Abstract

This study aims to design a framework of corporate governance innovation to reduce the credit risks of Micro, Small and Medium Enterprises (MSMEs) by using blockchain technology. The research design uses a qualitative approach with Grounded theory analysis for data analysis with open, axial, and selective coding. This framework consists of two stages, namely development and validation. In-depth interviews are used for data collection to develop the framework while focus group discussions are used for validation. The in-depth interviews are carried out with various stakeholders, such as the government, association, MSMEs, suppliers, and banking. Findings show that blockchain technology as corporate governance innovation framework has the potential to reduce asymmetric information and credit risk. The reason is that blockchain technology can facilitate recording, immutable, partial decentralisation, and storage of business and financial transactions on a digital network and all stakeholders can access information in a transparent and valid manner that can increase transparency, accountability, responsibility, and fairness. Results of the focus group discussion indicate the validity of the proposed framework.

PUBLIC INTEREST STATEMENT

MSMEs as risk borrowers because of their asymmetric information with financial institutions. MSMEs are unwilling to share information about real transactions and operational conditions, due to lack of trust or security guarantees for their data. Blockchain technology can provide a solution to this problem because of its characteristics of being safe, immutable, having a distributed storage, partial decentralisation and trustworthiness. This study proposes blockchain technology frameworks as corporate governance innovations that have the potential to increase transparency, accountability, responsibility, fairness. Thus, MSMEs can reduce their asymmetric information and credit risk for easier access to financial access, thereby improving their performance and sustainability.

1. Introduction

Business units in Indonesia are dominated by Micro, Small and Medium Enterprises (MSMEs), which account for 99% of the total national business units while the remaining 1% are large companies (Tambunan, Citation2017). MSMEs can absorb majority the number of workers (Susan, Citation2020) and can contribute to economic growth (Juminawati et al., Citation2021). However, MSMEs face difficulties in development due to limited access to financial institution (Maseko & Manyani, Citation2011; Myint, Citation2020). Banks cannot easily provide loans to SMEs because of their asymmetric information, and MSMEs do not have well-documented financial data, valuable assets and proven track record (Tambunan, Citation2017). This scenario prompts MSMEs to carry out opportunistic behaviours to prioritise their interests which harm creditors and other stakeholders, and thus become high-risk borrowers (Mutamimah & Hendar, Citation2017; Mutamimah et al., Citation2021).

Various efforts have been made to overcome the problem of credit risk, one of which is the implementation of corporate governance in MSMEs. Corporate governance (Mutamimah et al., Citation2021) as a system, mechanism, and structure to regulate, monitor and control the behaviours of MSME managers to reduce the moral hazards, and thus reduce the company credit risks. Banks have implemented corporate governance for evaluating creditworthiness based on the 5C rule, as follows: Capacity, Capital, Character, Collateral and Condition. However, MSMEs lack financial data, and thus the bank is only based on subjective perceptions as the basis for determining creditworthiness (Wasiuzzaman & Nurdin, Citation2019). This basis is also a source of credit risk, despite the bank having implemented corporate governance. These efforts are not effective as indicated by a research gap on the effect of corporate governance on credit risk. Mutamimah et al. (Citation2021) and Postnova (Citation2012) found that traditional corporate governance cannot effectively reduce MSMEs’ credit risk, contrary to Dao and Pham (Citation2015) that showed a can decrease of credit risk. The present study motivated by this unresolved problem of MSMEs credit risk.

In the current digital economy era, MSMEs can improve their business with digital innovation of corporate governance by applying blockchain technology. This new technology can facilitate the recording and storage of business and financial transactions on a network of digital blocks that ensures transparency, resilience and trust and thereby reduce credit. Singh et al. (Citation2020) stated that blockchain is described as decentralised ledger system, where their information is stored on computers and monitored by all stakeholders and allows for secure transactions without the need of any intermediary. Therefore, blockchain can be used to support the implementation of corporate governance. Singh et al. (Citation2020) also stated that blockchain plays a vital role in effective corporate governance, reinforced by Smith and Dhillon (Citation2020) that blockchain technology can secure financial transactions. Liu et al. (Citation2021) found that blockchain can facilitate the transformation of credible information, enabling banks to gain knowledge from collateral. Thus, blockchain technology can reduce asymmetric information between agents and principals (Lemieux, Citation2016).

Previous studies related to the application of blockchain technology to improve corporate governance performance in the non-financial and non-MSMEs fields have been carried out. Such research includes the implementation of blockchain technology in operations management (OM) with supply chain management (SCM) from the perspective of sustainable performance in the airport industry (DiVaio & Varriale, Citation2020). Blockchain technology was also used to integrate complex multi-tier supply networks that can reduce information asymmetry and opportunistic behaviours across different tiers of the supply network, and thus can enhance the visibility and transparency of suppliers’ sustainability practices across the different layers of the supply network (Najjar et al., Citation2023). Moreover, blockchain technology was also used to improve the value to gender equality (GE) and inclusion, in line with Sustainable Development Goal (SDG) 5 through the technology-oriented corporate governance (CG) models (DiVaio et al., Citation2023). However, the present study focuses on blockchain technology as a corporate governance innovation to reduce credit risk in MSMEs in Indonesia, which has never been examined. The purpose of this study is to develop a of corporate governance innovation framework to reduce credit risk for MSMEs by using blockchain technology. This article is divided into five parts. The first section is the Introduction followed by the literature review. The third section presents the research methods and the fourth shows the results and discussion. The fifth is the conclusion, limitations and implication.

2. Literature review

This review includes research on Credit Risk for MSMEs, Corporate Governance and Credit Risk for MSMEs, Blockchain Technology and Credit Risk and Corporate Governance Innovation Based on Blockchain Technology.

2.1. Credit risk for MSMEs

Credit risk is a crucial problem that has not been resolved. Therefore, managers must properly manage risk because of its impact on the company performance and sustainability (Mutamimah et al., Citation2022). MSMEs in Indonesia have several common characteristics, as follows: family business with management held by one person (Kurniawati et al., Citation2018); limited financial access (Maseko & Manyani, Citation2011); and has a high credit risk (Mutamimah & Hendar, Citation2017). Juniarti and Omar (Citation2021) and Kolapo et al. (Citation2012) defined credit risk as the possibility that the borrower cannot or are unwilling to repay the interest and capital according to time line of contract. Credit risk occurs due to asymmetric information (Yoshino & Taghizadeh-Hesary, Citation2018; Yudaruddin, Citation2020) and evaluation of creditworthiness for MSMEs based on the bank perception (Karlan et al., Citation2015), given their lack of financial statement data (Claessens & Tzioumis, Citation2006). Moreover, Maseko (Citation2011) found that most MSMEs lack accounting knowledge and do not have efficient records for measuring financial performance. This finding is reinforced by results (Wasiuzzaman et al., Citation2020) that one of the causes of difficulties for SMEs to access credit is the lack of available hard data, which financial institutions need to assess creditworthiness for loan requests. This creates a high credit risk for MSMEs (Ciftci et al., Citation2019; Mutamimah & Hendar, Citation2017; Mutamimah et al., Citation2021; Mutezo, Citation2013), who tend to receive more loans from small and medium-sized banks with whom they can interact personally and obtain long maturities (Yudaruddin, Citation2020). However, MSME owners are often ineffective in managing working capital, causing their asymmetric information for banks (Yudaruddin, Citation2020) and having a high credit risk (Mutamimah & Hendar, Citation2017). As expected, MSMEs have not developed given their limited access to finance (Maseko & Manyani, Citation2011; Myint, Citation2020). Abe et al. (Citation2015) stated that capital is an obstacle for MSMEs that do not manage working capital effectively and provide asymmetric information to banks, which hampers the application process and approval from the banking sector. Banks are not yet fully willing to provide loans to SMEs, due to having less information than that held by SMEs, causing irregularities in the management of loan capital and reinforced by the lack of financial statement data (Claessens & Tzioumis, Citation2006).

2.2. Agency theory, corporate governance and credit risk for MSMEs

Corporate governance was developed from agency theory (Jensen & Meckling, Citation1976), which states that agency conflict occurs when asymmetric information exists between the agent and the principal. Specifically, the information held by banks as principals is less than that held by MSMEs as agents. In this scenario, MSMEs often misuse the use of loan capital for consumption purposes rather than on business development, the lack of which causes difficulties in repaying their loans on time. Many methods and systems are applied by banks to evaluate creditworthiness and to prevent the credit risk. One method is corporate governance as a system, structure and mechanism to regulate and monitor the behaviours of MSME managers (Mutamimah et al., Citation2021). Therefore, applying corporate governance is important for MSMEs to follow its principles, namely: transparency, accountability, responsibility, independence and fairness. This is explained by stakeholders theory of corporate governance, its posits that all stakeholders (MSMEs, banking, suppliers, consumers, and government should concern on all stakeholders’ interests in its corporate governance process and have no stakeholders that get negative impacts. MSME managers are required to provide transparent financial and non-financial reports to banks and other stakeholders (Fülöp, Citation2014). Transparency can reduce information asymmetry between banks and MSMEs, thereby reducing credit risk. MSMEs must comply with corporate governance, such as with applicable regulations and regular monitoring and evaluation to demonstrate accountability. These tasks can help MSMEs to overcome irregularities in their management to continually and effectively run their business, and thus properly manage their credit risk (Ansong, Citation2013). MSMEs must be orderly in compiling financial reports at each period and with laws and regulations as a form of responsibility and independence to stakeholders, such as banks (Hanifah, Citation2015). MSMEs that apply fairness provide transparent and equal information disclosure on appropriate records and accounting standards to fulfil the rights of stakeholders such as banks (Abor & Adjasi, Citation2007; Hanifah, Citation2015). A standard for evaluating of MSMEs creditworthiness is corporate governance implementation as indicated by the 5C rule, as follows: Capacity, Capital, Character, Collateral and Condition. In addition, Juniarti and Omar (Citation2021) said that MSMEs credit risk evaluation relied on data to grant credit in supply chain finance. This system is used to evaluate the credit risk in three dimensions: financial status, non-financial status of SMEs, and transaction credit and reputation supervision based on the supply chain. However, the lack of financial data of MSMEs cause banks to rely on subjective perceptions for determining creditworthiness (Wasiuzzaman et al., Citation2020). This is also a source of credit risk, despite the bank having implemented corporate governance.

2.3. Blockchain technology and credit risk

Blockchain is an integration of several computer technologies including P2P networks, encryption algorithms, timestamps, consensus mechanisms and smart contracts. The blockchain has technical characteristics such as distributed storage, partial decentralisation, security, trustworthiness and resource openness (Zhang & Ma, Citation2020). Each user entity can then be allowed access to view, create or modify the selected data or records depending on its role (Dashottar & Srivastava, Citation2021). Blockchain requires large storage capacity and more processing power, which can speed up the creation of new records and search through current ones, as well as simplifying the active directory management. This capability not only improves data ownership and increases the credibility of information provided by users, but also addresses confidentiality and privacy concerns (Dashottar & Srivastava, Citation2021).

Credit data from the same information subject may be collected by several financial institutions as a resource of credit reporting agencies. When data ownership cannot be clearly determined, sharing data externally can lead to leakage of commercial information and cause harm to institutional interests (Zhang & Ma, Citation2020). Credit reporting is part of the financial infrastructure to prioritise the quality of credit data. Blockchain is a combination of several computer technology networks that can assist in credit reporting and solve difficult problems in sharing credit information in a targeted manner (Zhang & Ma, Citation2020). Liu et al. (Citation2021) found that the blockchain technology supported by the Internet of Things can facilitate the transformation of credible information and improve the information acquisition capabilities of traditional banks and regarding knowledge on collateral. In addition, the e-platform in the new architecture increases the involvement of banks in the supply chain and builds an equitable network to reduce warehousing risks. The use of smart contracts and collaborative mechanisms ensures process and outcome control in reducing liquidity risk. As a breakthrough technology, blockchain is leading a new period of global technological and industrial change.

One of the largest challenges faced by MSMEs is the hefty costs of credit and regulatory compliance, especially for negative accounts. MSMEs can start utilizing blockchain for cross-border payments and trade finance, to be used in managing credit risk (Dashottar & Srivastava, Citation2021). One of the uses of blockchain, which can be applied to MSMEs, is that users can make the network private and limit information transactions within one or a group of banks to effectively manage credit risk (Dashottar & Srivastava, Citation2021). Implementing blockchain can increase the speed of decision making and facilitate the rapid and efficient involvement of shareholders.

2.4. Corporate governance innovation based on blockchain technology

Blockchain can achieve an effective corporate governance, which when poorly implemented can be a major factor in corporate scandals and financial crises (Akgiray, Citation2019). Blockchain technology can eliminate several forms of negative intermediation and inefficiency, thus presenting great opportunities for better corporate governance (Akgiray, Citation2019; Lafarre & Van der Elst, Citation2018). This finding is supported by Mahyuni et al. (Citation2020) that blockchain can increase firm performance in terms of transparency, traceability, sustainability, trust and cost-efficiency. The potential of blockchain in improving corporate governance can be considered as an effective and efficient mechanism to ensure transparency and accountability in business affairs. Clarity and accessibility in communication channels on a peer-to-peer network infrastructure can help identify and fulfil responsibilities. Blockchain can observe the running of MSME management, and thus facilitates monitoring for fair and independent decision making (Akgiray, Citation2019). Blockchain in corporate governance can result in improved liquidity, lower fees, accurate records and transparent ownership (Daluwathumullagamage & Sims, Citation2020). Singh et al. (Citation2020) described Blockchain as a decentralised ledger system, where information is stored on computers and monitored by all stakeholders and allows for secure transactions without the need of any intermediary; however, cybercriminals can seize control over the network, and requires support in the implementation of corporate governance. Singh et al. (Citation2020) also stated that blockchain plays a vital role in effective corporate governance, which involves balancing the interest of different stakeholders of a company, such as the society, financial lenders, suppliers, customers, stakeholders and management. Blockchain helps corporate governance by increasing the transparency of the transactions of real estate, funds and shares.

Previous studies related to the application of blockchain technology in corporate governance in non-financial and non-SMEs fields have been carried out. For example, blockchain technology is used for operations management (OM) with supply chain management (SCM) in the airport industry from a sustainable performance perspective (DiVaio & Varriale, Citation2020). Data analysis was completed by reading and processing financial statements, non-financial reports and the website of one strategic airport infrastructure in southern Italy, and related information and data concerning blockchain technology and sustainable performance were collected. The A-CDM platform is one of the main blockchain technology applications in the airport industry that promotes cooperation between the main players in the aviation industry and the air traffic controllers (ATCs) to reduce fragmentation, inefficiency and uncoordinated operations. Najjar et al. (Citation2023) found that blockchain technology is used to integrate the complex multi-tier supply networks so as to reduce information asymmetry and opportunistic behaviours across the different tiers of the supply network, and thus can enhance the visibility and transparency of suppliers’ sustainability practices across the different layers of the supply network. The connectivity and rapid/immutable sustainable information sharing features associated with blockchain increase suppliers’ predictability and create robust sustainable supply networks. In addition, DiVaio et al. (Citation2023) found that blockchain technology is used to improve the value to gender equality (GE) and inclusion, in line with the Sustainable Development Goal (SDG) 5, through the technology-oriented corporate governance (CG) model. The study explains how blockchain must be used to promote GE in organisational environments, but also points out how it can worsen the marginalisation of women without implementation in a gender responsive manner. The findings indicate that Blockchain technology, characterised as a distributed technology, opens access to payments for women and overcomes obstacles related to the cultural, economic, social and national conditions of origin.

3. Research methods

This study proposes a research design using qualitative approach with Grounded theory analysis for data analysis, which includes open, axial and selective coding. This framework consists of two stages, namely, development and validation. Data collection is carried out for framework development using in-depth interviews, while framework validation was carried out using focus group discussions (FGDs). Informants of in-depth interviews include bank, government, MSMEs, suppliers, consumers, association, information technology experts, economic experts and production partners. The participants are from Central Java, distributed in four regions, namely, Semarang City, Semarang Regency, Solo City and Pekalongan Regency. The data analysis uses Grounded Theory, a systematic yet flexible method that emphasises data analysis, involves simultaneous data collection and analysis, uses comparative methods and provides tools for constructing theories/model/frameworks (Wertz et al., Citation2011). This data analysis consists of three main steps: first, open coding identifies the core concepts and their characteristics and dimensions; second, axial coding examines strategies, conditions and consequences; and third, selective coding builds the theory/frameworks (Glaser, Citation1992). This framework is validated by using FGDs. According to Ritchie et al. (Citation2003), typical focus groups involve 6–8 people who meet once, but the optimum group size depend on diversity in opinion on the issue, and a large group is more effective than a small one. The FGDs are carried out with various stakeholders (government, association, suppliers and banking) located in four different areas in Central Java, namely, Semarang City, Semarang Regency, Pekalongan Regency and Semarang City.

4. Results and discussion

4.1. Profiles of the informants and of FGD participants

The in-depth interviews are carried out with 23 informants, while the FGDs include 77 participants come from variated stakeholders, such as the government, association, suppliers and banking. The participants are located in Central Java that are distributed in four regions in Central Java, namely Semarang City, Semarang Regency, Solo City and Pekalongan Regency. Table shows the profile of the informants.

Table 1. Informants profile

This framework is validated by using four FGDs in four different areas in Central Java, namely, Semarang City, Semarang Regency, Pekalongan Regency and Semarang City. The total of FGD participants were 77 people representing of government, association, suppliers, banking, and MSMEs from the area mentioned. The profiles of the FGD participants are shown in Table .

Table 2. FGD participant profiles

4.2. Grounded theory analysis

This qualitative data analysis uses Grounded Theory. In this type of research design, a data analysis consists of three main steps: first, open coding that identifies the core concepts and their characteristics and dimensions; second, axial coding that examines strategies, conditions and consequences; and third, selective coding that builds a theory or framework.

4.2.1. Open coding

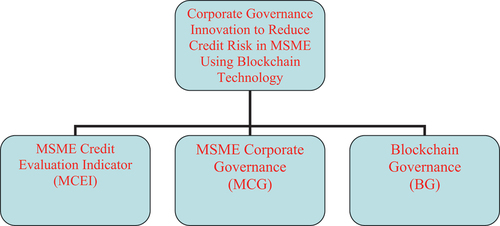

First, open coding is carried out to identify the core concepts and their characteristics and dimensions. The core concepts of corporate governance innovation to reduce credit risk in MSME using blockchain technology are then extracted, as shown in Figure .

Figure 1. Core concepts.

The extracted core concepts consist of MSME credit evaluation indicator (MCEI), MSME Governance (MG) and Blockchain Governance (BG). The characteristics and dimensions of each core concept are described in Table .

Table 3. Open coding for corporate governance innovation to reduce credit risk in MSME using blockchain technology

4.2.1.1. MSME’s credit evaluation indicators (MCEI)

To obtain credit, MSMEs must follow the procedure for granting credit. Procedure for granting credit means the stages that must be passed by MSMEs before it is decided to disburse credit. The goal is to make it easier for banks to assess the feasibility of a credit application, as shown in the following

Figure 2. Procedure for granting credit.

The credit applicant submits a proposal with attached required documents. The survey consists of Interview I, On the Spot and Interview II. On the spot is a field examination to review various objects that are used for business or collateral.

Banking regulates in assessing and determining eligibility to obtain credit, with the aim to reduce risks. Several banks use indicators to assess creditworthiness, such as the 5C as follows: Capacity, Capital, Character, Collateral and Condition (Wasiuzzaman et al., Citation2020). Capacity shows the borrower’s ability to meet debt and instalment payments. Capital is an investment of money in a business and size or level of risk of failure. Character is the attitude of MSMEs as borrowers in paying off their debts. Collateral is a form of guarantee owned by MSMEs as a safeguard if at any time the MSMEs cannot pay off their debts. Condition is an external condition that affects the MSME business operations. However, for larger loans, applying an assessment method using a feasibility study is necessary.

4.2.1.2. MSME corporate governance (MCG)

The results of in-depth interviews found several obstacles to evaluating MSME credit, including: a). Asymmetric information exists between banks as principals and MSMEs as agents, and therefore banks cannot properly access MSME business information and operations. b). MSMEs do not have standardised financial report data. Most MSMEs lack accounting knowledge and thus have no efficient records, which hinders the assessment of creditworthiness and causes adverse selection. In addition, the lack of knowledge of MSMEs has resulted in misuse, such as for consumption and for business development. In addition, the lack of financial and non-financial documents owned by MSMEs prompt banks to make invalid assessments based on the subjective perceptions of appraisers. This scenario causes an increase in bad loans. Therefore, to apply corporate governance is necessary for MSMEs to follow the principles of corporate governance, namely, transparency, accountability, responsibility, independence and fairness.

4.2.1.2.1. MSME stakeholders

Based on the results of in-depth interviews, MSME stakeholders have been identified. Furthermore, these stakeholders are selected in relation to the flow of information and transactions that can be used as evaluation material to reduce their credit risks. Stakeholders who are selected as participants in a blockchain-based system are described in Table .

Table 4. Participants in a blockchain-based system

4.2.1.2.2. MSME Stakeholders Business Transactions

In business, stakeholders are always involved, namely, government, suppliers, associations, production partners, financial institutions and consumers (See Table ). The government plays a role in providing assistance in the form of funds, equipment, training and implementation. The government has various policies to provide financing for MSMEs through grants or subsidies, organizing exhibitions, training and mentoring or simplifying tax administration for easier applications for MSMEs and business licenses. Suppliers provide raw materials, such as white cloth, stamps and dyes. The association consists of various MSMEs with a common vision and goals and thus they experience the same scenarios. The association holds exhibitions, exhibitions and even bridges communication with the government. Production partners are third parties who have sub-contracts with MSMEs that still cannot carry out the entire process independently. Financial institutions, including banking and non-banking, provide capital loans to allow MSMEs development. Consumers are stakeholders who are very important in the sustainability of MSMEs as a source of business continuity.

Table 5. Stakeholders model of transactions

4.2.1.2.3. Shared Information

Shared information is needed to reduce asymmetric information. Identification of such information is carried out through the flow of information between participants (stakeholders) in the network, as shown in Table .

Table 6. Shared information

4.2.2. Axial coding

In the axial coding, concepts are disaggregated into their components. Hence, the concepts extracted during the open coding are selected as categories to which other synonymous concepts are linked (See Figure ). The categories in axial coding are developed systematically and related to the subcategories (Table ).

Figure 3. Relations among categories.

Table 7. Categories in axial coding are developed systematically and related to the subcategories

4.2.3. Selective coding

4.2.3.1. Stakeholder interaction and control using Blockchain

Corporate governance is based on interest conflict between agents and principals, as explained by agency theory (Mutamimah et al., Citation2021). MSMEs’ corporate governance improves the quality and effectiveness of growth and profitability (Musah et al., Citation2022). Mutamimah et al. (Citation2021) found that corporate governance of MSMEs as shown by responsibility, independence and fairness do not affect SMEs’ credit risk Mutamimah et al. (Citation2021). Corporate governance of MSMEs is only arranged between banks as principals (creditor) and MSMEs as agents (debtor). Given that several business activities involve various stakeholders that can cause reduced sales of MSMEs, and thus they cannot pay off their loans, blockchain technology is needed as a corporate governance innovation. This finding is supported by Al Maqatari et al. (Citation2020) who stated that stakeholders such as policymakers, regulators, academicians and investors have a considerable interest in country-level corporate governance.

The consortium blockchain is chosen for the proposed platform, because of its higher transaction processing speed and flexible node authority settings. Every individual or group that can influence or be influenced by the goals of an organisation is a stakeholder (Freeman, Citation1984). Meanwhile, Atti et al. (Citation2019) describes a stakeholder is any person outside or inside the company who has a role in determining its success. Stakeholders are divided into two groups, namely, internal and external (Jones, Citation1995). Internal stakeholders are those who are within the scope of the company while external stakeholders exert influence from the outside. Mitchell et al. (Citation1997) showed the interdependence between companies and stakeholders.

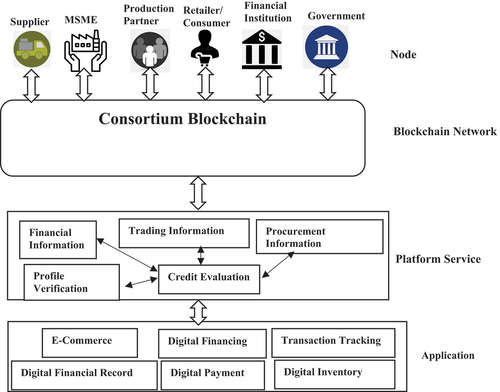

The blockchain-supported corporate governance innovation model for MSMEs includes six types of nodes, namely, MSMEs, Suppliers, Production Partners, Government, Financial Institutions and Retailers/Consumers. The nodes share data through platforms, as shown in Figure , with six types of participants, namely MSMEs, suppliers, production partners, consumers, financial institutions and the government.

Figure 4. Participants of the MSME blockchain network.

4.2.3.1.1. MSMEs

MSMEs are the subject of transactions on the platform, including suppliers and consumers. In this blockchain-based network, all MSMEs must upload relevant qualification information and historical transactions of the MSMEs are recorded. The blockchain ensures the authenticity of the data and cannot be falsified; thus, financial institutions can use the data to evaluate MSMEs loans without manual confirmation steps that are time-consuming, labour-intensive and costly. Blockchain platforms can also facilitate transactions between suppliers and retailers with the help of intelligent matching algorithms. Transaction information is recorded in the blockchain and cannot be changed, allowing MSMEs to track goods and logistics information. Moreover, the transparency of data can reduce asymmetric information.

4.2.3.1.2. Suppliers

The supplier offers logistics services for MSMEs on transportation, warehousing, inventory management and commodity management. Suppliers collect commodity inventory and logistics status information, including order information, availability information, transaction and delivery information and then update the data to the blockchain platform in real time. On the basis of such inventory information, financial institutions evaluate MSMEs loans and make decisions. Suppliers and retailers can track commodity logistics status at any time, which increases the trust of both parties and ensures the authenticity of transactions.

4.2.3.1.3. Production partner

Production partners offer services for several of the product manufacturing processes that are not carried out by MSMEs themselves. Such services include design, stamping/writing/printing, colouring, sizing and drying. With a production partner, MSMEs can save significantly on labour, materials and other costs related to production. However, service users must continue to carry out proper supervision to reduce their production costs, maintain the quality of their production and increase their profit margins. Production partners collect production status data—including service information, production request information, production information, transaction information, delivery information—and then update the data to the blockchain platform in real time. Financial institutions evaluate MSMEs loans and make decisions based on this information. MSMEs can track production status at any time, which increases the trust of both parties.

4.2.3.1.4. Retailer/Consumer

Consumers are buyers or users of product results, including direct users or retailers. The retailer/consumer collects information on product and availability, order, transaction and shipping and then updates the data to the blockchain platform in real time. Financial institutions evaluate MSMEs loans and make decisions based on sales information.

4.2.3.1.5. Financial institutions

On the platform, financial institutions provide facilities for distributing funds to MSMEs in need. Financial institutions can be banks or non-banks. Financial institutions evaluate MSMEs loans before channelling funds, and are hindered by the asymmetric information on MSMEs in producing accurate results. On the blockchain platform, financial institutions collect information on loans, submissions, disbursement, monitoring and from platforms related to MSMEs as a reference for accurate evaluations.

4.2.3.1.6. Government

The government acts as a regulator and facilitator, including the cooperatives and MSME offices, industry and trade offices and tax bureaus. In this framework, a consortium blockchain is used where the regulator is a specific node in the consortium blockchain which is responsible for reviewing the entry of new nodes and setting node permission levels.

4.2.3.2. Autonomous using smart contracts

Smart contracts are an important function in the blockchain technology model, because these can set the values that are conditions for transactions. Broadly speaking, smart contracts function to translate transactions that occur in the real world and convert them into programming languages on computers. In smart contracts, transaction terms are generally termed “asset value”, which must be met for a transaction to occur. Then, a product or material is interpreted into an asset in the blockchain, which is usually represented by an identification number. The smart contract design is shown in Table :

Table 8. Smart contracts

4.2.3.3. Application interaction using Blockchain network

Based on the results of the identification of problems faced by MSMEs and related stakeholders, a corporate governance innovation model using blockchain technology is developed to reduce credit risk, as shown in Figure .

Figure 5. Application Interaction using blockchain Network.

4.2.3.3.1. Profile verification

SMEs update their basic information to the platform through profile verification, which includes the registered capital of the company, type of company, certificate qualification and other information. Regulators use these data to evaluate whether nodes can enter the platform to transact with other nodes. MSMEs that are successfully registered can receive the services provided by the platform.

4.2.3.3.2. Trade information

Trading information consists of historical transaction data and current transaction status. Historical transactions include transaction totals, transaction amounts, transaction receipts and invoices, trading partners, default information and other data. The current transaction status includes order quantity and delivery date, payment amount and delivery date and product information from processing raw materials to final products. The data recorded on this platform is transparent and immutable, and therefore all nodes can access this information to make accurate judgments.

4.2.3.3.3. Procurement information

Procurement information includes data on order, availability, transaction and delivery information collected by the supplier. First, inventory management is important for MSME information management. MSMEs can easily manage inventory information by calling the procurement information module; In addition, inventory is the main guarantee factor in MSME financing. Financial institutions can also obtain procurement information to determine the MSME capacity. More importantly, buyers and sellers can obtain cargo transportation information to confirm transaction status through this module.

4.2.3.3.4. Financial information

Financial information consists of information on cash flow, profitability and leverage, liquidity, activity and investment ratios. Financial institutions also check pawned goods from time to time through this module. More importantly, buyers and sellers can obtain cargo transportation information to confirm transaction status through this module.

4.2.3.3.5. Credit evaluation

The credit evaluation module allows financial Institutions to examine the company credit before providing financial support to MSMEs. Banks can use the credit evaluation module to assess MSME loans and provide funds according to the results of the assessment. To ensure the reliability of the transaction, the buyer and seller evaluate each other by calling the credit evaluation module, and the results are important basis for both parties.

4.3. Validation result of frameworks

After the framework model has been developed, the next step is to validate the framework using the FGDs. Ritchie et al. (Citation2003) stated that usually, a participant in FGD consists of 6 to 8, but large participant is allowed if they have a different perspective, and different area. The area includes Semarang City, Semarang Regency, Pekalongan Regency and Semarang City. The participants of FGD are consisting of stakeholders: government, association, suppliers, banking, and MSMEs. This FGD process used the guidelines by explaining the framework of blockchain technology as a corporate governance innovation to reduce the credit risks of MSMEs, then asking for participants’ perception, then the results of FGD is presented in Table .

Table 9. Validation Result of blockchain technology as corporate governance innovation framework

Based on Table , the results show that corporate governance innovation frameworks using Blockchain technology to reduce MSME credit risk are valid. Specifically, the details are as follows: 1) Four stakeholders—government, association, suppliers and banking—consider that blockchain technology is potentially easy to use. Only MSMEs consider otherwise, possibly because the majority of MSMEs are between 50–70 years old (65%) who face difficulties in using blockchain technology; 2). All stakeholders consider that blockchain technology shows potential in reducing MSME credit risk; 3) All stakeholders assess that blockchain technology can also increase transparency; 4) Of the five stakeholders, only the government and banks can access data on blockchain technology at any time quickly. The reason is that associations, suppliers and MSMEs do not yet have sophisticated information technology and Internet signals are often interrupted; 5) All stakeholders consider that the data on the blockchain technology network cannot be changed without the agreement of all stakeholders involved in the blockchain networks; 6) Governments, associations, suppliers, banking and MSMEs consider that blockchain technology shows potential in eliminating the asymmetric information between stakeholders; 7) All stakeholders consider that Blockchain technology can increase fairness between stakeholders; 8) Government, association, suppliers, banking and MSMEs assess that blockchain technology has the potential to support the growth of MSMEs; 9) All stakeholders believe that blockchain technology can help eliminate fraud and moral hazards; 10) All stakeholders consider that blockchain technology can facilitate the increase responsibility and accountability.

5. Conclusion and implications

This study aims to develop blockchain technology frameworks as corporate governance innovations in reducing credit risk for MSMEs. The design is qualitative research using grounded theory for data analysis, consisting of open, axial and selective coding. Results of in-depth interviews with selected informants show that blockchain technology can facilitate the recording, partial decentralisation and storage of business and financial transactions on a digital network. All stakeholders can access but cannot change information in a transparent and valid manner. Thus, blockchain technology offers the potential to reduce asymmetric information and increase of transparency, accountability, responsibility and fairness. In addition, this technology can help reduce MSME’s credit risk and increase their performance and sustainability. The frameworks are then tested using FGDs from various stakeholders in four regions. The FGD results show the validity of the proposed frameworks. This research design frameworks of corporate governance innovation are based on blockchain technology in reducing credit risk only in Indonesian MSMEs. So, it cannot be generalized in other cases or different country.

5.1. Theoretical Implication

This study can develop agency theory and stakeholder theory in explaining corporate governance innovations based on blockchain technology. By this, all stakeholders’ interests are taken into account, and no stakeholders are harmed. In addition, this research can be used as a basis for developing research on corporate governance with blockchain technology in other fields, such as insurance, educational institutions and hospitals.

5.2. Managerial Implications

This study can encourage MSMEs and also can be a guide to apply corporate governance mechanism based on blockchain technology so that it can reduce asymmetric information and credit risk. In addition, MSMEs can be easy to get financial access from banking or other financial institution. Therefore, MSMEs need to improve their digital competence, infrastructure and budget.

Acknowledgments

The authors thank the Ministry of Education, Culture, Research and Technology of the Republic of Indonesia for the research funding 2022. The authors also gratitude to Universitas Islam Sultan Agung and informants for supporting our research project.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Mutamimah Mutamimah

Mutamimah, Mutamimah MSi is a lecturer of the Management Department, Faculty of Economics in Universitas Islam Sultan Agung Semarang. Her Bachelor’s degree in Management from Universitas Islam Indonesia, Master of Management, and economic doctoral degree from University of Gadjah Mada, Yogyakarta. Her research interests are financial management, corporate governance, and risk management.

Suryani Alifah

Dr. Suryani Alifah, MT is a lecturer of Faculty of Industrial Technology in Universitas Islam Sultan Agung Semarang, Indonesia. Her Bachelor of Electrical Engineering degree and Master’s degree in Electrical Engineering from Institut Teknologi Bandung. Her PhD in Electrical Engineering from Universiti Teknologi Malaysia. Her research interest is Information Communication Technology.

Made Dwi Adnjani

Made Dwi Adnjani, M.Si., M.I.Kom is a lecturer of Communication Studies, Faculty of Language and Communication in Universitas Islam Sultan Agung Semarang, Indonesia. Her Bachelor of Communication and Master of Communication Science from Universitas Diponegoro Semarang. Her research interests are Sociology, Media and Cultural Studies.

References

- Abe, M., Troilo, M., & Batsaikhan, O. (2015). Financing small and medium enterprises in Asia and the Pacific. Journal of Entrepreneurship and Public Policy, 4(1), 2–21. https://doi.org/10.1108/JEPP-07-2012-0036.

- Abor, J., & Adjasi, C. K. D. (2007). Corporate governance and the small and medium enterprises sector: Theory and implications. Corporate Governance the International Journal of Business in Society, 7(2), 111–122. https://doi.org/10.1108/14720700710739769.

- Akgiray, V. (2019). The potential for blockchain technology in corporate governance. OECD Corporate Governance Working Papers. 10.1787/ef4eba4c-en

- Al Maqatari, F. A., Farhan, N. H., Al-Hattami, H. M., Khalid, A. S. D., & Ntim, C. G. Impact of country-level corporate governance on entrepreneurial conditions. (2020). Cogent Business & Management, 7(1), 1797261. https://doi.org/10.1080/23311975.2020.1797261

- Ansong, A. (2013). Risk management as a conduit of effective corporate governance and financial performance of small and medium scale enterprises. Risk Management, 3(8), 352–678.

- Atti, G., Galantini, V., & Sartor, M. (2019). Stakeholder management. Quality Management: Tools, Methods, and Standards, 23–34. https://doi.org/10.1108/978-1-78769-801-720191002

- Ciftci, I., Tatoglu, E., Wood, G., Demirbag, M., & Zaim, S. (2019). Corporate governance and firm performance in emerging markets: Evidence from Turkey. International Business Review, 28(1), 90–103. https://doi.org/10.1016/j.ibusrev.2018.08.004.

- Claessens, S., & Tzioumis, K. (2006). Measuring firms’ access to finance. In Conference: Access to Finance: Building Inclusive Financial Systems, Organized by the Brooking Institution and the Word Bank in Washington, D.C., May 30-31. (pp. 1–25).

- Daluwathumullagamage, D. J., & Sims, A. Blockchain-enabled corporate governance and regulation. (2020). International Journal of Financial Studies, 8(2), 1–41. https://doi.org/10.3390/ijfs8020036

- Dao, B. T., & Pham, H. (2015). Corporate governance and bank credit risk: Default probability, distance to default. SSRN Electronic Journal, 1–22. https://doi.org/10.2139/ssrn.2708994

- Dashottar, S., & Srivastava, V. (2021). Corporate banking—risk management, regulatory and reporting framework in India: A blockchain application-based approach. Journal of Banking Regulation, 22(1), 39–51. https://doi.org/10.1057/s41261-020-00127-z.

- DiVaio, A., Hassan, R., & Palladino, R. (2023). Blockchain technology and gender equality: A systematic literature review. International Journal of Information Management, 68, 102517. Retrieved from. https://doi.org/10.1016/j.ijinfomgt.2022.102517

- DiVaio, A., & Varriale, L. (2020). Blockchain technology in supply chain management for sustainable performance: Evidence from the airport industry. International Journal of Information Management, 52, 102014. https://doi.org/10.1016/j.ijinfomgt.2019.09.010

- Freeman, R. E. (1984). Strategic management: Astakeholder approach. In Pitman.

- Fülöp, M. T. (2014). Why do we need effective corporate governance? International Advances in Economic Research, 20(2), 227–228. Retrieved from. https://doi.org/10.1007/s11294-013-9430-3.

- Glaser, B. G. (1992). Emergence vs. Forcing: Basics of grounded theory analysis. Sociology Press.

- Hanifah, H. (2015). The implementation of good corporate governance in efforts to increase profit in small medium enterprises (SMEs). International Journal of Business, Economics and Law, 7(3), 38–45.

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jones, T. M. (1995). Instrumental stakeholder theory: A synthesis of ethics and economics. Academy of Management Review, 20(2), 404–437. https://doi.org/10.2307/258852

- Juminawati, S., Hamid, A., Amalia, E., Mufraini, M. A., & Mulazid, A. S. (2021). Impact of small and medium enterprises on economic growth and development. Budapest International Research and Critics Institute-Journal (BIRCI-Journal), 4(3), 5697–5704. https://doi.org/10.33258/birci.v4i3.23685697

- Juniarti, R. P., & Omar, A. (2021, November). Technology Adoption in Small and Medium Enterprises (SMEs). Proceedings of the BISTIC Business Innovation Sustainability and Technology International Conference (BISTIC 2021) (pp. 91–101). Atlantis Press.

- Karlan, D., Bryan, G., Jakiela, P., & Keniston, D. (2015). Direct and indirect impacts of credit for SMEs. Research Note, 670. Retrieved from. http://pedl.cepr.org/sites/default/files/ResearchNote_670_KarlanBryanJakielaKeniston.pdf

- Kolapo, T. F., Ayeni, R. K., & Oke, M. O. (2012). Credit risk and commercial banks’ performance in Nigeria: A panel model approach. Australian Journal of Business and Management Research, 2(2), 31–38. https://doi.org/10.52283/NSWRCA.AJBMR.20120202A04

- Kurniawati, S. L., Sari, L. P., & Kartika, T. P. D. (2018). Development of good SME governance in Indonesia: An empirical study of Surabaya. International Journal of Economics & Management, 12(1), 305–319.

- Lafarre, A., & Van der Elst, C. (2018). Blockchain technology for corporate governance and shareholder activism. SSRN Electronic Journal, 07. https://doi.org/10.2139/ssrn.3135209

- Lemieux, V. L. (2016). Trusting records: Is blockchain technology the answer? Records Management Journal, 26(2), 110–139. https://doi.org/10.1108/RMJ-12-2015-0042.

- Liu, L., Zhang, J. Z., He, W., & Li, W. (2021). Mitigating information asymmetry in inventory pledge financing through the Internet of things and blockchain. Journal of Enterprise Information Management, 34(5), 1429–1451. https://doi.org/10.1108/JEIM-12-2020-0510.

- Mahyuni, L. P., Adrian, R., Darma, G. S., Krisnawijaya, N. N. K., Dewi, I. G. A. A. P., Permana, G. P. L., & Foroudi, P. Mapping the potentials of blockchain in improving supply chain performance. (2020). Cogent Business & Management, 7(1), 1788329. https://doi.org/10.1080/23311975.2020.1788329

- Maseko, N. (2011). Accounting practices of SMEs in Zimbabwe: An investigative study of record keeping for performance measurement (A case study of Bindura). Journal of Accounting and Taxation, 3(8), https://doi.org/10.5897/jat11.031

- Maseko, N., & Manyani, O. (2011). Accounting practices of SMEs in Zimbabwe: An investigative study of record keeping for performance measurement (A case study of Bindura). Journal of Accounting and Taxation, 3(8), 171–181. https://doi.org/10.5897/jat11.031.

- Mitchell, R. K., Agle, B. R., & Wood, D. J. Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. (1997). Academy of Management Review, 22(4), 853–886. https://doi.org/10.2307/259247

- Musah, A., Padi, A., Okyere, B., Adenutsi, D. E., & Ayariga, C. (2022). Does corporate governance moderate the relationship between internal control system effectiveness and SMEs financial performance in Ghana? Cogent Business & Management, 9(1). https://doi.org/10.1080/23311975.2022.2152159.

- Mutamimah, & Hendar. (2017). Islamic financial inclusion: Supply side approach. Proceedings of the 5th ASEAN International University Conference on Islamic Finance (5th AICIF) (pp. 1–9).

- Mutamimah, M., Tholib, M., & Robiyanto, R. (2021). Corporate governance, credit risk, and financial literacy for small medium enterprise in Indonesia. Business: Theory and Practice, 22(2), 406–413. https://doi.org/10.3846/btp.2021.13063.

- Mutamimah, M., Zaenudin, Z., & Cokrohadisumarto, W. B. M. Risk management practices of Islamic microfinance institutions to improve their financial performance and sustainability: A study on Baitut Tamwil Muhammadiyah, Indonesia. (2022). Qualitative Research in Financial Markets, 14(5), 679–696. https://doi.org/10.1108/QRFM-06-2021-0099

- Mutezo, A. (2013). Credit rationing and risk management for SMEs: The way forward for South Africa. Corporate Ownership & Control, 10(2), 153–163. https://doi.org/10.22495/cocv10i2c1art1.

- Myint, O. M. (2020). The effect of financial access on performance of SMEs in Myanmar. International Journal of Scientific & Research Publications (IJSRP), 10(6), 244–254. https://doi.org/10.29322/ijsrp.10.06.2020.p10230.

- Najjar, M., Alsurakji, I. H., El-Qanni, A., & Nour, A. I. (2023). The role of blockchain technology in the integration of sustainability practices across multi-tier supply networks: Implications and potential complexities. Journal of Sustainable Finance & Investment, 13(1), 744–762. https://doi.org/10.1080/20430795.2022.2030663.

- Postnova, A. (2012). Does good corporate governance reduce credit risk?. Helsinki. https://helda.helsinki.fi/dhanken/bitstream/handle/10138/37072/postnova.pdf?sequence=5&isAllowed=y

- Ritchie, J., Lewis, J., Nicholls, C. M., & Ormston, R. (2003). Qualitative research practice: A guide for social science students and researchers. SAGE.

- Singh, H., Jain, G., Munjal, A., & Rakesh, S. (2020). Blockchain technology in corporate governance: Disrupting chain reaction or not?. Corporate Governance, 20(1), 67–86. https://doi.org/10.1108/CG-07-2018-0261

- Smith, K. J., & Dhillon, G. (2020). Assessing blockchain potential for improving the cybersecurity of financial transactions. Managerial Finance, 46(6), 833–848. https://doi.org/10.1108/MF-06-2019-0314.

- Susan, M. (2020). Financial literacy and growth of micro, small, and medium enterprises in West Java, Indonesia. International Symposia in Economic Theory and Econometrics, 27, 39–48. https://doi.org/10.1108/S1571-038620200000027004

- Tambunan, T. T. H. (2017). Msmes and access to financing in a developing economy: The Indonesian experience. Financial Entrepreneurship for Economic Growth in Emerging Nations, 148–172. https://doi.org/10.4018/978-1-5225-2700-8.ch008

- Wasiuzzaman, S., & Nurdin, N. (2019). Debt financing decisions of SMEs in emerging markets: Empirical evidence from Malaysia. International Journal of Bank Marketing, 37(1), 258–277. https://doi.org/10.1108/IJBM-12-2017-0263.

- Wasiuzzaman, S., Nurdin, N., Abdullah, A. H., & Vinayan, G. (2020). Creditworthiness and access to finance: A study of SMEs in the Malaysian manufacturing industry. Management Research Review, 43(3), 293–310. https://doi.org/10.1108/MRR-05-2019-0221

- Wertz, F. J., Charmaz, K., McMullen, L. M., Josselson, R., Anderson, R., & McSpadden, E. (2011). Five ways of doing qualitative analysis: Phenomenological psychology, grounded theory, discourse analysis, narrative research, and intuitive inquiry. The Guilford Press.

- Yoshino, N., & Taghizadeh-Hesary, F. (2018). The roles of SMEs in Asia and their difficulty in assessing finance. Asian Development Bank Institute Working Paper, 1. https://www.adb.org/sites/default/files/publication/474576/adbi-wp911.pdf

- Yudaruddin, R. (2020). Determinants of micro-, small-and medium-sized enterprise loans by commercial banks in Indonesia. The Journal of Asian Finance, Economics & Business, 7(9), 19–30. https://doi.org/10.13106/jafeb.2020.vol7.no9.019

- Zhang, Y., & Ma, Z. F. (2020). Impact of the COVID-19 pandemic on mental health and quality of life among local residents in Liaoning Province, China: A cross-sectional study. International Journal of Environmental Research and Public Health, 17(7), 1–12. https://doi.org/10.3390/ijerph17072381.