?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Firm performance is one aspect of measuring a company’s level of success. This study aims to test whether there is an influence of foreign ownership and preference of company websites on firm performance as a proxy for ROA and ROE in companies in Indonesia. The population of this study was all companies listed in the Indonesia Stock Exchange (IDX) in 2021. The sample selection used purposive sampling and obtained 264 non-financial companies as the observation data. The data were collected from the company’s financial and annual reports. Multiple regression test was used to analyze this research. The results showed that the existence of foreign ownership and preference for company websites had a significant positive effect on firm performance. The finding indicates that firm performance proxied by ROA and ROE can be influenced by the company’s foreign ownership structure and the preference of the company website.

1. Introduction

Economic globalization drives dynamic changes that result in competition of understanding and monitoring firm performance (Boachie, Citation2020). This encourages companies to create progress and development with an innovation that enables increasing performance (Lee-Kuen et al., Citation2017). Measuring and evaluating firm performance is an important aspect for companies to achieve sustainable business (Aggarwal et al., Citation2019).

Performance is the result of a process that refers to and is measured over a certain period based on the conditions set by the company (Wiranata & Nugrahanti, Citation2013). Companies can be categorized as successful with one of the benchmarks in the form of firm performance. Firm performance is divided into two types, namely financial performance and non-financial performance (Ratnaningrum Aryani & Setiawan, Citation2020). Financial performance can be found in the company’s financial statements. Boachie (Citation2020) stated that firm performance can be improved by the existence of a foreign ownership structure and a company website (Ageeva et al., Citation2018).

Rashid (Citation2020) stated that the company’s performance is related to the company’s ownership structure. Foreign ownership will put more pressure on companies to improve firm performance. Foreign investors tend to see the business far ahead, so firm performance heavily influences investment (Al-Gamrh et al., Citation2020). Thus, the ownership of shares by foreign parties can directly affect the performance and value of the company. It is in line with the previous research by Wiranata and Nugrahanti (Citation2013) which stated that control by foreign shareholders impacts a good management system, technology and innovation, expertise, and marketing so that it has a positive impact on the company.

Technological developments in the business world are the cause of changes in the presentation of company information. Website technology companies allow companies to communicate with investors without being constrained by distance and time. The website is one of the company’s places to carry out financial and non-financial reporting (Aly et al., Citation2010). Palazzo et al. (Citation2020) stated that website has an advantage to disclose information about company performance quickly.

Agency theory provides the basis for this research which discusses the relationship between ownership and firm performance. Muhammad and Aryani (Citation2021) in their research found that foreign ownership can moderate the relationship with firm performance as measured by company profits because foreign investors understand and care more about the sustainability of the company in the long term. In addition, Nigel et al. (Citation2018) saw a foreign direct investment (FDI) perspective that can affect firm performance because of the tendency for foreign owners to always prioritize innovation in companies. Thus, it can be concluded that ownership and corporate websites can affect firm performance.

The topic of firm performance is still widely discussed at the present time (Bykova & Lopez-Iturriaga, Citation2018). Several studies have explained how foreign ownership affects firm performance. Rashid (Citation2020) conducted research in Bangladesh, and the result showed that foreign ownership and director ownership have significant positive results on accounting-based performance which is calculated using return on assets (ROA). This is because foreign ownership holds important control over the ranks of stakeholders to put pressure on management in improving firm performance. Furthermore, Al-Gamrh et al. (Citation2020) and Hamdan (Citation2018) found that foreign ownership has a significant positive effect on corporate performance as presented in financial performance in the form of ROA and ROE. The opposite result by Din et al. (Citation2020) showed that ownership structure has a significant positive effect on corporate performance when measured using ROE, but has no effect when measured using ROA. It implies that foreign shareholders effectively reduce information asymmetry and agency problems, thus improving accounting and corporate performance.

The inconsistency of previous research results encourages the researchers to conduct further analysis to expand the results of previous studies. This study includes the company website variable as a form of research innovation based on research by Ageeva et al. (Citation2019). Specifically, this study examines the effect of foreign ownership and preferences for using company websites on the performance of non-financial companies in Indonesia in 2021. In addition, this study provides empirical evidence on the composition of foreign ownership on firm performance and company websites on firm performance, especially financial performance that includes ROA and ROE.

The research is structured as follows. The first section presents a discussion of theoretical and literary reviews, followed by a hypothesis section. Research methods, including results, will be presented in the subsequent section. This research will be closed with conclusions, suggestions, and future research agendas.

2. Theoretical literature review

2.1. Theory agency

Agency theory implies that there is a conflict between the agent and the principal. This theory explains the relationship between a principal and their agents (Mizruchi, Citation2004); in this case, investors are the principal while the management is their agent. Jensen and Meckling (Citation1976) stated that agency relationships can occur when the principal assigns their agent a task in the principal’s interests. The agency theory assumes that the agents have a larger information gap than the principal. This information gap creates agency conflicts.

Considering the different interests between the management and agents, agency theory in this study is used to increase management motivation to optimize firm performance. Agency conflicts can be handled by improving firm performance to maintain the principal’s trust (Alabdullah, Citation2018; Aly et al., Citation2010; Boubaker et al., Citation2011).

Firm performance is a manifestation of performance and is a measure of management effectiveness and efficiency related to managing company resources. Firm performance can be categorized into two types, financial performance, and non-financial performance (Aggarwal et al., Citation2019). The company’s success, especially in the financial aspect, uses financial ratios contained in the company’s financial statements. Financial performance can be measured using return on assets (ROA) and return on equity (ROE). Return on assets (ROA) and return on equity (ROE) can reflect the level of efficiency in the use of assets and equity in company operations (Lee-Kuen et al., Citation2017).

2.2. Literature review and hypothesis development

2.2.1. Foreign ownership and firm performance

Previous studies on this matter have shown inconsistent results. Rashid (Citation2020), for example, stated that foreign ownership and director ownership have a significant positive effect on firm performance. In line with this research, Hamdan (Citation2018) and Al-Gamrh et al. (Citation2020) found that foreign ownership has a positive effect on firm performance in Saudi Arabia. A study by Din et al. (Citation2020) concluded that ownership structure has a significant positive effect on corporate performance as measured using ROE, while ownership structure does not affect corporate performance as measured using ROA. However, the researchers believe that foreign investment can encourage increased financial performance in companies (Carney et al., Citation2019). Foreign investors will put more pressure on companies, eventually improving firm performance (Gu et al., Citation2019). With the inconsistent results of the previous research and discussion, it is necessary to carry out further analysis to expand the results. In this case, the researchers formulate the hypothesis as follows:

H1:

Foreign ownership has a positive effect on firm performance.

2.3. Corporate website and firm performance

Abdi and Omri (Citation2020) found a negative and significant association between web-based disclosure and the company’s cost of debt evidence in the MENA countries. Yet, Boubaker et al. (Citation2011) discovered the use of the Internet as an information dissemination industry in France. The corporate relies on the company’s website to disclose its financial information to stakeholders

Ageeva et al. (Citation2018) conducted research using a sample of the Russian Federation. The results of this study indicated that the company’s website gives customers the freedom to provide criticisms and suggestions for the company’s products. In addition, the company’s website tends to have an attractive design that highlights the company’s image and directly attracts customers. Ageeva et al. (Citation2019) conducted another in-depth analysis to evaluate the importance of understanding and test the advantages of company websites and antecedent factors in England and Russia. This study concluded that several website excellences contribute to a company’s competitive advantage, including navigation, visuals, information, usability, customization, security, availability, website credibility, customer service, perceived corporate social responsibility, and perceived corporate culture (Farkas & Keshk, Citation2019). These advantages can improve firm performance due to easy access to information and the credibility of information (Thakur & Al Saleh, Citation2020). The corporate website also promotes corporate strategy renewal (Correia et al., Citation2021) and increases investors’ interest in the company (Palazzo et al., Citation2020)

Research on the relationship between company website preferences and firm performance is rarely researched, especially in Indonesia. It encourages the researchers to propose a hypothesis, formulated as follows:

H2:

Company website preferences have a positive effect on firm performance.

3. Research method

3.1. Data and sample

The data for this research are all non-financial companies listed on the Indonesia Stock Exchange (IDX) in 2021, a total of 508 companies. As this research was conducted in November 2022, 2021 was chosen as the observed year. The sample was selected using purposive sampling with the following criteria: (1) companies are listed on the Indonesia Stock Exchange (IDX); (2) financial reports and annual reports can be accessed on the IDX website and company website; (3) the company has an active and accessible website. According to these criteria, 199 out of 508 non-financial companies in Indonesia do not publish complete financial reports on the IDX website and company websites and thus were excluded from the research. In the data used, there were outliers with extreme values that could interfere with the analysis (Gujarati & Porter, Citation2008). Considering this, 45 companies were excluded from the sample, leaving 264 companies as the final samples (Table ).

Table 1. Sample Selection

This data were processed using Eviews 10 statistic software. Testing the data begins using the classic assumption test, namely the normality test, multicollinearity test, and heteroscedasticity test. This study uses three kinds of hypothesis testing, namely the coefficient of determination (R2), F test, and t-test. The use of multiple regression tests by considering the research data as cross-section data.

3.2. Variable measurement

3.2.1. Firm performance

According to (Din et al., Citation2020), firm performance applies ROA and ROE measurements. ROA and ROE are the most appropriate tools for measuring financial performance. ROA and ROE can calculate a company’s wealth and equity with the following formula:

3.3. Foreign ownership

In this study, foreign ownership is measured in percentage similar to that in the previous research by Bykova and Lopez-Iturriaga (Citation2018). It is formulated as follows:

3.4. Company website

The company website is calculated by INDEX which is in accordance with the research by Ageeva et al. (Citation2019). There are five indexes in total.

3.5. Control variables

This study uses three control variables, namely company size (Size), debt-equity ratio (DER), and cash turnover (CATR) which are consistently and positively related to firm performance as mentioned in the previous studies by Wiranata and Nugrahanti (Citation2013), Alabdullah (Citation2018), and Kao et al. (Citation2019). It shows that firm performance can be influenced by company size, debt ratio to equity, and cash turnover as formulated in Table below:

Table 2. Control variables

3.6. Regression models

The hypothesis in this study was tested with multiple regression analysis. The model is applied because this research analyzes the effect of two independent variables in the form of foreign ownership and company websites on one dependent variable, namely firm performance (Ghozali, Citation2011). As a condition of multiple regression testing, a classic assumption test is necessary to ensure the level of consistency of research data. The regression model is formulated as follows:

Notes:

ROA : Return on asset,

ROE : Return on equity,

FOWN : Foreign ownership,

COWEF : Corporate website,

SIZE : Size of company,

DER : Debt equity ratio, and

CATR : Cash turn over.

4. Result and discussion

4.1. Descriptive statistic

Descriptive statistics describe research descriptions with the aim that the data presented is easy to understand and informative. This study uses statistical data in the form of mean, minimum, maximum, and standard deviation. Table presents a descriptive statistical test based on the dependent variable using return on assets (ROA), while Table presents a descriptive statistical test with the dependent variable in the form of ROE.

Table 3. Descriptive statistic

Based on Table above, it can be seen that the research dependent variable is calculated using ROA. The results of the descriptive statistical test for 216 samples had a mean of 0.710795 and a standard deviation of 0.544437. In addition, the mean value is greater than the median value of 0.575000, this indicates that the ROA statistical test results have a positive skewness tendency, which means that the majority of the ROA samples have values below the average. The second result, the mean variable ROE value of 71.58716 is greater than the median value of 60.81000, this indicates that ROE has a positive skewness tendency, which means that the majority of the ROE samples have values below the average.

Statistical test results on the independent variable FOWN showed a mean value of 0.428030 greater than the median value of 0.340000. This shows that FOWN’s skewness tends to be positive. The results of the second independent variable test, namely COWEF, have a mean of 17.85606 which is smaller than the median value of 18.00000, this indicates that COWEF tends to be negative on skewness.

This study has three control variables, namely SIZE, DER, and CATR. Size has a mean value of 28.55420 and a median of 28.70000 which shows that size tends to have negative skewness. In the control variable, the mean DER value of 94.68148 is greater than the median value of 0.110000, meaning that the DER variable has a positive trend. CATR has a mean of 2.030565 and a median of 1.390000 which is greater than the median, and indicates that CATR has a positive skewness tendency.

4.2. Classic assumption test

4.2.1. Normality test

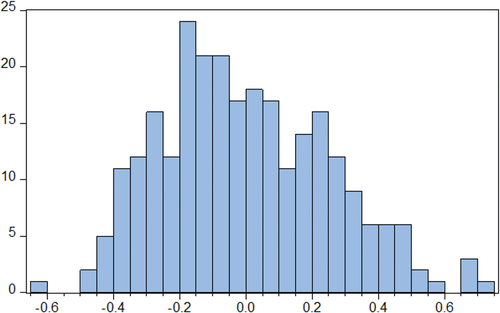

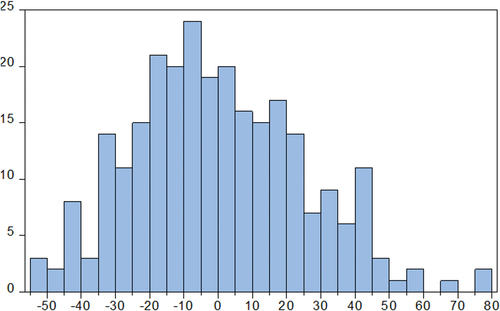

The normality test aims to determine whether the data collected is normally distributed or not. The regression model can be called good if it is close to normal (Ghozali, Citation2011). This study used the Kolmogorov-Smirnov test to perform a normality test. This study conducted a normality test with two stages, the first is to test the normality of firm performance with the dependent variable in the form of ROA. The second test is the normality of firm performance with the dependent variable in the form of ROE. The research normality test with a firm performance measurement tool in the form of ROA shows a probability value of 0.032718 > 0.05. This shows that the research data has a normal distribution (Figure ). The company’s performance norm test with ROE shows a probability value of 0.053058 > 0.05. This shows that the data in this study, especially firm performance as measured by ROE, has a normal distribution (Figure ).

Figure 1. Normality test dependent variable ROA.

Figure 2. Normality test dependent variable ROE.

4.3. Multicollinearity test

The multicollinearity test is used to determine the correlation among independent variables. To detect the existence of multicollinearity in this study, the researchers are looking at the tolerance value and variance inflation factor (VIF) <10% (Gujarati & Poter, Citation2008). The research multicollinearity test on the ROA variable is presented bellow

Table and Table above show that the multicollinearity test on the dependent variable ROA has a VIF value of less than 10%, so it can be concluded that the research data is free from multicollinearity (Gujarati & Poter, Citation2008).

Table 4. Multicollinearity test ROA

Table 5. Multicollinearity test ROE

Based on Tables above, there are similarities in the centered VIF values, however, the results of the coefficient of variance are different. The reason is the VIF value in model 1 (ROA) and model 2 (ROE). The VIF calculation only involves the coefficient of determination of an independent variable which is regressed with other independent variables, so it does not involve ROA or ROE variables at all. Meanwhile, the coefficient variance of ROA in Table and ROE in Table have different values because the two regression models are estimated at different dependencies; model 1 uses ROA and model 2 uses ROE as the dependent variable. Thus, the difference produces different regression coefficients in the two models.

4.4. Heteroscedasticity test

The heteroscedasticity test is useful for testing the regression model whether there is an unequal variance of the residuals or not. Detection of the presence of heteroscedasticity can be done by looking for the presence or absence of certain patterns on the scatterplot graph between the Y axis and the X axis as follows:

Table and Table above show that all probability values for the dependent variable, by measuring ROA, the independent variables FOWN and COWEF, and the control size DER and CATR variables, have a value of more than 0.05. So, it can be concluded that the data of this study did not perform heteroscedasticity.

Table 6. ROA heteroscedasticity test

Table 7. ROE Heteroskedasticity test

The occurrence of heteroscedasticity allows the emergence of problems. The way to overcome the problem of heteroscedasticity is by estimating the Fama Macbeth regression model with Huber-White (White-Hinkley) correction on the standard error model. This is done to obtain a robust standard error for inhomogeneous data to obtain reliable model test results. This test can be estimated using the Fama Macbeth regression model with the Huber-White (White-Hinkley) correction on the standard error model (Tables )

Table 8. Fama Macbeth model Estimation with Huber-White (White-Hinkley) ROA

Table 9. Fama Macbeth model Estimation with Huber-White (White-Hinkley) ROE

4.5. Regression result

This study uses three kinds of hypothesis testing, namely the coefficient of determination (R2), F test, and t-test. As presented in Table , the coefficient of determination test using the ROA variable shows a value of 0.779323, meaning that the model can explain the dependent variable of 77.9% which is influenced by other factors outside the variables of this study. The F test results show a result of 0.000000. The result indicates that the independent variables and control variables used in this study simultaneously affect the dependent variable.

The results in Table above show that the variable of foreign ownership (FOWN) and preference for company website (COWEF) has a probability value of 0.0000 or less than 0.05. This means that the FOWN variable affects the company’s performance variable as measured by ROA. This is in line with the research of Din et al. (Citation2020) and Al-Musali et al. (Citation2019) which proved that the return on assets owned by companies has an impact on improving firm performance. In addition, the COWEF variable influences the company’s performance variable as measured by ROA. This is in line with research by Ageeva et al. (Citation2018) which stated that the company’s website is very important for the company’s image which directly impacts the company’s performance (Abdi et al., Citation2018). The control variables in the form of SIZE, DER, and CATR have a value of more than 0.05 which means that there are no control variables that affect firm performance with ROA.

Table 10. Variable regression result based on ROA

Table below shows that the test for the coefficient of determination using the ROA variable has the value of 0.780797, meaning that the model can explain the dependent variable of 78%, the rest is influenced by other factors outside the variables of this study. The F test showed a result of 0.000000. This result indicates that the independent variables and control variables used in this study simultaneously affect the dependent variables.

Table 11. Variable regression results based on ROE

The results in Table above show that the foreign ownership (FOWN) and the preference for company website (COWEF) variables have a probability value of 0.0000 or less than 0.05. This means that the FOWN and COWEF variables affect firm performance variables as measured by ROE (Gu et al., Citation2019; Kao et al., Citation2019; Nigel et al., Citation2018). The control variables, namely SIZE, DER, and CATR, have a value of more than 0.05, which means that none of the control variables affects firm performance with ROE.

The results of the two tables above (Tables ) are estimated using the least square method with White-Hinkley (HC1) correction on the standard error model to estimate heteroscedasticity and obtain consistent standard errors and covariance models. Tables show a standard error that is not much different, meaning that the regression model obtained is not much affected by the heteroscedasticity effect or the use of the least square method to estimate the model is very good. Correction of White-Hinkley heteroscedasticity consistent standard errors gives more confidence that the model used is robust. Furthermore, the R-Square of the model is quite high; 77.9% for ROA and 78% for ROE. This is caused by the foreign ownership and corporate websites variables which have a significant effect on ROA and ROE. Thus, the R-square value obtained in this test is not affected by model specification errors, model inconsistency, or non-robust model, but purely by the significance of the independent variable on the dependent variable.

4.6. Robustness test

This study uses a robustness test by removing samples that record losses in the study period, namely 2021. The results are shown in Table dan Table below:

Table 12. Result of robustness test on dependent variable ROA

Table 13. Result of robustness test on dependent variable ROE

Tables above show the results of the resilience test after excluding companies that posted losses in 2021 with a sample of 231 companies. The results obtained after carrying out the robustness test did not have a significant difference from the regression results (Tables ), so it can be interpreted that this research model is robust and consistent.

5. Conclusion, limitation, and future research Agenda

Economic globalization encourages the creation of dynamic changes through increasing competition. As a result, understanding and monitoring firm performance is important for companies. This enables companies to create progress and development with innovations to improve firm performance. This relationship is played by investors as principals and management as agents. This action is in line with agency theory.

The results of this study indicate that foreign ownership and preference of company websites have a positive effect on firm performance which is proxied using ROA and ROE. This influence is based on the results of the regression test which has a probability value of 0.0000 on firm performance. These results imply that foreign ownership puts more pressure on companies to always improve firm performance and encourage progress by presenting information on company websites for easy access to information. Foreign ownership is believed to be more assertive in imposing corporate sanctions than local ownership.

This study contributes theoretically by providing empirical evidence about the impact of foreign ownership and preferences on company websites on firm performance. Practically this research provides an understanding, especially company management to improve company performance, one of which is through foreign ownership. This research can be generalized with consideration of the limitation includes, 1) this study measures company performance in 2021. This limitation provides an opportunity for further research to expand the research sample and add moderating variables based on developing issues, for example, the disclosure of carbon emissions. 2) This research focuses on examining foreign ownership and company website preferences, further research can examine other variables such as corporate governance on company performance.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Abdi, H., Kacem, H., & Omri, M. A. B. (2018). Determinants of web-based disclosure in the Middle East. Journal of Financial Reporting and Accounting, 16(3), 464–14. https://doi.org/10.1108/JFRA-11-2016-0093

- Abdi, H., & Omri, M. A. B. (2020). Web-based disclosure and the cost of debt: MENA countries evidence. Journal of Financial Reporting and Accounting, 18(3), 533–561. https://doi.org/10.1108/JFRA-07-2019-0088

- Ageeva, E., Melewar, T. C., Foroudi, P., & Dennis, C. (2019). Evaluating the factors of corporate website favorability: A case of UK and Russia. Qualitative Market Research, 22(5), 687–715. https://doi.org/10.1108/QMR-09-2017-0122

- Ageeva, E., Melewar, T. C., Foroudi, P., Dennis, C., & Jin, Z. (2018). Examining the influence of corporate website favorability on corporate image and corporate reputation: Findings from fsQCA. Journal of Business Research, 89, 287–304. https://doi.org/10.1016/j.jbusres.2018.01.036

- Aggarwal, R., Jindal, V., & Seth, R. (2019). Board diversity and fi rm performance: The role of business group affiliation. International Business Review, 28(December 2018), 1–17. https://doi.org/10.1016/j.ibusrev.2019.101600

- Alabdullah, T. T. Y. (2018). The relationship between ownership structure and firm financial performance: Evidence from Jordan. Benchmarking: An International Journal, 25(1), 319–333. https://doi.org/10.1108/BIJ-04-2016-0051

- Al-Gamrh, B., Al-Dhamari, R., Jalan, A., & Afshar Jahanshahi, A. (2020). The impact of board independence and foreign ownership on financial and social performance of firms: Evidence from the UAE. Journal of Applied Accounting Research, 21(2), 201–229. https://doi.org/10.1108/JAAR-09-2018-0147

- Al-Musali, M. A., Qeshta, M. H., Al-Attafi, M. A., & Al-Ebel, A. M. (2019). Ownership structure and audit committee effectiveness: Evidence from top GCC capitalized firms. International Journal of Islamic & Middle Eastern Finance & Management, 12(3), 407–425. https://doi.org/10.1108/IMEFM-03-2018-0102

- Aly, D., Simon, J., & Hussainey, K. (2010). Determinants of corporate internet reporting: Evidence from Egypt. Managerial Auditing Journal, 25(2), 182–202. https://doi.org/10.1108/02686901011008972

- Boachie, C. (2020). Corporate governance and financial performance of banks in Ghana: The moderating role of ownership structure. International Journal of Emerging Markets, 1746–8809. https://doi.org/10.1108/IJOEM-09-2020-1146

- Boubaker, S., Lakhal, F., Nekhili, M., & Hussainey, K. (2011). The determinants of web-based corporate reporting in France. Managerial Auditing Journal, 27(2), 126–155. https://doi.org/10.1108/02686901211189835

- Bykova, A., & Lopez-Iturriaga, F. (2018). Exports-performance relationship in Russian manufacturing companies: Does foreign ownership play an enhancing role? Baltic Journal of Management, 13(1), 20–40. https://doi.org/10.1108/BJM-04-2017-0103

- Carney, M., Estrin, S., Liang, Z., & Shapiro, D. (2019). National institutional systems, foreign ownership and firm performance: The case of understudied countries. Journal of World Business, 54(4), 244–257. https://doi.org/10.1016/j.jwb.2018.03.003

- Correia, E., Garrido, S., & Carvalho, H. (2021). Online sustainability information disclosure of mold companies. Corporate Communications, 26(3), 557–588. https://doi.org/10.1108/CCIJ-05-2020-0085

- Din, S. U., Arshad Khan, M., Khan, M. J., & Khan, M. Y. (2020). Ownership structure and corporate financial performance in an emerging market: A dynamic panel data analysis. International Journal of Emerging Markets, 17(8), 1973–1997. https://doi.org/10.1108/IJOEM-03-2019-0220

- Farkas, M., & Keshk, W. (2019). How Facebook influences non-professional investors’ affective reactions and judgments: The effect of disclosure platform and news valance. Journal of Financial Reporting and Accounting, 17(1), 80–103. https://doi.org/10.1108/JFRA-10-2017-0092

- Ghozali. (2011). Statistik Non Parametik Teori dan Aplikasi dengan Program IBM SPSS 23. Edisi 2 Semarang. Undip.

- Gu, V. C., Cao, R. Q., & Wang, J. (2019). Foreign ownership and performance: Mediating and moderating effects. Review of International Business & Strategy, 29(2), 86–102. https://doi.org/10.1108/RIBS-08-2018-0068

- Gujarati, D. N., & Porter, D. C. (2008). Dasar-dasar Ekonometrika. Edisi 5. Salemba Empat.

- Hamdan, A. (2018). Board interlocking and firm performance: The role of foreign ownership in Saudi Arabia. International Journal of Managerial Finance, 14(3), 266–281. https://doi.org/10.1108/IJMF-09-2017-0192

- Jensen, C., & Meckling, H. (1976). Theory of the firm: Managerial Behavior, agency Costs, and ownership structure. Journal of Financial Economics 3, 3, 305–360.

- Kao, M. F., Hodgkinson, L., & Jaafar, A. (2019). Ownership structure, board of directors and firm performance: Evidence from Taiwan. Corporate Governance (Bingley), 19(1), 189–216. https://doi.org/10.1108/CG-04-2018-0144

- Lee-Kuen, I. Y., Sok-Gee, C., & Zainudin, R. (2017). Gender Diversity and firms financial performance in Malaysia. Asian Academy of Management Journal of Accounting and Finance, 13(1), 41–62. https://doi.org/10.21315/aamjaf2017.13.1.2

- Mizruchi, M. S. (2004). Berle and means revisited: The governance and power of large U.S. corporations. Theory and Society, 33(5), 579–617. https://doi.org/10.1023/B:RYSO.0000045757.93910.ed

- Muhammad, G. I., & Aryani, Y. A. (2021). The impact of Carbon disclosure on firm value with foreign ownership as a moderating variable. Jurnal Dinamika Akuntansi Dan Bisnis, 8(1), 1–14. https://doi.org/10.24815/jdab.v8i1.17011

- Nigel, D., Sun, K., & Temouri, Y. (2018). Investigating the link between foreign ownership and firm performance – an endogenous threshold approach. Multinational Business Review, 26(3), 277–298. https://doi.org/10.1108/MBR-12-2017-0102

- Palazzo, M., Vollero, A., & Siano, A. (2020). From strategic corporate social responsibility to value creation: An analysis of corporate website communication in the banking sector. International Journal of Bank Marketing, 38(7), 1529–1552. https://doi.org/10.1108/IJBM-04-2020-0168

- Rashid, M. M. (2020). Ownership structure and firm performance: The mediating role of board characteristics. Corporate Governance (Bingley), 20(4), 719–737. https://doi.org/10.1108/CG-02-2019-0056

- Ratnaningrum Aryani, Y. A., & Setiawan, D. (2020). Balanced Scorecard: Is it Beneficial Enough? A Literature Review. Asian Journal of Accounting Perspectives, 13(1), 65–84. https://doi.org/10.22452/AJAP.vol13no1.4

- Thakur, R., & Al Saleh, D. (2020). Drivers of managers’ affect (emotions) and corporate website usage: A comparative analysis between a developed and developing country. Journal of Business and Industrial Marketing, 36(6), 962–976. https://doi.org/10.1108/JBIM-02-2020-0118

- Wiranata, Y. A., & Nugrahanti, Y. W. (2013). Pengaruh Struktur Kepemilikan Terhadap Profitabilitas Perusahaan Manufaktur di Indonesia. Jurnal Akuntansi Dan Keuangan, 15(1), 15–26. https://doi.org/10.9744/jak.15.1.15-26