?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines strategic response towards climate change mitigation by listed firms in the energy sector in Malaysia from 2010 to 2019. It also examines whether institutional pressures and attributes of the Chief Executive Officer (CEO) drive such strategic response. Using a TwoStep cluster analysis, and based on 271 firm-year observations, the results show that there are two types of strategic response portrayed by the energy firms, i.e. indifferent and emerging. To analyze the determinants of the firms’ strategic response, two logistic regression techniques are employed, i.e. robust standard errors clustered by firms and lagged structure approach. The results suggest that firms strategic response is shaped by institutional pressures and CEOs attributes, namely, CEOs with international experiences, and CEOs who have experiences in addressing environmental issues. These inferences are robust to several sensitivity tests, including the lagged structure approach, Heckman’s (1979) selection bias correction, an alternative measure of firms’ strategic responses, a matched-sample approach, and controlling for possible international pressures faced by the firms. Overall, the results indicate that in emerging countries, such as Malaysia, with weak pressures from non-governmental organizations, both the government and CEOs need to play dominant roles in addressing climate change issue.

1. Introduction

The 26th United Nations Climate Change Conference of the Parties (COP26), which was held in Glasgow in 2021 ended with the Glasgow Climate Pact that includes an Agreement by countries to begin reducing coal-fired power (Rincon, Citation2021). However, some have viewed the Agreement as below expectations, in that there is a lack of a stronger commitment to reduce greenhouse gas (GHG) emissions (Masood & Tollefson, Citation2021). Given that climate change presents the single biggest challenge faced by the world in achieving sustainable development (UNFCCC, Citation2020; World Bank, Citation2014) and it is striking harder and more rapidly (World Economic Forum, Citation2020), each individual country needs to take a lead towards reducing GHG emissions. Nonetheless, governments cannot undertake climate change initiatives alone and they require corporate sector to play its role in mitigating climate change (Wright & Nyberg, Citation2017).

In this paper, we examine firms’ strategic response towards climate change mitigation. We also examine whether institutional pressures and CEOs’ attributes drive such strategic response. We focus on listed firms in the energy sector in Malaysia, as it is the primary source of GHG emissions both globally (Lamb et al., Citation2021) and in Malaysia (Malaysia Ministry of Environment and Water, Citation2020).

Our study is motivated by three main considerations. First, little is known about how energy firms in emerging countries have responded to climate change issue even though this sector represents the largest GHG emitters (de Abreu et al., Citation2017). Thus far, research on firms’ strategic response towards climate change mitigation has concentrated on the largest firms worldwide (e.g., Damert & Baumgartner, Citation2018; Kolk & Pinkse, Citation2005; Weinhofer & Hoffmann, Citation2010) or firms in advanced countries, especially the Annex I countries, such as in Europe (e.g., Cadez & Czerny, Citation2016) and Canada (e.g., Boiral et al., Citation2012).

A few studies have attempted to address the lack of research, as discussed above, by analyzing firms in developing countries, such as in Pakistan (e.g., Jeswani et al., Citation2008), Malaysia (e.g., Amran et al., Citation2012, Citation2015), and Brazil (e.g., de Abreu et al., Citation2017). However, the data employed were outdated and long before the Paris Agreement in 2016. For example, de Abreu et al. (Citation2017) conducted a survey of general managers in 2013. In Malaysia, the research lacuna is more apparent, as the relatively recent studies on climate change have tended to focus on climate change reporting (e.g., Omar & Amran, Citation2017) or the impact of climate change on certain sectors, such as the agriculture sector (e.g., Tang, Citation2019). Thus, it is an open empirical question how energy firms in Malaysia, as an example of firms in a less advanced economy, have responded to climate change mitigation and what the drivers behind firms’ strategic responses have been.

Second, prior studies (e.g., Damert & Baumgartner, Citation2018; Lee, Citation2012; Weinhofer & Hoffmann, Citation2010; Wright & Nyberg, Citation2017) highlighted the lack of longitudinal studies on firms’ strategic response towards climate change mitigation. For example, Weinhofer and Hoffmann (Citation2010), Lee (Citation2012), Wright and Nyberg (Citation2017), and Damert and Baumgartner (Citation2018) emphasized the need for investigating firms’ strategic responses using a longer time horizon to provide insights into how these responses have progressed over time, and if indeed, they have progressed.

Third, research on the role of CEOs in relation to climate change mitigation strategies is relatively limited and with inconclusive evidence. Specifically, Siegel (Citation2014) and Walls and Berrone (Citation2017) highlighted that the role of corporate leaders (CEOs) in formulating initiatives on corporate social responsibility, including sustainability issues, is still an under-researched area in the literature relative to other organizational factors. A few fairly recent studies have attempted to address these research gaps by examining CEOs’ attributes in relation to climate change (e.g., Amran et al., Citation2015; Chithambo et al., Citation2020; Lewis et al., Citation2014). Nevertheless, thus far, the findings have been inconclusive, which suggest that further studies are needed.

We focus on energy firms in Malaysia, as an example of energy firms in emerging markets, as in 2018, Malaysia established a specific Ministry, i.e., the Ministry of Energy, Science, Technology, Environment and Climate Change (MESTECC), to address climate change issues. With the existence of MESTECC, intensified efforts towards tackling climate change have been evinced (Jaafar, Citation2019; Leoi, Citation2018). Accordingly, this institutional feature serves an appropriate setting for our investigation of the influence of institutional pressures via the establishment of a specific body on firms’ strategic response towards climate change mitigation.

Our study makes several contributions to the literature on environmental strategy and CEOs’ attributes. First, our study provides empirical evidence that strategic response toward climate change mitigation by energy firms in Malaysia, i.e., a less advanced country, are generally at the preliminary stage. Basically, there are two types of strategic response towards climate change mitigation portrayed by these firms, namely, indifferent and emerging. At an early stage, many of the energy firms examined are indifferent towards climate change mitigation.

Second, by focusing on energy firms from 2010 to 2019, our study responded to the call made by Wright and Nyberg (Citation2017) and Damert and Baumgartner (Citation2018) to investigate the corporate environmental strategies over a longer time horizon. In doing so, we provided empirical evidence that firms’ responses towards climate change mitigation have improved over time in light of the institutional pressures and the various climate change initiatives implemented. Rather than being indifferent to the issues surrounding climate change, these firms are more likely to take part in managing their GHG emissions.

Third, prior research has examined the impact of institutional pressures in the form of regulatory threats (e.g., Cadez et al., Citation2019; Clemens et al., Citation2008; Okereke & Russel, Citation2010). Our study focuses on institutional pressures via the establishment of one specific body, i.e., MESTECC. Our results provide support to the institutional theory and are consistent with prior studies (Daddi et al., Citation2020; Okereke & Russel, Citation2010; Reid & Toffel, Citation2009) who reported that institutional pressure is one of the critical factors that drive firms’ strategic response toward climate change mitigation. Accordingly, our results demonstrate the applicability of the institutional theory in explaining firms’ strategic response towards climate change mitigation in an emerging market, like Malaysia.

Fourth, prior studies (e.g., Lewis et al., Citation2014; Walls & Berrone, Citation2017) have highlighted the lack of studies on how CEOs’ attributes influence firms’ responses to environmental issues. Our results demonstrate that CEOs with international experiences, and CEOs experiences in tackling environmental issues, formulate better strategies in mitigating the adverse effects of climate change.

Finally, the results of prior studies are inconclusive with regard to the role of CEOs with international experiences, especially in the context of climate change mitigation strategies (e.g., Amran et al., Citation2015; Le & Kroll, Citation2017; Slater & Dixon-Fowler, Citation2009). Our results suggest that the influence of CEOs with international experiences on firms’ strategic response towards climate change mitigation varies, depending on the corporate activities pursued. Thus, our results contribute to the literature by highlighting the importance of analyzing climate change mitigation strategies independently rather than in combination.

The remainder of this paper is structured as follows: Section 2 describes the background of the study. Section 3 reviews the theoretical literature while Section 4 reviews the empirical literature and develops the hypotheses. Section 5 outlines the research design. Sections 6 presents the empirical results and discussions. Section 7 concludes the study.

2. Background

Malaysia has been a non-Annex 1 party to the United Nations Framework Convention on Climate Change (UNFCCC) since 1994. Unlike developed countries, such as Germany and the United Kingdom, which have laws to curb carbon emission, Malaysia has no specific legislation on carbon emissions reduction for its business organizations. Nevertheless, at an international level, the Malaysian government is supportive of progress towards climate change (see Table ).

Table 1. Key events in the Malaysian climate change initiatives and policies

In 2009, the then Prime Minister of Malaysia announced at the 15th Conference of Parties (COP15) in Copenhagen that the country has set a voluntary target towards reducing GHG emissions intensity of its GDP by 40% relative to 2005 level by 2020 (EPU, Citation2015). In conjunction with this target, the Malaysian government introduced several policies, such as the National Green Technology policy and the National policy on climate change. Moreover, the Tenth Malaysia Plan incorporated a strategy to address climate change, known as the climate resilient growth strategy (EPU, Citation2010, p. 100). The Eleventh and Twelfth Malaysia Plans continued the strategy on climate change from the previous Malaysia Plan.

In 2018, the 14th Malaysia General Election resulted in a change of government. The new government re-structured the Ministry of Natural Resources and Environment and the Ministry of Energy, Green Technology and Water as the Ministry of Energy, Science, Technology, Environment and Climate Change (MESTECC), resulting in Malaysia having one specific Ministry to address climate change issue for the very first time. From 2018 onwards, measures to address climate change issue have been on-going (see Table for detailed progress). Thus, by restructuring the Ministry as MESTECC and announcing various initiatives, climate change issues have been receiving increasing attention in Malaysia.

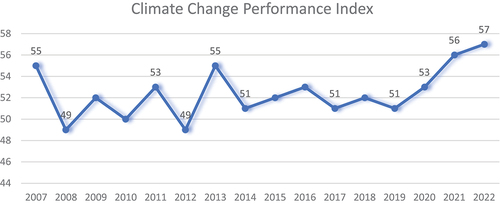

Despite the numerous initiatives by the government, the country has been having a discouraging Climate Change Performance Index. Since 2007, Malaysia has been scoring poorly on the Climate Change Performance Index (see Figure ). With the exception of 2008 and 2012, the country has been consistently ranked in a “very low” score group.Footnote1 In 2022, the Climate Change Performance Index for Malaysia worsened further, as the country was ranked 57 out of 64, thus placing Malaysia in the very low rank (Burck et al., Citation2023).

Figure 1. Climate change performance Index of Malaysia from 2007 to 2022.

The emergence of institutional pressures, as indicated by the existence of a specific Ministry in Malaysia, and the poor Climate Change Performance Index ranking, largely driven by high GHG emissions (Burck et al., Citation2023) provide an appropriate context for our study. This context raises an important question of whether institutional pressures can drive firms’ strategic response to climate change mitigation.

3. Theoretical literature review

Two theoretical frameworks are applied in this study, namely, the institutional theory and the resource-based view. The institutional theory focuses on the role of social influence and the pressure to conform in influencing firms’ actions (Oliver, Citation1997). The theory assumes that firms are motivated to comply with external influence and pressures to protect or gain legitimacy (Alatawi et al., Citation2023; Berrone et al., Citation2013; Daddi et al., Citation2020; Ntim & Soobaroyen, Citation2013; Solikhah et al., Citation2021). The institutions imposing such influence and pressures include the government, regulatory bodies, non-governmental organizations, and the media (Bansal, Citation2005; Berrone et al., Citation2013; Lebelhuber & Greiling, Citation2021).

In the context of climate change, institutional theory suggests that regulatory environment may pressure firms to take action in addressing climate change (Cadez et al., Citation2019). Formulating strategies to mitigate climate change then is one of the actions taken by the firms to comply with these pressures in order to maintain or gain their legitimacy (Pellegrino & Lodhia, Citation2012). Using institutional theory, prior studies include regulation or threat of regulation as the independent variables, and show that these regulations drive climate change mitigation strategies of the firms examined. For example, Kolk and Pinkse (Citation2005) reported that firms in European countries were formulating better strategies in addressing climate change, as they were anticipating the European Union’s regulation on GHG emissions. Likewise, a recent study by de Abreu et al. (Citation2021) documented that pressures from the government increased the likelihood of firms in the oil and gas sector in Canada to adopt a low-carbon strategy.

Unlike the institutional theory that emphasizes largely on the external pressures, the resource-based view focuses on internal processes of firms (Bansal, Citation2005; Clemens & Douglas, Citation2006). The resource-based view suggests that a company can gain a sustained competitive advantage if it makes use of the resources that are valuable, rare, non-substitutable and non-imitable (Amran et al., Citation2015; Barney, Citation1991; Elmghaamez et al., Citation2023; Lee & Rhee, Citation2006). Thus, a company’s actions and performance is influenced by the resources and capabilities that they acquired (Lee & Rhee, Citation2006).

In the case of climate change, the resource-based view suggests that a company will adopt effective environmental management strategy (such as the climate change mitigation strategies) if it possesses unique resources and capabilities that lead to competitive advantage (Backman et al., Citation2017). Empirical studies that have applied resource-based view in explaining corporate response to climate change include Lewis et al. (Citation2014), Amran et al. (Citation2015) and Chithambo et al. (Citation2020). Based on the resource-based view, these studies incorporate CEOs’ attributes, in particular the knowledge and experiences of CEOs, as the independent variables and argue that these CEOs attributes have a positive impact on firms’ strategic response towards climate change mitigation.

4. Empirical literature review and hypotheses development

4.1. Institutional pressures

Institutional pressures could come in the form of direct pressures, such as well-enforced regulation and strong monitoring (Amran et al., Citation2012; de Abreu et al., Citation2017; Okereke & Russel, Citation2010), or indirect pressures that include threat of regulations and request to disclose GHG emissions by specific bodies (Lewis et al., Citation2014; Pulver, Citation2007; Reid & Toffel, Citation2009). For example, Lewis et al. (Citation2014) argued that requests to disclose GHG emissions by the Carbon Disclosure Project (CDP), a non-profit organization, represent one type of institutional pressures. In addition, Pulver (Citation2007) showed that BP and Shell, the two major oil firms located in Europe implemented cooperative climate strategy in response to the unavoidability of mandatory GHG emissions reduction in the European Union. We extend these prior works in a different context that has been less explored by prior researchers, that is by focusing on institutional pressures through the establishment of one specific Ministry in Malaysia.

By drawing on the institutional theory, we expect that firms subjected to institutional pressures via the establishment of a specific Ministry to address the climate change issue (i.e., MESTECC) and the accompanying climate change initiatives will be more likely to have better strategic responses towards climate change mitigation, as follows:

H1:

Ceteris paribus, there is a significant positive association between institutional pressures (MESTECC) and firms’ strategic response towards climate change mitigation.

4.2. CEOs’ attributes

The influence of CEOs’ global perspective and their dedication to environmental issues on the firms’ strategic response is examined by employing two CEOs’ attributes. These are CEOs with international experiences and CEOs who have experiences in addressing environmental issues.

4.2.1. CEOs with international experiences

CEOs with international experiences can be considered as a firm’s resource which is inimitable and non-substitutable since the skills and knowledge that they acquired are difficult to attain through other means (Daily et al., Citation2000; Slater & Dixon-Fowler, Citation2009). The resource-based view argues that the broad knowledge and capabilities acquired by the CEOs through their living and working internationally help them in creating strategic business values (Le & Kroll, Citation2017; Meng et al., Citation2022; Slater & Dixon-Fowler, Citation2009). Accordingly, CEOs with international experiences are expected to bring in global perspective on climate change issues and policies, which are helpful in formulating effective strategies in mitigating climate change.

Thus far, prior studies have reported inconclusive results on the influence of CEOs with international experience on firms’ strategic actions. For example, Slater and Dixon-Fowler (Citation2009) and Le and Kroll (Citation2017) found a positive impact of CEOs with international experiences on corporate social performance and strategic change, respectively. In contrast, Amran et al. (Citation2015)’s study of five ASEAN countries including Malaysia in 2012 suggests that CEOs, whether international or local experiences, show no difference in formulating the climate change strategy.

Thus, drawing on the resource-based view of the firm, the following hypothesis is formulated:

H2a:

Ceteris paribus, there is a significant positive association between CEOs with international experiences (CEO_International) and firms’ strategic response towards climate change mitigation.

4.2.2. CEOs with experience in addressing environmental issues

CEOs’ exposure to environmental issues not only allows them to become aware of the climate risks and related opportunities but also enables them to become conscious of their environmental responsibility (Huang & Wei, Citation2023). Thus, from the perspective of the resource-based, CEOs with experiences in environmental issues can bring valuable insights and guide their firms to develop strong climate change mitigation strategies, which will enable these firms to remain competitive.

Empirical studies that examine the role of CEOs with environmental experiences or green-related experience on environmental engagement are scarce (Huang & Wei, Citation2023). The few studies that examined this issue include Walls and Berrone (Citation2017), Yang and Zhang (Citation2022), and Huang and Wei (Citation2023). For example, Walls and Berrone (Citation2017) argue and provide empirical evidence that CEOs who have experiences in addressing environmental issues positively influence the corporate environmental performance. In a similar vein, a recent study by Huang and Wei (Citation2023) also report a positive impact of the CEOs with green-related experience on environmental corporate social responsibility.

Thus, drawing on the resource-based view of the firm and the related empirical evidence, the following hypothesis is formulated:

H2b:

Ceteris paribus, there is a significant positive association between CEOs who have experiences in addressing environmental issues (CEO_Environment) and firms’ strategic response towards climate change mitigation.

5. Research design

5.1. Data collection

To gather firms’ strategic response towards climate change mitigation, we employed content analysis because this approach allows researchers to systematically filter a large number of texts (Krippendorff, Citation1980; Lee, Citation2012). Moreover, content analysis allows researchers to examine data over a longer time horizon (Downe‐Wamboldt, Citation1992), which is the focus of our study. In the context of climate change research, content analysis has been widely used by prior studies (e.g., Damert & Baumgartner, Citation2018; Lee, Citation2012; Sprengel & Busch, Citation2011; Weinhofer & Hoffmann, Citation2010) to identify corporate strategic response to climate change.

We focus exclusively on GHG management instead of various other climate change mitigation strategies for two reasons. First, as indicated by the Climate Change Performance Index (CCPI), the performance of the GHG emissions in Malaysia is poor (Burck et al., Citation2023). Second, GHG management represents an initial and critical step in mitigating climate change (Simnett et al., Citation2009). Thus, by focusing on GHG management, we aim to offer insights for reducing GHG emissions in the country.

As for the independent variables, data on CEOs attributes was collected from annual reports while financial data was extracted from Refinitiv Datastream database.

5.2. Research instrument

The research instrument that we employed to gauge firms’ strategic response towards climate change mitigation is a rating scheme that was developed by Damert and Baumgartner (Citation2018, p. 279). Following Md Zaini et al. (Citation2020), we examine the validity of the research instrument by consulting experts. Two university academic researchers who are expert in the sustainability and climate change research in Malaysia were consulted on the rating scheme. We also consulted industry experts from two listed firms concerning the climate change mitigation strategies of their firms. In addition, the research instrument deems valid, as it was in-line with the Global Reporting Initiatives (GRI) guidelines that was recommended by the Bursa Malaysia Sustainability Reporting Guidelines (Bursa Malaysia, Citation2015).

To assess inter-coder reliability, a pilot test of annual and sustainability reports of seven firms from 2017 to 2019 was conducted. Three independent coders including the first author were involved in the pilot test. Using the Krippendorff alpha, the results show an inter-rater reliability of 0.8203, indicating internal consistency of the coding procedure (Krippendorff, Citation2004). Following from the pilot test, two coders undertook the content analysis. The final score was based on a Likert scale, ranging from zero (no mention of GHG inventory at all) to four (estimated the GHG emissions, set the reduction target, and tracked the emissions).

5.3. Sample selection

This study focuses on all firms in the energy sectors that are listed on Bursa Malaysia stock exchange from 2010 to 2019. The list of the total population of listed firms in the energy sector was drawn from the website of the Securities Commission (Securities Commission Malaysia, Citation2020). Year 2010 was selected as a starting point because in 2010, the Malaysian government started to give greater emphasis to climate change issue due to the implementation of the National Climate Change Policy in 2009 and the Tenth Malaysia Plan (Economic Planning Unit, Citation2010). Table provides a summary of the sample selection. The final dataset comprises 300 firm-year observation.

Table 2. Sample selection

5.4. Variable measurement

5.4.1. Dependent variable: firms’ strategic response

The dependent variable is determined from the results of the TwoStep cluster analysis (see Section 6.1 for detailed discussion). Following from the TwoStep cluster analysis, the dependent variable is a probability of a firm to be in the emerging cluster and hence develops better strategic response toward climate change mitigation. Thus, it is a binary variable set to one for firms in the emerging cluster and zero for firms in the indifferent cluster. The different clusters have been employed by prior studies as proxies for a firm’s strategic response (e.g., Damert & Baumgartner, Citation2018; Jeswani et al., Citation2008; Lee, Citation2012).

5.4.2. Independent variables

Three independent variables are employed in this study. First, institutional pressures, proxied by the establishment of the Ministry of Energy, Science, Technology, Environment and Climate Change (MESTECC) in 2018. It is a dummy variable that takes the value of 1 from 2018 onwards when MESTECC was established, and zero in years prior to 2018.

Second, CEOs with international experiences. It is defined as CEOs who are exposed to living and working in a foreign country (Carpenter et al., Citation2001). It takes the value of 1 when a CEO possesses international experiences and zero otherwise.

Third, CEOs who have experiences in addressing environmental issues. It is defined as CEOs’ involvement with environmental activities, which include awards or honors received by CEOs for their environmental actions, or their previous appointments related to environmental issues (Walls & Berrone, Citation2017, p. 298). It takes the value of 1 when a CEO possesses environmental experiences and zero otherwise.

5.4.3. Control variables

We incorporate CEO_Tenure, CEO_Age, a firm’s size, and financial performance as control variables, as they have been found by prior studies (Clemens et al., Citation2008; de Abreu et al., Citation2021; Lee, Citation2012; Slater & Dixon-Fowler, Citation2009) to influence firms’ strategic response toward climate change. CEO_Tenure is measured based on the number of years that the CEOs have held the position (Weng & Lin, Citation2014), CEO_Age is the actual age of the CEO, firm size is measured using the natural log of total assets at the end of the prior year, and financial performance is measured by dividing net profit for the year by total assets.

5.5. Model specification

The regression model applied in this study is as per EquationEquation (1)(1)

(1) .

Where the subscripts i and t denote the firm and time in years, respectively (see Table for the definition of all variables).

Table 3. Operational definition of the variables

To estimate regression model as per EquationEquation (1)(1)

(1) , we employed two regression techniques. First, we employed robust standard errors clustered by firms to account for heteroskedasticity and correlation in the error terms, which may arise due to repeated measures. Second, we employed lagged structure approach. Following prior studies (e.g., Atif et al., Citation2020; Gul & Ng, Citation2018; Saeed et al., Citation2022), all the independent variables are lagged by one year to mitigate the possibility of an endogeneity issue arising from reverse causality. The rationale behind this approach is that the institutional pressures and firms’ internal resources (the CEOs attributes examined in this study) may take time to influence firms’ strategies, including their responses toward the climate change mitigation.

6. Empirical results and discussion

6.1. Cluster analysis: firms’ strategic response

To identify an optimal number of clusters, a TwoStep cluster analysis was conducted, which has resulted in two types of firms’ strategic response towards climate change, i.e., indifferent, and emerging. The indifferent cluster consists of 88% of the observations, while the emerging cluster represents the remaining 12% (see Table ). Our finding is consistent with Jeswani et al. (Citation2008), who reported that more than 75% of firms in Pakistan are categorized in the indifferent and beginner clusters. However, it is in contrast with Damert and Baumgartner (Citation2018), who documented that the corporate strategies of the 116 largest global automotive firms they examined from 2013 to 2014 are distributed almost evenly across four distinct clusters.

Table 4. Mean scores based on two types of strategies in mitigating climate change via GHG management

6.1.1. Firms’ strategic response: indifferent cluster

This cluster comprises largely observations from 2010 to 2016. Firms in this cluster scored very low on GHG management (a mean of 0.130 and a median of 0.000), indicating that they seem to have carried on “business as usual” without paying much attention to the GHG management. Their strategy is similar to indifferent (Jeswani et al., Citation2008), wait-and-see observer (Lee, Citation2012), and introverted laggard (Damert & Baumgartner, Citation2018) clusters identified in prior studies.

6.1.2. Firms’ strategic response: emerging cluster

This cluster is dominated by observations from 2017 to 2019. Firms in this cluster scored high on GHG management (a mean score of 3.394 and a median score of 4.000), indicating that they have monitored and prepared an inventory of GHG emissions. Their strategy resembles emerging (Jeswani et al., Citation2008), cautious reducer (Lee, Citation2012), and legitimating reducer (Damert & Baumgartner, Citation2018) clusters identified in prior studies.

6.2. Descriptive statistics

The results in Table suggest that firms in the emerging cluster faced stronger institutional pressures (MESTECC), have more CEOs with international experiences (CEO_International), and a greater number of CEOs experienced in addressing environmental issues (CEO_Environment) compared to firms in the indifferent cluster. They also have shorter CEOs’ tenure and are larger in size than those in the indifferent cluster. The tests of differences and the Chi-square test indicate that these differences are statistically significant. In addition, the results of Pearson correlation coefficients (unreported) suggest that multicollinearity is not an issue, as none of the independent variables and control variables are highly correlated.

Table 5. Descriptive statistics of the independent and control variables

6.3. Regression results

The dependent variable for our study is firms’ strategic response towards climate change mitigation, while the independent variables are institutional pressures (proxied by MESTECC) and CEOs’ attributes related to international and environmental exposures (i.e., CEO_International, and CEO_Environment, respectively). The results show that in both models (see Table ), the coefficients of MESTECC are positive and strongly significant, indicating that firms subjected to institutional pressures are more likely to formulate better strategic responses towards climate change mitigation. With a specific Ministry to address climate change, the government managed to intensify its climate change initiatives, such as through the setting up of the National Council of Climate Change Action, and discussing the need for the Climate Change Act, which create pressures for the energy firms. To gain legitimacy in the eyes of stakeholders, these firms then acquiesced with the institutional pressure by taking strategic actions to mitigate climate change (Berrone et al., Citation2013; Daddi et al., Citation2020; Lebelhuber & Greiling, Citation2021).

Table 6. Primary analyses: firms strategic responses, institutional pressures, and CEOs’ attributes

Our results are consistent with the findings of prior studies (de Abreu et al., Citation2017; Lewis et al., Citation2014; Reid & Toffel, Citation2009), which suggest that firms are more likely to engage in climate change strategies when institutional pressures are strengthened. These results confirm the predictions of institutional theory, which emphasize the importance of institutional pressures in influencing firms to respond and adopt certain practices for legitimacy purposes. Thus, our results demonstrate the applicability of the institutional theory in explaining response to climate change mitigation by firms in the energy sector in Malaysia, as an example of firms in developing countries.

As for CEOs’ attributes, the coefficients of CEO_International are positive and statistically significant, indicating that firms with CEOs who possessed international experiences are more likely to develop better strategic responses towards climate change mitigation. By working and living abroad, CEOs were exposed to different institutional environment and value system, which encourage them to have a global mindset (Slater & Dixon-Fowler, Citation2009). Moreover, the CEOs have developed better abilities and knowledge of international markets, which may help them in making strategic action (Le & Kroll, Citation2017; Meng et al., Citation2022), such as in mitigating climate change. Our findings are consistent with prior evidence from Slater and Dixon-Fowler (Citation2009) and Le and Kroll (Citation2017) who reported that CEOs with international experiences positively impacted the corporate social performance and strategic change, respectively. However, they differ from those of Amran et al. (Citation2015), who found no significant impact of CEOs with international experiences on firms’ climate change strategy in 2012. This difference may be attributed to the large gap in the years analyzed.

The coefficients of CEO_Environment are also positive and statistically significant, indicating that firms with CEOs who have experiences in addressing environmental issues are more likely to develop better strategic responses towards climate change mitigation. When CEOs are exposed to environmental issues, including climate risks and related opportunities, they are more conscious on their environmental responsibility (Huang & Wei, Citation2023). Moreover, the exposure provided the CEOs with a basis for assessing potential costs and benefits in engaging with environmental strategies (Walls & Berrone, Citation2017). Accordingly, these valuable experiences and insight allow the CEOs to formulate better strategies in mitigating climate change. Our results are consistent with prior studies who found a positive impact of CEOs with environmental experience on environmental performance (Walls & Berrone, Citation2017), environmental corporate social responsibility (Huang & Wei, Citation2023), and proactive environmental strategies (Yang & Zhang, Citation2022).

Overall, the results concerning CEOs’ attributes contribute to the literature on environmental strategies by emphasizing the significance of incorporating CEOs’ international and environmental exposures in models predicting firms’ strategic response to climate change mitigation. These findings also support the predictions of the resource-based view, which suggest that firms can leverage their valuable, rare, non-substitutable and non-imitable resources to formulate effective strategies (Amran et al., Citation2015; Barney, Citation1991; Elmghaamez et al., Citation2023; Lee & Rhee, Citation2006), such as strategies in mitigating climate change. Consequently, our results demonstrate the applicability of the resource-based view in explaining strategic response to climate change mitigation by energy firms in Malaysia, as an example of firms in a less advanced economy. With regard to the control variables, the results show that the coefficients of CEO_Tenure are negative and statistically significant, indicating that the longer the CEOs’ tenure, the less likely for the firms to adopt better strategic responses towards climate change mitigation. Possibly, this is because CEOs with longer tenure has often been associated with rigidity, and hence they are seen as more resistant to strategic change (Lewis et al., Citation2014; Miller, Citation1991; Weng & Lin, Citation2014). In addition, the coefficients of SIZE are statistically significant in a positive direction. These results are consistent with Lee (Citation2012) who suggested that larger firms are more likely to take strategic action towards managing their GHG emissions. Nevertheless, the results show that the coefficients of CEO_Age and Performance are statistically non-significant. Hence, we could not find sufficient evidence that CEOs’ age and financial performance affect firms’ strategic response towards climate change mitigation.

6.4. Robustness tests

To check the robustness of our results, we conducted several sensitivity tests, as discussed below.

6.4.1. Tests of endogeneity

Our analysis of the influence of CEOs’ attributes (i.e., CEOs with international experiences and those with experiences in addressing environmental issues) on firms’ strategic response to climate change mitigation may suffer from endogeneity issues arising from self-selection bias. Following prior studies (e.g., Bose et al., Citation2022; Gangi et al., Citation2019; Gul et al., Citation2020), we employ Heckman’s (Citation1979) two-stage model to address this self-selection bias. In the first stage, we estimate logistic regression using CEOs’ exposure to international or environmental experiences as the dependent variable. It is a dummy variable is a proxy for an existence of CEOs with international experience and/or those with experiences in addressing environmental issues. Based on prior studies (e.g., Carpenter et al., Citation2001; Slater & Dixon-Fowler, Citation2009), we include firms’ internationalization (Internationalization, measured in terms of an existence of foreign production) in the right-hand equation of the first-stage regression analysis. We also include CEOs’ characteristics (i.e., CEOs’ ethnicity, tenure and age) and all other control variables employed in EquationEquation (1)(1)

(1) into the first-stage regression analysis.

In the second stage, we compute an inverse Mills ratio (IMR) based on the estimated coefficients from the first stage. Next, we re-run EquationEquation (1)(1)

(1) after adding IMR. Table reports the results of the first-stage and the second-stage regressions. The coefficient of IMR is non-significant while the coefficients of all other variables are generally consistent with those in the primary analyses (in Table ), suggesting that our primary analyses are robust to self-selection bias.

Table 7. Endogeneity tests: Heckman’s (1979) two-stage model

6.4.2. Alternative measurement of the dependent variable

In this study, similar to Coles et al. (Citation2014) and Damert and Baumgartner (Citation2018), the dependent variable is derived from TwoStep cluster analysis. To test whether the results will be influenced by a specific clustering technique, we generate an alternative-dependent variable using the average linkage method, which is one of the agglomerative hierarchical clustering techniques that have been employed by prior studies (e.g., Munoz et al., Citation2015; Vărzaru et al., Citation2021). Using the alternative-dependent variable, we re-ran the regression analyses. The new results (see Table ) are generally consistent with those in the primary analyses, suggesting that the results are not biased by a specific clustering technique.

Table 8. Robustness tests: alternative measure of firms’ strategic responses, and imbalanced dataset

6.4.3. Imbalance dataset

The emerging cluster comprises a small number of observations, i.e., 33 firm-years, which may bias the results. We address this issue by match-pairing the 33 firm-years observations in the emerging cluster with the observations in the indifferent cluster based on a firm’ size, measured by prior year total assets. The results (see Table ) show that the coefficients of MESTECC, CEO_International, and CEO_Environment are largely consistent with the primary analyses, indicating that the main analyses are unlikely to be biased by the uneven observations.

6.4.4. Influence of international pressures

Although our measure for the institutional pressures (MESTECC) intends to capture changes in the regulatory environment in Malaysia throughout the ten-year period of analysis, it is possible that it may also capture other changes over time, in particular, the worldwide increased pressures for reducing the GHG emissions. Examples of international pressures include the Paris Agreement signed in 2016 to limit the global warming below 2 degrees Celsius that are signed by 194 parties worldwide (Hibiscus Petroleum Berhad, Citation2019; Hunnes & Ntim, Citation2019; Orazalin et al., Citation2023; Nathalia & Setiawan, Citation2022; United Nations, Citationn.d) and the International Maritime Organization that implemented Sulphur Cap regulations in 2020 to reduce marine sector emissions (Malaysia Marine and Heavy Engineering Berhad, Citation2019). Consequently, energy firms examined in this study may have formulated better strategic response towards climate change mitigation due to these international pressures. We attempt to control for these international pressures by incorporating three additional variables into EquationEquation (1)(1)

(1) . These are: (i) Foreign_sales, measured by the ratio of foreign sales to total sales, (ii) Foreign_sales_Dummy, a dummy variable set to 1 with an existence of foreign sales, and zero otherwise, and (iii) Strong_Legislation, a dummy variable set to 1 when a firm traded in a foreign country with strong climate change legislation as stated by the Climate change committee (Citation2020). We test the hypothesis that firms’ strategic responses are positively associated with the international pressures, by including these three measures, independently, and re-estimating EquationEquation (1)

(1)

(1) . The results (see Table ) show that the coefficients of the three measures of the international pressures are non-significant while the coefficients of the remaining variables are largely consistent with the primary analyses, suggesting that the primary analyses are unlikely to be driven by the international pressures.

Table 9. Robustness tests: controlling for international pressures

Overall, the robustness tests performed demonstrated that institutional pressures and firms’ internal resources examined in this study have a positive influence on firms’ strategic response in mitigating climate change, even when employing an alternative dependent variable measure, passing the endogeneity tests, addressing dataset imbalance, and accounting for international pressures.

7. Summary and conclusion

Climate change is considered as the biggest challenge that the world encounter in achieving sustainable development (UNFCCC, Citation2020; World Bank, Citation2014). As a result, research on firms’ strategic responses toward climate change mitigation is growing, especially focusing on the largest firms worldwide and firms in advanced countries. Since combatting climate change requires global efforts, we build on the prior research to examine how energy firms in Malaysia, as an example of firms in a less advanced economy, have responded to climate change mitigation and what the drivers to these climate change mitigation strategies.

We find that energy firms in Malaysia have responded to climate change mitigation in two ways, and these responses have evolved over time. One group of energy firms seems to be indifferent toward the climate change mitigation. Firms in this indifferent cluster tend to conduct their business as usual without managing the GHG emissions. Another group of energy firms have started taking actions to mitigate climate change. Firms in this emerging cluster have tracked and reported the GHG emissions, and set the emissions reduction targets.

To encourage firms’ engagement with climate change mitigation, policymakers should therefore adopt two different approaches. The first approach, targeted at firms in the indifferent cluster, must encourage them to publicly report their GHG emissions so that they are accountable for the impact of their business activities on the environment. Accordingly, the regulatory bodies need to standardize and monitor the reporting of GHG emissions. The second approach, aimed at firms in the emerging cluster, must provide incentives to encourage them to take further steps by setting up a clear target reduction plan in their GHG management and to focus on other climate change mitigation actions that can lessen GHG emissions.

In terms of drivers behind the firms’ strategic responses, our findings indicate two main factors significantly influence the responses of energy firms to mitigate climate change. First, we find that institutional pressures, as proxied by the establishment of a specific Ministry to address the climate change issue, positively impacted firms’ strategic response. Thus, these results underscore the need for regulatory bodies to enhance their enforcement and monitoring in order to improve firms’ strategic responses to mitigating climate change.

Second, we find that CEOs attributes, in particular, CEOs with international experiences and those with experiences in addressing environmental issues, positively influences the responses of energy firms to mitigate climate change. These results highlight the importance of increasing awareness of the climate change issue among CEOs, as their knowledge and experiences can assist firms in formulating better strategies to mitigate climate change. Both regulatory bodies and corporate board of directors should therefore include climate change programs in the directors’ training agenda and encourage CEOs, especially those with limited international and environmental exposure and longer tenures, to participate in these programs.

In interpreting the results of this study, at least two main limitations should be recognized. First, this study focusses on one specific sector, i.e., the energy sector, which may result in limited generalizability to other sectors. Nonetheless, other sectors, especially those that are environmentally sensitive, also encounter pressures to address climate change issue. Thus, future research should examine whether the CEOs attributes identified in this study are applicable in different industries with similar environmental concerns. Moreover, future research should explore the roles of board of directors in driving firms’ climate change strategies.

Second, the sample size is small with imbalanced dataset. Nevertheless, the robustness test performed in this study suggests that the uneven observation does not bias the results. In addition, the small number of observations represents the total population of listed firms in the energy sector in Malaysia. Future research should undertake comparative study approaches analyzing the determinants of climate change mitigation strategies among energy firms in countries that scored very poor in the Climate Change Performance Index. The results of such studies could then offer policy suggestions for improving climate performance worldwide.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. See Burck et al. (Citation2023) for the detailed ranking.

References

- Alatawi, I. A., Ntim, C. G., Zras, A., & Elmagrhi, M. H. (2023). CSR, financial and non-financial performance in the tourism sector: A systematic literature review and future research agenda. International Review of Financial Analysis, 89, 102734. https://doi.org/10.1016/j.irfa.2023.102734

- Amran, A., Ooi, S. K., Nejati, M., Zulkafli, A. H., & Lim, B. A. (2012). Relationship of firm attributes, ownership structure and business network on climate change efforts: Evidence from Malaysia. International Journal of Sustainable Development & World Ecology, 19(5), 406–21. https://doi.org/10.1080/13504509.2012.720292

- Amran, A., Ooi, S. K., Wong, C. Y., & Hashim, F. (2015). Business strategy for climate change: An ASEAN perspective. Corporate Social Responsibility and Environmental Management, 23(4), 213–227. https://doi.org/10.1002/csr.1371

- Atif, M., Alam, M. S., & Hossain, M. (2020). Firm sustainable investment: Are female directors greener? Business Strategy and the Environment, 29(8), 3449–3469. https://doi.org/10.1002/bse.2588

- Backman, C. A., Verbeke, A., & Schulz, R. A. (2017). The drivers of corporate climate change strategies and public policy: A new resource-based view perspective. Business & Society, 56(4), 545–575. https://doi.org/10.1177/0007650315578450

- Bansal, P. (2005). Evolving sustainability: A longitudinal study of corporate sustainable development. Strategic Management Journal, 26(3), 197–218. https://doi.org/10.1002/smj.441

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/10.1177/014920639101700108

- Berrone, P., Fosfuri, A., Gelabert, L., & Gomez-Mejia, L. R. (2013). Necessity as the mother of ‘green’ inventions: Institutional pressures and environmental innovations. Strategic Management Journal, 34(8), 891–909. https://doi.org/10.1002/smj.2041

- Boiral, O., Henri, J.-F., & Talbot, D. (2012). Modeling the impacts of corporate commitment on climate change. Business Strategy and the Environment, 21(8), 495–516. https://doi.org/10.1002/bse.723

- Bose, S., Ali, M. J., Hossain, S., & Shamsuddin, A. (2022). Does CEO–audit committee/board interlocking matter for corporate social responsibility? Journal of Business Ethics, 179(3), 819–847. https://doi.org/10.1007/s10551-021-04871-8

- Burck, J., Uhlich, T., Bals, C., Höhne, N., Nascimento, L., Tavares, M., & Strietzel, E. (2023). Climate change performance Index 2022. Retrieved from https://ccpi.org/download/climate-change-performance-index-2023/

- Bursa Malaysia. (2015). Sustainability reporting Guide. https://www.bursamalaysia.com/sites/5bb54be15f36ca0af339077a/content_entry5ce3b5005b711a1764454c1a/5ce3c83239fba2627b286508/files/bursa_malaysia_sustainability_reporting_guide-final.pdf?1570701456

- Cadez, S., & Czerny, A. (2016). Climate change mitigation strategies in carbon-intensive firms. Journal of Cleaner Production, 112(5), 4132–4143. https://doi.org/10.1016/j.jclepro.2015.07.099

- Cadez, S., Czerny, A., & Letmathe, P. (2019). Stakeholder pressures and corporate climate change mitigation strategies. Business Strategy and the Environment, 28(1), 1–14. https://doi.org/10.1002/bse.2070

- Carpenter, M. A., Sanders, W. G., & Gregersen, H. B. (2001). Bundling human capital with organizational context: The impact of international assignment experience on multinational firm performance and CEO pay. Academy of Management Journal, 44(3), 493–511. https://doi.org/10.2307/3069366

- Chithambo, L., Tingbani, I., Agyapong, G. A., Gyapong, E., & Damoah, I. S. (2020). Corporate voluntary greenhouse gas reporting: Stakeholder pressure and the mediating role of the chief executive officer. Business Strategy and the Environment, 29(4), 1666–1683. https://doi.org/10.1002/bse.2460

- Clemens, B., Bamford, C. E., & Douglas, T. J. (2008). Choosing strategic responses to address emerging environmental regulations: Size, perceived influence and uncertainty. Business Strategy and the Environment, 17(8), 493–511. https://doi.org/10.1002/bse.601

- Clemens, B., & Douglas, T. J. (2006). Does coercion drive firms to adopt ‘voluntary’ green initiatives? Relationships among coercion, superior firm resources, and voluntary green initiatives. Journal of Business Research, 59(4), 483–491. https://doi.org/10.1016/j.jbusres.2005.09.016

- Climate change committee. (2020). The UK climate change Act. https://www.theccc.org.uk/wp-content/uploads/2020/10/CCC-Insights-Briefing-1-The-UK-Climate-Change-Act.pdf

- Coles, T., Zschiegner, A. K., & Dinan, C. (2014). A cluster analysis of climate change mitigation behaviours among SMTEs. Tourism Geographies, 16(3), 382–399. https://doi.org/10.1080/14616688.2013.851270

- Daddi, T., Bleischwitz, R., Todaro, N. M., Gusmerotti, N. M., & Giacomo, M. R. (2020). The influence of institutional pressures on climate mitigation and adaptation strategies. Journal of Cleaner Production, 20 January 2020 244, 118879. https://doi.org/10.1016/j.jclepro.2019.118879.

- Daily, C. M., Certo, T. S., & Dalton, D. R. (2000). International experience in the executive suite: The path to prosperity? Research notes and communications. Strategic Management Journal, 21(4), 515–523. https://doi.org/10.1002/(SICI)1097-0266(200004)21:4<515:AID-SMJ92>3.0.CO;2-1

- Damert, M., & Baumgartner, R. J. (2018). Intra-sectoral differences in climate change strategies: Evidence from the global automotive industry. Business Strategy and the Environment, 27(3), 265–281. https://doi.org/10.1002/bse.1968

- de Abreu, M. C. S., de Freitas, A. R. P., & Reboucas, S. M. D. P. (2017). Conceptual model for corporate climate change strategy development: Empirical evidence from the energy sector. Journal of Cleaner Production, 165, 382–392. https://doi.org/10.1016/j.jclepro.2017.07.133

- de Abreu, M. C. S., Webb, K., Araújo, F. S. M., & Cavalcante, J. P. L. (2021). From “business as usual” to tackling climate change: Exploring factors affecting low-carbon decision-making in the Canadian oil and gas sector. Energy Policy, 148, 111932. https://doi.org/10.1016/j.enpol.2020.111932

- Downe‐Wamboldt, B. (1992). Content analysis: Method, applications, and issues. Health Care for Women International, 13(3), 313–321. https://doi.org/10.1080/07399339209516006

- Economic Planning Unit. (2010). Tenth Malaysia Plan 2011-2015. https://www.pmo.gov.my/dokumenattached/RMK/RMK10_Eds.pdf/

- Elmghaamez, I. K., Nwachukwu, J., & Ntim, C. G. (2023). ESG disclosure and financial performance of multinational enterprises: The moderating effect of board standing committees. International Journal of Finance & Economics. https://doi.org/10.1002/ijfe.2846

- EPU. (2010). Tenth Malaysia Plan 2011-2015. The Economic Planning Unit (EPU), Prime Minister’s department, Putrajaya. Retrieved March 5, 2021, from https://www.pmo.gov.my/dokumenattached/RMK/RMK10_Eds.pdf

- EPU. (2015). Economic Planning Unit (EPU). Prime Minister’s department. Eleventh Malaysia Plan 2016-2020. Anchoring growth on people. Retrieved March 5, 2021, from https://www.pmo.gov.my/dokumenattached/speech/files/RMK11_Speech.pdf

- Gangi, F., Meles, A., D’Angelo, E., & Daniele, L. M. (2019). Sustainable development and corporate governance in the financial system: Are environmentally friendly banks less risky? Corporate Social Responsibility and Environmental Management, 26(3), 529–547. https://doi.org/10.1002/csr.1699

- Gul, F. A., Khedmati, M., & Shams, S. M. (2020). Managerial acquisitiveness and corporate tax avoidance. Pacific-Basin Finance Journal, 64, 101056. https://doi.org/10.1016/j.pacfin.2018.08.010

- Gul, F. A., & Ng, A. C. (2018). Auditee religiosity, external monitoring, and the pricing of audit services. Journal of Business Ethics, 152(2), 409–436. https://doi.org/10.1007/s10551-016-3284-6

- Heckman, J. J. (1979). Sample selection bias as a specification error. Econometrica, 47, 153–161.

- Hibiscus Petroleum Berhad. (2019). Retrieved from https://www.bursamalaysia.com/market_information/announcements/company_announcement/announcement_details?ann_id=3303092

- Huang, R., & Wei, J. (2023). Does CEOs’ green experience affect environmental corporate social responsibility? Evidence from China. Economic Analysis and Policy, 79, 205–231. https://doi.org/10.1016/j.eap.2023.06.012

- Hunnes, J. A., & Ntim, C. G. (2019). More planet and less profit? The ethical dilemma of an oil producing nation. Cogent Business & Management, 6(1), 1648363. https://doi.org/10.1080/23311975.2019.1648363

- Jaafar, S. S. (2019). Climate governance initiative launches Malaysian chapter, first in Asia. The Edge Markets. Retrieved March 5, 2021, from https://www.theedgemarkets.com/article/climate-governance-initiative-launches-malaysian-chapter-first-asia

- Jeswani, H. K., Wehrmeyer, W., & Mulugetta, Y. (2008). How warm is the corporate response to climate change? Evidence from Pakistan and the UK. Business Strategy and the Environment, 18(1), 46–60. https://doi.org/10.1002/bse.569

- Kolk, A., & Pinkse, J. (2005). Business responses to climate change: Identifying emergent strategies. California Management Review, 47(3), 6–20. https://doi.org/10.2307/41166304

- Krippendorff, K. (1980). Content analysis: An introduction to its methodology. Sage.

- Krippendorff, K. (2004). Reliability in content analysis: Some common misconceptions and recommendations. Human Communication Research, 30(3), 411–433. https://doi.org/10.1093/hcr/30.3.411

- Lamb, W. F., Wiedmann, T., Pongratz, J., Andrew, R., Crippa, M., Olivier, J. G., Wiedenhofer, D., Mattioli, G., Khourdajie, A. A., House, J., Pachauri, S., Figueroa, M., Saheb, Y., Slade, R., Hubacek, K., Sun, L., Ribeiro, S. K., Khennas, S., de la Rue du Can, S., & Gu, B.… Minx, J. (2021). A review of trends and drivers of greenhouse gas emissions by sector from 1990 to 2018. Environmental Research Letters, 16(7), 073005. https://doi.org/10.1088/1748-9326/abee4e

- Lebelhuber, C., & Greiling, D. (2021). Strategic response to institutional pressures of climate change: An exploration among gas sector companies. Review of Managerial Science, 16(3), 1–43. https://doi.org/10.1007/s11846-021-00449-w

- Lee, S.-Y. (2012). Corporate carbon strategies in responding to climate change. Business Strategy and the Environment, 21(1), 33–48. https://doi.org/10.1002/bse.711

- Lee, S. Y., & Rhee, S.-K. (2006). The change in corporate environmental strategies: A longitudinal empirical study. Management Decision, 45(2), 196–216. https://doi.org/10.1108/00251740710727241

- Le, S., & Kroll, M. (2017). CEO international experience: Effects on strategic change and firm performance. Journal of International Business Studies, 48(5), 573–595. https://doi.org/10.1057/s41267-017-0080-1

- Leoi, L. S. W. E. (2018). Act-ing on climate change. The Star. Retrieved March 5, 2021, from https://www.thestar.com.my/news/nation/2018/12/12/acting-on-climate-change-malaysia-drafting-laws-in-efforts-to-overcome-any-possible-scenario

- Lewis, B. W., Walls, J. L., & Dowell, G. W. S. (2014). Research note and commentaries. Differences in degrees: CEO characteristics and firm environmental disclosure. Strategic Management Journal, 35(5), 712–722. https://doi.org/10.1002/smj.2127

- Malaysia Marine and Heavy Engineering Berhad. (2019). Retrieved from https://www.bursamalaysia.com/market_information/announcements/company_announcement/announcement_details?ann_id=3032855

- Malaysia Ministry of Environment and Water. (2020). Malaysia Third biennial update report to the UNFCCC. Retrieved March 11, 2021, from https://unfccc.int/sites/default/files/resource/MALAYSIA_BUR3-UNFCCC_Submission.pdf

- Masood, E., & Tollefson, J. (2021). ‘COP26 hasn’t solved the problem’: Scientists react to UN climate deal. Nature. Retrieved 30, 2021, from https://www.nature.com/articles/d41586-021-03431-4

- Md Zaini, S., Sharma, U., Samkin, G., & Davey, H. (2020, January). Impact of ownership structure on the level of voluntary disclosure: A study of listed family-controlled companies in Malaysia. Accounting Forum, 44(1), 1–34. https://doi.org/10.1080/01559982.2019.1605874

- Meng, S., Wang, P., & Yu, J. (2022). Going abroad and going green: The effects of top Management teams’ overseas experience on green innovation in the Digital Era. International Journal of Environmental Research and Public Health, 19(22), 14705. https://doi.org/10.3390/ijerph192214705

- Miller, D. (1991). Stale in the saddle: CEO tenure and the match between organization and environment. Management Science, 37(1), 34–52. https://doi.org/10.1287/mnsc.37.1.34

- Muñoz, R. M., Pablo, J. D. S. D., & Peña, I. (2015). Linking corporate social responsibility and financial performance in Spanish firms. European Journal of International Management, 9(3), 368–383.

- Nathalia, C., & Setiawan, D. (2022). Does board capital improve climate change disclosures? Cogent Business & Management, 9(1), 2121242. https://doi.org/10.1080/23311975.2022.2121242

- Ntim, C. G., & Soobaroyen, T. (2013). Corporate governance and performance in socially responsible corporations: New empirical insights from a Neo‐institutional framework. Corporate Governance an International Review, 21(5), 468–494. https://doi.org/10.1111/corg.12026

- Okereke, C., & Russel, D. (2010). Regulatory pressure and competitive dynamics: Carbon management strategies of UK energy-intensive companies. California Management Review, 52(4), 100–124. https://doi.org/10.1525/cmr.2010.52.4.100

- Oliver, C. (1997). Sustainable competitive advantage: Combining institutional and resource-based views. Strategic Management Journal, 18(9), 697–713. https://doi.org/10.1002/(SICI)1097-0266(199710)18:9<697:AID-SMJ909>3.0.CO;2-C

- Omar, N. B., & Amran, A. (2017). Corporate governance and climate change reporting in Malaysia. The International Journal of Academic Research in Business & Social Sciences, 17(12), 222–240. https://doi.org/10.6007/IJARBSS/v7-i12/3607

- Orazalin, N. S., Ntim, C. G., & Malagila, J. K. (2023). Board sustainability committees, climate change initiatives, carbon performance, and market value. British Journal of Management. https://doi.org/10.1111/1467-8551.12715

- Pellegrino, C., & Lodhia, S. (2012). Climate change accounting and the Australian mining industry: Exploring the links between corporate disclosure and the generation of legitimacy. Journal of Cleaner Production, 36, 68–82. https://doi.org/10.1016/j.jclepro.2012.02.022

- Pulver, S. (2007). Importing environmentalism: Explaining Petroleos Mexicanos’ cooperative climate policy. Studies in Comparative International Development, 42(3–4), 233–255. https://doi.org/10.1007/s12116-007-9010-8

- Reid, E. M., & Toffel, M. W. (2009). Responding to public and private politics: Corporate disclosure of climate change strategies. Strategic Management Journal, 30(11), 1157–1178. https://doi.org/10.1002/smj.796

- Rincon, P. (2021). COP26: New global climate deal struck in Glasgow. Science Editor, BBC News Website. Retrieved November 30, 2021, from https://www.bbc.com/news/world-59277788

- Saeed, A., Riaz, H., Liedong, T. A., & Rajwani, T. (2022). The impact of TMT gender diversity on corporate environmental strategy in emerging economies. Journal of Business Research, 141, 536–551. https://doi.org/10.1016/j.jbusres.2021.11.057

- Securities Commission Malaysia. (2020). List of shariah-compliant securities. Retrieved March 11, 2021, from https://www.sc.com.my/api/documentms/download.ashx?id=7b5e5a18-0108-48fe-8d2e-1f6bfc78f217

- Siegel, D. S. (2014). Responsible leadership. Academy of Management Perspectives, 28(3), 221–223. https://doi.org/10.5465/amp.2014.0081

- Simnett, R., Nugent, M., & Huggins, A. L. (2009). Developing an international assurance standard on greenhouse gas statements. Accounting Horizons, 23(4), 347–363. https://doi.org/10.2308/acch.2009.23.4.347

- Slater, D. J., & Dixon-Fowler, H. R. (2009). CEO international assignment experience and corporate social performance. Journal of Business Ethics, 89(3), 473–489. https://doi.org/10.1007/s10551-008-0011-y

- Solikhah, B., Maulina, U., & Ntim, C. G. (2021). Factors influencing environment disclosure quality and the moderating role of corporate governance. Cogent Business & Management, 8(1), 1876543. https://doi.org/10.1080/23311975.2021.1876543

- Sprengel, D. C., & Busch, T. (2011). Stakeholder engagement and environmental strategy–the case of climate change. Business Strategy and the Environment, 20(6), 351–364. https://doi.org/10.1002/bse.684

- Tang, K. H. D. (2019). Climate change in Malaysia: Trends, contributors, impacts, mitigation and adaptations. Science of the Total Environment, 650, 1858–1871. https://doi.org/10.1016/j.scitotenv.2018.09.316

- UNFCCC. (2020). Action on climate and SDGs. 2020 United Nations framework convention on climate change (UNFCCC). Retrieved April 11, 2021, from https://unfccc.int/topics/action-on-climate-and-sdgs/action-on-climate-and-sdgs

- United Nations. (n.d). https://www.un.org/en/climatechange/paris-agreement

- Vărzaru, A. A., Bocean, C. G., & Nicolescu, M. M. (2021). Rethinking corporate responsibility and sustainability in light of economic performance. Sustainability, 13(5), 2660. https://doi.org/10.3390/su13052660

- Walls, J. L., & Berrone, P. (2017). The power of one to make a difference: How informal and formal CEO power affect environmental sustainability. Journal of Business Ethics, 145(2), 293–308. https://doi.org/10.1007/s10551-015-2902-z

- Weinhofer, G., & Hoffmann, V. H. (2010). Mitigating climate change – how do corporate strategies differ? Business Strategy and the Environment, 19(2), 77–89. https://doi.org/10.1002/bse.618

- Weng, D. H., & Lin, Z. J. (2014). Beyond CEO tenure: The effect of CEO newness on strategic changes. Journal of Management, 40(7), 2009–2032. https://doi.org/10.1177/0149206312449867

- World Bank. (2014). Climate change is a challenge for sustainable development. Retrieved from https://www.worldbank.org/en/news/speech/2014/01/15/climate-change-is-challenge-for-sustainable-development.

- World Economic Forum. (2020). The Global Risks Report 2020. Retrieved March 5, 2021, from https://www.weforum.org/reports/the-global-risks-report-2020

- Wright, C., & Nyberg, D. (2017). An inconvenient truth: How organizations translate climate change into business as usual. Academy of Management Journal, 60(5), 1633–1661. https://doi.org/10.5465/amj.2015.0718

- Yang, C., & Zhang, L. (2022). CEO environmentally specific transformational leadership and firm proactive environmental strategy: Roles of TMT green commitment and regulative pressure. Personnel Review. https://doi.org/10.1108/PR-02-2021-0114