Abstract

This study is carried out to investigate the impact of CSR activities on bank attractiveness in Vietnamese commercial banks. The data was collected from 1167 customers in Ho Chi Minh city. The independent variables were CSR for customers, CSR for employees, and CSR for social public welfare, while the dependent variable was bank attractiveness, and an intermediate variable was bank reputation. SmartPLS 3.0 software was used to process the model in two steps. The findings revealed that all three components of CSR had a direct effect on bank reputation, with CSR for social public welfare having the greatest influence. Bank attractiveness also had a significant impact on a bank’s reputation. CSR components all had an indirect impact on bank attractiveness via the mediated influence of reputation. Academically, the research findings indicate that CSR activities are now important in attracting customers for Vietnamese commercial banks. In practice, the findings assist bank administrators in recognizing the importance of factors in CSR activities and being proactive in implementing and formulating strategies.

1. Introduction

Commercial banks have an important role, so they always receive the attention of stakeholders such as customers, employees, and community (Diaconu & Oanea, Citation2015). These institutions are the main source of capital mobilization and distribution for most economies in the world (Serwadda, Citation2018). The previous study show that efficient and responsible banks could boost the overall economy (Demetriades et al., Citation2023). Commercial banks provide three main services include deposit mobilization, lending, and payment via accounts (Atta-Mensah & Dib, Citation2008). The bank’s operational efficiency is created by attracting many customers to use their services, so the attractiveness of the bank is one of the factors that created success in business (Suyanto, Citation2021).

Previous studies have shown that the attractiveness of banks was influenced by many different elements including corporate social responsibility (CSR) (Marin & Ruiz, Citation2007; Zhang et al., Citation2020). Corporate social responsibility is defined as a company’s commitment to contributing to long-term development. Through these activities, banks can improve the quality of life of employees, and the community, which benefits both the business as well as the overall development of society (Zheng et al., Citation2022). In particular, CSR activities are aimed at better things for customers, so they will attract more attention from customers (Zaid & Al-Manasra, Citation2013). Furthermore, a previous study had also shown that reputation had a mediating effect on the relationship between CSR and bank attractiveness (Zhang et al., Citation2020).

In Vietnam, the concept of corporate social responsibility had been around for a long time. However, there are significant differences in the implementation of CSR activities at commercial banks (Tien et al., Citation2020). CSR activities in Vietnam are mostly imported from other countries (Nguyen et al., Citation2018). From a legal standpoint, Vietnam has environmental, employee, and customer protection regulations, but these regulations are less stringent in comparison to developed countries (Nahar et al., Citation2021). As a result, some banks in Vietnam fail to take their social responsibility seriously (Ngoc, Citation2018). This is reflected in business fraud, financial statements, wage violations, insurance regimes, and employee occupational safety concerns (Phước Hương & Công Trực, Citation2021).

However, banks have seen the long-term benefits of corporate social responsibility (Ngoc, Citation2018). Banks have also realized the importance of CSR and started to implement it more deeply and widely (NGUYEN et al., Citation2022). CSR scores of banks have increased significantly in the last five years (Van et al., Citation2020). Research at banks shows that CSR had an impact on customer satisfaction and loyalty (Van et al., Citation2020).

Although previous studies have shown certain results, these studies still have limitations. First, most of these studies were conducted for a region (Zhang et al., Citation2020) or just research for a bank (Marin & Ruiz, Citation2007). Second, because the level of CSR implementation in each country was different, the assessment results and the implications of the solution cannot be generalized to other countries, especially Vietnam. Third, the level of awareness and interest of customers in each country was also different, so it was not possible to infer the results obtained from previous studies for other countries such as Vietnam. These are the research gaps. Therefore, more studies are still needed to contribute empirical results as well as academic contributions to this research topic.

The purpose of this study is to determine the influence of CSR activities on the attractiveness of banks under the mediation of reputation. The research is conducted through three sections including understanding the theories as well as related previous research documents and proposing a research model. Then, data is collected from the samples and processed. From there, the author proposes implications for solutions. Academically, the results show the relationship between CSR, bank reputation, and attractiveness in a developing country where there is a commercial banking system under the management of the government. Practically, the research help managers realize the importance of CSR in attracting customers to have strategic solutions in banking development.

2. Literature review

2.1. Stakeholder theory

Stakeholder theory was commonly used in research on sustainable development business management (Garvare & Johansson, Citation2010). Stakeholder theory focused on the interests of stakeholders. The theory is concerned with the demands that organizations or people connected to the company’s operations make on the company. The concept of stakeholder had been introduced in the area of Strategic Management. In a broad meaning, stakeholders were divided into two groups including those that influence and those affected by the achievements of the organization’s activities (Freeman & Reed, Citation1983). The benefit of the organizations should be aligned with the interests of the stakeholders. If the organization operates to meet the needs of the stakeholders, the business will develop sustainably (Garvare & Johansson, Citation2010).

The commercial bank was an organization specializing in the financial sector, which was highly competitive (Rashid et al., Citation2020). Bank operations were often associated with information asymmetry problems (Bugandwa et al., Citation2021). The higher the problem of information asymmetry banks had, the harder it was to meet stakeholder needs. CSR activities help convey the message of the bank’s operating point of view as well as its business ethics (Sobhani et al., Citation2021). This was considered an action that the bank used to guide investors to understand the views of managers about the future of the bank (LumbanGaol et al., Citation2021).

In this study, this theory provided a theoretical framework for solutions to increase the bank’s understanding and reputation of the bank’s existing activities to benefit customers through CSR activities. Research results in China had shown that through CSR activities, 51 organizations had improved their reputation, thereby increasing customer satisfaction and attracting more customers (Zhang et al., Citation2020). Research by Aktekin et al. (Citation2018) had shown that CSR activities in the United State help managers increase the attractiveness of the organization and mobilize more capital from new outside investors. Other research in the Lebanese banking sector showed that factors such as customer care, service quality, integrity, trust, and financial strength were factors that affected a bank’s reputation (El-Chaarani & El-Abiad, Citation2020). Besides, many scholars also showed that CSR was one of the innovative activities that help banks attract and retain customers Geng et al., Citation2022; Narteh & Braimah, Citation2020; Wu & Shen, Citation2013.

2.2. Corporate social responsibility

There were numerous interpretations of CSR, but it was clear that CSR refers to a company’s social responsibility. World Bank state that CSR was a business commitment that contributes to economic and social development (Chung et al., Citation2015). CSR was defined as an unspoken agreement between business and society, where organizations strive to make a favorable impression on stakeholders to reap potential benefits (Zaid & Al-Manasra, Citation2013). CSR was an essential element of corporate operation in which companies voluntarily contribute to society in terms of environmental, economic, and social investments, and ethics (Kanji & Chopra, Citation2010). This was a strategy domain for businesses in which trust could be built between society and business (Woo & Jin, Citation2016).

In the banking sector, CSR activities play an important role. Based on stakeholder theory, CSR reduced risks in the bank’s operations (Neitzert & Petras, Citation2022), and increased bank operational efficiency (Platonova et al., Citation2018). CSR activities imply that the bank provides high-quality service and attentive customer care. Customers had many choices for products with low service costs and commissions. Customer service was provided continuously. They were always respected, and complaints were resolved promptly (Osakwe et al., Citation2020). A previous study had shown that CSR also helps increase the competitiveness of banks (Gangi et al., Citation2018), and consumer behavior was influenced by CSR (Ajina et al., Citation2019).

CSR was divided into many different groups, but in general, there were at least three dimensions including CSR for social public welfare, CSR for customers, and CSR for employees (Geng et al., Citation2022). Tsang (Citation1998) defined CSR activities into three categories include CSR for employees, CSR for the environment, and CSR for community involvement. CSR disclosure by banks had been identified by Castelo Branco and Lima Rodrigues (Citation2006) through terms of environment, employees, products, consumers, and community involvement. CSR was described by McDonald and Rundle‐Thiele (Citation2008) as employee interests, employee support, products, overseas operations, effect on the environment, and community engagement.

2.3. Corporate social responsibility and bank reputation

Reputation was defined as recognition by a variety of groups. Reputation brings commercial benefits to companies (Barnett et al., Citation2006). Therefore, corporations always try to boost their reputational capital, which allowed them to build relationships and expanded their businesses (CHONG & Tan, Citation2010). In the banking section, reputation also brings many important benefits (Muflih, Citation2021). Reputation reduces customers’ worries and doubts about the quality of the bank’s services (Rindova et al., Citation2005). Banks are famous and have a long history of give off a positive vibe (Muflih, Citation2021).

CSR for social public welfare was implemented by banks through charitable endeavors that have a positive impact on society and the environment (Hiller, Citation2013). Additionally, the bank also practices this type of CSR by giving green loans priority when granting credit. In this way, the bank encourages environmentally friendly production and consumption (Zaid & Al-Manasra, Citation2013). These activities boost bank reputations as well as trademarks.

Commercial banks’ reputations are impacted by CSR for social and public welfare. Scholars had noted this connection in various trends (Khair et al., 2013; Melo & Garrido‐Morgado, Citation2012). Previous study show that CSR for social public welfare boosted the reputation of banks (Zhang et al., Citation2020). When CSR activities were visible and relevant to interested parties, they had a positive impact on reputation. On the other hand, there is research showing that correlation between reputation and CSR might have been negative or insignificant (Melo & Garrido‐Morgado, Citation2012). On this note, the authors submit that:

Hypothesis 1.

There is an effect of CSR for social public welfare on the reputation of commercial banks.

CSR for customers refers to CSR activities that focus on clients (Hiller, Citation2013). CSR for customers provide high-quality services and puts their needs at the center of the bank’s core business processes (Bolton, Citation2004). These activities aim to build trust, respond to feedback quickly and efficiently, and create service fairness for all customers (Zhang et al., Citation2020).

Many scholars show that CSR for customers affected a bank’s reputation in many different ways, but mainly through ethical standards (Holt et al., Citation2004). By integrating the CSR view into their promotional activities, commercial banks are positioned and affect customers’ choices and perceived characteristics (Geng et al., Citation2022).

CSR activities had a positive impact on reputation when they were visible and relevant to interested parties. CSR activities for customers promote customer recognition for the bank (Forcadell & Aracil, Citation2017). The research results also show that CSR contributed to increased customer confidence and trust (Osakwe & Yusuf, Citation2021). However, there is research indicating the correlation between reputation and CSR could be negative or insignificant (Melo & Garrido‐Morgado, Citation2012). As a result, previous research findings on the effect of CSR on customers on commercial bank reputation are ambiguous. As a result, the author hypothesizes:

Hypothesis 2.

There is an effect of CSR for customers on the reputation of commercial banks.

Employee CSR refers to activities aimed at improving employee welfare, such as improving working conditions and establishing reasonable, clear, and transparent salary, and bonus policies, and employees are treated fairly (Nybakk & Panwar, Citation2015). Furthermore, these CSR activities aim to ensure worker safety and health (Zhang et al., Citation2020). This activity brings value and benefits to employees (Sobhani et al., Citation2021). Employees were key envoys and enactors of the organization’s CSR. Employees who communicate with clients ethically will gain their trust, thereby improving the bank’s reputation (Bugandwa et al., Citation2021).

Many scholars studied the effect of CSR employees on the reputation and the results were quite different (Bugandwa et al., Citation2020; Melo & Garrido‐Morgado, Citation2012; Shafique & Ahmad, Citation2022; Sobhani et al., Citation2021). The research result of Shafique and Ahmad (Citation2022) shows that CSR activities for employees had created a good cultural environment, promoting employees to stick with the organization for a long time and work more effectively, increasing financial efficiency since then improving the reputation of the bank. Besides, CSR for employees could be negatively correlated with the bank’s reputation if the CSR policy was unclear and not perceived by these employees (Melo & Garrido‐Morgado, Citation2012). As a result of the hypothesis:

Hypothesis 3.

There is an effect of CSR for employees on the reputation of commercial banks.

2.4. Bank reputation and bank attractiveness

The attractiveness of the organization is also the attitude of the stakeholders. This is understood as a positive attitude toward the organization, and the desire to initiate certain relationships (Zhang et al., Citation2020). An attractive bank is a great bank to collaborate with, this is the preferred bank to their customers (Zhang et al., Citation2020). The previous study recognized the significance of reputation in influencing consumers’ perceptions, attitudes, as well as behaviors (Narteh & Braimah, Citation2020).

The influence of bank reputation on bank attractiveness was found to have three different results. The first result showed that bank reputation had a positive effect on bank attractiveness (Narteh & Braimah, Citation2020; Suley & Yuanqiong, Citation2019). Through CSR activities, the bank had more access to community development activities, better known to customers, thereby attracting customers (Suley & Yuanqiong, Citation2019). The results show that the reputation boosted the bank’s selection of customers (Narteh, Citation2013). The second result showed a negative relationship between these two variables (Saxton, Citation1998). The third result showed that this effect was bi-directional (Narteh & Braimah, Citation2020). The following hypothesis is stated as follows:

Hypothesis 4.

There is an effect of bank reputation on bank attractiveness.

2.5. CSR and bank attractiveness are mediated by reputation

The bank’s reputation was created from safety, stability, accessibility, price, and service quality. Customers rated a famous bank when they experienced and felt satisfied (Narteh & Braimah, Citation2020). The impact of CSR on bank brand attractiveness is clear, but the role of reputation as a mediating factor in the relationship between CSR and bank attractiveness is unclear and these studies are scarce.

Based on the concept of stakeholder theory, the ethical issue of banks was increasingly emphasized. CSR was increasingly considered by institutional investors when allocating capital to banks (Garvare & Johansson, Citation2010). To attract and retain customers in a large and highly competitive market, the banking industry must adapt to technology, be customer-centric, and improve its reputation (Narteh & Braimah, Citation2020). To have a good reputation, a bank must be socially responsible to the community. This creates trust among stakeholders, then attracts more customers (Leclercq-Machado et al., Citation2022). The following hypothesis is presented in Figure :

Figure 1. Proposed model research.

Hypothesis 5.

CSR for customers and bank attractiveness are mediated by bank reputation.

Hypothesis 6.

CSR for employees and bank attractiveness are mediated by bank reputation.

Hypothesis 7.

CSR for social public welfare and bank attractiveness are mediated by bank reputation.

3. Methodology

3.1. Research design

The article’s research goal was to investigate the impact of corporate social responsibility (CSR) activities on bank attractiveness to customers. The authors surveyed customers who are using banking services in Ho Chi Minh City, to determine the impact of CSR activities on brand reputation and thus the attractiveness of banks. However, the survey results included a percentage of respondents who were bank employees because they were also customers of the bank for which they work. Customers were also among those who benefit from the bank’s community services, such as environmental and community activities.

The bank’s CSR activities were directed at three groups including the community, customers, and employees (Geng et al., Citation2022). Banking products, unlike those from other industries, were concerned with money. As a result, before using the service, customers need to thoroughly investigate the bank (Sayani & Miniaoui, Citation2013). The information about other stakeholders, such as community activities, the environment, average employee salaries, bonuses, and employee welfare policies, was published in the Annual report of Vietnamese commercial banks. Customers who used banking services could easily find this information on the banks’ websites. Furthermore, previous research had also shown that when banks perform well in CSR activities, their reputation improves, attracting more customers to use their services (Narteh & Braimah, Citation2020).

The quantitative research method was used in the study. In the data, 27 commercial banks reported CSR activities in their financial statements. The questionnaire was pre-tested with respondents who are experienced in banking services. All items were measured using a 5-point Likert scale, in which 1 indicates completely disagree, and 5 represents completely agree.

3.2. Data collection

Survey questions were conducted offline at commercial banks in HoChiMinh City and survey online using Google Forms. The duration of the survey was 5 months, from 5 October 2022 to 5 February 2023. Online survey questionnaires were used to collect about 64% of the data. Once a week, surveys will be prompted after being emailed. Questionnaires are also sent via Messenger, Facebook groups and Zalo groups by links or QR codes to acquaintances who are using the bank’s services. These acquaintances continue to pass on the link to other friends or relatives who are also customers of the commercial banks.

Ho Chi Minh City is one of the largest cities in Vietnam with the highest population density. This is an area where many businesses and banks are concentrated. Most people have a bank account and use payment services through accounts. Finding a respondent is also quite simple. However, a somewhat selective design was made to the questionnaire in order to select the right bank’s clients.

The minimum sample size in the Maximization Likehood measure, according to Hair et al. (Citation2014), is between 100 and 150. In SEM analysis, however, the small sample size is less than or equal to 100, the mean sample size is between 100 and 200, and the large sample size is greater than 200. The total number of survey questionnaires sent was 1200 and 1167 valid were collected, the response rate was 97.25%.

3.3. Measurements of variables

This study was conducted to find out the impact of CSR on bank attractiveness under the influence of bank reputation. The authors used measurement items from a previous study (Table ). Bank attractiveness (BAT) had four items, based on the research of Jones et al. (Citation2014). Bank reputation (AFR) had four items, and was referenced from the research of Muflih (Citation2021). CSR for customers (CSC) included four items, CSR for employees (CSE) had three items, and CSR for social public welfare (CSS) had four items, and these items were based on Zhang et al.’s research (Zhang et al., Citation2020).

Table 1. Contructs and items

3.4. Statistical data analysis

This study aims to test the theory, so PLS-SEM is used (Hair et al., Citation2011). This method is ideal for studies that seek to identify the primary explanatory explanations for a given target framework (Ringle & Sarstedt, Citation2016). SmartPLS 3.0 software was used to analyze the data. The model was evaluated through two steps including model measurement and structural model evaluation. The model is reflective (Sarstedt et al., Citation2019). In the first step, the study tested the measurement model’s reliability, convergent validity, and discriminant validity on each scale in the model.

To evaluate convergent validity, the authors perform construct reliability evaluation (Hair et al., Citation2014). Metrics tested include composite reliability (CR), average variance extract (AVE), Cronbach’s alpha, rho_A, and indicator loadings. CR measures internal consistency reliability, a cutoff value of 0.7 is considered satisfactory (Hair et al., Citation2014). AVE must be higher than 0.5, and Cronbach’s alpha greater than 0.70 to meet the required threshold (Fornell & Larcker, Citation1981).

Fonell-Larker and the Heterotrait-Monotrait ratio (HTMT) were used to assess discriminant validity on each scale in the model (Fornell & Larcker, Citation1981). The HTMT threshold value is 0.85. When HTMT is close to 1, it indicates a lack of discriminant validity.

The authors then evaluate the size and significance of the path coefficients in the second step. To test the significance of the path coefficient, the author employs the Bootstrap method. The single performance in Bootstrap is 5,000.

4. Findings and discussion

4.1. Descriptive statistics

According to the results, men made up 59% of the 1167 respondents, while women made up 41%. 39 percent of the population is under the age of 18, 40 percent is between 25 and 45, 19 percent is between 56 and 60, and the remaining 2 percent is over 60. 30% of people have high incomes (over 30 million VND), while 37% have middle incomes (between 10 and 20 million VND). 20% of respondents have a master’s degree, and about 65% have a bachelor’s degree. This demonstrates that the survey’s respondents are intelligent individuals who are capable of responding to its questions (Table ).

Table 2. Descriptive statistics

4.2. Results of the measurement model

The results from the measurement model estimation were displayed in Table , which include outer weights, outer loadings, CR value, Cronbach’s alpha, and AVE, rho_A. Table shows that all constructs had a CR greater than 0.7 (Hair et al., Citation2014), indicating that the results met the internal consistency reliability threshold. All items’ outer loadings ranged from 0.771 to 0.894, meeting the indicator reliability requirement (Hair et al., Citation2014).

Table 3. Results from the measurement model estimation

The study also discovered that the scale of the variables ranged from 0.819 to 0.897, indicating that the measurement model has internal consistency reliability. The rho_A coefficient ranged from 0.735 to 0.883, which met the requirement (Hair et al., Citation2019). The AVE of all constructs ranged from 0.652 to 0.811, which was greater than 0.5 and met the discriminant validity requirement (Hair et al., Citation2014).

Table displays the results of Fornell and Larcker’s proposed discriminant validity measurement. The square root of AVE for all constructs ranged from 0.809 to 0.901, meeting the criteria for measuring discriminant validity.

Table 4. Discriminant validity (Fonell-Larker)

The Heterotrait—Monotrait test measures discriminant validity more rigorously than the Fornell and Larcker criteria (Dijkstra & Henseler, Citation2015). Table showed that the results of all constructs were significantly less than 1, indicating discriminant validity.

Table 5. Discriminant validity (Heterotrait – Monotrait)

4.3. Results of the structural model assessment

Results of the structural model assessment presented in Table indicated that AFR had a positive effect on BAT, with a p-value of 0.000. With a p-value of 0.000, CSC and CSS were also found to have a direct and positive effect on AFR. With a p-value of 0.007, CSE had a positive effect on AFR. Hypotheses H1, H2, H3, and H4 had thus been confirmed.

Table 6. Results of the structural model assessment

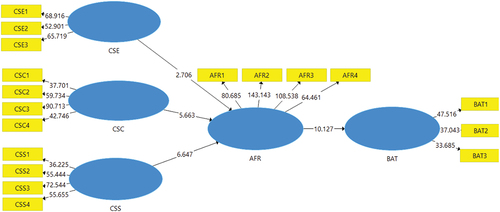

The indirect effect test results show that CSC and CSS affected BAT due to the indirect influence of AFR, p-value = 0.000. The findings also show that CSE affected BAT via the indirect influence of AFR (p-value = 0.009). Hypotheses H5, H6, and H7 had thus been confirmed. Figure depicts the structural model evaluation results.

Figure 2. Output bootstrapping.

4.4. Discussion

Hypothesis H1 (β = 0.244, p = 0.000) describes the impact of CSR for social public welfare on the reputation of commercial banks. The results found that CSR for social public welfare has a positive effect on the reputation. Giving back to the environment and engaging in charitable endeavors benefit the bank’s reputation. Hypothesis H2 (β = 0.221, p = 0.000) represents the effect of CSR for customers on the reputation of commercial banks. The results show that CSR for customers has a positive effect. CSR activities for customers help promote the bank’s reputation. In a highly competitive environment and sensitive activities for money, CSR for customers is a good and effective solution to help customers have better sympathy and brand recognition.

Hypothesis H3 (β = 0.107, p = 0.007) indicate the impact of CSR for employees on the reputation of commercial banks. This is the weakest of all the other relationships. The results also show that CSR for employees positively affects the reputation. This demonstrates that increasing CSR for employee activities improve the bank’s reputation. Banks should devote resources to implementing CSR activities for employees, which will increase bank’s reputation. Hypothesis H4 (β = 0.301, p = 0.000) shows the effect of bank reputation on bank attractiveness. This is the most important and strongest relationship compared to other relationships, showing that bank reputation has a positive influence on bank attractiveness. Bank reputation is a significant predictor of bank attractiveness. The bank’s reputation aid in the selection process. The bank’s attraction stems from the bank’s love, admiration, and pride.

Hypotheses H5 (β = 0.073, p = 0.007), H6 (β = 0.032, p = 0.009), H7 (β = 0.066, p = 0.009) represent the mediating role of bank reputation in the impact of CSR for customers, CSR for employees, CSR for social public welfare on bank attractiveness. The outcomes supported these constructive mediating roles. This also shows that the bank’s reputation is identified as a mediating factor, helping the bank’s CSR activities to be more attractive to customers. The bank’s CSR activities have increased the positive emotions of customers, and increased its reputation, thereby increasing the attractiveness of the bank. In which the impact of CSR for customers on bank attractiveness is most strongly mediated by bank reputation. This was because CSR for social and public welfare activities generated a lot of sympathy for the community, which spreads customers’ emotions when thinking about the bank’s brand, promoting the bank’s attractiveness.

The results demonstrate that all hypotheses are supported. The proposed model has been successful in achieving the study’s goals and identifying the influence of CSR elements on bank allure in Vietnamese banks. The stakeholder theory has been supported by research findings in Vietnam. The findings indicate that the bank will experience greater benefits when its operations are in line with the needs of its stakeholders, including customers, employees, and the community. The bank’s reputation is enhanced, which makes it more appealing to customers.

The core findings indicate that CSR for customers, CSR for employees, CSR for social public welfare have a direct effect on bank reputation, which in turn affects bank attractiveness. The majority of respondents agree that bank reputation plays an important role in attracting them to use the bank’s services. In Vietnam, a bank’s reputation is one of the determining factors for banks to acquire a customer base. Moreover, most of the survey opinions show that reputation can be created from CSR activities. Previous researchers have also shown similar results (Leclercq-Machado et al., Citation2022; Narteh et al., Narteh & Braimah, Citation2020; Zhang et al., Citation2020).

5. Conclusion and management implications

5.1. Conclusion

According to the findings, CSR for customers, CSR for employees, and CSR for public welfare are positively correlated to the bank’s reputation in Vietnam. The findings also show that CSR activities have an effect on bank reputation, which in turn affect the attractiveness.

Academically, the findings identify the impact of CSR on bank attractiveness in a developing country, where CSR activities recently receive attention, and implementation is limited due to a variety of factors including finance, knowledge, and legislation. The findings in Vietnam show CSR had a positive influence on the bank’s reputation, CSR activities are now important in attracting customers for Vietnamese banks. This is especially important for banks’ competitiveness strategies in the internationalized financial market environment. This acknowledgment also encourages banks to be more proactive in their interactions with stakeholders.

5.2. Management implications for solutions

According to the findings of the study, CSR activities are correlated to bank reputation in Vietnam. In a competitive environment, banks require a solution for deploying CSR activities to improve the bank’s reputation. This was one of the factors that helps the bank attract more customers. Furthermore, as a bank’s reputation improved, so did its attractiveness. As a result, in addition to CSR activities, the bank’s communication work is critical.

The level of implementation of CSR activities is heavily influenced by the financial situation, as well as the policy, the manager’s point of view, and the customer’s understanding. As a result, the implementation of CSR activities was also dependent on each bank’s available resources. The following solutions that banks can fully implement, bring tangible benefits to both the community and the bank itself.

5.2.1. CSR activities for employees

The human factor is always at the heart of every bank. The better the working environment, management, and operating mechanisms that meet employee benefits, the more motivated employees are to stick together and dedicate themselves. First, Vietnamese banks must ensure that working hours and overtime are by regulations (total working time cannot exceed 12 hours per day, and overtime cannot exceed 30 hours per month). The salary and bonus regulations have to be clear, transparent, appropriate, and by the law.

Another simple and practical CSR activity that the bank can undertake is to look after the lives of its employees. Vietnamese banks must ensure that a policy of regular health checks for employees with more specialized examination items is implemented. Adding fuel allowances for employees is a way to motivate them in the current environment of constantly rising gas prices. Furthermore, it is possible to create other appealing benefits such as sponsoring scholarships for employees’ children, providing membership cards for yoga classes, gym…

Additionally, ensuring good employee policies will assist employees in connecting with unity and good corporate culture. This is also why many successful businesses in CSR activities prioritize human resources to provide a stable life for employees.

Finally, promoting good policies for employees. Actively promoting employee care not only increases employee engagement but also generates sympathy for the bank among the general public. As the saying goes, a 10-person bank is your bank, but a 1,000-person bank is society’s. This is also why the local government always encourages the bank to have good employee policies, and the union looks after the employees. In a society where social media has such a large influence, each employee’s sharing about the bank is also an effective “soft” method of communication.

5.2.2. CSR activities for customers

Vietnamese banks can learn from other brands that are successful in developing effective customer-oriented CSR activities. Each bank’s operations have strengths and weaknesses. However, if the bank is to be successful, it must also understand how to learn and study good things from others to find the right direction for the bank’s long-term development.

Vietnamese banks, according to business philosophy, not only bring money to the community but also meaningful messages for them to absorb and improve their values. This will assist banks in delivering their products to the appropriate target audience while also increasing business efficiency.

Make a report on sustainable development (CSR Report). The disclosure of annual CSR activities should be treated as seriously as the enterprise’s financial statements. Vietnamese banks’ CSR reports are frequently sought after, widely influenced, and promoted business thinking that benefits the community. This is one of the factors that assist banks in better-maintaining sentiment, resulting in increased customer loyalty.

5.2.3. CSR for social public welfare

Environmental protection activities can be planned and implemented most appropriately and practically based on the characteristics of each bank. Vietnamese banks should increase loans for environmental projects such as wastewater treatment, waste treatment, hazardous waste, and the use of environmentally friendly technologies and products, as well as save energy and adapt to climate change. It is recommended to promote lending policies with preferential interest rates for these projects during the lending process. To appraise and advise the bank’s management effectively during the loan appraisal process, the bank must have human resources with environmental knowledge.

Transfer professional knowledge to society actively. Each Vietnamese bank’s most valuable asset is its expertise, which serves as the foundation for developing products to serve current consumers and potential customers. Banks can benefit from this rich asset by sharing useful knowledge with customers as a way to contribute to society: guiding customers on how to choose the right product for their financial situation, encouraging and supporting creative activities, and so on. Sharing knowledge is always welcome because what is “old” to one person may be completely “new” to another, making it always valuable.

Large Vietnamese banks can launch campaigns to plant trees, nurture seedlings, and donate to specialized organizations. It is possible to build energy-water-paper-saving movements right at the office for small and medium-sized banks, and each employee is encouraged to plant trees to decorate their desks.

Don’t put too much emphasis on the financial aspect of charity because it will put a strain on banks, particularly small banks. If the bank has a steady financial source, it can make cash donations to organizations that help children and the elderly. Employees can also be mobilized to donate old clothes and office supplies to schools in remote areas. This donation can be made directly or indirectly through intermediary organizations.

Every year, the banks may organize races or bicycle races to raise funds or to disseminate useful information to the community. Banks can participate in two ways: as sponsors or as participants. This not only increases brand recall but also encourages employees to participate in fitness activities.

Promote activities toward the environment. Love for mother nature has always been an eternal source of inspiration for people, and social responsibility for the environment has never ceased to appreciate people. This is a frequent and broad topic, and environmental responsibility is also on the creative horizon of social activists at Vietnamese banks.

Implement a “sensitive CSR” program for products and services at the bank. Vietnamese banks can encourage people to use their services when businesses borrow money from other banks to carry out projects that pollute the environment. The bank can promote communication strategies for the mobilization of savings deposits of customers to transfer that capital to projects that contribute to the protection of the environment. environmental protection. The “sensitive” CSR program always opens a wide door for any business, sometimes it’s an emerging event in that locality, building a bridge, helping to fulfill a child’s wish, or more broadly about social justice, gender equality …

6. Limitations of the research

This study was solely concerned with achieving the research objective of comprehending the impact of CSR on bank attractiveness through the mediated influence of bank reputation. As a result, the study did not include all of the factors that influence customer attraction. Furthermore, the bank’s survey subjects were primary customers, though there was a small percentage of respondents who were employees or recipients of the bank’s community services. The results did not compare the three banks’ behavior groups. As a result, future studies can be developed specifically for these subjects and compared to provide a more specific recommendation for the banks.

Ethical statement

The Ethical Committee of Ho Chi Minh City University of Economics and Finance, Vietnam on DATE 15 May 2023 (Ref. No. 320/QĐ-UEF) and University of Economics Ho Chi Minh City, Vietnam have granted approval for this study on DATE 13 May 2023 (Ref. No. 36/HĐ-KD-TH).

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Tang My Sang

Tang My Sang is currently working as a lecturer and researcher at Ho Chi Minh City University of Economics and Finance (UEF), Vietnam. She has held a number of leadership roles in this university. She has practical as well as theoretical expertise in the field of Education and Finance. Her research interest includes Education, Business management, Finance and Banking.

Nguyen Tien Hung

Nguyen Tien Hung is a lecturer and researcher at University of Economics Ho Chi Minh City (UEH), Vietnam. He is also the director of the Insurance Program. His research interest includes Education, Business management, Insurance.

Nguyen Ngoc Dinh

Nguyen Ngoc Dinh is a lecturer and researcher at University of Economics Ho Chi Minh City (UEH), Vietnam. He hold a number of important leadership roles in the university. His research interest includes Education, Business management, Insurance.

References

- Ajina, A. S., Japutra, A., Nguyen, B., Syed Alwi, S. F., & Al-Hajla, A. H. (2019). The importance of CSR initiatives in building customer support and loyalty: Evidence from Saudi Arabia. Asia Pacific Journal of Marketing & Logistics, 31(3), 691–18. https://doi.org/10.1108/apjml-11-2017-0284

- Aktekin, T., Dutta, D. K., & Sohl, J. E. (2018). Entrepreneurial firms and financial attractiveness for securing debt capital: A Bayesian analysis. Venture Capital, 20(1), 27–50. https://doi.org/10.1080/13691066.2017.1336894

- Atta-Mensah, J., & Dib, A. (2008). Bank lending, credit shocks, and the transmission of Canadian monetary policy. International Review of Economics & Finance, 17(1), 159–176. https://doi.org/10.1016/j.iref.2006.06.003

- Barnett, M. L., Jermier, J. M., & Lafferty, B. A. (2006). Corporate reputation: The definitional landscape. Corporate Reputation Review, 9(1), 26–38. https://doi.org/10.1057/palgrave.crr.1550012

- Bolton, M. (2004). Customer centric business processing. International Journal of Productivity & Performance Management, 53(1), 44–51. https://doi.org/10.1108/17410400410509950

- Bugandwa, T. C., Kanyurhi, E. B., Bugandwa Mungu Akonkwa, D., & Haguma Mushigo, B. (2021). Linking corporate social responsibility to trust in the banking sector: Exploring disaggregated relations. International Journal of Bank Marketing, 39(4), 592–617. https://doi.org/10.1108/IJBM-04-2020-0209

- Castelo Branco, M., & Lima Rodrigues, L. (2006). Communication of corporate social responsibility by Portuguese banks: A legitimacy theory perspective. Corporate Communications: An International Journal, 11(3), 232–248. https://doi.org/10.1108/13563280610680821

- CHONG, W. N., & Tan, G. (2010). Obtaining intangible and tangible benefits from corporate social responsibility. International Review of Business Research Papers, 6(4), 360. https://ink.library.smu.edu.sg/lkcsb_research/2939/

- Chung, K., Yu, J., Choi, M., & Shin, J. (2015). The Effects of CSR on customer satisfaction and loyalty in China: The moderating role of Corporate image. Journal of Economics, Business and Management, 3(5), 542–547. http://www.joebm.com/papers/243-M10014.pdf

- Demetriades, P. O., Rewilak, J. M., & Rousseau, P. L. (2023). Finance, growth and fragility. Journal of Financial Services Research, 1–21. https://doi.org/10.1007/s10693-023-00402-w

- Diaconu, I.-R., & Oanea, D.-C. (2015). Determinants of bank’s stability. Evidence from CreditCoop. Procedia Economics and Finance, 32(15), 488–495. https://doi.org/10.1016/s2212-5671(15)01422-7

- Dijkstra, T. K., & Henseler, J. (2015). Consistent partial least squares path modeling. MIS Quarterly, 39(2), 297–316. https://doi.org/10.25300/MISQ/2015/39.2.02

- El-Chaarani, H., & El-Abiad, Z. (2020 5). Determinants of banks reputation during crises. El-CHAARANI H and El-Abiad, 25. https://doi.org/10.2139/ssrn.3845201

- Forcadell, F. J., & Aracil, E. (2017). European banks’ reputation for corporate social responsibility. Corporate Social Responsibility & Environmental Management, 24(1), 1–14. https://doi.org/10.1002/csr.1402

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research This, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Freeman, R. E., & Reed, D. L. (1983). Stockholders and stakeholders: A new perspective on corporate governance. California Management Review, 25(3), 88–106. https://doi.org/10.2307/41165018

- Gangi, F., Mustilli, M., & Varrone, N. (2018). The impact of corporate social responsibility (CSR) knowledge on corporate financial performance: Evidence from the European banking industry. Journal of Knowledge Management, 23(1), 110–134. https://doi.org/10.1108/JKM-04-2018-0267

- Garvare, R., & Johansson, P. (2010). Management for sustainability–a stakeholder theory. Total Quality Management, 21(7), 737–744. https://doi.org/10.1080/14783363.2010.483095

- Geng, L., Cui, X., Nazir, R., & An, N. B. (2022). How do CSR and perceived ethics enhance corporate reputation and product innovativeness? Economic Research-Ekonomska Istraživanja, 35(1), 5131–5149. https://doi.org/10.1080/1331677X.2021.2023604

- Hair, R., JJ, S. M., & Ringle, C. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

- Hair, F. J., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory & Practice, 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Hair, F. J., Jr., Sarstedt, M., Hopkins, L., & Kuppelwieser, V. G. (2014). Partial least squares structural equation modeling (PLS-SEM) an emerging tool in business research. European Business Review, 26(2), 106–121. https://doi.org/10.1108/EBR-10-2013-0128

- Hiller, J. S. (2013). The benefit corporation and corporate social responsibility. Journal of Business Ethics, 118(2), 287–301. https://doi.org/10.1007/s10551-012-1580-3

- Holt, D. B., Quelch, J. A., & Taylor, E. L. (2004). How global brands compete. Harvard Business Review, 82(9), 68–75. https://hbr.org/2004/09/how-global-brands-compete

- Jones, D. A., Willness, C. R., & Madey, S. (2014). Why are job seekers attracted by corporate social performance? Experimental and field tests of three signal-based mechanisms. Academy of Management Journal, 57(2), 383–404. https://doi.org/10.5465/amj.2011.0848

- Kanji, G. K., & Chopra, P. K. (2010). Corporate social responsibility in a global economy. Total Quality Management, 21(2), 119–143. https://doi.org/10.1080/14783360903549808

- Leclercq-Machado, L., Alvarez-Risco, A., Esquerre-Botton, S., Almanza-Cruz, C., de las Mercedes Anderson-Seminario, M., Del-Aguila-Arcentales, S., & Yáñez, J. A. (2022). Effect of corporate social responsibility on consumer satisfaction and consumer loyalty of private banking companies in Peru. Sustainability, 14(15), 9078. https://doi.org/10.3390/su14159078

- LumbanGaol, G. A., Firmansyah, A., & Irawati, A. D. (2021). Intellectual capital, corporate social responsibility, and firm value in Indonesia’s banking industries. Jurnal Riset Akuntansi Terpadu, 14(1). https://doi.org/10.35448/jrat.v14i1.10229

- Maignan, I., Ferrell, O. C., & Hult, G. T. M. (1997). Corporate Citizenship: Cultural antecedents and Business benefits. Journal of the Academy of Marketing Science, 27(4), 455–469. https://doi.org/10.1177/0092070399274005

- Marin, L., & Ruiz, S. (2007). “I Need You Too!” Corporate identity attractiveness for consumers and the role of social responsibility. Journal of Business Ethics, 71(3), 245–260. https://doi.org/10.1007/s10551-006-9137-y

- McDonald, L. M., & Rundle‐Thiele, S. (2008). Corporate social responsibility and bank customer satisfaction a research agenda. International Journal of Bank Marketing, 26(3), 170–182. https://doi.org/10.1108/02652320810864643

- Melo, T., & Garrido‐Morgado, A. (2012). Corporate reputation: A combination of social responsibility and industry. Corporate Social Responsibility & Environmental Management, 19(1), 11–31. https://doi.org/10.1002/csr.260

- Muflih, M. (2021). The link between corporate social responsibility and customer loyalty: Empirical evidence from the Islamic banking industry. Journal of Retailing & Consumer Services, 61, 102558. https://doi.org/10.1016/j.jretconser.2021.102558

- Nahar, N., Mahiuddin, S., & Hossain, Z. (2021). The severity of environmental pollution in the developing countries and its remedial measures. Earth, 2(1), 124–139. https://doi.org/10.3390/earth2010008

- Narteh, B. (2013). Service quality in automated teller machines: An empirical investigation. Managing Service Quality: An International Journal, 23(1), 62–89. https://doi.org/10.1108/09604521311287669

- Narteh, B., & Braimah, M. (2020). Corporate reputation and retail bank selection: The moderating role of brand image. International Journal of Retail & Distribution Management, 48(2), 109–127. https://doi.org/10.1108/IJRDM-08-2017-0164

- Neitzert, F., & Petras, M. (2022). Corporate social responsibility and bank risk. Journal of Business Economics, 92(3), 397–428. https://doi.org/10.1007/s11573-021-01069-2

- Ngoc, N. (2018). The effect of corporate social responsibility disclosure on financial performance: Evidence from credit Institutions in Vietnam. Available at SSRN 3101658, 14(4), 109. https://doi.org/10.5539/ass.v14n4p109

- Nguyen, M., Bensemann, J., & Kelly, S. (2018). Corporate social responsibility (CSR) in Vietnam: A conceptual framework. International Journal of Corporate Social Responsibility, 3(1), 1–12. https://doi.org/10.1186/s40991-018-0032-5

- NGUYEN, X. H., DANG, T. Q., DINH, T. T. Q., DO, P. T., PHAM, T. U., & MAI, D. D. (2022). The impact of corporate social responsibility on brand value and financial performance: Evidence from bancassurance service providers in vietnam. The Journal of Asian Finance, Economics & Business, 9(6), 183–194. https://doi.org/10.13106/jafeb.2022.vol9.no6.0183

- Nybakk, E., & Panwar, R. (2015). Understanding instrumental motivations for social responsibility engagement in a micro‐firm context. Business Ethics: A European Review, 24(1), 18–33. https://doi.org/10.1111/beer.12064

- Osakwe, C. N., Ruiz, B., Amegbe, H., Chinje, N. B., Cheah, J. H., & Ramayah, T. (2020). A multi-country study of bank reputation among customers in Africa: Key antecedents and consequences. Journal of Retailing & Consumer Services, 56, 102182. https://doi.org/10.1016/j.jretconser.2020.102182

- Osakwe, C. N., & Yusuf, T. O. (2021). CSR: A roadmap towards customer loyalty. Total Quality Management & Business Excellence, 32(13–14), 1424–1440. https://doi.org/10.1080/14783363.2020.1730174

- Pérez, A., Martínez, P., & Rodríguez Del Bosque, I. (2013). The development of a stakeholder-based scale for measuring corporate social responsibility in the banking industry. Service Business, 7(3), 459–481. https://doi.org/10.1007/s11628-012-0171-9

- Phước Hương, L., & Công Trực, L. (2021). The role of corporate social responsibility, customer orientation and customer loyalty in banking sector in Tien Giang province. Scientific Journal of Van Hien University, 58(4), 13–26. https://doi.org/10.52932/jfm.vi58.32

- Platonova, E., Asutay, M., Dixon, R., & Mohammad, S. (2018). The impact of corporate social responsibility disclosure on financial performance: Evidence from the GCC Islamic banking sector. Journal of Business Ethics, 151(2), 451–471. https://doi.org/10.1007/s10551-016-3229-0

- Rashid, H. U., Nurunnabi, M., & Rahman, M. (2020). Exploring the relationship between customer loyalty and financial performance of banks: Customer open Innovation perspective. Journal of Open Innovation: Technology, Market, and Complexity, 6(4), 108. https://doi.org/10.3390/joitmc6040108

- Rindova, V. P., Williamson, I. O., Petkova, A. P., & Sever, J. M. (2005). Being good or being known: An empirical examination of the dimensions, antecedents, and consequences of organizational reputation. Academy of Management Journal, 48(6), 1033–1049. https://doi.org/10.5465/amj.2005.19573108

- Ringle, C. M., & Sarstedt, M. (2016). Gain more insight from your PLS-SEM results: The importance-performance map analysis. Industrial Management & Data Systems, 116(9), 1865–1886. https://doi.org/10.1108/IMDS-10-2015-0449

- Sarstedt, M., Hair, J. F., Cheah, J., Becker, J., & Ringle, C. M. (2019). How to specify, estimate, and validate higher-order constructs in PLS-SEM. Australasian Marketing Journal, 27(3), 197–211. https://doi.org/10.1016/j.ausmj.2019.05.003

- Saxton, M. K. (1998). Where do reputations Come from? Corporate Reputation Review, 1(4), 393–399. https://doi.org/10.1057/palgrave.crr.1540060

- Sayani, H., & Miniaoui, H. (2013). Determinants of bank selection in the United Arab Emirates. International Journal of Bank Marketing, 31(3), 206–228. https://doi.org/10.1108/02652321311315302

- Serwadda, I. (2018). Impact of credit risk management systems on the financial performance of commercial banks in Uganda. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 66(6), 1627–1635. https://doi.org/10.11118/actaun201866061627

- Shafique, O., & Ahmad, B. S. (2022). Impact of corporate social responsibility on the financial performance of banks in Pakistan: Serial mediation of employee satisfaction and employee loyalty. Journal of Public Affairs, 22(3), e2397. https://doi.org/10.1002/pa.2397

- Sobhani, F. A., Haque, A., & Rahman, S. (2021). Socially responsible HRM, employee attitude, and bank reputation: The Rise of CSR in Bangladesh. Sustainability, 13(5), 2753. https://doi.org/10.3390/su13052753

- Suley, W., & Yuanqiong, H. (2019). The impact of CSR reputation and customer loyalty: The Intervening influence of perceived service quality and trust. International Journal of Research in Business and Social Science, 8(4), 185–198. https://doi.org/10.20525/ijrbs.v8i4.302

- Suyanto, S. (2021). The effect of bad credit and liquidity on bank performance in Indonesia. The Journal of Asian Finance, Economics & Business, 8(3), 451–458. https://doi.org/10.13106/jafeb.2021.vol8.no3.0451

- Tien, N. H., Anh, D. B. H., & Ngoc, N. M. (2020). Corporate financial performance due to sustainable development in Vietnam. Corporate Social Responsibility & Environmental Management, 27(2), 694–705. https://doi.org/10.1002/csr.1836

- Tsang, E. W. K. (1998). A longitudinal study of Singapore beverages and hotel industries. Accounting Auditing & Accountability Journal, 11(5), 624–635. https://doi.org/10.1108/09513579810239873

- Van, L. T., Vo, D. H., & Ho, C. M. (2020). Financial inclusion, corporate social responsibility and customer loyalty in the banking sector in Vietnam. Journal of International Studies, 13(4), 9–23. https://doi.org/10.14254/2071-8330.2020/13-4/1

- Woo, H., & Jin, B. (2016). Apparel firms’ corporate social responsibility communications: Cases of six firms from an institutional theory perspective. Asia Pacific Journal of Marketing & Logistics, 28(1), 37–55. https://doi.org/10.1108/apjml-07-2015-0115

- Wu, M., & Shen, C. (2013). Corporate social responsibility in the banking industry: Motives and financial performance. Journal of Banking and Finance, 37(9), 3529–3547. https://doi.org/10.1016/j.jbankfin.2013.04.023

- Zaid, M. K. S. A., & Al-Manasra, E. A. (2013). The impact of corporate social responsibility dimensions on organizational attractiveness in Jordanian commercial banks. European Journal of Business and Management, 5(12), 175–183. https://citeseerx.ist.psu.edu/document?repid=rep1&type=pdf&doi=11677e72480f5138c7b57f3936c340e6f1abc0c2

- Zhang, Q., Cao, M., Zhang, F., Liu, J., & Li, X. (2020). Effects of corporate social responsibility on customer satisfaction and organizational attractiveness: A signaling perspective. Business Ethics: A European Review, 29(1), 20–34. https://doi.org/10.1111/beer.12243

- Zheng, Y., Rashid, H. U., Siddik, A. B., Wei, W., & Hossain, S. Z. (2022). Corporate social responsibility disclosure and firm ’ s productivity: Evidence from the banking industry in Bangladesh. Sustainability, 14(10), 6237. https://doi.org/10.3390/su14106237