Abstract

State-Owned Enterprises (SOEs) are companies whose majority shares are owned by the government. The prime focus of this paper, determine the impact of intellectual capital in State-Owned Enterprises (SOEs) on firm performance using the value chain as a mediating variable. This research methodology begins with selecting of respondents; respondents in this study were 207 general managers and directors from 69 Indonesian State-Owned Enterprises. The data used in this study’s analysis came from questionnaires filled out by respondents. Structural Equation Modelling is a tool for data analysis. The study’s key findings are statistical tests that show intellectual capital directly impact the value chain and firm performance. Research contribution to raise awareness of intellectual capital, relationships, and the value chain among stakeholders in state-owned enterprises. This finding indicates that SOEs have improved the value chain and firm performance through useful resource management. Furthermore, through mandatory company regulations, this study contributes formulating company policies, particularly internal performance regulations.

JEL classification:

PUBLIC INTEREST STATEMENT

The company always strives to maintain sustainability. To do so, the company must be able to improve the achievement of financial and non-financial performance. One of the efforts is to manage intellectual capital that can improve sound practices of the value chain at each phase of business processes. Any primary and supporting activities that provide non value added must be identifiable and eliminated when dealing with suppliers, processing products internally and retaining customers. Therefore, not only efficiency can be improved but also the quality of the products which in turns improve gaining overall firm’s performance. The findings from the study of 276 general managers as respondents at 69 SOEs in Indonesia, it shows that by improving intellectual capital capability, they are capable to provide a better value chain and finally improve firm’s performance. Thus, creative and innovative intellectual capital contributes to the performance of the company.

1. Introduction

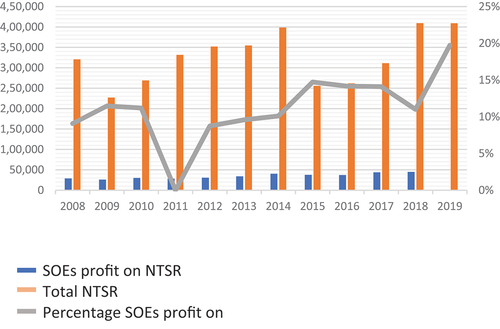

Firm performance is important in increasing competition. Companies are always required to be able to implement strategies to win the competition and make good use of all available resources to achieve goals. Performance measurement is needed to determine the company’s long-term goals (Al-Homaidi et al., Citation2018). Current business conditions have made performance not only measured from a financial perspective but also from non-financial aspects, both in private and public companies such as state-owned enterprises (SOE) (Hapsari et al., Citation2021; Hashom et al., Citation2020). State-Owned Enterprises are companies that stand on two sides; as government business entities that assist the movement of the country’s economy and as public service providers (Shin et al., Citation2017; Subbarayan & Jothikumar, Citation2017). On the other hand, government business entities must also generate profits, part of which is donated as Non-Tax State Revenue (in Indonesia known as PNBP). In Indonesia, the contribution of SOEs to the state in the form of dividends is expected to reach 30%, but in reality, it has yet to be achieved because there are still SOEs that suffer losses. The contribution of SOEs to the government can be seen from the amount of SOE profits that have flowed into Non-Tax State Revenue, as illustrated in Figure

Figure 1. SOEs Profit Contribution to Non-Tax State Revenue (NTSR).

Figure shows that the percentage of SOEs’ profit contribution to the government is in the range of 9% − 20%. This result still needs to meet the expectations of the SOE minister, which is 30%. The performance of SOEs is of public concern because as companies with full government support, they are expected to provide large profits (Rastogi, Citation2002; Vurro et al., Citation2014).

It can be seen from the fact that companies consider more than just financial performance (Al-Homaidi et al., Citation2020; Subbarayan & Jothikumar, Citation2017). For the company’s success in market competition, other factors must support financial performance. Companies must focus on their resources, internal business processes, and customer retention (Hapsari et al., Citation2021; Hashom et al., Citation2020). The balanced scorecard reflects all of these necessary aspects, bringing them together into an inseparable set of perspectives (Subbarayan & Jothikumar, Citation2017). All of these perspectives are performance indicators that complement one another. Human resources, specifically employees, are internal factors that influence firm performance (Shin et al., Citation2017; Sundram et al., Citation2020). Each employee in each division has a significant role implementing business processes. Cooperation between divisions will add value to the company’s ability to compete (Foster et al., Citation2022; Orji et al., Citation2022). To support all business process activities, a company requires human resource management. Employee knowledge assets are used to begin the management process. Intellectual capital is one approach to assessing and measuring knowledge assets (Islam & Polonsky, Citation2020; Nyamah et al., Citation2022). Human capital, structural capital, and customer capital are the three types of intellectual capital (Al-Homaidi et al., Citation2020; Islam & Polonsky, Citation2020). Intellectual capital is a one-of-a-kind resource that can give a business an advantage by improving performance and creating value (Rastogi, Citation2002; Vurro et al., Citation2014). According to Nyamah et al. (Citation2022).‘s research, intellectual has a significant impact if it is associated with the overall performance of the company.

A company’s performance chain is strongly supported by the value chain, which consists of two activities: primary activities and supporting activities (Islam & Polonsky, Citation2020; Vurro et al., Citation2014). Each activity has sub-activities that must add value to the company’s overall performance (Saputra et al., Citation2022). Implementing the value chain can improve firm performance, especially for those who have implemented the balanced scorecard (Saputra et al., Citation2022). This is demonstrated by Dana et al. (Citation2021).‘s research, which clarifies that all actors involved in every company activity must take an active role through restoring the performance of a firm.

Despite the fact that the definition and conceptualization of intellectual capital differ slightly, the study was initiated to investigate the intersection of the scope of intellectual capital (Foster et al., Citation2022). According to Ge and Xu (Citation2021), as well as Saeidi et al. (Citation2021), managerial skills and leadership style are critical elements in improving company performance, while structural capital is split into two components: infrastructure assets and intellectual property. Regarding infrastructure assets, Kweh et al. (Citation2019) also incorporate technologies and processes that help companies improve performance. Shah et al. (Citation2021) added the importance of culture and value chain, while Stewart included trademarks, patents and value chain. Ali et al. (Citation2020) argued that intellectual property is a “protected asset” with a legal definition and is another component of intellectual capital that improves company performance. The four researchers all agree that intellectual capital and the value chain are important determinants of company performance (Dana et al., Citation2021; Foster et al., Citation2022).

According to Wang et al. (Citation2021), intellectual capital impacts on company performance. Hejazi et al. (Citation2016) found that, among other things, intellectual capital and organizational culture impact on company performance. However, Surjandari and Minanari (Citation2019) found that intellectual capital has no direct relationship to company performance. Other factors, according to the researchers, may need to be considered. Individual or employee intellectual capital is integrated with the value chain in the organizational concept to improve company performance (Mohapatra et al., Citation2019). As a consequence, the value chain is hypothesized to act as a mediator among intellectual capital as well as organization performance (Kweh et al., Citation2019; Shah et al., Citation2021). As a result, it is hypothesized in this study that the value chain mediates the relationship between intellectual capital and company performance (Kweh et al., Citation2019; Shah et al., Citation2021). The statement already supports the findings from Islam and Polonsky (Citation2020); Kweh et al. (Citation2019); and Vurro et al. (Citation2014).

This research is based on the theory of interdependence, which states that there are reciprocal relationships between individuals who influence each other (Balliet et al., Citation2017). A relationship or relationship will exist if each individual can accurately predict the kinds of actions that other parties will take against him (Grizzard et al., Citation2020; Lee et al., Citation2015). Employee relationships, employee relationships with the program, employee relationships with leaders, and employee relationships with company value all have an impact on organizational performance (Astington, Citation2020; Johnson & Johnson, Citation2005). In this study, the ability level of employees with high intellectual capital will influence high-performance improvements. However, based on this theory, individual abilities are also determined by the value chain to be able to achieve company goals. Therefore, researchers link intellectual capital, value chain, and company performance (Grizzard et al., Citation2020; Lee et al., Citation2015).

A value chain can be implemented in a company if it is supported by human assets that consist of intellectual capital. Intellectual capital is a company’s knowledge and information resources capable of increasing competitiveness to improve performance (Almaqtari et al., Citation2019; Rahman et al., Citation2020; Xu & Liu, Citation2020). To sustain and remain competitive, state-owned enterprises must rely on having an integrated strategy but also ensure that they can provide competence employees and manage resources more efficiently and effectively (Hejazi et al., Citation2016; Wang et al., Citation2021). This research contributes to maintaining the existence of state-owned enterprises in terms of people’s purchasing power by providing employment and playing a role in ensuring public services, as well as being maintained during times of crisis or environmental uncertainty.

Having well managed, the companies can enable them to compete with their competitors. There is well-established empirical evidence for an association between Intellectual Capital, Value Chain, and performance. Research conducted by Buallay (Citation2017) found that integrating all human resources will support the value chain and impact business performance. Therefore, the results of this research back up the hypothesis that the availability of high-capability human resources is related to providing value-added within the value chain and better SOE performance in Indonesia. (Pucci et al., Citation2015; Surjandari & Minanari, Citation2019).

This study makes observations regarding to intellectual capital also the value chain and firm performance using the balanced scorecard concept in non-financial state-owned enterprises. Having considered the above discussions, the research objectives are formulated as follows:

To determine the effect of Intellectual Capital on Firm Performance.

To determine the value chain’s role in mediating the relationship between intellectual capital and firm performance.

2. Literature review and hypotheses

2.1. Theory of interdependence

Interdependence places great emphasis on social life which is contained in cooperative or cooperative social relations (Johnson & Johnson, Citation2005). Cooperation is a form of social interaction that includes collaborative efforts between parties or people who want to achieve company goals (Balliet et al., Citation2017; Rusbult & Van Lange, Citation2008). Interdependence is a relationship of interdependence in which each person lacks in social relations that are cooperative or cooperative to achieve common goals and one way to conceptualize this interaction is the outcome given and received by other people (Grizzard et al., Citation2020; Lee et al., Citation2015). Ultimately impact on the company’s overall achievement (Balliet et al., Citation2017). According to interdependence theory, relationship satisfaction is influenced by the level of comparison (Astington, Citation2020). Someone will be satisfied if a relationship is in accordance with their expectations and needs, for this reason the company must align the relationship between employees and company goals (Rusbult & Van Lange, Citation2008). In this context, companies need to pay attention to employee intellectuality in order to improve performance, and integrate it with the value chain (Astington, Citation2020; Balliet et al., Citation2017).

2.2. Firm performance

Kaplan & Norton (Citation2012) defined The Balanced Scorecard as a supplement to financial measures of previous performance are combined with indicators of future performance drivers. The Scorecard’s objectives and measures are generated from a business’s vision and strategy. The objectives and measures look at performance management from four directions: financial, customer, internal business processes, also learning and growth.

Horngren et al. (2021:538) stated that the Balanced Scorecard refers the organization’s mission and strategy into a set of performance indicators that serve as a framework for strategy implementation. The balanced scorecard does not focus on achieving financial goals alone. It also emphasizes the non-financial objectives that the organization must achieve in order to meet the financial objectives. The scorecard assesses organizational performance in four areas: finances, customers, internal business processes, and learning and growth.

As identified and improved by the opinion of experts, the measurement of the balanced scorecard involves 4 (four) perspectives which are the dimensions of the research. Those are financial perspective, customer perspective, internal business perspective, and learning and growth perspective.

As the first perspective, financial perspective is related to the process of revenues and expenditures within the company, or the company’s ability to manage financial to maintain stability. Financial performance usually is measured by using several ratios as profitability, Return On Assets and Return on Equity ratio. The basis for measuring profitability is the SOE’s should be comply according to the Decree of the Minister of State-Owned Enterprises Number: KEP-100/MBU/2002, rules and guidelines for measuring the level of SOE’s financial capability.

The second perspective is concern with customer loyalty. The needs of the customer products or services should be addressed including the functionality, quality, timeliness and economics (cost reduction and competitive price). Furthermore, the company must develop, retain and improve its relationship both with prospective and existing customers in exchange for price or cost. Satisfied customer will provide convincing tangible and intangible reason of purchasing certain product or service. Intangible factors that can attract potential customer such as reputation or image. Thus, in order to retain customer loyalty, the company should always concern and require in providing a better product or services (value added). The dimensions that can be used in the customer perspective are how the company serves customers and how the company communicates with customers.

The internal business perspective is an assessment of the size and synergy of each work unit. Managers are required to observe the company’s internal conditions to ensure that activities have been running according to the stipulated provisions. The dimensions of the internal business process perspective have 2 measurements, namely the stage of the company’s success rate in innovation and development and the stage of the level of success in providing after-sales service.

The learning and growth perspective is an important stage for companies to continue to pay attention to their employees, both in terms of employee welfare and increasing employee knowledge. An increased level of employee knowledge will better enable employees to participate in achieving the three perspectives previously discussed. The measurement dimensions used in this perspective are employee capability and information system capability.

2.3. Conceptual framework and research hypothesis

2.3.1. Intellectual capital and firm performance

Khan and Ali (Citation2017) stated that intellectual capital is an intangible asset that can be used as to improve business competitiveness and financial performance. McDowell et al. (Citation2018) reveal that intellectual capital can be measured using human, structural, and relational capital. Human capital is the ability of individuals in the organization measured through competence, ability to work in a team, and attitude. Good human capital can increase structural capital as a supporting resource. Xu and Liu (Citation2020) stated that structural capital is a company’s infrastructure in the form of databases, systems, strategies, and organizational culture that can improve company performance. Shah et al. (Citation2021) explained that the dimensions of structural capital measurement are the development of ideas carried out by employees, company infrastructure, and access to the information within the company. The last intellectual capital measurement is relational capital and usually has another term namely customer capital (Ali et al., Citation2020; Vurro et al., Citation2014). Relational capital considers the company’s relationship with its stakeholders, so it must maintain its image. The relationships between the company and the customer are seen from customer loyalty and satisfaction as well as relationships with suppliers (Al-Hattami et al., Citation2022; Mohapatra et al., Citation2019). Dimensions for measuring relational capital involve external relations and company image (Al-Hattami & Kabra, Citation2022; McDowell et al., Citation2018).

As the global economy has evolved, intellectual capital has become the primary asset of a company to sustain its operations (Almaqtari et al., Citation2022; Lee et al., Citation2015). The balanced scorecard is a framework and methodology for corporate strategy measuring performance that focuses on developing and monitoring strategy through a series of performance measures. (Cescon et al., Citation2016). According to Pucci et al. (Citation2015), the learning and growth perspective is fully support by the improvement of human resource competencies that are desperately needed. A human resource’s ability to work optimally is enhanced by extensive knowledge and experience (Almaqtari et al., Citation2022; Xu & Liu, Citation2020). Furthermore, as the economic growth has evolved, intellectual capital has become the most valuable asset for a company’s long-term viability (Almaqtari et al., Citation2019; Astington, Citation2020). Mohapatra et al. (Citation2019) pointed out that intellectual capital as an intangible resource is important for improving firm performance. This study suggests that intellectual capital be implemented to increase the company’s competitiveness (competitive advantage) (Al‐homaidi et al., Citation2019; Rahman et al., Citation2020). Definitions and previous studies explain that intellectual capital as measured by human capital, structural capital and relational capital affect firm performance based on the balanced scorecard (Al-Hattami et al., Citation2022; Khan & Ali, Citation2017; Xu & Liu, Citation2020).

H1:

intellectual capital has a positive effect on firm performance

2.3.2. Intellectual capital and value chain

The value chain defines the interconnected set of value-creating functions that businesses require in order to provide customers with their goods or services (Astington, Citation2020; McDowell et al., Citation2018). The value chain concept starts with suppliers providing basic raw materials, then moves them to a set of value-added activities in the production department, marketing products or services, and finally distributing goods or services to consumers as end users.Generally, it is split into two activities; primary activities and supporting activities (Al-Hattami & Kabra, Citation2022; Al‐homaidi et al., Citation2019; Buallay, Citation2017; Surjandari & Minanari, Citation2019). Each activity is divided into sub activities. Primary activities are the company’s main activities that must be carried out, including inbound logistics, operations, outbound logistics, marketing, sales, and services. Supporting activities support the main activities. Supporting activities involve procurement, research-technology and system development, human resource management, and firm infrastructure (Al-Hattami et al., Citation2022; Al‐homaidi et al., Citation2019; Astington, Citation2020).

Surjandari and Minanari (Citation2019) through their research that intellectual, as measured by human capital, structural capital, and relational capital can integrate value chains that are beneficial for the institution to the ministry level in decision making. According to the findings of this study, the support of intangible resources can be a deciding factor in a value chain. To be able to take advantage of intellectual capital, companies need to understand what is meant by intellectual capital (Khan & Ali, Citation2017). Through understanding the meaning of intangible assets, companies can develop and determine strategies as well policies to evaluate and maximize the productivity of their assets so as to provide a value chain to the company (Orji et al., Citation2022; Sundram et al., Citation2020). From the results of research on intellectual capital and its impact on the value chain, it is concluded that knowledge is very important and it can serve as a business strategy to face competitors and improve the value chain (Foster et al., Citation2022; Saeidi et al., Citation2021; Shin et al., Citation2017).

Orji et al. (Citation2022) stated that every company hopes their intangible resources are sometimes different from those of other companies. Knowledge is the most important resource and the excellence of a product or service comes from knowledge (Hapsari et al., Citation2021). The can produce products or services by implementing knowledge from resources. Companies can use intellectual capital to develop resources (Nyamah et al., Citation2022). Intellectual capital is organizational learning capable of carrying out the company’s business activities to provide added value. In state-owned enterprises, human resource management is inextricably linked to the dimensions of human capital, structural capital, and relational capital (Dana et al., Citation2021; Saeidi et al., Citation2021; Vurro et al., Citation2014).

Since the recruitment process, minimum requirements have been met for a given job and level. The company has provided adequate infrastructure for employee improvement (Shin et al., Citation2017; Sundram et al., Citation2020). Employee assessment is not only taken from knowledge ability but also from attitude. Having the appropriate resources, as needed, will support all activities within the company (Almaqtari et al., Citation2019; Al‐homaidi et al., Citation2019). Good cooperation between employees can support the smooth running of business activities within the company (Astington, Citation2020; Lee et al., Citation2015). Thus, the hypothesis that follows is proposed:

H2:

intellectual capital has a positive effect on value chain

2.3.3. Value chain and firm performance

Business processes are a series of company activities that add value to each other (Al-Hattami et al., Citation2022; Almaqtari et al., Citation2022). This activity starts from the purchase of materials, storage in warehouses, production processes, placement before sales and the company conducts marketing supported by the procurement process, placement of appropriate Human Resources, equipment, and supporting information technology (Al-Hattami & Kabra, Citation2022; Almaqtari et al., Citation2019; Al‐homaidi et al., Citation2019). Furthermore, this process develops and is known as the value chain (Astington, Citation2020). The value chain concept develops by describing company activities that add value to each activity, from processing raw materials into finished materials (final products) to sending them to customers (Ali et al., Citation2020; Hejazi et al., Citation2016; Wang et al., Citation2021). The value chain is an critical factor in a company ’s survival (Islam & Polonsky, Citation2020). All primary activities can potentially boost the company’s competitive advantage (Kweh et al., Citation2019; Surjandari & Minanari, Citation2019). Saeidi et al. (Citation2021) stated that a series of well-integrated business processes could fulfill each perspective in the balanced scorecard.

H3:

value chain has a positive effect on firm performance

2.3.4. Mediating role of value chain in the relationship between intellectual capital and firm performance

The achievement of a competitive advantage is supported by the company’s value chain, which is applied in all activities beginning with the procurement of raw materials and ending with finished products ready for sale (Dana et al., Citation2021; Foster et al., Citation2022). The company’s resources, as measured by intellectual capital, are used to support the execution of the company’s activities. (Ali et al., Citation2020; Islam & Polonsky, Citation2020; Vurro et al., Citation2014). According to Islam and Polonsky (Citation2020) their research results explain that the implementing intellectual capital in Malaysia can affect firm performance based on the balanced scorecard (Al-Homaidi et al., Citation2020; Shin et al., Citation2017). If the activities follow the company’s plan, all concepts in the balanced scorecard can be used (Al-Homaidi et al., Citation2018; Hashom et al., Citation2020). Intangible assets aid in the value chain’s implementation, in this case, competent Human Resources and their capabilities, as well as company infrastructure measured using intellectual capital (Foster et al., Citation2022; Hapsari et al., Citation2021; Hashom et al., Citation2020; Orji et al., Citation2022).

H4:

Value Chain has a mediating role in the relationship between intellectual capital and firm performance

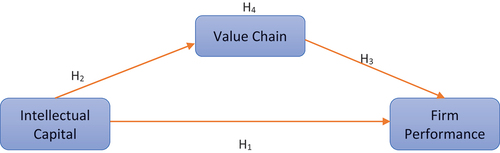

Using theories on intellectual capital, value chain and firm performance, a conceptual model can be developed by conducting studies on non-financial state-owned enterprises. Figure below is a research model that describes the correlation among intellectual capital, value chain and firm performance.

Figure 2. Research Model.

3. Research method

3.1. Collection of data

This research employs survey method. The population of this research was 76 (seventy-six) non-financial state-owned companies in Indonesia. Data from senior managers was gathered through online surveys (e.g., managing directors, general managers, and vice presidents) in the divisions of human resources, business development, and finance (Al-Homaidi et al., Citation2018). These high-level respondents were chosen because they certainly have in-depth knowledge of their organization, and they will answer all questionnaire items based on their knowledge and practice (Al-Homaidi et al., Citation2020). In about two weeks, a follow-up call was made to improve the response rate. We obtained a response of 69 (sixty-nine) companies. The completed questionnaires came from ten clusters; energy, oil and gas; mineral and coal, telecommunication, food and fertilizer, health, infrastructure, manufacture, plantation, logistic services, and tourist companies (Subbarayan & Jothikumar, Citation2017). Questionnaires that have been filled out and returned (complete three divisions) and can be processed are 69 SOEs with 207 respondents or 90 percent of the target respondents. The profile of respondents is described in terms of several characteristics (e.g., gender, age, education level, occupation). Table provides details of the respondent’ demographic characteristics.

Table 1. Demographic Profile

3.2. Statistical methodology

This study is a second-order model; we do confirmatory factor analysis (CFA) on the first- order and second-order. First-order measures validity and reliability for indicators on dimensions. The second-order measures validity and reliability for all latent variables (intellectual capital, value chain and firm performance). There are 50 items in the questionnaire divided into three sections (Al-Homaidi et al., Citation2018, Citation2020; Subbarayan & Jothikumar, Citation2017). The first part covers the construction of intellectual capital which consists of 3 (three) dimensions (human capital, structural capital and relational capital). Sixteen items measure intellectual capital, and they are adapted from previous research. Human capital uses indicators of competence, ability to work in teams, and attitudes, which are symbolized by HC1, HC2, and HC3. Structural capital uses indicators of idea development, company infrastructure and access to information within the company as symbolized by SC1, SC2, and SC3. Relational capital uses indicators of external relations and company image as symbolized by RC1 and RC2. Table shows the indicators and outcome measurement model for intellectual capital variables.

Table 2. Construct indicators and measurement model of IC

The second section covers the construct of the value chain, which entails two dimensions (primary activities and supporting activities). Eighteen items cover the value chain (Hapsari et al., Citation2021). All items are adapted from Foster et al. (Citation2022). The dimensions of primary activities use indicators of inbound logistics, operations, outbound logistics, marketing and sales, and services symbolized by PA1, PA2, PA3, PA, and PA5, respectively, symbolize—supporting activities function to support the main activities. Supporting activities involve several activities, namely procurement, research-technology and system development, human resource management and firm infrastructure denoted by SA1, SA2, SA3, and SA4, respectively. Table shows the indicators and outcome measurement model for value chain variables.

Table 3. Construct indicators and measurement model of Value Chain

The third section measures the balanced scorecard, which includes four dimensions of financial perspective, customer perspective, internal business processes, learning and objectives. There are 16 (sixteen) of these items which were adapted from Vurro et al. (Citation2014). The dimensions of financial perspectives are measured using Return on Assets (FP1) and Return on Investment (FP2). The customer perspective uses indicators of customer satisfaction service (CP1) and market share (CP2). The internal business process uses indicators of success in innovation (IBP1) and success in providing services (IBP2). Finally, the learning and growth perspective uses indicators of employee capability (LGP1) and information system capability (IBP2). Table shows the indicators and outcome measurement model for firm performance variables.

Table 4. Construct indicators and measurement model of Firm Performance

For all variables, the loading factor was greater than 0.70, average variance extracted (AVE) was greater than 0.50, and composite reliability was greater than 0.70; it fulfills the preferred rule of thumb. For instance, the intellectual capital variable has three dimensions involving: human capital (HC), structural capital (SC) and relational capital (RC). We also used Fornell Larcker to test the discriminant validity. According to this process, the AVE square root value of one construct must be greater than the inter-correlation value between constructs. A construct’s items must be more varied than those of other constructs in the model. The square root of the AVE of all constructs: intellectual capital (0.786), value chain (0.766), and firm performance (0.729) respectively is greater than the corresponding inter-correlations, as shown in Table .

Table 5. Discriminant Variable – Fornell Larcker

The data were analyzed using partial least square structural equation modeling approach (PLS-SEM) (Al-Homaidi et al., Citation2020). This study reports the measurement model and structural model (Subbarayan & Jothikumar, Citation2017). We evaluate the structural model’s suitability for representing observational data. We tested the direct effects in this step to see what the relationship was between each predictor variable and the outcome (all objectives) (Al-Homaidi et al., Citation2018, 2020). Finally, we examined the indirect effects of the value chain on the relationship between predictor variables and outcome.

4. Result and discussion

4.1. Assessment of the structural model

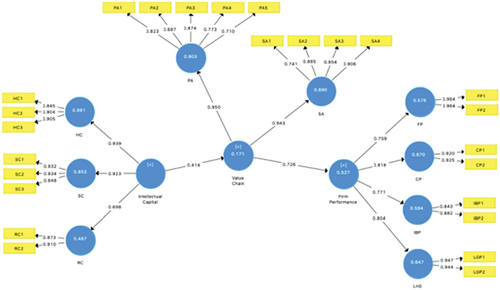

After confirming that all of the variables’ indicators are reliable and valid in the first step (see Figure below), the next step is to evaluate the structural model’s results and test the hypotheses. Structural model validation is carried out through evaluation of important criteria such as path coefficient (β), coefficient of determination for endogenous variables (R2), effect size (f2), relevance of predictions (q2). According Foster et al. (Citation2022) and Nyamah et al. (Citation2022) also emphasized by proposing that in determining the accuracy of predictions of a model if the value of R square is 0.25, 0.5 and 0.75 then respectively has low, moderate and substantial effect on endogenous variable. The threshold values and descriptions for every reference point are provided in the systematic structural model test below (see figure ).The findings in this study found that the value of R square of intellectual capital on value chain: R2 VC = 0.159.

Figure 3. Measurement Model.

The results of this test show that intellectual capital has a relatively minor impact on the value chain (weak). This study has also demonstrated the value of R square of intellectual capital and value chain on firm performance: R2 FP = 0.520. This finding suggests that intellectual capital and value chain have a moderate effect on firm performance (Shin et al., Citation2017; Vurro et al., Citation2014). The next step is to find out the effect size of the unobserved variable predictor by calculating the F square value. The results from F square test show (f2) = IC—VC = 0.206. This indicates that the effect size of intellectual capital on the value chain is moderate. The effect size of intellectual capital and value chain on firm performance are strong or quite high due to the (f2)=IC-FP = 0.623 and VC-FP = 1.115, respectively. The third step in testing the inner model (structural model) is evaluating the Q-square (Q2) predictive relevance. This predictive value is used to assess how well the model’s observation values and parameters are estimated. Results from Q2 show that Q2 predictive relevance = 0.711 and is greater than 0. Hence, the structural model has an adequate predictive relevance value.

The value of goodness of fit is generated through the standardized root mean squared residual (SRMR) and the normed fit index (NFI). Results from the standardized root mean square residual (SRMR) 0.115 lower than 1.0. Thus, it means the model has goodness of fit. Moreover, the normed fit index (NFI) is 61.2% supported by indicating marginal fit due to its value lower than 90%. (Table )

Table 6. Structural model results

4.2. Direct effect analysis

According to Subbarayan and Jothikumar (Citation2017), a bootstrap procedure is performed to predict t statistics and confidence intervals because there are no distribution assumption requirements in PLS. Table shows the path coefficient assessment results, which show that all of the proposed hypotheses are supported. The supported hypotheses are statistically significant at the 0.05 level.

Table 7. Direct Effect Analysis

4.3. Indirect effect analysis

The value chain that mediates the relationships between intellectual capital and firm performance was identified using mediation analysis (Nyamah et al., Citation2022). The statistical significance of the mediation effect was confirmed. Table shows the mediation analysis results, which show that both mediation hypotheses are statistically significant and supported.

Table 8. Indirect Effect Analysis

5. Discussion

The first hypothesis shows that intellectual capital has a significant positive effect on SOE’s performance. The results of this empirical research support the first hypothesis. Intellectual Capital is the foundation for companies to develop and have a competitive advantage (Rastogi, Citation2002; Shin et al., Citation2017). It is also a long-term capital consisting of human capital, structural capital and relational capital (Dana et al., Citation2021). Appropriate employee placement, continuous performance appraisal, and competency improvement are supported by the company’s infrastructure and good employee communication skills play an important role in advancing the learning and growth perspective (Foster et al., Citation2022; Ge & Xu, Citation2021). This initial perspective is good, so the internal business processes will run well and be able to produce the products expected by consumers (Ali et al., Citation2020; Wang et al., Citation2021). Loyal customers will certainly increase the company’s income which ultimately improves firm performance (Hejazi et al., Citation2016; Mohapatra et al., Citation2019; Surjandari & Minanari, Citation2019). This is in line with the research of Buallay (Citation2017) and Pucci et al. (Citation2015) that the test results using PLS SEM show that employee competencies supported by company infrastructure can increase firm performance.

The second hypothesis shows that intellectual capital has a significant positive effect on the value chain. Based on the results of the analysis, it can be stated that the second hypothesis is supported. Intellectual capital is recognized as one of the most important intangible assets in the current information age which represents a valuable resource and is capable of acting on knowledge (Shah et al., Citation2021; Surjandari & Minanari, Citation2019). The results of the research through respondents’ responses show that a good recruitment process is supported by the company’s infrastructure and how the company always maintains relationships with external parties to improve business processes as measured by the value chain through primary and supporting activities (Mohapatra et al., Citation2019; Pucci et al., Citation2015). Each State-Owned Enterprises (SOE) has a business process system that has been adapted to the main business, so that their needs for employees are also different (Khan & Ali, Citation2017; Xu & Liu, Citation2020). Recruiting employees in accordance with the required requirements will greatly assist all activities in each division of the company (McDowell et al., Citation2018; Pucci et al., Citation2015). The findings in this study support and prove the results of research of Wang et al. (Citation2021) stated that intellectual capital is able to produce a good management process and has a relationship with the value chain.

The third hypothesis shows that the value chain has a significant positive effect on SOE’s performance. In accordance with the results obtained, the third hypothesis is declared supported. Haque stated that the company’s main activities will run well if they are supported by supporting activities (Xu & Liu, Citation2020). These main activities include inbound logistics which is the process of procuring materials, processing materials into finished products (operations), how the company stores the finished products until they are transferred to consumers and when the company does market and sales (sales and marketing) (Khan & Ali, Citation2017; McDowell et al., Citation2018). To support all main activities, it is necessary to have equipment maintenance to keep it in good condition, procurement procedures by determining competent suppliers, availability of information technology that is able to support all activities and have employees who have the appropriate expertise (Ali et al., Citation2020; Hejazi et al., Citation2016; Wang et al., Citation2021). This business series is able to improve the company’s internal business processes (Buallay, Citation2017). The results of research related to the value chain on firm performance are in accordance with the results of research of Mohapatra et al. (Citation2019) which shows that value chain implementation is a key factor in the company’s competitive advantage as seen from the balanced scorecard. McDowell et al. (Citation2018) explained that primary activities consisting of the procurement process, workmanship, storage, and sales will improve firm performance. Shah et al. (Citation2021) corroborate the results of previous research which states that the successful implementation of corporate strategic management is supported by the value chain.

The fourth hypothesis is the mediating role of value chain on intellectual capital and SOEs performance. This result supports the fourth hypothesis. SOEs are very concerned about the minimum requirements for employees to be accepted so that during their work they will be able to improve their abilities and expertise (Hejazi et al., Citation2016; Wang et al., Citation2021). In addition, SOEs have prepared a career path, training centre or corporate university in large SOEs, healthy and competitive work rotations and appreciation for outstanding employees (Foster et al., Citation2022; Saeidi et al., Citation2021). The attitude of employees in accordance with the needs of SOEs will complement the company’s intellectual capital and will increase the perspective of learning and growth which is one of the performance measurement tools based on the balanced scorecard (Khan & Ali, Citation2017; Surjandari & Minanari, Citation2019; Wang et al., Citation2021). Xu and Liu (Citation2020) revealed that the right human resources in each division will minimize the occurrence of errors in work which also reduces the costs incurred for errors. The achievements of each division show excellent integrity which can result in added value to the product (Buallay, Citation2017; Mohapatra et al., Citation2019; Pucci et al., Citation2015). Superior products increase sales which will certainly affect the company’s revenue (Foster et al., Citation2022; Saeidi et al., Citation2021).

6. Conclusion

Intellectual Capital is long-term capital consisting of human capital, structural capital and relational capital. Human capital reflects a company’s capacity for developing the best solutions possible based on the knowledge of its employees. Human capital will increase if the company is able to use the knowledge possessed by its employees. The results show that SOEs have provided adequate facilities so that the employees are able to develop their ideas using them. SOEs always maintain a harmonious relationship (association network) with partners including reliable and quality suppliers, as well as with customers who are loyal and satisfied with the company’s services (Shah et al., Citation2021; Wang et al., Citation2021). This satisfaction is able to improve the company’s image in the community.

Intellectual capital which starts from a good recruitment process supported by infrastructure and how the company maintains good relations with external parties can improve business processes as measured by the value chain through primary and supporting activities (Foster et al., Citation2022; Mohapatra et al., Citation2019). The value chain in this study uses the Porter concept, indicating that players in every business activity must have the skills needed to carry out activities in business processes according to the company’s goals which can ultimately result in good firm performance.

The success of the value chain is supported by SOE’s success in managing intellectual capital. Talented human resources will be able to work together in every company activity to realize better productivity and firm performance. The implications of academic research, trying to enrich the study of state-owned enterprises in terms of performance and relational by increasing the value chain, through analyze the importance of intellectual capital. Socially, this research seeks to improve awareness of the importance of intellectual capital, especially state-owned companies. This research is also expected to increase stakeholder awareness.

These findings can assist SOEs directors, stakeholders, and decision makers in improving company performance. Implementing the value chain in accordance with the core business really helps management make priorities in carrying out its activities to obtain added value. The research results show that the proper value chain will improve the performance of SOEs so that they can help implement government programs.

7. Limitations and future research

The study’s limitation is that it only uses non-financial SOE to assess the extent to which non-financial companies implement intellectual capital and value chain. Although it has provided an important conceptual foundation, the findings of this study may need to provide a broad overview of the practice of intellectual capital and value chains across SOEs in Indonesia. Other researchers need to expand the scope of research by including all SOEs.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Harry Suharman

Harry Suharman Is an associate professor, Head of the Doctoral Study Program in accounting science, Padjadjaran University, Bandung, Indonesia. His major research focuses on corporate social responsibility, Management Control System, Strategic Management, Management Accounting, Accounting Information Systems.

Dini Wahjoe Hapsari

Dini Wahjoe Hapsari is a lecturer of Accounting Department, Economics and Business Faculty, Telkom University, Bandung Indonesia. Her major researches focus on corporate governance, intellectual capital, and financial reporting.

Nurul Hidayah

Nurul Hidayah is a lecturer of Magister Accounting Department, Economic and Business Faculty, Universitas Mercu Buana, Jakarta Indonesia. Her major research focus on Management Accounting, Financial Accounting and Public Sector Accounting

Rr. Sri Saraswati

Rr. Sri Saraswati is a lecturer of Accounting Department, Economics and Business Faculty, Telkom University, Bandung Indonesia. Her major researches focus on Corporate Governance, Organizational Behaviors and Management Accounting such as Lean Manufacturing.

References

- Al‐homaidi, E. A., Tabash, M. I., Farhan, N. H., & Almaqtari, F. A. (2019). The determinants of liquidity of Indian listed commercial banks: A panel data approach. Cogent Economics & Finance, 7(1), 1616521. https://doi.org/10.1080/23322039.2019.1616521

- Al-Hattami, H. M., & Kabra, J. D. (2022). The influence of accounting information system on management control effectiveness: The perspective of SMEs in Yemen. Information Development, 026666692210871. https://doi.org/10.1177/02666669221087184

- Al-Hattami, H. M., Senan, N. A. M., Al-Hakimi, M. A., & Azharuddin, S. (2022). An empirical examination of AIS success at the organizational level in the era of COVID-19 pandemic. Global Knowledge, Memory and Communication. Ahead-Of-Print. https://doi.org/10.1108/GKMC-04-2022-0094

- Al-Homaidi, E. A., Almaqtari, F. A., Yahya, A. T., & Khaled, A. S. D. (2020). Internal and external determinants of listed commercial banks’ profitability in India: Dynamic GMM approach. International Journal of Monetary Economics and Finance, 13(1), 34–18. https://doi.org/10.1504/IJMEF.2020.105333

- Al-Homaidi, E. A., Tabash, M. I., Farhan, N. H. S., & Almaqtari, F. A. (2018). Bank-specific and macro-economic determinants of profitability of Indian commercial banks: A panel data approach. Cogent Economics & Finance, 6(1), 1548072. https://doi.org/10.1080/23322039.2018.1548072

- Ali, M. A., Hussin, N., Abed, I. A., Othman, R., & Qahatan, N. (2020). Systematic review of intellectual capital and firm performance. Technology Reports of Kansai University, 62(8), 4199–4216.

- Almaqtari, F. A., Al‐homaidi, E. A., Tabash, M. I., & Farhan, N. H. (2019). The determinants of profitability of Indian commercial banks: A panel data approach. International Journal of Finance & Economics, 24(1), 168–185. https://doi.org/10.1002/ijfe.1655

- Almaqtari, F. A., Hashid, A., Farhan, N. H. S., Tabash, M. I., & Al‐ahdal, W. M. (2022). An empirical examination of the impact of country‐level corporate governance on profitability of Indian banks. International Journal of Finance & Economics, 27(2), 1912–1932. https://doi.org/10.1002/ijfe.2250

- Astington, J. W. (2020). The developmental interdependence of theory of mind and language. In Atkinson, Anthony A., Robert S. Kaplan, Ella, M. & Matsumura, S. (Eds.), Roots of human sociality (pp. 179–206). Routledge.

- Balliet, D., Tybur, J. M., & Van Lange, P. A. M. (2017). Functional interdependence theory: An evolutionary account of social situations. Personality and Social Psychology Review, 21(4), 361–388. https://doi.org/10.1177/1088868316657965

- Buallay, A. M. (2017). The relationship between intellectual capital and firm performance. Corporate Governance and Organizational Behavior Review, 1(1), 32–41. https://doi.org/10.22495/cgobr_v1_i1_p4

- Cescon, F., Costantini, A., & Grassetti, L. (2016). Strategic perspective in management accounting: Field-based evidence. Journal Management Accounting Research, 22(5), 1–25.

- Dana, L. -P., Rounaghi, M. M., Enayati, G., & Researcher, M. I. (2021). Increasing productivity and sustainability of corporate performance by using management control systems and intellectual capital accounting approach. Green Finance, 3(1), 1–14. https://doi.org/10.3934/GF.2021001

- Foster, B., Saputra, J., Johansyah, M., & Muhammad, Z. (2022). Do intellectual capital and environmental uncertainty affect firm performance? A mediating role of value chain. Uncertain Supply Chain Management, 10(3), 1055–1064. https://doi.org/10.5267/j.uscm.2022.2.006

- Ge, F., & Xu, J. (2021). Does intellectual capital investment enhance firm performance? Evidence from pharmaceutical sector in China. Technology Analysis & Strategic Management, 33(9), 1006–1021. https://doi.org/10.1080/09537325.2020.1862414

- Grizzard, M., Francemone, C. J., Fitzgerald, K., Huang, J., & Ahn, C. (2020). Interdependence of narrative characters: Implications for media theories. Journal of Communication, 70(2), 274–301. https://doi.org/10.1093/joc/jqaa005

- Hapsari, D. W., Yadiati, W., Suharman, H., & Rosdini, D. (2021). Intellectual capital and environmental uncertainty on firm performance: The mediating role of the value chain. Quality-Access to Success, 22(185), 169–175.

- Hashom, H., Ariffin, A. S., Sabar, R., & Ahmad, H. (2020). Halal-logistics value chain on firm performances: A conceptual framework. International Journal on Food, Agriculture and Natural Resources, 1(2), 8–14. https://doi.org/10.46676/ij-fanres.v1i2.10

- Hejazi, R., Ghanbari, M., & Alipour, M. (2016). Intellectual, human and structural capital effects on firm performance as measured by Tobin’s Q. Knowledge and Process Management, 23(4), 259–273. https://doi.org/10.1002/kpm.1529

- Islam, M. T., & Polonsky, M. J. (2020). Validating scales for economic upgrading in global value chains and assessing the impact of upgrading on supplier firms’ performance. Journal of Business Research, 110, 144–159. https://doi.org/10.1016/j.jbusres.2020.01.010

- Johnson, D. W., & Johnson, R. T. (2005). New developments in social interdependence theory. Genetic, Social, and General Psychology Monographs, 131(4), 285–358. https://doi.org/10.3200/MONO.131.4.285-358

- Kaplan, R. S., & Norton, D. P. (2012). Strategy & Learning and the Balanced Scorecard. Strategy & Leadership, 24(5), 18–24.

- Khan, S. N., & Ali, E. I. E. (2017). The moderating role of intellectual capital between enterprise risk management and firm performance: A conceptual review. American Journal of Social Sciences and Humanities, 2(1), 9–15. https://doi.org/10.20448/801.21.9.15

- Kweh, Q. L., Ting, I. W. K., Hanh, L. T. M., & Zhang, C. (2019). Intellectual capital, governmental presence, and firm performance of publicly listed companies in Malaysia. International Journal of Learning and Intellectual Capital, 16(2), 193–211. https://doi.org/10.1504/IJLIC.2019.098932

- Lee, S. Y., Pitesa, M., Thau, S., & Pillutla, M. M. (2015). Discrimination in selection decisions: Integrating stereotype fit and interdependence theories. Academy of Management Journal, 58(3), 789–812. https://doi.org/10.5465/amj.2013.0571

- McDowell, W. C., Peake, W. O., Coder, L., & Harris, M. L. (2018). Building small firm performance through intellectual capital development: Exploring innovation as the “black box. Journal of Business Research, 88, 321–327. https://doi.org/10.1016/j.jbusres.2018.01.025

- Mohapatra, S., Jena, S. K., Mitra, A., & Tiwari, A. K. (2019). Intellectual capital and firm performance: Evidence from Indian banking sector. Applied Economics, 51(57), 6054–6067. https://doi.org/10.1080/00036846.2019.1645283

- Nyamah, E. Y., Attatsi, P. B., Nyamah, E. Y., & Opoku, R. K. (2022). Agri-food value chain transparency and firm performance: The role of institutional quality. Production & Manufacturing Research, 10(1), 62–88. https://doi.org/10.1080/21693277.2022.2062477

- Orji, I. J., Ojadi, F., & Okwara, U. K. (2022). The nexus between e-commerce adoption in a health pandemic and firm performance: The role of pandemic response strategies. Journal of Business Research, 145, 616–635. https://doi.org/10.1016/j.jbusres.2022.03.034

- Pucci, T., Simoni, C., & Zanni, L. (2015). Measuring the relationship between marketing assets, intellectual capital and firm performance. Journal of Management & Governance, 19(3), 589–616. https://doi.org/10.1007/s10997-013-9278-1

- Rahman, H., Yousaf, M. W., & Tabassum, N. (2020). Bank-specific and macroeconomic determinants of profitability: A revisit of Pakistani banking sector under dynamic panel data approach. International Journal of Financial Studies, 8(3), 42. https://doi.org/10.3390/ijfs8030042

- Rastogi, P. N. (2002). Knowledge management and intellectual capital as a paradigm of value creation. Human Systems Management, 21(4), 229–240. https://doi.org/10.3233/HSM-2002-21402

- Rusbult, C. E., & Van Lange, P. A. M. (2008). Why we need interdependence theory. Social and Personality Psychology Compass, 2(5), 2049–2070. https://doi.org/10.1111/j.1751-9004.2008.00147.x

- Saeidi, P., Saeidi, S. P., Gutierrez, L., Streimikiene, D., Alrasheedi, M., Saeidi, S. P., & Mardani, A. (2021). The influence of enterprise risk management on firm performance with the moderating effect of intellectual capital dimensions. Economic Research-Ekonomska Istraživanja, 34(1), 122–151. https://doi.org/10.1080/1331677X.2020.1776140

- Saputra, K. A. K., Subroto, B., Rahman, A. F., & Saraswati, E. (2022). Eco-efficiency and energy audit to improve environmental performance: An empirical study of hotels in Bali-Indonesia. International Journal of Energy Economics and Policy, 12(6), 175–182. https://doi.org/10.32479/ijeep.13565

- Shah, S. Q. A., Lai, F. -W., Shad, M. K., Konečná, Z., Goni, F. A., Chofreh, A. G., & Klemeš, J. J. (2021). The inclusion of intellectual capital into the green board committee to enhance firm performance. Sustainability, 13(19), 10849. https://doi.org/10.3390/su131910849

- Shin, N., Kraemer, K. L., & Dedrick, J. (2017). R&D and firm performance in the semiconductor industry. Industry and Innovation, 24(3), 280–297. https://doi.org/10.1080/13662716.2016.1224708

- Subbarayan, A., & Jothikumar, J. (2017). Bank specific, industry specific and macro economic determinants of profitability of public sector banks in India: 2010-2016-A panel data approach. International Journal of Agricultural and Statistical Sciences, 13(2), 655–662.

- Sundram, V. P. K., Chhetri, P., & Bahrin, A. S. (2020). The consequences of information technology, information sharing and supply chain integration, towards supply chain performance and firm performance. Journal of International Logistics and Trade, 18(1), 15–31. https://doi.org/10.24006/jilt.2020.18.1.015

- Surjandari, D. A., & Minanari, M. (2019). The effect of intellectual capital, firm size and capital structure on firm performance, evidence from property companies in Indonesia. Jurnal Dinamika Akuntansi, 11(2), 108–121.

- Vurro, C., Russo, A., & Costanzo, L. A. (2014). Sustainability along the value chain: Collaborative approaches and their impact on firm performance. Symphonya Emerging Issues in Management, 2, 30–44. https://doi.org/10.4468/2014.2.04vurro.russo.costanzo

- Wang, Z., Cai, S., Liang, H., Wang, N., & Xiang, E. (2021). Intellectual capital and firm performance: The mediating role of innovation speed and quality. The International Journal of Human Resource Management, 32(6), 1222–1250. https://doi.org/10.1080/09585192.2018.1511611

- Xu, J., & Liu, F. (2020). The impact of intellectual capital on firm performance: A modified and extended VAIC model. Journal of Competitiveness, 12(1), 161. https://doi.org/10.7441/joc.2010.01.10