Abstract

We examined the nexus between four internal audit functions (IAF) and sustainability audits (SA) of manufacturing firms. The specific IAF employed in this study were; risk management practices (RMP), sustainability sensitivity (SS), internal audit effectiveness (IAE) and enactments, policies, standards, systems and procedures (EPS). In line with the four measures of IAE, the study puts forward to investigate four research hypotheses. The explanatory research design and quantitative research approach were applied to achieve the study’s objective. A sample of 1340 managers of SMEs were invited to complete a standard questionnaire based on extensive evaluations of prior empirical investigations. The samples were chosen using a straightforward random process from a population of 2495 manufacturing companies. The results were estimated using the partial Least Square Structural Equation Modelling (PLS-SEM) method. Findings from the study divulged that internal audit effectiveness, risk management process and sustainability sensitivity had significant positive relationship with sustainability audits. It is important for the creation of an audit department, the hiring of a permanent internal auditor, the provision of suitable logistics, the training of personnel on the value of internal audit, and the use of internal auditing standards and principles in the report-writing process for an enhanced sustainability audit.

1. Introduction

A company’s value system and ethical business practices are the foundation for corporate sustainability (DeSimone et al., Citation2021). According to research (Alsayegh et al., Citation2020; Vieira & Radonjič, Citation2020), firms participate in sustainability activities and reporting to promote brand value, reputation, and legitimacy, signal competitiveness, inspire workers, and help control processes. Such action is becoming more widely acknowledged as a significant aspect in corporate sustainability (Alsayegh et al., Citation2020). According to DeSimone et al. (Citation2021), sustainability reporting is becoming more and more important to firms’ global reporting procedures.

Despite an increase in demand for assurance to increase credibility therein (DeSimone et al., Citation2021) and a growth in the literature documenting the expansion of sustainability activities (Imasiku et al., Citation2020; Swann & Deslatte, Citation2019), assurance of sustainability is still in its infancy. According to previous studies, many CEOs anticipate internal auditors to ensure sustainability in order to lower the risk of legal liabilities for environmental wrongdoing and unfavorable public perceptions of unsustainable operations (Corazza et al., Citation2020; Hoffman, Citation2018).

Additionally, there is an increasing understanding that sustainability assurance enhances sustainability management and reporting systems by fostering internal organizational change and improvement as well as external transparency (Kiesnere & Baumgartner, Citation2019). Internal audit functions (IAFs) can add value to their firm by enhancing risk management and developing a deeper comprehension of new concerns, like sustainability.

Examining the effects of internal audit function elements such risk assessment, companies’ sensitive environments, internal audit effectiveness, and enactments, policies, standards, systems and procedures in sustainability audits is the primary goal of this study. This is significant because earlier study (DeSimone et al., Citation2021) emphasises organizational characteristics and external assurance while acknowledging the value of auditing sustainability activity and reporting. However, the research is limited in how it addresses corporate internal contextual factors that result in the voluntary assurance of sustainability strategies, programs, and reporting (Corazza et al., Citation2020; Hoffman, Citation2018). It also does not address whether IAFs are involved in the audit of sustainability activities and effectiveness (Boiral et al., Citation2019; Trotman & Trotman, Citation2015).

Although some qualitative studies have more completely studied the internal setting, they are nevertheless constrained by factors like country (Eulerich & Eulerich, Citation2020; Plant et al., Citation2019). It is important to conduct a study on variables that affect IAFs’ volunteer sustainability assurance because research has shown that stakeholder demands are the primary driver of sustainability assurance activities (Cohen & Simnett, Citation2015; Soh & Martinov‐bennie, Citation2018). According to studies (Clarkson et al., Citation2019; García‐sánchez et al., Citation2019), the need to increase the credibility of the information published in these reports is the primary driver behind an organization’s decision to request the assurance of external sustainability reports.

The assurance of sustainability reporting can be handled by multiple parties, and multiple parties may be involved (Braam & Peeters, Citation2018). Since external stakeholders may view internal assurance as less independent and more likely to be a window-dressing approach than external assurance, businesses are likely to favor external assurance rather than internal assurance in this process of establishing trust and credibility. This does not negate the need of IAFs in ensuring sustainability operations and reporting.

The IAFs as a source of sustainability audits for industrial companies are the main subject of this study. It is recognised that IAF involvement in sustainability assurance may complement external assurance rather than serve as a replacement for it. The study also advances prior research on elements that strengthen internal auditors’ contributions to enhancing organizations’ sustainability management systems (Brunelli & DiCarlo, Citation2020; Marrucci & Daddi, Citation2022; Samagaio & Diogo, Citation2022; Shonhadji & Maulidi, Citation2022). This is important since many stakeholders point out that by identifying these elements, the IAF may play a more active role. This may include a role of a consultant and a guarantor of the organization’s sustainability measures for its long-term performance, increasing its organizational relevance.

The study is conducted in Ghana, a developing economy. The bulk of manufacturing companies are engaged in the production of cement, food and beverages, oil-refining, and aluminum smelting, to name a few, with Accra Metropolis accounting for the largest share. Additionally, given the necessity of a comprehensive awareness of risk across these firms, managing internal audit function with the goal of strengthening sustainability audits in manufacturing companies is not overemphasized (Balaras et al., Citation2019; Samagaio & Diogo, Citation2022).

For two key reasons, the sample of manufacturing companies includes both companies that publish sustainability reports and those that do not. First off, sustainability assurance is not simply present when a report is published; it can also include reporting and/or activity. Therefore, according to DeSimone et al. (Citation2021), sustainability assurance encompasses sustainability plans, risk management, operations, and reporting. Second, internal auditors are in a position to assist in the development of a sustainability communication plan to inform external stakeholders of the outcomes and advancement made in relation to the organization’s economic, environmental, and social responsibilities. Many organisations have room to improve their sustainability management systems.

2. Motivation of the study

The Institute of Internal Auditors (IIA) emphasizes two primary tasks of internal auditors (IAs) in its revised standards: advising (consulting) services and assurance services (Simpson et al., Citation2016). Evidence, however, indicates that the ability of IAs to guarantee sustainability has not been widely pushed (Simpson et al., Citation2016; Soh & Martinov Bennie, Citation2015), leading to a myopic view of the nexus in various geographical areas. These academics clarify the necessity of educating IAs on the hazards connected to sustainability initiatives as well as the reporting procedures. As a result, DeSimone et al. (Citation2021) urge that the relationship between IAFs and sustainability audits be evaluated.

Numerous studies have asserted that external auditors should focus on the internal controls and risk assessment systems that businesses have implemented in order to deliver accurate, comprehensive, impartial, and pertinent audits (Fadzil et al., Citation2005; Hazaea et al., Citation2021; Tarjo et al., Citation2022). According to other research (Boiral et al., Citation2019; García‐sánchez, Citation2020; Perego & Kolk, Citation2012), firms may use the work of assurance providers to also strengthen their internal managerial and organizational capacities in sustainability activities and reporting processes. This could lead to conflicts of interest and compromise the impartiality of an assurance provider.

Therefore, hiring a qualified IA to serve as a manager’s consultant is a means to minimize conflicts of interest and could aid in maintaining the independence of the external assurer. The IAFs should also carry out value-added tasks like sustainability audits, and internal assurance may present chances for IAFs to contribute value by lowering the cost of sustainability assurance. While qualitative approaches have provided a more comprehensive analysis of the internal environment, their usefulness is limited by factors such as country-specific considerations (Eulerich & Eulerich, Citation2020; Plant et al., Citation2019). As a result, the results of earlier investigations are limited, uncertain, and inconsistent. To resolve some of the inconsistencies in the literature, it is crucial to undertake a study on the relationship between IAFs and sustainability audits in a developing country environment. It is against this backdrop that the current study provides a unique contribution on the nexus between internal audit functions and sustainability audits in manufacturing firms.

The study contributes to existing theories on internal audit and sustainability audits. Outcome from this study would help to ascertain whether the agency and stakeholder theories are violated or confirmed. As much as owner managers are interested in maximising their wealth from the firm, other interested parties require that the firm operates sustainably into a foreseeable future period requiring the firm to put in place a sound internal audit function.

For academic and practical purposes, the study’s findings are pertinent to a better understanding of the connection between internal audits and sustainability audits of manufacturing companies. It will also let management of these companies know how well internal resources are used to boost performance in light of shifting business environment conditions. The results of this investigation will also aid in resolving certain discrepancies in earlier research.

The findings of this study have implications for efforts being made around the world to increase awareness of the need for integrated sustainability assurance, particularly IAs, among those who write and utilize sustainability reports. The growing role of IAs in providing an integrated sustainable guarantee would also be known to users of sustainability data. Finally, IAs and trainers of internal audit services would be aware of the necessity of preparing and equipping an IA in order to improve the validity and applicability of sustainability audits.

The research is supported by the following objectives;

Assess the influence of risk management process on sustainability audits.

Examine the effect of sustainability sensitivity on sustainability audits.

Determine the influence of internal audit effectiveness on sustainability audits.

Evaluate the influence of enactments, policies, standards, systems and procedures on sustainability audits.

The remaining sections are arranged as follows. The study’s review of related literature and methodology are contained in sections 3 and 4 respectively. Sections 5 and 6 respectively shows the results and discussion. In section 7, the study’s conclusions and implications are presented.

3. Literature review

3.1. Theoretical review

The study is guided by two important theories in examining the relationship between internal audit function and sustainability audits. The theories utilised in this study are the agency theory and stakeholder theory. The section initially explains the agency theory, followed by the stakeholder theory.

3.1.1. Agency theory

The agency theory is one of the most well-established concepts in management and economics literature (Daily et al., Citation2003). This theory, developed by Jensen and Meckling (Citation1976), assumes that managers (agents) try to increase their benefit at the expense of the interests of the owners (principals), who hire managers. Owners suffer as a result of a dispute (principal-agent issue) brought on by managers’ conduct.

The challenges that occur in enterprises as a result of the division of ownership and management are addressed and are given particular importance in agency theory. Businesses typically find it impractical to put this idea into practice because contracts are frequently inadequate. Disclosure might be another strategy to lessen information asymmetry and, hence, agency costs by lining up the interests of shareholders and managers (Healy & Palepu, Citation2001; Watson et al., Citation2002).

Businesses operate like a “black box” to optimize their worth and profitability, claim Jensen and Meckling (Citation1976). By correctly coordinating their efforts, the stakeholders involved in the firm can collaborate to enhance their wealth. However, a conflict of interest arises when the parties’ interests diverge, and it can only be resolved by managerial ownership and control. The parties with self-interest also recognized that for the firm to meet their needs, it must exist. To assure the continuation of the business, they therefore perform magnificently. In a similar spirit, Fama (Citation1980) championed the idea that enterprises can be disciplined by the competition from other players, which monitors both the performance of the team as a whole and of particular individuals.

Perrow (Citation1986) criticized positivist agency researchers for concentrating only on the agent side and claimed that the “principal and agent problem” may also originate from the principal side. He emphasized that this perspective has no concern for the principals, who exploit, avoid, and control the agents. The agents work in a perilous environment with limited opportunities for intervention, while their principals exploit them unknowingly.

Hence, there is the need to ensure that effective internal audit function is put in place to maximise sustainability of the audit process in businesses (Shonhadji & Maulidi, Citation2022). Sustainability audits by the IAF are intended to assist organisations in achieving managerial commitment, controlling their sustainability activities, adhering to organisational sustainability policies, and complying with environmental regulations with an emphasis on an objective review (DeSimone et al., Citation2021). Accordingly, the current study examines the association between internal audit function and sustainability audits.

3.1.2. Stakeholder theory

“According to the stakeholder theory, a company endeavor’s primary goal is to provide as much value as possible for its stakeholders (Freeman, Citation2004; Citation1984). Senior management must make sure that the interests of customers, suppliers, employees, communities, and shareholders are aligned and pointed in the same direction for a business to succeed and last over time. Managers are accountable to more than just shareholders, according to Freeman (Citation2004). They must take into account every group or person who can influence or be impacted by the achievement of the firm’s objectives in addition to shareholders or stakeholder groups. Therefore, implementing an efficient internal audit function will go a long way toward assuring sustainable audits to the advantage of interested parties by protecting the asset of the SMEs from misuse (Samagaio & Diogo, Citation2022).

3.2. Empirical review

Despite the growing acceptance that businesses should report on pertinent sustainability issues, stakeholders may not always recognise the significance or value of these reports being independently assured. The goal of Ridley et al. (Citation2011) paper was to emphasise that the internal audit function can and does provide this assurance, significantly enhancing the effectiveness of corporate governance. The study, although is theoretical in nature, refers to a few “real-world” examples. Key internal auditing professional standards and recommendations are evaluated in character and in a comparatively organised way, along with earlier theoretical and empirical research. The article supports the claim that reporting sustainability policies, procedures, and measures has less value for stakeholders when there is no independent confirmation. The study provides evidence to demonstrate how internal auditing has not always been pushed globally in this function, despite the possibility for doing so. Similar to how more businesses are engaging in sustainability efforts, assurance of these efforts is a more recent development. As a result, DeSimone et al. (Citation2021) looked at the correlations between firms involving their internal audit functions (IAFs) in sustainability audits and the presence of risk assessment by internal auditors, sustainability sensitivity, IAF age, and release of sustainability reporting. They discovered inconclusive results between IAFs and sustainability audits for organisation types as well as continental analyses.

The purchase of products, services, and public works accounts for over 70% of the annual budget spent by the Ghanaian government. To control public procurement activities and guarantee openness, accountability, and value for money (VFM) in the procurement procedures, the Public Procurement Acts (Acts 663 and 914) were enacted (Adam & Kissi, Citation2021; Seyram, Citation2017). On the other hand, public officials in Ghana are misusing public monies to an unprecedented degree. The work by A. M. Karikari et al. (Citation2022) sought to solve this issue by creating a model that would explain the extent to which Internal Audit Effectiveness (IAE) influences VFM and sustainable public procurement (SPP). A cross-sectional survey method of public institutions in Ghana was utilised. The study employed 72 District Assemblies from the Greater Accra and Ashanti regions made up the study’s sample. Two hundred participants, including internal auditors, procurement officials, accountants, and finance officers, were chosen at random for the study using a stratified sample technique. The survey results were analysed and the study’s assumptions were tested using the Smart-PLS programme and the Structural Equation Modelling (SEM) methodology. The study found that the key predictors of IAE include top management support, external auditors’ involvement, internal audit independence, and competency of internal auditors. Once more, their investigation of the mediation showed that IAE promotes both VFM and SPP. The outcomes also demonstrate that a rise in VFM has a favourable impact on SPP.

In their 2015 article, Soh and Martinov-Bennie looked into the type and scope of internal audit functions’ (IAFs’) participation in environmental, social, and governance assurance (ESG) and consulting in Australia. The paper also investigated internal audit practitioners’ perceptions of the current and future importance of these issues and the adequacy of their skills and expertise in meeting the challenges associated with their involvement in these areas in order to identify emerging priorities and the profession’s capacity to respond to these. Information was gathered from 100 Chief Audit Executives and internal audit service provider partners. Results showed that respondents’ assurance and consulting efforts are mostly focused on governance issues, with social and environmental issues coming in second and third, respectively. While environmental issues are most frequently predicted to become more significant over the next five years and are believed to be in greatest need of further development of IAFs’ skills and experience, governance challenges are still thought to be of the greatest current importance to IAFs.

The relationships between internal audit functions and sustainability audits have been inconclusive. Accordingly, the context within which a study is conducted, and differences in internal audit functions may influence the outcome. For instance, as DeSimone et al. (Citation2021) revealed a significant influence of sustainability sensitivity on sustainability audits in listed companies and not-for-profit making firms, it was found otherwise in unlisted companies for the organisation type analysis. Risk management on the other hand was revealed to have a significant positive effect on all firms but the effect was substantial for unlisted firms. For the continental-level analysis, DeSimone et al. (Citation2021) revealed an insignificant effect of sustainability sensitivity on sustainability audits in Africa, Europe and Latin America, but significant for Asia and Oceania, and North America. The effect of risk management was however significant in Africa, and Asia and Oceania. A study by Pérez-Cornejo et al. (Citation2019) demonstrated that risk management processes are necessary for corporate reputation in Spanish firms. A study conducted in Ghana provided that internal audit effectiveness is pertinent for arousing value for money and sustainability procurement (see, A. M. Karikari et al., Citation2022). This is confirmed by other studies conducted in Ghana (Angmor & Diaboh, Citation2022; A. Karikari et al., Citation2023; Ziniyel et al., Citation2018, etc.). Mulyani et al. (Citation2019) found otherwise by revealing that internal audit effectiveness does not enhance corporate sustainability in Indonesia. In European countries, Simoni et al. (Citation2020) ascertained that sustainability sensitivity does not relate to sustainability assurance reports. Conversely, internal audit functions like enactments and policies had a significant positive influence on sustainability assurance reports as found by Simoni et al. (Citation2020).

Due to the inconclusive results exacerbated by geographical area and the choice of internal audit function parameters employed as well as the lack of enough study on the subject matter, it is important to revisit the relationship between IAFs’ and sustainability audits. The primary reason organizations request external sustainability reports is to increase the credibility of the information published, according to studies conducted by Clarkson et al. (Citation2019) and García‐sánchez et al. (Citation2019). Additionally, in the context of the study, manufacturing firms are required to be environmentally friendly to improve sustainability audits, as noted by Samagaio and Diogo (Citation2022). In this manner, we formulate the following hypotheses to guide the study;

H1:

There is a significant influence of risk management process on sustainability audits.

H2:

There is a significant effect of sustainability sensitivity on sustainability audits.

H3:

There is a significant influence of internal audit effectiveness on sustainability audits.

H4:

There is a significant influence of enactments, policies, standards, systems and procedures on sustainability audits.

4. Methodology

The goal of the study was to ascertain how internal audit functions affected sustainability audits of manufacturing companies in the Accra Metropolis. As a result, this section provides the research techniques required to fulfill the study’s objective. The quantitative research approach is specifically used in this study to increase the objectivity and verifiability of results in order to minimise the subjectivity or biases of the researcher. The explanatory research design was specifically used in the current study to evaluate the connection between the internal audit function and sustainability audits.

4.1. Population and sampling

The managers of manufacturing companies in Accra Metropolis were the study’s target group. Around 41% of manufacturing businesses are located in Accra, according to the Ghana Statistical Service (GSS) in 2015. Managing internal audit function toward improving sustainability audits in manufacturing companies is not overemphasised because of the requirement of a holistic understanding of risk across these companies (Samagaio & Diogo, Citation2022). The GSS reported that 2495 people worked in manufacturing enterprises in Accra Metropolis in 2015.

It is common knowledge that a sample is a portion of the population that is selected and studied (M. Saunders et al., Citation2009). Therefore, the sample size was determined using the Krejcie and Morgan (Citation1970) sample size determination table with a 5% and 95% margin of error and confidence level, respectively, because the targeted population of this study included managers of manufacturing enterprises in Accra Metropolis. According to the Krejcie and Morgan (Citation1970) sample size determination table, the proper sample size for this investigation, given the population size of 2495, was 335. As a result, the current study settled on a final sample of 1340 which exceeds the minimum sample size. For this study, a straightforward random selection method was deemed necessary.

4.2. Data collection and administration

The current study’s data came from primary data. Primary data was taken into consideration because it allows the researcher to get data directly from sources. In order to gather information from managers of manufacturing companies in Accra Metropolis, a systematic questionnaire was created. Questionnaire was chosen as the best method for gathering data from a large population because of its homogeneity and objectivity (M. Saunders et al., Citation2009). For this investigation, a seven-point Likert scale was used. The questionnaire was chosen from a variety of literary sources that fit the context and goal of the study (see, DeSimone et al., Citation2021; Thabit et al., Citation2019).

In order to encourage mitigation of errors in the comprehension of the research instructions and questions, the current study conducted a preliminary assessment (Kurzhals, Citation2021). According to the standard stated by M. N. Saunders et al. (Citation2015) for pre-testing, a sample of twenty-five (25) managers of manufacturing companies were taken into consideration for the pre-testing. The results of the pre-testing showed that the respondents were not overly sensitive to the items of questionnaire, the questions were not skipped, and they understood the various items within the questionnaire. In this regard, the scales were precise and useful.

The survey approach was deemed suitable for the current investigation. The information from respondents was gathered using a standardized questionnaire in accordance with the research objectives, necessitating the following steps. The distribution of the questionnaire and subsequent data collecting marked the start of the process. In addition to the researcher, three professionally trained field assistants assisted with the distribution and collection of the questionnaire.

4.3. Validity and reliability

In order to improve consistency and minimize biases, the study also made sure that the validity and reliability of the research instruments were adhered to (Belur et al., Citation2021). Therefore, in order to create reliability, it is necessary to provide a trustworthy measurement of a constant value (Weakley et al., Citation2021). This addresses the possibility that a known measurement approach could frequently result in comparable descriptions of a certain phenomenon.

The study uses the Cronbach’s Alpha coefficient to achieve this purpose as indicated in Table . This was obtained using the pre-test data. Following the assertion made by Belur et al. (Citation2021), on the desirability of the Cronbach’s Alpha coefficient, a minimum value of 0.7 addressing internal consistency of the research variable is necessary. It can be concluded from Table that the research variables have good internal consistency because of the Cronbach’s Alpha coefficients in excess of the 0.7 benchmark.

Table 1. Reliability values from cronbach’s alpha coefficients

4.4. Data processing and analysis

The Statistical Package for Social Sciences (SPSS) software, version 18, was used to record the responses received from managers of manufacturing companies. Each item on the questionnaire was assigned a code, which was then compared to the entries made in the SPSS to ensure that errors were kept to a minimum. In order to improve further statistical analysis, the data was subsequently cleansed by removing any conflicting data. The Partial Least Squares-Structural Equation Modeling (PLS-SEM) was used to conduct an inferential evaluation of the data in accordance with the study’s goals. To accomplish all the goals of the research, the PLS-SEM was used. Due to the PLS-SEM’s robustness in managing correlations between latent variables irrespective of normality issues unlike the covariance-based SEM (CB-SEM), it was chosen (Hair et al., Citation2019).

5. Results

The study examines the effect of IAF on SA of manufacturing firms at Accra Metropolis. Particularly, the study seeks to assess the effect of risk management process (RMP), sustainability sensitivity (SS), internal audit effectiveness (IAE) and Enactments, policies, standards, systems and procedures (EPS) on SA. The final sample for this study contained 1340 manufacturing firms at Accra Metropolis collected through the simple random approach. The quantitative strategy and explanatory design are consistent with the current study.

The majority of responders, or 57% of the overall sample size, are men, as shown in Table . So, the sample’s 43% of females. 36% of the sample’s respondents have job experience between 11 and 15 years, which is a fair amount. Individuals with more than 15 years of job experience come in second, comprising about 29% of the sample. The sample’s average employment experience is between six and ten years, with one to five years being the lowest. Additionally, almost 44% of the sample of responders have a graduate degree. Individuals with a professional qualification, who make up around 31% of the sample, come in second. Additionally, 15% of the sample has post-graduate education.

Table 2. Profile of respondents

5.1. Measurement model assessment

5.1.1. Construct reliability, indicator reliability, and convergent validity

The PLS-SEM results begin with a model evaluation to assess the fitness of the model by analysing the indicator’s reliability (loadings), construct’s reliability (as assessed by Cronbach’s Alpha and rho A), convergent validity, and discriminant validity (Hair et al., Citation2020). Additionally, composite reliability (CR) was used to evaluate construction dependability.

According to Table , all of the indicators loaded satisfactorily, with a loading coefficient of at least 0.7. (Hair et al., Citation2020). The CR and CA loadings in Table support the indicator’s default value of 0.7. 2020 (Hair et al., Citation2020). The effectiveness of combining indicators of various components to measure those constructs is indicated by the composite reliability (CR), which is illustrated in Table . Values of CR must typically be less than 0.70. (Hair et al., Citation2020). The constructs consistently have composite dependability (CR) values more than 0.7, as shown in Table , proving their durability (Hair et al., Citation2020). All indicators with AVE values above 0.6 are also loaded with convergent validity. Table ‘s least AVE of 0.662, which is higher on average than the variance described by the concept, suggests that the products have higher volatility, per the advice of Fornell and Larcker (Citation1981). The results show that the model is convergently valid because all hidden variables have an AVE above 0.5.

Table 3. Construct reliability, indicator reliability, and convergent validity

5.1.2. Discriminant validity

Discriminant validity assesses a construct’s distinctiveness (Hair et al., Citation2020). Tables assess the constructs’ discriminant validity to show how good the model is (Hair et al., Citation2020). According to Hair et al. (Citation2019), the discriminant validity evaluates the structural model for collinearity problems. The Heterotrait-Monotrait Ratio (HTMT) is used to evaluate the discriminant validity. The range of the HTMT cutoff scores is 0.85 to 1.0 (Hair et al., Citation2020).

Table 4. Heterotrait-monotrait ratio (HTMT)

Table 5. PLS predict for the constructs

The HTMT performs better since it can identify a lack of discriminant validity under typical study circumstances. HTMT scores (correlation values among the latent variables) should normally be less than 1.0 in order to obtain discriminant validity. The construct values in Table were all under 1.0. This illustrates how completely different one construct is from the others. PLS predict

The predictive ability of the numerous potential indicators and constructs that served as dependent variables in the SEM is shown in Table . The Q2 predict is first reviewed to make sure that the predictions outperform the naivest (above 0) benchmark (Hair et al., Citation2020). If the predicted outcomes are better than the baseline value, then other prediction statistics, such as RMSE and MAE, can be explored (above 0). In order to assess the prediction error of a PLS-SEM analysis, Hair et al. (Citation2020) state that the RMSE values are contrasted with a baseline value derived by a linear regression model (LM) that makes predictions for the measured variables.

Table shows that the Q2 predict values surpass the naivest benchmark, with indicator SCP2 having the lowest Q2 predict value at 0.257. From Table , it can be seen that the model has a moderate capacity for prediction because none of the dependent construct indicators have larger RMSE or MAE prediction errors compared to the naive LM benchmark except SA1. These values are PLS-SEM RMSE and MAE values, which are shown in bold. In this situation, it can be assumed that the PLS-SEM model has better predictive capabilities.

Standardized Root Mean Square Residual (SRMR) for the model is shown in Table , and according to Hu and Bentler (Citation1999) and Henseler et al. (Citation2016), it should be less than 0.08; the closer the Normed fit index (NFI) value is to 1.00, the better the fit. The model’s estimated Chi-Square, which is calculated by dividing the degrees of freedom (number of observations minus number of independent variables) by the estimated value of the Chi-Square, should be less than 3 (Mantel, Citation1963).

Table 6. Model fit summary

Table shows that the model’s SRMR values of 0.043 and 0.048 are less than 0.08, which indicates a reasonable model fit with few deviations from the expected and observed correlations. Additionally, the NFI value is greater than the threshold of 0.8; as a result, the model is considered to have marginal fit. As previously mentioned, the model’s Chi-Square evaluation is roughly 2.625 (i.e., 868.756/331), which is lower than the benchmark of 3 and indicates that the model has a decent fit.

5.2. Structural model assessment

The study further explores the research hypotheses after establishing construct and indicator reliability, as well as convergent and discriminant validity. By analysing the direction and strength using the coefficients, p-values reflecting the level of significance using 5000 bootstraps, coefficient of determination (R2 and R2 Adjusted), effect size (f2), Confidence Interval (CI), Q2 predict, Root Mean Squared Error (RMSE), Mean Absolute Error (MAE), and variance inflation factor (VIF) in Table , this work was completed.

Table 7. Summary of structural model

From Table , the endogenous variable is sustainability audits (SA) considered in this study. Hence, only direct relationships are performed in this study. It shows the effect of IAF (EPS, IAE, RMP and SS) on SA. The exogenous variables account for about 56.3% of the variations in SA, according to the model produced by Table . The relational variables have a negligible effect, according to Cohen’s f2. According to Table , the pathways are free of multicollinearity because the maximum VIF, which is 4.418 and less than 5 (Hair et al., Citation2020). The positive Q2 predict values and the closer they are to the adjusted R2 signify that the PLS-SEM model in general has a predictive relevance.

The study next reports the PLS-SEM path coefficients and significance in Figure after finishing the diagnostic tests. Figure can be used to address all of the study hypotheses in a single model. The factor loadings were omitted to improve clarity for easy comprehension.

Figure 1. Structural path coefficients and bootstrapping.

It can be seen from Figure that the first research hypothesis on the influence of RMP on SA is found to be positive and significant (β=0.225, p-value < 0.05). It suggests that the null hypothesis of no significant influence of RMP on SA is rejected. It can be said that a unit increase in RMP corresponds to a 0.225 unit increase in SA. Accordingly, risk management practices are needed to enhance sustainability audits among manufacturing firms at Accra Metropolis.

Moreover, the second research hypothesis on the effect of SS on SA is investigated. It can be seen that SS (β = 0.455, p-value < 0.05) has a significant positive effect on SA. Hence, the null hypothesis of no significant influence of SS on SA is rejected. In this manner, a unit increase in SS corresponds to a 0.455 unit increase in SA. It can then be concluded that SS is relevant in enhancing SA of manufacturing firms in Accra Metropolis.

Also, the third research hypothesis on the effect of IAE on SA is analysed. It is observable that IAE (β = 0.268, p-value < 0.05) has a significant positive effect on SA. In this regard, the null hypothesis of no significant influence of IAE on SA is rejected. This implies that a unit increase in IAE leads to a 0.268 unit increase in SA. It can then be concluded that IAE promotes SA of manufacturing firms in Accra Metropolis.

To end with, the fourth research hypothesis on the effect of EPS on SA is investigated. It is observable that EPS (β = −0.134, p-value > 0.05) has an insignificant effect on SA. It can be said that, the null hypothesis of no significant influence of IAE on SA is not rejected. This means that enactments, policies, standards, systems and procedures are weak enhancers of SA. It can then be concluded that EPS is not relevant in enhancing SA of manufacturing firms in Accra Metropolis.

5.3. Robustness

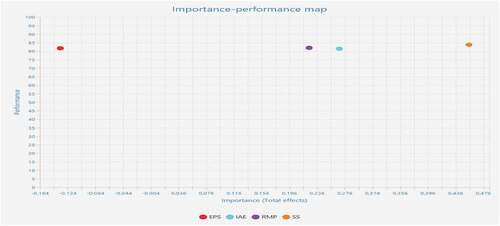

In this study, the importance-performance map (IPM) is used to evaluate the most crucial WCM activities that could improve SA. The IPM for risk management process (RMP), sustainability sensitivity (SS), internal audit effectiveness (IAE) and Enactments, policies, standards, systems and procedures (EPS) is given in Figure . It demonstrates explicitly how crucial each IAF approach included in this study is to the sustainability audits (SA) of manufacturing companies in Accra Metropolis.

Figure 2. Importance-performance map.

The importance performance map (IPM) of the exogenous factors employed in this investigation is shown in Figure . Comparatively, the IPM aids in determining the most significant IAF approach that contribute to sustainability audits. Figure reveals that SS is the most important IAF that has a crucial impact on sustainability audits (SA). This is not surprising because the more manufacturing firms ensure sustainability in their internal audit functions the more they become sustainable in their audits. The impact of IAF on SA is next followed by RMP, EPS, and finally IAE. Therefore, as SS has the greatest influence on FP, policy actions that affect IAF practices of manufacturing enterprises should give it a lot of weight. In this way, even if IAF techniques used by manufacturing companies in Accra Metropolis should not be considered equally, they should be observed and steps should be taken in priority order to improve SA.

Table demonstrates the total effects (direct) on SA. It can be seen from Table that the determinants of SA have a direct impact to a degree above 80%. Improvement in these factors would have serious repercussions on the SA of manufacturing firms. However, the most impact on SA is sustainability sensitivity. This is followed by IAE and RMP. Enactments, policies, standards, systems and procedures construct has the least relationship with sustainability audit. It is important that sustainability sensitivity in manufacturing firms is improved whereas enactments, policies, standards, systems and procedures are reviewed from time to time.

Table 8. Importance-performance values

6. Discussion

6.1. There is a significant influence of risk management process on sustainability audits

It was revealed from the first research hypothesis that RMP has a significant and positive influence on SA. It suggests that the null hypothesis of no significant influence of RMP on SA is rejected. Accordingly, risk management practices are needed to enhance sustainability audits among manufacturing firms at Accra Metropolis. For this reason, it can be concluded that consideration of fraud and corruption as key risks that need to be managed, presence of internal auditors and review of institution’s operations, constant evaluation of risks, good governance, presence and review of organisation’s governance, continuous evaluations of an entity’s governance process, and strengthened risk management and governance process are necessary in enhancing sustainability audits.

In this manner, owners’ interest as well as the interest of all other stakeholders would be met respectively in line with the agency and stakeholder theories where proper risk management contributes to sustainability audits. The IAF involvement, according to the respondents, helps with risk management because the costs of false reporting might be considerable (Trotman & Trotman, Citation2015). These expenses include fines for the CEO and the board as well as harm to the organization’s reputation for transparent reporting. Additionally, expert advice emphasises the significance of ensuring sustainability reporting, particularly the role of the IAF. This agrees with the outcome by DeSimone et al. (Citation2021) who found risk management pertinent in enhancing sustainability audits in Africa, and Asia and Oceania. The finding by Pérez-Cornejo et al. (Citation2019) is no exception, indicating that risk management is relevant for corporate reputation in Spanish firms.

6.2. There is a significant effect of sustainability sensitivity on sustainability audits

Moreover, the second research hypothesis revealed that SS has a significant positive effect on SA. Hence, the null hypothesis of no significant influence of SS on SA is rejected. This indicates that there is a significant positive effect of SS on SA. It can then be concluded that SS is relevant in enhancing SA of manufacturing firms in Accra Metropolis. Hence, factors such as making decisions based on the basis of sustainable development, using stricter laws and regulations to protect the environment, and resolving conflicts peacefully through discussion for sustainability development are needed for sustainability audits. This outcome is not surprising because environmental issues are considered relevant in terms of IAFs (Soh & Martinov Bennie, Citation2015). This partly agrees with the study by DeSimone et al. (Citation2021) who revealed a significant influence of sustainability sensitivity on sustainability audits in listed companies and not-for-profit making firms, but insignificant for unlisted companies in the organisation type analyses. DeSimone et al. (Citation2021) continental-level analysis found that sustainability sensitivity had an insignificant influence on sustainability audits in Africa, Europe, and Latin America, but a significant influence in Asia and Oceania, as well as North America. However, the present study contradicts this finding by demonstrating that manufacturing firms in Accra are required to prioritize environmental friendliness to enhance sustainability audits, as noted by Samagaio and Diogo (Citation2022).

6.2.1. There is a significant influence of internal audit effectiveness on sustainability audits

Also, from the third research hypothesis, it was found that IAE has a significant positive effect on SA. In this regard, the null hypothesis of no significant influence of IAE on SA is rejected. This means that there is a significant positive effect of SS on SA. It can then be said that IAE promotes SA of manufacturing firms in Accra Metropolis. It can be concluded that improvement in organizational operations, the creation of added value to the organization, reduction in incidences of fraud, accomplishment of objectives, determination of the adequacy and effectiveness of the firm’s internal control systems, reviews compliance with procedures, policies and plans as well as regulations of the service and reviews the service’s compliance with laws and regulations are needed for sustainability audits. This is in support of both the agency and stakeholder theories. The significant influence of IAE on sustainability agrees with the outcomes by Angmor and Diaboh (Citation2022), A. M. Karikari et al. (Citation2022), A. Karikari et al. (Citation2023) and Ziniyel et al. (Citation2018) conducted in Ghana but less consistent with the outcome by Mulyani et al. (Citation2019) performed in Indonesia.

6.3. There is a significant influence of enactments, policies, standards, systems and procedures on sustainability audits

To end with, the study revealed an insignificant effect of EPS on SA. It can be said that, the null hypothesis of no significant influence of IAE on SA is not rejected. This means that enactments, policies, standards, systems and procedures are weak enhancers of SA. It can then be concluded that EPS is not relevant in enhancing SA of manufacturing firms in Accra Metropolis. Hence, it can be concluded that factors such as presence and constant evaluations of an entity’s operations to help in the detection of acts of non-compliance are not relevant for sustainability audits.

Moreover, the detection of fraud through gross non-compliances of public finance officers, enforcement of statutory regulations, gives them the exposures to mitigate both the incidence of fraud and corruption risks, and constant evaluations of statutory guidelines for compliance gives them the exposures to identify the areas of fraud risks are not needed in promoting sustainability audits. Also, in the Upper West Region of Ghana Owusu-Ansah (Citation2017) revealed that most individuals disregard auditing enactments, standards, systems and procedures in hospitals. This violates the agency theory and stakeholder theory where managers are required to meet the interest of owners and other stakeholders respectively. A qualitative study in Tunisian public sector by Khelil and Khlif (Citation2021) found that one main barrier to internal auditors performing their position as assurance providers is the lack of legal protection, standards and procedures for them. The outcome obtained in this current study is less consistent with that of Simoni et al. (Citation2020) who revealed a significant positive relationship between policies and enactments and sustainability assurance reports.

7. Summary, conclusion, recommendations and suggestions for further studies

The study investigated the effect of IAF on SA of manufacturing firms at Accra Metropolis. Particularly, the study seeks to assess the effect of RMP, SS, IAE and EPS on SA of manufacturing firms at Accra Metropolis. The explanatory research design and quantitative research approach were applied to achieve the study’s objective. A sample of 1340 managers of manufacturing firms were invited to complete a standardised questionnaire based on extensive evaluations of prior empirical investigations. The PLS-SEM was used to estimate the study’s questions. It was appropriate to use a non-parametric approach, the PLS-SEM, after learning that the data distribution may have significantly deviated from normality.

7.1. Summary of findings

It was found from the first research hypothesis on the influence of RMP on SA that there is a positive and significant effect. It suggests that the null hypothesis of no significant influence of RMP on SA is rejected. Accordingly, risk management practices are needed to enhance sustainability audits among manufacturing firms at Accra Metropolis. Moreover, the second research hypothesis revealed that SS has a significant positive effect on SA. Hence, the null hypothesis of no significant influence of SS on SA is rejected. This indicates that there is a significant positive effect of SS on SA. It can then be concluded that SS is relevant in enhancing SA of manufacturing firms in Accra Metropolis. Also, from the third research hypothesis it was found that IAE has a significant positive effect on SA. In this regard, the null hypothesis of no significant influence of IAE on SA is rejected. This means that there is a significant positive effect of SS on SA. It can then be concluded that IAE promotes SA of manufacturing firms in Accra Metropolis. To end with, the study revealed an insignificant effect of EPS on SA. It can be said that, the null hypothesis of no significant influence of IAE on SA is not rejected. This means that enactments, policies, standards, systems and procedures are weak enhancers of SA. It can then be concluded that EPS is not relevant in enhancing SA of manufacturing firms in Accra Metropolis.

7.2. Conclusion

The study concludes from the first research hypothesis that consideration of fraud and corruption as key risks that need to be managed, presence of internal auditors and review of institution’s operations, constant evaluation of risks, good governance, presence and review of organisation’s governance, continuous evaluations of an entity’s governance process, and strengthened risk management and governance process are necessary in enhancing sustainability audits. It can be concluded from the second research hypothesis that factors such as making decisions based on the basis of sustainable development, using stricter laws and regulations to protect the environment, resolving conflicts peacefully through discussion for sustainability development are needed for sustainability audits.

Additionally, it can be concluded from the third hypothesis that improvement in organizational operations, the creation of added value to the organization, reduction in incidences of fraud, accomplishment of objectives, determination of the adequacy and effectiveness of the firm’s internal control systems, reviews compliance with procedures, policies and plans as well as regulations of the service and reviews the service’s compliance with laws and regulations are needed for sustainability audits. From the fourth hypothesis, the study however concludes that factors such as presence and constant evaluations of an entity’s operations to help in the detection of acts of non-compliance, detection of fraud through gross non-compliances of public finance officers, enforcement of statutory regulations, gives them the exposures to mitigate both the incidence of fraud and corruption risks, and constant evaluations of statutory guidelines for compliance gives them the exposures to identify the areas of fraud risks do not promote sustainability audits.

7.3. Recommendations

The study recommends from the first research hypothesis that managers of internal audit units of manufacturing firms should control the level of fraud, corruption, review the institution’s operations, incessant evaluation of risks, and effective governance in mitigating corruption. Also, from the second research hypothesis, it is recommended that preserving the nature of sustainability development and other environmental sensitivity should be the hallmark of managers such as internal auditors, operations, accountants and finance managers to ensure value for money.

Furthermore, effectiveness of internal audit processes should not be underestimated since it contributes to sustainability audits. Managers of manufacturing firms including internal auditors and the audit committee should ensure regular improvement of the organisations’ operations to create and add value, review compliance and ensure interdependence in the audit process to warrant continuous improvement of sustainability audits. From the fourth research hypothesis, the study recommends that there is the need for the creation of an audit department, the hiring of a permanent internal auditor, the provision of suitable logistics, the training of personnel on the value of internal audit, and the use of internal auditing standards and principles in the report-writing process for an enhanced sustainability audit.

7.4. Suggestions for further studies

Due to geographic disparities and the fact that the study was limited to SMEs in the Accra Metropolis, extrapolating its findings to the other 15 regions may be deceptive. Further research in this area can broaden the study’s scope to include additional regions, strengthening the generalization. Future research should additionally examine the relationship utilising performance measures such as financial, environmental accountability, etc. The use of an interview guide for a qualitative discussion of RMP, SS, IAE, EPS and SA were ignored in this study. Therefore, it is advised that future research consider a mixed-methods approach to ensure objectivity and dependability in evaluating the circumstances. The estimation technique used in this study was the Partial Least Squares Structural Equation Model (PLS-SEM). However, PLS-SEM is restricted to non-covariance-based correlation analysis. The relationship between the internal audit function and sustainability audits is still being researched.

Data availability statement

Data is available upon request

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Adam, N. S., & Kissi, E. (2021). Assessing the effects of Public Procurement on Prudent Public Financial Management in Ghana ( Doctoral dissertation).

- Alsayegh, M. F., Abdul Rahman, R., & Homayoun, S. (2020). Corporate economic, environmental, and social sustainability performance transformation through ESG disclosure. Sustainability, 12(9), 3910. https://doi.org/10.3390/su12093910

- Angmor, P. L., & Diaboh, M. B. (2022). Exploring the Effect of Internal Auditors’ Function on Financial Performance of Universal Banks in Ghana. ADRRI Journal (Multidisciplinary), 31(2 (8), April, 2022–June), 12–21.

- Balaras, C. A., Droutsa, K. G., Dascalaki, E. G., Kontoyiannidis, S., Moro, A., & Bazzan, E. (2019). Urban sustainability audits and ratings of the built environment. Energies, 12(22), 4243. https://doi.org/10.3390/en12224243

- Belur, J., Tompson, L., Thornton, A., & Simon, M. (2021). Interrater reliability in systematic review methodology: Exploring variation in coder decision-making. Sociological Methods & Research, 50(2), 837–865. https://doi.org/10.1177/0049124118799372

- Boiral, O., Heras-Saizarbitoria, I., Brotherton, M. C., & Bernard, J. (2019). Ethical issues in the assurance of sustainability reports: Perspectives from assurance providers. Journal of Business Ethics, 159(4), 1111–1125. https://doi.org/10.1007/s10551-018-3840-3

- Braam, G., & Peeters, R. (2018). Corporate sustainability performance and assurance on sustainability reports: Diffusion of accounting practices in the realm of sustainable development. Corporate Social Responsibility and Environmental Management, 25(2), 164–181. https://doi.org/10.1002/csr.1447

- Brunelli, S., & DiCarlo, E. (2020). Accountability, ethics and sustainability of organizations. Accounting, Finance, Sustainability, Governance and Fraud: Theory and Application, 4, 82–123. https://doi.org/10.1007/978-3-030-31193-3

- Clarkson, P., Li, Y., Richardson, G., & Tsang, A. (2019). Causes and consequences of voluntary assurance of CSR reports: International evidence involving Dow Jones Sustainability Index Inclusion and Firm Valuation. Accounting, Auditing & Accountability Journal, 32(8), 2451–2474. https://doi.org/10.1108/AAAJ-03-2018-3424

- Cohen, J. R., & Simnett, R. (2015). CSR and assurance services: A research agenda. Auditing: A Journal of Practice & Theory, 34(1), 59–74. https://doi.org/10.2308/ajpt-50876

- Corazza, L., Truant, E., Scagnelli, S. D., & Mio, C. (2020). Sustainability reporting after the Costa Concordia disaster: A multi-theory study on legitimacy, impression management and image restoration. Accounting, Auditing & Accountability Journal, 33(8), 1909–1941. https://doi.org/10.1108/AAAJ-05-2018-3488

- Daily, C. M., Dalton, D. R., & Rajagopalan, N. (2003). Governance through ownership: Centuries of practice, decades of research. Academy of Management Journal, 46(2), 151–158. https://doi.org/10.2307/30040611

- DeSimone, S., D’onza, G., & Sarens, G. (2021). Correlates of internal audit function involvement in sustainability audits. Journal of Management & Governance, 25(2), 561–591. https://doi.org/10.1007/s10997-020-09511-3

- Eulerich, A. K., & Eulerich, M. (2020). What is the value of internal auditing?–a literature review on qualitative and quantitative perspectives. A Literature Review on Qualitative and Quantitative Perspectives (April 22, 2020) Maandblad Voor Accountancy En Bedrijfseconomie, 94(3/4), 83–92. https://doi.org/10.5117/mab.94.50375

- Fadzil, F. H., Haron, H., & Jantan, M. (2005). Internal auditing practices and internal control system. Managerial Auditing Journal, 20(8), 844–866

- Fama, E. F. (1980). Agency problems and the theory of the firm. The Journal of Political Economy, 88(2), 288–307. https://doi.org/10.1086/260866

- Fornell, C., & Larcker, D. F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of Marketing Research, 18(3), 382. https://doi.org/10.2307/3150980

- Freeman, R. E. (1984). Strategic management: A stakeholder approach, Pitman.

- Freeman, R. E. (2004). The stakeholder approach revisited. Zeitschrift für wirtschafts-und unternehmensethik, 5(3), 228–254. https://doi.org/10.5771/1439-880X-2004-3-228

- García‐sánchez, I. M. (2020). Drivers of the CSR report assurance quality: Credibility and consistency for stakeholder engagement. Corporate Social Responsibility and Environmental Management, 27(6), 2530–2547. https://doi.org/10.1002/csr.1974

- García‐sánchez, I. M., Hussain, N., Martínez‐ferrero, J., & Ruiz‐barbadillo, E. (2019). Impact of disclosure and assurance quality of corporate sustainability reports on access to finance. Corporate Social Responsibility and Environmental Management, 26(4), 832–848. https://doi.org/10.1002/csr.1724

- Hair, J. F., Jr., Howard, M. C., & Nitzl, C. (2020). Assessing measurement model quality in PLS-SEM using confirmatory composite analysis. Journal of Business Research, 109, 101–110. https://doi.org/10.1016/j.jbusres.2019.11.069

- Hair, J. F., Sarstedt, M., & Ringle, C. M. (2019). Rethinking some of the rethinking of partial least squares. European Journal of Marketing, 53(4), 566–584. https://doi.org/10.1108/EJM-10-2018-0665

- Hazaea, S. A., Zhu, J., Khatib, S. F., Bazhair, A. H., & Elamer, A. A. (2021). Sustainability assurance practices: A systematic review and future research agenda. Environmental Science and Pollution Research, 29(4), 1–22. https://doi.org/10.1007/s11356-021-17359-9

- Healy, P. M., & Palepu, K. G. (2001). Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31(1–3), 405–440. https://doi.org/10.1016/S0165-4101(01)00018-0

- Henseler, J., Hubona, G., & Ray, P. A. (2016). Using PLS path modeling in new technology research: Updated guidelines. Industrial Management & Data Systems, 116(1), 2–20. https://doi.org/10.1108/IMDS-09-2015-0382

- Hoffman, A. J. (2018). The next phase of business sustainability. Stanford Social Innovation Review, 16(2), 34–39. https://doi.org/10.2139/ssrn.3191035

- Hu, L. T., & Bentler, P. M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal, 6(1), 1–55. https://doi.org/10.1080/10705519909540118

- Imasiku, K., Thomas, V. M., & Ntagwirumugara, E. (2020). Unpacking ecological stress from economic activities for sustainability and resource optimization in sub-saharan Africa. Sustainability, 12(9), 3538. https://doi.org/10.3390/su12093538

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Karikari, A., Amaning, M., Tettevi, N., K, P., Frimpong Owusu, D., & Opoku Ware, E. (2023). Internal audit effectiveness as a boon to public procurement performance: A multi mediation model. Cogent Economics & Finance, 11(1), 2164968. https://doi.org/10.1080/23322039.2023.2164968

- Karikari, A. M., Tettevi, P. K., Amaning, N., Opoku Ware, E., & Kwarteng, C. (2022). Modeling the implications of internal audit effectiveness on value for money and sustainable procurement performance: An application of structural equation modeling. Cogent Business & Management, 9(1), 2102127. https://doi.org/10.1080/23311975.2022.2102127

- Khelil, I., & Khlif, H. (2021). Internal auditors’ perceptions of their role as assurance providers: A qualitative study in the Tunisian public sector. Meditari Accountancy Research.

- Kiesnere, A. L., & Baumgartner, R. J. (2019). Sustainability management in practice: Organizational change for sustainability in smaller large-sized companies in Austria. Sustainability, 11(3), 572. https://doi.org/10.3390/su11030572

- Krejcie, R. V., & Morgan, D. W. (1970). Determining sample size for research activities. Educational and Psychological Measurement, 30(3), 607–610. https://doi.org/10.1177/001316447003000308

- Kurzhals, K. (2021). Quantitative Research: Questionnaire Design and Data Collection. In Recombination in Firms from a Dynamic Capability Perspective (pp. 177–207). Springer Gabler, Wiesbaden. https://doi.org/10.1007/978-3-658-35666-8_5

- Mantel, N. (1963). Chi-square tests with one degree of freedom; extensions of the Mantel-Haenszel procedure. Journal of the American Statistical Association, 58(303), 690–700. https://doi.org/10.1080/01621459.1963.10500879

- Marrucci, L., & Daddi, T. (2022). The contribution of the Eco‐Management and Audit Scheme to the environmental performance of manufacturing organisations. Business Strategy and the Environment, 31(4), 1347–1357. https://doi.org/10.1002/bse.2958

- Mulyani, S., Kasim, E., Yadiati, W., & Umar, H. (2019). Influence of accounting information systems and internal audit on fraudulent financial reporting. Opción: Revista de Ciencias Humanas y Sociales, 351, 323–338.

- Owusu-Ansah, R. (2017). Assessment of the Effectiveness of the Internal Audit System in Hospitals: The Case of St. Joseph Hospital in the Upper West Region of Ghana ( Doctoral dissertation).

- Perego, P., & Kolk, A. (2012). Multinationals’ accountability on sustainability: The evolution of third-party assurance of sustainability reports. Journal of Business Ethics, 110(2), 173–190. https://doi.org/10.1007/s10551-012-1420-5

- Pérez-Cornejo, C., de Quevedo-Puente, E., & Delgado-García, J. B. (2019). How to manage corporate reputation? The effect of enterprise risk management systems and audit committees on corporate reputation. European Management Journal, 37(4), 505–515. https://doi.org/10.1016/j.emj.2019.01.005

- Perrow, C. (1986). Complex organizations. a critical essay (3rd ed.). Glcnview.

- Plant, K., Barac, K., & Sarens, G. (2019). Preparing work-ready graduates–skills development lessons learnt from internal audit practice. Journal of Accounting Education, 48, 33–47. https://doi.org/10.1016/j.jaccedu.2019.06.001

- Ridley, J., D’silva, K., Szombathelyi, M., & Lenssen, G. (2011). Sustainability assurance and internal auditing in emerging markets. Corporate Governance the International Journal of Business in Society, 11(4), 475–488. https://doi.org/10.1108/14720701111159299

- Samagaio, A., & Diogo, T. A. (2022). Effect of Computer Assisted Audit Tools on Corporate Sustainability. Sustainability, 14(2), 705. https://doi.org/10.3390/su14020705

- Saunders, M., Lewis, P., & Thornhill, A. (2009). Research methods for business students. Pearson education.

- Saunders, M. N., Lewis, P., Thornhill, A., & Bristow, A. (2015). Understanding research philosophy and approaches to theory development.

- Seyram, H. K. (2017). The concept of value for money as applied in public procurement in Ghana. The case of Ho Municipal Assembly ( Doctoral dissertation).

- Shonhadji, N., & Maulidi, A. (2022). Is it suitable for your local governments? A contingency theory-based analysis on the use of internal control in thwarting white-collar crime. Journal of Financial Crime, 29(2), 770–786. https://doi.org/10.1108/JFC-10-2019-0128

- Simoni, L., Bini, L., & Bellucci, M. (2020). Effects of social, environmental, and institutional factors on sustainability report assurance: Evidence from European countries. Meditari Accountancy Research, 28(6), 1059–1087. https://doi.org/10.1108/MEDAR-03-2019-0462

- Simpson, S. N. Y., Aboagye-Otchere, F., & Lovi, R. (2016). Internal auditing and assurance of corporate social responsibility reports and disclosures: Perspectives of some internal auditors in Ghana. Social Responsibility Journal, 12(4), 706–718. https://doi.org/10.1108/SRJ-09-2015-0134

- Soh, D. S., & Martinov‐bennie, N. (2018). Factors associated with internal audit’s involvement in environmental and social assurance and consulting. International Journal of Auditing, 22(3), 404–421. https://doi.org/10.1111/ijau.12125

- Soh, D. S., & Martinov Bennie, N. (2015). Internal auditors’ perceptions of their role in environmental, social and governance assurance and consulting. Managerial Auditing Journal, 30(1), 80–111. https://doi.org/10.1108/MAJ-08-2014-1075

- Swann, W. L., & Deslatte, A. (2019). What do we know about urban sustainability? A research synthesis and nonparametric assessment. Urban Studies, 56(9), 1729–1747. https://doi.org/10.1177/0042098018779713

- Tarjo, T., Vidyantha, H. V., Anggono, A., Yuliana, R., & Musyarofah, S. (2022). The effect of enterprise risk management on prevention and detection fraud in Indonesia’s local government. Cogent Economics & Finance, 10(1), 2101222. https://doi.org/10.1080/23322039.2022.2101222

- Thabit, T. H., Aldabbagh, L. M., & Ibrahim, L. K. (2019). The auditing of sustainable development practices in developing countries: Case of Iraq. Revista AUS, 26(3), 12–19.

- Trotman, A. J., & Trotman, K. T. (2015). Internal audit’s role in GHG emissions and energy reporting: Evidence from audit committees, senior accountants, and internal auditors. Auditing: A Journal of Practice & Theory, 34(1), 199–230. https://doi.org/10.2308/ajpt-50675

- Vieira, A. P., & Radonjič, G. (2020). Disclosure of eco‐innovation activities in European large companies’ sustainability reporting. Corporate Social Responsibility and Environmental Management, 27(5), 2240–2253. https://doi.org/10.1002/csr.1961

- Watson, A., Shrives, P., & Marston, C. (2002). Voluntary disclosure of accounting ratios in the UK. The British Accounting Review, 34(4), 289–313. https://doi.org/10.1006/bare.2002.0213

- Weakley, J., Morrison, M., García-Ramos, A., Johnston, R., James, L., & Cole, M. H. (2021). The validity and reliability of commercially available resistance training monitoring devices: A systematic review. Sports Medicine, 51(3), 443–502. https://doi.org/10.1007/s40279-020-01382-w

- Ziniyel, D., Otoo, I. C., & Andzie, T. A. (2018). Effect of internal audit practices on financial management. European Journal of Business, Economics and Accountancy, 6(3), 39–48.