Abstract

Recently, there has been a growing concern regarding the impact of businesses on the environment and society and the pursuit of profit maximization. The current scenario has led to increased attention toward ESG disclosure and sustainability reporting and their probable impact on the performance of firms. Consequently, ESG disclosure and sustainability reporting have emerged as captivating subjects within corporate governance literature. Through a comprehensive review, this study aims to explore the current trends and patterns in sustainability reporting and ESG disclosure and their effects on firm performance. A dataset spanning 23 years (2000 to 2022) was compiled to conduct this analysis, comprising 656 scholarly publications obtained from the Web of Science. Utilizing the VOSViewer software, various bibliometric analyses were performed, including co-authorship, citation, cartography, and bibliographic coupling. The study’s findings indicate an average annual publication growth rate of 50.43% since 2010. However, despite this publication volume increase, most studies were conducted in developed countries like Italy, England, the USA, and China. The results of the keyword cluster analysis highlight sustainability and sustainability reporting as prominent research themes. In contrast, keywords like greenwashing and climate change were found to be less prevalent. Regarding the focus of the studies, the majority concentrated on analyzing the nexus between ESG disclosure, sustainability reporting, and firm performance regarding firm value and leverage, with a sizeable proportion exploring the impact of board diversity and gender diversity. The study also established a low link between sustainability reporting and firm performance.

1. Introduction

For decades, business environmental players like society, stakeholders, customers, and investors have expressed interest, demanding transparency from firms and organizations. As such, sustainability reporting has played a role in meeting environmental players’ transparency needs (Martínez et al., Citation2016; Nobanee et al., Citation2021; Sarpong et al., Citation2023). Whether required, voluntary, or solicited, disclosure of information relating to the environment, economics, and social impact of business activities is made possible through sustainability reporting and ESG disclosures. Sustainability reporting reduces information asymmetry, which helps increase transparency (Hamrouni et al., Citation2022; Nobanee & Ellili, Citation2016). As no man is an island, so are businesses. Businesses thrive in their existence by interacting with the environment and society. For the survival of businesses, environmental interactions are key in enabling self-sufficiency and reliance. To maximize sustainability regarding how businesses operate, adverse impacts such as harmful emissions, employee demoralization resulting from unfair treatment, and societal issues must be cut to the barest minimum. A firm’s performance would only be attributed to how effectively it minimizes such negative impacts (Utile, Citation2016). Due to changed awareness, societies have become more concerned about business sustainability (Burritt & Schaltegger, Citation2010). For most private and public firms, sustainability has been incorporated into management decisions, reporting, and accounting practices (Cebrián et al., Citation2013; Cobbinah et al., Citation2020; Osobajo et al., Citation2022; Sarpong et al., Citation2022).

The performance of firms over the last decades has been explained to denote the efficacy with which these firms utilize their limited resources to create value. Regarding value creation, firms endeavor to accrue sufficient returns while meeting the expectation of interested stakeholders (Brundtland, Citation1987). A firm’s performance can be viewed from financial or non-financial aspects. Considering these two measures of firm performance, Liu et al. (Citation2022) and Taouab and Issor (Citation2019) assert that firms that measure performance to include financial and non-financial operations have higher chances of survival and gain superior performance (Cobbinah et al., Citation2020). Firms with well-established structures for environmental sustainability are more likely to have their cost incurred offset by a decrease in their cost of capital. This presupposes that being socially responsible is a “product” sold to investors, which leads to increased returns. But there remains a query as to if this product is profit oriented. On the positive side, Gonçalves et al. (Citation2022) and Maama and Marimuthu (Citation2022) aver that the cost of capital is inversely proportional to the sustainability reporting score. Thus, considering this from the market standpoint, there is a favorable influence on the cost of capital for firms that adopt sustainable practices. On the far end, scholars like Mackey et al. (Citation2007) retort that the focus of investors is to maximize wealth at the expense of being sustainably responsible. They believe non-governmental organizations have to implement sustainability disclosure.

We are in a dispensation where investors consider not only financial reports of companies but also non-financial reports better to orient themselves in their choice of investment decision. Sustainability reporting, which breeds increased transparency, allows investors to make positive investment decisions (Arnold et al., Citation2012; Leins, Citation2020), which further translates into increased market power and competitive advantage. There is no denying that firms need to be legitimized and socially accepted to succeed. This can be achieved through social commitment and sustainability in their behavior (Hahn & Kühnen, Citation2013).

Unlike financial reporting, which thrives on generally accepted standards and frameworks, there has not been any universal standard for reporting sustainability. For firms that publish stand-alone reports, Global Reporting Initiatives (GRI’s) are generally put into use (Jørgensen et al., Citation2022; Sappor et al., Citation2023). Different bodies have come out with diverse sustainability reporting standards. According to Brown et al. (Citation2009), the most widely accepted and used standard comes from the Global Reporting Initiative’s (GRI’s) reporting standard. The Integrated Reporting Framework, developed by the International Integrated Reporting Council (IIRC) in the year 2012, sets out to present an in-depth organizational view through the alignment of strategies, performance, and business models, both environmental and social issues. Despite shareholders being the focus group the IR addresses, certain vital information regarding the organization’s impact on other interested parties has also been considered. It is no surprise that Deloitte in 2014 reports engagement with stakeholders among the essentials of the process involved in integrated reporting.

The introduction of the Sustainable Development Goals (SDGs) by the United Nations in 2015, aimed at achieving sustainable development by 2030, was a step further in the global sustainability agenda. Such allowed corporate organizations to operate toward a more sustainable world. The collaborative initiative between the GRI and the United Nations Global Compact (UNGC) 2018 permitted firms to include SDGs in their existing reporting and operation process. To succeed both in the short and long term and achieve SDGs in diverse fields, the degree to which firms contribute to achieving SDGs is vital (Agarwal et al., Citation2017; Moldavska & Welo, Citation2019). Based on the study of Majid et al. (Citation2022), when firms report on SDGs, it exhibits their willingness to commit to tackling sustainable development issues like changes in climate as affirmed in the Kyoto Protocol, poverty, and degradation of the environment.

Over the years, the ecosystem has experienced tremendous negative change resulting from the activities of businesses. This has resulted in the need to preserve the ecosystem while being concerned about global environmental issues, making sustainability reporting an essential developmental area in accounting in all economies across the globe and arousing much attention to research (Hahn & Kühnen, Citation2013; Tiscini et al., Citation2022). As a result, many studies have been done on the elements that motivate adopting new sustainability practices in their end-of-year annual reporting (Dissanayake et al., Citation2019; García‐Sánchez et al., Citation2022). In furtherance, other extant literature has explored how external assurance adoption of reporting on sustainability makes the disclosed information more transparent to boost stakeholders’ confidence (Girón et al., Citation2022; Yan et al., Citation2022).

Moreover, there have been complexities regarding various approaches used in examining sustainability reporting issues and their effect on firms’ performance. Studies on this nexus have elucidated inconclusive results, while most focus on developed countries. To explore whether sustainability reporting is performance-driven or corporate social responsibility driven, this paper analyses research trajectories by characterizing the features of studies published on sustainability reporting and firms’ performance from 2000 to 2022.

This paper summarizes past, present and forward-looking studies on sustainability reporting and firm performance. This study contributes innovative insights into investigating the relationship between sustainability reporting and firm performance through corporate social responsibility. This study adopted bibliometric analysis using 23 years dataset from the Web of Science database to uncover previously unknown trends and patterns in sustainability reporting and firm performance. Based on the findings from this study, there appears to be a high link between sustainability reporting and firm performance. This suggests that sustainability reporting necessarily results in improved financial performance for firms.

Furthermore, this study also found a strong link between sustainability reporting and corporate social responsibility. Therefore, highlighting the importance of firms’ ethical and social responsibilities in their sustainability reporting practices is an important area for researchers to consider and perhaps conduct extended studies to investigate and discover new drivers of sustainability reporting. This can lead to more effective regulations and policies encouraging sustainable business practices.

Moreover, this study also contributed to demonstrating the effectiveness of bibliometric analysis methodology in analyzing sustainability reporting and firm performance literature. This study, therefore, continues to set the pace for other researchers to adopt a similar methodology in their works leading to more rigorous and comprehensive analyses of sustainability reporting and firm performance. This study further calls for more research that bridges regional disparities in sustainability reporting leading to comparative analyses of sustainability reporting practices across different regions of the world. This can give researchers a better understanding of the factors that influence sustainability reporting practices and their impact on firm performance in different parts of the world. Unlike other related studies, this paper highlights the most impactful and notable prior studies to provide a comprehensive overview. Furthermore, the bibliometric review examined the questions below:

What are the most influential articles on sustainability reporting and firm performance?

What popular topics have been researched on sustainability reporting and firm performance?

What is the collaboration status on sustainability reporting and firm performance?

Is firm performance boost a primary concern for sustainability reporting?

The rest of the study is organized as follows: section 2 contains the literature review, section 3 comprises data and methodology, and Section 5 depicts the bibliometric results. The discussion and conclusion are shown in sections 6 and 6, respectively, and section 7 finally gives the limitations and future research directions.

2. Literature review

ESG (Environmental, Social, and Governance) and sustainability are two interconnected concepts that have gained significant attention in recent years, driven by the need to address pressing global challenges and promote responsible business practices. ESG issues involve the integration of all aspects of the sustainable development concept, which includes equitable distribution of resources, preservation of the environment, and economic growth (Wan et al., Citation2023) into the company’s business models to achieve business objectives (Gillan et al., Citation2021). ESG integration can lead to better risk-adjusted returns and lower volatility (Albuquerque et al., Citation2019; Friede et al., Citation2015), more diverse investors (El Ghoul et al., Citation2011), reduced capital costs (Hong & Kacperczyk, Citation2009) and better financial performance in both developed and emerging markets (Ahmad et al., Citation2021).

ESG factors represent a framework for evaluating companies’ or investments’ sustainability and ethical impact, with each component playing a distinct role. The environmental component of ESG considers a company’s impact on the natural environment, including resource use, pollution, and climate change. The social element of ESG considers a company’s impact on society, including labor practices, human rights, and community relations. The governance component of ESG considers a company’s management structure and practices, including factors such as board composition, executive compensation, and shareholder rights.

The ESG issues were founded on promoting peaceful cohabitation between humans and nature (Wan & Dawod, Citation2022). ESG serves as the standardized criteria for assessing a business’s performance in terms of how it affects the environment, society, and corporate governance and its overall quality (Alda, Citation2021). The ESG concept, an expansion of corporate social responsibility (CSR), has developed into an essential competitive strategy that ensures business survival and aids in building a company’s reputation. Shin et al. (Citation2023) established a connection between ESG and CSR and argued that CSR includes organizational policies that consider stakeholders’ expectations and the three components of ESG.

In recent years, incorporating ESG considerations into company decision-making and disclosing a company’s ESG performance to stakeholders has become very important to companies (Lokuwaduge & Heenetigala, Citation2017). Businesses adopt various ESG frameworks and standards to disclose their ESG performance, and they include; the Sustainability Accounting Standards Board (SASB), the International Integrated Reporting Council (IIRC) framework, the UN (Global Compact), Principles for Responsible Investment (PRI), United Nations Sustainable Development Goals (SDGs) and Global Reporting Initiative (GRI) framework.

On the other hand, sustainability is a broader concept encompassing ESG factors but extends beyond the financial and investment realm. Brundtland (Citation1987) believes that sustainability aims at fulfilling the present generation’s needs without jeopardizing the future generation’s capacity to fulfill their own needs while reporting denotes the partial or full disclosure of a firm’s information to all interested stakeholders. Hence by blending these two concepts, we arrive at sustainability reporting, which has been explained in a similar broad context by a wide spectrum of scholars. At the corporate level, Porter and Kramer (Citation2006) view sustainability reporting as meeting an organization’s stakeholders’ needs while having future concerns at heart. When firms integrate their annual reporting in social, economic, and environmental areas into their year-end corporate reporting, such practice constitutes sustainability reporting (Elkington, Citation2013). In addition, Hanh et al. (Citation2014) explains sustainability reporting as comprising a series of activities undertaken by organizations that creates a piece of evidence that the business incorporates social and environmental issues into their corporate operations and dealings with stakeholders. Sustainability reporting as a concept began to surface during the early days of 1980 when reports on the environment sprang up (Aifuwa, Citation2020). Having experienced a decade of transformational upgrades, sustainability reporting started with reporting on employees, to social and environmental reporting, and to report on the triple bottom line (Joseph, Citation2010). The three broad pillars of sustainability, social, environmental, and economic, have produced the “triple bottom line concept.” Over the past decades, sustainability reporting has been widely accepted by organizations across the globe, while a majority of these firms mainly emanated from developed countries and few from developing countries (South Africa being the most notable) (Shad et al., Citation2019).

On the contrary, Cooper and Michelon (Citation2022) and Oncioiu et al. (Citation2020) reiterate that regarding sustainability reporting acceptance, the opposite is said of less developed nations, like West African countries. In 2017, KMPG reported that out of the world’s renowned companies, 90 % of these companies practice sustainability reporting. In addition, Székely and Vom Brocke (Citation2017) aver in their studies that the sustainability reporting rate differs from company to company. They further expound that food and beverage, chemicals, automobiles, and oil and gas firms engage in sustainability reporting more than service, financial, and media firms. Investors, communities, regulators, employees, consumers, and many other important stakeholders are monitoring a company’s sustainability reporting of ESG operations more than ever.

Sustainability reporting and ESG disclosure have recently been considered a firm’s financial performance driver. This has increased studies on ESG disclosure, sustainability reporting, and financial performance nexus, particularly the motivational factor for voluntary reporting. For broader scope of analysis on this nexus, the study of Christensen et al. (Citation2021) presented a thorough literature on the study domain. Quite an appreciable number of scholars have concluded that reporting on sustainability and disclosing ESGs positively influences a firm’s performance. Firm performance invariable is measured by a range of proxies, including profitability (earnings per share, returns on asset, returns on equity), firm size (total assets), market-based proxies (share price of the market), and profit before tax (Delen et al., Citation2013; Dhaliwal et al., Citation2011; Oliver, Citation2013).

Dhaliwal et al. (Citation2011) reveal that firms that previously increased their cost of equity capital are most likely to engage in sustainability reporting and ESG disclosure in the current year. They further explain that these firms enjoy a reduced cost of equity capital when social responsibility performance is at a maximum. Firms are hence likely to exploit these benefits. A firm’s value is also considered to be influenced by sustainability reporting. Among the studies on how firm value is influenced by sustainability reporting, Yu and Zhao (Citation2015) identified two competing theories that justify how firm value is affected by sustainability, namely, value-destroying and value creation theory. Value destroying theory argues that sustainability activities are undertaken at the detriment of shareholders, whereas value increasing theory aims at risk reduction and enhancing firm value. According to Yu and Zhao (Citation2015), the capital market incentivizes the adoption of sustainability activities giving credence to the value-creating theory.

The legitimacy and stakeholder theories also explain the positive link between sustainability reporting and firm performance. Previous research has shown that ESG ratings are a quantitative tool to evaluate stakeholder satisfaction. Additionally, they can offer a competitive advantage by mitigating risks and improving financial and market performance. By establishing legitimacy for business activities and enhancing the liquidity of associated stocks, ESG ratings contribute to the overall success of companies (Li et al., Citation2022). Legitimacy theory goes beyond the goal of economic profits and speaks about value creation. Its deliberate implementation considers social activities as a means of demonstrating that their corporate action is legitimate and is in line with the norms of good citizenship. Esen (Citation2013) reports that a firm’s corporate reputation is enhanced when its sustainability reporting is high. This stems from the fact that sustainability reporting aids in meeting the information needs of stakeholders. The study of Odriozola and Baraibar‐Diez (Citation2017) also supports the assertion.

On the contrary, other studies exhibit a reverse link between sustainability and firm performance. The study of Axjonow et al. (Citation2018) establishes no reputational relationship within the terrain of non-professional stakeholders, even when firms embark on sustainability activities. In their research, Uwuigbe et al. (Citation2018) observed that market share prices exhibit an inverse relationship with sustainability reporting. In neutrality, Adams et al. (Citation2012) and Taiwo et al. (Citation2021) established from their respective studies that no association exists between sustainability reporting and firm performance. Their argument suggested that positive or negative connections result from inadequate empirical research that overlooks crucial control variables. Since sustainability reporting has become a fundamental factor influencing the decision-making processes of investors and other stakeholders, especially concerning investments and returns, this study aims to comprehensively investigate the relationship between sustainability reporting and firm performance within a broader review context. The goal is to shed light on the intricate nexus between sustainability reporting, encompassing ESG disclosure, and the performance of firms.

3. Data and methodology

3.1. Database source

Being an inclusive database, we used the Web of Science, a legitimate and dependable source, to undertake bibliometric analysis. With over 15,000 impactful global journals, the Web of Science database has international readers’ recognition with worldwide interdisciplinary integration (Guan & Ma, Citation2004). The Web of Science is enriched with accumulated data and does not give preference to publishers during data searches (Cohen, Citation2017; Harsanto & Firmansyah, Citation2023).

3.2. Inclusion and exclusion search criteria

To obtain the relevant number of papers on sustainability reporting and firm financial performance, past research articles were reviewed to get insight into the subject matter adequately. Since sustainability and ESG are interrelated, topical keywords related to this regard were sourced from various documents. The inclusion and exclusion criteria process are as follows;

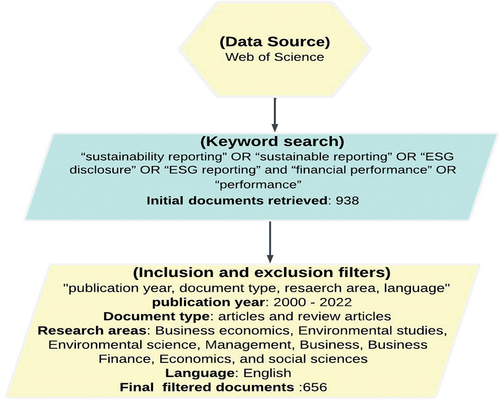

First, the study through the Web of Science database employed the topic search by utilizing the strings “sustainability reporting” OR “sustainable reporting” OR “ESG disclosure” OR “ESG reporting” and “financial performance” OR “performance.” This first search yielded a total of 938 documents. As these documents might have contained several others not directly related to our research focus, several exclusion criteria were applied to filter the initial documents.

In an orderly sequence, the second data filtering stage was done by year, document type, research area, and language. The search strategies were confined to ”2022, articles, review articles, business economics, environmental studies, environmental science, management, business, business finance, economics, social science, and English in those strings, respectively. Through this rigorous process, we arrived at 656 articles to be used for the bibliometric analysis. These processes took place on the 10th of May, 2023. Figure shows a pictorial walkway through the process.

Figure 1. Inclusion and exclusion criteria.

4. Methodology

Both meta-analysis and literature analysis are two unique approaches often employed in reviewing research studies. While meta-analysis is a quantitative method that combines and analyzes data from multiple studies, Literature analysis may involve qualitative or quantitative methods, or a combination of both, and typically aims to provide a comprehensive overview of existing research on a particular topic. The literature analysis was preferred over the meta-analysis as it includes various types of studies, be it case studies, theoretical research work, or qualitative studies, which otherwise may not be suitable to be included in the meta-analysis. Also, literature analysis allows for exploring contextual factors, such as historical or cultural influences, that may impact the research topic. It will enable researchers to consider the broader social, economic, or political context that may affect the findings or interpretations of individual studies.

Furthermore, the Literature analysis is flexible and adaptable to various research contexts and topics. It does not require strict adherence to predetermined statistical criteria or the availability of quantitative data, making it applicable to fields where quantitative data synthesis may not be feasible or appropriate. While meta-analysis has advantages, such as providing quantitative estimates of effect sizes and statistical power, literature analysis offers a more comprehensive and nuanced exploration of the existing literature, enabling researchers to address broader research questions and contextual factors.

We employed the bibliometric and systematic literature review approach encapsulating the qualitative and quantitative scope of literature (Alhossini et al., Citation2021; Lu et al., Citation2022) to assess publications on sustainability reporting and firm performance. Systematic review enhances the transparency of the study. Several other researchers have employed both approaches in similar studies ((Ibrahim et al., Citation2022; Nguyen et al., Citation2020). Bibliometric entails a scientific metric analysis of dominant articles published through mapping. The mapping aims to identify trends, gaps, and forward-looking issues in prior literature. Following the works of Bartolacci et al. (Citation2020) and (Effah et al., Citation2022), we categorize our analysis into four thematic blocks, namely, (1) bibliometric co-authorship analysis, (2) bibliometric citation analysis, (3) keyword/cartography analysis (4) bibliographic coupling analysis.

To ascertain the link between authors and their articles, the VOSViewer software was adopted for visualizing the bibliometric analysis (Antwi et al., Citation2022). Using the VOSViewer creates the space for examining bibliometric mapping in full. The VOS viewer’s viewing capabilities are notably beneficial for maps with at least a relatively significant number of elements. In addition, Vallaster et al. (Citation2019) state that VOSViewer makes prior and present literature comparisons very efficiently to reveal how particular research fields are developing. The current study uses bibliometric analysis to find the primary authors, the most significant keywords, citation and co-citation analysis, publishing sources, and country distribution analysis.

5. Mainresults

This section presents the results of the bibliometric analysis based on the four thematic blocks, namely;(1) bibliometric co-authorship analysis, (2) bibliometric citation analysis, (3) keyword/cartography analysis (4) bibliographic coupling analysis.

5.1. Number of publications

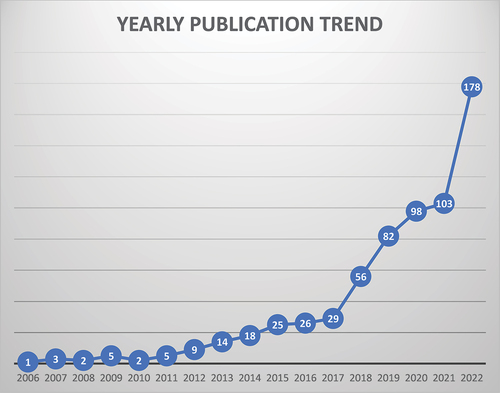

In academia, the development of research interest is mainly identified by the volume of published works. Figure depicts the total volume of publications annually that center on sustainability reporting, ESG disclosure, and firm performance. These publications also cover specific areas of corporate social responsibility and environmental, social, and governance disclosure. Beginning in 2011, the number of yearly publications has witnessed a marginal increase, with 2022 recording the highest publication of 178. From these figures, the authors are optimistic that yearly publications will continue to rise in the coming years. From 2017 to 2018, yearly publications almost doubled (from 29 to 56), raising a positive concern. The publications declined twice, one in 2008 and the other in 2010. However, these declines are considered insignificant compared to the marginal rise of the remaining years. Attributing the growth phases of a research domain to our current study, the authors argue that the present study is in the second phase, thus, the proper exponential growth stage. According to Dabi et al. (Citation2016), the proper exponential growth phase is where an increasing number of scientists are attracted to the many facets of the subject yet to be explored. Overall, it is evident that issues of ESG and sustainability have higher recognition, with various themes still unearthing.

Figure 2. Yearly literature growth.

5.2. Authorship analysis

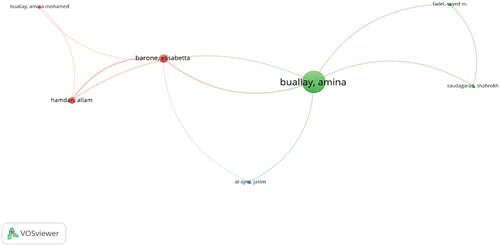

Comparable to other bibliometric research, we employed the VOSviewer to perform an authorship analysis to depict the list of authors who have exhibited significant influence in sustainability reporting, ESG disclosure, and firm performance studies. This analysis identifies each author to the number of articles published on the study topic. The top three contributing authors include Buallay Amina, Uyar Ali, and Karaman Abdullah S. Table lists the top 15 dominant authors. Buallay Amina remains on top of the list with 13 documents with 404 citations. The citations express the number of times articles on sustainability reporting, ESG disclosure, and performance have been cited by other Web of Science database articles. Ranked eleventh productive author in terms of published documents, Boiral Olivier recorded the highest citation of 558.

Table 1. Top 15 dominant authors

It is worth noting that older publications tend to have a higher probability of being cited than more recent publications. One potential explanation for this phenomenon is that, among various factors, the authors who have been most prolific during the 23-year analysis period may not necessarily be the most frequently cited. While Smith (Citation2007) argues that the number of citations reflects the quality and influence of an article, Whipple et al. (Citation2013) also aver that mostly, open access journals have higher chances of being cited due to their easy readability. The expansion of existing knowledge could also be achieved through collaborations. Usually, the co-occurrence between two or more authors is identified by their link strength. Figure highlights the co-authorship network visualization. Following the works of M. A. Khan (Citation2022), we set the following criteria for the co-authorship network visualization;

Figure 3. Co-authorship visualization.

The author’s minimum number of citations is 10

The author’s minimum number of documents is 2

By employing the set criteria on a total of 1583 authors from our sample, only 169 met the requirements, as seen in Figure . Authors having no connection with each other are excluded from the visualization. The size of the circular nodes corresponds with the number of articles, whereas the lines connecting the nodes show co-authorship collaborations. The colors depict the collaboration clusters. Figure identifies only 3 clusters with 10 links concerning our research topic. Both green and red clusters have the same number of reference items (3), with green having the highest link. The network visualization appears to be dominated by quite a sizeable number of researchers. Buallay Amina happens to be the only author amongst the top 15 influential authors.

5.3. Country activity analysis

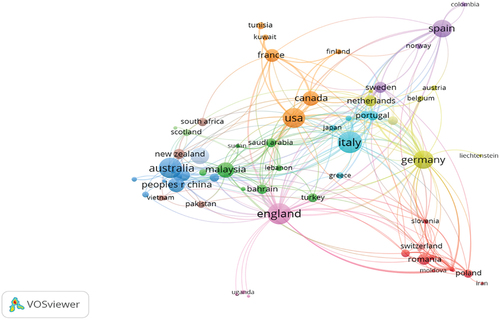

The study assigned total publications to countries to allow for further analysis of the subject matter. The findings reveal 71 countries affiliated with the study’s 656 articles. Among these countries, the top 10 in the list are shown in Table . Italy tops the chart with the highest publication of 73, followed by England and Australia with 69 and 64 publications, respectively. Although Canada ranks 8th with only 33 publications, it is regarded as the country with the third most citation, even ahead of Italy, which has the highest number of publications.

Table 2. Top 10 country publication dominance

Figure depicts the visualization of the network of countries that relates to this field of study and the link between countries. The most significant node represents countries with the higher co-authorship link, with Italy, Australia, and England being the top three. The study’s network visualization of country co-authorship validates Liao et al. (Citation2018) assertion that country closeness does not connote co-authorship advantage, For instance, between France and Germany. The dominance of European countries on ESG and sustainability reporting and performance is attributed to how industrialization continues to trigger environmental quality. Also, the availability of many top-class world universities engaged in innovative research endeavors could account for the higher publication from the top 10 countries. In particular, China has invested many resources into ESG and sustainability research over the last decade.

Figure 4. Country co-authorship visualization.

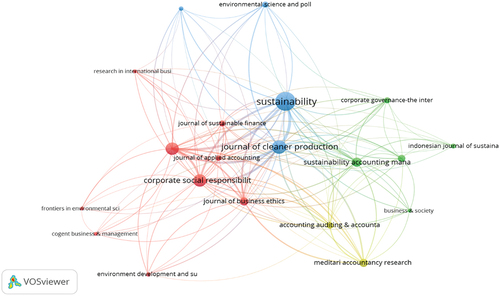

5.4. Most cited and highest published journals

Following the mapping criteria restriction of 5 maximum documents and 10 maximum citations, a total of 20 highly impactful journals were patronized by the various authors between the year 2000 to 2022. A journal’s citation is related directly to the specific articles published in the Journal. Thus, the corresponding Journal gets the same for every article’s citation. A network mapping was done from 656 documents, as shown in Figure . The largest node is “Sustainability,” with the highest publication of 97 documents, followed by “Corporate social responsibility and environmental management journal,” with 52 documents. Regardless, the “Journal of cleaner production” is the most influential, with the most citations (4291). The network mapping also identified four clusters showing how journals in the clusters cited each other. Cluster one consisted of the highest number of journals, namely, “business strategy and the Environment,” “cogent business & Management,” “corporate social responsibility and environmental management,” “Environment, “Development and Sustainability,” “Frontiers in Environmental science,” “journal of applied accounting research,” “journal of business ethics,” “Journal of sustainable finance and investment,” and “research in international business and finance.” These mainly relate to the management, finance, accounting, economics, and social sciences discipline. A deeper analysis corresponds the journals to top-tier publishing houses like Wiley, Springer, Taylor and Francis, Elsevier, and emerald group. Table shows the top 10 journals using their number of publications to order their positioning on the table.

Figure 5. Network visualization of top journals.

Table 3. Top 10 Journals with the most citations and publications

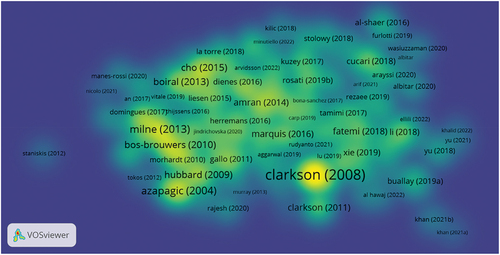

5.5. Literature citation analysis

In bibliometric review studies, citation analysis remains among the most employed techniques (A. Khan et al., Citation2022). Citation analysis is regarded as a quantitative tool for evaluating a discipline, a topic, an author, or a journal based on their total generated citations. Most cited documents are associated with having an influence level high above less cited one. A minimum of 10 citations per article was used as a criterion in VOSviewer. The VOSviewer criteria yielded 352 most cited documents. Among these documents, we identified the study of Clarkson et al. (Citation2008), titled “Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis,” as a highly cited document with 1390 citations.

The second most cited article was the paper by Azapagic (Citation2004) titled “Developing a framework for sustainable development indicators for the mining and minerals industry,” which received 567 citations. With 530 citations were the works of Milne and Gray (Citation2013) titled, “W(h)ither Ecology? The Triple Bottom Line, the Global Reporting Initiative, and Corporate Sustainability Reporting”. The rest of the documents all have a substantial number of citations to contributively address ESG disclosure, sustainability reporting, and firm performance research. Table summarizes the top 10 most cited articles on the subject matter. Concerning journals, 3 of these top 10 cited articles were published in the Journal of cleaner production and 2 in Business Strategy and the Environment.

Table 4. Top 15 cited articles

Figure shows the density visualization for the most cited works. Clarkson et al. (Citation2008) show the densest, connoting the highest citation.

Figure 6. Density visualization of most cited literature.

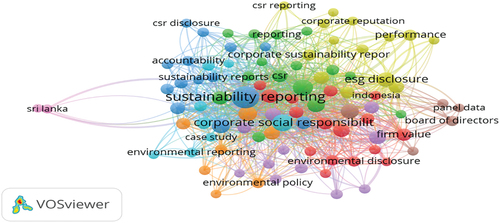

5.6. Cartography analysis

Chen et al. (Citation2021) believe that keywords reflect a particular topic in a specified discipline. To better appreciate the literature on ESG disclosure, sustainability reporting, and firm performance, visualization analysis for the most occurring keywords was done by setting the criteria for the minimum occurrence to 5. Sustainability reporting, corporate social responsibility, ESG disclosure, corporate governance, and global reporting initiative are among the notable keywords discovered through the search, as shown in Figure . These keywords have been concerning the subject matter for the past 23 years. Sustainability reporting has been the most used keyword by authors, appearing 267 times. The second most frequently used is corporate social responsibility, with 79 appearances. Table provides a summary of the top 15 keywords that have been used often on the subject of sustainability reporting, ESG disclosure, and firm performance. It is not a surprise that these two top the most appeared keyword. Due to the pace of industrialization expansion, the quest for multinational companies to be socially responsible is increasing alarmingly. Also, reporting on how companies contribute to sustainability has become necessary in keeping up with being socially responsible, fueling its highest occurrence. From the result of Figure , the keyword co-occurrence generated 6 clusters, namely, cluster 1 (red); sustainability, cluster 2 (green); sustainability reporting, cluster 3 (blue); financial performance, cluster 4 (yellow); global reporting initiative, cluster 5 (purple); gri, and cluster 6 (sky blue); corporate social responsibility. Below provides a summary of each of the clustered themes:

Figure 7. Authors keywords co-occurrence.

Table 5. Top 15 authors’ keywords

5.6.1. Cluster 1 and 2: sustainability and sustainability reporting

Cluster 1 is concerned with sustainability, having an occurrence of 75, 40 links, and total link strength of 70, whereas cluster 2 is concerned with sustainability reporting, having 48 links and 200 total link strength. Other keywords included in both clusters are board of directors, disclosure, corporate governance, environmental, ESG, ESG disclosure, ESG performance, ESG reporting, firm value, governance, social, corporate reporting, corporate sustainability, global reporting initiative, greenwashing, institutional theory, legitimacy theory, integrated reporting, non-financial reporting, reporting, stakeholder theory, sustainability indicators, and performance. Studies under the clusters focus on the diverse aspect of sustainability, including how ESG disclosure, particularly ESG scores, impact performance with a strong association with firm value, firm size, and age (Abdi et al., Citation2022) from the perspective of employees and community aspects of sustainability (Lawal et al., Citation2017), also the stakeholder theory (Schreck & Raithel, Citation2018), board diversity (Manita et al., Citation2018), board role performance (Tumwebaze et al., Citation2022) influencing ESG disclosure was significantly disclosed. These generate a competitive advantage for firm performance enhancement. Again, we discovered that applying the legitimacy theory resulted in a negative relationship between ESG disclosure and the cost of capital (Kumawat & Patel, Citation2022). In furtherance, the studies of Kumar et al. (Citation2022) identify the management of natural resources, social investments, emissions of greenhouse gasses, and energy as top-ranked sustainability indicators.

5.6.2. Cluster 3 and 4: financial performance and global reporting initiative

Cluster 3 is centered around financial performance, with 29 appearances, 25 links, and total link strength of 24. Cluster 4, on the other hand, is concerned with a global reporting initiative with 37 occurrences, 29 links, and 37 link strengths. Other keywords within these clusters include; environmental disclosure, environmental performance, environmental policy, stakeholder engagement, sustainability disclosure, sustainability report, accountability, board gender diversity, content analysis, corporate sustainability, firm performance, and stakeholders. Under these clusters

Scholars have given much attention to the financial performance aspects of sustainability and environmental disclosure, where being socially responsible connotes a high degree of accountability as influenced by the new European Union Directive 2014/95 on non-financial and diversity information (La Torre et al., Citation2018), compliance with global reporting initiatives (Laskar & Gopal Maji, Citation2018), the mixed impact of female board of director on ESG disclosure (Manita et al., Citation2018). On stakeholder engagement (Manning et al., Citation2019), identify it as an essential corporate governance mechanism positively related to sustainability reporting quality.

5.6.3. Cluster 5 and 6: GRI and corporate social responsibility

Cluster 5 is concerned with GRI having an occurrence of 30, links of 30, and total link strength of 28, whereas cluster 2 is concerned with corporate social responsibility, having 42 links and 71 total link strength. Assurance, CSR, information asymmetry, non-financial information, sustainable development goals, sustainable development, SDGs, and voluntary are the remaining keywords of both clusters. Regarding these clusters, studies have examined how board size and leverage affect the probability of having external assurance for the firms’ sustainability reports and how the Content Index Model improves the credibility of the assurance processes for GRI sustainability reports (Mori Junior & Best, Citation2017). Findings have disclosed that achieving sustainable goals becomes easy when firms engage in voluntary assurance (Misiuda & Lachmann, Citation2022). In countries like Norway, results have revealed unsatisfactory non-financial reports amidst a voluntary disclosure environment. Further, studies have examined the impact of ESG disclosure in reducing information asymmetry to create long-term value for investors (Mulchandani et al., Citation2022). Others disagree that ESD disclosure reduces information asymmetry (Hassani & Bahini, Citation2022).

6. Discussion

This study aims to evaluate trends and patterns of scholarly publications in ESG disclosure, sustainability reporting, and firm performance through bibliometric analysis. The finding from the yearly publication analysis demonstrates the studies in the domain of ESG disclosure, sustainability reporting, and firm performance is on the rise, with an average annual growth rate of 50.43% beginning the year 2010 due to the growing concern for environmental quality (Upadhyay & Kumar, Citation2020) by various international organizations. The tremendous growth signifies the decade’s demand for research on the subject. The growth trend suggests research on ESG disclosure and sustainability reporting will continue to increase even in the coming years, as inferred from the proper exponential growth stage identified by (de Solla Price, Citation1963). Among the list of 656 articles reviewed, it was determined that the studies undertaken by Azapagic (Citation2004), Clarkson et al. (Citation2008), and Milne and Gray (Citation2013) were the most impactful, as evidenced by their total citations and related journal source. The findings from these studies have set the ball rolling for further studies on the ESG disclosure, sustainability reporting, and firm performance nexus and the adoption of the global reporting initiative guidelines for sustainability reporting.

Among the highly impacted journals, sustainability received the highest number of publications. Most journal publications on sustainability over the years have welcomed studies within the scope of environmental quality addressing corporate social responsibility issues. Others like the Journal of cleaner production, corporate social responsibility, and Journal of business ethics, among others, have been identified by our studies. The predominance of these journals and their impact factor have accelerated the publication growth of the ESG disclosure, sustainability reporting, and firm performance nexus. Buallay, Uyar, and Karaman were identified from our analysis as the authors with the most documents, thus 13, 10, and 7, respectively. The author collaboration results, however, reveal a limited number of collaborations, even from the topmost prominent authors. Buallay remains the only author within the top 15 who has received collaborations from other authors in this research domain.

The country activity analysis also demonstrated about 90% of identified authors hailed from developed countries, of which the continent of Europe had the most significant number. Italy, a European country, recorded the highest number of publications. England, France, Spain, Germany, Canada, and Australia are among the countries that our analysis revealed. Asian countries such as China, India, Malaysia, and Indonesia have also contributed to this research domain. However, country collaborations were mostly limited to developed countries like the USA, Canada, Italy, Germany, France, Australia, England, and Spain. Europe has been at the forefront of developing regulations and frameworks for ESG disclosure and sustainability reporting. The European Union, for instance, has implemented directives such as the Non-Financial Reporting Directive and the Sustainable Finance Disclosure Regulation, which have encouraged research and reporting in these areas. Such regulations provide a conducive environment for scholars and researchers to investigate and analyze the impact of ESG disclosure and sustainability on firm performance.

Again, the cartography analysis uncovers interesting findings about ESG disclosure, sustainability reporting, and firm performance nexus. Our keyword visualization analysis identified 6 clusters, each having a unique importance. Sustainability, sustainability reporting, corporate social responsibility, financial performance, and global reporting initiative were all regarded as the major terms having evolved from this study, with varied centrality and impact. Environmental policy, firm value, accountability, climate change, developing country, and greenwashing have also evolved as minor terms. Taking into consideration the need to be socially responsible while at the same time maximizing profit, businesses concerned about finding a break-even between the two have fueled scholarly attention to ESG disclosure, sustainability reporting, and firm performance research (Zarefar et al., Citation2022). Research has highlighted board gender diversity as having the ability to influence a company’s ESG disclosure. Mostly, female-dominant board members are noted to be socially responsible and embark on CSR and report on it (Buallay et al., Citation2022). Our empirical findings suggest that regulators should consider implementing quotas for female participation on bank boards to promote sustainable improvements in the extent of ESG reporting. Leverage and firm value have mostly been employed as control variables in research investigating the determinants of ESG performance. Ownership structure, also a determinant of ESG performance, was seen to be understudied. Among the studies that have considered the influence of ownership structure on ESG disclosure, Existing literature has shed light on the significance of institutional shareholding (Coluccia et al., Citation2018). Yet, a need remains to examine the behavior of privately owned or closely held firms to gain a deeper understanding of their dynamics.

As a minor term, mining is associated with related climate change issues. Studies have pointed out climate-related disclosure to demonstrate how mining companies protect the environment in which they operate. The financial stability board of G-20 nations has established the Taskforce on Climate-related Financial Disclosure (TCFD), which has been used as a disclosure basis by most energy and mineral firms. The institutional, legitimacy, and stakeholders’ theories have also been identified. The stakeholder theory has been chiefly used as a theoretical base for ESG disclosure and sustainability reporting research. Prior studies have demonstrated that ESG ratings serve as a quantitative instrument for assessing stakeholder satisfaction and can provide a competitive edge by mitigating risks and enhancing financial and market performance by establishing legitimacy for business activities and improving the liquidity of associated stocks (Li et al., Citation2022). The institutional theory views organizations as interconnected with society, thereby linking corporate CSR and other accounting practices to the standards and values upheld by that society. The theory is extensively employed by researchers in the sustainability field to comprehend the connection between socially responsible movements and institutional change in corporate social responsibility (Avetisyan & Hockerts, Citation2017). It aids in identifying the factors influencing ESG performance and is also applied in integrated reporting (Tamimi & Sebastianelli, Citation2017).

7. Conclusion

Primarily, our study used 656 articles from the Web of Science database between the years 2000 to 2022. Network visualization based on knowledge of sustainability reporting, ESG disclosure, and performance was done using VOSviewer software to identify research trends and patterns. The visualization aided in identifying the number of yearly publications, dominant authors, country’s contributions, keyword densities, most cited journals, and most cited documents. The study further identified prior literature gaps. The yearly publication growth has increased in the volumes of papers published on ESG disclosure, sustainability reporting, and firm performance nexus. This is not surprising as governments and regulatory bodies worldwide are implementing stricter reporting requirements and disclosure standards related to ESG factors. These regulations require research to understand the implications and effectiveness of such reporting frameworks.

Among the journals in which the sample articles were published, we discovered majorly related to the scope of corporate governance, environmental quality, and climate change. Although the identified journals have a proven record of influence and impact as the paper goes through a strict review process to be approved of its originality, innovativeness, and marginal contributions, expansion could be made to other journals of an equally higher impact that share and offer limited scope to the subject domain. We believe this will expand the readability of this research domain for a more significant impact. Regarding the most influential authors and contributing articles, it was evident that studies focusing on ESG disclosure, sustainability reporting, and firm performance nexus garnered significant attention regarding publication numbers and total citations.

The outcome of the country activity analysis has revealed developed countries as being at the forefront regarding research on ESG disclosure, sustainability reporting, and firm performance. This draws attention for researchers to try and focus on developing economies. Developing nations might have less developed or enforceable regulations related to ESG disclosure, making it less of a priority for researchers and businesses. Without strong regulatory frameworks, there may be less motivation for companies to disclose ESG information, leading to a limited focus on researching its impact on firm performance.

From the cartography analysis, the six major terms center on how being socially responsible through reporting could provide a competitive advantage to enhance firm performance. This highlight concerns regarding the inconclusive findings on these relationships, as several business categorizations have yet to test this hypothesis. Also, consider the less attention greenwashing has gained in the research domain and how it could mislead consumers into purchasing based on false or exaggerated environmental claims. Research can help uncover such deceptive practices, enabling regulators and consumer protection agencies to act appropriately and safeguard consumers from misleading information. In summary, this bibliometric analysis provides insight regarding the relationship between ESG disclosure, sustainability reporting, and firm performance as follows;

Growing publication: There is a noticeable increase in publications focusing on ESG disclosure, sustainability reporting, and firm performance.

Emerging themes: Distinct themes are beginning to emerge within the research on ESG disclosure, sustainability reporting, and firm performance, indicating a more defined direction in studying this area.

Geographic Dispersion: Publications on ESG disclosure, sustainability reporting, and firm performance are geographically dispersed, suggesting a global interest in understanding and exploring this subject, although minimal research has been undertaken in developing countries.

Journal Focus: Journals dedicated to corporate governance, environmental quality, social responsibility, and climate change contribute to the literature on this topic.

Limited Collaboration: The analysis reveals a lack of collaborative research among scholars in ESG disclosure, sustainability reporting, and firm performance, indicating an opportunity for more interdisciplinary and collaborative efforts.

8. Limitations and future research directions

Although bibliometric analysis offers a broad range of insights for exploring sustainability reporting trends and firm performance, some limitations remain. First, the study’s reliance on the Web of Science database alone may have excluded many valuable publications that could have contributed to the research. To enhance trend analysis’s comprehensiveness, we recommend that future studies extend the database to include sources such as Scopus, ScienceDirect, and Google Scholar. Nonetheless, the study’s findings remain valid within the context of the utilized database.

Regarding review-based approaches in ESG disclosure and sustainability reporting, most reviews have typically employed either a bibliometric approach or a traditional systematic literature review. However, meta-analysis, commonly applied in the medical field to consolidate clinical trials, has been relatively limited within ESG disclosure and sustainability reporting. As a result, future studies should consider employing meta-analysis to evaluate quantitative studies and their respective data to identify the most significant variables that can impact the relationships under investigation.

Most importantly, the study identifies feasible future research directions. Firstly, due to the absence of standardized methods for measuring sustainability, exploring the potential bias in the relationship between ESG factors and firm performance resulting from the selection of rating agencies would be intriguing. This topic holds significance within the domain and offers an avenue for insightful investigation. Also, regulators and policymakers are emphasizing the integration of sustainability considerations into financial risk assessments. Examining how ESG ratings influence the probability of default can contribute to developing regulatory frameworks and guidelines that promote responsible and sustainable financial practices.

Finally, considering the growing utilization of technology in business operations, future research should explore the intersection between technology and sustainability reporting practices, particularly in the context of firms’ widespread adoption of sustainable operational practices. Such studies could examine the roles played by technology in collecting and analyzing sustainability data and its impact on financial performance. Additionally, it would be valuable to investigate the influence of technology on the effectiveness and credibility of sustainability reporting practices, considering the increasing presence of AI software aiding researchers in their investigations. By delving into these areas, researchers can gain insights into the potential benefits and challenges of incorporating digital tools into sustainability reporting and the overall implications for firms and stakeholders.

Credit Authorship contribution statement

George Nyantakyi: Idea conceptualizing, Data curation, writing, formal analysis, and writing. Francis Atta Sarpong: Writing, formal analysis, and revision. Philip Adu Sarfo: Editing, and revision. Nneka Uchenwoke Ogochukwu: Proofreading and editing. Winnifred Coleman: revision and Proofreading.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Abdi, Y., Li, X., & Càmara-Turull, X. (2022). Exploring the impact of sustainability (ESG) disclosure on firm value and financial performance (FP) in airline industry: The moderating role of size and age. Environment, Development and Sustainability, 24(4), 5052–23. https://doi.org/10.1007/s10668-021-01649-w

- Adams, M., Thornton, B., & Sepehri, M. (2012). The impact of the pursuit of sustainability on the financial performance of the firm. Journal of Sustainability Green Business, 1(1), 1–14.

- Agarwal, N., Gneiting, U., & Mhlanga, R. (2017). Raising the bar: Rethinking the role of business in the sustainable development goals.

- Ahmad, N., Mobarek, A., & Roni, N. N. (2021). Revisiting the impact of ESG on financial performance of FTSE350 UK firms: Static and dynamic panel data analysis. Cogent Business & Management, 8(1), 1900500. https://doi.org/10.1080/23311975.2021.1900500

- Aifuwa, H. O. (2020). Sustainability reporting and firm performance in developing climes: A review of literature. Copernican Journal of Finance Accounting, 9(1), 9–29. https://doi.org/10.12775/CJFA.2020.001

- Albuquerque, R., Koskinen, Y., & Zhang, C. (2019). Corporate social responsibility and firm risk: Theory and empirical evidence. Management Science, 65(10), 4451–4469. https://doi.org/10.1287/mnsc.2018.3043

- Alda, M. (2021). The environmental, social, and governance (ESG) dimension of firms in which social responsible investment (SRI) and conventional pension funds invest: The mainstream SRI and the ESG inclusion. Journal of Cleaner Production, 298, 126812. https://doi.org/10.1016/j.jclepro.2021.126812

- Alhossini, M. A., Ntim, C. G., & Zalata, A. M. (2021). Corporate board committees and corporate outcomes: An international systematic literature review and agenda for future research. The International Journal of Accounting, 56(1), 2150001. https://doi.org/10.1142/S1094406021500013

- Antwi, I. F., Carvalho, C., & Carmo, C. (2022). Corporate governance research in Ghana through bibliometric method: Review of existing literature. Cogent Business & Management, 9(1), 2088457. https://doi.org/10.1080/23311975.2022.2088457

- Arnold, M. C., Bassen, A., & Frank, R. (2012). Integrating sustainability reports into financial statements: An experimental study. Available at SSRN. https://doi.org/10.2139/ssrn.2030891

- Avetisyan, E., & Hockerts, K. (2017). The consolidation of the ESG rating industry as an enactment of institutional retrogression. Business Strategy and the Environment, 26(3), 316–330. https://doi.org/10.1002/bse.1919

- Axjonow, A., Ernstberger, J., & Pott, C. (2018). The impact of corporate social responsibility disclosure on corporate reputation: A non-professional stakeholder perspective. Journal of Business Ethics, 151(2), 429–450. https://doi.org/10.1007/s10551-016-3225-4

- Azapagic, A. J. J. (2004). Developing a framework for sustainable development indicators for the mining and minerals industry. Journal of Cleaner Production, 12(6), 639–662. https://doi.org/10.1016/S0959-65260300075-1

- Bartolacci, F., Caputo, A., & Soverchia, M. (2020). Sustainability and financial performance of small and medium sized enterprises: A bibliometric and systematic literature review. Business Strategy and the Environment, 29(3), 1297–1309. https://doi.org/10.1002/bse.2434

- Boiral, O. (2013). Sustainability reports as simulacra? A counter-account of a and A+ GRI reports. Accounting Auditing & Accountability Journal, 26(7), 1036–1071.

- Bos‐Brouwers, H. E. J. (2010). Corporate sustainability and innovation in SMEs: Evidence of themes and activities in practice. Business Strategy and the Environment, 19(7), 417–435.

- Brown, H. S., de Jong, M., & Levy, D. L. (2009). Building institutions based on information disclosure: Lessons from GRI’s sustainability reporting. Journal of Cleaner Production, 17(6), 571–580. https://doi.org/10.1016/j.jclepro.2008.12.009

- Brundtland, G. H. (1987). Our common future—Call for action. Environmental Conservation, 14(4), 291–294. https://doi.org/10.1017/S0376892900016805

- Buallay, A., Hamdan, R., Barone, E., & Hamdan, A. (2022). Increasing female participation on boards: Effects on sustainability reporting. International Journal of Finance & Economics, 27(1), 111–124. https://doi.org/10.1002/ijfe.2141

- Burritt, R. L., & Schaltegger, S. (2010). Sustainability accounting and reporting: Fad or trend? Accounting Auditing & Accountability Journal, 23(7), 829–846. https://doi.org/10.1108/09513571011080144

- Cebrián, G., Grace, M., & Humphris, D. (2013). Organisational learning towards sustainability in higher education. Sustainability Accounting, Management and Policy Journal, 4(3), 285–306. https://doi.org/10.1108/SAMPJ-12-2012-0043

- Chen, K., Wang, J., Yu, B., Wu, H., & Zhang, J. (2021). Critical evaluation of construction and demolition waste and associated environmental impacts: A scientometric analysis. Journal of Cleaner Production, 287, 125071. https://doi.org/10.1016/j.jclepro.2020.125071

- Cho, C. H., Laine, M., Roberts, R. W., & Rodrigue, M. (2015). Organized hypocrisy, organizational façades, and sustainability reporting. Accounting, Organizations & Society, 40, 78–94.

- Christensen, H. B., Hail, L., & Leuz, C. (2021). Mandatory CSR and sustainability reporting: Economic analysis and literature review. Review of Accounting Studies, 26(3), 1176–1248. https://doi.org/10.1007/s11142-021-09609-5

- Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2008). Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organizations & Society, 33(4–5), 303–327. https://doi.org/10.1016/j.aos.2007.05.003

- Clarkson, P. M., Overell, M. B., & Chapple, L. (2011). Environmental reporting and its relation to corporate environmental performance. Abacus, 47(1), 27–60.

- Cobbinah, B. B., Cheng, Y., Milly, N., & Sarpong, F. A. (2020). Relationship between determinants of financial assistance and credit accessibility of Small and Medium-Enterprises (Sme’s): A case study of SME’s in Takoradi metropolis in the Western Region of Ghana. Open Journal of Business and Management, 9(1), 430–447. https://doi.org/10.4236/ojbm.2021.91023

- Cohen, M. (2017). A systematic review of urban sustainability assessment literature. Sustainability, 9(11), 2048 https://doi.org/10.3390/su9112048.

- Coluccia, D., Fontana, S., & Solimene, S. J. S. (2018). Does institutional context affect CSR disclosure? A study on Eurostoxx 50. Sustainability, 10(8), 2823. https://doi.org/10.3390/su10082823

- Cooper, S., & Michelon, G. (2022). Conceptions of materiality in sustainability reporting frameworks: Commonalities, differences and possibilities. In Handbook of accounting and sustainability (pp. 44–66). Edward Elgar Publishing. https://doi.org/10.4337/9781800373518.00010

- Dabi, Y., Darrigues, L., Katsahian, S., Azoulay, D., De Antonio, M., & Lazzati, A. (2016). Publication trends in bariatric surgery: A bibliometric study. Obesity Surgery, 26, 2691–2699. https://doi.org/10.1007/s11695-016-2160-x

- Delen, D., Kuzey, C., & Uyar, A. (2013). Measuring firm performance using financial ratios: A decision tree approach. Expert Systems with Applications, 40(10), 3970–3983. https://doi.org/10.1016/j.eswa.2013.01.012

- de Solla Price, D. J. (1963). Little science, big science. Columbia University Press: https://doi.org/10.7312/pric91844

- Dhaliwal, D. S., Li, O. Z., Tsang, A., & Yang, Y. G. (2011). Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. The Accounting Review, 86(1), 59–100. https://doi.org/10.2308/accr.00000005

- Dissanayake, D., Tilt, C., & Qian, W. (2019). Factors influencing sustainability reporting by Sri Lankan companies. Pacific Accounting Review, 31(1), 84–109. https://doi.org/10.1108/PAR-10-2017-0085

- Effah, N. A. A., Asiedu, M., & Otchere, O. A. S. (2022). Improvements or deteriorations? A bibliometric analysis of corporate governance and disclosure research (1990–2020). Journal of Business Socio-Economic Development, 3(2), 118–133. https://doi.org/10.1108/JBSED-10-2021-0142

- El Ghoul, S., Guedhami, O., Kwok, C. C., & Mishra, D. R. (2011). Does corporate social responsibility affect the cost of capital? Journal of Banking and Finance, 35(9), 2388–2406. https://doi.org/10.1016/j.jbankfin.2011.02.007

- Elkington, J. (2013). Enter the triple bottom line. In the triple bottom line: Does it all add up?. Routledge.

- Esen, E. (2013). The influence of corporate social responsibility (CSR) activities on building corporate reputation. International Business, Sustainability and Corporate Social Responsibility, 11, 133–150. https://doi.org/10.1108/S2051-503020130000011010

- Friede, G., Busch, T., & Bassen, A. (2015). ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. Journal of Sustainable Finance & Investment, 5(4), 210–233. https://doi.org/10.1080/20430795.2015.1118917

- García‐Sánchez, I. M., Aibar‐Guzmán, B., Aibar‐Guzmán, C., & Somohano‐Rodríguez, F. M. (2022). The drivers of the integration of the sustainable development goals into the non‐financial information system: Individual and joint analysis of their influence. Sustainable Development, 30(4), 513–524. https://doi.org/10.1002/sd.2246

- Gillan, S. L., Koch, A., & Starks, L. T. (2021). Firms and social responsibility: A review of ESG and CSR research in corporate finance. Journal of Corporate Finance, 66, 101889. https://doi.org/10.1016/j.jcorpfin.2021.101889

- Girón, A., Kazemikhasragh, A., Cicchiello, A. F., & Monferrá, S. (2022). The impact of board gender diversity on sustainability reporting and external assurance: Evidence from lower-middle-income countries in Asia and Africa. Journal of Economic Issues, 56(1), 209–224. https://doi.org/10.1080/00213624.2022.2020586

- Gonçalves, T. C., Dias, J., & Barros, V. (2022). Sustainability performance and the cost of capital. International Journal of Financial Studies, 10(3), 63. https://doi.org/10.3390/ijfs10030063

- Guan, J., & Ma, N. (2004). A comparative study of research performance in computer science. Scientometrics, 61(3), 339–359. https://doi.org/10.1023/b:scie.0000045114.85737.1b

- Hahn, R., & Kühnen, M. (2013). Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. Journal of Cleaner Production, 59, 5–21. https://doi.org/10.1016/j.jclepro.2013.07.005

- Hamrouni, A., Bouattour, M., Ben Farhat Toumi, N., & Boussaada, R. (2022). Corporate social responsibility disclosure and information asymmetry: Does boardroom attributes matter? Journal of Applied Accounting Research, 23(5), 897–920. https://doi.org/10.1108/JAAR-03-2021-0056

- Hanh, T., Preuss, L., Pinkse, J., & Figge, F. (2014). Cognitive frames in corporate sustainability: Managerial sensemaking with paradoxical and business case frame. Academy of Management Review, 39(4), 463–487. https://doi.org/10.5465/amr.2012.0341

- Harsanto, B., & Firmansyah, E. A. (2023). A twenty years bibliometric analysis (2002–2021) of business economics research in ASEAN. Cogent Business & Management, 10(1), 2194467. https://doi.org/10.1080/23311975.2023.2194467

- Hassani, B. K., & Bahini, Y. (2022). Relationships between ESG disclosure and economic growth: A critical review. Journal of Risk and Financial Management, 15(11), 538. https://doi.org/10.3390/jrfm15110538

- Hong, H., & Kacperczyk, M. (2009). The price of sin: The effects of social norms on markets. Journal of Financial Economics, 93(1), 15–36. https://doi.org/10.1016/j.jfineco.2008.09.001

- Hubbard, G. (2009). Measuring organizational performance: Beyond the triple bottom line. Business Strategy and the Environment, 18(3), 177–191.

- Ibrahim, A. E. A., Hussainey, K., Nawaz, T., Ntim, C., & Elamer, A. (2022). A systematic literature review on risk disclosure research: State-of-the-art and future research agenda. International Review of Financial Analysis, 102217. https://doi.org/10.1016/j.irfa.2022.102217

- Jørgensen, S., Mjøs, A., & Pedersen, L. J. T. (2022). Sustainability reporting and approaches to materiality: Tensions and potential resolutions. Sustainability Accounting, Management and Policy Journal, 13(2), 341–361. https://doi.org/10.1108/SAMPJ-01-2021-0009

- Joseph, C. (2010). Content analysis of sustainability reporting on Malaysian local authority websites.

- Khan, M. A. (2022). ESG disclosure and firm performance: A bibliometric and meta analysis. Research in International Business Finance, 61, 101668. https://doi.org/10.1016/j.ribaf.2022.101668

- Khan, A., Goodell, J. W., Hassan, M. K., & Paltrinieri, A. (2022). A bibliometric review of finance bibliometric papers. Finance Research Letters, 47, 102520. https://doi.org/10.1016/j.frl.2021.102520

- Kumar, A., Shrivastav, S., Adlakha, A., & Vishwakarma, N. K. (2022). Appropriation of sustainability priorities to gain strategic advantage in a supply chain. International Journal of Productivity & Performance Management, 71(1), 125–155. https://doi.org/10.1108/IJPPM-06-2020-0298

- Kumawat, R., & Patel, N. (2022). Are ESG disclosures value relevant? A Panel-Corrected Standard Error (PCSE) approach. Global Business Review, 23(6), 1558–1573. https://doi.org/10.1177/09721509221128637

- Laskar, N., & Gopal Maji, S. (2018). Disclosure of corporate sustainability performance and firm performance in Asia. Asian Review of Accounting, 26(4), 414–443. https://doi.org/10.1108/ARA-02-2017-0029

- La Torre, M., Sabelfeld, S., Blomkvist, M., Tarquinio, L., & Dumay, J. (2018). Harmonising non-financial reporting regulation in Europe: Practical forces and projections for future research. Meditari Accountancy Research, 26(4), 598–621. https://doi.org/10.1108/MEDAR-02-2018-0290

- Lawal, E., May, G., & Stahl, B. (2017). The significance of corporate social disclosure for high‐tech manufacturing companies: Focus on employee and community aspects of sustainable development. Corporate Social Responsibility & Environmental Management, 24(4), 295–311. https://doi.org/10.1002/csr.1397

- Leins, S. (2020). ‘Responsible investment’: ESG and the post-crisis ethical order. Economy and Society, 49(1), 71–91. https://doi.org/10.1080/03085147.2020.1702414

- Liao, H., Tang, M., Luo, L., Li, C., Chiclana, F., & Zeng, X.-J. (2018). A bibliometric analysis and visualization of medical big data research. Sustainability, 10(1), 166. https://doi.org/10.3390/su10010166

- Liu, Y., Kim, C. Y., Lee, E. H., & Yoo, J. W. (2022). Relationship between sustainable management activities and financial performance: Mediating effects of non-financial performance and moderating effects of institutional environment. Sustainability, 14(3), 1168. https://doi.org/10.3390/su14031168

- Li, H., Zhang, X., & Zhao, Y. (2022). ESG and firm’s default risk. Finance Research Letters, 47, 102713 Li, Hao, Zhang, Xuan, Zhao, Yang, 2022. ESG and Firm’s Default Risk. Finance Research Letters. In press.

- Lokuwaduge, C. S. D. S., & Heenetigala, K. (2017). Integrating environmental, social and governance (ESG) disclosure for a sustainable development: An Australian study. Business Strategy and the Environment, 26(4), 438–450. https://doi.org/10.1002/bse.1927

- Lu, Y., Ntim, C. G., Zhang, Q., & Li, P. (2022). Board of directors’ attributes and corporate outcomes: A systematic literature review and future research agenda. International Review of Financial Analysis, 102424. https://doi.org/10.1016/j.irfa.2022.102424

- Maama, H., & Marimuthu, F. (2022). Integrated reporting and cost of capital in sub-Saharan African countries. Journal of Applied Accounting Research, 23(2), 381–401. https://doi.org/10.1108/JAAR-10-2020-0214

- Mackey, A., Mackey, T. B., & Barney, J. B. (2007). Corporate social responsibility and firm performance: Investor preferences and corporate strategies. Academy of Management Review, 32(3), 817–835. https://doi.org/10.5465/amr.2007.25275676

- Majid, M. F., Meraj, M., & Mubarik, M. S. (2022). In the pursuit of environmental sustainability: The role of environmental accounting. Sustainability, 14(11), 6526. https://doi.org/10.3390/su14116526

- Manita, R., Bruna, M. G., Dang, R., & Houanti, L. H. (2018). Board gender diversity and ESG disclosure: Evidence from the USA. Journal of Applied Accounting Research, 19(2), 206–224. https://doi.org/10.1108/JAAR-01-2017-0024

- Manning, B., Braam, G., & Reimsbach, D. (2019). Corporate governance and sustainable business conduct—E ffects of board monitoring effectiveness and stakeholder engagement on corporate sustainability performance and disclosure choices. Corporate Social Responsibility and Environmental Management, 26(2), 351–366. https://doi.org/10.1002/csr.1687

- Martínez, J. B., Fernández, M. L., & Fernández, P. M. R. (2016). Corporate social responsibility: Evolution through institutional and stakeholder perspectives. European Journal of Management and Business Economics, 25(1), 8–14. https://doi.org/10.1016/j.redee.2015.11.002

- Milne, M. J., & Gray, R. (2013). W (h) ither ecology? The triple bottom line, the global reporting initiative, and corporate sustainability reporting. Journal of Business Ethics, 118(1), 13–29. https://doi.org/10.1007/s10551-012-1543-8

- Misiuda, M., & Lachmann, M. (2022). Investors’ perceptions of sustainability reporting—A review of the experimental literature. Sustainability, 14(24), 16746. https://doi.org/10.3390/su142416746

- Moldavska, A., & Welo, T. (2019). A Holistic approach to corporate sustainability assessment: Incorporating sustainable development goals into sustainable manufacturing performance evaluation. Journal of Manufacturing Systems, 50, 53–68. https://doi.org/10.1016/j.jmsy.2018.11.004

- Mori Junior, R., & Best, P. (2017). GRI G4 content index: Does it improve credibility and change the expectation–performance gap of GRI-assured sustainability reports? Sustainability Accounting, Management and Policy Journal, 8(5), 571–594. https://doi.org/10.1108/SAMPJ-12-2015-0115

- Mulchandani, K., Mulchandani, K., Iyer, G., & Lonare, A. J. G. B. R. (2022). Do equity investors care about Environment, Social and Governance (ESG) disclosure performance? Evidence from India. Global Business Review, 23(6), 1336–1352. https://doi.org/10.1177/09721509221129910

- Nguyen, T. H. H., Ntim, C. G., & Malagila, J. K. (2020). Women on corporate boards and corporate financial and non-financial performance: A systematic literature review and future research agenda. International Review of Financial Analysis, 71, 101554. https://doi.org/10.1016/j.irfa.2020.101554

- Nobanee, H., Al Hamadi, F. Y., Abdulaziz, F. A., Abukarsh, L. S., Alqahtani, A. F., AlSubaey, S. K., Alqahtani SM, & Almansoori, H. A. (2021). A bibliometric analysis of sustainability and risk management. Sustainability, 13(6), 3277. https://doi.org/10.3390/su13063277

- Nobanee, H., & Ellili, N. (2016). Corporate sustainability disclosure in annual reports: Evidence from UAE banks: Islamic versus conventional. Renewable & Sustainable Energy Reviews, 55, 1336–1341. https://doi.org/10.1016/j.rser.2015.07.084

- Odriozola, M. D., & Baraibar‐Diez, E. (2017). Is corporate reputation associated with quality of CSR reporting? Evidence from Spain. Corporate Social Responsibility & Environmental Management, 24(2), 121–132. https://doi.org/10.1002/csr.1399

- Oliver, R. M. (2013). Financial performance measures in credit scoring. EURO Journal on Decision Processes, 1(3), 169–185. https://doi.org/10.1007/s40070-013-0017-2

- Oncioiu, I., Petrescu, A.-G., Bîlcan, F.-R., Petrescu, M., Popescu, D.-M., & Anghel, E. (2020). Corporate sustainability reporting and financial performance. Sustainability, 12(10), 4297. https://doi.org/10.3390/su12104297

- Osobajo, O. A., Oke, A., Lawani, A., Omotayo, T. S., Ndubuka McCallum, N., & Obi, L. (2022). Providing a roadmap for future research agenda: A bibliometric literature review of sustainability performance reporting (SPR). Sustainability, 14(14), 8523. https://doi.org/10.3390/su14148523

- Porter, M. E., & Kramer, M. R. (2006). The link between competitive advantage and corporate social responsibility. Harvard Business Review, 84(12), 78–92.

- Roca, L. C., & Searcy, C. (2012). An analysis of indicators disclosed in corporate sustainability reports. Journal of Cleaner Production, 20(1), 103–118. https://doi.org/10.1016/j.jclepro.2011.08.002