?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examined the influence of gender diversity on capital structure decisions among Ethiopian banks from 2010 to 2022. Clarifying the relationships between board composition and strategic financing choices carries academic and practical significance. Research questions focused on whether representation impacts leverage levels and the consistency of effects across contexts. The study aimed to address gaps in understanding governance’s implications in developing markets like Ethiopia. Annual reports of 15 established banks provided data on leverage, gender diversity percentages, board size and other governance traits, profitability metrics, and bank-specific characteristics. Panel data techniques, including GMM regression, addressed endogeneity concerns. Key findings found gender diversity consistently correlated with lower debt utilization, aligning with notions of improved monitoring. However, board size revealed nuanced relationships dependent on strategic considerations. The larger bank scale did not definitively elevate borrowing as predicted, indicating contextual contingencies warrant examination. Profitability is positively associated with leverage, as anticipated based on theoretical underpinnings. The research provides initial insights yet highlights avenues for deeper contextualized analyses. Continued learning promises to further our understanding of diversity’s strategic implications and empower balanced policies that leverage inclusion’s advantages.

PUBLIC INTEREST STATEMENT

This research examined how the makeup of corporate boards related to key financing choices within Ethiopia’s banking sector. Specifically, I studied if greater female representation on boards is connected to lower debt usage.

Why does this matter? A bank’s decision to rely more on debt or equity carries risk and return implications, impacting stability and growth. Meanwhile, ensuring diverse voices informs better decisions. The study’s findings provided preliminary insight, showing gender diversity consistently linked to more conservative debt levels. However, inconsistencies also emerged, emphasizing complexity requires nuanced thinking. Overall, continued learning can support a balanced policy. Evidence representation subtly shapes choices and warrants attention as regulatory frameworks progress. Understanding diversity’s subtle impacts also fosters well-rounded discussion. For the public, executives, and regulators, examining governance implications presents value. As environments change, clarifying relationships and optimizing board composition to harness diversity promises economic benefits.

1. Introduction

Firms’ capital structure decisions significantly impact risk profiles, performance, and valuation (Bandyopadhyay & Barua, Citation2016; Elmagrhi et al., Citation2018; Nouvellon & Pirotte, Citation2021; Tchakoute Tchuigoua, Citation2015). Optimizing structure necessitates exploring determinant factors, yet board diversity’s role has received insufficient attention (Al-Bassam et al., Citation2015; Ntim & Soobaroyen, Citation2013). This study addresses that gap by investigating gender diversity’s influence on banks’ structure in Ethiopia, adding to calls for localized diversity analyses.

Previous research indicates sound governance contributes to positive outcomes and stakeholder protection (Harasheh & De Vincenzo, Citation2023; Lu et al., Citation2022; Ntim & Soobaroyen, Citation2013; Pathak & Chandani, Citation2023; Singh & Nejadmalayeri, Citation2004). Studies found board diversity and composition positively impact financial and non-financial performance (Liang et al., Citation2011, Citation2011; Lu et al., Citation2022; Nguyen et al., Citation2020). However, developing nations face challenges in implementing governance standards (Liang et al., Citation2011; Pathak & Chandani, Citation2023; Singh & Nejadmalayeri, Citation2004). Ethiopian firms lag internationally in some areas, with enforcement remaining an obstacle (Börzel & Hackenesch, Citation2013; Tesemma, Citation2016). Research shows governance correlates with bank performance (Dessie, Citation2017; Tesemma, Citation2016), though compliance varies. Factors like board composition, independence, and size link to better outcomes (Menicucci & Paolucci, Citation2022; Mensah & Onumah, Citation2023). However, credit market discrimination persists (Gyapong et al., Citation2019; Weis et al., Citation2022), indicating governance issues impact decisions. While Ethiopia implemented policies promoting gender equality, socio-cultural norms and capacity limited progress (Ayalew & McMillan, Citation2021).

Theoretical and empirical gaps drive this study. Empirically, limited research considers diversity’s effect on decisions (Elmagrhi et al., Citation2018; Gyapong et al., Citation2019; Weis et al., Citation2022), despite evidence that balance enhances strategy (Issa et al., Citation2022). Gaps remain in representation and inclusion. Understanding diversity’s impact addresses SDG 5 goals (Kassie et al., Citation2013; Krstevska et al., Citation2017; Kyissima et al., Citation2020; Thippayana, Citation2014). This study investigates representation’s influence on leverage ratios and whether effects vary based on firm or macro traits.

This aims to address gaps by incorporating recent Ethiopian bank data and examining gender diversity’s nuanced impacts (Ayalew & McMillan, Citation2021; Nandom Yakubu & Oumarou, Citation2023). It considers wide-ranging determinants (Ayalew & McMillan, Citation2021), rigorously tests theories’ explanatory powers, and provides evidence-based inclusion policies promoting growth sustainably in line with extant literature (Al-Bassam et al., Citation2015; Bandyopadhyay & Barua, Citation2016; Nouvellon & Pirotte, Citation2021; Ntim, Citation2015; Ntim & Soobaroyen, Citation2013; Tchakoute Tchuigoua, Citation2015).

Despite evidence that gender balance enhances strategic decision-making, gaps persist in representation and inclusion. To make progress towards SDG 5 on gender equality, we must first understand the impact of diversity on crucial business outcomes like capital structure. This study investigates two salient yet under-researched questions: RQ1: Does gender diversity on corporate boards influence the capital structure as measured through financial leverage ratios? RQ2: Do the effects of gender diversity on leverage vary based on firm or macroeconomic characteristics?

This study aimed to address gaps in previous research on the impact of corporate governance on capital structure decisions in developing countries, with a focus on Ethiopia. It made several valuable contributions to the existing literature. The present study builds upon prior research by incorporating multiple theoretical frameworks proposed by Lu et al. (Citation2022) and employing a more recent dataset encompassing listed banks in Ethiopia. Unlike Ayalew and McMillan’s (Citation2021) study, which concentrated on private banks, this research extends its analysis to include listed banks, broadening the scope of the investigation. Furthermore, this study delves into the impact of gender diversity on capital structure decisions, a dimension not explored in the research conducted by Nandom Yakubu and Oumarou (Citation2023). However, it is worth noting that this study focuses solely on gender diversity and its influence on capital structure without considering other study variables such as bank-specific and macroeconomic factors. This novel approach adds depth to the understanding of governance and financing choices, shedding light on the unique role of gender diversity in shaping capital allocation strategies in Ethiopian banks.

The study contributes in several important ways. First, the empirical analysis rigorously examines the relationship between gender diversity, corporate governance, and capital structure in Ethiopia’s emerging economy. This new look at the intersection of gender representation and corporate financing decisions uncovers insights that can help policymakers promote inclusion, reduce gender disparities, and create equitable opportunities in line with SDG 5. Second, the study used an expansive panel dataset tracking 15 commercial banks in Ethiopia over a recent 13-year period from 2010–2022 to robustly explore the nuanced effects of gender diversity on leverage. Cutting-edge econometric techniques, difference GMM, and linear dynamic GMM, and overcome endogeneity concerns. Third, the analysis will encompass a holistic range of bank-specific and macroeconomic determinants of capital structure beyond gender factors, elucidating a multifaceted picture. Fourth, through rigorous hypothesis testing, the study will assess whether mainstream capital structure theories sufficiently explain financing behavior or if new perspectives are needed to capture gender’s influence. Finally, concrete evidence-based policy recommendations will be presented to foster gender balance at the upper echelons of Ethiopian corporations. In totality, the study makes significant strides to elucidate the role of gender diversity in financial decision-making and provide an invaluable knowledge base for promoting sustainable growth.

The study was organized into seven main sections, starting with an introduction outlining the research objectives, questions, and motivations. A background section that provided context on Ethiopia’s banking industry, issues with corporate governance and capital structure, and the need for the research came after this. A theoretical literature review then analyzed relevant theories, including agency theory, resource dependence theory, behavioral theories, critical mass theory, social role theory, and contingency theory. An empirical literature review and hypothesis development summarized prior evidence on board size and diversity, identified research gaps, and developed testable hypotheses. Next, a research design section detailed the sample and data, the operationalization of variables, and the specification of the analytical model. An empirical results and discussion section covered the statistical analysis and findings, robustness checks, and implications. Finally, a conclusion summarized the study’s key findings, contributions, limitations, future research directions, and theoretical and practical implications. Overall, the paper was organized in a way that made sense. It started by putting the study in its literary and historical context, and then went on to describe the methodology, the results, and the implications and future directions. Each part of the research was made clearer by its own section.

2. Background of the study

Ethiopia provides an important context to examine corporate governance’s influence on capital structure given the country’s extensive banking reforms and regulatory changes in recent decades. As emerging economies like Ethiopia transition and open their financial systems, corporate governance practices come under increasing scrutiny (Bezabeh & Desta, Citation2014). Although Ethiopia has taken steps to strengthen governance standards, gaps remain due to weak enforcement and implementation. Examining how governance and regulation affect banks’ financing choices can reveal areas for improvement.

Since the 1990s, Ethiopia has undertaken major reforms to modernize and expand its banking industry (Robertson, Citation2009). Regulatory oversight from the National Bank of Ethiopia (NBE) has driven changes in bank practices and performance (Hagos & Asfaw, Citation2014). However, research shows NBE policies have not fully resolved corporate governance deficiencies among Ethiopian banks (Hagos & Asfaw, Citation2014). Issues like limited board independence and diversity have persisted. Discrimination in lending markets also continues despite reforms aimed at inclusion (Weis et al., Citation2022). These weaknesses in governance likely influence how banks make financing and capital structure decisions. Studies demonstrate links between board practices and bank performance in Ethiopia (Tesemma, Citation2016). More independent boards and gender diversity are associated with higher profitability (Weis et al., Citation2022). This suggests shortcomings in governance, like concentrated power and minimal female representation, may negatively impact capital allocation and structure.

The need to promote sound governance is recognized in Ethiopia’s regulatory efforts. Corporate governance codes and banking reforms have sought to enhance board oversight and transparency (Robertson, Citation2009). However, legislative changes alone cannot resolve the cultural and systemic issues underlying poor governance. Given these regulatory pressures and remaining challenges, an in-depth examination of corporate governance’s influence on banks’ financing decisions is warranted. This can reveal where governance gaps manifest in capital structure outcomes. Findings may highlight areas for regulatory or policy enhancements to strengthen governance practices. Additionally, understanding these relationships provides banks with insights to improve governance mechanisms and capital allocation strategies.

Overall, Ethiopia’s extensive banking reforms juxtaposed with persistent governance issues make it an apt context to study corporate governance’s impact on capital structure. Regulatory efforts to date provide a foundation. However, research signals more work is required to align bank practices with policy goals. Examining how governance affects financing choices gives stakeholders’ valuable insights into mechanisms shaping banks’ capital allocation amidst reform efforts. This can inform measures to strengthen governance and responsible financing in Ethiopia’s banking sector. This study provides valuable new insights into the factors influencing the capital structures of banks in Ethiopia (Ayalew & McMillan, Citation2021). By applying multiple theoretical frameworks and utilizing recent data on listed banks, the research provides a more holistic examination of corporate governance’s impact on financing decisions (Lu et al., Citation2022). Unlike prior work focusing only on private banks (Ayalew & McMillan, Citation2021), this study analyzes listed banks while also considering the effect of gender diversity, an important angle not explored previously. Researchers employed the generalized method of moments (GMM) technique instead of traditional panel methods plagued by endogeneity issues (Ayalew & McMillan, Citation2021), yielding findings with greater validity. The outcomes carry practical implications, indicating how corporate governance and capital structure theories shape Ethiopian bank managers’ capital structure choices. Armed with these insights, executives can make more informed decisions regarding their optimal financing mix.

3. Theoretical literature review

This study adopts an integrative theoretical framework incorporating agency, resource dependence, and behavioral theories to examine corporate governance’s influence on capital structure. In this manuscript, I delve into the rich literature on corporate governance, drawing insights from the seminal work of Lu et al. (Citation2022). Our theoretical review section takes a comprehensive approach, examining the Economic and Governance Perspective (Agency Theory) and the Resource-oriented Perspective.

3.1. Agency theory, board gender diversity, and leverage (capital structure)

Agency theory provides a useful lens for understanding governance mechanisms’ role in aligning manager and shareholder interests to reduce agency costs. Characteristics of corporate boards, such as gender diversity, can help monitor financing choices and mitigate risks arising from conflicts of interest (Jizi et al., Citation2014; Sarhan et al., Citation2018). Recently, Ziyadeh et al. (Citation2023) demonstrated that governance practices moderate the impact of gender diversity on capital structure, improving oversight. Agency theory provides a useful lens for understanding how corporate governance mechanisms may impact capital structure decisions. At its core, agency theory posits that conflicts can emerge between shareholders (principals) and managers (agents) as their risk preferences differ (AA Zaid et al., Citation2020). When managers make financing choices that do not maximally benefit shareholders, agency costs arise (Amin et al., Citation2021).

Several studies have found evidence supporting agency theory’s proposition that increasing board independence, size, and gender diversity can help minimize such agency problems (García & Herrero, Citation2021). Larger and more independent boards, as well as those with greater female representation, are believed to enhance monitoring ability over management and curb discretionary behaviors (AA Zaid et al., Citation2020). This ostensibly leads to capital structure selections that are closer aligned with shareholders’ best interests (Nguyen et al., Citation2020; Sarhan et al., Citation2018). Notably, multiple empirical analyses have demonstrated that gender diversity, in particular, may play a moderating role in the governance-leverage relationship (Amin et al., Citation2021; Ben Saad & Belkacem, Citation2021). When more women are present in the boardroom, monitoring of financial policies seems to strengthen (García & Herrero, Citation2021).

However, agency theory has been criticized for erroneously assuming rational, self-interested actors when real-world behaviors are impacted by social and situational complexity (Ezeani et al., Citation2022). Additionally, results must be interpreted cautiously due to variances in research contexts, timeframes, and analytical methodologies between studies (Allini et al., Citation2015). Long-term, multi-country studies could help address these issues and better clarify precise impact pathways (Nguyen et al., Citation2020). Alternative frameworks considering behavioral implications may also offer additional insights overlooked by agency logic. Overall, while provoking useful debate, more work is still needed before definitive conclusions can be drawn.

3.2. Behavioral theory, board gender diversity, and capital structure

Behavioural theory provides an alternative perspective to agency theory’s rational assumptions in examining the relationship between corporate governance, capital structure, and board gender diversity. Behavioral theories recognize that cognitive biases and heuristics shape decision-making in systematic yet non-rational ways (Ali et al., Citation2023). Managers and board members are subject to social influences that impact objectivity. A key premise is that group diversity fosters debate and considers a wider range of perspectives, mitigating oversight shortcomings (Schneid et al., Citation2014). Notably, gender minority stress suggests women directors face unique social-psychological pressures that warrant more representation to properly account for.

Behavioral theories explain how governance practices shape group dynamics, impacting decisions. Social role theory notes that gender roles drive behaviors (Leventhal & Cameron, Citation1987; Nguyen et al., Citation2020), influencing how women’s participation impacts boards. Critical mass theory posits that a threshold percentage of women is needed to affect norms. Recent studies show critical mass improves CSR (Yang et al., Citation2019) and financial performance (Schneid et al., Citation2014). Recent empirical studies support these theories. Jizi et al. (Citation2014) find board independence lowers debt financing across U.S. firms (A.A. Zaid et al., Citation2020). show that gender-diverse boards improve debt ratios and governance in Malaysia. Yang et al. (Citation2019) provide evidence from China that female representation above 29% enhances CSR performance.

Empirically, studies have found board gender diversity positively impacts performance through these cognitive mechanisms rather than purely economic incentives, as agency theory predicts (Adusei & Obeng, Citation2019; Jouber, Citation2023). Effect sizes also differ across industries and national institutional contexts (Detthamrong et al., Citation2017; Schneid et al., Citation2014). However, overreliance on perceptual diversity assumptions overlooks complementary perspectives and downplays systematic biases. Additionally, small sample sizes in some analyses limit generalizability. Considering both rational and behavioral logics may offer a more complete picture of how board decisions unfold. Longitudinal, multi-level studies are still needed to disentangle network influences over time and fully validate underlying mechanisms. By integrating seminal theoretical foundations with recent empirical findings, this framework posits that board independence and gender diversity will positively influence capital structure decisions through enhanced oversight, resources, and gender balance dynamics. Examining how governance characteristics affect financing provides insights into mechanisms influencing responsible capital allocation. This can inform regulatory efforts to strengthen governance and firms’ competitiveness.

3.3. Resource dependency theory, board gender diversity, capital structure, and board size

Resource dependence theory posits that boards provide critical resources through their networks, expertise, and legitimacy (Alhossini et al., Citation2021; Ntim & Soobaroyen, Citation2013; Salancik & Pfeffer, Citation1978). Diverse boards expand resource pools, influencing financing access. Campopiano, Gabaldón, and Gimenez-Jimenez’s (Citation2022) work shows that minority directors provide unique resources that enhance equity financing.

The board of directors holds a crucial role in corporate governance, encompassing key responsibilities such as vision development, policy formulation, risk management, and resource utilization. They must adhere to ethical standards, promote transparency, and establish guidelines for conduct, accountability, and employee well-being. Resource dependency theory has been studied in relation to board size and its influence on various organizational outcomes. For example, Abeysekera (Citation2010) examined the impact of board size on intellectual capital disclosure by Kenyan listed firms, while Wang et al. (Citation2010) conducted an empirical analysis to determine if there is an optimal corporate board size. Sarhan, Ntim, and Al-Najjar (Citation2018) explored the relationship between board diversity, corporate governance, corporate performance, and executive pay. These studies contribute to our understanding of how board size affects organizational dynamics and performance. Furthermore, Ntim and Osei (Citation2011) investigated the impact of corporate board meetings on corporate performance in South Africa. The findings of these studies shed light on the role of board size in shaping organizational outcomes and offer insights for future research in this area (Lu et al., Citation2022).

Resource dependence theory provides a meaningful framework for investigating the relationships between board characteristics, capital structure, and leverage. The theory posits that firms rely on resources from external environments for survival (Salancik & Pfeffer, Citation1978). This dependence shapes organizational decision-making and structures. Larger boards can specifically aid access to valuable resources like advisory services and networks critical for financing decisions (Ahmed Sheikh & Wang, Citation2012; Butt & Hasan, Citation2009). The theory directly links board size to capital structure through its predicted mechanisms of expanded resource pools and networking functions. This suggests board size will moderate leverage levels as firms seek to mitigate environmental interdependence.

Prior empirical works have found support, with board size influencing debt ratios (Ahmed Sheikh & Wang, Citation2012; Butt & Hasan, Citation2009). However, national context also shapes resource contingencies, as Jackling and Johl (Citation2009) demonstrated. More recent analyses consider multiple governance aspects, as the theory implies (Nandom Yakubu & Oumarou, Citation2023). By accounting for interrelated board roles, theoretical adherence is strengthened. While not addressing behavioral elements like perceived independence, resource dependence theory adequately explains the structural reliance driving policy choices. Its overt connection to financing also surpasses agency theory’s relevance in this domain.

3.4. Contingency theory and other study variables

According to contingency theory, directors are required to respond to complex situations and strike a balance between internal and external factors through contingent actions, as there is no universally optimal approach to governing firms (Lu et al., Citation2022). Contingency theory provides a useful framework for investigating the moderating roles of various contextual factors. The theory posits there is no one best way to organize, and the most effective structure depends on contingencies like environmental dynamism, technology, size, and other key variables. As applied to banks, contingency theory suggests firm size influences the relationship between organizational characteristics and performance outcomes. Studies have examined how size moderates the effects of marketing strategies and digitalization (Hilal & Tantawy, Citation2022; Niemand et al., Citation2021).

Liquidity, economic conditions, and inflation also represent important contingencies. Research has tested their moderating role between characteristics like dividend policy, value, export performance, and profitability (Banalieva & Sarathy, Citation2011; Safari & Saleh, Citation2020). Even factors inside organizations like complexity and project management effort can act as contingencies shaping the profitability relationship (Feng & Fay, Citation2020; Kaufmann & Kock, Citation2022; Kazanjian & Drazin, Citation1990). Contingency theory thus provides a meaningful framework for understanding how various banking and environmental factors potentially strengthen or weaken linked relationships. Further research applying this lens could offer valuable contextual insights.

4. Empirical literature review and hypotheses development

4.1. Board gender diversity and leverage

The impact of gender diversity on corporate outcomes has gained significant attention, with higher representation of women on boards being associated with improved financial performance, enhanced monitoring of managers, and more effective decision-making processes. Several studies examine how board gender diversity impacts leverage and capital structure decisions in the banking and corporate sectors. Berhe (Citation2023) and Wondem and Batra (Citation2019) find that higher representation of women on boards is associated with lower debt ratios and higher performance in Ethiopian banks and firms. While Mehzabin et al. (Citation2023) and Yang et al. (Citation2019) do not specifically analyze gender diversity, they note the importance of board monitoring and governance for leverage decisions. In summary, studies provide evidence that higher representation of women on boards is associated with lower debt ratios and leverage, indicating gender diversity improves monitoring of financing choices. Research increasingly recognizes board gender diversity’s potential impacts, yet how it specifically shapes leverage levels remains understudied.

Prior work offers preliminary yet mixed evidence on this relationship. Ben Saad and Belkacem (Citation2022) found gender diversity lowered Algerian bank debt ratios, while García and Herrero (Citation2021) report null Spanish findings. AA Zaid et al. (Citation2020) observed that gender moderates Malaysian governance-leverage links, implying an interactive effect. Behavioral and resource theories provide rationales. From a behavioral perspective, diverse groups enhance decision quality by tackling oversight biases, which should influence leverage choices (Schneid et al., Citation2014). Women may also broaden strategic discussions on financial policy risks. Resource dependence theory suggests gender diversity expands board networks and advice channels on which firms rely for financing decisions (Hillman et al., Citation2007). Wider resource pools could strengthen leverage fitness. However, markets and cultural contexts likely shape gender diversity’s actual impacts. To help address these gaps, this study hypothesizes:

H1:

There is an inverse relationship between board gender diversity and bank leverage levels.

4.2. Board size (as proxy for corporate governance) and leverage

Existing studies indicate board size relates meaningfully to capital structure decisions such as leverage levels. However, the nature and contextual boundaries of this relationship warrant closer empirical examination. Prior work has found that board size influences leverage differently across settings. Ahmed Sheikh and Wang (Citation2012) observed an inverse Pakistani relationship, whereas Ezeani et al. (Citation2022) report no direct UK-France-Germany link. National institutions may shape size-leverage dynamics. Bokpin and Arko’s (Citation2009) Ghanaian findings suggested larger boards facilitate debt access, potentially by providing advisory resources and monitoring.

Hussain et al. (Citation2020) found size influences insolvency risk indirectly through leveraging in Pakistan versus Nigeria. Contingency theory implies different optimal board structures depending on strategic needs and environmental conditions. Size sufficient for advisory support in one context risks reduced oversight effectiveness elsewhere. Resource dependence theory also posits that board networks impact access to critical financing relationships. However, a threshold may exist where size sacrifices focus or independence. To further validate these perspectives and clarify boundary effects, this study hypothesizes:

H2:

There is an inverse relationship between bank board size and leverage.

4.3. Firm specific and macro-economic factors that influence capital structure

4.3.1. Bank size and leverage

Several studies examine how bank size impacts capital structure and leverage decisions. Birru (Citation2016) investigates the impact of capital structure on the financial performance of commercial banks in Ethiopia. The study finds that bank size, measured by total assets, is positively associated with debt ratios and leverage. Larger banks tend to have higher debt levels. Assfaw (Citation2020) studies the determinants of capital structure in Ethiopian private banks. The results show that bank size, measured by total assets or customer deposits, is positively related to debt ratios and the use of leverage.

Bukair (Citation2019) analyzes factors influencing Islamic banks’ capital structure in developing economies. The results show a positive correlation between debt ratios, leverage levels, and bank size, as measured by total assets or the number of branches. Bilgin and Dinc (Citation2019) examine factoring as a determinant of capital structure for large firms. They find that larger firms with more assets tend to have higher debt ratios and leverage. Ezeani et al. (Citation2022) investigate the impact of board governance on capital structure dynamics in UK, French, and German firms. While they do not explicitly study bank size, the results show that governance mechanisms influence leverage decisions. In conclusion, studies consistently show that larger bank sizes as measured by total assets, deposits, or branches are positively associated with higher debt ratios and leverage. Larger banks appear to rely more on debt financing. Thus, I can hypothesize that board size will have a positive impact on leverage decisions.

H3:

Larger bank sizes are positively associated with higher corporate leverage.

4.3.2. Profitability and leverage relationship

Several studies examine the relationship between profitability and leverage, finding mixed results. Osazuwa and Che-Ahmad (Citation2016) investigate the moderating effect of profitability and leverage on the relationship between eco-efficiency and firm value in Malaysia. However, they do not explicitly study the direct relationship between profitability and leverage. Rumler and Waschiczek (Citation2014) analyze how changes in financial structure have affected bank profitability in Austria. While they do not directly study the profitability-leverage relationship, the findings indicate that capital structure influences bank earnings.

Amidu (Citation2007) examines the determinants of capital structure for banks in Ghana. The study finds that higher bank profitability is associated with lower debt ratios and leverage. More profitable banks use less debt. Tarek Al-Kayed et al. (Citation2014) study the relationship between capital structure and the performance of Islamic banks. The results show that higher profitability is linked to lower gearing ratios and leverage, indicating profitable banks tend to be less leveraged.

However, Ayalew and McMillan (Citation2021) finds that higher levels of profitability are associated with higher debt ratios and leverage in Ethiopian private banks, indicating a positive relationship. Similarly, Agmas Wassie (Citation2020) and Zelalem (Citation2020) find evidence that higher profitability is correlated with higher leverage in Ethiopian construction companies and commercial banks, respectively. Despite these mixed findings, we propose the following hypothesis:

H4:

Profitability negatively affects leverage.

4.3.3. Liquidity ratio and leverage

Several studies find a negative relationship between bank liquidity and leverage, indicating that more liquid banks tend to have lower debt ratios. Ayalew and McMillan (Citation2021) examines the capital structure and profitability of Ethiopian private banks. The results show a correlation between higher liquidity ratios—as determined by the cash to total assets ratio and lower debt ratios and leverage.

Shibru (Citation2012) studies the determinants of capital structure for commercial banks in Ethiopia. According to the findings, banks with higher liquidity typically have lower gearing and debt ratios when compared to their total assets in terms of liquid assets. Udomsirikul et al. (Citation2011) investigate the relationship between liquidity and capital structure in Thai banks. They find that higher liquidity, as measured by cash holdings and liquid assets, is associated with lower leverage and debt levels. Zaman et al. (Citation2023) analyze whether bank affiliation affects firms’ capital structure, especially during financial crises. They do not explicitly study liquidity but note that bank financing decisions depend on factors like available internal resources.

Based on these findings, I hypothesize:

H5:

Higher bank liquidity ratios are negatively associated with corporate leverage.

4.3.4. Economic growth and leverage

Several studies find that macroeconomic factors like economic growth influence corporate capital structure and leverage decisions. Agmas Wassie (Citation2020) and Ayalew and McMillan (Citation2021) examine the determinants of capital structure for Ethiopian construction companies and private banks, respectively. While they do not explicitly study economic growth, they find that various firm-specific factors shape leverage decisions. Takele and Beshir (Citation2017) analyze factors determining insurance companies’ capital structure in Ethiopia. The results indicate that firm-level characteristics are more important determinants, though macroeconomic variables can also potentially influence leverage.

Graham et al. (Citation2015) provide a historical view of capital structure and leverage over the past century in corporate America. They find that macroeconomic conditions, like periods of economic growth, have impacted changes in debt usage over time. Ezeani et al. (Citation2022) investigate how board governance influences capital structure dynamics for UK, French, and German firms. While they do not explicitly study economic growth, the findings suggest contextual factors shape leverage decisions. Based on these findings, I hypothesize:

H6:

Faster economic growth is positively associated with higher corporate leverage.

4.3.5. Inflation and leverage

Several studies find that higher inflation is associated with lower corporate leverage. Hatzinikolaou et al. (Citation2002) study the impact of inflation uncertainty on capital structure using a sample of Dow Jones firms. They find that higher inflation is correlated with lower debt ratios and leverage; indicating firms adjust their financing mix under inflationary pressures. Homaifar, Zietz, and Benkato (Citation1994) develop an empirical model of capital structure and identify factors that influence financing decisions. Inflation is found to be negatively related to leverage; suggesting firms take on less debt during periods of high inflation.

Frank and Goyal (Citation2009) examine which factors reliably determine capital structure choices. They find that inflation is an important macroeconomic variable that tends to reduce corporate leverage. Adeneye and Kammoun (Citation2022) analyze how ESG performance influences capital structure decisions. While they do not explicitly study inflation, the findings indicate that macroeconomic factors shape financing choices. Based on these findings, I hypothesize:

H7:

Higher inflation rates are negatively associated with corporate leverage.

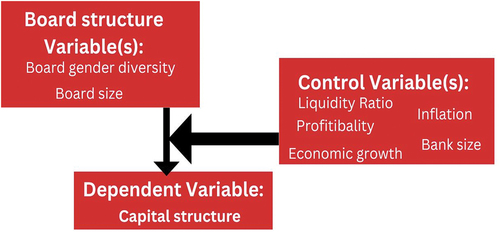

After reviewing the literature on determinants of capital structure in the Ethiopian context, a few key things stand out (Kibrom, Citation2010; Mekonnen, Citation2015). All the studies found that factors like profitability, size, growth opportunities, and tax benefits play an important role in how companies and banks decide their financing mix (Edeti & Garg, Citation2020; Wondem & Batra, Citation2019). Interestingly, regulatory pressure also seems to influence capital structure decisions in Ethiopia more than in developed markets (Mekonnen, Citation2015). In addition to static determinants, the research sheds light on the dynamic adjustment process. It appears Ethiopian firms target an optimal capital structure and move toward that target quickly when deviating too far, with overleveraged firms adjusting faster than underleveraged ones. Bank-specific traits like size and ownership further impact the speed and asymmetry of adjustment (Mekonnen, Citation2015). While more work remains, these findings start to provide useful insights for both academics and practitioners interested in the capital structure of Africa’s emerging markets. As a result, firms tend to take on less leverage under inflationary pressure. Given the study variables, the conceptual framework for the study is presented in Figure .

Figure 1. Conceptual framework.

5. Research design

5.1. Sampling and data collection

The researcher collected data to examine the relationship between various factors and the leverage levels of Ethiopian banks. The study made use of a panel dataset gathered from World Bank economic indicators and annual financial reports posted on the banks’ websites. The sample period spanned from 2010 to 2022. The study aimed to include all established banks in Ethiopia, which initially amounted to 17 at the time of the research. However, banks with incomplete or missing data for the sample period were excluded from the analysis. The final sample consisted of 15 banks, as summarized in Table . Data for the study was gathered from the publicly available annual reports and financial statements of the banks, ensuring the reliability and accuracy of the information used. Commercial banks (both private and state-owned) were utilized due to their access to reliable and comprehensive data as well as their large size. The study period was chosen based on consistent data availability. Given that the study relied solely on secondary financial and economic data sources, it did not involve primary data collection from human participants. As a result, ethical clearance for the research was not required. The researchers collected and analyzed financial data from the banks’ published financial reports over a 13-year period. While all established Ethiopian banks were initially targeted for the study, incomplete data for some banks necessitated their exclusion from the final sample. The researchers chose the sample period based on the consistent availability of required financial data across the banks included (Appendix A).

Table 1. Sampling procedure

5.2. Measurement of variables

The study examined the relationship between various factors and the capital structures (leverage) of Ethiopian banks (Ayalew & McMillan, Citation2021). The dependent variable was leverage, operationalized as the total debt to total assets ratio (Ayalew & McMillan, Citation2021). This served as a measure of how much banks rely on debt versus equity in their capital structures. The main independent variable of interest was gender diversity on banks’ boards of directors (Berhe, Citation2023; Wondem & Batra, Citation2019). This was measured as the proportion of women on the boards (Berhe, Citation2023), reflecting the representation of female directors. The study aimed to determine if higher gender diversity was correlated with lower leverage (Wondem & Batra, Citation2019).

To control for other potential influences, the researchers incorporated several bank-specific and macroeconomic variables into their models. The bank-specific control variables were bank size, liquidity ratio, and profitability (Ayalew & McMillan, Citation2021; Shibru, Citation2012). Bank size was measured as the natural log of total assets (Ayalew & McMillan, Citation2021). Liquid assets divided by total assets served as the basis for calculating the liquidity ratio (Shibru, Citation2012). Economic margins of businesses served as a proxy for profitability (Ayalew & McMillan, Citation2021). The macroeconomic control variables were economic growth and inflation. The annual percentage change in GDP served as a measure of economic growth (Takele & Beshir, Citation2017). The annual percentage change in the consumer price index served as a proxy for inflation (Hatzinikolaou et al., Citation2002). By taking into account these bank-specific and macroeconomic factors, the study tried to find out if there was a link between gender diversity and leverage. It also tried to control for other variables that could affect banks’ capital structures (Gujarati, Citation2021). Table provides definitions and measurements for all the variables used in the analyses.

Table 2. Description of study variables

5.3. Econometric model

Cross-sectional dependency, stationarity, and cointegration tests must be performed before econometric studies.

5.3.1. Cross-sectional dependence (CSD)

High cross-sectional dependence (CSD) between nations might skew estimates if CSD is not controlled (Pesaran, Citation2004, Citation2015). The CSD test works for balanced and unbalanced data and tests the null hypothesis of weak cross-sectional dependency against the alternative hypothesis of substantial dependence (Pesaran, Citation2015). To avoid false results in cross-sectional dependence, second-generation unit root tests are performed. Pesaran (Citation2007)‘s cross-sectional augmented Im, Pesaran, and Shin (CIPS) is used.

5.3.2. Unit root test

Applied researchers often test unit roots in time series investigations, which are now common practice and part of econometric courses. Tests for unit roots in panel data are rare. Two panel unit root tests are used if cross-sectional dependence is present. I can use the Levin-Lin-Chu (LLC) and cross-sectional Im, Pesaran, and Shin (CIPS) panel unit root tests because they require well balanced panel data. The Levin-Lin-Chu (LLC) model tests panel data with fixed effects, deterministic trends, and heterogeneous serially correlated errors. A variable is integrated of order one (I (1)) if it becomes stationary after a single difference.

I used the Levin-Lin-Chu (LLC) model to test panel data for unit roots. This approach is better than unit root testing because it accounts for fixed effects, individual deterministic trends, and heterogeneous serially correlated mistakes (Levin et al., Citation2002). The LLC test is a three-step technique that compensates for unit root tests’ inability to rule out alternative hypotheses with persistent deviations from equilibrium.

In the LLC panel unit root test, dmt represents the vector of deterministic variables, and αmi is the corresponding vector of coefficients for model m = 1, 2, 3. Specifically, d1t = {empty set}, d2t = {1}, and d3t = {1, t}. As the lag order pi is unknown, LLC recommends a three-step procedure to implement their test.

5.3.3. Panel cointegration test

Panel cointegration was used to assess cross-sectional variance in moderate time series data. These methods let us test panel cointegrating relationship hypotheses (Baltagi, Citation1996). We used econometric models to determine the relationship between gender diversity and leverage. In panel data with N cross-sectional units (indexed by ἰ) and T time periods (indexed by t), determining stationary dynamics includes pooling the cointegration slope coefficient across all units (indexed by ἱ). This yields the estimate equation:

In a panel data setting, if the linear combination of cointegrated variables yit and Xit is stationary (μit=I(0)), they are cointegrated. Conversely, if the linear combination is unit root non-stationary (μit=I(1)), they are not cointegrated. The error term μit is obtained by adding the contamination term β_i Xit to it, resulting in Vit. The presence of a unit root in Xit makes the contamination term a unit root process. Therefore, the nature of the linear combination determines the cointegration status of yit and Xit in a panel data setting. As the study variables are seven, Westerlund’s (Citation2005) test for cointegration is suitable for this study.

5.3.4. Dynamic GMM panel model specification

Since the research takes a panel approach, the model specification for panel data can be presented in the following manner:

The independent variables BSize (corporate governance) and GD (board gender diversity) determine the dependent variable LV. Additionally, the control variables LR, INF, BnS, and GDPg are used to mitigate other factors that may impair bank performance (Arora & Gaur, Citation2022; Vallelado & García‐Olalla, Citation2021). Board gender diversity (GD) and capital structure (LV) are examined using a dynamic system panel generalized method of momentum (GMM) technique (Zaid et al., Citation2020; Amin et al., Citation2022). This model uses selected corporate and macroeconomic factors (Adusei & Obeng, Citation2019) to control their impact on the relationship between the variables. The dynamic GMM estimator addressed reverse causality and dynamic endogeneity (Amin et al., Citation2022). I employed lagged structures and instrumental variable estimate methods from previous studies to address endogeneity (Amin et al., Citation2022). Following literature, I offer the two-step dynamic GMM model for equation 4 that uses lagged dependent variables as explanatory variables in GMM estimation.

Whereas,, represents the lag of the dependent variable LV (capital structure decisions from the previous year). All explanatory variable definitions can be found in Table .

5.3.5. Granger non-causality

Before GMM estimation, I examined the endogeneity problem, which is reverse causality from the dependent variable to the independent variable. I do this with Juodis et al. (Citation2021) Granger non-causality testing. The JKS non-causality test (Table ) shows that most variables are endogenous since they reject the null hypothesis. GMM was used, and all independent variables were endogenous.

Table 3. Summary of Descriptive analysis

Table 4. CSD, panel unit root results

Table 5. Westerlund (Citation2005) test for panel cointegration tests

Table 6. Diagnostic tests

Table 7. Granger non-causality test results

5.4. Panel data model diagnosis

In this study, I performed diagnostic tests for linear dynamic GMM and dynamic GMM to assure model reliability and validity. I tested models for heteroscedasticity, omitted variables, multicollinearity, and normality. I utilized Table for linear dynamic GMM and to illustrate these diagnostic test results.

6. Empirical results and discussion

6.1. Descriptive analysis

6.1.1. Summary statistics and correlation analysis

Table provides the summary statistics for the variables used in this study. We can see that on average, the leverage ratio (LV) for the Ethiopian banking sector sample was 0.615, with a standard deviation of 0.858. The average percentage of female directors on boards (GD) was 43.7%. The board size (BSize) averaged 8.359 members. Bank size (BnS), as measured by the natural log of total assets, was on average 10.203. The average liquidity ratio (LR) was 3.843. Profitability (PROFF) averaged 0.021, with GDP growth (GDPg) coming in at 8.94% annually over the sample period. Finally, average annual inflation (INF) was 16.378%.

Appendix B shows the Pearson correlation coefficients between the variables. Looking first at the dependent variable leverage ratio, we can see it is negatively correlated with gender diversity, board size, bank size, and liquidity ratio, as expected. Profitability has a strong positive correlation with leverage. Several of the independent variables are also correlated with each other. Notably, there is a negative correlation between gender diversity and board size, indicating more gender-balanced boards tend to be smaller. Bank size correlates negatively with gender diversity, board size, and liquidity, but positively only with liquidity ratio. GDP growth correlates negatively with board size, bank size, and inflation in the economy.

6.2. Pre-estimation tests

6.2.1. Cross-sectional dependence (CSD), panel unit root test (PURT) results

Table shows the results of Pesaran’s (Citation2004) cross-sectional dependence (CD) test and several common panel unit root tests, such as the Levin-Lin-Chu (LLC), Pesaran (Citation2007) CIPS, and Im-Pesaran-Shin (Im et al., Citation2003) tests. Starting with the CD test, I find strong evidence of cross-sectional dependence for all variables at their levels, as the CD statistics are significant at the 1% level. This suggests the need to employ estimation methods that control for cross-sectional dependence.

Turning to the panel unit root test results, at most levels, most series are nonstationary based on at least two of the tests. However, after first differencing to control for unit roots, all series become stationary according to the LLC, CIPS, and IPS tests. This confirms that all variables in the model are integrated in order one, I (1). In summary, these preliminary analyses indicate the presence of cross-sectional dependence and unit roots at different levels among the variables. Therefore, I employ panel estimation techniques that control for cross-sectional dependence and endogeneity, such as the GMM method. The results suggest the data is well-suited for advanced panel data analysis.

6.2.2. Cointegration results

Table reports the results of the Westerlund (Citation2005) panel cointegration test, which tests the null hypothesis of no cointegration against the alternative of cointegration. The test was conducted with 15 panels and 13 time periods to match the dataset dimensions. Two test specifications are reported: without panel-specific time trends and with panel-specific time trends included. In both cases, I can reject the null hypothesis of no cointegration, as the test statistics are statistically significant at the 5% and 1% levels, respectively. This provides strong evidence that cointegration, or a long-run equilibrium relationship, exists between the variables in the model. Notably, the results hold even after controlling for panel-specific time trends. This confirms that leverage and its determinants move together in the long run for Ethiopian banks.

6.3. Post estimation tests

6.3.1. Diagnosis test Results

6.3.1.1. Granger non-causality Test results

Table reports the findings of various diagnostic tests conducted on the panel regression model. First, the Breusch-Pagan test finds no evidence of heteroscedasticity, given the high p-value. Similarly, the Ramsey RESET test suggests I have not omitted any necessary variables from the model. Next, the variance inflation factors calculated show no issues with multicollinearity, as all are well below the critical threshold of 10. Finally, the Shapiro-Wilk normality test finds no reason to reject the normality of the residuals. Overall, these various checks indicate our model specifications and estimations passed with flying colors. Let’s now check for causal effects. Turning to Table , the Granger non-causality results examine whether the lags of the independent variables help forecast future values of leverage (LV). Based on the Juodis-Karavias-Sarafidis (JKS) approach, most covariates appear to cause Granger-cause leverage according to the p-values. Notably, lags in gender diversity, bank size, liquidity ratio, GDP growth, and inflation reliably cause Granger-caused leverage at 5% or 1% significance. Before estimating our model using GMM, it is important to first examine whether an endogeneity problem exists between the dependent and independent variables.

To test for this, I employed the Juodis et al. (Citation2021) Granger non-causality test. As shown in Table , the majority of independent variables exhibit statistically significant coefficients in the JKS test. This implies they reject the null hypothesis of non-causality and are therefore endogenous. Recognizing that endogeneity could bias our results, the generalized method of moments (GMM) estimation was adopted. GMM is specifically designed to produce consistent estimates in the presence of endogenous regressors. Accordingly, all independent variables were treated as endogenous in the GMM model. By first using the Granger causality test to identify potential endogeneity and then selecting GMM as an appropriate technique to account for it, I aimed to obtain reliable causal inferences from the empirical analysis. Checking for this econometric issue is an important step before interpreting estimated relationships between variables.

6.4. Decision results to select dynamic GMM

6.4.1. Decision results between system GMM and difference GMM

Table reports the coefficients from various panel data models estimated on the dataset, including pooled OLS, fixed effects, one-step difference GMM, two-step difference GMM, one-step system GMM, and two-step system GMM. The first thing to note is that the coefficient from the fixed effects model (0.425) is lower than the pooled OLS (0.643), suggesting the presence of unobserved heterogeneity. Following the guidelines established by Blundell and Bond (Citation1998) and Bond et al. (Citation2001), this outcome implies that Difference GMM would be more suitable than System GMM. Looking at the GMM estimators, the Difference GMM coefficients (one-step: 0.1626, two-step: 0.178) are lower than their System GMM counterparts (one-step: 0.214, two-step: 0.246). This lends further support to the conclusion that Difference GMM is preferable in this application, as it controls for endogeneity and unobserved heterogeneity without relying on overly restrictive assumptions.

Table 8. Decision results between system GMM and difference GMM

6.4.2. Difference GMM estimation results

Table shows the difference GMM estimation results, which investigate the impact of gender diversity and other factors on leverage in Ethiopian banks using one-step and two-step difference GMM estimations.

Table 9. Effect of gender diversity and other study variables on capital structure (leverages)

6.4.2.1. Gender diversity and leverage

Looking first at gender diversity (GD), both models find it has a negative and statistically significant association with leverage. This supports Hypothesis 1 and is consistent with prior studies finding that greater female representation correlates with lower debt usage. For gender diversity, the negative association in the one-step model aligns with Berhe (Citation2023) and provides partial validation of the agency theory perspective that representation lowers debt usage via improved monitoring (Agrawal & Knoeber, Citation1996). However, like Ben Saad and Belkacem (Citation2021), the insignificant two-step result resembles mixed findings and validates behavioral arguments that context shapes impacts (Krause et al., Citation2013).

6.4.2.2. Board size (proxy for corporate governance) and leverages

Turning to board size (BSize), the one-step model shows it negatively impacts leverage significantly. While only marginally significant in the two-step test, this provides some evidence in favor of Hypothesis 2 of an inverse relationship. The inverse board size effect in the one-step model lends some validation to resource dependence views that size enables advisory functions (Hillman et al., Citation2007) and converges with research findings that impacts depend on strategic needs (Hussain et al., Citation2020).

6.4.2.3. Bank size and leverage

Contrary to expectations stated in Hypothesis 3, bank size (BnS) has a negative coefficient in the one-step model. However, it becomes insignificant in the second step. Overall, the results do not strongly validate theories of larger banks relying more on debt. Contrary to expectations rooted in theories linking scale and resources to debt capacity (Barton & Gordon, Citation1988), bank size did not positively impact leverage in either model, resembling studies finding the relationship depends on market forces (Deesomsak et al., Citation2004; Agmas Wassie, Citation2020).

6.4.2.4. Relationship between profitability and leverage

In line with Hypothesis 4, profitability (PROFF) exhibits a strongly positive effect on leverage across both models. This confirms that more profitable banks utilize relatively more debt in their capital structures. The profitability-leverage relationship across models confirms the agency logic of earnings providing debt capacity (Jo & Lee, Citation1996) and matches evidence on performance enabling borrowing (Tarek Al-Kayed et al., Citation2014).

6.4.2.5. Liquidity ratio (LR) and inflation (INF)

Meanwhile, the coefficients for liquidity ratio (LR) and inflation (INF) are insignificant, failing to support hypotheses 5 and 7 of negative relationships.

6.4.2.6. Economic growth and leverage

Finally, GDP growth (GDPg) shows the expected positive sign stated in Hypothesis 6, albeit only at the 10% level for one-step GMM. The non-significant macro findings fail to validate expectations grounded in research that their effects rely on intervening institutional dynamics (Graham et al., Citation2015). Overall, the findings provide mixed support for the theoretical hypotheses while aligning with several prior empirical studies.

6.5. Robustness analyses

The results of the robustness analysis using linear dynamic panel data estimation are presented in Table . Several relationships provide further validation of factors identified as influencing Ethiopian banks’ capital structure. Once more, gender diversity (GD) negatively impacts leverage (LV) in both models, solidifying prior evidence that it corresponds to more prudent financing decisions. This corroborates the monitoring logic of agency theory (Elsayed & Wahba, Citation2016). Board size (BSize) too shows an inverse effect, achieving significance in the two-step model. This lends renewed credence to contingency perspectives on the strategic balancing of advisory and oversight functions (Pathan & Skully, Citation2010).

Table 10. Linear dynamic panel-data regression results

Larger bank scale (BnS) again significantly lowers LV, aligning with behavioral arguments that market heterogeneities must be accounted for (Doumpos et al., Citation2013). Higher profitability’s (PROFF) persistently strong positive correlation with LV strengthens conclusions on profit-enhancing debt capacity. Inflation’s (INF) emerging negative association further validates its debt-dampening influence in line with macroeconomic theory (Deesomsak et al., Citation2004). The robust models reinforce many core findings while shedding new light on factors like size and INF through the use of alternative methodologies. This enhances confidence in the implications drawn from Ethiopian banks’ financing behavior.

7. Discussions

This study assessed the impact of gender diversity and other factors on the capital structure of Ethiopian banks over the period 2010–2022. In this section, the key findings are summarized and contextualized within existing theory and empirics. Potential avenues for future research are also proposed. The consistent negative relationship between gender diversity and leverage across models strongly validates agency perspectives that representation enhances monitoring (Agrawal & Knoeber, Citation1996). However, discrepancies signal contextual contingencies that may condition this impact, aligned with behavioral arguments (Krause et al., Citation2013). Similarly, board size displayed mixed effects on leverage, supporting strategic contingency views on resource-oversight tradeoffs (Hillman et al., Citation2007).

Larger banks did not clearly raise borrowing as proposed. This aligns with studies contextualizing such relationships (Deesomsak et al., Citation2004) and implies that unaccounted influences shape realized associations. Positive profitability-leverage links uphold the underpinnings of agency-finance theory (Drobetz et al., Citation2013; Jo & Lee, Citation1996).

Inconclusive macro findings resemble research emphasizing intervening institutional factors (Graham et al., Citation2015; Homaifar et al., Citation1994). Therefore, while partially validating expectations, complexities warrant more pluralistic behavioral theorizing attentive to contextual idiosyncrasies. The study situates itself well within international diversity-governance-performance research (Berhe, Citation2023; Liang et al., Citation2011). Yet discrepancies highlight the need for region-specific nuance versus linear generalizations, as capacity challenges remain (Börzel & Hackenesch, Citation2013; Tesemma, Citation2016). Closer attention to local market dynamics could reconcile mixed outcomes (Deesomsak et al., Citation2004; Doumpos et al., Citation2013).

Future work may expand sample sizes, incorporate qualitative perspectives on managerial priorities, and develop contingency-based hypotheses accounting for governance-financing links’ potential dependencies on competitive conditions, stages of sector development, and regulatory reforms over time. Longitudinal case studies offer scope to track evolution and causal mechanisms in more depth. In closing, an enriched contextual understanding of diversity’s strategic impact holds relevance for regulators aiming to balance stability with representativeness through well-calibrated policies. Advancing inclusion promises economic benefits by mobilizing underutilized expertise towards improved resource allocation and stakeholder value.

8. Summary and conclusion

This study aimed to examine how gender diversity impacts the capital structure of Ethiopian banks. The findings provide valuable insights while also signaling opportunities for continued progress. In this conclusion, the main results are summarized alongside reflections on implications, limitations, and pathways forward.

Gender diversity consistently relates negatively to leverage across models, corroborating notions that representation enhances monitoring quality. Board size also displayed nuanced relationships tied to theories of strategic resource deployment. Higher profits predictably correlate with increased debt levels, validating the theoretical underpinnings. At the same time, inconsistencies emerged. Larger bank scale did not clearly elevate borrowing as posited, underscoring the need to account for contextual influences. Inconclusive macroeconomic relationships similarly highlighted contingencies. While validating some expectations, the mixed findings signal a role for pluralistic frameworks attentive to idiosyncrasies.

The findings connect meaningfully to international research yet likewise reveal opportunities for localized understanding. Situating impacts within Ethiopia’s evolving governance landscape and banking sector maturation offers potential to reconcile nuances. In this way, the study represents an initial step towards enriched contextual comprehension. Implications arise in several domains. For regulators, the results signify that balanced policies are prudent and promote inclusion alongside stability. Evidence that representation relates to prudent financing carries import as the sector modernizes. Insights for managers center on optimizing resources through diversity while satisfying stakeholders.

Limitations center around generalizability; necessitating sample expansions incorporating varied conditions over time could strengthen external validity. Quantitative analyses alone provide incomplete pictures; mixed methods combining managerial insights promise richer causal examination. Future pathways build upon these limitations. Longitudinal case studies offer the potential to track evolution and distinct mechanisms in depth. Developing contingency hypotheses tailored to Ethiopia’s economic trajectory and regulatory phases may reconcile discrepancies. Qualitative work incorporating varied viewpoints can lend context, which is absent here. Cross-country comparisons situating diversity’s impact within development levels also appear impactful.

In closing, this study makes an initial contribution to furthering understanding of board diversity’s strategic implications in Ethiopia. Continued rigorous, pluralistic, and localized research promises to not only deepen appreciation of impacts but also empower stakeholders working to realize inclusion’s advantages and mobilize underutilized expertise for optimized outcomes. Findings that representation relates to prudent choices carry hope that progress on diversity and performance can reinforce one another for sustained growth.

Availability of data and materials

Upon request, the data and materials will be made available.

Acknowledgments

The author is responsible for any errors or omissions in the paper.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Dereje Fedasa Hordofa

Dereje Fedasa Hordofa is a Lecturer at Dire Dawa University, Ethiopia. He is an esteemed member of the Ethiopian Economic Association (EEA), reflecting his dedication to contributing to the field of economics. Before his role as a Lecturer, Dereje gained valuable experience as a Customer Service Officer at the Bank of Abyssinia (BOA), where he honed his skills in the financial sector. He has published papers in peer-reviewed journals on topics such as board structure and bank performance, and factors influencing rural women’s economic empowerment. Mr. Hordofa holds several certificates in financial modeling, analysis, and valuation from respected institutions like the Corporate Finance Institute and Yale University. Overall, Dereje Fedasa Hordofa is a dedicated economics educator and researcher committed to advancing understanding of important economic and development issues facing Ethiopia and other nations.

References

- AA Zaid, M., Wang, M., TF Abuhijleh, S., Issa, A., WA Saleh, M., & Ali, F. (2020). Corporate governance practices and capital structure decisions: The moderating effect of gender diversity. Corporate Governance the International Journal of Business in Society, 20(5), 939–26. https://doi.org/10.1108/cg-11-2019-0343

- Abeysekera, I. (2010). The influence of board size on intellectual capital disclosure by Kenyan listed firms. Journal of Intellectual Capital, 11(4), 504–518. https://doi.org/10.1108/14691931011085650

- Adeneye, Y., & Kammoun, I. (2022). Real earnings management and capital structure: Does environmental, social and governance (ESG) performance matter? Cogent Business & Management, 9(1). https://doi.org/10.1080/23311975.2022.2130134

- Adusei, M., & Obeng, E. Y. T. (2019). Board gender diversity and the capital structure of microfinance institutions: A global analysis. The Quarterly Review of Economics & Finance, 71, 258–269. https://doi.org/10.1016/j.qref.2018.09.006

- Agmas Wassie, F. (2020). Impacts of capital structure: Profitability of construction companies in Ethiopia. Journal of Financial Management of Property and Construction. ahead-of-print(ahead-of-print). https://doi.org/10.1108/jfmpc-08-2019-0072

- Agrawal, A., & Knoeber, C. R. (1996). Firm performance and mechanisms to control agency Problems between managers and shareholders. The Journal of Financial and Quantitative Analysis, 31(3), 377–397. https://doi.org/10.2307/2331397

- Ahmed Sheikh, N., & Wang, Z. (2012). Effects of corporate governance on capital structure: Empirical evidence from Pakistan. Corporate Governance the International Journal of Business in Society, 12(5), 629–641. https://doi.org/10.1108/14720701211275569

- Al-Bassam, W. M., Ntim, C. G., Opong, K. K., & Downs, Y. (2015). Corporate boards and ownership structure as Antecedents of corporate governance disclosure in Saudi Arabian publicly listed corporations. Business & Society, 57(2), 335–377. https://doi.org/10.1177/0007650315610611

- Alhossini, M. A., Ntim, C. G., & Zalata, A. M. (2021). Corporate board Committees and corporate outcomes: An International systematic literature Review and agenda for future research. The International Journal of Accounting, 56(1), 2150001. https://doi.org/10.1142/s1094406021500013

- Ali, S., ur, R. R., Aslam, S., Khan, I., & Murtaza, G. (2023). Does board diversity reduce the likelihood of financial distress in the presence of a powerful Chinese CEO?. Management Decision, 61(6), 1798–1815. https://doi.org/10.1108/MD-01-2022-0007

- Allini, A., Manes Rossi, F., & Hussainey, K. (2015). The board’s role in risk disclosure: An exploratory study of Italian listed state-owned enterprises. Public Money & Management, 36(2), 113–120. https://doi.org/10.1080/09540962.2016.1118935

- Amidu, M. (2007). Determinants of capital structure of banks in Ghana: An empirical approach. Baltic Journal of Management, 2(1), 67–79. https://doi.org/10.1108/17465260710720255

- Amin, A., Ur Rehman, R., Ali, R., & Ntim, C. G. (2021). Does gender diversity on the board reduce agency cost? Evidence from Pakistan. Gender in Management: An International Journal, 37(2), 164–181. https://doi.org/10.1108/gm-10-2020-0303

- Arora, P., & Gaur, A. (2022). Peer directors’ effort, firm efficiency and performance of diversified firms: An efficacy-based view of governance. Journal of Business Research, 151, 593–608. https://doi.org/10.1016/j.jbusres.2022.07.035

- Assfaw, A. M. (2020). The determinants of capital structure in Ethiopian Private commercial banks: A panel data approach. Journal of Economics, Business & Accountancy Ventura, 23(1), 108–124. https://doi.org/10.14414/jebav.v23i1.2223

- Ayalew, Z. A., & McMillan, D. (2021). Capital structure and profitability: Panel data evidence of private banks in Ethiopia. Cogent Economics & Finance, 9(1). https://doi.org/10.1080/23322039.2021.1953736

- Baltagi, B. H. (1996). Testing for random individual and time effects using a Gauss-Newton regression. Economics Letters, 50(2), 189–192. https://doi.org/10.1016/0165-1765(95)00754-7

- Banalieva, E. R., & Sarathy, R. (2011). A contingency theory of Internationalization. Management International Review, 51(5), 593–634. https://doi.org/10.1007/s11575-011-0093-0

- Bandyopadhyay, A., & Barua, N. M. (2016). Factors determining capital structure and corporate performance in India: Studying the business cycle effects. The Quarterly Review of Economics & Finance, 61, 160–172. https://doi.org/10.1016/j.qref.2016.01.004

- Barton, S. L., & Gordon, P. J. (1988). Corporate strategy and capital structure. Strategic Management Journal, 9(6), 623–632. https://doi.org/10.1002/smj.4250090608

- Ben Saad, S., & Belkacem, L. Does board gender diversity affect capital structure decisions?. (2021). Corporate Governance the International Journal of Business in Society, 22(5), 922–946. ahead-of-print(ahead-of-print). https://doi.org/10.1108/cg-12-2020-0575

- Ben Saad, S., & Belkacem, L. (2022). How does corporate social responsibility influence firm financial performance?. Corporate Governance: The International Journal of Business in Society, 22(1), 1–22.

- Berhe, A. G. (2023). Board structure and bank performance: Evidence from Ethiopia. Cogent Business & Management, 10(1). https://doi.org/10.1080/23311975.2022.2163559

- Bezabeh, A., & Desta, A. (2014). Banking sector reform in Ethiopia. International Journal of Business and Commerce, 3(8), 25.

- Bilgin, R., & Dinc, Y. (2019). Factoring as a determinant of capital structure for large firms: Theoretical and empirical analysis. Borsa Istanbul Review, 19(3), 273–281. https://doi.org/10.1016/j.bir.2019.05.001

- Birru, M. W. (2016). The impact of capital structure on financial performance of commercial banks in Ethiopia. Global Journal of Management and Business Research, 16(8), 44–52.

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. https://doi.org/10.1016/s0304-4076(98)00009-8

- Bokpin, G. A., & Arko, A. C. (2009). Ownership structure, corporate governance and capital structure decisions of firms. Studies in Economics and Finance, 26(4), 246–256. https://doi.org/10.1108/10867370910995708

- Bond, S. R., Hoeffler, A., & Temple, J. R. (2001). GMM estimation of empirical growth models. Available at SSRN 290522.

- Börzel, T. A., & Hackenesch, C. (2013). Small carrots, few sticks: EU good governance promotion in sub-Saharan Africa. Cambridge Review of International Affairs, 26(3), 536–555. https://doi.org/10.1080/09557571.2013.807424

- Bukair, A. A. A. (2019). Factors influencing Islamic banks’ capital structure in developing economies. Journal of Islamic Accounting and Business Research, 10(1), 2–20. https://doi.org/10.1108/jiabr-02-2014-0008

- Butt, S. A., & Hasan, A. (2009, February 1). Impact of ownership structure and corporate governance on capital structure of Pakistani listed companies. Retrieved from papers.ssrn.com website: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1732511

- Campopiano, G., Gabaldón, P., & Gimenez-Jimenez, D. (2022). Women Directors and Corporate Social Performance: An Integrative Review of the Literature and a Future Research Agenda. Journal of Business Ethics, 182(3), 717–746. https://doi.org/10.1007/s10551-021-04999-7

- Deesomsak, R., Paudyal, K., & Pescetto, G. (2004). The determinants of capital structure: evidence from the Asia Pacific region. Journal of Multinational Financial Management, 14(4–5), 387–405. https://doi.org/10.1016/j.mulfin.2004.03.001

- Dessie, A. G. (2017). A critical analysis of the Ethiopian banking Law in light of the Basel Committee on banking Supervision’s corporate governance Principles for banks. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3576525

- Detthamrong, U., Chancharat, N., & Vithessonthi, C. (2017). Corporate governance, capital structure and firm performance: Evidence from Thailand. Research in International Business and Finance, 42, 689–709. https://doi.org/10.1016/j.ribaf.2017.07.011

- Doumpos, M., Gaganis, C., & Pasiouras, F. (2013). Financial Engineering Laboratory Bank Diversification and Overall Financial Strength: International Evidence Around the Crisis. Retrieved from https://www.fel.tuc.gr/Working%20papers/2013_03

- Drobetz, W., Gounopoulos, D., Merikas, A., & Schröder, H. (2013). Capital structure decisions of globally-listed shipping companies. Transportation Research Part E: Logistics & Transportation Review, 52, 49–76. https://doi.org/10.1016/j.tre.2012.11.008

- Edeti, A. G., & Garg, M. C. (2020). Impact of board composition on financial performance of commercial banks in Ethiopia. Journal of Hospitality and Tourism, 18(2), 54–69.

- Elmagrhi, M. H., Ntim, C. G., Malagila, J., Fosu, S., & Tunyi, A. A. (2018). Trustee board diversity, governance mechanisms, capital structure and performance in UK charities. Corporate Governance the International Journal of Business in Society, 18(3), 478–508. https://doi.org/10.1108/cg-08-2017-0185

- Elsayed, K., & Wahba, H. (2016). Reexamining the relationship between inventory management and firm performance: An organizational life cycle perspective. Future Business Journal, 2(1), 65–80. https://doi.org/10.1016/j.fbj.2016.05.001

- Ezeani, E., Kwabi, F., Salem, R., Usman, M., Alqatamin, R. M. H., & Kostov, P. (2022). Corporate board and dynamics of capital structure: Evidence from UK, France and Germany. International Journal of Finance & Economics, 28(3), 3281–3298. https://doi.org/10.1002/ijfe.2593

- Feng, C., & Fay, S. (2020). Store Closings and Retailer profitability: A contingency perspective. Journal of Retailing, 96(3), 411–433. https://doi.org/10.1016/j.jretai.2020.01.002

- Frank, M. Z., & Goyal, V. K. (2009). Capital structure decisions: Which factors are reliably important? Financial Management, 38(1), 1–37. https://doi.org/10.1111/j.1755-053X.2009.01026.x

- García, C. J., & Herrero, B. (2021). Female directors, capital structure, and financial distress. Journal of Business Research, 136, 592–601. https://doi.org/10.1016/j.jbusres.2021.07.061

- Graham, J. R., Leary, M. T., & Roberts, M. R. (2015). A century of capital structure: The leveraging of corporate America. Journal of Financial Economics, 118(3), 658–683. https://doi.org/10.1016/j.jfineco.2014.08.005

- Gujarati, D. N. (2021). Essentials of Econometrics. In Google Books. SAGE Publications. https://books.google.com/books?hl=en&lr=&id=2CI_EAAAQBAJ&oi=fnd&pg=PA9&dq=econometrics+gujarati&ots=bxPy68opUo&sig=1lEKWufJtZ4ZaXrqWK-Pu-P8_rw