Abstract

The author, a lecturer in Accounting at Pasim National University, completed her undergraduate studies at Telkom University Bandung (2014) and holds a Master's degree in Accounting from Unpad Bandung (2018). She is currently pursuing a Doctorate in Accounting at Airlangga University Surabaya (2023). With expertise in management accounting and financial management, she writes extensively in Sinta and Scopus-accredited journals, focusing on financial management, performance, and reporting.

PUBLIC INTEREST STATEMENT

This study explores the factors influencing the performance of State-Owned Enterprises (SOEs) in Indonesia with regard to environmentally sustainable economic development. The findings shed light on the significant roles played by key elements such as Institutional Ownership, the Board of Commissioners, and the Audit Committee in steering these entities towards eco-friendly economic growth. Notably, while Managerial Ownership’s impact remains non-significant, the involvement of institutional investors and vigilant governance bodies significantly contributes to enhancing Green Economy Performance (GEP). This research highlights the need for robust governance structures and policies to align business strategies with sustainability goals, ultimately promoting green economic performance and environmental conservation efforts in Indonesia. It underscores the immediate necessity for effective regulations and policies to foster ecologically responsible economic development in the nation’s SOEs.

1. Introduction

Indonesia is home to several State-Owned Enterprises (SOEs) whose capital is either fully or predominantly owned by the State or Government through direct investment from separated state assets. Pursuant to Law No. 19 of 2003 on State-Owned Enterprises, these enterprises are collectively referred to as State-Owned Enterprises (SOEs). The Board of Directors holds the responsibility for managing all activities within the SOEs, representing them in legal proceedings, and ensuring their compliance with budgetary, legal, and regulatory requirements. On the other hand, the Board of Commissioners and Supervisory Board are mandated to supervise the SOEs, ensuring that their interests and objectives are aligned. They are required to abide by the Articles of Association of the SOEs, along with applicable laws and regulations, and are expected to adhere to the principles of professionalism, efficiency, transparency, independence, accountability, responsibility, and fairness.

In the context under consideration, State-Owned Enterprises (SOEs) bear not only the responsibility of generating specific profits for the State or Government but also the mandate of fostering sustainable enterprises with a pronounced environmental focus (Ministry of SOE, Citation2018; OJK, Citation2022). The concept of the green economy assumes paramount significance in this context. The green economy delineates an economic paradigm that accentuates environmental sustainability, optimal resource utilization, and the mitigation of deleterious impacts on the natural world. In the context of the earlier discourse on SOEs’ corporate governance, this green economy paradigm gains escalating relevance as it mirrors the consciousness and accountability of government-owned enterprises in their pursuit of sustainable ventures that serve the greater good of the nation and society.

The heterogeneous array of SOEs in Indonesia thus finds itself vested with a substantial role and responsibility in adopting the tenets of the green economy. This adoption encompasses a dedicated emphasis on principles such as transparency, accountability, judicious exploitation of natural resources, sustainable innovations for environmental preservation, and the discharge of corporate social responsibility. This situation is intricately linked with the prevailing global environmental crises faced by Indonesia, akin to other nations, including challenges like climate change, pollution, waste management, resource depletion, and an array of related issues. The government’s role and commitment in addressing these challenges will be subjected to rigorous scrutiny, contingent upon their resolve to operate businesses that place heightened emphasis on environmental sustainability and responsible resource stewardship. When SOEs successfully integrate the principles of the green economy into their corporate governance, they contribute significantly to the advancement of sustainable economic growth and the amelioration of adverse environmental impacts (USAID, Citation2018; World Bank Group, Citation2021). This harmonizes with Indonesia’s vision of sustainable development.

Nevertheless, within an economic landscape characterized by feeble governance mechanisms, including the market of corporate control, external audit oversight, rating agencies, and institutional frameworks (pertaining to legal systems and financial institutions), supplementary factors assume paramount importance in sustaining these green economic commitments. Ownership structure, in this context, emerges as a pivotal governance mechanism for mitigating agency problems. This proposition rests upon the premise that the legal framework in Indonesia is yet to attain robustness, particularly in combating the endemic issue of corruption within the realm of SOEs at various echelons. Consequently, the composition of ownership structure serves as an efficacious tool for the oversight and supervision of SOEs, facilitating the selection of capable agents or company boards for their governance. Research conducted by Budiarti and Sulistyowati (Citation2014) and Munisi et al. (Citation2014) corroborates this assertion by elucidating the multifaceted motivations underlying ownership structures’ role in monitoring corporate affairs, management, and board structures.

The corporate board structure is shaped by the interests of various stakeholders, including owners or investors. Different owners may exhibit diverse characteristics of behavior and preferences for corporate governance that tend to influence the board structure of the company (Arora & Singh, Citation2023; Mak & Li, Citation2001; Munisi et al., Citation2014). In Indonesia, the corporate board structure adheres to a two-tier system consisting of a management board and a supervisory board. Shareholders appoint a group of company operations managers as well as supervisors and management advisors called commissioners, who are responsible and appointed or dismissed by the General Meeting of Shareholders (GMS). The board of directors, board of commissioners, and an independent commissioner who monitors the company independently and has no relationship with the company and shareholders make up the board structure of the company in Indonesia (FSA, Citation2014; IFC, Citation2014). In a more intricate context, as demonstrated in the study by Al-Jaifi et al. (Citation2023), the level of environmental performance is positively correlated with age and gender board diversity and inversely related to tenure board diversity.

Shareholders or owners aim to ensure the company’s survival and sustainability in the competitive industry while avoiding high agency problems. Therefore, shareholders choose agents who can manage the company with good governance. The board structure of a company is a good supervisory tool for shareholders. The board plays a crucial role in monitoring management compliance with relevant standards and preventing fraudulent practices and other issues (IFC, Citation2014). The ownership structure is categorized into four types: foreign ownership, managerial ownership, institutional ownership, and government ownership. Shareholders, or principals, hire other individuals or managers, or agents, to manage the company, which creates a principal-agent relationship. However, the principal-agent relationship can lead to agency problems within the company. High agency problems are prevalent in companies or countries with uncertain characteristics such as high industrial growth, emerging markets, and developing countries (Laiho, Citation2011; Munisi et al., Citation2014; Xu, Citation2016).

The structure of ownership and the composition of the board of commissioners play a pivotal role with far-reaching implications for corporate management and its dedication to embracing the principles of the green economy, a matter that extends to State-Owned Enterprises (SOEs) in Indonesia. In a more comprehensive perspective, managerial ownership has been demonstrated to have repercussions on the sustainability and overall performance of companies across diverse dimensions (Harianto & Isbanah, Citation2021; Junias et al., Citation2020; Mueller & Spitz-Oener, Citation2019; Munisi et al., Citation2014; Yamashita, Citation2020). In this intricate context, given the complexity of the principal-agent relationship within the ambit of ownership and corporate management, various other factors come into play and exert their influence on the performance of the green economy, with a notable emphasis on the presence and attributes of an audit committee. The study conducted by Waheed et al. (Citation2021) demonstrates that corporate governance mechanisms have an impact on the sustainability of the corporate social responsibility (CSR) and firm’s performance nexus. It also confirms the agency role of effective corporate governance mechanisms in the sustainable CSR and firm performance relationship.

In a study conducted by Bilal et al. (Citation2017), the composition of the audit committee emerges as a critical determinant of its effective functioning, notably in relation to its impact on earnings quality. However, the empirical evidence on this matter presents mixed results. The research posits that companies featuring financial experts on their audit committees tend to exhibit higher earnings quality. A meta-analysis of existing research has demonstrated a negative correlation between financial expertise and earnings management (Bilal et al., Citation2017). The final rule issued by the SEC to implement sections 406 and 407 of the Sarbanes-Oxley Act of 2002 mandates that the appointed individual should possess attributes highly pertinent to the role of an audit committee, often referred to as the “audit committee financial expert.” Another significant study by Ha (Citation2022) in this context indicates that audit committee independence and the size of the audit committee are significantly associated with the level of corporate governance disclosure (CGD). Effective corporate governance, as demonstrated by audit committee independence and size, plays a crucial role in ensuring transparency and accountability within companies. This, in turn, can positively impact the green economy performance of these companies by fostering responsible and sustainable practices, such as environmentally friendly initiatives and resource management (Elmghaamez et al., Citation2023; Karikari et al., Citation2022).

The examination of the influence of these factors within the context of green economy performance in the realm of SOEs in Indonesia assumes paramount significance, particularly as Indonesia embarks on a path of recovery following the challenges posed by the COVID-19 pandemic. The pandemic has ushered in socio-economic disruptions and exacerbated the looming threat of climate change in Indonesia. Consequently, the focus on environmental concerns and the performance of the green economy becomes especially timely. This juncture marks a transition from a carbon-intensive “black” economy to a green economy that champions renewable energy sources. This transformation aligns with the vision articulated by the President of Indonesia, Joko Widodo, who asserts that a green economy can be realized through the adept utilization of digital innovation and technology, ultimately paving the way for a sustainable economy. However, the attainment of a green economy necessitates substantial investments and financing to fortify Indonesia’s journey towards sustainability, as underlined by a body of research (Gielen et al., Citation2019; Li et al., Citation2022; Lowitzsch et al., Citation2020; Vakulchuk et al., Citation2020).

Mealy and Teytelboym (Citation2022) conducted a comprehensive study focusing on the green economy, wherein countries were ranked based on their competitiveness in exporting complex green products. To investigate this matter, the authors made use of an extensive dataset comprising traded green products and employed economic complexity methodologies. The outcomes of their research reveal that countries with higher rankings exhibit elevated rates of environmental patenting, reduced CO2 emissions, and more stringent environmental regulations. Remarkably, these trends persist even after adjusting for per capita GDP.

In a separate investigation, Mikhno et al. (Citation2021) delved into the necessity for market systems to account for negative externalities stemming from anthropogenic influences and environmental degradation associated with the expansion of industrial production. The authors put forward effective indices and instruments aimed at influencing both ecological and economic development. Their study also underscored the value of metrics that incorporate negative externalities, such as the Pigouvian tax. Furthermore, the research indicated that extensive economic development correlates with substantial decreases in per capita GDP levels. These findings emphasize the feasibility of implementing a green economy by European companies as part of a strategy aimed at mitigating environmental risks during the process of economic growth.

Furthermore, a study by Chariri et al. (Citation2017) illuminated a positive association between the audit committee and environmental performance. This finding aligns with the research conducted by Fauzyyah and Rachmawati (Citation2018), which identified a positive influence of the board of commissioners on CSR disclosure. Moreover, ownership structure emerged as a factor impacting CSR disclosure, with the audit committee exerting a positive influence on this aspect. In their investigation (2018), Fauzzyah and Rachmawati discerned a significant positive effect of the board of commissioners on CSR disclosure within SOEs listed on the Indonesia Stock Exchange. Additionally, they documented a substantial positive correlation between the audit committee and CSR disclosure.

Nevertheless, prior research on the performance of the green economy concerning the management of SOEs in Indonesia, particularly pertaining to the factors influencing this green economy performance, has been conspicuously absent. Consequently, the present study endeavors to contribute a distinct analytical perspective compared to previous research, with a particular focus on the green economy’s performance within the milieu of SOEs in Indonesia and the factors that exert influence upon it. In greater detail, the study seeks to scrutinize the impact of managerial ownership, institutional ownership, the audit committee, and the board of commissioners within 20 SOEs listed on the Indonesia Stock Exchange spanning the period from 2018 to 2021. The novelty inherent in this study lies in its examination of the multifaceted factors affecting green economy performance within the context of SOEs, which serve as a reflection of the government’s commitment to environmental sustainability within the economic sphere.

2. Background

The rationale for conducting this study is deeply rooted in the specific context of regulatory, reform, and policy issues and developments within the research setting. In order to provide a comprehensive understanding of the research’s appropriateness, this section will delve into these contextual factors, which underpin the significance of the study.

The research context in question is the domain of State-Owned Enterprises (SOEs) in Indonesia. SOEs, as defined by Law No. 19 of 2003, encompass enterprises whose capital is predominantly owned by the State or Government, and they play a pivotal role in the nation’s economic landscape. These entities are responsible for a multitude of functions, including generating profits for the State, upholding budgetary and legal compliance, and contributing to the nation’s welfare. The governance of SOEs is divided between the Board of Directors, tasked with managing their activities, and the Board of Commissioners and Supervisory Board, which oversee the interests and objectives of the SOEs.

Regulatory and policy issues are paramount in this context. Law No. 19 of 2003 provides the legal framework for the governance and operations of SOEs. This legal framework delineates the roles and responsibilities of various governing bodies within the SOEs, ensuring their compliance with budgetary, legal, and regulatory requirements. Additionally, these entities are mandated to adhere to the principles of professionalism, efficiency, transparency, independence, accountability, responsibility, and fairness. The regulatory framework, therefore, serves as the bedrock on which the governance of SOEs is established.

In recent years, Indonesia has embarked on reform programs aimed at enhancing the governance and performance of SOEs. These reforms have sought to promote transparency, efficiency, and sustainability in the operations of SOEs. Notably, the green economy has gained significance as part of these reform efforts, reflecting the country’s commitment to environmental sustainability and responsible resource management. The appropriateness of conducting this study is firmly rooted in the context of regulatory frameworks, reform initiatives, and policy developments within the realm of SOEs in Indonesia. These factors highlight the significance of exploring the governance structures and mechanisms within SOEs, particularly in the context of their commitment to the green economy. This sets the stage for a comprehensive examination of the factors that influence the green economy performance in SOEs, providing valuable insights into their role in Indonesia’s sustainable development journey.

3. Literature review and hypotheses development

3.1. Agency Theory

The Agency Theory is a relevant framework for analyzing the impact of managerial ownership, institutional ownership, audit committees, and boards of commissioners on green economy performance within the context of State-Owned Enterprises (SOEs). This theory provides the foundation for understanding the relationship between shareholders (principals) and corporate management (agents) and how these factors influence management behavior and decisions. In the context of the Agency Theory, shareholders act as principals who employ management to run the company. Shareholders have the duty to ensure that management acts to achieve their objectives. In the case of government-owned or state-owned enterprises like SOEs, the shareholders are the government or institutions representing public interests. Managerial ownership refers to shares owned by the company’s management, including the CEO and other top executives, while institutional ownership encompasses shares held by financial institutions such as pension funds, investment funds, or insurance companies. Additionally, audit committees and boards of commissioners, as integral parts of corporate governance, are responsible for overseeing and controlling corporate management (Jensen & Meckling, Citation1976; Zogning, Citation2017).

3.1.1. Corporate Governance Theory

The second theory employed in this research is the Corporate Governance Theory, which deals with how a company is structured and supervised by boards of commissioners and audit committees. This theory centers on the relationship between shareholders, boards of commissioners, corporate management, and relevant parties involved in company management. Within the framework of the Corporate Governance Theory, boards of commissioners are accountable for overseeing and providing guidance to corporate management. They must ensure that the company adheres to sound governance practices and complies with applicable laws and regulations. Audit committees play a crucial role in ensuring accountability and transparency in financial reporting and corporate governance (Beasley, Citation1996; Monks & Minow, Citation2011; Tricker, Citation2015).

In the context of green economy performance, both the Agency Theory and Corporate Governance Theory can help understand the influence of ownership structures, boards of commissioners, and audit committees as stakeholders in a company regarding the company’s commitment to green economy performance. In the context of green economy performance, for instance, the Agency Theory can shed light on how managerial and institutional ownership may affect a company’s practices and policies related to green economics. For example, managerial shareholders may have different incentives for adopting sustainable practices compared to institutional shareholders. Meanwhile, within the Corporate Governance Theory, the roles of boards of commissioners and audit committees in overseeing and guiding the company toward sustainable practices are crucial. They can ensure that the company complies with environmental guidelines and motivates management to adopt green economic (Chairina & Tjahjadi, Citation2023).

The green economy itself is an idea that aims to improve social welfare without harming the environment. Its program involves community empowerment and plays a crucial role in responding to three challenges for sustainable development: environmental, social, and economic. The theory of the green economy concept comes from environmental economics and economic ecology (Georgeson et al., Citation2017; Loiseau et al., Citation2016). The concept has six main topics discussed in a specific sequence, namely sustainable development, green investment in urban areas, tourism, business, education, and human resources, renewable energy production, product cycle, and conservation. All the topics mentioned relate to the business world in general. The green economy concept encompasses all ecological processes beyond just resource management, and it surpasses other concepts like circular economy (CE) and bioeconomics (D’Amato et al., Citation2017).

The performance indicator of the green economy in this study is based on Iavicoli’s et al. (Citation2014) green economy indicators, which comprise the following criteria: (1) It serves as a means to achieve sustainable development; (2) It generates decent work and green jobs; (3) It improves governance and the rule of law by promoting inclusivity, democracy, participation, accountability, transparency, and stability; (4) It promotes equity, fairness, and justice between and within countries and across generations; (5) It reduces poverty and enhances well-being, livelihoods, social protection, and access to essential services; (6) It safeguards biodiversity and ecosystems; (7) It maximizes resource and energy efficiency; (8) It observes planetary boundaries, ecological limits, and scarcity; (9) It utilizes integrated decision-making processes; (10) It internalizes externalities; (11) It measures beyond gross domestic product indicators and metrics.

Based on the constructs of agency theory and corporate governance theory, managerial ownership refers to the ownership of shares by a company’s management, expressed as a percentage of the total number of shares held by management. The extent of managerial share ownership in a company can signify a mutual interest between the management and the shareholders (Munisi et al., Citation2014). When managers possess shares in a company, they tend to act in the shareholders’ best interests, given the alignment of interests and a shared commitment to the company. This alignment can aid in mitigating agency problems (Jensen & Meckling, Citation1976). In this study, managerial ownership is quantified as the overall percentage of shares owned by the company’s management. As outlined by Fauzyyah and Rachmawati (Citation2018), information regarding managerial ownership can be located in the financial reports’ notes to the financial statements (CALK) of a company.

The study conducted by Sukhani and Hanif (Citation2023), for example, indicates that managerial ownership and the presence of independent boards of commissioners have a positive and significant influence on corporate social responsibility within the context of environmental performance. In a broader context, managerial ownership has also been shown to impact the sustainability and overall performance of companies in various aspects (Junias et al., Citation2020, Isbanah, 2021; Munisi et al., Citation2014; Mueller & Spitz-Oener, Citation2019; Yamashita, Citation2020).

Drawing from prior research on the correlation between managerial ownership and either company performance or green economy performance, it can be postulated that managerial ownership similarly exerts a positive influence on the performance of companies engaged in green economy activities. Companies operating in the green economy sector prioritize sustainability and environmentally-friendly practices, which suggests that managers who hold shares in these companies are likely dedicated to these values. Consequently, they are inclined to make decisions aligned with the company’s objectives and values, which can result in enhanced performance and positive outcomes for both the company and the environment. Thus, it can be hypothesized that managerial ownership positively affects the performance of companies in the green economy.

H1:

Managerial ownership has a positive significant effect on the performance of companies in the green economy

The concept of institutional ownership involves the ownership of shares in a company by institutions such as banks, insurance companies, and investment firms, rather than individuals. This ownership structure can be a useful mechanism for mitigating agency conflicts between a company’s owners and managers. By having a large institutional investor as a shareholder, it can encourage management to act in the best interest of all shareholders, not just themselves. Additionally, institutional investors may use their influence to encourage improved corporate governance and sustainability practices. Studies have shown that higher levels of institutional ownership are associated with better financial performance and reduced risk, making it a valuable component of a company’s ownership structure (Bhagat & Bolton, Citation2008).

Previous studies have indicated that institutional ownership can exert a substantial influence on the performance of companies in the green economy (Sánchez et al., Citation2020; Velte, Citation2020; Waheed et al., Citation2021). Institutional ownership, in the context of the green economy, may play a pivotal role in determining the trajectory and success of firms operating in this sector. Institutions that specialize in sustainable investments may demonstrate a greater propensity to invest in green economy companies, thereby expanding their access to capital and resources. Moreover, institutional investors may bring their expertise and knowledge to bear, providing critical guidance and support to firms in the green economy. Consequently, it is reasonable to posit that institutional ownership has a favorable impact on the performance of companies in the green economy.

H2:

Institutional ownership has a positive significant effect on the performance of companies in the green economy

The board of commissioners plays a vital role in the governance of a company, primarily overseeing the quality of financial statements and accessing relevant company information. The board of directors is responsible for providing information to the board of commissioners, and the latter is accountable for supervising and advising the board of directors. The board of commissioners ensures that the company upholds social responsibility and considers the interests of all corporate stakeholders impartially when monitoring the effectiveness of implementing good corporate governance.

Given the role of the board of commissioners in monitoring the quality of financial information and providing oversight to the board of directors, it can be hypothesized that the board of commissioners also plays a significant role in the performance of companies in the green economy (Al-Jaifi et al., Citation2023; Hermanto & Berutu, Citation2022; Potharla et al., Citation2021; Putra et al., Citation2020). In the green economy, companies are often required to adhere to strict environmental regulations and social responsibility standards, which may be more effectively monitored by a board of commissioners that is focused on these issues. A board of commissioners that is committed to good corporate governance and stakeholder engagement may be better able to ensure that a company is operating in a socially responsible manner and taking into account the interests of all stakeholders. Therefore, it can be hypothesized that the board of commissioners has a positive effect on the performance of companies in the green economy.

H3:

The Board of Commissioners have a positive significant effect on the performance of companies in the green economy

The audit committee serves as a supporter to the board of commissioners in fulfilling their duties as protectors against management fraud towards external parties. It acts as a mediator between the company’s management and the board of commissioners, reporting its findings from its supervisory role over the management’s activities towards business development. This is necessary to ensure that the findings from the audit committee’s supervisory actions are objective and reflective of the actual situation, encouraging the management to improve their efforts in aligning their business operations with the company’s values. The objectivity and fairness of the audit committee towards all stakeholders involved in the company’s affairs can be achieved through the establishment of an independent audit committee (Al-Jalahma, Citation2022).

Given the important role of the audit committee in supporting the board of commissioners in fulfilling their duties and providing objective oversight to the management of the company, it can be hypothesized that the presence of an independent audit committee is positively associated with the performance of companies in the green economy (Albawwat et al., Citation2020; Alqatamin, Citation2018; Ha, Citation2022). An independent audit committee is necessary to ensure that the findings from the committee’s supervisory actions are objective and reflective of the actual situation, and that the committee is fair towards all stakeholders involved in the company’s affairs. In the context of the green economy, this could be particularly important, as companies may face complex environmental regulations and stakeholder expectations that require objective oversight to ensure compliance and sustainability. Therefore, it can be hypothesized that the presence of an independent audit committee is positively associated with the performance of companies in the green economy.

H4.

The audit committee has a positive significant effect on the performance of companies in the green economy

4. Methods

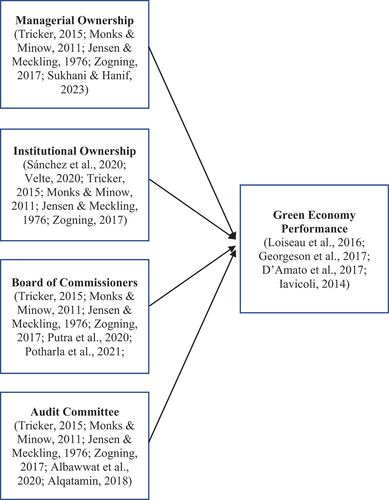

This study utilizes a quantitative research approach, employing secondary panel data. The data is drawn from state-owned enterprises (SOEs) listed on the Indonesia Stock Exchange over three consecutive years. The study’s variables are categorized into dependent and independent variables. The dependent variable in this study is Green Economy Performance (GEP). While independent variables are Managerial Ownership (MO), Institutional Ownership (IO), Board of Commissioners (BoC), and Audit Committee (AC).

The conceptual framework that serves as a reference for this study can be seen in the theoretical framework presented in Figure .

Figure 1. Theoretical framework of the study.

The author employs two panel data regression models to analyze the data. The first model used is the Fixed Effect Model (FEM), which allows for different intercepts for each company but the same regression slope. This model employs dummy variables to capture differences in intercepts. The second model is the Random Effect Model (REM), which assumes that each variable has a different random intercept and uses residuals that have a relationship between time and between companies. The models are estimated using panel data, which is a combination of cross-sectional data and time series data. The panel data is processed using Stata, a statistical software package commonly used for econometric analysis.

The research data utilized in this study were gathered from the financial statements of publicly traded State-Owned Enterprises (SOEs) listed on the Indonesia Stock Exchange from 2018 to 2021. The study population comprises all publicly listed State-Owned Enterprises on the Indonesia Stock Exchange that annually publish their financial statements, as shown in Table below.

Table 1. Listed company on the Indonesia Stock Exchange 2018–2021

4.1. Selection of panel data regression estimation technique

The selection of the panel data regression model estimation technique necessitates the implementation of various statistical tests to determine the model that best fits the dataset under analysis. In this study, two tests were employed to determine the most suitable model for the dataset: the Chow test and the Hausman test.

The results of the statistical tests pertaining to the data analysis model are displayed in the subsequent table:

Based on the outcomes of the tests as exhibited in Table , this study adopts the Random Effect Model as the appropriate model for data analysis. The selection of the Random Effect Model was made following model selection employing both the Chow test and the Hausman test. The Chow test yielded a probability value of 0.0000, suggesting the Fixed Effect Model as the more appropriate choice. Conversely, the Hausman test returned a probability value of 0.3311, leading to the selection of the Random Effect Model. In this study, the Random Effect Model was deemed the most suitable model for data analysis.

Table 2. Result of Chow test and Hausman test

The multiple linear regression equation utilized in this study is expressed as:

GEP = α + β1MOit + β2IOit + β3BoCit + β4ACit + ε

where:

GEP denotes Green Economy Performance.MOit signifies Managerial Ownership within company i during year t.IOit represents Institutional Ownership within company i during year t.BoCit designates the Board of Commissioners of company i during year t.ACit signifies the Audit Committee of company i during year t.α symbolizes the Constant.β1, β2, β3, and β4 denote the regression coefficients associated with each respective variable.ε represents the error term.

Hypothesis testing was conducted in accordance with the selected data analysis model, which is the Random Effect Model. Additionally, the researcher conducted supplementary analysis employing the Robustness Check (Two-step System GMM), considering the following factors: (1) The ability of GMM to estimate dynamic panel data; (2) GMM’s capacity to address issues of endogeneity, omitted variable bias, and unobserved panel heterogeneity; (3) The presence of a larger number of cross-section groups compared to the time span; and (4) The number of instruments being smaller or equal to the number of groups.

5. Empirical results

This study delves into the impact of ownership structure, institutional ownership, the board of commissioners, and the audit committee on the performance of the green economy within publicly listed State-owned Enterprises (SOEs) on the Indonesia Stock Exchange from 2018 to 2021. Employing a purposive sampling method, we meticulously selected 20 consistently listed companies, yielding a sample size of 80 observations. Research hypotheses were rigorously examined through Random Effect Model.

5.1. Results of descriptive statistics

Descriptive statistics provide an overview of the research data, both in a general sense and across different years. These statistics offer a general perspective on the data used in the study, as seen in Tables below.

Table 3. Statistic Descriptive

Table 4. Descriptive statistics (by year)

The descriptive statistics presented in Table provide a summary of key variables in the research dataset. These statistics give insights into the central tendencies, variability, and range of the data. Here’s a brief interpretation of the findings:

GEP (Green Performance Economy) has a mean value of approximately 0.629, with a standard deviation of 0.282. This suggests that the data on green performance varies, with a range from 0 to 0.91.

MO (Managerial Ownership) has a mean value of about 0.013 and a standard deviation of 0.051. The data ranges from 0 to 0.25.

IO (Institutional Ownership) has a mean of roughly 0.203, with a standard deviation of 0.223. The data varies from 0 to 0.88.

BoC (Board of Commissioners) has an average of 0.434 and a standard deviation of 0.142, with values ranging from 0.14 to 0.75.

AC (Audit Committee) has a mean of approximately 0.397, with a standard deviation of 0.108. The data ranges from 0.2 to 0.72.

Leverage ranges from 1.22 to 93.86, with a mean of 48.749 and a standard deviation of 21.717.

Firmage varies from 20 to 126, with a mean of 65.4 and a standard deviation of 26.619.

Size has a mean of 32.115 and a standard deviation of 1.74, with data ranging from 27.956 to 35.015.

Additionally, the Table provides a breakdown of these statistics by year, which can help identify trends or variations over time. GEP remained relatively stable from 2018 to 2021 but showed a decrease in 2021, while other variables also exhibited some changes over the years. From 2018 to 2021, the measurement of Managerial Ownership (MO) exhibited a consistently low range, fluctuating between 0.013 and 0.024. This range underscores the presence of minimal managerial ownership within the corporate entity during this period. However, a noteworthy decline became evident in 2021 when MO reached an exceptionally low value of 0.002, which plausibly indicates a significant reduction in managerial ownership. In 2018, the metric for Institutional Ownership (IO) reflected an average value of 0.154, unequivocally substantiating the existence of institutional ownership within the corporate structure. Subsequently, in 2020, IO demonstrated a discernible increase to 0.186, suggesting a heightened level of institutional participation in the realm of ownership. The apex of this trend materialized in 2021, with IO attaining its zenith at an average value of 0.323. This ascent unequivocally signifies a substantial upswing in institutional ownership.

Board of Commissioners (BoC) in 2018 reported an average of 0.369, delineating a substantial and influential composition of the board of commissioners within the corporate framework. Remarkably, from 2019 to 2021, BoC displayed commendable stability, maintaining a persistent and elevated level of board of commissioners’ participation, consistently surpassing the 0.43 threshold. Simultaneously, during the period spanning from 2018 to 2021, the Audit Committee (AC) remained notably steadfast, with averages oscillating between approximately 0.359 and 0.436. This unfluctuating trajectory underscores the robust sustainability and continuity of the company’s audit committee during the years under consideration.

5.2. Results of hypothesis test

Given the Random Effect Model as the selected analytical framework, this research is inherently free from classical assumptions. The Random Effect Model employs the Generalized Least Square (GLS) estimation method, which fundamentally conforms to the classical assumptions as elucidated by Gujarati (Citation2003). Nevertheless, a comprehensive examination of multicollinearity concerns was undertaken by means of the Pearson correlation method, with the objective of determining the existence of such issues within the research model. The outcomes of this meticulous multicollinearity analysis are meticulously detailed in Table below.

Table 5. Pearson correlation test results

In light of the extensive assessment, it is unequivocally evident that none of the correlation coefficients exceeded the threshold of 0.80, thus conclusively signifying that multicollinearity did not manifest as a notable concern within the context of this study.

The examination of the data through the utilization of the Random Effect Model, the selected analytical framework, has provided statistical outcomes, as delineated in Table presented subsequently.

Table 6. Main results

The statistical results, as presented in Table , provide valuable insights into the relationship between key variables and Green Economy Performance (GEP). The analysis yields the following key findings:

Managerial Ownership (MO)Managerial Ownership (MO) exhibits a positive but statistically non-significant relationship with GEP, as indicated by the coefficient of 0.040 (t-statistic = 1.150). This suggests that while there is a positive association between Managerial Ownership (MO) and Green Economy Performance (GEP), it is not significant at the conventional levels of significance.

Institutional Ownership (IO)Institutional Ownership (IO), on the other hand, demonstrates a statistically significant positive impact on GEP, with a coefficient of 0.074 (t-statistic = 1.650) at the 10% level of significance. This implies that Institutional Ownership (IO) has a noteworthy positive influence on Green Economy Performance (GEP), and the relationship is statistically significant.

Board of Commissioners (BoC)The Board of Commissioners (BoC) exhibits a statistically significant positive effect on Green Economy Performance (GEP), with a coefficient of 0.106 (t-statistic = 1.830) at the 10% level of significance. This implies that the presence and composition of the Board of Commissioners play a significant role in enhancing Green Economy Performance (GEP).

Audit Committee (AC)Audit Committee (AC) also displays a statistically significant positive impact on Green Economy Performance (GEP), with a coefficient of 0.070 (t-statistic = 1.870) at the 10% level of significance. This suggests that the presence and activities of the Audit Committee (AC) significantly contribute to improving Green Economy Performance (GEP).

The model’s explanatory power is reflected in the R-squared values, which range from 0.507 to 0.557, indicating a moderate to strong fit of the model. Furthermore, the presence of both Year and Industry Effects highlights the consideration of temporal and industry-specific variations in the analysis. These findings indicate that while Managerial Ownership (MO) does not exhibit a statistically significant effect on Green Economy Performance (GEP), its direction is positive. On the other hand, Institutional Ownership (IO), Board of Commissioners (BoC), and the Audit Committee (AC) demonstrate statistically significant positive influences on Green Economy Performance (GEP), emphasizing their significance in promoting green economic performance. These findings provide crucial insights for further research and policymaking in the context of green economy initiatives.

The robustness of these findings is bolstered by the results obtained through a Robustness Check employing the Two-Step System GMM, which is presented in the subsequent table:

The results of the Robustness Check (Two-Step System GMM) presented in Table offer additional insights into the relationship between key variables and Green Economy Performance (GEP). The key findings from this analysis are as follows:

Lagged Green Economy Performance (Lag(−1)): Lagged GEP shows a significant positive association with current GEP in models (1) and (3). This indicates that past performance in the green economy is a predictor of current performance. Model (3) is particularly robust, with a highly significant coefficient of 1.719 (t-statistic = 2.730), suggesting the enduring impact of previous green economic performance on the current state.

Managerial Ownership (MO): In model (1), Managerial Ownership (MO) demonstrates a non-significant positive relationship with Green Economy Performance (GEP), with a coefficient of 0.490 (t-statistic = 1.080). This implies that while there is a positive association between Managerial Ownership and GEP, it is not statistically significant at conventional levels.

Institutional Ownership (IO): In model (2), Institutional Ownership (IO) exhibits a statistically significant positive effect on GEP. The coefficient of 0.036 (t-statistic = 2.460) is significant at the 5% level. This suggests that Institutional Ownership has a noteworthy positive influence on Green Economy Performance, which aligns with previous findings.

Board of Commissioners (BoC): Model (3) shows a statistically significant positive effect of the Board of Commissioners (BoC) on GEP. The coefficient of 0.140 (t-statistic = 2.420) is significant at the 5% level, reinforcing the importance of the BoC’s role in promoting Green Economy Performance.

Audit Committee (AC): In model (4), the Audit Committee (AC) also reveals a statistically significant positive impact on GEP, with a coefficient of 0.279 (t-statistic = 2.000). This underscores the substantial contributions of the Audit Committee to enhancing Green Economy Performance, aligning with previous results.

Control Variables (LEV, AGE, SIZE): The control variables, including Leverage (LEV), Firm Age (AGE), and Firm Size (SIZE), exhibit varied effects in different models. These variables may have a complex interplay with the key determinants of GEP, requiring further investigation.

Table 7. Robustness Check

The Robustness Check provides consistent support for the relationship between Institutional Ownership, Board of Commissioners, and the Audit Committee with Green Economy Performance. The lagged Green Economy Performance (GEP) also remains a robust predictor of current performance. However, Managerial Ownership displays a non-significant relationship with GEP in this analysis. These findings emphasize the multifaceted nature of the factors affecting green economic performance within the context of State-Owned Enterprises. Further research may be warranted to explore the intricacies of these relationships.

The empirical findings provide crucial insights into the interplay between various ownership and governance factors and their impact on the green economy performance of SOEs.

Managerial Ownership (MO)The positive but non-significant relationship between Managerial Ownership (MO) and Green Economy Performance (GEP) is consistent with the theoretical expectation that managerial ownership might be associated with a more focused commitment to green economic objectives. However, the lack of statistical significance indicates that further research may be necessary to explore this relationship in depth.

Institutional Ownership (IO)The statistically significant positive effect of Institutional Ownership (IO) on GEP corroborates the theoretical notion that institutional investors can exert a positive influence on corporate sustainability initiatives. This finding aligns with prior empirical research suggesting that institutional ownership can promote environmental responsibility.

Board of Commissioners (BoC)The statistically significant positive impact of the Board of Commissioners (BoC) on GEP reinforces the importance of strong corporate governance in driving green economic performance. The presence and composition of the BoC play a pivotal role in enhancing sustainability initiatives, aligning with theoretical expectations.

Audit Committee (AC)The statistically significant positive effect of the Audit Committee (AC) on GEP underscores the crucial role played by the audit committee in promoting sustainability and green economic objectives. This finding resonates with theoretical arguments about the significance of internal control mechanisms in ensuring environmental responsibility.

The statistical findings are supported by the robustness check using the Two-Step System GMM, which reinforces the relationships between Institutional Ownership, Board of Commissioners, and the Audit Committee with Green Economy Performance. It also highlights the enduring influence of past green economic performance on the current state. These findings have substantial academic and practical implications. They provide a nuanced understanding of the factors that influence the green economy performance of SOEs, offering a foundation for further research and informing policy decisions aimed at promoting sustainability and responsible resource management within the Indonesian corporate landscape. The research findings have been consistent across different analytical methods, adding strength and credibility to the study’s outcomes.

6. Discussions

Based on the preceding test results, it is evident that the hypotheses regarding Managerial Ownership (MO), Institutional Ownership (IO), and the Audit Committee (AC) could not be substantiated in this study. This stems from the observation that Managerial Ownership (MO) demonstrates a positive but statistically non-significant association with Green Economy Performance (GEP). The coefficient of 0.040, with a t-statistic of 1.150, suggests a positive link between Managerial Ownership (MO) and GEP, though it fails to reach the conventional threshold of statistical significance. This implies that while Managerial Ownership (MO) may have a positive influence on GEP, this impact is not statistically significant.

On the other hand, Institutional Ownership (IO) displays a statistically significant positive influence on GEP. The coefficient of 0.074 with a t-statistic of 1.650, significant at the 10% level, underscores the substantial impact of Institutional Ownership on Green Economy Performance (GEP). This result implies that the involvement of institutional investors significantly contributes to enhancing GEP. This outcome underscores the substantial influence of institutional investors in advancing green economic objectives. In the case of SOEs in Indonesia, this signifies the critical role played by institutional ownership in steering these enterprises toward environmentally responsible economic development.

The presence and composition of the Board of Commissioners (BoC) are found to have a statistically significant positive effect on GEP. With a coefficient of 0.106 and a t-statistic of 1.830, significant at the 10% level, this finding underscores the pivotal role played by the Board of Commissioners in bolstering Green Economy Performance (GEP). A good Board of Commissioners (BoC) that understands the demands of the green economy is essential in providing direction for State-Owned Enterprises (SOEs) that focus on environmentally friendly economic development. However, in Indonesia, where SOE business policies are influenced by various factors and elements such as managerial ownership, institutional ownership, and audit committees, the Board of Directors’ role in transforming the environmental performance of SOEs is limited. This situation is ironic, given that the Government of the Republic of Indonesia has issued policies that encourage SOEs to build a green economy (Ministry of SOE, Citation2018). To achieve sustainable and environmentally friendly economic development goals, there is a need to evaluate and improve existing policies and regulations. The role and function of the Board of Commissioners must be strengthened to provide positive influence in directing SOE business strategies towards a more environmentally friendly direction. With a stronger Board of Commissioners, SOEs can play a more effective role in promoting sustainable economic development and contribute to environmental conservation in Indonesia.

Similarly, the Audit Committee (AC) is noted to exert a statistically significant positive impact on GEP. The coefficient of 0.070 with a t-statistic of 1.870, significant at the 10% level, highlights the substantial contributions of the Audit Committee to improving Green Economy Performance (GEP). This finding emphasizes the considerable contributions made by the Audit Committee (AC) in elevating Green Economy Performance (GEP). In the context of SOEs in Indonesia, the Audit Committee emerges as a driving force behind their endeavors to promote eco-friendly economic growth, thereby aligning with the government’s green economic policies in Indonesia.

This study highlights the importance of involving various elements in building a green economy within the SOE environment. In this context, the existence of SOE institutions that represent government policies is crucial. However, given that SOE management often involves political decisions that are not solely based on business interests, the direction of SOE business may not always align with the government’s economic vision, despite the demand for environmentally friendly economic development (Ministry of SOE, Citation2018; OJK, Citation2022). Nonetheless, the existence of SOEs as government business units is crucial for the sustainability of overall economic resource management.

The present study provides evidence that the Board of Commissioners plays a crucial role in promoting environmentally sustainable economic growth. For the successful implementation of green economy policies, it is imperative that companies possess a mature understanding and readiness to embrace the concept in the context of sustainable development (Astadi et al., Citation2022; Chaaben et al., Citation2022; Hermanto & Berutu, Citation2022; Putra et al., Citation2020). While the findings indicate that managerial ownership, institutional ownership, or audit committees do not exert a direct influence on green economy performance, these elements can significantly contribute to the direction of the business. Hence, the presence of key stakeholders such as owners, directors, commissioners, or audit committees, assumes a critical role in directing the business towards a more sustainable and environmentally responsible direction.

The findings of this study can be further examined through the lenses of Agency Theory and Corporate Governance Theory, shedding light on the implications of the observed relationships between key variables. Agency Theory posits that conflicts of interest may arise between the principal (the owner or shareholders) and the agent (management or executives) within an organization. In the context of this study, Managerial Ownership (MO) represents an aspect of the agent’s control over the organization. The positive but statistically non-significant relationship between Managerial Ownership (MO) and Green Economy Performance (GEP) suggests that while managerial ownership may align with the objectives of enhancing environmental performance, the lack of statistical significance implies that managerial interests may not always align with those of the shareholders. On the other hand, the statistically significant positive impact of Institutional Ownership (IO) on Green Economy Performance (GEP) is consistent with the Agency Theory’s predictions. Institutional investors often have a substantial stake in the performance of the company, and their involvement can act as a mechanism to align managerial decisions with shareholder interests. The observed significant influence of IO on GEP emphasizes the effectiveness of institutional investors in promoting green economic objectives (Jensen & Meckling, Citation1976; Zogning, Citation2017).

Corporate Governance Theory emphasizes the significance of governance structures and mechanisms in achieving organizational goals and aligning management with shareholder interests. The substantial positive effect of the Board of Commissioners (BoC) on Green Economy Performance (GEP), along with the statistically significant result, is in line with the core tenets of Corporate Governance Theory (Monks & Minow, Citation2011; Tricker, Citation2015). The Board of Commissioners (BoC) represents a critical element of corporate governance and plays a pivotal role in overseeing and guiding the management’s decisions. In this context, a robust Board of Commissioners (BoC) that comprehends and supports the green economy is essential in providing direction for State-Owned Enterprises (SOEs) striving for environmentally friendly economic development. Similarly, the significant positive impact of the Audit Committee (AC) on Green Economy Performance (GEP) resonates with the principles of Corporate Governance Theory.

The Audit Committee (AC) acts as a safeguard, ensuring transparency and accountability in the organization’s financial reporting and decision-making. The statistically significant relationship suggests that a vigilant Audit Committee is effective in ensuring that the environmental objectives of SOEs align with their actions. These findings are consistent with several previous studies, such as the study by Elmghaamez et al. (Citation2023), which indicates that the association between market-based performance outcomes and Environmental, Social, and Governance (ESG) disclosure is positively influenced by the compensation, nomination, and sustainability committee indexes, while it is negatively impacted by the audit committee index.

This study, viewed from the perspectives of both Agency Theory and Corporate Governance Theory, underlines the critical role of governance structures and mechanisms in shaping the green economic performance of State-Owned Enterprises in Indonesia. While Managerial Ownership may lack statistical significance, it highlights the need for vigilance in ensuring that management decisions align with shareholder interests. Institutional Ownership, the Board of Commissioners, and the Audit Committee, on the other hand, emerge as effective mechanisms in promoting environmentally sustainable economic development. The combination of several variables, as demonstrated in studies by Ntim and Soobaroyen (Citation2013) or Orazalin et al. (Citation2023), can support a company’s green economic performance. These findings underscore the importance of robust governance in fostering green economic performance and the need for continuous evaluation and enhancement of existing policies and regulations to further these objectives. It is imperative to provide a positive influence in directing state-owned enterprise (SOE) business strategies towards an environmentally friendly direction. The ultimate objective is for SOEs to play a more effective and proactive role in promoting sustainable economic development and contributing to environmental conservation efforts in Indonesia.

7. Summary and conclusion

The test results reveal that the Managerial Ownership (MO) variable demonstrates a positive yet statistically non-significant association with Green Economy Performance (GEP), as indicated by a coefficient of 0.040 (t-statistic = 1.150). In contrast, Institutional Ownership (IO) exhibits a statistically significant positive impact on GEP, with a coefficient of 0.074 (t-statistic = 1.650) at the 10% significance level. Furthermore, the Board of Commissioners (BoC) displays a statistically significant positive effect on Green Economy Performance (GEP), with a coefficient of 0.106 (t-statistic = 1.830) at the 10% significance level. Similarly, the Audit Committee (AC) also demonstrates a statistically significant positive impact on Green Economy Performance (GEP), with a coefficient of 0.070 (t-statistic = 1.870) at the 10% significance level.

The implications derived from this study underscore the immediate necessity for greater attention to be directed towards the formulation of effective policies and regulations aimed at fostering environmentally sustainable economic development in Indonesia. Within the realm of state-owned enterprises (SOEs), this research emphasizes the pivotal roles and functions of Institutional Ownership, the Board of Commissioners, and the Audit Committee in guiding SOE business strategies towards more ecologically friendly pathways. Consequently, there is also a need to strengthen the role of Managerial Ownership, a variable that exhibited limited influence, in promoting positive changes in SOE business strategies that prioritize sustainability and ecological friendliness.

This study is subject to several limitations and specific constraints that restrict the objective generalization of its results. Diverse studies with varying theoretical frameworks and different sets of variables within the context of State-Owned Enterprises (SOEs) in Indonesia can offer complementary insights to the conclusions drawn herein. Additionally, the scope of SOEs examined is exclusively drawn from Stock Exchange data over the past three years. This limitation is significant as the landscape of SOEs is dynamic and evolving, and the study does not encompass the entirety of SOEs operating in Indonesia.

About Authors.docx

Download MS Word (98.7 KB)Acknowledgments

The author wish to thank Prof. Dr. Noorlailie Soewarno, SE., MBA., Ak who has provided important suggestions in the preparation of this manuscript.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Supplemental material

Supplemental data for this article can be accessed online at https://doi.org/10.1080/23311975.2023.2282230

Additional information

Funding

Notes on contributors

Nastiti Rizky Shiyammurti

Nastiti Rizky Shiyammurti The author is a lecturer in the Accounting Study Program at Pasim National University. Completed undergraduate education at Telkom University Bandung in 2014. Obtained a Master’s degree in Accounting with a concentration in Auditing and Reporting at Unpad Bandung in 2018. Currently (2023) she is studying for a Doctorate in Accounting at Airlangga University Surabaya. The author actively writes in several scientific journals, both accredited at Sinta and Scopus, with the themes of financial management and financial performance and reporting. The author has expertise in the fields of management accounting and financial management. The author has attended character training at Pasundan University, Bandung in September 2023. Apart from that, she is the recipient of a research grant from the Ministry of Education and Culture in 2020 and 2022 and is a permanent financial consultant at a company operating in the Information Technology sector.

References

- Albawwat, A. H., Almansour, A., Al Zobi, M. K., & Alrawashedh, N. H. (2020). The effect of board of directors and audit committee characteristics on company performance in Jordan. International Journal of Financial Research, 11(6), 10–22. https://doi.org/10.5430/ijfr.v11n6p10

- Al-Jaifi, H. A., Al-Qadasi, A. A., & Al-Rassas, A. H. (2023). Board diversity effects on environmental performance and the moderating effect of board independence: Evidence from the Asia-Pacific region. Cogent Business & Management, 10(2), 2. https://doi.org/10.1080/23311975.2023.2210349

- Al-Jalahma, A. (2022). Impact of audit committee characteristics on firm performance: Evidence from Bahrain. Problems and Perspectives in Management, 20(1), 247–261. https://doi.org/10.21511/ppm.20(1).2022.21

- Alqatamin, R. M. (2018). Audit committee effectiveness and company performance: Evidence from Jordan. Accounting & Finance Research, 7(2), 48–60. https://doi.org/10.5430/afr.v7n2p48

- Arora, N., & Singh, B. (2023). Board characteristics, ownership concentration and SME IPO underpricing. Pacific Accounting Review, 35(1), 19–49. https://doi.org/10.1108/PAR-08-2020-0111

- Astadi, P., Setyorini, S., Sisilia, K. & Peranginangin, Y. (2022). The long path to achieving green economy performance for micro small medium enterprise. Journal of Innovation and Entrepreneurship, 11(16), 1–19. https://doi.org/10.1186/s13731-022-00209-4

- Beasley, M. S. (1996). An empirical analysis of the relation between the board of director composition and financial statement fraud. The Accounting Review, 71(4), 443–465.

- Bhagat, S., & Bolton, B. (2008). Corporate governance and firm performance. Journal of Corporate Finance, 14(3), 257–273. https://doi.org/10.1016/j.jcorpfin.2008.03.006

- Bilal, B., Chen, S., & Komal, B. (2017). Audit committee financial expertise and earnings quality: A meta-analysis. Journal of Business Research, 84, 253–270. https://doi.org/10.1016/j.jbusres.2017.11.048

- Budiarti, E. & Sulistyowati, C. (2014). Struktur Kepemilikan dan Struktur Dewan Perusahaan. Journal of Theoretical and Applied Management, 7(3). https://doi.org/10.20473/jmtt.v7i3.2709

- Chaaben, N., Elleuch, Z., Hamdi, B., & Kahouli, B. (2022). Green economy performance and sustainable development achievement: Empirical evidence from Saudi Arabia. Environment, Development and Sustainability, 1–16. https://doi.org/10.1007/s10668-022-02722-8

- Chairina, C., & Tjahjadi, B. (2023). Green governance and sustainability report quality: The moderating role of sustainability commitment in ASEAN countries. Economies, 11(27), 1–17. https://doi.org/10.3390/economies11010027

- Chariri, A., Januarti, I., & Yuyetta, E. N. A. (2017). Firm characteristics, audit committee, and environmental performance: Insights from Indonesian companies. International Journal of Energy Economics & Policy, 7(6), 19–26.

- D’Amato, D., Droste, M., Allen, B., Kettunen, M., Lähtinen, K., Korhonen, J., Leskinen, P., Matthies, B. D., & Toppinen, A. (2017). Green, circular, bio economy: A comparative analysis of sustainability avenues. Journal of Cleaner Production, 168, 716–734. https://doi.org/10.1016/j.jclepro.2017.09.053

- Elmghaamez, I. K., Nwachukwu, J., & Ntim, C. G. (2023). ESG disclosure and financial performance of multinational enterprises: The moderating effect of board standing committees. International Journal of Finance & Economics, 1–46. https://doi.org/10.1002/ijfe.2846

- Fauzyyah, R., & Rachmawati, S. (2018). The effect of number of meetings of the board of commissioners, independent commissioners, audit committee and ownership structure upon the extent of CSR disclosure. The Accounting Journal of Binaniaga, 3(2), 41–54. https://doi.org/10.33062/ajb.v3i2.232

- FSA. (2014) . Regulation of financial service authority number 33/POJK.04/2014 concerning the board of directors and the board of commissioners of issuers or public companies.

- Georgeson, L., Maslin, M., & Poessinouw, M. (2017). The global green economy: A review of concepts, definitions, measurement methodologies and their interactions. Geo: Geography and Environment, 4(1), 1–23. https://doi.org/10.1002/geo2.36

- Gielen, D., Boshell, F., Saygin, D., Brazilian, M. D., Wagner, N., & Gorini, R. (2019). The role of renewable energy in the global energy transformation. Energy Strategy Reviews, 24, 8–50. https://doi.org/10.1016/j.esr.2019.01.006

- Gujarati, D. N. (2003). Basic econometrics (4th Edition ed.). McGraw Hill.

- Ha, H. H. (2022). Audit committee characteristics and corporate governance disclosure: Evidence from Vietnam listed companies. Cogent Business & Management, 9(1), 1. https://doi.org/10.1080/23311975.2022.2119827

- Harianto, S. & Isbanah, Y. (2021). Peran financial knowledge, pendapatan, locus of control, financial attitude, financial self-efficacy, dan parental financial socialization terhadap financial management behavior masyarakat di kabupaten Sidoarjo. Jurnal Ilmu Manajemen, 9(1), 241–252.

- Hermanto, H., & Berutu, R. S. N. (2022). The influence of the number of board of commissioners, company size, risk monitoring committee, and financial performance on earnings management. International Journal of Science and Society (IJSOC), 4(1), 58–70. https://doi.org/10.54783/ijsoc.v4i1.416

- Iavicoli, I., Leso, V., Ricciardi, W., Hodson, L. L., & Hoover, M. D. (2014). Opportunities and challenges of nanotechnology in the green economy. Environmental Health, 13(78), 1–13. https://doi.org/10.1186/1476-069X-13-78

- IFC. (2014). The Indonesia corporate governance manual. IFC Advisory Services in Indonesia. OJK & IFC.

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs, and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Junias, D. T. S., Suharto, R. S. B. & Elim, M. A.(2020). The impact of managerial ownership on sustainability accounting. Advances in Social Science, Education and Humanities Research. Proceedings of the International Conference on Science and Technology on Social Science (ICAST-SS 2020), Padang, 544, 72–75.

- Karikari, A. M., Tettevi, P. K., Amaning, N., Ware, E. O., & Kwarteng, C. (2022). Modeling the implications of internal audit effectiveness on value for money and sustainable procurement performance: An application of structural equation modeling. Cogent Business & Management, 9(1), 1. https://doi.org/10.1080/23311975.2022.2102127

- Laiho, T. (2011). Agency theory and ownership structure – estimating the effect of ownership structure on firm performance. Department of Economics, Aalto University.

- Li, L., Lin, J., Wu, N., Xie, S., Meng, C., Zheng, Y., Wang, X., & Zhao, Y. (2022). Review and outlook on the international renewable energy development. Energy and Built Environment, 3(2), 139–157. https://doi.org/10.1016/j.enbenv.2020.12.002

- Loiseau, E., Saikku, L., Antikainen, R., Droste, N., Hansjürgens, B., Pitkänen, K., Leskinen, P., Kuikman, P., & Thomsen, M. (2016). Green economy and related concepts: An overview. Journal of Cleaner Production, 139, 361–371. https://doi.org/10.1016/j.jclepro.2016.08.024

- Lowitzsch, J., Hoicka, C. E., & van Tulder, F. J. (2020). Renewable energy communities under the 2019 European clean energy package – governance model for the energy clusters of the future? Renewable and Sustainable Energy Reviews, 122, 1–13. https://doi.org/10.1016/j.rser.2019.109489

- Mak, Y. T., & Li, Y. (2001). Determinants of corporate ownership and board structure: Evidence from Singapore. Journal of Corporate Finance, 7(3), 235–256. https://doi.org/10.1016/S0929-1199(01)00021-9

- Mealy, P., & Teytelboym, A. (2022). Economic complexity and the green economy. Research Policy, 5(8), 1–24. https://doi.org/10.1016/j.respol.2020.103948

- Mikhno, I., Koval, V., Shvets, G., Garmatiuk, O., & Tamošiūnienė, R. (2021). Green economy in sustainable development and improvement of resource efficiency. Central European Business Review, 10(1), 99–113. https://doi.org/10.18267/j.cebr.252

- Ministry of SOE. (2018). Annual Report of Ministry of SOE 2018. Strengthening BUMN in Building the Country. https://www.bumn.go.id/storage/kontenlaporan/files/files_1673252092.pdf

- Monks, R. A. G., & Minow, N. (2011). Corporate governance (5th ed.). John Wiley & Sons.

- Mueller, E., & Spitz-Oener, A. (2019). Managerial ownership and company performance in German small and medium- sized private enterprises. German Economic Review. https://doi.org/10.1111/j.1468-0475.2006.00154.x

- Munisi, G., Hermes, N., & Randoy, T. (2014). Corporate boards and ownership structure: Evidence from Sub-Saharan Africa. International Business Review, 23(4), 785–796. https://doi.org/10.1016/j.ibusrev.2013.12.001

- Ntim, C. G., & Soobaroyen, T. (2013). Corporate governance and social responsibility. Corporate Governance an International Review, 21(5), 468–494. https://doi.org/10.1111/corg.12026

- OJK. (2022). Indonesia Green Taxonomy. https://ojk.go.id/id/berita-dan-kegiatan/info-terkini/Documents/Pages/Taksonomi-Hijau-Indonesia-Edisi-1—2022/Taksonomi%20Hijau%20Edisi%201.0%20-%202022.pdf

- Orazalin, N. S., Ntim, C. G. & Malagila, J. K. (2023). Board Sustainability Committees, climate change initiatives, carbon performance, and market value. British Journal of Management, 1–30. https://doi.org/10.1111/1467-8551.12715

- Potharla, S., Bhattacharjee, K., Iyer, V., & McMillan, D. (2021). Institutional ownership and earnings management: Evidence from India. Cogent Economics & Finance, 9(1), 1. https://doi.org/10.1080/23322039.2021.1902032

- Putra, R. B., Yeni, F., Fitri, H., & Melta, D. J. (2020). The effect of board of commissioners ethnic, family ownership and the age of the company towards the performance of the company LQ45 company listed in Indonesia Stock Exchange. ADI Journal on Recent Innovation, 1(2), 85–92. https://doi.org/10.34306/ajri.v1i2.27

- Sánchez, I. M. G., Aibar-Guzmán, C., & Aibar-Guzmán, B. (2020). The effect of institutional ownership and ownership dispersion on eco-innovation. Technological Forecasting and Social Change, 158(1), 120173. https://doi.org/10.1016/j.techfore.2020.120173

- Sukhani, N., & Hanif, H. (2023). The role of environmental performance in the effect of Managerial ownership, independent board of commissioners, and social costs on corporate social responsibility disclosure. Journal of the Community Development in Asia, 6(2), 1–13. https://doi.org/10.32535/jcda.v6i2.2325

- Tricker, B. (2015). Corporate governance: Principles, policies, and practices. Oxford University Press.

- USAID. (2018). Indonesian Public Opinions on Environmental Issues. A National Survey. https://pdf.usaid.gov/pdf_docs/PA00TMNG.pdf

- Vakulchuk, R., Overland, I., & Scholten, D. (2020). Renewable energy and geopolitics: A review. Renewable and Sustainable Energy Reviews, 122, 1–12. https://doi.org/10.1016/j.rser.2019.109547

- Velte, P. (2020). Institutional ownership, environmental, social, and governance performance and disclosure – a review on empirical quantitative research. Problems and Perspectives in Management, 18(3), 282–305. https://doi.org/10.21511/ppm.18(3).2020.24

- Waheed, A., Hussain, S., Hanif, H., Mahmood, H., Malik, Q. A., & Ntim, C. G. (2021). Corporate social responsibility and firm performance: The moderation of investment horizon and corporate governance. Cogent Business & Management, 8(1), 1. https://doi.org/10.1080/23311975.2021.1938349

- World Bank Group. (2021). Climate Risk Country Profile Indonesia. The World Bank Group. https://climateknowledgeportal.worldbank.org/sites/default/files/2021-05/15504-Indonesia%20Country%20Profile-WEB_0.pdf

- Xu, L. (2016). Summary of principal—agent mechanism. Open Journal of Social Sciences, 4(8), 45–53. https://doi.org/10.4236/jss.2016.48006

- Yamashita, Y. (2020). The influence of capital structure and managerial ownership on company performance through agency cost as intervening variables. Journal of Accounting and Finance Management, 1(4), 195–211. https://doi.org/10.38035/jafm.v1i4.24

- Zogning, F. (2017). Agency Theory: A critical Review. European Journal of Business and Management, 9(2), 1–8.