Abstract

The aim of this study is to perform the impacts of corporate social responsibility (CSR) based on the firms’ performance (FP). These investigations also provide the mediating role of access to finance (AF) as well as business model innovation (BMI) using the relationship of CSR and FP. This study principally follows quantitative method. The smart use of the PLS SEM to investigate the data of the SMEs in Vietnam in 2020. The findings of this work indicate an important and positive effect of CSR on FP using the AF and BMI mediated in this relation. The study brings a mechanism by which corporate social responsibility results in firm performance: SMEs with improved CSR practices will be better positioned for AF and BMI those translating into improved competitiveness for improved firm performance in a sustainable direction. The originality of this study is to provide the comprehensive CSR practices based on the financial representations of SMEs in the developing countries. Moreover, this study shows a rare work that establishes a relationship between the financial SMEs performance and CSR practices in Vietnam through the financial and business model innovation as mediation, particularly that favors revisionist view of CSR in the current context of Vietnam. The objective of this work is to provide the important implications for business practitioners and managerial level of SMEs with respect to increase in CSR awareness as well as the importance of CSR long-term strategic planning in their corporate focus strategy.

PUBLIC INTEREST STATEMENT

In the globolisation’s context, corporate social responsibility (CSR) is the key aspect in contributing to the sustainable firm performance (FP). The findings of this study suggest that the better the businesses practice their CSR, the higher the possibility of access to finance (AF) and business model innovation (BMI), which in turn leads to improved FP. The originality of this study is to provide the comprehensive CSR practices based on the financial representations of SMEs. Moreover, this study shows a relationship between the financial SMEs performance and CSR practices in Vietnam through the financial and business model innovation as mediation, particularly the favours revisionist view of CSR in the current context of Vietnam. The study provided the important implications for business practitioners and managerial level of SMEs with respect to increase in CSR awareness as well as the importance of CSR long-term strategic planning in their corporate focus strategy.

1. Introduction

One of the strategic categories of firms’ operations is the corporate social responsibility (CSR) that has got huge popularity as well as significantly increasingly towards the sustainable development (Ye et al., Citation2020). CSR is perceived as a multidimensional perception that imitates a firm’s response to the expectations along with the needs of its various stakeholders with respect to the environment, society, and individuals (Yuan et al., Citation2020). It becomes a worldwide phenomenon that creates an attention among the academia, entrepreneurs, firms’ executive and public during the past few decades. Firms tend to increase by applying CSR principles for various reasons that may come from external pressure, internal motivation, or both, in such a way that CSR is seen as the focal point of sustainability (Soojeen et al., Citation2019). Nevertheless, whatever reason is behind the fact, the business dynamics majorly used to survive and develop in a sustainable direction by satisfying its stakeholders’ expectation and produce competitive advantages for firms, simultaneously, that indicate the social and environmental issues (Fernandez-Kranz & Santalo, Citation2010; Hawn & Ioannou, Citation2016).

The firm is considered as an entity of society, and it is expected to form the social responsibility for its operations. As a result, CSR practice generates valuable outcomes to perform the influences on the firm performance (FP), which provides the significant attention to its stakeholders, entrepreneurs, and business practitioners. The recent studies represent the relationship between FP and CSR and based on the inconsensous findings (Javed et al., Citation2020; Sharma, Citation2019). Most important findings of this study indicate that CSR has a vital and positive relationship with the performance of the firm (Blackburn et al., Citation1994; Graves & Waddock, Citation1994). In another sense, some findings defined that the relationship between FP and CSR is negative (Julian & Ofori-Dankwa, Citation2013; Klassen & Whybark, Citation1999), while some others determined that the relationship between both is neutral (Peloza, Citation2009; Surroca et al., Citation2010).

Although much work has been provided in the current literature based on the relationship between FP and CSR, however, integrated mediators of access to finance (AF) and business model innovation (BMI) into a single conceptual research model remained scarce. Importantly, with the presence of inconsistency of findings in the current literature as aforementioned those may be explained by different economy settings, different industry sectors and cultural or institutional (Han et al., Citation2016). From a business perspective, economy settings have a vital role to operate and it is necessary to conduct a new research on CSR and FP with the novel conceptual model. Thus, this study presents an integrated conceptual model to indicate a relationship between CSR on FP, mediating role of AF and BMI. Specifically, the focus of this work are SMEs as they need it properly (Das et al., Citation2020; Martinez-Conesa et al., Citation2017) and work as an emerging economy in Vietnam, where competition enhanced due to the global integration pressure. In addition, COVID-19 pandemic has been causing a global crisis that seriously affects the sharing economy activities (Hossain, Citation2021) as well as increase competitive pressure on businesses for competitiveness. SMEs is the driving force of emerging economy as its significant contribution to the economic development of the nation Beck et al. (Citation2005), reduce poverty (Vandenberg, Citation2006); create jobs (Lukács, Citation2005) and practice innovation (Terziovski, Citation2010). Moreover, there are many challenges linked to the AF in Vietnam for SMEs as compared to other regions, competitions, business model and lack of resources to support. These issues hinder the development of businesses and negatively effects on the competitiveness of businesses (Ciunova-Shuleska et al., Citation2017). Thus, this presented an intensive framework through research based on SMEs to enhance its performance in a sustainable manner.

This paper shows the important contributions based on the current literature of CSR and FP in order to differentiate these investigations from the previous studies. Firstly, it provides a comprehensive understanding of CSR concept and proper practices based SMEs in the new provided context in Vietnam. Indeed, SMEs in the new context will need it properly for survival and development because it is significantly flawed in current practices of SMEs. As Das et al. (Citation2020, p. 1) state, “Environmental and social practices are grossly ignored in SMEs more precisely in emerging markets”. Secondly, it defined a mechanism of how CSR improves FP by integrating AF and BMI as mediators in this relation. SMEs in Vietnam has various problems using the relationship of the finance approach and BMI as compared to other countries. This disclosure is significant in the current context of Vietnam where the pace of socio-economic development is faster than ever, particularly the recent major economic and medical achievements and even during the period of global crisis due to COVID-19 pandemic. Thirdly, this work provides the empirical support for SMEs in the manufacturing sector of the emerging economies regarding their sustainability strategy. Lastly, this paper can provide a deep vision of CSR for the supportable progress of SMEs that are crucial to the economy, from a broader perspective. Therefore, policy makers need to pay attention in order to make the reform in the policy to stimulate and enable SMEs in implementing properly along the initiatives of CSR voluntarily.

To address the objectives, this research based on some major questions, (1) “How do SMEs currently observe the CSR role in the Vietnam context as an emerging market?” (2) “How do current SMEs plan their CSR initiatives and implement them in the Vietnamese context?” (3) “How do current SMEs identify stakeholders in their business?” (4) “How is CSR associated with financial access of business and business model innovation for SMEs in the Vietnamese market?” (5) “How does CSR affect firm performance, especially in the context of increasing global integration, increasing competitive pressure?” and (6) “Whether or not access to finance and business model innovation mediate the relationship between CSR and firm performance?”

The structure of this study has six major sections. Section 1 is the introduction. Section 1 includes several subsections, which present the underpinning theories, relevant concepts, develop research hypotheses, and summarize systematic literature review. Section 2 presents the conceptual model. Section 3 presents the study design and methods. Section 4 designates the analysis and results interpretations. Section 5 is related to the findings of the study and provides theoretical and managerial implications. Section 6 concludes the investigations and section 7 highlights the limitations and scope of further research.

2. Literature revew and hypothesis development

2.1 Underpinning theories

This work used stakeholder theory (Freeman, Citation1984), resource advantage theory (Hunt & Morgan, Citation1995), and sustainability vision theory (Kantabutra, Citation2020) as underpinning theories. According to stakeholder theory perspective, stakeholders are those who are affected by business’s operations, simultaneously affect firm performance in various ways. In this regard, stakeholders include employees, customers, partners, communities, society at large, and the environment (Freeman et al., Citation2020). The stakeholder approach is crucial in exploring management-related areas such as CSR. CSR activities create cohesion between businesses and stakeholders; accordingly, businesses receive positive responses from stakeholders (Gunawan et al., Citation2020).

In addition, from resource advantage theory perspective (Hunt & Morgan, Citation1995), the competition process in market-based economies pertains to the context in which competition involves the continuing struggle between firms for competitive benefit and outstanding measures. Regarding the theory of sustainability vision (Kantabutra, Citation2020), an operative sustainable vision should be focused to addressing the interests of various stakeholders and increasing stakeholder satisfaction, those are affected by the business operations and can affect the business performance in various ways. Stakeholders include shareholders, owners, customers, organization members, the environment and community. In this context, corporate sustainability vision is demonstrated through consistently practicing socially responsible management for internal and external stakeholders.

Taking approach from the perspective of the stakeholder theory, enterprises practicing CSR feel pressure from stakeholders, thus, they sustain their efforts in management practices and business activities to meet stakeholder expectations. In return, they enhance the value of their resources in a way that increases competitive advantage and ultimately leads to improved business performance in a sustainable way. In the present context, AF and BMI are seen as a return to businesses from integrating their socially responsible activities and behaviors into management practices towards their stakeholders. In this regard, AF and BMI are considered as resource advantage of enterprises which are crucial in helping them improve their competitive advantages and firm performance. In this study, the main line of argument is that businesses can achieve their goals when they address the interests of their stakeholders in a sustainable way through CSR practices.

2.2 Corporate Social Responsibility (CSR)

The definition of CSR is evolved over time in a more stimulating and profound way to attract further attention from businesses and stakeholders (Singh & Misra, Citation2021). CSR is conceptually described as firm’s voluntariness in implementing socially and environmentally responsible management practices towards their various stakeholders for a sustainable future on the balance of economic, social, and environmental value (Le et al., Citation2021a; Leet al., Citation2021b; Sharma, Citation2019). In this regard, value-creating activities must be carried out with genuine effort and not compromise on environmental and social issues. According to Freeman et al. (Citation2020), business stakeholders include internal-stakeholders and external-stakeholders who can be affected by the business operations and, simultaneously, can affect the corporate performance in various ways. In the context of globalization and series of environmental challenges today, stakeholders are increasingly concerned in the behavior and responsibility of businesses to the environment and society for sustainable development (Gunawan et al., Citation2020; Singh & Misra, Citation2021).

In developed economies, CSR is commonly integrated into corporate strategies as a sustainable development strategy while this practice is lacking in developing countries (Bhatia & Makkar, Citation2020). According to Turker (Citation2009) and Vives (Citation2006), internal CSR practices are voluntary actions of firms to improve the well-being of internal stakeholders, such as the employees. Internal CSR practices basically include employee training and development, health and safety assurance, equal opportunities providing, work life balancing, healthy and creative work environment, and ability of participation in business operation. While Carroll (Citation1979) defined external CSR as voluntary actions of firms in relation to addressing society issues at large and its interaction with the physical environment. In addition, Cornelius et al. (Citation2008) determined that external CSR practices are perceived include marketing-related activities, volunteerism of employee, charitable-related donations, philanthropic-related activities, community-related projects and programs of environmental preservation and protection.

Carroll (Citation1991) determined the dimension of CSR, which consists of four major categories in relation to law; economics; ethics and charity and those that verified with numerous stakeholders of the society, such as customers, community, business owners, society and employees using the business relation towards improving and maintaining the good customers as well as spreading good behaviors and curbing, eliminating bad behaviors towards related firms’ stakeholders. In this study, CSR measures based on the dimension determined by Carroll (Citation1991) with modification so that it’s suitable with the context in Vietnam.

2.3 CSR and Firm Performance (FP)

The relationship between CSR and firm performance is theoretically argued from the perspective of stakeholder theory. From this point of view, CSR practices show the concern of the business to the issues of interest to stakeholders (Famiyeh, Citation2017; Mahrani & Soewarno, Citation2018). In return, this leads to improved corporate reputation in front of stakeholders, enhanced competitive advantage, and ultimately to improved firm performance. According to Feng et al. (Citation2017); Martinez-Conesa et al. (Citation2017), the success of a business depends on its ability to build relationships with stakeholders. According to Freeman (Citation1984), stakeholder theory can well explain the positive relationship between CSR and firm performance.

The current literature shows that the relationship between CSR and firm performance is approached from different angles and with mixed results (Velte, Citation2021). In which, some empirical literature shows that CSR practices have a positive relationship with business outcomes in terms of competitive edge (Eyasu et al., Citation2020); value of stock (Asogwa et al., Citation2020); market value (J. W. Lee, Citation2020); environmental and social performance (Padilla-Lozano & Collazzo, Citation2021); financial performance and competitive advantage (K. H. Lee & Min, Citation2015); sustainability performance (Le et al., Citation2021b; Jain & Winner, Citation2016). While other literature argued that the impact of CSR practices on firm performance is negative because implementing CSR is a cost (Huang et al., Citation2020).

According to Soewarno et al. (Citation2021), CSR has a positive and significant impact on the corporate performance. In this context, CSR is assumed to have a positive association with firm performance because consistent implementation of CSR initiatives can lead to embedding its associated responsible practices into the corporate culture. Accordingly, it affects the dynamics of enterprises in implementing initiatives that benefit stakeholders, the environment and society. As a result, this leads to positive attitudes of stakeholders towards the business, proactive innovation in the way doing things, improved corporate reputation, enhanced competitive advantages and market performance, and improved firm performance in a sustainable way (Islam et al., Citation2021; Javed et al., Citation2020; Kong et al., Citation2020).

Given the above discussions, the association between firm performance and CSR can be assumed as follows:

H1:

CSR has a significant positive association with financial performance.

2.4 CSR and Access to Finance (AF)

The association between firm performance and CSR is theoretically debated based on the stakeholder theory perspective. From this approach, practicing CSR leads to positive attitude of stakeholders towards the business, improves the business reputation in front of stakeholders, stimulates investment desire from outside investors and ultimately leads to high AF (Taghian et al., Citation2015; Zahari et al., Citation2020). According to Famiyeh (Citation2017) and Taghian et al. (Citation2015), businesses that sustainably implement CSR can achieve long-term and competitive benefits because of their ability to control risks and good relationships with human resources and stakeholders.

The relationship between CSR and AF was positively demonstrated (Ansong & Wanasika, Citation2017). In the context of many uncertainties in the business environment, investors expect enterprises to well control financial and operational risks. In the context of CSR, the integration of CSR strategy into corporate development strategy guides their business activities in an ethical and responsible manner. Gradually, these practices are embedded in their corporate culture that guides the business activities to be persistently ethical and responsible. This leads to improved reputation of the business in the market and heightened creditability, which in turn leads to improved AF (Ansong & Wanasika, Citation2017; DiGiulio et al., Citation2007). Furthermore, businesses that actively address environmental and social issues often strongly attract socially responsible investors (Ansong & Wanasika, Citation2017). In addition, businesses that are capable to well control environmental issues and risks are more likely to access to capital (Cheng et al., Citation2014; Sharfman & Fernando, Citation2008).

Based on the above argument, the hypothesis about the association between AF and CSR is proposed as follows:

H2.

CSR positively affects access to finance.

2.5 CSR and Business Model Innovation (BMI)

The association of CSR and BMI is discussed from a stakeholder theory point of view. From this perspective, consistency in practicing socially responsible management for internal and external stakeholders improves corporate culture in the way that guides all business behaviors and actions to be beneficial to stakeholders, environment and society at large. As a result, this leads to a positive attitude of stakeholders towards the business. For employees, internal stakeholder, this stimulates their innovative and creative thinking to optimize business processes to improve operational efficiency for cleaner environment and better society (Wang et al., Citation2020). For external stakeholders, CSR stimulates their positive collaboration for the business which is critical to the success of BMI.

BMI is a concept that attracts remarkable attention of strategy makers and researchers at most as it plays a very important role in business strategy to achieve organizational goals. According to Casadesus-Masanell et al. (Citation2010) and Mitchell and Coles (Citation2003), BMI can help firms to reach the potential customers and build association with them to “find a first-mover benefit”, at the same time “helps firms to establish dynamic benefits, which are hard to find the competitors in order to imitate the dynamic environment of the business”. BMI states to “the search for novel firm logics, and some new directions to capture and create the value for its stakeholders. Its emphasises mainly to find the new directions to produce revenues and generate the value propositions for partners, suppliers and customers” (Casadesus-Masanell et al., 2010).

According to Visnjic et al. (Citation2016), BMI can be classified into two subcategories including product-oriented BMI and customer-oriented BMI which can be measured across three dimensions of innovation for “value creation, value proposition and value capture” (Clauss, Citation2017). In this context, CSR can promote BMI because it involves innovative activities and changes for creating value, improving value, and adding value into the existing value. Socially responsible company impresses their responsiveness to the concerns of various stakeholders on environmental and social issues, which in return, beneficial to the business in terms of reputation. Accordingly, businesses can have supportive collaboration from stakeholders, which is very important in implementing BMI for value generation (McWilliams & Siegel, Citation2001).

In addition, CSR can positively associate with BMI because of its possibility of creating new business opportunity and business strategy. As aforementioned, CSR practice can lead to improved creative and innovative thinking for the betterment of the environment and society. As a result, this leads to a high possibility of BMI. Besides, environmental challenges that threaten human development also put pressure on traditional business models and open up opportunities for innovative business model (Halkos & Skouloudis, Citation2018). On the other hand, CSR can affect BMI because CSR has a significant role on the risk-taking of business leaders. In the context of BMI, leader’s ability to take risks is crucial to the ability to realize BMI. Meanwhile, CSR is demonstrated to positively influence the risk-taking ability of leaders because they understand the value that CSR brings to their businesses and the advantage of the first mover (Dunbar et al., Citation2016).

Given the above discussion, the hypothesis about CSR and BMI can be supposed as:

H3.

CSR has a positive impact on BMI.

2.6 Access to Finance (AF) and Firm Performance (FP)

The association of AF and FP can be debated mainly based on the perspective of resource advantage theory. From this approach, AF is seen as an advantageous resource that is obtained through the reputation of the business in front of its stakeholders, investors and financial institutions in particular. In the context of escalating competition and uncertainty in the business environment, AF is critical to a business’s ability to realize business opportunities. Therefore, it affects the long-term performance of the business. According to Abdisa and Hawitibo (Citation2021), financial availability and AF are strongly linked to firm performance. Empirical literature shows that the degree of impediment to AF for small businesses more challenging than that for larger businesses (Abdisa, Citation2018).

In terms of macroeconomics, businesses play a very important role in the national and regional economies. Specifically, it contributes to economic growth, job creation and poverty reduction. This role is increasingly enhanced in developing and developed countries (Fowowe, Citation2017). In fact, many businesses are willing to expand their business to find growth opportunities, however, the issue of AF is recognized as one of the biggest obstacles in the implementation of the development strategy (Fowowe, Citation2017). This financing gap is more severe for small businesses and in developing economies (Fowowe, Citation2017). According to Malhotra et al. (Citation2007), lack of finance is a huge obstacle to the development and growth of enterprises. Financial capital has a positive relationship with firm efficiency (Giang et al., Citation2019). On the other hand, access capacity to finance that allows certain advantages to firms in the relations to take market opportunity and transform it into business opportunity for firms. Building a network to enhance the possibility of accessing finance is considered as an important solution for firms that unable firms to utilize the business opportunities and make it possible to revenue for firms.

Based on these investigations, the hypothesis about the association between AF and FP can be assumed as below:

H4.

Access to finance positively affects FP.

2.6 BMI and Firm Performance (FP)

From the resource advantage theory perspective, BMI is seen as an advantageous resource of the enterprise that can benefit the business in terms of increasing competitive advantage. According to Khaddam et al. (Citation2021), BMI has a significant influence on the performances of the firm. In this regard, BMI provides productivity, return on sales, market value and financial performance for businesses (Gerdoçi et al., Citation2018). According to Bashir et al. (Citation2017), the efficiency ratio in terms of profitability brought by BMI is about four times against traditional innovation that is just based on a product or service. SMEs those implement BMI have higher performance than other businesses without BMI implementation (Carayannis et al., Citation2014; Futterer et al., Citation2018; Karimi & Walter, Citation2016; Kim & Min, Citation2015). In addition, to the venture business projects that implement BMI will provide competitive advantage and long-term survival in a dynamic market (Velu, Citation2015). According to Latifi et al. (Citation2021), BMI can improve business performance in a way that it can seize new market opportunities, improve efficiency, and enhance competitive advantage.

BMI involves the pursuit of new logic in the process of creating value and capturing value for stakeholders. This new logic focuses on exploring new ways that fit the business environment to generate revenue and define the value proposition for stakeholders such as customers, partners, suppliers. BMI is simply described as the change, adjustment in the components of the existing business model that associate with the resources, activities, customers, partners, distribution, and communication (Marolt et al., Citation2018). According to Visnjic et al. (Citation2016), BMI is approached through product-oriented innovation and customer-oriented innovation that benefit the business in a way that enhances their competitive advantage and distances their differentiation from other businesses. Therefore, BMI not only facilitates businesses conquer new customers, new markets, establish associations with them to gain first-mover advantages, but also helps companies to form the dynamic advantages that are not easy for the competitors to reproduce in a dynamic business situation. In this context, BMI was introduced as an enabler to help businesses achieve their goals and improve performance (Kranich & Wald, Citation2018).

Given the above discussion, the hypothesis about the impact of BMI on FP can be assumed as below:

H5.

BMI positively affects FP

2.7 Firm Performance (FP)

FP is considered to show the results of business operations (Fatoki, Citation2011), such as the enterprise fulfills its goals when selling products to the international markets (Navarro et al., Citation2010). Business results of enterprises are expressed in three specific areas includes (1) financial performance, which is expressed as profit, return on investment, return on asset and so on; (2) product market performance is manifested by sales, market share and shareholder return, expressed as total shareholder dividend and value-added dividend (Richard et al., Citation2009).

Business results can be accessed in several ways, such as (1) from a financial perspective that considers business results through overall profits, return on asset, profit margins and profitability and (2) non-financial perspective, which focus on measuring business performance through subjective perception of enterprises, business satisfaction (Ngatno et al., Citation2016; Zahra, Citation1993). Business results assessing way are normally dependent on the firm’s context and expectation of the researchers, who expect to see the firm’s status at what angle. This study measures the business results based on a financial approach such as sales growth, profitability, return on assets and return on investment.

This study approached systematic literature review. Table summarizes systematic literature review on the field of CSR and FP.

Table 1. Literature review on csr and fp

3. Conceptual model

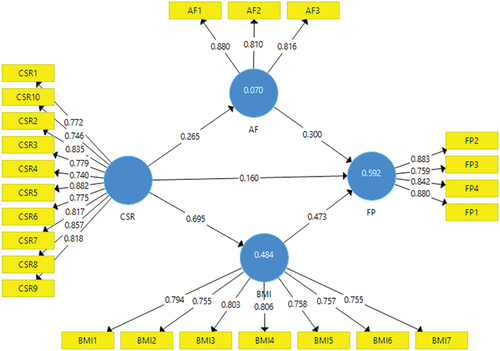

The conceptual study of the model based on literature review is provided in Figure . This model explores the association between corporate social responsibility (CSR) and firm performance (FP) with mediating characters of access to finance (AF) as well as business model innovation (BMI). This model includes FP and CSR as the dependent and independent variables as well as AF and BMI as the mediating variables.

Figure 1. Effects of CSR based on the firm performanace.

The construction of the variables of these investigations shows that FP has four types related to finance, CSR has ten economics-related items, society, law, and ethnics while AF has three items related to ability to access finance and BMI has seven items related to capacity of innovation of business model. The hypotheses of this model are proposed as follows.

4. Research design and methodology

This manuscript examines the association between FP and CSR, with mediating role of AF and BMI in this relation. To test the hypotheses, we targeted the experts, executives, and head of departments of firms for those who have been selected by the simple random method.

This study majorly adopted quantitative method. Subjects selected for this study are those SMEs perating in manufacturing sector from ten years above in the South of Vietnam. SMEs were defined on the basis of the employee numbers that an enterprise registered not more than 250 employees is recognized as an SME (IFC, Citation2009).

The structure of the questionnaire consists of three main parts. The first part is about the survey respondents’ demographics. The second part presents the opened questions for respondents’ perspectives that majorly include: (a) The situation of CSR understanding and practices by SMEs in Vietnam; (b) the reality of challenges that SMEs in Vietnam are facing in the framework of increasing competition because of global integration pressures and fast economic and social growth; (c) The importance of properly implementing CSR for the benefits of SMEs using the new Vietnam context; (d) Suggestion for SMEs to change for better. The third part covers closed questions, five-point Likert, from 1 to 5 means strongly disagree to agree. The survey was studied by ten experts in CSR, finance, and business with respect to the content clarity, readability, and comprehension of the questionnaire for the study.

Questionnaires were sent to respondents in two main ways: directly and via google drive, whichever is the best. We retrieved 385 questionnaires representing a 98.71% response rate for the analysis. All survey received will be checked to remove the incomplete survey that has a missing value. Finally, we retained 380, representing 97.44% of the response rate for the final study. The collected data was analyzed using Partial Least Square Structural Equation Model (PLS SEM).

5. Analysis and results

5.1 Sample characteristic

Table below presents the sample features in this work based on the population representative

Table 2. Sample characteristics

5.2 Assessing reliability of the scale

Hair et al. (Citation2010) defined that testing reliability as an assessment of the consistency degree between multiple measurements of a variable. This study evaluates the constancy of the whole domain along with the reliability of each productivity factor with the use of composite reliability indexes and Cronbach’s Alpha to bring all essential basis for the appropriate outcomes. These investigations indicate that the coefficient of Cronbach’s Alpha for all variables is not lesser than 0.7 precisely 0.755 of AF, 0.793 of FP, 0.88 of BMI and 0.91 of CSR. At this stage, it is possible to conclude that the reliability of scale is satisfied according to Cronbach’s Alpha index. However, the study extends further this work in order to present strongly affirm the scale consistency, hence composite consistency was applied for this persistence. These investigations indicate that the values of the compound consistency are not lesser than 0.7, especially 0.859 of AF, 0.866 of FP, 0.907 of BMI and 0.925 of CSR. Hair et al. (Citation2016) investigated the cumulative consistency that lies around 0.7 and 0.95, which shows the reliability of satisfactory level. Therefore, these results confirm the scale reliability perform good and satisfactorily. The comprehensive summary of these results is performed in Table . Furthermore, the indicator consistency was authenticated by measuring the outcomes based on the outer loadings. Table represents the outer loading outcomes that show each value is not lesser than 0.7. Based on these results, it is established that the reliability is performed in each individual indicator.

Table 3. Cronbach’s alpha and composite reliability results

Table 4. Results of outer loading

In addition, the indicator reliability was checked by assessing outer loadings’ results. Table shows the results of outer loading where all values are greater than 0.7. It means that all individual indicators are reliable.

5.3 Assessing validity

The way to measure the validity performances is proposed by Hair et al. (Citation2010). Moreover, its practicality assessed the collection of the data along with the reflection is also presented. Anderson et al. (Citation1988) concluded that the research perceptions validity include discriminant validity and convergent validity of the scales.

5.4 Convergent validity

Fornell and Larcker (Citation1981) indicated that the values of the convergence are applied to demonstrate the convergence of the items of measurement using their individual constructions. Hair et al. (Citation2010) proposed that the index of AVE should be equal or over to 50% and the factors of extraction can be more understandable than other combination of extraction. The factors of external loading and EVA results are provided in Table . This Table depicts that the values of the factors of external loading and EVA are not lesser than 0.7 and 0.5. These performances cross the mentioned level, which is called a satisfactory level of degree based on the validity of the convergence. This means a precise latent variable clarifies not less than variance in order to compare the consistent indicators (Hair et al., Citation2011). It is concluded that the observed variables are engrossed on the concepts of the research, which is involved in the supported convergent validity.

Table 5. Convergent validity

5.5 Discriminant validity

Fornell and Larcker (Citation1981) presented the distinction using the AVE square root of each construction of the research system is not lesser than all the correlation internal values based on the residual structures. Table shows the hidden structures that have been applied to distinguish from one another that leads to the satisfaction of the discriminatory test. In the next step of the research, individual valuation shows the independently assessing schemes based on the different scale concepts to prove that these perceptions are not interrelated. Table authenticates the discriminant analysis values, where the diagonal measures are the factor’s square root performances. The lower left values in the diagonal represent the partial correlation performance. These outcomes indicate that the values of the square root are the factor’s average is not lesser than the values of the partial correlation. Hence, the satisfactorily distinctiveness is concluded based on the research perceptions.

Table 6. Fornell and Larcker criteria

Heterotrait-Monotrait Ratlo (HTMT) represents a new standard to measure the discriminant rationality. Moreover, HTMT was calculated to indorse the discriminant soundness of the measurement system. Kline (Citation2011) indicated that HTMT is close to 1, which designate a deficiency of discriminant soundness and the values of the threshold can be 0.85. If this value is lesser than 0.85 then the discriminant validity is concluded of the research system is recognized. HTMT performances are not greater than 0.85 in this work to support the discriminant soundness. HTMT measures in this work are summarized in Table .

Table 7. HTMT (Heterotrait monotrait ratlo)

5.6 Evaluation of structural model

The first step taken placed was assessing Standardized Root Mean Square Residual (SRMR) value, which is considered as a report of model fit. It is an absolute portion of fit and is recognized as the standardized difference between the predicted correlation and observed correlation. According to Hu et al. (Citation1999), the model can be concluded as a good fit, if its SRMR value is less than 0.8. In this study, SRMR’s result of saturated model is 0.79 meaning that the model fit is supported. In addition, we took into consideration of the path coefficient analysis to assess the relationships of the variables in this research model. Figure represents that each path factor is taken as positive, which means that the relations of the research concepts are taken as positive. In conclusion, the hypotheses of the proposed research are recognized.

Figure 2. Result analysis of research model.

In addition, Table indicates the variable path coefficients of the research system. It designates that CSR has a positive effect on BMI at 0.695 as the path coefficient between AF and CSR is not greater then 0.265, while it is lowest at 0.160 between CSR and FP. In addition, the second strongest positive impact has been established for the relationship between BMI and FP at 0.473 while that between AF and FP is lower at 0.300. It implies that to enhance the performance of SMEs in Vietnam context, BMI is the most priority subject that need to be concerned and focused. According to the relationship of cause-effect, SMEs in Vietnam can be considered CSR as a strategic action that produces the values to government, the firms’ stakeholders, community, and society, meanwhile it improves the innovation of business model to stay proactive against competitors and attractive to customers.

Table 8. Path coefficients

The procedure is enhanced to check multicollinearities for all variables of the predictor latent by evaluating variance inflation factors (VIF). Collinearity is known as one of the conditions where highest correlation is performed in the independent variables. The divergence is performed in most of the literature based on the VIF relation as the threshold values for the collinearity (Cenfetelli & Bassellier, Citation2009; Kline, ; Petter et al., Citation2007). The suggested performances are 10, 5, and 3.3; that means a VIF equal/greater to the threshold measure to suggest the presence of collinearity in the multicollinearity or variables. Hair et al. (Citation2009) proposed a common VIF threshold value is around 10. This study performs that the VIF is below 10 and can be settled with non-multicollinearity problems in the variables of the research system. These VIF performances are summarized in Table .

Table 9. Variance Inflation Factors values (VIF)

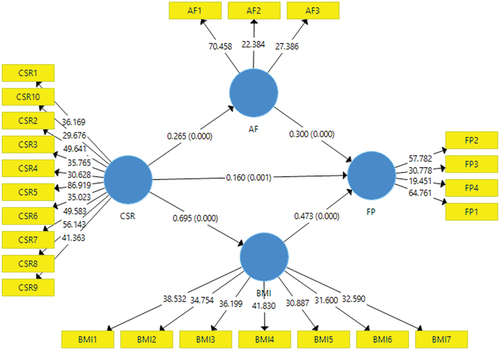

Moreover, the importance of the analysis of the path coefficient was directed using Bootstrap scheme with 5000 emulators. Bootstrapping allocates accuracy measures (prediction error, bias, confidence intervals, variance) to sample approximations” (Efron & Tibshirani, Citation1993). “This scheme is used to estimate the distribution of the samples around any statistic based on the random sampling schemes” (Varian, Citation2005). The bootstrapping outcomes indicate that the statistical performance P-value <5% and t > 1.96 that approve the propositions of this research system. Alternatively, these outcomes show the research system suitability using research statics, whereas the hypotheses acceptance indicates the practical results for FP. In brief, the positive effects of BMI on FP, AF on FP, CSR on FP, CSR on BMI, and CSR on AF are established in these investigations, given in Figure and Table .

Figure 3. Bootstrapping’s results.

Table 10. Bootstrapping’s results

6. Discussion and implications

6.1 Discussion

The analysis shown in Table indicates the research hypotheses are supported. Specifically, hypothesis 1 is accepted asserting that CSR has a vital and positive association with FP (β = 0.160, t = 3.266, p < 0.05). This finding to some extent supports previous literature of Javed et al. (Citation2020); Kong et al. (Citation2020); Islam et al. (Citation2021) those contended that CSR practices are beneficial to FP. In addition, this finding endorses the notion of Feng et al. (Citation2017); Martinez-Conesa et al. (Citation2017) by reinforcing the importance of business-stakeholder relationships for business success. This finding further supports the argument of Yáñez-Araque et al., (Citation2021) who argue that the viability of the business is no longer a matter of maximizing profits for the business but also creating value and benefits for stakeholders in a sustainable way, in today’s dynamic environment. However, this finding contrasts with previous literature of Crisóstomo et al. (Citation2011); Kao et al. (Citation2018) who argues that CSR practices negatively affect FP because it contributes to the burden of operating costs of businesses. Besides, Joseph et al. (Citation2018) signified that CSR have an impotent and positive effect on the financial performance of the firm, however, taking into further consideration by its key components, then only governance measures positively effect a firm’s financial routine, while social components and environmental components do not have any evidence for those relationships.

Besides, hypothesis 2 is supported confirming that CSR positively and significantly affects the enterprise’s AF (β = 0.265, t = 5.643, p < 0.001). These findings coincide previous literature of Taghian et al. (Citation2015); Zahari et al. (Citation2020); Ansong and Wanasika (Citation2017); Cheng et al. (Citation2014); Sharfman and Fernando (Citation2008) asserting that CSR leads to positive attitude of stakeholders towards the business, improves the business reputation in front of stakeholders, stimulates investment desire from outside investors and ultimately leads to high AF. Besides, this finding contrasts with the argument of Goss and Roberts (Citation2011); Richardson and Welker (Citation2001) who argue that CSR has no association with firm’s AF.

The result indicates that hypothesis 3 is accepted which confirms that CSR has a positive and significant association with BMI (β = 0.695, t = 27.554, p < 0.001). These concluding remarks support the preceding literature of Visnjic et al. (Citation2016); Halkos and Skouloudis (Citation2018); Dunbar et al. (Citation2016) asserting that socially responsible management practices towards internal and external stakeholders arouse the positive attitudes of stakeholders towards businesses, raise their awareness of the changes needed for value generation for stakeholders and the business. As a result, this facilitates the realization of BMI. In addition, this finding to some extent supports the revealment of previous studies of Sanchez-Hernandez et al. (Citation2019) who suggest that firm’s innovations must respond to the expectations of stakeholders. In addition, supporting the finding of Bacinello et al. (Citation2020) revealing that multi-dimensional CSR practices that address the interests of various stakeholders positively affect the firm’s innovation outcomes. This finding supports the exploration of Mendes et al. (Citation2021) who investigated that CSR has a vital and positive association with all kinds of corporate innovation.

In addition, hypothesis 4 is supported which affirms that AF positively and significantly affects FP (β = 0.300, t = 5.371, p < 0.001). This finding supports previous literature of Abdisa and Hawitibo (Citation2021); Fowowe (Citation2017); Malhotra et al. (Citation2007); Giang et al. (Citation2019) those contended that AF positively associate with FP according to the business opportunity approach. In this context, the lack of finance or difficulty in accessing finance affects the long-term performance of the business because it is not possible to realize the business opportunity in the new era. This means losing a competitive advantage in the marketplace when new business opportunities can be taken by competitors.

Hypothesis 5 is accepted which asserts that BMI has a crucial association with FP (β = 0.473, t = 9.551, p < 0.001). These outcomes support the previous investigations of Latifi et al. (Citation2021) who found that BMI has a direct and significant relationship with FP. Further, supporting previous literature of Khaddam et al. (Citation2021); Bashir et al. (2018); Kranich and Wald (Citation2018).; Gerdoçi et al. (Citation2018); Karimi and Walter (Citation2016); Futterer et al. (Citation2018) contending that BMI creates different benefits for the business in the way that establishes dynamic advantage driving innovation towards the product or the customer as the new logics to create value. In this regard, businesses create value by creating competitive advantages in the marketplace, improving operational efficiency, and ultimately leading to improved corporate performance.

6.2 Theoretical implications

This paper is of great contribution to existing literature in some respects. Firstly, it significantly broadens the literature by broadening the study of the role of CSR on FP, with finance access and business model innovation integrated as mediators in this relation. This is particularly significant for SMEs in the new given context as aforementioned in a developing economy of Vietnam. These outcomes indicate that SMEs therefore should perceive CSR a strategic long-term plan that involves all firms’ stakeholders’ interest towards sustainability. This work provides the supports of the theory of sustainability vision and stakeholders of Kantabutra (Citation2020) and Freeman (Citation1984). The finding implies that the proper practicing of CSR, the firm remains committed to its shareholders with appropriate qualifications, transparency in communication and operations, environment respect, and employee development, social welfare engagement. This in turn improves relationships between firm and its stakeholders, leading to an increase in their love, admiration, and trust for the firm those help access to finance and innovate business model more favorable. This will result in generating benefits for the firm to help and improve its performance based on the sustainable direction. These implications help to address the current situation of SMEs in Vietnam related to CSR awareness and CSR practices as aforementioned. While the new context of global integration increases competitive pressure, Vietnamese SMEs not only face competitive challenges with enterprises in Vietnam, but also with potential multinational enterprises those have strong financial capacity, attractive business model, strong market experience and a strong CSR awareness, CSR strategic plan and practices. Therefore, changing for the better is not an option but a must for SMEs to improve its competitiveness against rivals in the new settings.

The second contribution is for multidimensional measures of CSR that developed through the four CSR proportions discussed by Turker (Citation2009) based on the SMEs using the developing economy. However, the concept of CSR is popular and comprehensively provide the understanding with the concepts and its aspects that are still provocative. These outputs provide the solutions of the current problem based on SMEs in Vietnam related to the observations of CSR. Generally, SMEs narrowly consider CSR related to philanthropy instead of multidimensional investigations. Such inadequate awareness can lead to serious deficiencies in the company’s CSR strategic planning, which affect the benefits that should be obtained from CSR to improve firm performance.

This research may be essential to entrepreneurs, investors, shareholders, and policy makers towards sustainable progress for the SMEs and the Vietnamese economy in general.

6.3 Managerial implications

This research provides significant measures for CSR execution in organizations, especially SMEs in Vietnam’s developing economy. The first point of our outcomes is that CSR strategic planning must be at the heart of corporate strategy, whereby all actions and activities must be environmental-driven and social-driven, not geared toward short-term assistances. Indeed, SMEs in Vietnam exist traditionalist view of CSR. Accordingly, they conceive CSR as a cost driver that causes higher prices those reduce firm competitiveness and negative impact on firm performance in general. This study favors the revisionist view of CSR. Accordingly, CSR is conceived as a crucial driver for bringing values to business which help reduce cost, increase efficiency those increase firm competitiveness. Therefore, CSR must be perceived as investment-related issue, not cost-related issue.

Second, this study proposes that firms implement CSR on a voluntary and sustainable basis towards sustainable development goals. In today’s Vietnamese context, economic integration brings many opportunities and at the same time many challenges for the country and businesses, SMEs. In which, the biggest challenge is how to balance between economic development and environmental and social sustainability. In other words, economic growth without negative impacts on environment as committed in the Paris Agreement on climate change that requires specific and practical action plans from 2020. Accordingly, the role of business is very important to contribute to this commitment. Besides, the global consumers are increasing their awareness of environmental and social issues so they tend to be more sensitive in making consumption options. On the positive side, this is an opportunity for businesses those have long-term CSR strategic planning and sustainable CSR implementation on the voluntary basis.

7. Conclusion

The remarkable contributions of these investigations have been presented in the literature. The comprehensive perception of CSR for SMEs is presented in the new framework of a developing economy as Vietnam. The context is considered as most complex than ever as aforementioned. Secondly, this study contributes conceptual and empirical support with respect to the positive relationship between the firm and CSR performance using the mediating features of access to finance and business system innovation. The findings indicate that well performed CSR helps facilitate finance access and business model innovation those will result in improving firm performances. Importantly, this study proposes that SMEs should raise proper awareness of CSR because this will greatly influence the strategic planning of CSR in order to optimize the true value of CSR for businesses as aforementioned. Lastly, this work offers significant, theoretical, and managerial consequences that may have a high application value for SMEs in Vietnam.

8. Limitation and future studies

This study may exist some limitations that may offer opportunities for future studies. Firstly, the sample of this study focus on manufacturing firms which may not represent for other business sectors. Secondly, the data gained from businesses in the South of Vietnam, so it may not represent for businesses in other regions. Thirdly, this study used quantitative method so future studies many consider the mix method approach.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Quang Huan Ngo

Ngo Quang Huan is the dean of School of Management at University of Economics, Ho Chi Minh City, Vietnam. His major research areas are Corporate Social Responsibility, Corporate Governance and Finance related, Corporate Social Responsibility (CSR) related, Sustainability related. He has published the articles in the prestigious journals in ISI/SSCI and Scopus index. Email: [email protected]

Thanh Tiep Le

Thanh Tiep Le holds a Ph.D. degree in Business Administration. Currently he is also lecturer and researcher at Ho Chi Minh City University of Economics and Finance (UEF). Besides, he is a visiting lecturer at University of Economics, Ho Chi Minh City (UEH), Vietnam. His research interests include Corporate Social Responsibility (CSR), Corporate Governance, Circular Economy, Corporate Sustainability, Quality Management, Operation Management, and Supply Chain Management. He has published the articles in the prestigious journals in ISI/SSCI, ABDC rank A, B and Scopus index. Email: [email protected]

References

- Abdisa, L. T. (2018). Power outages, economic cost, and firm performance: Evidence from Ethiopia. Utilities Policy, 53, 111–23. https://doi.org/10.1016/j.jup.2018.06.009

- Abdisa, L. T., & Hawitibo, A. L. (2021). Firm performance under financial constraints: Evidence from sub-Saharan African countries. Journal of Innovation and Entrepreneurship, 10(1), 38. https://doi.org/10.1186/s13731-021-00177-1

- Agyemang, O. S., & Ansong, A. (2017). Corporate social responsibility and firm performance of Ghanaian SMEs. Journal of Global Responsibility, 8(1), 47–62. https://doi.org/10.1108/JGR-03-2016-0007

- Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: A review and recommended two-step approach. Psychological Bulletin, 103(3), 411–423. https://doi.org/10.1037/0033-2909.103.3.411

- Ansong, A., & Wanasika, I. (2017). Corporate social responsibility and firm performance of ghanaian SMEs: The role of stakeholder engagement. Cogent Business & Management, 4(1), 1333704. https://doi.org/10.1080/23311975.2017.1333704

- Asogwa, C. I., Ugwu, O. C., Okereke, G. K. O., Samuel, A., Igbinedion, A., Uzuagu, A. U., Abolarinwa, S. I., Ntim, C. G., & Ntim, C. G. (2020). Corporate social responsibility intensity: Shareholders’ value adding or destroying? Cogent Business & Management, 7(1), 1–28. https://doi.org/10.1080/23311975.2020.1826089

- Bacinello, E., Tontini, G., & Alberton, A. (2020). Influence of maturity on corporate social responsibility and sustainable innovation in business performance. Corporate Social Responsibility and Environmental Management, 27(2), 749–759. https://doi.org/10.1002/csr.1841

- Bahta, D., Yun, J., Islam, M. R., & Ashfaq, M. (2020). Corporate social responsibility, innovation capability and firm performance: Evidence from SME. Social Responsibility Journal, 17(6), 840–860. https://doi.org/10.1108/SRJ-12-2019-0401

- Bashir, M., & Verma, R. (2017). Why business model innovation is the new competitive advantage. IUP Journal of Business Strategy, 14(1), 7.

- Bastič, M., Mulej, M., & Zore, M. (2020). CSR and financial performance – linked by innovative activities. Naše gospodarstvo/Our Economy, 66(2), 1–14. https://doi.org/10.2478/ngoe-2020-0007

- Beck, T., Demirguc-Kunt, A., & Levine, R. (2005). Smes, growth, and poverty: Cross-country evidence. Journal of Economic Growth, 10(3), 199–229. https://doi.org/10.1007/s10887-005-3533-5

- Bhatia, A., & Makkar, B. (2020). CSR disclosure in developing and developed countries: A comparative study. Journal of Global Responsibility, 11(1), 1–26. https://doi.org/10.1108/JGR-04-2019-0043

- Blackburn, V., Doran, M., & Shrader, C. B. (1994). Investigating the dimensions of social responsibility investigating and the consequences for corporate financial performance. Journal of Managerial Issues, 6(2), 195–212. https://www.jstor.org/stable/40604020

- Carayannis, E. G., Grigoroudis, E., Sindakis, S., & Walter, C. (2014). Business model innovation as antecedent of sustainable enterprise excellence and resilience. Journal of the Knowledge Economy, 5(3), 440–463. https://doi.org/10.1007/s13132-014-0206-7

- Carroll, A. B. (1979). A three-dimensional conceptual model of corporate performance. The Academy of Management Review, 4(4), 497–505. https://doi.org/10.2307/257850

- Carroll, A. B. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 34(4), 39–48. https://doi.org/10.1016/0007-68139190005-G

- Casadesus-Masanell, R., & Ricart, J. E. (2010). From strategy to business models and onto tactics. Long Range Plan, 43(2), 195–215.

- Cenfetelli, R. T., & Bassellier, G. (2009). Interpretation of formative measurement in information systems research. MIS Quarterly, 33(4), 689–707. https://doi.org/10.2307/20650323

- Cheng, B., Ioannou, I., & Serafeim, G. (2014). Corporate social responsibility and access to finance. Strategic Management Journal, 35(1), 1–23. https://doi.org/10.1002/smj.2131

- Ciunova-Shuleska, A., Palamidovska-Sterjadovska, N., Osakwe, C. N., & Ajayi, J. O. (2017). The impact of customer retention orientation and brand orientation on customer loyalty and financial performance in SMEs: Empirical evidence from a balkan country *. Journal of East European Management Studies, 22(1), 83–104. https://doi.org/10.5771/0949-6181-2017-1-83

- Clauss, T. (2017). Measuring business model innovation: Conceptualization, scale development, and proof of performance. R&D Management, 47(3), 385–403. https://doi.org/10.1111/radm.12186

- Cornelius, N., Janjuha-Jivraj, S., Wallace, A., Woods, J., & Wallace, J. (2008). Corporate social responsibility and the social enterprise. Journal of Business Ethics, 81(2), 355–370. https://doi.org/10.1007/s10551-007-9500-7

- Crisóstomo, V. L., Freire, F. D. S., & Vasconcellos, F. C. D. (2011). Corporate social responsibility, firm value and financial performance in Brazil. Social Responsibility Journal, 7(2), 295–309. https://doi.org/10.1108/17471111111141549

- Das, M., Rangarajan, K., & Dutta, G. (2020). Corporate sustainability in SMEs: An Asian perspective. Journal of Asia Business Studies, 15(1), 109–138. https://doi.org/10.1108/JABS-10-2017-0176

- DiGiulio, Α., Migliavacca, Ρ. Ο., & Tencati, A. (2007). What relationship between corporate social performance and the cost of capital (working paper). Bocconi University.

- Dunbar, C. G., Li, Z., & Shi, Y. (2016). Corporate social responsibility and CEO risk-taking incentives. SRPN: Corporate Social Responsibility Issues (Topic). https://doi.org/10.2139/ssrn.2828267

- Efron, B., & Tibshirani, R. (1993). An introduction to the bootstrap. ( ISBN 0-412-04231-2). Chapman & Hall/CRC.

- Eyasu, A. M., Arefayne, D., Ntim, C. G., & Ntim, C. G. (2020). The effect of corporate social responsibility on banks’ competitive advantage: Evidence from Ethiopian lion international bank S.C. Cogent Business & Management, 7(1), 1–23. https://doi.org/10.1080/23311975.2020.1830473

- Famiyeh, S. (2017). Corporate social responsibility and firm’s performance: Empirical evidence. Social Responsibility Journal, 13(2), 390–406. https://doi.org/10.1108/SRJ-04-2016-0049

- Fatoki, O. O. (2011). The impact of human, social and financial capital on the performance of Small and Medium-Sized Enterprises (SMEs) in South Africa. Journal of Social Sciences, 29(3), 193–204. https://doi.org/10.1080/09718923.2011.11892970

- Feng, M., Wang, X., & Kreuze, J. G. (2017). Corporate social responsibility and firm financial performance. American Journal of Business, 32(3–4), 106–133. https://doi.org/10.1108/AJB-05-2016-0015

- Fernandez-Kranz, D., & Santalo, J. (2010). When necessity becomes a virtue: The effect of product market competition on corporate social responsibility. Journal of Economics and Management Strategy, 19(2), 453–487. https://doi.org/10.1111/j.1530-9134.2010.00258.x

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Fowowe, B. (2017). Access to finance and firm performance: Evidence from African countries. Review of Development Finance, 7(1), 6–17. https://doi.org/10.1016/j.rdf.2017.01.006

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Pitman.

- Freeman, R. E., Phillips, R., & Sisodia, R. (2020). Tensions in stakeholder theory. Business and Society, 59(2), 213–231. https://doi.org/10.1177/0007650318773750

- Futterer, F., Schmidt, J., & Heidenre-Ich, S. (2018). Effectuation or causation as the key to corporate venture success? Investigating effects of entrepreneurial behaviors on business model innovation and venture performance. Long Range Planning, 51(1), 64–81. https://doi.org/10.1016/j.lrp.2017.06.008

- Gerdoçi, B., Bortoluzzi, G., & Dibra, S. (2018). Business model design and firm performance: Evidence of interactive effects from a developing economy. European Journal of Innovation Management, 21(2), 315–333. https://doi.org/10.1108/EJIM-02-2017-0012

- Giang, M. H., Trung, B. H., Yoshida, Y., Xuan, T. D., & Que, M. T. (2019). The causal effect of access to finance on productivity of small and medium enterprises in vietnam. Sustainability, 11(19), 5451. https://doi.org/10.3390/su11195451

- Goss, A., & Roberts, G. S. (2011). The impact of corporate social responsibility on the cost of bank loans. Journal of Banking & Finance, 35(7), 1794–1810. https://doi.org/10.1016/j.jbankfin.2010.12.002

- Graves, S., & Waddock, S. A. (1994). Institutional owners and corporate social performance. Academy of Management Journal, 37(4), 1034–1046. https://doi.org/10.2307/256611

- Gunawan, S., Budiarsi, S. Y., Hartini, S., & Liu, G. (2020). Authenticity as a corporate social responsibility platform for building customer loyalty. Cogent Business & Management, 7(1), 1–18. https://doi.org/10.1080/23311975.2020.1775023

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2010). Multivariate data analysis (7th ed.). Prentice Hall.

- Hair, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2016). A primer on partial least squares structural equation modeling (PLS-SEM) (2nd ed.). Sage Publications.

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory & Practice, 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Halkos, G., & Skouloudis, A. (2018). Corporate social responsibility and innovative capacity: Intersection in a macro-level perspective. Journal of Cleaner Production, 182, 291–300. https://doi.org/10.1016/j.jclepro.2018.02.022

- Han, J. J., Kim, H. J., & Yu, J. (2016). Empirical study on relationship between corporate social responsibility and financial performance in Korea. Asian Journal of Sustainability and Social Responsibility, 1(1), 61–76. https://doi.org/10.1186/s41180-016-0002-3

- Hawn, O., & Ioannou, I. (2016). Mind the gap: The interplay between external and internal actions in the case of corporate social responsibility. Strategic Management Journal, 37(13), 2569–2588. https://doi.org/10.1002/smj.2464

- He, F., Miao, X., Wong, C. W., & Tang, Y. (2020). Corporate social responsibility and operating performance: The role of local character in emerging economies. Sustainability, 12(12), 4874. https://doi.org/10.3390/su12124874

- Hossain, M. (2021). The effect of the Covid-19 on sharing economy activities. Journal of Cleaner Production, 280, 124782.

- Huang, K., Sim, N., & Zhao, H. (2020). Corporate social responsibility, corporate financial performance and the confounding effects of economic fuctuations: A meta-analysis. International Review of Financial Analysis, 70, 101504. https://doi.org/10.1016/j.irfa.2020.101504

- Hu, L.T., & Bentler, P.M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: conventional criteria versus new alternatives. Structural Equation Modeling, 6(1), 1–55.

- Hunt, S. D., & Morgan, R. M. (1995). The comparative advantage theory of competition. Journal of Marketing, 59(2), 1. https://doi.org/10.1177/002224299505900201

- IFC (International Finance Corporation). (2009). The SME banking knowledge guide. The World Bank Group.

- Islam, T., Islam, R., Pitafi, A. H., Xiaobei, L., Rehmani, M., Irfan, M., & Mubarak, M. S. (2021). The impact of corporate social responsibility on customer loyalty: The mediating role of corporate reputation, customer satisfaction, and trust. Sustainable Production and Consumption, 25, 123–135. https://doi.org/10.1016/j.spc.2020.07.019

- Jain, R., & Winner, L. H. (2016). CSR and sustainability reporting practices of top companies in India. Corporate Communications: An International Journal, 21(1), 36–55. https://doi.org/10.1108/CCIJ-09-2014-0061

- Javed, M., Rashid, M. A., Hussain, G., & Ali, H. Y. (2020). The effects of corporate social responsibility on corporate reputation and firm financial performance: Moderating role of responsible leadership. Corporate Social Responsibility and Environmental Management, 27(3), 1395–1409. https://doi.org/10.1002/csr.1892

- JF, <. C. I. D. A., Jr., Black, W. C., Babin, B. J., & Anderson, R. E. (2009). Multivariate data analysis (7th edn ed.). Pearson Prentice Hall.

- Joseph, D. N., Ibrahim, M., & Sare, Y. A. (2018). Corporate social responsibility and financial performance nexus. Journal of Global Responsibility, 9(3), 301–328. https://doi.org/10.1108/JGR-01-2018-0004

- Julian, S. D., & Ofori-Dankwa, J. C. (2013). Financial resource availability and corporate social responsibility expenditures in a sub-saharan economy: The institutional difference hypothesis. Strategic Management Journal, 34(11), 1314–1330. https://doi.org/10.1002/smj.2070

- Kantabutra, S. (2020). Toward an organizational theory of sustainability vision. Sustainability, 12(3), 1125. https://doi.org/10.3390/su12031125

- Kao, E. H., Yeh, C.-C., Wang, L.-H., & Fung, H.-G. (2018). The relationship between CSR and performance: Evidence in China. Pacific-Basin Finance Journal, 51, 155–170. https://doi.org/10.1016/j.pacfin.2018.04.006

- Karimi, J., & Walter, Z. (2016). Corporate entrepreneurship, disruptive business model innovation adoption, and its performance: The case of the newspaper industry. Long Range Planning, 49(3), 342–360. https://doi.org/10.1016/j.lrp.2015.09.004

- Khaddam, A., Irtaimeh, H., Al-Batayneh, A., & Al-Batayneh, S. (2021). The effect of business model innovation on organization performance. Management Science Letters, 11(5), 1481–1488. https://doi.org/10.5267/j.msl.2020.12.026

- Kim, S. K., & Min, S. (2015). Business model innovation performance: When does adding a new business model benefit an incumbent? Strategic Entrepreneurship Journal, 9(1), 34–57. https://doi.org/10.1002/sej.1193

- Klassen, R. D., & Whybark, D. C. (1999). The impact of environmental technologies on manufacturing performance. Academy of Management Journal, 42(6), 599–615. https://doi.org/10.2307/256982

- Kline, R. B. (1998). Principles and Practice of Structural Equation Modeling (2nd ed. ed.). The Guilford Press.

- Kline, R. B. (2011). Principles and Practice of Structural Equation Modeling (3rd ed.). The Guilford Press.

- Kong, Y., Antwi-Adjei, A., & Bawuah, J. (2020). A systematic review of the business case for corporate social responsibility and firm performance. Corporate Social Responsibility and Environmental Management, 27(2), 444–454. https://doi.org/10.1002/csr.1838

- Kranich, P., & Wald, A. (2018). Does model consistency in business model innovation matter? A contingency‐based approach. Creativity and Innovation Management, 27(2), 209–220. https://doi.org/10.1111/caim.12247

- Latifi, M.-A., Nikou, S., & Bouwman, H. (2021). Business model innovation and firm performance: Exploring causal mechanisms in SMEs. Technovation, 107, 102274. https://doi.org/10.1016/j.technovation.2021.102274

- Lee, J. W. (2020). CSR impact on the firm market value: Evidence from tour and travel companies listed on the Chinese stock markets. Journal of Asian Finance Economics, and Business, 7(7), 159–167. https://doi.org/10.13106/jafeb.2020.vol7.no7.159

- Lee, K. H., & Min, B. (2015). Green R&D for eco-innovation and its impact on carbon emissions and firm performance. Journal of Cleaner Production, 108, 534–542. https://doi.org/10.1016/j.jclepro.2015.05.114

- Le, T. T., Ngo, Q. H., & Leonardo, A. S. (2021a). Contribution of corporate social responsibility on SMEs’ performance in an emerging market – the mediating roles of brand trust and brand loyalty. International Journal of Emerging Markets. https://doi.org/10.1108/IJOEM-12-2020-1516

- Le, T. T., Ngo, Q. H., Tran, T. T. H., & Tran, D. K. (2021b). The contribution of corporate social responsibility on SMEs performance in emerging country. Journal of Cleaner Production, 322, 129103. https://doi.org/10.1016/j.jclepro.2021.129103

- Lukács, E. (2005). The economic role of SMEs in world economy, especially in Europe, in. European Integration Studies, 4(1), 3–12.

- Mahmood, F., Qadeer, F., Sattar, U., Ariza-Montes, A., Saleem, M., & Aman, J. (2020). Corporate social responsibility and firms’ financial performance: A new insight. Sustainability, 12(10), 4211. https://doi.org/10.3390/su12104211

- Mahrani, M., & Soewarno, N. (2018). The effect of good corporate governance mechanism and corporate social responsibility on financial performance with earnings management as mediating variable. Asian Journal of Accounting Research, 3(1), 41–60. https://doi.org/10.1108/AJAR-06-2018-0008

- Malhotra, M., Chen, Y., Criscuolo, A., Fan, Q., Hamel, I. I., & Savchenko, Y. (2007). Expanding access to finance: Good practices and policies for micro, small and medium enterprises. WBI Learning Resource Series. World Bank. https://doi.org/10.1596/978-0-8213-7177-0

- Marolt, M., Lenart, G., Borstnar, M. K., Vidmar, D., & Pucihar, A. (2018). Smes perspective on business model innovation. 31th Bled eConference Digital Transformation – Meeting the Challenges June 17 - 20, 2018, Bled, Slovenia.

- Martinez-Conesa, I., Soto-Acosta, P., & Palacios-Manzano, M. (2017). Corporate social responsibility and its e?ect on innovation and ?rm performance: An empirical research in SMEs. Journal of Cleaner Production, 142, 2374–2383. https://doi.org/10.1016/j.jclepro.2016.11.038

- McWilliams, A., & Siegel, D. (2001). Corporate social responsibility: A theory of the firm perspective. The Academy of Management Review, 26(1), 117–127. https://doi.org/10.2307/259398

- Mendes, T., Braga, V., Correia, A., & Silva, C. (2021). Linking corporate social responsibility, cooperation and innovation: The triple bottom line perspective. Innovation & Management Review. https://doi.org/10.1108/INMR-03-2021-0039

- Mitchell, D., & Coles, C. (2003). The ultimate competitive advantage of continuing business model innovation. The Journal of Business Strategy, 24(5), 15–21. https://doi.org/10.1108/02756660310504924

- Navarro, A., Losada, F., Ruzo, E., & Díez, J. A. (2010). Implications of perceived competitive advantages, adaptation of marketing tactics and export commitment on export performance. Journal of World Business, 45(1), 49–58. https://doi.org/10.1016/j.jwb.2009.04.004

- Ngatno, N., Apriantni, E. P., & Widayanto. (2016). Human capital, entrepreneurial capital and SME’s performance of traditional herbal industries in central Java, Indonesia: The mediating effect for competitive advantage. Archives of Business Research, 3(4), 9–25. https://doi.org/10.14738/abr.44.2097

- Padilla-Lozano, C. P., & Collazzo, P. (2021). Corporate social responsibility, green innovation and competitiveness – causality in manufacturing. Competitiveness Review, 32(7), 21–39. https://doi.org/10.1108/CR-12-2020-0160

- Peloza, J. (2009). The challenge of measuring financial impacts from investments in corporate social performance. Journal of Management, 35(6), 1518–1541. https://doi.org/10.1177/0149206309335188

- Petter, S., Straub, D., & Rai, A. (2007). Specifying formative constructs in information systems research. MIS Quarterly, 31(4), 623–656. https://doi.org/10.2307/25148814

- Richard, P. J., Devinney, T. M., Yip, G. S., & Johnson, G. (2009). Measuring organizational performance: Towards methodological best practice. Journal of Management, 35(3), 718–804. https://doi.org/10.1177/0149206308330560

- Richardson, A. J., & Welker, M. (2001). Social disclosure, financial disclosure and the cost of equity capital. Accounting, Organizations & Society, 26(7–8), 597–616. https://doi.org/10.1016/S0361-3682(01)00025-3

- Sanchez-Hernandez, M. I., Gallardo-Vazquez, D., Dziwinski, P., & Barcik, A. (2019). Innovation through corporate social responsibility: Insights from Spain and Poland. In Corporate social responsibility: Concepts, methodologies, tools, and applications (pp. 1086–1102). IGI Global.

- Sardana, D., Gupta, N., Kumar, V., & Terziovski, M. (2020). CSR “sustainability” practices and firm performance in an emerging economy. Journal of Cleaner Production, 258, 120766. https://doi.org/10.1016/j.jclepro.2020.120766

- Sharfman, M. P., & Fernando, C. S. (2008). Environmental risk management and the cost of capital. Strategic Management Journal, 29(6), 569–592. https://doi.org/10.1002/smj.678

- Sharma, E. (2019). A review of corporate social responsibility in developed and developing nations. Corporate Social Responsibility and Environmental Management, 26(4), 712–720. https://doi.org/10.1002/csr.1739

- Shekar, M. C., & Kumaran, R. (2019). Impact of CSR on firms’ financial performance – a study of select indian IT companies. IPE Journal of Management, 9(1), 85–94. https://ssrn.com/abstract=3427685

- Singh, K., & Misra, M. (2021). The evolving path of CSR: Toward business and society relationship. Journal of Economic and Administrative Sciences, 38(2), 304–332. https://doi.org/10.1108/JEAS-04-2020-0052

- Soewarno, N., Tjahjadi, B., & Fitriyah, M. (2021). The role of corporate social responsibility on the relationship of competitive pressure and business performance of batik industry in central Java, Indonesia. The Journal of Asian Finance, Economics & Business, 8(1), 863–871. https://doi.org/10.13106/jafeb.2021.vol8.no1.863

- Soojeen, S. J., Ko, H., Chung, Y., & Woo, C. (2019). CSR, social ties and firm performance. Corporate Governance the International Journal of Business in Society, 19(6), 1310–1323. https://doi.org/10.1108/CG-02-2019-0068

- Stojanovic, A., Milosevic, I., Arsic, S., Urosevic, S., & Mihajlovic, I. (2020). Corporate social responsibility as a determinant of employee loyalty and business performance. Journal of Competitiveness, 12(2), 149–166. https://doi.org/10.7441/joc.2020.02.09

- Surroca, J., Tribo, J. A., & Waddock, S. (2010). Corporate responsibility and financial performance: The role of intangible resources. Strategic Management Journal, 31(5), 463–490. https://doi.org/10.1002/smj.820

- Taghian, M., D’Souza, C., & Polonsky, M. (2015). A stakeholder approach to corporate social responsibility, reputation and business performance. Social Responsibility Journal, 11(2), 340–363. https://doi.org/10.1108/SRJ-06-2012-0068

- Terziovski, M. (2010). Innovation practice and its performance implications in small and medium enterprises (SMEs) in the manufacturing sector: A resource-based view. Strategic Management Journal, 31(8), 892–902. https://doi.org/10.1002/smj.841

- Turker, D. (2009). How corporate social responsibility influences organizational commitment. Journal of Business Ethics, 89(2), 189–204. https://doi.org/10.1007/s10551-008-9993-8

- Vandenberg, P. (2006). Poverty reduction through small enterprises, in: Poverty reduction through small enterprises: Emerging consensus. Unresolved Issues & ILO Activities, 75, 1–59.

- Varian, H. (2005). Bootstrap tutorial. Mathematica Journal, 9, 768–775.

- Velte, P. (2021). Meta-analyses on Corporate Social Responsibility (CSR): A literature review. Management Review Quarterly, 72(3), 627–675. https://doi.org/10.1007/s11301-021-00211-2

- Velu, C. (2015). Business model innovation and third-party alliance on the survival of new firms. Technovation, 35, 1–11. https://doi.org/10.1016/j.technovation.2014.09.007

- Visnjic, I., Wiengarten, F., & Neely, A. (2016). Only the brave: Product innovation, service business model innovation, and their impact on performance. Journal of Product Innovation Management, 33(1), 36–52. https://doi.org/10.1111/jpim.12254

- Vives, A. (2006). Social and environmental responsibility in small and medium enterprises in Latin America. The Journal of Corporate Citizenship, 21(21), 39–50. https://doi.org/10.9774/GLEAF.4700.2006.sp.00006