?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The research questions that are solved in this paper are as follows: (1) how the value relevance of accounting information evolved from a developing country perspective and (2) how the accounting reform impacts on value relevance. This study aims to assess the value relevance of accounting information released by non-financial firms listed on the Vietnam stock exchange for the period of 2010–2020. Our paper will contribute more supportive empirical evidence about the usefulness of value relevance research through doing research in Vietnam as a developing country, where experiences switching from a planned economy to an open economy and the regulations change continuously. We provide useful literature overview and important implications for both equity investors and standard setters. Based on usefulness information theory and asymmetric information theory, research hypotheses are designed. The study then uses the Ohlson price model to test these hypotheses. In the model, the explanatory variables, namely, book value per share, earnings per share, and share prices as independent variable, are examined; panel corrected standard error estimator (PCSE) is applied. The findings reveal that both earnings and book value of equity exhibit a positive and significant effect on stock prices. Earnings explain the higher variation in stock market values on the Vietnam Stock Exchange compared to book value of equity. The study, however, finds a decreasing trend in the change of the value relevance over the period 2010–2020 and accounting reforms in 2014 did not improve the value relevance.

1. Introduction

Value relevance of accounting information is one of the fundamental characteristics of accounting quality mentioned in accounting standards and academic research. The definition of value relevance is stated as a criterion in accounting standards, such as International Accounting Standard Board (IASB) articulated “Relevant financial information is capable of making a difference in the decisions made by users. Financial information is capable of making a difference in decisions if it has predictive value, confirmatory value, or both” (IASB, 2018, Conceptual Framework for Financial Reporting). The predictive value manifests itself if users can use accounting information as input data to analyse and predict future results from which to make their own decisions. The information is confirmatory if it confirms or provides feedback on a previous change.

Consistent with the criterion of IASB, under the conceptual Framework stated by the Financial Accounting Standard Board (FASB), an accounting amount is relevant if “it is capable of making a difference to financial statement users’ decisions”, Qualitative Characteristics of Accounting Information. All stated criteria are operationalized to measure the value relevance of empirical research. Besides, value relevance could be assessed using two different approaches: direct and indirect methods. In terms of the direct method, academic researchers developed a series of questions to assess the qualitative characteristics. Jonas Gregory and Blanchet (2000) have drawn five questions to assess the predictive value of value relevance based on earnings, and disaggregated information to evaluate the risk and opportunities to better understand a company’s prospects; further questions to assess confirmatory relating to disclosure accounting information, using estimates and assumptions to prepare financial statements. This method could be meaningful to assess the value relevance of each firm but would not enhance the usefulness of value relevance research for standard setters. Indirect methods are popular in accounting research, the value relevance studies are designed to “assess whether particular accounting amounts reflect information that is used by investors in valuing firms’ equity” (M. E. Barth et al., Citation2001). Therefore, accounting information is deemed relevant if it has a significant correlation with the equity market value of a company, which could be measured as stock price or stock return. Then, literature tests the association between accounting amounts and stock market metrics, and the results are seen as a proxy for value relevance. Beaver (Citation1968) and Ball and Brown (Citation1968) were the first researchers to investigate the value relevance of accounting earnings. After that, Ohlson (Citation1995) developed the definition of “value relevance” in an efficient market with accounting information including expected abnormal earnings and equity book value equal to stock markets. The Ohlson model covered important bottom lines of income statements and statements of financial position and allowed “other information”, which led to more usefulness of the model, so past studies adopted the Ohlson model to test the relevance of earnings and equity book value. In short, the indirect approach has several valuation models, such as using earnings and changes in earnings as representations of accounting numbers to assess value relevance of earnings (namely, return regression model) or combining earnings and book value as representations of accounting information (which is derived from Ohlson, Citation1995). This paper applies the Ohlson price model to evaluate the value relevance of accounting information in Vietnam stock market.

In the context of changing accounting regimes, Vietnam experiences flexibility in making accounting estimates, which triggers doubt on the value relevance of accounting information to investors. In addition, Vietnam’s stock market is being assessed as a frontier market, with a low regulatory environment and transparency. The paper is conducted with the research objectives of analysing and assessing the current situation and trends of fluctuations in value relevance of listed non-financial firms during the period from 2010 to 2020, then giving policy implications and recommendations.

Two main research questions we address are as follows: (1) how the value relevance of accounting information evolved in the global integration-oriented economy and (2) how the accounting reform impacts on value relevance.

The study investigates the relevance of accounting information in Vietnam in the period 2010–2020. Vietnam represents a suitable context for research because of its distinctive accounting regimes. The current accounting practice in Vietnam is different from domestic standards, and the legal system is conservative. This matter demands a harmonisation of accounting approaches and standards or convergence with international standards. Furthermore, the choice of this research period and Vietnam context is motivated by the fact that transition process in Vietnam can be seen as completed by 2000 by joining and becoming a member of the World Trade Organization (WTO), but until now, the stock market is still considered a frontier stock market, not yet upgraded to an emerging stock market, according to reports of the MSCI index (Morgan Stanley Capital International) and FTSE index (Financial Times Stock Exchange). This means that Vietnam’s institutions must be restructured, capital markets must be developed, and new accounting regulations must be introduced and keep progress moving. Vietnam has experienced shifting in economic and political systems, as well as changes in accounting regulations during the past 20 years. Moreover, the capital market has certain shortcomings with the Stock Price growth of some loss-making and fraud-prone companies. This situation will lead to concerns about the relevance of the information disclosed to investors, and investors may not rely on the financial accounting information to make decisions. Therefore, Vietnam is an ideal environment for statistical research to gain insight into the value relevance of accounting information based on the relationship between stock price and accounting measures.

The current paper seeks to make the following contributions to the existing literature. Firstly, this paper will enrich the usefulness of “value relevance” research for standard-setters. Holthausen and Watts (Citation2001) raised doubts about the usefulness of value relevance research to accounting standard-setters because these studies ignored important factors that influence the accounting standard (e.g. contracting) and link to valuation models. However, M. E. Barth et al. (Citation2001) offered a contrasting view and clarified misconceptions in the paper of Holthausen and Watts and then emphasised the role of value relevance studies in providing insights for standard setter, particularly, the value relevance studies are designed to test information used by equity investors rather than other users, so value relevance valuation models are relevant. Several empirical evidence is supportive of the conclusion of M. E. Barth et al. (Citation2001), by recognizing the importance of institutional factors and addressing how accounting regimes can affect value relevance of accounting information and demonstrate the validity of value relevance methodology. Ali and Hwang (Citation2000) find that countries where private-sector bodies are not involved in standard-setting processes have lower value relevance; also, value relevance is lower when tax rules influence financial accounting reporting. Paper of Katerina (Citation2006) confirms the value relevance of a transition economy is lower than in a well-developed market economy with well-developed accounting regulation. Many other studies show the correlation between institutional factors or accounting environments with value relevance such as Habib and Weil Citation2014 and Ahmed (Citation2018). Many studies have shown the validity of this value relevance approach, especially in cross-country comparison and the trend in value relevance. Studies have been conducted in both developed markets (Collins et al., Citation1997; Francis & Schipper, Citation1999; King & Langli, Citation1998) and emerging markets (Bismark & Opoku Appiah, Citation2018; Graham & King, Citation2000) and have shown mixed results due to differences in accounting regimes and measurements. Briefly, our paper will contribute more supportive empirical evidence about the usefulness of value relevance research through conducting research in transition country—Vietnam where experience switching from a planned economy to an open economy and regulatory reform are continuous and show how accounting regime can affect the value relevance of accounting information.

Secondly, in the paper, we consider the value relevance of more accounting numbers, including amounts that reflect information about assets and liabilities, not only earnings or both earnings and book value. Finally, we find controversial results to past studies, the value relevance of earnings and book value in Vietnam, has declined. Prior researches have found an increase in value relevance of accounting numbers in transition economy (Kell Hellstome, 2006) due to improvements in control and enforcement mechanisms that have a positive influence on the value relevance in the new economy. In order to investigate the trend in value relevance of earnings and book value, in accounting literature, studies measure value relevance by explanatory power R2 of the Ohlson price model on time trend, such as Outa et al. (Citation2017), Avwokeni (Citation2018), Bismark and Opoku Appiah (Citation2018), and M. E. Barth et al. (Citation2018). Nevertheless, in this paper, we regress residual standard deviation as an alternative measure on time trends, due to the inappropriateness of R2 according to Zhaoyang (Citation2007).

Again, the objective of this paper is to examine the value relevance of listed companies in the Vietnam Stock market, and to demonstrate better information that investors use to assess firm value and equity valuation. Moreover, the current paper could draw the role of new regulation in 2014 in accounting quality and understanding the value relevance of accounting information provides insights into whether current accounting policies are relevant in a transition economy. The empirical findings from Vietnam will have implications and can serve as an example for national, regional, and international investors and regulators regarding the usefulness of accounting information when making investment decisions. The paper is organised as follows. Section 1 raises research questions and purposes, Section 2 describes research context in Vietnam with accounting environment and stock market, while section 3 lists theories to explain hypotheses. Section 4 builds the hypotheses. Section 5 discusses the research design, while Section 6 discusses the results of the current study. Finally, Section 7 concludes and summarises the study.

2. Background of Vietnam stock exchange and accounting environment

The Vietnam Stock Exchange was established in 1998 and started growing in 2006 when regulations in terms of the stock market were issued. Currently, the exchange boasts of more than 700 listed companies categorised into different industrial sectors, namely, finance, manufacturing, distribution, insurance, and other many other corporate bonds. The development of the financial market attracts more and more local and foreign investors.

Although Morgan Stanley Capital International (MSCI) considered the Vietnam Stock Market to upgrade from frontier market to emerging market in 2019 but until now Vietnam has failed, Vietnam capital market still faces many potential issues regarding efficiency. Some studies evaluate the level of efficiency over different time periods and heance come to different conclusions.During the period of strong fluctuations of stock prices (such as stock bubbles from 2007 to 2008), market could not achieve weak-form efficiency, but during the period of decline stability, weak-form efficiency could be reached, as from 2010 to 2013, after the financial crisis, or from 2019 to present with the Covid pandemic. According to Vo Xuan Vinh (Citation2015), there have been many firms facing financial difficulties in after fianacial crisis in Vietnam. To improve the effectiveness of the capital market, most authors mention the improvement of disclosed information from listed companies. Due to instability of the market and the financial crisis, the change of regulation from accounting, taxation to corporate governance in Vietnam is to help the market be more adaptive. New accounting regulations were issued in 2014 to comply with global integration, and new corporate governance regulations were updated in 2017, which aim to enhance the transparency of information. Thus, evaluating the value relevance of information in the Vietnam context during 2010–2020 is appropriate because Vietnam is a new economy with an unstable stock market. This study will investigate the impact of new regulations on the quality of disclosed accounting information and support regulators in building appropriate rules.

2.1. Vietnam accounting environment

As a communist country with a strong centralised system, accounting standards and other accounting regulations are promulgated by the Ministry of Finance in Vietnam. In the first period, the Vietnamese Ministry of Finance retained the uniformed accounting system (UAS) to control and supervise firms more easily. By the time Vietnam joined the WTO to integrate into the world, Vietnam had attempted to converge with International Accounting Standards/International Financial Reporting Standards (IAS/IFRS) during the period 2001–2005 with the World Bank’s financial support (Narayan & Godden, Citation2000) to be accepted as a WTO member. From 2001 to 2005, Vietnam issued the first 26 standards under the support of the International Accounting Standard Board (IASB) and based on IAS/IFRS issued up to 2003. Detailed regulations were attached to guide the application of the standards in practice, as well as other additional amendments to align with financial policies and accompanying tax regulations. However, currently, new IFRS have been promulgated with subsequent amendments, but the Vietnam Accounting Standard (VAS) has not been updated. The level of convergence between VAS and IFRS is assessed to be quite high at the beginning (84%) and then drops to 63% in 2013 (Pham Hoai Huong, Citation2016). During the period 2010–present, the Ministry of Finance has only changed accounting regulations to be closer to the international accounting system, International Financial Reporting Standard (IFRS), by replacing Decision 15/2006/QD-BTC issue in Citation2006 with Circular 200/Citation2014/TT-BTC issued in 2014. Accounting regulations became the main guide for accounting practice at companies. The Vietnam Ministry of Finance has proposed a road map to apply IFRS with three stages: preparation phase (2019–2021); testing phase (2022–2025); mandatory phase (from 2025).

Circular 200/Citation2014/TT-BTC issued by Vietnam Finance Ministry on 22/12/2014, the essence of the accounting information is defined as the same as the definition listed in IFRS. Particularly, Article 101 Clause 2 Requirements for Information presented in Financial Statements states that “Financial information must be relevant to help users of financial statements predict, analyse and make economic decisions.” Relevance does not mean faithful presentation, or reliability in all material aspects. Subsequently, the Accounting Law No. 88/2015/QH13 was promulgated in favor of the Accounting Law promulgated in 2003 updating regulations regarding accounting documents and the preparation of financial statements. The changes in new regulations concentrate on the following items: taxes payable, “Foreign-currency-denominated assets”, inventory; Long-term assets; revenues and expenses, and owner’s equity. Compared to old regulations, new regulations are more flexible in designing accounting documents and accounting books. Besides, it is required to disclose and publish more information in the notes of financial statements. For example, the requirement of addressing characteristics of the business operation of the company: normal production and business cycles; demonstration of corporate governance structure; addressing the accounting policy applied for two cases where the enterprise meets the assumption of continuous operation and the enterprise does not; additional information for the items presented in the Statement of Financial Position, such as bad debts; financial loans, and lease debts; work in progress. Thus, new accounting regulations have been inherited but have not been fully applied international standards; so, the impact of this reform on the value relevance or quality of accounting information needs scrutiny to determine whether accounting regulation is effective or not.

3. Theoretical framework

The core theory applied in the paper to explain the research purpose is “usefulness information theory”. Research on value relevance will be meaningful to support the usefulness of information theory that indicates that disclosed information needs to be useful for users to make their own decisions. Information is compulsory to be published on the financial market, and the information users are mostly investors. After that, the investor seeks to profit from investment activity through an increase in the firm value from received dividends or an increase in the stock price of companies. Previous studies have considered the use of accounting information from both an instrumental and symbolic perspective (Ouda & Klischewski, Citation2019). The instrumental use of accounting information is mainly related to relevant information of decision-making that can affect the efficiency of an organisation and enhance its performance, while the symbolic use relates to legitimizing and confirming their decisions. Government politicians mainly need accounting information that improves the efficiency of the decision-making process. In our study, accounting information use is defined as instrumental use based on the purpose of use. The theory of useful information is also the basis for the drafting and promulgation of accounting standards. The definition of accounting information usefulness first appeared in accounting standards in 1966 in the United States, and has so far been concretized in written documents while concretizing the usefulness under the standards of relevance and reliability (according to the FASB and IASB). For example, the definition in IFRS “general purpose financial reporting is useful to present and potential investors, lenders and other creditors, who use that information to make decisions about buying, selling or holding equity or debt instruments” (IASB 2018). For equity investors, accounting information is used to assess the market value of a firm and its stock price.

The second theory is asymmetric information theory; G.A. Akerlof was one of the first researchers to study “asymmetric information theory” as well as the effects of asymmetric information on the market in general since 1970. In the stock market, asymmetric information occurs between the company as a provider of information and the investor as a decision-maker, or between investors in trading stocks. The listed companies have untransparent and incomplete financial information, uncovered and manipulated financial information, and sold shares at a price higher than the company’s real value, giving investors many disadvantages. Then, it can lead to the situation where companies with poor performance are traded more. Internal users have more information, and knowledge of the true value of the firm than external users. The solution to minimise the impact of asymmetry is the signaling expressed through providing transparent accounting information from the business. Financial reporting is a tool to reduce adverse choices, thereby reducing improvements in stock market performance and reducing market incompleteness (Scott, Citation2006). Therefore, the more information published, the lower the information asymmetry.

Finally, valuation theory; the value relevance of financial accounting information shows the ability of financial statements to capture proper information that affects stock price on market (Francis & Schipper, Citation1999). Popular valuation models under review are the price model and the return model. In both models, stock price and stock return are dependent variables and accounting figures are independent variables. Studies measure value relevance by a significant regression correlation, while the price model regresses market share price on accounting information such as earnings per share (EPS) and book value per share (BVS), and the return model regresses stock return on earnings (Easton & Harris, Citation1991). Accounting information will be relevant if the regression is significantly positive. The price model is based on Ohlson’s paper (Citation1995) which addressed “the idea that some value-relevant events may affect future expected earnings as opposed to current earnings, that is, accounting measurements incorporate some value-relevant events only after a time delay”. Dependent variables in the price model show reasonable summaries of two components of financial statements, namely, the balance sheet and the income statement. In addition, to investigate the value relevance, the Ohlson approach allows for “other information”, presenting a role for information that is reflected in price, but is reflected with a lag in the accounting numbers (Beaver, Citation2002). Thus, it is reasonable to adopt a price model in the current paper.

4. Empirical literature review and hypotheses development

Earnings and book value of equity are two primary accounting summary measures in the value relevance literature. Following a large literature review, earnings and book value of equity are relevant to investment decision-making, with a difference in usefulness level shown as different R-squared or adjusted R-squared of linear regression models. King and Langli (Citation1998) tested the price model in European countries, Graham and King (Citation2000) compared and tested the relevance of Asian countries from Indonesia, Malaysia, the Philippines, South Korea, Taiwan, and Thailand, the R squared ranged from 16.9%, lowest in Taiwan and highest in Korea (68.3%), the Philippines (68%), Thailand (39.7%), Taiwan (16.9%), Indonesia (30.8%), South Korea (68.3%), and Malaysia (27.7%). Table summarises R-squared, which represents the level of value relevance in accounting information in countries, including developed and developing countries. Aboubakar Mirza et al (Citation2019) did a study about value relevance in the Malaysian Capital Market over the period 2012–2016 and concluded that earnings, book value of equity, and cash flow from operations significantly and positively explain the variation in stock price with an R2 of 66.6%. The findings highlighted that earnings were not the most relevant accounting information because of the perception of managerial bias in financial reporting. M. E. Barth et al. (Citation2018) recommended that other amounts, such as assets, liabilities, tangible assets, and so on, which are important for firm value, be more relevant. Applying the usefulness information theory, value relevance is an expression of usefulness, share prices are likely to change upon the publication of a firm’s financial statements, so we propose the following hypothesis.

H1:

Earnings and book value are values relevant to investors in the Vietnam stock market.

Table 1. Summarising the R-squared or Adjusted R-square of price model

In developed countries, some previous studies have shown a decline in the value relevance of information, namely, Lev and Zarowin (Citation1999), which investigated the relationship between stock prices and accounting measures of US firms over 20 years, and found a weaker association between stock price and earnings for firms with more intangible assets and a decline in the value relevance of earnings and book value from the late 1970s to the early 2000s. Dichev and Tang (Citation2008) examined 1,000 US businesses over a 40-year period and concluded that it reduced the cost of the accounting information and set requirements for accounting regulation at fair value instead of the historical price. Collin et al. (Citation1997) suggested that the presence of poor financial performance and loss-making companies was responsible for the decrease. By contrast, the latest study by M. E. Barth et al. (Citation2018), studied between 1962 and 2014 in the United States, shows no evidence of a decrease in the relevance of information.

In developing countries that have new economies and are on the verge of changing policies, the results mostly show the growing value of relevance. For example, the study comes from Katerina (Citation2006) who investigated capital markets in the Czech Republic between 1991 and 2004. During this period, the Czech Republic is considered a transition country with its own accounting system. At the same time, the author compares the value relevance of information in the Czech stock market with the Swedish financial market, which is a developed country with a perfect accounting legal framework. The results also showed that the value relevance of accounting information in Sweden is higher than in the Czech Republic. Omran and Tahat (Citation2019) tested the Kuwait market in the period 2015–2018 and concluded that accounting information is relevant, but the book value information tends to increase while the earning value tends to decrease. Vietnam is an emerging economy, and the stock market has been considered to upgrade from frontier market to emerging market. It has performed regulation reform during the period 2010–2020, including the accounting regulation of 2014 and other tax rules. The paper expects an increasing relevance of earnings and book value.

H2:

The relevance of earnings and book value has increased.

Beaver (Citation2002, p. 460) stated that “value relevance research demands an in-depth knowledge of accounting institutions, accounting standards” and consideration of accounting context will enhance the richness of value-relevance research. To transition economies, transforming accounting regulation is necessary to satisfy the requirements of the market economy as well as integrate with the global economy. K. Hellstrom (2006) suggested that the beginning of the reforming period could lack value relevance, but the implementation of new accounting regulations would have a positive effect on value relevance. Habib and Weil (Citation2008) tested the influence of new accounting rules in Australia and found a corresponding increase in the incremental explanatory power of equity book values in the post-regulation period. Many countries around the world have undergone reform of their accounting systems, most commonly the full adoption of IFRS, and the impact of this reform on value relevance gives different results. Bhatia and Mulenga (Citation2019) synthesised 90 empirical research papers published between 1993 and 2016 from various countries across continents, and the majority of them concluded that accounting information is relevant across continents before and after IFRS adoption but showed improvement in accounting information after IFRS adoption.

Under the IFRS regime, earning manipulation and information asymmetry are less, which leads to higher disclosure and increase in the value relevance and quality of accounting information. This is the conclusion of research by M. E. Barth et al. (Citation2008) who collected data from 327 firms in 21 different countries that adopted IFRS between 1994 and 2003. Similarly, Iatridis and Rouvolis (Citation2010) evaluated the benefits of IFRS over UK GAAP regarding value relevance; the IFRS-based model had a higher R2 and positive significant coefficients for both net profit and book value compared to the GAAP-based model. In the model of profit on stock returns, the IFRS model also had a higher R2 and positive coefficient compared to the UK GAAP model. Adoption of higher-quality standards (IFRS) leads to an increase in the value relevance of both the equity book value and the earnings. Next, Ahmed (Citation2018) did a comparative study of IFRS conversion between European countries using the Ohlson model and showed that voluntary IFRS negatively affects the value relevance of equity book value and earnings. However, for mandatory IFRS adoption firms, the higher-quality standards (IFRS) lead to an increase in the value relevance of both equity book value and earnings. Japhet (Citation2022) reviewed some value relevance studies in African markets, using the Ohlson model, and made comparisons of the explanatory power R2 of sample pre-implementation IFRS and post-implementation IFRS. Findings were consistent with the fact that there was a higher value relevance during the IFRS regime (Avwokeni, Citation2018; Outa et al., Citation2017). In particular, according to the study of Tunyi et al. (Citation2020), though IFRS allows more managerial discretion, such as the IFRS 3 amendment, the value of intangible assets becomes greater in high-quality institutional contexts.

A few papers on the relationship between accounting reform and value relevance in Vietnamese markets were found. As mentioned, in the period 2010–2020, Vietnam has changed accounting rules, specifically, in 2014, the Ministry of Finance issued Circular 200/TT-BTC and Circular 202/TT-BTC to replace Decision 15/QD-BTC issued in Citation2006. The change in the view of recording information as “Substance over form” shows the willingness to change the legal framework to converge with the international regulatory framework, a higher-quality standard with a requirement for more information. And drawing on asymmetric information theory, accounting regulations aim to promote transparency and minimise asymmetries. Therefore, the authors expect that the change in regulations in Vietnam will also increase financial reporting standards.

H3:

Accounting reform positively affects the value relevance of accounting information.

5. Research method

5.1. Data

The dataset consists of all non-financial enterprises listed on the Hanoi Stock Exchange (HNX) and Ho Chi Minh City Stock Exchange (HOSE). The study period is between 2010 and 2020. There are a total of 745 listed firms in the Vietnam Stock Market from HOSE and HNX stock markets, the two markets that classify sectors according to different standards. HNX is sub-sectoral according to HaSIC standards—the classification standard of Hanoi Stock Exchange, while HOSE adopts the global industry classification standard—GICS, and the market measurement index is the VN index. The industrial sector accounts for the largest proportions in both HOSE and HNX (Table ).

Table 2. Industry classification

The unselected firms were insurance companies, securities companies, insurance companies, and banks due to differences in accounting regulations and accounting regimes; and the sample excludes missing data. Table presents a sample selection in this paper.

Table 3. Sample selection

After collection of data and selection of appropriate observations, the research sample has 5985 firm-year observations that provide sufficient research information. The dataset will be designed as tabular data and processed through STATA 14 statistical software. With the dataset obtained, the paper reclassifies enterprises according to Vietnamese industry classification regulations (Table ).

Table 4. Industry reclassification

5.2. Research design

The Ohlson price model that implies “that the market value equals the book value adjusted for (i) the current profitability as measured by abnormal earnings and (ii) other information” (Ohlson, Citation1995) will be applied in the paper. The model expresses the market value of firms as a linear relationship with equity book value and earnings (stock price). To examine the value relevance of earning and equity book value, the paper adopts the following model (1):

If BVS and EPS are value relevant, there will be an association between the total market value and earnings and book value and the coefficients on earnings and book value will be statistically significant. The dependent variable is the stock price, which could be collected at the end of the fiscal year or 1 month, 3 months, and 6 months after the fiscal year or at the time of released financial statements. Due to the ineffective stock market in Vietnam and the deadline for the financial statement’s submission being 90 days after the end of the fiscal year, this paper will take stock prices at 3 months after the end of fiscal year. The independent variables include book value per share and earning per share. Book value per share (BVS) refers to a firm’s total assets minus total liabilities divided by the number of ordinary shares. EPS is calculated by dividing the earnings after interest and taxes of a firm by its weighted average number of ordinary shares. The steps in performing quantitative studies of regression analysis are as follows:

Step 1: Examining the value relevance of earning per share and book value per share

We regress models 1.2. and 3 to test the usefulness of earning and book value using an estimator of the covariance matrix of the estimated parameter (PCSE—Panel corrected standard error). This paper used the Immtest (White ’test’, 1980) to detect heteroscedasticity, and the Wooldridge test to detect autocorrelation. To overcome the problem of the model encountered with the cross-section data, many studies use the FGLS estimator (Feasible Generalized Least Squares) for the regression model. However, FGLS estimators do not calculate the R2 and are not suitable for large denominator cross-data (the number of observations is much greater than the number of years of observations) because of their tendency to produce unacceptable standard errors unit (Beck & Katz, Citation1995) and ignorance heterogeneity. Therefore, Beck & Katz propose to use PCSE (Panel Corrected standard Error). PCSE has been used in many value relevance studies to deal with the problems of autocorrelation, heteroscedasticity, and cross-sectional dependence (Aboubakar Mirza et al., Citation2019).

Where: Pit = market price per share for firm i 3-month after the end of financial year t; EPSit = the earnings per share of firm i at time t;

BVSit = the book value per share of firm i at time t;

and ε it = other value relevant data.

In addition, the paper also developed the Ohlson model to check the value relevance of some accounting amounts (refer to Ferguson et al, Citation2020 and M. E. Barth et al., Citation2018). In detail, resource information reflected in equity valuation includes assets and liabilities. To test the relevance of this resource information, we develop model 1 and decompose book value into its components:

Where i and t denote the firm and year, respectively, Pit is a dependent variable measured by the stock price of the firm’s i after the 3-month ending fiscal year t. Accounting figures are independent variables, including EPS is the earnings per share; other items on balance sheet scaled on number of outstanding share are cash (CASH), receivable (RECEIV), investment (FINANCE), inventory (INVENT), noncurrent assets such as property, plant and equipment, intangible assets and goodwill (NOCA), and total liabilities (LIAB).

Step 2: Assess the value relevance of loss firm group and positive profit firm group.

Adopting regression model 1, the paper compared and evaluated the regression results of a research sample consisting only of positive profit enterprises with those of negative profit enterprises. Findings in this step are helpful to explain the empirical results in step 1.

Step 3: Assess the evolution of value relevance.

To find out the trend in value relevance, we regress on time (Year), and the following equation is performed:

Where: dependent variable (VR) is measured by R squared taken from yearly regression model 1 (M. E. Barth et al., Citation2018; Bismark & Opoku Appiah, Citation2018); or the residual variance or equivalently residual standard deviation as alternative measure (Zhaoyang, Citation2007). Independent variable (Year) is time corresponding to year 1, year 2, …year 11

Step 4: Assess the impact of accounting reform on value relevance.

To examine the effect of accounting regulation in the post-reform period, we use both multivariate and univariate approaches. Multivariate analysis is performed by running Equationequation 6(6)

(6) . In this method, accounting reform is considered as moderator in the relationship between accounting numbers (EPS and BVS) and Stock price. If accounting reform in 2014 positively affects value relevance, both BVS and EPS would positively interact with the regulatory variable as a dummy variable.

Where: Pit = market price per share for firm i 3-month after the end of financial year t; EPSit = the earnings per share of firm i at time t; BVSit = the book value per share of firm i at time t; and Y is a dummy variable that takes “1” if year t from 2015 to 2020 (the year that the new accounting regulation took effect) and takes “0” otherwise.

Then, the paper conducts a univariate analysis that compares the adjusted R2 s between the pre- and post-regulatory periods derived from EquationEquations (1)(1)

(1) –(Equation3

(3)

(3) ).

Step 5: Control variable—Impact of Firm size on Value relevance

Value relevance of accounting information could be affected by firm-specific economic factors. Firm size is a possible fundamental economic factor that could affect the relationship between stock price and accounting numbers (Collins et al., Citation1997). Therefore, it is important to investigate value relevance after controlling for the effect of a firm-specific variable. In the paper, we partition the sample into large and small firms (Brimble & Hodgson, Citation2007; Chandrapala, Citation2013; Chen et al., Citation1999; Collins et al., Citation1997). Consistent with Brimble and Hodgson (Citation2007), Bismark Badu and Kingsley Opoku Appiah (Citation2018) and compliance with Vietnam regulations, total assets are used as the benchmark for the classification of firms as either large or small. A univariate analysis, which compares the adjusted R2 s between two samples taken from EquationEquation 1(1)

(1) -Equation3

(3)

(3) is performed.

6. Empirical results and discussion

6.1. Descriptive statistics

Table presents the descriptive statistics of dependent variable and independent variable of the model Ohlson. The share price (P) is at 31/3 following the fiscal year t. Data statistics show that the lowest share price is 400 VND and the highest is 261,500 VND, the average value is 21,478 with a dispersion of 23,836. The lowest equity-to-book value (BVS) indicator is −8,302. The reason for the negative value is that the BVS of Truong Thanh Wood Industry Group Joint Stock Company (TTF) in 2019 and 2020 are negative (1879) and (2030), respectively, because the company has accumulated losses for many consecutive years with accumulated losses of more than 3,000 billion VND. The book value of equity per share on average is 18,312, and standard deviation is 11,150. The earning per share (EPS) is measured by the company’s after-tax profit indicator on the average number of outstanding shares, with the largest value of 78,880 and the smallest (12,648) due to the enterprise operating loss. On the other hand, the mean is 2,532 and the dispersion is not high with a value of 3,361.

Table 5. Descriptive statistics

6.2. Test for multicollinearity

Table illustrates the results of Pearson correlation. The BVS and EPS variables are correlated with the dependent variable, which is the stock price (P) variable. This also means that the linear regression model Ohlson (1) would be ideal for research. There is no coefficient exceeding 0.8, so the regression model that considers the value relevance of net income, equity book value, and other accounting amounts is appropriate.

Table 6. Pearson correlation (* significance at 0.1 level , ** significance at 0.05 levels, *** significance at 0.01 significance levels

6.3. Empirical finding and discussion

Hypothesis H1:

Earnings and book value are values relevant to investors in the Vietnam stock market.

In this section, the paper tests H1 hypothesis by using the Price model developed by Ohlson (Citation1995) and the R-squared of regression result is used as the key metric for measuring value relevance of accounting information. Pit = β0 + β1*BVSit + β2*EPSit + εit (1)

BVS and EPS will be relevant if the coefficients of BVS (β1) and EPS (β2) are positive and significant. As can be seen in Table , the explanatory power of price regression (1) is 41.8%, and both independent variables are significant at 1% level. According to Ohlson’s accounting-based valuation framework (1995), the coefficient on abnormal earnings is α1=ω/(R-ω) where R is the discount rate and ω is the persistence coefficient. Assuming a discount rate of 10%, the coefficient of 3.93 equals a persistence of about 85% which can be considered quite high for sample firms. In conclusion, the paper accepts Hypothesis 1 and the threshold of 42% for Vietnam’s financial market is quite optimistic. Besides, when separately evaluating the usefulness of earnings and book value of equity based on model 2 and model 3, the EPS-R2 is higher in both periods with 0.404 in comparison with the BVS-R2, meaning that the ability to explain stock price changes of EPS is 40% while BVS is only 21%. Briefly, EPS is more relevant for investment decision-making than BVS.

Table 7. Result of regression test

Column 4 in Table indicates the independent variables, including Cash, Receive, Finance, Inven, and Nonca all have positive regression coefficients and are significant at the level of 1%. In other words, the growth of business scale (assets) will increase the stock price. With the adjusted R-square of model 4 of 0.436 being higher than that of model 1, this means that these indicators can explain more the variance of stock prices and are relevant to decision-making. Finally, the independent NONCA variable has the opposite effect on the dependent variable (coefficient is less than 0 and has a statistical significance of less than 1%), this shows the relevance of the liabilities amount, the larger the debt, the lower the stock price.

The above empirical findings in this study support useful accounting information theory and articulate the role of accounting information for users from both a practical and regulatory perspective. Accounting numbers (earnings, equity book value, and other amounts) are relevant, and this conclusion is consistent with past empirical research (Aboubakar Mirza et al.,Citation2019; M. E. Barth et al., Citation2018; Bismark Badu & Kingsley Opoku Appiah, 2018; Graham & King, Citation2000; King & Langli ,Citation1998). These findings also insist on the usefulness of the Ohlson valuation model. Vietnam is an inefficient market, and the Ohlson approach allows delayed recognition of accounting numbers, so we select stock prices at the surrounding announcement date. At this date, the accounting information is relevant to users. A further analysis is performed with stock price at the fiscal year-end in order to check the robustness of the results, which measure stock price as the independent variable in EquationEquation 1(1)

(1) , at the end of the fiscal year. As per the robustness analysis shown in Table , both EPS and BVS are significantly positive with stock price. Therefore, accounting information at the end of the financial year and the announcement date are both relevant. This will reduce the price reaction at the earnings announcement date, reduce the information asymmetry, and affirm that financial reports will mitigate the information asymmetry in the Vietnam context. Furthermore, in the Ohlson approach, the concepts of forecasting relevance and time-series persistence of earnings are different. With an efficient market assumption, the timing of information is not a primary concern, which means that the accounting information could reflect the price reaction over a longer time before the information announcement date, so the value relevance research sets market value at a point in time as a function of accounting reports at the end of the financial year. Thus, even in Vietnam, an inefficient market, it is still reasonable to adopt the Ohlson model.

Next, BVS is less relevant than EPS, which may be due to the perception of managerial bias in the financial reporting (examples: allowance for bad debts and inventory obsolescence). Therefore, to enhance the value relevance of BVS, we imply that firms need more explanations in the note of financial statements about accounting estimates. Overall, to improve the value relevance of accounting numbers, we recommend enhancing the forecast and confirmatory value of financial statements by providing more disclosure and explanations about the financial volatility of accounting amounts on financial statements.

Moreover, Collin et al. (Citation1997) found that earnings are a value-relevant factor in profit firms, while the book value of equity is relevant in loss firms. In the dataset, firms with positive profitability account for nearly 95% of the sample, with 5658 firm-year observations with positive profits; therefore, the empirical results in models 2 and 3 are reasonable, which show that EPS is more useful than BVS. To increase the reliability of the study, the paper further tested regression models 2 and 3 against two separate samples, a sample of companies with positive profits and a sample of companies with negative profits. Table represents the intercept of earning and book value coefficients that are both positive and significant in a group of positive earning firms, while EPS-R2 is higher than BVS-R2. On the other hand, in loss-making firms, EPS is insignificant and R-squared is quite low, while BVS is positive and significant at the 1% level. Thus, investors should focus more on the book value of equity as a proxy for assessments than earnings in terms of firms with the worst financial performance.

Hypothesis H2:

The relevance of earnings and book value has increased.

Table 8. Result of regression test with positive earning firms and negative earning firms

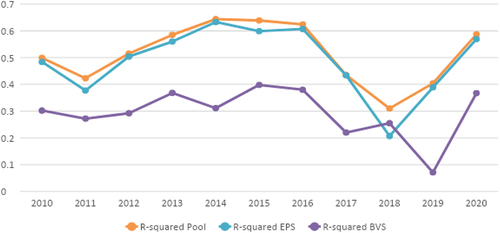

Table demonstrates the results of yearly cross-sectional regression. Overall, the average coefficients and the t-statistics for book value and earnings were significant and positive for all the models (p < 0.01). Moreover, the mean R-squared suggests earnings can explain more than 50% of the variation in stock price. The results across the two models confirm H1 that book value and earnings were relevant to shareholders. If companies make a profit, their share price will increase. The results emphasise that the income statement and the statement of financial position provide more useful information to market participants in the Vietnam capital market. R-squared of model 2 ranges from 0.37 to 0.63, regarding the value relevance of earning, which is higher than the R-squared of model 3, which shows the value relevance of book value below 0.45 on average.

Table 9. Pooled and yearly cross-sectional regressions on earnings and book value (standard errors in parentheses *** p < 0.01, ** p < 0.05, * p < 0.1)

There is a fluctuation in R-squared of all three models during the research period in Figure , while R2 increased in the pre-reform period from 2011 and gradually decreased in the post-reform period, with a peak in 2014.

Figure 1. The fluctuation of explanatory power adjusted R2.

Table presents the formal test results on the time-varying pattern of R-squared. OLS regressions are run for the following equation: VR = θ0 + θ1 *Yeart + εit (5), where VR is the R-squared at time t of EquationEquation 1(1)

(1) , Year is time corresponding to year 1, year 2, …year 11. There is a negative correlation between R2 and time, but it is insignificant, so there is no statistical evidence of a time trend on value relevance for the period 2010–2020.

Table 10. Association between R2 and time trend 2010–2020

However, in accounting studies, making across-sample R2-comparisons based on linear models is popular, but R2-comparisons are rarely done in econometrics, so Zhaoyang gu (2007) suggests the residual variance, or equivalently residual standard deviation as an alternative measure of explanatory power for across-sample comparison. The economic meaning of residual dispersion contrasts with R2 because the residual variances or standard deviations measure the dispersion of components in the price model (1) that cannot be explained by the accounting variables. Thus, the paper reassesses the trend of value relevance with residual dispersion. Residual standard deviations are taken for each year from regression the model 1. Table reports the descriptive numbers of residual standard deviations and regression test results of the following equation: VR = θ0 + θ1 *Yeart + εit (5), where VR represents the estimated residual standard deviation and Year is time corresponding. The positive correlation between time and residual standard deviation reveals an increasing trend in pricing errors in model 1 which contrasts with a decreasing trend in the value relevance of accounting information. Briefly, this study rejects hypothesis 2. This finding is similar to previous studies, examples: Lev and Zarowin (Citation1999), Dichev and Tang (Citation2008), Collin et al. (Citation1997), and Bismark Badu and Kingsley Opoku Appiah (2018). In the paper, the value of earnings and equity book value were expected to improve and increase. However, the findings in Table provide evidence of a decline in value relevance that suggests a decline in the usefulness of financial statements during the study period from 2010 to 2020. The reasons may be due to the increase in non-financial information in the Vietnam Stock market, corporate governance regulations have also been reforming and encouraging firms to disclose more voluntary information. Another reason could be the incompleteness of accounting reform, which has not yet updated the full international standard.

Hypothesis H3:

Accounting reform positively affects the value relevance of accounting information.

Table 11. Association between residual dispersion and time trend 2010–2020

To examine the effect of accounting regulation in the post-reform period, we run the regression of Stock price (Pt) on BVS and EPS, and then add Y as a dummy variable that takes “1” if year t from 2015 to 2020 (the year new accounting regulation took effect) and takes “0” otherwise.

In this study, the coefficient of interaction between BVS and EPS with Y indicates how much the value relevance of equity book value and earnings during the period of old accounting regulation differs from the period of new accounting regulation. It is hypothesised that upon the issuance of new accounting rules, the value relevance of equity book value (α 4) and earnings (α 5) increases. That is, the differential intercepts α 4 and α 5 are expected to be positive. However, the resulting Panel A in Table represents that only the interaction coefficient of earning is positive and significant statistically, while book value has significance at the 1% level but is negative. New accounting rules only improve the relevance of earnings and do not affect the relevance of accounting information in general. Another approach is adopted to test the impact of the 2014 regulatory reform on value relevance, a univariate approach. In a univariate test, the adjusted R2 s is compared between the pre- and post-regulatory regimes. After regression models 1, 2, and 3 for the periods 2010–2014 and 2015–2020, adjusted R2s are indicated in panel B. The explanatory power of accounting information and each proxy EPS and BVS on the variance of stock price is 49,6%, 46,9%, and 30,4%, respectively, greater during the pre-reform period. These figures consolidate the negative influence of accounting regulations on value relevance and are also consistent with the decline in time trend, so we reject hypothesis 3. Our findings are different from those of Bhatia and Mulenga (Citation2019) Outa et al. (Citation2017) and Avwokeni (Citation2018) which show the increase in value relevance due to the adoption of IFRS, but are similar to those of Bismark Badu and Kingsley Opoku Appiah (2018) which find a negative impact of IFRS on the value relevance of book value and earnings in Ghana and Habid and Weil (2008) who found a negative influence of new accounting rules in Australia on the value relevance of earnings. Higher regulations are expected to enhance the quality of accounting information and minimise the information asymmetry, but the paper shows that new accounting regulations in 2014 in Vietnam do not improve the relevance of earnings and book value. The reason could be explained by the fact that Vietnam has not yet updated its domestic standard, so there are differences between accounting policies and domestic standards, which trigger a multitude of accounting policies and choices, then confuse accountants. Basiem (Citation2021) “suggests that the relevance of accounting information to the market may be affected by its reliability in terms of establishing firm value”, so the flexible accounting policies will facilitate managerial discretion and reduce the reliability of accounting information. The road map of the Vietnam government on the full application of IFRS has three stages: the preparation phase (2019–2021); the testing period (2022–2025); and the mandatory period after 2025. With the negative impact of accounting regulation, in 2014, we recommend that governments accelerate the process of issuing policies guiding the application of IFRS to facilitate its future applications, which will contribute to harmonisation between the accounting approach and standards. Tunyi et al. (Citation2020) find a significant positive impact of the IFRS amendment on the value relevance of intangible assets, and more importantly, this improvement is only effective in the presence of strong institutions. Therefore, the study of Tunyi et al. (Citation2020) suggests that “introduction of accounting standards and reforms should be pursued jointly with efforts to improve the broader institutional environment within which companies operate”, such as control of corruption, government effectiveness, political stability, and so on. Thus, the other reason for the inefficiency of the accounting reform in Vietnam could be due to the institutional environment.

Table 12. Impact of accounting reform on value relevance

6.4. Control variable: impact of firm size on value relevance

Many previous studies provide statistical evidence that accounting information from large companies is more relevant than that from small and medium companies. According to Habid and Weil (2008), small and medium firms include start-up firms, which are more likely to face financial distress. Furthermore, the level of information disclosure from large firms is better, and more information may help investors choose a better portfolio. Hodgson and Clarke (Citation2000) examined the relevance of 121 Australian companies between 1989 and 1996, using stock returns rather than share prices to measure dependent variables in the Ohlson model due to scale problems, and finally found a positive correlation between firm size and value relevance. Brimble and Hodgson (Citation2007) re-examined the value relevance in the Australian market between 1974 and 2001. Bismark Badu and Kingsley Opoku Appiah (2018) tested hypotheses on firm-size in Ghana, an emerging market, and also came to the same conclusion.

Table presents that, overall, the group of large companies has a higher adjusted R2 and a higher adjusted EPS-R2, a lower BVS-R2. Besides, earnings of large firms explained stock price better than book value of equity, but the explanatory power of earnings and book value in small firms seems to be equal, with EPS-R2 0.235 and BVS-R2 of 0.230. The different results can be explained by the fact that in the study sample, there are 328 firm-year observations that companies had negative profits year-on-year. Of these 328 observations, 44 are small firms. The proportion of loss firms in the small group is 8%, and in the large group, the loss firms account for 5%. The higher percentage of loss companies in the group triggers a higher relevance of BVS, in line with the results of the study in Table .

Table 13. Difference of value relevance between small and large companies

7. Conclusion

This study was motivated by investigating the value relevance of financial accounting information in the Vietnam stock market, where there is a lack of value relevance testing over the long term. We used the Ohlson (Citation1995) price model to examine the hypotheses stated. The findings indicate that both book value, earnings, and other accounting amounts in the financial statement together explain the share price with a positive coefficient. This result is consistent, validates the theory that earnings and book value are statistically related to share prices, and is consistent with past studies in both emerging economies. However, earnings are more relevant than equity book value. As accounting information is value relevant to market participants, standard setters and accounting practitioners must constantly review financial reporting standards to sustain the relevance of accounting information, and Vietnamese regulations need more explanation about the definition of value relevance. Also, we recommend improving the value relevance by enhancing the forecast and confirmatory value of financial statements with more explanations about accounting estimates.

Other empirical findings include a decreasing trend in value relevance for 11 years and new accounting regulations in 2014 that do not enhance value relevance. Therefore, the study provides a useful literature overview and important implications for both investors and standard-setters. We imply that adoption of International Financial Reporting Standards in Vietnam should accelerate to harmonise accounting regulations with accounting standards.

The limitations of the paper are (1) only using the price model of Ohlson to examine the value relevance and (2) purpose of the paper towards equity investors in the stock market; some other information users such as credit investors and financial institutions need information and use accounting information for different purposes. (3) We currently do not consider institutional contexts such as political problems or corruption. Therefore, further research could consider a different model instead of the Ohlson model to measure the value relevance of accounting information for other users. Besides, the sample excluded listed financial companies (banks, insurance companies, and other financial companies) due to the difference in accounting regime. This limitation of the paper is also a new step for future research on different samples.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Huu Anh Nguyen

Huu Anh Nguyen is a Professor, Dean of School of Accounting and Auditing, National Economics University, Hanoi, Vietnam. His main research interests include corporate finance, accounting, and contemporary financial economics. He has published several research papers.

Thi Tra Giang Dang

Thi Tra Giang Dang is a lecturer at the School of Accounting and Auditing, National Economics University, Hanoi, Vietnam. Her research and teaching interests are in the areas of contemporary issues in accounting, corporate finance, and corporate governance.

References

- Ahmed, K. (2018). IFRS and value relevance: A comparison approach before and after IFRS conversion in the European countries. Journal of Applied Accounting Research, 19(1), 60–23. https://doi.org/10.1108/JAAR-05-2015-0041

- Ali, A., & Hwang, L. (2000). Country-specific factors related to financial reporting and the value relevance of accounting data. Journal of Accounting Research, 38(1), 1–21. https://doi.org/10.2307/2672920

- Avwokeni, A. J. (2018). On the value relevance argument: Do market participants place a premium on future prospects of the firm? Journal of Financial Reporting and Accounting, 16(4), 660–676. https://doi.org/10.1108/JFRA-02-2017-0012

- Ball, R., & Brown, P. (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research, 6(2), 159–178. https://doi.org/10.2307/2490232

- Barth, M. E., Beaver, W. H., & Landsman, W. R. (2001). The relevance of the value relevance literature for financial accounting standard setting: Another view. Journal of Accounting and Economics, 31(1–3), 77–104. https://doi.org/10.1016/S0165-4101(01)00019-2

- Barth, M. E., Ken, L., & McClure, C. (2018). Evolution in value relevance of accounting information. Stanford University Graduate School of Business Research Paper No. 17-24, Available at SSRN: https://ssrn.com/abstract=2933197orhttps://dx.doi.org/10.2139/ssrn.2933197

- Barth, M. E., Landsman, W. R., & Lang, M. (2008). International accounting standards and accounting quality. Journal of Accounting Research, 46(3), 467–498. https://doi.org/10.1111/j.1475-679X.2008.00287.x

- Basiem, A.-S. (2021). The consequence of earnings management through discretionary accruals on the value relevance in Saudi Arabia. Cogent Business & Management, 8(1), 1. https://doi.org/10.1080/23311975.2021.1886473

- Beaver, W. H. (1968). The information content of annual earnings announcements. Journal of Accounting Research, 6(3), 67–92. https://doi.org/10.2307/2490070

- Beaver, W. H. (2002). Perspectives on recent capital market research. The Accounting Review, 77(2), 453–474. https://doi.org/10.2308/accr.2002.77.2.453

- Beck, M., & Katz, J. N. (1995). What to do (and not to do) with time-series cross-section data. The American Political Science Review, 89(3), 634–647. https://doi.org/10.2307/2082979

- Bhatia, M., & Mulenga, M. J. (2019). Value relevance of accounting information: A review of empirical evidence across Continents. Jindal Journal of Business Research, 8(2), 179–193. https://doi.org/10.1177/2278682118823307

- Bismark, B., & Opoku Appiah, K. (2018). Value relevance of accounting information: An emerging country perspective. Journal of Accounting & Organizational Change, 14(4), 473–491. https://doi.org/10.1108/JAOC-07-2017-0064

- Brimble, M., & Hodgson, A. (2007). On the intertemporal value relevance of conventional financial accounting in Australia. Accounting & Finance, 47(4), 599–622. https://doi.org/10.1111/j.1467-629X.2007.00241.x

- Chandrapala, P. (2013). The value relevance of earnings and book value: The importance of ownership concentration and firm size. Journal of Competitiveness, 5(2), 98–107. https://doi.org/10.7441/joc.2013.02.07

- Chen, C. J. P., Chen, S., & Su, X. (1999). Is accounting information value-relevant in the emerging Chinese stock market? Journal of International Accounting, Auditing & Taxation, 10(1), 1–22. https://doi.org/10.1016/S1061-9518(01)00033-7

- Circular 200/2014/TT-BTC issued by Vietnam Finance Ministry on 22/12/2014.

- Collins, D. W., Maydew, E. L., & Weiss, I. S. (1997). Changes in the value-relevance of earnings and book values over the past forty years. Journal of Accounting and Economics, 24(1), 39–67. https://doi.org/10.1016/S0165-4101(97)00015-3

- Decision 15/2006/QD -BTC issued by Vietnam Finance Ministry on 20/03/2006.

- Dichev, I. A., & Tang, V. W. (2008). Matching and the changing properties of accounting earnings over the last 40 years. The Accounting Review, 83(6), 1425–1460. https://doi.org/10.2308/accr.2008.83.6.1425

- Easton, P., & Harris, T. (1991). Earnings as an explanatory variable for returns. Journal of Accounting Research, 29(1), 19–36. https://doi.org/10.2307/2491026

- Ferguson, A., Kean, S., & Pündrich, G. (2020). Factors affecting the value-relevance of capitalized exploration and evaluation expenditures under IFRS 6. Journal of Accounting, Auditing & Finance, 36(4), 802–825. https://doi.org/10.1177/0148558X20916337

- Francis, J., & Schipper, K. (1999). Have financial statements lost their relevance? Journal of Accounting Research, 37(2), 319–352. https://doi.org/10.2307/2491412

- Graham, R., & King, R. (2000). Accounting practices and the market valuation of accounting numbers: Evidence from Indonesia, Korea, Malaysia, the Philippines, Taiwan, and Thailand. The International Journal of Accounting, 35(4), 445–470. https://doi.org/10.1016/S0020-7063(00)00075-3

- Habib, A., & Weil, S. (2008). The impact of regulatory reform on the value-relevance of accounting information: Evidence from the 1993 regulatory reforms in New Zealand. Advances in Accounting, 24(2), 227–236. https://doi.org/10.1016/j.adiac.2008.08.010

- Hodgson, A., & Clarke, S. P. (2000). Earnings, cash flow and returns: Functional relations and the impact of firm size Accounting and Finance. Accounting & Finance, 40(1), 51–73. https://doi.org/10.1111/1467-629X.00035

- Holthausen, R., & Watts, R. (2001). The relevance of the value-relevance literature for financial accounting standard setting. Journal of Accounting and Economic, 31(1–3), 3–75. https://doi.org/10.1016/S0165-4101(01)00029-5

- Iatridis, G., & Rouvolis, S. (2010). The post-adoption effects of the implementation of international financial reporting standards in Greece. Journal of International Accounting, Auditing & Taxation, 19(1), 55–65. https://doi.org/10.1016/j.intaccaudtax.2009.12.004

- Japhet, I. (2022). Value relevance and changes in accounting standards: A review of the IFRS adoption literature. Cogent Business & Management, 9(1), 2039057. https://doi.org/10.1080/23311975.2022.2039057

- Katerina, H. (2006). The value relevance of financial accounting information in a transition economy: The case of the Czech republic. European Accounting Review, 15(3), 325–349. https://doi.org/10.1080/09638180600916242

- King, R. D., & Langli, J. C. (1998). Accounting diversity and firm valuation. The International Journal of Accounting, 33(4), 529–567. https://doi.org/10.1016/S0020-7063(98)90012-7

- Lev, B., & Zarowin, P. (1999). The boundaries of financial reporting and how to extend them. Journal of Accounting Research, 37(2), 353–385. https://doi.org/10.2307/2491413

- Mirza, A., Malek, M., & Abdul-Hamid, M. (2019). Value relevance of financial reporting: Evidence from Malaysia. Cogent Economics & Finance, 7(1), 1651623. https://doi.org/10.1080/23322039.2019.1651623

- Narayan, F. B., & Godden, T. (2000). Financial management and governance issues in Vietnam. The Asian Development Bank.

- Ohlson, J. A. (1995). Earnings, book values and dividends in security valuation. Contemporary Accounting Research, 11(2), 661–688. https://doi.org/10.1111/j.1911-3846.1995.tb00461.x

- Omran, M., & Tahat, Y. A. (2019). Does institutional ownership affect the value relevance of accounting information? International Journal of Accounting & Information Management, 28(2), 323–342. https://doi.org/10.1108/IJAIM-03-2019-0038

- Ouda, H. A. G., & Klischewski, R. (2019). Accounting and politicians: A theory of accounting information usefulness. Journal of Public Budgeting, Accounting & Financial Management, 31(4), 496–517. https://doi.org/10.1108/JPBAFM-10-2018-0113

- Outa, E., Ozili, P. K., & Eisenberg, P. (2017). IFRS convergence and revisions: Value relevance of accounting information quality from East Africa. Journal of Accounting in Emerging Economies, 7(3), 352–368. https://doi.org/10.1108/JAEE-11-2014-0062

- Pham Hoai Huong. (2016). Vietnam’s path to converging with international accounting standards. Corporate Ownership & Control, 14(1), 644–655. https://doi.org/10.22495/cocv14i1c4art11

- Scott, W. R. (2006). Financial accounting theory. Pearson Prentice Hall.

- Tunyi, A., Ehalaiye, D., Gyapong, E., & Ntim, C. (2020). The value of discretion in Africa: Evidence from acquired intangible assets under IFRS 3. The International Journal of Accounting, 55(2), 2050008. https://doi.org/10.1142/S1094406020500080

- Xuan Vinh, V. (2015). Using Accounting Ratios in Predicting Financial Distress: An Empirical Investigation in the Vietnam Stock Market. Journal of Economics and Development, 17(1), 41–49. https://doi.org/10.33301/2015.17.01.03

- Zhaoyang, G. (2007). Across-sample incomparability of R2s and additional evidence on value relevance changes over time. Journal of Business Finance & Accounting, 34(7–8), 1073–1098. https://doi.org/10.1111/j.1468-5957.2007.02044.x