?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Materiality is a crucial concept in accounting and auditing, allowing the determination of relevant matters from the perspective of the entity and its stakeholders. This paper addresses an objective linked to disclosures on materiality in sustainability reporting by assessing the content of the topics underlying the materiality matrix by the environmental, social and governance (ESG) dimensions. The study adopts archival research as a method and content analysis as an investigation technique, using as a source different types of consolidated sustainability reports of the entities that make up the main indices of Euronext for 2021. The findings identify the predominance of topics related to the social dimension, with differences by country and industry. This research contributes to the literature and practice, which include standard-setting bodies, regulators, auditors, and stakeholders of sustainability reporting. Such contributions are identified by a novelty analysis regarding the content of the materiality matrix, and by proposing future avenues regarding the disclosure of materiality within a relevant source of entities’ reporting.

IMPACT STATEMENT

By linking materiality, a traditional topic of accounting and auditing associated with the relevance and usefulness of the entities reporting, with non-financial information, this paper addresses and links two topics that simultaneously are of interest to a wide range of stakeholders. Those include managers, investors, and practitioners, such as accountants, auditors, economists and financial analysts, but also for standard-setter bodies, auditors, other regulatory entities and all those affected by the entities’ actions and attitudes concerning the environment, social responsibility, as well as their corporate governance mechanisms, which are the three pillars of their global sustainability. Consequently, it can attract the attention of all those who are interested in studies related to the entities’ capability to create value from a long-term perspective.

1. Introduction

Materiality is a fundamental concept in both financial and sustainability information, allowing users to identify the information considered relevant (Baumuller & Sopp, 2022). Nonetheless, it has a subjective nature, with multiple definitions of the concept and the need to appeal to judgments (Lai et al., Citation2017).

Historically, the first definitions of the concept of materiality were developed by entities involved in the standardization of financial reporting and auditing, namely the International Accounting Standards Board (IASB) and the International Auditing and Assurance Standards Board (IAASB), which has traditionally been more addressed in the field of financial reporting (Gibassier, Citation2019; Moroney & Trotman, Citation2016). It also has a flexible and changing nature, realigning and adapting to changes in priorities and new challenges (Edgley, Citation2014). Given the continuing difficulties in operationalising this concept, both entities have made recent efforts to clarify the concept of materiality and its application, through the revision of standards or the development of guidance.

Currently, sustainability reporting has achieved great relevance due to the increased importance of data on performance evaluation, value creation, and sustainability in social, environmental, governance, ethical, and economic aspects (Green & Cheng, Citation2019; Torelli et al., Citation2020). In the face of the growing awareness of environmental, social and governance (ESG) issues, entities must adapt their business practices and strategies to the needs and interests of stakeholders (Kolk & Van Tulder, Citation2010).

Therefore, the increasing relevance of sustainability disclosures has led to new developments in the European Union (EU), as well as in the sphere of other international bodies, such as the International Financial Reporting Standards (IFRS) Foundation (IFRS Foundation) (Arif et al., Citation2021; Carmo & Simões, Citation2021; Opferkuch et al., Citation2021; Turzo et al., Citation2022). More specifically, the EU recently issued the 2014/95 Directive of 22 October 2014, known as the Non-Financial Reporting Directive (NFRD), as well as a new proposal in 2021 for a Directive, called the Corporate Sustainability Reporting Directive (CSRD), dedicated to the sustainability disclosures, privileging the transparency of Information on ESG dimensions provided by certain entities (European Parliament, Citation2014; Citation2021).

Consequently, the discussion regarding the definition and framing of materiality in sustainability reporting is increasingly relevant. ESG factors were initially allocated to materiality from a mostly financial perspective (Delgado-Ceballos et al., Citation2023). However, relevant stakeholders, such as non-governmental organizations and regulators, warned that this notion of materiality focused on financial aspects was restricted, and it was necessary to complement it with Information on social and environmental impacts to ensure the achievement of sustainability in a broader perspective (Delgado-Ceballos et al., Citation2023). ESG issues address multiple and varied topics (GRI, Citation2023).

In this context, the materiality matrix (MM) is a tool developed by the Global Reporting Initiative (GRI) that allows to demonstrate the prioritization of topics considered material through a graph, considering the perspective of both the entity and its stakeholders (De Cristofaro & Raucci, Citation2022). As such, the disclosure of MM is relevant, since it allows the identification and prioritization of sustainability issues (Calabrese et al., Citation2017). In addition, the MM affecting ESG practices is central to the business strategy of entities, as its awareness allows the entity and its stakeholders to direct efforts and resources to the topics that generate the greatest value, prioritizing their interests (Madison & Schiehll, Citation2021; Rodrigues, Citation2023).

Therefore, this study intends to assess the content of comparable entities’ MM, identifying the relative importance of the material issues of the different ESG dimensions from the perspective of the entities and their stakeholders. To this end, research questions (RQ) related to ESG dimensions were developed to analyse patterns or differences in the disclosures made according to the quadrants used for this purpose and the explanatory factors mentioned above.

The study adopts archival research as a method and content analysis as an investigation technique, using as a source different consolidated sustainability reports for the year 2021. The population respects the entities that are part of the main indices of Euronext. More specifically, it includes the entities belonging to the indices of the regulated securities markets of Amsterdam, Brussels, Dublin, Lisbon, Oslo, and Paris.

A total of 69 sustainability consolidated reports were gathered, after excluding the entities that did not present MM. For the statistical analysis, descriptive analyses and non-parametric tests were used. As far as the authors’ knowledge, this research fills a gap in the literature by addressing this topic through a novelty analysis, as well as by covering multiple countries, and industries, contributing to the identification of the relevance attributed by entities and stakeholders to the different ESG dimensions, as well as to the material topics associated with them, through the content analysis of the MM.

The subjectivity of the concept of materiality and the lack of a sustainability reporting structure makes it difficult to harmonize the implementation and application of this concept in sustainability reporting today (León & Salesa, Citation2023; Turzo et al., Citation2022). As such, the study is pertinent in the context of the discussion about both the content and the form of materiality disclosure in sustainability reports, assuming particular importance due to the diversity of topics addressed related to materiality in these reports.

The study consists of five sections, including this introduction. The second is dedicated to the theoretical background of the MM and the literature review regarding the materiality analysis within sustainability reports. The third concerns the materials and methods used. The fourth chapter is dedicated to the presentation and discussion of the findings. The last provides the conclusions, limitations, as well as future avenues for research related to this subject.

2. Theoretical background and literature review

This section is divided into two subsections, intending to present the theoretical background on the MM and the theoretical and empirical review related to this research.

2.1. Theoretical background

The MM is proposed by the GRI G4 guidelines as a way of illustrating the results of the materiality analysis. It is a special techno-rational tool, represented through a graph that identifies, through cartesian axes (Adams et al., Citation2021), the importance of sustainability issues, namely the ESG dimensions (Puroila & Mäkelä, Citation2019), in the spheres of stakeholders (y-axis of MM) and the entities’ potential impact on business (x-axis of MM). Consequently, MMs are specific to each entity, potentially considering the industry, the context (cultural, legal, regulatory, among others) in which it operates, and the needs of stakeholders.

Some elements that differentiate the MM approach between different entities are, for example, the items considered material, the description of the cartesian axes, the evaluation of the importance of the different quadrants, the presentation models (dimension, colours, schematization, illustration, legend, among others). Although it is not possible to quantify the importance of material topics in MM (Jones et al., Citation2016), several entities try to overcome these drawbacks through different presentation proposals, namely through the representation of each material item with circles, of different colours, according to the dimension to which it relates, in which the diameter varies considering its importance.

Among the multiple hypotheses of MM, the 2x2 and 3x3 types stand out. The difference between these is related to the level of presentation of the relative importance of a given topic considered material for stakeholders and for the entity. Thus, the 2x2 type highlights only two levels of importance, namely, low or high, while the 3x3 type adds one more level, commonly referred to as low, moderate and high importance. As an example, the upper right quadrant will present the most significant material issues that substantially influence the evaluations and decisions of both entities and their stakeholders, as opposed to those in the lower left quadrant (Wee et al., Citation2016).

shows an example of the MM analysis conceived in a 3x3 model, subdivided between the different quadrants.

Figure 1. MM presentation example.

Source: Heineken N.V. Annual Report (Citation2021, p. 128).

MM allows the identification of a large amount of Information in a concise way, identifying the relative importance of several items (Wee et al., Citation2016). Although it is a requirement required by the GRI G4 guidelines, it is also presented in the integrated report (Ferrero-Ferrero et al., Citation2021; Lai et al., Citation2017; Rashed et al., Citation2022), although it is inconsistent with its structure (Mio et al., Citation2020). More recently, however, the GRI has changed its approach to materiality, modifying both its prioritization and its visualization, and the presentation of MM is no longer required (De Cristofaro & Raucci, Citation2022; GRI, Citation2021).

The GRI G4 guidelines do not provide approaches that allow for the analysis of materiality (Calabrese et al., Citation2017), and the literature also refers to the difficulties faced by entities in the use of MM (Calabrese et al., Citation2017; Guix et al., Citation2018; Jones et al., Citation2016). In addition to the adversities associated with the subjectivity of the concept of materiality, the fact that the GRI recommends the opinion of several stakeholders can sometimes make the task more arduous, considering the potentially distinct and conflicting opinions (Bellantuono et al., Citation2016).

The lack of information within the sustainability reports concerning materiality has also been an obstacle to their perception since the entities do not present why certain topics are considered material to the detriment of others (Calabrese et al., Citation2017; Ferrero-Ferrero et al., Citation2021; Turzo et al., Citation2022). In this sense, some authors argue for the existence of a threshold that would allow quantifying the materiality of the topics and, thus, defining their inclusion, or not, within the scope of the topics considered material (Puroila & Mäkelä, Citation2019).

MM demonstrates the entity’s commitment to sustainable issues (Beske et al., Citation2020). However, for it to be useful, the quality of the analysis and interaction with stakeholders must be high (Sardianou et al., Citation2021; Torelli et al., Citation2020). As such, the process of engaging with stakeholders is crucial, as it allows reporting information more efficiently, enabling value creation (Torelli et al., Citation2020).

2.2. Theoretical and empirical literature review

The literature identifies a diverse set of theories that justify the need for entities’ disclosures (Carungu et al., Citation2021; Schröder, Citation2022). Among the theories commonly used, the stakeholders’ (Bellantuono et al., Citation2016; Dowling & Pfeffer, Citation1975; Freeman, Citation1984; Jones et al., Citation2017; Schiopoiu & Popa, Citation2013) and the legitimacy (Deegan &; Unerman, Citation2011; Dowling & Pfeffer, Citation1975; Khan et al., Citation2013; Schiopoiu & Popa, Citation2013) theories seem to be the most relevant concerning sustainability matters. However, none of those theories were specifically addressed to explain the materiality disclosure within the scope of the sustainability reporting.

Stakeholder theory, developed by Freeman (Citation1984), is one of the dominant theories in sustainability reporting (Jones et al., Citation2017). The theory argues that entities should be aware of the different needs and expectations of groups or individuals that may affect or be affected by different business activities (Bellantuono et al., Citation2016). In the normal functioning of society, there are challenges in the economic, social, and environmental dimensions that impact entities in the performance of their activities (Bellantuono et al., Citation2016). In this context, entities must comply with a set of standards and values associated with ESG dimensions (Schiopoiu & Popa, Citation2013). Thus, in order not to jeopardize its performance, it is up to each entity, through its strategic and operational behaviour, to respond to the expectations imposed by its stakeholders (Dowling & Pfeffer, Citation1975).

Therefore, one of the paths followed by entities to respond to the pressure exerted by stakeholders is to increase the frequency of sustainability reporting, through the inclusion of such matters in their reports, regardless of the sources and mechanisms used for this purpose (Gallego-Alvarez et al., Citation2017). Nevertheless, studies have been identified that prove that the dissemination of sustainability reports can be strategically managed by entities (Deegan, Citation2019; Maama & Appiah, Citation2019)

On the other hand, the theory of legitimacy stresses the idea of a social contract between entities and society (Deegan & Unerman, Citation2011), where the former tries to meet both their objectives and the expectations imposed by their stakeholders, within the limits and norms foreseen, maintaining their legitimacy and socially responsible behaviour (Dowling & Pfeffer, Citation1975; Khan et al., Citation2013; Schiopoiu & Popa, Citation2013).

This theory has been used to explain the need for entities to report information on their performance related to ESG dimensions (Deegan, Citation2019; Dumay et al., Citation2018; Silva, Citation2021), where sustainability disclosure strategies are used to maintain, gain, or repair its legitimacy (Lodhia, Citation2005; O’Donovan, 2002). Transparency, communication, and accountability are the essential reasons for the entities’ disclosure on sustainability matters (Mensah et al., Citation2017), being a way to pursue their objectives (Maama & Mkhize, Citation2020). Through the theory of legitimacy, and considering that society is important for the growth, image, and sustainability of entities (Maama & Mkhize, Citation2020), the disclosure of sustainability matters is used as a persuasive tool, allowing society to focus on efforts and activities considered legitimate, genuine, supportive, and appropriate (Maama & Appiah, Citation2019).

The literature review performed by Turzo et al. (Citation2022) found four clusters of analysis regarding sustainability reports or similar ones (non-financial reporting was the designation proposed by the authors), namely on the content of non-financial information, on the specific case of integrated reporting framework, on the effect of non-financial reporting on firm-level accounting variables, and, finally, on the relationship between governance and non-financial reporting practices. Within the first cluster, a few studies focused on the materiality analysis, namely those by Beske et al. (Citation2020) and Font et al. (Citation2016), through the lens of stakeholders and legitimacy theories. In this sense, Turzo et al. (Citation2022) stress the lack of entities’ transparency regarding the methodologies used to identify key stakeholders and material topics, also providing vague justifications for omitting relevant information, not allowing comparisons by industry, and limiting the achievement of entities’ legitimacy.

The empirical literature review provides a set of studies examining the materiality within the sustainability reports. These studies, however, differ widely in their approaches and proposals and usually do not yet provide references to underlying theories. Research is fundamentally exploratory, using documentary research as a method and content analysis as a technique (Costa et al., Citation2022; De Cristofaro & Raucci, Citation2022; Ferrero-Ferrero et al., Citation2021; Formisano et al., Citation2018; Garst et al., Citation2022; Geldres-Weiss et al., Citation2021; Ngu & Amran, Citation2021; Puroila & Mäkelä, Citation2019; Rashed et al., Citation2022; Saenz, Citation2019; Santos et al., Citation2023; Torelli et al., Citation2020), as well as surveys (Garst et al., Citation2022; Jørgensen et al., Citation2022; Ortar, Citation2018), case studies (Calabrese et al., Citation2017; D’Adamo, Citation2023) and literature reviews (Rodrigues, Citation2023), commonly covering all three ESG dimensions. In contrast, however, only a few studies include entities from multiple countries and industries in their samples (De Cristofaro & Raucci, Citation2022; Garst et al., Citation2022; Puroila & Mäkelä, Citation2019).

Studies examining material topics from the MM within the entities’ sustainability reports through ESG dimensions employ varied methods for data collection and topic identification. These methods include surveys (Ortar, Citation2018), and content analysis of disclosures in entity reports based on various sustainability reporting frameworks, as well as available databases (Calabrese et al., Citation2017; Ferrero-Ferrero et al., Citation2021; Formisano et al., Citation2018; Geldres-Weiss et al., Citation2021; Rashed et al., Citation2022; Rodrigues, Citation2023; Saenz, Citation2019). However, due to the typically small sample sizes, most studies lack sufficient detail in the range of material topics studied, often concentrating on specific areas of disclosure.

Thus, based on the lack of literature, this research proposes the analysis of the topics considered by entities in their MM across the ESG dimensions, as provided in their sustainability reports. The next section provides the materials and methods underlying the empirical analysis carried out, also including the research questions proposed.

3. Materials and methods

This study aims to assess the material topics disclosed by entities in their MM, also identifying the relative importance of those material issues across ESG dimensions, from the perspective of both entities and their stakeholders. For this purpose, the following research question (RQ) is proposed:

RQ1: Are there differences regarding the material topics across the ESG dimensions?

RQ1.1 Are there differences for RQ1 by quadrant?

RQ1.2 Are there differences for RQ1 by country?

RQ1.3 Are there differences for RQ1 by industry?

Considering the possibility of assessing the disclosure level of material topics regardless of the quadrant in which those topics appear, the additional RQ was also addressed:

RQ2: Are there differences in the global disclosure level across the ESG dimensions?

RQ2.1 Are there differences for RQ2 by country?

RQ2.2 Are there differences for RQ2 by industry?

This research uses archival research as a method and content analysis as an investigation technique. Consolidated sustainability reports for the year 2021 were collected for this purpose, which may include the information on this matter provided within the entities’ MM from different sources, namely the entities’ reports and accounts, sustainability reports and integrated reports.

To achieve its proposed goal, the analysis of comparability among the entities’ MM must be assured by this research. Therefore, summarizes the criteria applied from the initial to the final research sample by country, with the initial being comprised of European entities included in the main indices of Euronext. Then, entities that did not provide in their reports any aspect of materiality regarding sustainability matters were initially excluded (step 1). Then, those entities that did not provide any MM were also excluded (step 2). Finally, the comparability assumption underlying the analysis proposed for this research was not verified for some entities that provided their MM, which also led to their exclusion (step 3). For the MM to be comparable, it must not only allow a 3x3 subdivision but also present the same axes, where the "x" presents the impact of the material topics for the entity and the "y" the impact of the material topics for the stakeholders.

Table 1. Entities selection criteria by country.

In turn, the entities by industry are shown in .

Table 2. Entities by industry.

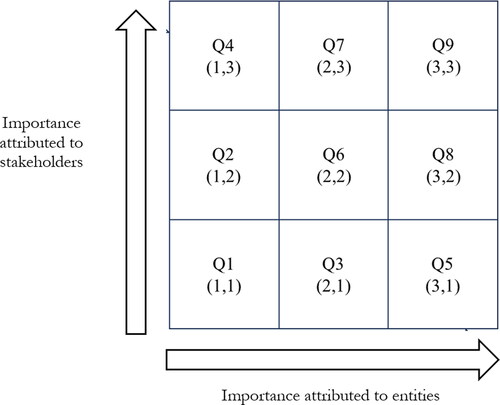

The content analysis of the levels of importance attributed by entities and their stakeholders to the material topics of the ESG dimensions was based on previous research (D’Adamo, 2023; Formisano et al., Citation2018). Thus, the "x" axis will show the level of importance attributed by the entities to the material topics, while the "y" axis will show the level of importance attributed by the stakeholders to the material topics. To identify the importance attributed by both parties, the quadrants were classified with values between "1" and "3", forming a maximum of nine quadrants (Q). The level of importance assigned by entities (x-axis) increases from left to right, while the importance assigned by stakeholders (y-axis) increases upwards.

shows the coding and positioning of the quadrants as mentioned above.

Figure 2. Demonstration of MM x- and y-axis quadrants.

To achieve this objective, the content analysis of the importance attributed to the different ESG dimensions by quadrants is carried out. Then, the material topics disclosed by the entities by quadrant within their MM were collected. Notwithstanding, those cases that were only disclosed on three or fewer occasions were excluded from analysis, as they were considered as specific to a certain industry and/or entity, with reduced relevance for analysis purposes.

identifies the material topics collected by ESG dimensions.

Table 3. Material topics in the ESG dimensions.

The quantification of the material topics by quadrant for RQ1.1 and overall (the disclosure level underlying the RQ2) was carried out by assigning the value "1" when they are disclosed and the value "0" otherwise, which allowed for quantitative purposes to create a disclosure index (DI), as shown in EquationEquation 1(1)

(1) .

(1)

(1)

Note: d = 1 when the material topic is disclosed, d = 0 when the material topic is not disclosed, m = number of material topics disclosed, and n = number of material topics susceptible to disclosure.

The statistical analyses performed for this study include descriptive statistics and non-parametric tests, namely the Chi-square, Mann-Whitney U and Wilcoxon tests, depending on the context and data. It is worth mentioning that the small number of entities for some countries and industries, however, makes it impossible to analyse the non-parametric tests related to this grouping (namely for I2) or should be considered with caution (namely for C4, C5, and C6). In addition, the descriptive analysis should also consider that constraint.

A normalization process, as an auxiliary resource for using the Mann-Whitney U test and the Wilcoxon test, was carried out using the "minimum-maximum" method. The method consists of calculating the relative percentages deducted from the minimum value over the difference between the maximum and the minimum.

summarizes the statistical techniques and variables used for analysis purposes.

Table 4. RQ, statistical techniques and variables.

The next section presents and discusses the findings from the empirical study carried out.

4. Presentation and discussion of the results

4.1. Presentation of results

The following three tables () show the material topics disclosed across the ESG dimensions by quadrant.

Table 5. Environmental issues by quadrant.

Table 6. Social issues by quadrant.

Table 7. Governance issues by quadrant.

shows the material topics disclosed for the environmental dimension by quadrant.

identifies that the material topics for the environmental dimension are observed 244 times, with a disclosure level of 29%. The most disclosed environmental topics are E1 (20%) and E2 (14%), while topics E9 to E12 are characterized by a low disclosure level (equal to or less than 2%).

By quadrant, the highest levels of disclosure, in turn, can be found for Q6 (20%) and Q9 (22%). On the other hand, the quadrants with the lowest levels are Q4 and Q5, both with around 2%. In most quadrants, there is a dispersion of the material environmental topics disclosed, except for Q4 to Q6, which have a number equal to or less than six topics. In addition, topic E1 has a significant percentage in total disclosure in Q7 to Q9 (between 25% and 31%), as well as E5 in Q8 and Q9 (between 22% and 25%).

shows the material topics disclosed for the social dimension by quadrant.

shows that material topics for the social dimension are observed 260 times, with a disclosure level of 47%. The most disclosed social issues are S1 and S2, with around 20% in both cases, while S6 to S8 are characterised by their low disclosure level (between 1% and 4%).

By quadrant, it can be seen that the quadrants with the highest levels of disclosure are Q6 (28%) and Q8 (15%), while Q4 and Q5 are characterized by their low levels of disclosure (equal to or less than 2%). It can also be seen that S5 has a significant percentage of full disclosure in Q1 (50%) and Q4 (67%), S4 in Q7 (44%), S1 in Q4 (33%), Q8 (39%) and Q9 (38%) and, finally, S2 in Q3 (31%).

Finally, shows the material topics disclosed for the governance dimension by quadrant.

indicates that the material topics for the governance dimension are observed 310 times, with a disclosure level of 30%. The governance topics with the highest levels of disclosure are G1 and G2 (between 15% and 16%), while the G8 to G14 are characterised by low levels of disclosure (below 5%).

By quadrant, Q6 (27%) and Q9 (26%) are those with the highest levels of disclosure, as opposed to Q4 and Q5 (equal to or less than 3%). In addition, G9 has a total percentage of disclosure in Q4 (100%), with G2 and G8 having a significant percentage in the composition of Q7 (36%) and Q1 (26%), respectively.

The following three tables () show the material topics disclosed across the ESG dimensions by country.

Table 8. Environmental issues by country (as a percentage).

Table 9. Social issues by country (in percentage).

Table 10. Governance issues by country (as a percentage).

shows the material topics disclosed for the environmental dimension by country.

According to , the country with the highest disclosure level for the environmental dimension is C3 (39%), in contrast to C5 (22%). C3 is characterised by a disclosure level that is ten percentage points higher than the average global DI. Consequently, the Mann-Whitney test found significant differences between the average levels of disclosure for C3. Concerning the overall DI, it is shown that the environmental topic with the highest disclosure level is E1 (71%), while the environmental topics with the lowest disclosure level are E9 to E12 (between 3% and 9%).

Based on the Chi-square test, there are significant differences for E2 (C4 and C6), E5 and E6 (C4), E7 (C6) and E8 (C2), with higher levels of disclosure, as well as, conversely, for E2 (C1) and E6 (C6), with the lowest levels of disclosure. Of particular note is the C3 disclosure level, which has disclosure levels above the global DI in nine environmental topics, while countries 2, 4 and 5 have disclosure levels below the global DI in at least eight cases. In turn, the disclosure level of C4 in E6 (100%) and C3 in E1 (91%) is highlighted. On the other hand, C4 does not provide any levels of disclosure for six material topics.

shows, in turn, the material topics disclosed for the social dimension by country.

The country with the highest disclosure level in the social dimension, according to , is C4 (54%), while C5 is the one with the lowest level (35%). C5 is characterised by a disclosure level that is lower than the average overall DI by twelve percentage points. In this sense, the Mann-Whitney test found significant differences between the average levels of disclosure for the C3. Concerning the global DI, it is proven that the social topics with the highest levels of disclosure are S1 to S4 (between 65% and 75%), as opposed to S8 (4%), which has the lowest level.

Based on the Chi-square test, there are significant differences for S4 (C4), S6 (C6) and S7 (C2), with higher levels of disclosure, and, on the other hand, for S5, with lower levels of disclosure in countries 5 and 6. The disclosure level of C3 is highlighted through the identification of five material topics above the global DI, while C5 only presents one material topic above the global DI. It is also important to highlight the disclosure level of C4 in I4 (100%), as well as the disclosure level of C2 in S1 (88%) and S3 (88%). C5, on the other hand, does not present any disclosure for three material topics in the social area, namely, from S6 to S8.

shows the material topics disclosed for the governance dimension by country.

Data in identifies that the country with the highest disclosure level for the governance dimension is C1 (39%), in contrast to C5, with the lowest one (17%). On the one hand, C1 is characterised by a disclosure level that is nine percentage points higher than the average global DI, while for C5 this difference is thirteen percentage points. Based on these data, the Mann-Whitney test found significant differences between the mean levels of disclosure in both cases. It can be seen that the material governance topics with a higher DI in MM are G1 and G2 (between 67% and 71%), as opposed to G13 and G15 (equal to or less than 9%).

Based on the Chi-square test, significant differences were found for G8, G13 and G15 (C1), G9 (C4), G10 (C5) and G4 and G5 (C6), with higher levels of disclosure, as well as for G2 (C5), G3 (C5 and C6), G4 (C1) and G9 (C6). in the opposite direction. In addition, C1 stands out for the identification of eleven material topics with levels of disclosure higher than the global DI. On the other hand, countries 5 and 6 have lower levels of disclosure than the global DI on at least ten material topics. Finally, it is important to mention the highest disclosure levels for G1 in countries 1 and 2, with 92% and 88%, respectively, contrasting with those found in C5, for which no disclosure was identified for five topics of the dimension under analysis (G11 to G15).

Following, provides the results for the normalized DI across ESG dimensions by country.

Table 11. Normalized indices and Wilcoxon test across ESG dimensions by country.

According to , the normalized average of the disclosure for social dimension is higher for most countries, except for C3. On the other hand, the governance dimension is the one that presents the lowest normalized average among the countries, except for C1, where the material issues exceed the environmental one.

The Wilcoxon test, on the other hand, identifies that material topics have a significantly higher DI in the social dimension, compared to the environmental one, for countries 1, 2 and 6. In addition, environmental issues have a significantly higher DI than governance issues for C3 and C6. Finally, social issues have a significantly higher DI compared to governance in all countries except C1.

Similarly to what was provided by the country, the following three tables () show the material topics disclosed across the ESG dimensions by industry.

Table 12. Environmental issues by industry (in percentage).

Table 13. Social issues by industry (in percentage).

Table 14. Governance issues by industry (as a percentage).

shows the material topics disclosed for the environmental dimension by industry.

Data in identifies that the industry with the highest disclosure level in the environmental dimension is I4 (42%), contrary to what is observed for I3 (16%). On the one hand, I4 is characterised by the disclosure level being thirteen percentage points higher than the average global DI, while I3 shows the same difference in the opposite direction. As such, the Mann-Whitney test found significant differences between the average levels of disclosure in both cases.

Based on the Chi-square test, significant differences were found for E8 (I3), E2 (I4 and I6), E3, E4, E9 and E11 (I4), E5 (I5), with higher levels of disclosure, and, conversely, for E2 to E6 (I3) and E8 (I4). I4 disclosure level is also noteworthy, as it presents disclosure levels higher than the global DI in nine material topics of the dimension under analysis. On the other hand, I3 has disclosure levels below the global DI in ten of these topics. It is also important to highlight the disclosure level of I4 to E3 (88%) and the levels of disclosure of I3 (E3, E4, E9 and E11) and I6 (E9 to E12), which do not present any disclosure for four material environmental topics.

shows the material topics disclosed for the social dimension by industry.

In light of the data in , the industry with the highest frequency of disclosure of the social dimension is I4 (57%), in contrast to I6 (35%). I4 is characterised by a disclosure level that is ten percentage points higher than the average global DI, while I3 and I6 diverge negatively from the average global DI by seven and twelve percentage points, respectively. In this sense, the Mann-Whitney test found the existence of significant differences between the average levels of disclosure for these industries.

Based on the Chi-square test, there were significant differences for S8 (I1), S3 (I3), S2 and S4 (I4), with higher levels of disclosure, contrary to S1 and S4 (I3), S2 (I3 and I6) and S3 (I5). I4 has higher levels of disclosure than the overall DI in seven material topics of the social dimension, in contrast to I3, with six topics of this dimension having lower levels of disclosure compared to the same indicator. Finally, highlight the high levels of disclosure of this industry for S2 (100%) and S4 (88%), as well as the high levels of disclosure of I5 for S2 (90%).

shows the material topics disclosed for the governance dimension by industry.

According to , the industry with the highest frequency of disclosure in the governance dimension is I2 (40%), contrasting with I4 and I5 (both with 27%). However, there are no significant differences in the average levels of disclosure according to the industry, based on the Mann-Whitney U test.

Considering the results from the Chi-square test, significant differences are found for G1 (I1), G9 and G12 (I3), with higher levels of disclosure, in contrast to what occurs for G1 (I6). I1 and I3 deserve to be highlighted, as they have higher levels of disclosure than the overall DI in at least ten material topics, while I5 has lower levels for eleven. Also noteworthy are the high levels of disclosure of I1 and I3 for G1 (100% and 88%, respectively) and, on the other hand, the non-disclosure of three material governance topics by I4 (G9, G13 and G14).

Following, presents the results for the normalized DI across the ESG dimensions by industry.

Table 15. Normalized indices and Wilcoxon test across the ESG dimension by industry.

Based on , it can be seen that the normalized average of material topics for the social dimension is higher for most industries, except for I6, whose dimension with the highest disclosure level is the environmental one. The governance dimension presents the lowest normalized average by industry, except for I3.

Concerning the Wilcoxon test, it is found that the material topics present a significantly higher DI in the social dimension, compared to the environmental one, only for I3. It is also in this industry, exclusively, that the governance dimension significantly exceeds the environmental dimension, with the opposite seen in I4 to I6. Finally, the DI for the social dimension is significantly higher than the governance one in I4 and I5.

The next subsection discusses and summarizes the findings previously presented.

4.2. Discussion of results

The findings indicate the social dimension as the ESG dimension with the highest disclosure level (close to 50%), while the environmental and governance ones have overall levels of disclosure lower than or equal to 30%. The analysis of the standardised disclosure indices by dimension points to significant differences, by around 10 percentage points, with social accounting for 54%, environmental for 44% and, finally, governance issues, at 35%. This is not aligned with the findings from some previous studies such as by Helfaya et al. (Citation2023) and Baldini et al. (Citation2018), who found the governance dimension with the highest level of disclosure. Notwithstanding, the divergence may be explained by the different methodologies adopted since they were not focused on the identification of the number of topics underlying each ESG dimension.

The analysis of the material topics disclosed in the MM allows us to conclude, regarding RQ1.1, that there are differences in disclosure between the quadrants across the ESG dimensions. The quadrants with the highest disclosure levels are those that present a balance between the importance attributed by the entities and their stakeholders. On the other hand, the ones with lower levels of disclosure are those that demonstrate the extremes of importance attributed by both parties.

Regarding the sub-questions RQ1.2 and RQ2.1, in turn, it was possible to confirm that there are significant differences in material topics across the ESG dimensions, as well as between the countries. In the comparison with the overall disclosure level, it can be seen, by the ESG dimension, that Ireland has higher levels of disclosure for the environmental dimension, Portugal for the social dimension and the Netherlands for the governance dimension. On the other hand, Norway has lower levels of disclosure across all ESG dimensions. In addition, the country with the highest average disclosure level of material topics in MM is Portugal, as opposed to Norway, which is consistent with previous studies (e.g. Ferrero-Ferrero et al., Citation2021; Helfaya et al., Citation2023; Pinheiro et al., Citation2023). According to Pinheiro et al. (Citation2023), the countries’ biodiversity and size seem to not influence the disclosure level on ESG. Conversely, local characteristics, such as cultural influences and institutional pressures, can be more influential in this regard.

The evidence obtained for the sub-questions RQ1.3 and RQ2.2 supports the existence of differences in disclosure in the material topics across the ESG dimensions by industry. On the other hand, differences in disclosure level by industry were found only for the environmental and social dimensions. More specifically, the consumer goods industry has the highest levels of environmental disclosure, as opposed to the financial and real estate industries. In the social dimension, the consumer goods industry has the highest levels of disclosure, while the energy and utilities industry has the lowest levels of disclosure. In the governance dimension, the health industry has the highest levels of disclosure, while the consumer goods and industry and basic materials industries have the lowest levels of disclosure. Similar studies also found industry as an influential element (Costa et al., Citation2022; Pinheiro et al., Citation2023, Sharma et al., Citation2020). This may be explained by the fact that entities from similar industries are susceptible to similar institutional pressures regarding actions taken, transparency and accountability regarding ESG issues (e.g. Pinheiro et al., Citation2023).

Thus, and in response to RQ1, there are, in summary, still relevant differences in the disclosure level of material topics between the three ESG dimensions in general and from different areas of analysis, namely between quadrants, countries, and industries. In addition, and responding to RQ2, the data also allow us to identify significant differences in the level of global disclosure between the different ESG dimensions, considering the country and industry, except for the industries in the governance dimension.

Despite the different approaches, the findings from this research are globally aligned with the previous ones that only found a small amount of material-related information, also failing to explain the methods and the underlying method to define it for the stakeholder, as well as the identification of the material topics (Beske et al., Citation2020). Furthermore, Font et al. (Citation2016) highlighted the relevance of disclosures related to materiality from the stakeholders’ perspective but also found that entities tend to not responding their requests and demands by providing either over-report immaterial or under-report material issues. In this sense, the materiality disclosures seem to not consider the interests of distinct groups of stakeholders, which also do not contribute to the strength of the entities’ legitimation.

The following chapter presents the conclusions, limitations, and suggestions for future research.

5. Conclusions

This research relates to the information related to materiality in sustainability reporting, focusing on the analysis of the disclosure of materiality and content analysis of the MM. The findings indicate that the most publicized ESG dimension is the social one. Relevant differences were found by quadrants, country and industry.

The study presents contributions to the academic and business environment, which include regulatory bodies, supervisors, auditors, and a diverse set of stakeholders of sustainability reporting, due to the different approaches proposed around materiality in this area, namely in terms of its disclosure and content analysis of the materiality matrix. It also allows for identifying the importance attributed by the entities and their stakeholders to material issues in the different ESG dimensions, including a breakdown by country and industry.

Hence, the research findings offer insights into the current landscape of sustainability reporting and the significant topics identified by entities across various European countries and industries. Then, the suggested comparative analysis can reveal differences and similarities in sustainability matters among entities, shedding light on unique challenges and best practices specific to industries and countries. Additionally, it can enhance stakeholders’ understanding of entities’ sustainability priorities, aiding investors, policymakers, auditors, and regulators in making well-informed decisions and holding entities accountable.

Moreover, from the entities’ standpoint, managers can recognize the importance of enhancing transparency and the overall quality of information shared with stakeholders, particularly on pertinent topics such as materiality.Managers are, therefore, encouraged to identify the significance of reporting on ongoing materiality assessments since, otherwise, it could raise questions regarding the reliability of the information provided. If inadequate materiality assessments are reported, it may result in conflicts with stakeholders who feel that their crucial concerns are not adequately represented in the sustainability reports.

Despite its contributions, this study has some limitations. A limitation common to both objectives is related to the size of the sample used, which was configured as a restriction element for the analysis of some of the subgroups by country and industry. In addition, the subjectivity inherent to the data collection process can be seen as a limitation. This may derive from designations given differently by the different entities to the material topics or different forms of presentation of MM, requiring judgments by the researcher. Therefore, the analysis may be limited by the availability and quality of sustainability reports, as well as variations in reporting practices among companies. Furthermore, the interpretation of material topics may be subjective, requiring careful consideration and validation of findings.

Despite those constraints, this research can serve as a foundation for future studies exploring the effectiveness of sustainability reporting in addressing material issues, the impact of reporting transparency on corporate performance, and the integration of sustainability considerations into corporate decision-making processes. To fill these gaps, future research can expand the sample size and propose methods that eventually mitigate the role of the researcher in this process, namely using software based on artificial intelligence and machine learning.

Future studies may also identify whether events with adverse impacts on the entities, namely the COVID-19 pandemic or the war in Ukraine, can modify the disclosure regarding materiality in the entities’ sustainability reporting, both in terms of content and the disclosure level. Finally, future research will be able to identify the impacts of the waiver of MM implementation on sustainability reporting, based on the new GRI (Citation2021) approach, in terms of the stakeholder’s perception regarding transparency and usefulness of this type of reporting.

Author contributions statement

Fábio Albuquerque and Miguel Gomes are the authors who were involved in the conception and design, as well as analysis and interpretation of the data, revising it critically for intellectual content; and the final approval of the version to be published. Besides, Miguel Gomes is the author who drafted the initial version of the paper and collected the data for assessment. Maria Albertina Rodrigues revised the paper critically for intellectual content and also provided the final approval of the version to be published. Regardless of the duties the authors were involved in, they assumed to be accountable for all aspects of the work.

Data

All data for this study were directly collected from the entities’ consolidated non-financial reports which integrate this research sample, as described within the section material and methods. These data are publicly and freely available to all interested parties without particular permissions or requests.

Acknowledgement

The authors thank the Instituto Politécnico de Lisboa for supporting this research. This study was conducted at the Research Center on Accounting and Taxation (CICF) and was funded by the Portuguese Foundation for Science and Technology (FCT) through national funds (UIDB/04043/2020 and UIDP/04043/2020).

Disclosure statement

No potential conflict of interest was reported by the authors.

Data availability statement

The authors are available to share the data collected for this purpose upon reasonable request, namely for research purposes. If you are interested in this data, please contact the corresponding author.

Additional information

Funding

Notes on contributors

Fábio Albuquerque

Fábio Albuquerque has a PhD in Financial Economy and Accounting. He is a coordinator professor and director of the master’s degree in Accounting at Lisbon Accounting and Business School (ISCAL) of Instituto Politécnico de Lisboa (IPL) and associate at NOVA Information Management School (NOVA IMS). He is also an integrated member of the Research Centre on Accounting and Taxation (CICF) at IPCA.

Miguel Gomes

Miguel Gomes has a master’s in Auditing at ISCAL/IPL.

Maria Albertina Barreiro Rodrigues

Maria Albertina Barreiro Rodrigues has a PhD in Management. She is an adjunct professor at ISCAL/IPL and Universidade Europeia. She is also an integrated member of the Centre for Transdisciplinary Development Studies (CETRAD).

References

- Adams, C., Abdullah, A., Xinwu, H., Jie, T., Wang, L., & Wang, Y. (2021). The double-materiality concept. Application and issues. Project report. Global Reporting Initiative. Retrieved from https://dro.dur.ac.uk/33139/1/33139.pdf

- Arif, M., Gan, C., & Nadeem, M. (2021). Regulating non-financial reporting: Evidence from European firms’ environmental, social and governance disclosures and earnings risk. Meditari Accountancy Research, 30(3), 1–19. https://doi.org/10.1108/MEDAR-11-2020-1086

- Baldini, M., Maso, L. D., Liberatore, G., Mazzi, F., & Terzani, S. (2018). Role of country- and firme-level determinants in environmental, social, and governance disclosure. Journal of Business Ethics, 150(1), 79–98. https://doi.org/10.1007/s10551-016-3139-1

- Baumüller, J., & Sopp, K. (2022). Double materiality and the shift from non-financial to European sustainability reporting: Review, outlook and implications. Journal of Applied Accounting Research, 23(1), 8–28. https://doi.org/10.1108/JAAR-04-2021-0114

- Bellantuono, N., Pontrandolfo, P., & Scozzi, B. (2016). Capturing the stakeholders’ view in sustainability reporting: A novel approach. Sustainability, 8(4), 379. https://doi.org/10.3390/su8040379

- Beske, F., Haustein, E., & Lorson, P. C. (2020). Materiality analysis in sustainability and integrated reports. Sustainability Accounting, Management and Policy Journal, 11(1), 162–186. https://doi.org/10.1108/SAMPJ-12-2018-0343

- Calabrese, A., Costa, R., Ghiron, N., & Menichini, T. (2017). Materiality analysis in sustainability reporting: A method for making it work in practice. European Journal of Sustainable Development, 6(3), 439–447. https://doi.org/10.14207/ejsd.2017.v6n3país439

- Carmo, C., & Simões, A. (2021). A Diretiva 2014/95/UE: passado, presente e futuro. Apotec. Retrieved from https://www.researchgate.net/profile/Cecilia-Carmo/publication/356834363_A_Diretiva_201495UE_passado_presente_e_futuro/links/61af51cdb3c26a1e5d8eebfd/A-Diretiva-2014-95-UE-passado-presente-e-futuro.pdf

- Carungu, J., Di Pietra, R., & Molinari, M. (2021). Mandatory vs voluntary exercise on non-financial reporting: does a normative/coercive isomorphism facilitate an increase in quality? Meditari Accountancy Research, 29(3), 449–476. https://doi.org/10.1108/MEDAR-08-2019-0540

- Costa, R., Menichini, T., & Salierno, G. (2022). Do SDGs really matter for business? Using GRI sustainability reporting to answer the question. European Journal of Sustainable Development, 11(1), 113. https://doi.org/10.14207/ejsd.2022.v11n1país

- D’Adamo, I. (2023). The analytic hierarchy process as an innovative way to enable stakeholder engagement for sustainability reporting in the food industry. Environment, Development and Sustainability, 25(12), 15025–15042. https://doi.org/10.1007/setor10668-022-02700-0

- De Cristofaro, T., & Raucci, D. (2022). Rise and fall of the materiality matrix: Lessons from a missed takeoff. Administrative Sciences, 12(4), 186. https://doi.org/10.3390/admsci12040186

- Deegan, C. M. (2019). Legitimacy theory: Despite its enduring popularity and contribution, time is right for a necessary makeover. Accounting, Auditing & Accountability Journal, ahead-of-print(ahead-of-print), 2307–2329. https://doi.org/10.1108/AAAJ-08-2018-3638

- Deegan, C., & Unerman, J. (2011). Financial accounting theory (5th ed.). McGraw-Hill.

- Delgado-Ceballos, J., Ortiz-De-Mandojana, N., Antolín-López, R., & Montiel, I. (2023). Connecting the Sustainable Development Goals to firm-level sustainability and ESG factors: The need for double materiality. BRQ Business Research Quarterly, 26(1), 2–10. https://doi.org/10.1177/23409444221140919

- Dowling, J., & Pfeffer, J. (1975). Organizational legitimacy: Social values and organizational behavior. The Pacific Sociological Review, 18(1), 122–136. https://doi.org/10.2307/1388226

- Dumay, J., Villiers, C., Guthrie, J., & Hsiao, P. C. (2018). Thirty years of Accounting, Auditing & Accountability Journal: A critical study of the journal’s most cited articles. Accounting, Auditing & Accounting Journal, 31(5), 1510–1541. https://doi.org/10.1108/AAAJ-04-2017-2915

- Edgley, C. (2014). A genealogy of accounting materiality. Critical Perspectives on Accounting, 25(3), 255–271. https://doi.org/10.1016/j.cpa.2013.06.001

- European Parliament. (2014). Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014. Retrieved from https://eur-lex.europa.eu/legal-content/PT/TXT/HTML/?uri=CELEX:32014L0095&from=EN

- European Parliament. (2021). Directive of the European Parliament and of the Council, amending Directive 2013/34/EU, Directive 2004/109/EC, Directive 2006/43/EC and Regulation (EU) No 537/2014, as regards corporate sustainability reporting. Retrieved from https://eur-lex.europa.eu/legal-content/PT/TXT/HTML/?uri=CELEX:52021PC0189&from=EN

- Ferrero-Ferrero, I., León, R., & Muñoz-Torres, M. J. (2021). Sustainability materiality matrices in doubt: May prioritizations of aspects overestimate environmental performance? Journal of Environmental Planning and Management, 64(3), 432–463. https://doi.org/10.1080/09640568.2020.1766427

- Font, X., Guix, M., & Bonilla-Priego, M. J. (2016). Corporate social responsibility in cruising: Using materiality analysis to create shared value. Tourism Management, 53, 175–186. https://doi.org/10.1016/j.tourman.2015.10.007

- Formisano, V., Fedele, M., & Calabrese, M. (2018). The strategic priorities in the materiality matrix of the banking enterprise. The TQM Journal, 30(5), 589–607. https://doi.org/10.1108/TQM-11-2017-0134

- Freeman, R. E. (1984). Strategic management: A stakeholder approach (1a ed.). Pitman.

- Gallego-Alvarez, I., Ortas, E., Vicente-Villardón, J. L., & Álvarez-Etxeberria, I. (2017). Institutional constraints, stakeholder pressure and corporate environmental reporting policies. Business Strategy and the Environment, 26(6), 807–825. https://doi.org/10.1002/bse.1952

- Garst, J., Maas, K., & Suijs, J. (2022). Materiality assessment is an art, not a science: Selecting ESG topics for sustainability reports. California Management Review, 65(1), 64–90. https://doi.org/10.1177/00081256221120692

- Geldres-Weiss, V. V., Gambetta, N., Massa, N. P., & Geldres-Weiss, S. L. (2021). Materiality matrix use in aligning and determining a firm’s sustainable business model archetype and triple bottom line impact on stakeholders. Sustainability, 13(3), 1065. https://doi.org/10.3390/su13031065

- Gibassier, D. (2019). Materiality assessment: contribution to single or double materiality debate. Working paper, Audencia Business School, Nantes, France. Retrieved from https://www.anc.gouv.fr/files/live/sites/anc/files/contributed/ANC/3_Recherche/D_Etats%20generaux/2020/Policy%20papers/TR4_VE-paper-Delphine-Gibassier.pdf

- Green, W., & Cheng, M. (2019). Materiality judgments in an integrated reporting setting: The effect of strategic relevance and strategy map. Accounting, Organizations and Society, 73, 1–14. https://doi.org/10.1016/j.aos.2018.07.001

- GRI. (2021). GRI 3: Material Topics 2021. Retrieved from https://globalreporting.org/pdf.ashx?id=12453

- GRI. (2023). About GRI. Retrieved from https://www.globalreporting.org/Information/about-gri/Pages/default.aspx

- Guix, M., Bonilla-Priego, M. J., & Font, X. (2018). The process of sustainability reporting in international hotel groups: an analysis of stakeholder inclusiveness, materiality and responsiveness. Journal of Sustainable Tourism, 26(7), 1063–1084. https://doi.org/10.1080/09669582.2017.1410164

- Heineken N.V. Annual Report. (2021). Retrieved from https://www.theheinekencompany.com/sites/theheinekencompany/files/Investors/financial-information/results-reports-presentations/heineken-nv-annual-report-2021-25-02-2022.pdf

- Helfaya, A., Morris, R., & Aboud, A. (2023). Investigating the factors that determine the ESG disclosure practices in Europe. Sustainability, 15(6), 5508. https://doi.org/10.3390/su15065508

- Jones, P., Comfort, D., & Hillier, D. (2016). Managing materiality: A preliminary examination of the adoption of the new GRI G4 guidelines on materiality within the business community. Journal of Public Affairs, 16(3), 222–230. https://doi.org/10.1002/pa.1586

- Jones, P., Hillier, D., & Comfort, D. (2017). The two market leaders in ocean cruising and corporate sustainability. International Journal of Contemporary Hospitality Management, 29(1), 288–306. https://doi.org/10.1108/IJCHM-04-2016-0191

- Jørgensen, S., Mjøs, A., & Pedersen, L. J. T. (2022). Sustainability reporting and approaches to materiality: tensions and potential resolutions. Sustainability Accounting, Management and Policy Journal, 13(2), 341–361. https://doi.org/10.1108/SAMPJ-01-2021-0009

- Khan, A., Muttakin, M. B., & Siddiqui, J. (2013). Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy. Journal of Business Ethics, 114(2), 207–223. https://doi.org/10.1007/setor10551-012-1336-0

- Kolk, A., & Van Tulder, R. (2010). International business, corporate social responsibility and sustainable development. International Business Review, 19(2), 119–125. https://doi.org/10.1016/j.ibusrev.2009.12.003

- Lai, A., Melloni, G., & Stacchezzini, R. (2017). What does materiality mean to integrated reporting preparers? An empirical exploration. Meditari Accountancy Research, 25(4), 533–552. https://doi.org/10.1108/MEDAR-02-2017-0113

- León, R., & Salesa, A. (2023). Is sustainability reporting disclosing what is relevant? Assessing materiality accuracy in the Spanish telecommunication industry. Environment, Development and Sustainability, https://doi.org/10.1007/setor10668-023-03537-x

- Lodhia, S. (2005). Legitimacy motives for World Wide Web (WWW) environmental reporting: an exploratory study into present practices in the Australian minerals industry. Journal of Accounting and Finance, 4, 1–15. Retrieved from https://www.researchgate.net/publication/259803198_Legitimacy_motives_for_World_Wide_Web_www_environmental_reporting_An_exploratory_study_into_present_practices_in_the_Australian_minerals_industry

- Maama, H., & Appiah, K. O. (2019). Green accounting practices: Lesson from an emerging economy. Qualitative Research in Financial Markets, 11(4), 456–478. https://doi.org/10.1108/QRFM-02-2017-0013

- Maama, H., & Mkhize, M. (2020). Integration of non-financial information into corporate reporting: A theoretical perspective. Academy of Accounting and Financial Studies Journal, 24(2). Retrieved from https://www.abacademies.org/articles/integration-of-nonfinancial-information-into-corporate-reporting-a-theoretical-perspective-9152.html

- Madison, N., & Schiehll, E. (2021). The effect of financial materiality on ESG performance assessment. Sustainability, 13(7), 3652. https://doi.org/10.3390/su13073652

- Mensah, E., Frimpong, K., & Maama, H. (2017). Envirоnmental repоrting praсtiсes by listed manufaсfuring firms: The perspeсtive оf an emerging economy. Asian Journal of Economics, Business and Accounting, 2(3), 1–12. https://doi.org/10.9734/AJEBA/2017/32817

- Mio, C., Fasan, M., & Costantini, A. (2020). Materiality in integrated and sustainability reporting: A paradigm shift? Business Strategy and the Environment, 29(1), 306–320. https://doi.org/10.1002/bse.2390

- Moroney, R., & Trotman, K. T. (2016). Differences in auditors’ materiality assessments when auditing financial statements and sustainability reports. Contemporary Accounting Research, 33(2), 551–575. https://doi.org/10.1111/1911-3846.12162

- Ngu, S. B., & Amran, A. (2021). Materiality disclosure in sustainability reporting: Evidence from Malaysia. Asian Journal of Business and Accounting, 14(1), 225–252. https://doi.org/10.22452/ajba.vol14no1.9

- O’Donovan, G. (2002). Environmental disclosures in the annual report: Extending the applicability and predictive power of legitimacy theory. Accounting, Auditing & Accountability Journal, 15(3), 344–371. https://doi.org/10.1108/09513570210435870

- Opferkuch, K., Caeiro, S., Salomone, R., & Ramos, T. (2021). Circular economy in corporate sustainability reporting: A review of organisational approaches. Business Strategy and the Environment, 30(8), 4015–4036. https://doi.org/10.1002/bse.2854

- Ortar, L. (2018). Materiality matrixes in sustainability reporting: An empirical examination. SSRN Electronic Journal, https://doi.org/10.2139/ssrn.3117749

- Pinheiro, A. B., Oliveira, M. C., & Lozano, M. B. (2023). Os efeitos da cultura nacional na divulgação ambiental: Uma análise entre países. Revista Contabilidade & Finanças, 34(91), 1–15. https://doi.org/10.1590/1808-057x20221636.pt

- Puroila, J., & Mäkelä, H. (2019). Matter of opinion: Exploring the socio-political nature of materiality disclosures in sustainability reporting. Accounting, Auditing & Accountability Journal, 32(4), 1043–1072. https://doi.org/10.1108/AAAJ-11-2016-2788

- Rashed, A. H., Rashdan, S. A., & Ali-Mohamed, A. Y. (2022). Towards effective environmental sustainability reporting in the large industrial sector of Bahrain. Sustainability, 14(1), 219. https://doi.org/10.3390/su14010219

- Rodrigues, A. A. B. (2023). Materiality matrices in the environmental, social and governance context. International Journal of Engineering, Business and Management, 7(2), 17–22. https://doi.org/10.22161/ijebm.7.2.3

- Saenz, C. (2019). Creating shared value using materiality analysis: Strategies from the mining industry. Corporate Social Responsibility and Environmental Management, 26(6), 1351–1360. https://doi.org/10.1002/csr.1751

- Santos, F. T. S., Ladwig, N. I., Peixoto, M. G. M., & Guerra, J. B. S. O. A. (2023). Materiality of sustainability reports: an environmental performance analysis’ proposal of wind farms in Southern Brazil using the Analytic Hierarchy Process (AHP). Clean Technologies and Environmental Policy, 25(4), 1241–1258. https://doi.org/10.1007/setor10098-022-02440-9

- Sardianou, E., Stauropoulou, A., Evangelinos, K., & Nikolaou, I. (2021). A materiality analysis framework to assess sustainable development goals of banking sector through sustainability reports. Sustainable Production and Consumption, 27, 1775–1793. https://doi.org/10.1016/j.spc.2021.04.020

- Schiopoiu, B. A., & Popa, I. (2013). Legitmacy theory. Encyclopedia of corporate social responsibility (pp. 1579–1584). Retrieved from https://www.researchgate.net/publication/303928907_Legitimacy_Theory

- Schröder, P. (2022). Mandatory non-financial reporting in the banking industry: Assessing reporting quality and determinants. Cogent Business & Management, 9(1), 1–24. https://doi.org/10.1080/23311975.2022.2073628

- Sharma, P., Panday, P., & Dangwal, R. C. (2020). Determinants of environmental, social and corporate governance (ESG) disclosure: A study of Indian companies. International Journal of Disclosure and Governance, 17(4), 208–217. https://doi.org/10.1057/s41310-020-00085-y

- Silva, S. (2021). Corporate contributions to the Sustainable Development Goals: An empirical analysis informed by legitimacy theory. Journal of Cleaner Production, 292, 125962. https://doi.org/10.1016/j.jclepro.2021.125962

- Torelli, R., Balluchi, F., & Furlotti, K. (2020). The materiality assessment and stakeholder engagement: A content analysis of sustainability reports. Corporate Social Responsibility and Environmental Management, 27(2), 470–484. https://doi.org/10.1002/csr.1813

- Turzo, T., Marzi, G., Favino, C., & Terzani, S. (2022). Non-financial reporting research and practice: Lessons from the last decade. Journal of Cleaner Production, 345, 131154. https://doi.org/10.1016/j.jclepro.2022.131154

- Wee, M., Tarca, A., Krug, L., Aerts, W., Pink, P., & Tilling, M. (2016). Factors affecting preparers’ and auditors’ judgements about materiality and conciseness in integrated reporting. ACCA. Retrieved from https://www.integratedreporting.org/wp-content/uploads/2016/08/pi-materiality-conciseness-ir-FINAL.pdf