Abstract

This paper provides an explorative and interrogative profile of digital capital on SMEs within the agricultural food sector, focusing on SME farmers. Digital capital is deemed the new capital essential for farmers. The paper examines the opportunities and threats offered by digital capital and explores how it influences agricultural SME performance and how it leads to digital inequalities. The study purposively sampled three South African agricultural provinces and adopted a purposive sampling technique to collect quantitative and qualitative data. With the undoubted contribution of SMEs to social and economic fronts, the study chronicled how digital capital has improved the value chain processes while unearthing the barriers to digital tools access. It emerged that SMEs face many adoption challenges; hence it is debatable to link positive SME performance to digital capital adoption. It emerged that agricultural SMEs mostly adopt complimentary service digital tools, indicating that digital capital is a catalyst for inequalities. While the government has implemented some initiatives to promote digital capital adoption, such interventions remain inadequate. The study contemplates other initiatives that could be adopted to address the barriers SMEs face in this digital era, hence closing the inequalities gap within the industry. SMEs should be subject to public policy support and protection, particularly on digital capital incentives and sponsorship. The government must regulate some digital capital tools which are more harmful than productive.

1. Introduction and study context

It is common knowledge that digitalisation has become a core attribute in the business space. There has been much scholarly work surrounding the potential of digital technologies, particularly their disruptive nature to business models. In their AI-driven marketing study, Huang and Rust (2022) emphasised the need for firms to pivot towards using technologically driven tools and metrics to improve their overall business practices. Several authors have already shared the above sentiments, and they are no longer preaching pivoting toward digital technologies adoption and or either term them as technological tools, but they refer to technological tools and metrics as “digital capital”, which captures extended digital tools attributes (Ragnedda et al., Citation2022). The rapid increase in ICT innovation development and the hype surrounding digitisation capabilities have made “digital capital” be viewed as a prerequisite for company success in this digital era (Ragnedda et al., Citation2022; Ragnedda, Citation2018). Because digital capital adoption is happening outside its areas of natural occurrence, i.e. outside ICT (Davenport & Ronanki, Citation2018), the agricultural sector firms have not been spared. In South Africa, the agricultural sector is an important sector that inhabits around 32 000 commercial farmers (2020). From the existing agricultural companies, small-scale farmers contribute 22.4% of the total income generated (Stats SA, Citation2019), thus indicating their importance.

However, within the agricultural sector, SMEs’ positioning towards adopting digital capital has been somehow subjective and focused on certain technologies that influence a certain process within the value chain. The cause for this discourse has been the nature of digital capital: the costs associated with adoption, lack of knowledge and government neglect. Despite the state drawbacks, Mhlongo and Dlamini (Citation2022) state that some SMEs within the agriculture space are already utilising at least one digital capital tool in their operations in South Africa. Furthermore, SMEs’ socio-economic contribution to the economy must appreciate their importance and support them in this digital era (Nieuwenhuizen, Citation2019). SMEs play a critical role in agri-business, ensuring continued socio-economic growth, increasing mass agricultural production, and improving food accessibility (Kamariotou et al., Citation2022). Thus, the study focuses on SMEs’ reactions at different touchpoints with digital capital through the lens of adoption barriers, inequalities, performance, and the state’s role. This enables the study to examine different interaction levels regarding the country’s digital capital and Agri-sector SMEs. Considering that digital capital presents a threat or an opportunity for SMEs, it depends on how they strategically tackle it (Sjödin et al., Citation2018).

Firstly, there is a need to define and comprehend digital capital, a broad term whose boundaries continue to increase. Many researchers have attempted to quantify digital capital and developed a series of studies and definitions. Merisalo and Makkonen (Citation2022) acknowledge that digital capital is a continuous conversion of digital technologies with other physical capital. They elaborate that digital capital takes two forms, “traditional technological tangible assets” such as computers, routers, internet software, online purchasing platforms and connectivity infrastructure. At the same time, the other form is intangible assets of technologies that currently drive the digital economy’s prowess. Under the intangible assets, the digital capture of customer behaviours and trade patterns, the big data and analytics capabilities are catalysts for business growth and success (increased market share and profit). In a nutshell, the above definitions view digital capital as an extension of the physical attributes of digital tools to more intangible elements, such as skills for data analytics. These application systems can perform tasks without human interaction and online commercial interactions. The views are closely connected to the definition of Ragnedda (Citation2018, 2369), who describes digital capital as “the accumulation of digital competencies (information, communication, safety, content-creation and problem-solving) and digital technology”. Echoing Bourdieu’s (Citation1983) sentiments, Ragnedda et al. (Citation2020, p. 4) have simplified the definition of digital capital and referred to digital capital as “a set of internalised abilities and aptitudes” (digital competencies) as well as “externalised resources” (digital technology) that can be historically accumulated and transferred from one arena to another for commercial use”. The two last definitions are similar but differ in emphasising that different industries can use them for profit-making.

Therefore, in this study, guided by the definitions above, digital capital is the accumulation and usage of intangible and tangible digital assets to improve company practices. This implies that digital capital relates to physical digital technologies such as robots, computer systems, online applications, ICT infrastructure, and intangible technology competencies for problem-solving, data analytics, information communication, safety, and content creation. Adopting digital capital competencies and technologies means companies consent to the notion that digital capital can improve their business value chains and be disruptive. Therefore, SMEs in agriculture can adopt digital capital as many tools and competencies are available. The technology adoption, agricultural development and inequality phenomenon date back to the mid-80s hence not peculiar to the African set-up (Kueh, Citation1985). The digital divide gap in South Africa has been perceivably been mainly due to rapid technological advancements globally and differences in financial capital between big companies and SMEs. Theoretically, the dimension of digital capital continues to challenge SMEs due to the lack of quantifying tangible and intangible boundaries, as some researchers present (Merisalo & Makkonen, Citation2022). The study’s indicator components are guided by Ragnedda (Citation2018), which was further refined by Ragnedda et al. (Citation2020) on the theoretical concepts of the background between the evolution of digital capital and other capital. Bourdieu’s (Citation1983) study on capital conceptualisation is the key basis for the digital definition and quantification of the study.

In South Africa, the agricultural food sector has three distinct categories: animal production, horticulture, and crop production. It is a highly concentrated but monopolised industry, as 15%-22% of producers account for 80% of the total agriculture output (Stats SA, Citation2019). Animal production contributes more than total output, while horticulture contributes slightly below a third and crops just below a quarter. In 2016, the sector’s contribution to the over-country GDP had reduced drastically from 11% in the early 1960s to 2.2% 2016 (World Bank, Citation2018). However, the sector continues to grow in terms of internal industry growth, with 13.1% growth recorded as of 2019, thus outshining other sectors (Citation2019). The decline in GDP industry contribution is linked to the rise and growth of other sectors such as mining, service, and manufacturing (FAO, Citation2016); while internal industry growth has been associated with increased demand, both internal and external, the growth of small-scale farmers post-Apartheid era and technology integration (Born et al., Citation2021; SEDA, Citation2021). This shows that SMEs within the industry play an important role, and some are affiliated with digital capital. As SMEs contribute 22.4% of the income outcome for the industry (Stats SA, 2019), it is evidence that they cannot be neglected, considering the concentration levels of the sector.

Like many other SMEs in different industries, small farmers face challenges like market access, funding, unfair competition, and expensive machinery (SEDA, Citation2021). Since digital capital is inconclusive, some see it as a threat while others as an opportunity, depending on how they engage with it, but its impact cannot be ignored for SMEs. As Bennett (Citation2008) indicates, the difference between the pre-digital and post-digital eras is that some could benefit, and some suffer due to technological advancements. Equally, Huang and Rust (2022) lament the casualties in case of failure to be agile and adapt AI technologies for business improvement. The study’s discoveries prove to be true as technology overlaps with Agri-business, particularly for SMEs, which has become a nightmare, while for others, it has proven to be a blessing. The same sentiments are shared by Brynjolfsson et al. (Citation2019), who emphasise the mismatch between technology gains and adoption costs, particularly for small players in different industries. On the other hand, Qvist-Sørensen (Citation2020) postulates that the outcome will be guided by a combination of market learning and entrepreneurial orientations for firms that are well-poised to take advantage of the opportunities presented by digital technologies because they adopt attitudes and behaviours that support the generation and use of market insight, proactive innovation, and openness to new ideas. Sussan and Acs (Citation2017) explicitly agree that a significant gap in empirical evidence links SMEs’ success to digital capital adoption.

(Citation2019)) indicated that it strives for an industry with fewer challenges and promotes SMEs’ activity while encouraging the adoption of digital capital components. This area is of major concern as the sector seeks to improve and rebuild from past challenges. This study thus sought to examine the opportunities and challenges digital capital presents for small food agricultural firms in South Africa. It further sought to explore the inequality claims, assess adoption as linked to performance, and investigate the government’s role in addressing digital capital access inequalities. The study sought to address the following questions:

What digital capital technologies and competencies are food agricultural SME firms adopting, and what adoption challenges (barriers) do they face?

What is the influence of digital capital on food agricultural SMEs’ performance?

What is the digital capital causal effect of industry inequality?

How do food agricultural SMEs perceive the government’s role in supporting their digital capital adoption journey?

2. Literature review

Given the multidisciplinary nature of the study, literature has been drawn from various independent themes. The study brings together digitisation, digital capital, SMEs and agriculture in one place. While there is undoubtedly much literature in these distinct disciplines, there seems to be a dearth of literature on the application of digital capital in agriculture, worst still in the context of agricultural SMEs in Africa. However, there appears to be some sporadic interest lately in the broader digitisation and innovation in agriculture. For instance, Wedajo and Jilito (Citation2020) examined the value of social ties, how mutually supportive social network associations can drive agricultural innovation, and how farmers use such networks to scale up agricultural innovation. Debesa et al. (Citation2020) study analysed the suitability of GIS and remote sensing-based for major cereal crops in South-West Ethiopia. Ouma et al. (Citation2020) explored an innovation platform to enhance marketing decisions for smallholder farmers in Kenya.

Various authors also have evaluated technological innovations performance and the application of Public-Private-Partnerships (PPPs) in agricultural institutes (Kolaj et al., Citation2019; Kolomoiets et al., Citation2021; Saruchera & Phiri, Citation2016; Spielman et al., Citation2010). Thus, these sample articles indicate that the interests have been in broader innovation, as opposed to specifics around digital capital in the agricultural sector.

This section presents a review of the literature on digital capital adoption and its challenges, an assessment of whether digital capital and firm performance is a threat or opportunity, digital capital inequalities, and the role of the Government in addressing such inequalities.

2.1. Digital capital adoption and its challenges

In an ideal environment, small businesses would embrace digital capital. There will be a clear definition, with the boundaries clearly identified and accompanied by positive attitudes towards adoptions. The literature suggests that digital capital uses digital technology tools and intangible assets to improve the company’s value chain (Manyika et al., Citation2017); therefore, digital capital should transform every business and enhance value. Ideally, digital capital will have limited access barriers to a healthy digital ecosystem. Proper adoption guidelines (frameworks) would reduce uncertainties and threats for SMEs within the agricultural sector. More so, digital capital should give opportunities to all food manufacturers regardless of size and financial strength. Small businesses must be able to go pound for pound with big firms as digital capital would have facilitated equal success opportunities and fair and healthy competition. Because in most scenarios, SMEs face many challenges, such as finance, skilled labour, and infrastructure, which normally creates unfair competition due to limited stamina to fend off competition. Therefore, the state would pitch in and assist SMEs in different ways to avoid failure.

However, the current landscape is completely far off from the ideal situation. Digital capital has become a broad concept and continues to expand as more studies emerge. Many definitions of digital capital have become confusing and vague on what it is and how potential adopters should examine it. Some authors claim the intangible attributes of tangible digital technologies, while others claim it is the accumulation of digital competencies. Others view it as an extension of technology progressions from traditional technologies (Sussan & Acs, Citation2017). Because of vague digital boundaries or characteristics, it has produced a series of adoption challenges. Large companies with strong financial positions can make digital capital part of the core capital. Small businesses are negatively suffering from these discoveries as they are not at par in terms of adoption with larger firms. The uncertainty surrounding the benefits of Agri-SMEs is ever-increasing. The ability to classify digital capital adoption phases where it would be clear in terms of levels of adoption still seems farfetched, as any company which adopts a certain technological tool is deemed to be a digital capital adopter even though the tool plays a minimal role in the overall or actual company production. Digital capital has created gaps that have led to economic challenges for SMEs. Additionally, a lack of government intervention and support is visible. Instead of digital capital creating opportunities for agricultural SMEs, it has become a huge subjective threat.

Consequently, the gap between the ideal situation and the current landscape has some consequences that justify this research’s need. Because of so much uncertainty surrounding digital capital, it has led to a lack of knowledge and ability to quantify the phenomena. Additionally, limited literature on digital capital dimensions has resulted in adoption barriers, as small manufacturers may not have a clear view of this capital. Furthermore, despite so much hype and potential benefits that emerge from the digital capital association, there has been sparingly less literature on successful digital capital adoption equating to positive company performance. Instead, most previous studies have extended their arguments and linked digital capital to the digital divide, significantly increasing the inequality gaps between small and large firms. Not only has digital capital facilitated digital inequality gaps, but it has also increased the severity of challenges small businesses face when pivoting towards adoption. The costs associated with digital capital integration, the need for skilled labour, and ICT infrastructure, amongst other factors, have become more severe due to the nature of digital capital. Subsequently, there are visible trails of small firms’ failure due to digital capital and lack of government support.

Additionally, there has been an unfair practice as larger firms utilise digital capital components to drive SMEs within the food agriculture sector into insolvency. This has affected the overall agro-food sector value chain, which is already complex, concentrated, and highly monopolised in South Africa, increasing inequalities. This has given strong affirmation that digital capital does not drive small business success; instead, it facilitates their downfall, which is not a pleasant position considering the crucial role SMEs play in the economy of South Africa.

2.2. Digital capital and firm performance: Threat or opportunity?

The threat element should be viewed through the lens that the attributes of digital capital should accommodate SMEs, and they must be able to navigate through barriers easily; hence if not, they are a threat, while opportunities should relate to the benefits of adoption how it improves performance. Small firm producers play a critical role in the industry as they contribute over 22% of the income generated within the sector (Department of Agriculture, Forestry and Fisheries DAFF, Citation2019). Agri-sector SMEs contribute toward the actual output production. They intensify competition which leads to product affordability. They create employment and facilitate innovation by bringing new ways to enhance their processes. There are many opportunities that SMEs within the food agriculture sector can exploit from “business-to-business”, “business-to-consumer”, and the state. ITA (2020) indicates growing demand to increase the country’s informal small-scale and subsistence farming. The opportunities may include auxiliary services such as marketing and or advertising at the business-to-business level, being involved in core commodity production, and with the increased application of digital technologies, SMEs may offer smart-farming solutions (Born et al., 2020).

Despite the mentioned opportunities, the current prevailing conditions in the food agriculture sector in South Africa are that most small producers face huge challenges while large farmers also have their own fair share of problems. As earlier statistics indicated, the industry is in the hands of a few, and SMEs face market access challenges. The market is saturated with many promotional wars where price and product differentiation are critical (ITA 2019). Additionally, the land reform programmes neglect their needs, lack of finance is still a major concern, access to digital technology troubles them, volatile exchange rates negatively impact their international trade practices, shrinking local markets due to economic challenges, and COVID-19 is a major concern, whether distorted patterns significantly affect SMEs production and shortages in skilled labour is a challenge (SEDA, Citation2021; Stats SA, 2021; (Citation2019)).

2.3. Digital capital inequalities

Digital capital offers great opportunities while posing a threat to small agricultural firms. The magnitude of benefits and threats for SMEs remains vague but very visible. Countless times it has been documented that those small businesses play a crucial role in any economy. South Africa is not excluded, statistics indicate the importance of small businesses, and when narrowing it down to the agricultural sector context guided by their income contribution of 22.4% (Stats SA, 2019), it is evident enough that they are important. Additionally, (Citation2019) has emphasised SMEs’ role in the food industry as they contribute to employment creation, poverty reduction, hunger elimination, and the overall contribution to the country’s output.

Notwithstanding the immense contribution made by smallholder food producers, adjudicating from their nature of limited resources (Tchouwo et al., Citation2021), which tends to impact their value chain services, they are always at risk of failure. Digital capital is a crude proxy for SMEs’ success. Initially, most adopters were influenced by the hype and potential of digital capital though it was the solution to their challenges. Instead, it has created a digital divide, the source of inequalities.

Ragnedda (Citation2018) refers to the digital divide as the technology benefits realisation gaps between countries or firms considering the socio-economic background. Mistry (Citation2014) states that the term “digital divide” has been used to refer to the gap between those who have access to utilise ICT and those who do not. Citation2022) view digital capital as an extension of all capital but targeted to technological integration. To operationalise the above definitions for this paper, the digital divide is the gap in access to equal digital capital technologies and competencies due to limited resources within the agricultural food sector of South Africa. Considering the nature and boundaries of digital capital, guided by earlier discussions and past literature discoveries, this technology-related phenomenon is very costly to acquire and integrate within business value chain processes (Brynjolfsson et al., Citation2019). Maintenance and adaptation (due to continuous innovation) costs emerge because of digital capital adoption. High costs have negatively affected the adoption appetite of small-scale farmers as they cannot afford some of the new digital capital inventions, which will have the necessary influence on their actual production rather than on auxiliary services.

In the agricultural sector, which is labour and machine-intensive (Tsan et al., Citation2019), digital capital has been most welcomed by those who can afford larger firms. Not only is it expensive, but it requires high-end skills and technical abilities to integrate and use. The agriculture sector has also been a victim of circumstances due to illiteracy levels prevailing in the South African economy regarding technology-related subjects (Born et al., Citation2021). Marr (Citation2019) argues that technological innovations are very complex; hence only a few can comprehend them.

Therefore, skilled and literate humans are retained by larger firms with financial resources to afford them or offer lucrative packages. Smallholder farmers have expressed their challenges (SEDA, Citation2021). For SMEs to continue participating in the Agri-sector while utilising digital capital, a proper digital vendor ecosystem must exist to help in their digital transformation journey (DTI, 2019). This includes equal infrastructure development, such as the availability of internet connectivity, routers, broadband pipelines, and wireless services (Tsan et al., Citation2019). However, most researchers have documented in South Africa that this is a major concern because of poor digital infrastructure (SEDA, Citation2021). For example, the country has the most expensive data tariffs in the SADC region (Born et al., Citation2021). This can be regarded as a national problem, but large firms have privately engaged in equipping themselves with proper infrastructure, whereas small farmers struggle due to costs associated with such activity. Lastly, the lack of government support has been attributed as a barrier to digital capital adoption by small food agricultural producers. It is well-documented how the state plays a pivotal role in supporting SMEs through different initiatives (Park et al., Citation2020). However, small farmers cry foul of government neglect.

2.4. The role of the government

In the current digital era of rapid technological growth and innovation, the role of information and communication technology (ICT) as a catalyst to enhance economic development and the quality of life in developing countries has become an increasingly important debate. Davenport and Ronanki (Citation2018) believe it is now a prerequisite for firms to be digitally affiliated to guarantee business success. However, this can be subjective as our earlier discussions saw that digital capital does not guarantee business success or improved performance; instead, it has been cited as a driver for inequalities, thus a source for small food producers’ failure. Literature on the digital divide calls for broad-spectrum interdisciplinary frameworks to guard against this gap increase (Bloom, 2017). The challenges seem more severe with all the benefits digital capital brings because governments are expected to bridge existing inequality gaps. Current trends suggest disapproval of the support initiatives as smallholder farmers do not have confidence in the initiatives (SEDA, Citation2021). Cries for digital equality continue to carry on. Xu (2020) suggests that many forces often increase the digital divide, and equally so, many forces can provide the means to bridge the gaps, and the Government is at the centre of the means to assist small-sized farmers.

3. Research methodology

The study was primarily exploratory. Guided by the study’s objectives and research questions, the exploratory empirical study sought to explore the digital capital technologies, adoption and non-adoption reasons, challenges, perceptions, perspectives, and opinions to solve the research. The study utilised both quantitative and qualitative research methods. Quantitative and qualitative data were deemed appropriate, given the mixed nature of the research objectives and the associated research questions. Mixed methods have been proven for their complementarity and ability to highlight multiple perspectives and unravel complex phenomena (Leech et al., Citation2010; Saruchera et al., Citation2014). Table below justifies the study’s adoption of mixed methods.

Table 1. Justification of mixed methods

3.1. Research population and sampling

A research population is a group of individuals, institutions or objects with similar characteristics used for a scientific probe (Black, 2019). The population must meet research demands. The population for this study consisted of the food agricultural sector SMEs in Gauteng, Limpopo, and Mpumalanga provinces. An estimate of 32 000 commercial farmers (DAFF, 2020), according to an income contribution of 22.4%, can be attributed to 7,000+ small businesses widely geographically dispersed across the country (Stats SA, 2021). The study adopted the purposive sampling technique, and 50 SMEs were purposively identified. The purposive sampling technique, or judgement sampling, is the deliberate, non-random selection method where the researcher selects participants because of their qualities (Etikan & Bala, Citation2017). In this case, SMEs had the appropriate information, knowledge, and experiences surrounding digital capital debates, inequalities, and how the government supports or neglects them. There are no supporting theories for the choice of purposive sampling or a set number of participants (Etikan et al., Citation2016). The study selected 50 participants because it was deemed enough and would capture all the necessary information needed to achieve the exploratory nature of the paper’s objectives. The SMEs under consideration were those who were five years old or less. This was guided by the definition of SMEs and the possibility of adopting digital capital after their formation (SEDA, Citation2021; (Citation2019). The SMEs are experienced participants with a great understanding of the phenomenon; thus, purposive sampling was best suited for this study.

Due to time limitations, the research purposively sampled SMEs from different clusters (provinces) because of their geographic dispersions, thus in Gauteng, Mpumalanga, and Limpopo. This clustering allowed the study to generalise findings as they have different characteristics, and their actual product contribution in the market is different as some provinces dominate in one or more Agri-products. Their location plays a vital role in understanding the different views surrounding government support and digital capital access.

3.2. Data collection

The study utilised both primary and secondary sources. The primary sources of data collection were self-administered questionnaires. Secondary data was drawn from journal articles, books, websites, and blogs. This served to assist in the theoretical contributions toward solving the research problem. The self-administered questionnaire was developed around the sub-themes and/or measurement scales addressing the research objectives. Questions about the identified themes were drawn from the extant literature. The study followed proper procedures, and ethical clearance was obtained through the Southern Centre for Inequality Studies (SCIS) [Protocol H21/07/07] before data collection.

4. Discussion of findings

4.1. Profile of food agricultural SMEs

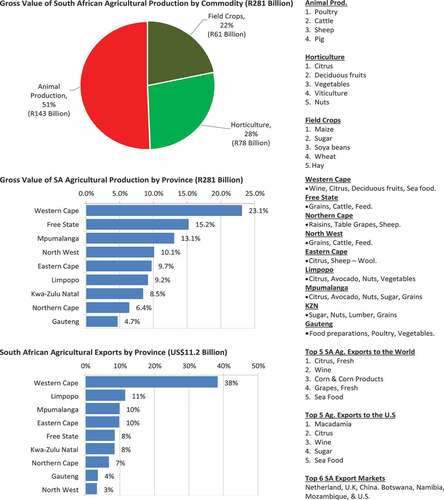

As indicated earlier, the South African food agricultural industry has three broad divisions: animal production, horticulture, and crops. Understanding the overall agriculture sector laid the foundation for understanding SMEs’ profiles and justified some research method choices. All provinces participate in the overall output. The sector is also export-dominated, with citrus fruits, wine and seafood as part of the products exported (Department of Agriculture, Forestry and Fisheries DAFF, Citation2019). Figure below illustrates the industry summarised by the Department of Agriculture, Forestry and Fisheries (DAFF).

Figure 1. The gross value of SA agriculture productivity by commodity, province, and province export.

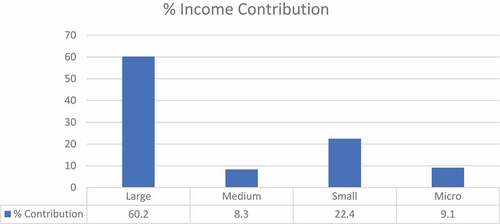

Figure indicates that in terms of gross value rated by commodities which is at R281 billion, with animal production is the most dominant, with just above half of the total commodity at 51%, equivalent to R143 billion, while horticulture came second with 28% equating to R68 billion and field crop occupying the last spot with 22% which was equivalent to R61 billion. This translates to that meat production dominates the food agriculture sector in South Africa. Furthermore, Figure captures the gross production value by province, where the Western Cape Province leads the pack with 23.1% of the total gross value. Free state follows it with 15.2%, Mpumalanga with 13.1%, North-West with 10.1, Eastern Cape with 9.7%, Limpopo with 9.2%, Kwazulu-Natal with 8.5%, Northern Cape with 6.4% and lastly Gauteng with 4.7%. Such outcomes can be expected because Gauteng is the smallest province in the country in geographic terms; hence land for commercial agricultural use may be limited. Statistics SA (2019) estimated that the % income contribution within the sector stood at 22.4% compared to other sizes. Large firms contributed 60.2%, medium 8.3% and micro 9.1%. This clearly indicates that SMEs play an important role as they are the second-best contributors to the income generated by the industry. Figure below illustrates the findings.

Figure 2. Income by enterprise size (%contribution) in the agriculture and related services industry, 2019.

Guided by the above statistics, the study purposively targeted SMEs from Gauteng Limpopo and Mpumalanga. Out of the 50 intended small-sized farmers, 48 responses were obtained and were useable, representing a 96% response rate, which was considered acceptable. Table below illustrates the summarised SMEs profile for the study. The table captures extended demographics, including gender, education levels, position held within the firm, length of service in a particular position, core product, and location.

Table 2. Demographics descriptive statistics

Table shows that male representation dominates the food agriculture SME industry with 56.3%, while females trail behind with 38%. 6% of respondents preferred not to state their gender orientation. The economic well-being of the respondents is modally average. The majority of the respondents have post-matric qualifications such as degrees (31.3%), certificates (29.2%) and Matric (29.2%). Most respondents (45.8%) were the owners or directors of the company (farm owners in the case of farms), followed by 22.9% and 16.7% of the respondents emanating from marketing and production, respectively. Only 8.3% of the respondents emerged from IT. The results also imply that most SMEs within the food agriculture sector are owner-managed, typical of most SMEs in many industries globally (Wang, Citation2016).

Moreover, considering the socio-economic landscape of South Africa, the owner-managing style is taken as a measure to reduce the operational cost that the owners can incur through hiring externally. Two-thirds of the participants (66.7%) had at least more than a year but less than three years in the role, 27.1% had more than 3 years in the role, and 6.3% had less than a year. These statistics aligned with the discoveries that most respondents were owners and had been operating for less than 3 years, which can be linked with the definition of an SME, which can be regarded as a firm that is 5 or less years old (SEDA, Citation2021).

Most (70.8%) of the SMEs in this study produce or process meat and meat products, including poultry, sheep, cattle, and piggery. This was followed by 16.7%, who focused on fruits, and 12.5% of the respondents focused on crops. The statistics are consistent with the overall industry distribution as discovered by (Citation2019)), which indicates that animal production dominates the sector with 51% of total output contribution, horticulture being second with 28%, while crops contribute 22% of the gross output. This was then expected that animal farmers would dominate the participation index. Furthermore, the table reveals that most of the respondents (47.9%) were from Gauteng, followed by Limpopo, with 29.2%, and Mpumalanga province represented 22.9% of the respondents. Although Gauteng has the least gross income contribution compared to other provinces, it is the most populated province, meaning the likelihood of most respondents coming from the province was expected. The province is service industry-dominated by limited land for agriculture compared to other provinces. Limpopo and Mpumalanga provinces have vibrant Agri-economies, with the former contributing 9.2% and the latter contributing 13.1% of the total gross value production output (Department of Agriculture, Forestry and Fisheries DAFF, Citation2019). The purposive participant selection allowed the study to generalise findings since participating SMEs had different geographic locations, offering different products and different exposures. It can be concluded that most small-sized farmers are male-owned. They are coined on animal production, Gauteng has the least agricultural activity, and most individuals have at least some formal education.

4.2. Digital capital adoption

This area is of major concern as the sector seeks to improve and rebuild from past challenges. (Citation2019)) indicated that it strives for an industry with fewer challenges and promotes SMEs’ activity while encouraging the adoption of digital capital components. SMEs indicated that the adoption of digital capital comes with great promise to improve their performance which is realised in the form of increased market access as some digital capital technologies and competencies permit them, smart farming through drones which reduces costs of production and efficiently optimises resources, such as delivery costs (Born et al., Citation2021). The research participants indicated the adoption of digital capital tools and competencies to fight the barriers and challenges they face and improve on their already existing positive, which the digital capital opportunities present. Table indicates the types of digital capital that small-sized firms adopt to address the threats and opportunities presented.

Table 3. Types of digital capital adopted

The results varied as the participants were required to indicate one or more options if applicable. The preferred top three digital tools by the food manufacturing SMEs in South Africa seem to be Communication Technologies, i.e., Chatbots. Social Media (87.5%), Virtual worlds, Websites, and the Internet (75.0%) and Mobile applications and drones (68.8%). Remote working tools (including ERP tools) are slowly becoming popular amongst SMEs, with 43.8%. 37.5% of the respondents noted adopting automated machinery in their production processes. On the bottom three were the Next Generation Payment Methods (27.1%), Cloud Computing (14.6%), and only one firm (2.1%) indicated the use of robots. Qualifying the above statistics using the qualitative discussions obtained from the field, most of these small firms adopted digital capital technologies linked to complementary value chains processes such as marketing, logistics, and communication. The above discoveries align with Citation2019) arguments, which establish that small firms may struggle to adopt the high costs associated with digital capital technologies and machinery for core value production. This clearly indicates that digital capital is a threat because it is expensive for SMEs. Most participants indicated that the internet enabled them to reach other new markets, compete online, interact with customers virtually and use social media as a marketing tool.

The increased internet use was also fast-tracked by the COVID-19 pandemic, which disrupted the value chain processes. Mobile applications, drones and virtual working tools were common among SMEs. Drones and remote sensing systems are utilised as precision and optimisation techniques for irrigation since water is a critical input. Mobile applications have facilitated smart contracts, ensuring transparent and fairly executed contracts. This is consistent with (Citation2019) sentiments that mobile applications have become highly used in the country’s Agri-sector as they increase participation within the value chain practises due to increased connectivity for farmers to markets, suppliers, and other service providers. This has rejuvenated the e-commerce industry. Deloitte South Africa (2020) recorded a 31% increase in online food purchases in 2020 in South Africa. This presents a gap for small-scale farmers to also distribute products and gain more access to markets which has been a major challenge. These SMEs may also engage in strategic partnerships with companies like Takealot, which are dominating the digital retail field. Within that application sphere, participants indicated pivoting towards having their own mobile applications to engage with customers on product and service delivery. The applications will give these SMEs that competitive tool, and not only are these mobile applications coined on “business-to-customer” interactions, but they also overlap to “business-to-business” side as they facilitate information sharing on funding opportunities, disease outbreaks, theft matters, and weather forecasts which can enable effective and efficient planning.

More so, on the distribution side, mobile applications and big data analytics competencies have enabled producers to connect with markets appropriately while shortening value chain times, thus reducing wastage problems. Von Bormann and Gulati (Citation2014) estimated that about 34% of food produced annually for human consumption goes to waste. This means digital applications have the potential to reduce such challenges. Overly, big data analytics assisted small firms with reduced distribution costs associated with fuel consumption, delivery planning, and theft. Data analytics gave participants survival, engagement, and competitive powers. This finding is consistent with Born et al. (Citation2021), who postulate that small-scale farmers have strongly indicated applying big data analytics as a primary decision-making mode. Over the years, data has been generated rapidly; hence, analysing it and obtaining meaningful insights to act on has allowed small-sized farmers to understand the necessary elements of their operations. Tsan’s et al. (Citation2019) say whether data analytics enables farmers to plan on crop plantation and animal preparation for mating seasons, logistics planning for food delivery, and sales and marketing of the consumables to avoid cases of waste. Data analytics provides adopters with predictive, diagnostic, prescriptive, and descriptive capabilities. Apart from big data analytics, digital capital is utilised for payment solutions by SMEs.

As the participants indicated adopting some next-generation payment methods, it was visible that it was handy. Generally, farming practices are rurally concentrated, which may not be easily accessed, and banks may be far from money deposits. Although Point of Sales (POS) machines have partially solved the gap, new technological innovations for fintech have developed applications in which all payments are to be completed digitally without internet connectivity at some point, and only a smartphone is necessary. These applications with improved smart payment methods have proven secure, fast, and convenient for both parties, thus highly embracing many SMEs within the sector. Complementary to payment methods, these applications have allowed SMEs to access finance through crowdfunding applications. Investors have developed applications that allow farmers to access finance online. The process is paperless, and approval does not have delays. This addresses bureaucracy challenges found in Government and other financial services providers. Lastly, cloud computing and robots were coined to appreciate their potential and how they can disrupt their value chain processes as they were pivoting towards adoption.

Having deliberated on the literature presented and the actual position on the ground, it can be denoted that SMEs within the agricultural sector in South Africa have adopted at least one of the digital capital tools and competencies. The interesting discovery is that most of these technologies are for auxiliary services and do not form the core value production chain; hence their influence is very limited. The tools focus more on the value chain process’s support, monitoring, evaluation, distribution channels, and marketing. This translates that when linking the adopted digital capital tools to performance, it may be weak, subjective, and inconclusive to link digital capital to positive SME performance, where they realise an increase in profit margins, increased market share, or easy access to market as these elements can be quantified as performance indicators. Additionally, these help with decision-making processes that are difficult to link to success or improved performance since other elements must be considered.

4.3. Perceptions of digital capital inequalities

The study surveyed participants on the sources of the digital divide to get those comprehensive industry opinions on digital inequalities from SMEs and possible solutions. Guided the study objectives, the survey covered equal access, equal opportunity, government assistance, and digital capital empowerment construct to meet the objectives. Table below shows the respondents’ views on digital capital as the source of inequalities.

Table 4. Respondents’ views on digital inequalities

Table indicates that most of the respondents, 37.5%, strongly disagreed, and 18.8% disagreed that they had equal access to digital technologies. 29.2% of the participants were neutral, 10.4 agreed, and 4.2% strongly agreed they had equal access to digital capital technologies. Respondents who at least disagreed constituted 56.3% of the total, while 29.2% were neutral, and 14.5% at least agreed. With a mean of close to 2 (disagree) and a standard deviation of 1.2, it proves that respondents disagreed that they had equal access to digital capital technologies. The results align with the earlier discoveries that most of these SMEs do not have the financial strength to acquire the core-value production digital capital tools; hence they have limited access as access is only granted to firms who can afford those technologies; thus, in most cases, larger firms. During the survey, some participants indicated that where there is equal access, most digital capital technologies must be able to purchase easily, but they are expensive. In most cases, these are imported. Therefore, in that regard, larger firms are already ahead and will channel the tools into use, which will have a greater impact on their value chain processes, whilst SMEs are left stranded with limited systems that do not have much impact.

From the table, 4.2% strongly disagreed, 4.2% disagreed, 39.6% were undecided, 27.1% agreed, and 25% strongly agreed that limited government intervention had created digital inequalities. The statistics had a mean of close to 4 (agreed) and a standard deviation of close to 1, asserting the findings’ consistency. This was expected as previous researchers had indicated that lack of government support in this digital era would have a negative impact on SMEs as they will not be able to finance the digital capital expenses or build the necessary infrastructure (SEDA, Citation2021). Respondents expressed their distress about government neglect even though the state advocates for digital capital adoption. SMEs cited that digital capital must be coupled with necessary skills they do not possess, high costs they cannot afford, and a viable digital ecosystem in which they are side-lined by larger firms, yet, with government entities, these could be made available. The reality is that the state ignores them. This creates inequalities and leads to SME failure as big firms can navigate those barriers because of their financial abilities and networks, thus creating unfair competition caused by digital capital. This is consistent with earlier discussed findings and past literature, indicating that the agricultural sector is dominated by few yet very concentrated. Lack of government intervention is detrimental to SMEs’ survival; hence the state should act in the interest of both parties to level the ballooning inequality gap caused by digital capital.

Furthermore, at least 54.2% (29.2% strongly disagreed & 25% disagreed) of the respondents disagreed that they have equal empowerment to access digital capital resources, while 27.1% could neither confirm nor deny, 16.7% agreed, and 2.1% strongly agreed. With a mean of close to 2 (disagree) and a standard deviation of 1.1, proving consistency in responses, most respondents disagreed that the sector empowers them to access digital capital equally. Participants affiliated empowerment with equal prioritisation. However, the position in the Agri-sector is that those small farmers are discriminated against in their demands for transformative technologies through high prices. SMEs are regarded as high credit risk such that suppliers neglect them and focus on making a profit by engaging larger firms who pay hefty monies for digital capital technologies.

Lastly, at least 47.9% disagreed (10.4% strongly disagreed & 37.5% disagreed) that SMEs are equally empowered to embrace digital capital, while 29.2% were neutral, 16.7% agreed, and 6.3% strongly agreed. Due to a lack of funding, skilled labour, and digital infrastructure (caused by provincial clustering), some respondents vividly expressed their concerns about the lack of equal opportunity to embrace digital capital. Embracing digital capital has to do with the preparedness and ability to handle the technologies and competencies of digital capital. The actual position is that most of these SMEs indicated a state of unpreparedness as they do not have the infrastructure to support smart-farming technologies; they lack skills, information, and access to appropriate networks. However, larger firms, due to their long existence, have networked and have viable industry relationships, they can access information and build support structures, and they can also accommodate smart-farming solutions and can acquire the necessary skills to fully embrace digital capital, thus creating a digital divide because small firms cannot do that.

By qualifying the literature and the research findings, we can affiliate digital capital as the source of digital inequality. SMEs are characterised by limited finance, high expertise, and limited market share; hence they have been the serious victims of this digital divide. Large firms that are financially stable channel resources towards accumulating digital capital, which enhances their competitive capabilities. Digital technologies are expensive, complex, and require high-level expertise, but most agricultural SMEs do not have those resources. The food agriculture industry is both human and machine-dominated (Ernst et al., Citation2019; Saruchera, Citation2014), so acquiring extra resources (ICT, Smart-agriculture technology) is a daunting task for smallholder farmers, thus giving large firms a competitive edge.

Additionally, industry giants acquire cutting-edge digital capital technologies, which form part of their core processes within the value chain and will make them highly competitive. This means they have already reduced production costs, produced quality products, saved resources, and efficiently evaluated outcomes; therefore, they have more resources to channel towards marketing, distribution, and access to more markets, which results in SMEs being out of business. That on in own side-lines small-sized farmers as customers will buy quality at a lower cost. On the other hand, SMEs cannot afford such equipment, thus widening the digital divide gap. Only the bigger players benefit in this digital era. Although some digital capital technological advancements have allowed SMEs to invest, these have a limited impact on business performance and success as they do not form part of the primary company practices. Because of such developments, digital capital is regarded as a source of digital inequalities.

4.4. Perceptions of the government’s role

The study aimed to explore how the state’s role through certain departments would assist food agriculture SMEs and guard them against the larger firm’s exploitation through digital capital adoption. We have already unearthed that digital capital requires many investments, including financial, human, infrastructure and viable ecosystem investments, to name a few, and the challenge is that food SMEs do not have those kinds of resources; hence, the state is expected to assist them. Table below illustrates the views of the respondents regarding government intervention.

Table 5. Respondents’ views on government support

Table above indicates that 18.8% of the respondents strongly disagreed that the Government offers adequate support to sustain their business, 33.3% strongly disagreed, 29.2% could confirm nor deny, 14.6% agreed, and 4.2% strongly agreed. This view’s popular neutrality was supported with a mean of close to 3 (neutral) and a standard deviation of 1.1, proving that the responses are consistent. Appreciating the state’s role, the participant’s mixed reactions were justified as, during the interactions, the state indeed offered them support to sustain their businesses. Financial resources such as loans, production resources such as tractors, and advisory support from departments like SEDA and DAFF were regarded as very helpful. However, they strongly cited that the state makes promises with little action regarding digital capital support. This is consistent with Ouma-Mugabe et al. (Citation2021) discoveries that establish that the state is a whistle-blower and over-promise SMEs with weak policies and initiatives that are never successful. Therefore, mixed response dominance is expected as the state supported them but not adequately. Considering that government support is not solely rooted in financial and skills support but also includes designing policies that will protect small firm farmers, there is currently not much the Government is doing, particularly on digital inequalities, so that SMEs can harness digital capital benefits. The ones who collectively disagreed happen to be the ones who are in deep rural locations which have never received any support and never meet the requirements for certain support initiatives, while the ones who collectively agreed could have been those who are near access to information regarding certain support initiatives, and these could be based in Gauteng since most of the government offices are there. These views exhumed further discoveries of location discrimination as it was visible that most potential beneficiaries from state support were the ones close to big cities, and inadequate support grows as you further away from those cities. Hence the arguments could be justified why neutral response domination.

Furthermore, Table shows that 29.2% strongly disagreed, 29.2% disagreed, 27.1% were neutral, 14.6% agreed, and no one strongly agreed that the Government offers adequate support to encourage digital capital technologies adoption. Responses were consistent and acceptable to disagree, with a mean of close to 2 (disagree) and a standard deviation of 1. Digital capital is coined on the tools and competencies and other factors to consider, such as the ethics, legal and regulatory issues of digital capital. Maisiri et al. (Citation2021) indicate that the South African Government does not understand the 4.0 technology landscape; hence they cannot offer any support to firms since they find it complex themselves, and creating policies or support initiatives is a mammoth task. This is evident as the industry is less regulated, and most big firms are doing as they please in adoption without any form of adoption boundaries.

Marr (Citation2019) also hinted that middle to less-developed economies could not put measures in place as they were merely users rather than producers. However, this can be an inconclusive argument as users also need protection since the Government somehow regulates every industry through its ministerial divisions. In addition, government policies should aim to minimise the digital divide and create a fair and competitive environment while promoting SMEs. Indeed, this is not the case since most small-sized firms cited a lack of technology adoption regulation as one of the significant contributors to their downfall. Apart from regulatory issues, the Government should provide re-skilling and upskilling models and workshops, offering advisory networks and easy access to information surrounding digital capital adoption, which is not the case as small farmers indicate non-existence. So, the majority at least disagreed that the government offered them adequate support that encouraged digital capital adoption was justified.

Table further indicates the explorative ways the study examined how the state supports SMEs’ digital capital transformation efforts. 25% of the respondents strongly disagreed, 29.2 disagreed, 39.6% were undecided, 4.2% agreed, and 2.1% strongly agreed that the government supported their digital capital transformational journey. A mean of 2.29, thus close to 2 and a standard deviation of 0.9, close to 1, makes the results acceptable and consistent, therefore indicating disapproval of government support towards their digital capital transformation journey. Digital capital transformation is a systematic and complex approach company adopts to implement innovative digital technologies (Matt et al., 2015). Hence SMEs may not have the necessary resources (skilled labour, finance, infrastructure & structure); thus, the Government must intervene and support small businesses. Chen (Citation2020) comments that although digital transformation has positively impacted business performance, productivity and or growth, many obstacles can prevent small businesses from adopting; however, it is the role of the Government to then offer the much-needed adequate support.

However, within the agricultural food sector, SME respondents cited that their digital capital transformation joinery has not been supported that much as there are areas that have never been addressed and are crucial for successful transformation. As the definition suggests that this is a complex exercise, and with a lack of skills prevailing in the area, there is a need for digital training. Training continues to be on the agenda but is not practically done. Furthermore, the promotion of digital capital tools, innovative funding ways and facilitation platforms for SMEs to interact with relevant government departments and established businesses to allow information and skill dissemination is missing, yet they are important for digital capital transformation. All the internet has facilitated bridging some of the skills and information gaps; SMEs stipulate that the state should do more to complement their efforts.

Lastly, 16.7% of the respondents strongly disagreed, 45.8% disagreed, 31.3% were neutral, 6.3% agreed, and none strongly agreed that the Government is providing adequate intervention tools to support SMEs’ digital capital adoption. A mean of close to 2 (disagree) and a standard deviation of 0.8, which is close to 1, indicated consistency in findings that accurately conclude that most respondents disagreed with the statement that the Government provides support tools to assist in their digital capital adoption efforts. To justify their views, participants indicated that the Government had never done anything for them in that regard. However, in some areas, they indicated that they had been given some support in the form of computers. They had an internet connection and could easily get help from the agriculture, forestry, and fisheries departments. This proved pivotal; as previously indicated, the industry is geographically discriminatory. Some SMEs benefit because they are close to government departments, while others do not enjoy the same privileges. Therefore, redressing geographical barriers was important for them. Some respondents cited the lack of infrastructure improvements and redistribution as a major concern. As they cannot afford ICT infrastructure such as routers, they expected the state to engage in fibre connection, which did not affect their digital capital adoption moves. The participants cried foul on the costs of data and electricity, which increased their production costs. They indicated that the Government must restructure its tariffs on the two crucial factors.

Adjudicating the discussion and arguments presented around the state’s role in supporting SMEs within the food agriculture sector, it is clear that the Government does not support small farmers as it should. SMEs face many challenges, such as high production costs, lack of expertise, ICT infrastructure, and necessary vendor ecosystems to adopt digital capital. Notwithstanding government efforts, they are not adequate to be praised. The Government must engage in a series of initiatives to commend their efforts. There is a need for regulation to protect SMEs against the digital divide. There is a need for educational exercises for re-skilling and upskilling.

5. Conclusions, implications and recommendations

SMEs do play a critical role in the economy. Small firms contribute toward employment creation, total GDP, and improved living standards. With the rise of technology outside its main areas, agricultural food sector SMEs have pivoted toward using any technology to enhance their performance. Digital capital is a new phenomenon that firms are adopting. There are physical and digital tools and intangible assets. SMEs are faced with many challenges in adopting digital capital, which is mainly attributed to limited resources. Therefore, we discover that food Agri-sector SMEs adopt digital capital tools and competencies that are less costly. They do not have much of an impact on their performance as they do not form part of the actual production inputs.

Therefore, we can conclude that no feasible evidence indicates that SMEs’ performance improves after digital capital adoption. Because of the limited resources SMEs have and the cost nature of digital capital, SMEs fail to adopt the more important digital capital tools while big firms enjoy the benefits of adopting those. This created the digital divide. The digital divide is, therefore, the source of digital inequalities. Thus, digital capital is not only glamorous, as it leads to potential SME failure. To manage the severe negative impact caused by digital capital, the Government is expected to act, but in the current state, the Government is doing little or none to support and protect food agricultural SMEs. There are many ways in which the state can support and protect SMEs. This can be through education, re-skilling, upskilling, funding, networking, infrastructure distribution and a viable digital ecosystem. The reality is that the state over-promises and under-deliver. Therefore, we conclude that government intervention is weak and needs more action.

SMEs have the power to be disruptive adopters, where digital capital will enable them to be successful if barriers to adoption are removed. However, the major implication is administering and ensuring that every firm has equal opportunity and access to those digital capital tools and competencies. Past studies have viewed global South nations as users rather than adopters of digital capital resources; hence, policymakers may struggle to regulate some systems they do not know about creating. They may face resistance from industry benefactors as they are away, that should the situation change, and they will become the victim of circumstances since the playing field will be levelled.

From a theoretical point of view, the findings suggest that digital capital has been in the past difficult to quantify as it is regarded as a new phenomenon. Thus, the study provides a clear definition of what digital capital is. The study’s findings allude to the past scholarly works that digital capital tends to be more of a hindering capital to SMEs who cannot afford it than larger firms. Furthermore, the findings imply that technology continues to create a digital divide in the emerging and developing economies’ farming landscape with a limited government attempt to create a fair environment.

Apart from the theoretical lens, from a managerial perspective, the results imply that managers should align both their short-term and long-term strategic goals around digital capital as it is visible that it can be regarded as equal to other farming capitals, such as human capital and finance, to name a few. Furthermore, the findings imply that management should channel their investments into re-skilling and up-skilling their staff to be technologically aligned regardless of industry. As a result, the findings infer that management should train their staff around digital capital tools to improve all aspects of their business practices.

As for managing the agricultural SMEs, the Government must promote educational initiatives that will embark on digital upskilling and re-skilling. This will help SMEs reduce illiteracy and the cost of hiring or attracting technology-skilled talent. Digital training increases digital knowledge and the capability to integrate digital capital. This can be done in short-educational programmes or short-term digital certificates. There is also a need for funding schemes provided by the state which will assist SMEs in boosting their financial cash flows and acquiring top-notch digital capital technologies. Already been extensively discussed that SMEs have limited financial resources, and digital capital attracts huge investments, so that these loans will bridge that financial gap. This can happen in partially guaranteed loans.

Additionally, through its ministries, the state should build a collaborative digital ecosystem allowing SMEs to participate actively. A healthy digital ecosystem means there is a potential for skills-sharing, financial investors, advisors, and other important stakeholders who can assist SMEs too. This will also bridge the digital divide gaps, which is the culprit for digital inequalities. With the increased use of Artificial intelligence and virtual worlds, this can be in the form of applications and be facilitated online to cut other related expenses for SMEs, such as travel costs.

The study recommends that SMEs become more agile and adopt more digital capital tools or competencies to have a combined effort that may influence performance. The internet has many free learning materials that can be useful for them rather than relying on government support. Because digital capital adoption does not guarantee success, SMEs must engage in their own research to seek contextualised understanding of digital capital tools offered and examine their suitability to their needs rather than adopting them due to industrial pressure, as this might be costly in the long run. Additionally, agricultural SMEs must foster relationships amongst themselves as it will help them develop synergies and innovative ways to solve their challenges.

6. Limitations and directions for future research

In cognisance of the geographical dispersion of the target respondents, this exploratory study was based on a relatively small sample of fifty respondents within a set of limited parameters. The quantitative components of the study were primarily descriptive. Future studies could consider larger samples with enhanced parameters and employ more advanced quantitative analytical methods. Future studies could also consider conceptualising and modelling the application of more specific digital capital tools within the integrated functional structures of agricultural enterprises.

Acknowledgments

The Future of Work(ers) Research Project at the Southern Centre for Inequality Studies is supported by the International Development Research Centre (IDRC), the Ford Foundation and the Friederich Ebert Stiftung South Africa.

The contributions provided by the Editor and anonymous reviewers of the manuscript are greatly appreciated.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Bennett, A. (2008). “Things they do look awful cool:” ageing rock icons and contemporary youth audiences. Leisure/Loisir, 32(2), 259–22.

- Born, L., Chirinda, N., Mabaya, E., Afun-Ogidan, O., Girvetz, E., Jarvis, A., & Kropff, W. (2021). Digital agriculture profile: South Africa. Food and Agriculture Organisation.

- Bourdieu, P. (1983). The field of cultural production, or: The economic world reversed. Poetics, 12(4–5), 311–356.

- Brynjolfsson, E., Rock, D., & Syverson, C. (2019). 1. Artificial intelligence and the modern productivity paradox: A clash of expectations and statistics. University of Chicago Press.

- Chen, Y. (2020). Improving market performance in the digital economy. China Economic Review, 62(1), 101482. https://doi.org/10.1016/j.chieco.2020.101482

- Davenport, T. H., & Ronanki, R. (2018). Artificial intelligence for the real world. Harvard Business Review, 96(1), 108–116.

- Debesa, G., Gebre, S. L., Melese, A., Regassa, A., & Teka, S. (2020). GIS and remote sensing-based physical land suitability analysis for major cereal crops in Dabo Hana district, South-West Ethiopia. Cogent Food & Agriculture, 6(1), 1780100. https://doi.org/10.1080/23311932.2020.1780100

- Ernst, E., Merola, R., & Samaan, D. (2019). Economics of artificial intelligence: Implications for the future of work. IZA Journal of Labour Policy, 9(1), 1–35. https://doi.org/10.2478/izajolp-2019-0004

- Etikan, I., & Bala, K. (2017). Sampling and sampling methods. Biometrics & Biostatistics International Journal, 5(6), 00149. https://doi.org/10.15406/bbij.2017.05.00149

- Etikan, I., Musa, S. A., & Alkassim, R. S. (2016). Comparison of convenience sampling and purposive sampling. American Journal of Theoretical and Applied Statistics, 5(1), 1–4. https://doi.org/10.11648/j.ajtas.20160501.11

- FAO. (2016). AQUASTAT Country profile – South Africa. Food and Agriculture Organization of the United Nations (FAO).

- Kamariotou, M., Kitsios, F., Charatsari, C., Lioutas, E. D., & Talias, M. A. (2022). Digital strategy decision support systems: Agrifood supply chain management in SMEs. Sensors, 22(1), 274–288. https://doi.org/10.3390/s22010274

- Kolaj, R., Osmani, M., Borisov, P., & Skunca, D. (2019). Empowering partnering links as opportunities for development of the regions: Can PPPs work in agriculture? Bulgarian Journal of Agricultural Science, 25(3), 468–473.

- Kolomoiets, T., Galitsina, N., Sharaia, A., Kachuriner, V., & Danylenko, O. (2021). International experience of public-private partnership in agriculture. Amazonia Investiga, 10(41), 160–168. https://doi.org/10.34069/AI/2021.41.05.16

- Kueh, Y. Y. (1985). Technology and agricultural development in China: Regional spread and inequality. Development and Change, 16(4), 547–570. https://doi.org/10.1111/j.1467-7660.1985.tb00224.x

- Leech, N. L., Dellinger, A. B., Brannagan, K. B., & Tanaka, H. (2010). Evaluating mixed research studies: A mixed methods approach. Journal of Mixed Methods Research, 4(1), 17–31. https://doi.org/10.1177/1558689809345262

- Maisiri, W., van Dyk, L., & Coeztee, R. (2021). Factors that Inhibit sustainable adoption of industry 4.0 in the South African manufacturing industry. Sustainability, 13(3), 1013. https://doi.org/10.3390/su13031013

- Manyika, J., Lund, S., Chui, M., Bughin, J., Woetzel, J., Batra, P., & Sanghvi, S. (2017). Jobs lost, jobs gained: Workforce transitions in a time of automation. McKinsey Global Institute, 150(1), 1–148.

- Marr, B. (2019). Artificial intelligence in practice: How 50 successful companies used AI and machine learning to solve problems. John Wiley & Sons.

- Merisalo, M., & Makkonen, T. (2022). Bourdieusian e-capital perspective enhancing digital capital discussion in the realm of third-level digital divide. Information Technology & People, 35(8), 231–252. https://doi.org/10.1108/ITP-08-2021-0594

- Mhlongo, S., & Dlamini, R. (2022). Digital inequities and societal context: Digital transformation as a conduit to achieve social and epistemic justice: Digital transformation as a conduit to achieve social and epistemic justice. Innovation Practices for Digital Transformation in the Global South: IFIP WG 138, 94, Invited Selection, 72(1), 1–15.

- Mistry, J. J. (2014). A Conceptual Framework for the Role of Government in Bridging the Digital Divide. Journal of Global Information Technology Management, 8(3), 28–46. https://doi.org/10.1080/1097198X.2005.10856401

- Nieuwenhuizen, C. (2019). The effect of regulations and legislation on small, micro and medium enterprises in South Africa. Development Southern Africa, 36(5), 666–677. https://doi.org/10.1080/0376835X.2019.1581053

- Ouma-Mugabe, J., Chan, K. Y., & Marais, H. C. (2021). A critical review of policy instruments for promoting innovation in manufacturing small and medium enterprises (SMEs) in South Africa. Entrepreneurship, Technology Commercialisation, and Innovation Policy in Africa, 237–258.

- Ouma, M. A., Onyango, C. A., Ombati, J. M., & Mango, N. (2020). Innovation platform for improving rice marketing decisions among smallholder farmers in Homa-Bay County, Kenya. Cogent Food & Agriculture, 6(1), 1832399. https://doi.org/10.1080/23311932.2020.1832399

- Park, S., Lee, I. H., & Kim, J. E. (2020). Government support and small-and medium-sized enterprise (SME) performance: The moderating effects of diagnostic and support services. Asian Business & Management, 19(2), 213–238. https://doi.org/10.1057/s41291-019-00061-7

- Qvist-Sørensen, P. (2020). Applying IIoT and AI–Opportunities, requirements and challenges for industrial machine and equipment manufacturers to expand their services. Central European Business Review, 9(2), 46–77. https://doi.org/10.18267/j.cebr.234

- Ragnedda, M. (2018). Conceptualising digital capital. Telematics and Informatics, 35(8), 2366–2375. https://doi.org/10.1016/j.tele.2018.10.006

- Ragnedda, M., Addeo, F., & Laura Ruiu, M. (2022). How offline backgrounds interact with digital capital. New Media & Society, 14614448221082649. https://doi.org/10.1177/14614448221082649

- Ragnedda, M., Ruiu, M. L., & Addeo, F. (2020). Measuring digital capital: An empirical investigation. New Media & Society, 22(5), 793–816. https://doi.org/10.1177/1461444819869604

- Saruchera, F. (2014). Determinants of commercialisation of technological innovations in developing economies: a study of Zimbabwe’s research institutes ( Doctoral dissertation). University of KwaZulu-Natal.

- Saruchera, F., & Phiri, M. A. (2016). Technological innovations performance and public-private-partnerships. Corporate Ownership & Control, 13(4), 549–557. https://doi.org/10.22495/cocv13i4c4p4

- Saruchera, F., Phiri, M. A., & Chitakunye, P. (2014). Consumer perceptions about E10 fuel in Zimbabwe: Managerial implications. Journal of Contemporary Management, 11(1), 470–490.

- SEDA. (2021). SMME quarterly update: 1st Quarter 2021.

- Sjödin, D. R., Parida, V., Leksell, M., & Petrovic, A. (2018). Smart factory implementation and process innovation: A preliminary maturity model for leveraging digitalization in manufacturing moving to smart factories presents specific challenges that can be addressed through a structured approach focused on people, processes, and technologies. Research-Technology Management, 61(5), 22–31.

- Spielman, D. J., Hartwich, F., & Grebmer, K. (2010). Public-private partnerships and developing‐country agriculture: Evidence from the international agricultural research system. Public Administration and Development, 30(4), 261–276. https://doi.org/10.1002/pad.574

- Stats South Africa. (2019). Trends in the agricultural sector. South Africa Department of Statistics. 2019. Department of Agriculture, Forestry and Fisheries (DAFF), 2019.

- Sussan, F., & Acs, Z. J. (2017). The digital entrepreneurial ecosystem. Small Business Economics, 49(1), 55–73. https://doi.org/10.1007/s11187-017-9867-5

- Tchouwo, C. T., Poulin, D., & Veilleux, S. (2021). Understanding the specific characteristics and determinants of open innovation in small and medium-sized enterprises: A systematic literature review. International Journal of Innovation Management, 25(06), 2150063. https://doi.org/10.1142/S1363919621500638

- Tsan, M., Totapally, S., Hailu, M., & Addom, B. K. (2019). The digitalisation of African agriculture report 2018–2019. CTA.

- Von Bormann, T., & Gulati, M. (2014). The food-energy-water nexus: Understanding South Africa’s most urgent sustainability challenge. WWF-SA.

- Wang, Y. (2016). What are the biggest obstacles to the growth of SMEs in developing countries? -A picture emerging from an enterprise survey (No. 09/2016). IES Working Paper.

- Wedajo, D. Y., & Jilito, M. F. (2020). Innovating social connectedness for agricultural innovations in eastern Ethiopia. Cogent Food & Agriculture, 6(1), 1809943. https://doi.org/10.1080/23311932.2020.1809943

- World Bank. (2018). The World Bank Annual Report 2018 ( English). World Bank Group http://documents.worldbank.org/curated/en/630671538158537244/The-World-Bank-Annual-Report-2018.