?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the impact of Digitalized Environmental, Social, and Governance (DESG) practices on rural banks in Ghana, focusing on their relationship with stakeholder engagement, customer loyalty, brand equity, and financial performance. The study collected data from 724 respondents, including bank customers and officials. The study finds that DESG practices directly and positively affect rural banks’ brand equity using Partial Least Squares Structural Equation Modeling (PLS-SEM). Additionally, stakeholder engagement indirectly and positively mediates the relationship between DESG and brand equity. Meanwhile, customer loyalty significantly mediates DESG and brand equity, and the combination of stakeholder engagement and customer loyalty jointly and significantly mediates the relationship between DESG and brand equity. Furthermore, DESG and brand equity indirectly and significantly impact rural banks’ financial performance during the study. These results underscore the essential role of digitalizing ESG practices in enhancing banks’ brand equity and overall performance. As a result, the study recommends that rural banks invest in digital infrastructure and platforms to enable effective stakeholder engagement, customer loyalty programs, and ESG reporting.

1. Introduction

The importance of environmental, social, and governance (ESG) factors in promoting sustainable and responsible business practices is increasingly recognized by companies worldwide. Financial institutions, particularly banks, play a significant role in promoting sustainable economic development in the communities they serve. In Ghana, rural banks are a vital part of the country’s financial system, providing essential banking services to rural communities. However, many rural banks face challenges in maintaining customer loyalty and brand equity due to limited access to technology and resources.

To address these challenges, this study investigated how rural banks could leverage the digitalization of ESG practices to enhance their brand equity and financial performance. The banking sector’s crucial role in promoting sustainable economic development has been emphasized by many researchers, such as Lins et al. (Citation2017). According to Demirguc-Kunt and Levine (Citation2000), banks provide essential financial services for businesses and individuals to grow and develop in rural communities. Adopting ESG practices can help banks reduce their environmental impact, improve social outcomes, and ensure good governance, as highlighted by Deloitte (Citation2020). There has been a growing interest in recent years among researchers in how banks’ ESG practices affect their brand equity globally. Deloitte (Citation2020) defines brand equity as the integration of environmental, social, and governance concerns into banks’ operations and decision-making processes. Experts such as Carroll and Shabana (Citation2010) and Goddard (Citation2017) have highlighted the increased demand from banks’ stakeholders for ESG practices to achieve ethical and socially responsible behavior.

Rural areas often have trouble accessing financial services, so rural banks are essential for promoting financial inclusion and helping rural areas grow (Goddard, Citation2017). Despite facing various challenges, such as limited access to digital financial services, rural banks in Ghana have the potential to enhance service delivery and increase financial inclusion by digitalizing ESG practices (Durugbo & Amankwah‐Amoah, Citation2019). Studies have shown that ESG performance positively impacts brand equity, which can contribute to a company’s financial performance by attracting new customers and retaining existing ones (Ajour El Zein et al., Citation2019; Puriwat & Tripopsakul, Citation2022). Additionally, the role of stakeholder engagement and customer loyalty in mediating the relationship between ESG practices and brand equity has been recognized by several studies (Puriwat & Tripopsakul, Citation2022).

Only a little research has been done on how ESG practices and brand equity work together in rural Ghanaian banks. Nevertheless, findings from studies in emerging markets have suggested that ESG disclosure is positively associated with a firm value (Aboud & Diab, Citation2018; Behl et al., Citation2022; Y. Li et al., Citation2018). In developing countries like Ghana, there is mounting evidence of the positive impact of corporate social responsibility (CSR) on customer loyalty (G. K. Amoako, Citation2017; Anlesinya, Citation2016; Hussainey & Al‐Najjar, Citation2012; Manokaran et al., Citation2018) Kotsantonis et al. (Citation2016) and Tantawi et al. (Citation2012) demonstrated that the integration of ESG practices could improve a bank’s reputation and brand equity. There still needs to be more research on how digitalization affects ESG practices in rural banks, especially in developing countries like Ghana, despite the increasing significance of ESG practices in the banking industry.

Ackah et al. (Citation2014) and KPMG (Citation2019) revealed that rural banks in Ghana are essential for rural development and ensuring that underserved communities have access to financial services. Nevertheless, these banks need more infrastructure and resources, making it hard to reach out to their customers (Cobbinah et al., Citation2020). Digitalization can make rural banks more efficient and help them reach more people, which can help them improve their ESG practices and serve their stakeholders better (Domeher et al., Citation2014; Jibril et al., Citation2020; Mensah, Citation2017; F. A. Sarpong et al., Citation2022). With the help of digital technologies, rural banks can learn about their customers’ needs and preferences and tailor their services to meet those needs. This helps Ghana and other African countries develop sustainably. Rural banks in Ghana are becoming more aware of digitizing their environmental, social, and governance (ESG) practices to stay competitive and improve their brand equity. Digital technology integration into ESG reporting processes is one common strategy rural Ghana banks use (Xia, Citation2022). This includes using digital platforms to collect and analyze data on crucial ESG metrics like carbon emissions and waste management practices (Appiah-Konadu et al., Citation2022).

It is not just digitalization that can help rural banks in Ghana improve their ESG practices and brand equity, but also stakeholder engagement. Researchers have shown that stakeholder engagement significantly shapes a bank’s ESG practices and brand equity (Werther & Chandler, Citation2005). Stakeholder engagement involves a company’s interactions in response to the needs and expectations of its stakeholders, such as customers, suppliers, regulators, and local communities (Archie & Carroll, Citation2014). For rural banks in Ghana, it means engaging with their stakeholders to understand their needs and expectations better. Using digitalization to improve stakeholder engagement through new communication channels and real-time feedback mechanisms (Tandon et al., Citation2020), rural banks in Ghana can strengthen their ESG practices and brand equity while better serving their stakeholders.

Along with digitalization and stakeholder engagement, customer loyalty is essential to improving ESG practices and brand value in Ghana’s rural banks. Studies in developing countries like Ghana have shown that corporate social responsibility (CSR) positively impacts customer loyalty (Hussainey & Al‐Najjar, Citation2012). As such, rural banks in Ghana must strive to incorporate ESG practices into their CSR strategies to improve customer loyalty and enhance their brand equity. By leveraging digitalization and stakeholder engagement to understand better and respond to the needs and expectations of their customers, rural banks can build strong relationships with their customers and establish a loyal customer base. This can, in turn, enhance the bank’s reputation and brand equity, leading to increased profitability and sustainability. In short, incorporating ESG practices into CSR strategies and prioritizing customer loyalty is essential for rural banks in Ghana to remain competitive and achieve long-term success.

This study contributes to the knowledge of how rural banks in Ghana can remain competitive and sustainable by exploring the relationship between the digitization of ESG and brand equity and its impact on financial performance. While previous studies conducted in Ghana on ESG focused on SMEs, this study fills the gap within the Ghanaian setting. There is no study conducted on digitalizing ESG among Ghanaian banks. The study further conducted a comparative analysis using the four main sectors of Ghana. This enabled the researchers to understand how digitalizing ESG could enhance the brand equity and financial performance of rural banks. The study’s main findings were obtained through a reliable PLS-SEM method, revealing a positive effect of digital ESG practices on rural bank brand equity in Ghana. The study focused mainly on rural areas due to their limited access to technology in implementing ESG, especially within the banking sector. This can lead to efficient and effective operations, resulting in cost savings and improved profitability. For example, implementing a digital system for environmental risk management can help rural banks identify and address potential environmental issues, reducing the risk of financial losses associated with environmental damage. This study highlights the importance of stakeholder engagement and customer loyalty in enhancing brand equity through digital ESG practices. The study focuses on the impact of digitalization on ESG practices in rural banks in a developing country like Ghana. By examining this topic, the study contributes to the existing literature on the impact of digital ESG practices on brand equity. The study’s results offer valuable insights for rural banks, policymakers, and stakeholders on the importance of digitalizing ESG practices to promote financial inclusion and support rural development. Thus, this study can be a practical guide for organizations looking to improve ESG practices and brand equity through digitalization.

The study comprises five main parts to facilitate readers’ comprehension of the research process. In the second part, the researchers review prior studies related to the topic to establish a strong foundation. The third section details the researchers’ methodology and offers insight into their strategy. In the fourth part, the researchers present and analyze their findings, revealing the influence of digital ESG practices on brand equity in rural banks. Lastly, in the concluding part, the researchers summarized the study based on their findings, providing significant guidance for policymakers, stakeholders, and rural banks seeking to enhance their ESG practices and brand equity.

2. Literature review

2.1. Conceptual framework

To better understand the impact of the digitalization of environmental, social, and governance (ESG) practices on brand equity in rural banks in Ghana, a conceptual framework combining stakeholder theory and a customer-based brand equity model can be employed. The Brand Equity Model, initially proposed by Aaker (Citation1991), posits that strong brand equity can lead to higher brand loyalty and a more favorable brand image, resulting in increased sales and market share. The model implies that digitalizing ESG practices in rural banks could positively impact brand equity, increasing customer loyalty and stakeholder engagement. This notion is supported by prior research, indicating that stakeholder engagement and customer loyalty can mediate brand equity through digitalizing ESG practices. Adopting such a framework can offer valuable insights into implementing digital ESG practices in rural banking in Ghana and promote sustainable development in the region.

Furthermore, the Stakeholder Engagement and Customer Loyalty Mediation Model suggest that stakeholder engagement mediates the relationship between ESG practices and customer loyalty. According to Zumente and Bistrova (Citation2021) and Archie and Carroll (Citation2014), stakeholder engagement positively impacts brand equity and customer loyalty. The stakeholder theory posits that organizations have multiple stakeholders, and their actions affect various stakeholders, including customers, employees, suppliers, shareholders, and the community. The customer-based brand equity model emphasizes the importance of customer loyalty and engagement in creating brand equity. By combining these models, this study explores the impact of digital ESG practices on brand equity in rural banks in Ghana. It uses a robust and reliable PLS-SEM method to analyze data and finds a positive effect of digital ESG practices on rural bank brand equity in Ghana. The study highlights the importance of stakeholder engagement and customer loyalty in improving brand equity through digitalizing ESG practices.

As we move towards a more digital world, the importance of environmental, social, and governance (ESG) practices has increased. Deloitte (Citation2020) highlights the significance of ESG practices in creating value for stakeholders and establishing a strong brand image. In the context of rural banks in Ghana, integrating ESG practices through digitalization can influence stakeholders’ perceptions and engagement with the bank. This engagement, in turn, can impact the level of customer loyalty and the overall brand equity of the bank. Research has shown that corporate sustainability and ESG performance positively impact brand equity (Agus Harjoto & Salas, Citation2017; Alcaide González et al., Citation2020).

Additionally, stakeholder engagement has positively impacted brand equity (Sartori et al., Citation2012; H. M. D. Wang, Citation2010). ESG disclosure has also been found to positively impact firm value, an essential component of brand equity (Lokko et al., Citation2021). These findings suggest that digitalizing ESG practices in rural banks can positively impact their brand equity, particularly through the mediating roles of stakeholder engagement and customer loyalty. By combining the brand equity model and the stakeholder engagement and customer loyalty mediation model, we have a comprehensive framework for studying how the digitalization of ESG practices impacts the brand equity of rural banks in Ghana. This framework enables us to explore how stakeholder engagement and customer loyalty mediate the relationship between the digitalization of ESG practices and brand equity. Figure illustrates this framework.

Figure 1. Conceptual framework.

ESG practices positively impact rural banks’ brand equity by creating customer loyalty and stakeholder engagement. Incorporating ESG practices into marketing and branding strategies can enhance customer loyalty. Increased stakeholder engagement builds trust and a positive reputation for the bank, boosting its brand equity. In Africa, ESG practices promote sustainable development and responsible corporate behavior (Hussainey & Al‐Najjar, Citation2012). In Ghana, ESG practices help rural banks establish their brand and differentiate themselves in a competitive market. Digitization makes it easier for rural banks to track and report ESG performance and engage with stakeholders and customers on ESG issues. This has been clearly illustrated in Figure . The framework explains the research hypotheses and the theory that guides their formulation.

2.2. Conceptual review

2.2.1. Digitization of ESG of rural banks

Digitizing rural banks has become more critical in recent years because it can help more people access money, promote sustainable development, and improve the quality of financial services (Nayak, Citation2018). Digital technologies like mobile banking, online payments, and digital wallets can help underserved communities access financial services (Adejumo et al., Citation2020; Nguyen et al., Citation2020; Singh & Malik, Citation2019). This is especially true in rural areas with few bank branches. The digitalization of rural banks in Africa and Ghana can boost financial inclusion, promote sustainable development, and enhance the quality of financial services (Abor et al., Citation2022). However, the slow adoption of digital technologies, particularly in remote areas, is a significant challenge due to the need for more necessary infrastructure like reliable electricity and internet connectivity.

Additionally, lower levels of financial literacy in rural areas can make it difficult for customers to effectively use digital banking services (Adejumo et al., Citation2020). Balancing the adoption of new technologies with the preservation of traditional banking practices and values is another challenge for rural banks. They must ensure that digitization does not lead to a loss of personal interaction with customers, which is a crucial aspect of rural banking (Appiah & Gabrielsson, Citation2023). Digital transformation is revolutionizing rural banking in Ghana and other African countries. Rural banks can overcome geographical barriers and reach underserved communities by adopting digital technologies such as mobile banking, online payments, and digital wallets. This leads to improved financial inclusion and reduced costs for low-income customers (Nguyen et al., Citation2020). However, rural banks must ensure that digital services are user-friendly and accessible to people with low digital literacy, especially in remote areas.

Stakeholders, particularly investors, and customers, are increasing pressure on businesses to be more open and responsible. Hence, environmental, social, and governance (ESG) policies have gained significance. Digitalization is one strategy that may be used to improve ESG procedures by facilitating more efficient data collection, management, and distribution. According to KPMG (Citation2019), digitalizing ESG processes may benefit a company’s reputation, brand value, and financial performance. Research demonstrates that organizations that digitalize ESG procedures appeal more to sustainability-minded investors and consumers (Jung & Park, Citation2022). In addition, digitization may enhance the openness and accountability of ESG reporting, resulting in increased stakeholder participation and consumer loyalty. By effectively using digital tools and technology, firms may fulfill the rising need for ESG transparency and produce favorable business results.

According to Rastogi et al. (Citation2022) and Ayakwah et al. (Citation2021), digitalization can enhance the brand equity of rural banks in Ghana by improving their sustainability performance, transparency, and stakeholder engagement. The use of digital technology may also enable these banks to understand better and meet their customers’ preferences and expectations, resulting in increased customer loyalty, as noted by C. J. Wang (Citation2019). However, there are still challenges to be addressed. Given the complexity and diversity of ESG data, it can be challenging to collect and maintain accurate, trustworthy, and current data, as highlighted by Bansal and Pruthi (Citation2021). Moreover, organizations must ensure that their ESG practices align with their values and goals while also understanding digital technology’s potential biases and limitations, as suggested by Liu et al. (Citation2020).

At rural banks in Ghana, the link between digitalizing ESG practices and brand equity is made through stakeholder involvement and customer loyalty. Digital transformation may promote stakeholder involvement, enhancing the firm’s reputation and brand equity (). Moreover, ESG disclosure is favorably related to customer happiness, leading to greater customer loyalty (X. Li et al., Citation2021). The use of digital technology in environmental, social, and governance (ESG) practices may increase stakeholder participation and consumer happiness, hence enhancing brand equity (X. Li et al., Citation2021; Malik et al., Citation2020; Pina & Dias, Citation2021; Wahyuni et al., Citation2020).

2.3. Empirical review

ESG practices directly affect a bank’s brand equity by encouraging customer loyalty and stakeholder participation. ESG practices are becoming more critical as rural banks in Ghana try to build their brand and stand out in a very competitive market. These hypotheses aim to examine the possible influence of digitization of ESG practices on the brand equity of rural banks in Ghana, along with the mediating roles of stakeholder involvement and customer loyalty. This study’s results will shed light on the significance of ESG practices in the financial sector, especially for rural banks in Ghana, and how digitization might boost their brand equity.

2.3.1. Digitalization of Environmental, Social, and Governance (ESG) practices positively affects brand equity

In support of this idea, many studies have been done to show that ESG practices have a positive effect on brand equity. Puriwat and Tripopsakul (Citation2022) discovered that in both established and developing markets, ESG performance had a favorable impact on brand equity. They observed that ESG performance enhances the brand perception and consumer trust, increasing brand equity. Moreover, Ben Salah and Ben Amar (Citation2022) and Niu et al. (Citation2022) discovered that business sustainability had a beneficial effect on brand equity. Their research revealed that businesses that participate in sustainable activities are viewed as socially responsible and dependable, which ultimately helps to improve their brand equity, customer retention, and stakeholder participation. As rural banks in Ghana attempt to create their brand and distinguish themselves in a competitive market, ESG practices are becoming more crucial. These hypotheses aim to examine the possible influence of digitization of ESG practices on the brand equity of rural banks in Ghana, along with the mediating roles of stakeholder involvement and customer loyalty. This study’s results will shed light on the significance of ESG practices in the financial sector, especially for rural banks in Ghana, and how digitization might boost their brand equity.

Similarly, Zhou (Citation2022), Lestari and Adhariani (Citation2022), and Laboure et al. (Citation2021) discovered that environmental, social, and governance (ESG) disclosure had a favorable impact on the value of a company. They observed that ESG disclosure results in increased openness and accountability, which have a beneficial effect on the brand equity of companies. According to these results, rural Ghana banks’ digitization of ESG practices would favorably impact their brand equity. The digitization of ESG practices may assist rural banks in enhancing their operational transparency and accountability, reputation, and consumer confidence. This will have a beneficial effect on their brand equity. Thus, the research hypothesized:

H1

Digitalization of Environmental, Social, and Governance (ESG) practices of Rural Banks has a positive effect on their brand equity in Ghana.

2.3.2. Stakeholder engagement mediates the relationship between the digitalization of ESG practices and brand equity

Recent research has shown how vital stakeholder involvement is to a company’s brand equity growth. It has been found that high levels of stakeholder engagement are suitable for brand equity, while low levels of participation may hurt it. For instance, Archie and Carroll (Citation2014) and Sartori et al. (Citation2012) demonstrated that stakeholder participation significantly influences brand equity, increasing perceived brand value in developed markets. Similarly, Bhamra et al. (Citation2018) discovered that a company’s environmental, social, and governance (ESG) performance, particularly in the areas of environmental and social responsibility, can enhance its image, build consumer trust, and lead to higher brand equity in both established and developing markets.

Also, Puriwat and Tripopsakul found in 2012 that ESG disclosure in developing African markets can positively affect business value, which is linked to better brand equity. The study shows how important it is for stakeholders to help African businesses build brand equity. Additionally, Goddard (Citation2017) and Xia (Citation2022) noted that financial inclusion, a form of stakeholder involvement, positively impacts rural development in Ghana. This research highlights the importance of involving stakeholders such as consumers and communities to support economic growth and development, which can be tied to the brand equity of rural banks in Ghana. These studies suggest that stakeholder participation, including ESG performance and financial inclusion, can significantly impact a company’s brand equity (Liu et al., Citation2020, Citation2022). In particular, high levels of stakeholder involvement have been shown to benefit rural banks’ brand equity in Ghana. Therefore, companies should prioritize engaging their stakeholders and implementing socially responsible practices to enhance brand equity.

H2

Stakeholder engagement mediates the relationship between the digitalization of ESG practices and the brand equity of Rural Banks in Ghana.

2.3.3. Customer loyalty mediates the relationship between the digitalization of ESG practices and brand equity

The third study hypothesis says that digitalizing environmental, social, and governance (ESG) activities in Ghana’s rural banks may affect customer loyalty, affecting brand equity. Several studies have shown that customer loyalty is the link between corporate social responsibility (CSR) and brand value. In the hotel industry, Kim and Lee (Citation2015) discovered that customers who saw a hotel as socially responsible were more loyal, which benefited the company’s brand equity. Similarly, Bansal and Pruthi (Citation2021), Zameer et al. (Citation2019), Ajour El Zein et al. (Citation2019), Guan et al. (Citation2021), and T. Tran et al. (Citation2022) found that CSR engagement by banks boosted customer loyalty, which was associated with more significant brand equity.

Moreover, Africa-specific research has established the link between consumer loyalty and brand equity. According to Agyei-Boapeah (Citation2020), Appiah-Konadu et al. (Citation2022)‘s study in Nigerian banks, customer loyalty has a substantial impact on brand equity. Appiah-Konadu et al. observed in Ghana that more significant customer satisfaction led to increased customer loyalty, which positively affected a bank’s brand equity. In addition, Appiah and Gabrielsson (Citation2023) and Agus Harjoto and Salas (Citation2017) discovered a significant correlation between customer loyalty and the profitability of rural banks in Ghana. Our results highlight the significance of building customer loyalty to enhance the success and growth of rural banks in Ghana and imply that customer loyalty may positively impact their brand equity.

H3

: Customer loyalty mediates the relationship between the digitalization of ESG practices and the brand equity of Rural Banks in Ghana.

2.3.4. Stakeholder engagement and customer loyalty jointly mediate the relationship between the digitalization of ESG practices and the brand equity

The fourth study hypothesis argues that stakeholder engagement and customer loyalty jointly moderate the association between the digitalization of environmental, social, and governance (ESG) practices and brand equity of rural banks in Ghana. This hypothesis posits that the positive impacts of digitizing ESG practices on brand equity may be mediated through stakeholder engagement and customer loyalty.

Recent research shows that stakeholder engagement and consumer loyalty may affect the link between corporate social responsibility (CSR) and brand equity. For instance, K. Amoako and Boateng (Citation2022) and X. Li et al. (Citation2021) discovered that CSR initiatives were more likely to result in loyal consumers valuing the bank’s interaction with stakeholders, enhancing brand equity. Similarly, Malik et al. (Citation2020) found that in the hotel industry, consumers who saw hotels as socially responsible and engaged with stakeholders were more loyal, increasing brand equity. Researchers such as Ackah et al. (Citation2014), Adu and Okyere (Citation2017), and Agyei-Boapeah (Citation2020) investigated the impact of the digitalization of ESG, stakeholder engagement, and customer loyalty on the brand equity of Nigerian banks in an African environment. According to their study, stakeholder engagement and customer loyalty significantly influence Nigerian banks’ brand equity. These results imply that stakeholder participation and customer loyalty also impact the brand equity of rural banks in Ghana.

Additionally, Anlesinya (Citation2016), Appiah-Konadu et al. (Citation2022), and Ayakwah et al. (Citation2021) did research in Ghana to investigate the impact of customer satisfaction and stakeholder participation on customer loyalty in the banking industry. High levels of customer satisfaction and stakeholder engagement led to increased customer loyalty, which had a favorable impact on the bank’s brand equity, as shown by the findings. Together, these studies indicate that stakeholder engagement and consumer loyalty may jointly function as mediators between ESG practices and brand equity. In conclusion, the results corroborate the hypothesis that stakeholder engagement and customer loyalty mutually moderate the link between the digitalization of ESG practices and brand equity in rural banks in Ghana.

H4

: Stakeholder engagement and customer loyalty jointly mediate the relationship between the digitalization of ESG practices and brand equity of Rural Banks in Ghana.

2.3.5. Digitization of ESG and brand equity improves financial performance

The last hypothesis says that rural banks are more likely to do well financially if they put ESG and brand equity first, use digitization initiatives, and encourage stakeholder participation and customer loyalty. This idea is backed up by studies showing how digitization improves the performance of rural banks in various ways.

First, digitization may improve banks’ environmental, social, and governance (ESG) performance by making tracking and reporting environmental, social, and governance (ESG) indices easier. This enables banks to identify improvement areas and establish goals to decrease their environmental impact, boost their social responsibility, and enhance their governance processes (Bătae et al., Citation2020; Domeher et al., Citation2014; Nyantakyi et al., Citation2023). The research on rural banks in Ghana revealed a correlation between ESG performance and financial success (Goddard, Citation2017). Hence, it can be deduced that rural banks that prioritize sustainability and digitization are more likely to exhibit superior financial performance.

Digitization has been shown to improve the brand equity of rural banks by making them more visible, easier to get to, and better for customers. This effect on brand equity could bring in new customers and strengthen relationships with existing ones, leading to more money. The research on Vietnamese banks reveals that digital marketing tactics might enhance brand recognition, hence enhancing the financial performance of rural banks. Digitalization may favor the financial performance of rural banks by increasing their efficiency and lowering their expenses (Jibril et al., Citation2020; Kotsantonis et al., Citation2016; Mensah, Citation2017; Niu et al., Citation2022). Deploying digital financial services and automating regular processes may result in cost savings and productivity benefits. This enhanced efficiency may lead to more excellent financial performance for rural banks. Consequently, rural banks that prioritize sustainability and brand equity, employ digitization techniques, and encourage stakeholder participation and customer loyalty would be more likely to achieve financial success (Behl et al., Citation2022). Using digital tools and platforms, rural banks may increase their competitiveness and resiliency in an increasingly digital and ESG-focused financial sector, according to these studies.

H5

: Digitization of ESG and brand equity improves the financial performance of rural banks in Ghana.

3. Research methodology

3.1. Research design

A quantitative research design was used to evaluate the study’s hypotheses and answer the research questions. In particular, the study collected data from rural banks in Ghana using a cross-sectional survey approach (Kwarteng et al., Citation2021; T. Sarpong & Sarpong, Citation2020; F. A. Sarpong et al., Citation2020). One of the critical advantages of cross-sectional surveys is that they are relatively quick and cost-effective compared to other survey designs (Makwetta et al., Citation2021; Osei-Mireku et al., Citation2020; T. Sarpong et al., Citation2020). This research used the Partial Least Squares Structural Equation Modeling (PLS-SEM) technique. PLS-SEM is an efficient method for examining the connections between latent variables, such as brand equity, digitization of environmental, social, and governance (ESG) practices, stakeholder engagement, and consumer loyalty (Chin & Newsted, Citation1999; Sappor et al., Citation2023). It is also helpful in investigating complicated interactions between latent variables in small to moderate samples (Fornell & Larcker, Citation1981; Hair et al., Citation2013).

The research thoroughly examined the associations between the latent variables and acquired information about the path coefficients, R2, and goodness-of-fit indices using PLS-SEM analysis (Kir et al., Citation2021; Owusu et al., Citation2022). This study gave valuable insights into the mediating relationship between stakeholder involvement and consumer loyalty, allowing for the successfully testing of the research hypotheses. In addition, PLS-SEM is a robust and adaptable technique for investigating the intricate links between the digitization of ESG practices, stakeholder engagement, customer loyalty, and brand equity in rural banks in Ghana.

3.2. Sampling procedure

The target population for this research consists of customers and employees of rural banks in Ghana. The rural banks considered for this study were registered under the Association of Rural Banks, Ghana, which has over 144 rural and community banks with over 850 branch networks offering financial services nationwide. The survey targeted all customers from rural banks. The customers’ respondents were chosen based on the following criteria: they had to be at least 18 years old, hold an account with any rural bank in Ghana, conduct financial transactions with their bankers, and be citizens of Ghana. Aside from the customers, key employees of the rural banks were also engaged in the study.

Before distributing the questionnaire, respondents were given a consent form to read and sign to register their interest in the study formally. Paper surveys and internet platforms (such as Google Forms) were used to gather data to meet rural bank customers’ and officials’ hectic schedules. This study’s data-gathering process lasted eight months, from June 2022 to January 2023. Google Forms distributed the surveys to the selected banks, and the results were gathered and evaluated using the necessary statistical tools. The questionnaire data was then used to evaluate the hypotheses and draw conclusions on the links between the digitalization of environmental, social, and governance (ESG) practices, stakeholder involvement, customer loyalty, and brand equity of rural banks in Ghana. The sample size was calculated using a specified equation:

The formula for estimating sample size without knowing the population size, using a 95% confidence level and a margin of error of 5%, is:

Where: n is the sample size, Z is the Z-value for the desired level of confidence (e.g., 1.96 for 95% confidence), p is the estimated proportion of the population with the characteristic of interest (expressed as a decimal), e is the desired margin of error (expressed as a decimal). Since we did not have an accurate estimate of p, we adopted the common approach by assuming a conservative value of 0.5, which represents maximum variability and ensures the largest sample size (Lakens, Citation2022).

According to Lakens (Citation2022) and Kline (Citation2016), this research needed a minimum sample size of 384 participants. To adjust for missing data and get a sample size more representative of the community, the researchers gathered data from 724 respondents, including customers and banking personnel. Kir et al. (Citation2021) and Owusu et al. (Citation2022) proposed a minimum sample size of 100 to 150 for doing Structural Equation Modeling (SEM). Thus, the present sample size is deemed sufficient for SEM.

This research used convenience sampling because it made data collection from a population of 537 customers and 187 bank executives straightforward and accessible (Etikan et al., Citation2016). This approach was selected owing to the ease and accessibility of the sample population, which is pertinent to the issue of the study. Bank official’s such as executive and senior management, ESG managers/officials and customer relationship managers were involved in the study to provided details on the overall information on rural bank’s ESG strategies, monitoring compliance with ESG standards, and engaging with stakeholders. These were people with access to bank’s commitment to sustainable practices and stakeholder engagement through digitalizing ESG practices. Involving customer relationship managers in the study provided valuable information on how digitalizing ESG practices influences customer perception and loyalty towards the rural bank. Moreover, customer of the rural banks were involved in the study to provide valuable insights into the impact of digitalization and ESG practices on brand equity, stakeholder engagement, and customer loyalty through feedback and loyalty metrics.

3.3. Data collection instrument

The use of questionnaires as a data collection instrument has been widely accepted in various fields of research, including the social sciences, health, and education (Fowler & Barry, Citation1993). This study aims to examine the relationships between the digitalization of environmental, social, and governance (ESG) practices, stakeholder engagement, customer loyalty, and brand equity in rural banks in Ghana. We employed five-point Likert scale questionnaire items as our primary data collection tool to measure the perceptions of rural banks’ official and customers in Ghana regarding the impact of digitalization on ESG practices. (see Appendix A). Details of the variable definitions has been explained below as illustrated in Table .

Table 1. Variable measurement

One of the common problems with data collection of this nature is the common method bias. The common bias method is when a researcher assumes a variable is evenly distributed, which can lead to flawed conclusions. Researchers such as Jordan and Troth (Citation2020), Chang et al. (Citation2010) may address this problem with diagnostic tests such as Harman’s single-factor or the marker variable approach. In addition, strategies like including control variables and aggregating data at a higher level may be implemented. Yet, it is essential to avoid common method bias from arising in the first place by using several data collection techniques and verifying the validity and reliability of the measuring instruments. In this research, controlling factors such as the size, age, and location of rural banks were incorporated to minimize the issue of the commonly used biased technique and enhance the multicollinearity of the analysis.

4. Main results and discussions

The banking sector in Ghana is regulated by the Bank of Ghana and consists of 23 licensed banks that serve approximately 17.5 million customers, both individuals and businesses. In addition, over 140 rural and community banks operate in Ghana to provide financial services to rural communities, farmers, and small businesses. The banking sector in Ghana has been growing steadily over the past decade, but it faces several challenges, such as high levels of non-performing loans, limited access to credit for small and medium-sized enterprises, and a lack of financial inclusion in rural areas. To address these issues, more data on the total banking sector in Ghana, including financial performance indicators and customer demographics, is needed to inform strategies for improving stakeholder engagement and customer loyalty in both rural and urban areas. Rural banks in Ghana play a vital role in providing financial services to rural communities, but they face unique challenges, such as limited resources and access to technology. However, digitalizing environmental, social, and governance (ESG) practices may provide an opportunity for rural banks to enhance their sustainability performance, engage with stakeholders more effectively, and improve customer loyalty. The study hence adopted primary data in collecting information on the relationship that existed between DESG, stakeholder engagement, customer loyalty and financial performance of rural banks in Ghana.

Table showed that a total of 724 people participated in the survey, with 317 of them being male and 407 being female. The most common age group was 38–47, comprising 193 customers and bank officials. This included 150 customers and 43 bank officials.

Table 2. Biographical information of respondents

More than 27% of the total respondents were over 47 years old. The study again revealed that 189 respondents were between 28 and 37 years old, which made up 26% of all respondents. On the other hand, the lowest age group was between 18 and 27 years old, representing just 21% of the total participants.

Regarding education level, most respondents (37%) had at least a diploma degree, while only 33% had a minimum high school education. Almost one-third of respondents (30%) had completed their first degree or higher. The survey also revealed that 20% of the customer respondents identified as public workers, 22% were entrepreneurs, and 36% worked in NGOs. This information is essential for rural banks in Ghana to understand their client base and tailor their digital strategies to meet their needs.

The banks officials included 64 senior managers who hold key decision-making positions within the bank. We further collected data from 67 ESG managers who are responsible for integrating environmental, social, and governance considerations into their operations. Customer Relation Managers constituted 30% of 187 rural banks’ officials involved in the study.

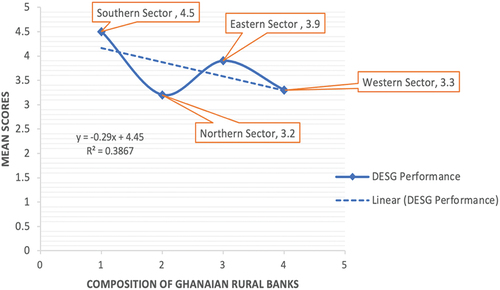

Surprisingly, the survey found that most customer respondents (32%) did much business with their bank, while only 18% did very little business with their bank. This highlights the potential for digitization to increase customer engagement and loyalty by making rural banking services more accessible and convenient. The demographic data are significant since they provide a deeper insight into the research participants. This information assists the researchers in determining why the respondents answered the questions as they did. The study revealed that the majority (33%) of the respondents were found in the southern sector of Ghana. This was followed by the eastern sector, with 26% of respondents in this sector. For the northern sector, only 21% of the total respondents were involved in the study. This was done to ensure the equal involvement of all four main sectors in Ghana.

The study further investigated the rural banks’ digitalized ESG among the four main sectors in Ghana as seen in Figure . The study revealed that the rural banks in the southern sector achieved higher performance in digitalizing ESG(M = 4.5), followed by the Eastern sectors, Western sector, and Norther sector with a mean score of 3.9, 3.3 and 3.2. This implied that the rural banks in the southern sector of Ghana have a higher level of digitalization of ESG practices than those in the other sectors. Hence, there appear to be regional disparities in the level of digitalization of ESG practices in rural banks in Ghana. The study suggests that rural banks in the other sectors of Ghana (Eastern, Western, and Northern) may need to invest more resources and effort in digitalizing their ESG practices to catch up with the banks in the southern sector. The R2 suggest that variations in DESG among Ghanaian rural banks could explain 38.67% performance of the four main sectors of the location of rural banks.

Figure 2. Difference in DESG among the four main sectors.

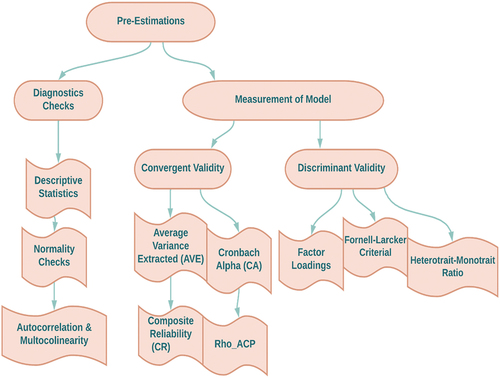

4.1. Pre-diagnostics test

To ensure the reliability and accuracy of our findings, we conducted a comprehensive pre-diagnosis test that included many tests. They included analyzing descriptive statistics, confirming normality, evaluating possible autocorrelation and multicollinearity concerns, and verifying convergent and discriminant validity.

We used several metrics, such as composite reliability, factor loadings, average variance extracted, Cronbach’s alpha coefficient, and Rho_ACP, to measure convergent validity. In addition to the Fornell-Larcker criterion and the heterotrait-monotrait ratio, we assessed the discriminant validity of the model. By undertaking these tests, we confirmed that our analysis was solid and thorough and that our conclusions were dependable and genuine. This can be found in Figure .

Figure 3. Pre-estimations of the model.

4.1.1. Descriptive statistics

The descriptive statistics table summarizes the most important statistical measurements of the study’s variables. This information in Table is crucial in understanding the respondents’ overall perception of the constructs. The table shows each variable’s average score (mean), highest and lowest values, standard deviation (SD), excess kurtosis and skewness. The results revealed that respondents generally had a positive perception of the constructs, with digitalized ESG (DESG) having the highest mean value (4.21) and financial performance (FP) having the lowest mean value (3.58). The standard deviation values, which indicate the spread of the data, ranged from 0.49 to 0.93, with financial performance (FP) having the lowest value and digitalized ESG (DESG) having the highest value. The kurtosis values range from 1.027 to 2.835, indicating that all constructs have heavier tails than the normal distribution. Finally, the skewness values range from −0.428 to −0.103, meaning that all constructs are approximately symmetrical. These statistics provide valuable insights into respondents’ perceptions and data distribution across the constructs.

Table 3. Descriptive statistics of Empirical data

4.1.2. Multicollinearity and autocorrelation

Multicollinearity and autocorrelation are issues that can affect the accuracy and consistency of results in PLS-SEM. In our study, we took steps to evaluate these issues by examining the tolerance and variance inflation factor (VIF) values for each construct in the correlation matrix provided in Table . The tolerance values show how much of a variable’s variance the other variables in the model can account for. The tolerance values in our table ranged from 0.727 to 1.539, which is within the acceptable range and suggests that none of the variables are highly correlated (Hair et al., Citation2017).

Table 4. Correlation matrix of the constructs

The VIF values show how much a coefficient’s variance has grown because of multicollinearity. In our study, the VIF values ranged from 2.44 to 4.76, below the threshold of 5, indicating that multicollinearity is not a significant issue in our model. We also examined the correlation matrix and found that the highest correlation coefficient between any two variables was 0.405, which is not significant enough to cause autocorrelation. Overall, our analysis suggests that multicollinearity and autocorrelation are not major concerns in our model, strengthening our results’ validity and reliability. To address the problem of multicollinearity further, we also analyzed each construct’s cross-loadings and path coefficients and found no indication of excessive cross-loadings or route coefficients.

4.1.3. Validity and reliability

In this study, we wanted to ensure that the questions we used to measure the five constructs (digitalized ESG, stakeholder engagement, customer loyalty, brand equity, and financial performance) were reliable and valid. To do this, we used several measures to assess the quality of the items, including factor loading (FL), Cronbach’s alpha (CA), composite reliability (CR), rho_ACP, and the average variance extracted (AVE). We found that all five constructs were acceptable in terms of validity and reliability, with most of the questions meeting or exceeding the minimum threshold values. For the digitalized ESG, we found that all the questions were very reliable and valid. Both stakeholder engagement and customer loyalty constructs had high levels of reliability, with all of their questions meeting the minimum threshold values for reliability and validity. While the brand equity construct was acceptable in terms of reliability, the convergent validity could have been better due to low AVE scores. Lastly, the financial performance construct had sufficient reliability and good convergent validity. Overall, the results suggest that the questions we used in this study to measure the constructs were of good quality. However, some constructs performed better than others regarding reliability and convergent validity. Please refer to Table for a more detailed summary of the results.

Table 5. Results of validity and reliability of items constructs

Using the Fornell-Larcker criteria and the Heterotrait-Monotrait (HTMT) ratio, the discriminant validity analysis, a crucial test to determine the uniqueness of each construct, was undertaken. The Fornell-Larcker criteria check whether each construct’s average variance extracted (AVE) is larger than the shared variance between that construct and other constructs in the model. The findings of this study as seen in Table indicated that all constructs satisfy the Fornell-Larcker criteria, showing that each construct in the model is distinct from the others.

Table 6. Discriminant validity

In addition, the Heterotrait-Monotrait (HTMT) ratio measures the correlation between items within each construct to the correlation between each pair of constructs. All of the HTMT ratios were lower than the required cutoff of 0.90 as indicated in Table , showing that the components can tell things apart. This research proves that the measurements we use to test the characteristics in our model are accurate and show that each construct is different. These results make our model more reliable and valid, giving us more faith in the conclusions of the analysis.

4.2. Results from PLS-SEM

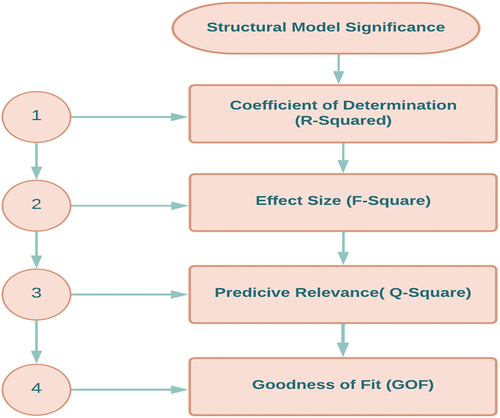

4.2.1. Measurement of the model: Model goodness and fitness

This section of the study aims to assess the validity of a Partial Least Squares Structural Equation Modeling (PLS-SEM) model based on several criteria. PLS-SEM is a common technique for studying complicated interactions between latent variables, and it may be used to evaluate theoretical models in various areas (Ahakwa et al., Citation2021). Using R-squared, Adjusted R-squared, Goodness of Fit Index, Root Mean Square Error of Approximation, Comparative Fit Index, and Tucker-Lewis Index, we analyze the model fit in this article. The composition of these criteria may change based on the study design and PLS-SEM software used, as seen in Figure .

Figure 4. Structural model significance.

We used several metrics, such as adjusted R2, Q2, and F2, to measure how well our proposed models worked and how accurate they were. We also utilized recommended threshold values for the goodness of fit index, as outlined in Table . In Model 1, which included control variables such as firm size, firm age, and location, we observed an R2 value of 0.286 and an adjusted R2 of 0.304. The Q2 value was 0.259, indicating satisfactory predictive relevance, while the F2 value was 0.381, surpassing the recommended threshold of 0.35. These findings suggest that the model is both predictive and has an acceptable level of goodness of fit.

Table 7. Model goodness and fitness

Model 2 explored the direct impact of ESG on brand equity (BE), resulting in an R2 value of 0.483 and an adjusted R2 of 0.529. The Q2 value was 0.387, and the F2 value was 0.368, indicating a moderate level of predictive relevance. So, this model accurately predicts how ESG will directly affect BE. However, the model’s direct effect of ESG on financial performance (FP) showed only a slight variance (an R2 value of 0.240 and an adjusted R2 of 0.351). Although the Q2 value was 0.473, the F2 value was 0.439, which is below the recommended threshold, suggesting the model may not have solid predictive relevance for the direct effect of ESG on FP. We also explored the impact of BE on FP, resulting in an R2 value of 0.582 and an adjusted R2 of 0.596, with a Q2 value of 0.279 and an F2 value of 0.392, indicating moderate to good predictive relevance.

In Model 3, we investigated the mediation effect of stakeholder engagement (SE) and customer loyalty (CL) on the relationship between ESG and BE. The Q2 values were more significant than 0 for all three indirect effect paths, indicating moderate to good predictive relevance. Specifically, the Q2 values were 0.429 for (SE → DESG → BE), 0.368 for (CL → DESG → BE), and 0.279 for (SE & CL → DESG → BE), with corresponding F2 values of 0.358, 0.419, and 0.391, respectively.

Finally, we analyzed the effect of both ESG and BE on FP, resulting in an R2 value of 0.439 and an adjusted R2 of 0.583. The Q2 value was 0.581, and the F2 value was 0.460, indicating moderate predictive relevance for the effect of ESG and BE on FP. Overall, our findings suggest that the proposed models have good predictive relevance and an acceptable level of goodness of fit. However, we noted weaker predictive relevance for some direct effect paths, highlighting the continued research’s importance.

4.2.2. Hypothesis testing

Below is a discussion of the research findings examining the link between maximizing digitalizing ESG and brand equity in rural banks in Ghana, with a particular emphasis on the role of stakeholder involvement and customer loyalty as mediators. As shown in Table , the study’s findings shed light on the considerable influence of numerous factors on the outcomes of interest.

Table 8. Hypothesis testing

Firm size, age, and location have been found as important control factors, with company size and age having beneficial impacts on ESG and brand equity. It was also discovered that location favorably impacted ESG, brand equity, and stakeholder involvement. According to Model 1, company size (β = 0.691, t = 9.278, 95% CI [0.273, 0.582], p < 0.05), firm age (β = 0.348, t = 8.492, 95% CI [0.479, 0.783], p < 0.05), and location (β = 0.680, t = 7.469, 95% CI [0.138, 0.469], p < 0.05) are significant predictors of the dependent variable (brand equity).

In Model 2, both the direct effect of maximizing DESG on brand equity (β = 0.513, t = 11.812, 95% CI [0.692, 1.068], p0.05) and the direct effect of brand equity on financial performance (β = 0.537, t = 13.478, 95% CI [0.473, 1.278], p < 0.05) are significant, providing support for the hypothesized relationships. In a similar line, the researchers discovered that the direct impact of boosting DESG on financial success is statistically substantial ((β = 0.386, t = 8.393, 95% CI [0.438, 0.800], p < 0.05). These results highlight the importance of brand equity in fostering customer loyalty and rural banks’ need to pursue ESG initiatives to strengthen their brand equity. This indicates that successful stakeholder involvement and customer loyalty programs may amplify the beneficial benefits of ESG on brand equity, highlighting the need for rural banks to implement such programs.

The third model investigates the moderating effects of stakeholder involvement and consumer loyalty on the link between optimizing ESG and brand equity. The findings suggest that stakeholder engagement (β = 0.248, t = 9.749, 95% CI [0.539, 0.632], p < 0.05), customer loyalty connections (β = 0.458, t = 10.483, 95% CI [0.386, 0.473], p < 0.05), and the combination of stakeholder engagement and customer loyalty connections (β = 0.683, t = 12.683, 95% CI [0.582, 0.639], p < 0.05) all In addition, the impact of optimizing ESG and brand equity on financial performance is statistically significant (β = 0.472, t = 8.493, 95% CI [0.472, 0.494], p < 0.05).

According to the research, both ESG and brand equity were shown to influence financial performance directly. This emphasizes the significance of integrating ESG and brand equity concerns into the financial plans of rural banks, which has the potential to boost their overall financial performance. Overall, this study’s results highlight the significance of digitization in rural banks to enhance interest returns. The report highlights the need for rural banks in Ghana and abroad to emphasize ESG initiatives, increase stakeholder involvement and customer loyalty ties, and include brand equity considerations in their financial plans.

4.2.3. Additional analysis

In order to thoroughly understand the research hypotheses in the Ghanaian context, sub-groups (northern, eastern, western, and southern sectors) analysis was further conducted to shed additional light on the relationship between digitalization of ESG practices and brand equity in rural banks in Ghana. By delving deeper into the data and exploring various sectors that may impact this relationship, we can better understand how rural banks in Ghana can leverage digitalization to enhance their ESG practices and, ultimately, their brand equity, as illustrated in Table .

Table 9. Sub-group analysis of hypothesis

Based on the results presented in Table , a comparison can be made between the four sectors regarding their goodness of fit and model fitness using the adjusted R2, Q2 and F2 values. The adjusted R2 indicates that the proportion of variance explained by the model was highest for the Eastern sector (0.420), followed by the Southern sector (0.385), the Northern sector (0.328), and the Western sector (0.142). This suggests that the model fits better for the Eastern and Southern sectors, while it has less explanatory power for the Northern and Western sectors.

Again, a comparison was made using the models’ predictive power(Q2 >0 value). This measures the predictive ability of the model was above 0.35 for all four sectors. This indicates that the model has good predictive power for all sectors.

Moving away from the above, the study further analyzed the effective size, where it was found that F2 >0.35, which measures the overall fitness of the model, was above 0.35 for the Eastern and Southern sectors, indicating good model fitness. However, it was below 0.35 for the Northern and Western sectors, indicating poor model fitness. In light of these results, it can be concluded that the Eastern and Southern sectors have higher goodness of fit and model fitness than the Northern and Western sectors. It is important to note that the results are based on the specific variables and hypotheses tested in this study and may not necessarily apply to other contexts or variables.

4.3. Discussions

Five leading research objectives guided the study. Based on the analysis of the study, it was revealed that digitalizing ESG practices have a beneficial impact on brand equity. The link between the digitization of ESG practices and brand equity is mediated through stakeholder engagement. Also, the association between the digitization of ESG practices and the brand equity of rural banks in Ghana is mediated through customer loyalty. Lastly, the link between the digitization of ESG practices and brand equity is mediated through stakeholder involvement and customer loyalty. Lastly, Ghanaian rural banks’ financial performance is enhanced by digitalizing ESG and brand equity. Details of the results are discussed below:

Regarding the first objective, the study found a positive relationship between the digitalization of ESG practices and brand equity. The outcome of this study is consistent with earlier findings that customers are growing more socially and environmentally concerned and are more willing to support businesses that promote ESG practices. The results show that organizations should emphasize ESG digitalization initiatives as part of their overall sustainability strategy to increase brand equity (Ben Salah & Ben Amar, Citation2022; Dicuonzo et al., Citation2022; Menicucci & Paolucci, Citation2023; Niu et al., Citation2022; Puriwat & Tripopsakul, Citation2022; Zhou, Citation2022). However, it is essential to recognize that ESG digitization initiatives may not be sufficient to increase brand equity. To improve their brand image and reputation, businesses should also prioritize establishing trust and credibility with their stakeholders through effective stakeholder engagement. For instance, a study by some scholars (Laboure et al., Citation2021; Lestari & Adhariani, Citation2022; Mensah, Citation2017) revealed that customers perceive companies with good ESG practices to be more trustworthy credible, leading to increased brand equity.

Moreover, the digitalization of ESG contributes to banks’ enhanced brand perception and consumer trust, resulting in increased brand equity. However, it is essential to highlight that not all research has shown a correlation between ESG practices and brand equity. It can be asserted that ESG disclosure positively impacts business reputation rather than brand equity. According to the authors, brand equity is a smaller concept focusing on consumer impressions of a brand’s distinctive value proposition. In contrast, corporate reputation is a larger concept encompassing perceptions of the company’s general character and conduct.

Findings from the second research objective identified stakeholder engagement as a critical element in enhancing brand equity. The study found that the relationship between the digitization of ESG by rural firms and their brand equity can be mediated by stakeholder engagement. Stakeholder participation mediates the relationship between the digitalization of ESG practices and brand equity. In other words, Archie and Caroll’s (Citation2014) study supports the idea that stakeholder participation mediates the connection between ESG digitalization and brand value. The research indicates that effective stakeholder involvement may improve a company’s standing in the eyes of its key constituencies. The study shows that stakeholder engagement may boost a rural bank’s brand equity if it prioritizes ESG practices and uses digitalization efforts to improve its ESG performance. By consulting with community members, rural financial institutions may learn about the problems of their customers and other stakeholders. This might enhance their standing in the eyes of their target audience and potential investors.

Additionally, the study by some scholars (Bhamra et al., Citation2018; Goddard, Citation2017; Liu et al., Citation2020, Citation2022; Puriwat & Tripopsakul, Citation2022; Xia, Citation2022) found that stakeholder engagement positively influences brand equity. Companies prioritizing stakeholder engagement will likely see an increase in brand equity and a competitive advantage in the market. Other researchers found no correlation between stakeholder participation and brand equity. For instance, Turker discovered that stakeholder participation did not affect brand equity. This shows that stakeholder participation’s effect on brand equity depends on the context and stakeholder engagement. According to the research, the findings suggest that stakeholder engagement is crucial to ESG digitization and brand equity. Stakeholder engagement may boost brand image, consumer loyalty, and financial performance. So, to reap the advantages of ESG digitalization, organizations must improve ESG processes and involve stakeholders.

The third objective of the study was to investigate whether customer loyalty mediates the relationship between the digitalization of ESG practices and brand equity. One of the most critical factors in developing rural banks in Ghana is the loyalty of their customers. According to the results, rural banks that invest in digital efforts to boost customer satisfaction are more likely to keep their existing customers and attract new ones (P. K. T. Tran et al., Citation2021). The study found that customer loyalty significantly mediates the relationship between the digitalization of ESG practices and brand equity. This finding is consistent with previous research that has emphasized the importance of customer loyalty in enhancing the value of a brand (Agus Harjoto & Salas, Citation2017; Appiah & Gabrielsson, Citation2023; Bansal & Pruthi, Citation2021; Zameer et al., Citation2019). Our results suggest that digitalizing ESG practices can enhance customer loyalty, improving brand equity. These investigations support the hypothesis that the relationship between the digitization of ESG practices and the brand equity of rural banks in Ghana is mediated through customer loyalty. Rural banks in Ghana may increase customer loyalty, boost brand awareness, and boost profits by emphasizing sustainability and introducing digitalization efforts that enhance the consumer experience. This demonstrates why it is crucial to think like a customer while digitizing environmental, social, and governance (ESG) activities.

Moreover, the fourth research finding suggests that stakeholder engagement and customer loyalty jointly and positively mediate the relationship between the digitalization of ESG practices and brand equity. The results support previous studies (K. Amoako & Boateng, Citation2022; X. Li et al., Citation2021), where researchers affirmed that banks in Ghana have a positive association between their ESG practices and brand equity, which is mediated via stakeholder involvement and consumer loyalty. According to the findings, financial institutions may improve brand equity by placing a premium on sustainable practices, particularly those actively seeking stakeholder participation and customer loyalty. Stakeholder engagement affects brand equity differently depending on the situation (Ackah et al., Citation2014; Malik et al., Citation2020). So, organizations must do detailed needs assessments and establish unique engagement methods to build stakeholder confidence. One must know the area’s history, culture, and social dynamics to achieve this. According to the reviewed and contrasted empirical data, stakeholder participation in ESG digitalization projects may improve brand equity. Stakeholder involvement may boost brand image, consumer loyalty, and financial performance. Stakeholder participation may affect brand equity depending on the context and degree. So, firms must carefully examine stakeholder requirements and expectations and establish specific engagement methods to generate trust and confidence.

The last goal was determining how digitizing ESG and brand equity improves financial performance. This supports prior findings suggesting that ESG practices improve financial success (Anlesinya, Citation2016; Appiah-Konadu et al., Citation2022; Ayakwah et al., Citation2021; Buallay, Citation2019; El Khoury et al., Citation2023). Our results suggest that digitalization may increase brand equity and financial performance. Digitalizing ESG practices have cost implications. Stakeholder engagement and customer loyalty link ESG digitalization to brand equity. Our results reinforce the importance of stakeholder participation and customer loyalty in building brand equity. These studies strongly support the idea that digitalizing ESG and brand equity may improve rural bank financial performance in Ghana. Rural banks in Ghana may improve their financial performance by emphasizing sustainability and digitization.

5. Conclusions

To sum up, this research aimed to look at how digitalization might improve environmental, social, and governance (ESG) metrics and brand equity in rural banks in Ghana, with an eye on how these metrics can mediate stakeholder involvement and customer loyalty. The research showed that rural banks’ brand equity in Ghana increased as their ESG policies became more digital. This link was moderated by stakeholder involvement and consumer loyalty, and the combined mediating impact of these two variables was also found to be statistically significant. Digitalization of ESG and brand equity were also proven to impact the financial performance of rural banks positively. Significant ramifications for rural banking in Ghana and elsewhere are found in this research. The research shows how digitization may help boost ESG practices and brand equity, which can boost financial results. As a mediator between ESG practices and brand equity, the report highlights the importance of rural banks prioritizing stakeholder involvement and customer loyalty programs. The research offers helpful information for rural banks that want to strengthen their environmental, social, and governance (ESG) standards, build customer loyalty, and increase profits. Some practical implications of this research topic could include the following:

Firstly, the findings of this study could help rural banks in Ghana leverage and improve the use of digital devices such as mobile banking, online portals, and social media to enhance customer engagement and experience. This will increase rural banks’ customers’ access to financial services and provide convenience, which could reduce transaction costs and improve comfort for customers.

Secondly, the decision by firms to digitalize ESG practices by enhancing their bank’s reputation and increasing its attractiveness to environmentally conscious customers. This includes banks such as rural banks’ decision to invest in projects geared towards improving their ESG and financial performance.

Thirdly, the study’s findings suggest the need for rural banks to engage with their stakeholders, such as customers, employees, and local communities, by leveraging digital platforms. Continuous efforts to engage with their stakeholder could foster a sense of community and encourage customer loyalty. For instance, rural banks could benefit from digitization through social media to solicit customer feedback and address their concerns in real time.

Lastly, besides those above, rural banks can further enhance their ESG performance and stakeholder engagement, improving their brand equity. This will give them a positive brand image that can attract new customers, increase customer retention, and enhance their financial performance.

Overall, this research topic has practical implications for rural banks in Ghana looking to enhance their ESG performance, stakeholder engagement, and brand equity through digitalization. One possible theoretical significance is a better grasp of how stakeholder involvement may pave the way for the acceptance and implementation of environmental, social, and governance (ESG) policies, which influence consumer loyalty. In addition, this discussion added to the expanding body of work on how digitization and sustainability practices interact, especially in developing economies like Ghana. It can shed light on how rural banks might use digital technology to have a positive social and environmental effect while also boosting their bottom line and public standing.

6. Recommendations, limitations, and suggestions for further studies

6.1. Recommendations

The study’s results show that Ghana’s rural banks would benefit from digitizing their ESG processes, boosting both their brand value and bottom line. Financial institutions should focus on making good stakeholder engagement and customer loyalty programs so that their ESG initiatives positively affect their brand equity. By investing in digital infrastructure and platforms, rural banks can improve their stakeholder engagement, customer loyalty programs, and environmental, social, and governance (ESG) reporting. Also, they should keep their stakeholders informed of their ESG activities and developments to earn their confidence and support.

As the research demonstrated a strong correlation between ESG, brand equity, and financial success, rural banks may want to include these concepts in their financial plans. This may be done by boosting the bank’s brand equity and investing in creating financial goods and services that align with ESG principles. The above suggestions can only come to fruition if rural banks in Ghana put money toward modernizing their ESG procedures for the digital age. Using today’s available technology and software solutions to improve data collection, processing, and reporting is possible. As a result, ESG procedures will become more effective, and the expenses and mistakes usually associated with them will also be reduced. In addition, it is recommended that rural banks in Ghana emphasize stakeholder participation by identifying and including essential stakeholders, including staff, customers, suppliers, and the community, in decision-making processes linked to ESG practices. Regular feedback systems, training and awareness initiatives, and inclusive decision-making methods are all ways to achieve this goal.

Also, rural banks should try to make their customers more loyal by emphasizing customer service, customized offerings, and reaching out to the community. Brand recognition and customer loyalty for rural banks will rise as a result. The digitization of environmental, social, and governance (ESG) practices and brand equity is complicated. Rural banks would do well to adopt a holistic strategy that considers the combined mediating effects of stakeholder engagement and customer loyalty links on this topic. Incorporating these two considerations into ESG processes and using data-driven methods to monitor and assess their impact on brand value are two ways to achieve this goal. The research concludes by stressing the significance of ESG and brand equity concerns in rural banks’ financial strategies. When choosing where to invest or lend money, rural banks should emphasize environmental, social, and governance (ESG) initiatives and evaluate the possible effect on brand equity and financial performance. To accomplish this, one might use a “triple bottom line” strategy that values not just monetary gain but also social and environmental impact.

6.2. Limitations and area of further studies

Many caveats should be considered despite the study’s valuable findings. First, the research only looks at rural banks in Ghana, which may make the results less applicable to other situations. Also, convenience sampling may inject bias into the sample. Future research can overcome these restrictions by using a larger sample size and expanding their investigation into the effect of ESG practices on brand equity. Even though this research shows mediating results between stakeholder involvement and customer loyalty, more research needs to be done to find out how they work.

Future studies could be helped by researching how stakeholders are involved and how loyal customers affect brand equity. As the report concludes, digitization is essential for optimizing the beneficial effects of ESG policies on brand equity and financial success. However, the exact digital tools and platforms that may aid in this process have yet to be investigated. The digital technologies and tactics that might help digitize ESG practices in rural banks could be the subject of future study.

Authors’ contribution

Francis Atta Sarpong; Conceptualization, literature review and final manuscript, Peter Sappor; Literature Review, Discussion, Proof Reading, George Nyantakyi; Analysis and Discussion, Isaac Ahakwa; Literature and proofreading, Owusu Esther Agyeiwaa; Investigation and conceptualization, Benjamin Blandful Cobbinah; data collection and visualization.

Consent to participate

Approved

Consent to publish

All authors reviewed and approved the manuscript for publication.

Ethics approval

Was sorted

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Francis Atta Sarpong

Francis Atta Sarpong is a PhD candidate at the School of Finance, Zhongnan University of Economics and Law, Wuhan, China. His main research interests lie in sustainable accounting and finance, green financing, energy financing, green investment and financial risk.Peter Sappor is an assistant lecturer at the Department of Accounting of the University for Development Studies, Ghana. He is a researcher with peculiar interest in financial reporting, accounting education, accounting ethics, sustainability reporting, management and cost accounting.

References

- Aaker, D. A. (1991). Managing brand equity: Capitalizing on the value of a brand name. New York: The Free PressAgarwal, MK & VR Rao, 1997. An empirical comparison of consumer-based measures of brand equity. Marketing Letter, 7(3), 237–37.

- Abor, J. Y., Agoba, A. M., Mumuni, Z., & Yawson, A. (2022). Monetary policy, central banks’ independence, and financial development in Africa. In The economics of banking and finance in Africa: Developments in Africa’s financial systems (pp. 227–267). Springer International Publishing.

- Aboud, A., & Diab, A. (2018). The impact of social, environmental and corporate governance disclosures on firm value: Evidence from Egypt. Journal of Accounting in Emerging Economies, 8(4), 442–458. https://doi.org/10.1108/JAEE-08-2017-0079

- Ackah, D., Kondegri, M. P., & Agboyi, M. R. (2014). The role and impact of rural banking on SMES (Small Medium Enterprise) in Ghana. Global Journal of Management Studies and Researches, 1(5), 311–323.

- Adejumo, O. O., Adejumo, A. V., & Aladesanmi, T. A. (2020). Technology-driven growth and inclusive growth-implications for sustainable development in Africa. Technology in Society, 63, 101373. https://doi.org/10.1016/j.techsoc.2020.101373