Abstract

This study explores the role of perceived customer value and loyalty relationships in mobile wallet (M-wallet). The study further investigates trust and satisfaction as drivers of loyalty and examines the role of trust in the traditional value-satisfaction-loyalty relationship. A total of 214 responses from M-wallet users were captured using a structured questionnaire in a cross-sectional survey design. The data collected was analyzed with the help of structural equation modeling. Trust and satisfaction in M-wallet are both found to be mediating the perceived customer value and loyalty relationship. Furthermore, results also confirm the sequential mediation impact of trust and satisfaction between the perceived customer value and loyalty relationship. The findings help practitioners in tailoring their customer relationship strategies to promote M-wallet loyalty. Finally, this study recommends that managers should emphasize leveraging trust and satisfaction to shape loyalty in addition to customer value. They should focus on initiatives to win trust, satisfy the customers, and enhance long-term customer relationships.

1. Introduction

The popularity and growth of real-time, account-to-account payments using mobile wallets (M-wallet) is increasing across the world. M-wallet transactions were 102.7 billion dollars in 2020, and by 2025, they are expected to reach 2,582.8 billion dollars, with the Asia-Pacific region topping the list with more than $58 billion in contributions (ACI, Citation2021). Increasing penetration of internet and smartphones has caused a rapid growth of e-commerce that has, in turn, driven the M-wallet markets. The COVID-19 pandemic of 2020 has further pushed the need for providing quick and inexpensive access to digital cash.

M-wallets are the digital equivalent of a physical wallet. Money can be preloaded into an M-wallet application through credit cards, debit cards, or net banking. Whenever a transaction is made, money gets transferred from the buyer’s M-wallet to the seller’s bank account or M-wallet. M-wallets can be used for consumer-to-consumer payments, consumer-to-business payments, and business-to-business payments (Shin, Citation2009). However, M-wallet service providers are increasingly facing the problem of retaining customers. The two-pronged challenge they face is not only becoming the M-wallet of choice for users but also promoting loyalty in the long run. Further, these M-wallet service providers are aware that the cost of attracting new customers exceeds the cost of retaining the existing customers (Garrouch, Citation2021; GS & Arivazhagan, Citation2021; To et al., Citation2021; Too et al., Citation2001), and customer loyalty leads to profitability in the long run. While the extant literature has examined consumers’ perception, attitudes, and adoption intention of M-wallets (Al-Hattami et al., Citation2023; Amoroso & Magnier-Watanabe, Citation2012; Gupta, Citation2022; Shaw & Kesharwani, Citation2019; Shin, Citation2009), studies exploring the factors that propel consumer loyalty towards a particular M-wallet service provider is scant (Amoroso & Ackaradejruangsri, Citation2018, Citation2018; Gong et al., Citation2020; Joshi & Chawla, Citation2023).

Past studies on M-wallet loyalty have primarily examined consumers’ usage perspective; specifically, factors such as consumer self-efficacy, inertia, habit, perceived usefulness, innovativeness, privacy and security, and relative convenience and advantages (Amoroso & Ackaradejruangsri, Citation2018; Daragmeh et al., Citation2021; Gong et al., Citation2021; Grover, Citation2020; Ly et al., Citation2022; Mombeuil & Uhde, Citation2021; Putri et al., Citation2022). However, perceived value (PV), an important variable, has been left out and needs to be studied in this context (Kaur et al., Citation2020). Customers feel attached to a firm because they perceive the value obtained from that firm is higher than that available from other firms (Anderson & Srinivasan, Citation2003; Senić & Marinković, Citation2014). Therefore, PV has emerged as the prime concern in all marketing activities (Holbrook, Citation1999). Further, it is positively related to loyalty and profitability (Salem Khalifa, Citation2004). Moreover, Kaur et al. (Citation2020) have recognized the need to discover the impact of PV in the post-adoption stages, especially customer loyalty towards M-wallets.

Based on the theory of investment model of commitment (TIMC) and Relational Mediator Meta-Analytic Framework (RMMA), PV can be stretched with trust, satisfaction, and loyalty (Palmatier et al., Citation2006; Rusbult et al., Citation2012). McKnight et al. (Citation1998) argued that trust is a very crucial factor impacting consumer behavior in a financial transaction. Trust acts as a crucial intervening variable in the association between the customer’s relational benefits and their loyalty (Palmatier et al., Citation2006). Further, trust and satisfaction are crucial in the PV-loyalty relationship (Chen, Citation2012; Hamouda, Citation2019). Trust is one of the critical factors for online/digital money transactions (Amoroso & Magnier-Watanabe, Citation2012; Chiu et al., Citation2017) and lays the foundation for service providers to build a long-term relationship with the users as trust reduces uncertainty and vulnerability (Berry, Citation1995; Ndubisi, Citation2007).

On the other hand, relational satisfaction is the customer’s affective or emotional state toward a relationship, typically evaluated cumulatively over the history of exchanges (Rusbult et al., Citation2012). The relational satisfaction helps the service providers to extend the relationship, win the trust of the customer, and attain customer satisfaction (Bügel et al., Citation2010; Givertz & Segrin, Citation2005). Satisfied customers may retain or strengthen their connection with the service provider as well as recommend the service provider to other potential consumers (Kumar et al., Citation2013). Satisfaction is an important consequence and a key indicator of customer patronage and desire for future purchases (Chen, Citation2012; Mittal & Kamakura, Citation2001). Likewise, service management literature claims that PV is one of the major predictors of customer satisfaction (e.g., Blanchard & Galloway, Citation1994) and the latter impacts loyalty behaviors (Anderson & Fornell, Citation1994).

However, the association between satisfaction and loyalty is found to be context-dependent (Anderson & Srinivasan, Citation2003) and this association is not explored in the context of M-wallet. Thus, it is important to investigate the role of trust and satisfaction in the PV-loyalty relationship in the context of M-wallet. To address this gap, this study seeks first to establish the relationship between perceived value and loyalty towards M-wallets. It then asks an important question: How do trust and satisfaction influence the perceived value and loyalty relationship of M-wallets in the emerging market context?

The combination of emerging economies and M-wallets will expand the body of knowledge even further. For example, an emerging economy like India is expected to become the biggest market for M-wallet, and its digital payment volume is expected to surpass 52 billion payments by 2024 (ACI, Citation2021). The various government initiatives like Digital India along with the demonetization in 2016 have given a boost to M-wallet adoption and usage (Sharma & Kulshreshtha, Citation2019). In 2019, India witnessed a 163% growth in mobile-based payments crossing $287 billion (S&P Global Market Intelligence, 2020). With an increasing number of consumers adopting M-wallets, a large number of service providers are joining the market, creating many options for the consumer to choose from. Thus, retaining customers and building loyalty is essential to outweigh the growing competition in the M-wallet service providers’ market.

The present study extends the line of research by identifying the role of trust and satisfaction as mediators in the PV-loyalty relation in the context of M-wallet. The study contributes to the M-wallet literature by exploring the role of trust and satisfaction as serial mediators in the PV-loyalty relationship, thus, helping the M-wallet service providers to retain customers and increase their profitability. The present study is expected to augment academicians’ and service providers’ understanding of M-wallet loyalty in an emerging economy by clearly identifying the underlying mechanism that promotes loyalty. This will help practitioners in tailoring better customer relationship management strategies to promote M-wallet loyalty. This study is dissimilar from previous research on modeling customer loyalty in M-wallet. It posits PV as a predecessor of the trust-satisfaction-loyalty association along with exploring the serial-mediation effect. Moreover, the study applies the (TIMC) and (RMMA) frameworks as theoretical foundations to model of PV-loyalty relationship of M-wallet users.

The rest of the paper is structured as follows. The next section is a literature review from which hypotheses are derived and a model, which focuses on the factors associated with customer loyalty towards M-wallets, is developed. Section three elaborates on the sample, data analysis, results, and findings. Section four presents an account of the theoretical and practical implications of the study, and the limitations and gives directions for future research.

2. Review of literature

The construct PV is much explored in the marketing literature (e.g., Abu ELSamen, Citation2015; Lapierre, Citation2000; Sánchez-Fernández & Iniesta-Bonillo, Citation2007). Sánchez-Fernández and Iniesta-Bonillo (Citation2007) summarized PV as a subject-object relationship: that value is comparative due to its relative, situational, and personal character and it is perceptual, preferential, and cognitive-affective. It has been proven that PV is strongly linked to customer loyalty and profitability (Khalifa, 2004). Therefore, the relationship between PV and loyalty has attracted the attention of scholars across the world (El-Adly, Citation2019; Gounaris et al., Citation2007; Pura, Citation2005).

In the case of digital money and online commerce transactions such as M-banking, M-commerce, internet banking, to name a few, PV is found to be a crucial variable impacting loyalty (Chuah et al., Citation2014; Johan et al., Citation2022; Karjaluoto et al., Citation2019; Rahi et al., Citation2017), customer satisfaction and repurchase intention (Chopdar & Balakrishnan, Citation2020; Lee et al., Citation2007). Moreover, in the context of M-wallet, published studies that explore loyalty have predominantly explored users’ points of view. More specifically, factors such as consumer self-efficacy, inertia, attitudes, trust, habit, perceived usefulness, continued intention to use, privacy, and security have been explored (Amoroso & Ackaradejruangsri, Citation2018; Cao et al., Citation2018; Daragmeh et al., Citation2022; Mombeuil & Uhde, Citation2021; Thakur & Srivastava, Citation2014).

Amoroso and Ackaradejruangsri (Citation2018) argued that the predictive power of loyalty of an M-wallet is greatly increased when consumer attitudes and satisfaction are combined with habit. Amoroso and Ackaradejruangsri (Citation2018) explored the role of customer innovativeness, attitudes, and satisfaction on loyalty among M-wallet users. The authors reported that customer innovativeness acted as a mediator in forecasting loyalty. Daragmeh et al. (Citation2021) argued that the COVID-19 pandemic highly influenced the adoption and usage of digital payment services. In an emerging market scenario, Kaur et al. (Citation2020) investigated the relationship between several characteristics and intentions to use/recommend M-wallet. They concluded that relative advantage, complexity, observability, and compatibility were all strongly linked to M-wallet user’s intentions to recommend one. Mombeuil and Uhde (Citation2021) studied the continuous use intention of foreign users living in China. They concluded that relative advantages and convenience along with perceived security and privacy positively influence continuous use intention.

Table summarizes the studies of M-wallet highlighting the antecedents, consequences, mediators/moderators, location of study and research methodology. Most of the studies have used survey method for collecting data. Furthermore, from Table it is evident that the studies conducted are broadly in the domain of adoption, continued usage, and related factors of M-wallet and structural equation modeling (SEM) is the most preferred methodology. However, the intervening role of trust and satisfaction in the PV-loyalty relationship has not been explored. This paper is an attempt to fill this research gap.

Table 1. Review of literature on M-wallet

3. Theoretical background

The conceptual model used in this study is based on the theory of TIMC (Rusbult et al., Citation2012) and RMMA (Verma et al., Citation2016) frameworks. TIMC presents a rationale for the commitment that people show in a myriad of dyadic and organizational relationships, whereas RMMA provides support in explaining the mediating role of trust and satisfaction on loyalty.

The theory of TIMC argues that the level of satisfaction, perceived absence of alternatives, and investment size are antecedents of commitment (Rusbult, Citation1983; Rusbult et al., Citation2012). Theoretically, satisfaction grows in intensity as a person’s needs for friendship, belonging, and security needs are addressed. As a result, the theory recommends that satisfaction be included in a commitment model. Second, the theory of TIMC argues that commitment also depends on the perceived absence of alternatives. The availability and attractiveness of alternatives have an impact on the level of satisfaction, and ultimately on the commitment. If relationships continue despite the availability and attractiveness of the alternatives, there must be more to it than satisfaction that explains the level of commitment that individuals demonstrate. We argue while engaging with M-wallet services, trust helps to generate a sense of safety and dependability, which influences loyalty behavior. Therefore, we claim that trust helps in creating higher levels of customers’ satisfaction in their relationship with their M-wallet service provider. As a result, the theory offers a critical justification for the integration of trust as a precursor of customer satisfaction in a model of customer loyalty.

Lastly, the investment size can be increased by the parties in a relationship in various ways such as investing time and energy, building assets and social networks, and investing in the form of sharing valuable confidential information. We argue that the investment size will increase only if the individual parties perceive that the value extracted from the relationship is more than the investment made. In simple terms, the higher the perceived value, the more will be the investment size, thereby increasing the satisfaction and loyalty behavior. As a result, the theory of TIMC provides a critical theoretical justification for the integration of PV as a precursor of customer satisfaction in a model of customer loyalty.

The RMMA framework proposes trust and relationship satisfaction as mediators of perceived value and loyalty relationships (Palmatier et al., Citation2006). Therefore, RMMA also supports the model proposed in this study.

4. Hypothesis development

4.1. Perceived value and loyalty

PV is buyers’ overall assessment of the utility (Zeithaml, Citation1988) and is calculated as the proportion of a consumer’s perceived benefits and costs. Consumers’ perceived costs comprise monetary and nonmonetary (time, energy, stress, and so on) expenditures. Customers are more likely to feel fairly treated if they believe the rewards, they get from the service outweigh the costs associated with it. The assessment of comparative incentives associated with the offering generates the customer’s PV. PV is a primary reason for patronage (Holbrook, Citation1999) as it leads to the likelihood of the customer repurchasing the goods or services (Pura, Citation2005).

The extant literature indicates that PV is a significant predictor of customer loyalty (e.g., Fandos Roig et al., Citation2009; Hamouda, Citation2019). According to Anderson and Srinivasan (Citation2003), when PV is low, customers are more likely to migrate to rival firms. Huré et al. (Citation2017) have also illustrated that consumers’ enhanced utility in mobile banking is positively related to loyalty. Sirdeshmukh et al. (Citation2002) opined that PV is a primary goal and loyalty follows PV. As long as the value exchanged in such a relationship is superior, the PV of a consumer influences their level of loyalty to the service provider. Therefore, we postulate that a customer would feel attached to the M-wallet service provider when its PV is higher than other players in the market.

The RMMA framework supports this argument. RMMA conceptualizes PV under the customer-focused antecedents that predict loyalty behavior. Moreover, TIMC also supports this relationship, as it postulates that the size of the investment entities built while maintaining relationships impacts the commitment. Furthermore, the investment of energy, time, information, assets, and social network are the several ways of constructing and enlarging the investment size. Furthermore, both users of M-wallet and the service provider devote their valuable resources in building and sustaining relationships. Users will increase their investment size only when the PV is higher than the costs/efforts of building and maintaining the relationship. Findings from previous research support the overall notion that PV has a role in consumer loyalty (Fandos Roig et al., Citation2009; Hamouda, Citation2019; Karjaluoto et al., Citation2019). Thus, we hypothesize:

H1: Perceived value of a M-wallet positively affects loyalty towards the M-wallet.

5. Mediation of trust

M-wallet service providers attempt to enhance user’s perceived value by offering promotions, cash-back schemes, and other rewards that further increase customer loyalty (Joshi and Chawla, Citation2022; Ajina et al., Citation2023, Citation2023; Al-Hattami et al., Citation2023; Lee et al., Citation2022; Yang et al., Citation2023). M-wallets entail a considerable amount of uncertainty compared to conventional money transfers; trust is thus essential in mitigating the risk and improving customer loyalty (Bagla & Sancheti, Citation2018). The role of trust, is one of the crucial factors in the case of M-wallets, as the transactions are monetary, personal, sensitive, and confidential and the service providers should do their best to win it (Chiu et al., Citation2017; Loh et al., Citation2021; Suh & Han, Citation2002). Thus, to attain customer loyalty, there must be trust between the users and service providers (Shergill & Li, Citation2005). In the context of M-wallet, the term “trust” refers to a user’s conviction that the M-wallet will do its job as expected by the customer. Chatterjee and Bolar (Citation2019) concluded that without gaining trust, the investment made in features like user-friendly interface, adoption, and usage intentions of the M-wallet will suffer. Trust in M-wallet transactions leads to attracting and retaining customers (Pal et al., Citation2020). Therefore, PV can be converted into favorable outcomes such as loyalty only after trust is established. No matter how valuable the services are, loyalty or patronage behavior will come only after the trust is established.

The RMMA framework argues that trust is one of the crucial mediators that impact loyalty behaviors (Palmatier et al., Citation2006). Trust is conceptualized as confidence in an exchange partner’s reliability and integrity, and it is one of the most powerful relationship marketing tools that lays the “cornerstone” of long-term relationships. RMMA framework also argues that trust is more critical in service settings due to the intangible nature of service offerings. Therefore, trust will have a catalytical role in M-wallet due to the intangibility aspect coupled with monetary and confidential information exchanges. TIMC also supports the mediating role of trust in a PV-loyalty relationship. The tenet of TIMC that people with commitment would have recognized the lack of alternatives supports the relationship between trust and consumer loyalty. More specifically, TIMC research demonstrates that reliance and trust increase when a person believes that the best alternative to a relationship is, on average, less alluring than the existing one (Rusbult et al., Citation2012). Therefore, PV is likely to be influenced by trust, causing increased loyalty. Thus, we hypothesize:

H2: Trust in a M-wallet mediates the relationship between perceived value and loyalty.

6. Mediation of satisfaction

Customer satisfaction is defined as the overall positive or negative feeling about a provider’s net value of services (Woodruff, Citation1997). The extant literature on relationship marketing identifies satisfaction as a key indicator of customer patronage (Kaya et al., Citation2019; Ndubisi, Citation2007; Sharifi & Esfidani, Citation2014). Yadav and Arora (2019) argued that higher satisfaction levels contribute to higher levels of consumer loyalty in the context of M-wallet. Furthermore, many published studies argued that customer satisfaction promotes loyalty (Chen, Citation2013). More precisely, in the sense of emerging information and communication technology, customer satisfaction with M-wallet, M-banking, and M-shopping has emerged as a good indicator of loyalty (Lin & Wang, Citation2006; Methlie & Nysveen, Citation1999; Prasad Yadav & Arora, Citation2019). Kabadayi (Citation2016) argued that dissatisfied customers are more likely to explore alternatives, thereby affecting loyalty.

PV is a crucial determinant of consumer satisfaction and loyalty in e-services (see, e.g., Chen, Citation2012). PV may help M-wallet users in the assessment of utilities, but loyalty will come after customer satisfaction, that is, the customer’s belief in the probability of service leading to a positive outcome. As per TIMC, the satisfaction level in any relationship is a determinant of the level of commitment displayed. Furthermore, it is argued that satisfaction grows in strength as a person’s needs for security, camaraderie, and affiliation are addressed.

According to the RMMA framework, relational satisfaction is a mediator that impacts loyalty. Customer satisfaction is an outcome of relational satisfaction and gives service providers an opportunity to build and strengthen the relationship with the customer. Customer satisfaction is an important consequence and a key indicator of customer patronage and desire for future purchases (Mittal and Kamakura, Citation2001; Chen, Citation2012). Therefore, customer satisfaction mediates the relationship between PV and loyalty. In line with the above argument and consistent with the published literature on satisfaction and loyalty (e.g., Akroush & Mahadin, Citation2019; Anderson & Srinivasan, Citation2003; Bitner, Citation1992) we hypothesize:

H3: Satisfaction in a M-wallet mediates the relationship between the perceived value of and loyalty towards the M-wallet.

6.1. Serial mediation of trust and satisfaction

Intriguingly, a multitude of digital payment literature has demonstrated that there is no one factor impacting consumers’ loyalty, attitude, or intent, regardless of the controversy surrounding the influence of the three constructs mentioned above on their level of loyalty. Instead, a variety of variables and how they are interwoven with one another affect their intention. For instance, consumers stick to the same M-wallet service providers as they have developed trust and are also satisfied with the services. There is seldom any dichotomy between the two factors. Trust is the foundation upon which satisfaction is built, and a satisfying mobile wallet experience can lead to repeat use and loyalty. This argument can be witnessed in practice as well. For example, BHIM, one the leading M-wallet service providers in India is investing in building trust through security, reliability, ease of use, and customer support to enhance user satisfaction and ensure long-term loyalty in the competitive marketplace.

PV can increase the trust levels of consumers where satisfaction thrives. Reichheld and Schefter (Citation2000) and Lin and Wang (Citation2006) argued that trust is a primary reason for the adoption and trialability of m-commerce and leads to customer satisfaction. However, as discussed above, trust and satisfaction have been avowed as the bases for loyalty (Thakur, Citation2014; Yang & Peterson, Citation2004).

Following the TIMC and RMMA frameworks, this study unifies PV, trust, satisfaction, and loyalty. TIMC argues that there are other variables that impact the satisfaction, size of the investment, and quality of alternatives that impact the commitment. The RMMA framework proposes that relationship marketing has a large, direct effect on seller objective performance, which implies that additional meditated pathways like trust and customer satisfaction in our case may explain the impact on loyalty. More specifically, we ground our argument using TIMC, that trust is the factor that acts as a precursor to satisfaction and impacts the commitment levels. While the RMMA framework clearly outlines the sequence of trust and satisfaction as mediators of PV and loyalty relationship (Palmatier et al., Citation2006).

Using this view, we hypothesize that PV (utility assessment) may lead to attitudes (trust and customer satisfaction), which affect the propensity to make repeat purchases (customer loyalty). Therefore, it is hypothesized that trust and satisfaction together can mediate the relationship among PV and loyalty:

H4: Trust and satisfaction serially mediate the relationship between perceived value and loyalty towards a M-wallet.

7. Research methodology

The data in the study was gathered using a survey based on a self-administered questionnaire as has been often employed in e-commerce research (e.g., Eid, Citation2011; Kassim & Abdullah, Citation2010).

8. Pilot testing

A pilot study evaluates the applicability of research tools, as well as the feasibility and efficacy of a complete survey and its associated protocol, to assure the success of a full-scale study (Van Teijlingen et al., Citation2001). Forty-five participants who took part in the pilot test provided acceptable construct reliability as well as validity scores. A suitable model was found using exploratory factor analysis (EFA) and Varimax rotation, and these components explained a sizable portion of the variation (72%) in the data. Factor loadings of the items vacillated from 0.70 to 0.90. The informants demonstrated consistency in their responses for each construct, as evidenced by Cronbach’s alpha values higher than the minimum acceptable value of 0.70.

The final questionnaire was structured in three parts. The first part elicited general information about online purchases and usage of M-wallets. This part formed the qualifying questions for the respondents to proceed further. Only the respondents successfully completing this part were assigned the second part, which included questions regarding the key constructs (PV, trust, satisfaction, and loyalty) used in the research, and well-established scales from the literature were adopted (refer to Annexure A). PV was measured with a four-item scale adopted from Chang et al. (Citation2009); trust was measured with a five-item scale adopted from Shaw (Citation2014); satisfaction was measured with a five-item scale; and loyalty was measured with a three-item scale, both adopted from Deng et al. (Citation2010) (APPENDIX A). A seven-point Likert scale was used to evaluate each item, with 1 denoting strong disagreement and 7 denoting strong agreement. The last part of the questionnaire captured the demographic information of the respondent.

9. Sampling design

The conceptual model was tested in this research utilizing a cross-sectional survey method and a structured questionnaire. India was chosen for data collection since it is a rapidly expanding online commerce and M-wallet transactions market. By administering the questionnaire to individuals who had previously used an M-wallet, the conceptual model was put to the test. Youth make up a significant portion of the respondent base because they use M-wallets more frequently than other age groups (Choudhury & Dey, Citation2014). Graduate and postgraduate students were given a link to an online survey we developed, and in exchange for a little incentive, they were asked to share it with their acquaintances who were both students and non-students. According to Fernando et al. (Citation2018), the sampling method was similar to snowball sampling. The individual must be 21 or older and have used an M-wallet at least once in the last three months to be eligible to participate. An M-wallet brand that the respondents are familiar with should be named, and their usage experience should be evaluated. If a responder used more than one M-wallet brand, they were asked to rank that brand based on their level of familiarity.

We were successful in gathering 214 responses throughout the course of six months. 214 samples from the 250 disseminated questionnaires were chosen for analysis since the remaining questionnaires were either missing pieces or errors. According to Chen et al. (Citation2022), the sample size is more than enough to generate a medium effect size (f2 = 0.14) using the G*Power software.

M-wallet users from varied backgrounds make up the sample for this study. The respondents’ gender distribution was approximately equal, with 64.02% being men. 10.28% and 15.42% of the sample consisted of respondents in the 21–25 and 26–30 age groups, respectively, while 56.07% were in the 31–35 age group. 50 % of the respondents have a diploma and undergraduate degrees, and the rest, 50 %, have postgraduates and PhD. All the respondents were employed, and 70% had annual family income in the 8–12 and 12–18 lacs range. Table summarizes this information and details the samples’ demographic profile.

Table 2. Summary of the respondents

10. Analysis of the results

The data collected for this study was analysed using structural equation modelling with partial least square (PLS-SEM version 3.3.3). PLS-SEM is a widely used tool due to its ability to work with smaller samples, no prior assumption on data distribution, and higher statistical power than covariance-based (CB) SEM (Hair et al., Citation2019; Rigdon et al., Citation2017). The fundamental approach of PLS-SEM involves determining coefficients and various parameters by minimizing unexplained variance while maximizing explained variance, as outlined by Hair et al. (Citation2012). This technique involves computing partial regression relationships within both the measurement and structural models through ordinary least square regressions, making it particularly advantageous when dealing with a limited sample size, as suggested by Hair et al. (Citation2012). Additionally, for a more precise treatment of a multiple-mediator model, PLS-SEM is a suitable approach, as highlighted by Carrión, Nitzl, and Roldán (2017). Therefore, PLS-SEM is a suitable method for the data analysis in this study.

The analysis is divided into two stages, with the first stage focusing on evaluating the measurement model and the second stage assessing the structural model, as outlined by Hair et al. (Citation2012). A detailed description of the measurement model can be found in Table . The Average Variance Extracted (AVE) surpasses the threshold of 0.5, and the convergent validity for individual item loadings exceeds 0.70, aligning with the criteria set by Hair et al. (Citation2012) and Henseler et al. (Citation2014). Additionally, the Composite Reliability (CR) surpasses the acceptable threshold of 0.70, in line with the standard proposed by Henseler, Ringle, and Sinkovics (2009). Consequently, the findings regarding item reliability, CR, and AVE provide strong support for convergent validity.

Table 3. Summary results of the measurement model and convergent validity

Discriminant validity serves as a measure to assess the extent to which constructs differ from one another. It is determined by comparing each latent variable’s square root of the Average Variance Extracted (AVE) with its correlations with other constructs (please see Tables for details). Following the Fornell-Larcker criterion, it is imperative that the diagonal values in these tables are higher than the values in the corresponding columns, demonstrating that each construct is distinct from the others. Further, we also validated the discriminant validity with hetero trait-mono trait (HTMT) ratio. Table shows that all values are below 0.9 as suggested by Henseler et al. (Citation2015).

Table 4. Discriminant validity: fornell-larcker criterion

Table 5. Discriminant validity: HTMT Ratio

11. Common method bias

Although a survey might assist researchers in obtaining a variety of samples, this approach itself may erode the validity of results, a phenomenon known as common method bias (Podsakoff et al., Citation2003). We used two key strategies namely, procedure design and statistical control, to reduce common method bias. For the former, an anonymous pilot test of the survey questionnaire was undertaken with the participants. For the latter, Harman’s one-factor test was conducted. In accordance with the findings, the first component only accounted for 34.62% of the overall variation, meeting the cutoff criterion of 50% (Fornell & Bookstein, Citation1982).

11.1. Hypotheses testing

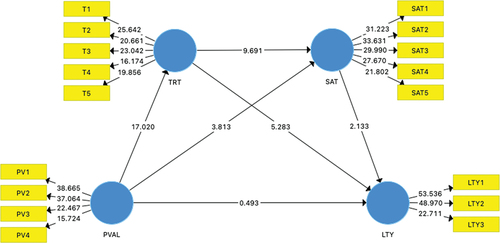

The study uses structural model in order to test the proposed hypothesis and is shown in Figure . Multicollinearity concerns have been addressed by assessing the Variance Inflation Factor (VIF) values. It is worth noting that all VIF values are below 3, indicating that the data can be considered free from collinearity issues (Hair et al., Citation2011). Furthermore, all the VIFs value of less than 3.3 in the model indicated the model can be considered free from common method bias (Kock, Citation2015).

Figure 1. Structural model.

Following the multicollinearity analysis, the main effects of the hypotheses were analyzed. The results are given in Table . Following the Baron and Kenny (Citation1986) approach to mediation analysis, we checked the relationship of PV to loyalty (H1), which was found to be significant (p < 0.05). We further checked for the mediating relationship of trust (H2), satisfaction (H3), and trust and satisfaction in series (H4). As the relationship of PV to loyalty (H1) turned out to be insignificant in the presence of mediating variables, trust and satisfaction, thus confirming full mediation of trust and satisfaction between the PV and loyalty relationship.

Table 6. Results of hypotheses testing

11.2. Model fit

The model fit can be checked with the Standardized Root Mean-Square Residual (SRMR) value of the analysis. The results show that SRMR value is 0.093, which is less than 0.1, indicating the model fit (Henseler et al., Citation2014).

11.3. R2 and Q2 values assessment

The evaluation of the structural model relies on the R2 value, which measures the squared correlation between actual and predicted values of a specific endogenous construct and assesses the model’s predictive accuracy. R2 represents the cumulative impact of exogenous variables on endogenous latent variables and quantifies the total variation in endogenous constructs explained by all associated exogenous constructs (Hair et al., Citation2013). In the current study, the endogenous variables, namely Loyalty, Satisfaction, and Trust, exhibit R2 values of 0.45, 0.61, and 0.45, respectively. These values demonstrate that the structural model constructed in this study possesses predictive relevance.

Furthermore, blindfolding (Hair et al., Citation2013) was used to cross-validate the model’s predictive relevance for each of the individual endogenous variables. It generated cross-validated redundancy Q2 values for all endogenous variables with an omission distance of eight. Since all of the Q2 values (0.33, 0.39, and 0.25) are greater than zero the structural model has a predictive relevance.

12. Discussion

This study was guided by two main objectives. The first one was to examine the PV—customer loyalty relationship in the context of M-wallet. The second one was to investigate the sequential mediating influence of trust and customer satisfaction in the relationship between and customer loyalty. Several conclusions have been drawn from this research. First, consumers may be loyal to M-wallet service providers if they find value in the products and services offered by the firm. Thus, only when the PV of the M-wallet is high, the loyalty would be high, which is found to be true from the results of the study. The study’s findings confirm that PV has a positive and significant influence on increasing customer loyalty, which is consistent with previous research by Pura (Citation2005), Fandos Roig et al. (Citation2009), and Rahi et al. (Citation2017). However, the relationship becomes insignificant the moment we explore the role of the mediating variables in the model. The results direct us to the point that there are some other variables that lead to a higher loyalty indirectly, as argued in hypotheses 2–4.

Second, the study builds upon the PV-loyalty literature to identify the variables that may better explain the relationship. To do so, the present study explored the mediating role of trust and satisfaction. The mediating relationship of PV-trust-loyalty and PV-satisfaction-loyalty have both been found to be significant. Our results resonate with those from earlier studies that claim that trust plays a catalytic role in the PV-customer loyalty relationship (Hoang, Citation2019; Yuen et al., Citation2018). Previous studies also indicate a lack of trust as a hindrance in fostering loyalty (Kim & Ferrin, Citation2008) in the customer. Higher PV leads to trust in the M-wallet being used, eventually leading to positive loyalty towards that M-wallet. Thus, the results of the study confirm the mediating relationship of trust between PV and loyalty.

Third, this study also highlights the importance of satisfaction in the PV-loyalty relationship as a mediating variable. The results are in conformity with the traditional value-satisfaction-loyalty literature (e.g., Gallarza & Saura, Citation2006; Xu et al., Citation2015).

Finally, this study also establishes the sequential mediation effect between PV and loyalty. The results indicate that to build loyalty it is important to have the trust of the consumer and they must be satisfied with the services offered by the M-wallet. This becomes even more important in today’s digital age when consumers are losing trust in the service provider due to privacy concerns.

Based on the results, we critically discuss the implications of the serial mediation hypothesized in the present study. In the M-wallet context, trust plays a crucial role in the PV-customer loyalty dynamic (Shaw, Citation2014; Talwar et al., Citation2020). In this industry, users place their trust in the service provider to safeguard their financial information and transactions, effectively bridging the gap between PV and customer loyalty (Al-Dwairi & Al-Ali, Citation2022). For users to confidently utilize M-wallets, they must believe in the security of their financial data and transactions. PV contributes to this trust-building process by offering features and advantages that enhance the perception of security. Previous studies have shown that trust acts as a mediator (Prasetya & Shuhidan, Citation2023) in the connection between PV and customer loyalty. As users perceive greater value in M-wallets, such as safety, convenience, rewards, and user-friendliness, their trust in the service provider tends to grow, ultimately resulting in heightened satisfaction and ultimately to loyalty.

Furthermore, the M-wallet literature emphasizes the importance of user satisfaction (Ajina et al., Citation2023, Citation2023). Users must experience overall satisfaction with mobile wallets, encompassing factors like ease of use, reliability, and the availability of desired features. When users perceive significant value in M-wallet offerings, such as cost-effectiveness, rewards, and smooth transactions, they are more inclined to be satisfied with the service. This, in turn, exerts a positive influence on their repeat use and loyalty behavior (Al-Hattami et al., Citation2023; Daragmeh et al., Citation2022).

When users transact using a M-wallet to manage their money, they need to believe that the service provider is keeping their financial information safe and secure. This trust forms a link between how much user think the M-wallet is worth and how loyal they are to that M-wallet. So, trust is like a bridge between how useful the mobile wallet is and how much users like it. Users also need to be happy with how the M-wallet works overall. This means it should be easy to use, reliable, and have all the features they want. When they’re satisfied, they are more likely to stick with that M-wallet and keep using it, which leads to loyalty. Therefore, the sequence of events is like first M-wallet have the value, therefore trial happens. After few transactions if the experience is positive it will lead to trust. Once they trust it, over a period of time, they become satisfied. This satisfaction will lead to repeat usage, positive word-of-mouth and loyalty behavior. Our results are in sync with other serial mediation models leading to PV to loyalty (e.g., Aye, Citation2021; Moriuchi & Takahashi, Citation2022) and extends this discussion in the M-wallet context.

13. Implications

13.1. Theoretical implications

This research adds to the academia and practice by offering insight into customers’ M-wallet loyalty behavior. First, the study recognizes the driving forces of customer loyalty and their relations with PV. PV holds significant importance due to its role as an antecedent that influences trust and satisfaction in a cause-and-effect relationship. The study uses the RMMA framework to explain the PV—customer loyalty relationship. Specifically, the study adds value to the consumer-focused antecedents and outcomes by exploring the relation between PV and customer loyalty through customer-focused relational mediators of trust and satisfaction.

The next implication of this research highlights the mediation role of trust in the PV—customer loyalty relationship. This research shows that trust influences loyalty behavior by enhancing the perception of value derived via M-wallet usage. By offering greater PV, businesses can achieve two important outcomes among their customers: Value Equity and Relationship Equity, as outlined by Rust, Zeithaml, and Lemon (2000). Value Equity refers to the unique benefits customers receive in exchange for their money, encompassing factors like price, convenience, and quality, as described by Vogel et al. (Citation2008). On the other hand, Relationship Equity pertains to the elements that create a bond between customers and a brand, beyond the value they obtain from their transactions. In this context, we argue that PV contributes to both Value Equity and Relationship Equity, fostering the development of trust. Existing research suggests that trust plays a pivotal role in driving customer loyalty, especially in online financial transactions (Purwanto et al., Citation2020; Thakur, Citation2014). Consequently, the presence of trust is a key factor in promoting loyalty in the usage of mobile wallets (Singh & Sinha, Citation2020). Given the nature of the financial services industry, building trust is essential to ensure customer loyalty. Additionally, trust in a mobile wallet service provider not only attracts new customers but also retains existing ones (Pal et al., Citation2020).

Further, another key research implication of this study is the significance of customer satisfaction in the relationship between Perceived Value (PV) and loyalty. This suggests that PV can impact user satisfaction, bolster their connection with an M-wallet service provider, and consequently, reinforce their loyalty. This observation is supported by the findings of Fatima et al. (Citation2018). It’s noteworthy that PV has a direct impact on customer satisfaction. In practical terms, when an M-wallet service delivers greater value, it increases the likelihood of higher customer satisfaction, as confirmed by Karjaluoto et al. (Citation2019). Consequently, a higher PV cultivates a sense of dependence among M-wallet users, which, in turn, amplifies the service provider’s commitment to ensuring customer satisfaction. The presence of contented users results in a mutual reliance on the M-wallet, establishing a strong connection between PV and customer satisfaction. There are various intervening factors via which the service provider’s and users’ interests converge, resulting in a customer satisfaction—loyalty connection. First, customer satisfaction leads to profitability (Gronholdt et al., Citation2000). Second, satisfaction reduces the search for alternative behavior (Kabadayi, Citation2016). Third, customer satisfaction encourages customer interaction and, as a result, customer loyalty (Hoang, Citation2019). Fourth, the literature presents empirical evidence for customer—customer loyalty relationships Amin, Citation2016; Prasad Yadav & Arora, Citation2019; Thakur, Citation2014.

The fourth important implication of this study is the presence of a serial mediation effect. The association between PV and loyalty is mediated by trust and satisfaction. This conclusion implies that the impact of PV on loyalty will be influenced first by trust, which will lead to higher levels of satisfaction and eventually to long-term loyalty.

Scholars have argued whether PV, trust, or customer satisfaction are the antecedent constructs of loyalty (Hoang, Citation2019; Lin & Wang, Citation2006). In this aspect, the findings back up the earlier assertion that PV has a greater impact on satisfaction. Furthermore, a previous study (Sivadas & Baker‐Prewitt, Citation2000) has revealed that satisfied clients are not always loyal. As a result, experts contend that trust promotes an increase in the emotive response as a result of service adoption and usage, and hence contributes to the firm’s worth Gupta et al., Citation2020; Suh & Han, Citation2002. As a result, the debate on trust and customer satisfaction is skewed in favor of the assumption that trust is an antecedent of customer satisfaction.

This study’s findings add to the growing body of research. While PV contributes to both trust and satisfaction, serial mediation means that the constructs of trust and satisfaction do not contribute significantly to consumer loyalty on their own. Second, this study has demonstrated that TIMC processes’ premise that satisfaction is the primary factor that drives the commitment—loyalty relationship is appropriate, even if it is trust that causes customer satisfaction. Furthermore, this study also supports the RMMA framework confirming the mediating role of trust and satisfaction and building the argument of serial mediation.

Thus, this study provides a comprehensive understanding of the role of PV, trust, and satisfaction in building customer loyalty.

13.2. Practical implications

This research holds significant implications for M-wallet service providers. Firstly, it underscores the crucial role of Perceived Value (PV) in shaping customer loyalty to M-wallet services. To enhance PV, M-wallet providers should strive to reduce costs while maintaining service quality, as suggested by McKinsey (Citation2016). It’s vital to ensure that customers perceive the incentives for usage, referrals, cashback, rewards, etc., as corresponding with the service received, providing good value for their time and effort. To achieve this, it is essential to understand the strategies employed by other M-wallet providers, allowing for the creation of offers that not only meet customer expectations but are also perceived as distinctive in terms of PV. By doing so, M-wallet providers can cultivate a base of loyal customers.

To boost their Perceived Value (PV), M-wallet service providers should invest in delivering precise services of an optimal quality level, which must be consistently upheld. Achieving this requires M-wallet service providers to gain a deep understanding of their customers’ touchpoints, end-to-end journeys, perspectives, and experiences. They should conduct thorough analyses of customer data to formulate effective strategies aimed at maximizing PV, as recommended by McKinsey (Citation2016). Managers should maintain ongoing vigilance over M-wallet users’ behaviors, enabling them to fine-tune and offer exceptional customer experiences that align with customer expectations. When these experiences are seen as appealing and delightful, they will enhance customers’ Perceived Value of the M-wallet service provider. Therefore, M-wallet service providers should prioritize enhancing the value-for-money proposition, which in turn has a positive impact on customer loyalty.

Second, the mediating variables that influence the PV-loyalty relationship are trust and satisfaction. Managers of M-wallet can actively encourage loyalty by winning both consumers’ trust and satisfaction. PV impacts trust, which eventually makes the customers happy and satisfied and motivates them to exhibit patronage behavior, leading to their loyalty. In order to win the consumers’ trust and satisfaction it is of utmost importance for the managers to ensure that the team maintains the safety and privacy of the transactions, as these are monetary, personal, sensitive, and confidential. Additionally, it is essential for customer care personnel to possess a high level of financial expertise and in-depth knowledge about the firm’s services. Moreover, these contact personnel should possess strong social skills to ensure that customers always feel well attended to.

14. Limitations and future research

The study provides an overview of the factors affecting loyalty in M-wallet services. Despite the above-mentioned contribution to the literature on M-wallet, the present study has a few limitations. First, the study has considered a unidimensional PV scale for the sake of simplicity. Future studies may consider a multi-dimensional PV scale as it may be helpful in examining the complex nature of consumers’ value perceptions (Sánchez-Fernández & Iniesta-Bonillo, Citation2007). Second, this study adopted a cross-sectional approach for data collection. For more insights and to increase the power of the model, longitudinal studies need to be conducted. Third, this study has used the survey method with SEM as the analysis technique. Future studies may consider other research methodologies such as experimental design, and simulations to explore this research agenda. Fourth, this study has considered only two mediators namely, trust and satisfaction. Future studies may look at other mediators to increase the predictive power of the model. For example, the role of commitment as one of the mediating variables may be explored. Commitment and trust have been identified as critical in building loyalty in the e-services context (Chen, Citation2012). Fifth, no moderating effect was explored in this study. Some of the moderators that may be explored include but are not limited to, the age of the relationship and the level of usage. Finally, future studies may also look into various contexts to generalize the model by investigating these relationships in a multi-country setting.

Author Bio.docx

Download MS Word (16.4 KB)Disclosure statement

No potential conflict of interest was reported by the authors.

Supplemental material

Supplemental data for this article can be accessed online at https://doi.org/10.1080/23311975.2023.2281050

Additional information

Funding

Notes on contributors

Amol S. Dhaigude

Amol S. Dhaigude is working as an Associate Professor, Department of Operations & Supply chain management and Quantitative Methods at S P Jain Institute of Management and Research, Mumbai, India. He is Fellow (OM&QT) from IIM Indore, India. He is actively engaged in research in supply chain coordination, tourism management, and services operations and published papers in high impact factored well reputed international journals. He is profound case-writer and teacher.

Archit Vinod Tapar

Archit Vinod Tapar is working as an Assistant Professor in IIM Rohtak, India. He is a Fellow (Marketing) from IIM Indore, India. His research interest includes brand management, services marketing, tourism marketing, and e_tailing. He has published and showcased his research work in journals & conferences of repute worldwide.

Mohammad Shameem Jawed

Mohammad Shameem Jawed is working as an Assistant Professor in IIM Visakhapatnam, India. He is a Fellow (Finance & Accounting Area) from IIM Indore, India. His teaching and research interests lie in the fields of Financial Analytics, Corporate Finance, Capital Market Regulation & Governance, Market Liquidity, Equity & Startup Financing, Cost Management and Tourism Management.

Giridhar B Kamath

Giridhar B Kamath is working as an Associate professor in the Department of Humanities and Management, Manipal Institute of Technology, Manipal Academy of Higher Education, Manipal, India. His teaching and research interests lie in the fields of Marketing Management, Sports Marketing, Tourism Management, and System Dynamics.

References

- Abu ELSamen, A. A. (2015). Online service quality and brand equity: The mediational roles of perceived value and customer satisfaction. Journal of Internet Commerce, 14(4), 509–23. https://doi.org/10.1080/15332861.2015.1109987

- ACI. (2021). Retrieved March 2, 2022 https://investor.aciworldwide.com/news-releases/news-release-details/global-real-time-payments-transactions-surge-41-percent-2020

- Ajina, A. S., Javed, H. M. U., Ali, S., & Zamil, A. M. (2023). Are men from Mars, women from Venus? Examining gender differences of consumers towards mobile-wallet adoption during pandemic. Cogent Business & Management, 10(1), 2178093. https://doi.org/10.1080/23311975.2023.2178093

- Ajina, A. S., Joudeh, J. M., Ali, N. N., Zamil, A. M., & Hashem, T. N. (2023). The effect of mobile-wallet service dimensions on customer satisfaction and loyalty: An empirical study. Cogent Business & Management, 10(2), 2229544. https://doi.org/10.1080/23311975.2023.2229544

- Akroush, M. N., & Mahadin, B. K. (2019). An intervariable approach to customer satisfaction and loyalty in the internet service market. Internet Research, 29(4), 772–798. https://doi.org/10.1108/IntR-12-2017-0514

- Al-Dwairi, R. A. D. W. A. N., & Al-Ali, O. M. A. R. (2022). The role of trust and satisfaction as mediators on users’ continuous intention to use mobile payments: Empirical study. Journal of Theoretical & Applied Information Technology, 100(9), 3035–3047.

- Al-Hattami, H. M., Al-Adwan, A. S., Abdullah, A. A. H., Al-Hakimi, M. A., & Duradoni, M. (2023). Determinants of customer loyalty toward mobile wallet services in post-COVID-19: The moderating role of trust. Human Behavior and Emerging Technologies, 2023, 1–13. https://doi.org/10.1155/2023/9984246

- Amin, M.(2016). Internet banking service quality and its implication on e-customer satisfaction and e-customer loyalty. International Journal of Bank Marketing, 34(3), 280–306.

- Amoroso, D. L., & Ackaradejruangsri, P. (2018). The mobile wallet explosion in Thailand: Factors towards predicting consumer loyalty. Asia Pacific Journal of Information Systems, 28(4), 290–307. https://doi.org/10.14329/apjis.2018.28.4.290

- Amoroso, D. L. & Magnier-Watanabe, R.(2012). Building a research model for mobile wallet consumer adoption: The case of mobile suica in Japan. Journal of Theoretical & Applied Electronic Commerce Research, 7(1), 94–110.

- Anderson, E. W., & Fornell, C. (1994). A customer satisfaction research prospectus. In R. T. Rust & R. L. Oliver (Eds.), Service quality: New directions in theory and practice (pp. 241–268). Sage Publications.

- Anderson, R. E., & Srinivasan, S. S. (2003). E‐satisfaction and e‐loyalty: A contingency framework. Psychology & Marketing, 20(2), 123–138. https://doi.org/10.1002/mar.10063

- Aye, A. C. (2021). The mediating role of perceived value and customer satisfaction on the relationship between service convenience and loyalty: A case study of a Private Bank in Myanmar. Human Behavior, Development & Society, 22(2), 60–71.

- Bagla, R. K. & Sancheti, V.(2018). Gaps in customer satisfaction with digital wallets: Challenge for sustainability. Journal of Management Development, 37(6), 442–451.

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1192. https://doi.org/10.1037/0022-3514.51.6.1173

- Berry, L. L. (1995). Relationship marketing of services—growing interest, emerging perspectives. Journal of the Academy of Marketing Science, 23(4), 236–245. https://doi.org/10.1177/009207039502300402

- Bitner, M. J. (1992). Servicescapes: The impact of physical surroundings on customers and employees. Journal of Marketing, 56(2), 57–71. https://doi.org/10.1177/002224299205600205

- Blanchard, R. F. & Galloway, R. L.(1994). Quality in retail banking. International Journal of Service Industry Management, 5(4), 5–23.

- Bügel, M. S., Buunk, A. P., & Verhoef, P. C. (2010). A comparison of customer commitment in five sectors using the psychological investment model. Journal of Relationship Marketing, 9(1), 2–29. https://doi.org/10.1080/15332660903551883

- Cao, X., Yu, L., Liu, Z., Gong, M., & Adeel, L. (2018). Understanding mobile payment users’ continuance intention: A trust transfer perspective. Internet Research, 28(2), 456–476. https://doi.org/10.1108/IntR-11-2016-0359

- Chang, H. H. Wang, Y. H. & Yang, W. Y.(2009). The impact of e-service quality, customer satisfaction and loyalty on e-marketing: Moderating effect of perceived value. Total Quality Management, 20(4), 423–443.

- Chatterjee, D., & Bolar, K. (2019). Determinants of mobile wallet intentions to use: The mental cost perspective. International Journal of Human–Computer Interaction, 35(10), 859–869. https://doi.org/10.1080/10447318.2018.1505697

- Chawla, D. & Joshi, H.(2019). Consumer attitude and intention to adopt mobile wallet in India–an empirical study. International Journal of Bank Marketing, 37(7), 1590–1618.

- Chen, L. Y. (2013). Antecedents of customer satisfaction and purchase intention with mobile shopping system use. International Journal of Services and Operations Management, 15(3), 259–274. https://doi.org/10.1504/IJSOM.2013.054442

- Chen, S. C. (2012). The customer satisfaction–loyalty relation in an interactive e-service setting: The mediators. Journal of Retailing and Consumer Services, 19(2), 202–210. https://doi.org/10.1016/j.jretconser.2012.01.001

- Chen, C. C., Chang, C. H., & Hsiao, K. L. (2022). Exploring the factors of using mobile ticketing applications: Perspectives from innovation resistance theory. Journal of Retailing and Consumer Services, 67, 102974. https://doi.org/10.1016/j.jretconser.2022.102974

- Chiu, J. L. Bool, N. C. & Chiu, C. L.(2017). Challenges and factors influencing initial trust and behavioral intention to use mobile banking services in the Philippines. Asia Pacific Journal of Innovation and Entrepreneurship, 11(2), 246–278.

- Chopdar, P. K., & Balakrishnan, J. (2020). Consumers response towards mobile commerce applications: SOR approach. International Journal of Information Management, 53, 1–16. https://doi.org/10.1016/j.ijinfomgt.2020.102106

- Choudhury, D., & Dey, A. (2014). Online shopping attitude among the youth: A study on university students. International Journal of Entrepreneurship and Development Studies, 2(1), 23–32.

- Chuah, S. H. W. Marimuthu, M. Kandampully, J. & Bilgihan, A.(2017). What drives Gen Y loyalty? Understanding the mediated moderating roles of switching costs and alternative attractiveness in the value-satisfaction-loyalty chain. Journal of Retailing & Consumer Services, 36, 124–136.

- Daragmeh, A., Sági, J., & Zéman, Z. (2021). Continuous intention to use e-wallet in the context of the COVID-19 pandemic: Integrating the health belief model (hbm) and technology continuous theory (tct). Journal of Open Innovation: Technology, Market, and Complexity, 7(2), 132. https://doi.org/10.3390/joitmc7020132

- Daragmeh, A., Saleem, A., Bárczi, J., & Sági, J. (2022). Drivers of post-adoption of e-wallet among academics in Palestine: An extension of the expectation confirmation model. Frontiers in Psychology, 13, 984931. https://doi.org/10.3389/fpsyg.2022.984931

- Deng, Z., Lu, Y., Wei, K. K., & Zhang, J. (2010). Understanding customer satisfaction and loyalty: An empirical study of mobile instant messages in China. International Journal of Information Management, 30(4), 289–300. https://doi.org/10.1016/j.ijinfomgt.2009.10.001

- Eid, M. I. (2011). Determinants of e-commerce customer satisfaction, trust, and loyalty in Saudi Arabia. Journal of Electronic Commerce Research, 12(1), 78–93.

- El-Adly, M. I. (2019). Modelling the relationship between hotel perceived value, customer satisfaction, and customer loyalty. Journal of Retailing and Consumer Services, 50, 322–332. https://doi.org/10.1016/j.jretconser.2018.07.007

- Fandos Roig, J. C., García, J. S., & Moliner Tena, M. Á. (2009). Perceived value and customer loyalty in financial services. The Service Industries Journal, 29(6), 775–789. https://doi.org/10.1080/02642060902749286

- Fatima, J. K., Mascio, R. D., & Johns, R. (2018). Impact of relational benefits on trust in the Asian context: Alternative model testing with satisfaction as a mediator and relationship age as a moderator. Psychology & Marketing, 35(6), 443–453. https://doi.org/10.1002/mar.21097

- Fernando, A. G., Sivakumaran, B., & Suganthi, L. (2018). Comparison of perceived acquisition value sought by online second-hand and new goods shoppers. European Journal of Marketing, 52(7/8), 1412–1438. https://doi.org/10.1108/EJM-01-2017-0048

- Fornell, C., & Bookstein, F. L. (1982). Two structural equation models: LISREL and PLS applied to consumer exit-voice theory. Journal of Marketing Research, 19(4), 440–452. https://doi.org/10.1177/002224378201900406

- Gallarza, M. G. & Saura, I. G.(2006). Value dimensions, perceived value, satisfaction and loyalty: An investigation of university students’ travel behaviour. Tourism Management, 27(3), 437–452.

- Garrouch, K. (2021). Does the reputation of the provider matter? A model explaining the continuance intention of mobile wallet applications. Journal of Decision Systems, 30(2–3), 150–171. https://doi.org/10.1080/12460125.2020.1870261

- Givertz, M. & Segrin, C.(2005). Explaining personal and constraint commitment in close relationships: The role of satisfaction, conflict responses, and relational bond. Journal of Social & Personal Relationships, 22(6), 757–775.

- Gong, X., Cheung, C. M., Liu, S., Zhang, K. Z., & Lee, M. K. (2021). Battles of mobile payment networks: The impacts of network structures, technology complementarities and institutional mechanisms on consumer loyalty. Information Systems Journal, 32(4), 696–728. https://doi.org/10.1111/isj.12366

- Gong, X., Cheung, C. M., Zhang, K. Z., Chen, C., & Lee, M. K. (2020). Cross-side network effects, brand equity, and consumer loyalty: Evidence from mobile payment market. International Journal of Electronic Commerce, 24(3), 279–304. https://doi.org/10.1080/10864415.2020.1767427

- Gounaris, S. P. Tzempelikos, N. A. & Chatzipanagiotou, K.(2007). The relationships of customer-perceived value, satisfaction, loyalty and behavioral intentions. Journal of Relationship Marketing, 6(1), 63–87.

- Gronholdt, L., Martensen, A., & Kristensen, K. (2000). The relationship between customer satisfaction and loyalty: Cross-industry differences. Total Quality Management, 11(4–6), 509–514. https://doi.org/10.1080/09544120050007823

- Grover, P. A. K. (2020). User engagement for mobile payment service providers–introducing the social media engagement model. Journal of Retailing and Consumer Services, 53, 1–13. https://doi.org/10.1016/j.jretconser.2018.12.002

- GS, A. P., & Arivazhagan, R. (2021). A study on user perceived trust in mobile wallet. International Journal of Management, IJM, 12(3), 125–133. https://doi.org/10.34218/IJM.12.3.2021.011

- Gupta, R. K. (2022). Adoption of mobile wallet services: An empirical analysis. International Journal of Intellectual Property Management, 12(3), 341–353. https://doi.org/10.1504/IJIPM.2022.124634

- Gupta, A., Yousaf, A., & Mishra, A. (2020). How pre-adoption expectancies shape post-adoption continuance intentions: An extended expectation-confirmation model. International Journal of Information Management, 52(6), 1–13. https://doi.org/10.1016/j.ijinfomgt.2020.102094

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory & Practice, 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2013). Partial least squares structural equation modeling: Rigorous applications, better results and higher acceptance. Long Range Planning, 46(1–2), 1–12. https://doi.org/10.1016/j.lrp.2013.01.001

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

- Hair, J. F., Sarstedt, M., Ringle, C. M., & Mena, J. A. (2012). An assessment of the use of partial least squares structural equation modeling in marketing research. Journal of the Academy of Marketing Science, 40(3), 414–433. https://doi.org/10.1007/s11747-011-0261-6

- Hamouda, M. (2019). Omni-channel banking integration quality and perceived value as drivers of consumers’ satisfaction and loyalty. Journal of Enterprise Information Management, 32(4), 608–625. https://doi.org/10.1108/JEIM-12-2018-0279

- Henseler, J., Dijkstra, T. K., Sarstedt, M., Ringle, C. M., Diamantopoulos, A., Straub, D. W., Ketchen, D. J., Hair, J. F., Hult, G. T. M., & Calantone, R. J. (2014). “Common beliefs and reality about partial least squares: Comments on Rönkkö & Evermann (2013). Organizational Research Methods, 17(2), 182–209. https://doi.org/10.1177/1094428114526928

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Hoang, D. P. (2019). The central role of customer dialogue and trust in gaining bank loyalty: An extended SWICS model. International Journal of Bank Marketing, 37(3), 711–729. https://doi.org/10.1108/IJBM-03-2018-0069

- Holbrook, M. B. (1999). Introduction to consumer value. In M. B. Holbrook (Ed.), Consumer value. A framework for analysis and research (pp. 1–28). Routledge.

- Huré, E., Picot-Coupey, K., & Ackermann, C. L. (2017). Understanding omni-channel shopping value: A mixed-method study. Journal of Retailing and Consumer Services, 39(1), 314–330. https://doi.org/10.1016/j.jretconser.2017.08.011

- Johan, A. P., Lukviarman, N., & Putra, R. E. (2022). Continuous intention to use e-wallets in Indonesia: The impact of e-wallets features. Innovative Marketing, 18(4), 74–85. https://doi.org/10.21511/im.18(4).2022.07

- Joshi, H., & Chawla, D. (2023). Identifying unobserved heterogeneity in mobile wallet adoption–A FIMIX-PLS approach for user segmentation. International Journal of Bank Marketing, 41(1), 210–236. https://doi.org/10.1108/IJBM-03-2022-0132

- Kabadayi, S.(2016). Customers’ dissatisfaction with banking channels and their intention to leave banks: The moderating effect of trust and trusting beliefs. Journal of Financial Services Marketing, 21, 194–208.

- Karjaluoto, H., Shaikh, A. A., Saarijärvi, H., & Saraniemi, S. (2019). How perceived value drives the use of mobile financial services apps. International Journal of Information Management, 47, 252–261. https://doi.org/10.1016/j.ijinfomgt.2018.08.014

- Kassim, N., & Abdullah, N. A. (2010). The effect of perceived service quality dimensions on customer satisfaction, trust, and loyalty in e‐commerce settings. Asia Pacific Journal of Marketing & Logistics, 22(3), 351–371. https://doi.org/10.1108/13555851011062269

- Kaur, P., Dhir, A., Bodhi, R., Singh, T., & Almotairi, M. (2020). Why do people use and recommend m-wallets? Journal of Retailing & Consumer Services, 56, 1–11. https://doi.org/10.1016/j.jretconser.2020.102091

- Kaya, B., Behravesh, E., Abubakar, A. M., Kaya, O. S., & Orús, C. (2019). The moderating role of website familiarity in the relationships between e-service quality, e-satisfaction and e-loyalty. Journal of Internet Commerce, 18(4), 369–394. https://doi.org/10.1080/15332861.2019.1668658

- Kim, D. J., Ferrin, D. L. A. R. (2008). A trust-based consumer decision-making model in electronic commerce: The role of trust, perceived risk, and their antecedents. Decision Support Systems, 44(2), 544–564. https://doi.org/10.1016/j.dss.2007.07.001

- Kock, N.(2015). Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of E-Collaboration (IJEC), 11(4), 1–10.

- Kumar, V., Dalla Pozza, I., & Ganesh, J. (2013). Revisiting the satisfaction–loyalty relationship: Empirical generalizations and directions for future research. Journal of Retailing, 89(3), 246–262. https://doi.org/10.1016/j.jretai.2013.02.001

- Lapierre, J.(2000). Customer‐perceived value in industrial contexts. Journal of Business & Industrial Marketing, 15(2/3), 122–145.

- Lee, Y. Y., Gan, C. L., Liew, T. W., & Yan, Z. (2022). The impacts of mobile wallet app characteristics on online impulse buying: A moderated mediation model. Human Behavior and Emerging Technologies, 2022, 1–15. https://doi.org/10.1155/2022/2767735

- Lee, T., Jun, J., & Schierholz, R. (2007). Contextual perceived value?: Investigating the role of contextual marketing for customer relationship management in a mobile commerce context. Business Process Management Journal, 13(6), 798–814. https://doi.org/10.1108/14637150710834569

- Lin, H. H., & Wang, Y. S. (2006). An examination of the determinants of customer loyalty in mobile commerce contexts. Information & Management, 43(3), 271–282. https://doi.org/10.1016/j.im.2005.08.001

- Loh, X.-M., Lee, V.-H., Tan, G. W.-H., Ooi, K.-B., & Dwivedi, Y. K. (2021). Switching from cash to mobile payment: What’s the hold-up?. Internet Research, 31(1), 376–399.

- Ly, H. T. N., Khuong, N. V., & Son, T. H. (2022). Determinants affect mobile wallet continuous usage in covid 19 pandemic: Evidence from Vietnam. Cogent Business & Management, 9(1), 2041792. https://doi.org/10.1080/23311975.2022.2041792

- Madan, K., & Yadav, R. (2016). Behavioural intention to adopt mobile wallet: A developing country perspective. Journal of Indian Business Research, 8(3), 227–244. https://doi.org/10.1108/JIBR-10-2015-0112

- McKinsey. (2016), “Customer experience: Creating value through transforming customer journeys”, available at: www.mckinsey.com/business-functions/marketing-and-sales/our-insights/customerexperience-creating-value-through-transforming-customer-journeys (Retrieved August 9, 2020).

- McKnight, D. H., Cummings, L. L., & Chervany, N. L. (1998). Initial trust formation in new organizational relationship. Academy of Management Review, 23(3), 472–490. https://doi.org/10.2307/259290

- Methlie, L. B. & Nysveen, H.(1999). Loyalty of on-line bank customers. Journal of Information Technology, 14, 375–386.

- Mittal, V. & Kamakura, W. A.(2001). Satisfaction, repurchase intent, and repurchase behavior: Investigating the moderating effect of customer characteristics. Journal of Marketing Research, 38(1), 131–142.

- Mombeuil, C.(2020). An exploratory investigation of factors affecting and best predicting the renewed adoption of mobile wallets. Journal of Retailing & Consumer Services, 55(102127), 1–9.

- Mombeuil, C., & Uhde, H. (2021). Relative convenience, relative advantage, perceived security, perceived privacy, and continuous use intention of China’s WeChat pay: A mixed-method two-phase design study. Journal of Retailing & Consumer Services, 59, 1–10. https://doi.org/10.1016/j.jretconser.2020.102384

- Moriuchi, E., & Takahashi, I. (2022). The role of perceived value, trust and engagement in the C2C online secondary marketplace. Journal of Business Research, 148, 76–88. https://doi.org/10.1016/j.jbusres.2022.04.029

- Ndubisi, N. O. (2007). Relationship quality antecedents: The Malaysian Retail banking perspective International. International Journal of Quality & Reliability Management, 24(8), 829–845. https://doi.org/10.1108/02656710710817117

- Pal, A. De’, R. & Herath, T.(2020). The role of mobile payment technology in sustainable and human-centric development: Evidence from the post-demonetization period in India. Information Systems Frontiers, 22, 607–631.

- Palmatier, R. W., Dant, R. P., Grewal, D., & Evans, K. R. (2006). Factors influencing the effectiveness of relationship marketing: A meta-analysis. Journal of Marketing, 70(4), 136–153. https://doi.org/10.1509/jmkg.70.4.136

- Podsakoff, P. M., MacKenzie, S. B., Lee, J. Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 88(5), 879. https://doi.org/10.1037/0021-9010.88.5.879

- Prasad Yadav, M. & Arora, M.(2019). Study on impact on customer satisfaction for E-wallet using path analysis model. International Journal of Information Systems & Management Science, 2(1).

- Prasetya, M. E., & Shuhidan, S. M. (2023). Security, risk and trust in e-wallet payment systems: Empirical evidence from Indonesia. Management & Accounting Review (MAR), 22(1), 353–378.

- Pura, M.(2005). Linking perceived value and loyalty in location‐based mobile services. Managing Service Quality: An International Journal, 15(6), 509–538.

- Purwanto, E. Deviny, J. & Mutahar, A. M.(2020). The mediating role of trust in the relationship between corporate image, security, word of mouth and loyalty in M-banking using among the millennial generation in Indonesia. Management & Marketing. Challenges for the Knowledge Society, 15(2), 255–274.

- Putri, E., Praswati, A. N., Muna, N., & Sari, N. P. (2022). E-Finance transformation: A study of M-Wallet adoption in Indonesia. Jurnal Ekonomi Pembangunan: Kajian Masalah Ekonomi dan Pembangunan, 23(1), 123–134. https://doi.org/10.23917/jep.v23i1.15469

- Rahi, S. Yasin, N. M. & Alnaser, F. M.(2017). Measuring the role of website design, assurance, customer service and brand image towards customer loyalty and intention to adopt internet banking. Journal of Internet Banking and Commerce, 22(08), 1–18.

- Reichheld, F. F., & Schefter, P. (2000). E-loyalty: Your secret weapon on the web. Harvard Business Review, 78(4), 105–113.

- Rigdon, E. E. Sarstedt, M. & Ringle, C. M.(2017). On comparing results from CB-SEM and PLS-SEM: Five perspectives and five recommendations. Marketing: ZFP–Journal of Research and Management, 39(3), 4–16.

- Rusbult, C. (1983). A longitudinal test of the investment model: The development (and deterioration) of satisfaction and commitment in heterosexual involvements. Journal of Personality & Social Psychology, 45(1), 101–117. https://doi.org/10.1037/0022-3514.45.1.101

- Rusbult, C., Agnew, C., & Arriaga, X. (2012). The investment model of commitment processes. In P. A. M. Van Lange, A. W. Kruglanski, & T. Higgins (Eds.), Handbook of theories of social psychology (Vol. II, pp. 218–231). Sage Publications.

- Salem Khalifa, A.(2004). Customer value: A review of recent literature and an integrative configuration. Management Decision, 42(5), 645–666.

- Sánchez-Fernández, R., & Iniesta-Bonillo, M. A. (2007). The concept of perceived value: a systematic review of the research. Marketing Theory, 7(4), 427–451. https://doi.org/10.1177/1470593107083165

- Senić, V. & Marinković, V.(2014). Examining the effect of different components of customer value on attitudinal loyalty and behavioral intentions. International Journal of Quality & Service Sciences, 6(2/3), 134–142.

- Sharifi, S. S., & Esfidani, M. R. (2014). The impacts of relationship marketing on cognitive dissonance, satisfaction, and loyalty: The mediating role of trust and cognitive dissonance. International Journal of Retail & Distribution Management, 42(6), 553–575. https://doi.org/10.1108/IJRDM-05-2013-0109

- Sharma, G. & Kulshreshtha, K.(2019). Mobile wallet adoption in India: An analysis. The IUP Journal of Bank Management, 18(1), 7–26.

- Shaw, N. (2014). The mediating influence of trust in the adoption of the mobile wallet. Journal of Retailing and Consumer Services, 21(4), 449–459. https://doi.org/10.1016/j.jretconser.2014.03.008

- Shaw, B., & Kesharwani, A. (2019). Moderating effect of smartphone addiction on mobile wallet payment adoption. Journal of Internet Commerce, 18(3), 291–309. https://doi.org/10.1080/15332861.2019.1620045

- Shergill, G. S., & Li, B. (2005). Internet banking–an empirical investigation of a trust and loyalty model for New Zealand banks. Journal of Internet Commerce, 4(4), 101–118. https://doi.org/10.1300/J179v04n04_07

- Shin, D. H. (2009). Towards an understanding of the consumer acceptance of mobile wallet. Computers in Human Behavior, 25(6), 1343–1354. https://doi.org/10.1016/j.chb.2009.06.001

- Singh, N. Srivastava, S. & Sinha, N.(2017). Consumer preference and satisfaction of M-wallets: A study on North Indian consumers. International Journal of Bank Marketing, 35(6), 944–965.

- Singh, N., & Sinha, N. (2020). How perceived trust mediates merchant’s intention to use a mobile wallet technology. Journal of Retailing & Consumer Services, 52, 1–13. https://doi.org/10.1016/j.jretconser.2019.101894