Abstract

This study examines the impact of big data analytics capabilities (BDAC) on sustainability reporting disclosure on Facebook (SRDF) and the moderating impact of tone at the top’s attributes on the relationship between BDAC and SRDF. A total of 100 publicly listed companies (PLCs) in Malaysia that mentioned using social media during the year 2019 were chosen as this study’s sample. This study was underpinned by positivist research paradigm and used quantitative data collection methods (questionnaire and content analysis). Based on the structural equation modelling (SEM) employed, the results of the study showed that BDAC implementation had a significant impact on SRDF. The presence of a specific tone (certainty) at the top in Chief Executive Officer’s (CEO) letters strengthened the relationship between BDAC and SRDF, but other attributes of tone at the top showed insignificant results. This study acknowledges the important contribution of dynamic capabilities, such as BDAC and a specific tone at the top, i.e., certainty, in promoting sustainability reporting on social media from the perspective of dynamic capabilities view (DCV) theory. Thus, companies are suggested to implement BDAC and communicate certainty in the tone at the top to improve their sustainability reporting on social media, particularly on Facebook.

1. Introduction

There is growing literature discussing the potential roles of big data in corporate reporting, in line with the trend of digitisation of accounting practices. Arnaboldi et al. (Citation2017) argued that big data revolution, in tandem with the popularity of social media platforms, could change accounting practices, including sustainability reporting. In this context, big data analytics (BDA) facilitates the analysis and categorisation of data into useful information for business decision-making leading to improved corporate sustainability performance (Choi & Park, Citation2022). Corporations’ ability to utilise big data to gain strategic and operational insights is known as big data analytics capabilities or BDAC (Mikalef et al., Citation2018). Despite the increasing number of studies that relate BDA with sustainability reporting, research that explores the impact of BDAC implementation on sustainability reporting through social media is rather limited (De Camargo Fiorini et al., Citation2018; Lombardi & Secundo, Citation2020). Since social media has become a popular medium for sustainability reporting (Lodhia et al., Citation2020), it is useful to understand whether the implementation of BDAC improves the extent of sustainability reporting communicated on social media. Two-way interactions between companies and stakeholders allow for more efficient stakeholder engagement on sustainability issues, and BDAC enables companies to generate valuable insights for improved sustainability reporting on social media.

Companies need to set the right tone at the top to drive corporate sustainability goals that are vital in maintaining good relationships with stakeholders. Corporate chief executive officer (CEO) plays a significant role in shaping corporate strategic decisions (Sariol & Abebe, Citation2017) and leading corporate sustainability initiatives. Following that, the CEO’s language, which communicates the vision and values of the company on external communication platforms (Mayfield et al., Citation2014), channels the tone that sets the corporate direction and significantly influences shareholders’ value creation (Shin & You, Citation2017). Prior literature suggests that certain attributes of tone at the top affect the extent of sustainability reporting (Cho et al., Citation2010; Latan et al., Citation2018). This study contributes to the existing literature by examining the moderating roles of five different attributes of tone at the top provided by Hart (Citation2000) in the relationship between BDAC and sustainability reporting on social media. It highlights the interaction between BDAC implementation and different attributes of tone at the top in influencing sustainability reporting communicated through social media. Different attributes of tone at the top may affect the relationship between BDAC and sustainability reporting on social media differently. Therefore, identifying the best possible tone for the CEO’s language that promotes corporate sustainability on social media is paramount, particularly when companies have implemented BDAC for sustainability reporting on social media. This is to ensure the right deployment of dynamic capabilities that are represented by BDAC and tone at the top to attain corporate sustainable development as explained by dynamic capabilities view theory.

The corporate mission of achieving sustainable development supports the Sustainable Development Goals (SDGs) introduced by the United Nations in 2015 with the aim to end poverty, protect the planet, and ensure the global well-being of society. This universal call is highly relevant, especially in developing and emerging countries including Malaysia that are confronted with ongoing sustainability issues, such as climate change and poverty (Musa, Citation2021). The rapid adoption of Industry 4.0 technologies in Malaysia (Luthra & Mangla, Citation2018) presents a favourable case to investigate the use of social media for sustainability reporting since it is one of the sources of Industry 4.0 technologies. This study focuses on sustainability reporting on Facebook since the platform seems to be the most popular social media platform in Malaysia (Moorthy et al., Citation2019). As of January 2021, 86% of Malaysians were active users of social media platforms, and about 24.81 million were active Facebook users (Müller, Citation2021). The World Bank Group (Citation2017) also reported that two-thirds of Malaysians were active Facebook users.

Many corporations have disclosed sustainability information on social media in response to the rising global awareness of sustainability issues and to reap the potential benefits of social media. Despite the many benefits of communication on social media, its usage has given rise to an information overload problem (Roetzel, Citation2019) that may hinder users’ ability to make informed decisions and increase the likelihood of information misinterpretation due to the difficulty of selecting meaningful, relevant, and reliable information (Fowler & Pitta, Citation2013). BDAC can help solve this problem by better managing unstructured data from social media platforms. Alongside BDAC, setting the right tone at the top is vital to promote corporate sustainability (Kiesnere & Baumgartner, Citation2019). The Volkswagen emissions scandal highlighted the importance of a suitable corporate culture to aid business sustainability (Crête, Citation2016). Based on the above arguments, this study examined (1) the impact of BDAC implementation on sustainability reporting and (2) the moderating role of tone at the top in the relationship between BDAC and sustainability reporting on Facebook in Malaysia, from the dynamic capabilities view theory.

The findings of this study provide companies with insights regarding the significant role of BDAC and specific tone at the top in improving sustainability reporting on social media. Corporate capabilities in managing social media platforms via the use of big data technologies enable companies to manage their relationships with stakeholders and allow for combined efforts to address sustainability issues. The presence of a specific tone, such as certainty in CEOs’ letters or statements, together with BDAC implementation, has a greater impact on sustainability reporting on social media. This notion highlights the critical role of top management support, along with dynamic competencies, such as BDAC, in driving corporate sustainability initiatives. Therefore, companies and stakeholders should be vigilant in preparing and understanding the CEO’s letters or statements since not all tones exhibit corporate commitments towards sustainability efforts.

The rest of this paper is structured as follows: Section 2 discusses the extant literature on BDAC implementation, tone at the top, and sustainability reporting on social media, along with the theoretical framework and hypothesis development. This is followed by an explanation of the research methodology employed in Section 3. Section 4 presents the results and discusses the findings. Section 5 highlights the concluding remarks, theoretical and practical implications of the study, limitations, and suggestions for future research.

2. Literature review and hypothesis development

2.1. Dynamic capabilities view (DCV) theory

Dynamic capabilities view (DCV) theory posits that companies need to have the ability to integrate, build, and reconfigure internal and external competencies to address rapidly changing business environments (Teece, Citation2014). These capabilities allow companies to design their own organisational identity, basic elements, and processes, which are essential for survival (Fornell & Larcker, Citation1981). BDAC is also a contributing factor to the dynamic internal and external environment of companies as it facilitates companies’ information management for better decision-making. DCV emphasises flexible internal and external organisational processes that are channelled from the top management. Eikelenboom and de Jong (Citation2019) believe that dynamic capabilities are important for economic, social, and environmental performance.

In the context of this study, BDAC, tone at the top, and SRDF represent the dynamic capabilities required by companies to compete in a dynamic business environment, addressing the sustainable development challenges, circular economy, and big data economy. Other than investment in BDAC implementation as a source of dynamic capability, top management support is also vital for companies in order to reconfigure their resources and capabilities according to the environment (Hermano & Martín-Cruz, Citation2016). Based on the above, DCV was adopted in this study to examine the impact of BDAC on SRDF, moderated by the tone at the top. In operationalising DCV, this study first considered BDA infrastructure, management, and personnel’s capabilities to measure BDAC. Second, tone at the top was measured using the content analysis method where CEOs’ statements in annual/sustainability reports were analysed using the DICTION software developed by Hart (Citation2000).

2.2. Impact of BDAC implementation on sustainability reporting on social media

Sustainability reporting on social media has received considerable attention, in line with the development of digitisation of accounting practice and web 2.0 application. It refers to “the use of social media for external and internal corporate communication about sustainability, following a two-way interaction between an organisation and stakeholders” (Kaplan & Haenlein, Citation2010; Reilly & Hynan, Citation2014). Several studies have provided empirical evidence on sustainability reporting on social media. Manetti and Bellucci (Citation2016) highlighted a limited number of global organisations using social media to engage with stakeholders to define the contents of sustainability reports. Sustainability reporting on social media was more apparent among high-ranked companies (Reilly & Larya, Citation2018) and focused on social issues rather than environmental issues (Lodhia et al., Citation2020).

Social media technologies were found to enable change in sustainability reporting communication that could enhance stakeholder engagement (Al-Sartawi & Hamdan, Citation2019; Lodhia, Citation2018). Al-Htaybat and von Alberti-Alhtaybat (Citation2017) found that corporate reporting communication through social media reduced the limitations of corporate annual reports and enabled companies to report progress and share information at any time of the year. This is the nature of future corporate reporting, i.e., interactive, intelligent, and real-time (Deloitte, Citation2018). Since social media is a source of big data (She & Michelon, Citation2019), the application of BDAC can help companies improve their understanding of sustainability reporting. As an advanced form of information technology capability (Gupta & George, Citation2016), BDAC was found to have a positive impact on CSR management practices (Wang et al., Citation2020) and corporate reporting via social media (Wiencierz & Röttger, Citation2017). However, literature on sustainability reporting through social media is rather limited, particularly in the context of developing countries. The ability of BDAC to provide business insights using data management, infrastructure, and talent capabilities (Wamba et al., Citation2017) may help companies improve the extent of sustainability reporting disclosure on social media. This is based on the evidence that BDA has been proven useful in other business domains, such as risk management (Akinbowale et al., Citation2023) and strategic communication. While huge and unorganised data seem useless, companies can utilise BDAC to select and organise data for specific purposes, including for sustainability reporting on social media.

Since many companies in Malaysia are in a position to leverage the big data economy (Wong et al., Citation2015) alongside the circular economy, an examination of the impact of BDAC implementation on sustainability reporting disclosure through social media is highly relevant in order to observe the development of a circular economy through the adoption of Industry Revolution 4.0 (Yatim, Citation2018). This study focused on sustainability reporting disclosure on Facebook (SRDF), following the popularity of the social media platform globally (Bellucci & Manetti, Citation2017) and in Malaysia (Moorthy et al., Citation2019). Therefore, this study proposes the following hypothesis:

H1: There is a positive association between big data analytics capabilities (BDAC) and sustainability reporting disclosure on Facebook (SRDF).

2.3 Impact of BDAC implementation on sustainability reporting on social media: the moderating role of tone at the top

Implementing a specific technology in a company may have different effects on corporate performance depending on several moderating factors, such as the support of top management (Behl, Citation2022). Top management plays a significant role in determining corporate policies and strategies (Kabuye et al., Citation2019; Makhdoomi, Citation2018), including on matters pertaining to sustainability reporting. Tone at the top is used to define a company’s top management leadership and to set a company’s cultural environment and corporate value. It refers to the non-verbal tone of the top management (Patelli & Pedrini, Citation2015), which can be assessed by reviewing the CEO’s letter in the annual report or sustainability report. The CEO’s letter is important because it provides information on a company’s important policies, reflects the important issues confronting the company, and highlights the steps that leadership will take to address them; hence, the letter is a reflection and a depicter of CEO leadership (Cong et al., Citation2014).

Prior studies have assessed the role of the CEO’s tone in influencing corporate sustainability practices, reducing corporate environmental impact, and improving corporate reputation (Cong et al., Citation2014). According to Amernic et al. (Citation2010), there are five attributes of the non-verbal tone of CEO leadership that can be measured using the DICTION automated content analysis software. These attributes are certainty, optimism, activity, commonality, and realism. Certainty shows resoluteness and completeness; optimism entails the positivity of a person, group, concept, or event in a company; activity reflects the implementation of ideas; commonality indicates cooperation and agreed-upon values in a company; and realism measures the tangible and immediate matters that affect the people in a company.

Other than using the CEO’s letter, several studies have also assessed the tone used in specific corporate disclosures, such as environmental disclosure and corporate accountability disclosure in annual reports. Fisher et al. (Citation2019) highlighted the significance of disclosure type in determining a specific tone. Certainty seems to be related to sustainability management control, certification of assurance providers, and financial performance, thus suggesting the use of certainty in the tone to signal flexibility (Hassan, Citation2019). Similarly, Cho et al. (Citation2010) revealed that the non-verbal tone in the environmental disclosures by worst performers would be less certain than that of better performers among American companies. The findings of Cho et al. (Citation2010) provide empirical support regarding the roles of non-verbal tone in managing stakeholders’ impressions of an environmental disclosure. Similarly, Feng and Gao (Citation2020) documented an increase in the degree of realism and certainty of mandatory environmental disclosures following the release of the Securities and Exchange Commission’s (SEC) guidance for American companies. In another study, Arena et al. (Citation2015) revealed a negative association between optimism and future environmental concerns of companies with a low stakeholder orientation. Overall, different attributes of the tone used have different impacts on corporate outcomes. While most prior literature focused on selected attributes of tone at the top, this study included all five attributes to present comprehensive evidence on the moderating role of tone at the top in the relationship between BDAC and SRDF.

If top management backs the implementation of BDAC, it could help the growth of sustainability reporting on social media. As prior literature has shown, having support from top management makes it easier to put corporate practices into action, which drives corporate outcomes. For example, Chatterjee et al. (Citation2022) found that top management support strengthens the relationship between remote work flexibility and corporate performance. Behl (Citation2022) also points out that the support of top management moderates the relationship between BDAC and corporate performance. In the context of this study, it suggests that the joint effect of BDAC and a specific tone at the top influences the extent of sustainability reporting on social media by focusing on disclosures made on Facebook, being a popular social media platform, particularly in Malaysia. Since Du and Yu (Citation2020) demonstrated the importance of clear communication and tone in conveying information on corporate social responsibility, it is interesting to explore the impact of a specific tone at the top in influencing the relationship between BDAC and SRDF. In this study, the CEO’s letter was assessed to determine whether different attributes of tone at the top strengthened the existing relationship between BDAC and SRDF. Therefore, this study hypothesised the moderating role of tone at the top’s attributes as follows:

H2a: Certainty strengthens the relationship between BDAC and SRDF.

H2b: Optimism strengthens the relationship between BDAC and SRDF.

H2c: Activity strengthens the relationship between BDAC and SRDF.

H2d: Commonality strengthens the relationship between BDAC and SRDF.

H2e: Realism strengthens the relationship between BDAC and SRDF.

Figure summarises the framework of the study that incorporates the relationship between big data analytics capabilities (BDAC), tone at the top (measured by certainty, optimism, activity, commonality, and realism), and sustainability reporting disclosure on Facebook (SRDF).

Figure 1. Research framework.

3. Research methodology

3.1. Sample and data collection

The sample of this study was drawn from Bursa Malaysia’s public listed companies that mentioned using social media in their annual reports or sustainability reports and on their corporate websites during the year 2019. There were 320 companies that used social media in 2019 identified and selected as the initial sample of this study. Since the business community pays much attention to social media due to its growing popularity and role as one of the big data sources (Chae, Citation2015), the chosen sample is considered relevant for the objective of examining the impact of BDAC on sustainability reporting on Facebook. According to Ghani et al. (Citation2019), companies continually monitor social media platforms to extract information that can facilitate decision-making in order to improve business performance. Perhaps, this phenomenon is also applicable to sustainability reporting on Facebook. Besides, purposive sampling has been proven beneficial in analysing sustainability reporting in prior studies (Kamatra & Kartikaningdyah, Citation2015) at the company’s level of analysis (Amin et al., Citation2020; Shamim et al., Citation2019).

A web-based questionnaire on BDAC implementation, which had been pilot-tested, was administered to the 320 sample companies from September 2019 to April 2020. A total of 100 questionnaires were returned, giving a 31% response rate. The responses were gathered from the companies’ representatives that had big data and business analytics experiences, either from executive, middle management, or top management level. In order to achieve a collective response, the respondents were advised to consult other employees within their companies for information about which they lacked expertise.

Next, based on the 100 questionnaires returned, where each questionnaire represents one company (Bahrami & Shokouhyar, Citation2022; Mikalef et al., Citation2019), the Facebook posts (text only) of the 100 companies (represents the final sample companies) were content analysed manually for sustainability-related information disclosures during the year 2019. Consequently, the CEO letters from annual reports or sustainability reports published for the year 2019 of the 100 sample companies were content analysed using DICTION automated software to obtain scores for tone at the top attributes (certainty, optimism, activity, commonality, and realism). The response rate of 31% is considered sufficient since sustainability is still an emerging research issue in developing countries, including Malaysia. Prior sustainability-related studies conducted in Malaysia have reported response rates ranging from 10% to 40% (Mohd Fuzi et al., Citation2019; Mokhtar, Citation2015).

3.2. Measurement of research variables

3.2.1. Sustainability reporting disclosure on Facebook (SRDF)

SRDF was measured via content analysis of the Facebook posts of 100 companies that answered the questionnaire on BDAC implementation. The SRDF index was developed based on the GRI Guideline (GRI: Global Reporting Initiative, Citation2015a; Manetti & Bellucci, Citation2016; Ramananda & Atahau, Citation2019) and Bursa Malaysia’s Sustainability Reporting Guideline (Amran et al., Citation2015; Bursa Malaysia, Citation2018) that consist of three dimensions, namely environmental, social, and economic dimensions. These guidelines have been applied in many studies examining various sustainability reporting mediums, such as annual reports, stand-alone sustainability reports, and sustainability reporting on social media and were cross-checked against each other to ensure completeness. The companies’ Facebook posts from January 2019 to December 2019 were screened for sustainability-related information disclosure on Facebook. The Facebook posts were categorised according to the SRDF index (refer Appendix 1) formulated to measure the extent of sustainability reporting on Facebook. For each indicator in the SRDF index, a score of 1 was given if the company disclosed sustainability-related information on Facebook, and 0 otherwise. Data gathered from the content analysis procedure was tested for test–retest reliability to ensure the consistency of the coding output. Results from the Kruskal–Wallis test showed insignificant differences between the data sets collected at two different times, indicating consistency and reliability of the data collected.

3.2.2. Big data analytics capabilities (BDAC)

In this study, BDAC was measured in three dimensions, namely, (1) BDA management capability, (2) BDA infrastructure capability, and (3) BDA personnel capability, adapted from Wamba et al. (Citation2017). This measurement is considered reliable because it is based on the previous well-tested scales provided by Kim et al. (Citation2012) for measuring IT capabilities. BDA management capability consists of planning (PLAN) and coordination and control (COD-COL) dimensions. While planning entails adopting the goals and strategies required to implement BDA in a company, coordination, and control involves synchronising all business units to ensure BDA-related activities are performed optimally. Next, the BDA infrastructure capability consists of connectivity (CN) that refers to the integration of database management systems, hardware, and applications (Gupta & George, Citation2016) and compatibility (CP) that allows transparent flow of information in an organisation. Finally, BDA personnel capability was measured on technical knowledge and technological management knowledge (TK-TMK) and business knowledge and data-driven sustainability culture (BK-DDSC). The data gathered from the web-based questionnaire used to measure BDAC implementation was assessed for non-response bias and common method variance (CMV) to ensure data validity prior to structural model assessment. Non-response bias was tested by examining the difference in responses between early and late groups of respondents. The independent t-test results showed insignificant difference between these two groups of respondents. Hence, non-response biasness was not an issue in this study. CMV was assessed using Harman’s single-factor test. The result showed that the common factor variance can be explained by 42%, thus not an issue in this study (Shamim et al., Citation2019).

3.2.3. Tone at the top

Tone at the top refers to “the shared set of values that an organisation has to channel from the most senior executives” (Hart, Citation2000). This study measured tone at the top by examining five attributes, namely certainty, optimism, activity, commonality, and realism. These attributes were examined from CEOs’ letters to stakeholders. The score for each attribute was generated using the DICTION computer-assisted program designed by Hart (Citation1984) to determine the tone of the non-verbal message. The program uses artificial intelligence techniques and relies on linguistic theory to perform the word count (Bligh et al., Citation2004). According to Sydserff and Weetman (Citation2002), the coding process in DICTION has relatively strong objectivity concerning face validity and reliability as it has been used in several research settings (see, Cho et al., Citation2010; Cong et al., Citation2014; Fisher et al., Citation2019). Table summarises the measurement of each research variable used in this study.

Table 1. Summary of measurements of research variables

4. Findings and analysis

4.1. Measurement model

Table presents the descriptive analysis of BDAC, tone at the top, and SRDF based on the data collected using a questionnaire and content analysis techniques. The mean values for the different elements of BDAC ranged from 3.14 to 3.72 (based on a 5-point Likert scale survey), indicating an acceptable level of BDAC implementation among the sample companies. For the tone at the top, the certainty attribute reported a mean value of 67.45, reflecting the confidence of the top leadership of Malaysian companies regarding the policies adopted by their organisations. Similarly, the mean value of 53.19 for optimism depicted a parallel relation with the certainty in the non-verbal tone, indicating that Malaysian companies’ top-management teams were optimistic about their companies’ prospects to adopt new measures. Realism recorded the lowest mean score, indicating that although the top management was certain and optimistic about their practices, they lacked a realistic view. SRDF was measured on the economic (mean = 62.88), environmental (mean = 51.29), and social (mean = 64.44) dimensions, with less posts were related to environmental sustainability compared to the other two dimensions. Considering that environmental sustainability is very much related to climate change, which represents one of the SDGs, Malaysian companies should give equal attention to all dimensions of sustainability.

Table 2. Descriptive result

The measurement model of this study was examined on Smart PLS 3.0 for reliability and validity. Reliability refers to the capability of the scale to measure the variable fully (Kline, Citation2013). A Cronbach alpha value that is greater than 0.80 shows that the constructs are reliable (Cronbach, Citation1971). Table shows that most of the constructs reported satisfactory Cronbach’s alpha values exceeding 0.80 (Fornell & Larcker, Citation1981).

Table 3. Reliability assessment

Although connectivity and compatibility reported Cronbach’s alpha values of <0.80, they were retained in the model because their composite reliability values were >0.80. Ramayah et al. (Citation2018) suggested that composite reliability values ranging from 0.70 to 0.90 are satisfactory. Therefore, the construct measurements of the research variables used in this study were deemed reliable. Validity assessment was conducted using the heterotrait-monotrait (HTMT) ratio test. Discriminant validity issues can be solved using the measures suggested by Ramayah et al. (Citation2018). Ideally, highly correlated indicators must be merged into one construct. This approach has the theoretical backing of measurement theory, which suggests merging two strongly related constructs. If merging is not possible, highly correlated indicators must be eliminated from the study. The indicators eliminated must not exceed 20% of the total indicators in the model. Considering the treatment guidelines for discriminant validity provided by Ramayah et al. (Citation2018), this study eliminated several items and merged COL with COD, TK with TMK, and BK with DDSC to improve discriminant validity. All the HTMT values shown in Table are <0.90, which are satisfactory (Gold et al., Citation2001).

Table 4. Discriminant validity results

4.2. Structural model results and discussion

The structural model results are shown in Table for direct paths and moderation analysis obtained by incorporating 5,000 subsamples. The p-value of 0.00 indicates a significant impact of BDAC on SRDF. Hence, H1 was supported. The predictive power of the model was estimated using R2. Henseler et al. (Citation2009) categorised the variance caused by an independent variable on a dependent variable into weak (<0.25), moderate (0.25–0.50), and substantial (0.50–0.70). The adjusted R2 for SRDF (0.08) showed that BDAC caused a weak variance in SRDF. This effect can be cross validated using Q2, where >0 means predictive relevance of the model. In this study, we obtained a Q2 value of 0.08.

Table 5. Structural model results

The result for H1 implies that BDAC implementation allows companies in Malaysia to improve their sustainability reporting on Facebook. This finding is in line with Al-Htaybat and von Alberti-Alhtaybat (Citation2017)’s findings on the use of big data to improve business function and reporting. According to the authors, BDAC implementation can help companies improve their social media platform management for reporting and disclosure purposes and BDA assists companies in managing their stakeholders’ perceptions and expectations. Bellucci and Manetti (Citation2017) provided further evidence on the use of Facebook by top US philanthropic organisations to share sustainability information and how Facebook changed their relationship with stakeholders.

In line with DCV that suggests BDAC as a dynamic capability (Mikalef et al., Citation2018), Malaysian companies are adopting BDAC to manage stakeholders’ informational demands. BDAC is a necessary innovative strategy, and sustainability reporting is directly related to a company’s strategy (Herremans et al., Citation2016). Ruggiero and Cupertino (Citation2018) opine that innovation in terms of adopting new technologies is crucial because it enables companies to address new challenges associated with sustainability reporting, including managing the complexity of sustainability data, addressing the increasing demand for transparency, and integrating sustainability into business strategy. The finding also supports Wanner and Janiesch (Citation2019)’s study, which acknowledged the role of BDAC in improving sustainability reporting. Since social media is a source of big data, results from this study suggest that BDAC improves SRDF. This study also supports the GRI reporting vision 2025, which envisions companies having the capability to communicate with stakeholders outside the bounds of the annual sustainability reporting system through online platforms, including social media (GRI: Global Reporting Initiative, Citation2015b). It also narrates that the role of reporting needs to be dynamic, which is consistent with DCV propositions and this study’s finding that analysed the non-traditional form of reporting (i.e., Facebook).

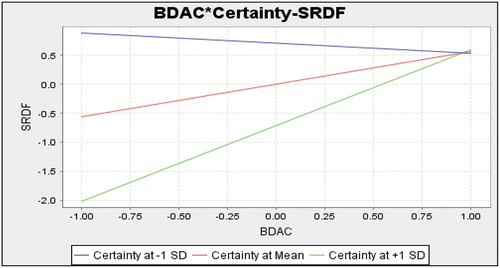

A two-stage approach in Smart PLS was used to analyse the moderated paths. This approach is recommended when one of the research variables is formative in nature (Ramayah et al., Citation2018). H2a was supported (p= 0.04), showing a significantly positive moderation effect of certainty on BDAC and SRDF. All other moderating hypotheses (H2b–H2e) showed insignificant results. An interaction plot is recommended to visualise the significant moderating impact (Dawson, Citation2014) of certainty between BDAC and SRDF. In Figure , the green-line slope means the relationship moved towards a stronger trend when the tone at the top has certainty in their non-verbal communication in annual or sustainability reports. Hence, these companies tended to disclose a greater extent of sustainability-related information on Facebook.

Figure 2. Simple slope analysis.

Overall, our findings indicate the joint effect of BDAC and certainty in the tone at the top in influencing the extent of SRDF. Certainty in the tone at the top, which signals flexibility in companies, is linked to sustainability-related disclosures (Cho et al., Citation2010; Feng & Gao, Citation2020; Fisher et al., Citation2019; Li et al., Citation2022). Since different attributes of tone at the top may signal different messages to stakeholders, it is useful for companies and stakeholders to understand the different messages signalled by these different attributes of tone at the top. This understanding may enable the companies to convey the right message to the stakeholders, and subsequently, the message conveyed is understood by the stakeholders. Effective communication between these two parties may partly reduce the information asymmetry problem. In the context of this study, the findings indicate that companies that communicate certainty in their CEO’s letter and implement BDAC disclose a significantly greater extent of sustainability reporting on Facebook. It has been apparent that BDAC improves sustainability reporting on social media in Malaysia, specifically on the Facebook platform. The certainty tone of the CEOs’ letters has led to a greater improvement in the sustainability reporting on Facebook, as indicated by a higher SRDF index.

The results for control variables showed an insignificant impact of industry type, consumer proximity, firm age, size, profitability, and leverage on SRDF. These results contradict the extant literature that examined the determinants of sustainability reporting in corporate annual reports or stand-alone sustainability reports. Nevertheless, this study observed a small impact of the control variables on SRDF, as the R2 value increased slightly when the control variables were introduced into the research model. Therefore, it is interesting to suggest that the determinants of sustainability reporting depend on the sustainability reporting medium used in a study.

5. Conclusion

This study acknowledges the significant roles of (1) BDAC and (2) the joint effect of BDAC and a specific tone at the top (certainty) in promoting SRDF among PLCs in Malaysia. It contributes to the existing literature by proposing that companies should implement BDAC and demonstrate certainty in the tone at the top, which represent two critical dynamic capabilities to cope with the rapidly changing business environment, in line with the DCV theory. SRDF can also be viewed as a tool to address legitimacy and stakeholders’ informational needs. The increasing demand from stakeholders that requires companies to operate responsibly has prompted many companies to utilise social media to communicate with the stakeholders. BDAC enables companies to analyse the data collected through social media in order to improve corporate sustainable strategies and decision-making. When the BDAC implementation is combined with certainty in the tone at the top, greater improvement on the extent of SRDF has been apparent as these two resources represent the dynamic capabilities that help companies adapt to the changing demands of stakeholders and compete in the Industrial Revolution 4.0 era.

5.1. Theoretical and practical implications of the study

The findings of the study have several implications. Theoretically, this study acknowledges the application of DCV theory in explaining sustainability reporting on social media. It highlights the important roles of BDAC and the certainty tone of the top in promoting sustainability reporting on social media, particularly in the context of Malaysia, a developing country that is actively involved in sustainability initiatives.

The findings of the study also have several practical implications: First, companies may have greater awareness of the role of BDAC, tone at the top, and social media in promoting corporate sustainability and, hence, may invest sufficient resources to implement BDAC, use specific tone at the top, and communicate SRDF to stakeholders. Second, companies are motivated to fully utilise the advantages offered by BDAC and social media in order to maximise returns from investment in the dynamic capabilities. Third, stakeholders such as regulators, investors, creditors, and society as a whole may be informed of the dynamic capabilities that can drive corporate sustainability. Hence, they may support those companies to support the global call for sustainable development. For example, regulators, such as Malaysia Digital Economy Corporation (MDEC), Bursa Malaysia and Securities Commission Malaysia (SC) may provide support in terms of intensifying the awareness and educational programmes, providing access to the required infrastructure, and improving the existing regulations to promote BDAC, top management leadership, and SRDF among companies. The voluntary disclosures of sustainability reporting on social media is seen in line with the Global Reporting Initiatives (GRI) reporting’s 2025 vision that aims to digitalise sustainability reporting for interactivity purposes. In addition, investors and creditors may be motivated to invest in companies that are actively involved in BDAC and SRDF, as well as demonstrating good top management leadership on SRDF.

5.2. Limitation of the study and suggestion for future research

Since the development of BDAC and SRDF in Malaysia is still at an infancy stage, the study was conducted on a limited number of companies. Perhaps, more conclusive evidence could be gathered in the future as more companies are ready to invest in BDAC and SRDF on a larger scale. Future studies could also be extended to include evidence from other countries, especially developing countries that have limited studies on this topic. This study focuses on three dimensions of BDAC with five attributes of tone at the top only. Further exploration of different dimensions of BDAC and corporate governance indicators may produce different results.

Research ethics approval

This work received research ethics clearance from the University of Malaya Research Ethics Committee (UMREC) with the reference number UM.TNC2/UMREC – 936.

Disclosure statement

The authors report there are no competing interests to declare.

Additional information

Funding

References

- Akinbowale, O. E., Mashigo, P., & Zerihun, M. F. (2023). The integration of forensic accounting and big data technology frameworks for internal fraud mitigation in the banking industry. Cogent Business & Management, 10(1), 2163560. https://doi.org/10.1080/23311975.2022.2163560

- Al-Htaybat, K., & von Alberti-Alhtaybat, L. (2017). Big data and corporate reporting: Impacts and paradoxes. Accounting, Auditing and Accountability Journal, 30(4), 850–20. https://doi.org/10.1108/AAAJ-07-2015-2139

- Al-Sartawi, A. M., & Hamdan, A. (2019). Social Media Reporting and Firm Value. In Conference on e-Business, e-Services and e-Society (pp. 356–366). Springer, Cham.

- Amernic, J., Craig, R., & Tourish, D. (2010). Measuring and assessing tone at the top using annual report CEO letters. The Institute of Chartered Accountants of Scotland.

- Amin, M. H., Mohamed, E. K. A., & Elragal, A. (2020). Corporate disclosure via social media: A data science approach. Online Information Review, 44(1), 278–298. https://doi.org/10.1108/OIR-03-2019-0084

- Amran, A., Ooi, S. K., Mydin, R. T., & Devi, S. S. (2015). The impact of business strategies on online sustainability disclosures. Business Strategy and the Environment, 24(6), 551–564. https://doi.org/10.1002/bse.1837

- Arena, C., Bozzolan, S., & Michelon, G. (2015). Environmental reporting: Transparency to stakeholders or stakeholder manipulation? An Analysis of disclosure tone and the role of the board of directors. Corporate Social Responsibility and Environmental Management, 22(6), 346–361. https://doi.org/10.1002/csr.1350

- Arnaboldi, M., Busco, C., & Cuganesan, S. (2017). Accounting, accountability, social media and big data: Revolution or hype? Accounting, Auditing & Accountability Journal, 30(4), 762–776. https://doi.org/10.1108/AAAJ-03-2017-2880

- Aydiner, A. S., Tatoglu, E., Bayraktar, E., Zaim, S., & Delen, D. (2019). Business analytics and firm performance: The mediating role of business process performance. Journal of Business Research, 96(October 2018), 228–237. https://doi.org/10.1016/j.jbusres.2018.11.028

- Bahrami, M., & Shokouhyar, S. (2022). The role of big data analytics capabilities in bolstering supply chain resilience and firm performance: A dynamic capability view. Information Technology & People, 35(5), 1621–1651. https://doi.org/10.1108/ITP-01-2021-0048

- Behl, A. (2022). Antecedents to firm performance and competitiveness using the lens of big data analytics: A cross-cultural study. Management Decision, 60(2), 368–398. https://doi.org/10.1108/MD-01-2020-0121

- Bellucci, M., & Manetti, G. (2017). Facebook as a tool for supporting dialogic accounting? Evidence from large philanthropic foundations in the United States. Accounting, Auditing & Accountability Journal, 30(4), 874–905. https://doi.org/10.1108/AAAJ-07-2015-2122

- Bligh, M. C., Kohles, J. C., & Meindl, J. R. (2004). Charting the language of leadership: A methodological investigation of President Bush and the crisis of 9/11. Journal of Applied Psychology, 89(3), 562–574. https://doi.org/10.1037/0021-9010.89.3.562

- Chae, B. K. (2015). Insights from hashtag# supplychain and Twitter analytics: Considering Twitter and Twitter data for supply chain practice and research. International Journal of Production Economics, 165, 247–259. https://doi.org/10.1016/j.ijpe.2014.12.037

- Chatterjee, S., Chaudhuri, R., & Vrontis, D. (2022). Does remote work flexibility enhance organization performance? Moderating role of organization policy and top management support. Journal of Business Research, 139, 1501–1512. https://doi.org/10.1016/j.jbusres.2021.10.069

- Choi, H. Y., & Park, J. (2022). Do data-driven CSR initiatives improve CSR performance? The importance of big data analytics capability. Technological Forecasting and Social Change, 182, 121802. https://doi.org/10.1016/j.techfore.2022.121802

- Cho, C. H., Roberts, R. W., & Patten, D. M. (2010). The language of US corporate environmental disclosure. Accounting, Organizations and Society, 35(4), 431–443. https://doi.org/10.1016/j.aos.2009.10.002

- Cong, Y., Freedman, M., & Park, J. D. (2014). Tone at the top: CEO environmental rhetoric and environmental performance. Advances in Accounting, 30(2), 322–327. https://doi.org/10.1016/j.adiac.2014.09.007

- Crête, R. (2016). The Volkswagen scandal from the viewpoint of corporate governance. European Journal of Risk Regulation, 7(1), 25–31. https://doi.org/10.1017/S1867299X0000533X

- Cronbach, L. J. (1971). Test validation. In R. L. Thorndike (Ed.), Educational measurement (2nd) ed., pp. 443–507). American Council on Education.

- Dawson, J. F. (2014). Moderation in management research: What, why, when, and how. Journal of Business and Psychology, 29(1), 1–19. https://doi.org/10.1007/s10869-013-9308-7

- de Camargo Fiorini, P., Seles, B. M. R. P., Jabbour, C. J. C., Mariano, E. B., & de Sousa Jabbour, A. B. L. (2018). Management theory and big data literature: From a review to a research agenda. International Journal of Information Management, 43, 112–129. https://doi.org/10.1016/j.ijinfomgt.2018.07.005

- Deloitte. (2018). Crunch time 7: Reporting in a digital world. Deloitte Development LLC. https://www2.deloitte.com/content/dam/Deloitte/us/Documents/finance-transformation/us-crunch-time-seven-reporting-in-a-digital-world.pdf

- Du, S., & Yu, K. (2020). Do corporate social responsibility reports convey value relevant information? Evidence from report readability and tone. Journal of Business Ethics, 172(2), 253–274. https://doi.org/10.1007/s10551-020-04496-3

- Eikelenboom, M., & de Jong, G. (2019). The impact of dynamic capabilities on the sustainability performance of SMEs. Journal of Cleaner Production, 235, 1360–1370. https://doi.org/10.1016/j.jclepro.2019.07.013

- Feng, S., & Gao, L. S. (2020). The verbal tone in mandatory environmental disclosures: Evidence from changes in disclosures following SEC guidance. Social and Environmental Accountability Journal, 40(2), 116–139. https://doi.org/10.1080/0969160X.2020.1719172

- Fisher, R., van Staden, C. J., & Richards, G. (2019). Watch that tone: An investigation of the use and stylistic consequences of tone in corporate accountability disclosures. Accounting, Auditing and Accountability Journal, 33(1), 77–105. https://doi.org/10.1108/AAAJ-10-2016-2745

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Fowler, D., & Pitta, D. (2013). Advances in mining social media: Implications for marketers. Journal of Information Technology Management, 24(4), 25–33.

- Gavana, G., Gottardo, P., & Moisello, A. M. (2017). Sustainability reporting in family firms: A panel data analysis. Sustainability (Switzerland), 9(1), 1–18. https://doi.org/10.3390/su9010038

- Ghani, N. A., Hamid, S., Targio Hashem, I. A., & Ahmed, E. (2019). Social media big data analytics: A survey. Computers in Human Behavior, 101(December2017), 417–428. https://doi.org/10.1016/j.chb.2018.08.039

- Gold, A. H., Malhotra, A., & Segars, A. H. (2001). Knowledge management: An organizational capabilities perspective. Journal of Management Information Systems, 18(1), 185–214. https://doi.org/10.1080/07421222.2001.11045669

- GRI: Global Reporting Initiative. (2015a). G4 sustainability reporting guidelines. Reporting principles and standard disclosures. https://www.globalreporting.org/information/g4/Pages/default.aspx

- GRI: Global Reporting Initiative. (2015b). Sustainability and reporting trends in 2025: Preparing for the future. Global Reporting Initiative.

- Group, W. B. (2017). The Malaysia Development Experience Series - Open Data Readiness Assessment (ODRA) Report. May, 76. wbg.org/Malaysia

- Gupta, M., & George, J. F. (2016). Toward the development of a big data analytics capability. Information and Management, 53(8), 1049–1064. https://doi.org/10.1016/j.im.2016.07.004

- Hahn, R., & Kühnen, M. (2013). Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. Journal of Cleaner Production, 59, 5–21. https://doi.org/10.1016/j.jclepro.2013.07.005

- Hart, R. P. (1984). Systematic analysis of political discourse: The development of DICTION. In K. Sanders et al. (Eds.), Political communication yearbook (pp. 1–5). Southern Illinois University Press.

- Hart, R. P. (2000). DICTION 5.0: The text-analysis program. Sage.

- Hassan, A. (2019). Verbal tones in sustainability assurance statements: An empirical exploration of explanatory factors. Sustainability Accounting, Management and Policy Journal, 10(3), 427–450. https://doi.org/10.1108/SAMPJ-06-2017-0051

- Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modeling in international marketing. In Sinkovics, R.R., & Ghauri, P.N. (Eds.), New challenges to international marketing (pp. 277–319). Emerald Group Publishing Limited.

- Hermano, V., & Martín-Cruz, N. (2016). The role of top management involvement in firms performing projects: A dynamic capabilities approach. Journal of Business Research, 69(9), 3447–3458. https://doi.org/10.1016/j.jbusres.2016.01.041

- Herremans, I. M., Nazari, J. A., & Mahmoudian, F. (2016). Stakeholder relationships, engagement, and sustainability reporting. Journal of Business Ethics, 138(3), 417–435. https://doi.org/10.1007/s10551-015-2634-0

- Kabuye, F., Bugambiro, N., Akugizibwe, I., Nuwasiima, S., & Naigaga, S. (2019). The influence of tone at the top management level and internal audit quality on the effectiveness of risk management practices in the financial services sector. Cogent Business & Management, 6(1), 1704609. https://doi.org/10.1080/23311975.2019.1704609

- Kamatra, N., & Kartikaningdyah, E. (2015). Effect corporate social responsibility on financial performance. International Journal of Economics and Financial Issues, 5(2015), 157–164. https://www.econjournals.com/index.php/ijefi/article/view/1361

- Kaplan, A. M., & Haenlein, M. (2010). Users of the world, unite! The challenges and opportunities of Social Media. Business Horizons, 53(1), 59–68. https://doi.org/10.1016/j.bushor.2009.09.003

- Kiesnere, A. L., & Baumgartner, R. J. (2019). Sustainability management emergence and integration on different management levels in smaller large‐sized companies in Austria. Corporate Social Responsibility and Environmental Management, 26(6), 1607–1626. https://doi.org/10.1002/csr.1854

- Kim, G., Shin, B., & Kwon, O. (2012). Investigating the value of sociomaterialism in conceptualizing IT capability of a firm. Journal of Management Information Systems, 29(3), 327–362. https://doi.org/10.2753/MIS0742-1222290310

- Kline, R. (2013). Exploratory and confirmatory factor analysis. In Applied quantitative analysis in the social sciences (pp. 171–207). Routledge.

- Latan, H., Jabbour, C. J. C., de Sousa Jabbour, A. B. L., Wamba, S. F., & Shahbaz, M. (2018). Effects of environmental strategy, environmental uncertainty and top management’s commitment on corporate environmental performance: The role of environmental management accounting. Journal of Cleaner Production, 180, 297–306. https://doi.org/10.1016/j.jclepro.2018.01.106

- Li, Z., Jia, J., & Chapple, L. J. (2022). Textual characteristics of corporate sustainability disclosure and corporate sustainability performance: Evidence from Australia. Meditari Accountancy Research.

- Lodhia, S. (2018). Is the medium the message? Meditari Accountancy Research, 26(1), 2–12. https://doi.org/10.1108/MEDAR-08-2017-0197

- Lodhia, S., Kaur, A., & Stone, G. (2020). The use of social media as a legitimation tool for sustainability reporting. Meditari Accountancy Research, 28(4), 613–632. https://doi.org/10.1108/MEDAR-09-2019-0566

- Lombardi, R., & Secundo, G. (2020). The digital transformation of corporate reporting–a systematic literature review and avenues for future research. Meditari Accountancy Research, 1179–1208. https://doi.org/10.1108/MEDAR-04-2020-0870

- Luthra, S., & Mangla, S. K. (2018). Evaluating challenges to Industry 4.0 initiatives for supply chain sustainability in emerging economies. Process Safety and Environmental Protection, 117, 168–179. https://doi.org/10.1016/j.psep.2018.04.018

- Makhdoomi, U. M. (2018). Top management commitment and diversity challenges in telecom sector top management commitment and diversity challenges in telecom sector. Asian Journal of Managerial Science, 7(1), 53–56. https://doi.org/10.51983/ajms-2018.7.1.1288

- Malaysia, B. (2018). Sustainability Reporting Guide (2nd Edition). Bursa Malaysia.

- Manetti, G., & Bellucci, M. (2016). The use of social media for engaging stakeholders in sustainability reporting. Accounting, Auditing & Accountability Journal, 29(6), 985–1011. https://doi.org/10.1108/AAAJ-08-2014-1797

- Mayfield, J., Mayfield, M., & Sharbrough, W. C. (2014). Strategic vision and values in top leaders’ communications. International Journal of Business Communication, 52(1), 97–121. https://doi.org/10.1177/2329488414560282

- Mikalef, P., Boura, M., Lekakos, G., & Krogstie, J. (2019). Big data analytics capabilities and innovation: The mediating role of dynamic capabilities and moderating effect of the environment. British Journal of Management, 30(2), 272–298. https://doi.org/10.1111/1467-8551.12343

- Mikalef, P., Pappas, I. O., Krogstie, J., & Giannakos, M. (2018). Big data analytics capabilities: A systematic literature review and research agenda. Information Systems and E-Business Management, 16(3), 547–578. https://doi.org/10.1007/s10257-017-0362-y

- Mohd Fuzi, N., Habidin, N. F., Janudin, S. E., & Ong, S. Y. Y. (2019). Critical success factors of environmental management accounting practices: Findings from Malaysian manufacturing industry. Measuring Business Excellence, 23(1), 1–14. https://doi.org/10.1108/MBE-03-2018-0015

- Mokhtar, N. (2015). The extent of environmental management accounting (EMA) implementation and environmental reporting (ER) practices: Evidence from Malaysian Public Listed Companies. University of Malaya. http://studentsrepo.um.edu.my/5921/

- Moorthy, K., T’ing, L. C., Wei, K. M., Mei, P. T. Z., Yee, C. Y., Wern, K. L. J., & Xin, Y. M. (2019). Is Facebook useful for learning? A study in private universities in Malaysia. Computers & Education, 130, 94–104. https://doi.org/10.1016/j.compedu.2018.12.002

- Müller, J. (2021). Social media users as a percentage of the total population Malaysia 2021, accessed on 7th April 2021. Statista. https://www.statista.com/statistics/883712/malaysia-social-media-penetration/

- Musa, M. N. (2021, October 30). Sustainability: How Malaysia can identify gaps and solutions. New Straits Times. https://www.nst.com.my/opinion/columnists/2021/10/741121/sustainability-how-malaysia-can-identify-gaps-and-solutions

- Patelli, L., & Pedrini, M. (2015). Is tone at the top associated with financial reporting aggressiveness? Journal of Business Ethics, 126(1), 3–19. https://doi.org/10.1007/s10551-013-1994-6

- Ramananda, D., & Atahau, A. D. R. (2019). Corporate social disclosure through social media: An exploratory study. Journal of Applied Accounting Research, 21(2), 265–281. https://doi.org/10.1108/JAAR-12-2018-0189

- Ramayah, T., Cheah, J., Chuah, F., Ting, H., & Memon, M. A. (2018). Partial least squares structural equation modeling (PLS-SEM) using smartPLS 3.0: An Updated Guide and Practical Guide to Statistical Analysis (2nd version). Pearson.

- Reilly, A. H., & Hynan, K. A. (2014). Corporate communication, sustainability, and social media: It’s not easy (really) being green. Business Horizons, 57(6), 747–758. https://doi.org/10.1016/j.bushor.2014.07.008

- Reilly, A. H., & Larya, N. (2018). External communication about sustainability: Corporate social responsibility reports and social media activity. Environmental Communication, 12(5), 621–637. https://doi.org/10.1080/17524032.2018.1424009

- Roetzel, P. G. (2019). Information overload in the information age: A review of the literature from business administration, business psychology, and related disciplines with a bibliometric approach and framework development. Business Research, 12(2), 479–522. https://doi.org/10.1007/s40685-018-0069-z

- Ruggiero, P., & Cupertino, S. (2018). CSR strategic approach, financial resources and corporate social performance: The mediating effect of innovation. Sustainability, 10(10), 3611. https://doi.org/10.3390/su10103611

- Sariol, A. M., & Abebe, M. A. (2017). The influence of CEO power on explorative and exploitative organizational innovation. Journal of Business Research, 73, 38–45. https://doi.org/10.1016/j.jbusres.2016.11.016

- Shamim, S., Zeng, J., Shariq, S. M., & Khan, Z. (2019). Role of big data management in enhancing big data decision-making capability and quality among Chinese firms: A dynamic capabilities view. Information and Management, 56(6), 103135. https://doi.org/10.1016/j.im.2018.12.003

- She, C., & Michelon, G. (2019). Managing stakeholder perceptions: Organized hypocrisy in CSR disclosures on Facebook. Critical Perspectives on Accounting, 61, 54–76. https://doi.org/10.1016/j.cpa.2018.09.004

- Shin, T., & You, J. (2017). Pay for talk: How the use of shareholder‐value language affects CEO compensation. Journal of Management Studies, 54(1), 88–117. https://doi.org/10.1111/joms.12218

- Sydserff, R., & Weetman, P. (2002). Developments in content analysis: A transitivity index and diction scores. Accounting, Auditing & Accountability Journal, 15(4), 523–545. https://doi.org/10.1108/09513570210440586

- Teece, D. J. (2014). The foundations of enterprise performance: Dynamic and ordinary capabilities in an (economic) theory of firms. Academy of Management Perspectives, 28(4), 328–352. https://doi.org/10.5465/amp.2013.0116

- Wamba, S. F., Gunasekaran, A., Akter, S., Ren, S., fan, J., Dubey, R., & Childe, S. J. (2017). Big data analytics and firm performance: Effects of dynamic capabilities. Journal of Business Research, 70, 356–365. https://doi.org/10.1016/j.jbusres.2016.08.009

- Wang, C., Zhang, Q., & Zhang, W. (2020). Corporate social responsibility, Green supply chain management and firm performance: The moderating role of big-data analytics capability. Research in Transportation Business & Management, 37, 100557. https://doi.org/10.1016/j.rtbm.2020.100557

- Wanner, J., & Janiesch, C. (2019). Big data analytics in sustainability reports: An analysis based on the perceived credibility of corporate published information. Business Research, 12(1), 143–173. https://doi.org/10.1007/s40685-019-0088-4

- Wiencierz, C., & Röttger, U. (2017). The use of big data in corporate communication. Corporate Communications: An International Journal, 22(3), 258–272. https://doi.org/10.1108/CCIJ-02-2016-0015

- Wong, K. L., Chuah, M. H., & Ong, S. F. (2015). Are Malaysian companies ready for the big data economy? A business intelligence model approach.

- Yatim, P.(2018). Circular economy for sustainable development. New Straits Times. https://www.nst.com.my/opinion/columnists/2018/02/332848/circular-economy-sustainable-development