?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper aims to examine financial literacy, investment decisions and personal financial management nexus among the Small and Medium Enterprises (SMEs) employees in the private sector in Ghana. The study employed a structured questionnaire with close-ended questions to collect data from 400 respondents using convenience sampling approach. The study adopted a Partial Least Square Structural Equation Model (PLS-SEM) for analysis. The results of the study reveal a positive significant link between personal financial management and financial literacy; a positive significant correlation between investment decision and personal financial management; and a mediated effect of investment decision between financial literacy and personal financial management. This implies that individuals need to receive training in appropriate money management techniques in order to foster a more competitive and effective market for consumption and savings. The theoretical contribution of this study follows the theory of planned behavior phenomenon where the psychology factors influence the investment decisions of individuals. This present study originates by examining financial literacy, personal financial management and investment decision nexus among private sector employees.

1. Introduction

The business world has experienced rapid development, growth and expansion where many sectors, including the financial sector, are now being digitalized (Shahab et al., Citation2018; Utami et al., Citation2021). Conventional approach in financial services has faced some challenges as more people are influenced by the advancement in technology which manifests in how they invest their money (Copur & Gutter, Citation2019). The need for careful and meticulous financial literacy vis-a-vis personal financial management has become pivotal in balancing the rapid growth in technology and the ability to make good investment decisions. That is financial literacy is very essential for the survival of every human being (Pangestu et al., Citation2020). Financial literacy deficiencies go a long way to affect individual’s daily money management and their ability to make savings for their long-term goals (Tahir et al., Citation2021).

Individuals with higher level of financial literacy are better equipped to manage their personal finances, making informed decisions and achieve their financial goals (Lusardi et al., Citation2014). This means financial literacy is essential for individual well-being and decision making. It involves budgeting, savings, investments, and risk management that are crucial for individuals, households, and organizations during their developmental process (Fazal, Citation2017). Due to the multi-faceted nature of financial products and services financial markets offer, it becomes important to possess sufficient knowledge to navigate them effectively and efficiently. Oteng (Citation2019) argues that making wise investment decisions requires a certain level of financial literacy. That is potential and current investors or shareholders must be knowledgeable about investment decision to be able to evaluate the prospects of investments, the profitability of business based on their capital and returns, the time they will stick their money in long term or short term, the risk of investing in specific industries and the opportunities they have in order to make optimum revenues and gains from their investments in the future (Alaaraj & Bakri, Citation2020).

Financial literacy is one of the globally recognized fundamental tools for economic development. Pangestu et al. (Citation2020) posit that if every fellow citizen was financially literate and capable of making appropriate economic decisions, it would not be an exaggeration when one says the country is prosperous. That is, financially literate population contributes to a healthier economy where they are more likely to engage in productive financial activities such as: investing in education, setting-up businesses or participating in the formal financial system which spur economic growth, create employment opportunities and reduce poverty (Lusardi et al., Citation2014). Financial literacy is not limited to making good investment decisions only, it also guides individuals in assessing, evaluating and making appropriate retirement plans which will serve as a reliable source of income in the long term (Copur & Gutter, Citation2019). Lusardi et al. (Citation2018) posit that appropriate retirement plans are very imperative because most people who failed to do so arrive close to retirement carrying a lot more debt than previous generations did. Though some individuals may be financially literate, their failure to make investment can have an impact on their long-term financial objectives. This means investment decisions could mediate financial literacy and personal financial management of individuals who have their personal finances at heart.

Personal financial management can be viewed as the process of controlling income and organizing expenses through a detailed financial plan and is considered a crucial variable between financial literacy and investment decision as it has the potential to be influenced by both financial literacy and investment decision (see Ansar et al., Citation2019; Baihaqqy et al., Citation2020; Kumari, Citation2020; Refera et al., Citation2018). It involves learning to keep track of cash inflows and tailoring the use of the inflows to fit expenses. Personal financial management provides a systematic way of utilizing income. Many studies have investigated the relationship between financial literacy and investment decisions (see Alaaraj & Bakri, Citation2020; Baihaqqy et al., Citation2020; Hamza & Arif, Citation2019; Kumari, Citation2020); and also the relationship between financial literacy and personal financial management (see Ansar et al., Citation2019; Humaidi et al., Citation2020, Novitasari et al., Citation2021 and; Refera et al., Citation2018; Yogasnumurti et al., Citation2021). However, the link between these three variables was isolated by literature (see Baihaqqy et al., Citation2020; Kumari, Citation2020; Alaaraj & Bakri, Citation2020; Hamza & Arif, Citation2019; Humaidi et al., Citation2020, Novitasari, Citation2021 and; Yogasnumurti et al., Citation2021) specifically among private sector employees in Ghana. The attitude, subjective norms and perceived behavioral and psychology factors that seek to explain the relationship between financial literacy, personal financial management and investment decision nexus failed to be addressed in existing literature (Ajzen, Citation1985). What is the relationship between financial literacy and personal financial management among private sector employees in Ghana? Does the level of financial literacy influence investment decisions among private sector employees in Ghana? How does investment decision impact personal financial management? Is there a mediating role of investment decision between financial literacy and personal management among the private sector employees in Ghana? Existing literature fails to provide empirical answers to these questions which calls for further studies. In the light of this, the study identifies a knowledge gap and seeks to conduct an empirical study to reveal the mediation of financial literacy and personal financial management by investment decisions. The objectives of this study are not farfetched, that is: – to examine the relationship between financial literacy and personal financial management; to explore the relationship between financial literacy and investment decision; to explain the relationship between investment decision and personal financial management; and finally, to investigate the mediating role of investment decision between financial literacy and personal financial management – all in the context of private sector employees in Ghana.

On the empirical front, the study contributes to existing literature by focusing on the Small and Medium Enterprises (SMEs) in the private sector by engaging employees through a structured questionnaire with close-ended questions based on the research objectives; to assess the mediation of financial literacy and personal financial management by investment decisions; the relationship between financial literacy and personal financial management; and financial literacy and investment decision. The contribution of this study is theoretically providing a theoretical phenomenon to the theory of planned behavior in terms of investment decision and personal financial management of employees within the SMEs in Ghana. From the locus of methodology, the study used Partial Least Squares Structural Equation Modeling (PLS-SEM) to test the hypotheses of the study. In similar empirical research, Abdullah and Tursoy (Citation2023) and El Gammal et al. (Citation2020) support the suitability of this approach with the study’s objectives. This methodology distinguishes this study from others that use simple or cross-sectional regression, as well as a wide range of statistical techniques, such as multiple regressions, factor analysis, and analysis of variance (Abdullah & Tursoy, Citation2023; El Gammal et al., Citation2020). Consequently, this study seeks to make the following specific contributions to existing literature: firstly, the study seeks to provide a general empirical evidence by filling the existing gap in literature which will serve as basis for further studies of the constructs. Also, the study seeks to add to the body of knowledge on the nexus of financial literacy, investment decision and personal financial management drawing from the theory of planned behavior. To the best of our knowledge, even though the theory of planned behavior has been used to individually explain the variables of this study, none has explained financial literacy, investment decision and personal financial management in a single study. Therefore, this will make a significant contribution to existing literature.

This paper is organized as follows. The next section presents a brief background of the study. Section three presents the theoretical review whereas the section four contains the empirical literature review and hypothesis development of the study. Section five presents the research design and section six presents the data analysis and discussion of results. Finally, conclusions and implications of the study are presented in section seven.

2. Background

The need for acquiring financial literacy has taken a pivotal shift in the twenty-first century where individuals are more concerned about their personal finances than ever before (Lusardi, Citation2019). Life expectations rising, straining of social welfare systems and pension plans such as the debt restructuring or hair-cut in pension funds- as evidenced in the current case of Ghana; 2022 and 2023. The aggression from the holders of such securities has potential influence on their decision to invest in government securities. The need for individuals to find alternative means of investing their funds to secure their retirement period and earn a considerable return on their investment has become necessary. Lusardi (Citation2019) argued that in many countries, employer-sponsored benefit pension plans are swiftly giving way to private defined contribution plans which is subsequently shifting the responsibility for retirement saving and investment from employers to employees. That is, employees are taking their fate into their own hands by evaluating and making appropriate investment plans that will adequately secure their retirement period. In effect, within the context of rapid changes and development in the financial sector, Lusardi (Citation2019) proposed that it is essential to understand whether individuals possess the needed skills to effectively navigate the maze of daily financial decisions they face; within the context of a broader economy. That is the investment decision of individuals is also influenced by the policy reforms and developments within the economy (Lusardi, Citation2019). In Ghana, significant portion of the population lacks adequate financial literacy. The World Bank’s Global Findex database indicates that in 2017, only 34% of Ghanaian adults had basic financial knowledge and understanding of financial concepts. This not only deprives them the ability to make good financial decisions but also has financial and economic development implications on the country (Khan et al., Citation2022).

The scope of this study was limited to the employees of Small and Medium Scale Enterprises (SMEs) in the Greater Accra Region of Ghana. According to Ghana Statistical Service IBES Report, 2017; approximately 1,823,070 individuals were employed by the private sector which forms about 87% of the working group. Ghana, in perspective, has faced quite a number of financial crises; the latest among these crises is the debt exchange (i.e., hair-cut) which caused panic and fear among investors. Most people became conservative and reserved by making investments for fear of losing their money. Due to the relationship between financial literacy and economic development (Lusardi et al., Citation2014), the impact of this relationship among the employees of SMEs will be significantly representative hence justifies the context of this study.

This provides further justification for general objectives of this study - to investigate the relationship between financial literacy and personal financial management; mediating for investment decision among the private sector employees.

3. Theoretical literature review

Existing literature has discussed theories that sought to explain the relationship between financial literacy among individuals and their ability to make good and profitable investment decisions (see Doran et al., Citation2010; Kumari, Citation2020; Sivaramakrishnan et al., Citation2017). Theories such as the consumer socialization theory, social cognitive theory and the theory of planned behavior were mentioned among the behavioral theories to explain this relationship (see Doran et al., Citation2010; Kumari, Citation2020; Sivaramakrishnan et al., Citation2017). The studies by Sivaramakrishnan et al. (Citation2017), Doran et al. (Citation2010), Kumari (Citation2020) with behavioral theory underpinning (social cognitive and theory of planned behavior) indicated that subjective and objective financial literacies are significant influencers of investment intentions to predict actual investment in the stock market. When making investment decisions, cognitive biases have an effect on people by making them depend excessively on predicted observations and previous experiences while discounting information that they deem implausible and failing to consider the big picture (Oteng, Citation2019). This implies that cognitive factors in relation to financial literacy consciously or unconsciously guide individuals to partially interpret and read meanings into the investment information available. Despite high level of financial literacy among some finance professors and their insight regarding market efficiency and significant optimal investment strategy driven by behavioral factors, their investment participation is not accounted for in the stock market (Doran et al., Citation2010). The theory of planned behavior (see Sara et al., Citation2023; Sulistianingsih & Santi, Citation2023) is also related to the consumer socialization theory which predicts that communication among consumers affects their cognitive, affective, and behavioral attitudes (Ward, Citation1974). Through socialization with financial literates, individuals get to acquire knowledge on financial literacy and the related skills to adopt good financial management practices which will help in making good investment decisions.

This study is therefore anchored on the Theory of Planned Behavior (TPB); proposed by Ajzen (Citation1985) which explains the relationship between human behavior and their decision making. The study by Sulistianingsih and Santi (Citation2023) with TPB underpinning postulates that investor psychology factors have significant influence on investing. TPB explains this relationship with the attitudes (A), the subjective norms (SN) and the perceived behavioral control (PBC) of individuals as factors which influence decision-making. The negative or positive evaluations of the outcomes or consequences of making a particular investment decision have an influence on the personal financial management of an individual irrespective of the level of financial literacy: Attitude (A). The social influence or pressure of significant people (such as family, friends, or colleagues) on the dimensions of financial literacy (i.e., financial knowledge, financial attitude, and financial behavior) can also inform personal financial management practices of an individual: Subjective Norms (SN). Then again, the individual’s perception of their ability to put their financial literacy skill to use by managing their personal finances through profitable investment decision is also explained by the third facet of TPB: Perceived Behavioral Control (PBC). Financial decisions made by individual investors are not only based on company values but driven by their emotions (Sulistianingsih & Santi, Citation2023). Narrowing this further to the context of this study, the attitude of private sector employees to evaluate the outcomes (positive or negative) of making investment in a particular investment portfolio will influence their personal financial management. They may prefer less risky investment portfolios that will maximize their returns. The attitude of individuals, based on their level of financial literacy, towards personal financial management, their subjective norms and perceived behavioral control over their intention to make investment decisions reveals four thematic areas which direct the study’s hypothesis development. These thematic areas are consistent with the general objective of the study to examine the nexus of financial literacy, investment decision and personal financial management. The foregoing discussion therefore, reveals the relationship between Financial Literacy and Personal Financial Management; the relationship between Financial Literacy and Investment Decision; the relationship between Investment Decision and Personal Financial Management and finally, the Mediation of Financial Literacy and Personal Financial Management by Investment Decision.

4. Empirical literature review and hypothesis development

4.1. Financial literacy and personal financial management

Financial literacy is the ability to understand and effectively use various financial skills, including personal financial management, budgeting, and investing to make effective decisions across a range of financial contexts to improve the financial well-being of individuals (Lusardi, Citation2019). Several studies were conducted to investigate the relationship between financial literacy and financial management and have discovered a significant effect (see Refera et al., Citation2018; Ansar et al., Citation2019; Humaidi et al., Citation2020, Novitasari, Citation2021 and; Yogasnumurti et al., Citation2021). Refera et al. (Citation2018) conducted a study to examine the relationship between financial literacy and personal financial management practices based on the evidence from the survey of Urban Dwellers in Addis Ababa, Ethiopia. The study used primary data from 402 urban dwellers and the results of the analysis showed that there was a positive relationship between financial literacy and financial behavior. The study emphasized that there was the need for comprehensive national studies to incorporate the context of rural population in order to support the ongoing financial literacy enhancement efforts in Ethiopia. The findings of Refera et al. (Citation2018) was also confirmed by Ansar et al. (Citation2019) which investigated the relationship between future orientation and financial literacy toward personal financial management practices among Generation Y in Malaysia. The study was specifically focused on those who were born between 1981 and 2001 and come from selected regions. A total of 146 valid questionnaires were used for the analysis using the Structural Equation Modelling (SEM) techniques. The findings of the study displayed that future orientation and financial literacy have a significant positive effect on personal financial management practices. Even though Refera et al. (Citation2018) and Ansar et al. (Citation2019) have consistent findings, both studies paid no specific attention to private sector employees but had a wider scope. Humaidi et al. (Citation2020) sought to examine the effect of financial technology, demographics and financial literacy on the financial management of the productive age population in Surabaya. The study used primary data from the questionnaire used to collect data from 180 respondents selected by way of judgmental sampling. The study employed SPSS for the data analysis and the results of the study reveal that the variables demographics such as sex, age and income did not have any influence on the financial management behavior in Surabaya however, financial literacy and financial technology have a significant positive effect on financial management. This study was skewed to financial-technology and demographic characteristics hence failed to limit the scope to SME employees. Also, Novitasari et al. (Citation2021) analyzed the effect of financial literacy, parents’ economic and student lifestyle on students’ personal financial management. The results of the study demonstrate that financial literacy has a significant effect on students’ personal financial management. In a related study by Yogasnumurti et al. (Citation2021) which focused on investigating whether there is an influence between the level of financial literacy of college students on personal financial management at the Faculty of Economics and Islamic Business UINSU-Medan. The findings of the study show that financial attitude and financial literacy have a positive and significant effect on personal financial management.

It can be observed from literature that financial literacy cannot be studied in isolation of its relationship with personal financial management due to the significant relationship that exists between the two. However, no specific study has private sector employees in scope to investigate the relationship between financial literacy and personal financial management. Studies reviewed above provide the basis for developing the first hypothesis and hence predict that there is a positive relationship between financial literacy and personal financial management among private sector employees in Ghana.

H1:

There is a significant relationship between financial literacy and personal financial management among private sector employees.

4.2. Financial literacy and investment decision

Kumari (Citation2020) defined financial literacy as the possession of knowledge and skills that enable informed and effective money management. The relationship between financial literacy and investment decision is very crucial and cannot be disregarded in this study. Many studies have been conducted to investigate the effect of financial literacy on investment decisions and have found a positive and significant relationship however there exists a gap which requires further studies.

For instance, Baihaqqy et al. (Citation2020) sought to describe how the educational level of investors influences their understanding of financial literacy and its effect on investment decision-making in capital markets with the use of a quantitative descriptive design. Data collection was conducted from January to February 2020 with the use of questionnaires by engaging 108 investors who were members of PT Bursa Efek, Indonesia. The findings of the study reveal that there is a significant correlation between the investor education level and their understanding of financial literacy which subsequently influences their financial decisions. Baihaqqy et al. (Citation2020) posit that in order to make an investment decision in the capital markets, knowledge of financial literacy is necessary. This was confirmed in Kumari (Citation2020) who examines the impact of financial literacy on investing decisions among undergraduates in the western province in Sri Lanka. The study focused on how the students’ level of financial literacy influenced their financial opinions, decisions and practices. A total of 200 students from four public universities in the western province of Sri Lanka participated in the study. The findings of the study revealed that financial literacy positively and significantly influences the investment decisions. Alaaraj and Bakri (Citation2020) also sought to examine the effect of financial literacy on investment decision-making among investors in South Lebanon by expressing financial literacy in terms of knowledge and awareness while investors’ decision-making is described as the act of investors in the attempt to interpret, anticipate, investigate and assess the steps and transaction for decision-making. For the purpose of the research objective, the study adopted a quantitative approach in which 150 self-administered questionnaires were collected using convenience sampling and analyzed with the use of SPSS. The results of the study showed a positive and a significant relationship between financial literacy and investment decision making. Thus Baihaqqy et al. (Citation2020) and Alaaraj and Bakri (Citation2020) have consistent findings and are related but have different country-scope which leaves a gap in the Ghanaian context.

In a related study but with contradictory findings, Hamza and Arif (Citation2019) examine the impact of financial literacy on investment decisions with the mediating effect of personality traits based on the big-five model. The study used data collected from 235 respondents from Karachi with the use of a convenience sampling technique for analysis. The results of the study reveal that financial literacy did not have a significant effect on investment decisions through agreeableness, conscientiousness and extraversion. The findings further reveal that financial literacy has a significant negative impact on investment decisions. This adds up to literature in order to build on the understanding of investor behavior from the perspective of the big-five personality traits.

From the studies reviewed above, it can be observed that financial literacy has a positive and significant relationship with investment decisions (see Alaaraj & Bakri, Citation2020; Baihaqqy et al., Citation2020; Kumari, Citation2020) except for Hamza and Arif (Citation2019) who, from the perspective of personality traits, posit otherwise. However, no specific study focused on the Ghanaian context to investigate this relationship. The study therefore formulates its second hypothesis and predicts that there is a significant relationship between financial literacy and investment decision among private sector employees in Ghana.

H2:

There is a significant relationship between financial literacy and investment decision among private sector employees.

4.3. Investment decision and personal financial management

Investment decision can play a central role where personal financial management practices such as financial behavior can influence investment decisions. Several studies have examined the relationship between investment decision and other variables such as financial literacy, financial behavior, risk and other variables (see Alaaraj & Bakri, Citation2020; Arianti et al., Citation2018; Baihaqqy et al., Citation2020; Fernando & Pribadi, Citation2022; Kumari, Citation2020; Wangi & Baskara, Citation2021) and have established significant relationships. Some studies also posit that there is a significant relationship between investment decision and financial behavior.

For example, Fernando and Pribadi (Citation2022) sought to examine the impact of financial behavior, financial literacy, income and financial risk tolerance in the case of Surabaya University Students’ investment decision. The study employed an online survey to gather data from 224 respondents and analyzed the data using Binary Logistic regression through IBM SPSS tool. The findings of the study show that financial behavior has an effect on the investment decisions of Surabaya university students. Also, the objective of Arianti et al. (Citation2018) was to analyze and measure the influence of financial literacy, financial behavior and income on investment decisions. The study used a quantitative research method by using primary data collected from 100 students by way of random sampling. The SPSS tool was used to analyze the data collected with the relevant validity and reliability tests performed. The results of the study show that financial behavior has a significant effect on investment decisions. This is confirmed in the study by Wangi and Baskara (Citation2021) who sought to investigate the effect of financial attitude, financial behavior, financial knowledge and sociodemographic factors on the behavior of individual investment decisions a BNI Sekuritas Denpasar City. The non-probability sampling technique was employed to gather data from 200 respondents and analyzed with the use of multiple linear regression analysis techniques. It was revealed from the findings of the study that there is a positive effect of financial behavior on investment decision. Wangi and Baskara (Citation2021) posit that the public needs to realize the importance of financial management or financial behavior in managing funds due to the gravity of its impact on investment decision.

It can be observed, from the studies reviewed above, that financial behavior and investment decision have a significant relationship however no studies have explicitly investigated the relationship between personal financial management and investment decision. This leaves a vacuum which requires further studies. Financial behavior is just part of the personal financial management practices hence this study predicts that there exists a significant relationship. This forms the basis for the third hypothesis of the study which posits that there is a significant relationship between personal financial management and investment decision among private sector employees in Ghana.

H3:

There is a significant relationship between investment decision and personal financial management among private sector employees.

4.4. Mediation of financial literacy and personal financial management by investment decision

The company’s decision to invest its money now is based on the expectation that the potential rewards will outweigh the associated risks in the long run. Investment decisions, according to (Madi & Yusof, Citation2018), are choices made in relation to investments that offer benefits above the minimal interest rate earned. Investment project finance refers to the application of several forms of money in the project’s financing. Large-risk initiatives are anticipated to yield high returns that are based on the cash flow of the project that exceeds the investment. The evaluation of these high-risk investment proposals involves a high hurdle rate. A number of the company’s investment choices can serve as an example of how the business is expanding. The company’s expansion demonstrates its ability to manage its investments profitably, enabling it to select from a variety of profitable investment options. The company’s expansion offers investors the hope of rising profits in the future. The circumstance will generally improve the relationships between financial management and literacy among people and corporate entities. In this sense, the study produced the following hypothesis:

H4.

Investment Decision mediates the relationship between Financial Literacy and Financial Management.

4.5. Conceptual framework

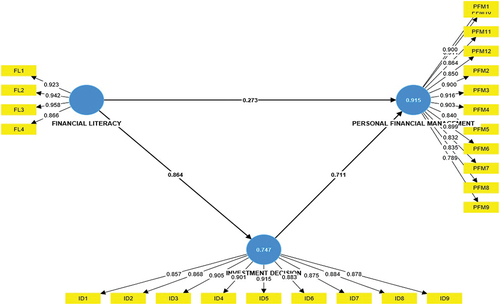

To purposefully bring all aspects of our current study together through a process that explains their connections, discrepancies, overlaps, tensions, and the contexts influencing the research setting and the study of phenomena in that setting, a conceptual framework becomes necessary (Ravitch & Riggan, Citation2016). In Figure , we therefore display our conceptual framework and underlying assumptions that connect financial literacy and financial management discussed earlier, with investment decisions serving as the mediating factor.

Figure 1. Conceptual framework.

5. Research design

Consistent with existing literature (see Cohen et al., Citation2017), the study used a cross-sectional survey design where deductive reasoning was applied to the quantitative data. The survey design allows the collection of data from different units over a specific period. Since the study is conducted over a limited time period, the cross-sectional survey was deemed more appropriate (Cohen et al., Citation2017). The partial least square structural equation model (PLS-SEM) was adopted. The use of a PLS-SEM is supported by similar empirical research (Abdullah & Tursoy, Citation2023; El Gammal et al., Citation2020) as they argue that it provides researchers with flexible approach to model complex relationships, handle non-normal data, and explore predictive relationships in a wide range of disciplines. It also allows for conducting and combining a vast variety of statistical procedures such as multiple regressions, factor analysis, analysis of variance, and others (Abdullah & Tursoy, Citation2023; El Gammal et al., Citation2020). Although it is often seen as complicated and difficult to understand, PLS-SEM is getting more and more popular due to its ability to model complex relationships. The stated objective is deconstructed into testable hypotheses expressed in their null forms. In all, four main hypotheses were tested, one hypothesis for each of the relationships discussed above.

This approach combines component analysis and multiple regression analysis to look at the structural relationship between independent, dependent, and latent variables. Using bootstrapping with number of replicates, the study assesses the mediation models by measuring each model’s degree of confidence (Hair et al., Citation2014). The route coefficient is calculated with a value of + 1 to illustrate the significant positive relationship in the structural model. When the structural path coefficient by bootstrapping significantly differs from its standard error, the study used p-values and t-values. At a significance threshold of 5%, the anticipated t-value was 6.926.

5.1. Sample size and data collection technique

In the context of this study, the target population comprises employees of SMEs in the Greater Accra Region. It is estimated that approximately 1,823,070 are employed by SMEs in the Greater Accra Region (Ghana Statistical Service IBES Report, 2017). Hence the target population of this study comprised 1,823,070 employees of SMEs in the Greater Accra Region. The selected participants were assured of the benefits of the study to the organization to ensure a minimum dropout rate. For this study, sample size was therefore established using Yamane’s simplified formula (1967) as shown below:

Where:

n = expected sample size

N = study population

e = margin of error and confidence interval is 95%

5.2. Measurement of variables

The Reflective Measurement Model (RMM) was adopted in the measurement of the latent variables used in the study. In RMM, the latent construct is considered the underlying factor that influences the observed indicators whereas the observed indicators are seen as reflective of the latent construct. A five-point Likert scale was used to measure the observed indicators of each constructs. The main dependent variable used in the study was Personal Financial Management: measured with 12 observed indicators. The independent variable used was Financial Literacy: measured with four observed indicators whereas nine observed indicators were used to measure Investment Decision, the mediating variable. Due to limited space, the observed indicators of the variables were not presented in the study.

5.3. Validity and reliability

The study employed three major variables namely, Financial Literacy, Personal Financial Management, and Investment Decision. Both content and the construct validity of this study were also ensured. The validity and reliability of a research study are two different but related research criteria for consistency (Straus, Citation2017). Therefore, Cronbach’s Alpha coefficient of 0.70 was used as a cut-off point for assessing the internal consistency of the research item and scales to guarantee study reliability (Biasutti & Frate, Citation2017; Singh, Citation2017). To eliminate logical flaws and biases in the study, the researchers emphasized the validity and reliability of the constructs.

6. Empirical results and discussion

6.1. Exploratory factor analysis

In order to identify the underlying latent factors in a set of observed variables, exploratory factor analysis (EFA), a multivariate statistical technique can distinguish between and concentrate on the theoretical underpinnings and conjectural constructs that can explain the arrangement and ordering of the assessed variables (Watkins, Citation2018). Inherently, the EFA looks for observed items that highly correlate with one another but have weak correlations with any external variables. However, there are a few rules that must be observed in order to utilize the EFA accurately. Watkins (Citation2018) advises using 10–15 participants per variable to more effectively collect population-level data. For instance, a ratio or interval scale should be used to evaluate each variable. Of course, there are more standards that need to be met.

6.1.1. Common method bias

To lessen the incidence of common method bias, two factors were ensured: procedural design and statistical control. Reasonable attention was given to the survey design process in accordance with some of the suggestions made by Podsakoff et al. (Citation2003). Harman’s one-factor test was used as a statistical analysis. The findings demonstrate that there is not any problem of common method bias because the single factor extraction was 15% and was below the 50% threshold value (see Table ).

Table 1. Common method bias

6.1.2. KMO and bartlett’s test

The results in Table show that the study’s KMO sampling adequacy was 0.928. The result demonstrates that, whether measured against 0 or an identity matrix, values within this dimension are relatively significantly associated with one another. Exploratory factor analysis would be able to produce real-value estimations based on the experiment’s desired sample size. Table 6.1.2 indicates the relevance of this with a p value less than 0.05. The results suggest that the internal correlations between variables may be caused by other causes.

Table 2. KMO and Bartlett’s test

6.2. Evaluation of measurement scale

Similar to Ringle et al. (Citation2015), a two-step procedure employing Partial Least Squares Structural Equation Modelling (PLS-SEM) was used to examine the suggested model. The study initially assessed the validity and reliability of the data using reflecting measurement methods

6.2.1. Reliability

Internal consistency and reliability is assessed using two key tests. Examples include composite reliability (CR) and Cronbach’s alpha (CA). Contrary to composite reliability (CR), which assesses how well one group of items anticipates the underlying variables in another, Cronbach’s alpha (CA) gives a reliability score based on correlations across apparent indicator constructs. The CA and CR values must be between 0.70 and 0.95 to be considered valid. Table displays the model’s internal consistency reliability, with CR scores ranging from 0.958 to 0.974 for all variables and CA scores from 0.942 to 0.971.

Table 3. Reliability and validity

6.2.2. Validity

The study performed convergent and discriminant validity tests which make up construct validity. The study ensured that items positively correlate with other items of the same construct in order to fulfill the criteria for convergent validity (Churchill, Citation1979). The convergent validity was established because every AVE value was greater than 0.50 (see Table ). The researchers used Heterotrait-Monotrait (HTMT) ratio of correlations to establish the discriminant validity of the constructs. From Table , it can be seen that all values were less than the 0.85 criteria (Henseler et al., Citation2015) hence indicates acceptable discriminant validity among the constructs. Additionally, the AVE was found to be greater than the equivalent squared correlations among the latent variables (see Table ).

Table 4. Discriminant validity

6.2.3. Multicollinearity test

The significance of the indicators in the study and their interactions are examined using multicollinearity test. In cases where there is multicollinearity between two independent variables, it is advisable to use only one of such variables. Due to multicollinearity, the constructs would become a dependent variable rather than an independent one. The results of the multicollinearity test are acceptable as shown in Table . All values of VIF are less than the 5 threshold hence no problem of multicollinearity.

6.3. Descriptive statistics

Table presents the statistical summary of the study’s variables. The standard deviation demonstrates how well the mean values represent the data, whereas the mean numbers serve as a summary of the raw data (Field et al., Citation2009). It can be seen that the financial literacy score (M = 3.66; SD = 1.354), investment decision score (M = 3.94; SD = 1.116), and personal financial management score (M = 3.92; SD = 1.108). The results demonstrate that all constructs’ departures from their respective means were not statistically significant, proving that the calculated or statistical mean and the observed mean are the same. Also, on average, the respondents were neutral to items under each construct (neutral = 3).

Table 5. Descriptive statistics and normality statistics

6.3.1. Normality test

Kurtosis and skewness, two further metrics of data normality, are also included in Table . Wilson et al. (Citation2010) suggest using these two metrics as effective methods for displaying the probability distribution of a data collection. According to the criterion, most of the variables must fall between −2 and + 2. However, Table findings demonstrate that every variable is within the acceptable limits for this study.

6.4. Boot trapping resampling technique

Investigators can more precisely assess the precision and predict the behavior of one or more target constructs by using a structural equation model, also known as an internal model. By resampling the data

5,000 times and taking standard error into consideration, the coefficients of the mediating model are examined for consistency (Hair et al., Citation2014). Numerous indicators, including collinearity, p value, path coefficient, coefficient of determination, effect size (f2), and impact size, are taken into account below the structural model (g2). A significant relationship between two or more measurements is known as collinearity. The variance inflation factor was used to gauge the level of collinearity between the latent variables.

6.4.1. Predictive relevance

The R2 values of 0.75, 0.50, and 0.25 are categorized as significant, moderate, and weak, respectively, by Henseler (Citation2018). However, Chin et al. (Citation2020) state that it is crucial to understand the R2 when considering the related field’s environment into consideration. According to Table and Figure , the model offers a respectable level of prediction accuracy (R2 Adjusted) values 0.747 and 0.914 for investment decision and personal financial management. The results showed that financial literacy and personal financial management together explained 91.4% of the fluctuation in the personal financial management. As a result, the model is able to anticipate the future and has strong predictive power.

Figure 2. Measurement model assessment.

Table 6. R-square and adjusted R-square

6.5. Hypotheses for direct and indirect relationship

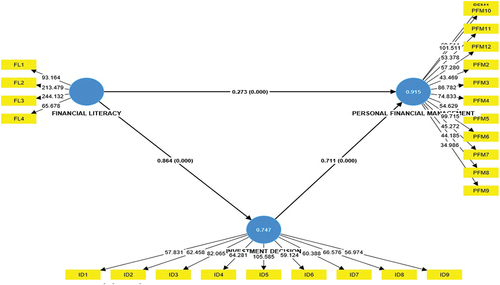

The four hypotheses proposed in the study were evaluated in this section. The study’s primary objective was to investigate the mediating function of investment decision in the relationship between employees’ personal financial management and financial literacy in the private sector. According to the study’s hypothesis, there is a direct correlation between employees in the private sector’s degree of personal financial management and their financial literacy. The results of Table and Figure show that personal financial management and financial literacy have a positive and significant link (B = 0.273; SD = 0.039; t = 6.926; P-value = 0.000 < 0.05). According to the findings, while all other things stay constant, there would be a 27.3% improvement in personal financial management for every gain in financial literacy. The findings support the hypotheses put forward in the study and in line with other studies (see Refera et al., Citation2018; Ansar et al., Citation2019; Humaidi et al., Citation2020, Novitasari, Citation2021 and; Yogasnumurti et al., Citation2021). The study also made the assumption that the financial literacy of private sector employees and their decision of investments are clearly related. The results of Table show that financial literacy and investment choice have a positive and significant association (B = 0.864; SD = 0.013; t = 66.490; P-value = 0.000 < 0.05). According to the findings, while all other things stay constant, there would be 86.4% improvement in investment decision for every gain in financial literacy. The findings support the hypotheses put forward in the study and consistent with existing literature (see Alaaraj & Bakri, Citation2020; Arianti et al., Citation2018; Baihaqqy et al., Citation2020; Fernando & Pribadi, Citation2022; Kumari, Citation2020; Wangi & Baskara, Citation2021). The study also assumed that there is a direct link between employees in the private sector’s investment decision and their personal financial management. Findings from Table show a significantly positive correlation between investment decision and personal financial management (B = 0.711; SD = 0.036; t = 19.494; P-value = 0.000 < 0.05). According to the findings, while all other things stay constant, there would be 71.1% improvement in personal financial management for every gain in investment decision. The findings support the hypotheses put forward in the study and are consistent with existing literature (Alaaraj & Bakri, Citation2020; Arianti et al., Citation2018; Baihaqqy et al., Citation2020; Fernando & Pribadi, Citation2022; Kumari, Citation2020; Wangi & Baskara, Citation2021) where investment decision and personal financial management were found to be significantly related.

Table 7. Hypothesis for direct and indirect relationship

Figure 3. Structure model evaluation.

Further, it has been shown in the research that the association between financial literacy and individual financial management of employees in the private sector is mediated by investment decision. Results in Table demonstrated that the link is mediated by investment decision (B = 0.615; SD = 0.032; t = 19.157; P-value = 0.000 < 0.05). The findings indicate that investment decision act as a mediator in the link between financial literacy and personal financial management. Furthermore, the results imply that a greater degree of investment decision-making will enhance the relationship (61.5%) between understanding your finances and managing them. However, this finding being novel in nature is linked with the theory of planned behavior framework where the attitude of private sector employees to evaluate the consequences of making investment will influence their personal financial management. This implies that psychology factors have significant influence on investing and personal management (Sara et al., Citation2023; Sulistianingsih & Santi, Citation2023)

6.6. Discussion of key findings

In this part, the main findings are described together with pertinent literature. The study’s primary objective was to investigate the mediating effect of investment decision in the relationship between financial literacy and personal financial management among private sector workers. The next section below discusses the main findings in relation to the specified objectives.

The objective one assessed if there is a direct correlation between employees in the private sector’s degree of personal financial management and their financial literacy. The results showed that personal financial management and financial literacy have a positive and significant link (B = 0.273; SD = 0.039; t = 6.926; P-value = 0.000 < 0.05). According to the findings, while all other things stay constant, there would be a 27.3% improvement in personal financial management for every gain in financial literacy. The findings support the hypotheses put forward in the study. The findings are in line with those of Nyamute and Maina (Citation2011), who looked at personal financial management behaviors of both employees with and without financial education. Utilizing a prepared questionnaire, 192 employees provided the survey data. The results demonstrated how personal financial management behaviors are influenced by financial literacy. It is advised that people strive to learn the fundamental concepts of money management so they may better handle their own funds. The results back up Olima (Citation2013), which examined the level of financial literacy among Kenya Revenue Authority workers and the effects of their understanding on those workers’ savings practices and readiness for social security. The study made use of primary information acquired through semi-structured questionnaires. Because financial education programs direct program creation and improvement, the study’s findings showed that financial literacy has a significant influence on financial management. The findings are in line with Jayantilal’s (Citation2017) evaluation of financial literacy and its effect on Bank of Baroda (Kenya) Limited employees’ personal financial management. The study, which concentrated on the 173 bank workers, utilized a descriptive quantitative research approach. Structured questionnaires were used to gather data, and they were given to bank personnel using convenience sampling. According to the study, financial literacy has a favorable impact on personal financial management among Bank of Baroda (Kenya) Limited workers, which results in increased investment practice, more balanced deposits, and a reduced debt-to-income ratio.

Also, the second hypothesis made the assumption that the financial literacy of private sector employees and their decision of investments are clearly related. The results showed that financial literacy and investment choice have a positive and significant association (B = 0.864; SD = 0.013; t = 66.490; P-value = 0.000 < 0.05). According to the findings, while all other things stay constant, there would be 86.4% improvement in investment decision for every gain in financial literacy. The findings support the hypotheses put forward in the study. The findings correspond with those of Baihaqqy et al. (Citation2020), who looked at how financial literacy affected investment decisions in Indonesian society. Using a survey method and 400 research samples made up of Baby Boomers, Gen Xers, and Gen Y/NetGen, the study took a quantitative approach. The results showed that investment decisions are influenced by financial knowledge. The findings back up Arianti et al. (Citation2018), who also looked at and calculated how financial behavior, income, and financial literacy affect investment decision-making. The quantitative descriptive research approach was used in the investigation. Information was acquired from 100 students via questionnaire. The study’s findings showed that investment decisions are influenced by financial knowledge. The findings also align with those of Raut (Citation2020), who investigated the influence of prior practices and financial literacy on the investment choices of individual investors. A self-administered questionnaire was used in the investigation. According to the research, investors’ choices are significantly influenced by societal pressure, which may be decreased by having a strong grasp of money matters.

The objective three also assumed that there is a direct link between employees in the private sector’s investment decision and their personal financial management. Findings showed a significantly positive correlation between investment decision and personal financial management (B = 0.711; SD = 0.036; t = 19.494; P-value = 0.000 < 0.05). According to the findings, while all other things stay constant, there would be 71.1% improvement in personal financial management for every gain in investment decision. The findings support the hypotheses put forward in the study. Although similar studies have not looked at the impact of investment decision on personal financial management, other studies have examined the effect on investment decision on firm value and performance. Fauziah and Asandimitra (Citation2018), for instance, examined how investment choices influenced the firm values of chemical and basic industrial enterprises listed on the Indonesia Stock Exchange (IDX) between 2012 and 2016. The research method used in this study is causal research. Forty-nine businesses make up the sample chosen intentionally. The findings demonstrated that the investments made had no impact on the company’s worth. Additionally, Nugraha et al. (Citation2020) conducted study to examine the effects of finance, investment, and dividend policies on firm value in the manufacturing industry between 2014 and 2018. With a total sample of 15 manufacturing businesses represented on the Indonesia Stock Exchange, the study employed a quantitative descriptive methodology. The data was processed with Eviews-10. According to the results, policy, investment choices, and dividend policy all have a considerable influence on business value. The study suggests that company management should keep raising the bar for itself in terms of investment choices and pay-out practices. Putri and Budyastuti (Citation2021) also identified and investigated the impacts of investment decisions, dividend policy, and profitability on firm value in Indonesia’s stock exchange-listed production enterprises between 2016 and 2018. The results showed that while company value is positively influenced by profitability and dividend policy, firm value was unaffected by investment decisions.

Furthermore, the objective four stated that investment decision is a mediator in the relationship between financial literacy and individual financial management of employees in the private sector. Results showed that the relationship is mediated by investment decision (B = 0.615; SD = 0.032; t = 19.157; P-value = 0.000 < 0.05). The finding demonstrates that investment decision mediates the association between financial literacy and personal financial management. Furthermore, the results imply that a greater degree of investment decision-making will enhance the relationship (61.5%) between understanding your finances and managing them. The results confirm the study’s declared hypothesis. Prior studies did not examine the mediating function of investment decision in the relationship between financial literacy and personal financial management, but instead examined investment decision as an intervening variable on other factors, for instance, Hendrawaty et al. (Citation2020) investigated the influence of the chief executive officer’s financial literacy on the corporate financial performance of small and medium-sized enterprises (SMEs) by examining the mediating function of sources of investment decisions that include financial statement, proponent information, and neutral information. 301 executives from SMEs in Indonesia were the primary source of the data. The indirect impacts demonstrated that the link between the business performances of the CEO was strongly mediated by sources of investment decision. The direct and indirect effects of financial decisions, dividend policy, and company value, as well as the function of investment decisions as a mediator, were also investigated and studied by Sulistiono and Yusna (Citation2020). Data were gathered using an intentional sample strategy, and the population was selected based on population factors. Multiple regressions were used to evaluate the data, and the Sobel Test was used to look for any relevant mediators. The findings demonstrated that the connection is mediated by investment choice.

7. Summary and conclusion

The major goal of the study was to better understand how investment decision influences workers’ individual financial literacy and their personal financial management. To accomplish the goals outlined in the study, the study employed a quantitative technique using a descriptive and explanatory research design.

The participants in the study were workers at SMEs in the Capital of Ghana. To gather primary data, the researchers employed a convenience sample strategy. The information was gathered from 400 employees of SMEs using a well-structured questionnaire. Descriptive statistics and a normality test were performed on the data. In conclusion, it has been shown that investment decisions and personal financial management are significantly and positively impacted by financial literacy. The findings also demonstrated that investment decision significantly affect personal financial management. Additionally, it was shown that investment decision mediates the link between financial literacy and personal financial management. The results imply that people’s financial management may be improved by increasing their understanding of financial literacy and investment decision. These relationships are predicted by the theory of planned behavior (Ajzen, Citation1985).

Based on the findings we therefore suggest that borrowers make plans for their spending patterns and payment of debts to avoid being crippled financially by the severity of interest rate swings. Similarly, financial literacy training programs will be of help since their provision will give thorough knowledge on borrowing and investment portfolios. And in light of the rise in financial literacy, there will be an increase in the quantity and diversity of financial literacy training program providers, some of which will include complete information on debt and investments. Again, consumers should receive training in appropriate money management techniques in order to foster a more competitive and effective market for consumption and savings.

A number of difficulties were encountered during the study. To mention few, some respondents were compelled to withhold personal information because they viewed it as being of a private nature and occasionally of competitive value. People understandably experience embarrassment when disclosing information that reveals shortcomings in their personal management, especially when secrecy is not guaranteed. Some respondents may have given responses that were prejudiced or dishonest because they believed that sharing information about how well they understand specific parts of financial management and how they use it for financial benefit was too crucial. The study was also conducted at a certain period which became a major flaw of this current study as it did not record the respondents’ degrees of financial literacy or their long-term financial management strategies. This is significant because rational consumers’ knowledge and tastes evolve over time. Again, the study was done in a unilateral region. In order to determine if there is uniformity regarding the impact of financial education on personal financial management among participants in the various organizations, it is advised that similar study be reproduced in other organizations and the findings be compared. It is also advised that follow-up studies on respondents, similar to this, be conducted throughout time. The influence of financial management on SME workers in the capital of Ghana was the primary goal of this research on financial education. Therefore, it is advised that research be conducted among personnel from various organizations across the nation to strengthen the validity and coherence of the results.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Abdullah, H., & Tursoy, T. (2023). The effect of corporate governance on financial performance: Evidence from a shareholder-oriented system. Iranian Journal of Management Studies, 16(1), 79–20.

- Ajzen, I. (1985). From intentions to actions: A theory of planned behavior. Springer.

- Alaaraj, H., & Bakri, A. (2020). The effect of financial literacy on investment decision making in Southern Lebanon. International Business and Accounting Research Journal, 4(1), 37–43. https://doi.org/10.15294/ibarj.v4i1.118

- Ansar, R., Karim, M. R. A., Osman, Z., & Fahmi, M. S. (2019). The impacts of future orientation and financial literacy on personal financial management practices among generation Y in Malaysia: The moderating role of gender. Asian Journal of Economics, Business and Accounting, 12(1), 1–10. https://doi.org/10.9734/ajeba/2019/v12i130139

- Arianti, B. F., Azzahra, K., & Romadhina, A. P. (2018). The influence of financial literacy, financial behavior and income on investment decision. Economics and Accounting Journal, 1(6), 1–10. https://doi.org/10.33122/ijase.v1i6.107

- Baihaqqy, M. R. I., Disman, N., Sari, M., & Ikhsan, S. (2020). The effect of financial literacy on the investment decision. Budapest International Research and Critics Institute-Journal (BIRCI-Journal), 3(4), 3073–3083.

- Biasutti, M., & Frate, S. (2017). A validity and reliability study of the attitudes toward sustainable development scale. Environmental Education Research, 23(2), 214–230. https://doi.org/10.1080/13504622.2016.1146660

- Chin, W., Cheah, J. H., Liu, Y., Ting, H., Lim, X. J., & Cham, T. H. (2020). Demystifying the role of causal predictive modeling using partial least squares structural equation modeling in information systems research. Industrial Management & Data Systems, 120(12), 2161–2209. https://doi.org/10.1108/IMDS-10-2019-0529

- Churchill, G. A., Jr. (1979). A paradigm for developing better measures of marketing constructs. Journal of Marketing Research, 16(1), 64–73. https://doi.org/10.1177/002224377901600110

- Cohen, L., Manion, L., & Morrison, K. (2017). Approaches to qualitative data analysis. In Research methods in education (pp. 643–656). Routledge.

- Copur, Z., & Gutter, M. S. (2019). Economic, sociological, and psychological factors of the saving behavior: Turkey case. Journal of Family and Economic Issues, 40(2), 305–322. https://doi.org/10.1007/s10834-018-09606-y

- Doran, J. S., Peterson, D. R., & Wright, C. (2010). Confidence, opinions of market efficiency, and investment behavior of finance professors. Journal of Financial Markets, 13(1), 174–195. https://doi.org/10.1016/j.finmar.2009.09.002

- El Gammal, W., Yassine, N., Fakih, K., & El-Kassar, A. N. (2020). The relationship between CSR and corporate governance moderated by performance and board of directors’ characteristics. Journal of Management & Governance, 24(1), 411–430. https://doi.org/10.1007/s10997-018-9417-9

- Fauziah, A., & Asandimitra, N. (2018). The influence of investment decisions, funding decisions, dividend policy, and profitability on firm value (studies of chemical and basic industry companies listed on the idx for the 2012-2016 period). Journal of Management Science, 6(3), 84–92.

- Fazal, H. (2017). Effect of emotional intelligence on investment decision making with a moderating role of financial literacy. China-USA Business Review, 16(2), 53–62. https://doi.org/10.17265/1537-1514/2017.02.002

- Fernando, F., & Pribadi, D. A. (2022). The impact of financial literacy, financial behavior, income, and financial risk tolerance in the case of surabaya university students’ investment decision. iBuss Management, 10(1), 1–25.

- Field, R., Hawkins, B. A., Cornell, H. V., Currie, D. J., Diniz‐ Filho, J. A. F., Guégan, J. F., Kaufman, D. M., Kerr, J. T., Mittelbach, G. G., Oberdorff, T., O’Brien, E. M., & Turner, J. R. G. (2009). Spatial species‐ richness gradients across scales: A meta‐ analysis. Journal of Biogeography, 36(1), 132–147. https://doi.org/10.1111/j.1365-2699.2008.01963.x

- Hair, F. J., Sarstedt, J., Hopkins L, M., & Kuppelwieser V, G. (2014). Partial least squares structural equation modeling (PLS-SEM) an emerging tool in business research. European Business Review, 26(2), 106–121. https://doi.org/10.1108/EBR-10-2013-0128

- Hamza, N., & Arif, I. (2019). Impact of financial literacy on investment decisions: The mediating effect of big-five personality traits model. Market Forces, 14(1), 1–60.

- Hendrawaty, E., Widiyanti, M., & Sadila, I. (2020). CEO financial literacy and corporate financial performance in Indonesia: Mediating role of sources of investment decisions. Journal of Security and Sustainability Issues, 9(1), 118–133.

- Henseler, J. (2018). Partial least squares path modeling: Quo vadis? Quality & Quantity, 52(1), 1–8. https://doi.org/10.1007/s11135-018-0689-6

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Humaidi, A., Khoirudin, M., Adinda, A. R., & Kautsar, A. (2020). The effect of financial technology, demography, and financial literacy on financial management behavior of productive age in Surabaya, Indonesia. International Journal of Advances in Scientific Research and Engineering, 6(1), 77–81. https://doi.org/10.31695/IJASRE.2020.33604

- Jayantilal, D. A. (2017). The effect of financial literacy on personal finance management: A case study on employees of Bank of Baroda (Kenya) Limited [ Doctoral dissertation]. United States International University-Africa.

- Khan, F., Siddiqui, M. A., & Imtiaz, S. (2022). Role of financial literacy in achieving financial inclusion: A review, synthesis and research agenda. Cogent Business & Management, 9(1), 2034236. https://doi.org/10.1080/23311975.2022.2034236

- Kumari, D. T. (2020). The impact of financial literacy on investment decisions: With special reference to undergraduates in Western Province, Sri Lanka. Asian Journal of Contemporary Education, 4(2), 110–126. https://doi.org/10.18488/journal.137.2020.42.110.126

- Lusardi, A. (2019). Financial literacy and the need for financial education: Evidence and implications. Swiss Journal of Economics and Statistics, 155(1), 1–8. https://doi.org/10.1186/s41937-019-0027-5

- Lusardi, A., Hasler, A., & Oggero, N. (2018). Financial fragility in the US: Evidence and implications. Global Financial Literacy Excellence Center. The George Washington University School of Business.

- Lusardi, A., Mitchell, O. S., & Curto, V. (2014). Financial literacy and financial sophistication in the older population. Journal of Pension Economics & Finance, 13(4), 347–366. https://doi.org/10.1017/S1474747214000031

- Madi, A., & Yusof, R. M. (2018). Financial literacy and behavioral finance: Conceptual foundations and research issues. Journal of Economics & Sustainable Development, 9(10), 81–89.

- Novitasari, D., Juliana, J., Asbari, M., & Purwanto, A. (2021). The effect of financial literacy, parents’ social economic and student lifestyle on students personal financial management. Economic Education Analysis Journal, 10(3), 522–531. https://doi.org/10.15294/eeaj.v10i3.50721

- Nugraha, N. M., Nugraha, D. N. S., & Sapitri, S. (2020). The effect of funding, investment and dividend policies on firm value in the manufacturing industry sectors. Solid State Technology, 63(3), 3858–3868.

- Nyamute, W., & Maina, J. M. (2011). Effect of financial literacy on personal financial management practices [ Doctoral dissertation]. University of Nairobi.

- Olima, B. (2013). Effect of financial literacy on personal financial management on Kenya Revenue Authority employees in Nairobi [ Doctoral dissertation]. University of Nairobi.

- Oteng, E. (2019). Financial literacy and investment decisions among traders in the Techiman Municipality. Research Journal of Finance & Accounting, 10(6), 50–60.

- Pangestu, S., Karnadi, E. B., & Foroudi, P. (2020). The effects of financial literacy and materialism on the savings decision of generation Z Indonesians. Cogent Business & Management, 7(1), 1743618. https://doi.org/10.1080/23311975.2020.1743618

- Podsakoff, P. M., MacKenzie, S. B., Podsakoff, N. P., & Lee, J. Y. (2003). The mismeasure of man (agement) and its implications for leadership research. The Leadership Quarterly, 14(6), 615–656. https://doi.org/10.1016/j.leaqua.2003.08.002

- Putri, N., & Budyastuti, T. (2021). The effect of investment decisions, dividend policy and profitability on firm value in the Indonesian manufacturing companies. American Journal of Humanities and Social Sciences Research (AJHSSR), 5(4), -47–53.

- Raut, R. K. (2020). Past behaviour, financial literacy and investment decision-making process of individual investors. International Journal of Emerging Markets, 15(6), 1243–1263. https://doi.org/10.1108/IJOEM-07-2018-0379

- Ravitch, S. M., & Riggan, M. (2016). Reason & rigor: How conceptual frameworks guide research. Sage Publications.

- Refera, M. K., Dahliwal, N. K., & Kaur, J. (2018). Effect of financial literacy on personal financial management practices: Evidences from the survey of urban dwellers in Addis Ababa, Ethiopia. Management Today, 8(2), 129–140. https://doi.org/10.11127/gmt.2018.06.02

- Ringle, C., Da Silva, D., & Bido, D. (2015). Structural equation modeling with the SmartPLS. Brazilian Journal of Marketing, 13(2), 1–18. https://doi.org/10.5585/remark.v13i2.2717

- Sara, I. M., Udayana Putra, I. B., Kurniawan Saputra, K. A., & Jaya Utama, I. W. K. (2023). Financial literacy, morality, and organizational culture in preventing financial mismanagement: A study on village governments in Indonesia. Cogent Business & Management, 10(1), 2166038. https://doi.org/10.1080/23311975.2023.2166038

- Shahab, Y., Ye, Z., Riaz, Y., & Ntim, C. G. (2018). Individual’s financial investment decision-making in reward-based crowdfunding: Evidence from China. Applied Economics Letters, 26(4), 261–266. https://doi.org/10.1080/13504851.2018.1464643

- Singh, A. S. (2017). Common procedures for development, validity and reliability of a questionnaire. International Journal of Economics, Commerce and Management, 5(5), 790–801.

- Sivaramakrishnan, S., Srivastava, M., & Rastogi, A. (2017). Attitudinal factors, financial literacy, and stock market participation. International Journal of Bank Marketing, 35(5), 818–841. https://doi.org/10.1108/IJBM-01-2016-0012

- Straus, M. A. (2017). The conflict tactics scales and its critics: An evaluation and new data on validity and reliability ( pp. 49–74). Routledge.

- Sulistianingsih, H., & Santi, F. (2023). Does SME’s financing decisions follow pecking order pattern? The role of financial literacy, risk preference, and home bias in SME financing decisions. Cogent Business & Management, 10(1), 2174477. https://doi.org/10.1080/23311975.2023.2174477

- Sulistiono, S., & Yusna, Y. (2020). Analysis of the effect of funding decision and dividend policy on the firm value and investment decision as mediation (study on manufacturing companies in Indonesia stock exchange). In 1st Annual Management, Business and Economic Conference (AMBEC 2019), Indonesia (pp. 173–177). Atlantis Press.

- Tahir, M. S., Ahmed, A. D., & Richards, D. W. (2021). Financial literacy and financial well-being of Australian consumers: A moderated mediation model of impulsivity and financial capability. International Journal of Bank Marketing, 39(7), 1377–1394. https://doi.org/10.1108/IJBM-09-2020-0490

- Utami, N., Sitanggang, M. L., & Sitanggang, M. L. (2021). The analysis of financial literacy and its impact on investment decisions: A study on generation z in Jakarta. Inovbiz: Jurnal Inovasi Bisnis, 9(1), 33–40. https://doi.org/10.35314/inovbiz.v9i1.1840

- Wangi, L., & Baskara, I. (2021). The effect of financial attitude, financial behavior, financial knowledge, and sociodemographic factors on individual investment decision behavior. American Journal of Humanities and Social Sciences Research (AJHSSR), 5(2), 519–527.

- Ward, S. (1974). Consumer socialization. Journal of Consumer Research, 1(2), 1–14. https://doi.org/10.1086/208584

- Watkins, M. W. (2018). Exploratory factor analysis: A guide to best practice. Journal of Black Psychology, 44(3), 219–246. https://doi.org/10.1177/0095798418771807

- Wilson, A., Cortes, P., Kouro, S., Rodriguez, J., & Abu-Rub, H. (2010). Model predictive control of multilevel cascaded H-bridge inverters. IEEE Transactions on Industrial Electronics, 57(8), 2691–2699. https://doi.org/10.1109/TIE.2010.2041733

- Yogasnumurti, R. R., Sadalia, I., & Irawati, N. (2021). The effect of financial, attitude, and financial knowledge on the personal finance management of college students. In Proceedings of the 2ndEconomics and Business International Conference-EBIC, Indonesia (pp. 649–657).