Abstract

The purpose of this study is to determine how corporate social responsibility (CSR) promotes the financial performance of the telecom industry in Ghana. The study developed the role of mediating and moderating variables such as corporate reputation (CR) and customers’ purchasing intention (CPI). This study uses cross-sectional data from the telecom industry in Ghana. The structural equation model was employed through Smart PLS to explain the relationships between CSR and the firm’s financial performance. The findings indicate a positive and significant impact of CSR on firms’ financial performance. This implies that CSR has a direct relationship with a firm’s performance. The study has also revealed that CSR has a positive and significant effect on a firm’s performance through the mediating role of CPI. The finding again indicates that CR does not mediate the relationship between CSR and FP. The finding further shows that CPI does not play any moderating role between CSR and a firm’s financial performance. This study has added to empirical research to the body of knowledge on CSR and firms’ performance in the telecom industry. Entrepreneurs and senior management might use the study’s findings to improve a company’s success. A valuable contribution to this study is the mediating and moderating impact of CR and CPI, which can be reinforced further in future studies.

1. Introduction

The concept of corporate social responsibility (CSR) has recently received a lot of interest in both the academic and commercial worlds. Businesses employ CSR to acquire a competitive edge and forge synergistic relationships with stakeholders. In industrialised countries, the concept of corporate social responsibility (CSR) is well-known, and the application of CSR by businesses is crucial for sustaining the ecosystem for sustainable development, which benefits society, the environment, stakeholders, and the organisation. In developing nations, corporate social responsibility (CSR) is gaining popularity; yet, in certain circumstances, such as Ghana, the adoption of CSR in a business setting is not voluntary due to a lack of emphasis on the potential benefits of CSR. Corporate social responsibility (CSR) is a concept in management that encourages businesses to incorporate social and environmental issues into their everyday operations and relationships with stakeholders.

There are different viewpoints and definitions of corporate social responsibility (CSR), for instance, (Harjoto & Laksmana, Citation2018). Still, Carroll’s (Citation1991) definition of CSR as a concept that combines society’s economic, ethical, moral, business, and legal expectations of corporations is the most frequently used in research. According to Chuang et al., Citation2018; Wang et al., Citation2020; Endrikat et al., Citation2020, corporate social responsibility incorporates social and environmental concerns into corporations’ actions and the consideration of stakeholders’ concerns. Businesses should focus on non-financial goals, such as social and environmental difficulties, to ensure that their economic activities are environmentally and socially sustainable, regardless of the financial objectives that must be reached (Franks et al., Citation2014). According to a substantial body of research, CSR has various effects, primarily on firm financial performance.

Even though numerous studies have investigated the influence of CSR on the financial success of businesses, the current empirical evidence is inconsistent for instance, (Rhou et al., Citation2016; Theodoulidis et al., Citation2018; Cho et al., Citation2019; Nirino et al., Citation2020; Wei et al., Citation2020; Tiep et al., Citation2020; Mitra, Citation2021; Achour & Boukattaya, Citation2021) who found a negative relationship between CSR and firms’ financial performance. While some studies (Nguyen, Citation2018; Shabbir, Citation2018; Long et al., Citation2020; Tangngisalu et al., Citation2020; Tiep et al., Citation2020; Okafor et al., Citation2021; Dakhli, Citation2021) indicate a positive association between the two variables. Most of these studies have been carried out in developing countries while less attention has been given to the topic in developing countries. In addition, there has been an increase in awareness of corporate social responsibility lately in Ghana but not much study has been conducted on the topic. This study reexamined the impact of CSR strategies on financial performance in the context of a firm’s financial performance in light of the contradictory findings about the relationship between CSR strategies and financial performance.

2. Literature review

2.1. Theoretical review

Through the use of several theoretical frameworks, the relationship between corporate social responsibility and financial success has been studied. This study will expand on three theories: the stakeholders’ theory of CSR, the business ethics theory of CSR, and the shareholders’ value theory of CSR. In the 1990s, the stakeholder theory gained popularity as an alternative to and challenge to the shareholder value theory (Freeman, Citation1984). It asserts that the number of stakeholder pressure groups has substantially expanded since the 1960s and that the significance of stakeholder pressures should not be underestimated. As ethical and pragmatic as it should be, business success presupposes a larger spectrum of stakeholder interests than just those of shareholders. Stakeholder theory gives distinct social issues precedence over issues unrelated to the organisation. CSR is therefore described as the responsibility of the company’s stakeholders.

The foundation of business ethics is a more outstanding social obligation and the moral obligation corporations have to society (Bigg, Citation2004). This approach validates CSR based on three interconnected ethical arguments: Changing and increasing social reactions and social expectations for various social crises are examples. Eternal or intrinsic moral values are characterised as normative and universal principles like social justice, fairness, and human rights, and Kantian ethics always drives them. Corporate citizenship is the role of a company in society as a better citizen who contributes to social welfare. According to the business ethics framework, CSR is considered a philanthropic and ethical responsibility rather than a legal and commercial one. CSR emerges where legal obligations begin to fade.

According to the shareholder value theory, as described by Nobel Laureate Milton Friedman in 1970, a company’s primary social purpose is to maximise profits while abiding by the law. Neoclassical economists such as Hayek argue that the role of business is to conduct transactions that benefit society and the economy and that this function should not be confused with other social activities performed by non-profit organisations and governments. Otherwise, it is not the most effective method of distributing resources in a free market. Economists such as agency theorists believe that the corporation’s owners are its managers and stakeholders and that, as agents, they have a fiduciary duty to prioritise the shareholders’ interests.

2.2. Empirical review

Financial performance and corporate social responsibility have been the subject of several studies (Rhou et al., Citation2016; Martinez-Conesa et al., Citation2017; Wei et al., Citation2020; Tiep et al., Citation2020; Nirino et al., Citation2020; Mitra, Citation2021; Dakhli, Citation2021). Despite this, empirical evidence on CSR has been contradictory. Therefore, additional research on the connection between CSR and financial performance is necessary. According to researchers, the inconsistent findings about the effects of CSR on business performance are due to a lack of clarity in the CSR dimension and the use of multiple firm performance measures (Margolis & Walsh, Citation2003; Wood & Jones, Citation1995). Numerous academics have utilised aggregated CSR dimensions/scores to examine the relationship between CSR and enterprise value (Park & Lee, Citation2009; Lee & Park, Citation2009, 2010). As the notion that CSR has many traits and motivations has strengthened (Clarkson, Citation1995; Aragon-Correa et al., Citation2008), a small number of studies in the hospitality literature have endeavoured to study the various facets of the CSR dimension (Kang et al., Citation2010; Kim & Kim, Citation2014; Lee et al., Citation2013).

Basuony et al. (Citation2014) investigate the influence of corporate social responsibility (CSR) on business performance. They discovered that corporate social responsibility substantially impacts the performance of businesses. In addition, they assert that all CSR dimensions have a substantial relationship with a company’s financial performance. They concluded by stating that more significant and older firms have a beneficial impact on financial performance (profitability), leading to an increase in the use of better CSR practices. Martinez-Conesa et al. (Citation2017) utilise structural equation modelling to evaluate the relationship between organisational innovation and firm performance for a sample of 552 Spanish businesses. The results indicate that innovation performance somewhat mediates the relationship between CSR and business performance. Rana (Citation2018) studies the effect of Corporate Social Responsibility (CSR) on the financial performance of Pakistan Stock Exchange-listed pharmaceutical companies. In this study, spending on Education, Healthcare, and the Environment, as well as donations and the Workers Welfare Fund, were used as proxies for CSR measurement, and Earnings per Share (EPS), Financial success was measured using Return on Assets (ROA) and Return on Equity (ROE). According to the research, CSR has a positive effect on the financial performance of a company. He emphasised that CSR is a crucial tool for Pakistan’s pharmaceutical business growth.

Azumah (Citation2020) examines the influence of Corporate Social Responsibility (CSR) on the performance of Nigerian manufacturing firms. Case study of Ariaria shoe manufacture and footwear company ltd, Abia State, Nigeria (2005–2006). Annual aggregate data were subjected to ordinary least square regression to determine the nature of the link between the dependent and independent variables. Profit after tax (PAT), asset financial value (AFV), and return on investment were the performance indicators (ROI). Non-financial performance indicators include the average manufacturing capacity utilisation (AMCU), the employee productivity rate (EMR), and the business output rate (COR). The findings indicate that CSR positively and significantly impacts manufacturing enterprises’ financial and non-financial performance. Nirino et al. (Citation2020) examine the effect of corporate social responsibility (CSR) on the financial performance (F.P) of enterprises in the food and beverage (F&B) industry.

The researchers employed a conceptual model that predicts a positive impact of CSR governance on CSR outcomes (environmental and social) and their influence on a company’s financial performance. The results indicate that CSR has varied effects on financial performance. Tiep et al. (Citation2020) examine the impact of corporate social responsibility (CSR) on business performance by analysing the function of mediating variables such as corporate reputation (C.R) and customer purchasing intent (CPI). The study used qualitative and quantitative methodologies, such as Smart PLS, to evaluate firm data in 2019 in southern Vietnam (SEM). The findings show that corporate social responsibility has a favourable and statistically significant impact on business success through the mediating roles of C.R and CPI

Dakhli (Citation2021) examines the relationship between corporate social responsibility (CSR) and firms’ financial success and the impact of audit quality on this connection. The research utilises a panel dataset of 200 French companies listed between 2007 and 2018. CSR has a positive effect on financial performance proxies such as return on assets (ROA), return on equity (ROE), and Tobin’s Q (T.Q), indicating that engaging in social activities may help companies achieve better financial results. According to him, the influence of CSR on corporate financial performance is more substantial for firms audited by the Big Four. This empirical research has supported the claims made by experts regarding the mixed impact of CSR on a company’s performance. This suggests that the varied effects of CSR on a company’s performance were due to the clarity of the CSR dimension and the usage of numerous firm performance measurements (Wood & Jones, Citation1995; Margolis & Walsh, Citation2003). In addition, the empirical evaluation revealed that CSR research had been undertaken in several economic jurisdictions and industry sectors, with various performance criteria for each region.

2.2.1. Corporate social measures

CSR is a long-term development concept that encompasses all aspects of society, including environmental concerns, social welfare, education, and global warming (McWilliams et al., Citation2006; Lai et al., Citation2010). CSR includes sponsorship, philanthropic events, volunteer work, and other creative endeavours (Polonsky and Speed, Citation2001; Lichtenstein et al., Citation2004). Consideration of CSR as a marketing strategy is crucial for businesses. As an inherent part of their operations, many multinational organisations encourage global enterprises to engage in corporate social responsibility (Oberseder et al., Citation2011; Green and Peloza, Citation2014). CSR is increasingly the main marketing focus and is essential to a company’s marketing and branding efforts. CSR emphasises finances and environmental awareness (Waagstein, Citation2011; Oberseder et al., Citation2014). Participation in CSR activities provides various benefits for businesses, including image enhancement, brand development, excellent sales, an enhanced reputation, and a change in customer attitudes. (Lai et al., Citation2010; Groza et al., 2011).

According to Fombrun et al. (2015), CSR may be measured based on the following criteria: product and service quality, innovation and creativity, working environment, compliance, civil rights, leadership and performance, and productivity. Although CSR demonstrates a corporation’s responsibility to society, it also indicates that enterprises that offer consumers goods and services are becoming more aware of their social responsibilities, environmental preservation, and ecological balance.

2.2.2. Corporate social responsibility (CSR) and firms performance (F.P)

According to McWilliams and Siegel (Citation2001), CSR has positive, negative, and neutral effects on companies’ financial success. Crisostomo et al. (Citation2011) discovered a negative link between corporate social responsibility (CSR) and firm value in Brazil because consumers and the capital market do not appreciate CSR. Friedman (1970) and advocates of the utility theory believe that CSR does not boost corporate value because it often incurs additional expenditures that put the firm at a disadvantage relative to less socially responsible firms (e.g., Vance, Citation1975; Aupperle et al., Citation1985). On the other hand, research that finds no association between CSR and firm performance argues that too many variables are at play. Therefore no relationship should be anticipated (Ullmann, 1985). Others have concluded that such firms are compensated by various direct and indirect benefits, including increased company goodwill, which enhances the company’s image and creates a positive relationship between social responsibility and financial performance Beurden & Gossling, 2008).

New empirical research demonstrates that CSR and company performance has a small but positive correlation (Aguinis & Glavas, Citation2012). According to DiSegni et al. (Citation2015), companies that actively promote social responsibility and environmental sustainability have much higher profit metrics than their industry and sector. Chen and Wang discovered, based on data collected in China in 2007 and 2008, that firms’ social responsibility initiatives can improve their financial success in the current year and have significant implications for their financial performance in future years. Multiple studies, including Yu. and Choi, 2014; Ilona and Kazlauskaite, 2012; Arendt and Brettel, Citation2010; Vilanova et al., 2009; Beurden and Gossling, Citation2008; and Smith and Higgins, 2000, found a statistically significant positive correlation between corporate social responsibility and overall firm performance (CSR). The following hypothesis, which parallels earlier research, is advanced:

Hypothesis 1. Corporate social responsibility positively and significantly impacts the Firm’s Performance (F.P).

2.2.3. Corporate social responsibility (CSR) and corporate reputation (C.R)

According to Ali (Citation2011), the CSR function of companies and organisations was demonstrated more clearly and to a much greater extent throughout the 1990s than was previously thought. Consequently, the extensive range of CSR activities they engage in encompasses, among other things, business ethics, labour practices, community responsibilities, and reducing environmental consequences from production and communal activities. Improving and building a company’s image in the community and society is a strategic decision. Concurrently, C.R. is being built into society. According to Kotler (Citation2005), CSR will aid companies in enhancing their brand position, reputation, and image. Moreover, according to Dimosthenis et al. (Citation2015), social responsibility enhances brand image and firm standing, increases sales, fosters employee commitment and loyalty, boosts productivity, enhances quality, and offers additional benefits. This study analyses the direct and indirect implications of corporate social responsibility in a developing economy and new ways CSR may impact corporate responsibility. Thus, it is assumed that CSR has a beneficial effect on C.R. Hence research hypothesis two and three was:

Hypothesis 2. Corporate social responsibility is positively related to corporate reputation.

Hypothesis 3. Corporate reputation mediates the relationship between corporate social responsibility (CSR) and firms’ performance.

2.2.4. Corporate social responsibility (CSR) and consumer’s purchasing intention (CPI)

Several kinds of research have investigated the correlation between CSR and the actions of various stakeholders. Ali et al. (Citation2010) examined the relationship between corporate social responsibility and customer behaviour. Ali et al. (Citation2011) examined the influence of CSR on investor behaviour. While Ali et al. (Citation2010) looked at how CSR affects employee behaviour at work, this current study looked at how CSR affects employee behaviour outside of the workplace. Holmes and Kilbane (Citation1993), Berger et al. (Citation1999); Mohr et al. (Citation2001); Nelling and Webb (Citation2006); Sen and Bhattacharya (2001) studied the effect of CSR on CPI in the interim. Hence, the fourth hypothesis:

Hypothesis 4. Customer Purchasing Intention (CPI) is positively influenced by Corporate Social Responsibility (CSR) practices.

2.2.5. Corporate reputation (C.R.) and firms’ performance (F.P.)

According to Rose and Thomsen (Citation2004), a company’s corporate reputation is an intangible asset that directly or indirectly affects its financial performance. Conversely, a company’s financial . According to Ali (Citation2011), stakeholders objectively perceive the essential aspects of a company’s reputation. These criteria are brand reputation, company image, social contribution value, and operational transparency. According to a prior study, organisations must be profitable before their performance may be enhanced by enhancing their reputation. This means businesses must first meet their duties to shareholders and investors to free up funds for non-economic activities (such as philanthropy) to achieve CSR goals. These activities are a strategic tool for strengthening the organisation’s reputation (Porter & Kramer, Citation2002; Walsh et al., Citation2009). Prior research has demonstrated that C.R. is a crucial component of the link between CSR and financial performance. Previous research has shown that C.R. moderately affects the relationship between CSR and F.P. Based on this theoretical foundation, hypothesis H5 is established as follows:

Hypothesis 5. Corporate reputation (C.R.) positively influences Firms’ Performance (F.P.)

2.2.6. Customers’ purchasing intention (CPI) and firms’ performance (F.P.)

According to Voss et al. (Citation2003), purchase intention is a measured customer attitude toward a given product or brand’s service. According to Bian and Moutinho (2011), buy intention is when a person plans to acquire goods or services from a particular brand. In other words, buying intention refers to a consumer’s purpose in purchasing a specific good or service from a particular brand (Dodds et al., Citation1991). According to Gupta and Zeithaml (Citation2006), purchase intention or consumer behaviour entails deciding when to purchase, how much to purchase, where to purchase, and other aspects of a particular product or service, resulting in increased sales, profits, and business performance. Based on this theoretical foundation, hypothesis H6 is established as follows:

Hypothesis 6. Customers’ purchase intention (CPI) has a positive effect on a Firm’s Performance (F.P.).

Hypothesis 7. Customers’ purchase intention (CPI) mediates the relationship between corporate social responsibility (CSR) and firms’ performance.

Hypothesis 8. Customers’ purchase intention (CPI) moderates the relationship between CSR and FP.

2.2.7. Firm’s performance (F.P.)

These include, among others, sales revenue, return on equity, return on assets, rate of return, revenue growth, liquidity ratio, liquidity ratio, and stock price. In this study, we apply Kotler’s performance measures (Kotler, Citation2005), including Increased sales and market share; Increased ability to attract, retain, and motivate people; Reduced costs; Improved corporate image and reputation; Increased investor attractiveness; and Strengthened brand positioning. Figure depicts the hypothesised relationships and variables.

Figure 1. Conceptual Framework.

3. Research methodology

3.1. Research approach

This study was carried out using both qualitative and quantitative techniques. This study evaluates the connection between CSR, C.R., CPI, and F.P. by the conceptual framework presented below. The study used the SEM technique to measure the four key variables under study.

3.2. Sample design and data collection

The population of this study included the Ghanaian telecom industry. After considering the number of telecom companies, the study chose a sample from the population of businesses in the region in the various provinces with 5–99 employees. The preliminary information was gathered by a 5-level structured questionnaire survey, where the first order correlated with uttering disagreement. The 5-level equates to completely agreeing because the amount of consent increases with the higher number. The sample size was determined based on the number of observed variables utilised in the study. The participants in this study were the Ghanaian telecom industry. Accordingly, the sample size is established using the study’s question-to-population ratio, which ranges from 5/1 to 10/1. (Hair et al., Citation2010). Since 35 variables in this study can be observed, 350 samples are required. However, the authors chose to disseminate 400 surveys to minimise hazards throughout the sample collection procedure. The simple approach of gathering samples of random probability was adopted.

3.3. Measurement of variables

Due to the theoretical construct’s complexity and the fact that measures of a single dimension offer a somewhat constrained view of a firm’s performance in the pertinent social and environmental domains, it was challenging to create a truly representative measure of CSR (Wolfe, Citation2003). A wide range of CSR measurements has been developed in earlier studies (Waddock & Graves, Citation1997). They consist of the Moskowitz reputational scales (Bowman & Haire, Citation1975; McGuire et al., Citation1988; Preston & O’Bannon, Citation1997), the Fortune reputational and social responsibility index, forced-choice survey instruments (Aupperle, Citation1991; Aupperle et al., Citation1985), content analysis of corporate documents (Wolfe, Citation2003), behavioural and perceptual measures, and case study methodology (Clarkson, Citation1995). Recent trends in the usage of corporate social responsibility data from KLD have greatly assisted the large number of CSR-related research that has been carried out (Margolis et al., Citation2007).

A thorough literature review served as the foundation for introducing measurement items. Operationalisations that had been shown effective in earlier studies were employed to facilitate cumulative research. The operationalisation of the variables using multi-item constructions. Items included environmental responsibility and CSR practices with the four stakeholders (suppliers, consumers, employees, and the local community). This concept was modified by Lindgreen et al. (Citation2009) and Hammann et al. (Citation2009). The following factors were used to measure innovation performance in earlier research (Bocquet et al., Citation2013; Lee & Choi, Citation2003; Manu, Citation1992). These factors reflect the company’s innovation concerning new or improved products (goods or services) and processes.

According to respondents’ ratings of their organisation’s success compared to competitors in the market, items from other studies (Aragon-Correa et al., Citation2008; Judge & Douglas, Citation1998; Quinn & Rohrbaugh, Citation1983) were used to operationalise firm performance. Objective data on the financial success of these businesses are rarely available, partly because the owners are not legally obligated to provide this data, hence perceptions of financial performance have previously been employed in the literature examining SMEs (Lubatkin et al., Citation2006). Additionally, this strategy was used because CEOs are widely believed to be knowledgeable sources, especially regarding their companies’ performance. Further, evidence indicates a high correlation between CEO self-reports of performance and objective measurements of corporate performance (He & Wong, Citation2004; Chang and Hughes, Citation2012). We selected a competitive performance-focused variable, similar to that employed by Marín et al. (Citation2012) or Gallardo-Vázquez and Sánchez-Hernández, to quantify company performance (2013).

4. Presentation and discussion of the results

4.1. Testing research model

According to Williams et al. (Citation1991) and Ritchie (Citation1992), testing a research model is done to ensure that it and its components are acceptable and adequate for the particular study setting. Basic statistics were performed, and PLS-SEM analysis included the assessment of Measurement and Structural Model was performed. The measurement model establishes the reliability and validity of the construct. The structural model ascertains the significance of hypothesised relationships. Different hypotheses were proposed to evaluate the relationship of predictors to the outcome.

H1: Corporate social responsibility has a positive and significant impact on performance.

H2: Corporate social responsibility is positively related to corporate reputation.

H3: Corporate reputation mediates the relationship between corporate social responsibility (CSR) and firms’ performance.

H4: Customer Purchasing Intention (CPI) is positively influenced by corporate social responsibility (CSR) practices.

H5: Corporate reputation (C.R.) positively influences firms’ performance (F.P.)

H6: Customers’ purchase intention (CPI) positively affects a Firms’ Performance (F.P.)

H7: Customer purchasing intention (CPI) mediates the relationship between corporate social responsibility (CSR) and firms’ performance.

H8: Customers’ purchase intention (CPI) moderates the relationship between CSR and F.P.

4.2. Measurement model

The quality of the constructs in the study is assessed based on the evaluation of the measurement of the model. The quality criteria assessment starts with evaluation factors loadings and establishes the construct reliability and construct validity.

4.3. Factor loading

The factor loading refers to the “extent to which each item in the correlation matrix correlates with the given principal component. According to Pett et al. (Citation2003), factor loading can range from −1.0 to + 1.0, with higher absolute values indicating a higher correlation of the item with the underlying factor. The factor loading is presented in Table .

Table 1. Factor Loading (FL)

4.4 Indicator multicollinearity

The Variance Inflation Factor (VIF) statistic is used to assess multicollinearity in the indicators (Fornell and Bookstein, Citation1982). According to Hair et al. (Citation2016), multicollinearity is not a severe issue if VIF values are below 5. Table presents the VIF values for the indicators in the study and reveals that the VIF for each indicator is below the recommended value.

Table 2. Indicator Multicollinearity

4.5. Reliability analysis

According to Mark (1996), reliability is the extent to which a measuring instrument is stable and consistent. The essence of reliability is repeatability. “If an instrument is administered repeatedly, will it yield the same result” (P. 285)? The most commonly used methods for establishing reliability include Cronbach Alpha and Composite Reliability (C.R.). The results for both Cronbach Alpha and Composite Reliability results are presented in Table . The Cronbach Alpha ranged from .832 to .894, whereas Composite Reliability statistics ranged from .877 to .919. Both reliability indicators have a value over the required threshold of .70 (Hair et al., Citation2011). Hence, construct reliability is established.

Table 3. Cronbach’s alpha evaluation results and composite reliability

4.6. Convergent validity

Convergent validity is the degree to which multiple attempts to measure the same concept agree. The idea is that two or more measures of the same thing should covary if they are valid measures of the concept (Bagozzi et al., Citation1991, p 423). When the AVE value exceeds or exceeds the recommended value of 0.50, items converge to measure the underlying construct and establish convergent validity (Fornell and Larcker, Citation1981). Convergent validity results based on the AVE statistics show that all the constructs except CPI CR, CSR, and F.P. have slightly lower than AVE. However, the C.R. values for all the constructs were more significant than 0.70. Hence convergent validity is not an issue. Table shows the result of AVE for each of the constructs.

Table 4. Construct Convergent Validity (AVE)

4.7. Fornell and lacker criterion

According to Fornell and Larcker’s (Citation1981) criterion, discriminant validity is established when the square root of AVE for a construct is greater than its correlation with all other constructs. In this study, the square root of AVE (in Bold Italics) for a construct was greater than its correlation with other constructs except for access to finance (Table ). Hence, providing strong support for the establishment of discriminant validity.

Table 5. Discriminant Validity—Fornell and Larcker Criterion

4.8. Heterotrait -monorait ratio (HTMT)

HTMT is based on the estimation of the construct. Discriminant validity is established on the HTMT ratio. However, the threshold for HTMT has been debated in the existing literature. For example, Kline (Citation2011) suggested a threshold value of 0.85 or less, while Teo et al. (Citation2008) recommend a liberal threshold value of 0.90 or less. The HTMT in Table shows that the HTMT ratio is less than the required threshold of 0.90.

Table 6. Discriminant Validity—HTMT

4.9. The goodness of fit (Model’s predictive)

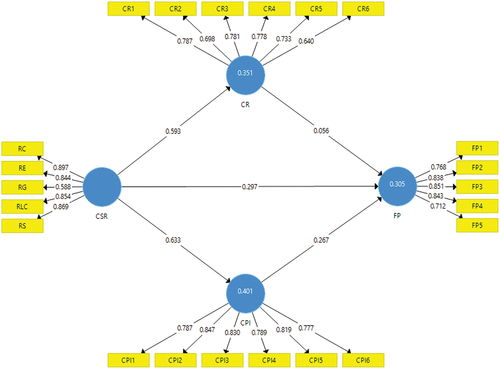

To ascertain the best fits, the coefficient of determination (R2) was. The analysis results reveal an R2 value of 0.401 for customer purchasing intention, 0.351 for corporate reputation and 0.305 for financial performance. This indicates that a 40.1% variation in customer purchasing intention can be attributed to corporate social responsibility. It also shows that a 35.1% variation in corporate reputation can explain corporate social responsibility and it further revealed that a 30.5% variation can be attributable to corporate social responsibility, corporate reputation and customer purchasing intention. Based on the recommended 0.10 cutoff value proposed by Falk and Miller (Citation1992), results indicated that this model obtained acceptable R2 statistics for the variables. Figure show the result of the R2 which is more that the recommended value suggested by Falk and Miller (Citation1992).

Figure 2. Measurement Analysis Result.

4.10. Structural model

The next step in structural modelling is assessing the hypothesised relationship to substantiate the proposed hypotheses.

4.11. Hypothesis testing

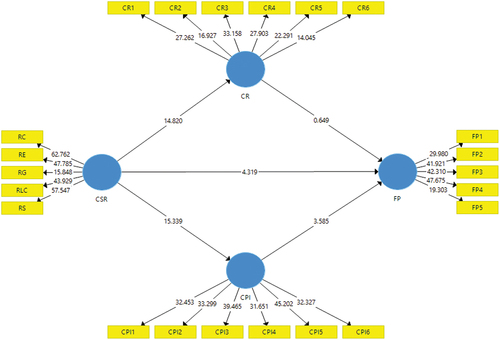

The study tested eight hypotheses. The first hypothesis evaluates whether corporate social responsibility positively and significantly impacts the firms’ performance. The result shows that CSR has a direct effect on firms’ performance (β = 0.298, t = 4.319, p < 001). The study concludes that CSR is positively related to the firm’s performance. Hence, Hypothesis 1 was accepted. The second hypothesis evaluates the positive relationship between corporate social responsibility and corporate reputation. The result indicates that CSR is positively related to CR (β = 0.593, t = 14.82, p < 001). Hence, the H2 is accepted.

The study also reveals that corporate social responsibility directly affects customers’ purchasing intention (β = 0.633, t = 15.339, p < 001). The study concludes that CSR influences the customer’s purchasing intention, improving the firms’ performance. Therefore, hypothesis 4 was accepted. The fifth hypothesis proposed that corporate reputation (C.R) positively influences firms’ performance (F.P). The finding shows a positive relationship between corporate reputation and firms’ performance, but statistically insignificant (β = 0.055, t = 0.649, p = 0.517). Hence the hypothesis was not accepted. The result further reveals that customers’ purchasing intention has a direct relationship with the firm’s performance (β = 0.268, t = 0.3.585, p < 001). Therefore, hypothesis 6 was accepted.

4.12. Mediation relationship

Mediation analysis was performed to assess the mediating role of C.R on the relationship between CSR and FP. The results (see Table ) revealed that the total effect of CSR on FP was significant (H1: β = 0.500, t = 11.361, p < 001). With the inclusion of the mediating variables (CR), the impact of CSR on FP became significant (β = 0.298, t = 4.319, p < 001). The indirect effect of CSR on FP through CR was found insignificant (β = 0.032, t = 0.597, p = 0.551). This indicates that the relationship between CSR and FP is not mediated by CR. The study further checked the mediating role of CPI on the relationship between CSR and FP. The results (see, also Tables ) indicates that the total effect of CSR on FP was significant (H1: β = 0.500, t = 11.361, p < 001). With the inclusion of the mediating variables (CPI), the impact of CSR on FP became significant (β = 0.298, t = 4.370, p < 001). The indirect effect of CSR on FP through CPI was found significant (β = 0.170, t = 3.243, p < 001). This shows that the relationship between CSR and FP is partially mediated by CPI. Figure shows the result of the meditation role of CR between CSR and FP. Table shows the result of the R2 which is more that the recommended value suggested by Falk and Miller (Citation1992). See for the result of all the hypotheses tested in the studies. See Table for the result of all the hypotheses tested in the studies.

Figure 3. Modle Analysis Result.

Table 7. Goodness Fits

Table 8. Direct Relationship Result

Table 9. Mediation Analysis Result

Table 10. Moderation Result

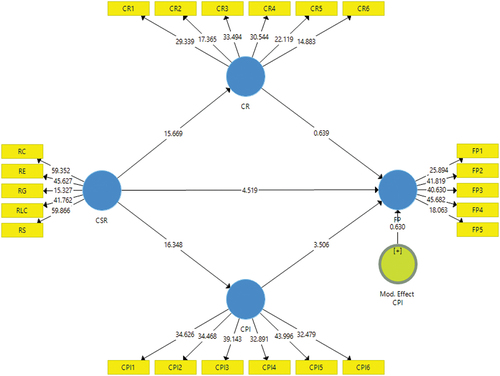

4.13. Moderation relationship

Moderation describes a situation in which the relationship between two constructs is not constant but depends on the values of a third variable, referred to as a moderator variable.

H8: Customers’ purchase intention (CPI) moderates the relationship between CSR and F.P.

The hypothesis sought to ascertain the moderating role or effect of customers’ purchase intention (CPI). The results revealed that customer purchase intention (CPI) does not moderate the relationship between corporate social responsibility (CSR) and financial performance (FP) (β = 0.070, t = 0.630, p = 0.529). Hence, the hypothesis was not supported. Figure depicts the results of the moderation relationship between CSR, CR, CPI and FP.

Figure 4. Moderation Analysis Result.

5. Discussion and conclusion

In this study, CSR plays a critical role in enhancing the company’s reputation (CR) and driving up purchasing intent (CPI). This finding is consistent with the finding by (Mubeen & Arooj, Citation2014; Singh, Citation2014; Rana, Citation2018; Nirino et al., Citation2020; Wei et al., Citation2020; Dakhli, Citation2021). However, this finding contradicts the work by Singh (Citation2014) who found a negative effect of CSR on the firm’s performance. On the other hand, CR and CPI have a substantial impact on the performance of firms (FP). Additionally, the finding suggests a positive significant impact of CSR on firms’ performance through the mediating role of CPI. As a result, companies that actively practise social responsibility will benefit from increased customer interest in doing business with them and reputational benefits. To maximise resources and get the best results, businesses should have a social responsibility strategy that focuses on the community and employees. Business performance will be enhanced due to social responsibility.

Research demonstrates that social responsibility helps businesses build their reputation, which in turn boosts customers’ propensity to make purchases. Therefore, to work toward a comprehensive performance, corporate executives need to be innovative. For these businesspeople to create conditions for their companies to grow more sustainably, they must find ways to improve society. Additionally, CSR aids in enhancing a company’s reputation with clients and business partners, giving it a competitive edge and a leg up when attracting investment, particularly international investment.

The findings of this study can be fascinating and helpful to managers, policymakers, and investors. They also have practical ramifications. This study encourages board members to carefully consider investing financial resources in creating policies that raise the levels of social behaviour components in order to improve overall corporate performance because they emphasise the significance of CSR as a significant driver of financial performance. Despite the crucial role the telecom sector has played over the years in the CSR space, which has increased the concept of CSR’s legitimacy, this research argues that policymakers and regulators should continue to encourage CSR practices among businesses. The findings offer investors advice for companies looking to boost company performance through high-quality staff hiring as well as participation in social activities.

Despite these benefits, there are certain limitations to this study that could be resolved in follow-up investigations. The choice of independent variables and the study’s industry constitute the initial restriction. The study only considers CSR as one independent variable. In order to give a thorough analysis of corporate social responsibility drivers, future research may also take into account additional independent variables, such as the age of the firm, the industry it operates in, the makeup of the board of directors, etc.

Author’s contributions

The authors acknowledge that they made a significant original contribution to the study. The final document was read and approved by the author(s).

Availability of data and materialss

We affirm that the information in this paper is original and that the author/researcher did the original research from which it was derived.

Conflicts of interest

We have studied the instructions on competing interests and can attest that none of the authors has any, either financial or non-financial, competing interests in the paper.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Aguinis, H., & Glavas, A. (2012). What We Know and Don’t Know About Corporate Social Responsibility: A Review and Research Agenda. J. Manag, 38, 932–19. https://doi.org/10.1177/0149206311436079

- Ali, I. (2011). Influence of corporate social responsibility and corporate reputation on the development of consumer purchase intentions. Romanian Review of Social Sciences, 1, 19–27.

- Ali, I., Rehman, K. U., Ali, S. I., Yousaf, J., & Zia, M. (2010). Corporate social responsibility influences on employee retention and organizational performance. African Journal of Business Management, 4(13), 2796–2801.

- Aragon-Correa, J. A., Hurtado-Torres, N., Sharma, S., & Garcia-Morales, V. J. (2008). Environmental strategy and performance in small firms: A resource-based perspective. Journal of Environmental Management, 86(1), 88e103. https://doi.org/10.1016/j.jenvman.2006.11.022

- Arendt, S., & Brettel, M. (2010). Understanding the influence of corporate social responsibility on corporate identity, image, and firm performance. Management Decision, 48(10), 1469–1492. https://doi.org/10.1108/00251741011090289

- Aupperle, K. E. (1991). The use of forced-choice survey procedures in assessing corporate social orientation. Res Corp. Soc. Perform Policy, 12, 269e279.

- Aupperle, K., Carroll, A., & Hatfield, J. (1985). An empirical examination of the relationship between corporate social responsibility and profitability. Academy of Management Journal, 28(2), 446e463. https://doi.org/10.2307/256210

- Azumah, J. (2020). Impact of Corporate Social Responsibility on the Performance of Manufacturing Firms in Nigeria. International Journal of Managerial Studies and Research, 8(7), 1–15. https://doi.org/10.20431/2349-0349.0807001

- Bagozzi, R. P., Yi, Y., & Phillips, L. W. (1991). Assessing Construct Validity in Organizational Research. Administrative science quarterly, 36, 421–458. https://doi.org/10.2307/2393203

- Basuony, M. A. K., Elseidi, R. I., & Mohamed, E. K. A. (2014). The impact of corporate social responsibility on firm performance: Evidence from a Mena country. Corporate Ownership and Control, 12(1CONT9), 761–774. https://doi.org/10.22495/cocv12i1c9p1

- Berger, I. E., Cunningham, P. H., & Kozinets, R. V. (1999). Consumer persuasion through cause-related advertising. Advances in Consumer Research, 26, 491–497.

- Beurden, P. V., & Gössling, T. (2008). The worth of values - a literature review on the relation between corporate social and financial performance. Journal of Business Ethics, 82(2), 407–424.

- Bocquet, R., Bas, C. L., Mothe, C., & Poussing, N. (2013). Are firms with different CSR profiles equally innovative? Empirical analysis with survey data. European Management Journal, 31(6), 642e654. https://doi.org/10.1016/j.emj.2012.07.001

- Bowman, E., & Haire, M. (1975). A strategic posture toward corporate social re-responsibility. California Management Review, 18(2), 49e58. https://doi.org/10.2307/41164638

- Chang, Y. -Y., & Hughes, M. (2012). Drivers of innovation ambidexterity in small-to medium-sized firms. Eur. Manag. J, 30(1), 1e17.

- Cho, S. J., Chung, C. Y., & Young, J. (2019). Study on the relationship between CSR and financial performance. Sustainability, 11(2), 343.

- Clarkson, M. (1995). A stakeholder framework for analysing and evaluating corporate social performance. The Academy of Management Review, 20(1), 92e118. https://doi.org/10.2307/258888

- Crisóstomo, V. L., De Souza Freire, F., & De Vasconcellos, F. C. (2011). Corporate social responsibility, firm value and financial performance in Brazil. Social Responsibility Journal, 7(2), 295–309. https://doi.org/10.1108/17471111111141549

- Dakhli, A. (2021). The impact of corporate social responsibility on firm financial performance: Does audit quality matter? Journal of Applied Accounting Research. https://doi.org/10.1108/JAAR-06-2021-0150

- Dimosthenis, T. M., & Apostolos, D. Z. (2015). The effects in the structure of an organization through the implementation of policies from corporate social responsibility (CSR). Procedia-Social and Behavioral Sciences, 148, 634–638.

- DiSegni, D. M., Huly, M., & Akron, S. (2015). Corporate social responsibility, environmental leadership and financial performance. Soc. Responsib. J, 11, 131–148.

- Dodds, W. B., Monroe, K. B., & Grewal, D. (1991). Effects of price, brand, and store information on buyers’ product evaluations. Journal of Marketing Research, 28, 307–319.

- Falk, R. F., & Miller, N. B. (1992). A Primer for Soft Modeling. University of Akron Press.

- Fornell, C., & Bookstein, F. L. (1982). Two Structural Equation Models: LISREL and PLS Applied to Consumer Exit-Voice Theory. Journal of Marketing Research, 19, 440–452. https://doi.org/10.2307/3151718

- Fornell, C., & Larcker, D. F. (1981). Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics. Journal of Marketing Research, 18, 382–388. https://doi.org/10.2307/3150980

- Freeman, R. E. (1984). Strategic Management. A Stakeholder Approach. Pitman.

- Gupta, S., & Zeithaml, V. (2006). Customer metrics and their impact on financial performance. Marketing Science, 25(6), 718–739.

- Hair, J., Black, W., Babin, B., & Anderson, R. (2010). Multivariate Data Analysis (7th ed.). Prentice Hall.

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2016). A primer on partial least squares structural equation modelling (PLS-SEM) (2nd ed.). Sage.

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–151.

- Hammann, J., Weber, R., & Lowenstein, R. (2009). Self-interest through delegation: An additional rationale for the principal-agent relationship. The American Economic Review, 5, 55e70.

- He, Z. L., & Wong, P. K. (2004). Exploration vs exploitation: An empirical test of the ambidexterity hypothesis. Organize. Sci, 15(4), 481e494.

- Holmes, J. H., & Kilbane, C. J. (1993). Cause-related marketing: Selected effects of price and charitable donations. Journal of Nonprofit and Public Sector Marketing, 7(4), 67–83.

- Judge, W. Q., & Douglas, T. J. (1998). An empirical assessment of performance implications of incorporating natural environmental issues into the strategic planning process. Journal of Management Studies, 35(2), 241. https://doi.org/10.1111/1467-6486.00092

- Kang, K. H., Lee, S., & Huh, C. (2010). Impacts of positive and negative corporate social responsibility activities on company performance in the hospitality industry. Int. J. Hosp. Manage, 29(1), 72–82.

- Kline, R. B. (2011). Principles and Practice of Structural Equation Modeling (3rd ed.). The Guilford Press.

- Kotler, P., & Lee, N. (2005). Corporate Social Responsibility: Doing the Best for Your Company and Your Cause. Wiley. com.

- Lai, C. S., Chiu, C. J., Yang, C. F., & Pai, D. C. (2010). The effects of corporate social responsibility on brand performance: The mediating effect of industrial brand equity and corporate reputation. Journal of Business Ethics, 95(3), 457–469.

- Lee, H., & Choi, B. (2003). Knowledge enablers. Processes and Organisational Performance: an Integrated View and Empirical Examination. J. Manag. Inf. Syst, 20(1), 179e228.

- Lindgreen, A., Swaen, V., & Johnston, W. J. (2009). Corporate social responsibility: An empirical investigation of U.S. organisations. Journal of Business Ethics, 85(2), 303e323. https://doi.org/10.1007/s10551-008-9738-8

- Lubatkin, M. H., Simsek, Z., Ling, Y., & Veiga, J. F. (2006). Ambidexterity and performance in small- to medium-sized firms: The pivotal role of top management team behavioural integration. J. Manag, 32(5), 646e672.

- Manu, F. A. (1992). Innovation orientation. Environment and Performance: a Comparison of U.S. and European Markets. J. Int. Bus. Stud, 23(2), 333e359.

- Margolis, J. D., Elfenbein, H. A., & Walsh, J. P., (2007). Does it Pay to Be Good? a Meta-analysis and Redirection of Research on Corporate Social and Financial Performance. Working Paper. Harvard Business School.

- Marín, L., Rubio, A., & Ruiz, D. M. (2012). Competitiveness as a strategic outcome of corporate social responsibility. Corp. Soc. Responsib. Environ. Manag, 19(6), 364e376.

- Martinez-Conesa, I., Soto-Acosta, P., & Palacios-Manzano, M. (2017). Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. Journal of Cleaner Production, 142, 2374–2383. https://doi.org/10.1016/j.jclepro.2016.11.038

- McGuire, J., Sundgren, A., & Schneeweis, T. (1988). Corporate social responsibility and firm financial performance. Academy of Management Journal, 31(4), 854e872. https://doi.org/10.2307/256342

- McWilliams, A., & Siegel, D. (2001). Corporate social responsibility: A theory of the firm perspective. Academy of Management Review, 26(1), 117–127.

- Mitra, N. (2021). Impact of strategic management, corporate social responsibility on firm performance in the post mandate period: Evidence from India. International Journal of Corporate Social Responsibility, 6(1), 1. https://doi.org/10.1186/s40991-020-00052-4

- Mohr, L. A., Webb, D. J., & Harris, K. E. (2001). Do consumers expect companies to be socially responsible? The impact of corporate social responsibility on buying behaviour. The Journal of Consumer Affairs, 55(1), 45–72.

- Mubeen, M., & Arooj, A. (2014). Impact of Corporate Social Responsibility on Firms’ Financial Performance and Shareholders’ wealth. European Journal of Business and Management, 6(31), 181–188.

- Nelling, E., & Webb, E. (2006), Corporate Social Responsibility and Financial Performance: The Virtuous Circle Revisited. Working Paper, Drexel University and Federal Reserve Bank of Philadelphia.

- Nirino, N., Miglietta, N., & Salvi, A. (2020). The impact of corporate social responsibility on firms’ financial performance, evidence from the food and beverage industry. British Food Journal, 122(1), 1–13. https://doi.org/10.1108/BFJ-07-2019-0503

- Oberseder, M., Schlegelmilch, B. B., & Gruber, V. (2011). Why don’t consumers care about CSR? A qualitative study exploring the role of CSR in consumption decisions. Journal of Business Ethics, 104(4), 449–460.

- Pett, M. A., Lackey, N. R., & Sullivan, J. J. (2003). Making Sense of Factor Analysis: The Use of Factor Analysis for Instrument Development in Health Care Research. SAGE Publications, Thousand Oaks. https://doi.org/10.4135/9781412984898

- Polonsky, M. J., & Speed, R. (2001). Linking sponsorship and cause-related marketing: Complementary and conflicts. European Journal of Marketing, 35(11/12), 1361–1389.

- Porter, M. E., & Kramer, M. R. (2002). The competitive advantage of corporate philanthropy. Harvard Business Review, 80, 56–68.

- Preston, L., & O’Bannon, D. (1997). The corporate social e financial performance relationship. Business & Society, 36(4), 419e430. https://doi.org/10.1177/000765039703600406

- Quinn, R. E., & Rohrbaugh, J. (1983). A spatial model of effectiveness criteria: Towards a competing values approach to organisational analysis. Manag. Sci, 29(3), 363e377.

- Rana, I. (2018). Impact of corporate social responsibility on financial performance evidence from pharmaceutical sector listed companies of Pakistan. European Business & Management, 4(1), 1. https://doi.org/10.11648/j.ebm.20180401.11

- Rhou, Y., Singal, M., & Koh, Y. (2016). CSR and financial performance: The role of CSR awareness in the restaurant industry. International Journal of Hospitality Management, 57, 30–39. https://doi.org/10.1016/j.ijhm.2016.05.007

- Ritchie, J. (1992). Becoming Bicultural. Huia Press.

- Rose, C., & Thomsen, S. (2004). The impact of corporate reputation on performance: Some Danish evidence. European Management Journal, 22, 201–210.

- Singh, S. (2014). Impact of corporate social responsibility disclosure on the financial performance of firms in the UK. Masters Thesis. Business Administration- Financial Management, 10(1), 9–19.

- Teo, T., Wong, S. L., & Chai, C. S. (2008). A cross-cultural examination of the intention to use technology between Singaporean and Malaysian pre-service teachers: An application of the TAM. Educational & Society, 11(4), 265–280.

- Tiep, L. T., Huan, N. Q., & Hong, T. T. T. (2020). Impact of corporate social responsibility on firms’ performance in southern enterprises of Vietnam. International Review of Management and Marketing, 10(4), 17–24.

- Vance, S. C. (1975). Are socially responsible corporations good investment risks?. Management review, 64(8), 19–24.

- Voss, K. E., Spangenberg, E. R., & Grohmann, B. (2003). Measuring the hedonic and utilitarian dimensions of consumer attitude. Journal of Marketing Research, 40(3), 310–320.

- Waagstein, P. R. (2011). The mandatory corporate social responsibility in Indonesia: Problems and implications. Journal of Business Ethics, 98(3), 455–466.

- Waddock, S. A., & Graves, S. B. (1997). The corporate social performance- financial per-performance link. Strategic Management Journal, 18(4), 303e319. https://doi.org/10.1002/(SICI)1097-0266(199704)18:4<303::AID-SMJ869>3.0.CO;2-G

- Walsh, G., Mitchell, V. W., Jackson, P. R., & Beatty, S. E. (2009). Examining the antecedent and consequences of corporate reputation: A customer perspective. British Journal of Management, 20, 187–203.

- Wei, A. P., Peng, C. L., Huang, H. C., & Yeh, S. P. (2020). Effects of Corporate Social Responsibility on Firm Performance: Does Customer Satisfaction Matter? Sustainability (Switzerland), 12(18), 1–18. https://doi.org/10.3390/su12187545

- Williams, D., Beard, J. D., & Rymer, J. (1991). Team projects: Achieving their full potential. Journal of Marketing Education, 13(1), 45–53.

- Wolfe, L. (2003). An annotated bibliography introduces path analysis of the social sciences and some emergent themes. Struct. Equ. Model, 10(1), 1e34.