Abstract

Globally, taxes is a crucial source of income for various governments. However, in spite of the numerous importance of taxes for the socioeconomic growth of developed and developing countries, Jordan as a developing country faces challenges of tax evasion. It is pivotal in this regard to reduce tax evasion among Small and Medium Sized Enterprises (SMEs). This study aimed to examine the relation between tax transparency and sales tax evasion among Jordanian SMEs considering the role of moral obligation as the moderating factor between the endogenous and exogenous variables. Using a quantitative approach, this study surveyed 400 SMEs owners/managers. Only 45% of these surveys were valid for further analysis. For hypothesis testing and data analysis, the partial least squares structural equational modelling (PLS-SEM) technique was used. The results revealed that tax transparency had negative and significant influence on sales tax evasion. This study also provides evidence that the model’s ability to explain tax evasion and the influence of tax transparency on sales tax evasion are both greatly strengthened by the integration of moderating role of moral obligation. This study contributes to the existing body of knowledge on this subject and can help scholars and practitioners investigate the effects of tax transparency and moral obligation on sales tax evasion among SMEs. Hence, tax authorities, and policymakers should incorporate these factors to formulate effective strategies to combat tax evasion in Jordan, which could lead to an overall improvement in the country’s revenue collection.

1. Introduction

The study seeks to unravel the influence of tax transparency on sales tax evasion among Jordanian SMEs identifying the moderating role of moral obligation. The research is grounded theoretically in Social Psychological Theories, implying that tax transparency and moral obligation impact tax behaviour. According to literature, moral obligation (e.g., Alleyne & Harris, Citation2017; Braithwaite et al., Citation2010; Culiberg, Citation2018; Owusu, Bekoe, Anokye, & Anyetei, Citation2019) has a negative and significant effect on tax evasion. Previous studies have yielded conflicting findings when studying the connection between tax openness and tax evasion. According to certain studies, there is a link between tax evasion and transparency, which suggests that increased transparency can reduce tax evasion. Other research, however, have discovered either no association or even a favourable relationship between tax evasion and tax transparency. In order to understand the relationship between tax transparency and tax evasion, it is crucial to take into account the potential moderating influence of moral obligation (Baron & Kenny, Citation1986). Policymakers and tax authorities can better understand the elements that drive tax compliance behaviour and devise more effective tax policies and enforcement techniques to promote tax compliance and prevent tax evasion by considering the effects of moral obligation.

Siahaan (Citation2013) defined tax transparency as a characteristic of governments subject to full disclosure of information regarding law and rules, strategies, procedures, and acts. In general, transparency is an intentional attempt to make available all legally releasable negative or positive information in an accurate, balanced, timely, and unequivocal manner to enhance the public’s reasoning ability and hold organisations accountable for their actions, policies and practices (Rawlins, Citation2008). Enofe et al. (Citation2019) indicated that transparency comprises accessibility to and the clarification of official information available to the public for decision-making, making people more aware of government actions. This puts them closer to the government and creates a comprehensive understanding of government policy. Nowadays, taxpayers demand more tax transparency information. They also want the government to be more transparent about their taxes; transparency is commonly described as the free flow of information (Holzner & Holzner, Citation2006; Piotrowski, Citation2008).

Better transparency often translates into dramatically increased economic development. The correlation between more openness in public procurement efficiency and accelerated economic growth is based on three causal channels: increased competition, increased foreign direct investment, and decreased corruption (Kiow et al., Citation2017). Regarding taxation, transparency is critical from the first day of implementing a tax system in the policy arena to the last day of its economic effect. Information importance depends on the taxpayer’s needs and not just what the tax authority provides. Tax transparency is a mutual responsibility of the tax authority and the taxpayer. It involves a transparent, participatory government mechanism and simple and tractable tax rules. The increased use by taxpayers of voluntary disclosure programmes is also linked to the increased tax transparency worldwide and the deterrent effect of greater transparency and information exchange (Hildreth, Citation2005).

In regard to moral obligation, it can be understood as a sense of duty or responsibility to behave in ways that align with commonly accepted ethical principles or societal norms, while it is true that internal constraints can influence a person’s moral obligations, that is not often the only factor at work (Sabucedo et al., Citation2018). Milesi and Alberici (Citation2018) stated that an individual’s moral obligation should be grounded in their own personal values and beliefs, and should motivate them to act in accordance with their conscience, even if doing so comes at a cost or is unlikely to succeed. The importance of personal responsibility and autonomy in ethical decision-making, as individuals are seen as being responsible for determining their own moral obligations based on their own beliefs and values. It also acknowledges that there may be situations where acting on one’s moral obligations may come at a cost, whether that be personal, financial, or social, but that individuals should still feel compelled to act in accordance with their conscience (Sabucedo et al., Citation2018). In the perspective of taxation, moral behaviour can refer to an individual’s internal motivation or desire to pay taxes in a manner that is consistent with ethical principles or societal norms. This can include a sense of duty or obligation to contribute to the common good by paying one’s fair share of taxes, as well as a desire to comply with the law and avoid penalties or legal consequences (Kondelaji et al., Citation2016). This is aligned with Young et al., (Citation2016) who characterized moral behaviour as an internal motivation to comply to moral principles and ethical values.

Moral obligation has been widely recognized as an important factor that influences tax compliance behaviour. Taxpayers who feel a strong sense of moral obligation are more likely to comply with tax regulations and pay their taxes in full, even in the absence of external enforcement measures. This is because they view paying taxes as a civic duty or moral obligation that is essential for the functioning of society. Moral obligation is a source of intrinsic motivation for taxpayers, as it stems from their own personal beliefs and values (Sadjiarto et al., Citation2020). Moreover, it can also act as a deterrent for tax evasion. When taxpayers feel a strong sense of moral obligation, they are less likely to engage in tax evasion, as they view it as a violation of their ethical principles. Overall, the perception of what is right or wrong is a crucial component of moral obligation and plays a central role in shaping tax compliance behaviour, by promoting ethical values and a sense of duty among taxpayers, policymakers and tax authorities can encourage greater tax compliance and reduce the incidence of tax evasion (Alm & Torgler, Citation2011). Taxpayers with low tax morality are less likely to pay their required taxes and are more probable to engage in tax evasion (Oberholzer, Citation2008; Torgler, Citation2006; Torgleret al., Citation2008). According to Frey and Torgler (Citation2007), the behaviour of tax officials can have a significant impact on taxpayer’s perceptions of the tax system, including their sense of moral obligation and sincerity towards paying taxes. When tax officials are respectful, considerate, and responsive to taxpayers’ needs and concerns, it can help to foster a positive relationship between taxpayers and the tax system. Hence, the study will make a significant literary contribution, since most Jordanian efforts to far have serious methodological and generalization flaws, which highlights how important this work is.

2. Background of the study

Taxation is vital to the economic growth of both developed and developing countries. In developing countries, taxes can be especially important as they provide a critical source of revenue for governments to fund public services and infrastructure that are essential for economic growth and poverty reduction, taxes can also help to promote a more equitable distribution of wealth and reduce inequality, as they can be used to finance social programs that provide a safety net for vulnerable populations (Sebele-Mpofu, Citation2020; Umar et al., Citation2019; Vincent and Ntim, Citation2021). Essentially, each government raises revenue through taxes in order to offer citizens with the social amenities they require for economic and social progress. Notwithstanding the significant benefits that taxes give for both developed and developing countries’ economic development, Jordan, as of the developing countries, confronts challenges with tax evasion (N. M. Al-Rahamneh & Z. Bidin, Citation2022). Almost all nations in the globe deal with the global problem of tax evasion. A nation’s most important source of funding for economic development is tax revenues. Tax evasion is a global issue because it affects every nation that relies on tax as a source of revenue (Androniceanu et al., Citation2019; Musimenta and Ntim, Citation2020). Despite various attempts to solve this quandary, it remains a foreboding and persistent problem. Tax evasion not only reduces a country’s revenue but also disrupts infrastructure provision, which affects a country’s social and economic well-being. As a result, taxpayers’ willingness to pay taxes is critical to ensuring a successful and sustainable influx of government funds.Tax revenue is indeed a vital source of funding for governments and plays a crucial role in financing economic development and providing public goods and services (Rashid, Citation2020). However, tax evasion can pose a significant challenge to tax authorities in their efforts to collect tax revenue from taxpayers (Siddiquee & Saleheen, Citation2021). When individuals and firms evade taxes, they are essentially reducing the amount of revenue that the government can collect, which can in turn limit the government’s ability to fund development projects, infrastructure, social welfare programs, and other essential public services (Rashid, Citation2020; Siddiquee & Saleheen, Citation2021; Wahab, et al., Citation2022). Tax evasion is viewed as a serious problem that requires attention and action from governments, policymakers, and other stakeholders. Encouraging tax compliance, improving tax enforcement mechanisms, and addressing the underlying economic and social factors that contribute to tax evasion are all important steps that can help to mitigate the negative impacts of tax evasion and ensure that governments have the resources they need to provide essential public services (N. M. Al-Rahamneh & Z. B. Bidin, Citation2022). Rashid (Citation2020) Rashid’s (Citation2020) description of tax evasion as an illegal act that violates the law and social norms to reduce one’s tax liability is a commonly accepted definition. Tax evasion involves deliberately failing to report income, claiming false deductions or credits, or engaging in other illegal activities to avoid paying taxes owed to the government (Mason et al., Citation2020). claimed that firms may be less inclined to comply with tax laws if they perceive an unfavourable impact on their government or an unfair policymaking process is consistent with the broader literature on tax compliance. Research has shown that perceptions of fairness and equity in the tax system can have a significant impact on individuals’ willingness to comply with tax laws, as well as on their attitudes towards the government and the policy-making process. Androniceanu et al. (Citation2019) found a strong relationship between tax evasion and public policies, including tax laws and regulations, enforcement mechanisms, and social welfare policies. For example, countries with high levels of income inequality, weak social safety nets, or ineffective tax enforcement mechanisms may be more susceptible to tax evasion, as individuals and firms may perceive that their tax contributions are not being used fairly or effectively. Also he stated that finding effective solutions to tackle the problem of tax evasion is indeed a highly debatable issue, as it requires a comprehensive and multifaceted approach that takes into account the diverse factors that contribute to tax evasion in different contexts. Such solutions may include improving tax laws and regulations, strengthening tax enforcement mechanisms, addressing economic and social inequalities, and promoting a culture of tax compliance and civic responsibility. It is important for policymakers to engage in ongoing dialogue and collaboration with scholars, civil society organizations, and other stakeholders to develop effective and sustainable solutions to address the problem of tax evasion.

While psychological factors such as transparency have been studied in the broader field of taxation, there is a lack of research specifically examining the relationship between transparency and tax evasion among SMEs. SMEs represent a significant portion of the economy and play a critical role in generating employment and driving economic growth. Therefore, understanding the factors that influence tax compliance among SMEs is of great importance. Furthermore, the perception of transparency may vary across different countries and regions, particularly between developed and less developed countries. Transparency may be perceived differently in less developed countries, where there may be different cultural, social, and economic factors that shape the attitudes and behaviors of SMEs towards tax compliance. The opposite can be deduced for individuals in developing countries, where most regions are still deprived of development. However, it is important to note that generalizing about the attitudes and behaviours of individuals in less developed nations can be problematic, as there is a great deal of diversity within and between these contexts. Additionally, perceptions of moral behaviour and tax compliance can be influenced by a wide range of factors, including cultural norms, religious beliefs, and historical and political contexts. As such, it is important to approach the question of moral behaviour and tax compliance in less developed nations with nuance and sensitivity to the unique cultural and societal factors. This study starts with an introduction, followed by a literature review and the elaboration of the methodology. Data analysis and results are then presented, followed by the discussion, Conclusion and implications, and Limitations and Recommendations for Further Studies.

3. Theoretical literature review

3.1. Tax transparency and tax evasion

Transparency in taxation is essential because when taxpayers lose trust in the government and its tax system, it leads to noncompliance, which in turn causes sharp practices such as fraud or tax evasion (Kiow et al., Citation2017). Thus, tax transparency is the extent to which taxpayers have ready access to any required tax information. Governments must be more transparent and open with their taxes to decrease taxpayers’ evasion behaviour. Governments can exploit information transparency as an opportunity to increase the voluntary compliance of existing taxpayers and attract new ones, a high level of tax transparency can encourage better voluntary compliance by assuring taxpayers that their tax payments achieve the desired objectives (Siahaan, Citation2013).

However, a sound tax system ensures accountability and transparency in government, which contributes to the development of the countries and drives foreign investment inflow and good trade relationships (Enofe et al., Citation2019); consequently, taxes and tax transparency are essential for a country’s sustainable development. The loss of tax revenue via tax evasion and government non-transparency are thought to adversely impact a nation’s development. One reason for revenue loss is that self-employed individuals and SMEs are more apt to evade tax due to the lack of third-party reporting (Kleven et al., Citation2016). Also, tax transparency is necessary for the sustainable growth of a nation. Nevertheless, limited tax transparency is problematic. When considering the risks associated with taxpayer privacy, all-embracing tax transparency might not benefit society. The costs of complete tax transparency might be high (Noked, Citation2018). Subsequently, more studies are required to assess if full tax transparency is optimal because little empirical research has considered the impact of tax transparency on taxation.

Siahaan (Citation2013) empirically examined the moderating role of trust in the relationship between tax transparency and voluntary tax compliance. This research indicated that the perception of transparency amongst people might increase confidence among taxpayers. Also, taxpayers need more information on what is happening in government. Therefore, increasing tax transparency can encourage greater voluntary compliance by ensuring taxpayers that their tax payments achieve the desired objectives. This study covered privately-owned organisations within service industries. It showed that the direct effect of tax transparency on voluntary taxpayer compliance was insignificant. In contrast, tax transparency has a considerable and significant indirect impact on compliance behaviour through trust., leading to reduced tax evasion. Transparency is critical in local taxation because taxpayers can lose confidence in a system. If they lose confidence, they react negatively through illegal practices like tax fraud or evasion (Lachhebet al., Citation2016). Therefore, tax transparency is a primary factor influencing tax evasion behaviour.

Kiow et al. (Citation2017 reported that direct tax transparency had an insignificant impact on voluntary tax compliance behaviours, but they found that the indirect effect of tax transparency through trust on voluntary tax compliance behaviour was significant and positive. That means a significant association exists between trust in government and government’s transparency and voluntary tax compliance behaviour, which would eventually enhance voluntary tax compliance behaviour and, conversely, discourage tax evasion. Generalising the findings to other sectors or industries could be done by further study.

Tayibet al., (Citation1999) researched local taxpayer behaviour. They found that most respondents would be more willing to pay taxes more rapidly if given financial information. This result meant that taxpayers needed a transparent tax system by the local authority. This result aligns with Siahaan (Citation2013), whose study postulated that tax transparency positively influenced tax compliance behaviour through trust in government. Conversely, Abdul–Razak and Adafula (Citation2013) revealed that there was less consideration for transparency and responsibility in government and that these negative consequences influenced the taxpayers’ compliance decision, whereby taxpayers had reservations and doubts about paying tax to the government (Dutt et al., Citation2019) stated that the empirical proof on the effectiveness of tax transparency measures was still limited and inconclusive. On the other hand, investors could expect that the influenced firms would decrease their tax evasion activities as intended by the legislation because they would face higher reputational costs.

Therefore, further research should investigate the behavioural and informational determinants of information transparency and its relation to tax evasion (Campuzano, Citation2015). Tax transparency is to what extent taxpayers have instant access to the necessary tax information. Governments need to be more accessible, transparent and open about their taxes to increase voluntary compliance for taxpayers. Governments should use the accessibility of records as an incentive to boost current taxpayers’ voluntary compliance and attract new ones.

In general, most developed nations like the United States, New Zealand, and Greece are increasingly becoming aware of the necessity of transparency and information disclosure. The United States has been a pioneer in international transparency and taxation. Aside from its economic and political importance, tax transparency is essential. Thus, it is necessary to secure legislative acceptance of the universal standards and reports and remove secrecy in state regimes (Alberto et al., Citation2016). According to Erlend et al. (Citation2015), under Greek legislation, a declaration of the proposed budget is followed by lists of tax evaders by the Ministry of Finance from the preceding year. The Commissioner of Inland Revenue in New Zealand annually issues a Tax Evaders Gazette that lists those taxpayers convicted for evading their tax liabilities or had a punitive tax levied. In Jordan, Alasfour (Citation2019) argued that governments must develop a high trust-based culture and strategies to produce normative ethical values to mitigate tax evasion and increase voluntary compliance. One way to achieve this is by enforcing the state’s transparency.

3.2. Moral obligation and tax evasion

According to Ozili (Citation2020), there are more than two perspectives on the ethics and morality of tax evasion. The first perspective argues that tax evasion is immoral and therefore no taxpayer should engage in it. This perspective is based on the moral principle that individuals have an obligation to contribute to society by paying their fair share of taxes. From this perspective, tax evasion is seen as a breach of this obligation and an act that undermines the stability of society. The second perspective argues that tax evasion is not necessarily immoral, and that taxpayers have a right to keep as much of their income as possible. This perspective is often associated with libertarian or individualistic views of society, which prioritize individual freedom and autonomy over social responsibility. From this perspective, taxes are seen as a form of coercion by the government, and tax evasion is seen as a legitimate way of resisting this coercion. Ultimately, the ethical dilemma of tax evasion is a complex and multifaceted issue that requires careful consideration of a variety of factors (McGee, Aljaaidi, & Musaibah, Citation2012). Taxpayers’ moral obligation determines the degree to which they engage in tax evasion. It has the potential to affect taxpayers’ willingness to engage in tax evasion (Nangih & Dick, Citation2018). Taxes imposed by the appropriate authority is acknowledged to be ethical, which is consistent with the moral development theory. As stated by Ajzen (Citation2002) in Rahayu and Day (Citation2015), according to the principle of life, ethics, guilt is a moral obligation that every individual has while carrying out something. The moral obligation carried arises from inside ourselves in the form of each person’s conscience and is not imposed by third parties. Taxpayers’ ethical obligations are part of their responsibility to state funding by consistently making tax payments. If a taxpayer feels responsible for state commitments, he will follow through on his tax obligations (Rahayu & Day, Citation2015). According to Mustikasari (Citation2007), indicators of moral obligations include: violations of ethics, feelings of remorse, and life values. Additional indicators highlighted by Putra and Jati (Citation2017) include: duty for financing state upkeep is a shared burden, feeling concerned if not carrying out tax duties, and a sense of guilt in oneself if engaging in tax evasion.

Moral development, according to Kohlberg (Citation1969) who extended Piaget’s theory, is a continual lifetime mechanism. In summary, Kohlberg’s theory proposed that individuals progress via phases of moral reasoning and decision-making., and that achieving higher stages of moral development leads to a greater ability to internalize moral values and principles and to act in accordance with a sense of moral obligation. In the context of the moral development theory, individuals who have achieved higher stages of moral development are more likely to act in accordance with universal principles of justice and fairness, even if it requires them to sacrifice their own self-interest for the benefit of others. This can manifest in the context of taxation as a willingness to pay taxes even if it means a personal financial sacrifice, in order to contribute to the common good. Alm and Torgler (Citation2011) argued in the context of taxation that moral obligation for tax law is founded on ethics, i.e., what society considers as just or bad. In the context of tax evasion, the moral development theory suggests that taxpayers who feel a strong moral commitment to help others may forego their own gains. It also points out the effect of moral obligation on the taxpayer’s relations as the primary factor influencing evasion (Kohlberg & Hersh, Citation1977). Consequently, investigating the role of moral obligation as a moderator in the relations between tax transparency and sales tax evasion behaviour is essential in understanding the factors that drive tax compliance behaviour. By identifying the factors that influence taxpayers’ compliance behaviour, policymakers and tax authorities can design more effective tax policies and enforcement strategies to promote tax compliance and reduce tax evasion. Previous studies have demonstrated that moral obligation has a negative and significant impact on tax evasion (Alleyne & Harris, Citation2017; Braithwaite et al., Citation2010; Culiberg, Citation2018; Owusu, Bekoe, Anokye, & Anyetei, Citation2019). Previous research examining the relationship between tax transparency and tax evasion is complex, and previous studies have produced mixed results. Some studies have found a negative relationship between tax transparency and tax evasion, indicating that greater transparency can lead to lower levels of tax evasion. However, other studies have found either no relationship or even a positive relationship between tax transparency and tax evasion. Therefore, it is important to consider the potential moderating effect of moral obligation on the relationship between tax transparency and tax evasion (Baron & Kenny, Citation1986). By taking into account the influence of moral obligation, policymakers and tax authorities can better understand the factors that drive tax compliance behaviour and design more effective tax policies and enforcement strategies to promote tax compliance and reduce tax evasion.

4. Empirical literature review and hypotheses development

In taxation, transparency is essential. When taxpayers lose trust in a tax system and government, this lost trust may cause non-compliance, leading to fraud and tax evasion (Kiow et al., Citation2017). Few studies have examined tax transparency and tax evasion, and their results have been mixed. Some found that tax transparency negatively correlates with tax evasion, and tax transparency influenced taxpayers ‘evasion behaviour. The greater the tax transparency, the higher the deterrence of tax evasion (Kiow, Salleh, & Kassim, Citation2017; Lachheb et al., Citation2016; Noked, Citation2018; Siahaan, Citation2013). Conversely, Abdul–Razak and Adafula (Citation2013) revealed less consideration for transparency and responsibility in government. These adverse effects influenced individual tax compliance decisions because taxpayers had doubts about paying taxes to the government. Grounded on these arguments and using socio-psychological theories positing that tax transparency would have a negative and direct effect on sales tax evasion behaviour.

In summary, tax transparency is an essential factor in tax evasion behaviour. Nevertheless, limited studies have examined the direct effect of tax transparency on tax evasion, especially in the sales tax context of Arab and Middle Eastern nations, particularly in Jordan. Limited researches concentrated on the association between tax transparency and sales tax evasion among Jordanian SMEs to the best available knowledge. Additional study is required to determine the association between tax transparency and sales tax evasion among SMEs in Middle Eastern and Arab nations, especially Jordan. Thus, tax transparency is a significant contribution of the current study as a determinant factor of sales tax evasion at the business level. Utilising socio-psychological theories and the above discussion, this hypothesis is posited:

H1:

There is a negative relationship between tax transparency and sales tax evasion behaviour of SMEs in Jordan.

In addition, it can be highlighted that socio-psychological theories are increasingly using moral obligation to assess the level of tax evasion. This study demonstrates that the negative relationship between transparency and tax evasion behaviour may be moderated by moral obligation. Due to the high levels of tax evasion that the tax system is notorious for (Alasfour, Citation2019). The literature also highlighted the need for new methods to fully visualize the sophisticated behaviour of tax evasion and the integration of social norms (Torgler, Schaffner, & Macintyre, Citation2007). According to Baron and Kenny (Citation1986), a moderating variable is introduced when two or more variables have an inconsistent relationship. When taxpayers have a high sense of moral obligation, tax evasion is anticipated to be negligible. This implies that the negative relationship between tax transparency and tax evasion behaviour will be strengthened in the presence of the moderating influence of moral obligation. Based on prior considerations of the moderating impact of the moral obligation, it’s conceivable that the initial association between transparency and tax evasion will be strengthened. Based on the previous explanation of moral obligation’s moderating influence and socio psychology theories, this study hypothesized that moral obligation strengthen the negative relationship between tax transparency and tax evasion. Thus, this study proposes incorporating moral obligation as a moderator to strengthen the relationship between tax transparency and sales tax evasion. Given the above discussion and using this explanation of moral obligation’s potential moderating effect, the following hypothesis is posited:

H2:

Moral obligation strengthens the negative relationship between tax transparency and sales tax evasion behaviour of SMEs in Jordan.

5. Theoretical framework

Theoretical framework demonstrated in Figure has been developed based on Social Psychological Theories, implying that tax transparency and moral obligation impact tax behaviour. Following the literature discussed and the above hypothesizes developed, Figure shows the theoretical framework which depicts the direct as well as indirect relationships of the constructs under consideration, the dependent variable is tax transparency, while the independent variable is tax evasion, at the same vain moral obligation serve as moderating variable between tax transparency and tax evasion. As a result, this study suggests the following theoretical framework, as illustrated in Figure , based on the prior discussions.

Figure 1. Theoretical Framework.

6. Research design

In order to assess the impact of tax transparency and moral obligation on tax evasion in Jordanian SMEs, this study employs a quantitative research design. Quantitative design methods are also the most appropriate and logical choice when studying the relationships between variables and testing hypotheses (e.g., Creswell, Citation2014; Naser, & Hamzah, Citation2018, Citation2022; Sekaran, Citation2003). Quantitative research typically aims to test hypotheses or provide answers to specific research questions (Zikmundet al., Citation2013). Studies of tax behaviour generally employ quantitative approaches, both in developing and developed nations (Fjeldstad & Semboja, Citation2001; Saad, Citation2011; Verboon & van Dijke, Citation2011). Creswell (Citation2013) confirmed further that a quantitative strategy was suitable for complex research including a variety of variables. To examine the factors in consideration, predetermined instruments and closed-ended questions can be utilized, enabling statistical methods to be applied to statistics and data (Creswell & Creswell, Citation2017; Trochim & Donnelly, Citation2007).

The data were collected from SMEs of Jordan. Using a self-administered survey approach. A simple random sample technique was used in this study. Because the current study’s unit of analysis is an organizational level, the major respondents comprised owners/managers whose viewpoints are crucial in understanding the factors driving sales tax evasion behaviour and because they represent the organization. In order to determine the reliability of the questionnaire, a pilot study with 30 individuals who were not involved in the study was conducted to validate it. The results of this pilot study gave researchers the opportunity to make the necessary adjustments to the study questions to ensure their readability and clarity. To ensure understandable responses and the major goals of the study, the questionnaire’s questions were written in Arabic.

The population of this study comprises 166,154 SMEs (services, trade, and manufacturing) operating in Jordan. For the minimum sample size determination, Per Krejcie and Morgan (Citation1970) well-known Morgan’s table is used, if a population is between 75,000 and 1,000,000, a sample between 382 and 384 is appropriate. Thus, accordingly, the sample size in this study should be 382. However, to compensate for potential non-response, Israel (Citation1992) recommended expanding the sample size by at least 30%. Hence, the current study’s sample size was boosted and distributed to 400 SMEs owners/managers to overcome a potentially low non-response rate. Hence, a total of 180 questionnaires were returned and usable.

6.1. Measures

A multi-item scale is used to measure the theoretical constructs in the conceptual framework. The response was measured using a five-point Likert scale (1 “Strongly Disagree” to 5 “Strongly Agree”).

6.1.1. Tax transparency

Tax transparency operationally defined as taxpayers’ perceptions of tax authority characteristic of being open in the clear official information available to the taxpayers for decision-making, rules, and actions. This definition aligns with Siahaan (Citation2013), who defined tax transparency as a feature of government being available to evident disclosure of information, rules, strategies, procedures. The tax transparency is measured with four items using adapted from Rawlins (Citation2008).

6.1.2. Moral obligation

The present study operationally defined moral obligation as internal responsibility in which SMEs taxpayers follow their sense of “what is right and what is wrong” to evade, comply, cheat or not in paying sales tax. This definition aligns with Beck and Ajzen (Citation1991) and Bobek and Hatfield (Citation2003), who defined moral obligation as “an individual’s internalised ethical rules, which reflect their personal beliefs about right and wrong.” Four items measured moral obligation. One item was adapted from Bobek and Hatfield (Citation2003), and three items were adapted from Beck and Ajzen (Citation1991).

6.1.3. Tax evasion

Tax evasion is defined as illegal and intentional actions under-reporting sales tax, failing to file tax returns correctly, concealing, misrepresenting, and deception in tax invoice details to pay very little sales tax. This definition aligns with Koumbiadis et al. (Citation2014), who defined tax evasion as “illegal and intentional acts in which organisations and individuals engaged in reducing their legal tax liabilities by under-reporting sales income and failing to file tax returns properly at the correct time.” Along the same lines, Abdul-Jabbar and Pope (Citation2008) emphasised that tax evasion can be described as fraud, mistakes, income reduction, or misreporting. The present research measured sales tax evasion by adapting 14 items from Gilligan and Richardson (Citation2005) to measure SMEs tax evasion, which originated from Roberts’ study (Citation1994).

7. Empirical results and discussion

The current study’s data was analyzed using Smart PLS 3.3.9 and the Partial Least Squares -Structural Equation Modelling (PLS-SEM) analysis technique. PLS-SEM is a statistical technique that many researchers are using to analyze empirical data in a variety of disciplines, including tax behavior (Farouk et al., Citation2018). PLS-SEM modeling is appropriate for analyzing complex models containing a large number of items, variables, and relationships (Chin, Citation2010). PLS-SEM was utilized in this study to evaluate the measurement and structural models. As recommended Hair et al., (Citation2021), PLS-SEM analytical technique includes two stages. The assessment of the measurement model includes assessing indicator reliability, internal consistency reliability, convergent validity, and discriminant validity. Assessment of the structural model includes testing path coefficients significance, calculating R2 and f2, and determining the model’s predictive relevance using Q2.

7.1. Assessment of measurement model

According to Hair et al. (Citation2017), the construct’s reliability and validity in the measurement model must first be assessed. The hierarchical component modeling technique was employed in this study since the constructs are higher-order and the model is Reflective-Reflective. The repetitive-indicator approach was used to evaluate the model (Hair et al. Citation2017). Cronbach’s Alpha and composite reliability were used to measure indicator reliability, and convergent-validity and discriminant validity were used to test concept validity. Results indicate that the composite reliability (CR) values of moral obligation, tax transparency, and tax evasion are 0.960, 0.785, and 0.972, as stated in Table , and the value of Cronbach’s Alpha is 0.946 (moral obligation), 0.766 (tax transparency), and 0.965 (tax evasion), respectively. The AVE threshold value should be greater than 0.5. The convergent validity values in the current assessment are 0.859 (moral obligation), 0.571 (tax transparency), and 0.690 (tax evasion), as shown in Table .

Table 1. Convergent validity for reflective measurement model of the constructs

The Fornell and Larcker (Citation1981) criterion is one of the indicators used to assess the model’s discriminant validity, according to (Hair et al., Citation2017). Table shows that for all reflective constructions, the square root value of AVE (diagonal) is greater than the correlations (off-diagonal). All of the values indicate that there is no issue with multi-collinearity among the constructs. Furthermore, to be aligned with the recent reporting of the PLS-SEM results (Hair et al., Citation2017)., the new Heterotrait—Monotrait ratio (HTMT), introduced by Henseler, Ringle, and Sarstedt (Citation2015), was also used. The ratio of “between-trait correlations” to “within-trait correlations” is described as HTMT (Hair et al., Citation2017). The HTMT criterion’s threshold value is 0.9, which means that two of the concept measurements should not correlate above 0.9 to establish its discriminant validity. As shown in Table , all of the respective values were confirmed to be below the threshold limits.

Table 2. Fornell and Larcker’s (Citation1981) criterion

Table 3. HTMT ratio of the constructs (N = 180)

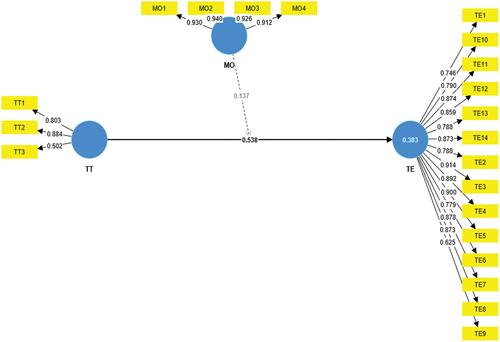

The measurement model constructed utilizing Smart PLS is shown in Figure .

Figure 2. The measurement model.

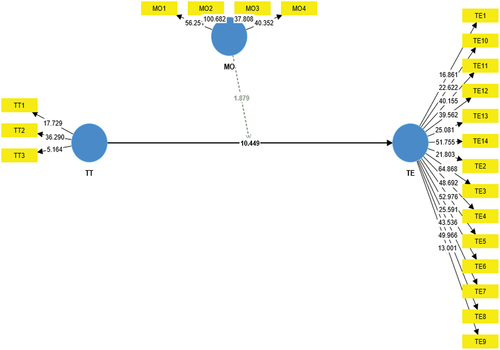

After the measuring model’s reliability, convergent validity, and discriminant validity were established, The hypotheses were verified in Step 2 by analyzing the structural equation model. Figure depicts the path coefficient estimates and R-square values, while Figure depicts the path coefficient t-value estimates.

Figure 3. Structural Model for Direct Effect (p- values).

7.2. Assessment of the structural model

Once the measurement model assessment criteria are met, we must evaluate the following model, known as the structural model. The hypothesis testing (path-coefficient), effect size (2), and coefficient of determination are all evaluated in the structural model evaluation (R2 value). In Smart-PLS, 1000 sample sizes were boot-strapped with a 5% threshold of significance and a one-tailed test. We evaluated the T-statistics and p-value either accepting or rejecting the hypothesis during hypothesis testing. Cohen (Citation1988) classified f2 into three groups in the structural model: 0.02 to 0.14 denote a small effect, 0.15 to 0.34 denote a medium effect, and 0.35 and above denote a large effect. According to Table , the effect size (f2) of the two endogenous variables—tax transparency and moral obligation—is 0.155 and 0.095, indicating a medium and small effect, respectively. As shown in Table and Figure , the first hypothesis postulated a negative relationship between tax transparency and sales tax evasion behaviour of SMEs in Jordan, The findings show a significant negative relationship with (β = 0. 0.563, t = 10.281, p < 0.01, P = 0.000**), H1 was accepted. The second hypothesis proposed that moral obligation strengthens the negative relationship between tax transparency and sales tax evasion behaviour of SMEs in Jordan.The findings illustrated in Table show (β= −0.205, t = 2.714, p < 0.05, p = 0.003), which presumes that H2 was accepted. As presented in Table , the model’s coefficient of determination (R2 -value) is 0.410, indicating a medium effect. This demonstrates that the endogenous factors, tax transparency and moral obligation, account for 41% of the variance in the endogenous variable, tax evasion. A cross-validated redundancy measure (Q2) value greater than zero, as recommended by Hair et al. (Citation2017) and Henseler, Haenlein, and Reinartz (2009), demonstrates the model’s predictive relevance. As shown in Table , the results of this test demonstrated that the study’s model has predictive relevance value for the endogenous variable.

Table 4. Effect sizes, f2

Table 5. Path coefficients of the exogenous constructs predicting tax evasion

Table 6. Results of the moderating effect hypothesis testing

Table 7. Coefficient of determination, R2

Table 8. Predictive relevance (Q2)

8. Discussion

It is clear that the global community now faces a challenge in combating tax evasion. Therefore, it is crucial to have a clear grasp of the elements that influence sales tax avoidance. One aspect that has been scientifically proven to be a determinant of tax evasion is tax transparency. Tax transparency seems to draw attention because of its characteristics and the frequency with which rules, tax laws, regulations, and requirements change, and it also seems to have theoretical and empirical significance. As a result, there is a strong demand for ongoing research in this area because it offers both tax administrators and academics challenging research opportunities. In essence, this is based on earlier research on the factors that influence tax evasion, which are primarily obtained from a non-economic perspective. It then suggests future research to incorporate political and tax transparency aspects into tax evasion models. Additionally, the research on tax compliance showed that industrialized nations were primarily the focus of tax evasion literature, which included both analytical and empirical investigations.

The integration of Social Psychological Theories establishes and supports the suggested conceptual framework of this research, indicating that tax transparency on sales tax evasion. The moderating impact of moral obligation on this relationship among Jordanian SMEs is investigated in the current study. The model, which is based on social psychological theories, contends that tax transparency has an impact on tax evasion behavior. The Social Influence Theory focuses on how other people affect a person’s thoughts, feelings, and behavior. An individual is influenced by their environment, according to Bandura’s Social Learning Theory, which is connected to the theory of social influence. The way in which the impact of others on a person’s beliefs, behavior, and feelings is defined as social influence. As a result, it might be advantageous to combine results by looking into moral obligation as a moderating factor. As a result, this study examined the conceptual framework that was suggested based on earlier talks, as shown in Figure .

To be more specific, this study set out to investigate the relation between tax transparency and sales tax evasion behaviour among Jordanian SMEs. Additionally, the study investigated the moderating effect of moral obligation on the relationship between tax transparency and sales tax evasion behaviour. The findings also revealed that tax transparency significantly influences sales tax evasion in line with this expectation. Thus, Hypothesis (H1) was supported. This findings regarding the linkage between tax transparency and sales tax evasion among SMEs in Jordan support the theoretical proposition. It also proves that tax transparency plays a considerable part in sales tax evasion. Tax transparency was determined to negatively and significantly affect sales tax evasion among Jordanian SMEs. Congruent with the predictions of the socio-psychological approach and theory of planned behaviour (Ajzen, Citation1991), the findings suggest that a higher level of transparency tends to have a higher deterrence level for sales tax evasion. This finding is consistent with previous studies Kiow et al., (Citation2017), Lachheb et al., (Citation2016), Noked (Citation2018), and Siahaan (Citation2013), these reported that high transparency negatively impacts the tax evasion level. This implies that the tax transparency in tax authorities’ disclosure of information, rules, strategies, procedures caused a decrease in sales tax evasion. This consequently reduced the taxpayer’s intention to engage in evasion behaviour. A direct impact of tax transparency would give evidence that the effect of tax transparency is implicit. The findings indicate that increasing tax transparency will decrease sales tax evasion among SMEs owners/managers who trust tax authorities and believe that paying sales taxes is transparent.

Enofe et al. (Citation2019) stated that transparency was the accessibility and clarification of official information available to the public for decision-making, making people more aware and having greater awareness of government actions. This puts taxpayers closer to the government and creates a comprehensive understanding of government policy. Aligned with the research objective, hypothesis H2 postulated that moral obligation strengthened the negative association between tax transparency and SMEs sales tax evasion behaviour in Jordan.

The moderating effect findings pointed out that moral obligation strengthened the negative relationship between tax transparency and sales tax evasion behaviour. The results support the interaction effect of the moral obligation on the association between tax transparency and sales tax evasion. So, arguably, moral obligation moderates the relationship between tax transparency and sales tax evasion. Reasonably, tax transparency substantially impacts taxpayers’ behaviour, when interacted with moral obligation, as the internal value of taxpayers. The original effect of tax transparency on tax evasion was significant. Still, when interacting with moral obligation, the influence becomes also significant because taxpayers’ internal values strengthened the effect of tax transparency as a determinant factor. This evidence of the moral obligation influence on SMEs’ owners/managers, and their perception of tax transparency has effect on tax evasion. Thus, SMEs taxpayers may consider moral obligation when the transparency level is higher.

9. Summary and conclusion

Tax evasion continues to be a complex and global challenge for policymakers, researchers, and tax authorities. While many strategies have been created and implemented, tax evasion remains a problem. Addressing different aspects of evasion might lead to optimal compliance. The current study offers empirical evidence by integrating psychological, and social determinants of tax evasion. The study provides additional insights into the relationship between tax evasion and its numerous determinants. The findings offer an understanding so that income and sales tax department (ISTD) can improve or design new strategies to obtain optimal voluntary compliance of SMEs sales taxpayers. Sales tax evasion in Jordan is becoming more prevalent. It reduces the ability of Jordan’s government to strengthen the national economy, boost self-reliance, and gain fiscal sustainability. Consequently, sales tax evasion is a crucial issue for the government. The government must consider factors that could impact sales tax evasion to mitigate sales tax evasion.

This study expanded the knowledge regarding sales tax evasion and its determinants among Jordanian SMEs, for whom sales tax evasion remains high. The current study’s findings confirmed a negative and significant relationship of tax transparency on sales tax evasion. Furthermore, the current study explored the moderating effect of moral obligation on the association between tax transparency with sale tax evasion. The results found that the moderating effect of moral obligation was positive and significant of tax transparency on sales tax evasion. Hopefully, this study will motivate the further development of theory and future research in this field. To sum up, it really is hoped that the problem of sales tax evasion would be completely highlighted at the government level and, at a later time, be taken into consideration for any taxation policy decisions in Jordan, particularly those concerning the SMEs sectors.

Jordanian governments continue to prioritise improving their ability to generate revenue from domestic sources. This is because of a dramatic decrease in its revenues and a significant reduction in foreign aid granted to Jordan. Therefore, the current research is vital to the tax authorities because the study reveals inherent tax evasion issues among Jordanian SMEs taxpayers who constitute a significant part of Jordan’s sales taxpayers. Controlling tax evasion and ensuring compliance will certainly aid Jordan’s government in decreasing its budget deficit and achieving fiscal sustainability. Tax evasion is a complicated behaviour that necessitates the study of various factors, extending from enforcement to voluntary and organisational perspectives. The present study’s model was developed by integrating these factors to build an extended model that can evaluate tax evasion behaviour in Jordan.

Another contribution was bridging the literature gap about sales tax evasion determinants, especially by SMEs owners/managers, and proposing a research framework investigating determinants of sales tax evasion in SMEs. This research’s model included social psychological and economic factors drawn from Fischer’s model and prior literature. Thus, this research improved the understanding of SMEs’ sales tax evasion determinants. Also, this proposed model is expected to provide helpful input to tax authorities in combating the tax evasion problems, particularly in the context of Jordan. Still, it can also be applied to other Middle Eastern countries. Consequently, Jordan’s governments need to raise awareness among SMEs owners and managers about the significance of paying sales taxes and the benefits of paying taxes. Tax transparency was found to significantly and negatively impact sales tax evasion among Jordanian SMEs. These findings imply a negative association between tax transparency and sales tax evasion. Tax transparency remains a significant factor in determining sales tax evasion behaviour. The significant role of tax transparency in tax evasion suggests that the government must understand taxpayers’ motives in-depth to assure low tax evasion. Also, it needs to inspire and formulate strategies and a high-trust-based culture to instil a normative ethical value to increase voluntary compliance by strengthening perceptions of the accountability and transparency of tax authorities in the state. The current research contributes to the accounting and taxation literature, adding to accounting literature on sales tax evasion and its determinants in developing nations like Jordan. The literature review illustrated that, even though tax compliance studies have received much attention, limited research has been done on indirect tax evasion.

10. Limitations and recommendations for further studies

This section introduces summary of findings indicated to all of contributions, implications, limitations and avenues for future research. Hence, it is indicated that even though the present study offers major contributions including theoretical and practical contributions, there are a few limitations which have to be considered. These limitations provide opportunities for future studies. Firstly, the data were collected from a single respondent in an organization utilizing a self-administered survey technique, which may have skewed our results. As a result, one goal for further studies ought to be to collect data from a numerous informant within an organization. Like some other compliance studies, self-reported surveys may not accurately reflect respondents’ actual behaviour (Van Dijke & Verboon, Citation2010). This limitation particularly happens when information is sought for embarrassing tax-sensitive issues. An additional limitation is that despite the repeated follow-ups after distributing the survey questionnaire, the present study had a response rate of 45%. However, this is acceptable for owners/managers of SMEs in Jordan. The respondents’ unwillingness to cooperate caused data collection limitations. This can be attributed to the sensitive nature of taxation issues, predominately tax evasion and a lack of concern in completing the questionnaire. The respondents may not give truthful responses. A lack of time to complete the questionnaire may have inhibited potential respondents. This study was limited to the quantitative research method utilising questionnaires, which did not allow the respondents to express their perspectives more fully. Although the coefficient of determination (R2 value) explained 41% of the variance in the endogenous variable, namely tax evasion, some other variables or factors may contribute to the remaining variance in the endogenous variable.

This study’s limitations and findings suggest that tax evasion behaviour might require future studies. The proposed model in the current study can offer reasonable explanations of taxpayers’ evasion in Jordan, the findings show. Thus, the model could be replicated to study other indirect taxes like the customs tax. Future research should consider additional factors to extend the research model. Consequently, additional factors may be relevant to understanding tax evasion behaviour in Jordan, but they were examined in this study. For instance, the factors of external audit, attitude and perceptions, tax service quality, and religion may influence the behaviour of Jordanian SMEs taxpayers but have not been studied so far. Thus, future research should enlarge the study’s model to integrate these factors. These variables might play increasingly crucial roles in evasion behaviour. Future research could also use a mixed methodology to understand complex evasion behaviour. Tax evasion among SMEs is a worldwide problem. Because SMEs account for the majority of businesses, tax evasion in SMEs has received a lot of attention. Many psychological components of tax evasion have previously been researched, but no conclusive conclusions have been discovered. Tax evasion persists despite the development and deployment of several strategies. To achieve maximum compliance, various factors of evasion could be addressed. This study incorporates socio-psychological factors of sales tax evasion to give empirical evidence as well as a novel perspective on the subject of tax evasion that may contribute in a better understanding of the issue. It also sheds further light on the interaction between SME owners-managers, tax-paying factors, and tax evasion. Moreover, to offer in-depth insights, the current study suggests adopting mixed techniques, combining quantitative and qualitative methods, including case studies interviews. A mixed methodology would enable future researchers to solicit potentially embarrassing, incriminating, or sensitive information. Finally, the current study’s findings might be used to complement knowledge to understand indirect tax evasion from a broader perspective.

Disclosure statement

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

References

- Abdul–Razak, A., & Adafula, C. J. (2013). Evaluating taxpayers’ attitude and its influence on tax compliance decisions in Tamale, Ghana. Journal of Accounting and Taxation, 5(3), 48–19. https://doi.org/10.5897/JAT2013.0120

- Abdul-Jabbar, H., & Pope, J. (2008). Exploring the relationship between tax compliance costs and compliance issues in Malaysia. Journal of Applied Law and Policy, (2008), 1–20.

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. https://doi.org/10.1016/0749-5978(91)90020-T

- Ajzen, I. (2002). Perceived behavioral control, self‐efficacy, locus of control, and the theory of planned behavior 1. Journal of Applied Social Psychology, 32(4), 665–683. https://doi.org/10.1111/j.1559-1816.2002.tb00236.x

- Alasfour, F. (2019). Costs of distrust: The virtuous cycle of tax compliance in Jordan. Journal of Business Ethics, 155(1), 243–258. https://doi.org/10.1007/s10551-017-3473-y

- Alberto, B., Jerónimo, R., & Fernando, V. (2016). A brief history of taxtransparency. Inter-American Development Bank, 1–21.

- Alleyne, P., & Harris, T. (2017). Antecedents of taxpayers’ intentions to engage in tax evasion: Evidence from Barbados. Journal of Financial Reporting and Accounting, 15(1), 2–21. https://doi.org/10.1108/JFRA-12-2015-0107

- Alm, J., & Torgler, B. (2011). Do ethics matter? Tax compliance and morality. Journal of Business Ethics, 101(4), 635–651. https://doi.org/10.1007/s10551-011-0761-9

- Al-Rahamneh, N. M., & Bidin, Z. (2022). The effect of tax fairness, peer influence, and moral obligation on sales tax evasion among Jordanian SMEs. Journal of Risk and Financial Management, 15(9), 407. https://doi.org/10.3390/jrfm15090407

- Al-Rahamneh, N. M., & Bidin, Z. B. (2022). The moderating role of moral obligation on the relationship between non-economic factors and tax evasion among SMEs: A conceptual framework. Journal of Accounting and Finance, 10(2), 425–432. https://doi.org/10.13189/ujaf.2022.100206

- Androniceanu, A., Gherghina, R., & Ciobănaşu, M. (2019). The interdependence between fiscal public policies and tax evasion. Administratie Si Management Public, 32, 32–41. https://doi.org/10.24818/amp/2019.32-03

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality & Social Psychology, 51(6), 1173. https://doi.org/10.1037/0022-3514.51.6.1173

- Beck, L., & Ajzen, I. (1991). Predicting dishonest actions using the theory of planned behavior. Journal of Research in Personality, 25(3), 285–301. https://doi.org/10.1016/0092-6566(91)90021-H

- Bobek, D. D., & Hatfield, R. C. (2003). An investigation of the theory of planned behavior and the role of moral obligation in tax compliance. Behavioral Research in Accounting, 15(1), 13–38. https://doi.org/10.2308/bria.2003.15.1.13

- Braithwaite, V., Reinhart, M., & Smart, M. (2010). 11 Tax non-compliance among the under-30s. Developing Alternative Frameworks for Explaining Tax Compliance, 59, 217.

- Campuzano, J. (2015). Tax transparency and willingness to pay. 4th Global Conference on Transparency Research, Lugano, Switzerland (pp. 1–33).

- Chin, W. W. (2010). How to write up and report PLS analyses. In Handbook of partial least squares (pp. 655–690). Springer. https://doi.org/10.1007/978-3-540-32827-8_29

- Cohen, M. A. (1988). Some new evidence on the seriousness of crime. Criminology, 26(2), 343–353. https://doi.org/10.1111/j.1745-9125.1988.tb00845.x

- Creswell, J. W. (2013). Research design: Qualitative approach, quantitative and mixed (4 ed.). United States of America.

- Creswell, J. W. (2014). A concise introduction to mixed methods research. SAGE publications.

- Creswell, J. W., & Creswell, J. D. (2017). Research design: Qualitative, quantitative, and mixed methods approaches. Sage publications.

- Culiberg, B. (2018). How can governments tackle consumption tax evasion? Shedding light on the antecedents of consumer attitudes and intentions. Journal of Nonprofit & Public Sector Marketing, 30(4), 367–386. https://doi.org/10.1080/10495142.2018.1452824

- Dutt, V. K., Ludwig, C. A., Nicolay, K., Vay, H., & Voget, J. (2019). Increasing tax transparency: Investor reactions to the country-by-country reporting requirement for EU financial institutions. International Tax and Public Finance, 26(6), 1259–1290. https://link.springer.com/article/10.1007/s10797-019-09575-4

- Enofe, A., Embele, K., & Obazee, E. P. (2019). Tax audit, investigation, and tax evasion. Journal of Accounting and Financial Management, 5(4), 47–66.

- Erlend, B. E., Slemrod, J., & Thoresen, T. O. (2015). Taxes on the internet: Deterrence effects of public disclosure. American Economic Journal: Economic Policy, 7(1), 36–62. https://doi.org/10.1257/pol.20130330

- Farouk, A. U., Idris, K. M., & Bin Saad, R. A. J. (2018). Moderating role of religiosity on Zakat compliance behavior in Nigeria. International Journal of Islamic & Middle Eastern Finance & Management, 11(3), 357–373. https://doi.org/10.1108/IMEFM-05-2017-0122

- Fjeldstad, O.-H., & Semboja, J. (2001). Why people pay taxes: The case of the development levy in Tanzania. World Development, 29(12), 2059–2074. https://doi.org/10.1016/S0305-750X(01)00081-X

- Fornell, C., & Larcker, D. F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. In: Sage Publications Sage CA.

- Frey, B. S., & Torgler, B. (2007). Tax morale and conditional cooperation. Journal of Comparative Economics, 35(1), 136–159. https://doi.org/10.1016/j.jce.2006.10.006

- Gilligan, G., & Richardson, G. (2005). Perceptions of tax fairness and tax compliance in Australia and Hong Kong-a preliminary study. Journal of Financial Crime, 12(4), 331–343. https://doi.org/10.1108/13590790510624783

- Hair, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2017). A primer on partial least squares structural equation modeling (PLS-SEM). Sage publications.

- Hair, J. F., Jr., Hult, G. T. M., Ringle, C. M., Sarstedt, M., Danks, N. P., & Ray, S. (2021). Partial Least Squares Structural Equation Modeling (PLS-SEM) Using R: A Workbook. In: Springer Nature. https://doi.org/10.1007/978-3-030-80519-7

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Hildreth, W. B. (2005). Tax transparency. In Encyclopaedia of Taxation and Tax Policy I. I. A. I. J. Cordes, I. I. A. I. D. Ebel, & J. Gravelle Urban Institute 2. https://barthildreth.com/images/uploads/files/HildrethonTaxTransparency.pdf

- Holzner, B., & Holzner, L. (2006). Transparency in global change: The vanguard of the open society. Pittsburgh. PA: University of Pittsburgh Press.

- Israel, G. D. (1992). Determining sample size. university of Florida IFAS extension. In. University of Florida.

- Kiow, T. S., Salleh, M. F. M., & Kassim, A. A. B. M. (2017). The determinants of individual taxpayers’ tax compliance behaviour in Peninsular malaysia. International Business and Accounting Research Journal, 1(1), 26–43. https://doi.org/10.15294/ibarj.v1i1.4

- Kleven, H. J., Kreiner, C. T., & Saez, E. (2016). Why can modern governments tax so much? An agency model of firms as fiscal intermediaries. Economica, 83(330), 219–246. https://doi.org/10.1111/ecca.12182

- Kohlberg, L. (1969). Stage and Sequence: The Cognitive Developmental Approach to Socialization. In D. Goslin, (Ed.), Handbook of Socialization Theory and Research (pp. 347–480). Rand McNally. https://doi.org/10.4236/ce.2011.22014

- Kohlberg, L., & Hersh, R. H. (1977). Moral development: A review of the theory. Theory into Practice, 16(2), 53–59. https://doi.org/10.1080/00405847709542675

- Kondelaji, H. M., Sameti, M., Amiri, H., & Moayedfar, R. (2016). Analyzing determinants of tax morale based on social psychology theory: Case study of Iran. Iranian Economic Review, 20(4), 581–598.

- Koumbiadis, N., Okpara, J. O., Pandit, G. M., Ritsatos, T., & Koumbiadis, N. (2014). Tax evasion and compliance; from the neo classical paradigm to behavioural economics, a review. Journal of Accounting & Organizational Change, 10(2), 244–262. https://doi.org/10.1108/JAOC-07-2012-0059

- Krejcie, R. V., & Morgan, D. W. (1970). Determining sample size for research activities. Educational and Psychological Measurement, 30(3), 607–610. https://doi.org/10.1177/001316447003000308

- Lachheb, H., Bouthanoute, R., & Bendriouch, M. (2016). For a local tax system dedicated to sustainable development incorporating governance, transparency and innovation. International Journal of Economics and Finance, 8(5), 212–219. https://doi.org/10.5539/ijef.v8n5p212

- Mason, P. D., Utke, S., & Williams, B. M. (2020). Why pay our fair share? How perceived influence over laws affects tax evasion. The Journal of the American Taxation Association, 42(1), 133–156. https://doi.org/10.2308/atax-52598

- McGee, R., Aljaaidi, K. S., & Musaibah, A. S. (2012). The ethics of tax evasion: A survey of administrative sciences’ students in yemen. International Journal of Business & Management, 7(16), 1. https://doi.org/10.5539/ijbm.v7n16p1

- Milesi, P., & Alberici, A. I. (2018). Pluralistic morality and collective action: The role of moral foundations. Group Processes and Intergroup Relations, 21(2), 235–256. https://doi.org/10.1177/1368430216675707

- Musimenta, D., & Ntim, C. G. (2020). Knowledge requirements, tax complexity, compliance costs and tax compliance in Uganda. Cogent Business & Management, 7(1), 1812220. https://doi.org/10.1080/23311975.2020.1812220

- Mustikasari, E. (2007). Kajian empiris tentang kepatuhan wajib pajak badan di perusahaan industri pengolahan di surabaya. Simposium Nasional Akuntansi X, 26, 1–42.

- Nangih, E., & Dick, N. (2018). An empirical review of the determinants of tax evasion in Nigeria: Emphasis on the informal sector operators in port harcourt metropolis. Journal of Accounting and Financial Management, 4(3), 15–23.

- Naser, I. M. M., & Hamzah, M. H. B. (2018). Pronunciation and conversation challenges among Saudi EFL students. JEES (Journal of English Educators Society, 3(1), 85–104. https://doi.org/10.21070/jees.v3i1.1228

- Naser, I. M. M., & Hamzah, M. H. B. (2022). Pronunciation difficulties and challenges in the field of research in Jordan. Journal of Humanities and Social Sciences, 6(14), 140–157. https://doi.org/10.26389/AJSRP.E090622

- Noked, N. (2018). Tax evasion and incomplete tax transparency. Laws, 7(3), 31. https://doi.org/10.3390/laws7030031

- Oberholzer, R. (2008). Attitudes of South African taxpayers towards taxation: A pilot study. Accountancy, Business and the Public Interest, 7(1).

- Owusu, G. M. Y., Bekoe, R. A., Anokye, F. K., & Anyetei, L. (2019). What factors influence the intentions of individuals to engage in tax evasion? Evidence from Ghana. International Journal of Public Administration, 43(13), 1–13. https://doi.org/10.1080/01900692.2019.1665686

- Ozili, P. K. (2020). Tax evasion and financial instability. Journal of Financial Crime, 27(2), 531–539. https://doi.org/10.1108/JFC-04-2019-0051

- Piotrowski, S. J. (2008). Governmental transparency in the path of administrative reform. Suny Press.

- Putra, I., & Jati, I. K. (2017). Analisis Faktor-Faktor yang Mempengaruhi Kepatuhan Wajib Pajak Kendaraan Bermotor di Kantor Bersama SAMSAT Tabanan. E-Jurnal Akuntansi Universitas Udayana, 18(1), 557–587.

- Rahayu, R., & Day, J. (2015). Determinant factors of e-commerce adoption by SMEs in developing country: Evidence from Indonesia. Procedia-Social & Behavioral Sciences, 195, 142–150. https://doi.org/10.1016/j.sbspro.2015.06.423

- Rashid, M. H. U. (2020). Taxpayer’s attitude towards tax evasion in a developing country: Do the demographic characteristics matter? International Journal of Applied Behavioral Economics (IJABE), 9(2), 1–19. https://doi.org/10.4018/IJABE.2020040101

- Rawlins, B. R. (2008). Measuring the relationship between organizational transparency and employee trust. Public Relations Journa, 2(2), 1–21. https://doi.org/10.1080/10627260802153421

- Roberts, M. L., & HITE, P. A. (1994). An experimental approach to changing taxpayers’ attitudes towards fairness and compliance via television. The Journal of the American Taxation Association, 16(1), 67–86. https://doi.org/10.1111/j.1467-9930.1994.tb00115.x

- Saad, N. (2011). Fairness perceptions and compliance behaviour: Taxpayers’ judgments in self-assessment environments. ( PHD degree DoctorL dessirtation), University of Canterbury,

- Sabucedo, J.-M., Dono, M., Alzate, M., & Seoane, G. (2018). The importance of protesters’ morals: Moral obligation as a key variable to understand collective action. Frontiers in Psychology, 9, 418. https://doi.org/10.3389/fpsyg.2018.00418

- Sadjiarto, A., Susanto, A. N., Yuniar, E., & Hartanto, M. G. (2020). Factors affecting perception of tax evasion among Chindos. Paper presented at the Advances in economics, business and management research: 23rd Asian Forum of Business Education (AFBE 2019).

- Sebele-Mpofu, F. Y. (2020). Governance quality and tax morale and compliance in Zimbabwe’s informal sector. Cogent Business & Management, 7(1), 1794662. https://doi.org/10.1080/23311975.2020.1794662

- Sekaran, U. (2003). Research Methods for Business: A Skill Building Approaches (4th ed.). John Wiley & Sons.

- Siahaan, F. O. (2013). The effect of tax transparency and trust on taxpayers’ voluntary compliance. GSTF Journal on Business Review (GBR), 2(3). https://doi.org/10.5176/2010-4804_2.3.213

- Siddiquee, N., & Saleheen, A. (2021). Taxation and governance in Bangladesh: A study of the value-added tax. International Journal of Public Administration, 44(8), 674–684. https://doi.org/10.1080/01900692.2020.1744645

- Tayib, M., Coombs, H. M., & Ameen, J. (1999). Financial reporting by Malaysian local authorities: A study of the needs and requirements of the users of local authority financial accounts. International Journal of Public Sector Management, 12(2), 103–120. https://doi.org/10.1108/09513559910263453

- Torgler, B. (2006). The importance of faith: Tax morale and religiosity. Journal of Economic Behavior and Organization, 61(1), 81–109. https://doi.org/10.1016/j.jebo.2004.10.007

- Torgler, B., Demir, I. C., Macintyre, A., & Schaffner, M. (2008). Causes and consequences of tax morale: An empirical investigation. Economic Analysis & Policy, 38(2), 313–339. https://doi.org/10.1016/S0313-5926(08)50023-3

- Torgler, B., Schaffner, M., & Macintyre, A. (2007). Tax compliance, tax morale and governance quality. International Studies Program Working Paper (No. 2007-17).

- Trochim, W., & Donnelly, J. P. (2007). The research methods knowledge base Mason (3rd ed). Thompson Publishing Group.

- Umar, M. A., Derashid, C., Ibrahim, I., & Bidin, Z. (2019). Public governance quality and tax compliance behavior in developing countries: The mediating role of socioeconomic conditions. International Journal of Social Economics, 46(3), 338–351. https://doi.org/10.1108/IJSE-11-2016-0338

- Van Dijke, M., & Verboon, P. (2010). Trust in authorities as a boundary condition to procedural fairness effects on tax compliance. Journal of Economic Psychology, 31(1), 80–91. https://doi.org/10.1016/j.joep.2009.10.005

- Verboon, P., & van Dijke, M. (2011). When do severe sanctions enhance compliance? The role of procedural fairness. Journal of Economic Psychology, 32(1), 120–130. https://doi.org/10.1016/j.joep.2010.09.007

- Vincent, O., & Ntim, C. G. (2021). Assessing SMEs tax non-compliance behaviour in Sub-Saharan Africa (SSA): An insight from Nigeria. Cogent Business & Management, 8(1), 1938930. https://doi.org/10.1080/23311975.2021.1938930

- Wahab, N. S. A., Ntim, C. G., Tye, W. L., & Shakil, M. H. (2022). Book-tax differences and risk: Does shareholder activism matter? Journal of International Accounting, Auditing & Taxation, 48, 100484. https://doi.org/10.1016/j.intaccaudtax.2022.100484

- Young, A., Lei, L., Wong, B., & Kwok, B. (2016). Individual tax compliance in China: A review. International Journal of Law and Management, 58(5), 562–574. https://doi.org/10.1108/IJLMA-12-2015-0063

- Zikmund, W., Babin, B., Carr, J., & Griffin, M. (2013). Business research methods (9th ed). Cengage Learning.