?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study looks into a theoretical model exploring the effects of ownership shares and directors’ proportions as majority shareholders on earnings management. Furthermore, the primary objective of this research is to investigate the moderating role of board meeting frequency between ownership shares and directors’ proportions as majority shareholders on earnings management. The current study employed a quantitative research methodology, using firms in Iraq from 2013 to 2018. In panel data regression, the researchers implemented three distinct models: the random effect model, the fixed effect model, and the common pooled model. The data were provided in two columns, one with control variables and one without control variables. This study also presents empirical evidence that ownership of shares by directors and majority shareholders was significant, implying that an increased number of shares possessed by directors and high majority shareholders would reduce earnings management. While the frequency of board meetings had no significant moderating effect on the relationship between director share ownership and earnings management, it did play a significant moderating role in the relationship between directors’ proportion as majority shareholders and earnings management. Finally, the contribution of these empirical findings as research makes a valuable addition to the existing body of academic literature on earnings management, particularly within the context of the Iraq earnings management scenarios. It also has the potential to make a meaningful contribution towards mitigating the prevalence of earnings management practices. Moreover, it offers unique insights into the significance of corporate governance in the context of Iraqi financial institutions.

1. Introduction

The emergence of accounting scandals in several areas, including Asia, the United States, and Europe, has prompted concern over the practice of earnings management (abbreviated as EM) efficacy standards. The anxieties are real, without a doubt, valid. Enron Corporation’s bankruptcy in 2001 is a well-known illustration of the devastation that may result from poor EM (Manab et al., Citation2015; Omware et al., Citation2020). The controversy drew public attention to developing better EM standards to prevent fraud and improper EM. The immediate responses were proposed EM reforms and enhanced listing standards (Kjærland et al., Citation2020). Consequently, the first motivation behind this study stems from the underlying notion that a correlation exists between insufficient corporate governance (abbreviated as CG) and efficacy standards for earning management.

However, corporate governance (CG) is not a novel concept. According to Jensen and Meckling (Citation1976), its requirement arose when a response to the split of ownership and control in public enterprises produced agency issues. As a result, the CG system presented reliable financial data and safeguarded shareholders’ interests (Fama & Jensen, Citation1983). The board’s guardian role becomes clear as financial information preparers and users’ knowledge asymmetry allows opportunism (Daghsni et al., Citation2016). Additionally, CG can decrease or even eliminate fraudulent behavior. Therefore, Mrabure and Abhulimhen-Iyoha (Citation2020) talked about how well corporate governance (CG) could protect shareholder interests from EM practices by setting up frameworks for things like openness, accountability, protecting minority shareholders, aligning interests, risk management, access to capital, and the legal and regulatory framework. They provide accurate and timely information about a company’s performance, financial health, and governance practices, mitigating the risks associated with opaque reporting.

CG frameworks also establish mechanisms for oversight, i.e. independent boards of directors as well as audit committees, to prevent abuses of power and fraud. Chen et al. (Citation2006) also link executive compensation to company performance, incentivizing management to behave in the best interests of shareholders. The effectiveness of CG depends on the legal and regulatory framework in the emerging market. Here, the level of board activity moderates the complex interplay between directors’ ownership of shares in the corporate governance context, especially when they hold a sizable portion as majority shareholders. One significant challenge lies in mitigating conflicts of interest that may arise when directors, driven by their significant shareholdings, navigate decisions that impact corporate performance and shareholder value. The imperative to balance personal financial gains with the broader interests of the company necessitates robust mechanisms for identifying, disclosing, and managing such conflicts (Zaid et al., Citation2020). The second motivation is that oversight issues emerge as a second challenge, requiring a vigilant and independent board to guarantee that the processes of decision-making remain objective as well as aligned with the company’s strategic goals rather than individual directorial interests.

Additionally, the third motivation is accountability issues, which further complicate this landscape, emphasizing the need for clear lines of responsibility and consequences for governance lapses (Ehren & Perryman, Citation2018). Transparency becomes paramount to address these challenges, demanding comprehensive disclosure practices that shed light on the intricate relationships between directors’ share ownership, earnings management, and board activities. Fourth and lastly, the risk of ethics violations looms large, underscoring the importance of fostering a corporate culture rooted in ethical principles to safeguard against misconduct and warrant the long-term viability and continuity of the organization. In navigating these multifaceted challenges, corporations must continually refine their governance frameworks to strike a delicate balance between shareholder interests, ethical conduct, and effective oversight.

Moreover, the agency theory discussed (specifically, the efficient monitoring hypothesis), that managerial ownership serves as a crucial external capital market governance (CG) instrument due to its advanced nature and effectiveness in information reception and processing. In general, institutional investors are more successful in mitigating information asymmetry in capital markets and constraining managerial discretion. Institutional investors engage in a firm’s governance in two ways: directly (via ownership) and indirectly (via the trading of their shares), according to Gillan and Starks (Citation2000). On how managerial ownership influences EM, scholars appear to adopt two different positions. One line of inquiry posits that the ongoing trading and dispersed ownership of institutional investors impede their ability to engage in active monitoring of the companies in which they have invested. An argument that is connected to Githaiga (Citation2023) posits that institutional proprietors might be disinclined to carry out their oversight responsibilities due to the potential adverse impact on their business relationships with the organization. As a consequence, institutional investors will prioritize immediate financial gains, and managers will face significant pressure to fulfill anticipated short-term objectives.

Consequently, managerial ownership may not restrict the flexibility of managers in EM and may even enhance their motivation to engage in EM. Despite extensive scholarly investigation into whether institutional ownership alleviates EM in different jurisdictions, the findings of these studies have been inconclusive. Some researchers found a negative correlation between EM and the percentage of ownership in an institution. To illustrate, Potharla et al. (Citation2021) examined the impact of EM and institutional ownership in India, utilizing data from 2011 to 2018 and a sample of 257 firms. It was determined that institutional ownership exerted a notably adverse influence. Gerged et al. (Citation2021) looked at 100 Jordanian-listed companies from 2010 to 2014 and found a negative relationship between earnings management and the amount of institutional ownership. They did this by looking at 500 firm-year observations. Furthermore, Velury and Jenkins (Citation2006) demonstrated a noteworthy positive correlation between earnings quality and institutional ownership, which suggests a reduced presence of EM. In their 2012 study, Lin and Manowan (Citation2012) examined a dataset consisting of 18,969 firm-year observations obtained from active US firms listed on Compustat between 1996 and 2001. The researchers documented an inverse correlation.

Nevertheless, a limited number of studies, including Peasnell et al. (Citation2005), which examined a sample of UK companies and found no correlation between institutional ownership and EM, dispute this notion. Kolsi and Grassa (Citation2017), utilizing panel data for 2004–2012 and a sample of 26 Islamic banks in the Gulf Cooperation Council (GCC) region, found no correlation between institutional ownership and EM. Furthermore, Chatterjee (Citation2020) determined, through the use of panel data and a sample of 783 private manufacturing enterprises in India spanning the years 2009 to 2016, that neither factor had an independent influence on EM. Moreover, using data from 2014 to 2019, Abou-El-Sood and El-Sayed (Citation2022) found no correlation between institutional ownership and the EM study of 225 publicly traded companies in the MENA region.

Extensive previous research has been done on corporate governance (CG) as well as executive compensation (EM), mostly in economies that use either two-tier or one-tier executive compensation structures. Notable examples include the United States, the United Kingdom, Italy, the Middle East in Egypt, Malaysia, as well as China in Southeast Asia (Abdulsamad et al., Citation2018; Alquhaif et al., Citation2017; Claessens & Yurtoglu, Citation2013; Khalil & Ozkan, Citation2016; Shahwan, Citation2015; Zalata et al., Citation2021), in which all have EM models that differ from the Iraq CG model in numerous respects. According to Ahmed et al. (Citation2021), to get good CG in Iraq, two main distinguishing aspects are the powers given to a majority of shareholders to effectively oversee the corporation and the fully non-executive board, rather than relying on the market for corporate control; significant shareholders typically participate actively in the company’s governance. As a result, the structure encourages controlling owners to take long-term responsibility for the organization.

Furthermore, the competitiveness of Iraqi enterprises in local markets demonstrates their success, and the ‘Iraq environment’ in globally competitive league tables suffers from poor economic competitiveness. Although Iraq’s new CG law frameworks exist, there has been less scholarly investigation conducted on the association of CG as well as EM in nations that follow the EM (The World Bank, Citation2019).

Therefore, this paper is willing to fill in the gaps about how ownership shares and the number of directors as major shareholders affect earnings management. Although most prior studies have concentrated on the usual way that corporate governance and earnings management work together, they have not looked at how these practices can change depending on the environment of the business and the ownership structure type. This work, thus, aims to reexamine the existing research on the correlation between the elements that contribute to the efficiency of the board of directors at an individual level, such as ownership shares, directors’ proportion as majority shareholders, and management practices. It also tests whether board activity, such as meeting frequency, mediates the relationship between ownership shares and directors’ proportion as major shareholders in earnings management. Hence, this study’s findings will be of interest to nations that adhere to similar structures of governance, encompassing the interaction between the board of directors, shareholders, and management, such as Jordan and several countries in the Arabic Gulf region. The study also attempts to draw attention to the possible benefits of the Iraq CG strategy to enhance profit quality by reducing EM. For that reason, the following main research questions are posed: Do the corporate governance mechanisms (ownership shares and directors’ proportion as majority shareholders) affect the earnings management of Iraqi listed companies? Does board activity play a moderating role in the correlation among ownership shares, directors’ proportion as majority shareholders, and the earnings management of Iraqi listed companies?

This study is significant because it aids corporate governance practitioners in restricting the use of earnings management strategies. This, in turn, leads to increased satisfaction among stakeholders and investors, especially in the Iraqi context. Hence, this study establishes a foundation for assessing whether the current optimal methods and criteria for inclusion improve effective management in the economic conditions of Iraq. The results are anticipated to offer more guidance to the Iraqi Securities Commission, Bursa Iraqi, and the Iraqi Institute of Corporate Governance regarding the corporate governance methods employed by Iraqi companies. The study also helps stakeholders, beneficiaries, and authorities devise policies that contribute to retaining transparency and credibility in financial reports.

Meanwhile, studying this issue helps lower agency cost rates, which could save firms millions of dollars in investment, not to mention preserving the integrity and image of the reports in Iraqi firms. It also helps develop firms in terms of performance to improve overall firm performance through the frequency of board meetings. Further, the study objective is to examine the effects of mechanisms of corporate governance, such as ownership shares and directors’ proportions as majority shareholders on earnings management as well as the moderate role of board activity in the Iraq context.

The subsequent sections of this work are organized as follows. The current section is designated as the first one, while the subsequent section is referred to as the background. The third section of the document serves as a theoretical review, while the fourth section focuses on literature and hypothesis creation. In this area, previous studies are reviewed, and hypotheses are formulated. The fifth section outlines the research design, while the empirical results are reported in the sixth section. The final section provides a concise overview of the article’s findings and analysis. Finally, the conclusion and the study’s limitations are presented at the end.

2. Background

Considerably, a company’s performance is associated with earnings, and earnings represent a summary of the performance, which is calculated using the accrual accounting method. In addition, prior research has shown that companies are inclined to employ these accounts to control announced profits (Cassell et al., Citation2015). Thus, earnings-based performance measures may lead to earnings management, called EM (Tahir et al., Citation2019). In this regard, there are many definitions of EM. As Healy and Wahlen (Citation1999) stated, earnings management (EM) refers to the deliberate use of subjective assessments by managers to alter financial figures. first, to influence stakeholders’ impressions of the company’s economic performance, or second, to affect the conclusion of a contractual agreement. However, firms have two options for managing earnings, as stated in the definition. For example, the managers may increase reported earnings by cutting and reselling assets that would retain and decrease employee development (Dakhlallh, Citation2020). Real EM deviates from the process of influencing reported income (Thiruvadi & Huang, Citation2011). Furthermore, a corporation may make modifications to accruals to attain the desired level of earnings. Accrual-based earnings management relies on managerial discretion in the preparation of financial reporting (Subramanyam, Citation1996). As a result, it is acceptable to conclude that organizations with lower earning thresholds are manipulated through accruals rather than actual operations (Kjærland et al., Citation2020). Therefore, this research’s focus is solely on EM.

Literature has also looked into a variety of reasons for managing earnings. There are many managerial objectives, including corporate value optimization (Beneish, Citation2001), initiated buyouts by management (Chung & Kallapur, Citation2003), initial public offerings (Gras-Gil et al., Citation2012), and satisfying financial experts, management, investors, and social and political pressure (Awfi, Citation2017; Cassell et al., Citation2015; Sachs et al., Citation2006; Zalata et al., Citation2019). The management has flexibility in presenting their stated earnings, and this is the essence of earnings management (Riahi & Arab, Citation2011). Nonetheless, information asymmetry is the next control challenge. On this point, asymmetry happens when managers know more about the firm than shareholders, and they prioritize their own interests over that of the stockholders, resulting in agency costs (Al-Shaer et al., Citation2017). A previous study has linked agency costs to EM latitude (Harris et al., Citation2019). EM must link the interests of senior management with those of shareholders to prevent EM. The sentence suggests that a key strategy to prevent earnings management is to guarantee that the senior management’s interests (such as executives and top-level decision-makers) are aligned with those of shareholders. When the incentives for management are strongly linked to the long-term performance of the firm and the value it provides to shareholders, they are less inclined to participate in short-term manipulative strategies that artificially inflate earnings.

However, the scope of the study is that Iraqi publicly traded organizations are to be subjected to a study of earnings management in non-financial as well as financial firms. Several factors contributed to the selection of Iraq as the research site for this study, including the fact that the nation has a long history of violence. To establish the presence of the agency problem, the research challenge must be met, making Iraq a relevant environment in which the agency problem is still present as a starting point. Second, the great majority of prior research was carried out in other countries, and at this time, there is no evidence accessible on these practices in Iraqi culture. Although many features of nations are shared in other areas, there are considerable disparities in corporate governance laws and listing requirements, institutional ownership concentration in a firm, and the balance between ownership of shares and directors’ proportion as majority shareholders on board structures. Because of these differences, the results of empirical studies undertaken in these nations will likely be inapplicable to the realities of Iraqi society.

In contrast to the auditor and other company laws, the legal systems demonstrated divergent views of investor protection laws, resulting in a different enforcement environment compared to those laws. This has an impact on the quality of reporting, with governance guidance laws showing weak enforcement when compared with other auditor and corporate laws, thereby affecting the quality of reporting. Aside from the banking as well as insurance industries, investment and financial services, industrial manufacturing, agriculture, telecommunications, hotel and tourism industries, and other sectors.

Here, the board of directors serves as an internal regulatory system to supervise the actions of managers. Cosma et al. (Citation2018) indicated that the board of directors is accountable for ensuring that the firm is managed in the shareholders’ interests for the long term. Although there is no recognized definition, the term ‘it’ refers to a comprehensive system that includes people, protocols, and operations that together provide effective management and protection of assets (Mousavi & Moridipour, Citation2013).

In addition, the data on the impact of CG policies on EM is equivocal. Thus, this current study includes board features extensively researched in the EM literature; essential features of the Iraq CG model will be investigated, including ownership of shares by directors and directors’ proportion as majority shareholders and the frequency of board meetings as moderating variables. The frequency means the board meetings are used to quantify board activity and are frequently used to signify the directors’ efforts. This paper used the activities of the board as moderator to investigate the ownership of shares by directors and the directors’ proportion as majority shareholders in a number of the meetings, affecting the practices of EM. Salem et al. (Citation2019) stated that an engaged board of directors is thought to be more successful in monitoring management. Akpan (Citation2015) notes that a widespread issue among directors is a lack of time to fulfill their duties, suggesting that more frequent board meetings will push directors to serve shareholders. The subject matter under consideration is literature on the activities of the board, and EM is rife with contradictions. Previous research by Daghsni et al. (Citation2016) has shown that having more board meetings often monitors board activities and keeps EM practices more effective. According to Alzoubi (Citation2019), frequent meetings decrease practices at the EM level. In comparison, other research exposes a positive link between the board meeting and EM (Daghsni et al., Citation2016) or no effect at all (Handayani & Ibrani, Citation2020). Based on contradicting literature, this study conducts an investigation.

3. Theoretical review

3.1. Agency theory and institutional theory

Earnings management, as defined by Klein (Citation2002), refers to the deliberate manipulation of a company’s financial performance to distort its true nature. Managerial manipulation refers to the act of managers using their judgment to arrange transactions in financial reports with the intention of either deceiving stakeholders about the actual financial condition or impacting transactions that rely on the reported accounting values. It is worth mentioning that companies in emerging markets engage in more earnings management than those in developed economies (Li et al., Citation2011). Although there has been a significant amount of research on the factors that influence earnings management in developed markets, such as the US and UK (e.g. Bédard et al., Citation2004; Wang & Yung, Citation2011), there is a lack of understanding and empirical evidence regarding the methods and motivations behind earnings management in emerging economies.

Theoretical perspectives propose agency theory, which holds that the splitting up of managers as well as shareholders may lead to contradictory objectives (Ball, Citation2013). This misalignment of goals may result in managers exercising discretion to manipulate earnings to align them closely with target levels, thereby attaining personal control benefits and pursuing self-interested aims. Notably, most research on earnings management based on agency theory has been done in developed markets or a single country. It has not looked into how earnings management activities change in countries with very different ways of owning businesses.

Related to that, the authors posit that the conventional agency theory (Jensen & Meckling, Citation1976) may not provide a comprehensive explanation for the variations in earnings management observed in emerging markets. This is because both firm-level and country-level factors that influence managerial behavior differ significantly from the Anglo-American governance system. On the other hand, the theory of institutionalized agency (Aguilera & Jackson, Citation2003; Seal, Citation2006; Zalata et al., Citation2019) improves understanding of how firm-level governance and national institutional issues affect earnings management. Agency and institutional theories acknowledge that their institutional environment has a significant impact on managers and owners/shareholders. These contexts influence the way individuals assess information, exercise their discernment, and articulate their decisions (Aguilera & Jackson, Citation2003; Filatotchev et al., Citation2013; Hoenen & Kostova, Citation2015; Ning et al., Citation2014). More precisely, it enables the examination of the particular patterns of shareholder concentration that are frequently seen in developing market countries, as well as the different types of ownership that are prominent in these regions (Chen & Yu, Citation2012; Filatotchev et al., Citation2013).

Nevertheless, in developing countries, companies demonstrate a less clear distinction between ownership and management in comparison to their counterparts in developed markets like the US and UK (Chen & Yu, Citation2012; Filatotchev et al., Citation2013). Publicly traded corporations in emerging nations often have a concentrated ownership structure, where top managers act as controlling shareholders or directly represent them. This underscores the need to reassess conventional theoretical methodologies in earnings management research, which typically concentrate on the conflicts between principals (owners) and agents (managers). Adopting an institutionalized agency theory approach recognizes that managers are agents who possess power granted by legal owners. Meanwhile, it also acknowledges that values and rules that are considered acceptable in a particular institutional setting also influence their actions (Seal, Citation2006). This paradigm establishes a connection between managerial accounting procedures and external institutional forces, making it more suitable for comprehending how ownership governance mechanisms within firms impact earnings management activities in emerging markets. Furthermore, it gives a useful lens for comprehending how aspects of the institutional context might affect these relationships.

4. Literature and hypotheses development

4.1. Ownership of shares on earnings management

Contemporary companies with widespread ownership and a need for expertise cannot personally oversee their operations. Consequently, they employ managers to handle the day-to-day running of the business on their behalf (Khuong et al., Citation2019). Managers have a responsibility to act in the best interest of the owners, but occasionally, they act in their own self-interest, which creates the principal-agent problem (Tahir et al., Citation2019). Agency theory, as described by Jensen and Meckling (Citation1976), is crucial for understanding how managers behave when they assign tasks to others, with the expectation that the person they delegate to would make decisions that align with the principal’s best interests. The concept of agency theory elucidates the phenomenon of earnings management, as it posits that managers are driven to manipulate earnings to augment their bonuses, compensations, and commissions, which are intricately linked to the financial performance of the organization. Managers are compelled to seek profit intentions in any behavior for their advantage, particularly in the short run (Khuong et al., Citation2019).

On the other hand, ownership of shares represents the ownership interest that individuals or entities have in a company. Individuals who possess shares in a firm are considered shareholders. The extent of their ownership is determined by the ratio of their shares to the total number of outstanding shares. Shareholders generally possess the privilege to participate in voting on specific issues that impact the firm, including the selection of directors, significant corporate choices, and modifications to the company’s bylaws. Shareholders have the potential to receive dividends as a form of profit on their investment, and they can also experience financial gains through the increase in value of their shares, known as capital appreciation.

Since ownership of shares by directors is deemed one of the CG characteristics, it is impossible to make a definitive theoretical forecast concerning the impact of ownership shares by directors on EM (Idris et al., Citation2018). Opportunistically, directors’ share ownership may reduce transparency, independence, and efficacy in overseeing financial statements. In this context, it is anticipated that managers of firms characterized by limited director ownership would use the discretionary flexibility afforded by accounting regulations to mitigate financial constraints. Therefore, depending on the ownership structure, the theoretical assumptions will also change. Ali et al. (Citation2008) indicated that long-term directors’ share ownership increases board and shareholder financial interest in the majority stakeholder in the firm. Consequentially, a long-term ownership view is compelled to prioritize the firm’s long-term growth strategy.

Furthermore, it highlights the significance of adopting a short-term ownership viewpoint that could potentially work against the company’s and the shareholders’ optimal interests. The contradictory assumptions in previous research on ownership of shares by directors and EM are reflected in the results. Evodila et al. (Citation2020) found a favorable correlation between ownership of directors’ shares and EM. On the contrary, in an old study, Ali et al. (Citation2008) uncovered a significant negative relationship. In addition, Kazemian and Sanusi (Citation2015) discovered no significant link in their meta-analysis. Based on the existing theoretical and empirical arguments, this study formulated the initial hypothesis:

(H1). Directors’ ownership of shares is inversely correlated with earnings management.

4.2. Directors’ proportion as majority shareholders

Directors’ percentage as majority shareholders suggests a scenario in which a sizable number of directors also hold a sizable stake in the company’s shares. The latter situation can impact corporate governance and decision-making dynamics within the company. Conflicts of interest in this relationship may arise in ways that differ from the owners’ expectations. Managers anticipate obtaining their advantages by engaging in actions that impact the shareholders’ interests. To mitigate conflicts of interest between those who provide mandates and those who receive them, it is necessary to establish monitoring procedures that restrict managerial self-interest. These are important issues because they affect the benefits for both the authorized parties and those authorized.

The correlation between majority shareholder ownership and earnings management can be intricate and contingent on the specific circumstances. According to Brennan (Citation2021), earnings management is the deliberate alteration of a company’s financial statements with the aim of achieving specific goals, such as fulfilling earnings targets, influencing stock prices, or portraying a more positive financial image than the actual economic situation. Here are a few ways in which majority shareholder ownership can be related to earnings management. First, the majority shareholders, especially those with a controlling interest, may have significant control and influence over the company’s management and decision-making. With greater control, Shareholders that possess a larger portion of the company’s shares have the ability to influence and put pressure on management to manipulate the company’s earnings to meet specific financial goals or present a more positive financial image to investors.

The second is the alignment of interests. In some cases, majority shareholders may have aligned interests with minority shareholders, seeking to enhance the overall value of the company. In such situations, there may be less incentive for earnings management, which could harm the company’s long-term prospects. The third is conflicts of interest. Conflicts of interest can arise if the majority shareholders’ interests diverge from those of minority shareholders. For example, the dominant shareholders may prioritize short-term profits, even if it involves manipulating earnings to benefit from higher stock prices or meet specific financial targets. The fourth is market perception. The majority of shareholders may be concerned about how the market perceives the financial performance of the company. EM can be used to create a positive image and maintain or increase the stock price, benefiting both majority and minority shareholders. Fifth is regulatory compliance. The regulatory environment can play a role in shaping the association between earnings management and majority shareholder ownership. Companies with majority shareholders may be subject to different governance requirements, and the regulatory framework can influence the degree of transparency and accountability.

Nevertheless, it is crucial to emphasize that the association between majority shareholder ownership and earnings management is contingent on various factors, including the specific dynamics of the company, the industry, the regulatory environment, and the individual motivations of the majority shareholders. Additionally, ethical considerations and the potential legal consequences of engaging in earnings management practices are critical factors that can influence the behavior of majority shareholders (Bhagat & Bolton, Citation2008), suggesting that increasing director share ownership will reduce the incidence of EM (Al-Fayoumi et al., Citation2010). Directors’ shareholdings are also related to lower information asymmetry (Jalan et al., Citation2020), potentially lowering agency costs and helping prevent EM (Katmon & Farooque, Citation2017). The research conducted by Goh et al. (Citation2013) investigates the impact of majority shareholder ownership on the manipulation of actual earnings. The investigation aims to determine if there is a conflict or agreement between the interests of majority and minority shareholders. A higher level of majority shareholder ownership reduces the extent of real earnings management when the interests of majority and minority shareholders are in agreement. Conversely, if the interests of majority owners and minority shareholders are not in agreement, there will be a rise in the manipulation of financial statements by majority shareholders, resulting in inflated earnings.

On the other hand, as the majority shareholder ownership increases, there is a large decline in actual earnings management within the bracket of upward earnings management incentives. This phenomenon mostly arises due to the heightened sensitivity of majority shareholders towards upward manipulation of actual results, which in turn has a detrimental impact on future performance. These findings indicate that when majority shareholders have a higher ownership stake, they are more effective in reducing the manipulation of actual earnings. This constructive role has had a sole impact on the years following the Asian economic crisis. These findings suggest that the economic downturn in Korea has heightened the awareness of most shareholders regarding the long-term expenses associated with real earnings management. The findings corroborate the convergence of interest hypothesis by examining actual earnings management as opposed to accruals-based earnings management. Yanping et al. (Citation2021) also looked into how equity pledges and the major shareholders’ shareholding ratio affect earnings management in Chinese A-share listed companies. They found that the shareholding ratio weakened the link between upward earnings management and equity pledges. These studies collectively imply that a variety of factors, such as the particular governance structure and the type of earnings management under consideration, have an impact on the correlation between earnings management and directors’ proportion as majority shareholders. Furthermore, a study conducted by Kim et al. (Citation2018) utilizing Korean corporations found that an increase in the ownership of the largest shareholders is associated with a decrease in the risk of equity mispricing in the quarters leading up to a Seasoned Equity Offering (SEO). The level of REM also reduces favorable market responses to ownership increases by the largest shareholders. The authors’ conclusion is that corporations manipulate their earnings to benefit the majority shareholders rather than the other shareholders. Thus, considering the discourse in this area, this study posited the second hypothesis:

(H2). Directors’ proportion as majority shareholders is inversely correlated with earnings management.

4.3. The frequency of board meetings as moderating role

According to Kjærland et al. (Citation2020), the number and length of the meetings indicate the extent of the board’s activity. Similar to Fadzilah (Citation2017), the board meetings indicate the board’s activity level as well as the degree of communication between the directors and stakeholders. Besides, Wai Kee et al. (Citation2017) revealed that a board that frequently meets better leads to improving the role of governance in monitoring financial reporting. Hence, more board meetings mean an opportunity to consider various boards’ decisions and quickly get to the final results (Al-Matari et al., Citation2014; Zaman et al., Citation2018). At the same time, Kjærland et al. (Citation2020) stated that the frequency of board meetings could bring about higher management monitoring quality, positively impacting the companies’ financial performance.

Consequently, holding board meetings more frequently can enhance the quality of profits by ensuring regular monitoring and supervision of the financial statements of the company (Kankanamage, Citation2016). Agency theory elucidates the correlation between the frequency of board meetings and the practice of earnings management. Elnahass et al. (Citation2022) found that in accordance with agency theory, a board that has more frequent meetings enhances its ability to provide valuable counsel, oversight, and discipline. In addition, as stated by Sáenz González and García-Meca (Citation2014), it resulted in a drop in the absolute value of discretionary accruals, in line with the premise of effective oversight suggested by agency theory. Furthermore, agency theory suggests that stakeholders and agents frequently have conflicting interests (Jensen & Meckling, Citation1976). Enhancing oversight and regulation is necessary to mitigate the agency’s conflict of interest. According to Ugwoke et al. (Citation2013), the board of directors should actively supervise the company’s operations to protect the interests of the shareholders, as viewed from the standpoint of agency theory. Daghsni et al. (Citation2016) also suggested that the board of directors should be prepared to increase the frequency of board meetings to provide heightened monitoring and control as necessary.

Therefore, many researchers revealed that the increase in board meeting frequency leads to fewer practices of earnings management and increases transparency in financial reports (Kankanamage, Citation2016). Therefore, Sukeecheep et al. (Citation2013) indicated that board meetings often allow for the observation of the activities of the board to limit the earnings management practice more effectively. Obigbemi et al. (Citation2016) also signified that it leads to a lower discretionary accrual value whenever the board has more meetings. Nevertheless, numerous studies have been conducted on the correlation between the frequency of board meetings and the practice of earnings management. Research has indicated a direct correlation between profit manipulation and the frequency of board meetings (Daghsni et al., Citation2016). Simultaneously, some research has discovered a detrimental correlation between the frequency of board meetings and the practice of manipulating earnings (Abbadi et al., Citation2016; Azzoz & Khamees, Citation2016; Fadzilah, Citation2017; Kankanamage, Citation2016). On the other hand, Sukeecheep et al. (Citation2013) found no significant link between how often board meetings are held and the practice of manipulating earnings. Consistent with this discussion, the study proposed the following third and fourth hypotheses:

(H3). The frequency of board meetings moderates the effect of directors’ ownership of shares on earnings management.

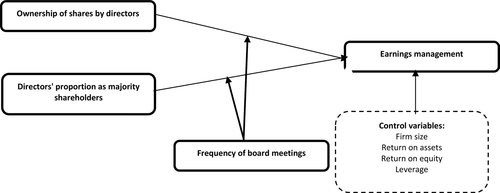

(H4). The frequency of board meetings moderates the effect of directors’ proportion as majority shareholders on earnings management ().

Figure 1. The research framework.

5. Research method

The present study utilized a quantitative methodology, focusing on the financial and non-financial enterprises listed on the Iraq Stock Exchange (ISX). The reason for combining the financial as well as non-financial Iraqi firms is that earnings management practices, the process of procedure in which managers participate in earring manipulation, are similar in both firms, whether financial or non-financial since the author’s focus is on earnings management (Talab et al., Citation2017). The Iraqi business laws offer identical provisions for both the financial and non-financial sectors. One of the reasons to examine Iraq is the destruction of infrastructure and capital components caused by terrorist actions, together with the loss of economic indicators due to a major decrease in oil prices in 2014 and 2015 (www.isx-iq.net). In addition to the fact that the Iraqi market for securities law was passed in 2004, there have been no effective investments by international corporations in Iraq in a way that stimulates the market’s activation. Besides, due to the disparity in capital between Iraqi companies and companies in the surrounding nations, the companies in the surrounding countries cannot be compared to Iraqi enterprises. For example, the capital requirements of Iraqi government-owned enterprises are tighter than in neighboring nations. These structural challenges constitute a significant hindrance to the efficient and cost-effective implementation of Iraq’s significant long-term reconstruction demands, as well as the short-term imperative to prioritize capital investment effectively, given the need for fiscal consolidation (The World Bank, Citation2019). The Iraqi Securities and Exchange Commission (ISXC) mandates that all firms listed in Iraq must provide disclosure of information pertaining to their stock offerings, annual reports, and reporting on significant events. The ISXC states that an annual report shall include the board of directors’ report. Therefore, public annual reports can provide information and data on corporate governance processes, earnings management techniques, and firm performance.

The study employed the purposive sampling technique to sample Iraqi financial as well as non-financial companies. According to Sekaran and Bougie (Citation2016), the inclusion and exclusion procedures to obtain the final samples are as follows. Initially, utility industries were excluded from the sample due to their distinct characteristics and the potential impact of specific laws on the outcomes. In addition, the utility industry was not included in the analysis because it follows conservative accounting practices that delay the reporting of income. This is because these industries operate based on fixed accounting rates of return. Hence, identifying managers’ opportunistic manipulative conduct would be a challenging issue. Furthermore, many insurance and investment organizations were not considered due to discrepancies in market values. These discrepancies arise from the inclusion of additional criteria, such as the value of operational choices. Furthermore, money transfer service companies were specifically excluded due to their distinct accounting rules, which pose challenges in accurately estimating discretionary accruals.

The present study used a sample of the listed firms on the Iraq Stock Exchange from 2013 to 2018. The sample consisted of publicly listed companies in Iraq from 2013 to 2018 (six years of observations) at the balance sheet date. The study was constrained to six years of data since the firm’s performance and earnings management practices often change over time. Additionally, the recent data for Iraqi firms with fewer missing numbers on the DataStream database was available from 2013 to 2018. One reason for selecting Iraqi companies for six years is the relatively small number of companies listed on the Iraqi stock exchange. These companies, both financial and non-financial, contribute significantly to the overall economic output. This ensures that the sample size is sufficient for conducting statistical procedures. Following that, the study used easily accessible data from the company’s website, www.isx-iq.net, and financial reports to the general public and other researchers. The selected firms were derived from the overall population of firms listed on the Iraqi stock exchange. The study initially included a total of 19 non-financial and 51 financial firms from the entire pool of Iraqi companies. These companies were selected from a total of 129 financial and non-financial companies registered on the Iraqi stock exchange for the period of 2013–2018. presents a concise overview of the specific information of the sample.

Table 1. Sample size.

reveals the unbalanced structure of the panel data. The presence of uneven panel data can be attributed to the varying listing dates of the companies. Firstly, a whole population of 129 firms was selected from the Iraqi Stock Exchange (ISX) in 2013. Of the 129 firms, 70 firms had a full six-observation year. The remaining firms had observations that spanned from one to four years. Several companies initiated their listing on the stock exchanges in various years, while several companies were removed from the exchanges after enduring three consecutive years of financial loss without a recovery. Hence, this study focused on analyzing a sample of 70 companies that were listed on the Iraqi Stock Exchange from 2013 to 2018, resulting in a total of 432 observations. In addition, the sectors (i.e. manufacturing, service, beverages, and construction) are not different from the non-financial institutions mentioned in . This is because the non-financial firms are referred to as ‘institutions (see column 3)’. Thus, beverages were grouped under agriculture. Service was grouped under Telecom, while construction was grouped under hotel and tourism. The data were then analyzed using STATA 13 because of its extensive use and widespread acceptance in panel data estimate techniques.

5.1. Measurement

5.1.1. Earnings management (EM)

In most of the literature on EM, the discretionary accruals approach for detecting EM was utilized. In this regard, to determine total accruals, the prior studies have differentiated among three commonly utilized approaches: the approach of balance sheet (Healy, Citation1985; Hill & Jones, Citation1992), the approach of cash flow (Moratis & van Egmond, Citation2018), and approach based on a financial statement (Beneish, Citation2001). Nevertheless, the cash flow technique directly quantifies discretionary accruals from the statement of cash flow, thus mitigating the risk of measurement mistakes. Therefore, this study utilized the financial statement approach to ascertain EM. Consequently, to calculate EM using the financial statement, the following model was used:

M-score shows the score of manipulation. The firm has earnings management if the result is more significant than −2.22 (Talab et al., Citation2017).

5.1.2. Ownership of shares by directors

This variable was assessed as the proportion of shares held by the directors out of the total number of shares issued (Idris et al., Citation2018). Therefore, the proxy for this variable was the number of directors who owned corporate shares directly or indirectly.

5.1.3. Directors’ proportion as majority shareholders

Directors’ proportion as majority shareholders refers to a situation where a majority of the directors also happen to be major shareholders (own a significant portion of the company’s shares) Yanping et al. (Citation2021). The proxy for this variable was the proportion of directors who held a majority of shares.

5.1.4. Frequency of board meetings

The frequency of board meetings is indicative of the level of activity of the board since it reflects both the number and duration of the sessions (Kjærland et al., Citation2020). The indicator for this variable was the frequency of board meetings conducted annually.

5.2. Control variables

5.2.1. Firm size

The impact of firm size on earnings management methods is considered to be significant (Cosma et al., Citation2018). The study conducted by Gull et al. (Citation2018) discovered a positive correlation between business size and EM level. The variable business size in this study was measured using the logarithm of total assets (SIZE).

5.2.2. Return on assets

The researchers included the Return on Assets (ROA) metric in their study as it is a financial indicator commonly used by companies (Evodila et al., Citation2020). Hence, the calculation of return on assets (ROA) was performed by dividing the net income by the total assets ratio (Pham & Tran, Citation2020).

5.2.3. Return on equity

The return on equity (ROE) is a financial metric that assesses a company’s profitability in relation to its equity. It is calculated by dividing the net income by the average shareholders’ equity. Therefore, Return on Equity (ROE) is calculated by dividing the net income of a fiscal year by the total equity and expressing it as a percentage.

5.2.4. Leverage

Leverage has been extensively utilized as a control variable according to Evodila et al. (Citation2020), which defined leverage as a variable that more clearly indicates the contracting’s possible problems. In this regard, a previous study (Fadzilah, Citation2017) measured the total debt of the firm divided by total assets. Therefore, the variable measurement in this research was the proportion of aggregate debt to aggregate assets (see ).

Table 2. Corporate governance variables measurement.

5.3. Model

The researchers developed the subsequent model to investigate the effect of CG (directors’ proportion as majority shareholders and ownership of shares by directors) and board activities as moderators on EM. In the current study, utilizing the statistical software ‘STATA’, the authors analyzed the data. From a theoretical standpoint, the relationship between the independent and dependent variables is described by a linear model. This means that the underlying theory of the phenomenon being examined assumes that the relationship between the independent variable(s) and the dependent variable is linear in nature. A linear model postulates that each alteration in the independent variable(s) leads to a commensurate alteration in the dependent variable. The study examined the relationship between variables. The variables that are influenced by other factors and the variables that are not influenced by other factors in this study are displayed in .

Table 3. Research variables.

The utilized regression model was panel data regression analysis. Panel data regression encompasses three distinct modeling approaches: the common/pooled model, fixed-effect model, and random effect model (Baltagi, Citation2005). Model selection tests were conducted to ascertain the optimal model that elucidated the relationship between variables and the rationale for its selection. The panel data regression is because it can be more statistically efficient than other forms of analysis since it exploits both cross-sectional and time-series variations, leading to more precise parameter estimates. displays the panel selection tests.

Table 4. Panel model selection test.

Once the best model was chosen, a conventional assumption test was conducted. This test verifies the model’s ability to observe the relationship between variables and forecast the value of the dependent variable based on the known value of the independent variable (Gujarati, Citation2004). The results of the classical assumption tests are displayed in .

Table 5. Classical assumption test.

After selecting the best model that matched the classical assumptions, the following phase involved testing the model’s quality (Walpole, Citation2012). The advantages of model tests are shown in . Once all the test requirements of the model were satisfied, the interpretation of the derived regression equation was conducted.

Table 6. Goodness test model.

6. Results and discussion

The discussion commences by employing descriptive analysis to ascertain the attributes of each variable in the study throughout the duration of the research. presents a comprehensive examination of the data.

Table 7. Descriptive analysis.

For the regression model to be valid, it is necessary for there to be no significant multicollinearity among the independent variables. This can be determined by examining the Variant Inflation Factor (VIF) value, which should be <10. All independent variables in this investigation had a VIF value of <10, as shown in . This outcome indicates that all independent variables are suitable for inclusion in the model.

Table 8. Multicollinearity test.

Before doing a detailed investigation of modeling in panel data regression analysis, panel model selection was carried out. The authors employed the tests described in the methodology section by conducting three tests, as indicated in . Fixed effect models were deemed optimal for elucidating the associations between research variables.

Table 9. Panel model selection test.

After the panel model was chosen, it was subjected to classical assumption testing rather than direct interpretation. The purpose of this test was to determine whether or not the chosen model could discern the impact of prediction. The assumptions that were applied included autocorrelation, heteroscedasticity, and normality. A breach of normality, heteroscedasticity, and the presupposition of autocorrelation persisted in . Each test had a probability value that was lower than 0.05.

Table 10. Classical assumption test.

In light of violations of heteroscedasticity and autocorrelation assumptions, Panel Corrected Standard Error/PCSE models were employed to transform fixed models (Greene, Citation2018). The ultimate mode employed is detailed in of the Regional Income.

Table 11. Hypothesis test.

The coefficient of determination was 0.1624 in the absence of the control model and 0.968 with the control variable, as shown in . The coefficient’s value indicates that in the absence of the control variable, the independent variables could account for 16.24% of the variance in the M-score, while in its presence, they could account for 96.8%. Other extraneous variables affected the remainder. As determined by the Regional Income Chi-square test, the M-score was influenced by each of the independent variables. The statistical probability value for identifying these results was chi-square = 0.00, which is significantly smaller than alpha = 0.05. The findings suggest that the modeling that was conducted was suitable.

Based on , all significant and influential variables were included in the summary derived from the partial test identified with the probability value, the t-test, for which the probability value was 0.000 < alpha 0.05. Onw_Sh, proportion, and MF had a significant positive effect on the M-score. MF had a moderated effect on proportion but not moderated Onw_Sh to M-score. In addition, control variables were not a central issue in this research. The authors added a control variable to strengthen the relationship, and the control variable increased the coefficient determination from 0.16 to 0.968. The significant variables were Fsize, Frmlev, and ROE.

Table 12. Summary.

In this research, ownership of shares by directors and majority shareholders was significant, implying that an increased number of shares owned by directors as well as majority shareholders will reduce EM. However, when they hold stock in the firm, directors are said to be more independent and more able to oversee their companies without bias. Consequently, companies are less prone to agency issues and EM (Lin & Hwang, Citation2010). Still, the frequency of board meetings did not exert a big effect on the relationship between directors’ ownership of shares and EM. This signified that the frequency of board meetings did not have much of an effect on directors’ ownership of shares, which increased the EM of Iraqi firms.

Here are a few reasons why the frequency of board meetings did not yield a big effect on the relationship between directors’ ownership of shares and EM. First, increased pressure, such as frequent board meetings, may create pressure on management to fulfill or surpass financial targets consistently. This pressure may potentially motivate executives to implement earnings management strategies to portray a more favorable financial picture, especially if there is a culture of unrealistic expectations or if executive compensation is tied to performance metrics. The second is limited oversight. Paradoxically, a high frequency of board meetings might result in superficial or ineffective oversight if board members are overwhelmed with information or lack the necessary expertise to scrutinize financial reports thoroughly. In such cases, management might exploit the situation by engaging in earnings management practices that could go unnoticed. Third is opportunities for manipulation. More frequent interactions between management and the board might provide additional opportunities for collusion or persuasion. Management could use these interactions to manipulate board members or present information in a biased manner, potentially facilitating earnings management activities.

In contrast, the frequency of board meetings’ moderating role on the association between directors’ proportion as majority shareholders and EM was significant. This means that the meeting frequency acts as a moderator in the above correlation, where a board with a majority of directors as shareholders will be more careful in making decisions. This indicates that the frequency of board meeting practices is vital in encouraging management to come up with good decisions in Iraqi firms, which can further reduce their EM.

7. Conclusion

Earnings management is an aggressive phenomenon that has persisted in the business world, including Iraq, and is increasing in prevalence there. Academics, regulatory bodies, and corporations are collaboratively endeavoring to identify the most effective corporate governance mechanism capable of eradicating this conduct. Not only is it of the utmost importance to prevent this opportunistic conduct, but earnings management has the detrimental effect of undermining the aims and objectives of organizations. The statistical analysis of the study’s results revealed that directors and high majority shareholders owned a significant number of shares; therefore, an increase in the number of shares held by these individuals would result in a decrease in EM. In contrast, the frequency of board meetings moderated the relationship between directors’ proportion as majority shareholders and EM in a significant way. In contrast, it had no significant effect on the relationship between interest paid by directors and ownership of shares by directors.

This study presents several contributions to the concept of empirical evidence that supports the implementation of mechanisms of corporate governance, which has varying impacts on the magnitude of earnings management practices. First, the findings highlight the significance of corporate governance attributes in enhancing firm performance and reducing unethical behaviors within Iraqi-listed companies. Second, the research provides significant insights for stakeholders, such as investors, analysts, accounting and auditing professionals, and other relevant parties to disseminate information to stakeholders concerning corporate governance efficiency, and the result also enhances public awareness of the overall level of corporate governance effectiveness. Third, the study supports the management in forming a well-defined overview of the most significant earnings management practices for Iraqi firms and the Middle East in general. Fourth, the study provides insights into the Iraqi Accounting Standard Board for future accounting standards due to the fact that Iraqi financial sector regulations have been struggling with the insertion of corporate governance laws (OECD, Citation2019). Therefore, such an examination will reinforce the environment of the economy as well as impact firm performance while also contributing to bridging some gaps in the issues of corporate governance laws to limit earnings management practices in Iraqi companies.

Practically, this study applies to researchers and practitioners in the Iraqi business context. First, the varied impact of corporate governance evidence supports the idea that distinct mechanisms of corporate governance have varying impacts on the practices of earnings management. Understanding these variations is crucial for designing effective governance frameworks that enhance firm performance and mitigate unethical behaviors. Second, the research has implications for various stakeholders, including investors, analysts, accounting and auditing professionals, and other relevant parties. These stakeholders can use the insights from the study to make informed decisions, assess corporate governance effectiveness, and enhance understanding of the dynamics between earnings management and governance mechanisms. The third is to enhance public awareness of the overall effectiveness level of corporate governance within Iraqi listed companies.

Furthermore, transparency in governance practices is crucial for building trust and confidence among the general public, and the research emphasizes the role of governance in achieving this transparency. Lastly, the study is not only applicable to Iraqi-listed companies but also has broader implications for nations with similar governance structures, such as Jordan and various countries in the Arabic Gulf region. This suggests that the interface between the board of directors, shareholders, and management is a universal concern, and the insights gained from this study can be valuable across different contexts.

The limitation of this study is that it did not provide in-depth details about the strength or shape of those relationships or more statistical analysis, such as effect sizing and sensitivity analysis, which could provide a better understanding of the dynamics involved because the current research model will need at least one more variable to check sensitivity analysis. Based on future research, the authors could add more variables and conduct effect sizing and sensitivity analysis. One other suggestion for future research directions is that since archival data served as the basis for measuring all of this study’s variables, the authors think mixed-method research designs would be extremely beneficial for future research. Bringing together these sources with first-hand information from surveys will also enhance researchers’ comprehension of managers’ perspectives and convictions regarding earnings management, as well as the influence of institutional forces in emerging markets. This will aid researchers in providing answers to several pivotal inquiries pertaining to earnings management and corporate governance. Inquiry, such as the following: To what extent do controlling shareholders influence managers to manipulate earnings, and to what extent are board members genuinely ‘independent’ from controlling shareholders? The authors anticipate that the utilization of qualitative data will serve to further demonstrate the suitability of institutionalized agency theory as a framework for comprehending governance in emerging markets.

Author contributions

Study conception and design: Farida Titik Kristanti; data collection: Hosam Alden Riyadh; analysis: Mohammed Ghanim Ahmed, Salsabila Aisyah Alfaiza, Evy Steelyana, and Abdalwali Lutfi; draft manuscript preparation and interpretation of results: Baligh Ali Hasan Beshr. The results were evaluated by all authors and the final version of the publication was approved by them.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The investigation utilized data from the websites of several firms and publicly available reports.

Additional information

Funding

Notes on contributors

Farida Titik Kristanti

Dr. Farida Titik Kristanti is an Associate Professor in Accounting and is currently vice dean for human resources and finance affairs at the School of Economics and Business at Telkom University, Indonesia. Her main research interests are corporate finance, family firms, small businesses, and gender diversity.

Hosam Alden Riyadh

Dr. Hosam Alden Riyadh is an assistant professor, lecturer, and researcher at Telkom University, Indonesia. His main research interests are financial accounting, corporate governance, and CSR. Dr.Hosam is a Certified Sustainability Reporting Specialist (CSRS) and a Certified Sustainability Reporting Assurer (CSRA).

Mohammed Ghanim Ahmed

Dr. Mohammed Ghanim Ahmed is a lecturer and researcher who obtained his Ph.D. degree from Universiti Sains Malaysia, Malaysia. His main research interests are financial accounting, corporate governance, and sustainability. Currently is joined to Nineveh Real Estate Bank, Iraqi Ministry of Finance, Iraq.

Salsabila Aisyah Alfaiza

Salsabila Aisyah Alfaiza is a lecturer and researcher at the School of Economics and Business at Telkom University, Indonesia. Her main research interests are general management and entrepreneurship. Salsabila Aisyah Alfaiza is currently a Ph.D. candidate at the University of Utara Malaysia.

Evy Steelyana W

Evy Steelyana W. has been serving as a lecturer and researcher at BINUS University since 2002, with a concentration in financial accounting, accounting management, and financial modelling. Her research has been published in several international publications (the Scopus Index), and she remains active in presenting her research at international academic conferences. Her field research focuses on public finance, public sector accounting, governance, and public-private partnerships. She is a professional with more than 20 years of experience in various sectors, both in the financial and banking sectors as well as in the real sector, both in global and local companies.

Abdalwali Lutfi

Dr. Abdalwali Lutfi is an associate professor in the college of business administration at King Faisal University. Dr. Lutfi holds a PhD in Accounting and Accounting Information System from the University Utara Malaysia. His teaching and research interests are in the areas of accounting and accounting information systems. Abdalwali Lutfi, one of the top 2% of scientists in the world.

Baligh Ali Hasan Beshr

Dr. Baligh Ali Hasan Beshr is Associate Professor in the Department of Administrative Sciences, College of Administrative and Financial Science, Gulf University, Sanad 26489, Kingdom of Bahrain. Dr. Baligh is a Ph.D. holder in Human Resource Management at Abdelmalek Saadi University in Morocco. Specialisation: Management and Development, Specialisation: Human Resources Management, He is a certified international trainer in human development by the International Federation of Human Resources, the International Business Academy in Kingstone, Britain, and the International Academy for Training in Britain, UK.

References

- Abbadi, S., Hijazi, Q., & Al-Rahahleh, A. (2016). Corporate governance quality and earnings management: Evidence from Jordan. Australasian Accounting, Business and Finance Journal, 10(2), 1–21. https://doi.org/10.14453/aabfj.v10i2.4

- Abdulsamad, A. O., Wan Fauziah, W. Y., & Lasyoud, A. A. (2018). The influence of the board of directors’ characteristics on firm performance: Evidence from Malaysian public listed companies. Corporate Governance and Sustainability Review, 2(1), 6–13. https://doi.org/10.22495/cgsrv2i1p1

- Abou-El-Sood, H., & El-Sayed, D. (2022). Abnormal disclosure tone, earnings management and earnings quality. Journal of Applied Accounting Research, 23(2), 402–433. https://doi.org/10.1108/JAAR-07-2020-0139

- Aguilera, R. V., & Jackson, G. (2003). The cross-national diversity of corporate governance: Dimensions and determinants. The Academy of Management Review, 28(3), 447. https://doi.org/10.2307/30040732

- Ahmed, M. G., Ganesan, Y., Hashim, F., & Sadaa, A. M. (2021). The effect of chairman tenure on governance and earnings management: A case study in Iraq. Journal of Asian Finance, Economics and Business, 8(3), 1205–1215. https://doi.org/10.13106/jafeb.2021.vol8.no3.1205

- Akpan, E. O. (2015). Corporate board meetings and company performance: Empirical evidence from Nigerian quoted companies. Global Journal of Commercial & Management Perspective, 4(1), 75–82.

- Al-Fayoumi, N., Abuzayed, B., & Yan, P. (2010). Ownership structure and earnings management in emerging markets: The case of Jordan. International Research Journal of Finance and Economics, 38, 29–45.

- Ali, S. M., Saleh, N. M., & Hassan, M.-S. (2008). Ownership structure and earnings management in Malaysian listed companies: The size effect. Asian Journal of Business and Accounting, 1, 89–116.

- Al-Matari, E. M., Al-Swidi, A. K., & BtFadzil, F. H. (2014). The effect on the relationship between board of directors characteristics on firm performance in Oman: Empirical study. Middle-East Journal of Scientific Research, 21(3), 556–574. https://doi.org/10.5829/idosi.mejsr.2014.21.03.21410

- Alquhaif, A. S., Latif, R. A., & Chandren, S. (2017). Women in board of directors and real earnings management: Accretive share buyback in Malaysia. Asian Journal of Finance & Accounting, 9(2), 48. https://doi.org/10.5296/ajfa.v9i2.11752

- Al-Shaer, H., Salama, A., & Toms, S. (2017). Audit committees and financial reporting quality. Journal of Applied Accounting Research, 18(1), 2–21. https://doi.org/10.1108/JAAR-10-2014-0114

- Alzoubi, E. S. S. (2019). Audit committee, internal audit function and earnings management: evidence from Jordan. Meditari Accountancy Research, 27(1), 72–90. https://doi.org/10.1108/MEDAR-06-2017-0160

- Awfi, Y. N. A. L. (2017). Ownership concentration: Its determinants and the impact on firm performance. Evidence from MENA region. Business School University of Portsmouth.

- Azzoz, A. R. A. M., & Khamees, B. A. (2016). The impact of corporate governance characteristics on earnings quality and earnings management: Evidence from Jordan. Jordan Journal of Business Administration, 12(1), 187–207. https://doi.org/10.12816/0030061

- Ball, R. (2013). Accounting informs investors and earnings management is rife: Two questionable beliefs. Accounting Horizons, 27(4), 847–853. https://doi.org/10.2308/acch-10366

- Baltagi, B. H. (2005). Econometric analysis of panel data (3rd ed.). John Wiley & Sons Ltd.

- Bédard, J., Chtourou, S. M., & Courteau, L. (2004). The effect of audit committee expertise, independence, and activity on aggressive earnings management. AUDITING: A Journal of Practice & Theory, 23(2), 13–35. https://doi.org/10.2308/aud.2004.23.2.13

- Beneish, M. D. (2001). Earnings management: A perspective. Managerial Finance, 27(12), 3–17. https://doi.org/10.1108/03074350110767411

- Bhagat, S., & Bolton, B. (2008). Corporate governance and firm performance. Journal of Corporate Finance, 14(3), 257–273. https://doi.org/10.1016/j.jcorpfin.2008.03.006

- Brennan, N. M. (2021). Connecting earnings management to the real world: What happens in the black box of the boardroom? The British Accounting Review, 53(6), 101036. https://doi.org/10.1016/j.bar.2021.101036

- Cassell, C. A., Myers, L. A., & Seidel, T. A. (2015). Disclosure transparency about activity in valuation allowance and reserve accounts and accruals-based earnings management. Accounting, Organizations and Society, 46, 23–38. https://doi.org/10.1016/j.aos.2015.03.004

- Chatterjee, C. (2020). Board quality and earnings management: Evidence from India. Global Business Review, 21(5), 1302–1324. https://doi.org/10.1177/0972150919856958

- Chen, C.-J., & Yu, C.-M J. (2012). Managerial ownership, diversification, and firm performance: Evidence from an emerging market. International Business Review, 21(3), 518–534. https://doi.org/10.1016/j.ibusrev.2011.06.002

- Chen, G., Firth, M., Gao, D. N., & Rui, O. M. (2006). Ownership structure, corporate governance, and fraud: Evidence from China. Journal of Corporate Finance, 12(3), 424–448. https://doi.org/10.1016/j.jcorpfin.2005.09.002

- Chung, H., & Kallapur, S. (2003). Client importance, nonaudit services, and abnormal accruals. The Accounting Review, 78(4), 931–955. https://doi.org/10.2308/accr.2003.78.4.931

- Claessens, S., & Yurtoglu, B. B. (2013). Corporate governance in emerging markets: A survey. Emerging Markets Review, 15, 1–33. https://doi.org/10.1016/j.ememar.2012.03.002

- Cosma, S., Mastroleo, G., & Schwizer, P. (2018). Assessing corporate governance quality: Substance over form. Journal of Management and Governance, 22(2), 457–493. https://doi.org/10.1007/s10997-017-9395-3

- Daghsni, O., Zouhayer, M., & Mbarek, K. B. H. (2016). Earnings management and board characteristics: Evidence from French listed firms. Arabian Journal of Business and Management Review, 6(5), 1–9. https://doi.org/10.4172/2223-5833.1000249

- Dakhlallh, M. M. (2020). Accrual-based earnings management, real earnings management and firm performance: Evidence from public shareholders listed firms on Jordanian’s stock market. Journal of Advanced Research in Dynamical and Control Systems, 12(1), 16–27. https://doi.org/10.5373/JARDCS/V12I1/20201004

- Ehren, M., & Perryman, J. (2018). Accountability of school networks. Educational Management Administration & Leadership, 46(6), 942–959. https://doi.org/10.1177/1741143217717272

- Elnahass, M., Salama, A., & Yusuf, N. (2022). Earnings management and internal governance mechanisms: The role of religiosity. Research in International Business and Finance, 59, 101565. https://doi.org/10.1016/j.ribaf.2021.101565

- Evodila, E., Erlina, E., & Kholis, A. (2020). The effect of information asymmetry, financial performance, financial leverage, managerial ownership on earnings management with the audit committee as moderation variables. Manajemen, Teknologi Informatika Dan Komunikasi (Mantik), 4(3), 1734–1745. https://doi.org/10.35335/mantik.Vol4.2020.987

- Fadzilah, N. S. B. M. (2017). Board of directors’ characteristics and earnings management of family owned companies. International Journal of Accounting & Business Management, 5(2), 68–83.

- Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. The Journal of Law and Economics, 26(2), 301–325. https://doi.org/10.1086/467037

- Filatotchev, I., Jackson, G., & Nakajima, C. (2013). Corporate governance and national institutions: A review and emerging research agenda. Asia Pacific Journal of Management, 30(4), 965–986. https://doi.org/10.1007/s10490-012-9293-9

- Gerged, A. M., Albitar, K., & Al-Haddad, L. (2021). Corporate environmental disclosure and earnings management—The moderating role of corporate governance structures. International Journal of Finance & Economics, 28(3), 2789–2810. https://doi.org/10.1002/ijfe.2564

- Gillan, S. L., & Starks, L. T. (2000). Corporate governance proposals and shareholder activism: The role of institutional investors. Journal of Financial Economics, 57(2), 275–305. https://doi.org/10.1016/S0304-405X(00)00058-1

- Githaiga, P. N. (2023). Board gender diversity, institutional ownership and earnings management: Evidence from East African community listed firms. Journal of Accounting in Emerging Economies, Vol. ahead-of-print No. ahead-of-print. https://doi.org/10.1108/JAEE-10-2022-0312

- Goh, J., Lee, H., & Lee, J. (2013). Majority shareholder ownership and real earnings management: Evidence from Korea. Journal of International Financial Management & Accounting, 24(1), 26–61. https://doi.org/10.1111/jifm.12006

- Gras-Gil, E., Marin-Hernandez, S., & Garcia-Perez de Lema, D. (2012). Internal audit and financial reporting in the Spanish banking industry. Managerial Auditing Journal, 27(8), 728–753. https://doi.org/10.1108/02686901211257028

- Greene, W. H. (2018). Econometric analysis (8th ed.). Pearson.

- Gujarati, D. (2004). Basic econometrics. McGraw-Hill Inc.

- Gull, A. A., Nekhili, M., Nagati, H., & Chtioui, T. (2018). Beyond gender diversity: How specific attributes of female directors affect earnings management. The British Accounting Review, 50(3), 255–274. https://doi.org/10.1016/j.bar.2017.09.001

- Handayani, Y. D., & Ibrani, E. Y. (2020). The effect of audit committee characteristics on earnings management and its impact on firm value. International Journal of Commerc and Finance, 6(2), 104–116.

- Harris, O., Karl, J. B., & Lawrence, E. (2019). CEO compensation and earnings management: Does gender really matters? Journal of Business Research, 98, 1–14. https://doi.org/10.1016/j.jbusres.2019.01.013

- Healy, P. M. (1985). The effect of bonus schemes on accounting decisions. Journal of Accounting and Economics, 7(1–3), 85–107. https://doi.org/10.1016/0165-4101(85)90029-1

- Healy, P. M., & Wahlen, J. M. (1999). A review of the earnings management literature and its implications for standard setting, (November 1998). SSRN Electronic Journal. https://doi.org/10.2139/ssrn.156445

- Hill, C. W. L., & Jones, T. M. (1992). Stakeholder-agency theory. Journal of Management Studies, 29(2), 131–154. https://doi.org/10.1111/j.1467-6486.1992.tb00657.x