Abstract

The purpose of the study is to examine the effect of QR code payment and mobile money on the performance of SMES in developing countries and the moderating role of dynamic capabilities. A survey method was used to gather data from the target population of SMEs that are making use of digital financial services in their business transactions. A total of 206 SMEs responded to the questionnaires. The study found that both mobile money usage and QR code payments have a significant and positive impact on SME performance. In addition to that, the study revealed that the effect of dynamic capabilities on firm performance was also statistically significant. The study also found the moderating effect was statistically significant for mobile money payments. However, for QR code payments, the moderation effect was not statistically significant. These findings imply that it is prudent for SMEs to adopt digital financial services for business transactions. Thus, improvement in the level of innovativeness in a dynamic business environment plagued by the COVID-19 pandemic will significantly improve SME performance. This will help make SMEs more robust and adjust themselves to the dynamics of the business environment.

1. Introduction

Small and medium-sized enterprises (SMEs) play a crucial role in the economies of developing countries; therefore, their survival and growth are major concerns for both academic and professional researchers (Akenroye et al., Citation2020; Bouwman et al., Citation2019; Dejardin et al., Citation2022; Donkor et al., Citation2018; Ferreira et al., Citation2020). The present digital revolution has generated enormous opportunities for the expansion of sophisticated payment systems (Abdulkader et al., Citation2020; Alam et al., Citation2021) and offers businesses, especially SMEs, more incentives than firms previously had (Alam et al., Citation2021; Kazan et al., Citation2018). In effect, digital financial service platforms are becoming widespread in all areas of society (Choi et al., Citation2020; Ruutu et al., Citation2017), especially with the advent of the COVID-19 pandemic.

With the advent of the COVID-19 pandemic, it became immediately apparent that digital financial services would play a significant role in keeping people connected, delivering vital financial support, and providing safe, no-contact payment methods for food, electricity, and other life necessities. Thus, the COVID-19 pandemic has vitalized the use of digital financial services, which are fast becoming key instruments in almost every sphere of life. For example, the COVID-19 pandemic restrictions have created the impetus for the QR code system of payment to be initiated in Ghana in 2020, making Ghana among the first African countries to implement this remarkable digital technology as a way of moving to a cashless system, digitalizing the economy, and ultimately presenting value-added opportunities for SMEs in Ghana.

The businesses of today’s world are moving towards digitalization, as digital technologies are compelling most firms to change or adapt their business models and provide solutions that offer new revenue and value-adding opportunities to organizations (Antonucci et al., Citation2020; Hoch & Brad, Citation2021; Kazan et al., Citation2018), especially for SMEs in developing countries. This is because there is mounting evidence that financial inclusion is crucial to the economy of every nation and a company’s success as well (Chauvet & Jacolin, Citation2017; Choi et al., Citation2020; Lorenz & Pommet, Citation2021; Nan et al., Citation2021; Yan et al., Citation2021). Yet, the underdevelopment of the financial infrastructure in developing countries limits the availability of financial services to a substantial part of the population (Demirguc-Kunt et al., Citation2018; Konte & Tetteh, Citation2023), creating cutting-edge opportunities for SMEs in developing countries to explore and exploit digital financial services. In particular, SMEs that endeavor to incorporate digital financial services into their business will end up creating value, gaining operational efficiency, and gaining a financial advantage leading to better performance (Choi et al., Citation2020; Martín-Peña et al., Citation2019; Martínez-Caro et al., Citation2020). More specifically, digital financial services enable SMEs to minimize transaction costs, such as money transfers, utility bill payments, and supplier and customer coordination (Aron, Citation2018; Nan et al., Citation2021), thereby increasing the availability of funds for business operations (Konte & Tetteh, Citation2023). Digital financial services facilitate an increase in sales turnover, sales income, and profits (Akyoo & Sife, Citation2015; Kirui & Onyuma, Citation2015), as well as business expansion for SMEs (Bosire & Ntale, Citation2018; Nan et al., Citation2021). Digital financial services can provide SMEs with the digital capabilities to enhance the responsiveness of their logistics (Nan et al., Citation2021), enhance the agility of the procurement process (Nan & Park, Citation2022), and improve the overall supply chain efficiency (Horne et al., Citation2015), which ultimately leads to improved SME performance (Choi et al., Citation2020; Martín-Peña et al., Citation2019; Martínez-Caro et al., Citation2020; Nan & Park, Citation2022). Despite the benefits and the extensive usage of digital financial services, there is a dearth of literature and empirical support for the role of digital financial services during the era of crisis in developing countries, which have already been plagued by undeveloped financial infrastructure. In particular, Nan et al. (Citation2021) argued that, while the literature has helped us grasp the benefits of digital financial services for SMEs in normal times, it owes us further investigation into the function and impact of digital financial services during times of economic uncertainty.

Further, for SMES to be competitive in a changing market environment, there’s a need to develop specific capabilities (Teece et al., Citation1997), as a lack of dynamic capability could render SMEs uncompetitive, particularly in a changing environment (Alcalde Calonge et al., Citation2022; Gnizy et al., Citation2014). SMEs can generate value and revenue through the use of digital technology. In line with this, digital financial services (such as mobile money and QR code) as capabilities of SMEs could position SMEs in developing economies to better serve a wide range of customers, especially with the restrictions that follow the COVID-19 pandemic, and ultimately achieve better performance. Implacably, SMEs can achieve an advantage over larger firms by utilizing operating processes and available specialized resources that can be tailored for specific customers’ needs and markets (Zahoor et al., Citation2023). Therefore, SMEs need to invest heavily in the development of dynamic capabilities (Cheng & Chen, Citation2013), since innovation is a strong support for ensuring their competitiveness (Ferreira et al., Citation2020; J. S. Wang, Citation2017). However, despite the fact that SMEs play a significant role in the growth and development of national economies, little emphasis has been paid to the capacity of SMEs to develop self-help strategies for establishing competitive advantage (Akenroye et al., Citation2020). It is worth noting that, despite the existence of an institutional framework and policy interventions to support innovation and enhance the growth and performance of SMEs, there is a rather high rate of persistent failure among SMEs, and SMEs are facing problems especially during the pandemic era (Amoah et al., Citation2020, Citation2020; Donkor et al., Citation2018; Martín-Peña et al., Citation2019). Moreover, while several other recent studies have used the technology acceptance model to examine human interaction with technology, the use of mobile money and QR code as capabilities by SMEs to achieve better performance, especially during crisis times, has received negligible attention in the literature. At best, studies such as Asnakew (Citation2020) and Okocha and Awele Adibi (Citation2020) concentrate on mobile banking technologies for business executives and consumers of formal banking products, with no regard to the use of mobile money and QR code systems as financial tools in business that could influence firm performance, despite the prospects associated with the use of mobile money and QR code systems.

Also, when it comes to digital financial services, previous literature pays more attention to mobile money payment (Bosire & Ntale, Citation2018; David-West et al., Citation2018; De Luna et al., Citation2019; Islam et al., Citation2018; Lorenz & Pommet, Citation2021; Patnam et al., Citation2020) and ignores another leading form of payment through the QR code (Gao et al., Citation2018; Liu et al., Citation2021; Yan et al., Citation2021); Thus, not much study has been conducted in this field of research concerning QR code especially in developing countries like Ghana. The QR code system in developing countries has not been embraced extensively as compared to mobile money. The knowledge gap between mobile money and QR code systems is perceived as being extensively huge, so it is not uncommon to find even educated people in developing countries having only a little or no knowledge about QR code systems. Just as QR code systems have not been extensively materialized in developing countries, the use of QR code systems for making payment has also not been extensively recognized as compared to mobile money services. This could be attributed to the low awareness level of the system, making it plausible for the QR code system to receive academic attention in developing countries like Ghana. Consequently, the study seeks to answer the question: to what extent do digital financial services (QR code and mobile money) influence the performance of SMEs under the boundary condition of dynamic capability?

This paper contributes to the literature on the nexus between digital financial services such as the QR code system and the performance of SMEs. Firstly, this present study extends the literature on the relationship between digital services and firm performance by exploring the unique role of dynamic capabilities in the digital payment platform and firm performance nexus. Notably, research linking a firm’s digital services and dynamic capabilities to the performance of SMEs is scarce. QR code as a payment service is in the early stages of implementation in Ghana, thereby making this study one of the crème de la crème studies on the subject and making a novel contribution to the literature. Lastly, the COVID-19 pandemic has therefore stressed the role of digital financial services, which has been weakly examined in the literature, especially in the context of developing countries. The study therefore contributes significantly to the literature by highlighting the important role of digital financial services during the COVID-19 pandemic era, especially in the context of SMEs in developing nations.

The remaining sections are as follows: literature review and hypothesis development that entails a theoretical review, digital financial services, hypothesis formulation, and the conceptual framework of the study. The subsequent sections are method and material, result, discussion, and conclusion of the study.

2. Literature review and hypothesis development

2.1. Theoretical framework

The study was underpinned by the theory of dynamic capabilities. Dynamic capabilities are the competencies that assist in adapting, integrating, and reconfiguring internal and external resources and skills to a changing environment (Alcalde Calonge et al., Citation2022; Teece et al., Citation1997). Adaptability, learning, and creativity are the most common manifestations of these DCs (Alcalde Calonge et al., Citation2022). The process and conventional perspective confirm that dynamic capabilities as part of the social organization learning process are uniquely determined by the unique history of each company, which brings specific knowledge and traditions to each organization that cannot be easily replicated (Zollo & Winter, Citation2002). For SMES to be competitive in the market, there’s a need to develop specific capabilities and engage in continuous learning, especially in a new or changing market environment (Teece et al., Citation1997; Zott, Citation2003). This means that a lack of dynamic capability could render SMEs uncompetitive, particularly in a changing environment (Gnizy et al., Citation2014). Small- and medium-sized enterprises (SMEs) can generate value and revenue through the use of digital technology. In line with this, the study conceptualized mobile money and QR codes as capabilities of SMEs that could position SMEs to better serve a wide range of customers, especially with the restrictions that follow the COVID-19 pandemic, and ultimately achieve better performance. For example, by replacing the reliance on paper forms and switching to digital financial services, SMEs can improve the overall user experience, increase customer satisfaction or loyalty, and ultimately improve firm performance. More so for SMEs, reliance on digital financial services will lead to cost savings, a faster time to market, increased efficiency, increased transparency, and full auditing capabilities, along with a high level of customer service, especially during a crisis. Again, these tools enable SMEs to ensure operational efficiency, minimize transaction costs, including money transfers, utility bill payments, employee payroll, and supplier and customer coordination (Aron, Citation2018; Nan et al., Citation2021), and increase funds availability for successful and smooth business operations (Konte & Tetteh, Citation2023). Implacably, SMEs can achieve an advantage over larger firms by utilizing operating processes and available specialized resources that can be tailored for specific customers’ needs and markets (Zahoor et al., Citation2023). Therefore, SMEs need to invest heavily in the development of dynamic capabilities (Cheng & Chen, Citation2013), since innovation is a strong support for ensuring a SME’s competitiveness (Ferreira et al., Citation2020; J. S. Wang, Citation2017).

2.2. QR code and mobile money

A digital financial service is an electronic transmission of information, including data and content, from multiple platforms and devices, such as the web and mobile, for financial transactions (Romdhane et al., Citation2020). The digital financial services considered in this study were mobile money and quick response (QR) Code. The term “mobile money” (MM) refers to a type of digital innovation that combines two previously separate fields: mobile phone technology and microfinance for assessing financial services (Nan et al., Citation2021). Mobile money service allows people to transfer funds between banks or accounts, deposit or withdraw funds, or pay bills by using a mobile phone (Gosavi, Citation2018; Kante & Kante, Citation2021; Romdhane et al., Citation2020), thereby reducing the amount of cash held for transactions. Mobile money services have been widely recognized in Ghana as they are spread across the length and breadth of the country. According to the payment system statistics of the Bank of Ghana (2019), “mobile money accounts for a total value of all transactions reaching $46 billion in 2018, representing 69% of nominal GDP in the same fiscal year”. The use of mobile money service as a financial tool, combined with its ease and flexibility, is seen as an enabler for its widespread acceptance in Ghana. As such, it is not uncommon to find mobile money service providers on every corner of the street, rendering financial services to the people (Amoah et al., Citation2020). Anticipating the opportunities that can be derived from this widely accepted mobile money service, banks have even now teamed up with mobile money service providers and pay interest on deposits and grant loans based on financial transactions in mobile money accounts (Gosavi, Citation2018) (MTN Ghana’s, Citation2020). annual report suggests that total revenue of GH 1.3 billion was realized in the year 2020 (MTN Ghana, Citation2020). This clearly shows the extent to which people are patronizing their mobile money services in Ghana.

A QR code is a type of matrix barcode (or two-dimensional code) that is much faster than traditional Universal Product Code (UPC) barcodes. A QR code is also known as a mobile barcode, as it can be scanned and read by a QR-Code reader, software that is installed on a mobile phone (Gao et al., Citation2018; Lorenzi et al., Citation2014). The main focus of the QR code in this study is on its use as a means of making payment. QR code payment refers to the use of mobile devices to use QR code systems and technologies to make mobile payments for goods, services, and invoices (De Luna et al., Citation2019; Liu et al., Citation2021; Lou et al., Citation2017). The universal QR Code payment system allows a customer to make payment for goods and services to a merchant from a mobile wallet or a bank account directly from a mobile phone (Cheng & Chen, Citation2013; Liu et al., Citation2021; Lou et al., Citation2017). QR code systems of payment are expected to be initiated in Ghana in 2020, making Ghana among the first African countries to implement this remarkable digital technology as a way of moving to a cashless system and digitalizing the economy. As a result, its usage in Ghana is relatively low.

2.3. Digital financial services and SMEs performance

Firm performance is an important construct in strategic management research. In the past decades, firm performance was equated to organizational efficiency, which is the degree to which an organization accomplishes its objectives without requiring an excessive amount of effort from its employees (Taouab & Issor, Citation2019). Organizations began to explore alternative performance evaluation methods. It is of no doubt that the businesses of today’s world are moving towards digitalization, where individuals and corporate entities prefer to make use of digital technologies as a means of changing their business models by providing solutions that offer new revenue and value-adding opportunities to individuals and organizations. In line with this, there has been a gargantuan shift from a product-based economy to one based on services, specifically digital services (Pascual-Fernández et al., Citation2021; Williams et al., Citation2008). The digital revolution is thus transforming firms and changing the nature of work across all regions of the world, including in Sub-Saharan Africa (Choi et al., Citation2020). Digital service platforms are becoming widespread in all areas of society. This widespread use of digital services is a result of the prospects associated with them, which individuals and corporate entities are eager to take advantage of (Ruutu et al., Citation2017). The emergence of digital services facilitates essential changes in products, services, innovation processes, and business models (Sjödin et al., Citation2020). A digital service makes it possible for information to be provided in a way that is easy to use and understand and includes trading services that generally submit forms for processing. The transition from paper forms to digital services benefits both organizations and customers (Kafetzopoulos & Psomas, Citation2015; Nan et al., Citation2021).

Digitalization is positively related to firm performance (Martín-Peña et al., Citation2019). In particular, small and medium-sized enterprises (SMEs) can gain operational efficiency and a financial advantage through the use of digital financial services. For instance, for operational efficiency, these tools enable SMEs to minimize transaction costs, including money transfers, utility bill payments, employee payroll, and supplier and customer coordination (Aron, Citation2018; Nan et al., Citation2021), thereby increasing the availability of funds for business operations (Konte & Tetteh, Citation2023). As a result, organizations may be able to devote a greater proportion of their limited financial resources to investment and expansion, as cost reduction may result in enhanced liquidity (Islam et al., Citation2018). In addition, digital financial services can facilitate an increase in sales turnover, sales income, and profits (Akyoo & Sife, Citation2015; Kirui & Onyuma, Citation2015), as well as business expansion for SMEs (Bosire & Ntale, Citation2018; Nan et al., Citation2021). Moreover, digital financial services can provide SMEs with the digital capabilities to enhance the responsiveness of their logistics by allowing them to receive customer payments much more quickly (Nan et al., Citation2021) and by facilitating the secure instant transfer of funds to suppliers, thereby enhancing the agility of the procurement process (Nan & Park, Citation2022). Also, digital financial services facilitate the flow of materials and financial resources, accelerating the turnover from capital to inventory to receivables (Nan et al., Citation2021), thereby improving overall supply chain efficiency (Horne et al., Citation2015) and innovativeness (Lorenz & Pommet, Citation2021), which will ultimately lead to improved SME performance (Martínez-Caro et al., Citation2020; Nan & Park, Citation2022). Hence, SMEs that endeavor to incorporate digital financial services into their business end up creating value for themselves, leading to better performance. In line with this, there are some empirical studies that have demonstrated how digital financial services drive firm performance. For instance, Patnam et al. (Citation2020) conducted a study on the real effect of mobile money using data from firms in 643 districts in India and found that mobile money serves as a powerful mechanism to improve the efficiency of risk-sharing arrangements. The results further revealed that companies adopting the novel payment technology are improving their sales by about 26% compared to those that do not. The study therefore suggests that:

H1a:

Mobile money services have a significant positive effect on SME performance

H1b:

QR code mobile payment has a significant positive effect on SME performance

2.4. The moderating role of dynamic capability

Dynamic capability is the operational capability that includes organizational learning processes and routines rooted in innovation knowledge and involves the transformation of a company’s innovation knowledge resources and routines (Cheng & Chen, Citation2013). There is an increasing number of research studies that observe dynamic capabilities as being at the heart of organizational strategy, value creation, and competitive advantage (Alcalde Calonge et al., Citation2022; Dejardin et al., Citation2022; Teece et al., Citation1997). Dynamic capabilities are the ability of the organization to integrate, build, and reconfigure internal and external capabilities to respond to rapidly changing environments (Alcalde Calonge et al., Citation2022; Cheng & Chen, Citation2013; Teece et al., Citation1997; W. Wang et al., Citation2019). Dynamic capabilities reflect a firm’s ability to achieve creativity and innovative forms of competitive advantage under given path dependencies and market positions (Ferreira et al., Citation2020). Dynamic capabilities are the exceptional capabilities that are of value to customers, rare, and which competitors find difficult to imitate (Gicheru & Kariuki, Citation2019). These exceptional capabilities are necessary for firms to gain a sustained competitive advantage and ensure superior organizational performance (Dejardin et al., Citation2022; Ferreira et al., Citation2020; Gicheru & Kariuki, Citation2019; Teece et al., Citation1997). Capability enables the accumulation of the additional knowledge required to exploit any available information and also enables the firm to more effectively exploit opportunities to anticipate and outpace competitors’ competitive actions (Alcalde Calonge et al., Citation2022).

Dynamic capability is a key driver and a main source of competitiveness and competitive advantage, with a positive impact on firm performance and firm survival (Breznik & Hisrich, Citation2014; Ferreira & Coelho, Citation2020). Thus, dynamic capabilities are an important trait for business success. Therefore, SMEs with a high level of dynamic capabilities are able to realize new opportunities in a business environment and convert the resources of organizations into tangible and intangible assets and capabilities (Khalil & Belitski, Citation2020; Makkonen et al., Citation2014). Thus, SMEs that are capable of identifying new opportunities and taking advantage of them become well positioned to gain a competitive edge over non-capable SMEs (Dejardin et al., Citation2022; Ferreira & Coelho, Citation2020). SMEs that are innovative are better positioned to achieve optimal levels of productivity than static firms without any innovation (Ferreira et al., Citation2020; Teece et al., Citation1997). There is thus strong empirical evidence to support a positive appraisal of higher innovative capability leading to improved competitiveness and higher performance (Dejardin et al., Citation2022; Donkor et al., Citation2018; Ferreira & Coelho, Citation2020). For example, Ferreira et al. (Citation2020) conducted a study to assess the relationship between dynamic capabilities, competitive advantage, innovation capabilities, and firm performance and revealed that dynamic capabilities have a positive impact on competitive advantage and firm performance. Bouwman et al. (Citation2019) evaluated the relationship between digitalization, business innovative practices, and business performance using 321 European SMEs and revealed that innovation has a direct effect on firm performance. The study therefore suggests that:

H2:

Dynamic capability has a significant positive effect on SME performance

The usage of digital financial services is believed to potentially impact user satisfaction and firm performance; however, their interaction with SMEs’ abilities to identify new opportunities and their level of innovativeness is perceived as another direction through which firm performance can be attained. The study therefore postulates that the relationship between digital financial services and firm performance is contingent on SMEs’ level of dynamic capability. This is because dynamic capability identifies a firm’s ability to attain creativity and innovative forms of competitive advantage for identified dependencies and market positions (Ferreira et al., Citation2020), as having such dynamic capabilities is crucial to creating process innovations (Alcalde Calonge et al., Citation2022). Thus, the ability of firms to identify new opportunities and take advantage of them is very critical for business success. For example, Kafetzopoulos and Psomas (Citation2015) revealed that innovation capability as a dynamic capability directly impacts product quality and operational performance positively, while indirectly impacting financial performance through operational performance. Pascual-Fernández et al. (Citation2021) also revealed that dynamic capability contributes to financial performance directly and indirectly through customer equity. Implacably, the study suggests that in a dynamic environment such as the era of the COVID-19 pandemic, SMEs’ ability to capitalize on new opportunities in the usage of digital financial services such as QR code and mobile money offers potential benefits to such SMEs by achieving the needed performance under the firms’ dynamic capability. The implication is that when SMEs adopt a high level of innovative capabilities in their firm, they will be able to take advantage of the dynamic environment, thereby increasing performance significantly. Given the fact that technology is more of a means to an end (Orlikowski & Iacono, Citation2001), mobile money and QR code can be regarded as a set of tools through which SMEs can achieve stellar performance and competitive advantage when engineered with the SMEs’ dynamic capability. The study hypothesized that mobile money and QR code as tools would produce more effective performance outcomes for SMEs. As tools, mobile money and QR code can enhance productivity, reduce transaction costs, improve efficiency, and ultimately improve firm performance when coalesced with SMEs’ dynamic capabilities. The study proposes that:

H3a:

Dynamic capability moderates the mobile money services and SME performance nexus

H3b:

Dynamic capability moderates the QR code money payment and SME performance nexus

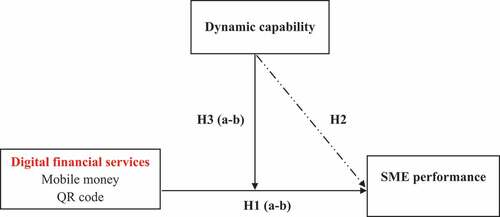

The study draws insight from dynamic capability theory (Teece et al., Citation1997) to establish a contingency effect of dynamic capabilities on the relationship between digital financial services (mobile money services and QR code payment) and the performance of SMEs, as demonstrated in Figure . In Figure , “a” (H1 and H3) and “b” (H1 and H3) refer to mobile money services and QR code payment, respectively.

Figure 1. The conceptual model.

3. Method and material

3.1. Data collection procedure

The study employs a survey research design method to assess the relationship between digital financial services, dynamic capability, and SME performance. The study’s population comprises SMEs in Kumasi, Ghana, that are making use of digital financial services (mobile money and QR code payment) in their business transactions. The data was collected from SMEs that have adopted mobile money and QR code modes of payment in Kumasi. Kumasi is noted for several SMEs and hence connotes a very large population of SMEs, which makes Kumasi an appropriate city for this study to be conducted. In terms of SME classification, it’s unclear what constitutes a small or medium-sized enterprise in Ghana because the term’s definition shifts over time and between different organizations. The following are the subcategories of SMEs as defined by the National Board for Small Scale Industries (NBSSI): Businesses are classified as either “micro” (with fewer than 5 employees), “small” (6–29), “medium” (30–99), or “large” (100+), with no more than $10,000 in fixed assets (not counting land and buildings). This definition has been considered for this study.

The respondents in these SMEs were members of top management and functional heads that had firsthand experience with the selected digital services. Thus, the purposive sampling technique used was to sample respondents from the SMEs who are capable of providing accurate responses to the questions and are in a managerial or top-level position in the organization to provide accurate responses to the questionnaire. The questionnaire was distributed to the respondents via email by the selected SMEs representatives. Each respondent was instructed to fill out the questionnaire and return it during the COVID-19 era (October to November, 2020). To increase the total response rate, each company was called as a reminder. 230 questionnaires were mailed to the sampled SMEs listed by the National Board of Small Scale Industries (NBSSI) using a simple random technique, and eventually 206 SMEs participated in the research. The study considered such a large sample size due to the fact that it was conducted at an early stage of QR code implementation and adoption. The SME types included in the study were heterogeneous SMES operating in the food and beverage, clothing and cosmetics, transportation, electrical, and pharmaceutical industries. The majority of the firms have been operating for 6 to 10 years.

3.2. Measure

The measurement instrument is developed after a review of the pertinent literature is conducted. The main variables of the study that the questions were set around are mobile money service, QR code usage, dynamic innovative capacity, and firm performance. The study adopted five items to measure mobile money service from Islam et al. (Citation2018). The study adopted five (5) items to measure QR code payment from Lou et al. (Citation2017). The study adopted five (5) items to measure dynamic capability from Janssen et al. (Citation2016). The study adopted twelve (12) items to measure organizational performance, adopted from Hooley et al. (Citation2005) and Vafaei-Zadeh et al. (Citation2020). Also, responses to various questions were scaled on a 7-point Likert scale from strongly disagree to strongly agree. The questionnaire is provided in Appendix 1.

4. Result

4.1. Reliability of measurement constructs

To ensure the measurement items’ internal consistency, an appropriate reliability test was performed using the Cronbach’s alpha statistic as proposed by Pallant and Bailey (Citation2005). The result of the reliability test is shown in Table . The results show that all the construct items had a Cronbach’s alpha value above 0.7, which confirms the internal consistency of the measured construct.

Table 1. Reliability test

4.2. Validity

Aside from the reliability test conducted, the study also performed an exploratory factor analysis (EFA) and a confirmatory factor analysis (CFA) to test the validity of the measured items. The Kaiser-Meyer-Olkin (KMO) and Bartlett’s test shows that the data collected for an exploratory factor analysis were appropriate as the Measure of Sampling Adequacy was above 0.6, i.e., 0.824 > 0.6, and the Bartlett’s Test of Sphericity of 1583.837 was statistically significant with a p-value of 0.000, signifying that the correlations between the items were sufficiently large. The study also did not have any issues with communalities, as all the measured items had extraction scores above 0.3. The exploratory factor analysis (EFA), together with the parallel analysis, maintained four (4) factors. These four factors explained 53.5% of the variance in the pattern of relationships among the items, with the first factor explaining 15.039% of the variation and the second factor explaining 14.808% of the variation.

Furthermore, the study proceeds to conduct confirmatory factor analysis (CFA) to determine the fitness model using the maximum likelihood presented in Table . It is expected that each construct’s factor loadings should be greater than or equal to the .50 criterion (Hair et al., Citation2020; Ledi et al., Citation2023). The loadings for all the measurement items were above the 0.5 threshold. Additionally, internal consistency was secured as the alpha scores of all the constructs were above the 0.7 threshold (Hair et al., Citation2020). The study also uses the average variance extracted to establish the convergence validity of the constructs. The study demonstrated convergence validity, as the AVE of all the constructs was above the 0.6 threshold (Fornell and Larcker, Citation1981). The model fit indices are as follows: CMIN = 576.862; DF = 318; CMIN/DF = 1.814; CFI = .915; GFI = .916; TLI = .895; RMSEA = .068. All these results confirm the validity of the measured items.

Table 2. Confirmatory factor analysis

4.3. Correlation analysis and discriminant validity test

The study also performed a correlation analysis and a discriminant validity test, and the results are presented in Table . The study revealed a significant positive relationship between mobile money service and firm performance (r = .516, p < .01) suggesting that mobile money service use and firm performance all change in the same direction. Similarly, the study further revealed a significant positive relationship between QR code payment service usage and firm performance (r = .302, p < .01) suggesting that QR code payment service usage and firm performance all change in the same direction. The study further revealed a significant positive relationship between dynamic capability and firm performance (r = .530, p < .01) suggesting that overall digital service usage and firm performance all change in the same direction. In addition, the study secured discriminant validity by comparing the square root of AVEs to intercorrelation scores. For discriminant validity to be achieved, it is expected that the square root of AVE is larger than the correlation coefficient of other constructs (Fornell and Larcker, Citation1981). The study achieves discriminant validity as the minimum AVE value of 0.646 was greater than the highest correlation score of 0.530.

Table 3. Correlation coefficients and discriminant validity

4.4. Hypothesis testing

This section starts by providing a descriptive analysis of the usage of mobile money and QR code. The respondents were asked to determine their level of mobile money usage, and the results revealed that all the respondents indicated that they are aware of mobile money services and use mobile money services as primary sources of financial tools. Aside from that, the respondents were further asked to indicate the frequency of using QR code payment, and it was found that 98 of them, representing 47.6% of them, use QR code payment on average, while the majority of 108, representing 52.4% of them, do not use QR code payment as a predominant digital financial service. Mobile money is therefore mostly used as compared to QR code payment, which is lightly used. It is worth mentioning that, unlike mobile money services, which are prevalently used as a digital financial service by SMEs in Ghana, QR code payment has not been extensively materialized in Ghana, and the use of QR code payment for making payments has also not been widely recognized as compared to mobile money services. The QR code system of payment was initiated in Ghana in 2020, making Ghana among the first African countries to implement this remarkable digital technology as a way of moving to a cashless system and digitalizing the economy. More so, the correlation score of .188 in Table indicates that mobile money and QR code can coexist and are capable of being utilized as complementary digital financial services. This is consistent with the study by Konte and Tetteh (Citation2023), who found that a combination of access to traditional financial services and mobile money leads to improvements in the productivity of SMEs.

The regression results in Table shows that mobile money usage predicts SMEs performance. The regression coefficient (β = 0.426) with a significant p-value of < .05 means that there is a significant and positive effect of mobile money usage on SMEs performance, suggesting that a one-unit increase in the level of mobile money usage will significantly yield a 42.6% increment in SMEs performance. This implies that mobile money usage has a major impact on the performance of the SMEs used in the study. Also, the R-square (R2 = 0.266) suggests that mobile money usage explains 26.9% of the variation in SMEs performance. The significant and positive relationship between mobile money usage and SMEs performance means hypothesis one (H1a) is supported. The regression coefficient (β = 0.259) with a significant p-value of < .05 means that there is a significant and positive effect of QR code payment on SMEs performance, suggesting that a one-unit increase in the level of QR code payment will significantly yield a 25.9% increment in SMEs performance. This implies that QR code payments have a significant impact on the performance of the SMEs used in the study. This significant and positive relationship between QR code payment and SMEs performance means hypothesis one (H1b) is supported. The regression coefficient (β = 0.427) with a significant p-value of < .05 means that there is a significant and positive effect of dynamic capabilities on SMEs performance, suggesting that a one unit increase in the level of dynamic capabilities will significantly yield a 42.7% increment in SMEs performance, supporting Hypothesis two (H2).

Table 4. Hypothesis testing

In order to determine the moderation role of dynamic capabilities on the relationship between digital service (mobile money usage and QR code payment), a regression model was run using SPSS with digital financial service (mobile money usage and QR code payment) as independent variables, dynamic capabilities as a moderating variable, and firm performance as a dependent variable, with the result presented in Table . Model 1 tests the effect of the independent variable (mobile money usage and QR code payment) and moderating variable (dynamic capabilities) on the dependent variable (firm performance). The Model 2 mainly tests the interaction effect of digital financial services and their dynamic capability on firm performance. From the model 2, the interaction effect of mobile money usage and dynamic capability had a significant effect on firm performance (β = 0.125; t = 2.425). This implies that dynamic capabilities significantly interact with mobile money usage to impact firm performance. Thus, hypothesis three (H3a) is supported. The conditional effect of the Hayes Process Macro further revealed that the moderation is at statistically significant high levels of dynamic capabilities. This interactive was possible because SMEs are in a better position to leverage any advantages, especially during a crisis era, stemming from their smaller size (unlike larger firms), nimble structures, and less formal environments (Wiklund et al., Citation2009), as well as the capability to make quick strategic decisions (Zahoor et al., Citation2023), such as the tendency to quickly introduce and utilize these tools during the COVID-19 pandemic. Mobile money can therefore be regarded as a tool through which SMEs can achieve stellar performance and a competitive advantage when engineered with their dynamic capabilities. The diagrammatic illustration of the interactive effect is presented in Figure .

Figure 2. Moderating of dynamic capabilities.

Table 5. Path analysis of dynamic capabilities

However, the moderating role of dynamic capabilities on the relationship between QR code payment and firm performance was not statistically significant as indicated by the regression coefficient (β = − 0.053; t = − 1.142). This insignificant moderating role of dynamic capabilities on the relationship between QR code payment and firm performance means hypothesis three (H3b) is not supported. The diagrammatic illustration of the outcomes of the results of the hypotheses paths is presented in Figure .

Figure 3. Conceptual model.

5. Discussion

A growing number of companies are rethinking their business models in light of new technologies such as digital technology (Antonucci et al., Citation2020), hence generating a growing interest in digital technology and digital platforms (Abdulkader et al., Citation2020; Ferreira et al., Citation2020; Hoch & Brad, Citation2021; Patnam et al., Citation2020). The paper examines the effect of digital financial services (QR code and mobile money payment platform) on the performance of SMEs with the moderating role of dynamic capability. The study found that mobile money and QR code payments have a significant and positive impact on firm performance. Thus, any attempt to improve QR code payment and mobile money usage in the firm will significantly improve firm performance. This is because customers may find it more convenient to make payment for purchased items using their cell phones or by just scanning the QR code rather than having to carry money with them before they can make payment for purchased items, as carrying money comes with its own risks, which may ultimately improve business transactions and customer satisfaction. This finding is supported by the study of Patnam et al. (Citation2020), who found that mobile money serves as a powerful mechanism to improve the efficiency of risk-sharing arrangements. Lou et al. (Citation2017) also revealed that current usage of QR code payments has a positive effect on transaction satisfaction, and the use of QR code payment technology can therefore be used to promote business.

The study further found that dynamic capabilities have a significant and positive impact on firm performance. This finding is in line with that of Ferreira et al. (Citation2020), whose study revealed that capabilities have a positive impact on competitive advantage and also a positive impact on firm performance. The study also revealed that, on the part of mobile money usage, dynamic capabilities significantly moderated the relationship between mobile money usage and firm performance. Hence, SMEs are encouraged to build on their level of dynamic capabilities. The moderating role of dynamic capabilities on the relationship between QR code payment and firm performance was not statistically significant. This could be because the level of usage of QR code payment is very low and hence may not have any significant impact in conjunction with dynamic capabilities.

The study found that digital financial services (mobile money usage and QR code payment) both have a significant and positive impact on firm performance. The implication of these findings is that it is worth adopting digital services (mobile money and QR code payment) for business transactions. Thus, improvement in the level of innovativeness in such a dynamic business environment will significantly improve firm performance. This positive effect is because such firms are able to acquire new important product information, respond to new product changes, master the products conditions, and identify new product opportunities ahead of their competitors, who may find it difficult to establish them. This will help make the firm more robust and help them adjust themselves to the dynamics of the business environment. In this way, they will be able to increase their market share, return on investment, increase sales, meet the preferences of customers, and achieve operational efficiency. Furthermore, SMEs should develop strategies to maximize their use so as to continuously improve performance. Even though QR code were less commonly used as a payment medium, their positive impact on performance was still statistically significant. Implacably, the management of SMEs should tap the full potential of QR code by increasing their adoption in their firms. Moreover, it is essential for SMEs to develop and improve their dynamic capabilities, as the study identified them as having a significant impact on firm performance. This can be achieved by responding to new product changes, acquiring important new product information, mastering the conditions of new products, and identifying new product opportunities. This is because innovative business models that leverage digital technology may enhance a company’s competitive position via its products and services (Hoch & Brad, Citation2021; Lou et al., Citation2017). SMEs should pay close attention to the factors that improve the digital financial services platform, particularly in relation to what customers want or require from the platform. This will increase the convenience and speed of usage to maximize market appeal and help small and medium-sized enterprises compete on the market.

For its theoretical implication, this study makes several noteworthy contributions to literature. First, this study extends our knowledge on the relationship between digital financial services and firm performance by exploring the unique role of dynamic capabilities in the digital financial services and firm performance nexus. Notably, research linking a firm’s digital financial services and dynamic capabilities to the performance of SMEs is scarce, especially during the COVID-19 pandemic era. QR code as a payment service is at the early stage of implementation in Ghana, thereby making this study one of the crème de la crème studies on the subject and making a novel contribution to the literature. This study contributes to existing knowledge by providing empirical evidence that digital financial services (mobile money service usage and QR code payment services) have a significant positive impact on firm performance. Secondly, this study has also broadened understanding of the moderating role of dynamic capabilities on digital financial services and firm performance. Lastly, the worldwide COVID-19 pandemic has disrupted work environments, and the sudden and widespread closures of borders, businesses, and public places, as well as the imposition of travel restrictions, have compelled SMEs to adapt seamlessly to digital working platforms. The COVID-19 pandemic has therefore stressed the role of digital financial services, which has been weakly examined in the literature, especially in the context of developing countries. The study therefore contributes significantly to the literature by highlighting the important role of digital financial services during the COVID-19 pandemic era, especially in the context of SMEs in developing nations.

6. Conclusion

The study found that mobile money and QR code payments have a significant and positive impact on firm performance, with dynamic capability playing a vital interactive role in this relationship. Organizations depend on simultaneously exploiting existing technologies and resources to secure efficiency and create value during the pandemic era. Organizations with a high level of dynamic capabilities are able to realize new opportunities in a business environment and convert their resources into tangible and intangible assets and capabilities. Therefore, by developing specific capabilities such as being open to QR code, SMES can remain competitive in the market, as the dynamic capability theory admonishes. It is worth noting that the business value of digitalization encompasses not only the integration of new digital technologies into the existing infrastructure but also how these new technologies may be utilized to improve company processes and produce business value. SMEs need to invest heavily in the development of dynamic capabilities as it has a massive influence on the performance of an organization, and they must systematically manage their company processes to maximize the full possibilities of these new technologies.

For the limitation of the study, the study was conducted at the early stage of QR code adoption, therefore the sample size was quite small, thereby creating less impetus for generalizations; further studies should consider a large sample for effective generalizations. This study focused on a relatively small sample size in Ghana, which limits its generalization to other areas in other cities of the country. It is therefore recommended for future researchers to widen the scope of the study to include several other cities as well as large firms so as to strengthen the generalization of findings as more and more companies are adopting QR code as a mode of payment over the past few years. Moreover, the study again did not consider certain variables that could have been used as either a mediating or moderating variable in the model, such as competitive advantage and customer satisfaction. Future researchers are encouraged to stand on these limitations and perform similar studies by introducing the identified mediating and/or moderating variables. A future study could also consider financial inclusiveness, especially for female entrepreneurs in rural areas, as well as the adoption of QR code as digital financial services by female entrepreneurs in rural areas, which would be beneficial to the literature. Lastly, future studies could consider the potential relation between mobile money and QR code, as mobile money and QR code can coexist and are capable of being utilized as complementary digital financial services.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Abdulkader, B., Magni, D., Cillo, V., Papa, A., & Micera, R. (2020). Aligning firm’s value system and open innovation: A new framework of business process management beyond the business model innovation. Business Process Management Journal. https://doi.org/10.1108/BPMJ-05-2020-0231

- Akenroye, T. O., Owens, J. D., Elbaz, J., & Durowoju, O. A. (2020). Dynamic capabilities for SME participation in public procurement. Business Process Management Journal, 26(4), 857–19. https://doi.org/10.1108/BPMJ-10-2019-0447

- Akyoo, S. E., & Sife, A. S. (2015). Mobile money services and the performance of microenterprises in Moshi District, Tanzania. African Journal of Finance and Management, 24(1–2), 42–50.

- Alam, M. M., Awawdeh, A. E., & Muhamad, A. I. B. (2021). Using e-wallet for business process development: Challenges and prospects in Malaysia. Business Process Management Journal, 27(4), 1142–1162. https://doi.org/10.1108/BPMJ-11-2020-0528

- Alcalde Calonge, A., Ruiz-Palomino, P., & Sáez-Martínez, F. J. (2022). The circularity of the business model and the performance of bioeconomy firms: An interactionist business-environment model. Cogent Business & Management, 9(1), 2140745. https://doi.org/10.1080/23311975.2022.2140745

- Amoah, A., Korle, K., & Asiama, R. K. (2020). Mobile money as a financial inclusion instrument: What are the determinants? International Journal of Social Economics, 47(10), 1283–1297. https://doi.org/10.1108/IJSE-05-2020-0271

- Antonucci, Y. L., Fortune, A., & Kirchmer, M. (2020). An examination of associations between business process management capabilities and the benefits of digitalization: All capabilities are not equal. Business Process Management Journal, 27(1), 124–144. https://doi.org/10.1108/BPMJ-02-2020-0079

- Aron, J. (2018). Mobile money and the economy: A review of the evidence. The World Bank Research Observer, 33(2), 135–188. https://doi.org/10.1093/wbro/lky001

- Asnakew, Z. S. (2020). Customers’ continuance intention to use mobile banking: Development and testing of an integrated model. The Review of Socionetwork Strategies, 14(1), 123–146. https://doi.org/10.1007/s12626-020-00060-7

- Bosire, J. M., & Ntale, J. F. (2018). Effect of mobile money transfer services on the growth of small and medium enterprises in informal sector of Nairobi County, Kenya. International Journal of Information Research and Review, 5(3), 5326–5333.

- Bouwman, H., Nikou, S., & de Reuver, M. (2019). Digitalization, business models, and SMEs: How do business model innovation practices improve performance of digitalizing SMEs? Telecommunications Policy, 43(9), 101828. https://doi.org/10.1016/j.telpol.2019.101828

- Breznik, L., & Hisrich, R. D. (2014). Dynamic capabilities vs. innovation capability: Are they related? Journal of Small Business and Enterprise Development, 21(3), 368–384. https://doi.org/10.1108/JSBED-02-2014-0018

- Chauvet, L., & Jacolin, L. (2017). Financial inclusion, bank concentration, and firm performance. World Development, 97, 1–13. https://doi.org/10.1016/j.worlddev.2017.03.018

- Cheng, C. C., & Chen, J. S. (2013). Breakthrough innovation: The roles of dynamic innovation capabilities and open innovation activities. Journal of Business & Industrial Marketing, 28(5), 444–454. https://doi.org/10.1108/08858621311330281

- Choi, J., Dutz, M. A., & Usman, Z., (Eds.) (2020). The future of work in Africa: Harnessing the potential of digital technologies for all. World Bank Publications. https://doi.org/10.1596/978-1-4648-1445-7

- David-West, O., Umukoro, I. O., & Muritala, O. (2018). Adoption and use of mobile money services in Nigeria. In Encyclopedia of information science and technology (4th ed., pp. 2724–2738). IGI Global.

- Dejardin, M., Raposo, M. L., Ferreira, J. J., Fernandes, C. I., Veiga, P. M., & Farinha, L. (2022). The impact of dynamic capabilities on SME performance during COVID-19. Review of Managerial Science, 17(5), 1–27. https://doi.org/10.1007/s11846-022-00569-x

- De Luna, I. R., Liébana-Cabanillas, F., Sánchez-Fernández, J., & Muñoz-Leiva, F. (2019). Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technological Forecasting and Social Change, 146, 931–944. https://doi.org/10.1016/j.techfore.2018.09.018

- Demirguc-Kunt, A., Klapper, L., Singer, D., & Ansar, S. (2018). The global findex database 2017: Measuring financial inclusion and the fintech revolution. World Bank Publications. https://doi.org/10.1596/978-1-4648-1259-0

- Donkor, J., Donkor, G. N. A., Kankam-Kwarteng, C., & Aidoo, E. (2018). Innovative capability, strategic goals and financial performance of SMEs in Ghana. Asia Pacific Journal of Innovation and Entrepreneurship, 12(2), 238–254. https://doi.org/10.1108/APJIE-10-2017-0033

- Ferreira, J., & Coelho, A. (2020). Dynamic capabilities, innovation and branding capabilities and their impact on competitive advantage and SME’s performance in Portugal: The moderating effects of entrepreneurial orientation. International Journal of Innovation Science, 12(3), 255–286. https://doi.org/10.1108/IJIS-10-2018-0108

- Ferreira, J., Coelho, A., & Moutinho, L. (2020). Dynamic capabilities, creativity and innovation capability and their impact on competitive advantage and firm performance: The moderating role of entrepreneurial orientation. Technovation, 92, 102061. https://doi.org/10.1016/j.technovation.2018.11.004

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 181, 39–50.

- Gao, S., Yang, X., Guo, H., & Jing, J. (2018). An empirical study on users’ continuous usage intention of QR code mobile payment services in China. International Journal of E-Adoption (IJEA), 10(1), 18–33. https://doi.org/10.4018/IJEA.2018010102

- Gicheru, J., & Kariuki, P. (2019). Influence of dynamic capabilities on performance of commercial banks in Kenya. Strategic Journal of Business & Change Management, 6(2), 1732–1745.

- Gnizy, I., Baker, W. E., & Grinstein, A. (2014). Proactive learning culture: A dynamic capability and key success factor for SMEs entering foreign markets. International Marketing Review, 31(5), 477–505. https://doi.org/10.1108/IMR-10-2013-0246

- Gosavi, A. (2018). Can mobile money help firms mitigate the problem of access to finance in Eastern sub-Saharan Africa? Journal of African Business, 19(3), 343–360. https://doi.org/10.1080/15228916.2017.1396791

- Hair, J. F., Jr., Howard, M. C., & Nitzl, C. (2020). Assessing measurement model quality in PLS-SEM using confirmatory composite analysis. Journal of Business Research, 109, 101–110.

- Hoch, N. B., & Brad, S. (2021). Managing business model innovation: An innovative approach towards designing a digital ecosystem and multi-sided platform. Business Process Management Journal, 27(2), 415–438. https://doi.org/10.1108/BPMJ-01-2020-0017

- Hooley, G. J., Greenley, G. E., Cadogan, J. W., & Fahy, J. (2005). The performance impact of marketing resources. Journal of Business Research, 58(1), 18–27. https://doi.org/10.1016/S0148-2963(03)00109-7

- Horne, D. R., Nickerson, D., & DeFanti, M. (2015). Improving supply chain efficiency through electronic payments: The case of micro-entrepreneurs in Kenya and Tanzania. Journal of Marketing Channels, 22(2), 83–92. https://doi.org/10.1080/1046669X.2015.1018074

- Islam, A., Muzi, S., & Rodriguez Meza, J. L. (2018). Does mobile money use increase firms’ investment? Evidence from enterprise surveys in Kenya, Uganda, and Tanzania. Small Business Economics, 51(3), 687–708. https://doi.org/10.1007/s11187-017-9951-x

- Janssen, M. J., Castaldi, C., & Alexiev, A. (2016). Dynamic capabilities for service innovation: Conceptualization and measurement. R&D Management, 46(4), 797–811. https://doi.org/10.1111/radm.12147

- Kafetzopoulos, D., & Psomas, E. (2015). The impact of innovation capability on the performance of manufacturing companies: The Greek case. Journal of Manufacturing Technology Management, 26(1), 104–130. https://doi.org/10.1108/JMTM-12-2012-0117

- Kante, M., & Kante, M. (2021). A stakeholder’s analysis of the effect of mobile money in developing countries: Thecase of orange money in Mali. In Perspectives on ICT4D and socio-economic growth opportunities in developing countries (pp. 224–251). IGI Global. https://doi.org/10.4018/978-1-7998-2983-6.ch009

- Kazan, E., Tan, C. W., Lim, E. T., Sørensen, C., & Damsgaard, J. (2018). Disentangling digital platform competition: The case of UK mobile payment platforms. Journal of Management Information Systems, 35(1), 180–219. https://doi.org/10.1080/07421222.2018.1440772

- Khalil, S., & Belitski, M. (2020). Dynamic capabilities for firm performance under the information technology governance framework. European Business Review, 32(2), 129–157. https://doi.org/10.1108/EBR-05-2018-0102

- Kirui, R. K., & Onyuma, S. O. (2015). Role of mobile money transactions on revenue of microbusiness in Kenya. European Journal of Business and Management, 7(36), 63–67.

- Konte, M., & Tetteh, G. K. (2023). Mobile money, traditional financial services and firm productivity in Africa. Small Business Economics, 60(2), 745–769. https://doi.org/10.1007/s11187-022-00613-w

- Ledi, K. K., & Ameza–Xemalordzo, E. (2023). Rippling effect of corporate governance and corporate social responsibility synergy on firm performance: The mediating role of corporate image. Cogent Business & Management, 10(2), 2210353.

- Liu, R., Wu, J., & Yu-Buck, G. F. (2021). The influence of mobile QR code payment on payment pleasure: Evidence from China. International Journal of Bank Marketing, 39(2), 337–356. https://doi.org/10.1108/IJBM-11-2020-0574

- Lorenzi, D., Vaidya, J., Chun, S., Shafiq, B., & Atluri, V. (2014). Enhancing the government service experience through QR codes on mobile platforms. Government Information Quarterly, 31(1), 6–16. https://doi.org/10.1016/j.giq.2013.05.025

- Lorenz, E., & Pommet, S. (2021). Mobile money, inclusive finance and enterprise innovativeness: An analysis of East African nations. Industry and Innovation, 28(2), 136–159. https://doi.org/10.1080/13662716.2020.1774867

- Lou, L., Tian, Z., & Koh, J. (2017). Tourist satisfaction enhancement using mobile QR code payment: An empirical investigation. Sustainability, 9(7), 1186. https://doi.org/10.3390/su9071186

- Makkonen, H., Pohjola, M., Olkkonen, R., & Koponen, A. (2014). Dynamic capabilities and firm performance in a financial crisis. Journal of Business Research, 67(1), 2707–2719. https://doi.org/10.1016/j.jbusres.2013.03.020

- Martínez-Caro, E., Cegarra-Navarro, J. G., & Alfonso-Ruiz, F. J. (2020). Digital technologies and firm performance: The role of digital organisational culture. Technological Forecasting and Social Change, 154, 119962. https://doi.org/10.1016/j.techfore.2020.119962

- Martín-Peña, M. L., Sánchez-López, J. M., & Díaz-Garrido, E. (2019). Servitization and digitalization in manufacturing: The influence on firm performance. Journal of Business & Industrial Marketing, 35(3), 564–574. https://doi.org/10.1108/JBIM-12-2018-0400

- MTN Ghana. 2020. Scancom PLC (MTN Ghana) (2020) annual report. Retrieved from https://mtn.com.gh/wp-content/uploads/2021/05/MTNGH-2020-Annual-Report.pdf

- Nan, W., & Park, M. (2022). Improving the resilience of SMEs in times of crisis: The impact of mobile money amid Covid‐19 in Zambia. Journal of International Development, 34(4), 697–714. https://doi.org/10.1002/jid.3596

- Nan, W., Zhu, X., & Lynne Markus, M. (2021). What we know and don’t know about the socioeconomic impacts of mobile money in Sub‐Saharan Africa: A systematic literature review. Electronic Journal of Information Systems in Developing Countries, 87(2), e12155. https://doi.org/10.1002/isd2.12155

- Okocha, F. O., & Awele Adibi, V. (2020). Mobile banking adoption by business executives in Nigeria. African Journal of Science, Technology, Innovation & Development, 12(7), 847–854. https://doi.org/10.1080/20421338.2020.1727107

- Orlikowski, W. J., & Iacono, C. S. (2001). Research commentary: Desperately seeking the “IT” in IT research—A call to theorizing the IT artifact. Information Systems Research, 12(2), 121–134. https://doi.org/10.1287/isre.12.2.121.9700

- Pallant, J. F., & Bailey, C. M. (2005). Assessment of the structure of the hospital anxiety and depression scale in musculoskeletal patients. Health and Quality of Life Outcomes, 3(1), 1–9. https://doi.org/10.1186/1477-7525-3-82

- Pascual-Fernández, P., Santos-Vijande, M. L., López-Sánchez, J. Á., & Molina, A. (2021). Key drivers of innovation capability in hotels: Implications on performance. International Journal of Hospitality Management, 94, 102825. https://doi.org/10.1016/j.ijhm.2020.102825

- Patnam, M., Yao, W., & Haksar, V. (2020). The real effects of mobile money: Evidence from a large-scale fintech expansion. IMF Working Papers, 2020(138), 1. https://doi.org/10.5089/9781513550244.001

- Romdhane, Y. B., Loukil, S., & Kammoun, S. (2020). Economic African development in the context of FinTech. In Employing recent technologies for improved digital governance (pp. 273–289). IGI Global.

- Ruutu, S., Casey, T., & Kotovirta, V. (2017). Development and competition of digital service platforms: A system dynamics approach. Technological Forecasting and Social Change, 117, 119–130. https://doi.org/10.1016/j.techfore.2016.12.011

- Sjödin, D., Parida, V., Kohtamäki, M., & Wincent, J. (2020). An agile co-creation process for digital servitization: A micro-service innovation approach. Journal of Business Research, 112, 478–491. https://doi.org/10.1016/j.jbusres.2020.01.009

- Taouab, O., & Issor, Z. (2019). Firm performance: Definition and measurement models. European Scientific Journal, ESJ, 15(1), 93–106. https://doi.org/10.19044/esj.2019.v15n1p93

- Teece, D. J., Pisano, G., & Shuen, A. (1997). Dynamic capabilities and strategic management. Strategic Management Journal, 18(7), 509–533. https://doi.org/10.1002/(SICI)1097-0266(199708)18:7<509:AID-SMJ882>3.0.CO;2-Z

- Vafaei-Zadeh, A., Ramayah, T., Hanifah, H., Kurnia, S., & Mahmud, I. (2020). Supply chain information integration and its impact on the operational performance of manufacturing firms in Malaysia. Information & Management, 57(8), 103386. https://doi.org/10.1016/j.im.2020.103386

- Wang, J. S. (2017). Theoretical connotation and dimension of dynamic management innovation capabilities. Logistics Engineering and Management, 39(2), 117–12.

- Wang, W., Cao, Q., Qin, L., Zhang, Y., Feng, T., & Feng, L. (2019). Uncertain environment, dynamic innovation capabilities and innovation strategies: A case study on Qihoo 360. Computers in Human Behavior, 95, 284–294. https://doi.org/10.1016/j.chb.2018.06.029

- Wiklund, J., Patzelt, H., & Shepherd, D. A. (2009). Building an integrative model of small business growth. Small Business Economics, 32(4), 351–374. https://doi.org/10.1007/s11187-007-9084-8

- Williams, K., Chatterjee, S., & Rossi, M. (2008). Design of emerging digital services: A taxonomy. European Journal of Information Systems, 17(5), 505–517. https://doi.org/10.1057/ejis.2008.38

- Yan, L. Y., Tan, G. W. H., Loh, X. M., Hew, J. J., & Ooi, K. B. (2021). QR code and mobile payment: The disruptive forces in retail. Journal of Retailing and Consumer Services, 58, 102300. https://doi.org/10.1016/j.jretconser.2020.102300

- Zahoor, N., Khan, H., Donbesuur, F., Khan, Z., & Rajwani, T. (2023). Grand challenges and emerging market small and medium enterprises: The role of strategic agility and gender diversity. Journal of Product Innovation Management. https://doi.org/10.1111/jpim.12661

- Zollo, M., & Winter, S. G. (2002). Deliberate learning and the evolution of dynamic capabilities. Organization Science, 13(3), 339–351. https://doi.org/10.1287/orsc.13.3.339.2780

- Zott, C. (2003). Dynamic capabilities and the emergence of intraindustry differential firm performance: Insights from a simulation study. Strategic Management Journal, 24(2), 97–125. https://doi.org/10.1002/smj.288

Appendix 1

Mobile Money

Our firm uses mobile money for financial transactions

Our firm uses mobile money to pay employees

Our firm uses mobile money to pay supplier

Our firm uses mobile money to pay utility bills

Our firm receive payments from customers through mobile money

Quick Response Code Payment

Our firm uses QR code payments to make payment for purchased items

Our firm receive money from my customers through QR code payment

Our firm uses QR code payments whenever possible in the business

Our firm uses QR code payments whenever appropriate to conduct payments

Our firm uses QR code payments frequently

Firm Performance

Our firm has stronger growth in sales revenue

Our firm is better able to acquire new customers

Our firm has a greater market share

Our firm able to increase sales to existing customers

Our firm is more profitable

Our firm is better able to reach financial goals

Our firm has improved in its customer service level.

Our firm has improved its overall product quality.

Our firm is able to minimize its cost of operation

Our firm has improved in delivery dependability.

Our firm has improved in its delivery speed.

Our firm is able to operate in high levels of flexibility

Dynamic Capabilities

Our firm is better at developing new ideas to help customers

Our firm is more able to fast track new offerings to customers

Our firm is better able to manage processes to keep costs down

Our firm is more able to package a total solution to solve customer problems

Our firm has a clear way of processing and developing ideas