Abstract

The objective of this study is to conduct a systematic review of the factors influencing the profitability performance of State-Owned Enterprises (SOEs). To achieve this objective, a qualitative method was employed, utilizing the Systematic Literature Review (SLR) approach to collect relevant data. A total of 328 published empirical articles were selected from the Scopus database and various journals, which served as the sample. This study presents an extensive examination of the literature on the trend of SOE profitability performance and its influencing factors. The obtained result showed that there was a notable increase in the number of articles published on this topic, particularly after 2015, with the highest number of publications occurring in 2022. It is important to note that the majority of these articles were predominantly published in China which aligned with the significant presence of SOE in the country. Most of the analyzed papers utilized quantitative methods and employed panel regression as the statistical tool for their data analysis. Furthermore, it was observed that corporate governance emerged as the most commonly studied independent variable in these articles. This study also offers insight into areas that warrants further investigation in terms of what has been examined and what is yet to be. Lastly, the study contributes to determining the overview of the state of the art of SOE performance and provides a knowledge gap for further analysis.

1. Introduction

State-Owned Enterprises (SOEs) play a significant role in numerous economies, serving as key drivers of economic growth, employment, and industrial development. In the last 20 years, the assets of the top 2000 global firms that are state-owned have increased twofold, reaching 20% of their total assets. Additionally, these assets account for approximately half of the Gross Domestic Product (GDP) worldwide (International Monetary Fund, Citation2020). Given these significant contributions, understanding and analyzing the performance of SEOs is of utmost importance for policymakers, stakeholders, and investigators. Therefore, this study specifically focused on exploring the profitability of SOEs, which serves as a critical indicator of their viability and ability to generate returns for shareholders while contributing to the overall economy.

In recent years, there has been an increasing interest among investigators to examine the performance of SOEs. The previous studies have employed a diverse range of variables, methodologies, and samples from multiple countries to observe and analyze the profitability performance of SOEs and provide predictions regarding their future outcomes. However, there is still a lack of comprehensive understanding regarding the extent of research conducted in this area and the remaining gaps that need to be addressed. To address this gap, the present study adopted a review research approach through the utilization of the Systematic Literature Review (SLR) methodology. Several tools were utilized to gather the necessary information from the chosen articles and conduct the data analysis. The SLR approach allows for a rigorous and structured examination of existing literature on a specific topic, facilitating the identification of research gaps, synthesis of key findings, and formulation of evidence-based recommendations. Numerous studies have utilized SLR to explore aspects related to SOEs or public sector organizations, such as Gakhar and Phukon (Citation2018) who examined the influencing factors of privatization, Ahunov (Citation2023) & Manes-Rossi et al. (Citation2020) that focused on non-financial reporting, and Grossi et al. (Citation2015) & Miążek (Citation2021) who investigated corporate governance. However, none of the aforementioned studies ventured beyond their respective areas of focus to identify the factors as comprehensively as this current study.

The primary objective of this study is to conduct a systematic review of the works of literature on the topic of SOE profitability performance. The following are the research objectives: (1) to determine the trends observed in empirical studies related to SOE profitability and (2) to determine the associated proxies of dependent and independent variables. Through this review, the research aims to contribute to the existing works of literature by expanding the body of knowledge and mapping the current state of the art in terms of SOE performance. Moreover, the findings of this study will have significant implications for both practitioners and investigators. Practitioners in this field can gain valuable insight into the factors that influence the profitability of SOE, while investigators will be able to identify avenues for further exploration of related topics. This study is organized as follows: Section 2 provides an introduction to the literature review, outlining the key themes and concepts related to SOE profitability. Section 3 details the methodology employed in conducting the systematic review. Section 4 presents the result of the study. Finally, section 5 presents the conclusion and highlights potential aspects for further study.

2. Literature review

This study focuses specifically on the topic of SOE profitability, which is a crucial aspect of organizational performance. Organizational or firm performance is a multidimensional concept that reflects the overall results of an organization in relation to its objectives. In the context of research, literature often uses the term “performance” is often used as a general umbrella term that encompasses various dimensions and aspects of organizational performance. This fact can sometimes lead to potential biases when attempting to build a comprehensive understanding of a specific topic in the field. Accordingly, previous studies have examined various dimensions of SOE performance, including production & efficiency (Boardman et al., Citation2016; Burki & Niazi, Citation2010; Y. Gao et al., Citation2021; Hong Nham et al., Citation2021; Le et al., Citation2019; Modén et al., Citation2008; Motohashi, Citation2008; H. Q. Nguyen, Citation2021; Y. Wu & Zhou, Citation2013; J. Yu & Nijkamp, Citation2008), sustainability (S. Chen et al., Citation2022; Guo et al., Citation2023; K.-C. Ho et al., Citation2022; Z.; W. Li et al., Citation2022; Pang et al., Citation2022; Pei & Pei, Citation2023; Y. Ren et al., Citation2023; Rong et al., Citation2022; H. Sun & Liu, Citation2023; W. Wu et al., Citation2022), and innovation (Boxu et al., Citation2022; Castelnovo, Citation2022; X. Gao & Zhang, Citation2023; Han & Gu, Citation2021; X. Jia et al., Citation2022; X.; Z. Citation2022Li & Zhao Citation2022; P. Yu & Hu, Citation2022; Yue, Citation2022; J. Zhang et al., Citation2022; S. Zhang et al., Citation2022).

This current study focuses exclusively on the financial performance of SOEs and examined more specifically the studies where profitability was considered as the variable. The profitability in this regard is based on a measure of the firm capability to generate profit and create value for stakeholders. Various measures have been used to gauge profitability, which may be interchangeably related to terms and indicators. For example, some authors used net profit to total assets, while others employ Earnings Before Interest Tax Depreciation Amortization (EBITDA) to total assets as indicators of profitability. Accordingly, to simplify analysis and identify patterns in evaluating the profitability performance of SOEs, hence research extracts and categorizes the diverse measures into separate groups. The following are examples of profitability instruments used in previous studies, they include Return on Asset (ROA) (Jin, Citation2023), Return on Equity (ROE) (Tang et al., Citation2021), Return on Investment (ROI) (Ngo et al., Citation2008), Tobin’s q value (Shen et al., Citation2021), earning per share (Loc et al., Citation2006), operating income (Luong et al., Citation2019), gross profit margin (Mbo & Adjasi, Citation2017), real profit (D. Li et al., Citation2007) and profit/employee (Sidki et al., Citation2023).

Previous study has extensively explored various factors that can influence the profitability performance of SOEs, as it is a crucial objective for every firm. The prior authors have conducted observations using a wide range of variables, diverse methods, as well as different samples and locations to facilitate the analysis and prediction of future SOE performance. However, no existing literature has synthesized the determinants of SOE profitability performance. Overall, this study aims to shed light on the factors identified by prior studies that impact the profitability performance of SOEs.

3. Methodology

This study employed a qualitative method, utilizing the Systematic Literature Review (SLR) approach. Unlike the quantitative method that typically follows a deductive paradigm by testing theories or hypotheses about a specific topic, the qualitative method operates in the opposite direction (Sekaran & Bougie, Citation2016). Furthermore, the study is considered qualitative when it relies primarily on qualitative tools such as descriptive statistics rather than employing advanced statistical or mathematical techniques (Strijker et al., Citation2020). The present study falls under the qualitative category as it involves reviewing published research and conducting descriptive analyses of the topic.

SLR focuses on systematically reviewing and evaluating that are relevant to the topic of the study. This approach is categorized as an investigative science aimed at enhancing the quality of reviews (Tranfield et al., Citation2003). It is an appropriate approach for identifying areas where either enough or little evidence exists (Petticrew et al., Citation2006). SLR is an important step in designing new intervention and evaluation, promoting the development of new methodologies, and guiding future research efforts. The purpose of systematic review is to identify all relevant empirical evidence that meets predetermined criteria in order to address a specific research question or hypothesis (Snyder, Citation2019). Systematic reviews are particularly valuable when there is uncertainty surrounding an issue, as they enable a comprehensive examination of all relevant articles. SLR involves synthesizing and comparing evidence, employing a systematic approach to address specific research questions, evaluating quantitative articles, and making significant contributions to informing policy and practice. The influence of systematic reviews has rapidly increased as users recognize their ability to tackle the vast amount of research information by distilling it into a manageable format (Petticrew et al., Citation2006).

To minimize bias, SLR employs a study protocol that delineates the pertinent plan for the given topic (Tranfield et al., Citation2003). The study adhered the protocols outlined in Tranfield et al. (Citation2003) and Kitchenham (Citation2004) which are widely adopted by several authors of SLRs, including Almaqtari et al. (Citation2020), T. H. H. Nguyen et al. (Citation2020), Hazaea et al. (Citation2021), and Mauludina et al. (Citation2023). In this study, the Scopus database was chosen due to its broad coverage across various disciplines and the presence of high-quality articles it contains. To initiate the SLR protocol, it is essential to identify its objective, as they serve as a crucial foundation for the entire process (Tranfield et al., Citation2003). Then, two research questions were formulated to advance the current understanding of the profitability performance of SOEs, which are as follows:

RQ1:

What are the publishing outlets, publications by years, and research methods that prior empirical studies have used to discuss the profitability performance of SOEs?

RQ2:

What are the determinants of the profitability performance of SOEs that have been addressed by prior empirical studies?

3.1. Article identification

3.1.1. Keyword and term identification

This stage involves the identification of keywords and terms to facilitate the extraction of relevant information. Several keywords were used to search articles related to the performance of State-Owned Enterprises (SOEs). The chosen keywords, “State Owned Enterprise” and “Performance”, were selected for their widespread usage and recognition among international organizations and scholars in the field (Grossi et al., Citation2015). By employing these general keywords, the objective was to encompass a broader scope of articles, leading to a substantial volume of studies about SOEs and firm performance. Accordingly, this process of keyword identification serves as a bridge to the subsequent stage, where the articles are identified, extracted, analyzed, and synthesized. It is also important to note that the key terms used in this study were solely focused on until the related articles were located.

3.2. Boolean search

Boolean search operators play a crucial role in aiding the extraction of articles relevant to research questions. These operators, such as AND, OR, publication date, material type, and language, were employed to streamline the search process effectively. In this study, the Boolean operator AND was used to connect different concepts and narrow down the search. Furthermore, the study specifically focused on research and review article material types, excluding unrelated documents from consideration. The article identification process was conducted without the imposition of any restrictions based on the research area, aspect, or publication year.

3.3. Quality assessment – inclusion and exclusion

During this stage, the quality assessment of the sampled articles for the current study is conducted. Several criteria of inclusion and exclusion were applied to select the relevant and high-quality articles, they include:

Relevant published empirical studies pertaining to the research question were incorporated.

Studies that explicitly addressed the profitability performance of state-owned enterprises (SOEs) and its determining factors were included.

Studies that are duplicate, non-English, non-research-based, not available in full-text, and not related to research question were excluded.

Proceedings, books, discussion outcomes, reports, and theses were not considered for inclusion in the study.

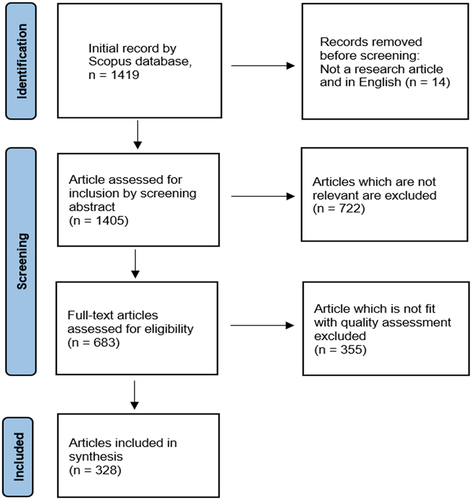

The initial query search on the Scopus database resulted in 1419 records when the keywords were electronically inputted. Notably, some of the obtained articles that did not meet the selection criteria and quality assessment, resulting in their exclusion. Furthermore, 14 papers that were not research-based and not in English were removed before the screening, leaving a total of 1405 articles for assessment. To ensure alignment with the research theme, the articles underwent a comprehensive review process that involved screening based on abstracts and full-text analysis. The first screening phase excluded 722 articles because they were irrelevant to the research questions. This was followed by a further screening of the remaining 683 articles, which ultimately led to the synthesis of the final set of 328 articles. The research selection process, including article identification, abstract and full-text screening, and finalization of samples, was visually presented using the PRISMA flow diagram (Figure ).

Figure 1. PRISMA flow diagram of Article Identification.

3.4. Data extraction and synthesis

In this stage, the samples of articles were carefully chosen and finalized. Several tools were utilized to extract the necessary information from the selected articles. Content analysis, Microsoft Excel, and manual extraction techniques were employed to gather the required data for the present study. Additionally, the retrieved articles underwent a descriptive analysis and were categorically examined using an in-depth interpretive approach in order to address the research questions. The subsequent section will present the results and discussion derived from the analyzed studies.

4. Discussion and results

4.1. Publishers’ outlets and citations

This subsection summarizes the retrieved articles based on their respective journals, publishers, and citations sourced from the Scopus database. Table shows that the published articles were dominated by Elsevier, Taylor & Francis, Wiley, Emerald & MDPI, and Springer which contains 91, 36, 33, 30, and 23 citations indicating 28%, 11%, 10%, 9%, and 7%, respectively. In terms of citation count, the 328 articles received a total of 8432 citations. It is worth noting that Elsevier emerged as the top contributor with 4563 citations, accounting for 54% of the overall total. Wiley, Springer, Emerald, Taylor & Francis, and MDPI follow with 1618, 608, 379, 358, and 288 citations, respectively. This distribution represents 19%, 7%, 4.5%, 4.2%, and 3% of the total citations. The dominance of these publishers in the published articles and citations signifies their significant role in shaping and advancing the discourse surrounding the profitability performance of State-Owned Enterprises (SOEs). Researchers and scholars are likely to rely heavily on publications from these reputable publishers to gain insights and contribute to the existing knowledge in this field.

Table 1. Publishers’ Outlets and Citations

These findings suggest that Elsevier is the most influential publisher in terms of citations within the scholarly discussions related to the topic. This conclusion is further supported by the fact that six out of the ten most cited articles in this area were published by Elsevier, as identified in the study by Q. Sun and Tong (Citation2003) (594 citations), W. Wu et al. (Citation2012) (302 citations), D. Zhang et al. (Citation2019) (223 citations), D. Qi et al. (Citation2000) (221 citations), Liao et al. (Citation2014) (208 citations), and Zhu et al. (Citation2016) (139 citations). Moreover, the total citations of these studies represent 20% of the total citations of articles.

It is logical to note that some research articles published in earlier years may have accumulated higher numbers of citations compared to more recent articles. The most cited study, Q. Sun and Tong (Citation2003) (594 citations), followed by Gupta (Citation2005) (335 citations) discussed the privatization issue in China and India. Both studies found that privatization is an effective way to improve the performance of SOEs. The third most cited study, W. Wu et al. (Citation2012), investigated the political connection on the performance of private firms and SOEs in China. They discovered that SOEs with politically connected managers underperform those without such managers. These mentioned studies represent early studies and serve as significant sources for more recent articles in this field.

provides a breakdown of the distribution of papers among the top 20 journals. The majority of the studies were published in renowned journals such as Sustainability (MDPI), Pacific Basin Finance Journal (Elsevier), World Development (Elsevier), China Economic Review (Elsevier), Asia Pacific Journal of Management (Springer), and Economics of Transition (Wiley). Specifically, these journals featured 26, 8, 6, 5, 5, and 5 studies, respectively. It is worth noting that this distribution of studies aligns with the dominant publisher mentioned in the previous table.

Table 2. Top 20 Journals by Number of Papers

4.2. Publication by year and country

With regards to publication by year, Figure represents the publication trend of articles from 1993 to 2023. Overall, the number of studies on SOEs and firm performance has varied but generally shown an upward trend. Prior to 2008, the annual publication count remained below 10 articles. Moreover, there has been a significant and rapid increase in the examination of SOE profitability performance since 2015 (representing more than 60% of all studies). This could be indicative of a growing interest among researchers in exploring the factors that impact the profitability performance of SOEs. It is also important to note that the highest number of articles were published in 2022, followed by 2021, 2020, 2019, and 2017 with values of 42, 36, 35, 26, and 17, respectively. These years accounted for 13%, 11%, 10,7%, 8%, and 4% of the total articles, respectively.

Figure 2. Publication by Year.

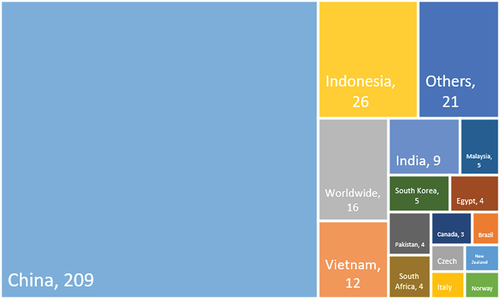

The articles were categorized based on their geographical focus and this information is presented in Figure . Most of studies were conducted in developing countries based on The World Economic Outlook Report issued in 2023 (International Monetary Fund, Citation2023), amounting to 87% of the articles. The distribution of these articles was primarily focused on the Emerging and Developing Asia Region, with 261 articles, followed by the Middle East and Central Asia, which accounted for 9 articles. The analysis revealed that the highest number of published articles originated from China, followed by Indonesia, worldwide (cross-country), Vietnam, and India, with respective counts of 209, 26, 16, 12, and 9 papers, representing 64%, 8%, 5%, 4%, and 3% of the total articles, respectively. Additionally, the “Others” category encompasses countries with only one published paper each. This distribution aligns with the prevalence of SOEs in those countries, indicating a correlation between the dominant research areas and the abundance of SOEs.

Figure 3. Publication by Country.

4.3. Research method and type of industry sample

Figure provides an overview of the research methods and approaches employed in the analyzed studies. In this regard, the study is categorized as quantitative if it employs deductive reasoning, which involves examining hypotheses or theories (Sekaran & Bougie, Citation2016). Quantitative studies typically emphasize the use of advanced mathematical and statistical approaches, rather than relying primarily on descriptive analysis as seen in qualitative studies. The majority of the studies, accounting for 95% of the articles, employed quantitative methods. Among these quantitative studies, the dominant approaches include panel regression, multiple regression, and other types of analysis, with 185, 71, and 21 articles indicating 60%, 23%, and 7%, respectively. In contrast, the qualitative side of study was less prevalent, comprising only 18 articles indicating 5% of the total, all of which utilized a case study approach. The prevalence of panel regression in previous studies indicates a focus on conducting comprehensive explorations of SOEs by incorporating diverse sets of variables and larger volumes of data.

Figure 4. Research Method and Approaches.

Figure provides an overview of the industry types mentioned in the published articles. The majority of articles focused on the general manufacturing industry, with 25 papers accounting for 8% of the total articles. This was followed by heavy polluted, bank, utility & vehicle, as well as energy & telecommunication, which had 11, 5, 4, and 3 papers accounting for 3%, 2%, 1.2%, and 0.9% of the total articles, respectively. Following this, various other industries were covered in the remaining articles, each with less than three publications. The inclusion of the manufacturing and heavily polluted industries, which are broad terms encompassing multiple firms, suggests that prior studies aimed to generalize their findings across different companies in these sectors.

Figure 5. Type of Industry Sample.

4.4. Factors affecting firm performance

This section provides an answer to the second research question outlined for the study, which focuses on the determinant variables of the profitability performance of SOEs, as addressed in prior studies. This section will explore profitability performance as the dependent variable and a variety of independent variables in the context of SOE extracted from previous works of literature.

4.4.1. Variables of SOE’s profitability performance

The literature revealed that previous studies have used various terms to describe profitability in the context of SEOs. In this study, the 328 sample articles were categorized into seven groups of profitability terms, as presented in Table . The results showed that the majority of profitability variables used in previous studies were related to return and asset ratio, with 180 articles focusing on this category. The common term mentioned in these works of literature is Return on Asset (ROA). However, it is important to note that the specific indicators and terms used for return may vary among the studies. For instance, some authors have used net profit (Alipour, Citation2013; Lam et al., Citation2013; W. Wu et al., Citation2012; D.-X. Yang et al., Citation2022), core profit (T. Ren et al., Citation2019), core income (X. Zhang et al., Citation2012), and revenue (G. Chen et al., Citation2006; Tsamenyi et al., Citation2010; Xue et al., Citation2022) as indicators of profitability. Others have employed Earnings Before Interest and Tax (EBIT) (Jin, Citation2023), Earnings Before Interest, Tax, Depreciation, and Amortization (EBITDA) (Lazzarini et al., Citation2015), Income Before Tax (IBTA) (Loc et al., Citation2006), and Operating Income Before Depreciation (OIBD) (Y.-R. Chen et al., Citation2020). The second highest number of articles, totaling 76, pertains to return and equity ratio, with Return on Equity (ROE) being the common term used in this category. Similar to the previous category, the terms and indicators used for return and equity ratios can vary among articles. For example, G. Chen et al. (Citation2008) used profit, Chan et al. (Citation2018) & Yang et al. (Citation2022) employed net profit, Menozzi et al. (Citation2012) & Ng et al. (Citation2009) used net income, J. L. Y. Ho et al. (Citation2011) made use of operating income, and Loc et al. (Citation2006) used IBTA.

Table 3. Variables of SOE’s Profitability Performance

In previous studies, the third highest focus, consisting of 71 papers, revolve around profitability associated with sales or the sales ratio. This category differs from the previous two categories as it solely examines the revenue and loss statement of a company, specifically emphasizing the use of sales terms or the relationship between sales and other accounts in the statement. The terms and indicators used within this category include sales (Arif et al., Citation2022; Putra et al., Citation2020; She et al., Citation2021; K. Wang et al., Citation2019), Return on Sales (ROS) (Inoue, Citation2020; Laporšek et al., Citation2021; Parida & Madheswaran, Citation2021), the proportion of sales (e.g. export sales to total sales) (Sharma et al., Citation2020; Singh et al., Citation2023), sales to cost (Y. Zhou et al., Citation2022), EBIT/sales (Chi et al., Citation2014; Q. Sun & Tong, Citation2003; A. Zhang et al., Citation2002), IBTA/sales (Loc et al., Citation2006), real sales (sales divided by Customer Price Index (CPI)) (L. Chen et al., Citation2007; Chi et al., Citation2014; Loc et al., Citation2006; X. Zhang et al., Citation2012).

The fourth-highest group of articles focused on the profitability of SOEs in relation to Stock or Share Ratios. The articles included in this category focused on exploring the SOEs listed in the stock market. The most terms or indicators used were Tobin’s Q Value (market value of equity and debt to total asset), which appeared in 56 papers, followed by abnormal return, earning per share, stock price or return, Price to Book (P/B) ratio, and IPO return, with 21, 9, 6, 4, and 1 papers, respectively. The aforementioned variables in this category have been used by various articles, including Tobin’s Q Value (W. Li et al., Citation2022; Y. Qi et al., Citation2022; Tang et al., Citation2022; M. Zhang et al., Citation2023), abnormal return (Brahma et al., Citation2023; Du et al., Citation2021; Yi et al., Citation2021; Zeng et al., Citation2022), earning per share (J. Chen et al., Citation2020; Deng & Cheng, Citation2019; Zheng & He, Citation2022), stock price or return (Santoso et al., Citation2019; D. Wang & Chong, Citation2017), Price to Book (P/B) ratio (Rossieta, Citation2017; T. Wang et al., Citation2014), and IPO return (T. Wang et al., Citation2018).

The next category of articles focused on profitability related to revenue or profit. These articles examined items from profit and loss statements either solely or compared to other accounts as a ratio. For example, net profit (Hai et al., Citation2022; Ma et al., Citation2022), operating revenue (Liao et al., Citation2014), profit (Putra et al., Citation2020), income (Luong et al., Citation2019), EBIT (J. Xu & Li, Citation2022), EBITDA (Munyo & Regent, Citation2016), net profit margin (Y. Zhou et al., Citation2022), operating profit margin (Inoue, Citation2020), price cost margin (Srivastava & Kathuria, Citation2020), gross profit margin (Mbo & Adjasi, Citation2017), net interest margin (Otchere & Chan, Citation2003) and real profit (D. Li et al., Citation2007) or real EBIT (Chi et al., Citation2014).

The last two groups of profitability performance were related to return and investment ratio, as well as return and employee ratio, with 19 and 16 papers, respectively. These categories used specific relationships to measure the effectiveness and efficiency of investment and employee expenditure. The indicators used include Return on Investment (ROI) (Arif et al., Citation2022; Sarfraz et al., Citation2022; Wardhani & Supratiwi, Citation2023), Return on Invested Capital (ROIC) (Bhatt, Citation2016; S. Xu & Guo, Citation2021; Y. Zhou et al., Citation2022), Return on Capital Employed (ROCE) (Chakrabarti & Ray, Citation2018) for the first category. Those three indicators are relatively similar in meaning and were sometimes used interchangeably. Meanwhile, in the return and employee ratio category, several indicators were utilized including profit/employee (Sidki et al., Citation2023; D. Xu et al., Citation2006) or net Income/employee (Bai et al., Citation2009; G. Chen et al., Citation2008), and sales/employee (Kuzman et al., Citation2018; Michelotti et al., Citation2017).

4.4.2. Determinant variables of SOE’s profitability performance

The performance of State-Owned Enterprises (SOEs)) is a relative concept and can be influenced by a range of factors (Gakhar & Phukon, Citation2018). This study aims to categorize and examine these factors based on prior research, as shown in . Accordingly, the main explanatory variables (independent/moderating/mediating) were extracted as proxies from the literature, while control variables were eluded. The variables were grouped into seven categories. They include corporate governance; firm characteristics; strategy, capability & internal environment; external environment; government & policy; innovation & technology; and human resources. With regards to the number of articles, variables related to corporate governance were dominant with a value of 303 articles, accounting for 92% of the total, followed by firm characteristic and strategy, capability & internal environment which have 114 and 97 papers, representing 35% and 29% of the total articles, respectively. However, the results were not aligned in terms of the number of detailed variables. The category with the highest number of variables was related to strategy, capability, & internal environment (53) and followed by corporate governance (47). These findings indicate that the majority of authors share common concerns regarding corporate governance, firm characteristics, as well as innovation & technology considering the ratio of the number of articles to the number of detailed variables.

Table 4. Proxies of Explanatory Variables

Table provides a detailed overview of variables, the number of articles, and recent literature samples for each respective group. The first category focuses on various corporate governance issues, including ownership structure, board matters, committee issues, and disclosures. The obtained results revealed that ownership/privatization was the most frequent studies attribute within corporate governance, with 120 papers addressing the topic. Additionally, board political connection, board size, and board independence were discussed in 24, 16, and 15 papers, respectively. These results are consistent with the nature of SOEs, which are characterized by state or national ownership. The literature further explores types of ownership, including state ownership or privatization (H. Li et al., Citation2023; Markin et al., Citation2022; F. Xie & Yang, Citation2023; X. Xie et al., Citation2022), ownership concentration (Ang et al., Citation2022; Boateng et al., Citation2017; H. Jiang & Zhang, Citation2018; B. Zhou et al., Citation2019), and foreign ownership (F. Jiang et al., Citation2013; Ye et al., Citation2021). The second most prevalent attribute was also related to state ownership, as political connections naturally arise when discussing the involvement of the state.

Table 5. Detailed Proxies of Explanatory Variables

In terms of firm characteristics, the variables observed in this category were often frequently used to moderate, mediate or control other explanatory variables. They help in understanding and analyzing various dynamics and behaviors of the firm. Furthermore, these variables were designed to represent the unique characteristics of the firm and were often represented as dummy variables with values of 0 or 1. Among the variables in this group, firm size is the most commonly used, appearing in 22 papers. It is followed by leverage, industry, listing, and location with values of 20, 13, 9, and 7, respectively. The firm size was used to measure the magnitude of a firm. This measurement was carried out using several constructs such as total assets (Amin & Haq, Citation2022; Apriyantopo et al., Citation2022; Marimuthu, Citation2021), total revenue/sales (G. Chen et al., Citation2008; Goldeng et al., Citation2008; Ng et al., Citation2009), total employment (Bai et al., Citation2009; Crowley et al., Citation2019; Ngwenya & Khumalo, Citation2012), and total transaction (Comstock et al., Citation2003). Following this, leverage was used to assess the financial condition of the firm and analyze the extent to which it relies on debt to operate. Several authors have employed different measures to construct leverage, such as debt-to-assets ratio (Amin & Haq, Citation2022; Ding et al., Citation2022; Marimuthu, Citation2021; Qiao et al., Citation2021; H. Zhang & Aumeboonsuke, Citation2022) and debt-to-equity ratio (G. Chen et al., Citation2008; Hermansjah et al., Citation2021; J. Jia et al., Citation2005; Khaq, Citation2020).

The subsequent category pertains to the strategy, capability, & internal environment of the firm. This particular group encompassed a wide range of variables that served as proxies for assessing firm performance. It corresponded to the diverse array of schemes and plans implemented in response to the complex nature of the business. The most commonly used variable in this group was financing (Chauvet & Jacolin, Citation2017; J. Chen et al., Citation2020; Lyu & Chen, Citation2022), which was followed by supply chain (Arif et al., Citation2022; Liang et al., Citation2023), intellectual capital (Suharman et al., Citation2022; J. Xu & Li, Citation2022), and organization slack (Fonseka et al., Citation2013, Citation2014); organization restructuring (Jefferson & Su, Citation2006; Rossieta, Citation2017) and business strategy (Arif et al., Citation2022; Lyu & Chen, Citation2022); performance contract/evaluation (Chhibber & Gupta, Citation2018; Gunasekar & Sarkar, Citation2019), financial constraint (Hai et al., Citation2022; Y. Wu & Huang, Citation2022), and market orientation (Llonch et al., Citation2011; Xiao et al., Citation2021), with values of 8, 5, 4, and 3, respectively. The utilization of financing plays a crucial role in shaping the capital structure of firms as part of their strategies to achieve their ultimate business objectives. Accordingly, the supply chain and intellectual capital variables were employed to assess the performance of the supplier network and intangible resources of the firm, respectively. Organizational slack was used as an indicator of the surplus or deficit condition of the resources of the firm.

The variables associated with the external environment of the firm ranked fourth in terms of their usage frequency. These variables encompassed characteristics originating from the industry, macroeconomic conditions, and crises. Among them, the most commonly studied variable was market competition, with nine papers dedicated to its analysis. Following this, variables such as the political climate, environmental uncertainty, Gross Domestic Product (GDP) and foreign direct investment have been examined in five, four, and three papers respectively. It is worth noting that the two most prominent sets of variables were strongly interconnected with state ownership, as they have direct implications for competition and politics. The primary measure employed to evaluate market competition was the Herfindahl-Hirschman Index (Apriyantopo et al., Citation2022; Chakrabarti & Mondal, Citation2017; Dai & Guo, Citation2020; Zeng et al., Citation2022), which assesses the degree of concentration in a specific market or industry. Accordingly, given that SOEs were established in part to meet societal demands and address market gaps, this index was utilized to examine its impacts on the performance of these enterprises. In addition to market competition, the political period metrics used include the election period (Harymawan et al., Citation2020; Kim et al., Citation2019), political events such as annual parliamentary meetings (B. Zhou et al., Citation2015), and changes in political regime (Z. Xu & Birch, Citation1999).

Considering the characteristic of state-linked companies, there was a substantial number of variables within the group that pertained to government & policy. The key variables used were government control, government support, and anti-corruption campaign with respective values of 8, 7, and 2. Accordingly, the government control metrics used include government institution (Chong & Galdo, Citation2007; Manh Hoang & Quy Thi, Citation2020; Zang et al., Citation2019), hierarchical layer (Park et al., Citation2006; Souto-Otero & Beneito-Montagut, Citation2015; Su et al., Citation2018), and government intervention (Mbo & Adjasi, Citation2017; L. Yang & Zhang, Citation2015). Regarding the government support variables, the most common forms of government support utilized were subsidies (Bu et al., Citation2017; M. Liu et al., Citation2019; Marimuthu, Citation2020; Singh et al., Citation2023; X. Wang et al., Citation2021). This form of support serves as a government instrument and tool for macroeconomic control to readjust the externality problems resulting from market failure.

The sixth category comprised variables associated with innovation & technology, among which are the Research & Development (R&D) investment/innovation and digitalization variables. These variables were represented by 17 and 5 papers, respectively. Furthermore, the innovation variables were classified into two major constructs namely innovation input and innovation output. The studies conducted by Ding et al. (Citation2022), Yan et al. (Citation2022), Ye et al. (Citation2021), H. Zhang and Aumeboonsuke (Citation2022), and Y. Zhou et al. (Citation2022) focused on innovation input. This construct encompassed the expenditures incurred during the research and development (R&D) activities. On the other hand, Hai et al. (Citation2022), Putra et al. (Citation2020), Shao et al. (Citation2020), and Tang et al. (Citation2021) examined innovation output, which involved the capitalization of the R&D process. The second variable, digitalization, is a critical construct due to its significant role in reshaping the world economy and its dominance role in the digital economy. Digitalization refers to the process of integrating advanced digital technologies and has been widely applied in all business processes. The most commonly used construct for digitalization was the frequency of digital keywords in financial or annual reports, as observed by Y. Ren and Li (Citation2023), H. Wang et al. (Citation2022), H. Wu et al. (Citation2023), Y. Wu and Huang (Citation2022), and Zeng et al. (Citation2022).

The final category focused on human resources and consisted of 10 explanatory variables. Among these variables, the most frequently studied was employee compensation, which was the subject of five papers. The metrics used to measure this variable included bonuses (Caiden & Kim, Citation1993; Michelotti et al., Citation2017; Raiser, Citation1997), employee stock plan ownership (Meng et al., Citation2011; Tian, Citation2022), and non-wage benefits (Michelotti et al., Citation2017) related to consumption and welfare benefits. In addition, employment and labor flexibility were examined in three and two papers respectively. The remaining variables, namely managerial morality, job challenge, union presence, objective performance measures, incentive system, labor training, and human resource management were represented by only a single paper each.

5. Conclusion and further study

In conclusion, this study provided a comprehensive review of the profitability performance of State-Owned Enterprises (SOEs) and their determinants. The study examines the empirical literature trends on SOE performance over a period of 30 years, identifying relevant explanatory variables based on prior studies. The obtained results showed that a total of 328 articles were found related to the topic published in different Scopus-indexed journals. Furthermore, the study trend revealed that there was a steady increase in the number of articles published after 2015, with the highest volume observed in 2022. Notably, a significant portion of these articles were published in China, which aligns with the substantial number of SOEs in the country. Regarding methodology, the majority of papers employed quantitative methods and utilized panel regression as the statistical tool for the analysis. Additionally, it was observed that the manufacturing industry was the most frequently mentioned industry type used across the studies.

The study identified the main explained and explanatory variables based on the existing works of literature. Furthermore, the profitability performance as a proxy of dependent variables was clustered into seven groups, namely return and asset ratio, return and equity ratio, sales or sales ratio, stock or share ratio, revenue and profit, return and investment ratio, as well as return and employee ratio. Among these groups, the most frequently utilized variables were associated with the return and asset ratio, encompassing various return indicators such as net profit, EBITDA, or IBTA. Additionally, the study grouped the proxy of SOE performance determinants, as independent variables, into seven categories. These categories include corporate governance; firm characteristics; strategy, capability, & internal environment; government & policy; innovation & technology; and human resources. It is also important to note that significant emphasis was laid on ownership, particularly in relation to corporate governance variables. This focus can be attributed to the nature of SOEs as organizations associated with ownership.

The study highlights important implications for future study as it expands the existing literature on state-owned organizations and identifies research gaps for future academic exploration. It contributes to providing an overview of the state-of-the-art of SOE performance, while also directing future investigators toward previously overlooked areas that have not been emphasized in prior studies. With regards to the geographical context, there is a need for future studies to expand their examination beyond China, as there is a notable gap in research pertaining to observations made in other countries. Additionally, the research also highlighted the limited number of studies that analyze SOEs in a cross-country context. One of the primary reasons for this is the authors’ avoidance of the differences in accounting, cultural, economic, legal, and political systems across various countries. However, with increased accessibility and availability of data, it is recommended that future research should engage in more cross-country studies to improve our understanding of SOEs on a global scale.

This study suggests the need for further research to expand the discussion and enrich the existing knowledge by conducting in-depth analyses using qualitative approaches. For example, employing qualitative studies with interview techniques as data collection methods can yield extensive and valuable data, enabling authors to comprehend behaviors, experiences, contributions, and other relevant factors (T. H. H. Nguyen et al., Citation2020). Additionally, it is suggested that future authors consider employing mixed methods, combining statistical approaches with qualitative techniques. This approach can potentially offer a better explanation of the profitability performance of SOEs. Furthermore, this review reveals that the majority of studies have focused on general manufacturing industries as their sample. This study recommends that further research ventures explore and specialize in industry areas that have received less attention in the current body of research to gain deeper insights into the specific dynamics and challenges faced by SOEs in different business contexts.

The performance of SOEs has been extensively studied, with numerous factors being investigated. However, this study reveals that certain variables remain limited in their exploration. Therefore, it is recommended that future research efforts provide further insights and focus on variables that have received less attention in the current study. For example, further investigation into areas like innovation and technology, particularly in terms of digitalization, would contribute to a better understanding of SOE performance. Accordingly, it is important to acknowledge the limitations of this study. Firstly, there is a possibility that relevant reference sources may have been inadvertently excluded from the chosen electronic database, which could have affected the comprehensiveness of this SLR. Secondly, despite implementing a rigorous systematic literature review protocol, there is still a potential risk of research bias (Tranfield et al., Citation2003). Thirdly, the scope of the discussion in this study is primarily focused on identifying and summarizing the determinants variables that have been addressed in prior studies regarding the profitability performance of SOEs. Future SLRs may consider synthesizing the effects of each determinant to provide broader recommendations for future research directions.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Supplemental Material

Download MS Word (215.2 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Supplementary material

Supplemental data for this article can be accessed online at https://doi.org/10.1080/23311975.2023.2234138

Additional information

Notes on contributors

Muhammad Alam Mauludina

Muhammad Alam Mauludina is a doctoral candidate at Department of Accounting, Universitas Padjadjaran, Indonesia. His research interests are related to Accounting Information Systems, Public Sector Organizations.

Yudi Azis

Yudi Azis is a lecturer at Department of Management, Universitas Padjadjaran, Indonesia.

Citra Sukmadilaga

Citra Sukmadilaga is a lecturer at Department of Accounting, Universitas Padjadjaran, Indonesia.

Hendra Susanto

Hendra Susanto is currently working as a Board Member of the Audit Board of the Republic of Indonesia.

References

- Ahunov, H. (2023). Non-financial reporting in hybrid organizations – a systematic literature review. Meditari Accountancy Research. https://doi.org/10.1108/MEDAR-01-2022-1558

- Alipour, M. (2013). Has privatization of state-owned enterprises in Iran led to improved performance? International Journal of Commerce & Management, 23(4), 281–31. https://doi.org/10.1108/IJCoMA-03-2012-0019

- Almaqtari, F. A., Al-Hattami, H. M., Al-Nuzaili, K. M. E., Al-Bukhrani, M. A., & Ntim, C. G. (2020). Corporate governance in India: A systematic review and synthesis for future research. Cogent Business & Management, 7(1), 1803579. https://doi.org/10.1080/23311975.2020.1803579

- Amin, M. Y., & Haq, Z. U. (2022). BRIC without B: Does ownership structure matters for firm performance in emerging economies? Quality and Quantity, 56(1), 217–226. https://doi.org/10.1007/s11135-021-01124-8

- Ang, R., Shao, Z., Liu, C., Yang, C., & Zheng, Q. (2022). The relationship between CSR and financial performance and the moderating effect of ownership structure: Evidence from Chinese heavily polluting listed enterprises. Sustainable Production and Consumption, 30, 117–129. https://doi.org/10.1016/j.spc.2021.11.030

- Apriyantopo, W., Aprianingsih, A., & Kitri, M. L. (2022). State-owned enterprises’ performance in Indonesia: A strategic typology perspective. Competitiveness Review, 33(4), 759–786. https://doi.org/10.1108/CR-01-2021-0019

- Arif, B., Sule, E. T., Herwany, A., & Febrian, E. (2022). The effects of business environment and supply chain governance on business strategies and company performance. Uncertain Supply Chain Management, 10(1), 37–42. https://doi.org/10.5267/j.uscm.2021.10.012

- Bai, C.-E., Lu, J., & Tao, Z. (2009). How does privatization work in China? Journal of Comparative Economics, 37(3), 453–470. https://doi.org/10.1016/j.jce.2008.09.006

- Bhatt, P. R. (2016). Performance of government linked companies and private owned companies in Malaysia. International Journal of Law and Management, 58(2), 150–161. https://doi.org/10.1108/IJLMA-11-2014-0062

- Boardman, A. E., Vining, A. R., & Weimer, D. L. (2016). The long-run effects of privatization on productivity: Evidence from Canada. Journal of Policy Modeling, 38(6), 1001–1017. https://doi.org/10.1016/j.jpolmod.2016.04.002

- Boateng, A., Bi, X. G., & Brahma, S. (2017). The impact of firm ownership, board monitoring on operating performance of Chinese mergers and acquisitions. Review of Quantitative Finance & Accounting, 49(4), 925–948. https://doi.org/10.1007/s11156-016-0612-y

- Bo, X., Fan, X. M., & Kong, A. (2023). The dark side of political promotion incentives: Evidence from firm performance. Finance Research Letters, 51, 51. https://doi.org/10.1016/j.frl.2022.103382

- Bo, L., Tang, D., Zhang, J., & Bethel, B. J. An investigation of the transmission mechanism of executive compensation control to the operating performance of state-owned listed companies. (2022). Sustainability, 14(10), 5819. Switzerland), 14(10. https://doi.org/10.3390/su14105819

- Boxu, Y., Xingguang, L., & Kou, K. (2022). Research on the influence of network embeddedness on innovation performance: Evidence from China’s listed firms. Journal of Innovation & Knowledge, 7(3). https://doi.org/10.1016/j.jik.2022.100210

- Brahma, S., Zhang, J., Boateng, A., & Nwafor, C. (2023). Political connection and M&A performance: Evidence from China. International Review of Economics and Finance, 85, 372–389. https://doi.org/10.1016/j.iref.2023.01.026

- Burki, A. A., & Niazi, G. S. K. (2010). Impact of financial reforms on efficiency of state-owned, private and foreign banks in Pakistan. Applied Economics, 42(24), 3147–3160. https://doi.org/10.1080/00036840802112315

- Bu, D., Zhang, C., & Wang, X. (2017). Purposes of government subsidy and firm performance. China Journal of Accounting Studies, 5(1), 100–122. https://doi.org/10.1080/21697213.2017.1292730

- Caiden, G., & Kim, K. (1993). Measuring the performance of state-owned enterprises in South Korea. Asian Journal of Political Science, 1(2), 110–143. https://doi.org/10.1080/02185379308434028

- Castelnovo, P. (2022). Innovation in private and state-owned enterprises: A cross-industry analysis of patenting activity. Structural Change and Economic Dynamics, 62, 98–113. https://doi.org/10.1016/j.strueco.2022.05.007

- Chakrabarti, A. B., & Mondal, A. (2017). Can commercialization through partial disinvestment improve the performance of state-owned enterprises? The case of Indian SOEs under reforms. Journal of General Management, 43(1), 5–14. https://doi.org/10.1177/0306307017719700

- Chakrabarti, A. B., & Ray, S. (2018). An exploratory study on the impact of pro-market reforms on the Indian corporate sector. Journal of Economic Policy Reform, 21(1), 1–20. https://doi.org/10.1080/17487870.2016.1235498

- Chan, K. K. Y., Chen, L., & Wong, N. (2018). New Zealand State-owned enterprises: Is state-ownership detrimental to firm performance? New Zealand Economic Papers, 52(2), 170–184. https://doi.org/10.1080/00779954.2016.1272626

- Chauvet, L., & Jacolin, L. (2017). Financial inclusion, bank concentration, and firm performance. World Development, 97, 1–13. https://doi.org/10.1016/j.worlddev.2017.03.018

- Chen, G., Firth, M., & Rui, O. (2006). Have China’s enterprise reforms led to improved efficiency and profitability? Emerging Markets Review, 7(1), 82–109. https://doi.org/10.1016/j.ememar.2005.05.003

- Chen, G., Firth, M., & Wei Zhang, W. (2008). The efficiency and profitability effects of China’s modern enterprise restructuring programme. Asian Review of Accounting, 16(1), 74–91. https://doi.org/10.1108/13217340810872481

- Chen, Y.-R., Jiang, X., & Weng, C.-H. (2020). Can government industrial policy enhance corporate bidding? The evidence of China. Pacific Basin Finance Journal, 60, 60. https://doi.org/10.1016/j.pacfin.2020.101288

- Chen, L., Li, S., & Lin, W. (2007). Corporate governance and corporate performance: Some evidence from newly listed firms on Chinese stock markets. International Journal of Accounting, Auditing and Performance Evaluation, 4(2), 183–197. https://doi.org/10.1504/IJAAPE.2007.015233

- Chen, S., Mao, H., & Sun, J. (2022). Low-carbon city construction and corporate carbon reduction performance: Evidence from a quasi-natural experiment in China. Journal of Business Ethics, 180(1), 125–143. https://doi.org/10.1007/s10551-021-04886-1

- Chen, J., Zhao, X., Niu, X., Fan, Y. H., & Taylor, G. (2020). Does M&A financing affect firm performance under different ownership types? Sustainability, 12(8), 3078. https://doi.org/10.3390/SU12083078

- Chhibber, A., & Gupta, S. (2018). Public sector undertakings: Bharat’s other Ratnas. International Journal of Public Sector Management, 31(2), 113–127. https://doi.org/10.1108/IJPSM-02-2017-0044

- Chi, J., Liao, J., & Li, F. (2014). The success of China’s non-tradable share reform. Corporate Ownership & Control, 11(4 Continued 3), 355–369. https://doi.org/10.22495/cocv11i4c3p6

- Chong, A., & Galdo, V. (2007). Should state-owned firms change CEOs before privatization? Some evidence from the telecommunications industry. Applied Economics Letters, 14(8), 591–595. https://doi.org/10.1080/13504850600592515

- Comstock, A., Kish, R. J., & Vasconcellos, G. M. (2003). The post-privatization financial performance of former state-owned enterprises. Journal of International Financial Markets, Institutions and Money, 13(1), 19–37. https://doi.org/10.1016/S1042-4431(02)00024-0

- Crowley, M. A., Meng, N., & Song, H. (2019). Policy shocks and stock market returns: Evidence from Chinese solar panels. Journal of the Japanese and International Economies, 51, 148–169. https://doi.org/10.1016/j.jjie.2019.02.006

- Dai, Z., & Guo, L. (2020). Market competition and corporate performance: Empirical evidence from China listed banks with financial monopoly aspect. Applied Economics, 52(44), 4822–4833. https://doi.org/10.1080/00036846.2020.1745749

- Deng, X., & Cheng, X. (2019). Can ESG indices improve the enterprises’ stock market performance?—an empirical study from China. Sustainability, 11(17), 4765. https://doi.org/10.3390/su11174765

- Ding, X., Jing, R., Wu, K., Petrovskaya, M. V., Li, Z., Steblyanskaya, A., Ye, L., Wang, X., & Makarov, V. M. (2022). The impact mechanism of green credit policy on the sustainability performance of heavily polluting enterprises—based on the perspectives of technological innovation level and credit resource allocation. International Journal of Environmental Research and Public Health, 19(21), 14518. https://doi.org/10.3390/ijerph192114518

- Du, M., Kwabi, F., & Yang, T. (2021). State ownership, prior experience and performance: A comparative analysis of Chinese domestic and cross-border acquisitions. International Journal of Accounting & Information Management, 29(3), 472–491. https://doi.org/10.1108/IJAIM-01-2021-0027

- Fonseka, M. M., Tian, G.-L., Yang, X., & Rajapakse, R. L. T. N. (2014). The interactions between different types of financial and human resource slacks on firm performance: Evidence from a developing country. South African Journal of Business Management, 45(3), 57–66. https://doi.org/10.4102/sajbm.v45i3.131

- Fonseka, M. M., Wang, P., & Manzoor, M. S. (2013). Impact of human resource slacks on firm performance: Evidence from a developing country. Zbornik Radova Ekonomskog Fakultet Au Rijeci, 31(2), 279–306. https://www.scopus.com/inward/record.uri?eid=2-s2.0-84890922288&partnerID=40&md5=86197ba032a767c46a6a2999d6b77bfd

- Gakhar, D. V., & Phukon, A. (2018). From welfare to wealth creation: A review of the literature on privatization of state-owned enterprises. International Journal of Public Sector Management, 31(2), 265–286. https://doi.org/10.1108/IJPSM-03-2017-0096

- Gao, Y., Cheng, G., & Ma, Y. (2021). An analysis of the comprehensive efficiency and its determinants of china’s national champions: competition neutrality vs. ownership neutrality. Structural Change and Economic Dynamics, 59, 320–329. https://doi.org/10.1016/j.strueco.2021.09.001

- Gao, X., & Zhang, W. Can innovation incentive policies improve the innovation performance of knowledge workers? evidence from chinese state-owned enterprises. (2023). Sustainability, 15(3), 2424. Switzerland), 15(3. https://doi.org/10.3390/su15032424

- Goldeng, E., Grünfeld, L. A., & Benito, G. R. G. (2008). The performance differential between private and state owned enterprises: The roles of ownership, management and market structure. Journal of Management Studies, 45(7), 1244–1273. https://doi.org/10.1111/j.1467-6486.2008.00790.x

- Grossi, G., Papenfuß, U., & Tremblay, M.-S. (2015). Corporate governance and accountability of state-owned enterprises: Relevance for science and society and interdisciplinary research perspectives. International Journal of Public Sector Management, 28(4–5), 274–285. https://doi.org/10.1108/IJPSM-09-2015-0166

- Gunasekar, S., & Sarkar, J. (2019). Does autonomy matter in state owned enterprises? evidence from performancecontracts in India. Economics of Transition & Institutional Change, 27(3), 763–800. https://doi.org/10.1111/ecot.12220

- Guo, C., Lai, H., Jiang, Y., & Wu, Y. (2023). Debt finance and environmental performance of heavily polluting companies in China: The perspective of the green credit guideline policy. Asia-Pacific Journal of Accounting and Economics, 30(1), 212–229. https://doi.org/10.1080/16081625.2021.1976227

- Gupta, N. (2005). Partial privatization and firm performance. The Journal of Finance, 60(2), 987–1015. https://doi.org/10.1111/j.1540-6261.2005.00753.x

- Hai, B., Yin, X., Xiong, J., & Chen, J. (2022). Could more innovation output bring better financial performance? The role of financial constraints. Financial Innovation, 8(1). https://doi.org/10.1186/s40854-021-00309-2

- Han, H., & Gu, X. (2021). Linkage between inclusive digital finance and high-tech enterprise innovation performance: Role of debt and equity financing. Frontiers in Psychology, 12, 12. https://doi.org/10.3389/fpsyg.2021.814408

- Harymawan, I., Nasih, M., Suhardianto, N., Shauki, E., & Ntim, C. G. (2020). How does the presidential election period affect the performance of the state-owned enterprise in Indonesia? Cogent Business & Management, 7(1), 1750330. https://doi.org/10.1080/23311975.2020.1750330

- Hazaea, S. A., Zhu, J., Al-Matari, E. M., Senan, N. A. M., Khatib, S. F. A., & Ullah, S. (2021). Mapping of internal audit research in China: A systematic literature review and future research agenda. Cogent Business & Management, 8(1). https://doi.org/10.1080/23311975.2021.1938351

- Hermansjah, R., Sugiarto, U., Hulu, E., & Hulu, E. (2021). The effect of government ownership on Indonesia’s state-owned enterprises’ (SOE) firm performance. Accounting, 7(6), 1347–1352. https://doi.org/10.5267/j.ac.2021.4.003

- Ho, K.-C., Li, H.-M., & Gong, Y. (2022). How does corporate social performance affect investment inefficiency? An empirical study of China market. Borsa Istanbul Review, 22(3), 515–524. https://doi.org/10.1016/j.bir.2021.06.016

- Hong Nham, N. T., Hong Tam, L. T., & The Dong, P. (2021). Use of the stochastic frontier approach to assessing the impacts of ownership structure on the efficiency of the construction industry in vietnam. Indian Journal of Economics and Development, 17(1), 1–10. https://doi.org/10.35716/IJED/20211

- Ho, J. L. Y., Yang, X., & Li, X. (2011). Control privatization, corporate governance, and firm performance: Evidence from China. Journal of International Accounting Research, 10(2), 23–56. https://doi.org/10.2308/jiar-10079

- Inoue, C. (2020). Election cycles and organizations: How politics shapes the performance of state-owned enterprises over time. Administrative Science Quarterly, 65(3), 677–709. https://doi.org/10.1177/0001839219869913

- International Monetary Fund. (2020). State-Owned Enterprises in the Time of COVID-19. https://www.imf.org/en/Blogs/Articles/2020/05/07/blog-state-owned-enterprises-in-the-time-of-covid-19

- International Monetary Fund. (2023). World economic outlook: A Rocky recovery. https://www.imf.org/en/Publications/WEO/Issues/2023/04/11/world-economic-outlook-april-2023

- Jefferson, G. H., & Su, J. (2006). Privatization and restructuring in China: Evidence from shareholding ownership, 1995-2001. Journal of Comparative Economics, 34(1), 146–166. https://doi.org/10.1016/j.jce.2005.11.008

- Jiang, F., Huang, J., & Kim, K. A. (2013). Appointments of outsiders as CEOs, state-owned enterprises, and firm performance: Evidence from China. Pacific Basin Finance Journal, 23, 49–64. https://doi.org/10.1016/j.pacfin.2013.01.003

- Jiang, H., & Zhang, H. (2018). Regulatory restriction on executive compensation, corporate governance and firm performance Evidence from China. Asian Review of Accounting, 26(1), 131–152. https://doi.org/10.1108/ARA-07-2016-0080

- Jia, J., Sun, Q., & Tong, W. H. S. (2005). Privatization through an overseas listing: Evidence from China’s H-share firms. Financial Management, 34(3), 5–30. https://doi.org/10.1111/j.1755-053X.2005.tb00108.x

- Jia, X., Wang, T., & Chen, C. (2022). Executive poverty experience and innovation performance: A study of moderating effects and influencing mechanism. Frontiers in Psychology, 13, 13. https://doi.org/10.3389/fpsyg.2022.946167

- Jin, H. (2023). Effects of decentralization on firm performance: Evidence from Chinese county-level quasi-experiments. Economic Modelling, 119, 106116. https://doi.org/10.1016/j.econmod.2022.106116

- Kaunda, E., & Pelser, T. (2022). A STRATEGIC CORPORATE GOVERNANCE FRAMEWORK for STATE-OWNED ENTERPRISES in the DEVELOPING ECONOMY. Journal of Governance & Regulation, 11(2, special issue), 257–276. https://doi.org/10.22495/jgrv11i2siart5

- Khaq, A. (2020). The relevance of corporate governance and capital structure to financial performance in state-owned enterprises (SOES). International Journal of Innovation, Creativity & Change, 12(5), 515–537. https://www.scopus.com/inward/record.urieid=2s285084409106&partnerID=40&md5=f438abe49cb1ebed6ea8b70981c1c530

- Kim, S., Shin, H.-H., & Yu, S. (2019). Performance of state-owned enterprises during public elections: The case of Korea. Emerging Markets Finance and Trade, 55(1), 78–89. https://doi.org/10.1080/1540496X.2018.1509789

- Kitchenham, B. (2004). Procedures for performing systematic reviews. Keele University and NICTA. https://doi.org/10.1080/23311975.2021.1938351

- Kuzman, T., Talavera, O., & Bellos, S. K. (2018). Politically induced board turnover, ownership arrangements, and performance of SOEs. Corporate Governance an International Review, 26(3), 160–179. https://doi.org/10.1111/corg.12238

- Lam, K. C. K., McGuinness, P. B., & Vieito, J. P. (2013). CEO gender, executive compensation and firm performance in Chinese-listed enterprises. Pacific Basin Finance Journal, 21(1), 1136–1159. https://doi.org/10.1016/j.pacfin.2012.08.006

- Laporšek, S., Dolenc, P., Grum, A., & Stubelj, I. (2021). Ownership structure and firm performance–The case of Slovenia. Economic Research-Ekonomska Istrazivanja, 34(1), 2975–2996. https://doi.org/10.1080/1331677X.2020.1865827

- Lazzarini, S. G., Musacchio, A., Bandeira de Mello, R., & Marcon, R. (2015). What do state-owned development banks do? Evidence from BNDES, 2002-09. World Development, 66, 237–253. https://doi.org/10.1016/j.worlddev.2014.08.016

- Le, M.-D., Pieri, F., & Zaninotto, E. (2019). From central planning towards a market economy: The role of ownership and competition in Vietnamese firms’ productivity. Journal of Comparative Economics, 47(3), 693–716. https://doi.org/10.1016/j.jce.2019.04.002

- Liang, S., Yu, R., Liu, Z., Wang, W., Wu, L., & Hu, X. (2023). An empirical study on the asset-light operation and corporate performance of China’s tourism listed companies. Heliyon, 9(2). https://doi.org/10.1016/j.heliyon.2023.e13391

- Liao, L., Liu, B., & Wang, H. (2014). China’s secondary privatization: perspectives from the split-share structure reform. Journal of Financial Economics, 113(3), 500–518. https://doi.org/10.1016/j.jfineco.2014.05.007

- Li, D., Moshirian, F., Nguyen, P., & Tan, L.-W. (2007). Managerial ownership and firm performance: Evidence from China’s privatizations. Research in International Business and Finance, 21(3), 396–413. https://doi.org/10.1016/j.ribaf.2007.02.001

- Li, W., Su, Y., & Wang, K. (2022). How does economic policy uncertainty affect cross-border M&A: Evidence from Chinese firms. Emerging Markets Review, 52, 52. https://doi.org/10.1016/j.ememar.2022.100908

- Liu, M., Liu, L., Xu, S., Du, M., Liu, X., & Zhang, Y. The influences of government subsidies on performance of new energy firms: A firm heterogeneity perspective. (2019). Sustainability, 11(17), 4518. Switzerland), 11(17. https://doi.org/10.3390/su11174518

- Liu, X., Zhao, R., & Guo, M. (2022). CEO turnover, political connections, and firm performance: Evidence from China. Emerging Markets Review, 55, 100965. https://doi.org/10.1016/j.ememar.2022.100965

- Li, Z., Wang, B., & Zhou, D. (2022). Financial experts of top management teams and corporate social responsibility: Evidence from China. Review of Quantitative Finance & Accounting, 59(4), 1335–1386. https://doi.org/10.1007/s11156-022-01077-5

- Li, H., Zhang, X., Khaliq, U., & Rehman, F. U. (2023). Emergency engineering reconstruction mode based on the perspective of professional donations. Frontiers in Psychology, 14, 14. https://doi.org/10.3389/fpsyg.2023.971552

- Li, X., & Zhao, Z. (2022). Corporate internal control, financial mismatch mitigation and innovation performance. PLoS ONE, 17(12), 1–29. https://doi.org/10.1371/journal.pone.0278633

- Llonch, J., Rialp, A., & Rialp, J. (2011). Marketing capabilities, enterprise optimization programs and performance in early transition economies: The case of Cuban SOEs. Transformations in Business and Economics, 10(3), 45–71. https://www.scopus.com/inward/record.uri?eid=2-s2.0-84856647645&partnerID=40&md5=f72fbaf9b8e9d225b865b5f76c62f759

- Loc, T. D., Lanjouw, G., & Lensink, R. (2006). The impact of privatization on firm performance in a transition economy. The case of Vietnam. The Economics of Transition, 14(2), 349–389. https://doi.org/10.1111/j.1468-0351.2006.00251.x

- Luo, J.-H., & Liu, Y. (2023). Does the reputation mechanism apply to independent directors in emerging markets? Evidence from China. China Journal of Accounting Research, 16(1), 100283. https://doi.org/10.1016/j.cjar.2022.100283

- Luong, T. C. T., Jorissen, A., & Paeleman, I. Performance measurement for sustainability: Does firm ownership matter. (2019). Sustainability, 11(16), 4436. Switzerland), 11(16. https://doi.org/10.3390/su11164436

- Lyu, B., & Chen, H. (2022). Effect of founder control on equity financing and corporate performance-based on moderation of radical strategy. SAGE Open, 12(2), 215824402210850. https://doi.org/10.1177/21582440221085013

- Manes-Rossi, F., Nicolò, G., & Argento, D. (2020). Non-financial reporting formats in public sector organizations: A structured literature review. Journal of Public Budgeting, Accounting & Financial Management, 32(4), 639–669. https://doi.org/10.1108/JPBAFM-03-2020-0037

- Manh Hoang, N., & Quy Thi, V. O. (2020). Government control and privatized firms’ performance: Evidence from vietnam. The Journal of Asian Finance, Economics & Business, 7(10), 663–673. https://doi.org/10.13106/jafeb.2020.vol7.no10.663

- Marimuthu, F. (2020). Government assistance to state-owned enterprises: A hindrance to financial performance. Investment Management & Financial Innovations, 17(2), 40–50. https://doi.org/10.21511/imfi.17(2).2020.04

- Marimuthu, F. (2021). FACTORS DRIVING the FINANCIAL PERFORMANCE of STATE-OWNED ENTERPRISES in an EMERGING MARKET. Journal of Management Information & Decision Sciences, 25(7), 1–17. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85112807634&partnerID=40&md5=4b672d07f7c20f1486ba7918f8f84b4e

- Markin, E. T., Skorodziyevskiy, V., Zhu, L., Chrisman, J. J., & Fang, H. (2022). Lone-founder firms in China: Replicating Miller et al. (2007) in a different context. Journal of Family Business Strategy, 13(4). https://doi.org/10.1016/j.jfbs.2021.100451

- Mauludina, M. A., Mulyani, S., & Adrianto, Z. (2023). Critical success factors for implementation of self-service business intelligence in management accounting. Academic Journal of Interdiciplinary Studies, 12(3), 291–307. https://doi.org/10.36941/ajis-2023-0078

- Ma, Q., Yan, G., Ren, X., & Ren, X. (2022). Can China’s carbon emissions trading scheme achieve a double dividend? Environmental Science and Pollution Research, 29(33), 50238–50255. https://doi.org/10.1007/s11356-022-19453-y

- Mbo, M., & Adjasi, C. (2017). Drivers of organizational performance in state owned enterprises. International Journal of Productivity and Performance Management, 66(3), 405–423. https://doi.org/10.1108/IJPPM-11-2015-0177

- Meng, R., Ning, X., Zhou, X., & Zhu, H. (2011). Do ESOPs enhance firm performance? Evidence from China’s reform experiment. Journal of Banking and Finance, 35(6), 1541–1551. https://doi.org/10.1016/j.jbankfin.2010.11.004

- Menozzi, A., Urtiaga, M., & Vannoni, D. (2012). Board composition, political connections, and performance in state-owned enterprises. Industrial and Corporate Change, 21(3), 671–698. https://doi.org/10.1093/icc/dtr055

- Miążek, R. (2021). Corporate governance in state-owned enterprises. A systematic literature review: An international perspective. International Journal of Contemporary Management, 57(4), 1–13. https://doi.org/10.2478/ijcm-2021-0011

- Michelotti, M., Vocino, A., Gahan, P., & Roloff, J. (2017). Non-wage benefits, corporate ownership and firm performance in post-communist economies: Evidence from Ukraine. The International Journal of Human Resource Management, 28(20), 2861–2892. https://doi.org/10.1080/09585192.2016.1139617

- Modén, K.-M., Norbäck, P.-J., & Persson, L. (2008). Efficiency and ownership structure: The case of Poland. The World Economy, 31(3), 437–460. https://doi.org/10.1111/j.1467-9701.2007.01065.x

- Motohashi, K. (2008). IT, enterprise reform, and productivity in Chinese manufacturing firms. Journal of Asian Economics, 19(4), 325–333. https://doi.org/10.1016/j.asieco.2008.05.001

- Munyo, I., & Regent, P. (2016). Exercise of ownership rights and efficiency in state-owned enterprises: The case of Uruguay. Management Research, 14(2), 150–165. https://doi.org/10.1108/MRJIAM-12-2015-0623

- Ngo, H.-Y., Lau, C.-M., & Foley, S. (2008). Strategic human resource management, firm performance, and employee relations climate in China. Human Resource Management, 47(1), 73–90. https://doi.org/10.1002/hrm.20198

- Nguyen, H. Q. Total factor productivity growth of Vietnamese enterprises by sector and region: Evidence from panel data analysis. (2021). Economies, 9(3), 109. 9(3. https://doi.org/10.3390/economies9030109

- Nguyen, T. H. H., Ntim, C. G., & Malagila, J. K. (2020). Women on corporate boards and corporate financial and non-financial performance: A systematic literature review and future research agenda. International Review of Financial Analysis, 71(June), 101554. https://doi.org/10.1016/j.irfa.2020.101554

- Ngwenya, S., & Khumalo, M. (2012). CEO compensation and performance of state owned enterprises in South Africa. Corporate Ownership & Control, 10(1 A), 97–109. https://doi.org/10.22495/cocv10i1art9

- Ng, A., Yuce, A., & Chen, E. (2009). Determinants of state equity ownership, and its effect on value/performance: China’s privatized firms. Pacific Basin Finance Journal, 17(4), 413–443. https://doi.org/10.1016/j.pacfin.2008.10.003

- Otchere, I., & Chan, J. (2003). Intra-industry effects of bank privatization: A clinical analysis of the privatization of the Commonwealth Bank of Australia. Journal of Banking and Finance, 27(5), 949–975. https://doi.org/10.1016/S0378-42660200242-X

- Pang, R., Shi, M., & Zheng, D. (2022). Who comply better? The moderating role of firm heterogeneity on the performance of environmental regulation in China. Environment, Development and Sustainability, 24(5), 6302–6326. https://doi.org/10.1007/s10668-021-01703-7

- Parida, M., & Madheswaran, S. (2021). Does ownership matter? Empirical evidence from the performance of Indian state and private coal mining companies. Resources Policy, 74, 102388. https://doi.org/10.1016/j.resourpol.2021.102388

- Park, S. H., Li, S., & Tse, D. K. (2006). Market liberalization and firm performance during China’s economic transition. Journal of International Business Studies, 37(1), 127–147. https://doi.org/10.1057/palgrave.jibs.8400178

- Pei, W., & Pei, W. (2023). Empirical study on the impact of government environmental subsidies on environmental performance of heavily polluting enterprises based on the regulating effect of internal control. International Journal of Environmental Research and Public Health, 20(1), 98. https://doi.org/10.3390/ijerph20010098

- Petticrew, M., & Roberts, H., Petticrew, M., Roberts, H. (2006). Systematic reviews in the social sciences: a practical guide. Blackwell Publishing Ltd. https://doi.org/10.1002/9780470754887

- Putra, I. A., Rofiaty, R., & Djumahir, D. (2020). Investigating the influence of entrepreneurial orientation and transformational leadership on organisational performance with the mediation of innovation: evidences from a state-owned electricity company in indonesia. International Journal of Innovation Management, 24(7), 2050085. https://doi.org/10.1142/S1363919620500851

- Qiao, T., Han, L., & Liu, Y. (2021). Does targeted poverty alleviation disclosure improve stock performance? Economics Letters, 201, 201. https://doi.org/10.1016/j.econlet.2021.109805

- Qi, D., Wu, W., & Zhang, H. (2000). Shareholding structure and corporate performance of partially privatized firms: Evidence from listed Chinese companies. Pacific Basin Finance Journal, 8(5), 587–610. https://doi.org/10.1016/s0927-538x(00)00013-5

- Qi, Y., Yu, J., Yang, S., & Xie, X. (2022). Local government consumption and firm performance. Evidence from the “TPCs” in China. Journal of Asian Economics, 80, 101477. https://doi.org/10.1016/j.asieco.2022.101477

- Raiser, M. (1997). Evaluating Chinese industrial reforms: SOEs between output growth and profit decline. Asian Economic Journal, 11(3), 299–323. https://doi.org/10.1111/1467-8381.00039

- Ren, Y., & Li, B. (2023). Digital transformation, green technology innovation and enterprise financial performance: empirical evidence from the textual analysis of the annual reports of listed renewable energy enterprises in China. Sustainability (Switzerland), 15(1. https://doi.org/10.3390/su15010712

- Ren, Y., Li, B., & Liang, D. (2023). Impact of digital transformation on renewable energy companies’ performance: Evidence from China. Frontiers in Environmental Science, 10, 10. https://doi.org/10.3389/fenvs.2022.1105686

- Ren, T., Liu, N., Yang, H., Xiao, Y., & Hu, Y. (2019). Working capital management and firm performance in China. Asian Review of Accounting, 27(4), 546–562. https://doi.org/10.1108/ARA-04-2018-0099

- Rong, R., Qiqi, W., Zhiyang, L., & Shaobo, L. (2022). Does the government procurement market favor corporate social responsibility in a weak institution? Evidence from China. Elementa: Science of the Anthropocene, 10(1), 574–595. https://doi.org/10.1525/elementa.2022.00016

- Rossieta, H. (2017). Good governance mechanism, agency problems and privatized SOEs performance: Empirical evidences from Indonesian stock exchange. International Journal of Economics & Management, 11(2 Special Issue), 287–307. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85050894652&partnerID=40&md5=4ecb3279eadd6606a399bd52425ae073

- Santoso, D. B., Wijaya, A. I., & Erlando, A. (2019). Has the corporate culture of state-owned enterprises changed after privatization? Opcion, 35(Special Issue 23), 979–994. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85077610617&partnerID=40&md5=e41f1b1efe9f637467438b95bbe196ae

- Sarfraz, M., Shah, S. G. M., Ivascu, L., & Qureshi, M. A. A. (2022). Explicating the impact of hierarchical CEO succession on small-medium enterprises’ performance and cash holdings. International Journal of Finance and Economics, 27(2), 2600–2614. https://doi.org/10.1002/ijfe.2289

- Sekaran, U., & Bougie, R. (2016). Reserach Methods for Bussiness a Skill-Bulding Approach (7th ed.). Wiley.

- Shao, D., Zhao, S., Wang, S., & Jiang, H. Impact of CEOs’ academic work experience on firms’ innovation output and performance: Evidence from chinese listed companies. (2020). Sustainability, 12(18), 7442. Switzerland), 12(18. https://doi.org/10.3390/SU12187442