?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper examines the sensitivity of tax revenue performance to IFRS adoption in Africa and the implication for tax policy. The study investigated how IFRS adoption affects the level of tax revenue performance in Africa. This study is one of the foundational studies, which has investigated IFRS adoption and tax revenue performance at both macro and cross-country levels. This approach presents better inclusive evidence to support tax reforms and provides the basis to validate tax regulatory apprehensions and suspicions of the adverse impact of IFRS adoption. The paper uses data from six African countries: Botswana, Ghana, Namibia, Nigeria, Sierra Leone, and South Africa for the analyses. The data are sourced from World Bank, International Monetary Fund, and Organisation for Economic Co-operation and Development (OECD). Annualised data from 1996 to 2020 are used. The paper employs Pooled Mean Group (PMG) as the primary estimator and is validated by Panel Dynamic Ordinary Least Square (DOLS). The results showed that IFRS adoption could pose a significant risk to tax revenue mobilisation in Africa as evident by the significant negative long-run estimates. The results further revealed short-run positive IFRS effects. This is affirmed by the country-level analyses and trajectory of tax revenue performance across the sample periods of 1996 to 2020 for the selected countries during the pre- and post-IFRS era. It is therefore safe for African countries to pursue tax-targeted IFRS reforms to minimise the possible adverse effect of IFRS on tax revenue.

1. Introduction

Globally, tax revenue continues to be one of the mainstays for economic development. It is a primary source of revenue for Government expenditure, growth, and development. The tax revenue in this context reflects revenues generated from all elements of sovereign taxes, such as direct and indirect taxes. According to Organisation for Economic Co-operation and Development (OECD), tax revenue may be operationalised as all tax-related revenues collected from profits and income, social security contributions, payroll or employment income, goods and services, transfer, and ownership of property and other associated taxes (operation and Development OECD, Citation2023). Generally, it is measured as a percentage of gross domestic product (GDP). It is regarded as one of the indicators that capture the degree to which governments control the resources of economies. These highlight the real and implicit importance of tax revenue.

However, Governments and tax authorities have often struggled to meet their tax revenue targets (Boateng et al., Citation2022; Lee & Yoon, Citation2020; Razali et al., Citation2018; Seidu et al., Citation2021). No country currently has tax revenue of more than 50% of its Gross Domestic Product (GDP) echoing the tax revenue mobilisation challenges worldwide. Nevertheless, some advanced countries are making inroads in boosting their tax revenue. For instance, the tax revenue to GDP for European countries, such as Denmark stands at 48.8% in 2021 (2020: 47.1%), France stands at 47.0% in 2021 (2020: 45.3%), Belgium at 46% (2020: 45.1), in the Americas, Cuba’s tax performance stands at 40.3% and Brazil at 31.6% of GDP and Organisation for Economic Co-operation and Development (OECD) average of 34.1% in 2021 (Eurostat, Citation2022; Eurostat, Citation2020; (operation and Development OECD, Citation2019, Citation2020; Seidu et al., Citation2021; World Bank, Citation2020).

Unfortunately, countries in Africa continue to report poor revenue performance. The currently available data show that the average tax revenue of African countries as at 2020 is 16.0% (2019: 16.1%) with a comparable average performance of 19.1% in Asian and Pacific countries, 21.9% in Latin America & the Caribbean (LAC), and the OECD members average of 33.6% (Citation2020; Eurostat, Citation2020; OECD, Citation2022; Seidu et al., Citation2021; World Bank, Citation2020). The persistent poor tax revenue performance has caused many researchers to explore the determinants of tax revenue performance with several streams of studies. Some studies have focused on incentives for tax avoidance (Agyei et al., Citation2019; Boateng et al., Citation2022; Christina, Citation2019; Kportorgbi, Citation2013), tax environment (Akitoby et al., Citation2020; Hanlon et al., Citation2014), ownership structure, and analysts interest (He et al., Citation2020; Khan et al., Citation2017), managerial ability and governance (Lee & Yoon, Citation2020), debt and financing needs (Platikanova, Citation2017; Razali et al., Citation2018; Seidu et al., Citation2021) and macroeconomic dynamics (Shivanda & Obwogi, Citation2018).

Another emerging stream of studies focuses on financial reporting framework and tax revenue implication. The motivation for this stream of empirical studies is that financial reporting and tax are interlinked (Braga, Citation2017; Hoogendoorn, Citation1996; Okafor et al., Citation2018). The nature of accounting standards could contribute to explaining the tax revenue performance challenges. It can be argued that since financial statements are the source for determining taxable earnings and tax liabilities, the nature of accounting standards could also have implications on tax liabilities and overall tax revenue performance. Thus, the adoption of International Financial Reporting Standards (IFRS), which is the popular accounting standards globally could have implications for tax revenue performance. The IFRSs are accounting standards issued and promoted by the International Accounting Standards Board (IASB) as harmonised global standards for preparing financial reports of adopters (El-Helaly et al., Citation2020; I. C. Queku, Citation2017; Okafor et al., Citation2018). IFRS used in this study encompasses international accounting standards (IAS) still in use, IFRSs themselves, IFRS for small and medium enterprises (IFRSsmes), and IFRS interpretations, which have been adopted and applied.

It is believed that the IFRS framework, its recognition criteria, and disclosures could either deter or enhance tax compliance, tax planning activity, and tax provisions (Braga, Citation2017; De Simone, Citation2016). Some have argued that the increased transparency through IFRS adoption (I. C. Queku, Citation2017, Citation2018) could limit aggressive tax planning activities, provisions, and income shifting (De Simone, Citation2016), thereby improving the tax revenue performance of adopting countries. However, others have opined that the complexities in revenue recognition, discretionary accruals, and principle-based framework offer opportunities for tax planning activities and tax avoidance (Braga, Citation2017; Sun, Zhan, Zhan & Zhan, Citation2022). According to De Simone (Citation2016), whether the level of equilibrium of tax planning activity increases after IFRS adoption is an empirical question that hinges on the trade-off of cost and benefit nexus between individual firms in the country and the tax authorities.

Despite the controversies and the heightened interest in the consequence of IFRS adoption, the implications of IFRS adoption on tax revenue performance in the empirical literature are still in their infancy globally (Okafor et al., Citation2018, Citation2019). Generally, the empirical literature under this stream of studies focuses almost exclusively on the IFRS implications on firm-level tax liabilities (Abedana et al., Citation2016; Adegbite, Citation2020; Braga, Citation2017; De Simone, Citation2016; Okafor et al., Citation2018, Citation2019). Since taxation is assessed at the taxpayers’ level, it is understandable to see this stream of studies. The findings from this stream have largely been inconclusive with mixed results (Braga, Citation2017; De Simone, Citation2016; Okafor et al., Citation2019).

Assessment of tax implication of IFRS adoption at the country or macro-level is rare in the literature. It is therefore useful and timely to extend the literature to macro-level analyses especially since the African continent continues to search for remedies for the troubling tax revenue (OECD, 2021,2020). This paper, therefore, attempts to follow a macro-level approach to provide comprehensive insight into the implication of IFRS adoption on tax revenue performance in Africa and to shed light on whether or not Africa needs tax-targeted IFRS reforms. This macro-level approach is warranted for three reasons. First, the macro-level approach consolidates and uses country-level data on tax and IFRS adoption for the analyses. This smoothens the differences in the data across industries and firms, a behaviour that is common in firm-level tax and IFRS compliance data. This approach could also minimise the effect of the heterogeneity characteristics of taxes across industries and jurisdictions (Agyei et al., Citation2019; Seidu et al., Citation2021) and the differences in firm-level IFRS compliance (Daske et al., Citation2013; I. C. Queku, Citation2018; Y. N. Queku, Citation2020). Thus, the consequence of the choice of industry/sector and the level and nature of IFRS compliance is likely to have accounted for the inconclusive and mixed results from firm-level analyses (see Braga, Citation2017; De Simone, Citation2016; Okafor et al., Citation2019) could be minimized through this approach. Third, some emerging studies have also used a country-level or a macro-level approach to assess the consequence of IFRS adoption with insightful evidence (El-Helaly et al., Citation2020; Gu & Prah, Citation2019; Leykun Fisseha, Citation2023; Oppong & Aga, Citation2019; Simbi et al., Citation2023). These studies have demonstrated that this approach could provide country-level evidence about the consequence of IFRS adoption, which may be relevant for informed policy decisions (Gu & Prah, Citation2019; Oppong & Aga, Citation2019; Simbi et al., Citation2023). Moreover, overall tax revenue target and performance are assessed at the country-level, therefore, it is more appropriate to investigate its sensitivity to IFRS using a macro-level approach.

Of closer relevance to this study is the approach used in studies such as El-Helaly et al. (Citation2020), Gu and Prah (Citation2019), Leykun Fisseha (Citation2023), and Oppong and Aga (Citation2019) which found macro-level analyses crucial in evaluating IFRS adoption. Nevertheless, none of the existing empirical studies has examined the effect of IFRS adoption on tax revenue performance at the macro-level. The paucity of empirical evidence might have contributed to the apprehension of some tax authorities making them suspicious of IFRS-based financial reports for tax purposes (Deloitte, Citation2021; Okafor et al., Citation2018; Okafor, Citation2015). For instance, Canada Revenue Agency (CRA) views IFRS-based financial reports with suspicion in meeting their revenue targets. CAR believes that IFRS compliance could impact the risk of inappropriate tax reporting and adjustments in corporate tax reporting (Canada Revenue Agency, CAR, Citation2010, Citation2012). Similarly, tax authorities in the Czech Republic have also declined to accept tax reporting based on IFRS for fear of adverse tax collection and possible deterioration in revenue targets (Jirásková & Molín, Citation2015; Procházka, Citation2014). Hungarian Tax Authorities (HTA) has also issued concerns about accounting adjustments for tax purposes and cautioned against tax returns, which are inconsistent with Hungarian accounting requirements.

Due to these regulatory concerns, many of these countries have implemented tax-targeted reforms where local accounting standards are used as the bases for tax returns rather than IFRS (Deloitte, Citation2021; Haag, 2022; KPMG, Citation2020). Some countries in Europe have tax accounting rules separate from IFRS so as not to upset tax calculation. However, African countries are rather realigning their tax laws with IFRS making IFRS rules the bases for taxation. Practically, Africans are not pursuing tax-targeted IFRS reforms. National tax authorities in Africa have increasingly relied on IFRS treatments to determine the tax treatments of some specific transactions (Adegbite, Citation2020; Egbunike & Okoye, Citation2017; Zwan, Citation2020). While the realignment of local tax rules to IFRS rather than tax-targeted reforms to separate tax accounting rules may lessen the administrative burden on the taxpayers, harmonise and simplify accounting-tax treatments, to some extent this may be slippery especially when there are tax regulatory concerns that IFRS could disturb tax revenue targets.

These tax regulatory concerns and tax-targeted IFRS reforms from even developed countries where it is believed to be fundamental beneficiaries of IFRS adoption (Daske et al., Citation2008) raise some fundamental question about the tax revenue performance impact of IFRS in the developing economies such as those in Africa. In fact, except for South Africa, which is one of the largest and most developed economies in Africa, the three high-performing tax revenue countries such as Seychelles, Tunisia, and Morocco have not fully adopted IFRS (operation and Development OECD, Citation2019, Citation2020). Thus, IFRS adoption may contribute to explaining the weakness in tax revenue performance in Africa. Although IFRS adoption likely contributes to or is one of the main drivers behind much of the observed country-level tax revenue performance bottlenecks, causality cannot be inferred (Akitoby et al., Citation2020). The only scientific basis for affirming or disaffirming the IFRS apprehension and suspicion is through empirical investigation.

This paper, therefore, builds on and makes three new contributions to the IFRS-tax literature. First, this study follows a macro-level approach to investigate the IFRS-tax nexus to present better inclusive evidence to support IFRS-tax reforms and policies. This macro-level analysis would provide comprehensive evidence to understand the dynamics of the IFRS-Tax Revenue nexus in Africa through analyses of composite tax revenue data, which encompasses all industries and taxable activities (Braga, Citation2017; Okafor et al., Citation2018, Citation2019). The findings could provide evidence of comfort or otherwise to tax authorities about the sensitivity of tax revenue mobilisation to IFRS adoption and the basis for reviewing their stance on IFRS.

Second, besides the composite analysis through the pooling of data across Africa, the study also recognises cross-border heterogeneity. Even though the heterogeneity problem may be handled through an estimation strategy, there might still be some level of conflict in pooled findings, which could lead to measurement errors and misleading decisions (Adeneye & Chu, Citation2020) and may eventually affect the holistic implications of findings especially in sensitive matters, such as IFRS adoption and taxation. This study would therefore decompose the data further into country-level and interrogate the dynamics of IFRS and tax revenue performance at the country level. The findings would deepen country-level understanding of tax revenue performance under the IFRS regime and the basis for tax reforms.

Third, although it may be naive to assume that the empirical findings from this paper will end the controversy on the tax implications of IFRS adoption in Africa, the findings would provide policymakers with foundational evidence to form views on the sensitivity of tax revenue to IFRS adoption. The paper provides policymakers with evidence that isolates or disentangles the aggregate and concurrent benefits and incentives of IFRS adoption by focusing on a tax-based effect of IFRS. The touted aggregate incentives and benefits of IFRS have often clouded policymakers’ judgments on IFRS implications and made it difficult for policymakers to identify, anticipate and monitor the potential incidental effects of IFRS closely and reasonably. Thus, the evidence from this paper could provide policy clarity on the IFRS-tax nexus and the bases for tax-targeted IFRS reforms to contain possible tax revenue risk exposure of IFRS adoption.

The rest of the paper is organised as follows: a literature review (IFRS-tax nexus: emerging tax-targeted IFRS reforms, theoretical consideration, empirical review, lessons leant and hypothesis development), methodology (empirical strategy, measurement of variables, model specification and estimation approach), results and discussions (descriptive statistics, panel unit root test, correlation matrix, empirical results, and discussions) and conclusions and implications.

1.1. IFRS-Tax Nexus: Emerging Tax-targeted IFRS Reforms

Currently, IFRS remains the most widely adopted accounting standard globally. IFRS has been adopted in over 167 jurisdictions worldwide (IFRS Foundation, Citation2023). The initial understanding was that adopting a new accounting standard, such as IFRS would not necessarily lead to consequences in taxes, especially since the primary aim of IFRS is to provide more useful financial information to users in general and not any specific interest group (Braga, Citation2017). However, emerging evidence suggests that alterations in adopters’ taxable income and increase in tax planning activities may have occurred with the IFRS adoption (Agarwal, Citation2019; KPMG, Citation2023).

Some IFRS specifics, such as IAS 12 and IFRS 15 have serious tax implications. The IAS 12 provides a varying array of guidelines for adjusting tax reporting of adopters which are often different from the local tax laws. Moreover, the complexities, uncertainties, and judgments under IFRS 15 determination of transaction prices, allocation of prices, and recognition of revenue could deepen accounting income-taxable income differentials (Haag, 2022; Waruiru, Citation2020) and open opportunities for planning activities, especially in jurisdictions where tax enforcement is weak. The bases, nature, and recognition criteria of revenue could have a significant effect on indirect taxes, such as sales tax and value-added tax (VAT), and direct taxes, such as corporate income tax (Imali, Citation2020). The changes in the accounting treatment of leases under IFRS 16 could also have significant corporate income tax and valued added tax implications on the adopters (Agarwal, Citation2019).

Additionally, the implementation of IFRS 9 and IFRS 17 are also expected to have significant implications for tax purposes. IFRS 9 could increase uncertainties in tax reporting, especially in the recognition of fair value adjustments and alternative measurements of expected credit losses. Furthermore, IFRS 17 which is expected to the implemented on or after 1st January 2023 would evoke tax effects on the measurements of insurance liabilities, and computation of both current and deferred tax (Ernst &Young EY, Citation2021). IFRS 17 has changed the revenue recognition of the insurance where insurance companies will longer associate their insurance revenue to insurance premiums received rather revenue will be measured as a reduction in insurance liability (i.e., amortisation over the contract life). This risk-based revenue recognition breeds complexities in accounting and tax dynamics and ultimately book-tax conformity differentials. Thus, direct taxes including current and deferred may significantly be affected. Moreover, according to the highlights from KPMG, transaction-based taxes including taxes on insurance premiums, unrecoverable VAT, and cross-border reinsurance may significantly be affected (KPMG, Citation2023).

Globally, tax and tax obligations of entities are driven largely by the accounting standards used in recognising business transactions and preparing financial statements. Many countries, which have either observed or suspected significant book-tax conformity differences from IFRS adoption have begun to implement IFRS-based tax reforms. In many jurisdictions, although IFRS is required in financial reporting, they have also mandated the use of local accounting standards as the starting point for tax computation (Braga, Citation2017; Chen & Gavious, Citation2015; Deloitte, Citation2010; Karampinis & Hevas, Citation2013). In Switzerland, effective 1 January 2013, IFRS users are required to also follow the Swiss Code of Obligations (Swiss CO) (Haag, 2022; KPMG, Citation2020). This reform requires that firms in Switzerland should prepare comparable Swiss CO financial statements to the IFRS-based financial statements.

In Cyprus, the Tax Department has continued to monitor IFRS implications on local taxes and issued IFRS-based tax reforms accordingly, especially when the implications are considered material. For instance, in May 2021 Cyprus issued tax implementation guidelines in response to IFRS 9, 15, and 16 (Deloitte, Citation2021). The Czech Republic requires the use of accounting results based on Czech accounting standards for computing income taxes. According to Price Waterhouse Coopers (PWC), companies that are obligated to prepare financial statements in line with IFRS are also required to prepare comparable statements for tax purposes in line with Czech accounting standards (PWC, Citation2023).

Besides the country-specific reforms, other international organisations have worked closely to implement IFRS-based tax reforms for the interest of their members. In Europe, the European Union (EU) has strived to engage IASB for rigorous reforms, especially in the area of tax implications of IFRS. For instance, the EU through the European Financial Reporting Advisory Group (EFRAG) was a key contributor to the introduction of IFRIC 23 to reduce the diversity in the accounting for deferred tax liabilities and assets on transactions relating to leases and decommissioning and to deepen certainties in tax implications (EFRAG, Citation2017). One of the biggest financial reporting-based tax reforms is the Organisation for Economic Co-operation and Development (OECD) Pillar II Model. This model provides mechanisms for Global Anti-Base Erosion (GloBE) rules to address tax revenue challenges. This model introduces a minimum global corporate tax rate of 15%. The 15% minimum tax applies to Multinational companies whose revenue is above EUR 750 million. Although the primary purpose of the reform targeted globalisation and digitalisation, it addresses tax concerns of financial reporting such as IFRS. This global tax reform has forced IASB to quickly realign IFRS-based tax reporting with the new reform. In January 2023, an exposure draft that introduces a “temporary exception to accounting for deferred taxes arising from the implementation of the Pillar Two model rules” was published (Ernst &Y oung EY, Citation2023).

However, in Africa, these IFRS-based tax reforms are still in their infancy. One of the possible reasons for the paucity of IFRS-based tax reforms is the limited empirical studies on the tax implications of IFRS adoption in Africa (Abedana et al., Citation2016; Adegbite, Citation2020). Policymakers often prefer to formulate policy based on evidence, therefore, where such sufficient-appropriate evidence is not available, policy intervention becomes challenging. Although commentaries and opinions may be available, these may not be appropriate evidence to warrant policy reforms. As echoed by the Institute of Chartered Accountants, England & Wales (ICAEW), “– asking people what they think is something that relatively few accounting researchers regard as an appropriate method of research. This may be in part because they do not know how trustworthy the answers are, but there is also a question as to whether all answers should be regarded as of equal value” (ICAEW, Citation2018, p. 12). It is therefore not surprising that ICAEW continues to compile empirical evidence on IFRS to support reforms within Europe. Following this trend, it is important to call out louder for researchers to explore IFRS tax implications in Africa and to provide evidence about whether or not Africa needs IFRS-based tax reforms.

2. Theoretical consideration

This paper is developed from the assumptions of bounded rationality theory (BRT). BRT is often accredited to Herbert Simon (Citation1956) and Nelson and Winter (Citation1982). It is believed that Simon is a primary contributor to this theory. The theory connects behaviour and rationality in decision-making. Bounded rationality refers to the behavioural patterns directed toward a particular goal within the limitations and boundaries of conditionality and constraints. The theory assumes that an individual or a firm would act within a specific boundary, constraint, and condition. These decision-makers anticipate and evaluate the consequences of the available alternatives and eventually choose the option or alternative that is good enough. Rationality projects behavioural traits, which are appropriate for achieving organisational goals, within the existing boundaries, conditions, or limits imposed by given constraints (Simon, Citation1956). This suggests that BRT integrates the constraints and conditionality on the decision makers (individual or firm) to process and adopt options that satisfy the expected utility of the decision made.

Following the assumption of limit to rationality and zeroing into a firm-level decision, Okafor et al. (Citation2019) explain that bounded rationality could be modified to account for fundamentals, such as uncertainties, risks, and difficulties in identifying and formulating environmental limitations, constraints, and complexities in cost functions. BRT, therefore, demonstrates how firms make rational decisions within the existing constraints and limitations when an optimal solution is not possible (Scott, Citation2000). Another foundational assumption of BRT is that decision-makers “satisfice” when the choice made is “good enough” instead of focusing on the option that only maximises or reaches optimality. This suggests that firms would not amass the resources to search for better alternatives when the status quo is satisfactory. It can be argued that BRT does not hypothesise value maximisation of choice; instead, it aims at satisfaction where rational decision maker searches for alternatives, which are good enough in relation to the pre-determined criteria. This implies that optimised decisions are reached when the firm or the decision maker opts for the best alternative as per the established criteria.

Nevertheless, when the status quo falls below the pre-established criteria, the firm would consolidate its resources to search and find a new alternative, which is ’good enough’ (Elster, Citation2001). BRT does not follow the maximisation assumption as the priority and therefore avoids the indeterminacy problem. A critical analysis of the assumptions of BRT reveals that firms do not necessarily follow rational choice theory to determine what is “good enough”, instead firms evaluate gains and losses associated with actions by measuring the extent to which such alternative deviates from a given reference point rather than just in absolute terms, and that the firm is more risk-averse for losses than for gains (Fiori, Citation2008).

These theoretical assumptions have been applied to firm-level decisions including tax compliance behaviour. Allingham and Sandmo (Citation1972) applied the BRT in their study of income tax evasion. Allingham and Sandmo (Citation1972) revealed that taxpayers are rational and therefore, their decision to avoid tax is dependent on the tradeoff between the payoff expected from underreporting or aggressive tax reporting and the severity of the expected punishment from tax authorities when caught cheating. Other studies employing these theoretical assumptions to tax compliance include Akhand and Hubbard (Citation2016); Farrar and Thorne (Citation2016); Hanlon et al. (Citation2014), and Lamantia and Pezzino (Citation2021).

This paper also borrows the assumptions of BRT and argues that taxpayers would adopt the “Good Enough Alternative” when they could not reach the optimal option due to bounded constraints and limitations. Taxpayers may not search for alternatives for maximising their after-tax benefits through tax reduction opportunities in IFRS when they are likely to incur higher costs arising from limit conditions and constraints set by the tax laws through misinterpretation of the tax laws, uncertainties surrounding sanctions, and penalties. Thus, since IFRS adoption enhances transparency through its disclosure requirements coupled with uncertainty surrounding reporting environments, taxpayers would be cautious in pursuing aggressive tax planning activities.

The implication is that transparency, full disclosures, and uncertainty in reporting environment of IFRS may constrain taxpayers in opting for aggressive tax reduction activities. For instance, “IAS 12: Income Tax” requires firms to disclose temporary differences arising from their transactions. Additionally, connected party or related party transactions are required to be disclosed under IAS 24 and this could expose illegalities in transfer pricing issues for tax assessment. The risk of these exposures and the consequence of these actions through IFRS adoption could cause taxpayers to opt for is “Good Enough Alternative” tax strategy instead of an optimal tax strategy, which may be risky. Thus, IFRS adoption would rather improve the tax revenue performance of the adopters’ country.

Furthermore, even though IFRS adoption may present opportunities for tax reduction activities, the presence of unresolved uncertainties, risk exposure through monitoring activities by tax authorities, and high enforcement culture may cause taxpayers especially firms to be skeptical about exploring the tax planning opportunities available through IFRS. Thus, these firms may maintain the status quo “is good enough” tax planning behaviour rather than seeking to maximise after-tax accounting returns. However, this could only stand when the risk imposed by tax enforcement is high. Most countries in Africa do not have vibrant tax enforcement systems to benefit from the transparency, full disclosures, and uncertainties created by IFRS. Moreover, the consequences for non-compliance are often not too severe, and where it is severe the probability of being caught is often too remote. This paper therefore agrees with Allingham and Sandmo (Citation1972) and argues that taxpayers in Africa are rational and therefore, their decision to avoid tax is dependent on the tradeoff between the payoff expected from underreporting or aggressive tax reporting and the severity of the expected punishment from tax authorities when caught cheating and the probability of being caught. Given the tax enforcement environment in Africa, it can be projected that a trade-off benefit exists for pursuing aggressive tax planning activities through IFRS fundamentals.

2.1. Empirical literature, lessons learnt, and hypothesis development

Empirical studies on the IFRS-tax nexus have largely been limited to firm-level analyses (Braga, Citation2017; De Simone, Citation2016; Okafor et al., Citation2019). Braga (Citation2017) investigated the relationship between IFRS adoption and corporate income tax avoidance. The author used firm-level data from 35 countries. Braga (Citation2017) observed that firms became more tax-avoidant after the IFRS adoption.

Okafor et al. (Citation2019)’s study is one of the empirical studies that responded to the tax regulatory concerns in Canada in respect of IFRS adoption. The study investigated whether IFRS adoption has affected corporate income tax avoidance in Canada using firm-level data. Okafor et al. (Citation2019) found that IFRS adoption has decreased corporate income tax avoidance in Canada. The authors observed a significant increase in tax payments of firms in Canada in the post-IFRS period. The findings from Okafor et al. (Citation2019) are inconsistent with some existing literature (Braga, Citation2017; De Simone, Citation2016). Adegbite (Citation2020) also examined how IFRS adoption affects tax estimates of manufacturing firms in Nigeria. The author concluded that IFRS adoption has had an adverse effect on the tax estimates of the firms. Adegbite (Citation2020) explained that the adopters use IFRS rules to engage in tax reduction activities. This conclusion corroborates with studies, such as Braga (Citation2017) but disaffirms the findings of Okafor et al. (Citation2019).

Evidence from the empirical study conducted by Sun, Zhang, Zhang, and Zhang, (Citation2022) also presented a new dimension of IFRS-corporate tax nexus. Sun et al., (Citation2022) investigated the consequences of IFRS adoption on corporate income tax avoidance. The authors revealed that the effect of an IFRS adoption on corporate income tax avoidance is conditional on the level of initial tax avoidance activities. Sun et al., (Citation2022) found that while adopters with a higher initial tax avoidance activity tend to be less tax aggressive in the post-IFRS adoption period, adopters with a lower initial tax avoidance activity tend to be more tax aggressive in the post-IFRS adoption period. The implication is that firm-level characteristics could determine the nature of IFRS implication on tax.

It can be observed that the commonality in these studies is that they have almost exclusively assessed tax implications of IFRS adoption at the firm. It is understandable as taxation is done at the taxpayers’ levels. These results have however been inconclusive. For instance, while studies, such as Adegbite (Citation2020), Braga (Citation2017), and De Simone (Citation2016) suggest that IFRS adoption increases corporate tax planning activities, the study of Okafor et al. (Citation2019) revealed that IFRS compliance rather increases tax liabilities of adopters. Better still, Sun et al., (Citation2022) also concluded that the effect of an IFRS adoption on corporate income tax avoidance is conditional on the level of initial tax avoidance activities. The mixed results at the firm-level analysis may be attributed to several factors. One fundamental possible reason is that tax in general and corporate income tax, in particular, is heterogenous across different industries, sectors, and jurisdictions (Agyei et al., Citation2019; Seidu et al., Citation2021). Therefore, so long as tax rules prescribe different tax treatments and tax concessions for different industries and sectors (i.e. priority versus non-priorities sectors), differences may exist in firm-level analyses. Another possible reason is that firms’ compliance with IFRS is also not homogeneous. Some prior empirical studies have classified firm-level adopters as either “Serious Adopters” or “Label Adopters” (Daske et al., Citation2013). Thus, IFRS effects are heterogeneous across firms.

Some emerging studies have strived to assess IFRS at the macro-level to minimise the effect of compliance differences among firms (El-Helaly et al., Citation2020; Gu & Prah, Citation2019; Oppong & Aga, Citation2019). These studies have demonstrated that this approach could provide consolidated and country-level evidence about the consequence of IFRS adoption, which may be relevant for informed policy decisions (Gu & Prah, Citation2019; Oppong & Aga, Citation2019). Moreover, overall tax revenue target and performance are assessed at the country-level, therefore, it is more appropriate to investigate its sensitivity to IFRS using a macro-level approach. Additionally, a macro-level investigation of the IFRS-tax nexus could present better inclusive evidence to support tax reforms and policies. The firm-level or micro-level investigations do not capture the composite tax revenue data of all industries and taxable activities (Braga, Citation2017; Okafor et al., Citation2018, Citation2019) as well as the composite tax revenue data. At best, these firm-level studies have emphasised corporate income tax, which is just a component of overall tax revenue. It is therefore critical and timely to extend the literature at both macro and cross-border analyses.

Following the empirical evidence that suggests a strong connection between IFRS adoption and tax revenue (Adegbite, Citation2020; Braga, Citation2017; De Simone, Citation2016; Okafor et al., Citation2019; Sun et al., Citation2022) coupled with the theoretical lessons from bounded rationality theory (Akhand & Hubbard, Citation2016; Allingham & Sandmo, Citation1972; Farrar & Thorne, Citation2016; Hanlon et al., Citation2014; Lamantia & Pezzino, Citation2021), this study argues that the IFRS framework, its recognition criteria, accounting adjustments, and provisions could enhance tax planning activity.

This paper therefore agrees with Allingham and Sandmo (Citation1972) and argues that taxpayers in Africa are rational and therefore, their decision to avoid tax is dependent on the tradeoff between the payoff expected from underreporting or aggressive tax reporting and the severity of the expected punishment from tax authorities when caught cheating and the probability of being caught. With a weak enforcement environment in Africa, taxpayers may rationally employ IFRS as a tool for tax planning activities. Thus, it is possible that the level of equilibrium of tax planning activity has increased in Africa after IFRS adoption and the trade-off of cost and benefit nexus between individual firms in the country and the tax authorities has skewed to the taxpayers at the detriment of tax authorities. IFRS complexities could exacerbate the risk of inappropriate or deliberate mistreatment of revenue recognition, borrowing cost, and impairment loss and may undermine tax revenue mobilisation. Following these transmission mechanisms of the IFRS adoption-Tax Revenue Performance nexus, this study postulates its directional hypothesis as:

H1:

IFRS adoption has a significant negative influence on tax revenue performance in Africa

2.2. Empirical strategy

This paper follows a causal design. It is believed that a causal design is suitable when a study seeks to investigate cause-and-effect relationships (Brains et al., Citation2011; Kabir, Citation2016). It is also appropriate when a study explores the nature and the extent to which a variable or group of variables are used to predict the outcome of another variable (Erickson, Citation2017). Therefore, since this paper primarily seeks to determine the nature and extent to which IFRS adoption affects tax revenue in Africa, it is suitable to follow a causal design.

This design is applied within quantitative analytical procedures coupled with the use of secondary data. Annualised data are used for the investigation spanning from 1996 to 2020. The data are collected from World Bank, International Monetary Fund, and OECD. Varying sources are used due to data gaps in World Bank Database. 1996 and 2020 are chosen as the starting and cut-off years, respectively, as they are the periods where most of the target countries have data. Sufficient data are available within these spans for both pre and post-IFRS analyses. Similar to some of the prior studies, the study focuses on all African Countries, which have adopted IFRS and meet the selection criteria (De Simone, Citation2016; Okafor et al., Citation2019). The selection criteria are as follows:

The country should have adopted IFRS for financial reporting

The country has no alternative financial reporting standards other than full IFRS and IFRS for Small and Medium Enterprises. This criterion is needed so as to identify the true effect of IFRS without any interacting effect from local accounting or other accounting standards.

Finally, the study excludes early adopters. The early adopters are operationalised as those countries, which adopt IFRS on or before 2005 (Tawiah, Citation2019). These countries do not have sufficient pre-IFRS data for the analysis.

Six (6) countries meet these criteria and therefore form the bases for the investigation.

2.3. Measurement of variables

The two main variables of interest are IFRS and tax revenue performance. Tax revenue performance is the dependent or response variable. It is measured by the widely used proxy, which focuses on the ratio of total tax revenue to gross domestic product (operation and Development OECD, Citation2019, Citation2020). Thus, the tax revenue encompasses all tax revenue: direct and indirect tax revenues, and scaled by the gross domestic product (GDP).

The independent variable is IFRS. The study follows the existing empirical literature to operationalise and measure IFRS adoption. This paper measures IFRS adoption using a binary variable, which takes the value of 1 in the year when IFRS is in use and 0 otherwise (Braga, Citation2017; Clements et al., Citation2010; De Simone, Citation2016; Gordon et al., Citation2012; Gu & Prah, Citation2019; Klibi & Kossentini, Citation2014; Okafor et al., Citation2019; Oppong & Aga, Citation2019; Simbi et al., Citation2023). The IFRS adoption represents the independent variable while tax revenue performance is the dependent variable.

Besides the variables of interest, it is believed that tax revenue performance is driven by macroeconomic variables. The literature has identified macroeconomic factors such as inflation, interest rate, and exchange rate as determinants of tax revenue performance (Birungi, Citation2015; Hung, Citation2017; Mahzar and Meon, 2016; Reiss, Citation2015). This study, therefore, controls for these variables. The paper measures inflation as the consumer price index over a given year consistent with the literature (Semuel & Nurina, Citation2014; Usman & Adejare, Citation2013). Although inflation is likely to increase tax revenue through consumption tax, it may be counterproductive as it translates into production cost and reduces overall tax revenue. Thus, high inflation could deplete tax revenue at the macro level. Real depreciation of local is also likely to shift revenue toward a more price inelastic and to goods, which are not heavily taxed including domestic substitutes and hence contribute to reducing tax revenues (Agbeyegbe, Citation2004). Thus, exchange rate depreciation could reduce tax revenue performance. The exchange rate used in this paper is measured as the rate of local currency per unit of the United State Dollar (USD) (Semuel & Nurina, Citation2014; Shivanda & Obwogi, Citation2018). Table presents the outcome of applying the sampling criteria.

Table 1. Sample size selection

Interest rate is the cost of borrowing money and could determine tax revenue performance through economic activities. Since the interest rate is tax deductible, it is likely that a high interest rate would undermine tax revenue performance even though the interest could also generate taxable income for the lending institutions. A high interest rate could also deter the demand for loanable funds, which could reduce income-generating activities; hence lowering tax revenue performance (Spengel et al., Citation2016). Thus, this study expects an interest rate to have a significant negative effect on tax revenue performance and therefore needs to be controlled especially in Africa with a high interest spread. Since there is no one interest rate but myriads of interest rates, this study measures interest rate as the average commercial lending rate (CLR). Table summarises these variables and their measurements.

Table 2. Measurement of variables and Apriori

2.4. Model specification and estimation approach

This paper follows panel model specification. Panel specifications reduce the consequences of the shortcomings of both time series and cross-sectional analyses. It is therefore not surprising that researchers are increasingly turning to panel data to allow for the combination of cross-sectional and time series features that offer a variety of econometric estimation techniques (Calderón & Liu, Citation2003; Carsamer et al., Citation2021; Christopoulos & Tsionas, Citation2004; Dawson, Citation2010; Samargandi et al., Citation2014; Y. N. Queku, Citation2020). The panel model corrects biases in both time series and cross-sectional studies and control for individual heterogeneity. The study conducts pre-diagnostic tests before the estimation of the main models. These diagnostics include multicollinearity and unit root tests. The general panel model is specified as:

Where:

Y is the dependent variable and represents the tax revenue performance of the selected countries

(TRP)

X is the regressor and represents IFRS adoption

M as the vector of the control variables (INF, INT, and EXR)

“i” denotes individual country-level observations

“t” denotes the time

Βj is the coefficient of IFRS adoption (IFRS)

θp is the vector of coefficients of the control variables

α is the intercept of the model or the constant

ε is the error term

The paper follows Pooled Mean Group (PMG) as the estimator for testing the hypothesis and estimates model (1). PMG is capable to address the problem of bias, which is caused by a possible correlation between the error term and the mean-differenced regressors. Although, alternatively Generalised Method of Moment (GMM) could also cure this bias, GMM is inefficient when T is large. This bias can only vanish with large numbers of data observations but cannot be corrected just by increasing the number of cross-sections.

In datasets with large T, the assumptions of a dynamic panel of GMM often become inappropriate, the estimation technique breaks down and results become unreliable. In this situation, the PMG of Pesaran et al. (Citation1999) becomes the popular alternative to address this bias and parameters’ heterogeneity problem. Thus, the novelty of the PMG estimator is that it is capable to handle heterogeneity in parameters in the tax revenue performance regressions. PMG estimator takes the form of Autoregressive Distributed Lag (ARDL) and adapts the setting to a panel framework where the intercepts, the short-run coefficients, and the cointegrating terms are allowed to differ across the various cross-sections. Therefore, with a dataset spanning twenty-four (24) years, the dataset is large enough making PMG quite suitable. Specifically, the PMG estimator is expressed as:

Where:

Y is the dependent variable and denotes tax revenue performance

X is the vector of the independent variable (IFRS) and control variables (INF, INT, and

EXR)

“i” = 1, 2, 3 … … .N, for countries in the sample

“t” denotes the time

ε is the error term

Both the dependent variable or response variable and the regressors have the same lag length in all the cross-sections.

2.5. Robustness check

Panel Dynamic Ordinary Least Square (DOLS) is used to test for the robustness of the results from the PMG. DOLS estimator is conducted to affirm the results from the PMG against suspected endogeneity problems and serial correlation challenges in the model. Panel DOLS estimator is widely known for its ability to handle endogeneity and serial correlation problems (Sulaiman & Abdul-Rahim, Citation2020). Therefore, Panel DOLS estimation would only validate the results from the PMG. The Panel DOLS estimation is expressed as:

Where:

the intercept or constant in the model

and

are the cointegrating vectors of a change in Xit on Yit

p and q are the lag and lead length.

is the error term.

3. Descriptive statistics

The estimation process of the paper begins with the pre-diagnostics to check the data properties, and stationarity of the data and to test for multicollinearity problems among the explanatory variables. Table reports the data properties of tax revenue performance, IFRS, interest rate (INT), exchange rate (EXR), and inflation (INF). The mean score of tax revenue performance of the selected African countries is 19.35828 with a standard deviation of 9.1204. This suggests that the average tax revenue is 19.35% of the GDP of African countries. This is less than the average of the Organisation for Economic Co-operation and Development (OECD) of 33.3% (OECD, Citation2022). This seems to suggest a decline in tax performance in recent times. IFRS adoption has a mean score of 0.3910 suggesting that 39.10% of the observations are post-IFRS periods suggesting that most of the African countries have adopted IFRS in recent periods. Thus, approximately, 10 years out of the 25-period series of data are post-IFRS periods. Regarding the control variables, the mean scores for INT, EXR, and INF are 18.1702, 668.9441, and 10.6665, respectively. These are relatively high especially the interest rate and the exchange rates. These suggest high operational cost and cost of financing. These could undermine residual incomes and tax revenue. The standard deviations for the variables are relatively high indicating a high deviation of individual observations from the mean scores.

Table 3. Descriptive properties of the variables

3.1. Correlation matrix

The study further checks for a multicollinearity problem using a correlation matrix. This test is very fundamental especially when there are multiple regressors and these regressors are expected to be estimated simultaneously in a model. Multicollinearity can negatively affect the stability of the estimations and the reliability of the results. The results are presented in Table . It can be observed that the correlation coefficients range from 0.0759 to 0.5380 in absolute terms. Values in this range are less than 0.8 thresholds. It is therefore safe to draw the conclusion that there is no multicollinearity problem among the regressors or the explanatory variables. Regarding the correlation between the tax revenue performance and the explanatory variables, the directions of the associations are consistent with the apriori presented in Table . All the variables have a negative significant association with tax revenue performance.

Table 4. Correlation matrix

3.2. Panel unit root

Given the relatively long period this study covers, it is imperative to check the stationarity properties of the data. Fisher Augmented Dickey-Fuller (ADF) and Fisher Phillips-Perron (PP) tests are employed to conduct the unit root tests. The study employs Levin, Lin, and Chu (LLC) as the tiebreaker when the results of Fisher ADF and Fisher PP are inconclusive. The results for the unit root tests as reported in Table suggest that tax revenue performance, inflation, and interest rate are stationary at level. However, the IFRS and the exchange rate are not stationary. The order of integration for the variables is therefore a mixture of I(1) and I(0). This is suitable for PMG and DOLS estimations.

Table 5. Results of stationarity analysis

3.3. Empirical results and discussions

The pre-diagnostics have been consistent with the data and the assumptions of the estimation approaches. The study proceeds to employ PMG to estimate the main model. Panel DOLS is further used for robustness checks. Table reports the results of the estimation. The long-run estimates suggest that IFRS adoption in Africa generates a negative effect on the tax revenue performance as exhibited by the negative coefficient of 0.1253 which is significant at 5 percent. The control variables are mixed in terms of directions and strength of significance. Only inflation meets the apriori in a direction (negative) in the long-run. An interest rate and an exchange rate are all positive. For brevity, these control variables are not discussed further.

Table 6. Pooled mean group and panel DOLS empirical estimation results

To clear any doubt about possible endogeneity problems in the long-run estimates generated by the PMG model, the study further estimated the same model by following panel DOLS specifications using one lead and lag for robustness checks. Panel DOLS is widely known for its power and ability to deal with serial correlation and endogeneity problems. Thus, the results from the panel DOLS do not only provide a robustness check of the PMG estimates but also serve as diagnostic checks for the PMG model against a serial correlation problem and an endogeneity bias. The results of the panel DOLS as reported in Table confirm the PMG long-run estimates as all the variables in the model retained their right directions (negative and positive) and the expected level of significance. It is therefore appropriate to concentrate on the results from the PMG estimates. The coefficient of IFRS is −0.1253. The associated p-value for the coefficient is less than 5% (denoted by **). This suggests that the coefficient is negative and significant at 5%. The implication is that the study rejects the null hypothesis that IFRS adoption could have a significant negative effect on tax revenue in Africa.

The findings seem to follow earlier studies, which suggest that IFRS adoption deepens tax planning activities and may reduce tax liabilities (Adegbite, Citation2020; Braga, Citation2017; De Simone, Citation2016), rather than the existing findings, which concluded that IFRS adoption does not reduce tax liabilities and its effect may be conditional (Okafor et al., Citation2019; Okafor, Citation2015; Sun et al., Citation2022). It is important to note that while these prior studies followed firm-level analyses with corporate income tax as the target, the present study conducted country-level analyses (El-Helaly et al., Citation2020; Gu & Prah, Citation2019; Oppong & Aga, Citation2019) with overall tax revenue (direct and indirect taxes) as the target of measurement. Therefore, it may be inappropriate to affirm or disaffirm the conclusions reached in these earlier studies.

Nevertheless, the findings in this study are consistent with the concerns of some tax authorities such as the Canadian Revenue Agency (CRA), tax authorities in the Czech Republic, and Hungarian Tax Authorities (HTA) that IFRS compliance could impact the risk of inappropriate tax reporting and adjustments and eventually adverse tax collection and deteriorating revenue targets (Canada Revenue Agency, CAR, Citation2010, Citation2012; Deloitte, Citation2021; Haag, 2022; Jiraskova, and Molin, 2015; Procházka, Citation2014).

The findings have theoretical implications. The findings extend the understanding of bounded rationality theory. The findings imply that firms and taxpayers view the status quo of their tax compliance strategy as not good enough. Therefore, they might have begun to consolidate their resources to explore tax-cutting opportunities in IFRS provisions, adjustments, and recognitions. This affirms the contribution of Elster (Citation2001). A further theoretical implication of the findings is that IFRS adopters in Africa view IFRS as a better alternative for tax planning when they assess gains and losses associated with the risk of non-compliance (Fiori, Citation2008) especially due to the weak tax enforcement environment. Taxpayers in African countries (firms) operate in environments where the tax risk of enforcement is generally considered low and the consequences of aggressive practices, non-compliance, and inappropriate tax reporting are not significant. As advanced by the BRT, these might have created opportunities for taxpayers (firms/institutions) to explore tax advantage provisions in IFRS to maximise their after-tax income, which is likely to reduce the overall tax revenue performance.

A policy implication of the negative IFRS and tax revenue performance nexus is that governments and tax authorities in Africa should, therefore, be concerned about IFRS-based tax returns. The findings suggest a possible increase in the level of equilibrium of tax planning activity in Africa after IFRS adoption. Thus, the trade-off of cost and benefit nexus between individual firms in the adopted countries in Africa and the tax authorities has skewed to the taxpayers at the detriment of tax authorities when tax revenue may be sacrificed. The adverse long run effect of IFRS on tax revenue may also imply that IFRS complexities have exacerbated the risk of inappropriate or deliberate mistreatment of revenue recognition, borrowing cost, and impairment loss and may undermine tax revenue mobilisation. The findings also seem to expose lapses in IFRS adoption in Africa and reveal that accounting standard setters in Africa might have inadvertently caused adopters to pursue aggressive tax reduction strategies at the expense of government tax revenue. The findings may also provide empirical evidence for other African countries which are still contemplating IFRS adoption.

A further possible practical reason for the observed significant negative IFRS-tax revenue nexus is that implementing IFRS-oriented tax returns (direct, sales, VAT, and other taxes) might have caused national governments to implicitly lose the power to effectively control the collection of taxes as per their fiscal needs. This is because IFRS primarily addresses the financial reporting needs of capital markets and investors and does not address the tax needs of states. Therefore, a change in any IFRS may lead to a significant change in revenue and expense treatments affecting sales taxes, VAT, and other indirect taxes and in the accounting profits, resulting in variance in direct taxes and thus variance in the overall tax revenue mobilisation. This mimics a severe risk of tax revenue. It may also be safe to institute tax-targeted IFRS reforms to minimise the adverse effect on tax revenue. Similar to tax-targeted IFRS reforms in some jurisdictions (Braga, Citation2017; Chen & Gavious, Citation2015; Deloitte, Citation2021; Haag, 2022; Karampinis & Hevas, Citation2013; KPMG, Citation2020; PWC, Citation2023), African countries could pursue separate tax accounting rules to minimise tax risk implications of IFRS. The adverse tax implication of IFRS adoption observed in this study could be minimised when the reforms critically review and provide tax-oriented guidelines on specific IFRSs whose provisions may significantly affect local indirect taxes, such as sales tax and value-added tax (VAT) and direct taxes, such as corporate income tax. Risk-based revenue recognition, which often breeds complexities in accounting and tax dynamics and ultimately book-tax conformity differentials might have also contributed to this adverse effect of IFRS adoption. Thus, direct taxes including current and deferred and other indirect taxes may significantly be affected and therefore an important element for tax-targeted IFRS reforms in Africa.

Furthermore, the PMG estimator distinguishes between long-run estimates and short-run estimates of IFRS adoption and tax revenue nexus. Although, the study found a significant negative long-run effect of IFRS adoption on tax revenue performance, the short-run effect is significant and positive. The short-run positive effect may be due to the cross-country heterogeneity in taxation and IFRS adoption in general and laxity in tax enforcement. The study conducts further country-level analysis to check varying short-run coefficients across the various cross-sections. For brevity, the details have not been reported. Nevertheless, in summary, it was found that Botswana, Ghana, Nigeria, and Sierra Leone retained their negative significant effect of IFRS adoption on tax revenue performance. However, Namibia and South Africa changed the direction of the coefficients though insignificant in respect of South Africa. Country-level pre- and post-IFRS tax revenue performance trend analyses confirm the PMG estimates.

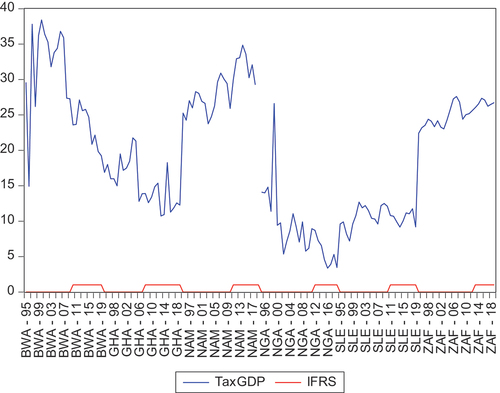

This paper graphically illustrates the trajectory of tax revenue performance across the sample periods of 1996 to 2020 for the selected countries during the pre- and post-IFRS era as reported in Figure . The graphical presentation in Figure shows a country-level trend of tax revenue during Pre and Post IFRS periods. In the graph, BWA, GHA, NAM, NGA, SLE, and ZAF denote Botswana, Ghana, Namibia, Nigeria, Sierra Leone, and South Africa. It can be observed from the figure that most of the best-performing tax revenue periods are in the pre-IFRS era for almost all the countries. Thus, apart from Namibia and South Africa which are reporting some relatively higher tax revenue figures in post-IFRS periods, the remaining countries are showing a relatively downward trend. This trend analysis and the patterns are consistent with the estimates reported from PMG as discussed earlier. Tax authorities in Africa could consider formulating tax-targeted IFRS strategies and reforms to mitigate possible adverse effects of IFRS-based tax returns.

Figure 1. Tax revenue performance trend (1996–2020).

4. Conclusion and implication

The paper examines the sensitivity of tax revenue performance to IFRS adoption in Africa and the implication for tax policy using data from World Bank, International Monetary Fund, and OECD. The data span for the investigation is from 1996 to 2020. Six African countries: Botswana, Ghana, Namibia, Nigeria, Sierra Leone, and South Africa were used for the analyses. The paper employs Pooled Mean Group (PMG) as the primary estimation approach and is validated by Panel Dynamic Ordinary Least Square (DOLS). The results show that IFRS adoption could pose a significant risk to tax revenue mobilisation in Africa as evident by the significant negative long-run estimates. The results further revealed a short-run positive effect, which may be due to cross-country heterogeneity in taxation and IFRS adoption in general. This is affirmed by both the country level analyses and the trajectory of tax revenue performance across the sample periods of 1996 to 2020 for the selected countries during the pre- and post-IFRS era.

The findings have implications for tax authorities, accounting standard setters, and taxpayers (firms). The evidence of the adverse effect of IFRS adoption on tax revenue performance implies that it is safe for tax authorities to be concerned about IFRS-based tax returns. IFRS compliance could impact the risk of inappropriate tax reporting and adjustments and could challenge tax revenue mobilisation efforts and deteriorate tax revenue targets. It is therefore recommended that tax authorities in Africa should deepen their tax enforcement laws and regulations to deter tax-aggressive practices. It is further recommended that these authorities should train their auditors to be skeptical about tax returns and to be alert to any identifying inappropriate adjustments and recognition of revenue and expenses.

The findings further imply that it may also be safe to institute tax-targeted IFRS reforms to minimise the adverse effect on tax revenue. Tax-targeted IFRS reforms should therefore be part of African efforts in improving tax revenue performance. Similar to tax-targeted IFRS reforms in some jurisdictions (Braga, Citation2017; Chen & Gavious, Citation2015; Deloitte, Citation2021; Haag, 2022; Karampinis & Hevas, Citation2013; KPMG, Citation2020; PWC, Citation2023), African countries could pursue separate tax accounting rules to minimise tax risk implications of IFRS. The adverse tax implication of IFRS adoption observed in this study could be minimised when the reforms critically review and provide tax-oriented guidelines on specific IFRSs whose provisions may significantly affect local indirect taxes, such as sales tax and value-added tax (VAT) and direct taxes, such as corporate income tax. Risk-based revenue recognition, which often breeds complexities in accounting and tax dynamics and ultimately book-tax conformity differentials might have also contributed to this adverse effect of IFRS adoption. Thus, direct taxes including current and deferred and other indirect taxes may significantly be affected and therefore an important element for tax-targeted IFRS reforms in Africa. African countries should consider developing tax accounting standards and guidelines that are separate from financial reporting standards (such as IFRS). This could harness the aggregate benefits and incentives of the use of IFRS without upsetting tax estimations and revenue.

Accounting standard setters could explore and investigate IFRS provisions, which may inadvertently breed tax-aggressive practices among adopters to make informed decisions. The negative long-run effect of IFRS adoption on government tax revenue implies that IFRS compliance could breed tax planning opportunities to reduce tax liabilities. Firms could therefore explore these opportunities and develop strategies to enhance the positive trade-off between the gains and cost of such tax planning.

4.1. Limitations and future studies

Despite the sound theoretical, policy, and practical implications of the findings, it is important to acknowledge some caveats when relying on the findings. The study relied on data from six African countries, which have fully adopted IFRS including IFRS for SMEs with no alternative accounting standards in use to project IFRS implications in Africa. The findings and implications may not be relied upon, to the extent that these countries’ economic and standard-setting environments are incongruent with other countries in Africa. Countries generally pursue independent interventions to mitigate risk for attaining economic targets including tax revenue targets. The study assumed a homogenous approach. This assumption could affect the outcome of this paper and the recommendations made. This paper did not explore IFRS-specific contents and provisions, which may create tax reduction opportunities. This type of study could unravel specific interventions required to smoothen IFRS migration and sustain tax revenue performance targets. Future researchers could explore this gap within the African context. Moreover, this study uses aggregate tax revenue data, future studies could target country-level specific tax revenues, such as sales tax or VAT and follow a similar macro-level approach to revisit the IFRS-tax nexus for deeper empirical insight.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Abedana, V. N., Omane-Antwi, K. B., & Owiredu, A. (2016). The impact of IFRS/IAS adoption on corporate income taxation in Ghana. International Journal of Accounting and Financial Reporting, 6(1), 72–21. https://doi.org/10.5296/ijafr.v6i1.9070

- Adegbite, T. A. (2020). The effects of IFRS adoption on taxation in Nigerian manufacturing companies. Financial Sciences, 25(4), 1–15. https://doi.org/10.15611/fins.2020.4.01

- Adeneye, Y., & Chu, E. Y. (2020). Managerial aversion and capital structure: Evidence from Southeast Asia. Asian Academy of Management Journal of Accounting and Finance, 16(1), 155–183. https://doi.org/10.21315/aamjaf2020.16.1.8

- Agarwal, R. (2019) INSIGHT: Accounting for leases—tax implications [ Accesed on 02/05/2023 from:https://news.bloombergtax.com/daily-tax-report-international/insight-accounting-for-leases-tax-implications

- Agbeyegbe, T. (2004). Trade Liberalization, Exchange Rate Changes, and Tax Revenue in Sub-Saharan Africa Terence Agbeyegbe, Janet Stotsky b and Asegedech WoldeMariam b Department of Economics. Hunter College, City University of NY, NY b International Monetary Fund.

- Agyei, S. K., Marfo-Yiadom, E., Ansong, A., & Idun, A. A. A. (2019). Corporate tax avoidance incentives of banks in Ghana. Journal of African Business, 2019(4), 1–16. https://doi.org/10.1080/15228916.2019.1695183

- Akhand, Z., & Hubbard, M. (2016). Coercion, persuasion, and tax compliance: The case of large corporate taxpayers. Canadian Tax Journal, 64(1), 31–63.

- Akitoby, B., Honda, J., Primus, K., & Keen, M. (2020). Tax revenues in fragile and conflict-affected states—why are they low and how can we raise them? IMF Working Papers, 2020(143), 1. https://doi.org/10.5089/9781513550848.001

- Allingham, M. G., & Sandmo, A. (1972). Income tax evasion: A theoretical analysis. Journal of Public Economics, 1(3), 323–338. https://doi.org/10.1016/0047-2727(72)90010-2

- Birungi, J. M. (2015). The effect of selected macroeconomic variables on government revenues in Rwanda (Doctoral dissertation, University of Nairobi).

- Boateng, K., Omane-Antwi, K. B., & Queku, Y. N. (2022). Tax risk assessment, financial constraints and tax compliance: A bibliometric analysis. Cogent Business & Management, 9(1), 2150117. https://doi.org/10.1080/23311975.2022.2150117

- Braga, R. N. (2017). Effects of IFRS adoption on tax avoidance. Revista Contabilidade and Finanças, 28(75), 407–424. https://doi.org/10.1590/1808-057x201704680

- Brains, C., Willnat, L., Manheim, J., & Rich, R. (2011). Empirical Political Analysis (8th ed.). Longman.

- Calderón, C., & Liu, L. (2003). The direction of causality between financial development and economic growth. Journal of Development Economics, 72(1), 321–334. https://doi.org/10.1016/S0304-3878(03)00079-8

- Canada Revenue Agency, CAR. (2010). IFRS Bulletin 11. Obtained pursuant to the Access to Information Act (ATIA). Canadian Revenue Authority.

- Canada Revenue Agency, CAR. (2012). International Financial Reporting Standards (IFRS). Obtained online on May 13, 2012 from http://www.craarc.gc.ca/tx/bsnss/tpcs/frs/menu-eng.html

- Carsamer, E., Abbam, A., & Queku, Y. N. (2021). Bank capital, liquidity and risk in Ghana. Journal of Financial Regulation and Compliance. https://doi.org/10.1108/JFRC-12-2020-0117

- Chen, E., & Gavious, I. (2015). The roles of book-tax conformity and tax enforcement in regulating tax reporting behaviour following international financial reporting standards adoption. Accounting and finance (early view; online first). Retrieved from https://doi.org/10.1111/acfi.12172.

- Christina, S. (2019). The effect of corporate tax planning on firm value. Accounting and Finance Review, 4(1), 01–04. https://doi.org/10.35609/afr.2019.4.1(1)

- Christopoulos, D. K., & Tsionas, E. G. (2004). Financial development and economic growth: Evidence from panel unit root and cointegration tests. Journal of Development Economics, 73(1), 55–74. https://doi.org/10.1016/j.jdeveco.2003.03.002

- Clements, C. E., Neil, J. D., & Stovall, S. O. (2010). Cultural Diversity. Journal of Applied Business Research (JABR), 26(2). https://doi.org/10.19030/jabr.v26i2.288

- Daske, H., Hail, L., Leuz, C., & Verdi, R. (2008). Mandatory IFRS reporting around the world: Early evidence on the economic consequences. Journal of Accounting Research, 46(5), 1085–1142. https://doi.org/10.1111/j.1475-679X.2008.00306.x

- Daske, H., Hail, L., Leuz, C., & Verdi, R. (2013). Adopting a label: Heterogeneity in the economic consequences around IAS/IFRS adoptions. Journal of Accounting Research, 51(3), 495–547.

- Dawson, P. J. (2010). Financial development and economic growth: A panel approach. Applied Economics Letters, 17(8), 741–745. https://doi.org/10.1080/13504850802314411

- Deloitte. (2010). CFO insights: IFRS: Select tax considerations. Retrieved from http://www.iasplus.com/en/binary/usa/1012cfotaxconsider.pdf.

- Deloitte. (2021) Cyprus Tax News [ Accessed on 02/05/2023 from https://www2.deloitte.com/content/dam/Deloitte/cy/Documents/tax/taxalerts/CY_TaxAlerts_28_05_21EN_Noexp.pdf]

- De Simone, L. (2016). Does a common set of accounting standards affect tax-motivated income shifting for multinational firms? Journal of Accounting & Economics, 61(1), 145–165. https://doi.org/10.1016/j.jacceco.2015.06.002

- EFRAG. (2017) EFRAG’s letter to the european commission regarding endorsement of IFRIC Interpretation 23 Uncertainty over Income Tax Treatments https://www.efrag.org/Assets/Download?assetUrl=%2Fsites%2Fwebpublishing%2FProject%20Documents%2F364%2FEndorsement%20Advice%20on%20IFRIC%2023%20Uncertainty%20over%20Income%20Tax%20Treatments.pdf

- Egbunike, P. A., & Okoye, O. P. (2017). Tax implication of International Accounting Standards (IAS 12) adoption: Evidence from Deposit Money Banks (DMBS) in Nigeria. International Journal of Social and Administrative Sciences, 2(2), 52–62. https://doi.org/10.18488/journal.136.2017.22.52.62

- El-Helaly, M., Ntim, C. G., & Al-Gazzar, M. (2020). Diffusion theory, national corruption and IFRS adoption around the world. Journal of International Accounting, Auditing & Taxation, 38, 1–22. 100305. https://doi.org/10.1016/j.intaccaudtax.2020.100305

- Elster, J. (2001). Ulysses unbound. The Philosophical Quarterly, 51(205), 181–210.

- Erickson, G. S. (2017). Causal research design. In New methods of market research and analysis (pp. 78–105). Edward Elgar Publishing.

- Ernst &Young (EY). (2021) Accounting for taxes considering the impact of IFRS 17 —What insurers need to know now

- Ernst &Y oung (EY). (2023) How OECD Pillar Two rules affect companies and their IFRS Reporting [ Accessed on 02/05/2023 from: https://www.ey.com/en_gl/ifrs/how-oecd-pillar-two-rules-affect-companies-and-their-ifrs-reporting]

- Eurostat. (2022): Taxation in 2021 [ Accessed from: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Tax_revenue_statistics&oldid=460966#:~:text=The%20ratio%20 of%202021%20tax,%2C%20Romania%2027.3%20%25%20of

- Eurostat European Commission. (2020): Taxation in 2019

- Farrar, J., & Thorne, L. (2016). Written communications and taxpayers’ compliance: An interactional fairness perspective. Canadian Tax Journal, 64(2), 351–370.

- Fiori, R. (2008). Fides e bona fides. Gerarchia sociale e categorie giuridiche.

- Gordon, L. A., Loeb, M. P., & Zhu, W. (2012). The impact of IFRS adoption on foreign direct investment. Journal of Accounting and Public Policy, 31(4), 374–398. https://doi.org/10.1016/j.jaccpubpol.2012.06.001

- Gu, S., & Prah, G. J. (2019). The effect of international financial reporting standards on the association between foreign direct investment and economic growth: evidence from selected Countries in Africa. Journal of Accounting, Business and Finance Research, 8(1), 21–29. https://doi.org/10.20448/2002.81.21.29

- Hanlon, M., Hoopes, J. L., & Shroff, N. (2014). The effect of tax authority monitoring and enforcement on financial reporting quality. The Journal of the American Taxation Association, 36(2), 137–170. https://doi.org/10.2308/atax-50820

- He, G., Ren, H. M., & Taffler, R. (2020). The impact of corporate tax avoidance on analyst coverage and forecasts. Review of Quantitative Finance & Accounting, 54(2), 447–477. https://doi.org/10.1007/s11156-019-00795-7

- Hoogendoorn, M. N. (1996). Accounting and taxation in Europe—A comparative overview. European Accounting Review, 5(sup1), 783–794.

- Hung, F. S. (2017). Explaining the nonlinearity of inflation and economic growth: The role of tax evasion. International Review of Economics & Finance, 52, 436–445. https://doi.org/10.1016/j.iref.2017.03.008

- ICAEW. (2018) The effects of mandatory IFRS adoption in the EU: A review of empirical research https://www.icaew.com/-/media/corporate/files/technical/financial-reporting/information-for-better-markets/ifbm-reports/effects-of-mandatory-ifrs-adoption.ashx

- IFRS Foundation. (2023) Who uses IFRS Accounting Standards? https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction/

- Imali, D. (2020). Tax Implications on IFRS 15 Revenue and IFRS 16 Leases. The Institute of Certified Public Accountants of Kenya, September(2020).

- Jirásková, S., & Molín, J. (2015). IFRS adoption for accounting and tax purposes: An issue based on the Czech Republic as compared with other European countries. Procedia Economics and Finance, 25, 53–58. https://doi.org/10.1016/S2212-5671(15)00712-1

- Kabir, S. M. S. (2016). Basic guidelines for research. An Introductory Approach for All Disciplines, 4(2), 168–180.

- Karampinis, N. I., & Hevas, D. L. (2013). Effects of IFRS adoption on tax-induced incentives for financial earnings management: Evidence from Greece. The International Journal of Accounting, 48(2), 218–247. https://doi.org/10.1016/j.intacc.2013.04.003

- Khan, M., Srinivasan, S., & Tan, L. (2017). Institutional ownership and corporate tax avoidance: New evidence. The Accounting Review, 92(2), 101–122. https://doi.org/10.2308/accr-51529

- Klibi, M. F., & Kossentini, A. (2014). Does the adoption of IFRS promote emerging stock markets development? Evidence from MENA countries. International Journal of Accounting, Auditing and Performance Evaluation, 10(3), 279–298. https://doi.org/10.1504/IJAAPE.2014.064242

- KPMG. (2020) The Swiss law on accounting and financial reporting [ Accessed on 02/05/2023 from: https://assets.kpmg.com/content/dam/kpmg/ch/pdf/explanation-of-the-most-important-provisions.pdf

- KPMG. (2023) IFRS 17: Tax considerations for insurers [ Accessed on 02/05/2023 from https://kpmg.com/xx/en/home/insights/2022/08/ifrs-17-considerations-for-insurers.html]

- Kportorgbi, H. (2013). Tax planning corporate governance and performance of listed firms in Ghana. Unpublished Master’s thesis. University of Cape Coast.

- Lamantia, F., & Pezzino, M. (2021). Social norms and evolutionary tax compliance. The Manchester School, 89(4), 315–405. https://doi.org/10.1111/manc.12368

- Lee, K., & Yoon, S. (2020). Managerial ability and tax planning: Trade-off between tax and nontax costs. Sustainability, 12(1), 370–383. https://doi.org/10.3390/su12010370

- Leykun Fisseha, F. (2023). IFRS adoption and foreign direct investment in Sub-Saharan African countries: Does the levels of Adoption Matter? Cogent Business & Management, 10(1), 2175441. https://doi.org/10.1080/23311975.2023.2175441

- Nelson, R., & Winter, S. G. (1982). An Evolutionary Theory of Economic Change. The Belknap Press of Harvard University Press.

- Okafor, O. N. (2015). Effects of IFRS on accounting quality and tax aggressiveness: Evidence from Canadian mandatory adoption.

- Okafor, O. N., Akindayomi, A., & Warsame, H. (2019). Did the adoption of IFRS affect corporate tax avoidance? Canadian Tax Journal, 67(4), 947–979. https://doi.org/10.32721/ctj.2019.67.4.okafor

- Okafor, O. N., Mains, D., Olabiyi, O. M., & Warsame, H. (2018). How Did the CRA Expect the Adoption of IFRS to Affect Corporate Tax Compliance and Avoidance. Can Tax Journal, 66(1), 1–22.

- Oppong, C., & Aga, M. (2019). Economic growth in European Union: Does IFRS mandatory adoption matter? International Journal of Emerging Markets, 14(5), 792–808. https://doi.org/10.1108/IJOEM-01-2018-0010

- Organisation for Economic Co-operation and Development (OECD). (2019). Revenue Statistics for 2018. OECD.

- Organisation for Economic Co-operation and Development (OECD). (2020). Revenue Statistics https://www.oecd.org/tax/tax-policy/revenue-statistics-2522770x.htm