?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study analyses the relationship between sustainability performance, convention signatures, sustainability offices, sustainability research, teaching programs, student clubs, financial statements, and the extent of sustainability reporting in higher education institutions (HEIs). The sample of this study was 153 unit of analysis of 57 HEIs which are registered in the Global Reporting Initiative database during the period 2010–2020. Descriptive, content, and multivariate regression analysis were used to analyze the data and test the hypotheses. The level of sustainability performance, convention signatures, sustainability offices, sustainability research, teaching programs, student clubs, financial statements have a significant effect on the extent of sustainability reporting. Moreover, the random effect model is the best approach for estimating the model. The study contributes to a better understanding of the determinants of HEIs sustainability reporting. Several previous studies only used one theoretical lens. The originality of this research is using a metatheoretical approach, namely stakeholder and legitimacy theory. The theoretical implication of these findings is that the combination of legitimacy and stakeholder theory is able to explain more broadly the model of HEIs sustainability reporting. Policymakers such as the government and other key stakeholders can use these findings as the basis for assessing an educational institution’s sustainability performance.

1. Introduction (5 halaman)

Research related to the relationship between institutional performance and sustainability disclosure is often found with corporate objects (Caesaria & Basuki, Citation2017; Firmialy et al., Citation2019; Gunarsih et al., Citation2020; Maqbool & Hurrah, Citation2021; Parvez & Agrawal, Citation2019; Septiani, Citation2022; Uwuigbe et al., Citation2018). Sustainability disclosure is a tool for establishing good relationships with stakeholders (Guix et al., Citation2018), improving the image, reputation and performance of institutions as well as public trust (de Grosbois, Citation2016). Consistent sustainability disclosure over the long term can increase legitimacy (Manteiro & Kabu, Citation2019) while managing institutional reputation (Clarke & Gibson‐Sweet, Citation1999). Brammer and Pavelin (Citation2004) argue that institutional reputation and performance will improve when institutions engage in sustainability activities and disclose them in their annual reports. These institutions are considered to have good values as intangible assets that can be translated positively in many ways, such as attracting customers, generating investment interest, attracting the best talent, motivating employees, increasing job satisfaction and generating more positive media coverage (Laufer & Coombs, Citation2006).

Similar research using Higher Education Institutions is still very limited (Ardillah, Citation2021; Atici et al., Citation2021; Dobson et al., Citation2010; Sánchez et al., Citation2013; Shan et al., Citation2021). The research on sustainability reporting by universities has not been much (Ceulemans et al., Citation2015) and is “still at a very early stage”. This is not only due to the small number of three universities that have reported sustainability progress (Fonseca et al., Citation2011). Previous research has found that the level of understanding of governance among UK higher education institutions is generally low, so consistency with previous research findings regarding general disclosure practices (Crossley et al., Citation2021). Moreover, there is no sustainability reporting standard for universities (Adams et al., Citation2013), unlike companies that already have Global Reporting Initiative (GRI) guidelines. Descriptive research on the relationship between IPT performance and IPT sustainability disclosure showed as much as 44.5% of IPT which is included in QS 2019, has courses integrated with the accounting and reporting environment in the educational curriculum (Ardillah, Citation2021).

The results of research investigating the relationship between sustainability practices in Higher Education Institutions and academic success show that there is no implied causal relationship. However, it can be verified that sustainability practices have a reflection in academic rankings. Higher ranking scores in environmental performance are reflected in IPT’s academic performance. The results show that disclosure of IPT’s sustainability is a tool for building competitive advantage for IPT (Atici et al., Citation2021). The differences between public and private higher education institutions in terms of sustainability disclosure show insignificant results. However, state and private IPTs in the best category are more interested in disclosing sustainability information (Sánchez et al., Citation2013).

Empirical evidence shows that sustainability disclosure is significantly and positively related to IPT ratings and provides confirmation that various disclosure channels play an important role when communicating with IPT stakeholders. In addition, sustainability disclosure through websites, annual reports and separate sustainability reports has a positive influence on the IPT ranking system. IPT sustainability disclosure is considered an important communication tool to meet the expectations of relevant stakeholders both internal and external (Shan et al., Citation2021). Evidence shows that sustainability can and has been mobilized as a vehicle for excellence competitive is related to the benefits obtained in relation to staff and student recruitment, research funding, IPT infrastructure and reputation (Dobson et al., Citation2010).

Sustainability has become an important and unavoidable challenge for organizations in the age of digitalization (Thomashow, Citation2014). Higher education institutions (HEIs) are places of learning where students can make informed decisions and where intellectually productive institutions can play an important role in influencing sustainable development (Adams et al., Citation2013; Barth et al., Citation2007; Ceulemans et al., Citation2015). The role of HEIs related to sustainable development goals has been recognized globally (Abad Segura & González-Zamar, Citation2021; Alawneh et al., Citation2021; Bautista et al., Citation2022; Caputo et al., Citation2021; Griebeler et al., Citation2021; Hansen et al., Citation2021; Salancik & Pfeffer, Citation1974). However, the development of sustainability reporting in HEIs is still in its early stages (Ossietzky, Citation2014; Sassen & Azizi, Citation2018; Sepasi et al., Citation2019).

Sustainability reporting (SR) may be a challenge for HEIs. While many universities have addressed sustainability issues, they represent only a small number of HEIs worldwide (Lozano et al., Citation2013). In addition, Ceulemans et al. (Citation2015) show that several universities have engaged in sustainability performance (SP), but not many have published reports on it. As of 2010, 95 universities in 35 countries had implemented SP measures. By 2022, this number had increased to 1,050 HEIs in 83 countries which is 67% use non-GRI frameworks. One of the factors explaining the lack of HEIs implementing SP is likely a lack of accountability, support, awareness, and resources; overcrowding of curricula; and an unwillingness of HEIs to change (Alghamdi et al., Citation2017; Calitz et al., Citation2018).

Several theories have been used to explain an institution’s sustainability disclosure practices. Empirical evidence regarding sustainability disclosure has been draws on many different theoretical perspectives (Gray et al., Citation1995). Some of this research even uses multiple theoretical perspectives, namely agency theory, stakeholder theory, legitimacy theory and institutional theory (Deegan & Blomquist, Citation2006).

The typology of social accounting theories by Deegan and Blomquist (Citation2006) and Brown and Fraser (Citation2006) is used to identify theories commonly used to study sustainability disclosures. With regard to sustainability issues, institutions are highly dependent on the perceptions and pressures of their external stakeholders. Several social accounting theories including Stakeholder, Legitimacy and Institutional Theory (Deegan, Citation2010; Unerman & Bebbington, Citation2007) and Shareholder Theory (Brown & Fraser, Citation2006) argue that external pressures influence institutions in different ways.

Shareholder theory suggests that equity providers demand a return of capital to compensate for the risks involved (Smith, Citation2003; Sundaram & Inkpen, Citation2004). Stakeholder theory posits that external pressures influence institutions through stakeholders’ demands on institutions (Kim et al., Citation1999; Phillips et al., Citation2017). Legitimacy theory posits that external pressures influence institutions through resource provision and social acceptance (Guthrie & Parker, Citation1989; Tilling, Citation2004). Institutional theory argues that external pressures influence institutions through the influence of the institutional environment and not necessarily by the need for efficiency (DiMaggio & Powell, Citation1983; Meyer & Rowan, Citation1977) even regardless of their usefulness actually (Carpenter & Feroz, Citation2001).

Management can not ignore external pressures, but suggested responses to these pressures vary between theories. Institutions will pursue legitimate and socially acceptable wealth maximization according to shareholder theory (Smith, Citation2003). They will pursue a balance of interests of various stakeholders according to stakeholder theory (Phillips et al., Citation2017). Legitimacy theory posits that institutions respond to external pressures through strategies of reducing legitimacy gaps, changing perceptions, deflecting attention and changing expectations (Dowling & Pfeffer, Citation1975). New institutional theory argues that institutions respond to external pressures through mechanisms of isomorphism (DiMaggio & Powell, Citation1983), and strategies of acquiescence, compromise, avoidance, defiance and manipulation (Oliver, Citation1991). The most commonly used theory to explain sustainability disclosure is legitimacy theory, followed by stakeholder theory, then institutional, and finally shareholder theory (Mahmood & Uddin, Citation2020).

Empirical research points to institutional legitimacy (Deegan, Citation2002) and stakeholder management (Deegan & Blomquist, Citation2006) as key motivations behind sustainability disclosures. The most well-known benefit of sustainability disclosure is that it reduces information asymmetry between an institution and its stakeholders, eliminating room for speculation, and thereby reducing the institution’s overall risk level (Cormier & Magnan, Citation1999). It can be concluded that legitimacy theory is more suitable in explaining voluntary sustainability disclosure, stakeholder theory would be better in explaining mandatory sustainability disclosures (Geerts et al., Citation2021).

Researchers have mostly used two theoretical perspectives, namely legitimacy and stakeholder theories, to explain factors affecting SR practices. Both theories posit that external pressures may affect institutions. According to legitimacy theory, organizations external may respond to pressures by giving the stakeholder the information to gain their support (Tilling & Tilt, Citation2010). Empirical research has demonstrated the legitimacy of institutions and the management of stakeholders as the driving factors for SR (Deegan et al., Citation2002). The most important benefit of SR is meeting expectations and reducing stakeholder pressures (Cormier & Magnan, Citation1999). In line with legitimacy theory, stakeholder theory asserts that external pressure is exerted by stakeholder demands on institutions (Kim et al., Citation1999; Phillips et al., Citation2017). Management cannot ignore external pressure, and it is expected to respond. SR may be used by institutions to negotiate and determine institutional relationships with society and stakeholders (Gray, Citation2010). From the stakeholder perspective, the survival of an institution requires support from stakeholders, and their consent should be sought and institutional activities adapted to obtain that approval. The stronger stakeholders are, the more institutions have to adapt. SR may be perceived as part of a dialogue between institutions and their stakeholders.

The review above shows that several previous research results have inconsistent results regarding the factors that influence sustainability disclosure. This is possibly caused by researchers only using one theoretical lens. This research uses Legitimacy and stakeholder theory as a basis for forming a research model to obtain more comprehensive results and resolve inconsistencies in results. It is hoped that universities can be greatly helped by the existence of a comprehensive model as best practice for Sustainable Reporting at Universities.

The objective of this study is to investigate the determinants of SR in HEIs using two theoretical perspectives in order to obtain more comprehensive results. By identifying the factors that influence SR, this study makes two major contributions. First, it provides valuable insight to improve understanding of the determinants influencing the SR practices of HEIs using two theoretical perspectives. Second, by combining multiple theoretical perspectives, namely legitimacy theory and stakeholder theory, this study enriches the literature on SR in the context of HEIs in the setting of emerging markets.

2. Background

Humanity’s challenges in the future are related to population pressure, climate change, energy security, environmental damage, air and food supplies and sustainable development. Sustainable development is development that meets the needs of the present without compromising the capabilities of future generations (Johnston, Citation2016). Sustainable Development Goals (SDGs) have been developed as a solution to address these problems. The education sector plays a role in achieving the SDGs. The role of Higher Education Institutions (HEIs) in influencing society is in the form of knowledge transfer and public involvement through three methods, namely teaching, research and community service (Corazza, Citation2018). Universities have various types, functions, sizes, complexities, energy requirements, electricity consumption, waste generation, water and material consumption, public transportation and educational activities, so that universities have a significant impact on the environment (Suwartha & Berawi, Citation2019). The relationship between SDGs and HEIs has become a very interesting issue discussed in recent years (Tan et al., Citation2014).

SDGs are a set of indicators, targets and universal sustainable development goals, as a continuation and extension of the millennium development goals (MDGs). All countries and all stakeholders play a role in collaborative partnerships to achieve 17 sustainable development goals (SDGs), which consist of three dimensions: environmental, social and economic (Mallow, Citation2020). It can be emphasized that the role of HEIs in realizing the SDGs is stakeholder pressure, seeking more competitive universities, sustainable values becoming fundamental and sustainability assessment, disclosing and reporting have become a cornerstone. There are several forms of realization of higher education, namely adopting educational policies that focus on sustainable development; to emphasize the need for university-wide policy development; to institute environmentally friendly practices at universities; to implement green policies; establish greening policies; establishing a greening curriculum; transforming university campuses into environmentally friendly areas; to contribute to society not only through infrastructure improvements; and to create awareness about sustainability among its graduates.

Public pressure on environmental responsibility differs between developing countries and developed countries (Ali et al., Citation2017). Anglo Saxons and Europeans dominate world university rankings. However, HEIs in the Asia Pacific region show real efforts regarding desirability (Nomura & Abe, Citation2011; Ryan et al., Citation2010; Suárez & Osca, Citation2020). Various declarations and efforts initiated by HEI related to achieving the SDGs have been carried out (Lozano et al., Citation2013). Several indices and tools have also been developed related to assessing HEIs’ sustainability performance (SP) (Caeiro et al., Citation2020). Sustainability frameworks have been developed in many countries (Gómezgutiérrez et al., Citation2017). Many studies recognize the importance of sustainability reporting (SR) as a form of accountability in various countries (Filho et al., Citation2019). However, research results show that the diffusion of SR is still at an early stage in higher education, and no significant diffusion has yet been achieved (Alonso-Almeida et al., Citation2015).

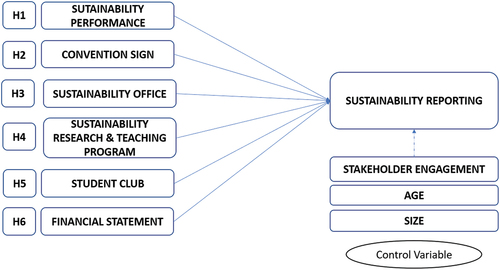

The dependent variable used in this study was the extent of the sustainability report disclosure. Based on the research of (Jorge et al., Citation2019) and (Richardson & Kachler, Citation2017), the following hypotheses are developed in this study. The design of the hypothesis in this study is based on the Legitimation Theory and Stakeholder Theory which explains which party becomes the responsibility of the entity (Freeman, Citation2010). Based on the previous research, we hypothesized that the sustainability reporting would be related to strategic commitment based on Legitimacy Theory which is Sustainability Performance, Convention Signed, Research Teaching Program, and Sustainability Office. Moreover, stakeholder demands are based on Stakeholder Theory which is Student Club and Financial Statement. This study uses control variables which are Stakeholder Engagement, Size and University Age.

The rest of the paper is organized as follows. First, we review the literature related to the variables in our study model. Second, we develop hypotheses to explain the interrelationships between the research variables. Third, we describe our methodology and results. Finally, before concluding, we present our discussion, as well as the implications and limitations of our research.

3. Theoritical literature review

Several theories have been used to explain an institution’s sustainability disclosure practices. Empirical evidence regarding sustainability disclosure has been draws on many different theoretical perspectives (Gray et al., Citation1995). Some of this research even uses multiple theoretical perspectives, namely agency theory, stakeholder theory, legitimacy theory and institutional theory (Deegan & Blomquist, Citation2006). The review above shows that several previous research results have inconsistent results regarding the factors that influence sustainability disclosure. This is possibly caused by researchers only using one theoretical lens. This research uses Legitimacy and stakeholder theory as a basis for forming a research model to obtain more comprehensive results and resolve inconsistencies in results. It is hoped that universities can be greatly helped by the existence of a comprehensive model as best practice for Sustainable Reporting at Universities.

There is a tendency in the literature to favor legitimacy theory to explain sustainability disclosures. Legitimacy theory is the most cited theory in sustainability disclosure studies (Campbell, Citation2003). Empirical research points to institutional legitimacy as the primary motivation behind sustainability disclosures (Deegan, Citation2004). Legitimacy theory is a theoretical framework that has been widely used in previous studies to test managers’ motivation to disclose certain social and environmental information in SR (Deegan, Citation2010; Unerman & Bebbington, Citation2007). There are two varieties of legitimacy, institutional and strategic/instrumental (Suchman, Citation1995). The institutional view is outside-in (society looks inside and imposes conditions), as opposed to the strategic view, which is inside-out (managers seek legitimacy by looking outside). The first strategy is typically used in the majority of studies linked to SR. When an entity’s values align with those of the larger social system of which it is a part, legitimacy is a state or circumstance that exists. The legitimacy of the entity is threatened whenever there is a disparity between its value and the value of the social system. Organizations have a social contract with society at large, and they work to make their value systems fit with society (Deegan, Citation2004; Deegan & Blomquist, Citation2006).

Legitimacy is viewed as a resource that forms the cornerstone of organizational survival (Dowling & Pfeffer, Citation1975). Managers are perceived as manipulators of those resources, and they attempt to recover the manipulation through legitimacy strategies if they see a legitimacy gap (Suchman, Citation1995). Depending on whether an organization wants to earn, maintain or increase legitimacy, the legitimacy strategy may be substantial or different (O’Donovan, Citation2002). Strategies include educating and enlightening audiences outside the organization, attempting to alter their perceptions, deflecting their attention to other problems, or attempting to alter their expectations to influence legitimacy. Therefore, SR may be seen as legitimizing instrument in this strategy.

Stakeholder theory focuses on how the environment affects organizations (Clarkson, Citation1995). However, it does not take the environment into account as a whole, instead concentrating only on how the organization and its many stakeholders are related. Normative stakeholder theory illustrates a company’s moral responsibility to all stakeholders. Instrumental stakeholder theory demonstrates the strategic management of important stakeholders (Berman et al., Citation1999). SR is viewed in both variations as a conversation between a company and its stakeholders (Gray et al., Citation1995). SR can be viewed from a normative (ethical) standpoint as a means to carry out accountability for all stakeholders or from an instrumental (strategic) standpoint as a managerial tool or instrument to manage powerful stakeholders. Based on an evaluation of stakeholder demands that influence and/or are affected by the company, decisions are taken regarding the “what” and “how” of SR (DiMaggio & Powell, Citation1983). The importance of stakeholders in determining sustainability actions and reporting has been supported by empirical studies (Roberts, Citation1992).

The extent to which disclosure or non-disclosure has an impact on financial returns, whether through reputational improvement or gaining competitive advantage, has been determined to be a key stakeholder issue. Secondary stakeholders, on the other hand, have been discovered to be more interested in SR, desire transparency, and care about society and the environment (Tilling & Tilt, Citation2010). A significant factor influencing SR was discovered to be the relative power of stakeholders (Roberts, Citation1992). There is evidence that stakeholders have a variety of demands for organizations some of which conflict with one another. Managers define numerous stakeholders and the needs they aim to address in the face of these conflicting demands (Unerman & O’Dwyer, Citation2007). Their decisions rely on why they are reporting on sustainability. Some academics offer normative expectations of stakeholders in various circumstances through the study of stakeholder perceptions. However, there are conflicting data that are more in line with the hypotheses and justifications of instrumental stakeholder theory (Belal et al., Citation2002). The majority of the reporting practices in use today are a cosmetic reaction to pressure from global markets. Belal et al. (Citation2007) demonstrate that the ambition of management to control a powerful stakeholder group is the primary driver of managers’ motivation for social reporting. They also raise concerns about the potential for such reporting to be taken into consideration, particularly when societal norms are pushed from the outside without taking local cultural, economic and social contexts into account.

The relationship between elements that influence reporting has been the subject of extensive prior research (Hummel & Schlick, Citation2016; Magali et al., Citation2020; Maqbool & Hurrah, Citation2021; Shan et al., Citation2021; Sohail et al., Citation2021; Zahid et al., Citation2021). SR practices in HEIs are substantially behind those in other industries, and they are far from using the industry’s potential to bring about transformative change through knowledge transfer. HEIs have to improve their reporting and management of SP to promote accountability and boost performance. This requires integrating social, environmental, and economic sustainability into HEIs’ processes. Adams et al. (Citation2013) justifies the need for such reporting for all HEIs to create and periodically assess their SR. SP is a holistic measurement of institutional performance from various aspects. It can drive the level of sustainability reporting as a legitimacy strategy. Thus, universities with high-quality SP will be more likely to disclose SR. Consequently, it appears that sustainability reports reflect actual SP (Papoutsi & Sodhi, Citation2020).

4. Empirical literature review

According to legitimacy theory, the connection between SR and SP is mixed. Poor performance by organizations can provide information to stakeholders to reduce their negative reactions and/or release of bad information to disguise their poor performance (Velazquez et al., Citation2006). Previous studies indicate that SP and SR are linked (Al-Tuwaijri et al., Citation2004; De La Poza et al., Citation2021; Grima et al., Citation2018; Jorge et al., Citation2019; Richardson & Kachler, Citation2017; van de Burgwal & Vieira, Citation2014).

Specifically, the evidence contributes to the existing literature by showing that higher education institutions with better governance tend to make higher risk disclosures than higher education institutions with poor governance (Elmagrhi & Ntim, Citation2023). Another paper indicates that HEI prioritizes long-term meetings social performance targets tend to provide low pay packages to their Vice Chancellors, whereas HEIs are the focus in achieving short-term reputation performance targets by paying high salary packages to their Vice Chancellors (Elmagrhi & Ntim, Citation2022).

The research results show that companies with better governance tend to pursue a more socially responsible agenda increasing Corporate Social Responsibility (CSR) practices. Apart from that, it was found that the combination of CSR and Corporate Governance (CG) practices had a stronger positive impact has an effect on Corporate Financial Performance (CFP) compared to CSR alone, which implies that CG has a positive effect on the relationship between CFP and CSR (Ntim et al., Citation2013). There is research that examines the relationship between corporate governance (CG) and corporate social responsibility (CSR), and its consequences. There is wide variation in the level of Corporate Sustainability Disclosure (CSD) across countries. Findings show that board size, gender diversity on the board, block ownership, and the presence of a poverty committee are significant determinants of CSD (Tran et al., Citation2021).

However, several studies have found a negative correlation between SP and SR (Cho & Patten, Citation2007; de Villiers & van Staden, Citation2006). Meanwhile, prior studies have also found that there is no correlation between SP and SR (Ingram & Frazier, Citation1980). Given the inconsistent results of past research, the purpose of the current study is to obtain empirical evidence regarding the relationship between SP and SR in the context of HEIs.

H1: Sustainability Performance has a positive effect on Sustainability Reporting.

One approach taken by activists is to encourage HEIs to sign sustainability documents (Lozano et al., Citation2013), such as strategic commitments to sustainability. Universities that sign sustainability declarations will be broader in their disclosure of SR. Entities that have carried out signatory conventions and have not taken specific actions related to sustainability will face protests from stakeholders. Accountability is a crucial issue that seems to profit from signing declarations without actually making any progress. It is essential for HEIs to expose themselves to the scrutiny of progress to determine whether commitments have been kept so that statements are more than just greenwashing (Bekessy et al., Citation2007). HEIs need to drive systemic transformation in the education sector. The transformation is carried out through the utilization of national policies, creating local and regional initiatives, making more substantial changes in the curriculum, as well as the cooperation of HEIs with external communities and various other stakeholders (Ryan et al., Citation2010).

H2: Convention signing has a positive effect on Sustainability Reporting.

The strategic commitment of HEIs is to support committed employees who have an impact on sustainability. HEIs with sustainability offices have better human and financial resources to create sustainable universities. This is done through developing, coordinating, and implementing sustainability reports. HEIs that have offices dedicated to sustainability activities are more likely to disclose SR (Rosenbloom, Citation2017). Wissink (Citation2012) also suggests that organizations that do well financially will have income available to engage in sustainability initiatives. Increasing investment in sustainability initiatives will boost SP, which will enhance reporting on sustainability and institutional sustainability policies (Uwuigbe et al., Citation2018).

H3: The presence of sustainability offices has a positive effect on Sustainability Reporting.

In terms of highlighting the importance of influential stakeholders, managers’ instrumental logic, and the use of reporting as a tool for managing influential stakeholders, stakeholder theory in SR offers some helpful insights. Stakeholder theory offers answers by describing numerous stakeholders and how they impact reporting. Both stakeholder theory and legitimacy theory shed light on the presence of such pressures and describe how firms take these demands into account when reporting. When HEIs are gaining pressures, they neglect internal elements (such as managers’ attitudes, priorities, and institutions) and instead pay attention to external ones (Adams, Citation2002). Strong stakeholders in HEI include professors involved in research and teaching initiatives, as well as students Internal stakeholders need to emphasize the importance of several sustainability factors, to all members of the organization (Ferrero et al., Citation2018). SR has largely been driven by internal motives, and the process results in small changes, like an increase in sustainability awareness and better communication with internal stakeholders (Ceulemans et al., Citation2015).

Sustainability teaching and research programs are one way to show a clear commitment to sustainability (Adams et al., Citation2013; Gumport, Citation2000; McGibbon & Van Belle, Citation2015). HEIs that have sustainability research and teaching programs related to sustainability will be broader in their communication of SR. The three functions of HEIs, namely research, teaching and community service, are expected to engage in sustainability at institutions that have adopted sustainability research and teaching programmes. This shows that these HEIs have better human and financial resources to create sustainable universities. According to (Maqbool & Hurrah, Citation2021), because there are resources that can be assigned to social or environmental domains, the presence of slack resources inside an organization is crucial. Corporate slack is the capacity to make use of offered resources and accomplish objectives. Sustainability research and teaching programmes on sustainability and the extent of SR by HEIs demonstrate a positive relationship. Based on a multitheoretical framework drawing from public accountability, legitimacy, resource dependency, and stakeholder perspectives. The results show that there is great variability in the relatively low overall level of voluntary disclosure by universities (44 percent), particularly with regard to the disclosure of teaching/research results (Ntim et al., Citation2013).

H4: The number of sustainability research and education programmes has a positive effect on Sustainability Reporting.

Students are key stakeholders in HEIs, and their activities have the potential to affect administrative choices. Students give a big impact on sustainability research (Beringer et al., Citation2008). Student initiatives with the sustainable campus project and the assessment framework of campus sustainability are employed to direct auditing and sustainable development. Based on stakeholder theory, if this student club related to sustainability is active on a campus, the HEI may be broader in its disclosure of SR. The management and operations of HEI will be more aware of sustainability issues and provide adequate information to stakeholders to assess the SP of the HEI if there are several student clubs dedicated to promoting sustainability on campus and in the community. It has previously been demonstrated that, despite being an understudied stakeholder group, students’ contributions to sustainability in HEIs are receiving increasing research attention (Richardson & Kachler, Citation2017). Students are attempting to increase the adoption of sustainability in higher education through multi stakeholder partnerships, group efforts and interdisciplinarity (Murray, Citation2018).

H5: The presence of student sustainability clubs on campus has a positive effect on Sustainability Reporting.

Sustainability and social responsibility impact an organization’s financial performance (Yang et al., Citation2020). Organizations’ employees have been shown to have a strong correlation with average assets. If HEIs have good commitments to sustainability, most of the activities of HEIs will focus on sustainability so that most of the allocation of funds owned will also focus on sustainability. This will automatically be relevant to accountability in the form of a financial statement for the utilisation of HEIs’ funding. The financial statement is a tool that can be used by stakeholders to measure the financial performance of HEIs. HEIs have to publish their financial statements, so it will be easier for stakeholders to monitor sustainability. This means that HEIs will more broadly disclose SR. Participants in the financial market have been paying closer attention lately to sustainability. Compared to public colleges, private HEIs make greater efforts to report on sustainability (Turan & Lambrechts, Citation2019). This study uses stakeholder theory to demonstrate that HEIs’ financial statements and the extent of SR by HEIs have a positive relationship.

H6: Financial statements have a positive effect on Sustainability Reporting.

5. Research design

This study uses an explanatory design by applying content, descriptive and inferential statistical analyses, especially for the panel data. We have data from many units and many points in time, with panel data, so we use 153 unit analysis of 57 HEIs over 10 years between 2010 and 2020 (Table ). A quantitative approach to hypothesis testing is used to investigate the impact of several variables that affect SR, and control variables were tested to build a best practice model. HEIs registered with the Global Reporting Initiative (GRI) comprise the study’s sample. Eighty-one HEIs with 249 sustainability reports make up the study’s population.

Table 1. Determination of the number of research Samples

The secondary data were taken from the GRI database for SR and the UI Green Metric (UIGM) Rank for SP in the form of panel data. In an international context, one of the sustainability assessment tools that is regarded as a best practice in the SR framework is the GRI database (Adams et al., Citation2013; Bedin & Faria, Citation2021; Fonseca et al., Citation2011; Grima et al., Citation2018; Lozano, Citation2011). The most popular global standard for SR is created by the GRI (Lozano, Citation2010) which provides performance metrics from the perspectives of the economy, environment, finance and society (GRI, Citation2020). SR based on the GRI has gained widespread recognition as a contributing element to corporate sustainability (Morhardt et al., Citation2002). This is indicated by an increase In the number of corporations issuing sustainability reports on the GRI database in 2020, totalling 50,000 reports. SR can be given through websites, annual reports, or separate sustainability reports.

To measure sustainable business, Universitas Indonesia launched a World University Ranking in 2010. This ranking is currently known as the UIGM World University Ranking. Universities can use the UIGM as a tool to address current global sustainability issues. Several literature reviews confirm that the UIGM is one of the best methods for assessing sustainability (Marrone et al., Citation2018). However, there is criticism of the UIGM rankings. Investigations of the UIGM’s strengths and weaknesses, as well as analyses in the form of literature reviews, survey questionnaires and evaluations of the guidelines, need to be continued (Ragazzi & Ghidini, Citation2017). The UIGM has received criticism regarding various sustainability concepts, challenges to university rankings and trade-offs between scientific and practical issues (Lauder et al., Citation2015). Several studies use the UIGM as a proxy for performance measurements (Ali & Anufriev, Citation2020; Ardillah, Citation2021; Atici et al., Citation2021; Galleli et al., Citation2021; Maçin, Citation2021; Sari & Faisal, Citation2022; Vitoreli et al., Citation2021). SP is measured using six categories from the UIGM: infrastructure and environment, energy and climate change, waste, water, transportation and education and research.

Table shows the sample data used from this research. There are 57 universities in the world registered with GRI from 2010 to 2020. After 2020, GRI will no longer provide data regarding higher education institutions. Only company data is available on the GRI website. So at this time analysis cannot be carried out for data on HEIs after 2020.

Table 2. List of higher education institutions

A panel data set combines time-series and cross-sectional data. The documentation technique, in the form of content analysis, was used for data-gathering (Hamilton & Waters, Citation2022; Trireksani et al., Citation2021). SR uses GRI indicators consisting of strategy and analysis, organizational profile, material aspects, bounds, stakeholder involvement, report profile, governance, ethics and integrity, as well as general reporting standards and economy, environment, employment practices and work convenience, human rights and society as specific reporting standards. Table shows the variable measurements. The data processing technique in this study uses the statistical programme E-views because it is recommended to process data using panel data regression techniques. The regression equation according to this report is as follows:

Table 3. Variable measurement

Where:

Yit : SR ᾳ : Constantß1 – ß6 : Regression coefficientX1it : SPX2it : CSX3it : SOX4it : SRTPX5it : SCX6it : FSeit : Error

Finding the best regression model to test the hypotheses is the goal of the estimate of the panel data regression model. The common effect model (CEM), the fixed effect model (FEM) and the random effect model (REM) are the three model techniques used to estimate the panel data regression model. The regression model’s estimation result has been translated into a log form. The CEM is the most basic model, simply combining time series and cross-section data without considering changes in time or entities. Since this study uses the ordinary least squares method, the behaviour of the data from an entity is constant across time. For variations in intercepts, the FEM analyses panel data uses dummy variables.

This approach assumes that the intercept between companies is different but that the intercept between times is the same, with a fixed slope between companies and between times. If the study uses many dummy variables, then the FEM or least square dummy variable are not able to identify the effect of the invariant variable. Therefore, the FEM is not identified in this study. The REM uses interference variables (error terms) that are interconnected between time and between individuals to overcome the weakness of using dummy variables. The estimation of this model uses the generalised least squares approach. The use of dummy variables can reduce the degree of freedom to reduce the efficiency of the parameters. The Chow test (FEM is better than CEM), Hausman test (FEM is better than REM) and LaGrange multiplier (REM is better than CEM) test are used to choose between the CEM, FEM and REM.

6. Empirical result and discussion

6.1. Empirical result

Table provides information about the features of data, including the median, minimum, maximum and standard deviation of the variables. Researchers log sustainability reporting as variable dependent as a solution to data abnormalities.

Table 4. Descriptive statistics

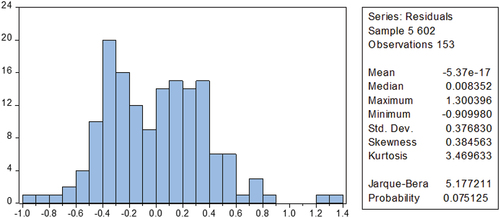

Classic assumption tests (normality, heteroscedasticity, multicollinearity and autocorrelation) must be carried out in panel data linear regression. This test is different for each model (FEM, CEM, REM). If the model chosen is ordinary least squares (FEM and CEM), then what must be tested is heteroscedasticity and multicollinearity. Meanwhile, if the generalized least square (REM) model is chosen, what must be tested is normality (Figure ), heteroscedasticity (Table ) and multicollinearity (Table ).

Figure 1. Empirical model.

Table 5. Heteroskedasticity test white

Table 6. Multicollinearity test

The results of panel data analysis show that the model chosen is the Random Effect Model (REM), so the classical assumptions required are the normality test and the multicollinearity test. Figure presents the results of the normality test which shows the Jarque-Bera probability value 0.075125 > sig 0.05 so that the data is normally distributed.

Figure 2. Normality test result.

The heteroscedasticity test is a test that assesses whether there is unequal variance in the residuals for all observations in the linear regression model. This test is one of the classic assumption tests that must be carried out in linear regression. Table show the results show that there is no heteroscedasticity because the beta parameter coefficient of the regression equation is not significant 0.6429 > 0.05.

The multicollinearity test aims to ensure that there is no correlation between independent variables. The multicollinearity test in Table shows the correlation between independent variables is below 0.8 so that the panel data regression in this study does not have multicollinearity problems.

Selection of the appropriate model between general effects, fixed effects, or random effects was carried out using the Chow test (FEM is better than CEM), Hausman test (FEM is better than REM), and LaGrange multiplier test (REM is better than CEM).

The Chow test results in Table show that between FEM and CEM, FEM is better than CEM because the probability is 0.000 < 5%. The Hausman test results in Table show that between REM and FEM, REM is better than FEM because the probability is 0.0575 > 5%. Meanwhile, the results of the LaGrange test in Table show that between REM and CEM, REM is better than CEM because the probability is 0.000 < 5%.

Table 7. Chow Test

Table 8. Hausman Test

Table 9. LaGrange Tes

Based on the LaGrange test, the most appropriate model between the general effects model and the random effects model is REM. The REM was chosen as the panel data regression model based on the LaGrange results. Table Panel B represents that the Brush Pagan significance is 0.0000 < sig. 0.05, so the REM was selected. The results of the panel data analysis show that the selected model is the REM, so the classical assumptions required are the normality test and the multicollinearity test. We perform different additional tests to deal with various types of endogeneity issues and the usage of different proxies of performance.

Table 10. Results of the regression analysis

Table Panel C presents the result of the normality test, which shows the Jarque-Bera probability value of 0.07512 > sig 0.05, so the data are spread normally. To make sure there is no correlation between the independent variables, the multicollinearity test was used. The multicollinearity test reveals that the independent variables’ correlation is less than 0.8, so the panel data regression in this study does not have multicollinearity problems.

The following results from the regression of panel data using the REM can be seen in Table Panel A. From 153 units of analysis of 57 HEIs, the results show that there are six significant variables with details of one significant variable at the 10% significance level, four variables at the 5% significance level and one variables at the 1% significance level. In Table Panel A, the independent variable in this study may explain the dependent variable by 31.99%, while the remaining 68.01% is explained by other variables outside the regression, according to the adjusted R-squared value of 27.7%.

Six variables affect SR. SP has a coefficient of 0.063088 (sig 0.0844), CS has a coefficient of 0.055450 (sig 0.0251), SO has a coefficient of −0.016266 (sig 0.0054), SRTP has a coefficient of 0.070772 (sig 0.0149), SC has a coefficient of −0.008237 (sig 0.0186) and FS has a coefficient of 0.068724 (sig 0.0292). The results of the control variable, SE with a coefficient of 0.107491 (sig 0.0000), have a positive effect, and AGE with a coefficient of −0.000405 (sig 0.0025) has a detrimental effect. SIZE, the model’s sole control variable, does not support it.

7. Discussion

The first hypothesis states that SR is positively impacted by SP. The p-value of SP is 0.0844 < sig 1%. Thus, H1 is accepted. It is concluded that SP has a significant positive effect on SR. The results suggest that HEIs with poor SP also publish their performance less. The positive information is spread, while negative information is kept under wraps, especially in the absence of independent performance data. If the parties involved do not believe that a lack of information equates to bad performance and punish non-reporting firms, this partnership will endure. This is reinforced by the absence of government regulations regarding SR. The results provide support for legitimacy theory. The results provide support for previous research showing that SP and SR are interrelated (Al-Tuwaijri et al., Citation2004; De La Poza et al., Citation2021; Grima et al., Citation2018; Jorge et al., Citation2019; Richardson & Kachler, Citation2017; van de Burgwal & Vieira, Citation2014).

The second hypothesis states that CS has a favourable impact on SR, as determined by CS. The p-value of the sign variable is 0.0251 < sig 5%. Thus, H2 is accepted. It is concluded that CS has an important, favourable impact on SR. Encouraging HEIs to sign statements supporting sustainability on campuses is one strategy used by activists to persuade HEIs to enhance sustainability (Lozano et al., Citation2013). This convention-signing would demonstrate a strategic commitment to sustainability, and case studies have utilised this expectation to scrutinise the conduct of HEIs that sign similar declarations but fail to take concrete steps to implement them. The results of this research provide support for legitimacy theory, where one of the approaches taken by activists is to encourage universities to sign sustainability documents as a strategic commitment to sustainability. Universities that sign sustainability declarations will have wider SR disclosures.

The third hypothesis states that office sustainability as measured by the existence of a sustainability office has a positive impact on SR. The p-value of the SO variable is 0.0054 < sig 10%. Therefore, H3 is accepted. It was concluded that SR was positively influenced by SO. The opportunity to publish sustainability reports is greater with the presence of SO as a strategic commitment to sustainability by universities that have sustainability offices have better human and financial resources to create sustainable universities. The results of this research support legitimacy theory, where the public recognizes the commitment of universities in the development, coordination and implementation of sustainability reports. This supports research (Rosenbloom, Citation2017; Uwuigbe et al., Citation2018; Wissink, Citation2012).

The fourth hypothesis states that SRTPs as measured by the presence of SRTP have a positive effect on SR. The SRTP p-value is 0.0200 < sig 5%. The research results show that sustainability research and teaching programs on sustainability and the level of SR by universities show a positive relationship. Thus, H4 is accepted. SRTP represents a clear commitment to sustainability. These results support stakeholder theory. Highlighting the importance of stakeholders in terms of the use of reporting as a tool for managing stakeholders, stakeholder theory offers a number of stakeholders and how they influence reporting. Powerful stakeholders in Higher Education include professors involved in research and teaching initiatives, as well as students. Sustainability teaching and research programs are one way to demonstrate a clear commitment to sustainability (Adams et al., Citation2013; Gumport, Citation2000; McGibbon & Van Belle, Citation2015). Those who have sustainability research and teaching programs related to sustainability will be more expansive in communicating SR. The three functions of higher education, namely research, teaching and community service, are expected to be able to implement sustainability in institutions that have adopted sustainability research and teaching programs. This shows that universities have better human and financial resources to create a sustainable university. According to (Maqbool & Hurrah, Citation2021), the existence of slack resources in an organization is very important.

The fifth hypothesis states that the SC has a favourable impact on SR. The p-value of SC is 0.0186 < sig 5%. Therefore, H5 is accepted. It can be said that SC significantly improves SR. SC can actively affect how much information is disclosed in SR. The primary stakeholders in HEIs are students, and their behaviour on campuses can have an impact on administrative choices (Filho et al., Citation2019). Students are key stakeholders in Higher Education, and their activities have the potential to influence administrative choices. Student initiatives with sustainable campus projects and campus sustainability assessment frameworks are used to guide audits and sustainable development. Because few student organizations are working to advance sustainability on campus and in the community, not many passionate and concerned students are putting bottom-up pressure on their organizations to change their policies and procedures. Based on stakeholder theory, if these sustainability-related student groups are active on campus, HEIs may be more expansive in disclosing SR. HEI management and operations would be more aware of sustainability issues and provide adequate information to stakeholders to assess SP HEI if there were several student clubs dedicated to promoting sustainability on campus and in the community. The results of this research support previous research which shows that students have had a major impact on sustainability research (Beringer et al., Citation2008; Murray, Citation2018; Richardson & Kachler, Citation2017).

The sixth hypothesis states that FS, measured using FSs’ presence, has a favourable impact on SR. The p-value of the SP variable is 0.0292 < sig 5%. Therefore, H6 is accepted. If HEIs have a low commitment to sustainability, then only a small part of the HEIs’ activities will focus on sustainability. Therefore, only a small amount of funds will be allocated to sustainability. This will instantly be relevant to the FSs that serve as accountability for the use of HEIs’ money. FSs are a way for companies to demonstrate their commitments to sustainability. This will be directly relevant to FS which functions as accountability for the use of Higher Education funds. FS is a way for companies to demonstrate their commitment to sustainability. The research results show support for stakeholder theory that PT financial reports and the SR level by PT have a positive relationship. This is automatically relevant to accountability in the form of financial reports on the use of PT funds. Financial reports are a tool that can be used by stakeholders to measure PT’s financial performance. Universities must publish their financial reports, so that it will be easier for stakeholders to monitor sustainability. Financial market players have recently paid more attention to sustainability. The results of this study provide support for previous research (Turan & Lambrechts, Citation2019; Yang et al., Citation2020).

Additional analyses were carried out by involving the control variables as a sensitivity analysis, namely SE, SIZE and AGE and various types of endogeneity issues. With a coefficient of 0.107491 at a significance level of 0.0000 < sig 1%, SE has a statistically significant positive effect. SR depends on how well the presented data capture stakeholder concerns (O’Dwyer & Owen, Citation2005). Low stakeholder involvement from the beginning of the process to ensure the usage of the proper indicators causes low SR because stakeholders do not participate in monitoring. The second control variable is SIZE as measured by the number of students, and it is not found to affect SR. This is due to the low pressure from stakeholders for the sustainability of HEIs so that large and small HEIs do not show any differences regarding sustainability. This is reinforced by the absence of government regulations regarding SR in HEIs. This outcome is consistent with (Jorge et al., Citation2019). The third control variable, AGE, has a significant negative effect with a coefficient of −0.000405 at a significance level of 0.0025 < sig 1%. This means that younger HEIs are more adaptive and better at responding to sustainability concerns.

8. Summary and conclusion

The objective of this study is to investigate the determinants of SR in HEIs using two theoretical perspectives in order to obtain more comprehensive results. This study provides a mapping related to SR by global HEIs that are registered in the GRI database. The results show that first, the level of SR by HEIs registered in the GRI from 2010 to 2020 is satisfactory at 59%. Second, the SR of HEIs is explained by SP, CS, SOs, SRTPs, SCs and FSs. By identifying the factors that influence SR, this study makes two major contributions. First, it provides valuable insight to improve understanding of the determinants influencing the SR practices of HEIs using two theoretical perspectives. Second, by combining multiple theoretical perspectives, namely legitimacy theory and stakeholder theory, this study enriches the literature on SR in the context of HEIs in the setting of emerging markets.

There are two implications of these findings. The theoretical implication suggests that legitimacy theory and stakeholder theory can explain the determinants of SR in the context of HEIs. The practical implication of this study suggests that HEIs may consider our models as a foundation for evaluating their sustainability performance. Therefore, key stakeholders, governments in particular, could take into consideration the regulation of SR at HEIs to support the accomplishment of sustainable development goals.

This study entails several limitations. First, the number of samples of universities that disclose SR is limited. This research only focussed on HEIs registered in the GRI database from 2010 to 2020. The study did not examine the impact of the observation period and the regulations during the study. Future studies could consider testing the determinants of HEIs in a larger context, such as the external factors of higher education institutions. Testing these factors will provide more robust results.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Maylia Pramono Sari

Maylia Pramono Sari is a lecturer of Accounting at the Department of Accounting, Universitas Negeri Semarang. She has been taking the Doctoral Program in Economics Faculty of Economics and Business Universitas Diponegoro, Semarang, Indonesia. She has published some articles in Cogent Business & Management, Montenegrin Journal of Economics, Quality Access to Success, International Journal of Sustainable Development and Planning; Journal of Governance and Regulation; Humanities & Social Sciences Reviews; International Journal of Financial Research; International Journal of Scientific & Technology Research; International Journal of Innovation, Creativity and Change; International Journal of Advanced Science and Technology; Academy of Accounting and Financial Studies Journal, Journal of Legal, Ethical and Regulatory Issues; Academy of Strategic Management Journal; Investment Management and Financial Innovations; Journal of Positive School Psychology.

Faisal Faisal

Faisal Faisal is a Professor of Accounting at the Department of Accounting, Universitas Diponegoro, Semarang, Indoensia. His main research is in sustainability reporting and enterprise risk management area. He has published some articles in the Journal of Financial Crime, International Journal of Emerging Market, Corporate Social Responsibility and Environmental Management, Cogent Economics & Finance, International Journal of Business Governance and Ethics, Cogent Business & Management; Australasian Accounting Business and Finance Journal; Journal of Human Resource Costing and Accounting, International Journal of Managerial and Financial Accounting.

Puji Harto

Puji Harto is a doctor of Accounting at the Department of Accounting, Universitas Diponegoro, Semarang, Indonesia. His main research is on corporate social responsibilities and good governance area. His main research is on corporate social responsibilities and good governance area. He has published some articles in the Journal of Islamic Accounting and Finance Research; the Academy of Accounting and Financial Studies Journal, the Journal of Public Health Research and Development, the Journal of Asian Finance, Economics and Business; International Journal of Supply Chain Management; International Journal of Scientific and Technology Research, International Journal of Energy Economics and Policy; Journal of Economics, Finance and Administrative Science.

References

- Abad Segura, E., & González-Zamar, M.-D. (2021). Sustainable economic development in higher education institutions: A global analysis within the SDGs framework. Journal of Cleaner Production, 294, 126133. https://doi.org/10.1016/j.jclepro.2021.126133

- Adams, C. A. (2002). Internal organisational factors influencing corporate social and ethical reporting: Beyond current theorising. Accounting Auditing & Accountability Journal, 15(2), 223–27. https://doi.org/10.1108/09513570210418905

- Adams, C. A., Mader, G. S., & Dzulkifli Abdul Razak, C. (2013). Sustainability reporting and performance management in universities: Challenges and benefits. Sustainability Accounting, Management and Policy Journal, 4(3), 384–392. https://doi.org/10.1108/SAMPJ-12-2012-0044

- Alawneh, R., Jannoud, I., Rabayah, H., & Ali, H. (2021). Developing a novel index for assessing and managing the contribution of sustainable campuses to achieve un sdgs. Sustainability, 13(21), 1–16. https://doi.org/10.3390/su132111770

- Alghamdi, N., den Heijer, A., & de Jonge, H. (2017). Assessment tools’ indicators for sustainability in universities: An analytical overview. International Journal of Sustainability in Higher Education, 18(1), 84–115. https://doi.org/10.1108/IJSHE-04-2015-0071

- Ali, E. B., & Anufriev, V. P. (2020). UI greenmetric and campus sustainability: A review of the role of African universities. International Journal of Energy Production and Management, 5(1), 1–13. https://doi.org/10.2495/EQ-V5-N1-1-13

- Ali, W., Frynas, J. G., & Mahmood, Z. (2017). Determinants of Corporate social responsibility (CSR) disclosure in developed and developing countries: A literature Review. Corporate Social Responsibility and Environmental Management, 24(4), 273–294. https://doi.org/10.1002/csr.1410

- Alonso-Almeida, M. D. M., Marimon, F., Casani, F., & Rodriguez-Pomeda, J. (2015). Diffusion of sustainability reporting in universities: Current situation and future perspectives. Journal of Cleaner Production, 106, 144–154. https://doi.org/10.1016/j.jclepro.2014.02.008

- Al-Tuwaijri, S. A., Christensen, T. E., & Hughes, K. E. (2004). The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Accounting, Organizations & Society, 29(5–6), 447–471. https://doi.org/10.1016/S0361-3682(03)00032-1

- Amber, W., & Ruiz, M. (2010). Sustainability assessment in higher education institutions. The STARS System. Ramon Llull Journal of Applied Ethics, 1(1), 25–42. http://www.raco.cat/index.php/rljae/article/view/270545/358109

- Ardillah, K. (2021). Environmental Accounting and reporting: Case study of Accounting education in Indonesia’s universities that includes in qs World University Rankings.

- Atici, K. B., Yasayacak, G., Yildiz, Y., & Ulucan, A. (2021). Green university and academic performance: An empirical study on UI GreenMetric and world university rankings. Journal of Cleaner Production, 291, 125289. https://doi.org/10.1016/j.jclepro.2020.125289

- Barth, M., Godemann, J., Rieckmann, M., Stoltenberg, U., & Adomssent, M. (2007). Developing key competencies for sustainable development in higher education. International Journal of Sustainability in Higher Education, 8(4), 416–430. https://doi.org/10.1108/14676370710823582

- Bautista-Puig, N., Orduña-Malea, E., & Perez-Esparrells, C. (2022). Enhancing sustainable development goals or promoting universities? An analysis of the times higher education impact rankings. International Journal of Sustainability in Higher Education, 23(8), 211–231. https://doi.org/10.1108/IJSHE-07-2021-0309

- Bedin, É. P., & Faria, L. C. D. (2021). Sustainability in higher education institutions (HEI): Merging the study Systematic Review, analysis content and bibliometrics. Macro Management & Public Policies, 3(3), 42–53. https://doi.org/10.30564/mmpp.v3i3.3670

- Bekessy, S. A., Samson, K., & Clarkson, R. E. (2007). The failure of non-binding declarations to achieve university sustainability: A need for accountability. International Journal of Sustainability in Higher Education, 8(3), 301–316. https://doi.org/10.1108/14676370710817165

- Belal, A. H., Al-Majed, A., & Khalil, N. Y. (2002). Spectrofluorimetric determination of vigabatrin and gabapentin in urine and dosage forms through derivatization with fluorescamine. Journal of Pharmaceutical & Biomedical Analysis, 27(1–2), 253–260. https://doi.org/10.1016/S0731-7085(01)00503-9

- Belal, A. R., Owen, D. L., & Adams, C. A. (2007). The views of corporate managers on the current state of, and future prospects for, social reporting in Bangladesh: An engagement-based study. Accounting Auditing & Accountability Journal, 20(3), 472–494. https://doi.org/10.1108/09513570710748599

- Beringer, A., Wright, T., & Malone, L. (2008). Sustainability in higher education in Atlantic Canada. International Journal of Sustainability in Higher Education, 9(1), 48–67. https://doi.org/10.1108/14676370810842184

- Berman, S. L., Wicks, A. C., Kotha, S., & Jones, T. M. (1999). Does stakeholder orientation matter? The relationship between stakeholder management models and firm financial performance. Academy of Management Journal, 42(5), 488–506. https://doi.org/10.2307/256972

- Bilodeau, L., Podger, J., & Abd-El-Aziz, A. (2014). Advancing campus and community sustainability: Strategic alliances in action. International Journal of Sustainability in Higher Education, 15(2), 157–168. https://doi.org/10.1108/IJSHE-06-2012-0051

- Brammer, & Pavelin. (2004). Building a Good Reputation. European Management Journal, 22(6), 704–713. https://doi.org/10.1016/j.emj.2004.09.033

- Brown, J., & Fraser, M. (2006). Approaches and perspectives in social and environmental accounting: An overview of the conceptual landscape. Business Strategy and the Environment, 15(2), 103–117. https://doi.org/10.1002/bse.452

- Caeiro, S., Hamón, L. A. S., Martins, R., & Aldaz, C. E. B. (2020). Sustainability assessment and benchmarking in higher education institutions-a critical reflection. Sustainability (Switzerland), 12(2), 1–30. https://doi.org/10.3390/su12020543

- Caesaria, A. F., & Basuki, B. (2017). The study of sustainability report disclosure aspects and their impact on the companies’ performance. SHS Web of Conferences, 34, 08001. https://doi.org/10.1051/shsconf/20173408001

- Calitz, A., Bosire, S., & Cullen, M. (2018). The role of business intelligence in sustainability reporting for South African higher education institutions. International Journal of Sustainability in Higher Education, 19(7), 1185–1203. https://doi.org/10.1108/IJSHE-10-2016-0186

- Campbell, D. (2003). Effects in environmental disclosures: Evidence for legitimacy theory? Business Strategy and the Environment, 12(6), 357–371. https://doi.org/10.1002/bse.375

- Caputo, F., Ligorio, L., & Pizzi, S. (2021). The contribution of higher education institutions to the SDGs—an evaluation of sustainability reporting practices. Administrative Sciences, 11(3), 97. https://doi.org/10.3390/admsci11030097

- Carpenter, V. L., & Feroz, E. H. (2001). Institutional theory and accounting rule choice: An analysis of four US state governments’ decisions to adopt generally accepted accounting principles. Accounting, Organizations & Society, 26(7–8), 565–596. https://doi.org/10.1016/S0361-3682(00)00038-6

- Ceulemans, K., Lozano, R., Alonso-Almeida, M., & Del, M. (2015). Sustainability reporting in higher education: Interconnecting the reporting process and organisational change management for sustainability. Sustainability, 7(7), 8881–8903. https://doi.org/10.3390/su7078881

- Cho, C. H., & Patten, D. M. (2007). The role of environmental disclosures as tools of legitimacy: A research note. Accounting, Organizations & Society, 32(7–8), 639–647. https://doi.org/10.1016/j.aos.2006.09.009

- Clarke, J., & Gibson‐Sweet, M. (1999). The use of corporate social disclosures in the management of reputation and legitimacy: A cross sectoral analysis of UK top 100 companies. Business Ethics: A European Review, 8(1), 5–13. https://doi.org/10.1111/1467-8608.00120

- Clarkson, M. E. (1995). A stakeholder framework for analyzing and evaluating Corporate social performance. Academy of Management Review, 20(1), 92–117. https://doi.org/10.2307/258888

- Corazza, L. (2018). The process of social accounting and reporting at University of Torino: Main challenges and managerial implications. World Review of Entrepreneurship Management and Sustainable Development, 14(1–2), 171–186. https://doi.org/10.1504/WREMSD.2018.089073

- Cormier, D., & Magnan, M. (1999). Corporate environmental disclosure strategies: Determinants, costs and benefits. Journal of Accounting, Auditing & Finance, 14(4), 429–451. https://doi.org/10.1177/0148558X9901400403

- Crossley, R. M., Elmagrhi, M. H., & Ntim, C. G. (2021). Sustainability and legitimacy theory: The case of sustainable social and environmental practices of small and medium-sized enterprises. Business Strategy and the Environment, 30(8), 3740–3762. https://doi.org/10.1002/bse.2837

- Deegan, C. (2002). Introduction: The legitimising effect of social and environmental disclosures – a theoretical foundation. Accounting Auditing & Accountability Journal, 15(3), 282–311. https://doi.org/10.1108/09513570210435852

- Deegan, C. (2004). Environmental disclosures and share prices - a discussion about efforts to study this relationship. Accounting Forum, 28(1), 87–97. https://doi.org/10.1016/j.accfor.2004.04.007

- Deegan, C. (2010). Organizational legitimacy as a motive for sustainability reporting. Sustainability Accounting and Accountability, 127–149.

- Deegan & Blomquist. (2006). Stakeholder influence on Corporate reporting: An exploration of the interaction between the world wide fund for nature and the Australian minerals industry.

- Deegan, C., Rankin, M., & Tobin, J. (2002). An examination of the corporate social and environmental disclosures of BHP from 1983-1997: A test of legitimacy theory. Accounting Auditing & Accountability Journal, 15(3), 312–343. https://doi.org/10.1108/09513570210435861

- de Grosbois, D. (2016). Corporate social responsibility reporting in the cruise tourism industry: A performance evaluation using a new institutional theory based model. Journal of Sustainable Tourism, 24(2), 245–269. https://doi.org/10.1080/09669582.2015.1076827

- De La Poza, E., Merello, P., Barberá, A., & Celani, A. (2021). Universities’ reporting on SDGs: Using the impact rankings to model and measure their contribution to sustainability. Sustainability, 13(4), 1–30. https://doi.org/10.3390/su13042038

- de Villiers, C., & van Staden, C. J. (2006). Can less environmental disclosure have a legitimising effect? Evidence from Africa. Accounting, Organizations & Society, 31(8), 763–781. https://doi.org/10.1016/j.aos.2006.03.001

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in Organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101

- Dobson, A., Quilley, S., & Young, W. (2010). Sustainability as competitive advantage in higher education in the UK. International Journal of Environment and Sustainable Development, 9(4), 330–348. https://doi.org/10.1504/IJESD.2010.035612

- Dowling, J., & Pfeffer, J. (1975). Pacific Sociological Association Organizational Legitimacy: Social Values and Organizational Behavior. Source: The Pacific Sociological Review, 18(1), 122–136. https://doi.org/10.2307/1388226

- Elmagrhi, M. H., & Ntim, C. G. (2022). Vice-chancellor pay and performance: The moderating effect of Vice-chancellor characteristics. Work, Employment and Society, 1–26. https://doi.org/10.2139/ssrn.4134997

- Elmagrhi, M. H., & Ntim, C. G. (2023). Non-financial reporting in non-profit organisations: The case of risk and governance disclosures in UK higher education institutions. Accounting Forum, 47(2), 223–248. https://doi.org/10.1080/01559982.2022.2148854

- Ferrero, I., Fernández-Izquierdo, M. Á., Muñoz-Torres, M. J., & Bellés-Colomer, L. (2018). Stakeholder engagement in sustainability reporting in higher education: An analysis of key internal stakeholders’ expectations. International Journal of Sustainability in Higher Education, 19(2), 313–336. https://doi.org/10.1108/IJSHE-06-2016-0116

- Filho, W. L., Emblen-Perry, K., Molthan-Hill, P., Mifsud, M., Verhoef, L., Azeiteiro, U. M., Bacelar-Nicolau, P., de Sousa, L. O., Castro, P., Beynaghi, A., Boddy, J., Salvia, A. L., Frankenberger, F., & Price, E. (2019). Implementing innovation on environmental sustainability at universities around theworld. Sustainability (Switzerland), 11(14), 1–16. https://doi.org/10.3390/su11143807

- Filho W. L., Tortato, U., & Frankenberger, F. (2019). Universities and sustainable communities: Meeting the goals of the agenda. Issue February.

- Firmialy, S. D., Wiryono, S. K., & Nainggolan, Y. A. (2019). Exploring the bi-directional relationship of stock return and sustainability performance through the sustainability risk lens (case of Indonesia). Jurnal Perspektif Pembiayaan dan Pembangunan Daerah, 7(2), 127–142. https://doi.org/10.22437/ppd.v7i2.7663

- Fonseca, A., Macdonald, A., Dandy, E., & Valenti, P. (2011). The state of sustainability reporting at Canadian universities. International Journal of Sustainability in Higher Education, 12(1), 22–40. https://doi.org/10.1108/14676371111098285

- Freeman, R. E. (2010). Strategic management: A stakeholder approach. Cambridge university press.

- Galleli, B., Teles, N. E. B., Santos, J. A. R. D., Freitas-Martins, M. S., & Hourneaux Junior, F. (2021). Sustainability university rankings: A comparative analysis of UI green metric and the times higher education world university rankings. International Journal of Sustainability in Higher Education, 23(2), 404–425. https://doi.org/10.1108/IJSHE-12-2020-0475

- Geerts, M., Dooms, M., & Stas, L. (2021). Determinants of sustainability reporting in the present institutional context: The case of port managing bodies. Sustainability (Switzerland), 13(6), 10–13. https://doi.org/10.3390/su13063148

- Gómezgutiérrez, D., Alejandro, J., & Sepúlveda, M. (2017). Sustainability indicators for universities: Revision for a Colombian case. Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc, 17(5). 2249-4596.

- Gray, R. (2010). Is accounting for sustainability actually accounting for sustainability…and how would we know? An exploration of narratives of organisations and the planet. Accounting, Organizations & Society, 35(1), 47–62. https://doi.org/10.1016/j.aos.2009.04.006

- Gray, R., Kouhy, R., & Lavers, S. (1995). Corporate social and environmental reporting a review of the literature and a longitudinal study of UK disclosure. Accounting Auditing & Accountability Journal, 8(2), 47–77. https://doi.org/10.1108/09513579510146996

- GRI. (2020). GRI index.

- Griebeler, J. S., Brandli, L. L., Salvia, A. L., Leal Filho, W., & Reginatto, G. (2021). Sustainable development goals: A framework for deploying indicators for higher education institutions. International Journal of Sustainability in Higher Education, 23(4), 887–914. https://doi.org/10.1108/IJSHE-03-2021-0088

- Guix, M., Bonilla-Priego, M. J., & Font, X. (2018). The process of sustainability reporting in international hotel groups: An analysis of stakeholder inclusiveness, materiality and responsiveness. Journal of Sustainable Tourism, 26(7), 1063–1084. https://doi.org/10.1080/09669582.2017.1410164

- Gumport, P. J. (2000). Academic restructuring: Organizational change and institutional imperatives. Higher Education, 39(1), 67–91. https://doi.org/10.1023/A:1003859026301

- Gunarsih, T., Setiyono, S., Sayekti, F., & Novak, T. (2020). Bi-directional in sustainability reporting and profitability: A study in Indonesian banks and non-banks. Jurnal Keuangan dan Perbankan, 24(1), 20–29. https://doi.org/10.26905/jkdp.v24i1.3588

- Guthrie, J., & Parker, L. D. (1989). Corporate social reporting: A rebuttal of legitimacy theory. Accounting and Business Research, 19(76), 343–352. https://doi.org/10.1080/00014788.1989.9728863

- Hamilton, S. N., & Waters, R. D. (2022). Mainstreaming standardized sustainability reporting: Comparing fortune 50 corporations’ and U.S. News & world report’s top 50 global universities’ sustainability reports. Sustainability, 14(6), 3442. https://doi.org/10.3390/su14063442

- Hansen, B., Stiling, P., & Uy, W. F. (2021). Innovations and challenges in SDG integration and reporting in higher education: A case study from the University of South Florida. International Journal of Sustainability in Higher Education, 22(5), 1002–1021. https://doi.org/10.1108/IJSHE-08-2020-0310

- Hummel, K., & Schlick, C. (2016). The relationship between sustainability performance and sustainability disclosure – reconciling voluntary disclosure theory and legitimacy theory. Journal of Accounting and Public Policy, 35(5), 455–476. https://doi.org/10.1016/j.jaccpubpol.2016.06.001

- Ingram, R. W., & Frazier, K. B. (1980). Environmental performance and Corporate disclosure. Journal of Accounting Research, 18(2), 614. https://doi.org/10.2307/2490597

- Jain, S., Aggarwal, P., Sharma, N., & Sharma, P. (2013). Fostering sustainability through education, research and practice. Journal of Cleaner Production, 61, 20–24. https://doi.org/10.1016/j.jclepro.2013.04.021

- Johnston, R. B. (2016). Arsenic and the 2030 agenda for sustainable development. Arsenic Research and Global Sustainability - Proceedings of the 6th International Congress on Arsenic in the Environment, AS 2016, 12–14. https://doi.org/10.1201/b20466-7

- Jorge, M., Andrades Peña, F. J., & Herrera Madueño, J. (2019). An analysis of university sustainability reports from the GRI database: An examination of influential variables. Journal of Environmental Planning and Management, 62(6), 1019–1044. https://doi.org/10.1080/09640568.2018.1457952

- Kim, D., Henriques, I., & Miller, K. (1999). Academy of/Management Review Stakeholder Influence Strategies.

- Lauder, A., Sari, R. F., Suwartha, N., & Tjahjono, G. (2015). Critical review of a global campus sustainability ranking: GreenMetric. Journal of Cleaner Production, 108, 852–863. https://doi.org/10.1016/j.jclepro.2015.02.080

- Laufer, D., & Coombs, W. T. (2006). How should a company respond to a product harm crisis? The role of corporate reputation and consumer-based cues. Business Horizons, 49(5), 379–385. https://doi.org/10.1016/j.bushor.2006.01.002

- Lozano, R. (2010). Diffusion of sustainable development in universities’ curricula: An empirical example from Cardiff University. Journal of Cleaner Production, 18(7), 637–644. https://doi.org/10.1016/j.jclepro.2009.07.005