Abstract

Implementing an enterprise resource planning (ERP) system is crucial if a company wants to compete globally and keep up with technological advances. This study examines the effect of information sharing and competent personnel on ERP. This study takes a quantitative approach using a questionnaire tested with covariance-based structural equation modelling. The sample includes 338 respondents from several Indonesian state-owned enterprises. The results show that information sharing positively affects the success of ERP system implementation. Next, competent personnel also positively affect the success of ERP implementation. Overall, this research is helpful for firms who want to implement an ERP system to manage information and personal arrangements accordingly so that the system can run as expected.

PUBLIC INTEREST STATEMENT

This study examines the impact of the individual capabilities of ERP users and information management in supporting the success of ERP implementation. The research was conducted taking the setting of Indonesian SOEs considering that many BUMNs have invested extensively expensivelyxtensivelyexpensively in ERP but failed and are not used in their daily activities. Concerns about ERP implementation failures inspire the emergence of the possibility of the end of game from ERP which is disastrous for BUMN companies in Indonesia. The role of personal competence and information management is the main determinant for end-of-game of game prevention of ERP.

1. Introduction

Companies must have an information system capable of providing reliable and consistent information on all activities to compete and survive (Ben Moussa & El Arbi, Citation2020; Elsayed et al., Citation2021). As a company’s leading resource, information must be managed to provide optimal benefits for managerial decision-making. Likewise, the benefits of information management in state-owned enterprises (SOE), as the main pillars of the national economy, have an essential role because SOEs are tasked with contributing to the development of the national economy (Ben Moussa & El Arbi, Citation2020), Traditional information governance results in various problems, such as data redundancy, late reports, and inappropriate decision-making. Therefore, there is a need for digital transformation in information management (Elsayed et al., Citation2021).

Digital transformation is an important factor in innovation development in today’s rapidly and dynamically growing global economy (Elsayed et al., Citation2021; Han et al., Citation2023; Liu & Zhao, Citation2022; Urban & Matela, Citation2022). One part of digital transformation is data sharing using a system capable of driving economic progress (Liu & Zhao, Citation2022; Wongsansukcharoen & Thaweepaiboonwong, Citation2023). Companies use digital technology to create or modify existing business models and processes or support organisational transformation (Plekhanov et al., Citation2022). Enterprise Resource Planning (ERP) has become a critical investment for firms that wish to maintain competitive advantages and succeed (Al-Okaily et al., Citation2021).

Essentially, an ERP system can be defined as one that integrates all subsystems, components, or elements that work together to achieve a mutual goal (Estensoro et al., Citation2022). Many manufacturing companies have successfully applied ERP systems (Wang et al., Citation2021). An ERP system covers all aspects of its business operations. Information technology has changed the receipt of information through data processing and storage (Plekhanov et al., Citation2022). It can change a company’s perspective and how it achieves its organisational goals. Thus, an ERP system can be considered a company-wide information system that integrates all aspects of a business.

It typically includes a database, one main applicationa ation, and unified interface across the entire enterprise (Plekhanov et al., Citation2022). It encompasses and tightly integrates everything from human resources to sales, manufacturing, distribution, accounting, and supply-chain management. This integration benefits companies in several ways; it enables companies to quickly react to competitive pressures and market opportunities, provide more flexible product configurations, reduce inventory, and tightener supply chains (Plekhanov et al., Citation2022)

For companies, success is the ability to achieve their goals, organise changes in shape and structure, and focus on processes, methods, and technology (Cregård, Citation2022). Company managements increasingly recognise that science-based expertise is conducive to good performance (Rodrigues et al., Citation2022). Successful ERP implementation improves an organisation’s performance by integrating all operational aspects. Specifically, the benefits of using ERP (Elsayed et al., Citation2021) include: 1) reducing labour costs in sales, finance, purchasing, human resources, and inventory; 2) reducing customer service cycle times in order, billing, shipping, payroll cycles and supporting supplier activities in order, information, and payment; 3) increasing productivity in terms of laborlabour, increased production volume, and reduced overtime; 4) improving quality in terms of data reliability and accuracy; and 5) improving customer service by facilitating access to customer inquiry data (Cregård, Citation2022). Other benefits include better financial management, for example, of assets.

Information systems are required to collect, process, and report information related to businesses (Istianingsih, Citation2021). The accuracy of the information system design is essential. The success of the implementation of an information system reflects a company’s intellectual capital (Rodrigues et al., Citation2022). ERP is a computing system that allows companies to automate raw material inventory, financing, and resource management using a database (Cregård, Citation2022). This generates real-time information about the corporate environment. The basis of an ERP system is a software application that provides a comprehensive solution fororganisational processes by enabling information and data flows. An ERP system administers processes such as financial accounting, customers, human resources, sales, marketing, and supply chains (Elsayed et al., Citation2021). The five elements are 1) storage, 2) administration and control, 3) human resources, 4) products, and 5) warehouse management. ERP systems are “comprehensive and packaged software that seeks to integrate the entire business process, and it’s to present a holistic business view of one information and IT [information technology] architecture” (Elsayed et al., Citation2021).

We convey that previous research examining the success of ERP has yet to accommodate the importance of personnel competence which is often the main factor in the failure of ERP implementation. This research fills this gap to prove that the quality of human resources in SOEs in Indonesia is the main determining factor for the success of ERP implementation, so it is not the end game. The bottom line of the End is the failure of the ERP implementation, which is disastrous for companies, mainly state-owned enterprises in Indonesia, which have invested heavily in ERP but failed. Consequently, the current paper seeks to contribute to the existing literature. First, adding a new variable, namely competent personnel, which has not been studied before as a determining factor for the end game of ERP implementation, Second, providing empirical evidence regarding the success of ERP implementation in Indonesian SOEs, Third, contributing to the development of knowledge regarding the critical success factors of ERP, and Fourth provide an analysis of the importance of training and information management among organisational members implementing ERP.

2. Background

Companies that implement and adopt ERPs include forest products, communications, professional services, and telecommunications companies (Rodrigues et al., Citation2022). Essentially, the more ERP software packages evolved, the more companies began using them. One such company in Indonesia is PT. Hutama Karya (Persero) officially began the transformation of its business processes by implementing ERP technology in 2022. Similarly, hundreds of billions of rupiah have been invested in Information Technology in all SOEs in Indonesia. With the flexibility to manage their funds, the configurations of Information Technology investments by SOEs have been diverse. Shahab et al. (Citation2019) point that was a difference between SOEs and non-SOEs related to financial difficulties in companies implementing CSR. The results of the research by (Shahab et al., Citation2019)show that non-state-owned companies can reduce financial difficulties when implementing CSR compared to state-owned companies. These results indicate that there are differences in the characteristics of SOEs and non-SOEs in dealing with the possibility of distress

Importantly, ERP is very expensive. Therefore, its successful implementation is a crucial factor for companies (Abu Madi et al., Citation2022). Measuring efficiency and productivity is relatively easy for most production goods manufacturing companies (Jaldell, Citation2019). However, measuring the successful implementation of an information system remains challenging. ERP system failure can occur because of complexity during usage, integration problems, lack of funds, project scheduling discrepancies, and user resistance to change. In general, ERP implementation requires approximately 0.82% of a company’s income, but can reach 13.65% of the income of small companies (Dewi & Asriani, Citation2019). Further, there are many cases in Indonesia where ERP implementation takes much longer than the general practice of 6 to 12 months (Dewi & Asriani, Citation2019). While many companies have successfully implemented ERP systems, research (Rodrigues et al., Citation2022) shows that more than half of ERP buyers were not entirely satisfied after finalising the ERP implementation process.

(Al-Okaily et al., Citation2021), examines the determinants of ERP user satisfaction. (Al-Okaily et al., Citation2021) draw upon the Information System Success Model (ISSM) to explore the influence of system, information, and service quality on the perceived usefulness and user satisfaction of ERP in Jordanian commercial banks. The research results of (Al-Okaily et al., Citation2021) show that the key factors influencing user satisfaction were system quality, information quality, and perceived usefulness.

Furthermore, as a complex software, ERP requires special user abilities. The various modules that exist in ERP software and complexity of using it often hinder its successful use (Abu Madi et al., Citation2022). Drawing on knowledge management theory, the success of ERP requires the competency of personnel and governance in information sharing to support the market response so that companies can realise competitive advantage (Grant & Preston, Citation2019). Early studies on cases of information technology adoption, such as ERP, revealed that information technology leads to macroeconomic growth (Wang et al., Citation2021).

This study empirically examines the links between information sharing, competent personnel, and the success of ERP implementation in Indonesian SOEs. We predict that personal competencies and information sharing positively affect the success of ERP system implementation. To test these relationships, we use structural equation modelling (SEM).Our findings can be insightful for enterprises, especially SOEs, to accelerate the success of their ERP implementations.

3. Theoretical literature review

3.1 Enterprise resource planning

Enterprise resource planning (ERP) is a digital information technology innovation used to develop production processes and business financial reporting (Ben Moussa & El Arbi, Citation2020). ERP is a new and important development for companies that also changes accounting reporting integrated with various other business units within the company (Elsayed et al., Citation2021; Knudsen, Citation2020). (Natu & Aparicio, Citation2022) stated that developing and implementing software, such as ERP, requires collaboration between the parties involved in the process. Companies apply information technology to increase productivity and help achieve quality, time standards, and stakeholder satisfaction (Rodrigues et al., Citation2022). As one of the data and information management solutions that is the prima donna of today’s business, ERP can integrate all existing processes within the company’s functional areas (Wang et al., Citation2021). This integration can be performed, for example, between departments or different locations.

(Raoof et al., Citation2021) reviewed the effect of corporate resource planning and entrepreneurial orientation on the organisational performance of manufacturing SME managers in Pakistan. The research results of (Raoof et al., Citation2021) show a close relationship between ERP adoption and superior company performance. Their findings justify the arguments in many studies that successful ERP implementation will drive company performance towards competitive advantage.

(Awa et al., Citation2016) demonstrated the critical role of the technology-organization-environment (T-O-E) framework in ERP adoption, The results show that ERP adoption by SMEs is driven more by technological factors than organisational and environmental factors. The existence of the model proposed by (Awa et al., Citation2016) provides a basis for investment decisions and developing ERP marketing programs in facing the challenges of ERP adoption.

3.2 Information Sharing

Communication theory argues that communication is a straightforward way to describe an act of communication by answering 1) who, 2) what is said, 3) which channel, 4) to whom, and 5) the effect (Elsayed et al., Citation2021). Effectiveness refers to the success of doing something well. It is a basic element in achieving goals or objectives determined by an organisation, activity, or program. If goals are achieved or objectives are met, they are considered effective (Elsayed et al., Citation2021). Information sharing is the achievement of, for example, a planning goal by understanding the answers to questions that arise so that the objective of information sharing is achieved. Information that can be identified, recorded, and communicated within specified timeframes allows all parties concerned to carry out their duties and responsibilities, and thus, provide the answers (Elsayed et al., Citation2021). Managers consider the following types of communication skills to be essential: 1) consumer communication, 2) internal communication, 3) corporate communication, 4) personal communication, 5) crisis or issue management, 6) communication with investors, and 7) international communication.

3.3 Personnel competence

Competent personnel can be actively involved in organisations. Support refers to the information, advice, or tangible assistance provided by those familiar with individuals in their social environment. For instance, management can provide emotional assistance and positively affect recipients’ behaviour (Vaux, Citation1988). competent personnel can provide genuine assistance in the process of managing, planning, organising, and controllorging an organisation. For instance, the management is responsible for company programs and fiscal matters (Rodrigues et al., Citation2022). In organisations, competent personnel in management can be generally divided into three basic levels: top, middle, and first-line managers. The top management consists of the leader, vice chairman, and CEO. They are responsible for the overall corporate strategy, operating policies, and ultimately, achieving the organization’sorganisation’s goals (Han et al., Citation2023). Middle management consists of managers, operational managers, and division heads, who together are responsible for implementing the plans and decisions of top managers, and overseeing implementation at two levels. First-line management consists of supervisors, coordinators, and office managers responsible for overseeing and coordinating employees, and handling various routines.

4. Hypothesis Development

4.1 Information sharing and the success of ERP system implementation

The design of the information systems [19] appropriate to a company’s needs can then be achieved. Using information systems with modern technology increases institutional trust (Elsayed et al., Citation2021; Yozi, Citation2019). Good information exchange between ERP system users and management can lead to a good system design, and help support ERP system implementation. The information process can reveal the exact characteristics of competent personnel’s fears concerning internal and external environments (Elsayed et al., Citation2021), (Istianingsih et al., Istianingsih Trireksani et al., Citation2020). However, measuring the effectiveness of communication in specific contexts requires attention to essential aspects. The success of communication depends on effective communication between experts and leaders in the organisation. As such, information sharing can mean close collaboration among employees to achieve their goals (Kocaman et al., Citation2022).

Managers must build relationships with employees to establish good and open communication (Dahlan et al., Citation2020; Elsayed et al., Citation2021). Success depends on information between departments, free information flow within the project team, and the ability to communicate the ERP system’s benefits (Ghosh & Skibniewski, Citation2010; Kocaman et al., Citation2022). Indeed, appropriate horizontal and vertical communication between various management levels is important for organisations (Dahlan et al., Citation2020). Thus, information sharing can significantly influence the successful implementation of ERP systems (Elsayed et al., Citation2021; Wickramasinghe & Gunawardena, Citation2010). Three forms of Information sharing, namely joint ventures, networks and Japanese style partnership, was also tested, and the result showed that ERP success in these there form of information sharing (Koh et al., Citation2008)

H₁: Information sharing positively affects the success of ERP system implementation.

4.2 The influence of competent personnel and success of ERP system implementation

Personal and user attitudes can positively influence the use of a system (Sukmadilaga, Citation2019). Budget users—in this case, management—are very influential in ERP implementation (Kocaman et al., Citation2022; Rodrigues et al., Citation2022; Tarigan et al., Citation2018). Managers, as competent personnel, are responsible for providing the active support required by the company. They manage changes in business processes due to the impact of new technology and help users who resist change by showing their commitment to success.

Competent personnel are required to successfully implement ERP (Chanchaichujit et al., Citation2020). ERP users should be able to understand management policies. Competent personnel has a powerful influence on the ERP adoption of users (Chanchaichujit et al., Citation2020). When users have a positive attitude towards ERP implementation, it can invariably be a success. Competent personnel can also affect system quality (Kocaman et al., Citation2022; Marota et al., Citation2017). The need for skill capabilities among top managers and key employees is crucial to facilitate the success of ERP (Kulikov et al., Citation2020)

H₂: Competent personnel positively affect the success of ERP system implementation.

4.3 The influence of information sharing and competent personnel simultaneously on the success of ERP system implementation

The effectiveness of open and honest information in project teams influences the success of ERP implementation systems [13]. This can ensure higher organisational quality and competence, but requires commitment from the user [13]. Management must open communication to lower levels to be open and effective [22], [23]. For instance, during ERP system implementation, managers must direct, monitor, and thoroughly evaluate the progress of the implementation. Meanwhile, management thinking should be sufficiently flexible to accept the significant changes that arise when ERP systems are being developed [22], [31]. Thus, competent personnel should effectively communicate and share information, which can influence the successful implementation of ERP systems. Figure presents the relationship between competent personnel and information sharing on the success of ERP implementation together.

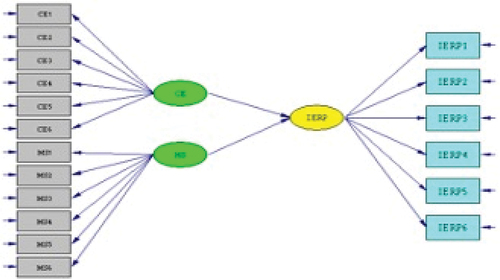

Figure 1. Illustrates the conceptual model of this research.

H₃:

Information sharing and competent personnel have a simultaneous positive effect on the success of ERP system implementation.

5. Research design

The study extracted primary data using a questionnaire survey administered to employees of Indonesian SOEs. The sampling technique used purposive sampling, with the respondent criteria being SOE employees who used the ERP system, worked for more than one year, and were willing to be research participants. Questionnaires were distributed in SOEs under the Ministry of Owned State Companies of the Republic of Indonesia. The population in this study is IT top management in SOEs. The total number of Indonesian SOEs was 91 by the end of 2022. In total, 500 questionnaires were sent to respondents, where 500 was the number of top management in IT of SOEs.

5.1 Variable operationalisation

The variables were operationalizedoperationalised based on previous research and used as the basis for compiling the questionnaire.

Figure illustrates that there are six indicators for the variable CE representing information sharing. These are CE1 for the importance of information, CE2 for need of good communication, CE3 for the scope of activities, CE4 for result and objective, CE5 for one way communication tools, and CE6 for the importance of two way communication tools. MS, representing the variable competent personnel, consists of MS1 for the need of initiative, MS2 for support implementation, MS3 for the ability to find solution soonolutionsoons of problems, MS4 for policies and regulations, MS5 for the support user, and MS6 for the focus on hiring personnel. Finally, IERP, representing ERP system implementation, consists of IERP1 for representing accuracy, IERP2 for focus on integration, IERP3 for alignment with its function, IERP4 for comprehensiveness, IERP5 for easily accessible, and IERP6 for importance of the availability of completed.

Figure 2. Indicators Model.

The data were analysed using the CB SEM method. The indicators used are listed in Table .

Table 1. Variable operationalisation

5.2 Data analysis

A covariance-based SEM (CB SEM) approach was used for data analysis. The results confirm the theory of the influence of exogenous variables on endogenous variables, as well as previous studies. SEM was used to focus on the latent constructs. SEM measures the structure of the covariance matrix by estimating the model parameters (Hair et al., Citation2022). Here, we measured the information sharing, competent personnel, and ERP system implementation success variables. They can also be compared using the covariance matrix derived from empirical data (Hair et al., Citation2022). The SEM software LISREL was used here.

The sample selection used a purposive method with sampling criteria of 1) being SOE employees who used the ERP system, 2) working for more than one year, and 3) being willing to be research participants.

Questionnaires were distributed in SOEs under the Ministry of Owned State Companies of the Republic of Indonesia. The population in this study is IT top management in SOE. The total number of Indonesian SOEs was 91 by the end of 2022. In total, 500 questionnaires were sent to respondents, where 500 was the number of top management in IT of SOEs.

Equation model

IERPit = α0 + β1MSit + β2CEit + εit

Description:

IERPit implementation of ERP ERP on company i and year t

α0 constant

MSit is information sharing on company i, year t

CEit is personnel competence on company i, year t t

β1 dan β2 regression coefficient for independent variable

eεit is the error term.

6. Empirical results and discussion

Questionnaires were distributed in SOEs under the Ministry of Owned State Companies of the Republic of Indonesia. The total number of Indonesian SOEs was 91 by the end of 2022. In total, 500 questionnaires were sent to respondents and 403 were returned (response rate of 80.6%). Of the returned ones, 15 were excluded as they did fulfill notulfillnot fulfil the sample criteria or were incomplete. Finally, we had 388 questionnaires from 51 Indonesian SOEs, as it can shown in Table :

Table 2. Sampling Criteria

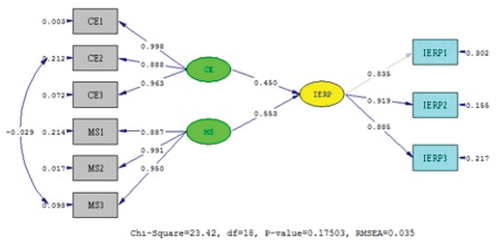

First, we examined the reliability and validity of the measurement instrument for each variable using the standardizedstandardised loading factor output value for each indicator. Testing was performed using LISREL 8.8 full version software. The instrument is reliable if the standardised loading factor is greater or equal to 0.7 (Hair et al., Citation2022). Consequently, CE1–CE3 were retained for CE, MS1–MS3 for MS, and IERP1–IERP3 for IERP. Figure presents the results of the reliability test.

Figure 3. Structural Model.

Figure suggests the correlation between each indicator and the total score per construct was significant at the 1% and 5% levels. For CE, CE1 had the highest correlation value of 0.998 among CE1–CE3. For MS, MS2 had the highest correlation value of 0.991 among MS1–MS3. Finally, for IERP, IERP2 had the highest correlation value of 0.919 among IERP1–IERP3. Thus, all measurement instruments met the valid criteria for measuring the constructs.

6.1 Reliability Test

The reliability test tested the consistency of the indicator in the questionnaire using construct reliability and variance extracted [32]. If the construct reliability exceeds 0.70 and variance extracted exceeds 0.5, then the construct reliability is adequate (Hair et al., Citation2022). Table lists the results for each latent variable.

Table 3. Construct-Reliability and Variance-Extracted

All three variables pass the reliability test. IERP has the highest construct reliability (0.71) and variance extracted (0.92).

6.2 Analysis Results

Table lists the results of the descriptive analysis.

Table 4. Descriptive analysis of research variables

Table shows that Competent Personnel has the highest actual score of 85.53% and highest average Likert score of 4.28. Meanwhile, Information sharing has the lowest actual score of 74.47% and lowest average score Likert of 3.72.

The goodness-of-fit test results in Table show a significant probability of 0.175 and an RMSEA of 0.035. The Normed Fit Index (NFI) is 0.992, Comparative Fit Index (CFI) is 0.98, IFI is 0.998, and RFI is 0.985. These indicators indicate that the model has good fit because the values are greater than 0.90. Cross-validation index (CVI) values were used to compare the models. The test results show a model CVI value of 0.998, and thus, is close to saturation. Hence, the model’s overall fit is good.

Table 5. Model Fit

The GFI value is 0.980, exceeding the 0.90 threshold, which indicates good fit. an Similarly, AGFI value of 0.985 indicates that a good model fit exceeds the 0.80 threshold. Overall, the model has a good level of fit. Further, the P value of 0.175 > 0.05 means that the model indicates a significant positive effect (Hair et al., Citation2022). It can be shown in Figure below.

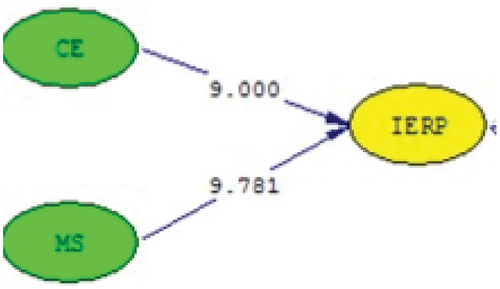

Figure 4. Result of Structural Model.

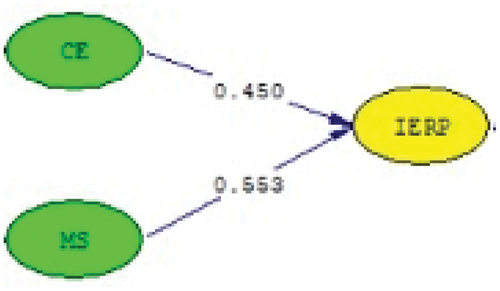

Figure shows the Information sharing has a significant positive effect on the success of ERP system implementation (t = 9.000 and>1.96). Thus, hypothesis H1 is supported. Further, competent personnel have a significant positive effect on the success of ERP system implementation (t = 9.781 and>1.96). Thus, hypothesis H2 is supported. It can be shown in Figure below.

Figure 5. Goodness of Fit of Structural Model.

Figure shows the coefficient values of the latent variables From Table , the goodness of fit test results show a significant probability value of 0.175 > 0.05. Therefore, hypothesis H3 is supported. Thus, information sharing and competent personnel simultaneously have a significant positive effect on the success of ERP implementation.

Discussion

The Influence of Information Sharing on the Success of ERP System Implementation

The results show that the effectiveness of communication significantly positively affects the success of ERP system implementation. Information sharing between departments is beneficial for successful ERP implementation. In particular, information sharing between top management and staff must be conducted openly. In some cases, information may only go one way (Cregård, Citation2022; Elsayed et al., Citation2021), and staff simply follow orders from top to bottom. Poor information-sharing is an indicator that good and transparent information is needed. Research shows that information can be shared routinely during regular coordination and evaluation meetings (Elsayed et al., Citation2021).

Constraints during the implementation process must be resolved, solutions for which can be obtained both internally and externally. They are a means of integrating all company components to facilitate management. Effective company management involves successful communication, effective management of human resources, and competitiveness (Cregård, Citation2022). ERP is implemented based on the company’s needs. Information sharing influences how ERP is implemented, and is required between divisions for the company to operate in an integrated fashion.

The Influence of Competent Personnel on the Success of ERP System Implementation

Next, the results show that competent personnel have a significantly positive effect on the success of ERP system implementation. In the questionnaireuestionnairethe , the personnel initiative received a high number of responses from the participants. Indeed, prior research shows that personnel initiatives may receive the support of staff and enable project implementation to run smoothly (Cregård, Citation2022). Indeed, the implementation of an ERP system represents a significant change in a company’s business operations. Competent personnel are one of the determining factors in a company’s success, and are very influential in the direction of company policy. ERP implementation in most companies is a top-down process. Thus, the competent personnel providers providerovidesprovide ideas while facilitating the ERP implementation process according to the company’s desired goals.

Adoption of new information systems such as ERP enables companies to use more consistent and reliable information. Because competitiveness concerns knowledge and communication with customers, human resources are now the main source of competitive advantage.The results of this study are in line with those expressed by (Raoof et al., Citation2021) that successful ERP implementation will increase competitive advantage. Therefore, competent human resources are a very important focus of a company’s development (Cregård, Citation2022) and success in implementing ERP. ERP systems can also help automate all these processes to ease communication between stakeholders (Abu Madi et al., Citation2022).

Further, the personnel must correctly understand the ERP system, usage, and desired output for the needs of the entity (Cregård, Citation2022). Institutions must provide appropriate resources—sometimes rapid cross-departmental personal mutations—which affect user competence. This change demands strong commitment from the person at all levels (Cregård, Citation2022). Further, personnel commitment can take the form of establishing regulations related to ERP systems.

The Influence of Information Sharing and Competent Personnel Simultaneously on the Success of ERP System Implementation

Finally, information sharing and competent personnel simultaneously have a significantly positive influence on the successful implementation of ERP systems. ERP Implementation will be successful if the information is avail real-timetablreliable real-time reliablee real-time reliablereal-timerelreal-real-timeiable readable real-timetable really-timereadablereal-timetablreally-timreal-real-timee rreal-real-timeealereal-time reliablerealable in real-time realeal-timereal time, and follows the function and availability of complete data. Top managers require proper and fast system output for management and decision-making. Sharing good information and having competent personnel will promote good ERP implementation. The findings of this study are not in line with the opinions of (Awa et al., Citation2016), who state that the most important factor is technology. The results of this study prove that environmental factors, in this case, competence and organisation (information management), are the dominant factors that determine the success of ERP implementation in Indonesian SOEs.

Users must be able to balance the designed system by paying attention to organizationrganizationthe needs of the organisation. Appropriate support should take the form of training to improve competence (Cregård, Citation2022), as observed in previous studies (Abu Madi et al., Citation2022; Ferran, Citation2008). Training is important to ensure that users can operate the ERP system correctly and in a manner that reflects the expected results at the time of planning. Effective information and good competent personnel can make a significant contribution to the process.

7. Summary and Conclusion

7.1 Limitations and direction for future research

This research has several limitations. First, the number of respondents is limited because not many Indonesian SOEs have implemented ERP systems primarily because of the high cost of these systems. Second, limitations remain in measuring variables using questionnaires. Even though a pretest was conducted to determine the respondents’ understanding of the questionnaire, some participants may have wrong perceptions or understanding of the questionnaire items.

Future research can focus on private sector companies, as the indicators of successful ERP implementation for them may differ from those for SOEs. In addition, future researchers should examine the impact of successful ERP implementation on overall business performance.

7.2 Managerial implications

Practically, considering the importance of the role of individual competence in ERP implementation, managers should pay special attention to the ability of each individual in the company to support ERP implementation and ultimately support the company’s success. Business practitioners must also pay attention to information management to optimally support the success of ERP implementation.

7.3 Conclusion

This study reveals that information sharing and competent personnel, both independently and simultaneously, significantly and positively influence the successful implementation of ERP systems. The results of this study confirm that the existence of ERP can still be maintained by taking into account the determinants of successful implementation. The potential for the End of ERP, which can destroy BUMN in Indonesia, can be reduced by increasing management personnel’s ability and properly managing information. ERP implementation in state-owned companies needs to pay attention to the skills of the employees who operate it.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Istianingsih Sastrodiharjo

Istianingsih Istianingsih Sastrodiharjo is a senior lecturer at the Faculty of Economics and Business at Bhayangkara University Jakarta Raya, Indonesia. His research interests are accounting information systems, CSR, and GCG implementation. The latest research project currently underway is regarding the application of intellectual capital in MSME companies.

Uswatun Khasanah is a lecturer in the accounting study program at Bhayangkara University, Jakarta Raya, Indonesia. His research interest is regarding accounting information systems and regional financial development in the public sector accounting area. The latest research is being done about accounting for Islamic boarding schools.

References

- Abu Madi, A., Ayoubi, R. M., & Alzbaidi, M. (2022). Spotting the critical success factors of enterprise resource planning implementation in the context of public higher education sector. International Journal of Public Administration, 1–14. https://doi.org/10.1080/01900692.2022.2085300

- Al-Okaily, A., Al-Okaily, M., Ai Ping, T., Al-Mawali, H., & Zaidan, H. (2021). An empirical investigation of enterprise system user satisfaction antecedents in Jordanian commercial banks. Cogent Business & Management, 8(1), 1918847. https://doi.org/10.1080/23311975.2021.1918847

- Annamalai, C., & Ramayah, T. (2013). Does the organizational culture act as a moderator in Indian enterprise resource planning (ERP) projects?: An empirical study. Journal of Manufacturing Technology Management, 24(4), 555–587. https://doi.org/10.1108/17410381311327404

- Awa, H. O., Ukoha, O., & Emecheta, B. C. (2016). Using T-O-E theoretical framework to study the adoption of ERP solution. Cogent Business & Management, 3(1), 1196571. https://doi.org/10.1080/23311975.2016.1196571

- Ben Moussa, N., & El Arbi, R. (2020). The impact of human resources information systems on individual innovation capability in tunisian companies: The moderating role of affective commitment. European Research on Management and Business Economics, 26(1), 18–25. https://doi.org/10.1016/j.iedeen.2019.12.001

- Chanchaichujit, J., Balasubramanian, S., & Charmaine, N. S. M. (2020). A systematic literature review on the benefit-drivers of RFID implementation in supply chains and its impact on organizational competitive advantage. Cogent Business & Management, 7(1), 1818408. https://doi.org/10.1080/23311975.2020.1818408

- Cregård, A. (2022). Municipal technostructure: Reacting to team development education from above. Public Money & Management, 42(8), 616–626. https://doi.org/10.1080/09540962.2020.1838089

- Dahlan, M., Suharman, H., & Poulus, S. (2020). The Effect of strategic priorities, value congruence and job challenge on SBU performance. International Journal of Innovation Creativity and Change, 12(5), 12514.

- Dewi, P. P., & Asriani, N. L. P. (2019). Analisis Faktor-Faktor Kesuksesan Penerapan Enterprise Resource Planning (ERP) Pada Perusahaan Pengguna ERP Wilayah Bali. Jurnal Riset Akuntansi Mercu Buana, 5(1), 39. https://doi.org/10.26486/jramb.v5i1.645

- Elsayed, N., Ammar, S., & Mardini, G. H. (2021). The impact of ERP utilisation experience and segmental reporting on corporate performance in the UK context. Enterprise Information Systems, 15(1), 61–86. https://doi.org/10.1080/17517575.2019.1706192

- Estensoro, M., Larrea, M., Müller, J. M., & Sisti, E. (2022). A resource-based view on SMEs regarding the transition to more sophisticated stages of industry 4.0. European Management Journal, 40(5), 778–792. https://doi.org/10.1016/j.emj.2021.10.001

- Ferran, C. (2008). Enterprise Resource Planning for Global Economies: Managerial Issues and Challenges: Managerial Issues and Challenges (1st ed) (pp. 289–307). IGI Global. 978-1599045337.

- Ghosh, S., & Skibniewski, M. J. (2010). Enterprise resource planning systems implementation as a complex project: A conceptual framework. Journal of Business Economics and Management, 11(4), 533–549. https://doi.org/10.3846/jbem.2010.26

- Grant, S. B., & Preston, T. A. (2019). Using social power and influence to mobilise the supply chain into knowledge sharing: A case in insurance. Information & Management, 56(5), 625–639. https://doi.org/10.1016/j.im.2018.10.004

- Hair, J. F., Hult, G. T., Ringle, C., & Sarstedt, M. (2022). A primer on partial least squares structural equation modeling (PLS-SEM). SAGE Publications.

- Han, H., Shiwakoti, R. K., Jarvis, R., Mordi, C., & Botchie, D. (2023). Accounting and auditing with blockchain technology and artificial Intelligence: A literature review. International Journal of Accounting Information Systems, 48, 100598. https://doi.org/10.1016/j.accinf.2022.100598

- Istianingsih. (2021). Earnings quality as a link between corporate governance implementation and firm performance. International Journal of Management Science & Engineering Management, 16(4), 290–301. https://doi.org/10.1080/17509653.2021.1974969

- Istianingsih Trireksani, T., Manurung, D. T. H., & Manurung, D. T. H. (2020). The impact of corporate social responsibility disclosure on the future earnings response coefficient (ASEAN Banking Analysis). Sustainability, 12(22), 9671. https://doi.org/10.3390/su12229671

- Jaldell, H. (2019). Measuring productive performance using binary and ordinal output variables: The case of the Swedish fire and rescue services. International Journal of Production Research, 57(3), 907–917. https://doi.org/10.1080/00207543.2018.1489159

- Knudsen, D. -R. (2020). Elusive boundaries, power relations, and knowledge production: A systematic review of the literature on digitalization in accounting. International Journal of Accounting Information Systems, 36, 100441. https://doi.org/10.1016/j.accinf.2019.100441

- Kocaman, B., Gelper, S., & Langerak, F. (2022). Till the cloud do us part: Technological disruption and brand retention in the enterprise software industry. International Journal of Research in Marketing, S0167811622000738. https://doi.org/10.1016/j.ijresmar.2022.11.001

- Koh, S. C. L., Gunasekaran, A., & Rajkumar, D. (2008). ERP II: The involvement, benefits and impediments of collaborative information sharing. International Journal of Production Economics, 113(1), 245–268. https://doi.org/10.1016/j.ijpe.2007.04.013

- Kulikov, I., Semin, A., Skvortsov, E., Ziablitckaia, N., & Skvortsova, E. (2020). Challenges of enterprise resource planning (ERP) implementation in agriculture. Entrepreneurship & Sustainability Issues, 7(3), 1847–1857. https://doi.org/10.9770/jesi.2020.7.3(27)

- Laswell, H. (2007). The structure and function of communication in society. In L. Bryson (Ed.) The communication of ideas (pp. 37–51). New York: Harper and Row. https://pracownik.kul.pl/files/37108/public/Lasswell.pdf

- Liu, H., & Zhao, Y. (2022). Cannot investors really price the book-tax differences correctly? Evidence from accelerated depreciation policies. China Journal of Accounting Studies, 10(3), 301–322. https://doi.org/10.1080/21697213.2022.2143671

- Marota, R., Ritchi, H., Khasanah, U., & Abadi, R. F. (2017). Material flow cost accounting approach for sustainable supply chain management system. 6(2).

- Natu, S., & Aparicio, M. (2022). Analyzing knowledge sharing behaviors in virtual teams: Practical evidence from digitalized workplaces. Journal of Innovation & Knowledge, 7(4), 100248. https://doi.org/10.1016/j.jik.2022.100248

- Plekhanov, D., Franke, H., & Netland, T. H. (2022). Digital transformation: A review and research agenda. European Management Journal, S0263237322001219. https://doi.org/10.1016/j.emj.2022.09.007

- Raoof, R., Basheer, M. F., Shabbir, J., Ghulam Hassan, S., & Jabeen, S. (2021). Enterprise resource planning, entrepreneurial orientation, and the performance of SMEs in a South Asian economy: The mediating role of organizational excellence. Cogent Business & Management, 8(1), 1973236. https://doi.org/10.1080/23311975.2021.1973236

- Rodrigues, A. C., Carvalho, H., Caetano, A., & Santos, S. C. (2022). Micro-firms way to succeed: How owners manage people. Journal of Business Research, 150, 237–248. https://doi.org/10.1016/j.jbusres.2022.05.062

- Shahab, Y., Ntim, C. G., & Ullah, F. (2019). The brighter side of being socially responsible: CSR ratings and financial distress among Chinese state and non-state owned firms. Applied Economics Letters, 26(3), 180–186. https://doi.org/10.1080/13504851.2018.1450480

- Sukmadilaga, C. (2019). Internet financial reporting (1sted.).

- Tarigan, Z. A., Mulyani, S., Maksum, A., & Muda, I. (2018). The role of conflict of interest in improving budget quality in local government. International Journal of Civil Engineering and Technology, 9(9), 696–707.

- Urban, B., & Matela, L. (2022). The nexus between innovativeness and knowledge management: A focus on firm performance in the hospitality sector. International Journal of Innovation Studies, 6(1), 26–34. https://doi.org/10.1016/j.ijis.2021.12.002

- Vaux, A. (1988). Social Support: Theory, Research, and Intervention. Praeger.

- Wang, X., Bu, L., & Peng, X. (2021). Internet of things adoption, earnings management, and resource allocation efficiency. China Journal of Accounting Studies, 9(3), 333–359. https://doi.org/10.1080/21697213.2021.2009180

- Wickramasinghe, V., & Gunawardena, V. (2010). Critical elements that discriminate between successful and unsuccessful ERP implementations in Sri Lanka. Journal of Enterprise Information Management, 23(4), 466–485. https://doi.org/10.1108/17410391011061771

- Wongsansukcharoen, J., & Thaweepaiboonwong, J. (2023). Effect of innovations in human resource practices, innovation capabilities, and competitive advantage on small and medium enterprises’ performance in Thailand. European Research on Management and Business Economics, 29(1), 100210. https://doi.org/10.1016/j.iedeen.2022.100210

- Xie, Y., James Allen, C., & Ali, M. (2014). An integrated decision support system for ERP implementation in small and medium sized enterprises. Journal of Enterprise Information Management, 27(4), 358–384. https://doi.org/10.1108/JEIM-10-2012-0077

- Yozi, V. (2019). Relationship between supply chain management effects on the tax information system and willingness to pay taxes. International Journal of Supply Chain Management, 8(3). https://doi.org/10.59160/ijscm.v8i3.3378