?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study was conducted to examine the relationship among environmental, social disclosure, sustainable development, and firm performance. The data is collected from 71 mining companies listed on Vietnam’s stock market from 2018 to 2021. Research results show that the level of environmental and social disclosure has direct impact on the level of sustainable development and firm performance of the company. Moreover, the results also show that the level of environmental and social disclosure has indirect impact on the firm performance of through the sustainability variable. Through findings, some recommendations are given for promoting social and environmental disclose of Vietnamese mining companies and similar countries to raise their awareness and responsibility for social and environmental information disclosure.

1. Introduction

Mining industry has been considered as one of the important economic sectors for development in many countries. Mineral resources are the basic natural resources, an important internal resource, and a comparative advantage for the economic development of each country (Qi, Citation2020). However, mining is also said to be one of the industries with the most environmental and social impacts. In Vietnam, recently, the activities of some mining enterprises have caused serious consequences to the environment and people’s health (Nguyen et al., Citation2017). The Government has issued Directive No. 03/CT-TTg, 30 March 2015, on requiring mining enterprises to make environmental impact assessment reports, certify the completion of works on environmental protection measures, comply with regulations on management, waste treatment and payment of environmental protection fees and issues affecting society, however, the implementation situation in enterprises is different. Therefore, complying with the transparency of environmental and social information required by the sustainability report is necessary, a measure for mining companies to improve the reputation and image of the company with domestic and foreign investors. Through environmental and social information transparency and responsible accountability, businesses can strengthen stakeholder trust.

There have been many studies on the relationship between environmental and social information disclosure to sustainable development and business performance, attracting the attention of executives, managers, and researchers in the world. However, the results on this relationship are different and quite diverse in previous studies. Research by (Wasara & Ganda, Citation2019) has shown that companies with high environmental and social commitment often behave more ethically than companies with low commitment, and thus attract the engagement of human resources and attracting investment, helping the company improve efficiency and develop sustainably. Research by (Liu et al., Citation2021), shows that companies with low economic efficiency often tend to disclose more environmental and social information in order to improve the image with stakeholders. Research by (Gupta & Das, Citation2022), has found a positive relationship between environmental and social disclosure to business performance. According to (Gallego‐álvarez & Pucheta‐martínez, Citation2022), businesses with high performance tend to pay more attention to the disclosure of non-financial information. Research by (Wasara & Ganda, Citation2019) has shown that businesses with low performance often pay little attention to the information needs of stakeholders. In addition, many other scholars have also focused on the relationship between corporate social and environmental responsibility disclosure, competitive advantage, capital efficiency, financial risk, etc. different countries (Ameer & Othman, Citation2012; Chen et al., Citation2015). All studies confirm the meaning and role of responsibility and social disclosure. To date, there have been many studies related to responsibility and social disclosure and its relationship with efficient and sustainable development in the world. However, there are inconsistencies in studies on the relationship between these variables.

Vietnam is a developing country, although the government has issued Circular 155/2015/TT-BTC “Guidelines for information disclosure on stock exchanges”, which requires companies to disclose information related to environment, society, and sustainable development. However, the implementation situation in enterprises is significantly different (Hoang & Tran, Citation2022; Nguyễn et al., Citation2019). The trend of deeper and broader integration requires that Vietnamese enterprises in general and mining enterprises need to work towards disclosing environmental and social information according to international standards of Global Reporting Initiative (GRI) in order to increase trust with investors, promote the development of the global capital market, expand cooperation relations and increase the competitiveness of enterprises in the international arena. The benefits are so, but the mining business managers are still afraid that the disclosure and transparency of information on sustainable development will be costly in terms of both financial resources and implementation time. Therefore, in this period, it is necessary to carry out propaganda activities to support businesses to grasp the benefits of making and disclosing information on the environment and society, to receive the support of corporate administrators in advocating for transparent sustainable development information. In fact, in Vietnam at present, there are no mandatory regulations and specific guidelines on the disclosure of sustainable development information, so businesses have not really paid attention and have not fully believed in the effectiveness of disclosure. This research is conducted to help administrators have a more correct view of the effectiveness of information disclosure on the environment and society, encouraging businesses to be transparent about environmental and social information on sustainability reporting, increase competitive advantage and international integration.

The rest of the paper is structured as follows: Section 2 discusses the relevant research and theoretical background. Part 3 builds research hypothesis, develops model and describes the research method used. Section 4 reports the research results and discussion. Section 5 concludes and recommends.

2. Literature review and theoretical background

2.1. Literature review

Sustainable development goals require businesses to consider the impact of actions in the present on the ecosystem, society and environment in the future. Therefore, information related to the environment and society has been and will receive the attention of business administrators, as well as scientific researchers. In the world, there are quite a few studies on environmental and social disclosure on corporate sustainability reports, case studies include Research by (Ameer & Othman, Citation2012) Collected data from 100 sustainable development companies globally in the period 2006 – 2010, research results have shown that there is a two-way relationship between corporate social responsibility practices and financial performance of the business (financial performance measured through ROA, profit before tax and operating cash flow). Research by (Chen et al., Citation2015) collected data from 75 companies. The company prepares a report according to GRI standards for the period 2012 – 2015, social responsibility information is evaluated according to the GRI standard version 2012 including 45 sets of indicators, this research self-assess the level of information disclosure for each indicator, numbers on a scale from 1 to 5. Research results show that the level of information disclosure on human rights, product responsibility and social responsibility has a small relationship, extreme to operational efficiency through ROE.

Research by (Cheng et al., Citation2016) uses the data set from Thomson Reuters ASSET4 to evaluate social responsibility information with a scale of 0 and 1. The results from this study show that the publication of 2008 social responsibility report has a positive effect on the 2009 performance of listed companies in China. Research by (Waworuntu et al., Citation2014), with the aim of examining the relationship between stakeholder engagement performance and corporate financial performance, to establish the extent and pattern information disclosure of leading listed companies in the ASEAN region. The research results show that the leading enterprises in Asia have increased their awareness of reporting social responsibility information because of the positive influence of this information on the performance of their businesses.

Research by (Berthelot et al., Citation2012) was conducted to address the question: Do investors attach importance to sustainability reports, the sample of the study is Canadian companies listed on Toronto Stock Exchange. The results show that investors appreciate and are very interested in the information presented in this type of report. The findings of the study are intended to support the relevance of the global sustainability reporting initiatives and play a role in promoting and enabling businesses to commit to voluntary environmental and society. Research by (Wasara & Ganda, Citation2019) was conducted to examine the relationship between sustainability disclosure and financial performance of mining companies listed on the Johannesburg Stock Exchange (JSE), data are extracted from sustainability reports over a 5-year period from 2010 to 2014. The results show that there is a positive relationship between environmental and social disclosure and financial performance. This implies that increased corporate reporting on environmental and social issues leads to higher financial performance. The study recommends policy changes for businesses, from voluntary to mandatory environmental and social disclosure.

Study of (Liu et al., Citation2021) was carried out to examine the linear and non-linear relationship between corporate social performance and banking performance using a dataset. Data are collected from Chineses banks for the period 2009 to 2018. The results show that the interaction variable of CSR (GOV*SOC) exhibits a negligible influence on return on assets (ROA), return on capital owner (ROE) and nominal profit margin (NIMP). Furthermore, other CSR variables such as (GOV*ENV) have a significant positive effect on ROA and ROE.

Research by (Gupta & Das, Citation2022) has found that if social responsibility disclosure strategies and measurement techniques are adequately addressed, the true effectiveness of CSR disclosure can be observed. The findings confirm a positive relationship between the disclosure of social responsibility and financial performance. The study by (Gallego‐álvarez & Pucheta‐martínez, Citation2022) was carried out to analyze the impact of corporate social responsibility disclosure on corporate performance. The sample used consisted of 9861 year-over-year observations of companies across the country collected from the Thomson Reuters database from 2009 to 2018. By using a generalized time-lapse estimator (GMM), research has found a positive relationship between social responsibility and corporate performance. In addition, the study also shows that ensuring social responsibility plays a positive role as a mediator between CSR disclosure and corporate performance. Thus, in the world in recent years, there have been quite a few studies evaluating the impact of social responsibility information disclosure on the performance of businesses; however, the studies were carried out in different countries, different ways to evaluate the variables in the model, so the research results are different.

In VietNam, the studies related to environmental and social disclosure usually include the following groups: (1) Studies that assess the importance of environmental and social disclosure on sustainability report to attract investment, improve the reputation and image of enterprises in the market, case studies include, research by (Hsu & Bui, Citation2022; Le et al., Citation2022; Tran, Citation2022); (2) Studies on factors affecting environmental and social information disclosure, the factors tested in the model include: Enterprise size, financial leverage, board size, the independence of the chief executive officer and independent auditor, researched by (Nguyễn et al., Citation2019; Pham et al., Citation2021; Thị Thanh Thủy & Hồng Nhung, Citation2021) (3) Studies on the impact of sustainability information disclosure on business performance, such as: (Hoang & Tran, Citation2022; Mai, 2022). However, the way to measure the variables on the level of information disclosure about society, the environment, and the measurement of performance varies between studies. Research by (Hoang & Tran, Citation2022), with a sample of 27 construction companies from 2014 to 2018, measures operational efficiency through the ROA indicator, and measures the level of information disclosure through a questionnaire. Research by ,My & My, Citation2022) measures information disclosure criteria through mandatory criteria, questionnaires are built with or without information disclosure. Thus, because the criteria for measuring the variables are different, so the level of impact of information disclosure on performance is different between studies, moreover this difference is also explained. This is because the selected sample is companies of different industries, with different research periods. Therefore, the research conducted with the sample of mining companies listed on the Vietnamese stock market for the period of 2018 to 2021 is necessary, to evaluate the impact of environmental and social disclosure on firm performance, is not entirely consistent with previous studies.

2.2. Theoretical background

To explain the motivation for businesses to publish sustainable development information in general and environmental and social information in particular, this research has applied the following theories:

- Signalling theory: This theory enables companies to engage with stakeholders more effectively by achieving all five dimensions of sustainability and explains investor responses to sustainability disclosures. Signaling theory suggests that businesses can attempt to signal “good news” using mandatory financial reporting and voluntary reporting of their environmental and social performance (Azzam et al., Citation2020; Garg, Citation2015). Research by (Laskar & Maji, Citation2016) argues that when some investors have more personal information than others, asymmetric information between firms and investors leads to adverse investor. To avoid this situation, enterprises voluntarily disclose information and give positive signals to the market (Laskar, Citation2018). According to this theory, the larger the firm, the greater the information imbalance (Connelly et al., Citation2011). In addition, companies with higher profits will tend to disclose more information to provide positive signals to investors about growth prospects, which will positively affect their stock prices.

- Stakeholder theory: Stakeholder theory was first used by Edward Freeman in 1984 in his work on strategic management (Guthrie & Parker, Citation1989). Stakeholders include any person or group of people who are interested in the company because they may be affected by the company’s activities (Freeman, Citation2001). Edward Freeman divides the parties with related interests and obligations into two groups: inside and outside the business. Managers and employees are stakeholders inside the business, stakeholders outside the business such as shareholders, suppliers and government agencies. Stakeholder theory has many applications, one of them for the field of information disclosure, the success of a company depends on the cooperation of stakeholders, so the company has a responsibility to provide information to stakeholders instead of just providing information to owners (Nejati et al., Citation2010). According to the theory of stakeholders, the greater the pressure from stakeholders, the more transparent businesses are required, especially those related to the environment and society, to meet the demand for information of related parties.

- Legitimacy theory: The theory of legitimacy is defined by Dowling & Pfeffer as follows: “An entity can exist when its value system is consistent with the value system of the larger social system” (Brown & Deegan, Citation1998). Inheritance and development of legalization theory, (Guthrie & Parker, Citation1989) argues that the theory of legalization is related to the strength of society, enterprises doing business in society must sign a social contract that managers agree to perform. The terms of this contract can be made clear, that is, the provisions of the law, or there are terms that are not clearly expressed, depending on the expectations of the social community. Legalization theory explains the responsibility of enterprises to perform environmental accounting as follows: (1) The need to implement environmental accounting comes from society, from dissatisfaction of the Government, pressures from the requirements of workers, consumers and stakeholders (Freeman, Citation2001); (2) Disclosure of information about the environment is the driving force for enterprises to achieve their desire to legalize their activities, through which to promote their corporate image to benefit businesses (Guthrie & Parker, Citation1989). Thus, disclosing environmental and social information publicly in the annual report is a way of expressing the strategy of the enterprise. This strategy implies that the business is operating legally and in a socially responsible manner.

3. Research model and research methodology

3.1. Research model

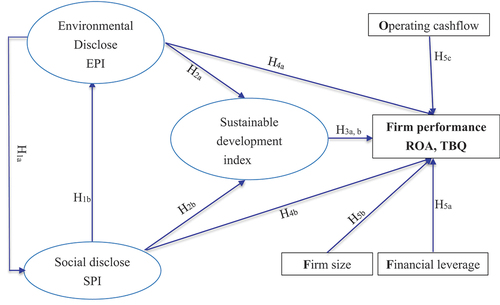

From the overview of studies and the theoretical basis for the explanation of the motivation for enterprises to disclose information about sustainable development, the model has been proposed to evaluate the impact between the level of disclosure environmental and social information according to GRI standards in reports on sustainable development and performance of mining enterprises listed on Vietnam’s stock market. The model was established based on previous studies, background theory, and development to match the characteristics of the research subjects who are mining enterprises in Vietnam, the model was then consulted by scientific researchers in the field for adjustment. The model is re-validated by experts and the completed model is included as shown in Figure .

Figure 1. Research model .

3.2. Research methodology

The research sample includes 71 mining companies listed on HOSE, HNX, OTC, and UPCOM out of a total of 82 companies as of 31 December 2021, accounting for 86.59% of the total. The data is collected from 2018 to 2021. Financial information of listed companies is taken from http://finance.vietstock.vn. The level of disclosure of environmental and social accounting information is obtained from annual reports, sustainability reports and corporate governance reports published on the Websites of 71 companies in the sample. The data used for the analysis include 262 observed variables belonging to 71 companies in 4 consecutive years 2018–2021, the research sample is presented in Table .

Table 1. Research sample statistics

The data are collected is calculated into variables in accordance with research requirements by Excel. The final step involves the calculated variables to be stored, analyzed, and tested through STATA 17.

3.3. Variable measurements

3.3.1. Environmental, social disclosure (EPI, SPI)

According to the Global Reporting Initiative’s Sustainability Reporting Guidelines (GRI, Citation2021), the total number of items to be disclosed is required for each environmental and social component. Regulatory environmental information covers eight areas from 301 to 308 and includes 32 items to be disclosed. Social information covers 19 fields from 401 to 419 and includes 40 items to be published. Depending on the content and the way the company publishes information related to each item to evaluate the score for each specified item. Scores are calculated in Table .

Table 2. Method to Assess Environmental and Social disclosure

The level of information disclosure for each specified item is weighted, depending on the quality of information provided to evaluate the score for each item, then average for each field and calculate the level of disclosure. Environmental information (EPI), the level of social information disclosure (SPI) is calculated according to the following formula: Information disclosure level of enterprises X = (Yi is the score of the ith information factor published by enterprise X, n is the total number of items to be published) (Wasara & Ganda, Citation2019). Similarly, the research has calculated the EPI and SPI indicators for each enterprise by year.

3.3.2. Sustainable development index (SDI)

To measure the sustainability index of enterprises, this research relies on the guidance of determining the Enterprise Sustainability Index by VBCSD 2021 (CSI, Citation2021). Enterprises in the research sample are enterprises that have participated in the program of Assessment and Announcement of Sustainable Businesses in Vietnam in 2021, research data is collected in conjunction with the time when enterprises declare declared to participate in the program in 2021; however, this research designed to learn more about the status of declaring items for 4 consecutive years from 2018 to 2021, on the same set of indicators in 2021. SDI set of indicators 2021 with 119 indicators in 4 areas: Sustainable Development Performance Index, Governance Index; Environmental Index; and Labor-Social Index. Each item is rated yes (1) or no (0). The total score of all items announced by the enterprise is Nsdi and divided by the total number of items to be announced is 119, we will calculate the SDI for each enterprise.

3.3.3. Firm performance

Firm performance is usually measured by four dimensions including value drivers, financial ratios, non-financial information and stock prices (Venkatraman & Ramanujam, Citation1986). However, this study only focuses on financial indicators to measure the performance of enterprises. In general, financial ratios to measure performance are developed from an accounting point of view, from a market point of view, or a combination of both. From an accounting point of view, operational efficiency is usually measured by return on assets (ROA), return on equity (ROE), and return on sale (ROS) ratios. From a market point of view, performance is measured by earning per share (EPS). The combined view of the two often uses the Tobin’s Q (TBQ) index to measure the performance of an entity, especially in relation to sustainability information (Ameer & Othman, Citation2012; Burhan & Rahmanti, Citation2012). TBQ shows the potential value of a company, so this metric helps to capture whether stakeholders appreciate the company stemming from the company’s social perception (Laskar, Citation2018). TBQ is a measure that combines accounting and market perspectives, which is calculated by dividing the market value by the book value of assets (Sum, Citation2013). In this study, the author selected two indicators, representing the views using financial ratios to measure performance, they are ROA and TBQ. This study uses these two indexes because of their representativeness.

3.3.4. Control variables

In order to enhance the explanatory power, this research has included in the model a number of control variables that have an impact on performance that have been tested from previous studies, namely (See Table ):

Table 3. The way to evaluate the Control Variables

4. Results and discussion

4.1. Descriptive statistics

Table presents the results of statistical analysis of dependent variables, independent variables and control variables in the research model. Theo (Tauchen, Citation1986), for the estimate to be reliable when performing regression analysis is n > 200. Theo (Hair et al., Citation2011), with 15–20 observations for a variable to be estimated, so the minimum sample size for the study is 120. Combining these principles, the sample size selected by the author is 262 observations of 71 enterprises, accounting for 86.59% in the overall is reasonable, the results ensure reliability. Table shows that the average environmental disclosure index is 2.615 and ranges from 1.287 to 3.947. The Social Disclosure Index averaged 2.987 and ranged from 1.965 to 3.925. The Sustainability Index averaged 0.798 and ranged from 0.386 to 1.000. It proves that the companies in the sample pay great attention to the disclosure of information to participate in the program of Assessment and Disclosure of Sustainable Enterprises. Firm sizes range from 2.765 to 15.768, showing that the size of enterprises in the sample is quite diverse. From those numbers, the research sample is quite broad enough to deduce the results of the population.

Table 4. Statistical analysis

4.2. Evaluation of correlation between variables

Table presents the results of the correlation coefficient test between the variables and the multicollinearity test. The results show that there is a correlation between the independent variables, the dependent variable and the control variable of the model, the performance of the business is positively correlated with the variables: Level of environmental, social information disclosure, sustainable development index, business size, cash flow from business activities and negative relationship (negative correlation) with financial leverage variable. At the same time, all pairs of correlated variables have a value of less than 0.8 and the Variance Inflation Factor (VIF) of the independent variables are all<5, which proves that between the independent variables does not occur multicollinearity phenomenon.

Table 5. Correlation and multicollinearity test

4.3. Discussing research results

The test results on the impact of environmental and social information disclosure on the sustainable development of enterprises are presented in Table . The results show that the hypothesis H1a is accepted and hypothesis H1b is rejected. It proves that the level of environmental disclosure has a significant impact on the level of social disclosure; however, the effect of social disclosure on environmental disclosure is not found. It is possible to explain this result that, once enterprises are interested in environmental disclosure, they are also interested in social disclosure, with the aim of satisfying stakeholders. Besides, some businesses think that just paying attention to social information disclosure is enough to satisfy stakeholders and attract investment. This result is consistent with the study of (Laskar, Citation2018), but has the opposite result with the study of (Mai, 2022). Hypothesis H2a and H2b are accepted, indicating that the level of environmental and social disclosure has a positive and strong influence on the sustainable development of the company. It explains that stakeholders are increasingly interested in environmental and social information, so the publication of environmental and social information in the annual report is one of the effective ways to attract investment, increase the efficiency of production and business activities and help enterprises develop sustainably. This result is consistent with the study of (Liu et al., Citation2021; Wasara & Ganda, Citation2019).

Table 6. Summary of the results of 1 and 2 hypothesis testing

The test results on the direct relationship and the indirect relationship of environmental and social disclosure to the performance of enterprises are presented in Table . The results show that, when considering variables depends on ROA, only the direct impact of environmental performance index on ROA of sample firms is considered. The β -path coefficient of environmental performance is positive but is not right, at the level (β = 0.258, p value<0.05). Moreover, the direct relationships of social performance index are not significant at 10% levels. The results only support for H3a, but none for H3b when considering the direct correlations with ROA. In addition, for the relationship between environmental, social performance index and ROA, this study discovers that SDI variable serves as a full mediator. Such a mediator is indirect only mediation, alternatively SDI fully mediates the economic/environmental disclosure to ROE. The direct effect of SDI in the relationship between social/environmental and ROE is statistically significant. It means that social performance and environmental performance lead to SDI and SDI in turn leads to higher financial performance measured by ROA. This result is a strong indicator that there is a relationship between environmental performance, social performance and financial performance, thus supporting for both H4a and H4b in terms of ROA as an endogenous construct.

Table 7. Summary of the results of the 3, 4 and 5 hypotheses testing

In terms of TBQ as dependent variable, both the direct impact of environmental, social performance on TBQ of sample firms is considered. The β -path coefficient of all is positive and statistically significant. The results support for all H3a and H3b when considering the direct correlations with TBQ. In addition, this result is a strong indicator that there is a relationship between environmental social performance on financial performance, thus supporting for both H4a and H4b in terms of TBQ as endogenous construct. This result is consistent with the study of (Gupta & Das, Citation2022) but has the opposite result with the study of (My & My, Citation2022).

To minimise the impact of other variables that may explain observed relationships with firm performance, three control variables (LEV, SIZ, and OCF) are included within the regression models. The connection between financial leverage and ROA is not significant and neither is size and ROA, thus it is impossible to make any conclusions regarding both of control variables, the opposite result with the study of (Wasara & Ganda, Citation2019). The interactions between financial leverage and TBQ are significant at 5% level, size and TBQ are significant at 10% level, indicating that financial leverage and size help to lead to higher financial performance measured by TBQ. The effect of operating cashflow on ROA or TBQ is significantly positive, indicating higher rate of operating cash flow creates a firm’s better financial performance. This result is consistent with the study of (Azzam et al., Citation2020; Gupta & Das, Citation2022).

5. Conclusion and recommendation

Section presents the results and discusses the results of the study. The results confirm the direct and indirect positive impact of the level of environmental and social information disclosure on economic performance through the meditated role of sustainable development. This finding is similar to previous studies such as (Azzam et al., Citation2020; Gupta & Das, Citation2022), of (Liu et al., Citation2021; Wasara & Ganda, Citation2019). In addition, the factors of financial leverage, business size and operating cash flow are also influencing factors to the level of sustainable development and business performance. Therefore, the transparency of information related to the environment and society is very necessary for businesses in the process of integrating with the international market. Transparency of information on social responsibility benefits both organizations and society, especially increasing the competitiveness of listed companies in the international arena, when investors are increasingly interested, paying attention more emphasis on corporate social responsibility. Therefore, right now, businesses need to have actions and policies to create favorable conditions for listed companies to publish environmental and social information on sustainable development reports. Based on the results of practical research, the study has proposed some recommendations to improve the level of social responsibility information disclosure of listed mining companies in Vietnam and other developing countries.

Firstly, there exists a direct relationship between environmental disclosure, social information disclosure, environmental and social information disclosure to the level of sustainable development. Therefore, to maintain and develop sustainably, mining enterprises need to fully implement solutions and plans according to the environmental impact assessment report in order to handle and minimize the risks on the environment. The formulation and implementation of plans for environmental improvement and restoration must be done right in the process of mineral extraction. To enforce and control the process of publicizing environmental and social impacts in mining enterprises, the state needs to have strict regulations and specific guidelines on requirements for preparing and presenting sustainability reports according to GRI standards.

Second, there exists a direct relationship between environmental and social disclosure to business performance, as well as an indirect relationship through the mediating role of sustainable development. Therefore, in order to improve the performance of mining enterprises themselves, it is necessary to have specific regulations on voluntary transparency of information on sustainable development reports. Mining enterprises need to step up investment in technology. Applying research and transferring advanced and environmentally friendly technologies while still creating products of high economic value. Mining enterprises need to increase investment in financial resources for the treatment of pollutants generated in the process of mining and using minerals such as building safe landfills, treating wastewater handling dust and harmful emissions, transporting and handling hazardous wastes.

Based on applying qualitative and quantitative research methods, this research assessed the impact of environmental and social information disclosure on the level of sustainable development and performance of mining companies. The results of the study once again confirm the role of information transparency, especially information related to the environment and society, in promoting growth and improving business performance. The results imply to the managers of enterprises in raising awareness about information disclosure on environment and society. The article contributes to richer research on sustainable development of information disclosure, as well as contributes to promoting environmental and social information disclosure in mining enterprises in the future. However, there are some limitations such as: (1) Operational efficiency in the study is only measured through financial performance with two indicators ROA and TBQ, without considering other measurement options. (2) The study has not considered the impact of environmental and social information disclosure on other indicators such as investment attraction, competitiveness index, financial risk, etc. However, the study considers these as suggestions for future studies.

Acknowledgments

This research is funded by the National Economics University (NEU), Vietnam. Author thanks anonymous reviewers for their contributions and the NEU for supporting this research.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Ameer, R., & Othman, R. (2012). Sustainability practices and corporate financial performance: A study based on the top global corporations. Journal of Business Ethics, 108(1), 61–20. https://doi.org/10.1007/s10551-011-1063-y

- Azzam, M., AlQudah, A., Abu Haija, A., Shakhatreh, M., & Ntim, C. G. (2020). The association between sustainability disclosures and the financial performance of Jordanian firms. Cogent Business & Management, 7(1), 1859437. https://doi.org/10.1080/23311975.2020.1859437

- Berthelot, S., Coulmont, M., & Serret, V. (2012). Do investors value sustainability reports? A Canadian study. Corporate Social Responsibility & Environmental Management, 19(6), 355–363. https://doi.org/10.1002/csr.285

- Brown, N., & Deegan, C. (1998). The public disclosure of environmental performance information—a dual test of media agenda setting theory and legitimacy theory. Accounting and Business Research, 29(1), 21–41. https://doi.org/10.1080/00014788.1998.9729564

- Burhan, A. H. N., & Rahmanti, W. (2012). The impact of sustainability reporting on company performance. Journal of Economics, Business, & Accountancy Ventura, 15(2), 257–272. https://doi.org/10.14414/jebav.v15i2.79

- Chen, L., Feldmann, A., & Tang, O. (2015). The relationship between disclosures of corporate social performance and financial performance: Evidences from GRI reports in manufacturing industry. International Journal of Production Economics, 170, 445–456. https://doi.org/10.1016/j.ijpe.2015.04.004

- Cheng, S., Lin, K. Z., & Wong, W. (2016). Corporate social responsibility reporting and firm performance: Evidence from China. Journal of Management & Governance, 20(3), 503–523. https://doi.org/10.1007/s10997-015-9309-1

- Connelly, B. L., Certo, S. T., Ireland, R. D., & Reutzel, C. R. (2011). Signaling theory: A review and assessment. Journal of Management, 37(1), 39–67. https://doi.org/10.1177/0149206310388419

- CSI. (2021). VBCSD The vietnam business council for sustainable development. https://vbcsd.vn/en/

- Freeman, R. E. (2001). A stakeholder theory of the modern corporation. Perspectives in Business Ethics Sie, 3(144), 38–48.

- Gallego‐álvarez, I., & Pucheta‐martínez, M. C. (2022). The moderating effects of corporate social responsibility assurance in the relationship between corporate social responsibility disclosure and corporate performance. Corporate Social Responsibility & Environmental Management, 29(3), 535–548. https://doi.org/10.1002/csr.2218

- Garg, P. (2015). Impact of sustainability reporting on firm performance of companies in India. International Journal of Marketing and Business Communication, 4(3), 38–45. https://doi.org/10.21863/ijmbc/2015.4.3.018

- GRI. (2021). GRI Universal Standar https://www.globalreporting.org/media/zauil2g3/public-faqs-universal-standards.pdf.

- Gupta, J., & Das, N. (2022). Multidimensional corporate social responsibility disclosure and financial performance: A meta‐analytical review. Corporate Social Responsibility & Environmental Management, 29(4), 731–748. https://doi.org/10.1002/csr.2237

- Guthrie, J., & Parker, L. D. (1989). Corporate social reporting: A rebuttal of legitimacy theory. Accounting and Business Research, 19(76), 343–352. https://doi.org/10.1080/00014788.1989.9728863

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLSSEM: Indeed a Silver Bullet. Journal of Marketing Theory & Practice, 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Hoang, B. A., & Tran, T. T. H. (2022). Corporate social responsibility disclosure and financial performance of construction enterprises: Evidence from Vietnam. CIGOS 2021, Emerging Technologies and Applications for Green Infrastructure, 1505–1514. https://doi.org/10.1007/978-981-16-7160-9_152

- Hsu, Y., & Bui, T. H. G. (2022). Consumers’ perspectives and behaviors towards corporate social responsibility—A cross-cultural study. Sustainability, 14(2), 615. https://doi.org/10.3390/su14020615

- Laskar, N. (2018). Impact of corporate sustainability reporting on firm performance: An empirical examination in Asia. Journal of Asia Business Studies, 12(4), 571–593. https://doi.org/10.1108/JABS-11-2016-0157

- Laskar, N., & Maji, S. G. (2016). Disclosure of corporate social responsibility and firm performance: Evidence from India. Asia-Pacific Journal of Management Research and Innovation, 12(2), 145–154. https://doi.org/10.1177/2319510X16671555

- Le, B. T. H., Nguyen, N. Q., & Nguyen, C. V. (2022). Assessment of the quality of non-financial information disclosure: Empirical evidence from listed companies in Vietnam. The Journal of Asian Finance, Economics & Business, 9(5), 111–118.

- Liu, Y., Saleem, S., Shabbir, R., Shabbir, M. S., Irshad, A., & Khan, S. (2021). The relationship between corporate social responsibility and financial performance: A moderate role of fintech technology. Environmental Science & Pollution Research, 28(16), 20174–20187. https://doi.org/10.1007/s11356-020-11822-9

- My, S. T., & My, H. T. (2022). Relationship between corporate social responsibility and bank performance of listed banks in Vietnam. Journal of Hunan University Natural Sciences, 49(1), 212–219. https://doi.org/10.55463/issn.1674-2974.49.1.27

- Nejati, M., Bin, A. S., & Amran, A. B. (2010). Sustainable development: A competitive advantage or a threat? Business Strategy Series, 11(2), 84–89. https://doi.org/10.1108/17515631011026407

- Nguyen, N. B., Boruff, B., & Tonts, M. (2017). Mining, development and well-being in Vietnam: A comparative analysis. The Extractive Industries and Society, 4(3), 564–575. https://doi.org/10.1016/j.exis.2017.05.009

- Nguyễn, L. S., Tran, T. T. H., & Nguyen, K. H. (2019). Factors affecting the level of disclosure of environmental accounting information: A case study of mining companies listed on the Vietnamese stock market. Development Economics Journal, March 261, 2019, 9.

- Pham, D. C., Do, T. N. A., Doan, T. N., Nguyen, T. X. H., Pham, T. K. Y., & Tan, A. W. K. (2021). The impact of sustainability practices on financial performance: Empirical evidence from Sweden. Cogent Business & Management, 8(1), 1912526. https://doi.org/10.1080/23311975.2021.1912526

- Qi, C. -C. (2020). Big data management in the mining industry. International Journal of Minerals, Metallurgy & Materials, 27(2), 131–139. https://doi.org/10.1007/s12613-019-1937-z

- Sum, V. (2013). Tobin’s Q and stock market performance. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2293527

- Tauchen, G. (1986). Finite state markov-chain approximations to univariate and vector autoregressions. Economics Letters, 20(2), 177–181. https://doi.org/10.1016/0165-1765(86)90168-0

- Thị Thanh Thủy, V., & Hồng Nhung, Đ. (2021). Green investment for sustainable development Empirical research in Vietnamese enterprises. Journal of Development Economics, 294, December 2021, 9.

- Tran, N. T. (2022). Impact of corporate social responsibility on customer loyalty: Evidence from the Vietnamese jewellery industry. Cogent Business & Management, 9(1), 2025675. https://doi.org/10.1080/23311975.2022.2025675

- Venkatraman, N., & Ramanujam, V. (1986). Measurement of business performance in strategy research: A comparison of approaches. Academy of Management Review, 11(4), 801–814. https://doi.org/10.2307/258398

- Wasara, T. M., & Ganda, F. (2019). The relationship between corporate sustainability disclosure and firm financial performance in Johannesburg Stock Exchange (JSE) listed mining companies. Sustainability, 11(16), 4496. https://doi.org/10.3390/su11164496

- Waworuntu, S. R., Wantah, M. D., & Rusmanto, T. (2014). CSR and financial performance analysis: Evidence from top ASEAN listed companies. Procedia-Social & Behavioral Sciences, 164, 493–500. https://doi.org/10.1016/j.sbspro.2014.11.107

Appendix 1

CSI 2021 Vietnam Corporate Governance Sustainability index