Abstract

The objective of this research is to review and synthesize the existing literature on the quality of Cost Accounting Systems (CAS) by manufacturing firms. A Systematic Literature Review (SLR) approach was used by adopting (170) articles in this field published from (2015) to (2023) and obtained from the Scopus database. The research found that traditional CAS is the main determinant of manufacturing firms. Therefore, the current research focuses on the quality of CAS, the benefits of the modern quality of CAS, and the challenges and methods of practicing the quality of CAS in manufacturing firms. This review comes to the idea that implementing CAS will enhance the performance of manufacturing firms and will assist with the preparation of various financial statements and decision-making. The results of the research shed light on the importance of the skills that accountants must possess in the current era and what is the role assigned. Thus, the contribution of this research is to provide integrated knowledge about the effects of recent technology innovations on the accountant’s job and skills. Professional firms and regulators consider the findings when reporting on the adaptation of guidelines, policies, and laws for the new environment.

1. Introduction

The quality of Cost Accounting Systems (CAS) in providing information that supports managers’ decisions is a significant research question in the management accounting literature. Much research has backed the deployment of more sophisticated CAS during the past few decades by improving the data these systems give (Amicarelli et al., Citation2022; Bux & Amicarelli, Citation2022; Weber & Wiegmann, Citation2021). Similar to this, many business consultants are urging firms to implement recently developed MAS, such as ABC, and a balanced scorecard to raise the quality of the information available that improves the decision-making technique (Mainar-Causapé et al., Citation2018; Erasmus, Citation2021; Teklay et al., Citation2021). Furthermore, the literature continues to focus on whether CAS can deliver high-quality information. In addition, competition in the markets requires the adoption of modern manufacturing techniques, the rise in fixed manufacturing costs as a percentage of the total cost of the product, the intensifying competition, particularly in the low-cost markets, necessitate the use of a cost system that offers relevant information, improves adaptability, and aids in more efficient managerial and strategic control (M. Chen et al., Citation2022; Moon et al., Citation2022; Parsamehr et al., Citation2022). The modern CAS, which overcomes the limitations of the traditional CAS and offers more representative cost measurements for improved decision-making, is one of the most crucial modern CAS (Mahal & Hossain, Citation2015). The Activity-Based Costing (ABC) method has even been hailed as one of the most significant managerial advancements in the last 100 years (Parker, Citation2016). It is a method of cost management that focuses on internal cost structures to be more integrated, strategic, and sensitive to competition than the conventional methods of short-term planning, control and decision-making, and product costing (Greer, Citation2015). As efforts are made to implement new methods of allocating overhead costs while calculating the costs of products or any other cost objects, the CAS has grown into an essential tool for increasing competitiveness in manufacturing firms.

According to Perčević and Hladika (Citation2016), the modern CAS focuses on accurately allocating overhead costs to products. Activities consume resource prices and cost objects (such as goods or services) in the process of cost allocation (Mahesha, Citation2022). In actuality, this means that in the first step, resource drivers are used to allocating resource costs to various activity centers. A collection of related activities that are typically organized by function or procedure make up an activity center. The factor for estimating resource consumption by events in activity areas is the resource drivers’ group. A cost item is added to the activity cost pool for each resource type designated to an activity center. Furthermore, each activity cost pool is tracked to cost objects in the second step using an activity engine that measures activity usage by cost objects (Elshaer, Citation2022). The overall cost of a specific product can then be determined by adding the costs of all the activities related to it. According to Shields (Citation2018), Jiang (Citation2019), and Nik Abdullah et al. (Citation2022), research on cost/management accounting was the primary focus of the previous literature. The emphasis, however, moved to performance evaluation and reward. In related research, Xie (Citation2019) reviewed the major themes for the period (2015–2017). The following topics were highlighted: development and integration of management accounting and control systems, performance evaluation, and compensation and incentives. On the other hand, CAS was one of the least covered subjects.

During the last two decades, the number of publications on CAS have grown significantly. As a result, the research on the factors that influence the quality of CAS has evolved and is currently a hot topic. Numerous studies in this area emphasize the variety of topics related to CAS and recommend reviewing the most recent data and identifying new research opportunities. Few publications have comprehensively assessed previous research, and the majority of these studies concentrated on a particular topic of CAS (Elshaer, Citation2022; Farkhodovna, Citation2022). Therefore, it is evident that a comprehensive and systematic examination of the factors that influence the quality of CAS is required in order to examine the current situation of providing a review and to suggest a potential research agenda. In contrast to earlier assessments, this work is not limited to particular regions, nations, or variables. The purpose of this research is to determine whether the quality of CAS has an impact on the quality of information used to make decisions. The research innovation is in the creation of a comprehensive framework that takes into account both the efficacy of cost information and the characteristics of how cost systems are structured. As a result, our research goes beyond earlier studies that usually concentrate on particular topics of cost system design and use (Alahdal, Citation2016; Busachi et al., Citation2017; Raghavan, Citation2019). Managers need precise and timely information to make decisions for the business. Consequently, the CAS needs to be improved. Additionally, the viability of creating CAS for manufacturing firms that would accurately depict their cost centers and financial success is investigated. Additionally, since nations that have adopted a form of CAS have done so in the industrial sector, this research concentrates on CAS as a tool for budgeting and costing.

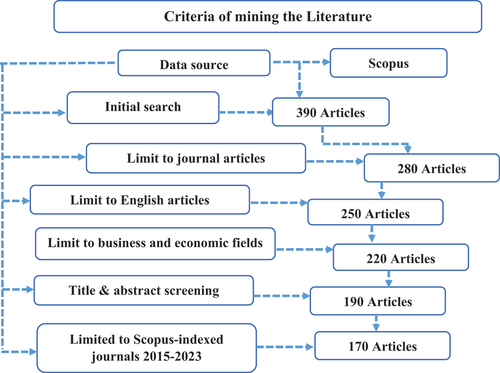

The Systematic Literature Review (SLR) on CAS seems to be helpful in this situation for addressing the ongoing issues regarding system effectiveness in manufacturing firms. In addition, to reveal the diversity of the information, SLR is useful for manufacturing firms in the different facets of research interests since it offers conceptual frameworks for comprehending the subject. In order to locate papers relevant to this review in the Scopus database, a research series was devised for this investigation containing the terms “costing systems”, “quality costing “, “Manufacturing Firms” and “costing activities.” The research was not restricted to a specific period or journal. The screening was done on the original sample of (390) articles. The final sample consists of (170) publications after the list had been trimmed down. In addition to costing systems, this research also looked at the literature theoretical frameworks, the yearly trend, and regional distribution. Given the aforementioned changes in the industrial sector in the past decades, the authors’ opinion is important to know the state of the art in the quality of CAS in a specific context—the context of manufacturing firms. And to the best of our knowledge, this is the first research to address this topic in this specific setting. To do this, the following research questions are derived:

Q1. What is the annual trend of the literature review?

Q2. What is the distribution of the earlier studies?

Q3. What are the most important findings of the studies on the quality of CAS in manufacturing firms?

Moreover, there is additional justification, as most of the previous literature focuses on individual aspects that lead to accounting reforms (De George et al., Citation2016; Grossi et al., Citation2020; Scarpellini, Citation2022). However, there are no studies examining both triggers and barriers to CAS implementation. Thus, the aim is to fill a gap in the existing literature, for theoretical development. This is the rationale for conducting this research.

Consequently, the current research seeks to add the following contributions to the existing literature.

▪ First: Provide an overview of the main studies on the CAS in manufacturing firms through SLR,with some indications for future research.

▪ Second: Exploring the impact of the quality of CAS in all developing and non-developingeconomies of the world.

▪ Third: The provide integrated knowledge about the effects of recent technology innovationson the accountants’ jobs and skills, which have not been discussed in the literature so far.

The remainder of this research is divided into the following sections. After the introduction, a section on literature is followed by a section on research techniques, which describes methods for gathering and analyzing samples. The search results are discussed in the results section. The recommendations section discusses possible research directions. The research conclusions and consequences, as well as their limitations, are discussed in the last part.

2. Background

A systematic framework used by a business to calculate the cost of its goods and measure its revenue is known as a CAS (Appelbaum et al., Citation2017; Feng et al., Citation2015). Additionally, CAS includes ABC, break-even analysis (BEA), full and variable cost analysis, variance analysis (VA), the simple cost of products sold, and inventory valuation. The pertinent literature (Antony et al., Citation2019; Noh et al., Citation2015) confirmed the value of using CAS as a database to fully understand the cost of the resources used. According to Teixeira et al. (Citation2022); Dodor and Akolgo (Citation2022), companies that use CAS effectively beat companies that don’t in terms of their ability to compete globally. In addition, markets in developing nations vary structurally from those in developed nations where the majority of earlier studies have been done. And there are few prior studies on CAS in developing nations in the literature (Gonzalez & Peña-Vinces, Citation2022), and the majority of study on these nations only focuses on financial accounting (Gao, Citation2022; He et al., Citation2022; Sadiq et al., Citation2022). The main source of information for business management, which is dependent on many strategic choices, particularly pricing, is the CAS (Hiromoto, Citation2019). Since the decision-making process has been ongoing and ingrained in the business before its founding, the inaccuracy of the information indicates that the decision is not sound. The production process is the core activity of manufacturing firms, and cost systems play a role in providing quality management information that can be relied upon to make the right decisions and cover the target period (Wang et al., Citation2018). As a result, the research sheds light on this subject, which will improve the role that cost systems play, thus the information produced will become reliable.

As a crucial first step in manufacturing finance reforms, the adoption of CAS in manufacturing firms gained traction in the late 1980s (Krishnan, Citation2023). These systems obtain unprocessed accounting service providers’ financial and human resource data and then summarize the information in cost terms using a set of predetermined cost units (Gusc et al., Citation2022). An efficient CAS can be used to determine average unit costs at the firm level, according to evidence from higher income settings (Vaughan et al., Citation2015). The resulting economic data such as the average cost per product is used to guide efforts for cost control and price setting (Kubasiewicz et al., Citation2016). In terms of data collection (scope, frequency, data sources, rules for determining cost centers, and evaluation approaches), a recent study restricted to high-income countries found substantial differences in cost accounting procedures in the industrial sector (Kihuba et al., Citation2016).

The cultures of developing economies differ from those of developed economies in terms of differences in per capita income, degree of industrialization, community attitudes and behaviors, and the living standards of economic agents (Fang et al., Citation2022; Orlando et al., Citation2022). Each of these factors affects how CAS is applied in a specific country. Therefore, economic agents in developing countries typically adhere to different accounting standards than those in developed economies. Thus, examining the impact of the quality of CAS in all developing and non-developing economies is one aspect of this research’s originality. Previous studies have used a variety of informational characteristics, including relevance and utility, as indicators of how well the quality of CAS is performing (Pedroso et al., Citation2020). Additionally, it is possible to see how well the CAS delivers high-quality data for making decisions. CAS gives managers the information they require to make choices about the launch of new goods or services, pricing, and operational redesign. It measures the extent to which managers depend on cost information when making decisions in terms of benefits (Chapman et al., Citation2021; Ren & Chen, Citation2022).

Besides the above-mentioned attributes, the quality and effectiveness of CAS have been measured in relevant research papers in terms of satisfying user needs, accuracy, comprehensiveness, and timeliness (Jansirani et al., Citation2020). More specifically, Rahmawati et al. (Citation2019) measured the use of a CAS in terms of its suitability for monitoring the organizational activities of a company, such as recognizing non-value-added activities, evaluating inventory, analyzing customer profitability, designing production and sales strategy, and so on. Further, the researchers examined how important a CAS is in price and cost reduction decisions, and it must possess a level of reliability data so that a business unit can successfully compete in the market. Additionally, the use of information technology to guarantee data collection and quality is one of the main factors that determine how they will be implemented the CAS to guarantee cost centers are found for all of the business’s goods (Alsharari, Citation2022).

Contrarily, CAS in manufacturing systems in low- and middle-income nations is frequently ineffective or non-existent (Kihuba et al., Citation2016). Furthermore, the absence of accurate cost and resource use data creates difficulties for costing and obscures the significance of economic factors in industrial sector decision-making (Kineber et al., Citation2023; Pokhilenko et al., Citation2023). As a result, accurate and timely economic data are crucial for managerial control processes like planning, budgeting, pricing, and performance assessment. Decision-makers can devise cost-control policies with the aid of reliable cost data.

3. Theoretical framework

Different information had been used by research to gauge the quality of CAS in manufacturing firms. First off, the relevance and usefulness of the information for making decisions can be a good indicator of the quality of CAS. As well, the degree to which a cost system provides supervisors with the required data to make decisions about the launch of new goods or services, pricing, or process reform is another indicator of the quality of this system (Rocha & Zavale, Citation2021; Tu & Huang, Citation2019). In other words, the extent to which supervisors rely on cost information while making decisions is an indicator of its usefulness (Stern & Stiglitz, Citation2021).

Previous research emphasized the relevance of the quality of CAS about the importance of the information for planning and control choices, which eventually increase the worth of the manufacturing firms (Rindfleisch, Citation2020; Al-Baghdadi et al., Citation2021; Asiaei et al., Citation2022). According to Banka et al. (Citation2022), cost systems are employed as business strategy tools. According to Hristov et al. (Citation2022), the quality of CAS in manufacturing firms can serve as a trustworthy barometer of how well the system is built to serve the strategic and operational decision demands essential for the adoption of strategic orientation. Due to more precise information on operations, support processes, and item costs, management concentrates its attention on the products and procedures that have the most potential to increase earnings. Additionally, having additional information about product costs will improve the decision-making process for product design, pricing, and promoting ongoing operational improvements (Dahmani et al., Citation2021; Rosário & Raimundo, Citation2021). Similarly, Da Silva Etges et al. (Citation2019) discovered that CAS performs better than other systems in terms of providing detail and classifying expenses to produce more pertinent and valuable data, which enhances profitability. In other words, effective cost systems appear to provide managers with worth data needed to make decisions that will improve performance.

Conventional product cost accounting techniques are based on discrete direct cost elements like labor, resources, or a residual indirect cost. The residual indirect cost is often known as the overhead is either written off as period cost (expenses) or allocated to products on an arbitrary basis (Bara et al., Citation2021; Shahzadi et al., Citation2018; Wojtowicz et al., Citation2019). The ABC system was established to determine the financial viability of the products, the most valuable customers, the value-added of the processes, and areas that require development. In other words, it examines the activities that are related to the production of a product (Teklay et al., Citation2021).

Afonso et al. (Citation2021) Claimed that the ABC system improves decision-making by removing biases from the conventional CAS and offering more representative cost measures. The ABC system has even been hailed as one of the most significant administrative advancements in the last 100 years (Larbi, Citation2021). It is a method of cost management that shifts the planning, control, and decision-making from a conventional short-term process toward a more integrated, strategic, and competitive manner of seeing internal cost structures (Duçi, Citation2021). The ABC system has been successfully employed by several businesses to alter their pricing strategy or allocate their resources more effectively. A well-designed ABC system has advantages beyond a precise grasp of costs. The ABC system motivates managers to enhance activity efficiency by eliminating activities that did not add value and focusing on the activities that are needed to achieve firm objectives (D. C. Pham, Citation2021).

While many studies have investigated the quality of CAS in the commercial sector, and public and non-profit sectors, there hasn’t been a lot of research done on manufacturing firms (M. Chen et al., Citation2022; Z. Chen et al., Citation2021). As a result, this research analyzed previous studies that related to the quality of CAS in manufacturing firms and offered some recommendations for future SLR-based studies.

4. Literature review and hypotheses development

The adoption of a contemporary CAS was found to be positively correlated with business performance in several earlier research because these techniques are used in the production process at various stages, which contributes to cost reduction, product quality improvement, and customer satisfaction (Singh & Ahuja, Citation2015). Modern CAS can give businesses a strong and unique advantage because they allow for cost-cutting while preserving quality (Chiarini & Vagnoni, Citation2015). These techniques allow businesses to perform well and gain a competitive edge. Companies are forced to use these strategies as a result of the rapid development and competitiveness in global markets, where they have turned to the best management accounting tools and approaches to assist grow their businesses and survive in the market (Saleh & Al-Nimer, Citation2022).

A study was conducted by Jadid (Citation2015) on Syrian oil companies to investigate how the costing method affected the performance and to clarify the significance, goals, and potential contribution of the CAS to control. The study is predicated on the suppositions that the deployment of the created CAS permits the evaluation of performance objectives and that it may effectively control the costs of oil production. The study found that the reality of the cost of the applied company system does not keep pace with the modern manufacturing environment, and a modern CAS can be applied to achieve good control over and provide information that enables performance evaluation compared to the actual outline.

Elagili (Citation2015) looked at how the CAS affected the management and financial choices made by Sudanese manufacturing companies. The study highlighted the issue of using actual expenses to measure the operational efficiency of manufacturing operations in the majority of Sudanese manufacturing companies, which makes it impossible to appropriately assess performance. Thus, a contemporary CAS is required to use the actual and planned data to monitor and assess performance. The purpose of the study was to provide insight into the value of the CAS, the effects of its implementation on the control process, and the effects of these factors on the rationalization of financial decisions in manufacturing firms.

Ahmad (Citation2018) studied the CAS and its role in cost control in manufacturing firms in Sudan. The problem of the study is the inability of grain mills to control costs under the complex economic, environmental, and manufacturing conditions in Sudan. Therefore, the study aimed to identify the extent to which the CAS is used in grain mills in Sudan, shed light on the obstacles to using this system, study the ability of grain companies to set accurate standards based on scientific principles of costs, and explain the effect of using the CAS on the efficiency and quality of cost control. The study hypothesized that there was a statistically significant correlation between the efficacy of cost control in Sudanese grain mills and the use of CAS. And the results showed that there is a statistically significant correlation between the profitability of Sudanese grain mills and the use of the CAS. The study came to several conclusions, the most significant of which is that the quality of cost control is determined by how well the CAS is applied and that the CAS aids management in focusing on problems and pinpointing their root causes.

According to experts in the field of accounting cost, firms should train their employees to become more specialized. The justification for this notion is that appropriately trained personnel are more likely to minimize negative operational impacts while costing projects (Al-Swidi et al., Citation2021). Employees must be familiar with the procedures associated with various CAS in order to use them efficiently and address any problems that might occur (Ellway & Walsham, Citation2015).

Other studies were summarized in () based on the basic information about the research, which includes the following: (1) author(s), (2) publication year, (3) paper topic, (4) the number of citations, and (5) paper results.

Table 1. Summary of different papers related to the CAS in manufacturing firms

Accordingly, the following hypotheses were proposed to be verified by the results of previous studies:

H1:

Implementing CAS may enhance the performance of manufacturing firms.

H2:

CAS may assist with the preparation of various financial statements, decision-making, budgeting for the future, and providing cost data that helps more in determining product prices.

H3:

Implementing the modern CAS has an important role in the functions and skills of the accountant.

H4:

CAS may face several difficulties, e.g. the CAS cannot reflect the current situation of the firm.

5. Methodology

5.1. Research design

This research presents SLR on the current state of research associated with the quality of CAS in manufacturing firms. Research in managerial accounting and economics frequently employs the SLR approach (Zakrzewska-Bielawska et al., Citation2022). A SLR may offer more objective conclusions compared to a regular review (Hazaea et al., Citation2022). Results that are subjective and biased may be lessened, and the inquiry status may be improved SLR (Khatib et al., Citation2022; Massaro et al., Citation2016). As a result, the SLR approach and the Scopus database were both used in this research. Utilizing Scopus, the largest abstract indexing database, prohibited us from skipping or excluding significant papers from our inquiry (Abbas et al., Citation2020; Abbas, Jusoh, et al., Citation2022; Abbas, Qureshi, et al., Citation2022; Hatzijordanou et al., Citation2019; Khatib et al., Citation2021). Additionally, this database contains data on a wide range of topics and has sophisticated search capabilities that help academics create search strings that yield trustworthy results, especially in broad fields like management accounting and economics (Ascani et al., Citation2021; Kroon et al., Citation2021).

The literature was searched using several keywords associated with the quality of CAS employed by manufacturing firms. Along with the keywords, a search for synonyms of the primary ideas was done to cover a wide range of potentially relevant terms. The final search string utilized in this research includes the terms “cost systems”, “Quality of cost systems*”, “managerial accounting”, “cost accounting*” cost accounting system “AND “Industrial companies*”, “Industrial sector*”, “manufacturing firms *” OR “activity-based costing”. All of the word derivatives were searched for using asterisks, such as those in “cost*”. These terms have been used in a number of earlier studies on management accounting and manufacturing firms (Al-Baghdadi et al., Citation2021; Saleh & Al-Nimer, Citation2022).

5.2. Article collection

() displays the inclusion and exclusion standards used to search the literature in the Scopus database. For the initial sample, a search of the research titles and abstracts using the aforementioned keywords produced (390) articles. Given the aim of comprehensively analyzing the development of the topic and incorporating a wide range of publications from the field of this research. Due to the researcher’s linguistic competence, publications that were not published in English or included in journals were excluded. The sample was reduced to (220) publications after deleting works that did not deal with business, management accounting, cost systems, or economics. The quality of CAS used by manufacturing firms must be addressed in each research for it to be included in this examination. Selected research papers were either:

Figure 1. The flowchart shows how samples are collected.

Archives: which provides a review related to the impact of the CAS in manufacturing firms as main content (including a literature review).

Behavioral: which uses empirical or observational methods to identify and analyze specific issues related to the impact of modern CAS on accountants’ roles and skills (including case studies, surveys, interviews, and empirical).

Concepts: which provide a discussion of challenges, issues, or trends related to the effects of recent technical innovations on the functions and skills of the accountant, which have not been discussed much in the literature so far.

The extensive search string used in this research led to the exclusion of many papers, which were then reviewed by looking at the sample titles and abstracts. After being screened, (190) articles that dealt with the subject of the research were found.

Following several SLRs (Farah et al., Citation2021; Mahdi Sahi et al., Citation2022), only journals included in the academic directory Scopus-indexed journals 2015–2023 made up the research sample. By solely taking into account publications from prestigious journals, we aimed to base our rating on the most thorough and significant research. Hladika (Citation2022) focused on journals in the first quartile (Q1) while (M. Chen et al., Citation2022) concentrated on ABS-rated journals. Following the quality assessment, 20 papers were eliminated, leaving (170) studies in excellent publications, as shown in () .

5.3. Quantitative analysis of selected literature

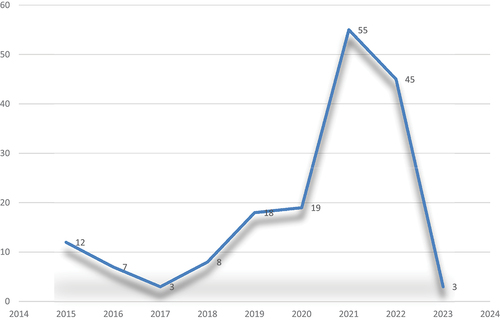

According to (), the annual publishing trend shows that interest in this topic has increased over time. The significance of a survey is highlighted by the fact that more than (72%) of the papers in this research date from the most recent time quantile, 2015–2023. After 2020, the quantity of research increased significantly. The advancement of technology and legislation are two potential practical drivers for this rise. The technological revolution has affected how manufacturing firms’ business and process information is presented, in addition to changing the public’s mindset. The COVID-19 pandemic brought environmental problems to the forefront of academics’ attention. In 2020, (19) papers were published which is the largest number of publications in recent years. Concerns have also been raised about the effects of COVID-19 on the economy. Velayutham et al. (Citation2021) for instance, examined how COVID-19 affects supply networks and how accounting data may be utilized to confront the interruptions. They found that COVID-19 affected production. By giving managers accurate accounting information at every step of the supply chain, such interruptions may be avoided. This accounting data may also be helpful to external stakeholders to lower the risks.

Figure 2. Publication trend of prior studies.

5.4. Geographical distribution analysis of selected literature

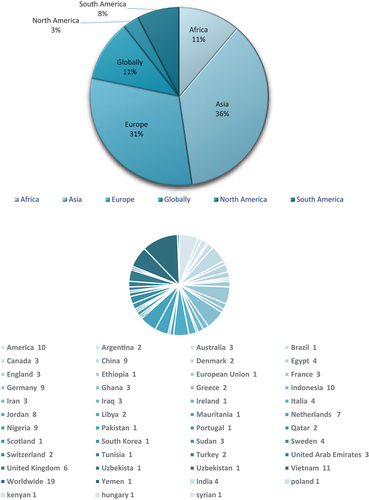

The analysis of geographical distribution showed that the majority of earlier investigations were carried out in developed nations. Data from advanced economies, like the US and the UK, were more prevalent there, as shown in (). Cost accounting methods have recently been mandated for use in the industrial sector of developing and transitional economies all over the world.

Figure 3. Geographical distribution analysis of selected literature.

Overall, 44% of the empirical publications in the sample were supported by data from a cross-country sample group. Only one cross-country research was done on the African market, with Asian and European companies receiving the majority of the attention (Bai et al., Citation2018). A larger cross-country comparative investigation of these systems was conducted in this research including Asia, Africa, Europe, South America, and North America. However, there no research has been research on Latin America to the best of our knowledge. The results of this research shed light on how economic policy, regulatory and legal restrictions, and the size of economies affect detection attempts when using a modern CAS, which may differ by country. Accounting methods (e.g., applicable cost systems) may differ not only across countries but also within countries (Bai et al., Citation2018; Raimo et al., Citation2021). Therefore, the quality of CAS is revealed to provide reliable information to stakeholders for decision-making. The results of the analysis according to () indicate that Africa included 19 articles, Asia 62 articles, Europe 52 articles, North America 5 articles, and South America 13 articles. In addition, the studies that were applied to all countries globally amounted to 19 articles.

6. Presentation and synthesis of the extracted findings

6.1. Cost accounting systems in manufacturing firms

Cost accounting, one area of accounting that had previously been employed primarily by the corporate sector, has recently undergone many improvements because of the attention of academics, and it is commonly used in the industrial sector (Alahdal, Citation2016). Some public sector businesses are gradually adopting cost accounting (Carlsson‐wall et al., Citation2022). The management community became aware of the growing worldwide competition among private firms (Aguinis et al., Citation2020; Azimovna et al., Citation2022). It is necessary to keep production costs under control for a firm to compete with other entities doing business in the same industry. This information was mentioned earlier (A. Sharma et al., Citation2021; Alvarez et al., Citation2021; Nani & Safitri, Citation2021).

It has been criticized that the standard architecture of CAS establishes a separation between fixed and variable costs (Da Silva Stefano et al., Citation2022; M. Chen et al., Citation2022). Assisting the management of the business in performing its different planning, control, and decision-making functions when it requires accurate, timely, and reliable cost information is the goal of the CAS (Asiaei et al., Citation2022; Ren & Chen, Citation2022; Yang et al., Citation2022). The CAS is a crucial resource for many administrative choices, including those involving pricing, determining the best product mix, measuring operational costs for the business, and ultimately assessing performance (Jahani et al., Citation2021; Paustian et al., Citation2019).

There is no doubt that the existence of CAS is necessary to provide suitable information to make judgments. However, with the amazing development of accounting systems, the decision-maker is no longer constrained by a lack of information (Biraro et al., Citation2021; Flayyih et al., Citation2021). In addition, there is an enormous of information that needs to be categorized and tabulated, which is the main issue. To make the best administrative judgments, the proper information must be chosen for the appropriate decision to make and assess the trade-offs of the numerous accessible options (Alahdal, Citation2016; Rahmawati et al., Citation2019).

6.2. Cost management practice in manufacturing firms

The practice of cost management involves properly classifying and dividing costs in order to determine the final price of the goods and services provided by the industrial unit. It also involves appropriately adjusting and providing pertinent information so that managers and business owners use it to guide the unit operations (Erasmus, Citation2021; Vallecillo et al., Citation2019). Additionally, costing is the process of calculating the expenses associated with each component of production or service (Busachi et al., Citation2017). Each product’s profit is determined by the difference between its sale price and its overall production costs (Palulun et al., Citation2021; Sarkar et al., Citation2022). In addition, the most important main rules of CAS are recording, classifying, and summarizing expenses to calculate the firm’s costs and profits. Also, to manage the firm’s finances and make informed decisions about where to allocate resources. CAS is essential for firms because it allows for accurate financial planning and management (Jansirani et al., Citation2020).

Cost is therefore very important to the product’s design and profitability (Shaturaev, Citation2022). For the project to be successful, the product must be manufactured according to the required processes in the first degree and be possible within the initial cost estimates in the second degree (Oluyisola et al., Citation2022; Pan & Zhang, Citation2021; Stauder & Kühl, Citation2022). There is now a lack of accurate and adequate costing systems because of the rapid expansion of information technology (Erasmus, Citation2021; Heidari et al., Citation2022). Therefore, it appears that a comprehensive costing information system is required.

6.3. Disadvantages of cost accounting systems

The term “cost accounting system” refers to the process of documenting transactions involving expenses paid and income received by a firm. This system also assists with the preparation of various financial statements and cost management (Nani & Safitri, Citation2021). Thus, this area of accounting helps managers adopt firm plans that are focused on efficiency and cost (Setyowati et al., Citation2021). However, the CAS faces several difficulties. For example, all of the recorded data is a historical analysis of recent transactions; the CAS cannot reflect the current situation of the firm (Yildiz & Ahi, Citation2022). Particularly considering that firm records serve as the foundation for the decision-making process. Therefore, based on the above discussion, the decision is to accept H4.

Moreover, several factors contribute to the constant variation in the price of raw materials, and other commodities (Rodrigue & Picard, Citation2022). These variations in cost are caused by a variety of factors, including economic and governmental regulations. The CAS is a complicated procedure. Without learning the procedures of it, a person cannot easily comprehend the process. Even for specialists, determining the accurate cost might be challenging at times (Walz & Guenther, Citation2021).

6.4. Advantages of cost accounting systems

Cost management and determining unit costs are the primary concerns of cost accounting in the industrial sector. Cost systems have been created in particular to calculate the total cost of the production for each unit of manufacturing (Han et al., Citation2021; Lund et al., Citation2021). According to Cao et al. (Citation2021), cost accounting is a system that calculates expenses and profit, performance, assesses inventories and manages individual behavior. In 1960, managerial accounting was originally introduced in response to the need to produce accounting information for managerial decision-making, particularly for both planning and control. Managerial accounting places a strong emphasis on appreciating the appropriate cost of particular decisions (Ghandour, Citation2021; Nielsen, Citation2022).

According to Kumar et al. (Citation2022), the contemporary CAS aids managers in planning for both the immediate and long-term future. Additionally, the CAS is essential for enhancing private-sector financial management (Raimo et al., Citation2021; Setyowati et al., Citation2021). A major result of private sector changes has been the emphasis on “service management” as opposed to “management” together with a parallel shift in emphasis from the traditional supervisory role of accounting towards cost management (Easterby-Smith et al., Citation2015; Hood & Dixon, Citation2015; Ojogiwa, Citation2021). The main purposes of CAS for the industrial sector are to improve decision-making, measure, and control performance, and help managers carry out planning and control functions (Shaqour, Citation2022). In addition, the most important characteristics of modern CAS are that it is easy to operate and easy to understand. It contributes to providing information to the management to assist in decision-making and budgeting for the future (Ren & Chen, Citation2022). It is also used in future planning and decision-making processes by the firm. Also, it contributes to providing cost data that helps more in determining product prices, and it also helps to predict the amount of time and resources wasted. Therefore, based on the above discussion, the decision is to accept H2.

6.5. Benefits of cost accounting systems

Cost accounting is now a common practice across most firms and enterprises (Dana et al., Citation2021). Most medium and large-sized businesses utilize a CAS to enrich the information provided by financial accounting (Elhossade et al., Citation2020; Lutfi et al., Citation2022; Ren & Chen, Citation2022; Salvy Goel & Berrones-Flemmig, Citation2022). In reality, the CAS is important for management, businesses, and the economy (Abou Taleb & Al Farooque, Citation2021; Hilorme et al., Citation2019 Keel et al., Citation2017). A CAS records how a firm interacts with its revenues and expenses to produce different financial statements and control costs (Chichan et al., Citation2021; Luo, Citation2021). A sound, effective CAS aids in discovering any unproductive activities, losses, or inefficiencies (Epelle & Gerogiorgis, Citation2020). In order to achieve the goal of the economy in a firm’s operations, cost reduction strategies, operations research techniques, and value analysis techniques are applied (Goli & Mohammadi, Citation2022; Grover et al., Citation2020). Manufacturing firms are making ongoing efforts to identify fresh and better ways to reduce costs (Azizi et al., Citation2021). CAS is also helpful for pinpointing the precise reasons behind changes in a firm profit or loss (Tran & Tran, Citation2022; Zhang, Citation2021). Additionally, it aids in identifying underperforming items or product lines so it can be discontinued, or substitute actions can be done.

Additionally, it gives management information and statistics to use as a reference for making financial decisions (Donthu et al., Citation2021; Huy & Hang, Citation2021; Tuffour et al., Citation2022). The CAS can also offer advice on a wide range of issues, including purchasing products, accepting orders that are below cost, and choosing a machine to buy from a variety of options. CAS is also very helpful for determining prices. It acts as a benchmark for measuring the suitability of selling prices. The computed price could help create estimates (Palo et al., Citation2020). According to Choong and Islam (Citation2020), the application of the variance analysis cost accounting technique identifies deviations from the pre-determined level and the appropriate action to eliminate such deviations in the future. CAS comparison also aids in cost management. Such a comparison can be done over time utilizing data from the same unit of businesses or many units within a single industry using approaches like uniform costing and inter-firm comparison (Reklitis et al., Citation2021; Veile et al., Citation2019). It is possible to compare the costs of jobs, processes, or cost centers. Additionally, a system of costing gives results that can be used by the government, wage tribunals, and other authorities to address different issues. Pricing fixation, price regulation, tariff protection, and pay level fixation are a few examples of these issues (Hofmarcher et al., Citation2020).

6.6. The importance of training employees on modern cost accounting systems

The training has been conceptualized from a variety of perspectives. For example, Van der Steen (Citation2022) defines it as a process that contributes to developing the capabilities and knowledge necessary for employees, in order to implement the various activities that serve the firm management. In other words, training equips workers with the skills that are necessary to perform their tasks more effectively. It is a costly but essential issue that will help firms become more productive and effective (Sal & Raja, Citation2016). Similar to this, staff members in Borshalina (Citation2021) research stated that training in the operation of modern CAS helped to be more confident and reduced errors.

According to experts in the field of accounting cost, firms should educate their employees to become more specialized. The justification for this notion is that appropriately trained personnel are more likely to minimize negative operational impacts while costing projects (Al-Swidi et al., Citation2021). Employees must be familiar with the procedures associated with various CAS in order to use them efficiently and address any problems that might occur (Ellway & Walsham, Citation2015). Training gives participants the skills necessary to apply real fix the issues they meet on the ground. Therefore, based on the above results, the decision is to accept H3.

According to Austin-Egole et al. (Citation2020), training contributes to raising employee motivation levels and organizational profitability. Additionally, it decreases the levels of stress and absenteeism. Similar to this, training decreases costs (work satisfaction, and loyalty to the business), and promotes knowledge transfer (Woldman et al., Citation2018). In conclusion, training enhances work performance and has a beneficial impact on production levels, user satisfaction, and decision-making that is appropriate for the firm needs (N. T. Pham et al., Citation2020). Jasim and Raewf (Citation2020) contend that manufacturing firms should allocate a portion of their revenues toward the creation of accounting software, the improvement of human resources, and the instruction of accountants in cost accounting methods.

7. Discussion and conclusion

Investigation into the quality of CAS has revealed several issues that require further research. The majority of studies about the quality of CAS focused on commercial firms (e.g., Dutta et al., Citation2021). That assessment indicates that several challenges and implications of the quality of CAS in manufacturing firms require further research. Some of these directions are outlined as follows. Sometimes researchers can’t access the data from underdeveloped countries because many annual reports are not available in English (Gligor et al., Citation2018; Omar & Inaba, Citation2020). However, since businesses now publish their annual reports in English, more essential data is now more readily available. Therefore, the research conducted in emerging markets and cross-country research should be increased. In order to account for differences in accounting, cultural, economic, legal, and political systems, most research chooses to collect data from one country. In terms of the presence of specific information, the computation of variance, and the frequency of reporting, the structure of the CAS has an impact on the relevance, correctness, timeliness, usability, compatibility, reliability, and accuracy of the information for decision-making (Chapman et al., Citation2021; Ren & Chen, Citation2022). Furthermore, it was found that cost analysis by cost center, product, and activity had a negative impact on the utility of cost information, which was unexpected. It can be inferred that a CAS that analyzes data using broad nature criteria, including cost centers, products, and activities, may not always give accurate data for decision-making that serves several purposes, such as carrying out a range of administrative tasks.

Overall, the consensus supports the theoretical assertion made in the management accounting literature that more functional CAS yields higher-quality information. For example, Jansirani et al. (Citation2020); R. Sharma and Villányi (Citation2022); Ifada and Saleh (Citation2022) all concurred that cost systems that provide exact information and more clearly define expenses have useable data and eventually help managers make decisions that would increase performance. Therefore, based on all the above results and discussion, the decision is to accept H1. The projected impact of decisions based on aggregate information is reportedly less than that of decisions based on specific information, according to (Ulfert et al., Citation2022). In the same vein, Lutfi (Citation2022) asserted that the opinions about the quality of CAS could serve as a reliable gauge of how well the system is crafted to support decision-making. Elagili (Citation2015) and Almatarneh et al. (Citation2022) emphasize the need of using CAS that provides helpful information for making planning and control decisions. Additionally, there are strong relationships between the fundamental dimension of the structure of CAS (Asiaei et al., Citation2022; Hamza et al., Citation2021; Jadid, Citation2015). This shows that although the CAS established in practice may adopt different forms their fundamental dimensions are internally consistent. As a result, each cost information quality level reveals a distinct aspect of how valuable cost information is for making decisions. However, has a significant correlation with the other quality criteria that any CAS must provide. In the same vein, the majority of the research supported the idea that businesses should allocate a portion of their profits to the creation of programs for human resources and accounting systems as well as the education of accountants on key accounting software in order to maximize the use of these systems within the business and boost performance (Al-Swidi et al., Citation2021; Jasim & Raewf, Citation2020; Sal & Raja, Citation2016).

The current research in the area of accounting information systems offers insightful information about the broad effects of control in CAS at different economic levels. Nevertheless, despite growing interest in CAS, there hasn’t been much research done on its use by manufacturing firms. The SLR approach used resulted in a final sample of (170) publications on CAS. The initiatives to disclose the quality of CAS are effective if the results of these many areas are systematically analyzed.

The research conclusions of the research have important Practical and theoretical implications. First, the research offers a comprehensive model that incorporates several facets of CAS design and application. This discussed model is applied in manufacturing firms. The model can nevertheless be simply applied to various industries because of its generality. Second, the research shows it is very important for a manager to have access to sophisticated cost information when making decisions, but at the same time, the design of cost systems was discovered to be a significant explanatory element the quality of CAS. Third, the research shows that training employees to operate a modern CAS helped increase confidence and reduce errors. Therefore, these findings might make technical cost system designers more aware of the beneficial dimensions of information. Additionally, the instruments of information quality investigated in this research may be a good starting point for monitoring and assessing the level of user satisfaction with the firm’s CAS. Such an assessment might also be carried out as part of a post-implementation review. The goal may be to pinpoint the areas within that scope that need to be improved in upcoming system development initiatives. The practical contribution of this research lies in providing an integrated understanding of the effects of recent technological developments on the accountant’s role and skills, which have been discussed far in the current research.

Future studies may be focused on helpful areas, as suggested by the results discussed above. The research restriction to manufacturing firms only makes it difficult to extrapolate the findings to other sectors of the economy. However, for the conclusions to be more broadly general, the research needs to be replicated in other economic areas. Finally, the research approach has relied on perceptual measurements of the cost system structure and information quality. Future studies could look at how cost system design decisions affect quantitative business performance indicators like profitability and cost structure. A crucial issue that could prompt a more thorough investigation into the components of comprehensive cost information that are associated with relevance improvement is the unexpectedly negative trend in the association between the level of detail in cost accounting information and relevance. In addition, more research is required on the competencies, skills, and roles that management accountants must play in order to improve the quality of cost accounting and reporting systems, and thus promote their adoption.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Qais Yaser Saleh

Qais Yaser Saleh Accounting Department, Business school, The Hashemite University, Zarqa, Jordan

References

- Abbas, A. F., Jusoh, A. B., Mas’od, A., & Ali, J. (2020). Bibliometric analysis of global research trends on electronic word of mouth using Scopus database. Journal of Critical Reviews, 7(16), 405–24.

- Abbas, A. F., Jusoh, A., Mas’od, A., Alsharif, A. H., Ali, J., & Tan, A. W. K. (2022). Bibliometrix analysis of information sharing in social media. Cogent Business & Management, 9(1), 1–23. https://doi.org/10.1080/23311975.2021.2016556

- Abbas, A. F., Qureshi, N. A., Khan, N., Chandio, R., & Ali, J. (2022). The blockchain technologies in healthcare: Prospects, obstacles, and future recommendations; lessons learned from digitalization. International Journal of Online and Biomedical Engineering (IJOE), 18(9), 144–159. https://doi.org/10.3991/ijoe.v18i09.32253

- Abou Taleb, M., & Al Farooque, O. (2021). Towards a circular economy for sustainable development: An application of full cost accounting to municipal waste recyclables. Journal of Cleaner Production, 280, 124047.. https://doi.org/10.1016/j.jclepro.2020.124047

- Afonso, P., Vyas, V., Antunes, A., Silva, S., & Bret, B. P. (2021). A Stochastic Approach for Product Costing in Manufacturing Processes. Mathematics, 9(18), 2238.. https://doi.org/10.3390/math9182238

- Aguinis, H., Villamor, I., Lazzarini, S. G., Vassolo, R. S., Amorós, J. E., & Allen, D. G. (2020). Conducting management research in Latin America: Why and what’s in it for you? Journal of Management, 46(5), 615–636.. https://doi.org/10.1177/0149206320901581

- Ahmad, M. (2018). The standard costs system and its role in cost control. Unpublished doctoral dissertation, Shendi University, Graduate School.

- Alahdal, W. M. (2016). The role of cost accounting system in the pricing decision-making in industrial companies of Taiz city, Yemen. International Academic Journal of Accounting and Financial Management, 3(7), 70–78.. https://doi.org/10.17323/1998-0663.2016.4.70.78

- Al-Baghdadi, E. N., Alrub, A. A., & Rjoub, H. (2021). Sustainable Business Model and Corporate Performance: The Mediating Role of Sustainable Orientation and Management Accounting Control in the United Arab Emirates. Sustainability, 13(16), 8947.. https://doi.org/10.3390/su13168947

- Almatarneh, Z., Jarah, B., & Jarrah, M. (2022). The role of management accounting in the development of supply chain performance in logistics manufacturing companies. Uncertain Supply Chain Management, 10(1), 13–18.. https://doi.org/10.5267/j.uscm.2021.10.015

- Alsharari, N. (2022). the Implementation of Enterprise Resource Planning (Erp) in the United Arab Emirates: A Case of Musanada Corporation. International Journal of Technology, Innovation and Management (IJTIM), 2(1), 1–22. https://doi.org/10.54489/ijtim.v2i1.57

- Al-Swidi, A. K., Gelaidan, H. M., & Saleh, R. M. (2021). The joint impact of green human resource management, leadership and organizational culture on employees’ green behaviour and organisational environmental performance. Journal of Cleaner Production, 316, 128112.. https://doi.org/10.1016/j.jclepro.2021.128112

- Alvarez, T., Sensini, L., Bello, C., & Vazquez, M. (2021). Management accounting practices and performance of SMEs in the Hotel industry: Evidence from an emerging economy. International Journal of Business and Social Science, 12(2), 24–35..

- Amicarelli, V., Roe, B. E., & Bux, C. (2022). Measuring Food Loss and Waste Costs in the Italian Potato Chip Industry Using Material Flow Cost Accounting. Agriculture, 12(4), 523.. https://doi.org/10.3390/agriculture12040523

- Antony, J., Sunder, M. V., Sreedharan, R., Chakraborty, A., & Gunasekaran, A. (2019). A systematic review of Lean in healthcare: A global prospective. International Journal of Quality & Reliability Management, 36(8), 1370–1391.. https://doi.org/10.1108/IJQRM-12-2018-0346

- Appelbaum, D., Kogan, A., Vasarhelyi, M., & Yan, Z. (2017). Impact of business analytics and enterprise systems on managerial accounting. International Journal of Accounting Information Systems, 25, 29–44.. https://doi.org/10.1016/j.accinf.2017.03.003

- Ascani, I., Ciccola, R., & Chiucchi, M. S. (2021). A structured literature review about the role of management accountants in sustainability accounting and reporting. Sustainability, 13(4), 2357.. https://doi.org/10.3390/su13042357

- Asiaei, K., Bontis, N., Alizadeh, R., & Yaghoubi, M. (2022). Green intellectual capital and environmental management accounting: Natural resource orchestration in favor of environmental performance. Business Strategy and the Environment, 31(1), 76–93.. https://doi.org/10.1002/bse.2875

- Austin-Egole, I. S., Iheriohanma, E. B. J., & Nwokorie, C. (2020). Flexible working arrangements and organizational performance: An overview. IOSR Journal of Humanities and Social Science (IOSR-JHSS), 25(5), 50–59..

- Azimovna, M. S., Ilkhomovna, U. D., & Shokhrukhovich, U. F. (2022). Innovative Strategies of Tourism Development in Uzbekistan. European Journal of Innovation in Nonformal Education, 2(1), 1–4..

- Azizi, M. R., Atlasi, R., Ziapour, A., Abbas, J., & Naemi, R. (2021). Innovative human resource management strategies during the COVID-19 pandemic: A systematic narrative review approach. Heliyon, 7(6), e07233.. https://doi.org/10.1016/j.heliyon.2021.e07233

- Bai, R., Lam, J. C., & Li, V. O. (2018). A review on health cost accounting of air pollution in China. Environment International, 120, 279–294.. https://doi.org/10.1016/j.envint.2018.08.001

- Banka, M., Tien, N. H., Dao, M. T. H., & Minh, D. T. (2022). Analysis of business strategy of real estate developers in Vietnam: The application of QSPM matrix. International Journal of Multidisciplinary Research and Growth Evaluation, 3(1), 188–196..

- Bara, N., Gautier, F., & Giard, V. (2021). An economic evaluation of operational decisions–an application in scheduling evaluation in fertilizer plants. Production Planning & Control, 32(9), 699–714.. https://doi.org/10.1080/09537287.2020.1751891

- Biraro, M., Zevenbergen, J., & Alemie, B. K. (2021). Good practices in updating land information systems that used unconventional approaches in systematic land registration. Land, 10(4), 437.. https://doi.org/10.3390/land10040437

- Borshalina, T. (2021). Indonesia of Batik Trusmi MSMEs: The Effect of User Technology Capability on Individual Performance with the Accounting Information Systems Effectiveness. Turkish Journal of Computer and Mathematics Education (TURCOMAT), 12(2), 1304–1312.. https://doi.org/10.17762/turcomat.v12i2.1211

- Busachi, A., Erkoyuncu, J., Colegrove, P., Martina, F., Watts, C., & Drake, R. (2017). A review of Additive manufacturing technology and Cost Estimation techniques for the defense sector. CIRP Journal of Manufacturing Science and Technology, 19, 117–128.. https://doi.org/10.1016/j.cirpj.2017.07.001

- Bux, C., & Amicarelli, V. (2022). Material flow cost accounting (MFCA) to enhance environmental entrepreneurship in the meat sector: Challenges and opportunities. Journal of Environmental Management, 313, 115001. https://doi.org/10.1016/j.jenvman.2022.115001

- Cao, M. M., Nguyen, N. T., & Tran, T. T. (2021). Behavioral factors on individual investors’ decision making and investment performance: A survey from the Vietnam Stock Market. The Journal of Asian Finance, Economics and Business, 8(3), 845–853..

- Carlsson‐wall, M., Goretzki, L., Hofstedt, J., Kraus, K., & Nilsson, C. J. (2022). Exploring the implications of cloud‐based enterprise resource planning systems for public sector management accountants. Financial Accountability & Management, 38(2), 177–201.. https://doi.org/10.1111/faam.12300

- Chapman, C. S., Kern, A., Laguecir, A., Doyle, G., Angelé-Halgand, N., Hansen, A., Hartmann, F. G. H., Mateus, C., Perego, P., Winter, V., & Quentin, W. (2021). Managing quality of cost information in clinical costing: Evidence across seven countries. Journal of Public Budgeting, Accounting & Financial Management, 34(2), 1–39. https://doi.org/10.1108/JPBAFM-09-2020-0155

- Chen, M., Liu, Q., Huang, S., & Dang, C. (2022). Environmental cost control system of manufacturing enterprises using artificial intelligence based on value chain of circular economy. Enterprise Information Systems, 16(8–9), 1856422.. https://doi.org/10.1080/17517575.2020.1856422

- Chen, Z., Zhang, X., & Chen, F. (2021). Do carbon emission trading schemes stimulate green innovation in enterprises? Evidence from China. Technological Forecasting and Social Change, 168, 120744.. https://doi.org/10.1016/j.techfore.2021.120744

- Chiarini, A., & Vagnoni, E. (2015). World-class manufacturing by Fiat. Comparison with Toyota production system from a strategic management, management accounting, operations management and performance measurement dimension. International Journal of Production Research, 53(2), 590–606.. https://doi.org/10.1080/00207543.2014.958596

- Chichan, H. F., Alabdullah, T. T. Y., & Tawfeeq Yousif Alabdullah, T. (2021). Does environmental management accounting matter in promoting sustainable development? A study in Iraq. Journal of Accounting Science, 5(2), 110–122.. https://doi.org/10.21070/jas.v5i2.1543

- Choong, K. K., & Islam, S. M. (2020). A new approach to performance measurement using standards: A case of translating strategy to operations. Operations Management Research, 13(3–4), 137–170.. https://doi.org/10.1007/s12063-020-00159-8

- Dahmani, N., Benhida, K., Belhadi, A., Kamble, S., Elfezazi, S., & Jauhar, S. K. (2021). Smart circular product design strategies towards eco-effective production systems: A lean eco-design industry 4.0 framework. Journal of Cleaner Production, 320, 128847.. https://doi.org/10.1016/j.jclepro.2021.128847

- Dana, L. P., Rounaghi, M. M., & Enayati, G. (2021). Increasing productivity and sustainability of corporate performance by using management control systems and intellectual capital accounting approach. Green Finance, 3(1), 1–14.. https://doi.org/10.3934/GF.2021001

- Da Silva Etges, A. P. B., Cruz, L. N., Notti, R. K., Neyeloff, J. L., Schlatter, R. P., Astigarraga, C. C., Falavigna, M., & Polanczyk, C. A. (2019). An 8-step framework for implementing time-driven activity-based costing in healthcare studies. The European Journal of Health Economics, 20(8), 1133–1145.. https://doi.org/10.1007/s10198-019-01085-8

- Da Silva Stefano, G., dos Santos Antunes, T., Lacerda, D. P., Morandi, M. I. W. M., & Piran, F. S. (2022). The impacts of inventory in transfer pricing and net income: Differences between traditional accounting and throughput accounting. The British Accounting Review, 54(2), 101001.. https://doi.org/10.1016/j.bar.2021.101001

- De George, E. T., Li, X., & Shivakumar, L. (2016). A review of the IFRS adoption literature. Review of Accounting Studies, 21(3), 898–1004.. https://doi.org/10.1007/s11142-016-9363-1

- Dodor, A., & Akolgo, I. G. (2022). Gaining Competitive Edge with a Comprehension of Complex System of Self-Organized Startup Businesses. Open Journal of Business and Management, 10(5), 2553–2577.. https://doi.org/10.4236/ojbm.2022.105127

- Donthu, N., Kumar, S., Pandey, N., & Gupta, P. (2021). Forty years of the International Journal of Information Management: A bibliometric analysis. International Journal of Information Management, 57, 102307.. https://doi.org/10.1016/j.ijinfomgt.2020.102307

- Duçi, E. (2021). The relationship between management accounting, strategic management accounting and strategic cost management. Academic Journal of Interdisciplinary Studies, 10(5), 376. https://doi.org/10.36941/ajis-2021-0146

- Dutta, G., Kumar, R., Sindhwani, R., & Singh, R. K. (2021). Digitalization priorities of quality control processes for SMEs: A conceptual study in perspective of Industry 4.0 adoption. Journal of Intelligent Manufacturing, 32(6), 1679–1698.. https://doi.org/10.1007/s10845-021-01783-2

- Easterby-Smith, M., Thorpe, R., & Jackson, P. R. (2015). Management and Business Research (Fifth ed.). SAGE Publications Ltd.

- Elagili, G. (2015). Adoption factors for the implementation of activity based costing systems: A case study of the Libyan cement industry. Unpublished doctoral dissertation, University of Salford (United Kingdom).

- Elhossade, S. S., Abdo, H., & Mas’ud, A. (2020). Impact of institutional and contingent factors on adopting environmental management accounting systems: The case of manufacturing companies in Libya. Journal of Financial Reporting and Accounting, 1–46.

- Ellway, B. P., & Walsham, G. (2015). A doxa‐informed practice analysis: Reflexivity and representations, technology and action. Information Systems Journal, 25(2), 133–160.. https://doi.org/10.1111/isj.12041

- Elshaer, A. M. (2022). Analysis of restaurants’ operations using time-driven activity-based costing (TDABC): Case study. Journal of Quality Assurance in Hospitality & Tourism, 23(1), 32–55.. https://doi.org/10.1080/1528008X.2020.1848745

- Epelle, E. I., & Gerogiorgis, D. I. (2020). A review of technological advances and open challenges for oil and gas drilling systems engineering. AIChE Journal, 66(4), e16842.. https://doi.org/10.1002/aic.16842

- Erasmus, E. G. (2021). Cost Management Practice and Financial Performance of Listed Deposit Money Banks in Nigeria. Journal of Accounting and Financial Management, 7(2), 1–14..

- Fang, W., Liu, Z., & Putra, A. R. S. (2022). Role of research and development in green economic growth through renewable energy development: Empirical evidence from South Asia. Renewable Energy, 194, 1142–1152.. https://doi.org/10.1016/j.renene.2022.04.125

- Farah, B., Elias, R., Aguilera, R., & Abi Saad, E. (2021). Corporate governance in the Middle East and North Africa: A systematic review of current trends and opportunities for future research. Corporate Governance an International Review, 29(6), 630–660. https://doi.org/10.1111/corg.12377

- Farkhodovna, I. U. (2022). Improving Cost Accounting in Energy Enterprises. Texas Journal of Multidisciplinary Studies, 9, 198–199..

- Feng, M., Li, C., McVay, S. E., & Skaife, H. (2015). Does ineffective internal control over financial reporting affect a firm’s operations? Evidence from firms’ inventory management. The Accounting Review, 90(2), 529–557.. https://doi.org/10.2308/accr-50909

- Flayyih, H. H., Mirdan, A. S., & Elkhaldi, A. H. (2021). Critical Success Factors of Strategic Accounting Information System and It’s Relation with Strategic Decisions Effectiveness. Annals of the University of Oradea, Economic Science Series, 30(30 (1)), 227–234. https://doi.org/10.47535/1991AUOES30(1)025

- Gao, J. (2022). Research on the corporate financial transformation with big data technologies. International Journal of Progressive Sciences and Technologies, 32(2), 08–12..

- Ghandour, D. (2021). Analytical Review of the Current and Future Directions of Management Accounting and Control Systems. European Journal of Accounting Auditing and Finance Research, 9(3), 42–73..

- Gligor, D., Tan, A., & Nguyen, T. N. T. (2018). The obstacles to cold chain implementation in developing countries: Insights from Vietnam. The International Journal of Logistics Management, 29(3), 942–958. https://doi.org/10.1108/IJLM-02-2017-0026

- Goli, A., & Mohammadi, H. (2022). Developing a sustainable operational management system using hybrid Shapley value and Multimoora method: Case study petrochemical supply chain. Environment, Development and Sustainability, 24(9), 10540–10569. https://doi.org/10.1007/s10668-021-01844-9

- Gonzalez, C. C., & Peña-Vinces, J. (2022). A framework for a green accounting system-exploratory study in a developing country context, Colombia. Environment, Development and Sustainability, 1–25.. https://doi.org/10.1007/s10668-022-02445-w

- Greer, W. L. (2015). An application of military cost–benefit analysis in a major defense acquisition. In Military Cost-Benefit Analysis (pp. 397–434). Routledge.

- Grossi, G., Kallio, K. M., Sargiacomo, M., & Skoog, M. (2020). Accounting, performance management systems and accountability changes in knowledge-intensive public organizations: A literature review and research agenda. Accounting, Auditing & Accountability Journal, 33(1), 256–280.. https://doi.org/10.1108/AAAJ-02-2019-3869

- Grover, P., Kar, A. K., & Dwivedi, Y. K. (2020). Understanding artificial intelligence adoption in operations management: Insights from the review of academic literature and social media discussions. Annals of Operations Research, 308(1–2), 177–213. https://doi.org/10.1007/s10479-020-03683-9

- Gusc, J., Bosma, P., Jarka, S., & Biernat-Jarka, A. (2022). The big data, artificial intelligence, and blockchain in true cost accounting for energy transition in Europe. Energies, 15(3), 1089.. https://doi.org/10.3390/en15031089

- Hamza, P. A., Hamad, H. A., Qader, K. S., Gardi, B., & Anwar, G. (2021). Management of outsourcing and its relationship with hotels’ performance: An empirical analysis of selected hotels in Erbil. International Journal of Advanced Engineering Research and Science, 8(10), 208–219. https://doi.org/10.22161/ijaers.810.24

- Han, X., Wang, Z., Xie, M., He, Y., Li, Y., & Wang, W. (2021). Remaining useful life prediction and predictive maintenance strategies for multi-state manufacturing systems considering functional dependence. Reliability Engineering & System Safety, 210, 107560.. https://doi.org/10.1016/j.ress.2021.107560

- Hatzijordanou, N., Bohn, N., & Terzidis, O. (2019). A systematic literature review on competitor analysis: Status quo and start-up specifics. Management Review Quarterly, 69(4), 415–458. https://doi.org/10.1007/s11301-019-00158-5

- Hazaea, S. A., Zhu, J., Khatib, S. F. A., Bazhair, A. H., & Elamer, A. A. (2022). Sustainability assurance practices: A systematic review and future research agenda. Environmental Science and Pollution Research, 29(4), 4843–4864. https://doi.org/10.1007/s11356-021-17359-9

- Heidari, A., Navimipour, N. J., & Unal, M. (2022). Applications of ML/DL in the management of smart cities and societies based on new trends in information technologies: A systematic literature review. Sustainable Cities and Society, 85, 104089. https://doi.org/10.1016/j.scs.2022.104089

- He, R., Luo, L., Shamsuddin, A., & Tang, Q. (2022). Corporate carbon accounting: A literature review of carbon accounting research from the Kyoto Protocol to the Paris Agreement. Accounting & Finance, 62(1), 261–298.. https://doi.org/10.1111/acfi.12789

- Hilorme, T., Perevozova, I., Shpak, L., Mokhnenko, A., & Korovchuk, Y. (2019). Human capital cost accounting in the company management system. Academy of Accounting and Financial Studies Journal, 23(2), 1–6.

- Hiromoto, T. (2019). Restoring the relevance of management accounting. In Management Control Theory (pp. 273–288). Routledge..

- Hladika, M. (2022). Use of Management Accounting Techniques in Croatian Manufacturing Companies. In Eurasian Business and Economics Perspectives: Proceedings of the 36th Eurasia Business and Economics Society Conference (pp. 187–199). Cham: Springer International Publishing. https://doi.org/10.1007/978-3-031-14395-3_10

- Hofmarcher, T., Romild, U., Spångberg, J., Persson, U., & Håkansson, A. (2020). The societal costs of problem gambling in Sweden. BioMed Central Public Health, 20(1), 1–14.. https://doi.org/10.1186/s12889-020-10008-9

- Hood, C., & Dixon, R. (2015). A government that worked better and cost less?: Evaluating three decades of reform and change in UK central Government.. Oxford University Press.

- Hristov, I., Chirico, A., & Ranalli, F. (2022). Corporate strategies oriented towards sustainable governance: Advantages, managerial practices and main challenges. Journal of Management & Governance, 26(1), 75–97.. https://doi.org/10.1007/s10997-021-09581-x

- Huy, D. T. N., & Hang, N. T. (2021). Factors that affect Stock Price and Beta CAPM of Vietnam Banks and Enhancing Management Information System–Case of Asia Commercial Bank. Revista Geintec-Gestao Inovacao E Tecnologias, 11(2), 302–308.. https://doi.org/10.47059/revistageintec.v11i2.1667

- Ifada, L. M., & Saleh, N. M. (2022). Environmental performance and environmental disclosure relationship: The moderating effects of environmental cost disclosure in emerging Asian countries. Management of Environmental Quality: An International Journal, 33(6), 1553–1571. https://doi.org/10.1108/MEQ-09-2021-0233

- Jadid, M. (2015). Measurement of standard costs system and its role in monitoring and performance evaluation in Syrian oil industry companies. Unpublished doctoral dissertation, University of Tishreen.

- Jahani, N., Sepehri, A., Vandchali, H. R., & Tirkolaee, E. B. (2021). Application of industry 4.0 in the procurement processes of supply chains: A systematic literature review. Sustainability, 13(14), 1–25. https://doi.org/10.3390/su13147520

- Jansirani, S., Purusothaman, N., & Muthukumaravel, S. (2020). Cost Accounting Systems Structure and Information Quality Properties: An Empirical Analysis. European Journal of Molecular & Clinical Medicine, 7(8), 5577–5586.

- Jasim, Y. A., & Raewf, M. B. (2020). Information technology’s impact on the accounting system. Cihan University-Erbil Journal of Humanities and Social Sciences, 4(1), 50–57.. https://doi.org/10.24086/cuejhss.v4n1y2020.pp50-57

- Jiang, D. (2019). Management Accounting Literature Review—Based on the Development of Management Accounting Research in 2015-2017. Modern Economy, 10(12), 2315–2334.. https://doi.org/10.4236/me.2019.1012145

- Keel, G., Savage, C., Rafiq, M., & Mazzocato, P. (2017). Time-driven activity-based costing in health care: A systematic review of the literature. Health Policy, 121(7), 755–763.. https://doi.org/10.1016/j.healthpol.2017.04.013

- Khatib, S. F. A., Abdullah, D. F., Al Amosh, H., Bazhair, A. H., & Kabara, A. S. (2022). Shariah auditing: Analyzing the past to prepare for the future auditing. Journal of Islamic Accounting and Business Research, 13(5), 791–818. https://doi.org/10.1108/JIABR-11-2021-0291

- Khatib, S. F. A., Abdullah, D. F., Elamer, A. A., & Abueid, R. (2021). Nudging toward diversity in the boardroom: A systematic literature review of board diversity of financial institutions. Business Strategy and the Environment, 30(2), 985–1002. https://doi.org/10.1002/bse.2665

- Kihuba, E., Gheorghe, A., Bozzani, F., English, M., & Griffiths, U. K. (2016). Opportunities and challenges for implementing cost accounting systems in the Kenyan health system. Global Health Action, 9(1), 30621.. https://doi.org/10.3402/gha.v9.30621

- Kineber, A. F., Oke, A., Hamed, M. M., Alyanbaawi, A., Elmansoury, A., & Daoud, A. O. (2023). Decision making model for identifying the cyber technology implementation benefits for sustainable residential building: A mathematical PLS-SEM approach. Sustainability, 15(3), 2458.. https://doi.org/10.3390/su15032458

- Krishnan, S. R. (2023). Decision‐making processes of public sector accounting reforms in India—Institutional perspectives. Financial Accountability & Management, 39(1), 167–194.. https://doi.org/10.1111/faam.12294

- Kroon, N., Alves, M. D. C., & Martins, I. (2021). The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review. Journal of Open Innovation, Technology, Market, and Complexity, 7(3), 163.. https://doi.org/10.3390/joitmc7030163

- Kubasiewicz, L. M., Bunnefeld, N., Tulloch, A. I., Quine, C. P., & Park, K. J. (2016). Diversionary feeding: An effective management strategy for conservation conflict? Biodiversity and Conservation, 25(1), 1–22.. https://doi.org/10.1007/s10531-015-1026-1

- Kumar, A., Alghamdi, S. A., Mehbodniya, A., Webber, J. L., & Shavkatovich, S. N. (2022). Smart power consumption management and alert system using IoT on big data. Sustainable Energy Technologies and Assessments, 53, 102555.. https://doi.org/10.1016/j.seta.2022.102555

- Larbi, G. M. (2021). Activity based-costing system through three generation: ABC-TDABC-PFABC. Business Sciences Review, 20(1), 90–108..

- Lund, H., Thellufsen, J. Z., Østergaard, P. A., Sorknæs, P., Skov, I. R., & Mathiesen, B. V. (2021). EnergyPLAN–Advanced analysis of smart energy systems. Smart Energy, 1, 100007.. https://doi.org/10.1016/j.segy.2021.100007

- Luo, Y. (2021). Retracted Article: Environmental cost control of coal industry based on cloud computing and machine learning. Arabian Journal of Geosciences, 14(12), 1–16.. https://doi.org/10.1007/s12517-021-07411-w

- Lutfi, A. (2022). Factors Influencing the Continuance Intention to Use Accounting Information System in Jordanian SMEs from the Perspectives of UTAUT: Top Management Support and Self-Efficacy as Predictor Factors. Economies, 10(4), 75.. https://doi.org/10.3390/economies10040075

- Lutfi, A., Alkelani, S. N., Al-Khasawneh, M. A., Alshira’h, A. F., Alshirah, M. H., Almaiah, M. A., Alrawad, M., Alsyouf, A., Saad, M., & Ibrahim, N. (2022). Influence of Digital Accounting System Usage on SMEs Performance: The Moderating Effect of COVID-19. Sustainability, 14(22), 15048. https://doi.org/10.3390/su142215048

- Mahal, I., & Hossain, A. (2015). Activity-based costing (Abc)–an effective tool for better management. Research Journal of Finance and Accounting, 6(4), 66–74..

- Mahdi Sahi, A., Mahdi Sahi, A., Abbas, A. F., & Khatib, S. (2022). Financial reporting quality of financial institutions: Literature review. Cogent Business & Management, 9(1), 2135210.. https://doi.org/10.1080/23311975.2022.2135210

- Mahesha, V. (2022). A comparative study of activity based costing and traditional costing as a fragment of pricing. SAARJ Journal on Banking & Insurance Research, 11(2), 1–9.. https://doi.org/10.5958/2319-1422.2022.00006.6

- Mainar-Causapé, A. J., Ferrari, E., & McDonald, S. (2018). Social accounting matrices: Basic aspects and main steps for estimation. Publications Office of the European Union.

- Massaro, M., Dumay, J., & Guthrie, J. (2016). On the shoulders of giants: Undertaking a structured literature review in accounting. Accounting, Auditing & Accountability Journal, 29(5), 767–801. https://doi.org/10.1108/AAAJ-01-2015-1939