?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines VAT compliance factors among SMEs in Nigeria. Specifically, the study assesses the influence of Taxpayer Perception and Attitudes (TPA), Organizational Characteristics (OC), Tax Compliance Cost (TCC), VAT Implementation Efficacy (VIE), revenue, profit, employees, customers, and SMEs size on VAT compliance among SMEs in Nigeria. Using both primary and secondary data in the study population comprised all registered SMEs in Nigeria. The study used a sample of 3,600 SMEs to carry out the analysis. Also, given a total of 18,000 observations, a panel data set of 3,600 SMEs from the years 2018 to 2022 was chosen from the financial records of SMEs. The results indicate that TPA, OC, TCC, and VIE influence VAT compliance. Furthermore, the study discovered that revenue has a positive but not significant effect on VAT compliance. More so, the size and level of profit generated have a positive and significant influence on VAT compliance by SMEs. However, a number of employees and customers have no significant effect on VAT compliance by SMEs. The study contributes to the existing body of knowledge by combining both qualitative and quantitative approaches on this subject and will assist researchers and practitioners in assessing the influence of VAT compliance among SMEs. Hence, policymakers and tax authorities should incorporate these factors in order to improve tax compliance among SMEs in Nigeria, which will eventually boost revenue generation.

1. Introduction

Value Added Tax (VAT) compliance is a crucial issue and relevant to tax revenue generation, which eventually strengthens the economy of the nation. At every level of production and distribution, commodities and services are subject to the consumption tax known as VAT. Businesses collect VAT on the government’s behalf and send it to the tax authorities. SMEs are essential to the economies of many nations, and it is impossible to exaggerate the importance of their involvement in the transfer of VAT to the appropriate tax authority. Small and Medium Enterprises (SMEs) are the backbone of the economy in many nations, and there are many benefits attached to SMEs sending their VAT back to the economy. First, it gives governments a reliable and predictable source of income that can be used to pay for public services like healthcare, education, and infrastructure improvement. Second, VAT remittance encourages companies to maintain proper records and adhere to tax laws, thus fostering the development of fiscal responsibility. In turn, this lowers the frequency of tax fraud and evasion. In addition, by leveling the playing field for firms, VAT remittance by SMEs supports economic growth. The competitive advantage that larger businesses may have over smaller ones is diminished when all enterprises are forced to remit VAT. In turn, this supports innovation and entrepreneurship as well as fair competition. In many nations, and especially in developing nations, VAT is a significant source of revenue, according to research by the International Monetary Fund (IMF). According to the paper, VAT has increased revenue collection in many nations and has boosted economic growth and budgetary stability. Another World Bank study discovered that the implementation of VAT in developing nations increased revenue collection and decreased dependency on other taxes like customs fees. The research also revealed that VAT promoted compliance and decreased tax evasion (Eniola & Ektebang, Citation2014; Razak et al., Citation2018). Furthermore, SMEs’ contributions to the economy’s VAT remittance are an important factor in the expansion of the economy, the maintenance of fiscal stability, and the delivery of public services. It supports entrepreneurship, encourages fair competition, and lowers the prevalence of tax fraud and evasion. As a result, it is critical that governments develop policies and programs that encourage SME VAT compliance as well as offer support and assistance to SME taxpayers.

VAT compliance is a critical component of taxes that considerably boosts a nation’s ability to generate money. Due to their propensity to underreport their taxable revenue or avoid taxes, many SMEs in Nigeria have found it difficult to comply with VAT regulations. Due to market distortions, reduced tax income, and unfair company rivalry, this noncompliance has a detrimental impact on the economy (Adeyemo & Oyedele, Citation2018). Therefore, it is necessary to pinpoint the key variables that have an impact on Nigerian SMEs’ ability to comply with VAT laws. This study attempts to evaluate these elements and offer suggestions for enhancing SME VAT compliance. In the entire world, SMEs account for the bulk of firms. SMEs promote entrepreneurship and push solutions to problems in societal groups, raising the standard of living. The significance of SMEs in economic and social growth, poverty reduction, increased employment, output, technology development, social standing, and higher standards has been established and acknowledged on a global scale, in both emerging and developed countries. However, many countries still struggle with SME development (Gyamera et al., Citation2023; Lim et al., Citation2020). Compliance with tax laws boosts tax revenue, which frequently results in a sharp increase in economic growth. From the first day of a tax system’s implementation in the political sphere to the last day of its economic impact, compliance is crucial. A transparent, democratic government structure and easily understandable tax laws are required for tax compliance. Higher tax compliance is also correlated with higher taxpayer use of voluntary disclosure programmes. Various studies on VAT compliance and SMEs in various nations have been undertaken, as well as in Nigeria (Adeniji & Olowookere, Citation2018; Akinlabi & Oyedele, Citation2019; Olaoye & Oyedijo, Citation2019), identifying factors that influence VAT compliance behavior. The focus of their studies was on a specific state or geographic region, and they were generally based on either a qualitative or quantitative method, which leaves the extant literature on this issue lacking in comprehensiveness. Therefore, more study is required to pinpoint the distinct elements that influence SME VAT compliance across Nigeria’s six geographical zones, as well as to combine qualitative and quantitative methods. By identifying the distinctive elements that affect SMEs’ compliance with the VAT in Nigeria, this study will add to the body of existing literature.

Based on the above, this study developed the following research objectives to be achieved by collecting data through a questionnaire and secondary data from the selected SMEs: The objectives of the study are to analyze taxpayer perceptions and attitudes, organizational characteristics, tax compliance costs, and VAT implementation efficacy on VAT compliance among SMEs in Nigeria using primary data. More so, the study examined the influence of revenue, profit, employee, customer, and SMEs size on VAT compliance among SMEs in Nigeria using secondary data. In addition, the study seeks answers to the research questions: what are the effects of taxpayer perception and attitudes, organizational characteristics, tax compliance cost, and VAT implementation efficacy on VAT compliance among SMEs in Nigeria? What are the influences of revenue, profit, employee, customer, and SMEs size on VAT compliance among SMEs in Nigeria?

To achieve the study objectives, the study employed ability to pay theory. This also includes the theoretical gap that this study attempts to fill because most previous studies in this area were based on psychological or economic deterrence theories. Consequently, the current paper seeks to make the following contributions to the existing literature: First, it sheds light on the relationship between SMEs and VAT compliance and offers in-depth insights on mixed techniques, combining quantitative and qualitative methods, which allow authors to solicit potentially embarrassing, incriminating, or sensitive information. Second, it contributes to the existing literature and practice by providing new evidence to support the ability to pay theory in explaining the influence of VAT compliance by SMEs. Third, the study’s findings will provide valuable insights into how to improve VAT compliance by SMEs, which will help policymakers, tax authorities, and SMEs learn how to improve VAT compliance and revenue generation. Finally, the current study’s findings might be used to complement knowledge and understand indirect taxes such as VAT from a broader perspective.

2. Background of the study

VAT is one of the categories of indirect tax that levies a charge at every production stage, distribution stage, and consumption chain stage. VAT was first introduced in France in 1954 by a politician and businessman called Carl Friedrich von Siemens. Since that time, many nations throughout the globe have adopted the VAT. The VAT Decree 102 of 1993, which was passed by the Federal Government of Nigeria (FGN) and became effective in 1994, was established to replace sales tax in the States. Several amendments have been made to VAT law in Nigeria, the most recent of which resulted in a 50% rate rise (from 5% to 7.5%), sparking ferocious arguments among a number of interest groups. Only businesses that make taxable supplies up to 25 million are obligated to charge, collect, and remit VAT as well as submit monthly VAT returns to Federal Inland Revenue Services (FIRS), according to the Finance Act, 2019; ICAN, Citation2022). Thus, it is expected that many SMEs may not meet the 25 million taxable supply threshold and, as such, should be exempted from VAT compliance obligations. However, upon meeting the threshold at any time in a year, such SMEs would be required to conform to the VAT requirements. The law in Nigeria requires that VAT returns be filed on a monthly basis and should be remitted to the FIRS every month on the 14th of each month (Finance Bill, Citation2022). The current sharing formula for VAT generated in Nigeria is 15%, 50%, and 35% to FG, States, and Local Government Areas (LGAs), including councils of the FCT, respectively. The shares of the states and those of the LGAs are shared amongst them using the factors of equality (50%) and population (30%) and derivation (20%) (Chartered Institute of Taxation of Nigeria CITN, Citation2022).

Globally, SMEs are important in most economies, predominantly in developed and developing economies where SMEs are considered the backbone of the economy. More so, SMEs are a vital element of Nigeria’s economy because of their immense potential for income redistribution, employment generation, and innovation. According to International Finance Corporation (IFC) studies, over 50% of jobs in Nigeria’s private sector and 96% of enterprises are SMEs. Because of this, SMEs can potentially represent a substantial portion of the government’s revenue base. Even though there are many benefits to registering for taxes, such as better access to capital, business opportunities, and stronger legal standing, it still means entering the tax system. It seems that some SMEs are still struggling to comply with the payment of VAT (Naicker & Rajarami, Citation2018; Tareq et al., Citation2022). According to Holcombe (Citation2010), VAT compliance is a substantial source of funding for economic governance in many nations throughout the world. Non-compliance with tax laws has continued to cost the country a lot of money, and revenue has declined. These revenue losses might have a substantial impact on the fortunes of many economies, especially those in developing nations like Nigeria. Due to the fact that VAT accounts for approximately 27.2% of total tax revenue collected by the Nigerian government, the FIRS has introduced online filing of VAT returns that automatically transmit information about business transactions to the tax administration via tax promo max in order to improve compliance (Appendix, Table ). VAT is pertinent to the potential increment to increase non-oil revenue significantly in Nigeria, which possesses a broader impact on economic growth due to its high potential contribution (Agbo & Nwadialor, Citation2020).

Due to the backdrop discussed, this study specifically examines the driving forces behind SMEs in Nigeria complying with VAT. A review of several empirical studies from various continents revealed disparate results for the factor influencing VAT compliance. Furthermore, the review also revealed that most past studies were done in EU countries, the MENA region, and Jordan, and they only considered primary data for their studies (Alognon et al., Citation2020; Alsughayer, Citation2021; Amanamah, Citation2016; Naomi, Citation2022; Shakkour et al., Citation2021; Sidek & Abdulraqeeb, Citation2022). More so, Eragbhe and Omoye’s (Citation2014) study that was conducted in Nigeria was based solely on tax compliance costs. This study, therefore, addresses these research gaps by ensuring variables such as taxpayer perception and attitudes, organization characteristics, tax compliance cost, and VAT implementation efficacy are considered in assessing VAT compliance among Nigerian SMEs, as well as by including secondary data, which include revenue, profit, employees, customers, and SMEs size, in the study. Despite the fact that this study uses data from Nigeria, the factors it discusses are universal and can serve as a guide for other nations looking to identify factors that affect VAT compliance to boost their revenue. Hence, it can also be referred to in a wider context, especially in nations with a tax system like Nigeria.

The rest of the paper is as follows: It starts with an introduction, while Section 2 discusses the background of the study, which focuses on Nigeria’s policy, the regulatory framework on VAT, and the developments of SMEs. followed by a theoretical literature review. Section 4 addresses empirical literature and hypotheses development. Research design was discussed in Section 5. The next section is empirical results and discussion, which discusses the results of the studies. Section 7 focuses on the summary and conclusion, which provide a study summary as well as limitations and recommendations for further study.

3. Theoretical literature review

3.1. Psychological theory

According to the Psychology Theory (PT) proposed by Sigmund Freud, a taxpayer’s motivation to pay taxes increases in direct proportion to their attitude toward fulfilling their obligations. Taxpayers’ attitudes toward the tax system and their motivation to adhere to the law are related (Fagbemi & Abogun, Citation2015; Schmolders, Citation1970; Strumpel, Citation1966). The psychological factors that can influence tax compliance observed in the literature include attitudes toward the government, taxation together with norms and justices, and taxpayers’ knowledge of tax law (Nichita et al., Citation2019; Rosalita & Aulia, Citation2023).

3.2. Economic Deterrence Theory (EDT)

EDT is a theory in criminology that was the first model employed to explicate tax compliance behavior. The theory was developed from the work of a modern philosopher (Bentham et al., Citation1789). It established the notion that someone is discouraged from committing crimes if the benefit realized is less than the penalty meted for committing such crimes (King’oina, Citation2016). Taxpayers decide whether to violate or obey tax law after considering the benefits accrued by successful evasion and the risk of being punished when caught. EDT stated that reasonable taxpayers forego paying taxes if the anticipated benefits exceed the risk of being punished when caught. EDT assumes that taxpayers act rationally. Each taxpayer is expected to optimize the potential utility of the tax non-compliance hazard by assessing financial benefits as against punishment risk during the tax audit (Alm et al., Citation2012).

3.3. Ability to pay theory

One of the most common theories that describes tax compliance in terms of universal sacrifice is the ability to pay theory. The British economist John Stuart Mill first proposed the theory in 1848. He stated that a reasonable and fair tax system must adhere to the premise that taxes should be assessed in accordance with the taxpayer’s capacity to pay. Modern tax policy has been greatly influenced by Mill’s ideas on the ability to pay principle, which are still frequently referenced and discussed by economists and decision-makers. A key idea in tax policy, particularly VAT compliance, is the ability to pay theory. According to this theory, taxes should be assessed in accordance with the taxpayer’s financial capacity. As a result, people with higher incomes or more resources should contribute a larger percentage of their income to taxes than those with lower incomes or fewer resources (Habes, Citation2019). The ability to pay principle is crucial in the context of VAT compliance because it ensures that the tax burden is allocated equally among taxpayers. If VAT is applied uniformly to all goods and services, irrespective of the taxpayer’s capacity to pay, it may disproportionately affect low-income earners, who may be required to spend a greater proportion of their income on basic goods and services subject to VAT (Sidek & Abdulraqeeb, Citation2022).

However, this study anchored on the ability to pay theory because it ensures that the tax burden is spread evenly among taxpayers and that compliance enforcement is carried out in a way that takes the taxpayer’s ability to pay into account. The ability to pay theory is a key idea in VAT compliance. More so, if the taxpayers have the ability and capacity to pay, it will lead to a perception or attitude to buy vatable goods, which will probably be influenced by organization characteristics, tax compliance costs, and VAT implementation efficacy. Also, it applies to how revenue and profit generated by SMEs, their employees, customers, and size influence VAT compliance.

3.4. Taxpayer perception/attitudes, organization characteristics, tax compliance cost, VAT implementation efficacy and VAT Compliance

One of the major factors influencing VAT compliance has been identified as the perception of taxation and general compliance levels. Taxpayers’ perceptions influence taxpayers’ attitudes toward paying taxes (Alabede et al., Citation2011; Alm et al., Citation2012; King’oina, Citation2016). According to Ya’u et al. (Citation2020), people base their choices on logical and rational thought. These choices are founded on anticipated outcomes, particularly in business organizations where relevant decisions are made by senior management and leadership. Decision-making approaches assume that decision-makers consider all available options before selecting the best one. Organizational characteristics have been emphasized as distinct features of SMEs that distinguish them from large organizations, influencing SMEs orientation in a variety of ways (Muda & Rahman, Citation2016). Key traits for VAT operationalization like human resources, record keeping, knowledge sharing, learning orientation, and culture are supported by the literature (Aladejebi & Oladimeji, Citation2019; Fauziati & Kassim, Citation2018). According to Pemstein et al. (Citation2019), the fundamental processes of VAT include the tax burden, the tax equity, the company’s gross earnings, sales, and others. According to Eragbhe and Omoye (Citation2014), costs associated with tax compliance include those related to obtaining, accounting for, and paying tax on the company’s products, earnings, and employee wages and salaries. In addition, it covers the expenses related to acquiring and updating the information necessary for this job, such as license fees and penalties (Sandford, Citation1995). Compliance, according to Muhammed (Citation2022), entails adhering to the rules, laws, policies, regulations, and standards. It may appear complicated and costly, but the cost of noncompliance will be greater. The determinant factor that impedes the effective implementation of the tax is referred to as implementation barriers. Overcoming these obstacles represents the SME’s VAT implementation efficacy. The imposition of VAT regulation by the appropriate authorities is to ensure that the major compliance hindrances undergone by SMEs are ultimately overcome (Jensen, Citation2018). Negative behaviors are sometimes displayed on purpose in non-compliance (Zabri et al., Citation2016). The unwillingness to involve an advisor is demonstrated as a determinant of compliance behavior, as is the ability and existence to employ IT specialists to generate an active VAT system internally, as well as the fact that SMEs frequently rely on publicly available information as a substitute for VAT advisors.

3.5. Revenue, profit, employee, customer, size of SMEs and VAT compliance

Revenue is a source of motivation and encouragement for being in business, in addition to acting as a lifeline for businesses and business owners. As such, small and medium enterprises (SMEs) must boost their revenue if they want to raise profits. According to Nguyen and Trinh (Citation2022), the nation’s budget revenue projections depend significantly on the taxpayer’s compliance with the VAT laws. By monitoring their income and concentrating on increasing it, they can also increase their profits, which will ultimately result in an increase in the amount of tax to remit to the tax authority (Fredrick & Peter, Citation2019; Shakkour et al., Citation2021). The foundation of a solid and long-lasting organization is its workforce, and this invariably means that the employee in charge of operations and processes in the organization cannot be valued as assets in monetary terms. Common to all SMEs, each employee becomes an integral part of the organizational framework, whether service- or production-oriented. Employees feel valued and admired if they are engaged and psychologically connected to their management and the organization. As a result of this, the organization experiences better productivity and greater profitability. Customers are the reason organizations stay in business, which is why they are being referred to as the king.” Operations and processes of the organization are directly related to the needs of the services and products offered by the organization (Benzarti & Dorian, Citation2019; Emmanuel et al., Citation2023; Gherghina et al., Citation2020). The number of employees determines the size of an organization. Also, the number of employees determined the volume of services and production, which eventually led to the revenue of the organization. Chelliah et al. (Citation2010) opined that size is regarded as one of the imperative factors in internationalization for SMEs in any nation. Firm size has been seen as a major factor in the effectiveness and efficiency of SMMEs because the larger the firm, the more it is able to attract customers through advertising, product marketing, and resource utilization, ultimately increasing the profitability and productivity of the organization. Previous empirical research on VAT compliance has been unable to disentangle the effects of profit, turnover, employees, customers, and size changes on VAT compliance by SMEs. This study fills the research gap among existing literature by employing secondary data on profit, turnover, employees, customers, and size gathered from selected SMEs to gauge VAT compliance by SMEs in Nigeria.

3.6. Gaps in the literature

Having reviewed many studies across the continent on VAT compliance among SME in the European Union (Alognon et al., Citation2020), Asia (Alshira’h & Abdul-Jabbar, Citation2019; Alsughayer, Citation2021; Shakkour et al., Citation2021; Sidek & Abdulraqeeb, Citation2022; Tareq et al., Citation2022), and Africa (Akumbo et al., Citation2020; Fredrick & Peter, Citation2019; Muhammed et al., Citation2017; Werekoh, Citation2022). It was observed that the majority of studies on VAT compliance, particularly among SMEs, were conducted in developed countries with a small number of SMEs. Also, previous studies have worked on VAT compliance, but VAT compliance determinants among SMEs have not been empirically assessed using both qualitative and quantitative approaches. Hence, this study made use of both primary and secondary data. To the best of the authors’ knowledge, this study will be the first to examine VAT compliance by SMEs using both primary and secondary data to arrive at its conclusion. The research broadens our understanding of how SMEs will improve their compliance with VAT. The government will make use of this study to identify factors to emphasize in order to motivate SMEs to voluntarily comply with VAT. Consequently, it will help tax practitioners understand areas in which to make policy decisions for SMEs.

4. Empirical literature review and hypotheses development

4.1. Taxpayer Perception/Attitudes (TPA) and VAT compliance

Eragbhe and Aronmwan (Citation2015) looked into how personal characteristics like age, gender, education, and other factors affected tax compliance in Nigeria. The researchers chose a sample of area taxpayers and adopted a descriptive quantitative methodology. The findings showed that individual beliefs and views had a significant influence on tax compliance. More so, Widianto (Citation2015), who examined demographic factors effects on Indonesia’s tax conformity, provided additional support for this claim. The researchers chose 2,383 Duren Sawit district taxpayers. Results showed that tax compliance was strongly influenced by gender, age, and schooling. Similarly, according to Hofmann et al. (Citation2017), societal and demographic factors had a significant influence on tax compliance. Researchers performed a meta-analysis of studies released in 111 nations from 1958 to 2012 in order to further validate this. Results indicated that age, gender, and income were significantly associated with tax compliance. More so, various authors have established the relationship between taxpayer perception and attitudes and VAT compliance (Fredrick & Peter, Citation2019; Gilligan & Richardson, Citation2005; Hofmann et al., Citation2017; Marandu et al., Citation2015; Tareq et al., Citation2022; Wanjohi, Citation2010; Widianto, Citation2015). The studies opined that several factors, such as thinking, opinion, perception, education, and others, influence tax compliance behavior. However, researchers believed that these findings were more frequent in developed countries. Literature seems to be lacking on the nexus between these variables in terms of empirical evidence, particularly in Nigeria, as most studies conducted focus on VAT and growth development (Inim et al., Citation2020; Usman, Citation2019). Hence, it leads to the hypothesis developed below:

H01:

TPA has no significant influence on VAT compliance amidst Nigeria SMEs

4.2. Organizational characteristics and VAT compliance

De Neve et al. (Citation2019) identified the management of tax burdens, tax law simplification, and the role of tax agents in informing and persuading the business sector as the three main contributors to VAT compliance. More so, Fredrick and Peter (Citation2019) looked at tax compliance among Ugandan single proprietors and SMEs’ owners. The findings indicated that, of all the demographic factors, gender was the most notable for having a clear and substantial connection to tax compliance. Additionally, Akumbo et al. (Citation2020) analyse the connection between individual characteristics and Ghanaian tax compliance. The findings showed that those with a degree expressed relatively greater compliance than those without one. More so, Tareq et al. (Citation2022) studied the factors that influence Jordanian SMEs’ intentions in tax law compliance. The research demonstrates that among the studied enterprises, the intentions for tax compliance were significantly influenced by subjective norms, attitudes, behavior, patriotism, and behavioral control. Furthermore, the empirical literature has shown different results on associations between VAT compliance and organizational characteristics (Agbo & Nwadialor, Citation2020; Alsughayer, Citation2021; Amanamah, Citation2016; Dabić et al., & Varc, Citation2019; Ghasia et al., Citation2017, Halim et al., Citation2019; Nyamwanza et al., Citation2014; Tehseen et al., Citation2019; Uzor, Citation2017). However, most of these studies were conducted in developed economies. There is a need to empirically analyze how organizational behavior influences VAT compliance among SMEs in emerging countries such as Nigeria. Hence, the hypothesis is formulated as follows:

H02:

Organizational characteristics do not significantly influence VAT compliance among SMEs.

4.3. Tax compliance cost and VAT compliance

According to Nyamwanza et al. (Citation2014), who empirically analyzed SMEs’ attitudes and behaviors impact on tax compliance, there is still a big challenge with understanding. Similar to this, Amanamah (Citation2016) studied the key elements influencing SMEs’ tax compliance in Ghana. The study considered 70 SMEs, which were chosen using a random sampling technique in order to administer seventy questionnaires. Findings displayed that the respondent remitted income tax to the Kumasi Municipal Assembly (KMA), VAT, and property tax. It was deduced from the study that tax rate reduction, development project implementation, penalty enforcement, and SMEs tax enlightenment encouraged voluntary tax compliance in KMA. More so, Msangi (Citation2015) examined Tanzania’s VAT compliance in light of ability and behavior choice theory. The results showed a positive correlation between tax rates and corporate income, suggesting that taxpayers’ financial capacity is the main driver of VAT compliance in Tanzania. To increase compliance, the researcher empathized with tax fairness and taxpayer convenience. Wadesango et al. (Citation2018) also looked into SMEs in Zimbabwe’s compliance with VAT. According to research, economic variables rank among the most important ones influencing VAT compliance in Zimbabwe. Naicker and Rajaram (Citation2018) evaluated which elements and expenses are most crucial for ensuring tax compliance. The study’s conclusions showed that South Africa’s SME’s most complicated tax is VAT, which is also referred to as a difficult and expensive tax to comply with. Similarly, Alsughayer (Citation2021) addressed the difficulties SMEs in Saudi Arabia have in complying with VAT laws and ranked these difficulties according to their respective severity. According to the study, providing taxpayers with sufficient tax education and knowledge lowers compliance costs and fines while increasing compliance. The bulk of research on VAT compliance and the cost of compliance in current literature was carried out in advanced countries (Shakkour et al., Citation2021; Sidek & Abdulraqeeb, Citation2022; Wadesango & Chirebvu, Citation2020; Wadesango et al., Citation2018). In addition, studies on tax compliance costs and VAT compliance by SMEs are limited, particularly in Africa. Therefore, this study formulated the hypothesis as follows:

H03:

Tax compliance cost insignificantly affects VAT compliance among SMEs.

4.4. VAT implementation efficacy and VAT compliance

Sidek and Abdulraqeeb (Citation2022) evaluated the results of government assistance for SME VAT compliance in the UAE. The study proposed a link between SMEs’ characteristics, efficacy, and VAT compliance. The advocates advocated that the government should simplify the VAT process, overpower the obstacles to VAT implementation, and enhance SMEs in the country for effective and productive VAT compliance. According to Nguyen and Trinh (Citation2022), the nation’s budget revenue projections depend significantly on the taxpayer’s compliance with the VAT laws. Few studies (Alshira’h & Abdul-Jabbar, Citation2019; Alognon et al., Citation2020; Usman, Citation2019) were carried out in terms of VAT implementation efficacy and compliance, some of which were conducted in Nigeria (Nura et al., Citation2017; Nwosu & Ochu, Citation2017) based on either the political and business environment among SMEs or the economic development of Nigeria. Thus, it is pertinent to examine the determinants of VAT implementation efficacy on VAT compliance in a country such as Nigeria, where VAT contributes to a larger percentage of non-oil revenue. This study formulated the following hypothesis:

H04:

VAT implementation efficacy does not drive VAT compliance among SMEs.

4.5. Turnover and VAT compliance

Turnover refers to the total sales realized by SMEs in a specific period. It is also referred to as the SMEs gross income in a specific period through the sales of their finished products. According to Adegbite and Shittu (Citation2017b), the incomes derived from goods and services provisions falling within SMEs activities after trade discounts, VAT, and other taxes have been deducted based on the incomes derived Turnover is the aggregate income SMEs realize from the disposal of products, minus VAT and discounts. It is calculated over a specific period, usually a quarter, daily, monthly, or annually. Turnover is useful because it provides information about SMEs businesses and finances. With the turnover, it is easy to realize the income generated daily, monthly, and annually. The findings revealed that tax aggressiveness has a negative relationship withIn addition, Soku et al. (Citation2023) used the Generalized Method of Moments (GMM) on a dataset of 65 countries to evaluate the relationship between environmental tax, carbon emission, and female economic inclusion. According to the study, enterprises with higher levels of female economic inclusion typically have environmental taxes that have a considerable negative impact on carbon emissions. Financial problems arise with SMEs when the turnover of the business cannot be properly managed and controlled. The products of any SMEs and the interaction with their customers give birth to higher turnover, which invariably dispenses profitability for the business. This also brings many customers to the company, which ultimately increases the VAT paid to the tax authority. The higher the SMEs customers, the higher the VAT paid to the tax authority because the burden of VAT falls on the final consumer of the products (Adegbite & Araoye, Citation2020). Therefore, it is hypothesized that:

H05:

Turnover generated by SMEs has no significant influence on VAT compliance.

4.6. Profit and VAT compliance

Profit refers to the income realized by SMEs when produced with custodian resources. The SMEs goal is to realize profit after product disposal. This shows the SMEs ability to generate revenue from the effective utilization of their resources within a specific period of time. Profitability involves a SME’s capacity to siphon the benefits from operational activities. According to Akanbi and Adegbite (Citation2016), to measure the growth of SME, dispense the profit at the end of the accounting year when other expenses have been deducted. More so, the impact of corporate governance on tax aggression as measured by agency problem type was investigated by Alkausar et al. (Citation2023). Profit usually acts as the SMEs ‘reward derived from the investment. Moreover, profit remains the absolute motivator for SMEs to engage in business, which is the difference between sales (income realized from the disposal of products) and total expenses, which include labor costs, material costs, and overhead costs. VAT is realized from the numbers of sales made by the SMEs, which is encouraged by the profit made on a single unit of sales. The higher the sales, the higher the profits, which is a motivator for the production of more products, which invariably beget VAT for the government (Alsughayer, Citation2021; Setyowati et al., Citation2023). It is, however, hypothesizing as follows:

H06:

Profit generated by SMEs has no significant effect on VAT compliance

4.7. Employees and VAT compliance

Employees refers to the workers employed by the organization, irrespective of whether it is a medium, small, or large organization. The essence of the employees in an organization is to exhibit their potency for the production of products to achieve the organization’s objectives. The impacts of employees in organizations are felt and cannot be underestimated because, according to Usman (Citation2019, Citation2022), employees are the backbone of SMEs due to their efficiency and effectiveness for organizational productivity. Employee contentment is pertinent to SMEs sustainability, and increased employee satisfaction enhances customer satisfaction, which ultimately leads to SMEs greater potential profitability and tenure (Reukauf, Citation2018). Wadesango and Chirebvu (Citation2020) investigated the variables that influence VAT compliance. The findings indicated that the major variables influencing VAT compliance are individual characteristics, VAT system characteristics, and environmental variables like the political and socioeconomic climate. Mohammed et al. (Citation2017) studied Nigerian SMEs and the impact of the political and business climate. The research found that variables such as employee behavior affect compliance behavior. Additionally, Alshira’h and Abdul-Jabbar (Citation2019) looked at how tax equity affected compliance with sales tax in Jordanian manufacturing SMEs. The research found, after analysis, that a significant correlation exists between tax compliance and tax fairness. In the same vein, Alognon et al. (Citation2020) used annual national data for twenty-six (26) European Union countries from 2000 to 2016 to investigate debit and credit card effects on usage and consumption (VAT) tax compliance. The research found that debit and credit cards significantly reduce tax evasion. More so, Shakkour et al. (Citation2021) used behavioral decision theory to evaluate VAT compliance using the taxpayer’s work-related capacity, personal attributes, and tax education and knowledge, as well as the audit system and tax compliance cost. The results showed that a strong positive correlation existed among VAT education, tax compliance, and individual traits. The study further concluded that a positive correlation existed between VAT compliance costs and the VAT compliance and audit systems in Jordan. The employees exhibit their potency to produce, advertise, and market the products simultaneously for the betterment of the SMEs. The products of the organization attracted the customers from whom or where the VAT is collected. The greater the efficiency, effectiveness, and productivity of the employees, the greater the customer patronage, which invariably increases VAT compliance in SMEs. However, it is hypothesized as:

H07:

There is no significant effect of SMEs employees on VAT compliance

4.8. Customers and VAT compliance

Customers refers to the number of people who patronize SMEs. They are the people targeted by the SMEs for whom their products are marketed. The number of customers in the organization determines the amount of income realized daily, monthly, annually, or periodically when the products are purchased by the customers. They bear the burden of VAT because they are the final consumers of the products. According to Reukauf (Citation2018), customer satisfaction is paramount and pertinent to the progress and profitability of SMEs. It was advocated that the enhancement of customers brings in more profit to the organization, which invariably increases compliance with VAT. Likewise, the impact of financial accounting services on the financial performance of SMEs was investigated by Gyamera et al. (Citation2023). The study used a survey approach and a quantitative strategy to gather data. For the analysis, the study used a sample of 320 SMEs. The findings show that SMEs can enhance their financial performance by employing financial accounting services. It is opined by Adegbite and Shittu (Citation2017a) that the patronage of customers in any investment increases VAT compliance because VAT is paid at every stage of the production. However, this hypothesized that:

H08:

There is no significant effect of SMEs customers on VAT compliance

4.9. SMEs size and VAT compliance

According to Csabay and Stehlikova (Citation2020), firm size is generally acceptable as a significant characteristic of SMEs structure, which also has an impact on SMEs competitiveness. It is also regarded as a determinant of SMEs innovativeness. Any changes in firm size distribution upwardly are an inevitable indicator of a progressive change in SMEs structure. Wahab et al. (Citation2018) studied how much the heterogeneity of the senior management team is associated with a firm’s level using Malaysian corporate governance legislation. The top management team’s bio-data heterogeneities are significantly associated with the firm’s book-tax disparity level. Similarly, it is noted by Doğan (Citation2013) that customer enhancement through firm size increases the level of VAT compliance of SMEs globally. Furthermore, Widianto (Citation2015), in a study conducted in Indonesia, observed that a positive, significant, and statistical effect of business size existed on revenue with reverence to tax compliance. In addition, Slemrod et al. (Citation2019) opined that there is a significant positive effect of income, sales, and size on VAT compliance. Abdul Wahab et al. (Citation2022) looked at selected Malaysian non-financial listed corporations to determine how book-tax discrepancies related to three distinct forms of risk: firm total risks, systematic risks, and idiosyncratic risks. The study found a correlation between firm total risk and book-tax differences that was positive, as well as idiosyncratic risk. Furthermore, a study on the relationship between tax transparency and sales tax evasion was carried out among Jordanian SMEs by Al-Rahamneh et al. (Citation2023), employing a quantitative approach and a survey of 400 managers and owners of SMEs. The study used the partial least squares structural equational modeling technique. The results demonstrated that sales tax was negatively impacted by tax transparency, and TCMR has a significant positive connection with SMEs tax compliance in Ghana. Thus, it is hypothesized that:

H09:

The higher size of SMEs leads to lower VAT compliance

4.10. Theoretical/Conceptual framework

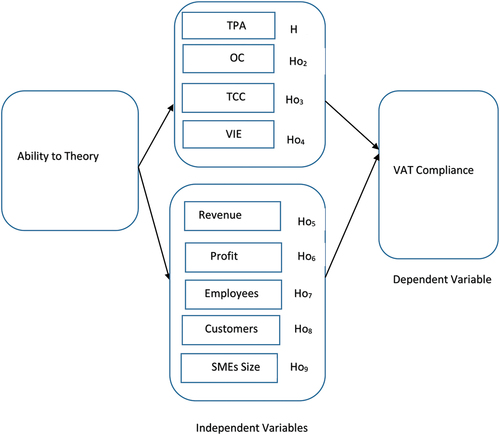

The conceptual framework in Figure below displays the interconnection between ability to pay theory, study dependent variable, and independent variables. The framework proclaims that the ability to pay has a greater influence on compliance decisions than other factors. When there is the ability to pay, it will motivate taxpayers to have a good perception or attitude toward purchasing taxable goods. The theory of ability to pay is important when enforcing VAT compliance. Many SMEs and those with high incomes may receive priority in tax authorities’ enforcement actions since they have a stronger financial capacity to pay the taxes due. This promotes the perception of a fair tax system and ensures that compliance is enforced while taking the taxpayer’s financial situation into account. The dependent variable is the VAT compliance, the independent variables are Taxpayer Perception and Attitudes (TPA), Organizational Characteristics (OC), Tax Compliance Cost (TCC), and VAT Implementation Efficacy (VIE), as well as revenue, profit, employees, customers, and SMEs size. The ability to pay theory links to these variables. The connections are that the citizens that have the ability will be interested and motivated in purchasing goods with a perception or attitude that will be predisposed by OC, TCC, and VIE. Likewise, ability to pay will influence SMEs owners to deduct VAT generated from revenue and profit, as well as the ability of employees, SMEs, and customers to improve compliance, which will eventually boost revenue generation.

Figure 1. Research design.

5. Research design

In this research, both qualitative and quantitative methods were employed. A survey approach was used to obtain the necessary primary data, while an ex-post facto research design was employed to gather the secondary data needed for the study. The population, sample size, and procedure for data collection are explained below. The questionnaire was administered to only SMEs that do not engage in goods exempt from VAT in Nigeria. Those who dealt with goods exempted from VAT were not considered because the major focus of the study is on VAT compliance.

5.1. Population, sampling and data collection

All of Nigeria’s officially registered SMEs make up the study population, and a multistage sampling technique was used in this study. There are (Micro Enterprises 41,469,947, Small Enterprises 71,288 and Medium Enterprises 1,793) in Nigeria. A stratified sampling technique was employed in order to divide SMEs in Nigeria into six geopolitical zones. In each zone, three states were randomly chosen, as shown in Appendix 2, Table , in order to capture a larger percentage of SMEs in all geographical zones, while two hundred and twenty (240) questionnaires administered to the managers and, in some cases, owners of the SMEs in every commercial center in each state were conveniently selected, totaling four thousand three hundred and twenty (4,320). Those who were not willing to answer the questionnaire were relieved. Three thousand three hundred and sixty (3,600) out of the 4,320 closed-ended and structured questionnaires that were distributed were found useful for the study. The questionnaire contains five (5) elements: demographic factor, taxpayer perceptions and attitudes, organizational characteristics, tax compliance cost, and VAT implementation efficacy, using a Likert scale of 1 to 5, where 1 means strongly disagreed and 5 means strongly agreed, adapted from the work of Sidek and Abdulraqeeb (Citation2022).

Furthermore, given a total of 18,000 observations, a panel data set of 3,600 SMEs from the years 2018 to 2022 is chosen from the financial records of selected SMEs as shown in Table . The research hypotheses were tested using ANOVA, Chi-square, MANOVA, and panel linear regression techniques. Pearson Chi-Square and ANOVA were used to determine the degree of association between taxpayer perceptions and attitudes, organization characteristics, tax compliance costs, VAT implementation efficacy, and VAT compliance among SMEs using qualitative data. Similarly, MANOVA was employed to analyze factors influencing VAT compliance. In addition, the variance inflation factor (VIF) was used to test the robustness of the data. More so, the panel least squares regression method was used as an analysis technique for the quantitative data obtained. For the purpose of robustness, the study employed a combination of cross-sectional and time series analysis. Multivariate regression methods were used using pooled or panel data. The reason for pooled or panel data is that the secondary data gathered was a mixture of cross-sectional and time series characteristics, which aided the study in determining factors influencing VAT compliance among SMEs in Nigeria.

Table 1. Sample selection for the Study in each State

5.2. Model specification

This study employs two empirical models, as illustrated below. The first model was adapted from the work of (Shakkour et al., Citation2021) with modification of additional variables such as organizational characteristics and implementation efficacy using primary data to analyse. The second model which was based on secondary data was adapted from the work of (Alognon et al., Citation2020).

5.2.1. Model 1

Y = ƒ(X), Y = dependent variables represented by VAT compliance;

X = independent variables

Therefore,

The econometric form of the model is captured as:

Where: VATC = VAT Compliance, TPA = Taxpayer Perception/Attitudes, OC = Organizational Characteristics, TCC = Tax Compliance Cost, VIE = VAT Implementation Efficacy; β0 Constant, β1, β2, β3, β4, = Slope Coefficients, £ = Error Term

5.2.2. Model 2

VAT = f(SMEs)

6. Empirical results and discussion

6.1. Demographical data of the participants

Table displays the social characteristics of respondents responses to the questionnaire shown in Appendix, Table , which cover gender, age, education, years of experience, and enterprise size. 68% of respondents were female, while 32% were male.. Likewise, 36% of respondents were between 21 and 30 years old, 44% were between 31 and 40 years old, 12% were between 41 and 50 years old, and 8% were 50 years old or older. Furthermore, 20% of the respondents had SSCE, 16% had a diploma, 52% had university certificates, and 12% had postgraduate certificates. Similarly, 24% of respondents had less than 5 years of experience, 20% had years of experience between 6 and 10, and 56% had more than 10 years of experience. This implies that the majority of the respondents are people with experience above 10 years. Furthermore, 60% of respondents were small business owners, while 40% were medium-sized business owners. Table shows the dependent and independent variables, and they were measured with references to previous authors that have measured them in the same way.

Table 2. Description and measurement of variables

Table 3. Demographics of respondents

6.2. Validity and reliability test

Table shows the results of factor analysis: Cronbach’s Alpha (CA), Composite Reliability (CR), and Average Variance Extracted (AVR). The CA and CR values of all the variables are greater than 0.7, which means that they are reliable. More so, the AVE values of the study variables are higher than 0.5, which also confirms that they are acceptable according to the standard.

Table 4. Convergence validity and instrument reliability

6.3. Factors influencing VAT compliance among SMEs

The results displayed in Table show that organization characteristics have the highest significant figure of 63.4041. This indicated that the current record-keeping system, human resources effectiveness, and learning need to be improved in order to maintain VAT compliance among SMEs. This was followed by the VAT implementation efficacy of SMEs with a Pearson chi-square value of 59.4582, which implied that time management, VAT laws, and the tax audit system include factors influencing VAT compliance among SMEs. More so, taxpayer perceptions and attitudes influence VAT compliance among SMEs, as indicated by the Pearson chi-square value of 51.7621. In the same vein, tax compliance costs also revealed a Pearson Chi-square value of 45.9013, meaning that the VAT rate, ability to pay, and unequal taxpaying cultures influence VAT compliance among SMEs.

Table 5. Factors influencing VAT compliance among SMEs

6.4. Factors influencing VAT compliance among SMEs using ANOVA

Table shows that Taxpayer Perception Attitudes (TPA) influence VAT compliance by 2.08%. Likewise, Organization Characteristics (OC) have a positive influence on VAT compliance by 0.9%. More so, Tax Compliance Cost (TCC) significantly influences VAT compliance by 2.01%. In addition, VAT Implementation Efficacy (VIE) displays a positive influence on VAT compliance by 1.3%. These decisions negated the null hypotheses of each variable on factors influencing VAT compliance; hence, all the study variables influence VAT compliance.

Table 6. ANOVA results on factors influencing VAT compliance among SMEs

6.5. Correlation matrix between factors influencing VAT compliance and VAT compliance among SMEs

Table indicates that taxpayer TPA have a positive connection with VAT compliance of 0.5475 × .This suggests that an increase in TPA will enhance VAT compliance in the country. Further, an OC also augment VAT compliance with a positive coefficient of 0.5797 × .In the same vein, TCC show a positive correlation with VAT compliance, with a coefficient of 0.7170 × .These findings imply that compliance costs determine the level of VAT compliance among SMEs. More so, VIE further displays a positive correlation with VAT compliance. This signifies that time management, VAT laws, and the tax audit system are positively correlated to VAT compliance. Having scrutinized and analyzed the correlation, it is thus sufficient to conclude that all the factors have a positive correlation with VAT compliance among SMEs in Nigeria.

Table 7. Correlation matrix between factors influencing VAT compliance among SMEs

6.6. Analysis of the effect of factors influencing VAT compliance among SMEs in Nigeria by MANOVA

A Multivariate Analysis of Variance (MANOVA) was employed to examine the significant effects of factors influencing VAT compliance on VAT compliance. The effect was discovered using four statistical parameters in MANOVA (W, P, R, and L). In accordance with Wilks’ lambda parameter, a one percent increment in TPA, OC, TCC and VIE will absolutely improve VAT compliance by 0.91%. This is further supported by Pillai’s trace, which brought out that an increase in those factors will enhance VAT compliance by 0.081%. However, the opinions of the remaining parameters (Wilks’ lambda and Lawley-Hotelling trace) are the same in the sense that both agreed on 0.088% as the effect that the variables under study will have on VAT compliance among SMEs in Nigeria. Hence, all the statistical parameters suggest that VAT compliance will increase when factors such as TPA, OC, TCC and VIE are improved. It was further supported by F (prob>F) equal to 0.0000e.

6.7. Wald test after MANOVA

To confirm the outcome of the MANOVA, the Wald test was conducted as shown in Table . The essence of this is to confirm the significant effect of factors influencing VAT compliance. Table indicates that factors such as TPA, OC, TCC and VIE will eventually increase VAT compliance when they are improved. This is advocated by Prob > F = 0.0000, which is less than the 0.05 significant level. Thus, TPA, OC, TCC and VIE will increase VAT compliance positively if they are properly monitored.

Table 8. Analysis of the effect of factors influencing VAT compliance among SMEs in Nigeria by MANOVA

Table 9. Wald test after MANOVA

6.8. Robustness test for secondary data variables

Table shows the Variance Inflation Factor (VIF) result, which revealed the mean VIF across the variables to be 1.85. Acceptable multicollinearity VIF threshold values are between 5 and 10. Thus, there is no multicollinearity problem across the study variables once all the values are less than 5.

Table 10. Variance inflation iactor

6.9. Effect of profit, turnover, employees, customers and SMEs ize on VAT compliance among SMEs

Table shows the results of panel data estimation techniques (pooled regression, robust regression, fixed effect, and random effect) on the effect of explanatory variables such as profit, revenue, employee, customer, and size on explained variables (VAT compliance). The findings showed differences in the magnitude, sign, and number of insignificant variables. The F-statistics and Wald-statistic values of 1.59 (0.00) and 2.31 (0.00) for fixed effect and random effect models, respectively, demonstrate that both models are valid for drawing inferences because they are both statistically significant at 5%. In order to select between the fixed effect and the random effect, the Hausman test was conducted. The p-value of the Hausman model is 7.48 > 0.05, and there is a correlation between error terms and explanatory variables. This indicates that the result of the random effect is statistically more appealing than the result of the fixed effect. Thus, the study made use of the random effect panel regression results to draw conclusions and make recommendations. The findings showed a positive and significant influence of profit on VAT compliance. With regards to revenue, it revealed a positive but not significant effect, while employee and customer behavior showed a negative but insignificant effect on VAT compliance. However, the size of SMEs revealed a positive and significant effect on VAT compliance.

Table 11. Panel regression result for research model 2

7. Summary and conclusion

7.1. Findings of research

The purpose of this study was to assess the factors that influence VAT compliance among SMEs in Nigeria. According to Shakkour et al. (Citation2021), in an effort to minimize tax evasion, the government employs a variety of strategies to strengthen compliance behavior among the general public. The authors opined that SMEs, comparatively, show a higher level of VAT compliance than corporate organizations. However, the authors discovered that diverse compliance is caused by a number of internal and external factors. Hence, the results of this study revealed a positive influence on perceptions and attitudes towards VAT compliance. This means that the more enthusiastic a taxpayer is about paying taxes, the more likely they are to do so. The result agrees with the findings of previous empirical studies (Fredrick & Peter, Citation2019; King’oina, Citation2016; Lourciro, Citation2016; Podlipnik, Citation2017). Similarly, the study discovers a positive effect of organization characteristics on VAT compliance among SMEs in Nigeria, which implies that organization characteristics positively influence VAT compliance. This result corroborates the outcome of the research findings in (De Neve et al., Citation2019; Sidek & Abdulraqeeb, Citation2022). Likewise, tax compliance costs also showed a positive relationship with VAT compliance among Nigerian SMEs, which means that tax compliance costs positively influence VAT compliance. The results agree with prior empirical results (Msang, Citation2015; Slemrod et al., Citation2019; Wadesango et al., Citation2018). In addition, VAT implementation efficacy showed a positive relationship with VAT compliance, which suggests that VAT implementation efficacy positively influences VAT compliance. The results agree with the research findings of Olaoye and Ekundayo (Citation2019). More so, the positive and significant effect of revenue and profit on VAT compliance implies that the more SMEs generate sales, the more they profit and comply with VAT, which supports the findings of (Lsughayer et al., 2021; Setyowati et al., Citation2023). Furthermore, the larger the SMEs, the more likely they are to comply with VAT and remit it to the appropriate authority, which corroborates the findings of (Slemrod et al., Citation2019; Widianto, Citation2015). Furthermore, negative and insignificant employee and customer numbers suggest that the more SMEs have a large number of employees and customers, the lower the VAT remitted, which negates the findings of (Reukauf, Citation2018; Shakkour et al., Citation2021).

7.2. Conclusion

One of the major setbacks confronting developing countries in collecting VAT is sometimes non-compliance by the taxpayers, particularly SMEs.Thus, according to this current study, taxpayer perception and attitude, organizational characteristics, tax compliance cost, and VAT implementation efficacy all influenced VAT compliance among SMEs. This means that the aforementioned are the determinants of VAT compliance in Nigeria. Furthermore, the study discovered that revenue has a positive but insignificant effect on VAT compliance. Revenue is only meant for SMEs and is not a determinant of the payment of VAT to regulatory authorities. More so, the size and level of profit generated have a positive and significant influence on VAT compliance by SMEs. Also, the number of employees and customers has no significant influence on VAT compliance by SMEs. Hence, the study recommended that the government, which is in charge of implementing the VAT, should play a significant role in promoting compliance by providing support to SMEs in the form of incentives, rebates, policy-organized training to raise awareness, and the creation of an environment that is conducive to SMEs’ growth and expansion of their businesses, which will eventually boost their sales revenue and increase the amount of VAT remitted to the government. Similarly, more efforts should be made by the regulatory authority to put more weight on enforcement of SMEs VAT compliance by way of punishment for defaulters. More so, the sharing formulae for VAT generated in Nigeria should be reviewed, such as the equality of 20%, population of 30%, and derivation of 50%, to enable the states’ governments to put more effort into sensitizing SME owners about VAT compliance in Nigeria.

7.3. Theoretical, practical, and policy implications of the study

The study has established the relationship between the factors influencing SMEs and VAT compliance with the aid of the ability to pay theory. Thus, the study strengthens the ability to pay theory in the sense that whoever has the capacity will purchase vatable goods, which will make SMEs generate more VAT to be remitted. Without money, citizens will not be able to purchase taxable goods from SMEs. More so, this study has contributed to existing studies by using both primary and secondary data to determine the factors influencing VAT compliance in the body of knowledge. This will be helpful to tax practitioners to help them understand the influence of VAT compliance among SMEs. In addition, the government will make use of this study to identify factors to emphasize in order to motivate SMEs to voluntarily comply with VAT. More so, it will help tax practitioners understand the area and give necessary advice to SMEs. Similarly, it will enable the FIRS, in collaboration with the Small and Medium Enterprises Development Agency of Nigeria (SMEDAN), to organize training for SMEs in Nigeria. More so, the two most prominent taxation professional bodies in Nigeria, the Institute of Chartered Accountants of Nigeria (ICAN) and the Chartered Institute of Taxation of Nigeria (CITN), in conjunction with the Ministry of Trade and Industry, can focus on accountancy and taxation programmes that will sensitize SMEs on VAT compliance.

7.4. Limitations and recommendations for further studies

Though this research succeeded in answering the stated objectives of the study, there are still some limitations that need to be developed through further research. For instance, primary data were collected from a single respondent, who is the owner of an SME, using a self-administered survey method, which may have skewed the outcome of the study. Future studies can collect data from tax authorities as well to get an accurate picture of respondents’ actual behavior. More so, this study only based its empirical findings on the compliance of SMEs with VAT in Nigeria. However, corporate organizations could also be considered in the future study to examine how they are complying with VAT compliance. Similarly, three states were selected from each geo-geographic zone. A future study can cover all the states in Nigeria to obtain data for the study. More so, the study was carried out in Nigeria, while further study can consider two or more countries with the same tax system. Future research should consider additional factors such as culture and religion, which may also have an influence on VAT compliance, to extend the research model. Similarly, future studies can also focus on compliance with other indirect taxes, such as excise taxes and customs fees.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Acknowledgments

We would like to thank the Tertiary Education Trust Fund, Nigeria, for financing this research project. We are indeed grateful for the grant, without which we would not be able to carry out the research. Our appreciation goes to the participants at the 3rd International Conference organized by the Faculty of Management Sciences, Bayero University, Kano, Nigeria held between January 10 and 12, 2023, for their constructive feedback on this research work.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Azeez Olasunkanmi Ojo

Azeez Olasunkanmi OJO is a Chief Lecturer at the Federal Polytechnic in Ayede, Oyo State, Nigeria. He has published journal articles in reputable local and international journals. Formerly, he was an Editor at the Ede Journal of Business (E-JOB), a publication of the School of Business Studies, Federal Polytechnic Ede, Nigeria. He is the current Dean of the School of Management Sciences at the Federal Polytechnic Ayede in Oyo State, Nigeria. Email: [email protected]

Saheed Akande Shittu

Saheed Akande Shittu has a PhD in Accounting from Ladoke Akintola University of Technology, Ogbomoso, Nigeria. He is a member of the Association of Accounting Technicians of West Africa (AATWA), the Institute of Chartered Accountants of Nigeria (ICAN), and the Chartered Institute of Taxation of Nigeria (CITN) and is currently the Ag. Head, Department of Accountancy, Federal Polytechnic Ayede, Oyo State, Nigeria. His area of research includes earnings management, corporate tax policy, and financial reporting. E-mail: [email protected]

References

- Abdul Wahab, N. S., Ntim, C. G., Tye, W. L., & Shakil, M. H. (2022). Book-tax differences and risk: Does shareholder activism matter? Journal of International Accounting, Auditing & Taxation, 48, 100484. https://doi.org/10.1016/j.intaccaudtax.2022.100484

- Adegbie, F. F., Enerson, J., & Olaoye, S. A. (2022). An empirical investigation into the relationship between electronic tax management system and tax revenue collection efficiency in selected states in South West, Nigeria. Archives of Business Research, 10(4), 93–25. https://doi.org/10.14738/abr.104.12195

- Adegbite, T. A., & Araoye, F. E. (2020). Value Added Tax (VAT) revenue and imported goods: Nigeria experience. 6(3), 22–29.

- Adegbite, T. A., & Shittu, S. A. (2017a). The analysis of the impact of corporate income tax on investment in Nigeria. World Wide Journal of Multidisciplinary Research Development, 3(3), 60–64.

- Adegbite, T. A., & Shittu, S. A. (2017b). The impact of value added tax on private investment in Nigeria. Account and Financial Management Journal, 2(4), 644–651. https://doi.org/10.18535/afmj/v2i4.03

- Adeniji, A. A., & Olowookere, A. E. (2018). Value-Added Tax (VAT) Compliance by Small and Medium enterprises (SMEs) in Nigeria: A review of the challenges and prospects. International Journal of Economics, Commerce and Management, 6(12), 88–105.

- Adeyemo, K. A., & Oyedele, A. O. (2018). Value-added tax compliance and small and medium enterprises performance in Nigeria. Research Journal of Finance & Accounting, 9(6), 184–193. https://doi.org/10.15640/ijat.v6n2a4

- Agbo, E. I., & Nwadialor, E. O. (2020). The genesis and development of value added tax administration: Case study of Nigeria. International Journal of Academic Research in Accounting, Finance and Management Sciences, 10(2), 15–30. https://doi.org/10.6007/IJARAFMS/v10-i2/7266

- Akanbi, T. A., & Adegbite, T. A. (2016). Analysis of the effect of financing on profitability of Small and Medium Enterprises (SMES) in Nigeria: Lagos State outlook. International Journal of Marketing and Technology, 6(8), 1–13.

- Akinlabi, B. H., & Oyedele, O. P. (2019). Value-added tax compliance by small and medium enterprises in Nigeria: A study of selected firms in Lagos state. African Journal of Accounting, Auditing and Finance, 8(1), 1–16.

- Akumbo, S., Mbilla, E., Abiire, M. A., Atindaana, P. A., Ayimpoya, R. N., & Polytechnic, B. (2020). Tax Education and Tax Compliance in Ghana. 8(1), 1–22.

- Alabede, J. O., Zainal Affrin, Z., & Idris, K. M. (2011). Individual taxpayers’ attitude and compliance behaviour in Nigeria: The moderating role of financial condition and risk preference. Journal of Accounting and Taxation, 3(1), 91–104. https://doi.org/10.22164/isea.v5i1.54

- Aladejebi, O., & Oladimeji, J. A. (2019). The impact of record keeping on the performance of selected small and medium enterprises in Lagos metropolis. Journal of Small Business and Entrepreneurship Development, 7(1), 28–40. https://doi.org/10.15640/jsbed.v7n1a3

- Alkausar, B., Nugroho, Y., Qomariyah, A., & Prasetyo, A. (2023). Corporate tax aggressiveness: Evidence unresolved agency problem captured by theory agency type 3. Cogent Business & Management, 10(2), 2218685. https://doi.org/10.1080/23311975.2023.2218685

- Alm, J., Kirkchler, E., Muehlbacher, S., Gangl, K., Hofmann, E., & Kogler, C. (2012). Rethinking the research paradigms for analysing tax compliance behaviour. CESifo Forum, ISSN 2190-717X, ifo Institut – Leibniz Institutfür Wirtschaftsforschung an der Universität München, München, 13(2), 33–40. http://hdl.handle.net/10419/166479

- Alognon, A. D., Koumpias, A. M., & Martinez-Vazquez, J. (2020). The impact of plastic money use on VAT compliance: Evidence from EU countries. https://scholarworks.gsu.edu/icepp/132.

- Al-Rahamneh, N. M., Al Zobi, M. K., & Bidin, Z. (2023). The influence of tax transparency on sales tax evasion among Jordanian SMEs: The moderating role of moral obligation. Cogent Business & Management, 10(2), 2220478. https://doi.org/10.1080/23311975.2023.2220478

- Alshira’h, A. F., & Abdul-Jabbar, H. (2019). The Effect of Tax Fairness on Sales Tax Compliance among Jordanian Manufacturing SMEs. Academy of Accounting & Financial Studies Journal, 23(2), 364–375.

- Alsughayer, S. A. (2021). VAT compliance challenges among SMEs: Evidence from Saudi Arabia. Journal of Accounting, Finance & Auditing Studies, 7(3), 34–59. https://doi.org/10.32602/jafas.2021.018

- Amanamah, R. B. (2016). Tax compliance among small and medium scale enterprises in Kumasi Metropolis, Ghana. Journal of Economics & Sustainable Development, 7(16), 5–16. https://core.ac.uk/download/pdf/234647611.pdf

- Bentham, J., Burns, J. H., Hart, H. L. A. (1789). An introduction to the principles of morals and legislation. Econlib Book. https://doi.org/10.1093/oseo/instance.00077240

- Benzarti, Y., & Dorian, C. (2019). Who really benefits from consumption tax cuts? Evidence from a Large VAT reform in France. American Economic Journal: Economic Policy, 11(1), 38–63. https://doi.org/10.1257/pol.20170504

- Chartered Institute of Taxation of Nigeria (CITN) Report. (2022). https://portal.citn.org/administration-of-value-added-tax-in-nigeria-goods-and-servicesexempt.

- Chelliah, S., Pandian, S., Sulaiman, M., & Munusamy, J. (2010). The moderating effect of firm size: Internationalization of small and medium enterprises (SMEs) in the manufacturing sector. African Journal of Business Management, 5(July 2014). https://doi.org/10.5539/ijbm.v5n6p27

- Csabay, M., & Stehlikova, B. (2020). Firm size distribution and the effects of ownership type. Journal of Competitiveness, 12(4), 22–38. https://doi.org/10.7441/joc.2020.04.02

- Dabić, M., Lažnjak, J., Smallbone, D., & Švarc, J. (2019). Intellectual capital, organisational climate, innovation culture, and SME performance: Evidence from Croatia. Journal of Small Business and Enterprise Development, 3(5), 189–201. https://doi.org/10.1108/JSBED-04-2018-01173

- De Neve, J.-E., Imbert, C., Spinnewijn, J., Tsankova, T., & Luts, M. (2019). How to improve tax compliance? Evidence from population-wide experiments in Belgium. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3389405

- Doğan, M. (2013). Does firm size affect the firm profitability? Evidence from Turkey. Research Journal of Finance & Accounting, 4(4), 53–60.

- Emmanuel, G., Williams, A. A., Ivy, E., Akwetey, H. M., Lexis, A. T., & Paul, K. A. (2023). An analysis of the effects of management accounting services on the financial performance of SME: The moderating role of information technology. Cogent Business & Management, 10(1), 2183559. https://doi.org/10.1080/23311975.2023.2183559

- Eniola, A. A., & Ektebang, H. (2014). SME firms performance in Nigeria: Competitive advantage and its impact. International Journal of Research Studies in Management, 3(2), 75–86. https://doi.org/10.5861/ijrsm.2014.854

- Eragbhe, E., & Aronmwan, E. J. (2015). Taxpayers Income, Tax Payers Attributes and Personal Income Tax Compliance. African Journal of Management Sciences, 4(5), 95–111.

- Eragbhe, E., & Omoye, A. S. (2014). SME characteristics and value added tax compliance costs in Nigeria. Mediterranean Journal of Social Sciences, 5(20), 614–620. https://doi.org/10.5901/mjss.2014.v5n20p614

- Fagbemi, T. O., & Abogun, A. (2015). Factors influencing voluntary tax compliance of small and medium scale enterprises in Kwara state, Nigeria. Entrepreneurial Journal of Management Sciences, 3(1), 62–77. http://hdl.handle.net/123456789/3988

- Fauziati, P., & Kassim, A. A. M. (2018). The effect of business characteristics on tax compliance costs. Advanced Science Letters, 24(6), 353–358. Microsoft Word - msl_2018_26.docx (growingscience.com). https://doi.org/10.1166/asl.2018.11608

- Finance Bill. (2022). House of Representatives Committee on Finance National Assembly complex, Abuja, Nigeria.An Invitation to One Day Public Hearing and Submission of Memoranda on the 2022 Finance Bill .

- Fredrick, W. W., & Peter, O. I. (2019). The influence of demographic factors on tax payercompliance in Uganda. The International Journal of Academic Research in Business & Social Sciences, 9(9), 537–557. https://doi.org/10.6007/IJARBSS/v9-i9/6328

- Ghasia, B. A., Wamukoya, J., & Otike, J. (2017). Managing business records in small and medium enterprises at Vigaeni ward in Mtwara-Mikindani municipality, Tanzania. International Journal of Management Research and Reviews, 7(10), 974–986. https://www.proquest.com/openview/fe167c038479603fea7eed382c876002/1?pq-origsite=gscholar&cbl=2028922

- Gherghina, Ș. C., Botezatu, M. A., Hosszu, A., & Simionescu, L. N. (2020). Small and medium-sized enterprises (SMEs): The engine of economic growth through investments and innovation. Sustainability, 12(1), 347.

- Gilligan, G., & Richardson, G. (2005). Perception of tax fairness and tax compliance in Australia and Hong Kong-A preliminary study. Journal of Financial Crime, 12(4), 331–342. https://doi.org/10.1108/13590790510624783

- Gyamera, E., Atuilik, W. A., Eklemet, I., Adu-Twumwaah, D., Issah, A. B., Tetteh, L. A., & Gagakuma, L. (2023). Examining the effect of financial accounting services on the financial performance of SME: The function of information technology as a moderator. Cogent Business & Management, 10(2), 2207880. https://doi.org/10.1080/23311975.2023.2207880

- Habes, M. (2019). The influence of personal motivation on using social TV: A uses and gratifications approach. International Journal of Information Technology and Language Studies, 3(1), 32–39. http://journals.sfu.ca/ijitl

- Halim, H. A., Ahmad, N. H., & Ramayah, T. (2019). Sustaining the innovation culture in SMEs: The importance of organisational culture, organisational learning and market orientation. Asian Journal of Business Research, 9(2), 14–26. https://doi.org/10.14707/ajbr.190059

- Hofmann, E., Voracek, M., Bock, C., & Kirchler, E. (2017). Tax compliance across sociodemographic categories: Meta-analyses of survey studies in 111 countries. Journal of Economic Psychology, 62, 63–71. https://doi.org/10.1016/j.joep.2017.06.005

- Holcombe, R. G. (2010). The value added tax: Too costly for the United States. Mercatus Center at George Mason University Journal, 16. https://wwwmercatus.org/system/files/VAT.Holcombe.pdf

- Inim, V. E., Udoh, F. S., & Ede, U. S. (2020). Taxation and the Growth of Small and Medium Enterprises in Nigeria. Asian Journal of Social Sciences and Management Studies, 7(3), 229–235. https://doi.org/10.20448/journal.500.2020.73.229.235

- Institute of Chartered Accountants of Nigeria (ICAN). (2022). Technical Bulleting on Entrepreneurship & SMEs-Bookkeeping, Taxation & Relevant Laws. Research and Technical Department, 4(1), 1–5.

- Jensen, S. (2018). Policy implications of the UAE’s economic diversification strategy: Prioritising national objectives. Economic Diversification in the Gulf Region, 2, 67–88. https://doi.org/10.1007/978-981-10-5786-1_4

- King’oina, J. O. (2016). Factors influencing value added tax compliance among the construction firms in Kisumu County, Kenya, Unpublished project submitted in partial fulfilment of the requirements of award of the degree of master of business administration (finance option) of the school of business. of the University of Nairobi.

- Kirti, D., Parsa, H. G., Rahul, A. P., & Milos, B. (2014). Change in consumer patronage and willingness to pay at different levels of service attributes in restaurants: A study in India. Journal of Quality Assurance in Hospitality & Tourism, 15(2), 149–174. https://doi.org/10.1080/1528008X.2014.889533

- Lim, D. S., Morse, E. A., & Yu, N. (2020). The Impact of the global crisis on the growth of SMEs: A resource system perspective. International Small Business Journal, 38(6), 492–503. https://doi.org/10.1177/0266242620950159

- Loureiro, J. (2016). The role of identifiability, geographical distance and social norms on tax compliance: An experimental study. In Universidade do Porto (Issue September).

- Marandu, E. E., Mbekomize, C. J., & Ifezue, A. N. (2015). Determinants of tax compliance: A review of factors and conceptualizations. International Journal of Economics and Finance, 7(9). https://doi.org/10.5539/ijef.v7n9p207

- Mohammed, N., Hijattulah, A., & Idawati, I. (2017). VAT Compliance and the Influence of Political and Business Environment: A Proposed Framework for Nigerian SMEs. Asian Journal of Business Management Studies, 8(2), 13–20.

- Msangi, S. Y. (2015). Evaluation and Analysis of Value Added Tax (VAT) compliance: A Case Study of Small and Medium Enterprises in Tanzania. M.Sc. Thesis, University of Southampton.

- Msangi, S. Y. (2015). Evaluation and Analysis of Value Added Tax (VAT) compliance: A Case Study of Small and Medium Enterprises in Tanzania. MSc. University of Southampton.

- Muda, S., & Rahman, M. (2016). Human capital in SMEs life cycle perspective. Procedia Economics and Finance, 35(6), 683–689. https://doi.org/10.1016/S2212-5671(16)00084-8

- Mu, R., Fentaw, N. M., & Zhang, L. (2022). The impacts of value-added tax audit on tax revenue performance: The mediating role of electronics tax system, evidence from the Amhara Region, Ethiopia. Sustainability, 14(10), 6105. https://doi.org/10.3390/su14106105