Abstract

Although studies on climate change and accounting have garnered paramount interest in last decade, there is a void in the literature in terms of a summary overview of climate change and accounting. This study aims to provide a state-of-the-art summary of the literature on climate change and accounting. For this, it uses the PRISMA protocol, VOSViewer, and R. The analysis is based on big data from Scopus for the period between 2013 and 2023. Similarly, co-occurrence and co-authorship analyses are also performed. The results show a significant increase in related research during the last decade, which reached its peak in 2022. This increase is attributed to increased publishing opportunities and intensive efforts, particularly in countries such as China and United States. Additionally, robust organizational support, such as universities, funding sponsors, and author productivity, are found to significantly contribute to this growth. Key events, such as the Paris Agreement, Sustainable Development Goals (SDGs), and accounting standards also play a pivotal role in driving this growth. This study shows the transformation of the accounting literature in addressing climate change, leading to the emergence of new disciplines, including Environmental Management Accounting (EMA) and carbon accounting. In conclusion, this study provides a comprehensive synthesis of the fragmented literature and suggests potential avenues for future review.

1. Introduction

Climate change caused by human activities is having significant impact on both physical ecosystems and societal transformations (Benavent et al., Citation2017; Cavicchioli et al., Citation2019). Furthermore, it represents a significant challenge that exerts far-reaching repercussions on the natural world, economy, and society. The United Nations (Citation2022) has declared that failure to address climate change poses the most critical risk confronting the global population. Furthermore, scientific consensus has firmly underscored the anthropogenic nature of climate change, sparking concerted international efforts to mitigate its impacts and foster adaptation to the evolving climate. The implications of this situation extend across various sectors, shaping the social, economic, and scientific landscapes, including those of finance and accounting (Auffhammer, Citation2018; Kundzewicz et al., Citation2018; Thomas et al., Citation2019). The finance and accounting disciplines are actively contemplating their roles and responsibilities to address this multifaceted issue.

Traditionally focused on financial reporting and compliance, accounting is undergoing a transformation to incorporate sustainability considerations into its practices. Climate change has introduced significant risks to businesses. These risks embody its physical impacts, such as extreme weather events, and transition risks related to evolving regulations, shifting consumer preferences, and technological advancements (Hasegawa et al., Citation2021; Malhi et al., Citation2021; Sam et al., Citation2020; Xie et al., Citation2018). First, extreme weather events such as floods, forest fires, and heat waves interrupt supply chains, damage infrastructure, and disrupt company operations (production delays and revenue loss) (Ali et al., Citation2023), thereby causing financial losses. Second, governments and other regulators are becoming increasingly aware of the need to mitigate greenhouse gas emissions and adapt to climate change. Therefore, new regulations and policies have been implemented, such as incentives on sustainable practices and carbon pricing (Haites, Citation2018). Third, with the increasing awareness of environmental issues, consumers increasingly prefer products and services with lower carbon footprints or support for sustainability (Nekmahmud et al., Citation2022). Moreover, climate change encourages innovation and resource efficiency through sustainable business models (Bocken et al., Citation2019; Geissdoerfer et al., Citation2018).

The relationship between climate change and accounting extends beyond mere financial reporting. It contains broader dimensions, such as the role of accounting in assessing natural capital, quantifying emissions, and identifying environmentally sustainable investments. Stakeholders are demanding heightened transparency, precision, and uniformity in environmental information disclosure (Kuo et al., Citation2013; Rashed et al., Citation2022). This demand has propelled endeavors to harmonize reporting standards (Cantele et al., Citation2018; Rounaghi, Citation2019). There have been several attempts to streamline accounting on climate change issues; for example, the Global Reporting Initiative (GRI), founded in 1997 by the Coalition for Environmentally Responsible Economies (CERES) and United Nations Environment Programme (UNEP), Sustainability Accounting Standards Board (SASB), International Financial Reporting Standard (IFRS), Task Force on Climate-Related Financial Disclosure (TCFD), which was created by the Financial Stability Board in 2015, Partnership for Carbon Accounting Financials (PCAF) introduced by Dutch banks in 2015, Greenhouse Gas Protocol created by World Resources Institute (WRI) and World Business Council for Sustained Development (WBCSD) in 1997, audit and assurance, and integrated reporting by the International Integrated Reporting Council (IIRC).

With the increasing urgency to address climate change, the field of accounting has stood at a critical juncture. Although substantial progress has been made, persistent challenges remain in terms of data accessibility, standardization, and development of robust methodologies. Several studies have examined climate change from various perspectives, such as board expertise (Nathalia & Setiawan, Citation2022), ownership structure (Giannarakis et al., Citation2018), and corporate governance (Naciti et al., Citation2022). Previous studies have also conducted bibliometric analyses on various topics, such as institutions, the Paris Agreement, carbon markets, green finance, tourism, investments, technological innovation, and diverse sectors (Du et al., Citation2015; Estevao, Citation2021; Joshi & Dash, Citation2023; Muchiri et al., Citation2022; Scott & Gössling, Citation2022; Tautiva et al., Citation2022; Tuest et al., Citation2022; Wang et al., Citation2018; Wohlgezogen et al., Citation2020; Xu & Liu, Citation2023). Tuest et al. (Citation2022) have performed a bibliometric analysis using separate management accounting and carbon keyword searches. This helps eliminate contributions from other accounting-related research, such as environmental accounting and taxation. Despite the increasing intersection of climate change analysis and accounting, there has been no concerted effort to synthesize existing knowledge in this domain. No previous investigations have bridged the gap between climate change and accounting through bibliometric analysis. While existing literature has relied on the Web of Science (WoS) database, this research adopts the Scopus database because it possesses unique attributes in the context of social and humanities; therefore, Scopus provides a better representation of the literature than WoS (Pranckutė, Citation2021), which is more suitable for bibliometric review (Abhilash et al., Citation2023; Ahmad et al., Citation2023; Antwi et al., Citation2022). The overarching objective of using Scopus is to comprehensively analyze the interplay between climate change and accounting.

This study contributes to the ongoing discourse by examining the relationship between climate change and accounting by asking the following question: How did research on climate change and accounting evolve and how could it advance further? Furthermore, a systematic review is conducted in four stages and uses bibliometric methods to synthesize the existing literature. This research contributes to the literature in the following ways: (1) It provides a comprehensive summary of the fragmented literature using big data technology, particularly bibliometric analysis. (2) The analysis identifies key historical milestones, such as influential authors, journals, and institutions. (3) It offers implications for policymakers, regulators, and businesses with respect to refining accounting practices to address the challenges and opportunities posed by climate change. Overall, the aforementioned contributions provide valuable insights that can broaden the scope of this research.

2. Literature review

Climate change has emerged as a global challenge with significant impacts on economies, societies, and ecosystems (Abbass et al., Citation2022; Feliciano et al., Citation2022; Filho et al., Citation2021; Rocha et al., Citation2022). Accounting has assumed a pivotal role in responding to the need to address this crisis. This field serves as a key instrument for comprehending, quantifying, and conveying the impacts of climate change on corporate operations and financial performance (Linnenluecke et al., Citation2015). The dynamic interaction between climate change and accounting involves a diverse array of dimensions, ranging from the intricacies in carbon emission calculations to the integration of climate risks and opportunities into the framework of financial reporting (Gulluscio et al., Citation2020; Ngwakwe, Citation2012).

An indispensable facet of the intricate nexus between climate change and accounting is the measurement and disclosure of greenhouse gas emissions and other environmental impacts. Organizations play a crucial role in precise and transparent accounting practices in the pursuit of shrinking their carbon footprint and augmenting their sustainability profiles (Gardner et al., Citation2019). Carbon accounting, a pivotal dimension in this context, entails meticulous tracking and computation of emissions. Furthermore, it empowers organizations to monitor their contributions to climate change and implement effective mitigation strategies. This imperative, extended beyond internal management practices, impacts external stakeholders, including investors, regulators, and discerning customers, all of whom increasingly advocate for heightened transparency in emissions reporting.

There have been several debates regarding the reporting of climate information. First, not all climate change-related information is financially material, but comprehensive disclosure provides a broad insight to stakeholders (Jorgensen et al., Citation2022; Venturelli et al., Citation2019). Second, the measurement and quantification of risks and opportunities associated with climate change is complex, uncertain, and potentially misleading (Simpson et al., Citation2021; Ye et al., Citation2021). Therefore, the development of metrics and standardized methodologies is necessary (Pinchot et al., Citation2021; Wright et al., Citation2011). The third is mandatory and voluntary disclosure. Fourth, credibility and greenwashing require independent third-party assurances to guarantee the accuracy of information provided by the company (Fernando et al., Citation2014). This highlights the importance of accounting in the debate on climate change issues in the business world.

The dynamic landscape of climate change necessitates the integration of climate considerations into financial reporting (Galeone et al., Citation2023). Accounting standards and reporting guidelines are required to improve the consistency, transparency, and comparability of information disclosure by companies (Ebaid, Citation2022). The lack of strict climate change regulations may allow companies to operate without significant disruptions; however, it can also hinder their motivation to invest in sustainable practices and demotivate them to address sustainability challenges (Hermundsdottir & Aspelund, Citation2021). Enhancing traditional financial reporting frameworks with climate-related data offers a more comprehensive depiction of organizational risks and opportunities while diminishing information disparities between management and investors. Disclosures pertaining to both physical and transition risks and long-term sustainability strategies empower investors to make judicious decisions that are harmonious with the Triple Bottom Line (3Ps) concept, which includes People, Planet, and Profit (Elkington, Citation1998). Incorporating non-financial metrics, such as environmental, social, and governance (ESG) factors, presents challenges and opportunities for accounting professionals to provide a holistic perspective on organizational performance. Accounting can support adaptation to climate change through the following actions: (i) assessment of vulnerability and adaptive capacity, (ii) estimation of the costs and benefits of adaptation, and (iii) disclosure of risks related to climate change impact (Linnenluecke et al., Citation2015). Unfortunately, the absence of regulations and a corporate culture with minimal social responsibility contributes to a notably low level of climate change disclosure (Nurunnabi, Citation2016), and some companies conduct disclosures at their own pace and use their own methods (Smith et al., Citation2008). Consequently, climate change and accounting need to be separated.

3. Methods

This study uses bibliometric analysis as a foundational method to enhance our understanding of climate change and accounting literature. The research questions were addressed by following the four distinct phases outlined within the PRISMA protocol (Figure ). These stages include identification, screening, eligibility, and inclusion (Hansen et al., Citation2022; Kuckertz & Block, Citation2021; Lim et al., Citation2022; Rojas Molina et al., Citation2022).

Figure 1. Research Protocol.

The identification stage considers several critical factors, including source type, search engine, categories, language, period, and keywords (Tautiva et al., Citation2022). This research exclusively targets journal articles, excluding other publication types, such as books, book chapters, and conference proceedings (Harsanto & Firmansyah, Citation2023), considering their limited contribution to the empirical and theoretical discussions. Regarding the search engine, this analysis solely relies on the Scopus database, a globally renowned repository featuring high-quality articles from prominent publishers (Alves & Mariano, Citation2018; Dangelico, Citation2016; Ochoa et al., Citation2019). The key distinction between Scopus and WoS lies in the fact that the former grants access to its entire content through a sole subscription without any modulations and provides overall coverage that WoS (Pranckutė, Citation2021) does not. This makes it easier to replicate the results of future studies. Within the spectrum of search categories, this study focuses on the Business, Management and Accounting, Economics, Econometrics, and Finance domains. To avoid language bias, the search language is exclusively English (Alatawi et al., Citation2023; Gulluscio et al., Citation2020; Stechemesser & Guenther, Citation2012). These are set to ensure a comprehensive and high-quality review (Ibrahim et al., Citation2022) and non-English research was separately reviewed by authors with appropriate language skills (Nguyen et al., Citation2020). The search timeframe covered the past decade, from 2013 to 2023. The authors used 2013 as the starting year for the analysis because several key events occurred in this year such as the introduction of the Task Force on Climate-related Financial Disclosures (TCFD) in 2013, The IPCC’s Fifth Assessment Report (AR5), and the UN Climate Change Conference (COP 19), which significantly declared the role of accounting in the context of climate change. Finally, the keywords used included the following: “Climate Change,” or “Environmental Management Accounting,” or “Carbon Performance,” or “Pollution Control,” or “Greenhouse Gas,” or “Gas Emission,” or “Carbon Management,” or “Carbon Emission,” or “Climate Change Disclosure,” and Accounting”.

In the initial identification stage 13,607 documents were identified based on keyword searches. Subsequently, a screening process was performed using specific identification criteria. Based on the data, we conducted a screening process that included the following aspects: year (N = 3,089 excluded), subject area (N = 9,039 excluded), language (n = 19), and source type (n = 190 excluded). This process culminated in a final count of 1,202 documents during the screening stage. The feasibility stage involved a meticulous review of keywords and titles to ensure that the selected articles were relevant to the research topic, which focused on climate change and accounting. This stage also included error checking of the data to ensure that they could be used for bibliometric analysis (N = 13 excluded). The inclusion stage was the final step, consisting of validation examinations, analysis of publication statistics, and bibliometric analysis based on 1.189 selected pieces of data. The validation process was independently conducted to ascertain the robustness and validity of the preceding stages. A preliminary statistical analysis was performed to extract various pertinent pieces of information. Finally, a comprehensive bibliometric analysis was performed using VOSviewer as the primary tool and R as the secondary tool (for visualization purposes) (Aria & Cuccurullo, Citation2017).

This study employs two bibliometric methods, namely, co-occurrence and co-authorship. The underlying assumption is that the frequent co-occurrence of words indicates a close relationship among the selected words (Zupic & Čater, Citation2015). Co-occurrence analysis is the method that focuses on instances in which two or more keywords appear together in documents or articles. This analysis identifies the relationships between keywords within the literature, helping to visualize conceptual connections through bibliometric networks (Callon et al., Citation1983). The co-occurrence analysis leads to conclusions regarding the development of climate change research and accounting. The second method, co-authorship analysis, explores collaborations between two or more authors in article writing. Authors who collaborated in the research and co-wrote articles were considered co-authors. This analysis reveals patterns of collaboration among authors, offering insights into collaborative networks involving individuals and institutions within academia. The co-authorship analysis leads to conclusions about the drivers of progress in climate change and accounting research. This complements the method used to answer the research questions.

4. Results and discussion

4.1. General characteristics of the literature

4.1.1. Evolution in the number of publications

As shown in Figure , there is a discernible increasing trend in the number of publications, with an average of 108 documents published annually. A significant surge occurred in 2015, which showed an increase of 60% in documents (n = 25); in 2017, there was an increase of 43% in documents (n = 30) and in 2022, there was an increase of 32% in documents (n = 44). The Sustainability Accounting Standard Board (SASB), founded in 2011, provides an accounting standard for identifying, managing, and reporting sustainability factors useful to investors. Later, the TCFD was founded in 2015 and operationalized in 2013, focusing on climate-related financial disclosures. This coincided with the period following the adoption of the Paris Agreement in December 2015, which marked a pivotal moment for the transparency and reporting of climate change initiatives. Therefore, publications on climate change and accounting have significantly and consistently increased since 2015. After the event, a significant increase occurred in 2017 (n = 30), but not in 2016 (n = 3). This assumption is based on the premise that an increased focus on climate change reporting and transparency by organizations took place in 2016, serving as the primary source for this research. This can also be explained by the increased publication activity in journals like the Journal of Cleaner Production (n = 15 in 2015 and n = 8 in 2017). The Accounting Auditing and Accountability Journal and Journal of Environmental Accounting and Management published articles on climate change and accounting, marking a return after not publishing in 2014. This included the Resources Conservation and Recycling Journal, which was first published in 2015 (n = 3). Subsequently, we observe that the publication trend in 2018–2020 experienced a fluctuating increase, and in 2022, there was a 32% increase in the number of documents (n = 44). This surge was consistent with the Sustainable Development Goals Report of 2022, which highlighted climate change as the most significant global risk faced by the world’s population (United Nations, Citation2022). This prompted a response from various stakeholders, including the academic community. Finally, we conclude the SASB, TCFD, Paris Agreement, and SDGs Agenda as key events influencing the increase in the number of publications.

Figure 2. Evolution in the number of articles production.

4.1.2. Distribution Across Global Regions and organizations

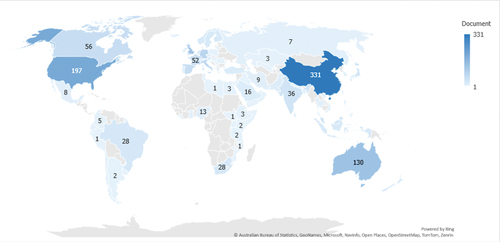

Over the past decade, China emerged as a leading country in terms of publications, boasting a total of 331 documents (Figure ), followed by the United States with 197 documents, Australia with 130 documents and the United Kingdom with 125 documents. Figure offers insight into the distribution of publications worldwide, shedding light on their contributions to the literature on climate change and accounting. A total of 92 countries contributed to the climate change and accounting literature, with the number of publications ranging from one to 331 documents. Among the top 15 countries with the highest publication rates, Asia stood out with the most significant density of 441 documents, closely trailed by Europe with 423 documents, then North America (n = 253), Australia (n = 130), South America (N = 28), and Southern Africa (N = 28). The main contributors in each region are the United Kingdom (Europe), the United Stated (North America), China (Asia), Australia (Australia and Oceania), Brazil (South America) and South Africa (Southern Africa).

Figure 3. Top 15 contributing countries.

Figure 4. Global distribution of publication density.

The high number of publications in several countries is also supported by the existence of regulations requiring climate change reporting. First, China enacted the National Development and Reform Commission (NDRC) Regulation 2014. Second, the United States introduced the EPA Mandatory Reporting of Greenhouse Gases Rule in 2019 under the Clean Air Act of 1970. Third, Australia introduced the National Greenhouse and Energy Reporting (NGER) scheme. Fourth, the United Kingdom launched the Companies Act (Strategic Reporting and Directors’ Report) 2013 regulation. Fifth, Germany introduced the Reform Act on Accounting Regulations 2014 (BillReg), which is to be amended by Directive 2014/95/EU.

Regarding the number of publications, the Chinese Academy of Sciences (China), Beijing Normal University (China), and Ministry of Education of the People’s Republic of China (China) have made substantial contributions to research on climate change and accounting over the past decade, each producing 43, 34, and 31 articles, respectively (as shown in Table ). Tsinghua University (China) contributed 30 publications, and the University of Chinese Academy of Sciences (China) contributed 20 publications. Organizations in China have contributed the most publications, followed by Australia, France, and the United States. Table also shows that, in China and Australia, there are organizations (universities) with a higher interest in climate change and accounting research than in other countries. This also highlights the fact that universities are the centers of climate change and accounting studies.

Table 1. Top 15 organizations contributing to research on climate change and accounting

The presence of numerous universities in China has resulted in climate change, and accounting research receiving significant funding support in the country. As shown in Table , eight organizations (research funding programs) came from China, with a total of 362 publications, followed by Europe and the United Kingdom, with 36 publications and 22 documents, respectively. The National Natural Science Foundation of China published 194 documents, or 16.32% of the total data used in this research. However, the Economic and Social Research Council, which is the largest funder of the studies of economics, social sciences, and human behavior in the United Kingdom, contributed only 11 papers to climate change and accounting literature.

Table 2. Top 15 organizations (funding sponsor) contributing to research on climate change and accounting

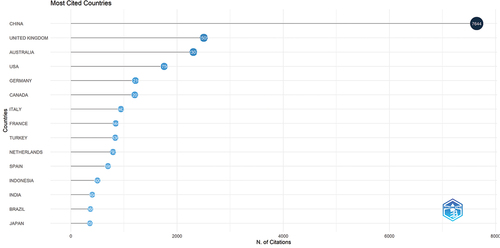

Figure shows the 15 countries with the highest number of citations. China had the highest number of citations (7,644), followed by the United Kingdom (2,505) and Australia (2,307). This indicates that articles from these countries are a major source of research on climate change and accounting research. This is consistent with the high production of documents, abundance of sponsorship funding, and mandatory regulations related to climate change and accounting in these countries. It is possible that the level of production, funding sponsors, and domestic regulations indicate the quality of the articles; therefore, it is often used as a reference for other research. Authors who have published many articles on a particular theme have a better understanding of the research field.

Figure 5. Top 15 most cited countries.

4.1.3. Journal analysis

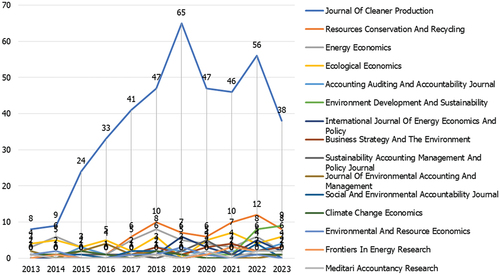

Figure provides a visual representation of the 15 journals that exhibited the highest publication on climate change and accounting between 2013 and 2023. The Journal of Cleaner Production topped the list, boasting the highest number of publications with 414 documents over the past decade. Following closely were Resource Conservation and Recycling and Ecological Economics, each contributing significantly with 63 and 47 documents, respectively. Additionally, economic and accounting journals, such as Energy Economics and Accounting Auditing and Accountability Journal, made substantial contributions, producing 46 and 21 documents, respectively.

Figure presents a visual representation of the annual number of publications from the top 15 journals in the field of climate change and accounting over the past decade. Among the selected journals, the Journal of Cleaner Production stood out as the only journal that consistently increased its publication count yearly in 2013–2019; this trend followed a decline in 2020 and 2021 and had a resurge in 2022. In 2019, this journal reached its peak by publishing the most articles on climate change and accounting in the last 10 years (n = 65). Several journals exhibited significant fluctuations in their research on climate change and accounting. For instance, Ecological Economics did not publish any articles on this topic in 2019. While reaching its peak in publications in 2019 with seven documents, the journal decreased to four articles in subsequent years. Resources Conservation and Recycling made its debut in publishing articles on climate change and accounting in 2015, with a substantial number of three documents. This number subsequently declined to one document in 2016 but reached its peak in 2022 with 12 documents. Environment Development and Sustainability first published one article on climate change and accounting in 2018 document; this year, it published only nine documents. From Figure , it can be concluded that there were annual publication fluctuations in each journal. Some new journals published related articles in the middle of the decade while the Journal of Cleaner Production and Energy Economics consistently published articles on climate change and accounting. Some journals experienced a collective decline in publication in 2020–2021. This coincides with the COVID-19 pandemic, when most universities (as organizations with the most publications) conducted distance learning, possibly affecting the level of research focus on climate change.

Figure 6. Top 14 journals by production.

Figure 7. Top 14 journals by annual production.

4.2. Network analysis of Co-occurrences

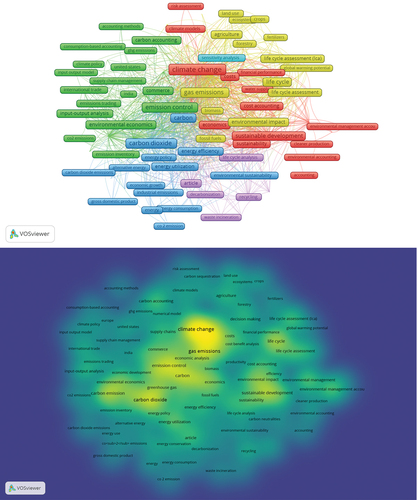

Figure presents a graphical depiction of the co-occurrence network obtained through bibliometric analysis using VOSviewer. This bibliometric network consists of nodes and edges (Van Eck & Waltman, Citation2014). Circular nodes denote keyword occurrences, with larger nodes indicating more extensive research on these keywords (Donthu et al., Citation2021). Edges, which connect lines between nodes, represent relationships and their strength within the research, with thicker edges signifying stronger or more frequent associations between nodes (Donthu et al., Citation2021). Furthermore, the proximity of nodes signifies the strength of the relationship between them.

Figure 8. Graphical representation of the co-occurrence network.

Figure highlights contributions from several fields and accounting related to climate change issues. These include environmental management accounting, emission inventory, cost accounting, management accounting, social accounting, sustainability accounting, carbon accounting, greenhouse gas accounting, consumption-based accounting, environmental accounting, accounting methods, and carbon management accounting. Additionally, the presence of keywords such as “carbon tax” and “carbon disclosure” underscore their significance in the accounting and taxation context, particularly in the efforts to address climate change issues. These keywords offer profound insights into the role and contribution of accounting in mitigating climate change and indicate the evolution of accounting into various new disciplines in response to the evolving needs and challenges of the business world.

Table illustrates the frequently associated keywords in research related to climate change and accounting. The Cluster column highlights the interconnectedness of variables within each cluster, although this does not exclude the possibility of keywords being connected to other clusters. The Link column indicates the frequency of keywords linked to others, whereas the Total Link Strength column shows the strength of the connections. A higher total link strength indicates a stronger network of keyword connections. Additionally, the Average Publishing Year (Avg. Pub. Year) indicates the period in which a keyword appeared in publications.

Table 3. Top 15 most frequently used keywords

Table presents the top 15 most frequently used keywords in climate change and accounting research, considering 121 keywords and six clusters represented by various colors. The term “Climate Change” emerged as the most prominent keyword, appearing 305 times, with a total link strength of 1,423. This signifies an extensive discourse on this topic, coupled with strong connections to other keywords. “Greenhouse Gases” and “Carbon Dioxide” followed with 265 and 193 occurrences, respectively. Considering the accounting-related terms, “Environmental Management Accounting” stood as the sole representative among the top 20 most frequently used keywords with 73 occurrences and the average publications year 2018.4247 (not included in Table ). Table shows the publication trends for this term between 2018 and 2019. The keyword “Climate Change” gained prominence with an average publication year of 2019.3541.

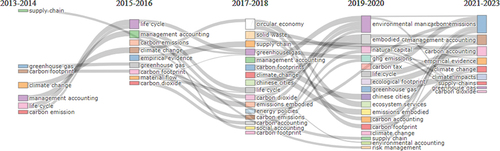

Accordingly, it can be concluded that the research trend for climate change and accounting peaked between 2018–2019. Climate change became a trending search keyword in 2019, coinciding with the IPCC’s Special Report on Global Warming of 1.5 °C, which has attracted the attention of various parties and supported by 41 authors from 40 countries. Figure reinforces this argument, showing that in the last decade, climate change and management accounting have become keywords that have been popping up yearly. Since 2013, research on accounting related to climate change has been growing. In 2017–2018, the term “carbon accounting” emerged, and in 2019–2020, followed by the terms “carbon tax” and “environmental management accounting.” This shows that the accounting discipline has evolved along the lines of climate change.

Figure 9. Thematic evolution by titles.

4.3. Network analysis of co-authorship

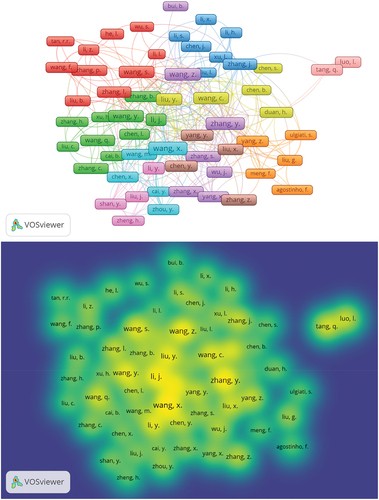

Transitioning to co-authorship analysis, Table introduces the 15 most productive authors in climate change and accounting literature. Wang, x., Zhang, y., and Wang, z. claimed the top positions with the highest number of Scopus publications, contributing 20, 19, and 17 documents, respectively. Wang, x. and Zhang, y. shared an average publication year of 2019 and Wang, z. has average publication year of 2020. Additionally, when examining the Total Link Strength, Wang, x., Zhang, y., and Li, j. exhibited the strongest network connections, underscoring their robust collaboration with other authors. Collaborative research efforts involving multiple authors can enrich climate change and accounting research by leveraging diverse experiences and expertise. Figure shows the authors’ network in this field.

Table 4. Top 15 highly productive authors

Figure visually represents 10 distinct clusters within the author network, denoted by the colors purple, yellow, red, green, blue, brown, orange, light purple, pink and light blue. These clusters indicate the grouping of authors based on specific research areas or focal points in climate change and accounting. Figure also conveys essential information regarding network density. Network density represents the degree to which the nodes within a network are interconnected through edges, thereby shedding light on the level of integration within the network. A higher network density indicates a greater number of connections linking certain nodes, which is indicative of a heightened level of interaction and relationships among the authors within the network. Wang and Zhang exhibited a significantly higher network density than their peers.

Figure 10. Graphical representation of the author’s network.

5. Conclusions

Overall, this study highlights the growing scholarly interest in the intersection of climate change and accounting to address the following questions: How has research on climate change and accounting evolved, and how could it advance further? The trajectory of investigations on this topic has displayed consistent expansion since 2013, despite a slight decrease in 2021, reaching its peak in 2022 with 183 publications. This significant increase can be attributed to several factors. First, a burgeoning number of journals accepted publications on climate change and accounting, including the inaugural contributions from Resources Conservation and Recycling and the International Journal of Energy Economics and Policy, each of which began to publish articles on this topic in 2015 and 2017. Second, the active involvement of publishing countries such as China, the United States, and Australia played a pivotal role. Several organizations, including the Chinese Academy of Sciences, Beijing Normal University, and Ministry of Education of the People’s Republic of China have made significant contributions to climate change and accounting research. Support from funding organizations, such as the National Natural Science Foundation of China (n = 194 documents), National Key Research and Development Program of China (n = 51 documents), and Fundamental Research Funds for Central Universities (n = 28 documents), has further catalyzed this growth. Finally, the momentum in climate change and accounting research has been fortified by the prolific efforts of authors such as Wang, x., Zhang, y., dan Wang, z., who have actively collaborated and published on this topic. Although the analysis shows an upward trend over the last decade, studies on climate change and accounting face major challenges, such as data availability. In some countries, for example, the G20 countries, there exists high population and trade. Although they have a vision for climate change mitigation, some countries do not require reporting on climate change, such as Argentina, Indonesia, India, Russia, and Saudi Arabia. This poses a challenge regarding data availability. However, it offers the potential for further research on the determinants of climate change disclosure (voluntary disclosure).

This study highlights the rapid advancement of climate change and accounting literature, mirroring the growing urgency and concerns surrounding climate change issues. Previous investigations have enriched the literature across various disciplines, including environmental management accounting, emission inventory, cost accounting, management, social, sustainability, carbon, and environmental accounting. This research has played a pivotal role and significantly contributed to climate change mitigation. Additionally, the emergence of topics such as carbon taxes and carbon disclosures has signified its growing importance over the past decade. Although the keyword does not fall among the top 15 most frequently used keywords, it provides both quantitatively and qualitatively opportunities for future research. Furthermore, there are several key events that have enhanced the relevance of climate change studies and accounting. They are as follows: SASB, TCFD, Paris Agreement, SDGs Agenda, Mandatory Climate Change Reporting Regulations, and several reports such as Special Report on Global Warming of 1.5 °C in 2018, which has succeeded in attracting the attention of various academics.

It is important to acknowledge the limitations of this study. First, the analysis exclusively focused on articles published in English-language journals, excluding papers published in languages like Spanish, German, French, Russian, Ukraine, or Chinese. Combining articles from different languages can introduce bias and errors in the bibliometric analysis process. Therefore, further research could separately analyze non-English literature to complement the literature on climate change and accounting. Second, specific document types including books, book chapters, letters, and conference proceedings were not included in the research. Additionally, the bibliometric analysis was confined to the Scopus database because of its established quality and support from previous reviews. Future investigations could explore other databases involving the WOS to expand their scope. Third, bibliometric analysis only analyzes bibliometric datasets (e.g., keywords, titles, abstracts, citations, and affiliations). Further research can perform systematic literature reviews to gather information, such as the methods used, theories used, and mapping causality effects that are not available in bibliometric analysis. Finally, this research exclusively employed VOSviewer as an analytical tool, leveraging its strengths in co-occurrence and co-authorship analyses to obtain information on the development of a topic and its drivers. Future reviews should consider integrating VOSviewer and R analyses to provide a more comprehensive graphical representation.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abbass, K., Qasim, M. Z., Song, H., Murshed, M., Mahmood, H., & Younis, I. (2022). A review of the global climate change impacts, adaptation, and sustainable mitigation measures. Environmental Science and Pollution Research, 29(28), 42539–19. https://doi.org/10.1007/s11356-022-19718-6

- Abhilash, A., Shenoy, S. S., & Shetty, D. K. (2023). Overview of corporate governance research in India: A bibliometric analysis. Cogent Business & Management, 10(1). https://doi.org/10.1080/23311975.2023.2182361

- Ahmad, G., Subhan, M., Hayat, F., & Al-Faryan, M. A. S. (2023). Unravelling the truth: A bibliometric analysis of earnings management practices. Cogent Business & Management, 10(1). https://doi.org/10.1080/23311975.2023.2194088

- Alatawi, I. A., Ntim, C. G., Zras, A., & Elmagrhi, M. H. (2023). CSR, financial and non-financial performance in the tourism sector: A systematic literature review and future research agenda. International Review of Financial Analysis, 89(July), 102734. https://doi.org/10.1016/j.irfa.2023.102734

- Ali, I., Arslan, A., Tarba, S., & Mainela, T. (2023). Supply chain resilience to climate change inflicted extreme events in agri-food industry: The role of social capital and network complexity. International Journal of Production Economics, 264(July), 108968. https://doi.org/10.1016/j.ijpe.2023.108968

- Alves, M. W. F. M., & Mariano, E. B. (2018). Climate justice and human development: A systematic literature review. Journal of Cleaner Production, 202, 360–375. https://doi.org/10.1016/j.jclepro.2018.08.091

- Antwi, I. F., Carvalho, C., & Carmo, C. (2022). Corporate governance research in Ghana through bibliometric method: Review of existing literature. Cogent Business & Management, 9(1). https://doi.org/10.1080/23311975.2022.2088457

- Aria, M., & Cuccurullo, C. (2017). Bibliometrix: An R-tool for comprehensive science mapping analysis. Journal of Informetrics, 11(4), 959–975. https://doi.org/10.1016/j.joi.2017.08.007

- Auffhammer, M. (2018). Quantifying economic damages from climate change. Journal of Economic Perspectives, 32(4), 33–52. https://doi.org/10.1257/jep.32.4.33

- Benavent, R. A., Tudo, J. L. A., Cogollos, L. C., & Aleixandre, J. L. (2017). Trends in scientific research on climate change in agriculture and forestry subject areas (2005–2014). Journal of Cleaner Production, 147, 406–418. https://doi.org/10.1016/j.jclepro.2017.01.112

- Bocken, N., Boons, F., & Baldassarre, B. (2019). Sustainable business model experimentation by understanding ecologies of business models. Journal of Cleaner Production, 208, 1498–1512. https://doi.org/10.1016/j.jclepro.2018.10.159

- Callon, M., Courtial, J.-P., Turner, W. A., & Bauin, S. (1983). Colloquium on the sociological analysis of scientific and technical research. Social Science Information, 22(2), 191–235. https://doi.org/10.1177/053901883022002003

- Cantele, S., Tsalis, T. A., & Nikolaou, I. E. (2018). A new framework for assessing the sustainability reporting disclosure of water utilities. Sustainability, 10(2), 1–12. https://doi.org/10.3390/su10020433

- Cavicchioli, R., Ripple, W. J., Timmis, K. N., Azam, F., Bakken, L. R., Baylis, M., Behrenfeld, M. J., Boetius, A., Boyd, P. W., Classen, A. T., Crowther, T. W., Danovaro, R., Foreman, C. M., Huisman, J., Hutchins, D. A., Jansson, J. K., Karl, D. M., Koskella, B., Mark Welch, D. B., & Webster, N. S. (2019). Scientists’ warning to humanity: Microorganisms and climate change. Nature Reviews Microbiology, 17(9), 569–586. https://doi.org/10.1038/s41579-019-0222-5

- Dangelico, R. M. (2016). Green product innovation: Where we are and where we are going. Business Strategy and the Environment, 25(8), 560–576. https://doi.org/10.1002/bse.1886

- Donthu, N., Kumar, S., Mukherjee, D., Pandey, N., & Lim, W. M. (2021). How to conduct a bibliometric analysis: An overview and guidelines. Journal of Business Research, 133(May), 285–296. https://doi.org/10.1016/j.jbusres.2021.04.070

- Du, H., Li, B., Brown, M. A., Mao, G., Rameezdeen, R., & Chen, H. (2015). Expanding and shifting trends in carbon market research: A quantitative bibliometric study. Journal of Cleaner Production, 103(September 2012), 104–111. https://doi.org/10.1016/j.jclepro.2014.05.094

- Ebaid, I. E. S. (2022). Does the implementation of IFRS improve transparency regarding the company’s financial conditions?: Evidence from an emerging market. PSU Research Review. https://doi.org/10.1108/PRR-11-2021-0063

- Elkington, J. (1998). Partnerships from cannibals with forks: The triple bottom line of 21st-century business. Environmental Quality Management, 8(1), 37–51. https://doi.org/10.1002/tqem.3310080106

- Estevao, J. (2021). Toward the Paris Agreement implementation impact on electricity sector: The emerging reality. International Journal of Energy Economics & Policy, 11(1), 1–8. https://doi.org/10.32479/ijeep.10276

- Feliciano, D., Recha, J., Ambaw, G., MacSween, K., Solomon, D., & Wollenberg, E. (2022). Assessment of agricultural emissions, climate change mitigation and adaptation practices in Ethiopia. Climate Policy, 22(4), 427–444. https://doi.org/10.1080/14693062.2022.2028597

- Fernando, A. G., Sivakumaran, B., & Suganthi, L. (2014). Nature of green advertisements in India: Are they greenwashed? Asian Journal of Communication, 24(3), 222–241. https://doi.org/10.1080/01292986.2014.885537

- Filho, W. L., Azeiteiro, U. M., Balogun, A. L., Setti, A. F. F., Mucova, S. A. R., Ayal, D., Totin, E., Lydia, A. M., Kalaba, F. K., & Oguge, N. O. (2021). The influence of ecosystems services depletion to climate change adaptation efforts in Africa. Science of the Total Environment, 779, 779. https://doi.org/10.1016/j.scitotenv.2021.146414

- Galeone, G., Onorato, G., Shini, M., & Dell’atti, V. (2023). Climate-related financial disclosure in integrated reporting: What is the impact on the business model? The case of Poste Italiane. Accounting Research Journal, 36(1), 21–36. https://doi.org/10.1108/ARJ-04-2022-0107

- Gardner, T. A., Benzie, M., Börner, J., Dawkins, E., Fick, S., Garrett, R., Godar, J., Grimard, A., Lake, S., Larsen, R. K., Mardas, N., McDermott, C. L., Meyfroidt, P., Osbeck, M., Persson, M., Sembres, T., Suavet, C., Strassburg, B., Trevisan, A. … Wolvekamp, P. (2019). Transparency and sustainability in global commodity supply chains. World Development, 121, 163–177. https://doi.org/10.1016/j.worlddev.2018.05.025

- Geissdoerfer, M., Vladimirova, D., & Evans, S. (2018). Sustainable business model innovation: A review. Journal of Cleaner Production, 198, 401–416. https://doi.org/10.1016/j.jclepro.2018.06.240

- Giannarakis, G., Zafeiriou, E., Arabatzis, G., & Partalidou, X. (2018). Determinants of corporate climate change disclosure for European firms. Corporate Social Responsibility and Environmental Management, 25(3), 281–294. https://doi.org/10.1002/csr.1461

- Gulluscio, C., Puntillo, P., Luciani, V., & Huisingh, D. (2020). Climate change reporting: A systematic literature review. Sustainability, 12(13), 60–88. https://doi.org/10.3390/su12135455

- Haites, E. (2018). Carbon taxes and greenhouse gas emissions trading systems: What have we learned? Climate Policy, 18(8), 955–966. https://doi.org/10.1080/14693062.2018.1492897

- Hansen, C., Steinmetz, H., & Block, J. (2022). How to conduct a meta-analysis in eight steps: A practical guide. Management Review Quarterly, 72(1), 1–19. https://doi.org/10.1007/s11301-021-00247-4

- Harsanto, B., & Firmansyah, E. A. (2023). A twenty years bibliometric analysis (2002–2021) of business economics research in ASEAN. Cogent Business & Management, 10(1). https://doi.org/10.1080/23311975.2023.2194467

- Hasegawa, T., Sakurai, G., Fujimori, S., Takahashi, K., Hijioka, Y., & Toshihiko, T. (2021). Extreme climate events increase risk of global food insecurity and adaptation needs. Nature Food, 2(8), 587–595. https://doi.org/10.1038/s43016-021-00335-4

- Hermundsdottir, F., & Aspelund, A. (2021). Sustainability innovations and firm competitiveness: A review. Journal of Cleaner Production, 280, 124715. https://doi.org/10.1016/j.jclepro.2020.124715

- Ibrahim, A. E. A., Hussainey, K., Nawaz, T., Ntim, C., & Elamer, A. (2022). A systematic literature review on risk disclosure research: State-of-the-art and future research agenda. International Review of Financial Analysis, 82(May), 102217. https://doi.org/10.1016/j.irfa.2022.102217

- Jorgensen, S., Mjos, A., & Pedersen, L. J. T. (2022). Sustainability reporting and approaches to materiality: Tensions and potential resolutions. Sustainability Accounting, Management and Policy Journal, 13(2), 341–361. https://doi.org/10.1108/SAMPJ-01-2021-0009

- Joshi, G., & Dash, R. (2023). A bibliometric analysis of climate investing. International Journal of Energy Economics & Policy, 13(3), 396–407. https://doi.org/10.32479/ijeep.14279

- Kuckertz, A., & Block, J. (2021). Reviewing systematic literature reviews: ten key questions and criteria for reviewers. Management Review Quarterly, 71(3), 519–524. https://doi.org/10.1007/s11301-021-00228-7

- Kundzewicz, Z. W., Krysanova, V., Benestad, R. E., Hov Piniewski, M., Otto, I. M., & Otto, I. M. (2018). Uncertainty in climate change impacts on water resources. Environmental Science & Policy, 79(October 2017), 1–8. https://doi.org/10.1016/j.envsci.2017.10.008

- Kuo, L., Chen, V. Y. J., Ferreira, J. M., Vila, J. E., & Anastasia Mariussen, J. (2013). Is environmental disclosure an effective strategy on establishment of environmental legitimacy for organization? Management Decision, 51(7), 1462–1487. https://doi.org/10.1108/MD-06-2012-0395

- Lim, W. M., Kumar, S., & Ali, F. (2022). Advancing knowledge through literature reviews: “What”, “why”, and “how to contribute. The Service Industries Journal, 42(7–8), 481–513. https://doi.org/10.1080/02642069.2022.2047941

- Linnenluecke, M. K., Birt, J., Griffiths, A., & Walsh, K. (2015). The role of accounting in supporting adaptation to climate change. Accounting and Finance, 55(3), 607–625. https://doi.org/10.1111/acfi.12120

- Malhi, G. S., Kaur, M., & Kaushik, P. (2021). Impact of climate change on agriculture and its mitigation strategies: A review. Sustainability, 13(3), 1–21. https://doi.org/10.3390/su13031318

- Muchiri, M. K., Erdei-Gally, S., Fekete-Farkas, M., & Lakner, Z. (2022). Bibliometric analysis of green Finance and climate change in post-Paris Agreement Era. Journal of Risk and Financial Management, 15(12), 561. 15(12. https://doi.org/10.3390/jrfm15120561

- Naciti, V., Cesaroni, F., & Pulejo, L. (2022). Corporate governance and sustainability: A review of the existing literature. Journal of Management & Governance, 26(1), 55–74. https://doi.org/10.1007/s10997-020-09554-6

- Nathalia, C., & Setiawan, D. (2022). Does board capital improve climate change disclosures? Cogent Business & Management, 9(1). https://doi.org/10.1080/23311975.2022.2121242

- Nekmahmud, M., Naz, F., Ramkissoon, H., & Fekete-Farkas, M. (2022). Transforming consumers’ intention to purchase green products: Role of social media. Technological Forecasting and Social Change, 185(March), 122067. https://doi.org/10.1016/j.techfore.2022.122067

- Nguyen, T. H. H., Ntim, C. G., & Malagila, J. K. (2020). Women on corporate boards and corporate financial and non-financial performance: A systematic literature review and future research agenda. International Review of Financial Analysis, 71(December 2019), 101554. https://doi.org/10.1016/j.irfa.2020.101554

- Ngwakwe, C. C. (2012). Rethinking the accounting stance on sustainable development. Sustainable Development, 20(1), 28–41. https://doi.org/10.1002/sd.462

- Nurunnabi, M. (2016). Who cares about climate change reporting in developing countries? The market response to, and corporate accountability for, climate change in Bangladesh. Environment Development and Sustainability, 18(1), 157–186. https://doi.org/10.1007/s10668-015-9632-3

- Ochoa, G. V., Alvarez, J. N., & Acevedo, C. (2019). Research evolution on renewable energies resources from 2007 to 2017: A comparative study on solar, geothermal, wind and biomass energy. International Journal of Energy Economics & Policy, 9(6), 242–253. https://doi.org/10.32479/ijeep.8051

- Pinchot, A., Zhou, L., Christianson, G., McClamrock, J., & Sato, I. (2021). Assessing physical risks from climate change: Do companies and financial organizations have sufficient guidance? World Resources Institute, February, 1–44. https://doi.org/10.46830/wriwp.19.00125

- Pranckutė, R. (2021). Web of science (wos) and Scopus: The titans of bibliographic information in today’s academic world. Publications, 9(1), 12. https://doi.org/10.3390/publications9010012

- Rashed, A. H., Rashdan, S. A., & Ali-Mohamed, A. Y. (2022). Towards effective environmental sustainability reporting in the large industrial sector of Bahrain. Sustainability, 14(1), 219. https://doi.org/10.3390/su14010219

- Rocha, J., Oliveira, S., Viana, C. M., & Ribeiro, A. I. (2022). Chapter 8 - climate change and its impacts on health, environment and economy. In Prata, J. C., Ribeiro, A. I., & Rocha-Santos, T. (Eds.), One Health (pp. 253–279). Academic Press.

- Rojas Molina, L. K., Pérez López, J. Á., & Campos Lucena, M. S. (2022). Meta-analysis: Associated factors for the adoption and disclosure of CSR practices in the banking sector. Management Review Quarterly, 0123456789(3), 1017–1044. https://doi.org/10.1007/s11301-022-00267-8

- Rounaghi, M. M. (2019). Economic analysis of using green accounting and environmental accounting to identify environmental costs and sustainability indicators. International Journal of Ethics and Systems, 35(4), 504–512. https://doi.org/10.1108/IJOES-03-2019-0056

- Sam, A. S., Padmaja, S. S., Kächele, H., Kumar, R., & Müller, K. (2020). Climate change, drought and rural communities: Understanding people’s perceptions and adaptations in rural eastern India. International Journal of Disaster Risk Reduction, 44(December 2019), 101436. https://doi.org/10.1016/j.ijdrr.2019.101436

- Scott, D., & Gössling, S. (2022). A review of research into tourism and climate change - launching the annals of tourism research curated collection on tourism and climate change. Annals of Tourism Research, 95, 1–13. https://doi.org/10.1016/j.annals.2022.103409

- Simpson, N. P., Mach, K. J., Constable, A., Hess, J., Hogarth, R., Howden, M., Lawrence, J., Lempert, R. J., Muccione, V., Mackey, B., New, M. G., O’Neill, B., Otto, F., Pörtner, H. O., Reisinger, A., Roberts, D., Schmidt, D. N., Seneviratne, S., Strongin, S. … Trisos, C. H. (2021). A framework for complex climate change risk assessment. One Earth, 4(4), 489–501. https://doi.org/10.1016/j.oneear.2021.03.005

- Smith, J. A., Morreale, M., & Mariani, M. E. (2008). Climate change disclosure: Moving towards a brave new world. Capital Markets Law Journal, 3(4), 469–485. https://doi.org/10.1093/cmlj/kmn021

- Stechemesser, K., & Guenther, E. (2012). Carbon accounting: A systematic literature review. Journal of Cleaner Production, 36, 17–38. https://doi.org/10.1016/j.jclepro.2012.02.021

- Tautiva, J. A. D., Huaman, J., & Oliva, R. D. P. (2022). Trends in research on climate change and organizations: A bibliometric analysis (1999–2021). Management Review Quarterly, (123456789). https://doi.org/10.1007/s11301-022-00298-1

- Thomas, K., Hardy, R. D., Lazrus, H., Mendez, M., Orlove, B., Rivera-Collazo, I., Roberts, J. T., Rockman, M., Warner, B. P., & Winthrop, R. (2019). Explaining differential vulnerability to climate change: A social science review. Wiley Interdisciplinary Reviews: Climate Change, 10(2), 1–18. https://doi.org/10.1002/wcc.565

- Tuest, Y. N., Soler, C. C., & Feliu, V. R. (2022). Bibliometric and systemic analysis of the relationship between management and carbon. Cuadernos de Gestion, 22(1), 215–228. https://doi.org/10.5295/CDG.211442YN

- United Nations. (2022). The Sustainable Development Goals Report 2022. https://unstats.un.org/sdgs/report/2022/The-Sustainable-Development-Goals-Report-2022.pdf

- Van Eck, N. J., & Waltman, L. (2014). Visualizing bibliometric networks. Measuring Scholarly Impact. https://doi.org/10.1007/978-3-319-10377-8_13

- Venturelli, A., Caputo, F., Leopizzi, R., & Pizzi, S. (2019). The state of art of corporate social disclosure before the introduction of non-financial reporting directive: A cross country analysis. Social Responsibility Journal, 15(4), 409–423. https://doi.org/10.1108/SRJ-12-2017-0275

- Wang, Z., Zhao, Y., & Wang, B. (2018). A bibliometric analysis of climate change adaptation based on massive research literature data. Journal of Cleaner Production, 199, 1072–1082. https://doi.org/10.1016/j.jclepro.2018.06.183

- Wohlgezogen, F., McCabe, A., Osegowitsch, T., & Mol, J. (2020). The wicked problem of climate change and interdisciplinary research: Tracking management scholarship’s contribution. Journal of Management and Organization, 26(6), 1048–1072. https://doi.org/10.1017/jmo.2020.14

- Wright, L. A., Coello, J., Kemp, S., & Williams, I. (2011). Carbon footprinting for climate change management in cities. Carbon Management, 2(1), 49–60. https://doi.org/10.4155/cmt.10.41

- Xie, W., Xiong, W., Pan, J., Ali, T., Cui, Q., Guan, D., Meng, J., Mueller, N. D., Lin, E., & Davis, S. J. (2018). Decreases in global beer supply due to extreme drought and heat. Nature Plants, 4(11), 964–973. https://doi.org/10.1038/s41477-018-0263-1

- Xu, J., & Liu, S. (2023). Current status, evolutionary path, and development trends of low-carbon technology innovation: A bibliometric analysis. Environment Development and Sustainability, (123456789). https://doi.org/10.1007/s10668-023-03640-z

- Ye, B., Jiang, J., Liu, J., Zheng, Y., & Zhou, N. (2021). Research on quantitative assessment of climate change risk at an Urban scale: Review of recent progress and outlook of future direction. Renewable and Sustainable Energy Reviews, 135, 110415. https://doi.org/10.1016/j.rser.2020.110415

- Zupic, I., & Čater, T. (2015). Bibliometric methods in management and organization. Organizational Research Methods, 18(3), 429–472. https://doi.org/10.1177/1094428114562629