Abstract

Though the Corporate Governance concept has gained paramount interest due to the spate of corporate scandals, there is a void in the literature in terms of a summary overview of corporate governance in the Indian context. The present study aims to provide a state-of-the-art summary of corporate governance in India. To do so, the study employs a bibliometric analysis with a systematic literature review approach with extensive use of Bibliometric R Packages and VOSViewer software. To this end, the study reviews a total of 344 articles published in the Scopus database between 2004 and 2022. Akin to this, the review performs performance analysis, science mapping, and network analysis. The findings show an increasing trend in publications since 2004 till date with an annual growth rate of 23.99%. The network analysis results delineate earnings management, gender diversity, ownership structure, board structure, board size, corporate governance, ownership, and firm performance as major research themes in this field. This study is the primary attempt to show the growth and evolution of CG research in India. Thus, the review contributes to the existing literature on CG at the country level and provides scope for further research. Also, the study findings help policymakers, academicians, and regulators to strengthen corporate governance practices in the country.

The growing number of corporate failures such as corporate scams, accounting frauds, abuse of corporate power, and many more have led the corporate world to introduce a suitable controlling mechanism. To this end, the concept of corporate governance has emerged across the globe. Accordingly, it established necessary controlling mechanisms with several attributes for their early adoption in and around the world. The growing corporate frauds particularly in developing countries necessitated all firms to adhere the CG practices. Since then, many scholars started to delve into this arena. Although there exist different strands of literature on CG in India, a summary overview of this field is scant. This present study provides an overview of CG research in the Indian context by delineating the current status and future directions to enhance this domain as interesting to all stakeholders.

1. Introduction

Corporate Governance (CG) is a pool of various policies, and practices which serve as a basic norm for all companies for their effective controlling mechanisms. The CG is defined as the process and structures by which a corporation is controlled and governed (Handa, Citation2018) with high legitimacy, accountability, and competence in policy strategy(Al-ahdal et al., Citation2020). It has gained prominence in both developed as well as developing nations due to major corporate scandals. The various corporate failures such as Enron, WorldCom led the companies to give more focus on CG practices (Rajab & Handley-Schachler, Citation2009). Further, the Global Financial crisis also stressed the importance of CG (Saggar & Singh, Citation2017). (Antwi et al., Citation2021) opined that CG became the main topic of interest due to multiple corporate failures. Hence, it resulted in the introduction of various policies at the country level. In turn, the act of Sarbanes–Oxley (or SOX Act) of 2002 in USA was introduced to respond the Enron’s failure to safeguard the investor’s interest. Further, Smith Report (2003) and the Higgs Report (2003), were also introduced to strengthen the corporate’s capability as against Enron’s failure. In addition, the OECD has come up with new CG (1999 and 2004) principles as major guidelines to strengthen CG practices (Zheng & Kouwenberg, Citation2019), particularly in emerging countries.

The concept of CG has become vital particularly for developing countries due to the fact of weaker governance structure. Hence, there requires a strong CG structure with high transparency, and managerial excellence to ameliorate corporate malpractices with the main intention to attract foreign investors (Al-ahdal et al., Citation2020). In India, the phenomena of CG emerged aftermath of fraudulent practices like “Big bull”, “Harshad Mehta’s scam”, and “Satyam Computers”. The country is evidenced for poor corporate management in terms of internal control, ignorance of core business, and many more (N. N. Arora & Singh, Citation2020). Accordingly, the Confederation of Indian Industry (CII) was introduced in India which laid down certain CG codes of conduct followed by the Ramakrishna Commission on Public Sector Undertakings (PSU’s) CG which was further focused on a good CG practice (Al-Homaidi et al., Citation2021). In 2000, based on the “Birla Committee recommendation” SEBI, the major capital market regulators accepted the inclusion of a new clause. The CG guidance was guided by clause 49. Also, the SEBI gave its approval to make certain amendments to this clause for further enhancement of listing agreements with mandatory and voluntary provisions in the case of listed companies before the arrival of the companies act 2013 (Kamath, Citation2019a). The clause necessitates the disclosure of all relevant CG attributes including ownership structure, related party transactions, board structure, external, compensation structure, internal audit, and many more. Later, the companies act 2013 arrived and provided a well-defined CG practice (Srivastava et al., Citation2019). Since then, many academicians, and scholars attempted to delve into this domain.

As far as studies are concerned with corporate governance in the Indian context, (Machold & Vasudevan, Citation2004) conducted a study on the CG model reforms at the country level and revealed the induced preference towards Anglo-American models, and on the emergence of diversity in the governance mechanism. It is likely noted that the dearth of literature focused on the impact of CG on firm performance. The studies revealed that CG affects positively on firm performance (Abdul Gafoor et al., Citation2018; Ghosh & Ansari, Citation2018; N. N. Gupta & Mahakud, Citation2020; Handa, Citation2018; M & Sasidharan, Citation2020; Maji & Saha, Citation2021; Panda & Bag, Citation2019; Shukla et al., Citation2021; Uppal, Citation2020; Pillania, Citation2012). Some studies showed mixed results (Al-Homaidi et al., Citation2019, Citation2021; N. Arora & Singh, Citation2020; Dey & Sharma, Citation2021; Gulzar et al., Citation2020; P. K. P. K. Gupta & Mittal, Citation2020; Sehrawat et al., Citation2020a; Minimol, Citation2021). Some studies showed no effect (Al-ahdal et al., Citation2020). The other facets of the study concentrated on CG and its impact on earnings management (Chatterjee, Citation2020; Kapoor & Goel, Citation2017; Potharla et al., Citation2021; Sehrawat et al., Citation2020b). However, there is a paucity of literature in terms of a comprehensive overview in the domain of CG in the Indian context. (Almaqtari, Shamim et al., Citation2020) reviewed 161 articles on CG and revealed that the board of directors issues, ownership structure, audit committee attributes, audit quality, board and audit committee independence, foreign and institutional ownership, and financial performance are the major topic of interest among Indian researchers. Although this piece of work reviewed past scholarly works, the understanding of the recent trends and themes in this field is lacking. Though there have been review studies on CG in different countries and regions, according to the authors’ knowledge, there has been no single study attempted to provide a state-of-the-art summary on CG by deploying Bibliometric software to uncover the recent trends in terms of major hotspot areas in this area. Moreover, with the growing myriad of literature in the realm of CG mechanisms in India, the different strands of literature emphasized numerous aspects. However, this present study is motivated by (Zheng & Kouwenberg, Citation2019) that highlighted the need for further investigation into the CG area, particularly from emerging countries’ perspective. To fill the void in the literature, the present study aims to provide a state-of-the-art summary of CG in the Indian context.

The novelty of the paper lies in study characteristics which makes it different by employing a bibliometric and systematic literature approach and thereby provides a summary overview of CG research in India. The main contributions of the paper discuss key takeaways of 344 articles on CG by employing the Bibliometric R Package, which is an extensively adopted technique in any discipline. The impetus of this method stemmed from the noticeable efforts to delineate the evolution of CG studies in India as well as the recent trends and themes in this domain. Further, this method is also different from other methods, which offer yearly publications, prominent authors, impactful documents, high-contributing journals, and authors’ collaboration networks. In addition, it also uncovers the major themes, and keyword co-occurrence in past studies and thereby guides all academicians in terms of existing as well as future hotspot topics in any area (Abbas et al., Citation2022). The review uncovered that earnings management, gender diversity, ownership structure, board structure, board size, corporate governance, ownership, and firm performance are the key hotspot topics in this segment. To the best of the authors knowledge, this is the first study to provide a summary overview of CG studies in India using Bibliometric and VOSViewer software that offer future directions for further enhancement of this arena.

To provide a summary overview of CG research, following previous studies and their scope, the study aims to answer the below-framed research questions:

RQ1. What is the publication trend for CG research?

RQ2. What are the most influencing articles contributing to the CG?

RQ3. Which are the top contributing journals in CG research?

RQ4. Who are the prominent authors in CG research?

RQ5. What are the major themes and studied topics on CG?

RQ6. What is the future scope of research on CG?

The main study objectives are as follows:

a. To know the production trend on year-on-year basis in CG research

b. To find the most impactful documents contributing to the CG research

c. To find the top publishing journals in the field of CG research

d. To find the prominent authors in CG research with their noteworthy contributions

e. To uncover the major themes and studied topics on CG research

f. To delineate directions for future research in CG domain

The findings of this review guide all stakeholders in several ways. Firstly, the potential and existing researchers can observe yearly publications which induces them to show interest in this arena (RQ1). The prospective researchers can identify key aspects of literature (RQ2), major contributing sources (RQ3) relevant authors and collaboration network (authors, country) (RQ4, RQ5), and the major themes that help to establish new knowledge (RQ5). Also, these findings lead various existing and potential researchers to further investigate this area to prove it as a new promising area for all stakeholders. (RQ6).

The other sections of the paper are formulated as follows. The study begins with literature about CG. Next, the paper describes the methodology employed, followed by the dissemination of major findings. Finally, the paper concludes the study and provides agenda for future research.

2. Methodology

The study follows bibliometric analysis through systematic literature review (SLR) evidence. The bibliometric analysis is an extensively used approach to find the knowledge autonomy of any research field (Li et al., Citation2017). Particularly, this analysis encapsulates the proper use of quantitative techniques with the aid of bibliometric information, and it helps in the assessment of the entire spectrum of articles in any field (Sahoo et al., Citation2022). In addition, the review also used a SLR method. It is a method that systematically synthesis and locates all studies with the alignment of a particular research question based on high transparency and quality at each level (MacAskill et al., Citation2021; Stechemesser & Guenther, Citation2012). In this review, the SLR is followed to synthesize the past literature (Blanco-mesa et al., Citation2017) due to its capacity to limit the bias (Goyal & Kumar, Citation2021). This review deploys “Scientific Procedures and Rationales for Systematic Literature Reviews” (“SPAR-4-SLR”) criteria. The rationale behind the choice of this method lies in the superior quality of “SPAR-4-SLR” over the “PRISMA Guidelines”. Moreover, this method follows three major stages which include “assembling”, “arranging”, and “assessing” articles (Paul et al., Citation2021). The review criteria are shown as follows:

2.1. Assembling

To identify, and acquire the spectrum of articles on CG, the research reviewed the past scholarly work where necessary insights were obtained, and accordingly various combination of keywords was formed. In the first search strategy, the keywords of “Corporate Governance” OR “CG” AND “India “were used which yielded 889 documents. The final strategy was done using the keywords of “Corporate Governance” OR “Board of director” OR “Ownership” OR “Code of Conduct” OR “Code of governance” OR “Corporate control” OR “Ownership concentration” OR “Corporate concentration” OR “Board” OR “director” OR “Governance of Corporation” OR “Corporate Practice” AND “India” were used which yielded a total of 7982 documents.

In line with the identification of keywords, the search strategy was done on 19–09-2022 to gather articles in the field where the search string followed was based on title, abstract, and keywords. The review used the Scopus database as this is the major database with higher quality scholarly articles than other databases (Comerio & Strozzi, Citation2019; Norris & Oppenheim, Citation2007), which is particularly more suitable for bibliometric review (Baas et al., Citation2020). Similarly, the Web of Science, an alternative database was also used where relatively a smaller number of results were obtained. Hence, the Scopus database was finalized for the data extraction process, and a total of 7982 documents were identified from the search process.

2.2. Arranging

For the sake of arranging the identified and acquired articles after the assembling stage, the study applied the category (code) function on the Scopus database to filter the gathered data according to “year, subject, document type, source type, publication stage, and language”. The search strategies were confined to “2022, Economics, Econometrics, Finance, Business Management, Accounting, and Social Sciences, articles, review, final, journal, India, and English” in those codes, respectively. However, the search results appeared only from 1978 to 2022 in the database. This led to yield a total of 1616 articles.

Furthermore, the data were downloaded and exported to an MS excel sheet and each article was read with a special emphasis on abstract, findings, and conclusion which yielded a 344 corpus of articles for review on a random cross-checking basis with confirmed consent using other databases such as Elsevier, Sage, Springer, Emerald, Taylor and Francis, and Google Scholar (Goyal & Kumar, Citation2021).

2.3. Assessing

To evaluate the entire assembled 344 articles on the CG research, the study applies the bibliometric approach to review. To this end, bibliometric analysis uses a quantitative technique that manifests scholarly works on a real-time basis (Donthu et al., Citation2021). In addition, the study integrates a systematic literature review method as it credibly increases the transparency of the study (Ellegaard & Wallin, Citation2015). Also, the bibliometric analysis mitigates bias and employs qualitative (subjectivity) review using quantitative (objectivity) tools (Burton et al., Citation2020) during the time of a large corpus of articles (100–1000 articles) (Donthu et al., Citation2021), as in this review with 344 articles. The study deploys bibliometric analysis to do performance analysis and science mapping analysis using Biblioshiny and VOSviewer. The former unpacks publication trends, influencing articles, prominent authors, top countries, and affiliations, and the latter shows the major themes and topics of CG research (Castriotta et al., Citation2019; Donthu et al., Citation2021; Van Eck & Waltman, Citation2017). The review based on the synthesis of past literature curates further research in this domain. The next sections of the paper report findings, whereby the narratives are provided by tables and figures.

3. Results

3.1. Performance analysis

The study done performance analysis as this analysis shows the performance of any research area (Donthu et al., Citation2021), which is particular to CG research in this paper. Moreover, this analysis delineates the publication trend, most influencing article, top contributing author, and authors’ research network (See Figure ).

Figure 1. shows the “SPAR4 SLR” diagram .

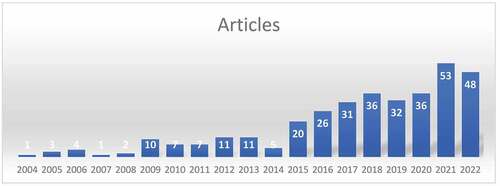

3.1.1. The publication trend

Figure shows the publication trend in the field of corporate governance. It is likely noted that the research in this domain has started since 2004. From 2015 onwards, the publication trend has changed and witnessed for increasing trend with an annual growth rate of 23.99%. The year 2021 is noted for its high number of scientific productions with a total of 53 productions.

Figure 2. Annual scientific production.

3.1.2. The most influencing articles

Table depicts the most influencing articles in the corporate governance research field in terms of total citations. It has demonstrated that the articles of ARORA A titled “corporate governance and firm performance in developing countries: evidence from India” and the article of (Sarkar et al., n.d.-a) titled “Board of Directors and Opportunistic Earnings Management: Evidence from India” are the most contributing articles in corporate governance research with their total 162 and 149 citations. Interestingly, these articles shed light on corporate governance and its impact on firm performance and earnings management.

Table 1. The most influencing articles

3.1.3. Top contributing journals

Table enumerates the top contributing journals in terms of their total production in the domain of corporate governance. The “Indian Journal of Corporate Governance” and “Corporate Governance” journals stand first and second place with a total of 41 and 15 publications, respectively. The Indian Journal of Corporate Governance as one of the top contributing sources led the researchers to contribute more towards these arena. Among top-rated journals, B and C-rated journals contributed significantly to this research segment.

Table 2. Top contributing journals

3.1.4. Most prominent authors

Table shows the most prominent authors in the field of corporate governance research. It has been pointed out that Singh B, Ghosh S, and Pattanayak JK are the prominent authors in the corporate governance study with a total of 10, 8, and 8 publications, respectively. The other most prolific authors are Gill S, Haldar A, Raithatha M, and Sharma JP.

Table 3. The most prolific authors

3.2. Science Mapping

The science mapping analysis is a major analysis that shows the existing body of knowledge on a particular research domain with a graphical representation (Donthu et al., Citation2021). It comprises thematic analysis, factorial analysis, temporal analysis, and network analysis. The thematic analysis is used to reveal major themes (Chandra et al., Citation2022), factorial analysis is used to investigate the intellectual structure of articles in a particular domain (Sahoo et al., Citation2022), and temporal analysis is used to uncover the major topics, and the word cloud analysis is employed to unpack the major themes about CG research (S. Kumar et al., Citation2022).

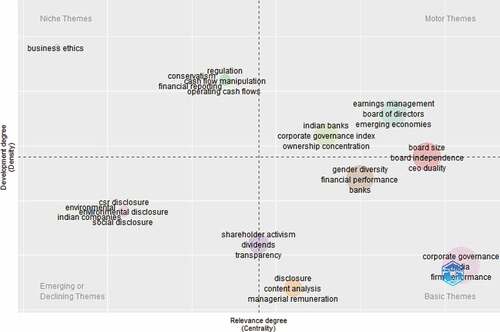

Figure shows a thematic analysis with four different quadrants with their varying impact and centrality level. The right upper quadrant is known as a motor theme with high impact and centrality. It includes keywords such as “Indian banks”, corporate governance index”, ownership concentration”, earnings management”, board of directors”, “emerging economies”, board size”, “board independence”, and “CEO duality”. Research in this segment focused on the impact of corporate governance with different CG proxies on banking sectors as well as earnings management. The right lower quadrant is known as a base theme with low impact and high centrality. Aithough they accounted for the low impact the keywords under themes are central to investigate. The various keywords under this theme include “gender diversity”, financial performance”, “banks”, “shareholders activism”, “dividend”, “transparency”, “managerial remuneration”, “corporate governance”, and “firm performance”. As these elements are central to this research domain, further research across various elements makes the study more fruitful. The upper left quadrant is known as the niche theme with high impact and low centrality. This theme includes “business ethics”, “conservativism”, “regulation”, cash flow management, “financial reporting”, and “operating cash flow” as major keywords. With the high impact of these elements in this domain, further investigation needs to be curated for a better understanding of various aspects of this domain. The lower left quadrant with low impact and low centrality is termed as an emerging or declining theme. The various elements in this quadrant include “CSR disclosure”, “environmental disclosure”, “social disclosure”, and “Indian companies”. Although there is low impact and centrality further studies need to be done with different perspectives to gain new insights into this area.

Figure 3. Shows a thematic map.

3.3. Network analysis

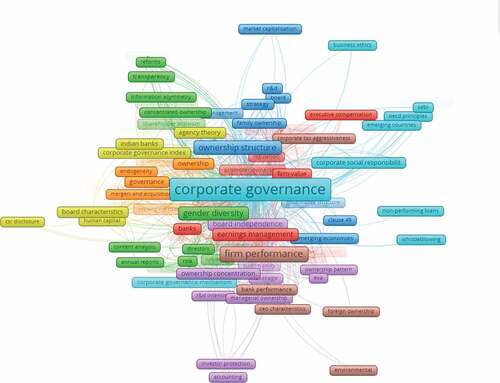

The network analysis considers the keyword co-occurrence technique with the aid of VOSviewer software. This analysis depicts the major clusters in any study field. Moreover, this technique includes a corpus of articles that show the major themes which characterize the intellectual structure in any research area (Abhilash et al., Citation2022). The major clusters of this analysis are illustrated in Table . Also, Table includes a descriptive summary of various clusters with their respective keyword.

Table 4. Descriptive summary of each theme

Figure shows a network analysis that delineates the major eight clusters in the CG study, namely, cluster 1 (red); earnings management, cluster 2 (green); gender diversity, cluster 3(blue); ownership structure, cluster 4(yellow); board structure, cluster 5 (purple); board size, cluster 6 (sky blue); corporate governance, cluster 7(orange); ownership, and cluster 8(brown); firm performance. Table shows an accompanied summary description including the “total occurrence” (TO) of each keyword, “Links” (L) of each keyword: which shows the unique occurrence of each term with other terms, and “total link strength” (TLS): which shows the total occurrence of each term with other terms in the entire topic (Donthu et al., Citation2021). However, the summary of each theme or cluster is as:

Figure 4. Shows the network analysis.

4. Cluster 1: Earnings management

Cluster 1 is concerned with earnings management and comprises 18 total occurrences, 55 total link strengths, and 27 links. The other keywords that fall under this cluster include board of directors, family firms, firm value, business groups, banks, performance, agency problem, promoter ownership, dividend policy, and institutional ownership. Under this cluster, the research focused on CG and its impact on earnings management where the strong association of board size, business, board independence, audit committee independence with discretionary accruals (Kapoor & Goel, Citation2017), board quality, and, business as earnings manipulation reduction technique (Chatterjee, Citation2020), ownership dilution during IPO exerted expiration period (Purayil & Lukose, Citation2020), also the CEO duality (Sehrawat et al., Citation2019), board diligent, and domestic institutional investors role in mitigating earnings management was strongly found (Sarkar et al., n.d.-a). It also showed CG mechanisms as predictors of EQ for Indian investors (Wasan & Mulchandani, Citation2020). Interestingly domestic institutional investment and foreign institutional investment proved as the major factors with their negative impact on EM (Potharla et al., Citation2021). It was evidenced that family-owned firms with board independence accounted for dividend policy (Rajput & Jhunjhunwala, Citation2019) and the increased dividend due to good CG practices (Pahi & Yadav, Citation2021). Further, banking studies revealed board size as a major determinant of banks’ performance particularly in high-income districts (Ghosh & Ansari, Citation2018).

5. Cluster 2: Gender diversity

Cluster 2 is concerned with gender diversity and comprises 21 total occurrences, 52, total link strength, and 27 links. Other keywords of this cluster are panel data, return on assets (ROA), women directors, independent directors, Tobins’q, shareholder activism, board composition, IPO, and transparency. Under this cluster, the researcher has given prominent importance to gender diversity where workforce gender diversity, board gender diversity in the bank (Maji & Saha, Citation2021), firm (Duppati et al., Citation2020), adverse effect of social capital on woman’s appointment (Haldar et al., Citation2020), the insignificant importance of women in the board witnessed on firm performance (Minimol, Citation2021). Also, the risk outcomes (Biswas, Citation2021), and financial distress due to a low number of women on the board were strongly found (Mittal & Lavina, Citation2018). As a matter of CG performance, the role of shareholder activism is exerted as a tool for overall firm performance (Islam, Citation2020).

6. Cluster 3: ownership structure

Cluster 3 is concerned with ownership structure which comprises 25 total occurrences, 60, total link strength, and 35 links. Other keywords of this cluster are financial performance, institutional investors, emerging economics, strategy, internationalization, and research and development (R and D). Under this cluster, the research focused on firm profitability with the existence of the CG mechanism. ROA and earning per share as a measure of profitability were found to be impacted by board diligence, size of audit committee, audit committee composition, diligence of audit committee, and size of a firm (Al-Homaidi et al., Citation2021), the board size, board independence, number of experts (Abdul Gafoor et al., Citation2018), CEO qualification, CEO duality (N. N. Gupta & Mahakud, Citation2020), CEO narcissism (Uppal, Citation2020), average remuneration of directors, and board committees (Handa, Citation2018), the presence of promoters, domestic institutions and foreign institutions exerted as the drivers of the financial performance (Panda & Bag, Citation2019). There is also evidence that a good CG induces group internationalization (Shanmugasundaram, Citation2020).

7. Cluster 4: board structure

Cluster 4 is concerned with board structure which comprises 12 total occurrences 21, total link strength, and 13 links. Other keywords of this cluster are board characteristics, agency theory, CG index, intellectual capital, and Indian banks. Under this cluster, the research has shown considerable efforts toward the construction of the CG index and revealed the increased efforts of banks in adhering to a strong CG practice (Gulati et al., Citation2020). It also found that board size, board attendance, and CEO duality are the key elements to reduce the problems of agency costs (Katti & Raithatha, Citation2018), where the induced effect of CG practices on firm intellectual capital performance particularly of large-sized firms (Kamath, Citation2019a), also the supreme importance of institutional investors shareholdings, and a number of members in the board on intellectual capital disclosure were well observed (Hidalgo et al., Citation2011).

8. Cluster 5: Board size

Cluster 5 is concerned with board size which comprises 15 total occurrences 60, total link strength, and 5 links. Other keywords of this cluster are board independence, ownership concentration, and leverage. Under this, the research has delved into CG and its effect on firm performance with the inclusion of board size as ownership concentration based on quantitative techniques such as panel data. The study also showed that companies enjoy the benefits due to good CG practices in terms of leverage (Jadiyappa et al., Citation2021).

9. Cluster 6: Corporate governance

Cluster 6 is concerned with corporate governance which comprises 167 total occurrences, 411 total link strength, and 130 links. Other keywords of this cluster are CSR, CG mechanism, and India. Under this cluster, the researchers have investigated the CG and CSR nexus with board independence, CEO duality, sustainability committee (Fahad & Rahman, Citation2020), and governance score to show their impact on CSR disclosure (F & N, Citation2020). The findings show that companies with a large proportion of independent directors promote good CSR committees (Bhatia & Makkar, Citation2020). Further, it also revealed that their connection is a resultant of firm’s ownership structure, stakeholder approach, government regulations, legislation, legal enforcement, and corporate disclosure culture (Uzma, Citation2016).

10. Cluster 7: Ownership

Cluster 7 is concerned with ownership which comprises eight total occurrences, 23 total link strength, and 17 links. Other keywords of this cluster are governance, emerging markets, panel regression, and disclosure. Under this cluster, the research has focused on CG practices in emerging countries such as India that evinced the country’s formal written CG code (Majumder & Banerjea Citation2012) and necessitate to endeavour the governance landscape in the country (Uzma, Citation2016) by adopting transparency in terms of disclosing CG regulations (Almaqtari, Shamim et al., Citation2020).

11. Cluster 8: Firm Performance

Cluster 8 is concerned with the firm performance which comprises 42 total occurrences, 116 total link strength, and 45 links. Other keywords of this cluster are CEO duality, board diversity, CEO compensation, and bank performance. Under this cluster, the research has focused on the financial performance of banking companies where the effect of CEO duality and CEO qualification (N. N. Gupta & Mahakud, Citation2020), board independence, and board size particularly in high-income districts (Ghosh & Ansari, Citation2018), number of board meetings and experts (Abdul Gafoor et al., Citation2018), the weak governance in public sector banks were observed (Pant & Radhakrishnan, Citation2019). See Figure .

Figure 5. shows the author’s researchcollaboration map with other countries across the globe. It was observed that Indian authors have a good research network with the USA, UK, Canada, UAE, Yemen, Denmark, and New Zealand. To broaden the present collaboration network, more studies in this domain are needed and that necessitates all prominent and new authors of different countries particularly with developed and emerging countries to conduct collaborative research works.

11.1. Authors collaboration network

11.2. Future steps as the way forward

The present study reviews existing literature in the domain of CG and provides an overview of this research field. Accordingly, the study findings show interesting facts and thereby create ample opportunities for future research as the way forward.

As board compensation is one of the major CG mechanisms, the proper understanding of compensation committee quality in assessing the pay-setting system, and the legal aspects such as law, pay-setting reforms, and other sorts of regulations need further study to understand the remuneration tactics (Gill & Kohli, Citation2018).

The dividend policy of any firm aims to contribute toward all shareholders. However, the understanding of CG and its impact on dividend policy is less explored and needs further research (Rajput & Jhunjhunwala, Citation2019).

Despite, the growing studies on whistle-blowing practices and their impact (Mehrotra et al., Citation2020), research on this aspect is in the infancy stage in India (Kanojia et al., Citation2020). Hence, there is further room for proper investigation into this aspect to formulate necessary policy frameworks with the expectation to maintain a strong CG practice in the country.

The malpractices such as fraud, earnings manipulation have come into the main picture in the corporate world (Mangala & Kumari, Citation2017), and the necessary techniques to detect and prevent in terms of better CG practices is the need of the decade. Further research to explore the effectiveness of the company’s CG on errors and fraudulent activities could be conducted.

With the growing importance of CG practices in corporates, the various accounting measures in the form of accounting standards, policy reforms, transparency, business ethics, CSR disclosure, sustainability reporting, green governance, earnings management (Almaqtari, Al-Hattami et al., Citation2020),

It has been well observed that CG disclosure is gaining prominence among all stakeholders. Hence, there is further room for future research to examine the major determinants of CG disclosure in the country.

So far, most of the studies focused on a quantitative approach like panel regression method. Further research could be fruitful by employing qualitative approaches such as in-depth interviews, surveys, content analysis, and many others.

The CG practices being a controlling mechanism in the corporate world seem to be a suitable measure for the mitigation of various malpractices. However, more studies in the domain of CG (both internal and external factors) and taxation perception such as taxation practices, and tax aggressiveness could be highly encouraged.

though there has been a handful of studies on CG in the country, research in the context of CG and corporate sustainability is lacking. Future could be encouraged by linking CG mechanism and corporate sustainability.

Furthermore, the concepts such as corporate sustainability, innovation, and technology adoption such as blockchain and many other elements could be a hot topic for future research.

12. Discussion

The present paper deploys bibliometric analysis and systematic review literature method and provides an overview of research in the realm of CG at the country level, particularly in India. The performance analysis demonstrates that research in the domain of CG is increasing with an annual growth rate of 23.99% since 2014 due to the major policy reforms in CG mechanisms such as the introduction of gender diversity regulation in 2013 and its compulsion by 2014 (Biswas, Citation2021). It also highlighted that CG research is in great demand for the decade. It was found that the studies of (A. A. Arora & Sharma, Citation2016; Balasubramanian & Black, Citation2010; N. Kumar & Singh, Citation2013; Sarkar et al., n.d.-b; Sarkar & Sarkar, Citation2009) referred to as high impactful articles. These studies with their interesting findings laid down a foundation and motivated the academicians for their succeeding research in the nexus of CG and its impact on firm performance and also on earnings management. Interestingly, the Indian Journal of Corporate Governance and Corporate Governance paved the way for academic contributions by publishing CG papers and added momentum to CG research. The most prominent authors list shows that Singh, Ghosh, and Patnaik are the most prolific authors in this area with a total of 10, and 8 articles, respectively. However, the trend of authors’ collaborative network shows the limited number of collaborations from foreign countries, namely, the USA, UK, Canada, UAE, Yemen, Denmark, and New Zealand which suggests more collaborations with both developed and developing countries to enrich the understandings on CG in and around the world.

The science mapping results unravel several interesting facts about CG research. The findings of the thematic analysis depicted major four clusters with their relative importance. The motor theme with high impact and centrality show “Indian banks”, corporate governance index”, ownership concentration”, earnings management”, board of directors”, “emerging economies”, board size”, “board independence”, and “CEO duality” as major terms evolved in the study. Further “gender diversity”, financial performance”, “banks”, “shareholders activism”, “dividend”, “transparency”, “managerial remuneration”, “corporate governance”, and “firm performance” has evolved as the base theme. With the growing concerns about CG practices in companies as well as banking firms, scholarly works have been given priority on CG and its impact on a company’s various aspects particularly financial performance (Chatterjee, Citation2020; Kapoor & Goel, Citation2017). It has been pointed out that CG is one of the controlling mechanisms in the corporate world, and the researchers have peeped into CG’s impact in the form of gender diversity on companies’ financial performance including dividend policy, and managerial remuneration with the expectation to improve high transparency in firm’s business affairs (Pahi & Yadav, Citation2021; Rajput & Jhunjhunwala, Citation2019). The niche theme shows “business ethics”, “conservativism”, “regulation”, cash flow management, “financial reporting”, and “operating cash flow” as the main elements. However, it is likely noted that there is room for further research in this domain due to their potential power. Also, the emerging or declining theme show “CSR disclosure”, “environmental disclosure”, “social disclosure”, and “Indian companies as major key elements. As there are requirements from various stakeholders to disclose nonfinancial aspects, this theme highlights the need for reporting this information. Furthermore, the network analysis with keyword co-occurrence revealed various key facts. It has shown earnings management, gender diversity, ownership structure, board structure, board size, corporate governance, ownership, and firm performance as major themes in the CG research field. Following the SEBI 2017 notifications regarding the performance evaluation of the firm’s board on company’s state of affairs (Kamath, Citation2019a), many researchers started to peep into various aspects of CG. It turned out that the CG mechanisms with its various proxies majorly focused on firm performance and earnings management. Since many of SEBI supported studies were focused on the impact of CG attributes such as gender diversity (Duppati et al., Citation2020; Maji & Saha, Citation2021; Mittal & Lavina, Citation2018), establishment of SEBI, clause 49 of listing agreements (Srivastava et al., Citation2018) on firm performance, this review, however, is of a different kind than other studies supported by the SEBI as it concentrates on the entire spectrum of CG research in the Indian context and thereby provides new insights in terms of its present status and future developments. Accordingly, the review findings suggest professionals to revamp the CG practices to align with global-level reforms.

13. Conclusion

The study based on bibliometric analysis and systematic literature review approach revealed the growing concerns on the part of various researchers and academicians, which can be understood by the recent hike in CG publication trends from 2004 till date with the inception of various policy measures related to corporate sustainability in terms of proper controlling mechanisms to uplift their image. By relying on the annual publication growth rate, the study expresses the need for more research work in the near future. The top publishing journals in this domain are of from this CG domain such as “Indian Journal of Corporate Governance”, “Corporate Governance “, which heralds the role of journals from a particular domain. It could be expanded further in some other journals so that new knowledge continued to be created. In the case of most relevant authors and contributing articles, it was well observed that the studies concerned with the nexus between CG and firm performance received overwhelming interest in terms of the number of publications and total citations. Further research with multiple aspects along with these topics would be more fruitful to obtain necessary insights.

The thematic analysis with the major four quadrants shows important keywords in the CG study due to their impact and centrality. It has turned out that the concept of CG has emerged with a focus on banks as well as a corporate financial performance with the inclusion of various CG elements. In addition, the research has also delved into nonfinancial aspects such as a firm’s financial and nonfinancial disclosure to enhance overall efficiency. It is worth noting point here that the integration of various CG components to advance this emerging concept.

The findings of network analysis depict earnings management, gender diversity, ownership structure, board structure, the board size, corporate governance, ownership, and firm performance as the major clusters in CG research. It is evident to note that role of boards remained to be a highly occurred topic in this research domain. A compelling rationale is its influencing power on various aspects such as firm performance, earnings management, executive compensation, accounting frauds, leadership, strategy, disclosure, and many more. Considering together these CG elements form the stepping stone for corporate sustainability. However, to enrich the understanding of CG in the Indian context identifies some areas such as board compensation, dividend policy, accounting standards, policy reforms, transparency, business ethics, CSR disclosure, sustainability reporting, green governance, and earnings management for future research.

The review outcome, however, eases scholars, regulators, and practitioners as they widen their understandings of CG and its plausible roles in the Indian corporate world. In this regard, it also devises certain policy measures to bolster CG practices. As there is a noticeable impact of boards in the corporate world, there is a vital role for regulators and other stakeholders to play in terms of strengthening the CG frameworks with a special emphasis on the company’s boards, executives’ remuneration, other non-financial aspects, and many more. It further calls for policy implications with the prime motive of drawing the attention of various stakeholders particularly firms, shareholders, and the public as a whole which results in the enhancement of the proper follow-up of effective CG code of conduct to rule out major potential corporate scams. Further, the review suggests the introduction of a country-specific norms for all companies to adhere to a proper code of conduct to align with global-level practices. As a result, it attains the attention of major stakeholders to achieve high transparency, efficiency, and accountability to safeguard the interest of all stakeholders.

Apart from the study findings, it also highlights some of the limitations. First, the study is based on the Scopus database whereas other forms of databases could be used in future studies. Second, the study is limited to the English language only. As this study enriches the understanding of CG research in India other countries are not included. As most of the studies focused on a quantitative approach like panel regression, it is highly encouraged to deploy qualitative forms of techniques such as narrative reporting in future research as a way forward.

Disclosure statement

Author(s) declares no conflict of interest.

Additional information

Funding

References

- Abbas, A. F., Jusoh, A., Mas’od, A., Alsharif, A. H., & Ali, J. (2022). Bibliometrix analysis of information sharing in social media. Cogent Business and Management, 9(1), 2016556. https://doi.org/10.1080/23311975.2021.2016556

- Abdul Gafoor, C. P., Mariappan, V., & Thyagarajan, S. (2018). Board characteristics and bank performance in India. IIMB Management Review, 30(2), 160–22. https://doi.org/10.1016/j.iimb.2018.01.007

- Abhilash, A., Shenoy, S., & Shetty, D. (2022). A state-of-the-art overview of green bond markets: Evidence from technology empowered systematic literature review. In Cogent Economics and Finance Vol. 10. https://doi.org/10.1080/23322039.2022.2135834

- Al-ahdal, W. M., Alsamhi, M. H., Tabash, M. I., & Farhan, N. H. S. (2020). The impact of corporate governance on financial performance of Indian and GCC listed firms: An empirical investigation. Research in International Business and Finance, 51. https://doi.org/10.1016/j.ribaf.2019.101083

- Al-Homaidi, E. A., Almaqtari, F. A., Ahmad, A., & Tabash, M. I. (2019). Impact of corporate governance mechanisms on financial performance of hotel companies: Empirical evidence from India. African Journal of Hospitality, Tourism and Leisure, 8(2), 1–21.

- Al-Homaidi, E. A., Mohammed Al-Matari, E., Tabash, M. I., Khaled, A. S. D., & Senan, N. A. M. (2021). The influence of corporate governance characteristics on profitability of Indian firms: An empirical investigation of firms listed on Bombay stock exchange. Investment Management and Financial Innovations, 18(1), 114–125. https://doi.org/10.21511/imfi.18(1).2021.10

- Almaqtari, F. A., Al-Hattami, H. M., Al-Nuzaili, K. M. E., & Al-Bukhrani, M. A. (2020). Corporate governance in India: A systematic review and synthesis for future research. Cogent Business and Management, 7, 1. https://doi.org/10.1080/23311975.2020.1803579

- Almaqtari, F. A., Shamim, M., Al-Hattami, H. M., & Aqlan, S. A. (2020). Corporate governance in India and some selected Gulf countries. International Journal of Managerial and Financial Accounting, 12(2), 165–185. https://doi.org/10.1504/IJMFA.2020.109135

- Antwi, I. F., Carvalho, C., & Carmo, C. (2021). Corporate governance and firm performance in the emerging market: A review of the empirical literature. Journal of Governance and Regulation, 10(1), 96–111. https://doi.org/10.22495/jgrv10i1art10

- Arora, A., & Sharma, C. (2016). Corporate governance and firm performance in developing countries: Evidence from India. Corporate Governance (Bingley), 16(2), 420–436. https://doi.org/10.1108/CG-01-2016-0018

- Arora, N., & Singh, B. (2020). Corporate governance and underpricing of small and medium enterprises IPOs in India. Corporate Governance (Bingley), 20(3), 503–525. https://doi.org/10.1108/CG-08-2019-0259

- Baas, J., Schotten, M., Plume, A., Côté, G., & Karimi, R. (2020). Scopus as a curated, high-quality bibliometric data source for academic research in quantitative science studies. Quantitative Science Studies, 1(1), 377–386. https://doi.org/10.1162/qss_a_00019

- Balasubramanian, N., Black, B. S., & Khanna, V. (2010). The relation between firm-level corporate governance and market value: A case study of India. Emerging Markets Review, 11(4), 319–340.

- Bhatia, A., & Makkar, B. (2020). Stage of development of a country and CSR disclosure – The latent driving forces. International Journal of Law and Management, 62(5), 467–493. https://doi.org/10.1108/IJLMA-03-2020-0068

- Biswas, S. (2021). Female directors and risk-taking behavior of Indian firms. Managerial Finance, 47(7), 1016–1037. https://doi.org/10.1108/MF-05-2020-0274

- Blanco-Mesa, F., Merigó, J. M., & Gil-lafuente, A. M. (2017). Fuzzy decision making: Abibliometric- based review. Journal of Intelligent & Fuzzy Systems, 32(3), 2033–2050.

- Burton, B., Kumar, S., & Pandey, N. (2020). Twenty-five years of The European Journal of Finance (EJF): A retrospective analysis. European Journal of Finance, 26(18), 1817–1841. https://doi.org/10.1080/1351847X.2020.1754873

- Castriotta, M., Loi, M., Marku, E., & Naitana, L. (2019). What’s in a name? Exploring the conceptual structure of emerging organizations. Scientometrics, 118(2), 407– 437. https://doi.org/10.1007/s11192-018-2977-2

- Chandra, S., Verma, S., Lim, W. M., Kumar, S., & Donthu, N. (2022). Personalization in personalized marketing: Trends and ways forward. Psychology and Marketing, September 2021. https://doi.org/10.1002/mar.21670

- Chatterjee, C. (2020). Board Quality and Earnings Management: Evidence from India. Global Business Review, 21(5), 1302–1324. https://doi.org/10.1177/0972150919856958

- Comerio, N., & Strozzi, F. (2019). Tourism and its economic impact: A literature review using bibliometric tools. Tourism Economics, 25(1), 109–131. https://doi.org/10.1177/1354816618793762

- Dey, S. K., & Sharma, D. (2021). Nexus between corporate governance and financial performance: Corroboration from Indian Banks. Universal Journal of Accounting and Finance, 8(4), 140–147. https://doi.org/10.13189/UJAF.2020.080406

- Donthu, N., Kumar, S., Mukherjee, D., Pandey, N., & Lim, W. M. (2021). How to conduct a bibliometric analysis: An overview and guidelines. Journal of Business Research, 133(April), 285–296. https://doi.org/10.1016/j.jbusres.2021.04.070

- Duppati, G., Rao, N., Matlani, N., Scrimgeour, F., & Patnaik, D. (2020). Gender diversity and firm performance: Evidence from India and Singapore. Applied Economics, 52(14), 1553–1565. https://doi.org/10.1080/00036846.2019.1676872

- Ellegaard, O., & Wallin, J. A. (2015). The bibliometric analysis of scholarly production: How great is the impact? Scientometrics, 105(3), 1809–1831. https://doi.org/10.1007/s11192-015-1645-z

- Fahad, P., & Rahman, P. M. (2020). Impact of corporate governance on CSR disclosure. International Journal of Disclosure and Governance, 17(2–3), 155–167. https://doi.org/10.1057/s41310-020-00082-1

- F, P., & N, K. B. (2020). Determinants of CSR disclosure: An evidence from India. Journal of Indian Business Research, 13(1), 110–133. https://doi.org/10.1108/JIBR-06-2018-0171

- Ghosh, S., & Ansari, J. (2018). Board characteristics and financial performance: Evidence from Indian cooperative banks. Journal of Co-Operative Organization and Management, 6(2), 86–93. https://doi.org/10.1016/j.jcom.2018.06.005

- Gill, S., & Kohli, M. (2018). Perceptual Determinants of Executive Compensation: Survey-Based Evidence from India. Indian Journal of Corporate Governance, 11(2), 159–184. https://doi.org/10.1177/0974686218797760

- Goyal, K., & Kumar, S. (2021). Financial literacy: A systematic review and bibliometric analysis. International Journal of Consumer Studies, 45(1), 80–105. https://doi.org/10.1111/ijcs.12605

- Gulati, R., Kattumuri, R., & Kumar, S. (2020). A non-parametric index of corporate governance in the banking industry: An application to Indian data. Socio-Economic Planning Sciences, 70. https://doi.org/10.1016/j.seps.2019.03.008

- Gulzar, I., Haque, S. M. I., & Khan, T. (2020). Corporate Governance and Firm Performance in Indian Textile Companies: Evidence from NSE 500. Indian Journal of Corporate Governance, 13(2), 210–226. https://doi.org/10.1177/0974686220966809

- Gupta, N., & Mahakud, J. (2020). CEO characteristics and bank performance: Evidence from India. Managerial Auditing Journal, 35(8), 1057–1093. https://doi.org/10.1108/MAJ-03-2019-2224

- Gupta, P. K., & Mittal, P. (2020). Corporate governance and risk bundling: Evidence from Indian companies. European Journal of Business Science and Technology, 6(1), 37–52. https://doi.org/10.11118/EJOBSAT.2020.004

- Haldar, A., Datta, S., & Shah, S. (2020). Tokenism or realism? Gender inclusion in corporate boards. Equality, Diversity and Inclusion, 39(6), 707–725. https://doi.org/10.1108/EDI-04-2019-0126

- Handa, R. (2018). Does corporate governance affect financial performance: A study of select Indian banks. Asian Economic and Financial Review, 8(4), 478–486. https://doi.org/10.18488/journal.aefr.2018.84.478.486

- Hidalgo, R. L., García-Meca, E., & Martínez, I. (2011). Corporate Governance and Intellectual Capital Disclosure. Journal of Business Ethics, 100(3), 483–495. https://doi.org/10.1007/s10551-010-0692-x

- Islam, A. U. (2020). Do Shareholder Activism Effect Corporate Governance and Related Party Transactions: Evidences from India? Indian Journal of Corporate Governance, 13(2), 165–189. https://doi.org/10.1177/0974686220966810

- Jadiyappa, N., Sisodia, G., Joseph, A., Shrivastsava, S., & Jyothi, P. (2021). Creditors’ governance, information asymmetry and debt diversification: Evidence from India. International Journal of Managerial Finance, 17(2), 282–302. https://doi.org/10.1108/IJMF-01-2020-0013

- Kamath, B. (2019a). Impact of corporate governance characteristics on intellectual capital performance of firms in India. International Journal of Disclosure and Governance, 16(1), 20–36. https://doi.org/10.1057/s41310-019-00054-0

- Kanojia, S., Sachdeva, S., & Sharma, J. P. (2020). Retaliatory effect on whistle blowing intentions: A study of Indian employees. Journal of Financial Crime, 27(4), 1221–1237. https://doi.org/10.1108/JFC-12-2019-0170

- Kapoor, N., & Goel, S. (2017). Board Characteristics, Firm Profitability and Earnings Management: Evidence from India. Australian Accounting Review, 27(2), 180–194. https://doi.org/10.1111/auar.12144

- Katti, S., & Raithatha, M. (2018). Governance practices and agency cost in emerging market: Evidence from India. Managerial and Decision Economics, 39(6), 712–732. https://doi.org/10.1002/mde.2940

- Kumar, S., Sharma, D., Rao, S., Lim, W. M., & Mangla, S. K. (2022). Past, present, and future of sustainable finance: Insights from big data analytics through machine learning of scholarly research. Annals of Operations Research. https://doi.org/10.1007/s10479-021-04410-8

- Kumar, N., & Singh, J. P. (2013). Effect of board size and promoter ownership on firm value: Some empirical findings from India. Corporate Governance (Bingley), 13(1), 88–98. https://doi.org/10.1108/14720701311302431

- Li, C., Wu, K., & Wu, J. (2017). A bibliometric analysis of research on haze during 2000–2016. Environmental Science and Pollution Research, 24(32), 24733–24742. https://doi.org/10.1007/s11356-017-0440-1

- MacAskill, S., Roca, E., Liu, B., Stewart, R. A., & Sahin, O. (2021). Is there a green premium in the green bond market? Systematic literature review revealing premium determinants. Journal of Cleaner Production, 280, 124491. https://doi.org/10.1016/j.jclepro.2020.124491

- Machold, S., & Vasudevan, A. K. (2004). Corporate governance models in emerging markets: The case of India. International Journal of Business Governance and Ethics, 1(1), 56–77. https://doi.org/10.1504/IJBGE.2004.004897

- Maji, S. G., & Saha, R. (2021). Gender diversity and financial performance in an emerging economy: Empirical evidencefrom India. Management Research Review, 44(12), 1660–1683. https://doi.org/10.1108/MRR-08-2020-0525

- Majumder, A., Maiti, S. K., & Banerjea, S. (2012). Corporate governance codes in BRICS nations: A comparative study. Indian Journal of Corporate Governance, 5(2), 149–169.

- Mangala, D., & Kumari, P. (2017). Auditors’ perceptions of the effectiveness of fraud prevention and detection methods. Indian Journal of Corporate Governance, 10(2), 118–142. https://doi.org/10.1177/0974686217738683

- Mehrotra, S., Mishra, R. K., Srikanth, V., Tiwari, G. P., & Kumar, E. V. M. (2020). State of Whistleblowing Research: A Thematic Analysis. FIIB Business Review, 9(2), 133–148. https://doi.org/10.1177/2319714519888314

- Minimol, M. C., & Khong, P. L. (2021). Gender Diversity and Firm Performance: Evidences from Emerging Markets. Economic Research Guardian, 11(1), 156–169.

- Mittal, S., & Lavina. (2018). Females’ Representation in the Boardroom and Their Impact on Financial Distress: An Evidence from Family Businesses in India. Indian Journal of Corporate Governance, 11(1), 35–44. https://doi.org/10.1177/0974686218763857

- Norris, M., & Oppenheim, C. (2007). Comparing alternatives to the Web of Science for coverage of the social sciences’ literature. Journal of Informetrics, 1(2), 161–169. https://doi.org/10.1016/j.joi.2006.12.001

- Pahi, D., & Yadav, I. S. (2021). Dividend Behavior of Indian Firms: New Evidence from Large Data Set. Journal of Asia-Pacific Business, 22(1), 4–38. https://doi.org/10.1080/10599231.2021.1866396

- Panda, B., & Bag, D. (2019). Does ownership structure affect firm performance in an emerging market? The Case of India. Asian Journal of Business and Accounting, 12(1), 189–227. https://doi.org/10.22452/ajba.vol12no1.7

- Pant, A., & Radhakrishnan, G. (2019). Corporate governance challenges in Indian banks: A public affairs perspective. Journal of Public Affairs, 19(4). https://doi.org/10.1002/pa.1946

- Paul, J., Lim, W. M., O’Cass, A., Hao, A. W., & Bresciani, S. (2021). Scientific procedures and rationales for systematic literature reviews (SPAR-4-SLR). International Journal of Consumer Studies. https://doi.org/10.1111/ijcs.12695

- Pillania, R. K. (2012). Corporate Governance in India: Study of the Top 100 Firms. Journal of Applied Economic Sciences (JAES), 7(19), 87–92.

- Potharla, S., Bhattacharjee, K., & Iyer, V. Institutional ownership and earnings management: Evidence from India. 2021. Cogent Economics and Finance. 9, 1. https://doi.org/10.1080/23322039.2021.1902032

- Purayil, P. V., & Lukose, P. J. (2020). Ownership dilution and earnings management: Evidence from Indian IPOs. Managerial Finance, 46(3), 344–359. https://doi.org/10.1108/MF-02-2019-0068

- Rajab, B., & Handley-Schachler, M. (2009). Corporate risk disclosure by UK firms: Trends and determinants. World Review of Entrepreneurship, Management and Sustainable Development, 5(3), 224–243. https://doi.org/10.1504/WREMSD.2009.026801

- Rajput, M., & Jhunjhunwala, S. (2019). Corporate governance and payout policy: Evidence from India. Corporate Governance (Bingley), 19(5), 1117–1132. https://doi.org/10.1108/CG-07-2018-0258

- Saggar, R., & Singh, B. (2017). Corporate governance and risk reporting: Indian evidence. Managerial Auditing Journal, 32(4–5), 378–405. https://doi.org/10.1108/MAJ-03-2016-1341

- Sahoo, S., Kumar, S., Sivarajah, U., Lim, W. M., Westland, J. C., & Kumar, A. (2022). Blockchain for sustainable supply chain management: Trends and ways forward. Electronic Commerce Research, 1–56. https://doi.org/10.1007/s10660-022-09569-1

- Sarkar, J., & Sarkar, S. (2009). Multiple board appointments and firm performance in emerging economies: Evidence from India. Pacific Basin Finance Journal, 17(2), 271–293. https://doi.org/10.1016/j.pacfin.2008.02.002

- Sasidharan, A. (2020). Does board Independence enhance firm value of state-owned enterprises? Evidence from India and China. European Business Review, 32(5), 785–800. https://doi.org/10.1108/EBR-09-2019-0224

- Sehrawat, N. K., Kumar, A., Lohia, N., Bansal, S., & Agarwal, T. (2019). Impact of corporate governance on earnings management: Large sample evidence from India. Asian Economic and Financial Review, 9(12), 1335–1345. https://doi.org/10.18488/journal.aefr.2019.912.1335.1345

- Sehrawat, N. K., Singh, S., & Kumar, A. (2020a). Does corporate governance affect financial performance of firms? A large sample evidence from India. Business Strategy and Development, 3(4), 615–625. https://doi.org/10.1002/bsd2.126

- Sehrawat, N. K., Singh, S., & Kumar, A. (2020b). Does corporate governance affect financial performance of firms? A large sample evidence from India. Business Strategy and Development, 3(4), 615–625. https://doi.org/10.1002/bsd2.126

- Shanmugasundaram, S. (2020). Internationalization and governance of Indian family-owned business groups. Journal of Family Business Management, 10(1), 76–94. https://doi.org/10.1108/JFBM-06-2019-0040

- Shukla, A., Narayanasamy, S., Ayyalusamy, K., & Pandya, S. K. (2021). Influence of independent directors on the market risks of Indian banks. Journal of Asia Business Studies, 15(1), 31–49. https://doi.org/10.1108/JABS-01-2020-0010

- Srivastava, V., Das, N., & Pattanayak, J. K. (2018). Corporate governance: Mapping the change. International Journal of Law and Management, 60(1), 19–33. https://doi.org/10.1108/IJLMA-11-2016-0100

- Srivastava, V., Das, N., & Pattanayak, J. K. (2019). Impact of corporate governance attributes on cost of equity: Evidence from an emerging economy. Managerial Auditing Journal, 34(2), 142–161. https://doi.org/10.1108/MAJ-01-2018-1770

- Stechemesser, K., & Guenther, E. (2012). Carbon accounting: A systematic literature review. Journal of Cleaner Production, 36, 17–38. https://doi.org/10.1016/j.jclepro.2012.02.021

- Uppal, N. (2020). CEO narcissism, CEO duality, TMT agreeableness and firm performance: An empirical investigation in auto industry in India. European Business Review, 32(4), 573–590. https://doi.org/10.1108/EBR-06-2019-0121

- Uzma, S. H. (2016). Embedding corporate governance and corporate social responsibility in emerging countries. International Journal of Law and Management, 58(3), 299–316.

- van Eck, N. J., & Waltman, L. (2017). Citation-based clustering of publications using CitNetExplorer and VOSviewer. Scientometrics, 111(2), 1053–1070. https://doi.org/10.1007/s11192-017-2300-7

- Wasan, P., & Mulchandani, K. (2020). Corporate governance factors as predictors of earnings management. Journal of General Management, 45(2), 71–92. https://doi.org/10.1177/0306307019872304

- Zheng, C., & Kouwenberg, R. (2019). A Bibliometric Review of Global Research on Corporate Governance and Board Attributes. Sustainability, 11(12), 3428. https://doi.org/10.3390/su11123428