distributed as well as dealing with differences in the measurement of variables (Bellemare & Wichman, Citation2020; Lütkepohl & Xu, Citation2012).

Moreover, the use of panel quantile regression to model the relationship in this study is to enable the researchers to examine and provide a deeper understanding of the determinants of inequality across the conditional distribution, particularly considering countries with the highest and least inequalities. For this reason, Koenker and Bassett (Citation1978) seminally introduced the quantile regression technique, which is a median-based regression analysis of the quantiles, a feature that is lacking in the traditional regression analysis, which are mean based, and may result in an inappropriate estimation of the relevant coefficients. Therefore, Equationequation (2)(2)

(2) can be rewritten as:

where i and t indicate the country and time, q indicates the quantile, 0 < q < 1, βk(q) represents the regression coefficient of quantile q, which varies with the change in q. The other variables are the same as above.

3.4. Econometric strategy

This segment describes the methodology employed in obtaining the empirical results for the model discussed above.

3.4.1. Diagnostic checks

Before estimating the relationship between the variables under consideration in this study, a few initial checks are conducted to ascertain the underlying features of the variables, this was done by initially checking the descriptive statistics and the correlation of the data. The study then began the diagnostic checks by testing the normality of the series using the Jarque & Bera (Citation1987) test. In the next step, this study conducted a test of slope homogeneity using the Pesaran & Yamagata (Citation2008) test, the results of which show both the statistics for Δ and Δ Adjusted. Moreover, mindful of the usage of trade and gross domestic product as factor variables that can spur interdependence between countries in the empirical investigation, the study uses the Peasaran (Citation2004) test to check for cross-sectional dependence. The essence of these diagnostic checks is to uncover any estimation issues necessary to determine the next appropriate steps to take regarding the estimation of the stationarity or unit root and cointegration and long-run relationship. This is ultimately a set of checks and balances to guard against biased or spurious results.

3.4.2. Unit root and Cointegration test

This study employs the Pesaran (Citation2014) cross-sectional augmented Im, Pesaran, and Shin (CIPS) method to test the stationarity of the series. The usefulness of this approach over the traditional approach has to do with its potential cross-sectional dependence and slope coefficients that are heterogeneous. Additionally, the Fisher augmented dickey-fuller was also used to assess the unit root.

Regarding cointegration, the error correction mechanism (ECM) cointegration approach by Westerlund (Citation2007) is used. As intimated earlier, because this test provides efficient results even with heterogeneous slope coefficients and cross-sectional dependence, it is very useful. This test consists of four statistics, two mean group statistics, and two panel statistics. For confirmatory reasons, the Kao cointegration is also estimated.

3.4.3. Method of moments quantile regression

To investigate the heterogeneous and distributional nexus between environmental tax and inequality, this study employs the recently developed and novel estimation technique of Method of Moments Quantile Regression (MMQR), credited to the works of Machado and Santos Silva (Citation2019). A model that can assist to appropriately capture the tail dynamics of the impact of environmental tax on the inequalities involved in a global sample that encapsulates both the “haves” and “haves not.” This is to ensure that the research question is addressed and the appropriate policy recommendations that will maximize welfare will be suggested.

The MMQR model addresses a number of limitations found in the traditional regression models (Ma, Citation2022; Sun & Razzaq, Citation2022; Wolde-Rufael & Mulat-Weldemeskel, Citation2022b). First, it provides accurate and vigorous results when the distribution of the dataset is non-parametric, contains outliers, minimal, or no correlation and non-normality of data. Secondly, the technique is able to determine the distributional and unique properties of several quantile values, therefore the problem of uneven distribution is appropriately addressed. Third, MMQR allows for the individual fixed effects across the conditional distribution, enabling the predictors to accommodate the location and scale functions (Alhassan et al., Citation2020). Again, MMQR is robust to discern the conditional heterogeneous covariance effects of GDP, Trade, Population density, urbanization, and environmental tax on income inequality, thus resolving the problem of unobserved heterogeneity. It also permits for not only a location-based asymmetry, because the parameters may depend on the position of the predicted variable, which is an income inequality, but also produces good estimates under diverse conditions, even if the model is non-linear. MMQR is described as a practice-based approach in view of its ability to simultaneously deal with heterogeneity and endogeneity via moment restrictions, hence, appeals to both asymmetric and non-linear estimations. A distinguishing factor of MMQR is its instinctiveness for handling non-crossing estimates, without giving invalid responses. In line with Machado and Santos Silva (Citation2019), for the conditional quantile of the random variable in the panel data for the location and scale is specified in Equationequation (3)(3)

(3) as follows:

where is the dependent variable,

is an i.i.d endogenous variable, (α, β,

, θ) are parameters to be assessed. The probability, P {

> 0} = 1.

is an i.i.d unobserved random variable distributed across individuals and is orthogonal to

satisfying the c, moment conditions (see, Ma, Citation2022; Sun, Citation2022). i = 1 … n, denotes the individual i fixed effects and N is a k-vector of known components of x (see, Adebola et al., Citation2022; Adeleye et al., Citation2021; Anser et al., Citation2021; Firpo et al., Citation2021; Ma, Citation2022; Mdaghri & Oubdi, Citation2022; Sun & Razzaq, Citation2022; Wolde-Rufael & Mulat-Weldemeskel, Citation2022b; Xie & Jamaani, Citation2022; Xin & Xie, Citation2022).

Again, is orthogonal to cross-sections (i) and time (t) in the expression as captured in Machado and Santos Silva (Citation2019). Thus, reserves and external variables stabilize. Hence, EquationEquation (1)

(1)

(1) , (Equation2

(2)

(2) ), and (Equation3

(3)

(3) ) might be rewritten as follows:

Where is the quantile distribution of the dependent variable (y), i.e., global inequality, which is dependent on the location of the independent variables

i.e., environmental tax, GDP, trade, population density, and urbanization and

is the fixed effects of an individual country, i.

≡ αi+

is the scalar coefficient, which shows the impact of the

th quantile on that of i (Ike et al., Citation2020), and

th sample quantiles, i.e.,, from 10th to the 90th quantiles (Mdaghri & Oubdi, Citation2022; Sun & Razzaq, Citation2022). N denotes a k-vector of known components of Nit, which is normalized to satisfy the Machado and Santos Silva (Citation2019) moment conditions E(U) = 0 and E(|U|) = 1 (see, Xie & Jamaani, Citation2022).

4. Results and Discussions

The empirical results gathered after the various tests of statistics and econometrics using Stata 17 are discussed in this section. The results of the descriptive statistics, correlation, normality checks, and the variance inflation factor (VIF) are shown in the first instance. Then, followed by the diagnostics checks, unit root testing, cointegration, results from MMQR, and robustness checks.

Table displays the descriptive statistics for the variables under study at the global, continental, and total population by `income levels.

Table 2. Descriptive Statistics

The results of the descriptive statistics show that the averages, minimum, maximum, and volatility of the various variables, particularly the averages of income inequality at the global level are recorded at (3.649), with America recording the highest averages of inequality continentally (3.875), and the upper middle-level countries per income levels also being the highest (3.84) among the rest. The results also show that globally, GDP is the most volatile among the variables, followed by population density and then environmental tax. Furthermore, Bulgaria, Bolivia, and Slovakia republic are the countries with the highest inequality (more than 4.0). India and Uganda also represent the countries with the highest environmental taxes.

In Table , the results first, show that the variables follow a non-normal or nonparametric distribution and hence will require a nonparametric econometric model. It is one of the considerations for selecting the MMQR as the main estimation model in the study.

Table 3. Normality, slope heterogeneity test, and cross-sectional dependence

Second, the results of the slope coefficient heterogeneity prove that the coefficients of the slope are heterogeneous, largely due to diversity in structures relative to tax, trade, and income as well as consumption patterns. Thirdly, the results of the cross-sectional dependence indicate the existence of cross-sectional dependence, which is expected since through trade, and globalization the economies of the world is expected to be intertwined. All the results are significant at traditional levels of 1%, 5%, and 10% each.

Table demonstrates the results of correlation analysis and is conducted to understand whether or not the variables are highly correlated, creating a multicollinearity issue.

Table 4. Pairwise correlations

Basically, the correlation matrix shows that all correlation coefficients do not exceed 0.8, clearly showing the absence of a serious multicollinearity problem. Again, the results of the Variance Inflation Factor (VIF) are also very low, all below the value 2 and certainly not up to the level that can cause multicollinearity. This is in consonance with prior studies that have employed VIF, such as Poursoleyman et al. (Citation2022).

Table , outlines the results of the unit root test, and this was carried out using the Pesaran Panel Unit Root Test with cross-sectional and first difference mean included in the estimates; however, for comparison purposes, the Fisher augmented Dickey–-Fuller type was also run to observe if any variation exists in the outcomes of the unit root test.

Table 5. Panel unit root

The results from the Pesaran test indicate that only inequality and trade are stationary at level but all variables are stationary at the first difference. The results from the Fisher ADF also show that all the variables are significant at level except economic growth and at the first difference, all variables are also significant except urbanization. The results verify that there is evidence of stationarity of all the variables used in the study at either level or first difference.

In Table , we then proceeded to check for the long-term cointegration among variables using the (Westerlund, Citation2007) test for panel cointegration.

Table 6. Cointegration test

The outcomes reported rejecting the null in the absence of cointegration in the favor of alternatives for the presence of long-term cointegrating relationships in both group and panel statistics among the factors under examination for both models. For comparison, the Koa test was also estimated. Both results demonstrate that long-term relationships are validated for the inequality (lini), environmental tax (et), gross domestic product(lgdp), trade (ltrade), population density (lpopudens), and urbanization (urb) in the study models.

Table depicts the results of MMQR estimation, where environmental taxes reduce global income inequality, and this generally demonstrates that in terms of the “big picture effect,” environmental tax is an effective strategy in reducing income inequality at the global level.

Table 7. MMQR results of environmental taxes on income inequality: Global level

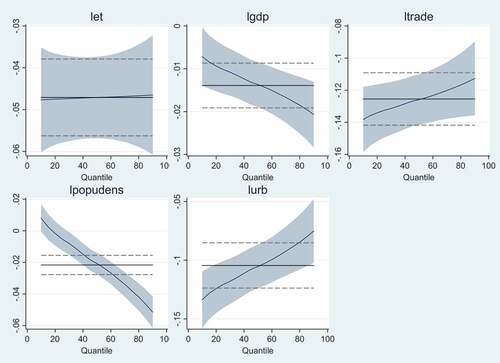

However, the results also show that this impact is significant across all quantiles. This is an indication that a more restrictive environmental tax policy results in a decline in global income inequality. Moreover, the magnitude of the coefficients is marginally larger at the smaller quantiles, and this suggests that countries with smaller magnitudes of income inequality (New Zealand and Slovenia) have a higher probability of experiencing a marginally bigger impact of environmental tax policies than countries with higher-income inequality (South Africa and Brazil). The above results are similar to the findings of Budolfson et al. (Citation2021) and Tirachini and Proost (Citation2021). The results further indicate that economic growth, trade, population density, and urbanization all have negative and significant effects on income inequality largely across all quantiles. This means that all these economic variables can narrow the gap in inequality especially. Population density impacts the inequality with very interesting tail dynamics, i.e., negative and significant at the early quantiles (1st and 2nd). The location parameters show that an increase in environmental taxes, trade, economic growth, population density, and urbanization can reduce the average global inequality. In terms of the scale parameters, all variables except economic growth and population density will decrease dispersions in the global inequality. Figure presents the graphical representation of the nexus as explained above.

Figure 1. Graphics of the impact of environmental taxes on income inequality: Global level.

Tables display the results of the environmental tax-inequality nexus at both the continental and income levels.

Table 8. MMQR results of environmental taxes on income inequality: High-income level

Table 9. MMQR results of environmental taxes on income inequality: Low-income level

Table 10. MMQR results of environmental taxes on income inequality: Upper middle-income level

Table 11. MMQR results of environmental taxes on income inequality: Lower middle-income level

Table 12. MMQR results of environmental taxes on income inequality: Africa

Table 13. MMQR results of environmental taxes on income inequality: Asia

Table 14. MMQR results of environmental taxes on income inequality: America

Table 15. MMQR results of environmental taxes on income inequality: Europe

Beginning with countries with a total population of high income levels in Table , the empirical findings suggest that environmental taxes reduce income inequality significantly in the small-to-medium quantiles (1st to 6th) but insignificant in the higher quantiles (7th to 9th), and this is similar to the findings from Oueslati et al. (Citation2017). Hence, these findings suggest that, environmental taxes significantly decrease inequalities only in high-income countries with smaller to medium-income inequalities, but countries with higher inequalities are not impacted significantly when tighter environmental taxes are rolled out. The magnitude of the coefficients also confirms the same. Trade and urbanization both impact inequality in high-income level countries negatively and significantly across all quantiles, but population density’s effect on inequalities is mixed, increasing the inequalities in countries with smaller inequalities (1st to 3rd) but reducing the inequalities in high-income level countries even though also negatively impact inequality but not significant. Economic growth in high-income countries rather widens the prevalent inequalities across all quantiles. The location parameters show that an increase in all the variables except economic growth can reduce the average global inequality. In terms of the scale parameters, all variables except population density and urbanization density will increase dispersions in the global inequality.

Table shows the results regarding low-income countries, where environmental taxes reduce inequalities but not significantly.

Countries with smaller inequalities per coefficient have a bigger probability of being affected. Both economic and trade also reduce inequalities in low-income countries but not significantly across all quantiles. Meanwhile, population density in a gradual manner positively impacts inequalities in low-income countries in a significant manner across all quantiles except 1st. Urbanization impacts inequalities in low-income countries negatively only within the smaller quantile regions but turns to impact positively from the medium to higher quantiles. The location parameters show that an increase in all the variables except population growth and urbanization can reduce the average global inequality. In terms of the scale parameters, all variables except trade will increase dispersions in the global inequality.

Table demonstrates the empirical results for the upper middle-income countries, these results show that the imposition of environmental taxes significantly reduces inequalities across all quantiles, per the coefficient is likely to have more impact in countries with smaller inequalities in this bracket.

Economic growth and population density, similarly reduce inequality across all quantiles. Trade impacts inequalities in these countries in both ways negatively (1st to 3rd quantiles) and positively (4th to 9th quantiles). Urbanization in this instance rather widens the inequality gap, with a bigger effect on countries with small inequalities in the upper middle-income level. The location parameters show that an increase in all the variables except trade and urbanization can reduce the average global inequality. In terms of the scale parameters, all variables except population density and urbanization will increase dispersions in the global inequality.

The results from Table show that environmental taxes reduce inequality at the lower middle-income level from across all quantiles but gradually, significantly only from the medium to higher quantiles.

Correspondingly, the likelihood of a bigger impact on countries with higher inequalities is huge as compared to countries with smaller inequalities. Further, the results show that while economic growth significantly increases inequalities across all quantiles, urbanization also increases the same but not significantly across all quantiles. The effect of population density on inequality varies from initially, insignificantly increasing it (1st and 2nd) then gradually reducing it (3rd to the 9th) but even from significantly increasing it from higher quantiles. The location parameters show that an increase in all the variables except economic growth and urbanization can reduce the average global inequality. In terms of the scale parameters, all variables except trade will decrease dispersions in the global inequality.

Table outlines the results of the relationship in the context of Africa.

The empirical evidence indicates that environmental taxes significantly reduce inequality across all quantiles but with reduced significance at the tail quantiles. Per the magnitude of the coefficient, African countries with higher inequalities are likely to suffer more severe effects. Economic growth and population density reduces inequalities in African countries across all quantiles. Trade significantly increases inequality in the early to medium quantiles, but the level of significance wanes towards the higher quantiles. Urbanization as usual has a mixed effect, significantly reducing inequality in earlier to medium quantiles to increasing the inequalities in higher quantiles in gradual significance. The location parameters show that an increase in all the variables except trade can reduce the average global inequality. In terms of the scale parameters, all variables except urbanization will decrease dispersions in the global inequality.

In Table , the empirical evidence regarding the Asian countries shows that environmental taxes reduce inequalities across all quantiles.

These findings are similar to the findings of Saelim (Citation2019). Economic growth and urbanization both similarly reduce inequality across all quantiles, but whilst the significance of the effect for economic growth is across all quantiles, in the case of urbanization it is insignificant across all quantiles. In Asian countries, trade and population density have gradually and significantly increased inequalities. The location parameters show that an increase in all the variables except trade and population density can reduce the average global inequality. In terms of the scale parameters, all variables except environmental tax and economic growth will increase dispersions in the global inequality.

Table , displays the results in the context of the American continent, and the empirical evidence depicts a mixed effect beginning with a significant increase in inequality up to the middle quantiles and then the significance reduces from the 6th to 7th quantiles, then begins to turn into a reducing inequality even though insignificant (Citation2020.

The result is consistent with the findings of American countries with smaller inequalities are likely to have severe effects. Trade and urbanization exhibit similar mixed effects with significant reduction in inequality in smaller quantiles, which gradually reduces significance and towards the tail begins to increase the inequalities. Economic growth also reduces inequalities across all quantiles but becomes significant from medium to higher quantiles. Population density significantly increases inequalities but at the tail end reduces in significance and turns into a negative effect. The location parameters show that an increase in all the variables except environmental taxes and population density can reduce the average global inequality. In terms of the scale parameters, all variables except trade and urbanization will decrease dispersions in the global inequality.

Table , shows the comparatively unique effect of environmental taxes on inequalities where the inequality gap widens with a more restrictive environmental tax policy.

Trade and urbanization, on the other hand, significantly reduce inequalities across all quantiles too. However, in a similar fashion to environmental taxes, economic growth, and population density increase inequality across all quantiles. The location parameters show that an increase in all the variables except trade and urbanization can increase the average global inequality. In terms of the scale parameters, all variables will increase dispersions in global inequality.

Overall, the results gathered in all the models estimated from the global, income level to continental levels have exhibited varied tail dynamics at both the higher and lower quantiles, confirmatory of the asymmetric character of environmental taxes and income inequality. Similarly, the other variables in the study, i.e., GDP, urbanization, population density, and trade, which are consistent with many economic variables, have also shown similar traits in the results of the estimated models. This is undoubtedly one of the justifications for the appropriateness of the model used.

Regarding Robustness analysis, Table encapsulates the results of a hierarchical regression of the nexus under consideration in this empirical investigation.

Table 16. Hierarchical Regression results for Environmental Tax and Global Income Inequality

These results are presented at the global, income and continental levels as conducted using the method of moments quantile regression. The results of this regression, as reported, are very similar to the signs of the coefficients obtained in the method of moments regression from Tables .

5. Conclusion and policy implications

5.1. Conclusions

The entire study is an analysis of the effect of environmental taxes on global inequality sub-analyzed into the country's income and continental levels. The study employed updated available data spanning from 1994 to 2020. A non-parametric panel econometric quantile regression is employed to address the objectives of the study. Prior to employing the non-parametric panel econometric quantile regression, preliminary diagnostic checks on the data were carried out. The tests conducted included a slope homogeneity test, a cross-sectional dependence test using Pesaran (Citation2015), a normality of series test using Shapiro–Wilk test, Westerlund (Citation2007) error correction cointegration, and unit root tests. The outcome of these tests encapsulates firstly, a non-normality of data, which is one of the considerations in choosing the non-parametric panel econometric quantile regression, secondly, the existence of cross-sectional dependence and the heterogeneity of the slope coefficients, thirdly, the stationarity of series found to be of mixed order, that is, I(0) and I(1) and confirmation of cointegration among the variables of the study. Furthermore, the method of moments quantile regression by Machado and Santos Silva (Citation2019) which is a non-parametric panel quantile regression approach was employed as the main estimation model. The main findings of the study show that environmental taxes represent a very good policy strategy to reduce global income inequality across all quantiles; therefore, a more restrictive environmental tax policy results in a decline in global income inequality. This is a finding that has ramifications for the “big picture effect”.

A decomposition of the global-level analysis based on income levels verifies that environmental taxes policy strategy will be a very good tool to reduce the menace of income inequality across all the countries with varied income levels from (high to low). Further, analysis of the results obtained implies that specific environmental tax policy interventions targeted at varied income levels will help achieve the global target of reducing inequality. The evidence in countries with high income levels shows that environmental tax policy is more effective when levied in high-income countries with smaller to medium inequalities compared to those with high inequalities. For low-income countries, moderate or less restrictive environmental tax policies should be crafted taking cognizance of the plight of the vulnerable and the poor. Regarding the upper middle-income group environmental tax policies can be cramping enough to derive the utmost significance needed to yield the required reduction in inequality. Lower middle-income countries per the empirical evidence should consider crafting environmental tax policies geared towards countries with medium to higher inequalities where the potency environmental taxes are significant.

A further sub-analysis on continental bases show that first, in Africa environmental taxes emphatically decrease inequalities but are possibly more effective in countries outside the extreme tails of income inequalities, because the level of impact for countries at the tails (smallest or highest inequalities) is not the same in significance. Therefore, environmental tax policy must be crafted to deal with the tail dynamics involved differently. Second, in Asia, the results indicate that environmental tax policies emphatically reduce the income inequalities among Asian countries but countries with higher inequality quantiles are likely to be the most affected. Third, the findings from the European evidence demonstrate that environmental taxes increase inequalities in Europe generally, but countries with smaller inequalities will likely suffer more in the widening of the gap. Fourth, the American experience presents mixed results in that, environmental taxes reduce inequality in American countries with a higher inequality gap but the American countries with smaller inequalities rather have the inequality gap further widened. Generally, the results gathered in all nine models estimated from the global to continental levels have exhibited varied tail dynamics at both the higher and lower quantiles, confirmatory of the asymmetric character of environmental taxes, and income inequality. The other variables in the study, i.e., GDP, urbanization, population density, and trade, which is consistent with many economic variables, have also shown similar traits in the results of the estimated models. This is undoubtedly one of the justifications for the appropriateness of the model used.

5.2. Policy Implications

The findings of this study have produced significant policy insights for all countries, especially within the context of global, income and continental levels. Firstly, all countries across the globe can in unison promote environmental taxes without compromising global inequality. Secondly, in view of the negative and significant coefficients found in the relationship between environmental taxes and inequality at the global level, a blueprint needs to be developed and implemented with a specific aim and a more concerted effort to increase environmental taxes, particularly for countries that are faced with high levels of inequality, in order to deal with the issues of inequality in a more frontal and holistic manner. In specifics, governments and policymakers must have this blueprint well-structured and streamlined to be part of the Nationally Developed Contributions for the reduction of greenhouse gas emissions. This would leapfrog the steps towards achieving sustainable development goal 10 and by extension the entire sustainable development goals, which are in line with the objectives of COP26. Practical roadmaps should also be agreed upon to promote global trade and urbanization but control global economic growth and population density as a means of ensuring that effective environmental tax policies are carved out to yield the needed reduction in global inequality.

Again, these results suggest that in order to draw environmental tax policy interventions that will achieve global equity, it is important to structure policy interventions from a global perspective by, for instance, developing global standards, which can then be customized to cater for the peculiarities of the various continents and other economic groupings.

In Africa, where the issues of inequalities are not only pronounced but have also been partly featured as one of the reasons for Africa’s under-development, it is no mean imperative for all the countries in Africa to consciously adopt and implement environmental tax policies and most importantly ensure African countries in the region of medium to high inequalities are targeted and made to double up their efforts as a way of resolving the issues of inequality taking cognizance of the African peculiar circumstances. This assertion is consistent with the findings of negative and significant coefficients from across all quantiles. Additionally, many African countries are import dependent and have become destinations for dumping carbon-intensive goods and services. One important tool to restrict and discourage the transactions of these carbon-intensive goods and services is to put restrictive environmental taxes on them, whilst also rolling out policies to reduce densely populated areas, and restrictive environmental taxes. Even more crucial, because Africa has the lowest average environmental taxes (1.40%)

In Europe, where evidence of positive and significant coefficients has been revealed, about the effects of environmental taxes on inequality, this is largely due to the fact that Europe already charges the highest environmental taxes (1.99%) globally, and also the continent with the lowest inequality (3.48 index). Thus, a concerted effort across Europe can be encouraged to explore a wide range of other effective environmental policy interventions apart from taxes via the promotion of economic growth and urbanization, especially making it more restrictive towards countries with higher inequalities. Measures should also be put in place to discourage population density.

The American experience of the nexus between environmental tax and inequality even though it is not progressive for countries with small-to-medium inequality, but environmental tax policies targeted at American countries with higher brackets of inequality could reduce inequality, hence make it progressive. However, policymakers should be circumspect in taxing countries within smaller to medium inequality brackets because that has the potential of widening the gap of inequalities among the same countries. Indeed, America has the highest inequality (3.87 index) globally. Similar to Europe, American countries should develop policies aimed at discouraging densely populated localities in the drive to implement environmental taxes, since that would facilitate addressing inequalities.

The Asian continent will require peculiar neutral policy intervention from the perspective of environmental taxes, where it will require just more than the taxes but other policy developments to boast urbanization in all Asian countries. Alternatively, the proportion of increment in the inequality gap could be targeted and neutralized by recycling the revenues from the taxes to incrementally and proportionally reduce the inequality gap. Trade policy interventions should also be encouraged in the Asian smaller and medium range of countries with inequalities. Pragmatic steps should also be taken to curb population density and slow the pace of economic growth by applying environmental taxes in this direction. The main reason why Asian countries must still embrace and continue to contribute to the global efforts is to support the needed signaling effect in the environment

5.3. Limitations and future recommendations

Future studies should address two key limitations of this study. This study employed a global, income level and continental samples. However, a comparative study of developed and developing countries or countries under sub-regional blocks would be an interesting investigation. Again, the effect of gender on the nexus between environmental tax and inequality would bring more flavor to the empirical evidence thus far.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Osman Babamu Halidu

Osman Babamu Halidu is a Senior Lecturer at the department of Accounting and Accounting Information Systems at the Kumasi Technical University. He is a former Head of department and has gained a wealth of industrial experience in the field of Accounting and Finance. Osman’s research interest include Tax policy, Accounting standards, and financial inclusion and performance.

References

- Abdullah, S., & Morley, B. (2014). Environmental taxes and economic growth: Evidence from panel causality tests. Energy Economics, 42, 27–35. https://doi.org/10.1016/j.eneco.2013.11.013

- Adebola, S., Opeyemi, M., & Kumar, A. (2022). Heliyon The impact of technological innovation on renewable energy production: Accounting for the roles of economic and environmental factors using a method of moments quantile regression. Heliyon, 8(March), e09913. https://doi.org/10.1016/j.heliyon.2022.e09913

- Adeleye, B. N., Id, R. O., Lawal, A. I., & Alwis, T. D. (2021). Energy use and the role of per capita income on carbon emissions in African countries. PLoS one, 1–17. https://doi.org/10.1371/journal.pone.0259488

- Aiyar, S., & Ebeke, C. (2020). Inequality of opportunity, inequality of income and economic growth. World Development, 136, 105115.

- Alhassan, A., Usman, O., Ike, G. N., & Sarkodie, S. A. (2020). Impact assessment of trade on environmental performance: Accounting for the role of government integrity and economic development in 79 countries. Heliyon, 6(9), e05046. https://doi.org/10.1016/j.heliyon.2020.e05046

- Althor, G., Watson, J. E. M., & Fuller, R. A. (2016). Global mismatch between greenhouse gas emissions and the burden of climate change. Nature Publishing Group, 1–6. https://doi.org/10.1038/srep20281

- Álvarez-verdejo, E., Moya-fernández, P. J., & Muñoz-rosas, J. F. (2021). Single Imputation Methods and Confidence Intervals for the Gini Index. Mathematics, 9(24), 3252.

- Anser, M. K., Adeleye, B. N., & Tabash, M. I. (2021). Current Issues in Tourism Services trade – ICT – Tourism nexus in selected Asian countries: New evidence from panel data techniques. Current Issues in Tourism, 1(1), 1–16. https://doi.org/10.1080/13683500.2021.1965554

- Antosiewicz, M., Fuentes, J. R., Lewandowski, P., & Witajewski-baltvilks, J. (2022). Distributional effects of emission pricing in a carbon-intensive economy. Energy Policy, 160(July2020), 112678.

- Bashir, M. F., MA, B., Shahbaz, M., Shahzad, U., & Vo, X. V. (2021). Unveiling the heterogeneous impacts of environmental taxes on energy consumption and energy intensity: Empirical evidence from OECD countries. Energy, 226, 120366. https://doi.org/10.1016/j.energy.2021.120366

- Bellemare, M. F., & Wichman, C. J. (2020). Elasticities and the Inverse Hyperbolic Sine Transformation. Oxford Bulletin of Economics and Statistics, 82(1), 50–61. https://doi.org/10.1111/obes.12325

- Bosquet, B. (2000). Environmental tax reform: Does it work? A survey of the empirical evidence. Ecological Economics, 34(1), 19–32. https://doi.org/10.1016/S0921-8009(00)00173-7

- Bruckner, B., Hubacek, K., Shan, Y., Zhong, H., & Feng, K. (2022). Impacts of poverty alleviation on national and global carbon emissions. Nature Sustainability, 5(4), 311–320. https://doi.org/10.1038/s41893-021-00842-z

- Budolfson, M., Dennig, F., Errickson, F., Feindt, S., Ferranna, M., Fleurbaey, M., Klenert, D., Kornek, U., Kuruc, K., Méjean, A., Peng, W., Scovronick, N., Spears, D., Wagner, F., & Zuber, S. (2021). Protecting the poor with a carbon tax and equal per capita dividend. Nature Climate Change, 11(12), 1025–1026. https://doi.org/10.1038/s41558-021-01228-x

- Burgess, M., & Whitehead, M. (2020). Just transitions, poverty and energy consumption: Personal carbon accounts and households in poverty. Energies, 13(22), 22. https://doi.org/10.3390/en13225953

- Caillavet, F., Fadhuile, A., & Nichèle, V. (2019). Assessing the distributional effects of carbon taxes on food: Inequalities and nutritional insights in France. Ecological Economics, 163, 20–31.

- Candeira, S., & Winter, F. (2021). Relationship between income inequality, socioeconomic development, vulnerability index, and maternal mortality in Brazil, 2017. BMC public health, 21(1), 1–8.

- Cao, J., Dai, H., Li, S., Guo, C., Ho, M., Cai, W., He, J., Huang, H., Li, J., Liu, Y., Qian, H., Wang, C., Wu, L., & Zhang, X. (2021). The general equilibrium impacts of carbon tax policy in China: A multi-model comparison. Energy Economics, 99, 105284. https://doi.org/10.1016/j.eneco.2021.105284

- Chancel, L. (2022). Global carbon inequality over 1990. https://doi.org/10.1038/s41893-022-00955-z.

- Chen, S. (2022). The inequality impacts of the carbon tax in China. Humanities and Social Sciences Communications, 9(1), 1–10. https://doi.org/10.1057/s41599-022-01285-3

- Chepeliev, M., Osorio-rodarte, I., & Van Der, M. D. (2021). Distributional impacts of carbon pricing policies under the Paris Agreement: Inter and intra-regional perspectives. Energy Economics, 102(December2020), 105530. https://doi.org/10.1016/j.eneco.2021.105530

- Cuomo, C. J. (2011). Climate change, Vulnerability, and responsibility. Hypatia, 26(4), 690–714. https://doi.org/10.1111/j.1527-2001.2011.01220.x

- Devi, S., & Gupta, N. (2019). Effects of inclusion of delay in the imposition of environmental tax on the emission of greenhouse gases. Chaos, Solitons, and Fractals, 125, 41–53. https://doi.org/10.1016/j.chaos.2019.05.006

- Dissou, Y., & Siddiqui, M. S. (2014a). Can carbon taxes be progressive? ☆. Energy Economics, 42, 88–100. https://doi.org/10.1016/j.eneco.2013.11.010

- Dissou, Y., & Siddiqui, M. S. (2014b). Can carbon taxes be progressive? Energy Economics, 42, 88–100. https://doi.org/10.1016/j.eneco.2013.11.010

- Firpo, S., Galvao, A. F., Pinto, C., & Poirier, A. (2021). GMM quantile regression. Journal of Econometrics, Xxxx. https://doi.org/10.1016/j.jeconom.2020.11.014

- Freire-González, J. (2018). Environmental taxation and the double dividend hypothesis in CGE modelling literature: A critical review. Journal of Policy Modeling, 40(1), 194–223. https://doi.org/10.1016/j.jpolmod.2017.11.002

- Fremstad, A., & Paul, M. (2020). The Impact of a Carbon Tax on Inequality. Ecological Economics, 163(July2018), 88–97. https://doi.org/10.1016/j.ecolecon.2019.04.016

- Gmbh, M. S. (2014). Environmental Taxation and Redistribution Concerns Author (s): Rafael Aigner Source: FinanzArchiv/Public Finance Analysis, June 2014, Vol. 70, No. 2 (June 2014), Published by: Mohr Siebeck GmbH & Co. KG Stable URL. 70(2), 249–277. https://doi.org/10.1628/001522114X681379

- Goulder, L. H. (1995). Environmental Taxation and the Double Dividend. International Tax and Public Finance, 183(2), 157–183. https://doi.org/10.1007/BF00877495

- Grottera, C., & Olimpio, A. (2017). Impacts of carbon pricing on income inequality in Brazil. Climate and Development, 9(1), 80–93. https://doi.org/10.1080/17565529.2015.1067183

- Hamilton, K., & Cameron, G. (1994). Simulating the Distributional effects of a Canadian carbon tax. Canadian Public Policy/Analyse de Politiques, 20(4), 385–399.

- Hardadi, G., Buchholz, A., & Pauliuk, S. (2021). Implications of the distribution of German household environmental footprints across income groups for integrating environmental and social policy design. Journal of Industrial Ecology, 25(1), 95–113. https://doi.org/10.1111/jiec.13045

- Hardardottir, H., & Erik, U. G. (2021). Parameterizing standard measures of income and health inequality using choice experiments. September, 2020, 2531–2546. https://doi.org/10.1002/hec.4395

- Hashem Pesaran, M., & Yamagata, T. (2008). Testing slope homogeneity in large panels. Journal of Econometrics, 142(1), 50–93. https://doi.org/10.1016/j.jeconom.2007.05.010

- Ike, G. N., Usman, O., & Asumadu, S. (2020). Science of the Total Environment Fiscal policy and CO 2 emissions from heterogeneous fuel sources in Thailand : Evidence from multiple structural breaks cointegration test. The Science of the Total Environment, 702, 134711. https://doi.org/10.1016/j.scitotenv.2019.134711

- Immurana, M., Aziz, A., Micheal, I., & Boachie, K. (2020). Does taxation on harmful products influence population health ? Evidence from Africa using the dynamic panel system GMM approach. Quality & Quantity, 0123456789. https://doi.org/10.1007/s11135-020-01043-0

- James, M. R., & Robson, S. (2012). Straightforward reconstruction of 3D surfaces and topography with a camera: Accuracy and geoscience application. Journal of Geophysical Research: Earth Surface, 117(F3).

- Jarque, C. M., & Bera, A. K. (1987). A Test for Normality of Observations and Regression Residuals. International Statistical Review / Revue Internationale de Statistique, 55(2), 163. https://doi.org/10.2307/1403192

- Joumard, I., Pisu, M., & Bloch, D. (2012). Tackling income inequality The role of taxes and transfers.

- Kerkhof, A. C., Moll, H. C., Drissen, E., & Wilting, H. C. (2008). Taxation of multiple greenhouse gases and the effects on income distribution. A case study of the Netherlands. Ecological Economics, 67(2), 318–326. https://doi.org/10.1016/j.ecolecon.2007.12.015

- Khoso, N., Rajput, S., Aziz, T., Hussain, A., & Jahanzeb, A. (2021). Trade Openness and Income Inequality: Fresh Evidence Based on Different Inequality Measures. Applied Economics Journal, 28(2), 63–81. https://so01.tci-thaijo.org/index.php/AEJ/article/view/245051

- Kirchner, M., Sommer, M., Kratena, K., Kletzan-slamanig, D., & Kettner-marx, C. (2019). CO2 taxes, equity and the double dividend – Macroeconomic model simulations for Austria. Energy Policy, 126(April2018), 295–314. https://doi.org/10.1016/j.enpol.2018.11.030

- Klenert, D., Schwerhoff, G., Edenhofer, O., & Mattauch, L. (2018). Environmental Taxation, Inequality and Engel’s Law: The Double Dividend of Redistribution. Environmental and Resource Economics, 71(3), 605–624. https://doi.org/10.1007/s10640-016-0070-y

- Koenker, R., & Bassett, G., Jr. (1978). Regression quantiles. Econometrica: Journal of the Econometric Society, 46(1), 33–50. https://www.Jstor.org/stable/1913643

- Kou, P., Han, Y., & Li, Y. (2021). An evolutionary analysis of corruption in the process of collecting environmental tax in China. Environmental Science and Pollution Research, 28(39), 54852–54862. https://doi.org/10.1007/s11356-021-13104-4

- Kuo, K. H. (2021a). The impact of environmental policy on wage inequality. International Journal of Economic Theory, 18, 1–14. https://doi.org/10.1111/ijet.12327

- Kuo, K. H. (2021b). The impact of environmental policy on wage inequality. International Journal of Economic Theory, 1–14. https://doi.org/10.1111/ijet.12327

- Labeaga, J. M., Labandeira, X., & López-Otero, X. (2021). Energy taxation, subsidy removal and poverty in Mexico. Environment and Development Economics, 26(3), 239–260. https://doi.org/10.1017/S1355770X20000364

- Liya, A., Qin, Q., Kamran, H. W., Sawangchai, A., Wisetsri, W., & Raza, M. (2021). How macroeconomic indicators influence gold price management. Business Process Management Journal, 27(7), 2075–2087. https://doi.org/10.1108/BPMJ-12-2020-0579

- Lütkepohl, H., & Xu, F. (2012). The role of the log transformation in forecasting economic variables. Empirical Economics, 42(3), 619–638. https://doi.org/10.1007/s00181-010-0440-1

- Ma, Q. (2022). On the sustainable trade development: Do Financial inclusion and eco-innovation matter? Evidence from method of moments quantile regression. Sustainable Development, 1960(January), 1–12. https://doi.org/10.1002/sd.2298

- Machado, J. A. F., & Santos Silva, J. M. C. (2019). Quantiles via moments. Journal of Econometrics, 213(1), 145–173. https://doi.org/10.1016/j.jeconom.2019.04.009

- Mamoon, D., & Murshed, S. M. (2013). Education bias of trade liberalization and wage inequality in developing countries. The Journal of International Trade & Economic Development, 8199. https://doi.org/10.1080/09638199.2011.589532

- Markkanen, S., & Anger-kraavi, A. (2019). Social impacts of climate change mitigation policies and their implications for inequality. Climate Policy, 3062. https://doi.org/10.1080/14693062.2019.1596873

- Maxim, M. R. (2020). Environmental fiscal reform and the possibility of triple dividend in European and non-European countries: Evidence from a meta-regression analysis. Environmental Economics and Policy Studies, 22(4), 633–656. https://doi.org/10.1007/s10018-020-00273-8

- McLaughlin, C., Elamer, A. A., Glen, T., AlHares, A., & Gaber, H. R. (2019). Accounting society’s acceptability of carbon taxes: Expectations and reality. Energy Policy, 131(December2018), 302–311. https://doi.org/10.1016/j.enpol.2019.05.008

- Mdaghri, A. A., & Oubdi, L. (2022). Bank-Specific and Macroeconomic Determinants of Bank Liquidity Creation: Evidence from MENA Countries. Journal of Central Banking Theory and Practice, 76(6), 55–76. https://doi.org/10.2478/jcbtp-2022-0013

- Mor, S., & Ghimire, M. (2022). Transparency and Nationally Determined Contributions: A Review of the Paris Agreement. Interdisciplinary Journal of Economics and Business Law, 11(2), 106–119.

- Nguyen, T. T. H., & song, W. (2021). Carbon Pricing and Income Inequality: An Empirical Investigation. Journal of Economic Development, 46(2), 155–182.

- Oueslati, W., Zipperer, V., Rousselière, D., & Dimitropoulos, A. (2017). Energy taxes, reforms and income inequality: An empirical cross- country analysis. International Economics, 150(January), 80–95. https://doi.org/10.1016/j.inteco.2017.01.002

- Patriarca, F., & Vona, F. (2012). Environmental Taxes, Inequality and Technical Change Environmental Taxes, Inequality and Technical Change. Revue de l’OFCE, 11. https://doi.org/10.3917/reof.124.0389

- Patuelli, R., Nijkamp, P., & Pels, E. (2005). Environmental tax reform and the double dividend: A meta-analytical performance assessment. Ecological Economics, 55(4), 564–583. https://doi.org/10.1016/j.ecolecon.2004.12.021

- Pearce, D. (1991). The Role of Carbon Taxes in Adjusting to Global Warming Author (s): David Pearce Published by: Wiley on behalf of the Royal Economic Society Stable URL. The Economic Journal. 938–948. http://www.jstor.org/stable/2233865

- Peichl, A., & Wissenschaftskolleg, H. (2017). SHIFTING TAXES FROM LABOR TO CONSUMPTION: MORE EMPLOYMENT AND MORE INEQUALITY? by N ico P estel. Review of Income and Wealth, 63(3), 542–563. https://doi.org/10.1111/roiw.12232

- Peng, J. T., Wang, Y., Zhang, X., He, Y., Taketani, M., Shi, R., & Zhu, X. D. (2019). Economic and welfare influences of an energy excise tax in Jiangsu province of China: A computable general equilibrium approach. Journal of Cleaner Production, 211, 1403–1411. https://doi.org/10.1016/j.jclepro.2018.11.267

- Pesaran, M. H. (2004). General Diagnostic Tests for Cross Section Dependence in Panels.

- Pesaran, M. H. (2014). Information in the yield curve: A Macro‐Finance approach. Journal of Applied Econometrics, 21(August 2012), 1–21. https://doi.org/10.1002/jae

- Pesaran, M. H. (2015). Testing Weak Cross-Sectional Dependence in Large Panels Testing Weak Cross-Sectional Dependence in Large Panels (pp. 4938). https://doi.org/10.1080/07474938.2014.956623

- Poursoleyman, E., Mansourfar, G., Homayoun, S., & Rezaee, Z. (2022). Business sustainability performance and corporate financial performance: The mediating role of optimal investment. Managerial Finance, 48(2), 348–369. https://doi.org/10.1108/MF-01-2021-0040

- Qiao, K., & Dowell, G. (2022). Environmental concerns, income inequality, and purchase of environmentally-friendly products: A longitudinal study of U. S. counties. Research Policy, 51(4), 104443. https://doi.org/10.1016/j.respol.2021.104443

- Rahman, M. M., & Alam, K. (2021). Clean energy, population density, urbanization and environmental pollution nexus: Evidence from Bangladesh. Renewable Energy, 172, 1063–1072. https://doi.org/10.1016/j.renene.2021.03.103

- Raza Abbasi, K., Shahbaz, M., Jiao, Z., & Tufail, M. (2021). How energy consumption, industrial growth, urbanization, and CO 2 emissions affect economic growth in Pakistan? A novel dynamic ARDL simulations approach. Energy, 221. https://doi.org/10.1016/j.energy.2021.119793

- Roberts, J. T. (2010). Global Inequality and Climate Change. Society & Natural Resources, 1920(2001). https://doi.org/10.1080/08941920118490

- Roosen, J., Staudigel, M., & Rahbauer, S. (2022). Demand elasticities for fresh meat and welfare effects of meat taxes in Germany. Food Policy, 106(December2021), 102194. https://doi.org/10.1016/j.foodpol.2021.102194

- Saelim, S. (2019). Carbon tax incidence on household demand: Effects on welfare, income inequality and poverty incidence in Thailand. Journal of Cleaner Production, 234, 521–533. https://doi.org/10.1016/j.jclepro.2019.06.218

- Säll, S. (2018). Environmental food taxes and inequalities: Simulation of a meat tax in Sweden. Food Policy, 74(June2017), 147–153. https://doi.org/10.1016/j.foodpol.2017.12.007

- Shan, M., Chao, C., Liu, X., & Yu, E. S. H. (2018). Environmental policy, firm dynamics and wage inequality in developing countries. International Review of Economics and Finance, 57(February), 70–85. https://doi.org/10.1016/j.iref.2018.02.013

- Silva, S., Soares, I., & Afonso, O. (2021). Assessing the double dividend of a third-generation environmental tax reform with resource substitution. Environment, Development and Sustainability, 23(10), 15145–15156. https://doi.org/10.1007/s10668-021-01290-7

- Sun, Y. (2022). Composite fiscal decentralisation and green innovation: Imperative strategy for institutional reforms and sustainable development in OECD countries. Sustainable Development, 1–14. https://doi.org/10.1002/sd.2292

- Sun, Y., & Razzaq, A. (2022). Composite fiscal decentralisation and green innovation: Imperative strategy for institutional reforms and sustainable development in OECD countries. Sustainable Development, 2021, 1–14. https://doi.org/10.1002/sd.2292

- Tirachini, A., & Proost, S. (2021). Economics of Transportation Transport taxes and subsidies in developing countries: The effect of income inequality aversion. Economics of Transportation, 25(June2020), 100206. https://doi.org/10.1016/j.ecotra.2021.100206

- Tomás, M., López, L. A., & Monsalve, F. (2020). Carbon footprint, municipality size and rurality in Spain: Inequality and carbon taxation. Journal of Cleaner Production, 266, 121798. https://doi.org/10.1016/j.jclepro.2020.121798

- UNFCCC. (2018). Climate Action Now. Climate Action Now: Summary for Policymakers 2018.

- UnitedNtions Environmental Programme. (2021). Making Peace with Nature. https://doi.org/10.18356/9789280738377

- Wang, J., Lin, J., Feng, K., Liu, P., Du, M., Ni, R., Chen, L., Kong, H., Weng, H., Liu, M., Baiocchi, G., Zhao, Y., Mi, Z., Cao, J., & Hubacek, K. (2019). Environmental taxation and regional inequality in China. Science Bulletin, 64(22), 1691–1699. https://doi.org/10.1016/j.scib.2019.09.017

- Wan, G., Zhang, X., & Zhao, M. (2022). Urbanization can help reduce income inequality. Npj Urban Sustainability, 2(1), 1–8. https://doi.org/10.1038/s42949-021-00040-y

- Westerlund, J. (2007). Testing for error correction in panel data. Oxford Bulletin of Economics and Statistics, 69(6), 709–748. https://doi.org/10.1111/j.1468-0084.2007.00477.x

- Wier, M., Birr-Pedersen, K., Jacobsen, H. K., & Klok, J. (2005). Are CO2 taxes regressive? Evidence from the Danish experience. Ecological Economics, 52(2), 239–251. https://doi.org/10.1016/j.ecolecon.2004.08.005

- Wolde-Rufael, Y., & Mulat-Weldemeskel, E. (2022a). The moderating role of environmental tax and renewable energy in CO2 emissions in Latin America and Caribbean countries: Evidence from method of moments quantile regression. Environmental Challenges, 6, 100412. https://doi.org/10.1016/j.envc.2021.100412

- Wolde-Rufael, Y., & Mulat-Weldemeskel, E. (2022b). The moderating role of environmental tax and renewable energy in CO2 emissions in Latin America and Caribbean countries: Evidence from method of moments quantile regression. Environmental Challenges, 6, 100412. https://doi.org/10.1016/j.envc.2021.100412

- Xie, P., & Jamaani, F. (2022). Does Green Innovation, Energy Productivity and Environmental Taxes Limit Carbon Emissions in Developed economies: Implications for Sustainable development. Structural Change and Economic Dynamics, September, 63, 66–78. https://doi.org/10.1016/j.strueco.2022.09.002

- Xin, N., & Xie, Z. (2022). Financial inclusion and trade adjusted carbon emissions: Evaluating the role of environment related taxes employing non-parametric panel methods. Sustainable Development, 1–13. https://doi.org/10.1002/sd.2375

- Yan, J., & Yang, J. (2021). Carbon pricing and income inequality: A case study of Guangdong. Journal of Cleaner Production, 296, 126491. https://doi.org/10.1016/j.jclepro.2021.126491

- Zahid, M., Fareed, Z., Ferraz, D., & Ikram, M. (2022). Exploring the heterogenous impacts of environmental taxes on environmental footprints: An empirical assessment from developed economies. Energy, 238. https://doi.org/10.1016/j.energy.2021.121753

- Zhao, Y., Chen, Y., Wang, C., & Cai, W. (2021). Recycling Carbon Pricing Revenue and the Effects on Income Inequality and Regional Disparity. A CGE-based Study of China, 20, 1–5.

- Zhao, S., Fujimori, S., Hasegawa, T., Oshiro, K., & Sasaki, K. (2022). Poverty and inequality implications of carbon pricing under the long ‑ term climate target. Sustainability Science, 0123456789. https://doi.org/10.1007/s11625-022-01206-y

- Zhao, Y., Wang, C., & Cai, W. (2022). Resources, Conservation & Recycling Carbon pricing policy, revenue recycling schemes, and income inequality: A multi-regional dynamic CGE assessment for China. Resources, Conservation & Recycling, 181, 106246. https://doi.org/10.1016/j.resconrec.2022.106246

- Zhou, Z., Zhang, W., Pan, X., Hu, J., & Pu, G. (2020). Environmental tax reform and the “double dividend” hypothesis in a small open economy. International Journal of Environmental Research and Public Health, 17(1). https://doi.org/10.3390/ijerph17010217