?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study, conducted between 2016–2021 on Southeast Asian mining companies, introduces the Modified Enterprise Risk Management (ERM) Index (MERMi) to measure the implementation of ERM based on the COSO 2017 principles. The study found that ERM implementation is influenced by industry competition, company complexity, international diversification, and financial leverage. Meanwhile, company size and complexity, along with ERM and industry competition, positively impact firm performance. However, international diversification and financial leverage do not have a significant effect on firm performance. The study also concludes that there are no significant differences between the factors influencing ERM implementation in Southeast Asia and in advanced ERM implementation countries such as the USA, Europe, and Germany. The findings emphasize the importance of integrating risk management into the corporate governance of the mining sector in Southeast Asia. The limitations of this research include the lack of precise company disclosures on ERM implementation, which could be addressed through more research in other sectors and by using ISO 31,000 as a replacement for measuring instruments.

Public Interest Statement

The initial purpose of this study was to establish an ERM assessment by developing the ERM Index. The study aims to introduce the ERM Index measurement by referring to the latest version of COSO (Citation2017) to provide a more straightforward but powerful way to measure the level of ERM application in a company. This index can be useful for companies that are not yet mature enough in their ERM implementation, such as some mining companies in Southeast Asian countries. We call this index a Modification of the ERM Index (MERMi). The second objective of this research is to examine the factors that influence ERM in Southeast Asia. The results of this study are expected to contribute to companies, especially in the mining sector, regarding the importance of implementing ERM.

1. Introduction

In recent years, enterprise risk management (ERM) has become increasingly necessary due to the growing complexity of risks, dependence on sources of risk, advanced methods of identifying and quantifying risks, technological advances, and strict regulations for companies to implement risk management. There has been a recent paradigm shift in how businesses perceive risk management holistically. Owing to the complexity of risks and the expansion of the existing legal framework, ERM has received considerable attention over the past several years (A. D. Malik, Citation2017; Chen et al., Citation2020; Lechner & Gatzert, Citation2017; Zungu et al., Citation2018). The ERM frameworks by COSO (2017) have the potential to improve firm performance (Farrell & Gallagher, Citation2015). Several companies that have implemented ERM have experienced improved firm performance and increased trust from their stakeholders (Chen et al., Citation2020; D. K. Nguyen & Vo, Citation2020; Lechner & Gatzert, Citation2017; Farrel & Gallagher, Citation2015; M. F. Malik et al., Citation2020).

Currently, the growth rate of ERM applications in developed countries is higher than in developing countries such as Southeast Asia (Ahmed & Manab, Citation2016; Horvey et al., Citation2020; Razali et al., Citation2011). This void is a result of a lack of comprehension and awareness of ERM and its impact on the operation of the firm. Therefore, this research is focused on the application of ERM in Southeast Asia, specifically in Indonesia, Malaysia, Thailand, Vietnam, and the Philippines, which are, on average, developing countries, especially in the mining sector. In some Southeast Asian countries that are rich in natural resources, the mining sector is a major concern because it is a significant contributor to the country’s national income, and small movements in this sector have a considerable impact on the growth of the country’s economy. Previous research on ERM and firm performance was mainly carried out in developed countries (Chen et al., Citation2020; D. K. Nguyen & Vo, Citation2020; Farrell & Gallagher, Citation2019; Lechner & Gatzert, Citation2017; M. F. Malik et al., Citation2020; Pagach & Warr, Citation2010), where the application of ERM is more mature. In this study, we will examine how the application of ERM works in countries whose level of ERM application is not yet mature, namely Southeast Asia.

Several previous studies have examined the relationship between ERM and performance, but the results have been inconsistent. Ahmed and Manab (Citation2016) and Joshi et al. (Citation2013) demonstrate a positive and statistically significant correlation between ERM and firm performance. In addition, M. F. Malik et al. (Citation2020) and Olve et al. (Citation2001) show that ERM may indirectly enhance the skills and competencies of organizational managers, thereby influencing firm performance. Similarly, Neely et al. (Citation2000) found that the impact of ERM on firm performance depends on the extent of stakeholder participation and the level of risk management maturity. However, research by Pagach and Warr (Citation2010) and Razali et al. (Citation2011) reveals that organizations using ERM do not experience an improvement in performance. Additionally, Neely et al. (Citation2000) discovered a negative correlation between ERM and Tobin’s Q. Based on the findings of earlier studies, there are still significant disparities in the performance of organizations that implement ERM, providing a foundation for future studies.

The primary objective of this study was to establish an ERM assessment through the development of the ERM Index. We aimed to introduce a simpler but powerful ERM Index measurement to assess the level of ERM implementation in a company, based on the latest version of COSO (2017). This index can be used by companies that are not yet mature enough in their ERM implementation level, such as some mining companies in Southeast Asian countries. We refer to this index as the Modification of the ERM Index (MERMi). The second objective of this research was to examine the factors that influence the use of ERM in Southeast Asia. There is no single framework or model that can predict how ERM and business performance will be affected by the most important factors.

Based on the available research (Chen et al., Citation2020; D. K. Nguyen & Vo, Citation2020; Gordon et al., Citation2009), there are several crucial aspects to consider while attempting to understand the connection between ERM and firm success. These include industry competitiveness, company complexity, firm size, international diversity, and financial leverage. The third goal of this study is to examine how ERM affects the performance of mining businesses in Southeast Asia. Mining companies in Southeast Asia were chosen as the research object because they face more uncertainty, challenges, and risks that can affect their performance compared to companies in developed countries. Therefore, there is a need for more improvement in the application of ERM. Strategic risk management has been the responsibility of the highest leadership in mining companies (Shad et al., Citation2019; Zungu et al., Citation2018).

Managing risks in the mining industry is crucial as it is a high-risk business that demands long-term capital investment and is influenced by global commodity prices. It has significant social impacts and impacts the environment while being strongly influenced by politics. Hence, decision-making in mining companies must focus on profitability and good risk control (Shad et al., Citation2019; Zungu et al., Citation2018).

Developing Southeast Asian countries face downside risks due to economic performance being vulnerable to trade tensions, unexpected weakening of the global economy, and shocks in global financial markets that cause capital outflows. Moreover, the COVID-19 pandemic has worsened the situation, leading to the weakening of the world economy. The mining industry has become a vital contributor to regional growth for ASEAN countries and is expected to be one of the most critical sectors in regional growth. The sector is essential in meeting the 2025 ASEAN Economic Community targets, including regional sustainability, as it supplies key raw materials to society and industry. Infrastructures, buildings, and manufacturing industries cannot function in the economy without an adequate and consistent supply of minerals. Furthermore, the mining sector plays a significant role in national economic development.

The current paper aims to make several contributions to the existing literature. Firstly, this research is expected to contribute to the development of financial management studies, particularly in terms of theories or concepts that explore how the application of enterprise risk management can enhance firm performance. Secondly, this research can offer insights into the factors that influence a company’s risk management. Thirdly, this research can contribute to the development of studies on the application of risk management in developing countries, specifically in Southeast Asia.

This paper is organized into 7 parts. Section 1 begins with an introduction, Section 1 describes the background analysis, Sections 2 and 4 summarize relevant literature, Section 4 describes the data and methodology used, Section 5 presents the findings, and Section 6 concludes with managerial and policy implications.

2. Background

The existence of risk management supports the realization of good corporate governance through business planning by considering potential risks (Raffles, Citation2011). Therefore, disclosing risk management is considered important because it enables decisions to be made to overcome these risks. For stakeholders, risk disclosure allows them to monitor the main objectives and provide protection from adverse effects of risk through appropriate risk treatment (Pradana & Rikumahu, Citation2014). Various studies have shown the importance of risk disclosure. For example, a study by Ntim, Osei, and Mensah (Citation2013) conducted after the global financial crisis found a significant increase in the number and quality of risk disclosures, which could be explained by heightened risk awareness. Better corporate governance can increase transparency and accountability regarding risk, positively impacting risk reporting. Elamer et al. (Citation2017) conducted a study on Islamic banks in the Middle East and North Africa and found that both Islamic and national banking governance contributed to risk management and disclosure. The study also revealed that banks with state ownership and those listed on the stock exchange had higher levels of risk disclosure. In conclusion, disclosure of risk management is crucial for the sustainability of the company and stakeholders.

Furthermore, mining companies face various operational, financial, environmental, and social risks that threaten their profitability and sustainability. Due to the complexity of mining operations, effective risk management strategies are essential to minimize negative impacts. Risk management has become a critical aspect of mining operations and significantly impacts company performance. This paper examines the importance of risk management in mining companies in Southeast Asia, based on information disclosed by companies. The mining industry has undergone significant changes over the years, with regulations, reforms, and policies playing a critical role in shaping risk management practices. Regulatory frameworks have evolved to address significant risks associated with mining operations. For example, in the United States, the Mine Safety and Health Administration (MSHA) was established to oversee mining operations and enforce safety regulations. Similarly, in Australia, the Department of Mines, Industry Regulation, and Safety (DMIRS) oversees mining operations to ensure compliance with safety and environmental regulations. These regulations aim to ensure that mining operations are conducted safely and mitigate risks associated with mining activities.

Reforms in the mining industry have also played a critical role in shaping risk management practices. These reforms aim to promote sustainable mining practices and reduce the negative impacts of mining on the environment and local communities. For instance, in Canada, the Extractive Sector Transparency Measures Act (ESTMA) requires mining companies to disclose their payments to governments, increasing transparency and accountability in the mining sector while promoting responsible mining practices. Similarly, the Raw Materials Initiative in the European Union emphasizes responsible sourcing and sustainable mining practices, requiring effective risk management strategies.

Policies have also been developed to promote responsible mining practices and effective risk management. The United Nations Guiding Principles on Business and Human Rights provide guidelines for companies to manage human rights risks associated with their operations. The guidelines require companies to conduct human rights due diligence and implement effective risk management strategies to mitigate human rights risks. The Global Reporting Initiative (GRI) provides guidelines for companies to report on their sustainability performance, including their risk management practices and the steps taken to mitigate risks.

Effective risk management is crucial to the performance of mining companies due to the high-risk nature of the industry. Accidents, environmental incidents, and community conflicts can significantly impact a company’s performance. Effective risk management strategies can help companies to mitigate these risks and minimize their negative impacts. Additionally, risk management strategies can help companies to identify opportunities for growth and improve their performance, such as identifying new markets, enhancing social and environmental performance, and improving their reputation.

Various studies have demonstrated the importance of risk management to the performance of mining companies. For instance, a study by Akkucuk, and Gurer (Citation2021) found that effective risk management practices positively affect mining companies’ financial performance. Risk management practices such as risk identification, assessment, and mitigation significantly impact mining companies’ financial performance. Similarly, a study by Gao et al. (Citation2020) found that effective risk management practices can help mining companies to improve their environmental and social performance. Companies that implement effective risk management strategies tend to have better social and environmental performance compared to companies that do not.

Risk management is essential to the performance of mining companies due to the high-risk nature of the industry. Reforms, policies, and regulations play a critical role in shaping risk management practices, promoting sustainable mining practices, and reducing the negative impacts of mining on the environment and local communities. Effective risk management strategies can help mining companies to mitigate risks, minimize negative impacts, and identify opportunities for growth and improvement.

In recent years, there has been an increasing focus on sustainability and responsible mining practices, driven by a growing awareness of the environmental and social impacts of mining operations. As a result, regulatory bodies and industry associations have developed several guidelines and frameworks for risk management in the mining sector, aimed at improving the industry’s overall performance in this area.

One such framework is the International Council on Mining and Metals (ICMM) Sustainable Development Framework, which includes a focus on risk management. The framework outlines ten principles that mining companies are expected to adhere to, ensuring sustainable development. Principle 6 states that companies should “implement effective risk-management strategies and systems, and continuously improve these to reflect changing circumstances and emerging risks.”

Similarly, the Mining Association of Canada (MAC) has developed a Towards Sustainable Mining (TSM) initiative, which includes a focus on risk management. The initiative comprises six areas of focus, such as tailings management, biodiversity conservation, and crisis management, all of which require robust risk management strategies to be effective.

The importance of effective risk management in the mining sector is further underscored by recent regulatory developments. In 2019, the Global Tailings Review, a multi-stakeholder initiative including representatives from the mining industry, investors, and civil society, launched guidelines aimed at improving the safety and sustainability of tailings storage facilities. The guidelines, which are intended to be applied globally, include a focus on risk management, and set out expectations for mining companies in this area, such as developing a risk management plan and appointing a senior executive responsible for risk management.

Besides regulatory developments, there have been high-profile incidents in the mining sector in recent years, highlighting the importance of effective risk management. One such incident was the collapse of the Brumadinho dam in Brazil in 2019, which killed 270 people and caused significant environmental damage (Lumbroso et al., Citation2021). The incident was attributed to a failure of risk management, leading to calls for increased regulation and oversight of mining operations.

The COVID-19 pandemic has also highlighted the importance of risk management in the mining sector, with the industry facing a range of new and complex risks related to the pandemic. These risks include operational disruptions due to illness or quarantine measures, supply chain disruptions, and health and safety risks for workers. Mining companies have had to rapidly adapt their risk management strategies in response to the pandemic, implementing new measures such as increased health and safety protocols and remote working arrangements.

In conclusion, effective risk management is essential for the long-term sustainability and performance of mining companies. The mining industry is subject to a range of complex and evolving risks, including environmental, social, and regulatory risks, and effective risk management is key to mitigating these risks and ensuring the continued success of mining operations. Regulatory frameworks and industry initiatives, as well as recent high-profile incidents and the COVID-19 pandemic, have all highlighted the importance of effective risk management in the mining sector. Therefore, it is critical that mining companies prioritize risk management and develop robust strategies and systems to ensure the sustainability of their operations (OECD, Citation2020).

3. Theoretical literature review

3.1. Agency Theory

Jensen and Meckling (Citation1976) stated that almost all contractual relationships, in which one party (agent) promises performance to another party (principal), have the potential to create or give rise to agency problems. The difficulty lies in the fact that the agent typically has better information than the owner about the relevant facts, and the owner cannot verify that the agent’s performance is as promised. As a result, agents have incentives to act opportunistically, reduce the quality of their performance, or even act in their own interest. This decreases the value of the agent’s performance to the owner, either directly or indirectly. To ensure the quality of the agent’s performance, the owner must monitor the agent. The more complex the tasks performed by the agent, and the greater the agent’s discretion, the greater the agency costs incurred (Fama, Citation1980).

The issue of agency problems has been extensively studied in various academic fields, such as accounting (Ronen & Balachandran, Citation1995; Watts & Zimmerman, Citation1983), finance (Fama, Citation1980; Jensen, Citation1986), economics (Jensen & Meckling, Citation1976; Ross, Citation1973; Spence & Zeckhauser, Citation1971), political science (Hammond & Knott, Citation1996; Weingast & Moran, Citation1983), sociology (Adams, Citation1996; Kiser & Tong, Citation1992), organizational behavior (Kosnik & Bettenhausen, Citation1992), dan marketing (Logan, Citation2000; Tate et al., Citation2010). The widespread existence of agency problems in various types of organizations has made this theory one of the most important theories in finance and economics.

In relation to agency theory and firm performance, one cannot overlook the importance of company management, as the achievement of a company’s goals is closely linked to the performance of its management.

3.2. Asymmetric information

Information asymmetry can arise from an imbalance in information mastery between agents and principals. This can provide managers with opportunities to engage in earnings management, which can mislead shareholders about the company’s performance. The theory of information asymmetry was developed by Akerlof (Citation1970), Spence (Citation1973), and Stiglitz (Citation1961) was formalized in 2001. Information asymmetry is a problem between agents and principals, as agents typically know more about the company’s states than principals, causing adverse problems. In a perfect market setting with perfect and costless information available to both parties, and no uncertainty about current and future trading conditions, parties are not disadvantaged due to information asymmetry. However, in the real world, information is often imperfect, with costs and risks associated with future conditions. Information is distributed asymmetrically between agents and principals. From the principal’s perspective, incomplete information about the quality underlying the management of the company can cause adverse problems (J. E. Stiglitz & Weiss, Citation1981).

To overcome this problem, an audit committee is necessary. This is expected to prevent fraud and incorporate information obtained by both principals and agents so that top management decisions are more balanced for the interests of principals and agents, leading to improved firm performance. Additionally, agency conflicts can be resolved by providing stock options. The agency theory explains firm performance, where companies with good performance increase company profits, which serves as a basis for investor considerations to invest in the concerned company.

3.3. Firm performance

Business entities adopt performance measurement systems to determine how well their products and services respond to customer needs and how effectively the company can improve (Brigham & Houston, Citation2021). Lingle and Schiemann (Citation1996) emphasized the need for strategic performance measures to drive company success, while Kaplan and Norton (Citation2001) recommend performance measurement as a basis for setting strategic objectives, continuous improvement, and cultural change. Performance measurement provides an effective method for determining whether a company is meeting its goals and achieving its mission. The performance measurement system is the main contributor to determining the company’s perception, coordination ability, and control over its environment. Companies use performance measurement systems to monitor and control activities, predict future internal and external circumstances, monitor behavior relative to goals, make decisions, and change the orientation and behavior of the company (M. F. Malik et al., Citation2020).

Regarding measuring firm performance, Tobin’s Q can be used, which calculates all elements of the company’s debt and share capital and is considered to provide the best information. Companies with high Q values have good investment opportunities or competitive advantages. In Tobin’s Q analysis, a Q > 1 indicates that the company’s market value is higher than the book value of its assets, which means that the company’s stock value is high (overvalued). A Q < 1 shows that the book value of the company’s assets is greater than the market value of the company, which means that the value of the company’s shares is undervalued. A high stock value reflects a high company value and vice versa, as the company value is positively related to the stock value (Wolfe & Sauaia, Citation2003).

Based on this explanation, a company’s current performance is determined by its management of existing resources and how well it utilizes them to create a sustainable competitive advantage and manage risks. Companies need to actively create policies related to improving firm performance to provide a positive signal to investors, shareholders, creditors, and other interested parties.

3.4. Enterprise risk management

The Committee of Sponsoring Organizations of the Treadway Commission (COSO) provides executive guidance on the global adoption of effective, efficient, and ethical business operations. COSO started developing a consistent definition of risk management in 2004. It revised the previous framework by facilitating the linkage of risks to targets and performance. Performance is a process that starts with planning, setting goals, establishing indicators and targets, and monitoring. In the new framework, the second element is clearer as a framework for formulating risk in strategy. Performance becomes a separate element, namely the third, in the new framework, with the application of risk management (from identification to risk response) in the context of achieving business strategies and objectives that introduce a new risk profile, namely risk, performance, risk appetite, and risk capacity. ERM 2017 focuses on strategy and identifying opportunities to create and maintain value. In the fourth element, control reviews risk and performance as a sub-element in the new framework COSO (2017).

Based on the COSO (2017) framework, there are five interrelated components supported by a set of principles, ranging from governance to monitoring, which are implemented in different ways for different organizations regardless of size, type, and sector. Adhering to these principles can provide management and the board with good expectations that the company understands and strives to manage risks related to its business strategy and objectives.

4. Empirical literature review and hypotheses development

4.1. Industry competition to ERM

Industrial competition is a fundamental concern for companies because the industry in which the company operates is assumed to be a factor influencing the implementation of ERM. Companies in the same industry compete for sales opportunities (market share) in that industry. Therefore, a company’s high sales in relation to the industry’s average sales imply that the company’s performance is better than the average of its competitors. If a company cannot compete, it becomes an obstacle because the company cannot obtain optimal profits on an ongoing basis (Manobi & Umar, Citation2021).

The intense industry competition faced by enterprises makes it necessary for them to face significant risks in obtaining a sustainable level of profit (Gordon et al., Citation2009). With the development of technology and changing consumer needs, companies must consider the level of competition in risk management to be able to compete and maintain their existence. Some industries, such as finance and mining, are heavily regulated by the government because they are identified as having such high risks that the application of ERM in these industries needs to be developed (Pagach & Warr, Citation2010).

Manobi and Umar (Citation2021) state that the level of competition faced by companies is proportional to their need for ERM because the higher the level of sales competition in an industry, the more valuable the ERM system is for the company. This is in line with the opinion of Gordon et al. (Citation2009), which states that there is a positive correlation between the level of industry competition faced by companies and their demand for ERM systems. It can be concluded that the more intense the industry competition, the greater the risks faced, and the more optimal application of ERM is needed by companies.

Table summarizes the literature review on the relationship between Enterprise Risk Management (ERM) and firm determinants in both developed and developing countries. In developed countries, Pagach and Warr (Citation2010) found no significant change in the relationship between ERM and firm determinants, while Grace et al. (Citation2010) concluded that the use of ERM can increase cost and revenue efficiency. Hoyt and Liebenberg (Citation2011) found that the early stages of ERM can increase the value of insurance companies. Maingot et al. (Citation2012) discussed the effect of the financial crisis on ERM disclosure in Canadian companies. Farrell and Gallagher (Citation2015) found that ERM positively influences firm value. In developing countries, Razali et al. (Citation2011) found that ERM has no effect in Malaysian publicly listed companies. Omasete (Citation2014) concluded that there is a positive relationship between risk management and financial performance in Nigerian insurance companies. Ahmed and Manab (Citation2016) carried a conceptual model to help companies implement better ERM. Danisman and Demirel (Citation2019) found that none of the three strategies (financial, operational, and risk management) increase the value of the company. Horvey and Ankamah (Citation2020) found that ERM drives firm performance at both the company level and the market level in Ghana.

Table 1. Literature review

4.2. Firm complexity to ERM

This means that companies with a greater number of business segments are considered more complex (Golshan & Rasid, Citation2012). Gordon et al. (Citation2009) found that the more complicated a company is, the less likely it is that information will be integrated, making it harder to set up a management control system, which increases the risk. Usually, a larger company size is accompanied by high complexity because the activities within it become increasingly complex, and the need for increased control is also greater (Rahmadani & Husaini, Citation2017). This is in accordance with agency theory, where the greater the complexity of tasks in a company, the greater the tendency of the company to experience agency problems, leading to higher risk. Therefore, it is important for companies to implement ERM to improve control, such as identifying material weaknesses in internal control. Compared to traditional risk management, ERM is considered better for providing integrated risk management for companies countries (Hoyt & Liebenberg, Citation2011). Golshan and Rasid (Citation2012), Gordon et al. (Citation2009), and Rahmadani and Husaini (Citation2017) found that company complexity has a positive effect on ERM, indicating that the more complex the company, the greater the need for the implementation of ERM systems.

4.3. Firm size to ERM

When designing and implementing a risk management control system, the size of the company becomes a significant issue. As a corporation grows, the types, timing, and scope of events that threaten it will change. This is because larger companies require more information, and their components are more complicated (Gordon et al., Citation2009). The large size of the company can also hinder the integration of information systems, increasing the possibility of risk. Large companies face more risks, including financial risks (Pagach & Warr, Citation2010). In accounting, enterprise size is a significant consideration when designing and implementing management control systems (Haka et al., Citation1985; Myers et al., Citation1991; Shields, Citation1995). Beasley et al. (Citation2005) and Hoyt and Liebenberg (Citation2008) also considered the size of the organization when constructing ERM systems. Large companies have more volatile cash flows, making them more susceptible to financial difficulties. Therefore, big companies tend to implement ERM systems more often than small companies (Lechner & Gatzert, Citation2018). This corresponds to the availability of resources, where larger companies have more resources to implement ERM. This is consistent with the research of Hasina et al. (Citation2018), Widyawati and Harsiah (Citation2018), which stated that company size has a positive effect on ERM.

4.4. International diversification to ERM

One theoretical framework that explains the relationship between international diversification, ERM, and company performance is the resource-based view (RBV) theory. According to this theory, a company’s resources and capabilities are key determinants of its competitive advantage and performance. ERM can be viewed as a critical resource that helps mining companies effectively manage risks and enhance their competitive advantage in international markets. Moreover, ERM can help mining companies address the challenges associated with managing risks across diverse international operations. By implementing a standardized approach to risk management, mining companies can better identify and prioritize risks across their international operations and allocate resources more effectively. ERM can also help mining companies establish a more comprehensive understanding of the risks they face in international markets and develop strategies to mitigate them.

While diversification is often seen as a technique for mitigating risk, focus can be more beneficial in the event of financial trouble. Diversification also deals with overseas market opportunities and the company’s growth strategy (Lechner & Gatzert, Citation2018). Companies entering the international market face greater risk, making ERM all the more necessary (Farrell & Gallagher, Citation2015). This is because international business involves different rules and regulations in different countries, creating complex risks countries (Hoyt & Liebenberg, Citation2011). Hoyt and Liebenberg (Citation2008) and Lechner and Gatzert (Citation2018) have shown that international diversification requires companies to implement ERM.

4.5. Financial leverage to ERM

One theoretical framework that explains the relationship among financial leverage, ERM, and company performance is the trade-off theory. According to this theory, there is an optimal level of financial leverage that maximizes the value of a company by balancing the benefits of debt financing with the costs of financial distress. ERM can help mining companies strike this balance by managing the risks associated with financial leverage and improving their financial performance. Financial leverage is considered an influential factor in making ERM implementation decisions. Companies with high levels of leverage often face high costs and difficulties, or high leverage indicates the company is more dependent on debt to pay its obligations, so the company has a high risk of default (Golshan & Rasid, Citation2012). Therefore, high-leverage companies tend to implement ERM to reduce the risk of debt repayment defaults (Liebenberg & Hoyt, Citation2003). Gatzert and Martin (Citation2015) also argue that companies with large financial leverage should be able to generate more profits by managing risk. This is in line with the research of Pagach and Warr (Citation2010); Razali et al. (Citation2011); Saedi et al. (Citation2012) which stated that the implementation of ERM is increasingly needed by increasing financial leverage because the risk is greater.

Therefore, this study proposes the following hypothesis:

H1:

The implementation of ERM increases with industry competition.

H2:

The implementation of ERM increases with the complexity of the company.

H3:

The implementation of ERM increases with the firm’s size.

H4:

The implementation of ERM increases with international diversification.

H5:

The implementation of ERM increases with higher levels of financial leverage.

4.6. ERM to firm performance

According to COSO (2004), business risk refers to the possibility of failures in a company that can interfere with the returns on investments and even affect the company’s performance. Investor confidence decreases when faced with such risks (Pangestuti et al., Citation2022). Effective enterprise risk management (ERM) programs not only protect shareholder value but also increase performance opportunities by managing risks. Relevant risk management enables an enterprise to cope with the risks it encounters. Azim and Abdelmoniem (Citation2015) found that managing market risk can reduce risk exposure and improve performance. Risk management can also minimize risks, reduce tax payments, and increase investment confidence. ERM provides businesses with a more comprehensive approach to risk management than conventional methods. It is believed that ERM improves performance by adopting a systematic and consistent technique to manage all risks faced, reducing the risk of failure.

When evaluating investment options, investors assess a firm from various perspectives to see how it can provide the greatest profits in the future (Maychael et al., Citation2022). One of the many factors assessed is the probability of estimated danger. Each investor has unique risk-taking preferences and levels of assurance. Therefore, to maintain a company’s performance in good condition, it is necessary to apply ERM to identify potential risks. This is in line with previous research conducted by Saedi et al. (Citation2012), Hoyt and Liebenberg (Citation2008), Lechner and Gatzert (Citation2017), Gordon et al. (Citation2009), and M. F. Malik et al. (Citation2020), which suggests that ERM has a positive effect on company performance. ERM can minimize the risk of failure of the company as a whole and improve its performance.

4.7. Industry competition to firm performance

Competition is an external force that affects performance and is influenced by the actions of companies targeting the same market segment. The conditions and intensity of competition differ from one industry to another, as exemplified by the degree of product differentiation, threats of competition between companies, and the bargaining power friction between sellers and buyers. Competition develops over time and depends on several interacting factors, such as the number and size of competing companies, growth rates, resource mobilization, and barriers. The strength and interaction between these factors affect the intensity of competition.

According to Barnett (Citation1997), intensity refers to the influence that a company has on the survival chances of another company. This suggests that the intensity of competition can affect the strength and effectiveness of marketing strategies, leading to poor performance results (Wu & Pangarkar, Citation2010). While competition can improve market orientation, which can affect a company’s performance through increased pressure on margins and decreased market share. This means that businesses have to choose the best way to get ahead of the competition and improve their performance.

4.8. Company complexity to firm performance

This includes the need for increased control, which can lead the company to implement a bureaucratic control strategy and potentially increase its success in achieving goals (Rahmadani & Husaini, Citation2017). Greater complexity, resulting from a diversity of business transactions, can lead to less information integration and a management control system with numerous obstacles. Ge and McVay (Citation2005), and Pangestuti et al. (Citation2022) identified material defects in internal control as essential components of ERM for complex companies. Hoyt and Liebenberg (Citation2008) found that the use of ERM was linked to the complexity of the organization. This is consistent with the research of Rahmadani and Husaini (Citation2017) which states that companies that are increasingly complex need to make the right decisions to run effectively and efficiently, thus potentially increasing their performance and minimizing agency problems.

4.9. Company size to firm performance

This reflects the company’s ability to generate profits, indicating that larger companies have the potential to generate higher profits. A high profit margin can contribute to improving the company’s overall performance. Therefore, managers engage in profit management to increase the company’s profit, taking advantage of the company’s large scale, which makes it easier to generate profits and maintain a strong reputation in the public eye. This is in line with agency theory, which explains company performance, stating that companies with good performance can increase profits, thereby becoming a basis for investor considerations when investing in the concerned company. This statement is consistent with the research conducted by Iswajuni et al. (Citation2018), Husna and Satria (Citation2019), and L. Nguyen et al. (Citation2021).

4.10. International diversification to firm performance

Essentially, global expansion is a strategy implemented by companies to grow and expand their reach in the international market, which can significantly enhance their performance. By broadening their market reach, this strategy offers several advantages, such as increased revenue and profitability. The greater the company’s diversification, the greater the influence on its performance. Companies with multiple divisions or business units tend to be more diverse (Golshan & Rasid, Citation2012; Pagach & Warr, Citation2010). This aligns with research conducted by Altaf and Shah (Citation2015) and Agustin and Setiawan (Citation2021), which indicates that international diversification has a positive impact on company performance. International diversification provides greater market opportunities, resulting in increased profitability and improved company performance.

4.11. Financial leverage to firm performance

Financial leverage plays a crucial role in the sustainability and success of a company. It is an external source of financing used to finance business operations and has a positive impact on a company’s performance through asset acquisition and expansion of its activities, leading to profits. However, financial leverage can also have a negative impact if it reaches a level that is too high due to the default payment of borrowed funds. In agency theory, high leverage results in high agency costs (Subramaniam et al., Citation2009), and the greater the agency costs, the higher the company’s financial risk, leading to weakened performance.

Therefore, to ensure that financial leverage improves a company’s performance, management must pay close attention and supervise the use of financial leverage in the company’s business activities. This discussion is in line with research conducted by AlGhusin (Citation2015); Zeitun and Saleh (Citation2015); Nency and Muharam (Citation2017), which found that the amount of debt can cause a decline in the company’s performance.

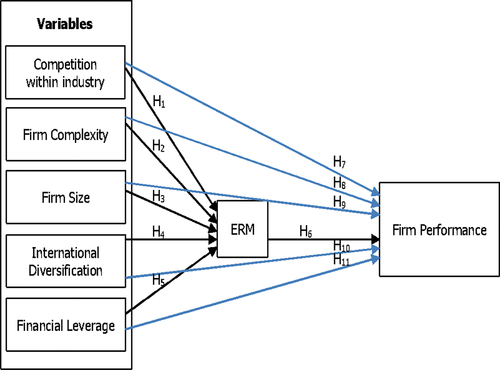

Figure explains about study examines the relationship between several independent variables (industry competition, complexity of the company, firm's size, international diversification, and financial leverage) and the dependent variable of company performance, with the intervening variable of Enterprise Risk Management (ERM). The independent variables in this study are factors that can potentially affect the implementation of ERM. The intervening variable in this study is ERM, which is the variable that is expected to mediate the relationship between the independent variables and the dependent variable. ERM refers to the process of identifying, assessing, and managing risks faced by a company. The implementation of ERM is expected to affect the dependent variable, company performance. The dependent variable in this study is company performance. The study aims to explore the relationship between the independent variables, intervening variable, and company performance. This study aims to explore the complex relationships between these variables and their effects on company performance, with ERM as an important mediating variable.

Figure 1. Research model .

Therefore, we also put forward additional hypotheses as follows:

H6:

ERM affects firm performance.

H7:

Industry competition affects firm performance.

H8:

Company complexity affects firm performance.

H9:

Company size affects firm performance.

H10:

International diversification affects firm performance.

H11:

Financial leverage affects firm performance.

5. Research design

5.1. Research samples

The sample for this study comprises all mining companies listed on the Southeast Asian Stock Exchange. The countries with stock exchanges include Indonesia, with the website www.idx.co.id; Malaysia, with www.bursamalaysia.com; Singapore, with www.sgx.com; Thailand, with www.classic.set.or.th; Vietnam, with www.hsx.vn; and the Philippines, with www.pse.com.ph. The mining sector was chosen because of its high-risk nature and significant contribution to a country’s national economy. Southeast Asian countries were selected because they are developing nations facing greater uncertainties, challenges, and risks that could affect firm performance when compared to developed countries. This requires more improvements in the implementation of ERM. A purposive sampling technique was used to obtain the research sample, in line with the specified criteria. The details are as follows.

Table presents the research sample for the study. The criteria for the research sample are companies in the mining sector listed on Southeast Asian Stock Exchanges during the period of 2016-2020. The table shows that there were 227 companies in the mining sector listed on Southeast Asian Stock Exchanges during this period. However, 22 mining sector companies in Southeast Asia did not publish complete financial statements during the years of 2016-2020. Therefore, the total number of research samples was 205. The research period for the study is from 2016 to 2020, which is 6 years. The total number of observed data in the study was 1230 data.

Table 2. Research sample

presents the dimensions and indicators of the Enterprise Risk Management Index used in the study. The dimensions include Governance & Culture, Strategy & Objectives Setting, Performance, Review & Revision, and Information, Communication, & Reporting. Under each dimension, there are several indicators that represent the specific aspects of the dimension. For example, under the Governance & Culture dimension, there are indicators such as GC1: Exercise Board Risk Oversight, GC2: Establishes Operating Structures, GC3: Defines Desired Culture, GC4: Demonstrates Commitment to Core Values, and GC5: Attracts, Develops, and Retains Capable Individuals. The table provides a clear and concise summary of the dimensions and indicators used in the study to assess the effectiveness of enterprise risk management in the mining sector.

Table 3. Dimensions and indicator of MERMI

5.2. Measurement and variable definition

This study will examine the relationship between the dependent and independent variables which are moderated by the moderating variable. The dependent variable is firm performance. The independent variables are industry competition, firm complexity, firm size, international diversification, and financial leverage. While the moderating variable is Enterprise Risk Management (ERM). The explanation and measurement of each variable are as follows:

5.2.1. ERM variable measurement

The measurement of ERM is conducted through an index called the Modified Risk Management Index (MERMi), which is based on the latest version of COSO (2017). This study aims to introduce a simpler, yet powerful measurement to assess the level of ERM implementation in a company. The MERMi index can be beneficial for companies that are not yet fully mature in their ERM implementation, such as some mining companies in Southeast Asian countries.

MERMi is an index that is derived from the company’s annual report, which discloses the company’s implementation of ERM. The index uses three values: 0, 1, and 2. A score of 0 is given to companies that do not disclose the dimensions and indicators of the COSO (2017) principles. If the company discloses the dimensions and indicators in a general or qualitative manner, it is given a score of 1. If the company discloses quantitatively, it is given a score of 2. All values are then totaled and divided by weights to obtain the MERMi value. The indicators are searched using a phrase search according to their names in the company’s annual financial statements. The 20 disclosure items in the ERM framework issued by COSO (2017) are used to measure risk management disclosures, and content analysis is used to analyze these disclosures.

To ensure the accuracy of the dimensions and indicators of the 20 items in COSO (2017), validity and reliability tests were conducted. The validity test ensures that the items measure what they are supposed to measure, while the reliability test measures the consistency of the results over time, assuming that the phenomena being studied does not change. The reliability coefficient was calculated using Cronbach’s Alpha test, and variables were considered reliable if they had a coefficient above the r table at a 95% confidence level (0.05).

5.2.2. Firm performance

The dependent variable in this study is firm performance. Firm performance is defined as a situation where investors have a positive view of the company’s performance, which is reflected in optimal returns and thereby increasing the prosperity of shareholders. The company’s performance is measured using Tobin’s Q, which is a revised calculation with simpler calculations aimed at obtaining the market value of the company’s debt (Gordon et al., Citation2009; Hoyt & Liebenberg, Citation2011; McShane et al., Citation2011; Razali et al., Citation2011); (Farrel & Gallagher, 2019).

5.2.3. Industry competition

The Herfindahl Hirschman Index (HHI) focuses on the large proportion of a particular market share in an industry. The results shown by the HHI have an identical pattern to the concentration ratio analysis approach. The HHI is another type of concentration measure often used to measure market concentration levels. The HHI is calculated by summing the squares of the market shares of all the companies in an industry. HHI values range from 0 to 1. If the HHI is close to zero, it means that there are many companies with almost the same size of business in the industry, and the market concentration is low. Conversely, the industry is a monopoly if the HHI is equal to one. The higher the HHI, the greater the concentration of industries, which shows the greater the size of the company.

5.2.4. Firm complexity

According to Doyle et al. (Citation2007), the complexity of an enterprise is correlated with the number of business segments within the company. In other words, adding business sectors increases the organization’s complexity. Therefore, this variable is calculated by determining how many business segments a company has (Doyle et al., Citation2007; Ge & McVay, Citation2005; Gordon et al., Citation2009).

5.2.5. Firm size

The size of companies can be determined by the total amount of assets they possess. Investors tend to pay greater attention to companies with larger asset sizes, as they tend to be in better financial condition. The natural logarithm of a company’s size is calculated by taking the average of all its assets (Hoyt & Liebenberg, Citation2011). There for, to measure the firm size variable, the formula is used:

Table provides a summary of the variables used in the study, along with their respective measurements, predictions, and sources. The first variable is firm performance, which is measured using Tobin's Q and obtained from the annual reports of the company. The second variable is ERM, which is categorized into ”2” if the statement qualitatively describes the application of ERM, ”1” if the statement describes quantitatively the application of ERM, and ”0” if the company does not apply ERM at all. The third variable is industry competition, which is measured using the Herfindahl Hirschman Index (HHI), the fourth variable is company complexity, which is measured by the number of business segments in an enterprise, the fifth variable is firm size, which is measured using the natural logarithm of book value of total assets, the sixth variable is international diversification, which is categorized into 1 (there is international diversification) and 0 (no international diversification) and the last variable is financial leverage, which is measured by book value of liabilities divided by market value of equity and all data obtained from the annual reports of the company.

Table 4. Summary definitions of variables

Table presents the results of construct validity for different instruments used in the study. The table shows the correlation value, significance level (Sig), and conclusion for each instrument. The study found that all instruments had a correlation value above 0.6 and a significance level of 0.000, indicating that they were valid measures for the constructs they were designed to measure. Therefore, all instruments were considered valid for use in the study.

Table 5. Result of construct validity

Table shows the instrument reliability for each of the constructs in the study. The table includes the number of items in each construct, the Cronbach's alpha value, and the conclusion about the reliability of the construct. The constructs included in the table are Governance & Culture (GC), Strategy & Objectives Setting (SO), Performance (PF), Review & Revision (RR), and Information, Communication, & Reporting (ICR). The Cronbach's alpha values for all constructs are high, ranging from 0.858 to 0.972, indicating that the instruments are reliable measures of their respective constructs. Therefore, the results obtained from the study can be considered valid and reliable.

Table 6. Instrument reliability

5.2.6. International diversification

International diversification is measured using a dummy variable that assigns a value of 1 to companies that diversify internationally and 0 to those that do not. The phrase “international diversification” is searched for to determine whether a company engages in international diversification (Hoyt & Liebenberg, Citation2011; Razali et al., Citation2011; Lechner & Gatzert, Citation2018; Farrel & Gallagher, 2019).

5.2.7. Financial leverage

Empirical evidence has shown that financial leverage is one of the driving factors for the implementation of ERM. In this study, the financial leverage variable is calculated by dividing the book value of liabilities by the market value of equity (Hoyt & Liebenberg, Citation2011; Farrel & Gallagher, 2015).

5.3. Data analysis

This study utilizes the Two Stage Least Squares (2SLS) method, which is a regression technique included in the group of structural equation analysis. Essentially, this approach involves two steps in solving the equation to ensure that it is unbiased. Firstly, the Ordinary Least Squares (OLS) method is employed to regress explanatory endogenous variables on instrumental variables and other exogenous variables to obtain unbiased exogenous variables. Secondly, the endogenous variables are regressed on the unbiased explanatory endogenous variables with other variables excluded.

The data analysis technique used in this study involved the following tests:

Construct Validity Test, which focused on the extent to which the measuring instrument showed measurement results that were in accordance with its definition. The definition was reduced to a theory, and if the definition was based on the right theory and the item statements were appropriate, then the instrument was considered constructively valid (Fraenkel et al., Citation2012). The validity of each construct in this study was calculated by comparing the correlation of each indicator item with the total item score. The indicator items were Governance & Culture, Strategy & Objectives Setting, Performance, Review & Revision, and Information, Communication & Reporting. An instrument was considered valid if it had a correlation value above 0.60.

Reliability Test, which determined the Cronbach alpha value of Governance & Culture, Strategy & Objectives Setting, Performance, Review & Revision, and Information, Communication & Reporting. Research was considered reliable if it gave consistent results for the same measurement, and it had a Cronbach alpha value above 0.70.

Descriptive Statistics, which were used to analyze data by describing the collected data without intending to make generalizing conclusions (Sugiyono, Citation2015). In this case, descriptive statistics were used to explain data in the form of tables, graphs, standard deviation, percentages, and so on to make it easier to understand.

Pearson Correlation Test, which tested the level of closeness of the relationship between variables. The basis for decision making in this test was a significance value<0.05, which meant that the variables were correlated. If the significance value was>0.05, it meant that the variables were not correlated. The guidelines for interpreting the correlation coefficient included:

If the coefficient value was 0.00-0.199, it meant that the relationship level was very weak.

If the coefficient value was 0.20-0.399, it meant that the level of relationship was weak.

If the coefficient value was 0.40-0.599, it meant that the level of relationship was moderate.

If the coefficient value was 0.60-0.799, it meant that the level of relationship was strong.

If the coefficient value was 0.80-1.000, it meant that the level of relationship was very strong.

(5) Panel Data Regression Method, which was a combination of time series and cross-section data. Time series was data arranged in time (daily, monthly, and yearly), while cross-section was data collected from various regions, companies, or regions at the same time.

(6) Robustness test, which tested the sensitivity and consistency of the research results using the main model. To test the robustness of the study’s findings, the researchers conduct further research by changing the research year to 2022. This would allow them to examine whether the results remain consistent over time and whether any changes in the business environment or regulatory landscape have affected the relationship between ERM implementation and firm performance.

6. Empirical result and discussion

6.1. Construct validity

To calculate the ERM value for each sample, the validity of each construct is determined by comparing the correlation of each indicator item with the total score. There are 20 indicators described in . The table below indicates that all item indicators are valid because the calculated Pearson correlation coefficient (r) is greater than the critical value of r.

6.2. Reliability

It is presented in the table the Cronbach Alpha values for Governance & Culture, Strategy & Objectives Settings, Performance, Review & Revision, and Information-Communication & Reporting. All of the values are above the r table = 0.06, indicating that the instruments used to measure the principles of COSO (2017) are reliable.

After being tested for validity and reliability, the MERMi value is calculated by summing all ERM disclosures and dividing them by the total number of items per indicator to obtain a final score. This score is further divided by the weight of each item, which is 20, to obtain a weighted score for each company per year.

6.3. Descriptive statistic

This descriptive statistics technique is used to determine the highest, lowest, mean, median, and standard deviation values of each variable used by the researcher, allowing for a better understanding of the distribution and central tendency of the data.

Table presents an overview of 1230 observations collected from a sample of 205 mining companies in Southeast Asia from 2016 to 2021. The interpretation of the results is as follows:

In terms of industry competition, the highest value is 0.183000, and the lowest value is 0.000000. The research sample ranges from 0.000000 to 0.183000, with an average of 0.012636 and a standard deviation of 0.026327. If the HHI value is close to zero, it indicates that there are many mining companies with similar sizes in the market, resulting in low market concentration.

For company complexity, the highest value is 10.00000, and the lowest value is 0.000000. The research sample ranges from 0.000000 to 10.00000, with an average of 2.141579 and a standard deviation of 1.796070. Based on the average value, the sample of mining companies has medium complexity, indicating that the integration of information and management control systems in the organization can be properly managed.

In terms of company size, the highest value is 25.60300, and the lowest value is 0.000000. The research sample ranges from 0.000000 to 25.60300, with an average of 17.28907 and a standard deviation of 4.200590. Based on the average value, mining companies in Southeast Asia are generally large.

In terms of international diversification, the highest value is 1.000000, and the lowest value is 0.000000. The research sample ranges from 0.000000 to 1.000000, with an average of 0.548413 and a standard deviation of 0.497853. Based on the average value, 55% of mining companies in Southeast Asia have diversified internationally by expanding their businesses in the global market. Diversification reduces operational and financial risks, but increases the complexity of risks.

For financial leverage, the highest value is 114.3290, and the lowest value is 0.000000. The research sample ranges from 0.000000 to 114.3290, with an average of 1.877989 and a standard deviation of 6.732773. Based on the average value, mining companies in Southeast Asia use more debt than share capital, increasing the risk of default payments. Management must pay close attention to the use of financial leverage in the company’s business activities.

In terms of ERM, the highest value is 0.625000, and the lowest value is 0.000000. The research sample ranges from 0.00000 to 0.625000, with an average of 0.300346 and a standard deviation of 0.194217. Based on the average value, mining companies in Southeast Asia are relatively good at implementing ERM to mitigate risks in their operational activities. ERM activities can improve the company’s ability to generate profits, overall performance, and investor confidence.

Finally, in terms of Tobin’s Q value, the highest value is 5.331000, and the lowest value is 0.000000. The research sample ranges from 0.000000 to 5.331000, with an average of 1.093426 and a standard deviation of 0.803363. Most mining companies in Southeast Asia have a good performance reflected by the company’s market value, which is higher than the value of the company’s assets.

Table 7. Descriptive statistic

6.4. Pearson correlation test

As a preliminary analysis, a correlation calculation was carried out to test the degree of relationship between variables. The decision-making criterion for this test was the significance value of<0.05, which indicates that variables are correlated. Conversely, a significance value>0.05 means that variables are not correlated, which can be observed from the Pearson correlation coefficient.

Table shows the results of the Pearson correlation test between the variables in the study. The table presents the correlation coefficients (Pearson's r) and the p-values for each pair of variables. The variables included in the table are Industry Competition (Ci), Firm Complexity (Fc), Firm Size (Fs), International Diversification (Id), Financial Leverage (Fl), Enterprise Risk Management (ERM), and Firm Performance (P).

Table 8. Pearson correlation test result

6.5. Regression

The results of the independent variable regression test against ERM can be seen in the table below:

The results presented in Table indicate that the probability of the industry competition variable’s correlation with ERM is 0.0000 which is less than the significance level of 0.05. This implies that the intense competition in the mining industry in Southeast Asia inclines companies towards implementing ERM. In today’s world, where technology and consumer needs constantly evolve, companies must consider risk management as a crucial factor in maintaining their competitive edge and existence. The mining industry is one of the most regulated sectors as it impacts many people. The industry has been identified as having a high risk, and hence the application of ERM should be given high priority.

Table 9. Result of independent variable regression test against ERM

The mining industry in Southeast Asia is highly competitive, with numerous companies striving to capture a significant market share and secure resources. This intense competition has led to increased complexity in mining operations as companies seek to gain a competitive advantage through technological innovation, operational efficiency, and risk management. ERM is a process that helps companies identify, assess, and mitigate risks that could impact their business operations. By implementing ERM, mining companies can better manage the risks associated with their operations, such as environmental risks, geopolitical risks, and regulatory risks, among others.

Several studies have examined the relationship between ERM and company performance. One theoretical framework used to explain this relationship is the resource-based view (RBV) of the firm. The RBV suggests that a company’s resources and capabilities are the primary determinants of its competitive advantage and ultimately its performance. In the context of ERM, a company’s ability to effectively manage risks can be viewed as a resource or capability that contributes to its competitive advantage and performance.

The findings of this study are consistent with research conducted by Gordon et al. (Citation2009); Golshan and Rasid (Citation2012); Manobi and Umar (Citation2021), which suggested a positive correlation between the level of industry competition faced by companies and the application of ERM systems. This means that the tighter competition in an industry will lead to higher risks, and companies need to implement ERM more optimally to overcome the risks that they will face.

The results of the regression analysis revealed that the complexity of a company had a significant impact on the implementation of ERM, as evidenced by a probability value of 0.0000 < 0.05. The study found that the mining industry in Southeast Asia is highly complex due to several factors such as changing regulations, geopolitical risks, and environmental concerns. As a result, mining companies operating in this industry are increasingly adopting ERM practices to mitigate risks and enhance their performance. Furthermore, ERM can also help mining companies maintain their social license to operate and improve their reputation.

The study also found that the size of a mining company in Southeast Asia did not have a significant impact on the implementation of ERM, as indicated by a probability value of 0.7736 > 0.05. This finding suggests that the dissemination of information in larger companies may be more complex, making the implementation of ERM more challenging. The agency theory provides a theoretical framework for understanding the relationship between firm size and ERM. According to this theory, larger companies have a higher level of separation between ownership and management, which can lead to conflicts of interest between managers and shareholders. ERM can help mitigate these conflicts of interest by ensuring that risks are managed in a way that aligns with the interests of shareholders and other stakeholders.

While some studies have suggested that larger companies require ERM implementation due to their increased exposure to risks, this study’s findings contradict that notion. Instead, the complexity of a company appears to be a more critical factor in determining the need for ERM implementation. This study’s findings are consistent with the research of Zenita et al. (Citation2021) and Golshan and Rasid (Citation2012) which highlights that the implementation of ERM in large companies may be complex and costly.

In conclusion, the study highlights the importance of implementing ERM practices in the mining industry in Southeast Asia. Companies operating in this industry face numerous risks and complexities, and ERM can help them mitigate these risks, improve their reputation, and enhance their performance. Moreover, the study suggests that the size of a company may not be the sole factor in determining the need for ERM implementation. Instead, the complexity of a company may be a more critical factor to consider.

The regression test results show that international diversification probability of 0.00000 < 0.05 against ERM. This explains why mining companies in Southeast Asia, that operate internationally, tend to implement ERM. International diversification is a common strategy for mining companies operating in Southeast Asia to reduce their exposure to risks and enhance their performance. However, international diversification also brings its own set of risks, including political instability, cultural differences, and changes in regulatory environments. Therefore, implementing Enterprise Risk Management (ERM) practices becomes crucial for mining companies to manage these risks and improve their performance. Companies that have entered the international market will usually face a higher number and complexity of risks because they must meet all the criteria in the global market, which means that the application of ERM becomes more necessary. In addition, Espinosa-Méndez et al., (Citation2021) suggest that international diversification can be used as a strategic decision that not only focuses on reducing risks caused by market demand but also considers growth strategies triggered by opportunities from international markets. The results of this study support previous research conducted by Hoyt and Liebenberg (Citation2011), Farrell & Gallagher Citation2015, Lechner and Gatzert (Citation2018).

The results of the regression of financial leverage also show an influence on ERM, where the probability value of leverage is 0.0003 < 0.50. This reflects that mining companies in Southeast Asia have higher financial leverage and rely more on debt to pay their obligations, which results in greater default risks. Financial leverage, or the use of debt to finance operations, is a common strategy in the mining industry in Southeast Asia as it can provide companies with access to additional capital and improve their financial performance. However, financial leverage also increases a company’s exposure to financial risks, such as interest rate fluctuations and credit defaults, making it important for mining companies to implement Enterprise Risk Management (ERM) practices to manage these risks and improve their performance. Moreover, ERM can help mining companies address the challenges associated with managing risks associated with financial leverage. By implementing a standardized approach to risk management, mining companies can better identify and prioritize financial risks and allocate resources more effectively. ERM can also help mining companies establish a more comprehensive understanding of the financial risks they face and develop strategies to mitigate them.

High corporate leverage also causes companies to have high agency costs, so the possibility of companies experiencing financial difficulties is higher (Subramaniam et al., Citation2009). Thus, companies with higher amounts of financial leverage tend to implement ERM to reduce the risk of debt repayment defaults. This is in line with research conducted by Golshan and Rasid (Citation2012), Lechner and Gatzert (Citation2018), Horvey et al. (Citation2020), Şenol et al. (Citation2017) and Jurdi and AlGhnaimat (Citation2021), which stated that the implementation of ERM can reduce financial leverage so that risks to debt repayment can be minimized. On the other hand, Gatzert and Martin (Citation2015) argue that implementing an ERM program requires a large initial investment and companies with a higher level of capital or lower level of leverage may find it easier to start an ERM program.

The results of the independent variable regression test and ERM on firm performance (Tobin’s Q) can be seen in the table below:

The results present’ed in Table indicate that the probability of industry competition impacting Tobin’s Q is 0.0223, which is less than the significance level of 0.05. This demonstrates that intense competition in the mining industry in Southeast Asia can affect a company’s performance. The impact of industry competition on a company’s performance depends on the effectiveness of the strategies implemented (Wu & Pangarkar, Citation2010). Existing mining companies need to adopt the right strategy to create a competitive advantage that can enhance their competitiveness and lead to higher profits. However, if a company fails to establish a competitive advantage during high industry competition, it may experience a decline in market share and margins that can adversely affect its performance.

Table 10. Result of independent variable regression test and ERM against dependent variable

Furthermore, the regression analysis reveals that the complexity of mining companies in Southeast Asia significantly influences firm performance with a probability value of 0.0000, which is less than the significance level of 0.05. The complexity of a company, which is reflected in its multiple business segments, can positively impact its performance. The formation of different segments and the division of labor due to the company’s large size can create value and increase the value of the company. Additionally, the complexity of the company leads to increased control, which can help companies implement bureaucratic control strategies to enhance their success. These findings are consistent with Rahmadani and Husaini (Citation2017) research, which shows a positive correlation between company complexity and firm performance.

The regression analysis indicates that the size of mining companies in Southeast Asia, measured by total assets, significantly affects firm performance with a probability value of 0.0013, which is less than the significance level of 0.05. The size of a company reflects its ability to generate profits, and larger companies tend to have greater success in obtaining f u nding. For this reason, larger companies tend to pursue higher profits as it reflects positively on their performance. These findings align with the research of Hoyt and Liebenberg (Citation2008); Gordon et al. (Citation2009); Hoyt and Liebenberg (Citation2011); Farrell & Gallagher Citation2015; Lechner and Gatzert (Citation2018), which show a positive relationship between company size and performance. However, these findings contradict those of Silwal (Citation2016), and Apriliani and Dewayanto (Citation2018), which suggest that a larger company size does not necessarily lead to better management and improved performance. Hence, the relationship between company size and performance may not be consistent across all studies.

The result of the regression analysis on international diversification and company performance was 0.7037, which is greater than 0.05. This indicates that international diversification has no significant effect on the performance of mining companies in Southeast Asia. This is because diversification can lead the company to lose focus on its main business segment, ultimately causing its performance to decline compared to companies that do not diversify. Additionally, the opportunity for success in diversification is just as likely as the risk of failure that the company may face. Therefore, companies need to increase their market share to create value for stakeholders (Amran et al., Citation2009). Clarke (Citation2004) also mentioned that diversified companies face asymmetric information problems compared to those that focus on a single country. The more geographically spread out a company becomes, the more complex it becomes, and the information asymmetry between managers and investors increases. When the international status leads to an increase in information asymmetry, managers tend to build many assets in other countries to cover up the adverse impact of their policies (Hope et al., Citation2008). To minimize risks, companies also need to make informed decisions regarding their investments.

The results of this study are consistent with those of Liebenberg & Hoyt (Citation2003); Hoyt and Liebenberg (Citation2008); Şenol et al. (Citation2017); and Jurdi and AlGhnaimat (Citation2021), all of which found that international diversification does not significantly affect company performance. However, Gao & Cho (Citation2015), Vithessonthi and Racela (Citation2016), and Agustin and Setiawan (Citation2021) argue the opposite, suggesting that international diversification enables companies to understand the global market and gain additional knowledge and information from business partners, providing easy access and innovation. The ease of access and innovation by companies expanding abroad is expected to provide opportunities for a larger market share and narrow the space for their competitors, potentially increasing sales and company performance.