Abstract

Transaction Cost Economics has been used in the healthcare context to discuss the make-or-buy dichotomy, focusing on minimizing production or governance costs, respectively. Nevertheless, it is important to recognize that there are other relevant costs, which influence these decisions in health care. Thus, the purpose of this research project was to study such additional variables which may significantly influence the dynamics of transaction costs in hospitals. Semi-structured interviewing was used to collect the data, complemented by some document analysis and observation in the visits made to the hospitals studied. The interviews were conducted during a period of three months, with directors and administrators of four Portuguese hospitals. A deeper study was developed in one of the hospitals where it was possible to get information from additional interviews and documents. Two important findings should be highlighted. Firstly, the internal transaction costs derived from the hospital’s own internal contracting process which generates retention costs of medical personnel and costs of control of the internal contract itself. Secondly, they were studied the intangible costs, particularly those related to the decision of carrying out a process that could deteriorate the patient’s health or her/his critical situation, making the total cost, including treatment and possible re-hospitalizations higher than the cost of having treated the patient internally since the initial cost was considered greater than treating the patient outside hospital facilities. These variables should be considered when studying or using TCE in hospitals, complementing and extending the traditional framework as it is discussed here.

1. Introduction

With the growing demand for health services due to increases in population, a generalized increase in people’s life expectancy, the complexity of diseases and the new treatments, the expenditure of health systems’ has been increasing significantly (Kruk & Freedman, Citation2008; Simões et al., Citation2017). Indeed, health services are a strategic variable within the economic context of almost countries, for example, in 2019, prior to the COVID-19 pandemic, OECD countries spent, on average, around 8.8% of their GDP on health. The United States spent by far the most on health care, equivalent to 16.8% of its GDP—well above Germany, the next highest spending country, at 11.7%. A group of 10 high-income countries, including France, Canada, Japan, and the United Kingdom, all spent more than 10% of their GDP on health care (OECD, Citation2021). Furthermore, with the aging of the population, the cost of health services tends to increase. This is one of the reasons why knowledge and cost control is increasingly important within organizations providing health services. Thus, due to the limited budget and growing needs, the contracting processes in the health system must be efficient.

Contracting processes in hospitals can be divided into two parts, an external contracting, which is the one performed between the government and the top management of each of the hospitals, and the other internal contracting, which is made between the top management and each department, or service within the hospital and which contributes greatly for the fulfillment of external contracting.

In Portugal, in the process of external contracting, we can find as closely involved the Central Administration of the Health System (ACSS), the Regional Administrations (ARS), the Ministry of Health (MH), and Service Entities (Hospitals) which through several iterations try to reconcile the needs of the population with the existing financial resources in the National Health Service (NHS). The outsourcing process is supported by the computer application SICA (Information System for Contract and Follow-up).

The external contracting begins with the planning of health needs and the definition of investment priorities, followed by the collection of information from the institutions that will be contracted and ends with the evaluation of the hospital’s performance and the fulfillment of the contracted objectives.

In the contracting phase, the contrato programa (the contract) is foreseen, in which the objective is to adjust production proposals to the health needs of the population, agreeing production levels and associated costs that ensure the principles of equity, effectiveness, and efficiency of the system with respect to the provision of the service and contributing to the economic and financial sustainability of the hospitals and in general of the NHS.

Furthermore, there is a contract between hospital’s top management and its services or departments (internal contracting) which is integrated with the external contract. For the effectiveness of this integration, each department or service must meet the cost and production levels established for them. This contracting process can be seen as a purchaser–provider relationship. Among the premises of internal contracting is the fact that this process must be integrated into a modern, responsible, and rigorous management culture. Thus, it allows promoting the responsibility and autonomy of professionals and teams, contributing to increase motivation and commitment, higher levels of productivity and efficiency of the services and thus reducing the inefficiencies of the system. In addition, in this process, top management must create mechanisms to ensure that commitments and objectives are internally assumed by the organization, and mechanisms to measure compliance, and reward mechanisms for compliance should be implemented (ACSS, Citation2011, Citation2016).

In the process of internal contracting, costs are fundamental variable. In contracting processes between parties, we have the so-called transaction costs, which depend on variables such as uncertainty, specificity of the assets involved, limited, or bounded rationality and opportunism.

To study this relationship, the transaction costs economics (TCE) theory was used by the fact that the dominant perspective informing the use of contracts is TCE (Bigelow & Argyres, Citation2008; Bustamante, Citation2019; Le Bon & Hughes, Citation2009; Schepker et al., Citation2014). In addition, it is a theory where one of the underlying pillars has to do with the estimation of the costs that for the hospital sector is still representing a great challenge. This is important to the extent that in the case of the hospital sector, it is properly regulated and depends largely on the government and not on the market, justifying studies focused on cost-efficiency rather than on the market price mechanism. However, with the appearance of private services in health systems, an increasingly major decision will be to provide the health service using government or public entities or subcontracting to private companies.

Furthermore, a better understanding of healthcare costs from the patients and society perspectives is also important for a better use and optimization of the involved public and private resources. This knowledge will legitimate good or better decisions made by policymakers, managers, and population in general. Indeed, decisions that could deteriorate patients’ health or worsen their critical situation, will sooner or later impact on the total cost, generating also negative externalities, including treatment and possible re-hospitalizations.

The TCE has been used in the context of health care to discuss the decisions to make or buy considering production and governance costs, respectively. It is important to recognize that there are other relevant costs that influence these decisions. The scope of this research project was to study such additional costs that can significantly influence the dynamics of transaction costs in hospitals. To collect the data, the semi-structured interview was used, supplemented with some documentary analysis and observation in the visits made to the studied hospitals. The interviews were conducted with directors and administrators of four Portuguese hospitals. A more in-depth study was carried out in one of the hospitals where it was possible to obtain information from interviews and additional documents.

This paper is organized in six sections. The next section provides a literature review focusing on the key aspects of TCE. This section highlights the characteristics of transactions, the type of decisions and costs that are generated in a contractual relationship, in addition to highlighting various TCE applications in the healthcare environment. The third section describes the materials and methods. The fourth contextualizes the case study. The fifth section presents and discusses the main results obtained, first identifying the transaction costs inherent to the internal contracting process, related to the increasing cost of production or deliver healthcare services, and then highlighting some contributions to TCE models and the literature, mainly the consideration of internal transaction costs and intangible costs. The sixth section presents the main conclusion and opportunities for further research.

2. Literature review

2.1. Transaction cost economics

The notion of the company as a “black box” was questioned by (Coase, Citation1937), for him, the fact that the economic system was thought to be coordinated by the price system was only a partial description. That there are at least two economic coordination mechanisms: the markets and the company. In the market mechanism, the price system is the one that guides – in decentralized manner – the needs and opportunities of resource allocation; in the company, the principle of organization is different because through the hierarchy, the inherent authority system makes the reallocation of resources. Throughout many decades, several authors studied Coase’s approaches, and it was Williamson (Citation1985) that synthesizes some ideas of his ancestors and poses the TCE, with which he tries to answer the question “why organizations exist?” For Williamson, the firm is a particular type of organization—it is a management hierarchy—that allows to manage the exchanges or transactions and, in this way, to minimize costs, unlike other types of organization, especially the markets. This theory explores the boundaries of the firm: which transactions are developed within, which are bought, which are outsourced, which are carried out jointly between two or more firms. Thus, unlike other theories of the firm, for which it was simply a black box, the TCE also tries to explain the mechanisms of government within it and its extension to other forms, such as vertical integration and diversification.

TCE is focused on two concepts, the transaction costs, and the governance structures. One of the central ideas is related to the premise that aligning transactions with the organizational structure contributes to the reduction of transaction costs. Initially, this topic was approached from the economics’ perspective, but in the last decades it has also been important in other areas, namely, in business administration., where it is applied as a normative idea to improve decision-making of administrators (Ghoshal & Moran, Citation1996; Roehrich et al., Citation2020; Schneider et al., Citation2013).

One of the central elements of TCE is that enterprise boundaries and how different levels of vertical integration can be explained by the cost of governance. The costs of governance are those costs that are related, with the search, negotiation, contracting, problem solving, and administration of the contracts. These can be internal because the firm can do what it needs, or external because the firm can buy what it needs. According to the TCE, the company must carry out the activities internally when its cost of external governance exceeds the cost of internal governance. The TCE focuses on the transaction and indicates that its cost is related to the characteristics of the transaction (Cevikparmak et al., Citation2022; Gulbrandsen et al., Citation2009; Williamson, Citation1985).

For approximately 15 years, between 1975 and 1991, TCE focused on the classical dichotomy “make or buy”. However, since 1991 different models have been presented that try to include these decisions as well as other variables and decisions that appear more and more in the competitive environment of the business (Dahlstrom & Nygaard, Citation2010; Eicher, Citation2018).

In the study of organizations in recent decades, two basic premises have been considered, in the first instance, that institutions matter and secondly that the determinants of institutions are susceptible of analysis using the tools of economic theory (Macher & Richman, Citation2008; Matthews, Citation1986; Rindfleisch, Citation2020). In this context, various theoretical approaches have been developed around these premises. For example, the contingency theory considers that everything is relative. The effectiveness of organizations, and at the end, profitability, depends on the fit of organizational structure and contextual variables. Contingencies explain that there is a functional relationship between environmental conditions and appropriate management techniques for the effective achievement of the objectives of the organization. Environmental variables are independent variables, while administrative techniques are dependent variables within a functional relationship (Donaldson, Citation2001; Fiesher, Citation1998; Luthans & Stewart, Citation1977).

An interesting application of the theory of contingency in healthcare services investigated the determinants and outcomes of management accounting practices used by public health-care managers. More specifically, it proposed and empirically tested a comprehensive, contingency-based research model which addresses three related issues which are related to: fist the use of management accounting the design of the management accounting system, second the satisfaction of top management with management accounting is an indicator of the good or bad design of a management accounting system, and finally with that financial performance is influenced by the use of management accounting, this demonstrated that the relationship between management accounting and its influence on decision-making within these organizations (Macinati & Anessi-Pessina, Citation2014).

Furthermore, institutional theory in management accounting research can be presented in three main streams: New Institutional Theory – NIT, Old Institutional Economics – OIE, and New Institutional Economics – NIE. New institutional economics is preoccupied with the origins, incidences, and ramifications of transaction costs. Indeed, if transaction costs are negligible, the organization of economic activity is irrelevant, since any advantages of one mode of organization appearing to hold over another will simply be eliminated by costless contracting (O. E. Williamson, Citation1979). NIE or Transaction Cost Economics – TCE provides a useful analytical framework to explore the functioning of contractual relationships after the purchaser—provider split. Transaction costs are the costs associated with making an economic exchange under alternative structures that govern the transaction. A shift from one governance structure to another can be seen as essentially a search for a governance structure that reduces the problems that emerge ex-post in a relationship between two parties, i.e. their transaction cost (Castaño & Mills, Citation2013).

The TCE sheds most light on firm limits and the circumstances under which it is best to arrange activities within a hierarchy versus interrelating in a market with providers or other contractors (Caniëls & Roeleveld, Citation2009; Harding & Preker, Citation2000). TCE is one of the most important perspectives in management and organizational studies; however, the debate continues on the empirical studies that support it (David & Han, Citation2004; Peng, Citation2021).

In recent decades, TCE has emerged as a dominant theory for the analysis of contractual structures and governance associated with economic exchanges, and TCE has been an established concept for analyzing economic organizations (Schneider et al., Citation2013). TCE recognizes in such exchange process frictions are generated which in turn generate transaction costs. The objective is then to minimize such transaction costs either by carrying out activities within the company or acquiring them in the market, which will depend on the costs generated by the exchanges (Donato, Citation2010).

TCE has been widely discussed in areas such as economics (North, Citation2016), marketing (O. Williamson & Ghani, Citation2012), supply chain management (Grover & Malhotra, Citation2003; Hennart, Citation2010; Roeck et al., Citation2020; Wacker et al., Citation2016), finance (Koo et al., Citation2020; Li et al., Citation2017; Thapa & Poshakwale, Citation2010), organizational theory, strategy (Jell-Ojobor et al., Citation2022; Sinnewe et al., Citation2016), law and public policy (Coggan et al., Citation2010; Dagdeviren & Robertson, Citation2016; Garrick et al., Citation2013; Prasad & Shivarajan, Citation2015), health economics (Hajli et al., Citation2015) and agricultural economics (DeBoe & Stephenson, Citation2016; Macher & Richman, Citation2008).

The key conceptual move to TCE is to describe firms not in neoclassical terms, as production functions, but in organizational terms, as governance structures-. The basic insight of TCE is to recognize that in a world of positive transaction costs, exchange agreements must be governed and that, contingent on the transactions to be organized, some forms of governance are better than others (Macher & Richman, Citation2008; Peng, Citation2021).

A contract is understood as an agreement between two or more persons—natural or legal—to create a legal system that regulates a business, or some economic relationship. The contracts constitute an agreement that defines the terms that allow each of the parties involved, protect and assert their rights, and also know their responsibilities (Hall, Citation1992). There is evidence that as a contract is drawn up, it may affect the coordination of the parties and the results that can be obtained in the contractual relationship (Schepker et al., Citation2014).

Williamson (Citation1985) relates three fundamental elements of the transaction costs theory and the processes of negotiation between the parties, these elements are as follows: the bounded rationality, the opportunism, and the specificity asset; this under the supposition that in all cases, there is a level of reasonable uncertainty.

Asset specificity refers to durable investments that are not amortized in support of transactions, whose opportunity cost is much lower in the best alternative uses or by alternative users if the original transaction is terminated prematurely. For Williamson (Citation1985) There are at least four types of specific assets, these are: site specificity, physical specificity, human asset specificity, and dedicated asset (Gulbrandsen et al., Citation2009)

An important dimension in a transaction is related to the degree of uncertainty, which depends on the opportunist behavior and the limited rationality of the agents involved. Uncertainty is related to the degree of asymmetric information among economic agents and is also linked to the likelihood that they will not meet the contracted commitments (Banterle & Stranieri, Citation2008). The importance of uncertainty depends on the level of specificity of the assets, i.e. an increase in uncertainty matters little for non-specific transactions, since new business relationships can be easily found and the continuity of the relationship has little value. On the other hand, when assets are specific to a given degree, increasing uncertainty makes it more necessary for the parties to develop a system for resolving things, as contractual gaps are expected to increase, and the chances of sequential adaptations will increase in number and importance as the degree of uncertainty rises.

Internally, opportunism may be related to conflicting objectives between the purchaser (i.e., top management) and service providers (i.e., departments, services, responsibility centers among other form of organizations within the hospital) related to consumer responsiveness, the quality, and the efficiency of the services (Harris et al., Citation2014).,

On the other hand, bounded rationality means that those involved in contracting are unable to accurately predict future events, such as how demand behavior and patient status will be, such as patient behavior and healthcare professional behavior (Marini & Street, Citation2007).

Both opportunism and bounded rationality in a contractual relationship generate additional production and administrative costs that should be managed. In this context, this paper focuses on the relationship between internal contracting and cost management. Particularly, the costs derived from the contractual relationship which may influence decision-making related to the services provided to comply with the agreements established in the contract.

2.2. Transaction cost economics in the healthcare sector

Several studies have been conducted using Transaction Cost Economics (TCE) in the healthcare sector (Marini & Street, Citation2007; Ruiz-Mallorquí et al., Citation2021). For example (Robinson & Casalino, Citation1996), used the logic of TCE in California hospitals, and focused on two types of healthcare decisions, vertical integration, based on unified ownership and virtual integration, based on contractual networks. Among the findings, this research highlights the potential advantages of large physician organizations in terms of economies of scale, enhanced risk bearing ability, reduced transaction costs related to negotiation, monitoring, and execution of what is agreed in the contract, the capacity for innovation in methods of managing care services and the reduction of the holdup problems. Because the market is imperfect (Acemoglu et al., Citation2009; Felder et al., Citation2021; Stiglitz, Citation2021), on the other hand, the virtual integration has as advantages, the easy adaptation to changes in the environment, and the maximization of the efficiency.

When most TCE studies focused on the make or buy decision and specific assets, on (Coles & Hesterly, Citation1998) they stressed the importance of including uncertainties in addition to assets. They argue that in the case of public institutions, decisions may be more pressured by political and non-economic aspects than by strictly economic reasons, which may be not the case in private entities where decisions to make or buy are more guided by principles related to the maximization of the efficiency and profit (Sanderson et al., Citation2019).

Although decisions to make or buy are important in most organizations (Ludwig et al., Citation2009; Tadelis & Williamson, Citation2012; Walker & Weber, Citation1984). For example, some Dutch hospitals where the level of subcontracting of their services is low and normally outsourcing does not affect the efficiency of hospitals. Thus, they question whether much importance should be attached to make or buy decisions. In contrast (Cuellar & Gertler, Citation2006), discuss the negative effect of vertical integration (with the objective of reducing transaction costs) on hospital efficiency, due to the absence of a competitive market, which generates inefficiencies that can be translated into high costs in the provision of services.

Donato (Citation2010) highlighted the potential of TCE in health systems, but the author questions the fact that its conceptualization is static, i.e., it does not consider the variations that can occur in a contractual relationship and the fact that trust and changes occur over time and do not necessarily compel to vertical integration. He suggests applying TCE jointly with the resource-based view (RBV) to cover these deficiencies. Other authors analyzed the contractual process between providers and clients, e.g., the New Zealand health system under the TCE’s eyes highlighting some benefits such as the improvement in the commercial relationship and the quality of accountability in service providers (Ashton et al., Citation2004; Ashton, Citation1998).

The main difference between the market and the internal organization can be framed in the following principles: markets promote great incentives and restrict the bureaucratic distortions that are present internally in the organizations, markets have the capacity to add demand and generate economies of scale but, on the other hand, the organization can have access to different forms of internal governance and efficiency management.

TCE has been applied to situations where there are contracting processes, whether there is a competitive market or not, or where the specificity of the assets is important (Delbufalo, Citation2021).

Authors such as Holmström and Roberts (Citation1998) recognize the importance of TCE in the modern economic theory, but criticize the fact that in TCE when speaking of specific assets, no reference is made to direct upfront costs in ex ante investments. For example, it does not differentiate between a specific asset that costs ten million and another one that costs one hundred million, inside and outside the contractual relationship (Alchian & Woodward, Citation1988; Carney & Gedajlovic, Citation1991).

Another problem identified by Holmström and Roberts (Citation1998) is related to the determination of transaction costs. This is because within an organization the same resources can perform several transactions, therefore, to know the cost of each transaction we would need a proper costing system.

From its beginnings that TCE has been defended as well as criticized. Nevertheless, immense works have been developed throughout the last decades aiming practical contributions of this theory. TCE is important to understand decisions about whether it is better for an organization to make or buy (Canıtez & Çelebi, Citation2018; Wong et al., Citation2021). This discussion will be addressed in the next section, particularly, how the theory of transaction costs has been used to address issues related to healthcare.

3. Materials and methods

The methodology used in this research was semi-structured interviewing. An interview is an exchange between the researcher and the participants where the participant shares information and the researcher must have a sense of presence or accompaniment in the story, interviewing is the most used and popular data collection method in qualitative research (Corbin & Morse, Citation2003; Monforte & Úbeda-Colomer, Citation2021). Indeed, an elementary feature of the qualitative research interview method has to do with the relationship that is established between the interviewee and the interviewer (Cassell & Symon, Citation2004; Kertzscher et al., Citation2022). There are different ways of conducting the interviews, being the interview usually face to face the dominant technique (Hollway & Jefferson, Citation2000; Peasgood et al., Citation2023); however, several studies have explored the interview via telephone (Pieper, Citation2011) or Internet and intranet-mediated (electronic) interfaces (Peasgood et al., Citation2023; Thunberg & Arnell, Citation2022; Zhang et al., Citation2017) which have the advantages of being less expensive and have a greater geographical extent, but do not allow the reactions of respondents to be perceived, which can be a valuable element in qualitative research (Hilgert et al., Citation2016; Novick, Citation2008). In this research, all interviews were conducted face to face.

Several months of research were used to design the script of the interview. An iterative process was used that considered the research questions, the objectives, the bibliographical references, experiences in terms of research methods, case study, action research, etc. After a literature review, a first version of the script was produced, based on four main topics: organizational structure, costing systems, variability, and elements associated with TCE and agency theory. Once these topics were defined, we proceeded to validate them with a hospital administrator.

After validating the topics, the literature was reviewed to design the set of questions that will reflect adequately the concepts under analysis (Boučková, Citation2015; Cardinaels et al., Citation2004; Castaño & Mills, Citation2013; Collins et al., Citation1999; Fama, Citation1980; Gosselin, Citation2006; Jensen, Citation1983; Toma et al., Citation2012; Verbeeten, Citation2011; Williamson, Citation1985). Thus, a second version was produced. Once with the second version, a pilot study was performed with a hospital administrator, which allowed to create the third and final versions that are shown in Appendix I.

The interviews were conducted during a period of 3 months, with directors and administrators of different hospitals. All the interviews were recorded, a confidentiality term was given to the participants. So, the names of the institutions were replaced by an interviewee code. The semi-structured interviews were carried out with the top management of different Portuguese hospitals, and also with elements of middle management and clinical staff in charge of clinical services. Four organizations were interviewed, two of which are hospital centers (which together comprise six hospitals). Table shows the details of the interviews.

Table 1. Details of the interviews

Hospital 1 has approximately 500 beds, Hospital 2 has 704 beds, Hospital 3 has 848 beds, and Hospital 4 has 354 beds. Operational revenue for 2019 for Hospital 1 was around to 85 million euros, for Hospital 218 million euros, for Hospital 3, 236 million euros, and for Hospital around 4, 178 million euros.

The following protocol was followed for the interview process:

Get contacts from hospital administrators and top management.

Contact interviewees via email.

Use institutional electronic mail, carry out standard mail, and make telephone contact.

Present yourself professionally.

Define interview motives and objectives.

Send a page with interview information.

Talk about data confidentiality policy.

Send a confidentiality term model.

Schedule interview

Conduct the interview.

Brief presentation of interview project and objectives

Ask the questions in the guide.

Record the interview (a voice recorder was used)

Make copies of the interview on the personal computer and on the investigator’s hard drive)

Transcribing interviews (on average, 1 h of interview involves 6–8 hours of transcription)

Coding of the interviews (the software Atlas Ti 8.0 was used)

Preliminary analysis and production of individual reports

Further individual analysis of interviews and overall analysis of all interviews

Produce key findings, findings, and conclusions, and share final executive report with respondents.

Each interviewee received a document guaranteeing the confidentiality of the information.

In the process of encoding interviews, many codes emerged, which after being debugged were grouped into five categories or families, which are: Organizational Structure (five codes were used), Cost Management (nine codes), Variability and Uncertainty (three codes), TCE (11 codes), and other aspects (11 Codes).

Organizational Structure: This category considered not only the organization of hospitals, but also the decision-making process and autonomy related to decision-making, in these categories, five codes were used: Organizational Structure, Hierarchical Structure, Responsibility Centers, Autonomy in Resource Management, and Autonomy in Decision-Making.

Cost Management: This category addresses aspects related to the cost management process, costing systems, the advantages and disadvantages of the current costing system, the background and the importance and usefulness of cost management for decision-making; nine codes were used: Cost Management, Cost Accounting, Costing Systems, Costing Systems Implementation, Problems with Costing Systems, Using of Cost Information, Cost Control, Incentive Policy, Level of Satisfaction with the Costing System.

Variability and Uncertainty: The existence and importance of internal and external variability within hospitals was also identified—internal variability understood as the variability that in the treatment and therefore in the cost that a certain disease has, and external variability that is associated with the level of demand—an aspect that also came to the light during the interviewin this case, the codes used are related to the internal and external variability and the management of said variability; for this were used three codes: Internal Variability, External Variability, Risk and Uncertainty Management.

TCE and Agency Theory: This category was used to identify aspects related to the process of outsourcing, internal, and its relationship with cost management, in this category are included the difficulty to measure the production, the specificity of the assets, and problems with the information. Thus, 11 codes were used: TCE, Asymmetry of the information, Production Indicators, Complexity in the production definition, Contractual relationship, Specificity of resources, Specificity of Assets, Outsourcing, Insourcing, Contract, Controlling.

Other: Other aspects related to external variables influencing internal cost management such as the importance of cost management in the context of this framework, some innovations within hospitals, and resistance to change, among others were aspects considered here; for these, 11 codes were used: Hospital Autonomy, Importance of Project Management, Innovation, Intangible Costs, Lack of Autonomy, Lack of Information Systems, Organizational Culture, Private Hospitals, Qualifications, Resistance to change.

To perform the analysis of the collected data through the interviews and to highlight the most important findings, two tools of the ATLAS.ti were particularly important: the CooC Table and the Code-Document-Table, which allow to identify the existing relations between citations and codes, allowing to establish empirical relationships between the code and the first analyses, which were contrasted with other findings from other interviewees, in addition to the theory and financial reports and other reports of the units interviewed.

4. Contracting process in Portuguese hospitals: the payment system

The Portuguese health system is an integrated health system from the financing units—the government—to the units that provide the services to the community. This integration is possible thanks to the contractual process between the health regional administrations, central administration, and hospital institutions. The contractual process is based on a relationship among financiers, buyers, and suppliers. The tool used for this purpose is called the “contract”, which defines the level and composition of the contracted production, the objectives to be achieved, as well as the indicators that allow to verify the performance of the institutions in the perspective of guaranteeing the principles of access, service quality, and financial economic performance. Once the contract has been drawn up, the service providers must coordinate their internal efforts to comply with the contract, which is achieved following a strategy defined at the macro level by the board of directors. In this sense, the means and internal communication strategies are relevant to the extent that clear, defined, and well-known objectives must be established by all those involved in the process. The articulation between the three levels of management, government, boards of directors and levels of intermediate management—departments, management centers, responsibility centers—is necessary to define clear objectives and policies that allow not only to comply with the contract but also to ensure the sustainability of the system and the quality of services in the short, medium, and long term (Matos et al., Citation2010). The contracting process aims to contribute to strengthening the diagnosis of the population’s health needs and to reinforcing the implementation of good care and organizational practices that ensure high levels of access, quality, and efficiency in the National Health Service (NHS), placing citizens and their families at the center of interventions of all care providers, reinforcing the articulation and coordination among them, valuing the performance of professionals and encouraging clinical and health Governance (ACSS, Citation2016). The contracting process takes place externally—e.g., between hospitals and government entities—and internally—between managers, departments, accountability centers, etc. According to (ACSS, Citation2016), In the Portuguese NHS, internal contracting processes should be integrated into a modern, responsible, and rigorous management culture, promoting the responsibility and autonomy of professionals and teams thus, contributing to increase motivation and commitment, levels of productivity and effectiveness of services, and to reduce inefficiencies and waste in NHS institutions.

The contracting process starts with the planning of health needs and the definition of investment priorities, followed by the collection of information from the institutions to be contracted and ends with the evaluation of the performance of the contracted goals. They are three distinct phases, which differ in terms of the objectives to which contracts are intended and which determine different interlocutors and responsibilities considering the time horizon.

The planning and collecting phases provide the basis for the negotiation and for the design of the contract, in which the objective is to adjust production proposals to the health needs of the population, agreeing production levels that ensure the principles of equity, effectiveness, and efficiency of the system—implying an effective knowledge of the population’s health needs—as well as their economic and financial sustainability.

In the monitoring phase of the implementation of the contract by the institutions, the objective is to systematically collect information that enables the comparative analysis of the real performance against the contracted one, to promote corrective measures or to establish good practices based on the good results achieved. This phase reveals critical to the fulfillment of the intended objective. Several aspects should be taken into consideration, namely, the impact of externalities and the quality of the data reported.

The contracting process takes place within a time horizon that normally starts at the second quarter of the year prior to the year for which it is intended to be the contracting, and the monitoring phase is carried out throughout the year. The process ends with the evaluation of the degree of compliance with the contracted goals and performance objectives achieved, allowing to determine the inherent consequences and apply the rules defined in the contract. This phase occurs after the closure of the year for which the contracting process was carried out, accompanied by the process of accounting of the billing process of the contract (ACSS, Citation2011).

At the internal level of hospitals, contracting takes place at the micro level and promotes the alignment of the objectives, for example, the number of treatments expected to be made can be contracted with the imaging area, thus making better use of resources, improving the efficiency of the processes. However, it is always framed by the external contracting that drives or limits it.

After a SOWT analysis regarding internal contracting in Portuguese hospitals, Matos et al. (Citation2010) emphasized as strengths the fact that the internal contracting based on the history of several years has been improved in these hospitals; in some hospitals there are already plans of intermediate management training and in some hospitals there is already an effective involvement of intermediate management levels in the contracting process.

Among the weaknesses and threats that they stand out are: excessive focus on operational management over strategic management, lack of accountability culture and quality in some organizations effectiveness vs. efficiency, poor involvement of middle management in hospital management, lack of leadership ability, lack of management training at the intermediate level of management, lack of autonomy in the management of human resources, legal difficulties to implement performance evaluation policies and incentive systems, lack of credible and integrated information systems to monitor qualitative and real-time results, lack of information systems that allow service and medical act, lack of real costing methodologies at national level, lack of definition of criteria and common language, explicit timetable, unique interlocutor, and documentary simplicity in external contracting. In addition to analyzing the needs of the population, one of the bases of the contract also focuses on the own capacity of the hospitals, which in turn is related to the capacity of each service, department, or responsibility center.

This generates that the top management of the hospital must “contract” the production with each service, department, or responsibility center to fulfill its objectives proposed in the contract that is to carry out an internal contracting process.

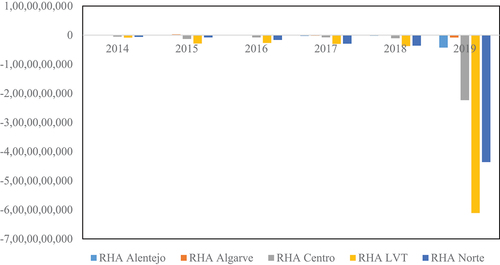

The internal contracting process is important to the extent that it will contribute to meeting the financial objectives set out in the outsourcing process. One of these objectives is that each hospital must plan and manage to achieve a positive EBITDA, eliminating the accumulation of new arrears and implementing the measures of containment and rationalization of costs to achieve this objective. This objective has not been fulfilled in recent years, as shown in Figure and Table . Indeed, the EBITDA for the 2014–2019 period has been mostly negative. This information is organized by each of the Regional Health Administration (RHA) in which the different hospitals in Portugal are grouped: RHA Alentejo (Region), RHA Algarve (Region), RHA Centro (Region), RHA LVT (Lisboa and Tagus Valley Region) and RHA Norte (Region).”

Table 2. Analysis of the negative eBITDA between 2014 and 2019 of Portuguese hospitals organized by RHAs

Crossing the information in Table with the one presented in Figure it is possible to predict that part of the breaches of the RHA is due to breaches in the contract with the hospitals, and the contract with the hospital in turn can be defined as a sum of internal contracts. Therefore, it is fundamental to analyze the internal contracting to determine the source of the non-compliances that will allow to determine intervention measures either via efficiency improvement or by the way of more injection of resources by the state. The process of internal contracting, its complexity, and implications will be analyzed in the following section.

5. Analysis and discussion of findings

The first section is focused on the dynamics of the contracting process in hospitals using the lens of TCE and the second section is related to additional issues on transaction costs in the context of hospitals, and the third section presents a TCE framework for contracting process in hospitals. The contract is the central axis of the process, but there are new elements which should be considered when talking about TCE in hospitals (i.e., the internal contracting process and the existence of intangible costs).

5.1. Internal Contract Process (ICP) from the perspective of TCE

The TCE is based on two important concepts, which are bounded rationality and opportunism. In hospitals, these aspects are even more complex because information is asymmetric among managers, medical staff, administrative staff, and patients (2013).

With respect to the bounded rationality in the contracting process, different opinions were found in the hospitals interviewed. When asked if it is easy for an administrator to know and control all activities of a director, the administrators, and director services remarked:

If it is at a quantitative level, yes, at the technical level no, nor do they have to tell […] for example, if we ask why this month we fewer patients have, one answer may be that the patients are more complicated, they have more problems, the pathologies are more differentiated, and this we cannot counter-argument.

In this case, it is difficult to control the doctors since they can make satisfactory decisions from the medical point of view but not necessarily optimal from the organization’s perspective (Ren & Huang, Citation2018), since the identification of a pathology can be complex and is subject to medical criteria (Bell-Aldeghi & Chopard, Citation2021).

Related to this subject is also the symmetric or asymmetric information that exists between the board of directors and the different units within the hospital. The asymmetry of information is linked to the organizational culture (Nestle et al., Citation2019) and the concept of trust (Eicher, Citation2018), and it is not perceived in the same way within the different hospitals as we can see from the next quotations.

The board of directors has inside information (HOSPITAL 1/INTERVIEWEE 1)

The business intelligence that we have is not only for the administration, it is for the doctors also, and for the directors of service, therefore they daily monitor whether they are above or below their activity, not only in [terms of] quantity but also in [terms of] quality indicators.

… … our opinion is that all agents need to have the maximum possible knowledge [… to support better] their actions, knowledge of information has more positive than negative effects …

These comments show opposite approaches, with different implications in day-to-day activities and strategic planning of the organization. In the cases where the culture of information sharing is more developed, it was observed that a better fulfillment of the contract and a better quality of management systems, than in the information was considered a privilege to the shared parsimoniously.

Another important aspect from the TCE perspective, has to do with the ability to define the product and to be able to measure the outcomes of the process. In the case of hospitals, the relationship of the contract with the provision of services can make this measurement difficult.

… The hospital is financed by the patient [instead of the level of activity he/she implies], but the more tests the patient does, the more costs the hospital has.

It is very difficult to determine production. (HOSPITAL 1/INTERVIEWEE 1)

We have to treat everyone; we cannot say that this patient does not interest us.

When you have a factory, you can decide not to make this product and make another […] therefore you can choose your production mix. We cannot choose the mix of services [that we offer]. [For instance,] if a doctor wastes a lot of time on one patient, the only thing I could do is to ask the doctor to try to be more efficient, and waste less time, but there could be quality problems. Difficulties to measure production always exist, but we try every day to minimize these difficulties.

As can be seen, there are also great difficulties in measuring hospital production (Santías et al., Citation2011). In addition to this, each patient is a specific clinical case, and the consumption of resources can be considered different when two apparently similar patients are compared (Kao et al., Citation2021). This creates external variability, what Mills (Castaño & Mills, Citation2013) calls uncertainty in quantity, i.e., not knowing how many patients are going to arrive, and internal variability, due to the variability in the number of resources that can be consumed by patients with similar pathologies. For the treatment of variability, several approaches were evidenced, from doing nothing to designing strategies to not only quantify the variability but also generate control measures.

… if there is a considerable deviation, we must understand it. There is variability of costs, but it may be visible, […] it becomes visible when it has an impact on the analysis of global deviations that we make in the hospital.

In Hospital 1, variability is important at the macro level, and they have information systems that allow to analyze deviations in a reasonable time for decision-making.

… we’ll always consider the average [costs] because […] even using the same procedure in patient A and patient B, we can get different costs …

In Hospital 1, another interviewee said that despite knowing the existence of internal variability in terms of trying to quantify it.

No, risks are e not discussed in the hospital. They are known to exist, but no attempt has been made to measure [risks] … (HOSPITAL 1/INTERVIEWEE 1)

We do not have any way to quantify variability, [but] we know that it exists. (HOSPITAL 4/INTERVIEWEE 8)

This shows that although there is internal variability and hospitals are aware of its existence, there are no clear tools for its quantification and treatment. In addition, despite hospitals being aware of the existence of variability, some have created mechanisms to try to understand it and other hospitals do not know how to treat it.

TCE also highlights the specificity of the assets. In this case, we find specificity by human resources since it is necessary to count with very qualified and specific personnel.

We currently have between 30 and 40 doctors doing their PhD, because we do a lot of clinical trials, a lot of clinical research … The hospital is not only doctors, although its core business is the clinic area …

Furthermore, we have also here, location specificity, because the services must be provided within the specific facilities of the hospital, and equipment specificity since the equipment would have little commercial value in alternative activities.

All these elements generate contracting difficulties, since the contracts are incomplete, and the hospital must incur in costs to control the network of established relationships. In this sense, the costs related to the control of the compliance with the contract. The cost of retention of the doctors is also relevant.

… the private health sector is robbing our professionals, […] we are supposed to have highly specialized and differentiated resources and we fail to maintain them, to captivate them […] they are trained here, but ending the specialization are immediately seduced by private hospitals […] the same happens with nursing, we have highly differentiated nurses, but they are leaving us because more and more private hospitals are opening new units, also very specialized and ask for our professionals because they are highly differentiated.

This is an important fact to consider, since to be competitive in the provision of health services, they are required very qualified and highly differentiated personnel. To retain them, retention policies and incentives must be developed, although it is true that due to monetary crisis, budget, and deficit constraints, among other factors, economic benefits are stagnant. But incentives through personal recognition, research, or training are highly valued by people in the health sector and incentive policies in this direction would guarantee qualified and motivated personnel that allow the fulfillment of the contract not only in terms of costs but also in the quality-of-service provision.

5.2. Intangible costs

One of the results of the interviews regarding the contracting process between the top management of hospitals and their departments or production centers has to do with the fact that hospitals are at various levels not only of contracting culture but also of compliance with contracts.

However, they all recognize that the estimation of production costs and service quality indicators, such as patient readmissions rate, are important. Indeed, they allow the identification of problems in outsourcing, identifying inefficiencies or opportunities to improve services and thus reduce costs without affecting quality.

In cases where costs cannot be reduced, an additional concern is related to increasing the volume of production, which could indicate an increase in income since, in the contract, revenues are correlated to the number of patients treated, considering minimum and maximum limits.

However, attending more patients does not mean increased income for all departments or internal areas of the hospital. For example, this problem was evidenced in the imaging service of one of the studied hospitals.

There is always a goal that is never fulfilled … which is to reduce demand. Because the hospital is not funded by diagnosis […] no, the hospital is funded by pathology, so the more tests the patient does, the costlier the patient will be for the hospital. Therefore, […] the increase in production is not an increase in revenue. At the same time, we also must have an efficient response and meet the response times. Response times are also a quality metric. But the fact that we have too much demand will not increase revenue. And the goals are to decrease the number of exams. And this is complicated. And we have not succeeded. […] Medicine is becoming more and more defensive, and a defensive medicine always involves a greater number of requests for examinations, there are many, many exams. HOSPITAL 1/INTERVIEWEE 2)

From this, it emerges an interesting paradox: it is necessary to reduce costs in a paradigm of more assistance/patients and more complex and expensive exams. This could be solved in several ways. It could be accepted that the cost will simply increase by increasing the complexity of the product and try to stabilize or maximize, if possible, the relationship between quality and cost, or simply maintain or reduce costs by sacrificing the quality of the services provided, which would not be expected from a system that wants to guarantee the quality of its citizens. The solution will be, probably, more focus on increasing the resources given to health, maintaining, or improving quality levels at the same time as processes are optimized in a continuous improvement effort to mitigate such increase in expenses.

In the case mentioned above, a greater number of tests performed means a greater increase in costs, but not a greater increase in revenues, which may affect hospitals’ EBITDA. In this sense, some hospitals are already trying to standardize some processes and homogenize at least the medical prescription for certain types of diseases to provide quality treatment without to harm the finances. This generates a challenge, on the one hand the financial balance must be guaranteed and on the other the main objective of healthcare organizations must be guaranteed, which is to diagnose and treat patients (Lee, Citation2017).

This comment made clear that the contracting process with the different departments is more complex because:

“To know the cost of a patient it is necessary that departments are interconnected since they are financed by” inpatient “or treated patient and not by number of exams, or number of times the patient consumes a certain resource within the hospital, which may vary not only from patient to patient but also from doctor to doctor.”

This reveals asymmetries in information and, in some cases, lack of information that not only makes difficult the calculation of production costs, but also makes it difficult to understand the internal transactions and the cost related to them.

The cost of a patient depends not only on their pathology but also on the tools used to diagnose the diseases, the treating prescribed by the physician, etc.

Re-admissions exist where the health status has deteriorated further, and the cost of the patient re-entered may be higher than in the initial state. This highlights one of the key variables in the contracting process identified by Castaño and Mills (Citation2013), the difficulty of measuring output and the difficulty of measuring results, one of the variables that generate incomplete contracts.

Here, the specificity of the assets is a critical variable to explain the existence of some of the transaction costs that are generated (David & Han, Citation2004). These internal transaction costs are related in the relationship of the top management with each of the directors or coordinators of the services, depending on how the hospital is organized, and will be influenced by the limited rationality, the opportunism, the specificity of the assets and the difficulty of defining measurement indicators.

The study contrasts with what was proposed by Castaño (Citation2013) applied in the hospital sector in Colombia and highlights the main elements of the TCE but without considering the internal contracting process and intangible costs, which is discussed in our paper. On the other hand, Ashton et al. (Citation2004) focused on the characteristics of the contract and Eicher (Citation2018) on the specificity of the assets and added the variable trust. Intangible costs call attention to the patient as one more element for the buy or make decision.

The logic of the TCE the decision would be to buy or what otherwise said to acquire in the market. For the study in analysis, it is important to consider that the decision is not so linear, inasmuch as because it is considered a public good, the process of “buying services is not so easy”, in addition hospitals must have an installed capacity Should be used and should strive to comply with what has been established in the contract, being a service mostly public the decision would be more for the improvement of internal efficiency than for making the decision to carry out the activities and services externally. Another factor has to do with the specificity of place specificity of place that in this case by service logistics some patients must be treated within the same hospital to guarantee the quality of service.

When we cannot do an examination inside the hospital, we have to do it, and of course these tools are useful in that sense because it is to prove that if we take the examination out, and introduce all the associated costs in carrying out an examination, it will not Being only the cost of the examination, will be the cost of the patient going, transportation, and other costs that are not even measurable, more that are clinical costs, are not measurable in monetary terms more than in terms of quality service, then in terms Of even hospitalization times can increase because also the fact that the patient leaves and the instability that sometimes creates this to the patient. If all this was measured it was easier to prove, everyone already knows that it is more expensive to do out there, roughly with the things that we know, maybe it was easier to make realize that the money that is spent every year to do exams abroad if it was used to remodel the services and acquire new equipment was much better used.

Hence the idea of having to consider the intangible costs, or the costs associated with the quality of the service, which in some cases are so high that even if a procedure outside the hospital is financially cheaper, the most appropriate and rational decision is performed within of the hospital. In the healthcare literature, the intangible cost is related to: the psychological pain to the family and loved one (Kirigia et al., Citation2009), the pain, the anxiety, and the depression (Haines & McPhail, Citation2011), the reduction of the desire to consume food or medicines (Akazili et al., Citation2008). All the intangibles are related to the decrease of the quality of life of the patient or the worsening of his/her health condition.

Seen from another point of view, that is, there are services that, despite being cheaper, should be provided in the hospital to reduce the risk of virus, deterioration of the patient’s quality, which in the end would not only affect quality, Health, but also the total cost due to the increase in the number of days in hospitalization, or due to possible future readmissions with more complications than the initial ones.

It is important then, besides considering the cost of the market and controlling the transaction, to consider the intangible costs.

5.3. Extending the traditional TCE: A framework

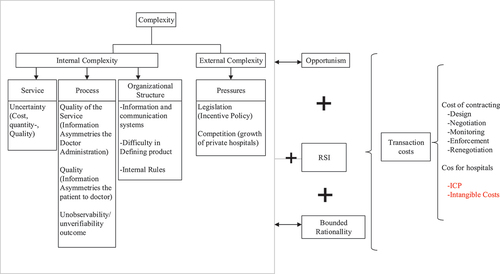

After analyzing all these elements, one of the first conclusions is that the internal contracting process in hospitals is a complex task. Due to the nature of hospitals' services and processes, the computation of production costs is complex, coupled with the existence of bounded rationality, opportunism, and specificity of human and physical assets. It also generates internal transaction costs related to the design of the contracts, their execution, and the monitoring itself, as well as learning costs (when new staff are needed) and costs that can be hidden due to inefficiency. These elements are represented in Figure .

Figure 2. The transaction cost of internal contracting in hospitals.

Figure highlights some elements that generate complexity in the hospital system, which make it difficult to estimate costs, contract compliance (whether internal or external) and finally generate transaction costs. In the figure, these elements were grouped according to whether they are internal or external to the hospital. Within a context of bounded rationality and opportunism, contract incompleteness and relationship-specific investment (RSI) create transaction costs (Castaño & Mills, Citation2013). Regarding to the specificity of assets, trust influences hospitals’ decisions on the internal or external contracting of their investments in assets (Eicher, Citation2018).

With respect to the external complexity, it involves two elements. The first one derived from the policies of the government, namely the absence of incentive policies to promote productivity. By not promoting productivity, inefficiency is generated in the system, which leads to cost overruns that do not allow the fulfillment of the contract.

Another element that generates internal complexity is related to the pressure exerted by competition (mainly from the private sector), which by having better conditions and flexibility is being taken the best professionals, which forces public hospitals to invest continuously to get professionals (which is a specific and scarce asset), which often must be trained, incurring in costs related to such training and learning process. This is a cost rarely is it considered in the costing exercises, but which generates a negative impact on the compliance of the contract.

The public–private partnership hospital had information systems that made it possible to calculate the cost of services rendered in a useful time for decision-making. In public hospitals, dissatisfaction with the cost management system was evident. The public hospital staff is not satisfied with their cost information system compared to private which has a reasonable degree of satisfaction of their system, which makes it clear that cost management systems will be more successful in the extent to which efficient information and communication systems exist and the widespread perception that cost-efficiency is a strategic variable for the good performance of a hospital.

With respect to internal complexity, the elements were grouped as follows: 1) considering product-derived complexity (the service offered to patients); 2) the complexity derived from the processes developed for the provision of the service; and 3) the complexity itself derived from the organizational structure.

With respect to the complexity derived by the services, the fact that there is internal variability (derived from the own pathologies) and external variability (derived from the type of patients that arrive at the hospital) should be highlighted. This added to the fact that pathologies are increasingly complex and increasingly more sophisticated diagnostics are required, which are more costly, and turn the estimation of the production cost and the analysis of the efficiency or inefficiency that will impact the contract more difficult.

On the other hand, the complexity derived from the processes is significant because most of the processes occur as result of the interaction between doctors and patients, and the variables associated to the efficiency, outputs, and quality of the service depend on the behavior of the doctor, of the patient, of the treatment and of the evolution of the pathology. All this generates asymmetry in the information, difficulty in estimating the cost and increase in cost control, which also has a negative impact on compliance with the contract. The transaction cost could be reduced if there is trust between the agents that interact within the hospital system (Eicher, Citation2018).

Finally, the complexity derived from the organizational structure contains elements such as the difficulty associated with the existence of multiple information systems which are not interconnected, which makes it difficult to control transactions and estimate the cost-of-service delivery.

The difficulty to define or parameterize cost objects since the contract assumes a value per DRG per patient and each patient consumes different resources even having the same pathology. Another element is related to the internal rules that result in a lack of autonomy for decision-making by the intermediate-level personnel, which can make it difficult to control costs and transactions because decisions are centralized in top management.

In addition to the internal and external complexity, the intangible costs derived from the effects that the purchase or decision-making may have on a patient’s health, or the outcome of a treatment are highlighted. In addition to the studies presented by Ashton et al. (Citation2004) that focus on the characteristics of the contract and Eicher (Citation2018) that focuses on the specificity of the assets and the trust, intangible costs call attention to the patient as one more element for the buy or make decision.

Some implications can be highlighted for policymakers such as: Hospitals’ internal complexity generates transaction costs which should be taken into consideration by policy and decision makers. The internal contracting process generates retention costs of medical personnel and costs of control of the internal contract itself which should be properly managed. Healthcare intangible costs are typically neglected but should be better managed because they impact significantly on the general efficiency and quality of the system and patients’ quality of life. Transaction costs must be better balanced with the quality of healthcare services.

6. Conclusions

Analyzing the aspects of TCE and cost management in hospitals we realize that hospitals are complex institutions where their internal contracting process is difficult to monitor due to internal and external elements. Such complexity, coupled with the specificity of the assets and the opportunism of the agents involved, generates costs that are mostly difficult to quantify or rare is considered in traditional cost accounting (such as design, control, and learning costs).

This complexity turns difficult the estimation of the cost of the services. Nevertheless, it is a fundamental variable to understand breaches in the internal or external contracting processes.

If the cost of the services can be estimated internally, comparing said cost with the market could help to identify inefficiencies or opportunities for improvement, or simply allow deciding whether the hospital’s production is done internally or can be subcontracted.

In this sense, it is important to use tools and theories that help to understand the dynamics related to contractual processes and their execution. TCE is one of these theories (David & Han, Citation2004).

One of the postulates of the TCE is that organizations exist to replace the market when the cost of controlling relationships exceeds the fact of performing transactions internally. However, it could be noted that organizations such as hospitals do not necessarily comply with this postulate, since while internal costs may be higher, the nature of the service, installed capacity, and legal conditions, this is in line with what is mentioned by Ghoshal and Moran (Citation1996) and Balakrishnan et al. (Citation2010).

They highlight that organizations are not mere substitutes for structuring effficient transactions when markets fail. Organizations possess unique advantages for governing certain kinds of economic activities through a logic that is very different from that of a market. TCE is “bad for practice” because it fails to recognize this difference. The decision of the organizations to carry out their activities or outsource them must be analyzed not only from the simple point of view of costs but also considering variables such as the quality of the service or the typology of services offered.

One of the main contributions of this paper is to include two important variables in the make or buy decision-making process. The first one has to do with internal transaction costs derived from the complexity of the internal contracting process. The internal contracting process generates transaction costs such as retention costs of medical personnel and costs of control of the internal contract itself.

The second aspect has to do with the intangibles costs, which are related to all those hidden or additional costs incurred if the decision was to carry out a process that could deteriorate the patient’s health or worsen their critical situation, affecting not only the patient but also making the total cost, including treatment, and possible re-hospitalizations, higher than the cost of having treated the patient internally since the initial cost was greater than treating the patient outside hospital facilities.

To broaden the spectrum of this work, future work has to do with in the study of other countries and carrying out a comparative analysis to determine if the results are typical of specific social-economic contexts or if they can be generalized to other hospital systems. Another important element of TCE has to do with the measurement of transaction costs; thus, a further work has to do with the design of costing systems to estimate the transaction costs.

Further research can be related with the application of a survey to many hospitals. To broaden the spectrum of the work and identify differences and similarities among healthcare systems, a comparative analysis across countries can be made. The measurement of the transaction costs is also an important issue, and further work should focus on the design of costing systems to estimate such costs. Comparisons among public, private, and semi-private hospitals could also be made to. A limitation of this work is that it does not have the participation of patients. Thus, future work we could study the effect that a decision of make or buy within the hospital may have on patients’ health.

6.1. Ethical considerations

For the development of this work, the anonymity of the people who participated in it and the confidentiality of the information were guaranteed so as not to affect the participants. In addition, all the people received informed consent of the process and that it would be carried out with the information.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Jiménez Victor

Victor Jimenez received his Ph.D. degree from the Department of Production and Systems at University of Minho (Portugal). Victor Jiménez holds a Master in Engineering at University of Valle and he is graduated in Industrial Engineering at University of Valle. He is Associated Professor at University of Valle, where he teaches Engineering Economics, costing and finance. He is integrated researcher at Algoritmi Research Centre. Apart from academia Professor Victor Jiménez is a member of the financial risk committee of a solidarity economic organization, and an advisor to companies in financial analysis, costs and budget management and feasibility studies for the creation of new businesses.

Afonso Paulo

Paulo Afonso is an Assistant Professor at the University of Minho (Portugal) with a focus on Management Accounting & Control, Strategic Analysis & Business Modelling. His research is related to Supply Chain Performance and Cost Management, Costing Models and Costing Systems for Decision Making, Strategic Investment Appraisal, Strategic Management, Business Model Design, Startups and Entrepreneurship. He holds a PhD in Management Accounting at the Manchester Business School - University of Manchester (UK); a Master in Industrial Engineering (Specialization on Investment Appraisal and Innovation Management) at University of Minho; and a Diploma in Economics at ISEG (Economics and Business School) - University of Lisbon (UTL). He is integrated researcher at Algoritmi Research Centre and collaborator in several research centres. He has been visiting professor and researcher in several universities and collaborates with the industry in his areas of expertise.

References

- Acemoglu, D., Johnson, S., & Mitton, T. (2009). Determinants of vertical integration: financial development and contracting costs. The Journal of Finance, 64(3), 1251–26. https://doi.org/10.1111/j.1540-6261.2009.01464.x

- ACSS. (2011). Manual do Processo de Contratualização - Hospitais e ULS, 35.

- ACSS. Termos de Referência para contratualização de cuidados de saúde no SNS para 2017. (2016). Retrieved from http://www.acss.min-saude.pt/wp-content/uploads/2016/12/Contratualizacao_Cuidados_SNS_Termos_Referencia_2017.pdf

- ACSS. (2019). Agregados Económico Financeiros. Retrieved June 1, 2020, from https://transparencia.sns.gov.pt/explore/dataset/agregados-economico-financeiros/?sort=tempo

- Akazili, J., Aikins, M., & Binka, F. N. (2008). Malaria treatment in Northern Ghana: What is the treatment cost per case to households? African Journal of Health Sciences, 14(1), 70–79. https://doi.org/10.4314/ajhs.v14i1.30849

- Alchian, A. A., & Woodward, S. (1988). The firm is dead: Long live the firm: A review of Oliver E. Williamson’s “The economic institutions of capitalism. Journal of Economic Literature, 26(1), 65–79. https://doi.org/10.2307/2726609

- Ashton, T. (1998). Contracting for health services in New Zealand: A transaction cost analysis. Social Science & Medicine, 46(3), 357–367. https://doi.org/10.1016/S0277-9536(97)00164-0

- Ashton, T., Cumming, J., & Mclean, J. (2004). Contracting for health services in a public health system: The New Zealand experience. Health Policy, 69(1), 21–31. https://doi.org/10.1016/j.healthpol.2003.11.004

- Balakrishnan, R., Eldenburg, L., Krishnan, R., & Soderstrom, N. (2010). The influence of institutional constraints on outsourcing. Journal of Accounting Research, 48(4), 767–794. https://doi.org/10.1111/j.1475-679X.2010.00381.x

- Banterle, A., & Stranieri, S. (2008). The consequences of voluntary traceability system for supply chain relationships. An application of transaction cost economics. Food Policy, 33(6), 560–569. https://doi.org/10.1016/j.foodpol.2008.06.002

- Bell-Aldeghi, R., & Chopard, B. (2021). Hospital multi-dimensional quality competition with medical malpractice. International Review of Law and Economics, 68, 106025. https://doi.org/10.1016/j.irle.2021.106025

- Bigelow, L. S., & Argyres, N. (2008). Transaction costs, industry experience and make-or-buy decisions in the population of early U.S. auto firms. Journal of Economic Behavior and Organization, 66(3–4), 791–807. https://doi.org/10.1016/j.jebo.2006.01.010

- Boučková, M. (2015). Management accounting and agency theory. Procedia Economics and Finance, 25(15), 5–13. https://doi.org/10.1016/S2212-5671(15)00707-8

- Bustamante, C. V. (2019). Strategic choices: Accelerated startups’ outsourcing decisions. Journal of Business Research, 105(June 2018), 359–369. https://doi.org/10.1016/j.jbusres.2018.06.009

- Caniëls, M. C. J., & Roeleveld, A. (2009). Power and dependence perspectives on outsourcing decisions. European Management Journal, 27(6), 402–417. https://doi.org/10.1016/j.emj.2009.01.001

- Canıtez, F., & Çelebi, D. (2018). Transaction cost economics of procurement models in public transport: An institutional perspective. Research in Transportation Economics, 69(November 2017), 116–125. https://doi.org/10.1016/j.retrec.2018.03.002

- Cardinaels, E., Roodhooft, F., & van Herck, G. (2004). Drivers of cost system development in hospitals: Results of a survey. Health Policy (Amsterdam, Netherlands), 69(2), 239–252. https://doi.org/10.1016/j.healthpol.2004.04.009

- Carney, M., & Gedajlovic, E. (1991). Vertical integration in franchise systems: Agency theory and resource explanations. Strategic Management Journal, 12(8), 607–629. https://doi.org/10.1002/smj.4250120804

- Cassell, C., & Symon, G. (2004). Essential guide to qualitative methods in organizational research. Athenaeum Studi Periodici Di Letteratura E Storia Dell Antichita, 388. https://do.org/Book

- Castaño, R., & Mills, A. (2013). The consequences of hospital autonomization in Colombia: A transaction cost economics analysis. Health Policy and Planning, 28(2), 157–164. https://doi.org/10.1093/heapol/czs032

- Cevikparmak, S., Celik, H., Adana, S., Uvet, H., Sauser, B., & Nowicki, D. (2022). Scale development and validation of transaction cost economics typology for contracts: A systems thinking approach. Journal of Purchasing & Supply Management, 28(3), 100769. https://doi.org/10.1016/j.pursup.2022.100769

- Coase, R. H. (1937). The nature of the firm. Economica, 4(16), 386–405. https://doi.org/10.1111/j.1468-0335.1937.tb00002.x

- Coggan, A., Whitten, S. M., & Bennett, J. (2010). Influences of transaction costs in environmental policy. Ecological Economics, 69(9), 1777–1784. https://doi.org/10.1016/j.ecolecon.2010.04.015

- Coles, J., & Hesterly, W. S. (1998). The impact of firm-specific assets and the interaction of uncertainty: An examination of make or buy decisions in public and private hospitals. Journal of Economic Behavior and Organization, 36(3), 383–409. https://doi.org/10.1016/S0167-2681(98)00102-4