Abstract

The paper focuses on a current study on sustainable accounting as well as potential future research issues. 679 publications dealing with sustainable accounting produced between 2003 and 2022 were assessed using a bibliometric and visualization tool for the Web of Science cor collection database and viewer-based literature. The study looks at cluster analysis, all-keyword co-occurrence analysis, and bibliographic coupling mapping. This study allows us to suggest future research directions that may be beneficial in reflecting on the major influence that technology will have on the expansion of sustainable accounting in a business. The survey identified four major research trends in accounting for sustainability: reporting and disclosure, sustainability as part of management control systems, accounting and environmental management, stakeholder involvement and accountability, sustainability and business social responsibility. Education and Information Sharing About Sustainable Accounting, Green Sustainable Accounting, Technology Usage in Sustainable Accounting, Including AI, Big Data, and IoT, and ESG: Sustainable Accounting. This report presents a thorough examination of research trends in the intersection of sustainable accounting, as well as prospective research directions.

1. Introduction

The area of sustainability accounting is expanding with the goal of capturing the social and environmental effects of an organization’s operations and incorporating them into decision-making procedures (Ehnert et al., Citation2016; Fonseca et al., Citation2014). It acknowledges that businesses have obligations not only to their shareholders but also to the larger community and the environment (Cho et al., Citation2015). A framework for understanding an organization’s influence on these larger stakeholders and taking measures in keeping with their values and objectives is provided by sustainability accounting. As the need for corporations to account for their social and environmental consequences grows, sustainability accounting has emerged as a reaction (Hörisch et al., Citation2020). The foundation of sustainability accounting is in the ideas of sustainable development, which places a strong emphasis on combining environmental, social, and economic factors when making decisions (Schaltegger, Citation2021). Organizations are assisted by sustainability accounting in identifying possibilities to enhance their social and environmental performance as well as in managing the risks connected to sustainability-related concerns. Furthermore, it gives stakeholders the knowledge they require to assess an organization’s sustainability performance and make educated decisions (Schaltegger et al., Citation2022).

Sustainable accounting is a crucial factor that might affect how stakeholders, such as investors, regulators, and consumers, decide to act. On the best ways to gauge and report sustainability performance, there isn’t much agreement. This is a difficulty for businesses looking to show their dedication to sustainability, as well as for stakeholders wishing to assess the sustainability performance of a company (Fagerström et al., Citation2017; Gil-Marín et al., Citation2022; Lee, Citation2019). Investigating the role and efficacy of sustainable accounting in diverse situations is a possible research subject. It is unknown, yet, how various approaches to sustainable accounting work. These queries may yield important data regarding the most effective methods for creating sustainable accounting using bibliometric analysis.

Scientific literature makes it clear that accounting for sustainability is necessary. Sustainable accounting methods may assist firms in achieving better sustainability outcomes by offering a framework for measuring, reporting, and monitoring sustainability performance, according to a growing body of scientific research. R. Adams et al. (Citation2016) discovered that firms may identify and handle sustainability risks, including climate change and resource depletion, with the use of sustainability accounting. Sustainability accounting, according to (Schaltegger et al., Citation2018) may aid firms in increasing resource efficiency, cutting waste, and increasing sustainability-related innovation. Moreover (Albareda & Hajikhani, Citation2019), discovered that sustainable accounting may aid firms in improving their decision-making and performance results by assisting them in aligning their sustainability goals with their overall strategy. Ullah & Sun (Citation2021) investigated the connection between company innovation and sustainability accounting. The study discovered that by encouraging sustainable practices and raising stakeholder participation, sustainability accounting may favorably impact innovation. In general, a sizable body of research has focused on the contribution of sustainable accounting to the promotion of creative thinking.

Sustainability accounting has emerged as a framework for corporations to account for their social and environmental implications, and it has resulted in a growing amount of literature on the subject. The benefits of sustainable accounting have been emphasized in the literature for recognizing sustainability risks, enhancing resource efficiency, supporting sustainability-related innovation, and aligning sustainability goals with overall strategy. Furthermore, research suggests that sustainable accounting may have a positive influence on organizational innovation and contribute to creative thinking. There is, however, a scarcity of extensive literature evaluations on sustainable accounting, which hinders our understanding of the issue. This study seeks to fill that gap by conducting a thorough literature evaluation and identifying research gaps and potential research opportunities. Furthermore, using bibliometric approaches, this analysis tries to identify the most and least sustainable accounting-related nations and publications. Therefore, completing a comprehensive literature review and bibliometric analysis can give vital insights into the present status of sustainable accounting research, identify research gaps, and recommend future study subjects. Through its analysis and debate of sustainable accounting, the ultimate purpose of this work is to contribute to the creation of efficient management systems.

While the research is confined to a few topics, such as: what is the state of the art through the WoS database, such as years of publication, journals, the most prolific countries, relevant authors, and productive universities? What is the current state of the art using VOSviewer software, such as source networks, country networks, university networks, and author networks? What is content analysis for sustainable accounting using VOS viewer software? What are the present and future trends in sustainable accounting?

This study’s review contributes significantly to the topic of sustainable accounting by integrating existing research and identifying needs for further study. This study presents a thorough picture of the current state of sustainable accounting research, including the most and least sustainable accounting-related nations and publications, by conducting a systematic literature analysis and applying bibliometric methodologies. In addition, the assessment emphasizes the critical role that sustainable accounting plays in improving an organization’s social and environmental performance and decision-making processes. The review’s assessment of sustainable accounting’s contribution to the fostering of innovation also offers future study possibilities.

Furthermore, the study adds to the body of knowledge by thoroughly assessing the present state and future directions of sustainable accounting research. The report provides significant insights for scholars, policymakers, and practitioners interested in sustainable accounting by identifying research gaps and trends. This technique can assist the progress of sustainable accounting by providing a path for future study. The manuscript’s uniqueness stems from its use of bibliometric analysis to provide a quantitative assessment of the state of the sustainable accounting literature, identify emerging trends and research gaps, and identify essential components of sustainability accounting and management for business.

There is a dearth of thorough literature reviews in the present study on sustainable accounting, which might offer important new perspectives. By performing a systematic literature review, which can assist future researchers in gathering scattered material, identifying research gaps, and suggesting areas for future research, this work seeks to close this gap. This study also aims to identify the most and least sustainable accounting-related nations and publishers using bibliometric approaches. The report’s main goal is to concentrate on the key concepts that might affect sustainable accounting and lay the groundwork for further investigation in this field. This literature review’s ultimate goal is to further the creation of efficient management systems through its investigation and discussion of sustainable accounting.

2. Research methods

A bibliometric study will be performed to develop a research trend map for sustainable accounting between 2003 and 2022. The study will concentrate on metrics such as the average yearly manuscript, total contribution by country, most cited papers, leading authors’ contributions over time, most significant keywords, trend concerns, visualization approaches, and connection cluster analysis. Bibliometric analysis is a distinct form of literary study that utilizes mathematical and quantitative methodologies to assess successful interaction via textual materials (Behl et al., Citation2022). There has been an upsurge in the use of literature reviews as an analytical tool in recent years, highlighting bibliometric analysis as a crucial and effective strategy for evaluating scientific progress. Bibliographic research has been aided by technological advancements and internet access to bibliographic databases such as Web of Science, Scopus, and Google Scholar. Environmental accounting (Shoeb et al., Citation2022), green accounting (Ferieka et al., Citation2022), ethical accounting (Poje & Zaman Groff, Citation2022), and climate accounting (Zheng et al., Citation2022) will be the focus of our research. There will be numerous stages to the research process.

To prepare the way for future studies, it is critical to identify research gaps and trends in the field of education. Despite the fact that various studies on latency analysis have been undertaken, a thorough evaluation that establishes a framework for future study and maps the global research on delay analysis has not been conducted (Akbari et al., Citation2020; Alsharif et al., Citation2021; Khan & Muktar, Citation2020). The purpose of this research is to undertake scientometric analyses to find the most focused research topics and to conduct a literature analysis on delayed analytical methodologies in sustainability accounting. The steps that follow detail the study’s technique for reaching this goal.

2.1. Sample size and data collection

Many databases, including Dimensions Database, Google Scholar, Web of Science, and Scopus, are accessible for mapping bibliographic data. The Web of Science database was used for scientometric analysis in this study, which included all academic papers linked to delay assessments in sustainability accounting.

The Web of Science (WoS) database is an academic database that includes a wide range of fields, including sustainability accounting. It provides a broad and trustworthy collection of academic papers, guaranteeing that the scientometric analysis performed in this study is thorough and rigorous. Furthermore, the WoS database contains a citation indexing capability that enables citation analysis, revealing the most cited publications and authors in the subject. This may be a very useful technique for identifying critical research gaps and future research initiatives.

Relevant keywords were picked in order to collect scholarly papers relating to delay studies in sustainable accounting. As a result, papers from various categories were downloaded and used in the bibliometric analysis from the Web of Science database. While evaluating the relevant papers, it was discovered that phrases like “environmental accounting,” “green accounting,” “ethical accounting,” and “climate accounting” were often utilized in the titles, abstracts, and keywords. As a result, Vosviewer was used to extract new keywords from all articles related to sustainable accounting.

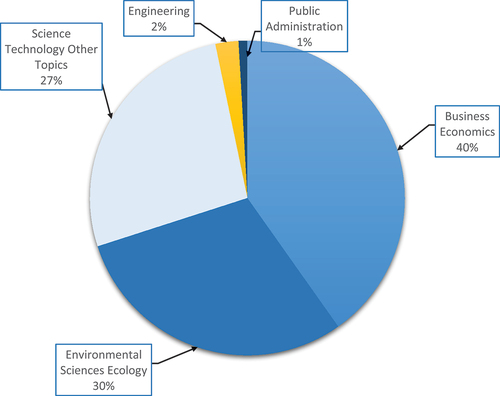

The Web of Science database’s “Advanced Search” option was used to find pertinent academic papers on delay studies in sustainability accounting. The search query was “ALL = sustainability OR accounting AND “sustainability accounting,” Language: (English), and Document Types: (All). The results were restricted to the following Web of Science categories: business economics, environmental sciences, ecology, and science technology other topics, engineering, public administration, social sciences other topics, energy fuels, government law, development studies, education educational research, and physics. The search returned 679 published publications between 2003 and 2022. The analysis included only publications published in English and classified as Articles, Books, or Proceedings papers, whereas non-scientific sources such as unreviewed books and white papers were removed as shown in Figure .

Figure 1. Paper inclusion/exclusion flowchart.

Sustainability accounting is a fast-emerging area that has received a lot of interest because of its potential to help with the transition to a more sustainable economy. It incorporates a number of concepts, including environmental accounting, social accounting, and economic accounting, all of which strive to assess the impact of organizational actions on the environment, society, and economy. Many elements have an impact on sustainable accounting as shown in Figure (Ascani et al., Citation2021).

Figure 2. Research area.

2.2. Data analysis

While researching any scientific issue, it is critical to employ a credible science mapping approach. VOSviewer, Gephi, CiteSpace, Sci2, and HistCite are among the software tools available for this purpose. Gephi is open-source and free software that allows you to visualize and explore graphs and networks. CiteSpace, on the other hand, is a free scientific mapping tool for analyzing and visualizing concepts and relationships in literature. VOSviewer, a popular platform for showing data in an appealing graphical format, has text-mining capabilities. VOSviewer was chosen as the instrument of choice for this inquiry after a thorough examination of the available software. As a result, as proposed by (Xie et al., Citation2020) scientific papers retrieved from the Web of Science database using relevant keywords were evaluated using VOSviewer software.

By utilizing the VOSviewer program, the study was able to identify current trends in delay analysis in sustainability accounting, as well as gaps in the literature, future research subjects, and the most notable nations, organizations, journals, publishers, and authors in the area. The study used the scientometric approach of “Mappings Using Bibliographic Data,” which included citation and bibliographic coupling analyses, to accomplish this. Citation analysis was performed to determine the authors who were most commonly referenced in the area, while bibliographic coupling analysis was used to analyze the nations that produced the most articles on delay analysis. Overall, this technique contributed to a thorough overview of the present status of research in this area.

3. Findings

3.1. WoS analysis

To comprehend the research landscape of sustainability accounting, it is necessary to track the publication activity of multiple entities such as authors, journals, affiliations, and nations across time. Such metrics shed light on the topic’s evolution and organization, as well as the important participants in the area. This section summarizes the findings of important bibliometric analyses conducted between 2003 and 2022 to investigate the evolution of the literature on sustainable accounting. The investigation involves an evaluation of the most major academic institutions and their links, as well as 679 publications published in 28 scientific journals.

Figure shows how the literature on sustainable accounting has grown at an exponential rate in recent years. Over the first decade, the number of publications was restricted to 5–10 per year, but in 2006, there was a rapid jump to 32, indicating an increase in the application of sustainability concepts in accounting. The number of publications increased over the next two years, reaching 40 in 2015 and 33 in 2016. The greatest substantial increase in publications, however, happened in 2017. The year 2020 had the largest number of publications with 128, but the bulk of citations were recorded in 2022, reaching 2807.

Figure 3. Documents by year of publication 2003–2022.

Many reasons have contributed to the recent increase in publications relevant to sustainable accounting. For starters, there is a rising interest in sustainability in both the public and commercial sectors, which has raised the need for study in this field. Moreover, legal requirements for sustainability reporting, such as the GRI and SASB, have raised the demand for research in sustainability accounting. Investor pressure has also played a role, with investors becoming more interested in firms’ ESG activities and demanding more information on sustainability performance, resulting in a greater emphasis on sustainability accounting and reporting (Bennett & James, Citation2017; McKinnon et al., Citation2015). Several businesses have realized the value of CSR and have incorporated sustainability into their business strategies, necessitating research in sustainability accounting to support their efforts. Lastly, advances in technology and data availability have enabled academics to undertake more in-depth assessments of sustainable accounting methods, resulting in a better knowledge of the area and spurring more study (Jones & Wynn, Citation2021).

Table provides a thorough overview of the most prestigious journals and publishers that have published research on sustainable accounting. The Sustainability Accounting, Management, and Policy Journal is the premier publication in this discipline, with 313 papers published and 2,836 citations. The Indonesian Journal of Sustainable Accounting and Management is close behind, having published 75 articles and gained 223 citations. These two journals account for more than half (57.14%) of all published publications in this field. These articles have made major contributions to the advancement of research on sustainability accounting, which is critical for establishing successful methods for addressing environmental, social, and economic concerns. These studies’ findings can assist policymakers, managers, and stakeholders in making educated decisions to support sustainable development.

Table 1. Most relevant journals

According to Table , six countries contributed 61.26% (416 out of 679) of the studied articles: Australia, the United States, England, Germany, Indonesia, and Spain. Australia generated the greatest number of publications (95, or 13.99%), demonstrating that the nation has a strong academic and research infrastructure, funding sources, and a high demand for sustainability accounting research. Furthermore, the country has access to high-quality publication channels, which contributes to the considerable amount of scientific research undertaken in Australia on these themes.

Table 2. Most productive countries

Sustainability accounting is a significant subject of research in Australia, with an emphasis on themes such as carbon accounting, social and environmental reporting, sustainable supply chain management, the Sustainable Development Goals, and environmental management accounting. Researchers have explored the efficiency of various accounting techniques and systems, as well as the obstacles and possibilities connected with adopting sustainable practices in firms. Their work has influenced policy and practice in a range of contexts and industries, including manufacturing and agriculture.

Table ranks the most influential authors in sustainable accounting research according to the total number of publications and citations in the WoS database. Throughout the review period, each of the top authors produced at least seven publications. Schaltegger S emerged as the most productive and well-regarded author, with 21 papers and 761 citations to their name. This ranking shines a light on the leading researchers in sustainable accounting, giving significant insights for both scholars and practitioners.

Table 3. Most relevant authors

Table shows that the majority of the prominent publishing affiliations in sustainable accounting research are university institutions. Among the 99 papers examined, 65 were associated with Australian universities and 34 with German institutions. Leuphana University emerged as the most productive university, with 24 articles published. This ranking highlights academic institutions’ important role in developing sustainable accounting research and provides significant information for scholars and practitioners interested in this topic.

Table 4. Top productive universities

Several publications and research institutes dedicated to sustainable accounting have been established by Australian institutions. But, universities and research institutions throughout the world have also played an important role in improving sustainable accounting as a field. Several schools offer courses and degree programs in sustainability accounting, preparing students to face sustainability concerns in the corporate sector. Sustainability accounting research centers and institutes have also been formed across the world, contributing to the field’s development through research and outreach initiatives. University and research institution contributions have been critical in expanding sustainability accounting as a subject of study and practice, promoting sustainability more broadly, and furthering global sustainable development goals.

3.2. VOSviewer analysis

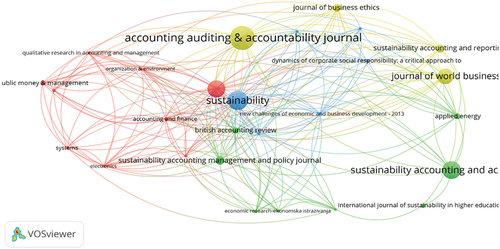

Bibliographic coupling is a bibliometric measure that analyzes the overlap of two sources’ reference lists to determine their similarity. It is often used in bibliometrics to study research domain structures and uncover relationships between various sources. The number of references shared by two sources is tallied and reported as a percentage or proportion of the total number of references in each source to assess bibliographic coupling. A high level of bibliographic coupling between two sources implies that they are linked and may be part of the same research tradition or topic. Low bibliographic coupling, on the other hand, may signal that the sources are unconnected or belong to different research traditions (Sustacha et al., Citation2022).

In Figure , for instance, the highest circle relates to sustainability and includes the seven most notable works on sustainable accounting. Accounting, Auditing & Accountability Journal has gotten the most citations (482) and the most total link strength (232), with Sustainability coming in second (310). The standards also call for at least one reference from each of the articles. The research found 209 linkages with a total link strength of 867, resulting in four separate clusters.

Figure 4. Visualization of source networks.

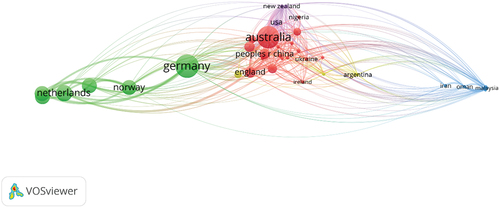

Figure depicts the network of collaboration across nations and regions in a certain scientific subject. Based on at least one document criterion, the analysis presents up to fifty of the most representative bibliographic linkages. The things are named and represented by circles, with the size of the label and circle indicating their weight, with the largest label and circle being the most significant object. The distance between items represents the degree of relatedness across nations in the research domain, while the lines connecting them indicate the presence of links between them. The ability to compare nations or regions with comparable features is the key advantage of this map. Nations on the same continent frequently have similar profiles; therefore, they show next to each other on the map (Wang et al., Citation2018).

Figure 5. Visualization of countries networks.

The biggest circle in Figure shows Germany, which is strongly related to surrounding nations such as Austria, the Czech Republic, Denmark, the Netherlands, Norway, Poland, and New Zealand. Germany contributes significantly to research on various topics related to sustainability, such as environmental accounting, social accounting, corporate sustainability reporting, sustainable finance, integrated reporting, life cycle assessment, sustainability management, climate accounting, socially responsible investing, and the circular economy. Germany is predicted to account for 15.95% of all link strengths in this study domain. Furthermore, a significant fraction of research on sustainable accounting and its consequences (about 28% of published publications) focuses on multidisciplinary subjects such as psychology, sociology, and political science. A study on the evolution of sustainable accounting and its environmental consequences emphasized the unique accounting linkages to sustainability as well as the growth of intelligent accounting practices in Germany and other nations. Figure further shows that these issues are strongly related to the five research clusters in the partnership network.

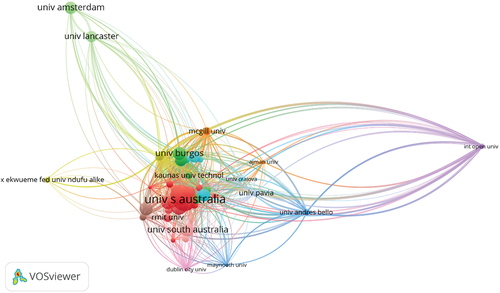

Figure depicts an organizational collaboration network based on at least one document and up to fifty of the most significant bibliographic relationships. The default item representation is a circle with a label, with the size of the label and circle corresponding to the weight of the item, with the most significant object having the largest label and circle (De Camargo et al., Citation2020).

Figure 6. Visualization of universities networks.

The distance between items in Figure represents the degree of relationship between them, and the lines linking them show affiliations. The key advantage of the map is its ability to find colleges with comparable qualities. The study developed nine groups since institutions from the same continent tend to have similar characteristics and are clustered together on the map. The biggest circle represents the University of South Australia (Australia), which has the most citations (610). According to Figure , Leuphana University (Germany) ranks second in terms of citations (333) and overall link strength (205), based on three published works on sustainable accounting and the permissible total connection strength on the map (456). The high degree of collaboration between Australian and German institutions shows an active interchange of sustainable accounting approaches and practices.

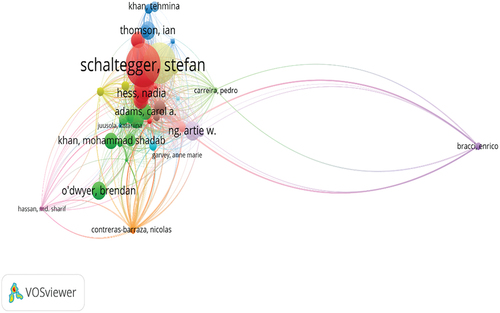

A subset of bibliographic coupling is author bibliographic coupling (ABC), which happens when two authors cite the same article(s) in publications published by the same authors. According to the ABC assumption, the more references two authors have in their collected works, the more comparable their research is. The research looked at the use of document bibliographic linking for data mining and scientific visualization (Mcgee et al., Citation2019). Figure depicts the top 128 contributing authors in terms of the number of publications mentioned, with Schaltegger, Stefan; Burritt, Roger L.; Lodhia, Sumit; Larrinaga, Carlos; and Ng, Artie W., receiving the most citations in sustainable accounting papers, totaling 1433. There are 42 publication citations connected to sustainable accounting for each of the top 128 authors. The red, green, and purple clusters in Figure correspond to the names of authors whose research focuses on the keywords stated in the image. Furthermore, the purple cluster in Figure stands out in terms of other authors’ participation and interest in other clusters.

Figure 7. Visualization of authors’ networks.

3.3. Keywords analysis

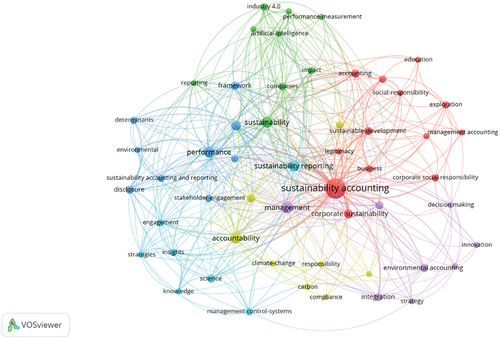

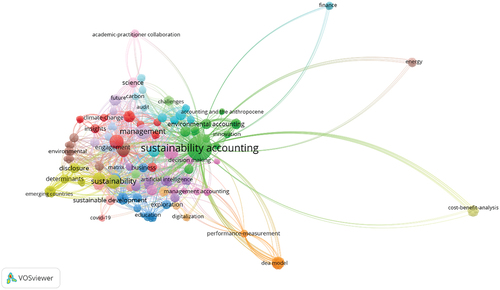

Bibliographic data from the Web of Science Core Collection database was used in bibliometric studies and mapping with the VOSviewer program. Co-occurrence analysis was employed to determine the entire power between keywords and their occurrences. The volume of the clusters indicates the potency and significance of terms, with the curving lines and colors highlighting the importance of word clusters and linkages between them. The keyword co-occurrence map in Figure consists of 279 text-data terms, with 54 fulfilling the two thresholds. Six clusters make up the map, with the sustainability accounting term being the strongest cluster, appearing 32 times and related to nearly every other keyword, indicating significant impact. The clusters’ many keywords include management, sustainability, performance, accountability, and sustainability reporting, listed in order of strength.

Figure 8. Keyword co-occurrence.

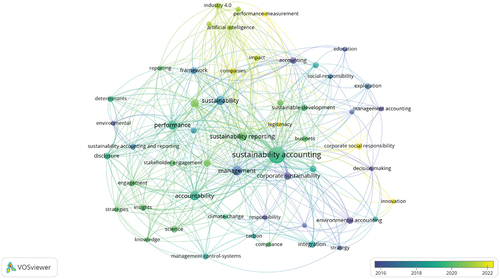

Figure depicts the evolution of sustainable development and management activities since their commencement in 2016. The specific starting year indicates that the accountability actions were planned, and the gradual implementation strategy suggests a patient and deliberate approach. According to the schedule, the community embraced sustainable accounting practices in 2018, and there was an emphasis on artificial intelligence in 2020. Technology, innovation, corporate social responsibility (CSR), and environmental, social, and governance (ESG) concerns were acknowledged as important beyond 2022. Yet, the effectiveness of these efforts cannot be judged only on the basis of the beginning locations represented in the figure. To assess their success, other criteria such as particular goals, techniques, and outcomes would need to be examined.

Figure 9. Growth of keyword co-occurrence.

According to Table of the VOSviewer statistical technique, “sustainable accounting” is the most commonly used author keyword in the literature, followed by “management.” Other similar names, such as “environmental accounting,” “green accounting,” “ethical accounting,” and “climate accounting,” also suggest an emphasis on sustainable accounting. When the frequency of these phrases is added together, they occur 209 times, indicating that “sustainable accounting” is the most regularly used keyword in the literature. The average year of publication indicates how long experts have used this phrase in their work. Interest in collaboration-related articles increased significantly in 2022, whereas technology- and innovation-related publications received greater attention in 2018, 2020, and 2022. The overall link strength of a node reflects the strength of its connections, with “sustainable accounting” having the greatest link strength of 121, demonstrating its significant inter-relatedness to the issue (N. J. Van Eck & Waltman, Citation2018).

Table 5. Keywords selected for network parameters

4. Discussion

The study sought to investigate the geographical distribution of innovation in sustainable accounting research as well as the patterns of individual and organizational publications. The findings found that Australia, Europe, North America, and Asia were the primary research regions, with no research from Africa or South America included in the analysis. This conclusion is consistent with prior research by (Benameur et al., Citation2023; Bosi et al., Citation2022; Maier et al., Citation2020; Nobanee et al., Citation2021; Pasko et al., Citation2021; Rodrigues et al., Citation2021; Sanguankaew & Vathanophas Ractham, Citation2019; Schaltegger et al., Citation2013) all of which focused on adoption barriers rather than long-term accounting concerns in African countries. As a result, the study underlines the importance of more research on underrepresented regions as well as an in-depth examination of the unique issues these regions face in adopting sustainable accounting practices.

The goal of this study, depicted in Figure , is to highlight key and recent breakthroughs in sustainable accounting research by connecting innovations with current concerns connected to the application of sustainable accounting. The study seeks to simplify technical jargon, identify patterns, and improve understanding of recent breakthroughs and research trends in order to provide corporate stakeholders and scholars with a comprehensive overview of the intellectual landscape and future research prospects in sustainable accounting.

Figure 10. Topic network map.

Bibliometric data analysis is a valuable technique for evaluating a certain area’s performance in the literature, allocating research money, and identifying major variables that drive study in a specific subject (Burnes & Cooke, Citation2013; Vysochan et al., Citation2021). This study used a refined search query that yielded 679 papers from the Web of Science database to determine the most prevalent phrases in sustainable accounting. According to the statistics, 40% of the publications were about business and economics, while 30% were on environmental sciences and ecology. Since 2003, the number of publications on this topic has grown, with the most papers published in 2020. The research also sought to identify the most influential journals, universities, and authors in this sector, as well as track international collaboration through the use of a country visualization map. Germany, Austria, the Czech Republic, Denmark, the Netherlands, Norway, Poland, and New Zealand are among the nations that provide the greatest contributions to international cooperation. Table displays the top terms in the keyword co-occurrence network generated by the VOSviewer program, arranged by high occurrence frequency.

4.1. Common research topics

In this section, we will study the most regularly referenced publications in each of the previously provided clusters. Furthermore, we will assess research subjects based on the number of publications in each study field as shown in Figure .

Figure 11. Common trend’s reputation.

4.1.1. Accounting for sustainability: reporting and disclosure

The technique of incorporating environmental, social, and governance (ESG) considerations into financial reporting and decision-making processes is referred to as accounting for sustainability. As they educate stakeholders about how firms are handling their sustainability risks and opportunities, reporting and disclosure are crucial components of accounting for sustainability. Several formats for reporting and disclosing sustainability data are available, including stand-alone reports, integrated reports, and the incorporation of sustainability data in annual reports. It often encompasses a wide variety of sustainability-related topics, including supply chain management, resource consumption, human rights, and labor standards (C. A. Adams, Citation2018; Ibrahim et al., Citation2022).

For a number of reasons, reporting and disclosure are crucial. They first provide stakeholders, such as investors, clients, staff members, and the general public, with openness and accountability (Rimmel, Citation2020). In addition, they support firms in identifying and managing sustainability opportunities and risks, which improves decision-making and generates long-term value (Liu et al., Citation2019) who support the standardization and comparability of sustainability data so that stakeholders can compare performance across various businesses and industries and make educated decisions. Organizations could think about adopting existing frameworks and standards, including those of the Task Force on Climate-related Financial Disclosures, the Sustainability Accounting Standards Board, or the Global Reporting Initiative (GRI), to guarantee effective reporting and disclosure (TCFD). Organizations may align their reporting with international best practices and stakeholder expectations by using these frameworks, which offer advice on sustainability reporting concepts, indicators, and metrics (Bini et al., Citation2020; Cooper & Michelon, Citation2022).

4.1.2. Sustainability is included in management control systems

The importance of sustainability in the corporate sector has grown, and many organizations are increasingly integrating sustainability into their management control systems. Systems for managing and controlling activities, such as financial performance, risk management, and operational effectiveness, are known as management control systems (Hörisch et al., Citation2017). Sustainability may be incorporated into management control systems in a number of different ways. To track and assess the environmental, social, and economic effects of the organization’s operations, sustainability metrics can be developed. The performance measurement and reporting systems of the organization can then incorporate these metrics (Luque-Vilchez & Larrinaga, Citation2016).

Using sustainability as an important consideration throughout the decision-making process is another method for integrating sustainability into management control systems. This may entail performing sustainability effect analyses prior to making important choices or employing sustainability standards to analyze potential partners or suppliers. Besides, a lot of businesses are setting up sustainable governance frameworks to manage their sustainability initiatives. In order to manage the company’s sustainability strategy and objectives, this may entail establishing a sustainability committee or designating a Chief Sustainability Officer (CSO) (Lu et al., Citation2022). Lastly, risk management procedures can incorporate sustainability. This may entail identifying, evaluating, and including sustainability-related risks in the organization’s risk management systems (Narayanan & Boyce, Citation2019; Rehman et al., Citation2021; Slacik et al., Citation2021).

4.1.3. Accounting and management of the environment

To encourage sustainable growth and safeguard the environment, accounting and environmental management are two linked but separate professions. A subset of accounting known as “environmental accounting” accounts for the costs and advantages of corporate activities on the environment. It entails monitoring and documenting how an organization’s operations affect the environment, including greenhouse gas emissions, the use of natural resources, and waste production. Businesses can find ways to decrease their environmental impact and enhance environmental performance by using environmental accounting (Fuzi et al., Citation2020; Qian et al., Citation2015).

On the other side, environmental management entails creating and putting into practice plans and measures to lessen the damaging effects of human activity on the environment. It covers a variety of tasks, including preventing pollution, reducing waste, improving energy efficiency, and conserving resources. Businesses may lower operational expenses, better manage their environmental impact, and comply with environmental standards with the aid of environmental management (Alhossini et al., Citation2021). Combining environmental accounting and management may assist companies in achieving sustainable development by achieving a balance between their economic, social, and environmental objectives. They may also help society as a whole by supporting resource conservation, defending community health and well-being, and reducing the effects of climate change (Braun et al., Citation2018; Burritt et al., Citation2019; Gray et al., Citation2017).

4.1.4. Involvement of stakeholders and accountability

Stakeholders are people or organizations that are interested in or impacted by an organization’s actions and choices. Employees, clients, suppliers, local communities, governing bodies, and environmental organizations can all be considered stakeholders in the context of environmental accounting and management. Organizations may better understand their influence on the environment and the interests and concerns of individuals impacted by their operations by involving stakeholders in environmental accounting and management. Engagement with stakeholders may also assist firms in finding chances for cooperation, establishing credibility and confidence, and enhancing their overall environmental performance (Atkins & Maroun, Citation2018; Tipu, Citation2022).

A crucial component of environmental accounting and management is accountability. Stakeholders hold organizations responsible for their environmental effects and their attempts to mitigate them. This responsibility may be expressed in a variety of ways, such as by reporting on environmental performance, abiding by environmental laws, and reacting to criticism and concerns from stakeholders. Accountability in environmental accounting and management depends on openness and communication. Organizations should be open about how they affect the environment and how they try to mitigate that effect. In order to keep stakeholders informed about environmental performance, advancements, and difficulties, they should also constantly interact with them. Effective environmental accounting and management depend on involving stakeholders and encouraging responsibility. Organizations may increase trust and credibility, support sustainable development, and help create a world that is healthier and more resilient by involving stakeholders and taking responsibility for their environmental effects (Lauwo et al., Citation2022; Lozano, Citation2022).

4.1.5. Sustainability and business social responsibility

Business social responsibility (BSR) and sustainability are two ideas that are getting more and more attention in the modern world. Sustainability and BSR both refer to a company’s dedication to moral and accountable practices that consider the effects of its activities on its social and natural surroundings. The term “sustainability” describes an organization’s capacity to conduct its operations in a way that satisfies current requirements without jeopardizing the ability of future generations to satisfy their own needs. This includes reducing adverse environmental effects, making efficient use of resources, and preserving a healthy and effective staff (Schaltegger et al., Citation2019).

On the other hand, BSR describes a company’s dedication to moral behavior that advances society as a whole. This might involve charitable endeavors, involvement in the community, staff participation, and attempts to lessen environmental impact and encourage sustainable practices. In actuality, BSR and sustainability frequently overlap and strengthen one another (Nguyen et al., Citation2020). A company that uses renewable energy and lessens its carbon impact, for instance, is supporting sustainability and exemplifying BSR by acting to combat climate change. Similar to this, a company that interacts with its community and funds charitable causes is advancing BSR and assisting in the development of stronger, more resilient local communities. In the end, companies that value sustainability and BSR are not only doing what is right for society and the environment, but they are also more likely to succeed in the long run. Businesses are under increasing pressure from customers, shareholders, and other stakeholders to be accountable for their actions and to positively affect society. Those that fail to do so run the danger of damaging their reputations and losing money (Baker et al., Citation2022; De Stefano et al., Citation2018; Maroun & Lodhia, Citation2017).

4.1.6. Education and information sharing about sustainable accounting

The goal of sustainable accounting is to incorporate environmental, social, and governance (ESG) considerations into financial reporting and decision-making processes. It is essential to corporate sustainability because it enables businesses to recognize and address their influence on society and the environment. To promote knowledge of and comprehension of this idea among many stakeholders, education and information exchange regarding sustainable accounting are essential. Business executives, investors, decision-makers in politics, and the general public are some of these stakeholders (Cunha & Moneva, Citation2018).

Academic programs and training courses are used to enhance knowledge of and exchange information about sustainable accounting. Professionals who want to implement sustainable accounting practices in their firms can benefit from these programs by gaining the skills and knowledge needed. University research on sustainable accounting should also be encouraged in order to progress the discipline and pinpoint best practices. By contrast, conferences, seminars, and workshops should be used to advance education and information sharing. Experts, practitioners, and stakeholders may get together at these events to exchange knowledge, talk about problems, and present creative solutions. A community of practice for sustainable accounting may be developed with their assistance. They can also offer networking possibilities (Patten & Shin, Citation2019).,

Organizations may also spread knowledge about sustainable accounting by using a variety of communication platforms. To inform stakeholders about the company’s sustainable practices and initiatives, businesses may, for instance, produce reports, webinars, and social media posts. They can also work with trade groups and non-governmental organizations (NGOs) to spread best practices and encourage sustainable accounting. To encourage the adoption and implementation of sustainable accounting across organizations, education and information exchange are essential. Stakeholders may better comprehend the advantages of sustainable accounting and its function in attaining long-term sustainability by increasing awareness and developing capability (McNamara & Sepasgozar, Citation2021; Modugno & DiCarlo, Citation2019).

4.1.7. Target

The approach of incorporating environmental, social, and governance (ESG) factors into financial reporting and decision-making processes is known as accounting for sustainability. This includes reporting and releasing statistics on supply chain management, resource consumption, human rights, and labour standards. It is crucial for a variety of reasons, including giving transparency and responsibility to stakeholders, assisting companies in identifying and managing sustainability risks and opportunities, and producing long-term value. Reporting and disclosure also encourages the standardization and comparability of sustainability data, allowing stakeholders to compare performance across different organizations and industries and make educated decisions. Furthermore, sustainability is rapidly being integrated into management control systems, where it is used to measure and analyze an organization’s environmental, social, and economic impacts, as well as to drive decision-making processes. Finally, accounting for sustainability entails integrating environmental accounting and management, as well as incorporating stakeholders and fostering responsibility.

4.2. Future research directions

The next part will examine projected future research directions in the subject of sustainable accounting after analyzing current important concerns in this area as shown in Figure .

Figure 12. Future trend’s reputation.

4.2.1. Green sustainable accounting

The economic, environmental, and social effects of corporate operations are the subject of green, sustainable accounting. It entails monitoring, calculating, and disclosing both the financial and non-financial costs and benefits resulting from a company’s operations. The objective of sustainable green accounting is to provide decision-makers with a more thorough understanding of the performance of the organization, including its effects on society and the environment. Businesses may use this information to help stakeholders evaluate the company’s social and environmental responsibilities and to help them allocate resources and make investments more wisely (Busco et al., Citation2018; C. A. Adams, Citation2017).

Many metrics and indicators, including waste output, greenhouse gas emissions, water and energy usage, and social and economic effects on local populations, can be included in sustainable green accounting. Creating integrated reports that mix financial and non-financial data or sustainability reports may also be a part of it. For companies wanting to understand and manage their social and environmental consequences, green-sustainable accounting is a crucial tool. It may also encourage more sustainable behaviors and decision-making (Dhar et al., Citation2022; Ng, Citation2018; Rounaghi, Citation2019).

4.2.2. Technology usage in sustainable accounting, including AI, big data, and IoT

In order to monitor and lessen their environmental impact, increase resource efficiency, and encourage social responsibility, corporations are increasingly using technology. Artificial intelligence (AI), big data, and the Internet of Things are three important technologies that are particularly pertinent in this situation (Misra et al., Citation2020).

Artificial intelligence (AI) is being used to examine huge amounts of information and find patterns and insights that might help firms become more sustainable. AI algorithms, for instance, may be used to examine data on energy use and pinpoint places where efficiency might be increased. AI may also assist firms in detecting opportunities and hazards in the supply chain, such as identifying suppliers with high levels of waste production or carbon emissions. Sustainable accounting is supported by the use of big data. Businesses may better understand their sustainability performance and see chances for improvement by gathering and analyzing vast volumes of data from several sources. For instance, big data analytics may be used to examine supply chain data and see possibilities for increased efficiency or to examine consumer data and spot chances for more environmentally friendly product design. To track and control resource use, IoT technology is also being utilized more and more in sustainable accounting. IoT devices may be used to gather data on energy, water, and other resource use in real-time, giving companies more precise and in-depth information on how well they are performing in terms of sustainability. Businesses may use this to pinpoint areas for improvement and track their development over time (Li et al., Citation2022; Mancini et al., Citation2021; Teh & Rana, Citation2023; Tiwari & Khan, Citation2020).

In order to monitor and improve a company’s sustainability performance and help create a more sustainable future, technology is becoming an increasingly significant part of sustainable accounting. Businesses may obtain deeper insights into their sustainability performance and take more effective action to lessen their environmental footprint and promote social responsibility by utilizing technologies like AI, big data, and IoT. Javaid, M (Javaid et al., Citation2022).

4.2.3. ESG: sustainable accounting

ESG-sustainable accounting is no longer simply a passing fad; it is quickly elevating to the status of being fundamental to company reporting and decision-making. Companies are increasingly being held accountable for their ESG performance due to increased public awareness of the effects of climate change, social injustice, and corporate governance standards (Nguyen et al., Citation2020). As a result, ESG-sustainable accounting techniques and frameworks have gained widespread adoption. ESG-sustainable accounting is projected to continue to grow in significance and be integrated even more into business decision-making processes in the future. Many prospective developments in ESG sustainable accounting are listed below (Bose, Citation2020; Eng et al., Citation2022; Shen et al., Citation2020; Tettamanzi et al., Citation2022):

Increased uniformity: Investors and other stakeholders may find it challenging to assess the ESG performance of various firms due to the existing lack of consistency in ESG reporting. ESG reporting standards may become more standardized and unified in the future to enhance comparability and transparency.

Climate change will certainly receive more attention as its effects worsen, so it is probable that businesses’ climate-related risks and opportunities will also receive more attention. Increased reporting requirements for measures connected to climate change, such as greenhouse gas emissions, energy usage, and exposure to physical and transitional hazards, may result from this.

More emphasis on social concerns: While environmental issues have historically been the main focus of ESG reporting, social issues including human rights, diversity and inclusion, and labor standards are now receiving more attention. In the future, it’s possible that these concerns may be the subject of additional reporting requirements and that more businesses will incorporate social factors into their decision-making.

Innovation fueled by technology: With the development of technology, it’s possible that new platforms and tools may emerge that make it simpler for businesses to gather, evaluate, and report on ESG data. Blockchain technology, for instance, might be applied to provide a safe, open system for monitoring and validating ESG data.

Even though businesses and investors want to better understand and manage their ESG risks and opportunities, it is probable that ESG sustainable accounting will continue to develop and become more complex.

4.2.4. Target

The point of view is that as organizations face increased pressure to address their environmental, social, and governance consequences, sustainable accounting, including green accounting and ESG-sustainable accounting, has become increasingly relevant. AI, big data, and IoT are all playing an increasingly important role in sustainable accounting, giving deeper insights into sustainability performance and assisting businesses in identifying chances for improvement. Sustainable accounting has the advantage of assisting organizations in making better informed decisions by taking into consideration not just their financial performance but also their environmental and social implications. This, in turn, can lead to more environmentally friendly practices, more resource efficiency, and increased social responsibility. Transparent reporting of ESG performance may also help to improve a company’s reputation, recruit socially conscious investors, and ultimately contribute to a more sustainable future.

4.3. Theoretical and practical implications

The incorporation of sustainable accounting has theoretical as well as practical implications. Theoretical implications include incorporating environmental, social, and governance considerations into financial reporting, resulting in a more holistic perspective of a company’s activities. Standardization of sustainability accounting gives a level playing field for businesses to compare their sustainability performance with peers in the sector, fostering openness and responsibility. Sustainability accounting also encourages stakeholder participation, which improves accountability and transparency while also strengthening connections between firms and their stakeholders. The practical implications of sustainable accounting, on the other hand, include risk management, resource efficiency, and reputation management. Companies may identify and manage sustainability risks by incorporating sustainability measures into decision-making processes, decreasing risks and enhancing resilience. Sustainability accounting promotes resource efficiency and waste reduction while finding areas for operational efficiency and cost savings. Transparent reporting of sustainability data may help a company’s reputation and attract socially conscious investors, distinguishing it from competitors.

5. Conclusion

This study contributed significantly to the field of sustainable accounting by suggesting crucial topics for future research and offering vital insights into the subject’s progress. The study examined significant publications and journals related to sustainable accounting from the WoS core collection using bibliometric analysis. This approach offers researchers critical information for future research and enables a thorough examination of the subject’s progress by issue, context, and measurement.

The study’s findings indicate that sustainable accounting is still in its early phases of publication, with just a few qualitative research methodologies used. Yet, the study revealed that while sustainable accounting has grown in relevance in the domains of commerce and information systems library science, it has expanded relatively marginally in development studies and educational administration. The research also emphasizes the importance of company culture in sustainable accounting as a basic approach to human connections. This study adds to our understanding of sustainable accounting by identifying crucial topics for further investigation. The study underlines the significance of continuing to investigate the issue using a variety of qualitative research approaches as well as the importance of sustainable accounting in a variety of sectors. The study’s findings can be used to guide future research and contribute to the continued growth of sustainable accounting as a subject of study.

During evaluating the findings of this study, there are various limitations to consider. For starters, the study only used the Web of Science core collection database, which may not be representative of all papers on sustainable accounting. Including other datasets might offer a more complete picture of the field. Second, the analysis was restricted to articles published between 2003 and 2022, which may not reflect recent advancements in the field of sustainable accounting. The bibliometric study also has certain limitations, such as the likelihood of missing important articles owing to the search term and criterion limits, as well as the inability to judge the quality of papers included in the analysis. Furthermore, the analysis only included papers in English, which may have omitted significant non-English language publications. Finally, while bibliometric analysis can give insights into publishing trends and patterns, it cannot provide a comprehensive examination of published content. Methodologies that include qualitative research might give a more nuanced view of the topic matter.

The study revealed that few of these methods have been employed in sustainable accounting research, therefore one significant proposal is to examine the use of qualitative research methodologies. Qualitative research methods can provide a more in-depth understanding of a topic and can supplement the quantitative approach of bibliometric analysis. Furthermore, the additional study might look into the relevance of sustainable accounting in fields other than commerce and information systems library science, such as development studies and educational administration. The research emphasizes the relevance of corporate culture in supporting sustainable accounting methods, hence another subject for examination is the link between business culture and sustainable accounting. Future research could additionally examine the possible uses of sustainable accounting in areas other than those included in this paper. Finally, in addition to following publishing trends on the subject, it would be beneficial to evaluate the actual impact of sustainable accounting methods on firms and society as a whole. These research ideas can help us better comprehend sustainable accounting and its possible applications.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Adams, C. A. (2017). The sustainable development goals, integrated thinking and the integrated report. Integrated Reporting (IR), 1–25.

- Adams, C. A. (2018). Debate: Integrated reporting and accounting for sustainable development across generations by universities. Public Money & Management, 38(5), 332–334. https://doi.org/10.1080/09540962.2018.1477580

- Adams, R., Jeanrenaud, S., Bessant, J., Denyer, D., & Overy, P. (2016). Sustainability‐oriented innovation: A systematic review. International Journal of Management Reviews, 18(2), 180–205. https://doi.org/10.1111/ijmr.12068

- Akbari, M., Khodayari, M., Danesh, M., Davari, A., & Padash, H. (2020). A bibliometric study of sustainable technology research. Cogent Business & Management, 7(1), 1751906. https://doi.org/10.1080/23311975.2020.1751906

- Albareda, L., & Hajikhani, A. (2019). Innovation for sustainability: Literature review and bibliometric analysis. Innovation for Sustainability: Business Transformations Towards a Better World, 35–57. https://doi.org/10.1007/978-3-319-97385-2_3

- Alhossini, M. A., Ntim, C. G., & Zalata, A. M. (2021). Corporate board committees and corporate outcomes: An international systematic literature review and agenda for future research. The International Journal of Accounting, 56(01), 2150001. https://doi.org/10.1142/S1094406021500013

- Alsharif, A. H., Md Salleh, N. Z., Baharun, R., & Rami Hashem, E. A. (2021). Neuromarketing research in the last five years: A bibliometric analysis. Cogent Business & Management, 8(1), 1978620. https://doi.org/10.1080/23311975.2021.1978620

- Ascani, I., Ciccola, R., & Chiucchi, M. S. (2021). A structured literature review about the role of management accountants in sustainability accounting and reporting. Sustainability, 13(4), 2357. https://doi.org/10.3390/su13042357

- Atkins, J., & Maroun, W. (2018). Integrated extinction accounting and accountability: Building an ark. Accounting, Auditing & Accountability Journal, 31(3), 750–786. https://doi.org/10.1108/AAAJ-06-2017-2957

- Baker, M., Gray, R., & Schaltegger, S. (2022). Debating accounting and sustainability: From incompatibility to rapprochement in the pursuit of corporate sustainability. Accounting, Auditing & Accountability Journal, 36(2), 591–619. https://doi.org/10.1108/AAAJ-04-2022-5773

- Behl, A., Jayawardena, N., Pereira, V., Islam, N., Del Giudice, M., & Choudrie, J. (2022). Gamification and e-learning for young learners: A systematic literature review, bibliometric analysis, and future research agenda. Technological Forecasting & Social Change, 176, 121445. https://doi.org/10.1016/j.techfore.2021.121445

- Benameur, K. B., Mostafa, M. M., Hassanein, A., Shariff, M. Z., & Al-Shattarat, W. (2023). Sustainability reporting scholarly research: A bibliometric review and a future research agenda. Management Review Quarterly, 1–44. https://doi.org/10.1007/s11301-023-00319-7

- Bennett, M., & James, P. (Eds.). (2017). The green bottom line: Environmental accounting for management: Current practice and future trends. Routledge.

- Bini, L., Bellucci, M., Bini, L., & Bellucci, M. (2020). Accounting for sustainability. Integrated Sustainability Reporting: Linking Environmental and Social Information to Value Creation Processes, 9–51. https://doi.org/10.1007/978-3-030-24954-0_2

- Bose, S. (2020). Evolution of ESG reporting frameworks. Values at Work: Sustainable Investing and ESG Reporting, 13–33. https://doi.org/10.1007/978-3-030-55613-6_2

- Bosi, M. K., Lajuni, N., Wellfren, A. C., & Lim, T. S. (2022). Sustainability reporting through environmental, social, and governance: A bibliometric review. Sustainability, 14(19), 12071. https://doi.org/10.3390/su141912071

- Braun, A. T., Kleine-Möllhoff, P., Reichenberger, V., & Seiter, S. (2018). Survey concerning enablers for material efficiency activities in manufacturing, their supply chains and the transformation towards circular economy (No. 2018-3). Reutlinger Diskussionsbeiträge zu Marketing & Management. https://doi.org/10.15496/publikation-23180

- Burnes, B., & Cooke, B. (2013). K urt L ewin’s field theory: A review and re‐evaluation. International Journal of Management Reviews, 15(4), 408–425. https://doi.org/10.1111/j.1468-2370.2012.00348.x

- Burritt, R. L., Herzig, C., Schaltegger, S., & Viere, T. (2019). Diffusion of environmental management accounting for cleaner production: Evidence from some case studies. Journal of Cleaner Production, 224, 479–491. https://doi.org/10.1016/j.jclepro.2019.03.227

- Busco, C., Granà, F., & Izzo, M. F. (2018). Sustainable development goals and integrated reporting. Routledge.

- Cho, C. H., Laine, M., Roberts, R. W., & Rodrigue, M. (2015). Organized hypocrisy, organizational façades, and sustainability reporting. Accounting, Organizations & Society, 40, 78–94. https://doi.org/10.1016/j.aos.2014.12.003

- Cooper, S., & Michelon, G. (2022). Conceptions of materiality in sustainability reporting frameworks: Commonalities, differences and possibilities. In Handbook of accounting and sustainability (pp. 44–66). Edward Elgar Publishing. https://doi.org/10.4337/9781800373518.00010

- Cunha, D. R., & Moneva, J. M. (2018). The elaboration process of the sustainability report: A case study. Revista Brasileira de Gestão de Negócios, 20(4), 533–549. https://doi.org/10.7819/rbgn.v0i0.3948

- De Camargo, L. F., Moraes, A., Dias, D. R., & Brega, J. R. (2020). Information visualization applied to computer network security: A case study of a wireless network of a university. In Computational science and its applications–ICCSA 2020: 20th international conference, Cagliari, Italy, July 1–4, 2020, Proceedings, Part II 20 (pp. 44–59). Springer International Publishing. https://doi.org/10.1007/978-3-030-58802-1_4

- De Stefano, F., Bagdadli, S., & Camuffo, A. (2018). The HR role in corporate social responsibility and sustainability: A boundary‐shifting literature review. Human Resource Management, 57(2), 549–566. https://doi.org/10.1002/hrm.21870

- Dhar, B. K., Sarkar, S. M., & Ayittey, F. K. (2022). Impact of social responsibility disclosure between implementation of green accounting and sustainable development: A study on heavily polluting companies in Bangladesh. Corporate Social Responsibility & Environmental Management, 29(1), 71–78. https://doi.org/10.1002/csr.2174

- Ehnert, I., Parsa, S., Roper, I., Wagner, M., & Muller-Camen, M. (2016). Reporting on sustainability and HRM: A comparative study of sustainability reporting practices by the world’s largest companies. The International Journal of Human Resource Management, 27(1), 88–108. https://doi.org/10.1080/09585192.2015.1024157

- Eng, L. L., Fikru, M., & Vichitsarawong, T. (2022). Comparing the informativeness of sustainability disclosures versus ESG disclosure ratings. Sustainability Accounting, Management and Policy Journal, 13(2), 494–518. https://doi.org/10.1108/SAMPJ-03-2021-0095

- Fagerström, A., Hartwig, F., & Cunningham, G. (2017). Accounting and auditing of sustainability: Sustainable Indicator Accounting (SIA). Sustainability: The Journal of Record, 10(1), 45–52. https://doi.org/10.1089/sus.2017.29080.af

- Ferieka, H., Meutia, M., & Taqi, M. (2022). The Growth of green accounting in Indonesia: A bibliometric analysis using R. Proceedings of the 3rd International Conference on Advance & Scientific Innovation (ICASI) (pp. 177–197).

- Fonseca, A., McAllister, M. L., & Fitzpatrick, P. (2014). Sustainability reporting among mining corporations: A constructive critique of the GRI approach. Journal of Cleaner Production, 84, 70–83. https://doi.org/10.1016/j.jclepro.2012.11.050

- Fuzi, N. M., Habidin, N. F., Janudin, S. E., & Ong, S. Y. Y. (2020). Environmental management accounting practices, management system, and performance: SEM approach. International Journal of Quality & Reliability Management, 37(9/10), 1165–1182. https://doi.org/10.1108/IJQRM-12-2018-0325

- Gil-Marín, M., Vega-Muñoz, A., Contreras-Barraza, N., Salazar-Sepúlveda, G., Vera-Ruiz, S., & Losada, A. V. (2022). Sustainability accounting studies: A metasynthesis. Sustainability, 14(15), 9533. https://doi.org/10.3390/su14159533

- Gray, R., Adams, C., & Owen, D. (2017). Social and environmental accounting. In The Routledge companion to critical accounting (pp. 243–259). Routledge.

- Hörisch, J., Burritt, R. L., Christ, K. L., & Schaltegger, S. (2017). Legal systems, internationalization and corporate sustainability. An empirical analysis of the influence of national and international authorities. Corporate Governance, 17(5), 861–875. https://doi.org/10.1108/CG-08-2016-0169

- Hörisch, J., Schaltegger, S., & Freeman, R. E. (2020). Integrating stakeholder theory and sustainability accounting: A conceptual synthesis. Journal of Cleaner Production, 275, 124097. https://doi.org/10.1016/j.jclepro.2020.124097

- Ibrahim, A. E. A., Hussainey, K., Nawaz, T., Ntim, C., & Elamer, A. (2022). A systematic literature review on risk disclosure research: State-of-the-art and future research agenda. International Review of Financial Analysis, 82, 102217. https://doi.org/10.1016/j.irfa.2022.102217

- Javaid, M., Haleem, A., Singh, R. P., Suman, R., & Gonzalez, E. S. (2022). Understanding the adoption of Industry 4.0 technologies in improving environmental sustainability. Sustainable Operations and Computers, 3, 203–217. https://doi.org/10.1016/j.susoc.2022.01.008

- Jones, P., & Wynn, M. (2021). The leading digital technology companies and their approach to sustainable development. Sustainability, 13(12), 6612. https://doi.org/10.3390/su13126612

- Khan, M. H., & Muktar, S. N. (2020). A bibliometric analysis of green human resource management based on Scopus platform. Cogent Business & Management, 7(1), 1831165. https://doi.org/10.1080/23311975.2020.1831165

- Lauwo, S. G., Azure, J.D. -C., & Hopper, T. (2022). Accountability and governance in implementing the sustainable development goals in a developing country context: Evidence from Tanzania. Accounting, Auditing & Accountability Journal, 35(6), 1431–1461. https://doi.org/10.1108/AAAJ-10-2019-4220

- Lee, W. J. (2019). Toward sustainable accounting information: Evidence from IFRS adoption in Korea. Sustainability, 11(4), 1154. https://doi.org/10.3390/su11041154

- Li, J., Herdem, M. S., Nathwani, J., & Wen, J. Z. (2022). Methods and applications for artificial intelligence, big data, internet-of-things, and blockchain in smart energy management. Energy and AI, 11, 100208. https://doi.org/10.1016/j.egyai.2022.100208

- Liu, F. H., Demeritt, D., & Tang, S. (2019). Accounting for sustainability in Asia: Stock market regulation and reporting in Hong Kong and Singapore. Economic Geography, 95(4), 362–384. https://doi.org/10.1080/00130095.2018.1544461

- Lozano, R. (2022). Organisational change management for sustainability. In Toward sustainable organisations: A holistic perspective on implementation efforts (pp. 75–88). Springer International Publishing. https://doi.org/10.1007/978-3-030-99676-5_5

- Lu, Y., Ntim, C. G., Zhang, Q., & Li, P. (2022). Board of directors’ attributes and corporate outcomes: A systematic literature review and future research agenda. International Review of Financial Analysis, 84, 102424. https://doi.org/10.1016/j.irfa.2022.102424

- Luque-Vilchez, M., & Larrinaga, C. (2016). Reporting models do not translate well: Failing to regulate CSR reporting in Spain. Social and Environmental Accountability Journal, 36(1), 56–75. https://doi.org/10.1080/0969160X.2016.1149301

- Maier, D., Maier, A., Așchilean, I., Anastasiu, L., & Gavriș, O. (2020). The relationship between innovation and sustainability: A bibliometric review of the literature. Sustainability, 12(10), 4083. https://doi.org/10.3390/su12104083

- Mancini, D., Lombardi, R., & Tavana, M. (2021). Four research pathways for understanding the role of smart technologies in accounting. Meditari Accountancy Research, 29(5), 1041–1062. https://doi.org/10.1108/MEDAR-03-2021-1258

- Maroun, W., & Lodhia, S. (2017). Sustainability and integrated reporting by the public sector and not-for-profit organizations. In Sustainability accounting and integrated reporting (pp. 101–120). Routledge.

- Mcgee, F., Ghoniem, M., Melançon, G., Otjacques, B., & Pinaud, B. (2019, September). The state of the art in multilayer network visualization. Computer Graphics Forum, 38(6), 125–149. https://doi.org/10.1111/cgf.13610

- McKinnon, A., Browne, M., Whiteing, A., & Piecyk, M. (Eds.). (2015). Green logistics: Improving the environmental sustainability of logistics. Kogan Page Publishers.

- McNamara, A. J., & Sepasgozar, S. M. (2021). Intelligent contract adoption in the construction industry: Concept development. Automation in Construction, 122, 103452. https://doi.org/10.1016/j.autcon.2020.103452

- Misra, N. N., Dixit, Y., Al-Mallahi, A., Bhullar, M. S., Upadhyay, R., & Martynenko, A. (2020). IoT, big data, and artificial intelligence in agriculture and food industry. IEEE Internet of Things Journal, 9(9), 6305–6324. https://doi.org/10.1109/JIOT.2020.2998584

- Modugno, G., & DiCarlo, F. (2019). Financial sustainability of higher education institutions: A challenge for the accounting system. Financial Sustainability of Public Sector Entities: The Relevance of Accounting Frameworks, 165–184. https://doi.org/10.1007/978-3-030-06037-4_9

- Narayanan, V., & Boyce, G. (2019). Exploring the transformative potential of management control systems in organisational change towards sustainability. Accounting, Auditing & Accountability Journal, 32(5), 1210–1239. https://doi.org/10.1108/AAAJ-04-2016-2536

- Ng, A. W. (2018). From sustainability accounting to a green financing system: Institutional legitimacy and market heterogeneity in a global financial centre. Journal of Cleaner Production, 195, 585–592. https://doi.org/10.1016/j.jclepro.2018.05.250

- Nguyen, T. H. H., Ntim, C. G., & Malagila, J. K. (2020). Women on corporate boards and corporate financial and non-financial performance: A systematic literature review and future research agenda. International Review of Financial Analysis, 71, 101554. https://doi.org/10.1016/j.irfa.2020.101554

- Nobanee, H., Alhajjar, M., Abushairah, G., & Al Harbi, S. (2021). Reputational risk and sustainability: A bibliometric analysis of relevant literature. Risks, 9(7), 134. https://doi.org/10.3390/risks9070134

- Pasko, O., Chen, F., Oriekhova, A., Brychko, A., & Shalyhina, I. (2021). Mapping the literature on sustainability reporting: A bibliometric analysis grounded in Scopus and web of science core collection. European Journal of Sustainable Development, 10(1), 303. https://doi.org/10.14207/ejsd.2021.v10n1p303

- Patten, D. M., & Shin, H. (2019). Sustainability accounting, management and policy journal’s contributions to corporate social responsibility disclosure research: A review and assessment. Sustainability Accounting, Management and Policy Journal, 10(1), 26–40. https://doi.org/10.1108/SAMPJ-01-2018-0017

- Poje, T., & Zaman Groff, M. (2022). Mapping ethics education in accounting research: A bibliometric analysis. Journal of Business Ethics, 179(2), 451–472. https://doi.org/10.1007/s10551-021-04846-9

- Qian, W., Burritt, R., Chen, J., & John Sands Ki-Hoon Lee, P. (2015). The potential for environmental management accounting development in China. Journal of Accounting & Organizational Change, 11(3), 406–428. https://doi.org/10.1108/JAOC-11-2013-0092

- Rehman, S. U., Bhatti, A., Kraus, S., & Ferreira, J. J. M. (2021). The role of environmental management control systems for ecological sustainability and sustainable performance. Management Decision, 59(9), 2217–2237. https://doi.org/10.1108/MD-06-2020-0800

- Rimmel, G. (Ed.). (2020). Accounting for sustainability. Routledge.

- Rodrigues, M., Do Céu Alves, M., Oliveira, C., Vale, V., Vale, J., & Silva, R. (2021). Dissemination of social accounting information: A bibliometric review. Economies, 9(1), 41. https://doi.org/10.3390/economies9010041

- Rounaghi, M. M. (2019). Economic analysis of using green accounting and environmental accounting to identify environmental costs and sustainability indicators. International Journal of Ethics and Systems, 35(4), 504–512. https://doi.org/10.1108/IJOES-03-2019-0056

- Sanguankaew, P., & Vathanophas Ractham, V. (2019). Bibliometric review of research on knowledge management and sustainability, 1994–2018. Sustainability, 11(16), 4388. https://doi.org/10.3390/su11164388

- Schaltegger, S. (2021). Sustainability learnings from the COVID-19 crisis. Opportunities for resilient industry and business development. Sustainability Accounting, Management and Policy Journal, 12(5), 889–897. https://doi.org/10.1108/SAMPJ-08-2020-0296

- Schaltegger, S., Beckmann, M., & Hockerts, K. (2018). Collaborative entrepreneurship for sustainability. Creating solutions in light of the UN sustainable development goals. International Journal of Entrepreneurial Venturing, 10(2), 131–152. https://doi.org/10.1504/IJEV.2018.092709

- Schaltegger, S., Christ, K. L., Wenzig, J., & Burritt, R. L. (2022). Corporate sustainability management accounting and multi‐level links for sustainability–A systematic review. International Journal of Management Reviews, 24(4), 480–500. https://doi.org/10.1111/ijmr.12288

- Schaltegger, S., Gibassier, D., & Zvezdov, D. (2013). Is environmental management accounting a discipline? A bibliometric literature review. Meditari Accountancy Research, 21(1), 4–31. https://doi.org/10.1108/MEDAR-12-2012-0039

- Schaltegger, S., Hörisch, J., & Freeman, R. E. (2019). Business cases for sustainability: A stakeholder theory perspective. Organization & Environment, 32(3), 191–212. https://doi.org/10.1177/1086026617722882

- Shen, H., Ng, A. W., Zhang, J., & Wang, L. (2020). Sustainability accounting, management and policy in China: Recent developments and future avenues. Sustainability Accounting, Management and Policy Journal, 11(5), 825–839. https://doi.org/10.1108/SAMPJ-03-2020-0077

- Shoeb, M., Aslam, A., & Aslam, A. (2022). Environmental accounting disclosure practices: A bibliometric and systematic review. International Journal of Energy Economics & Policy, 12(4), 226–239. https://doi.org/10.32479/ijeep.13085

- Slacik, J., Grüb, B., & Greiling, D. (2021). New wine in old bottles: Governing logics for applying sustainability management control systems in Austrian electric utilities. International Journal of Energy Sector Management, 16(1), 50–77. https://doi.org/10.1108/IJESM-06-2020-0016

- Sustacha, I., Baños-Pino, J. F., & Del Valle, E. (2022). Research trends in technology in the context of smart destinations: A bibliometric analysis and network visualization. Cuadernos de Gestión, 22(1), 161–173. https://doi.org/10.5295/cdg.211501is