?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study examined the relationship between IR assurance and investment decision-making. The study used a sample of 100 companies that have a public listing on the Johannesburg Stock Exchange (JSE) over a three-year period (2018, 2019 and 2020) to collect the secondary data used to measure the variables. Using a multiple regression approach to analyse the data, the findings of this study displayed an increase in companies assuring their IRs and confirm a positive influence between IR assurance and investment decision-making. The results obtained in this study provided empirical evidence that companies are increasingly adopting the practice of assuring both financial and non-financial information in their IRs. This research is limited to a sample of listed companies in a single country. Thus, future studies could consider a cross-country study both in developed and developing countries. The study place emphasis on the need for IR assurance to boost investment decision-making, thereby increasing transparency and credibility among the company’s stakeholders. The study is one of the few studies that bridged the gap in the literature in the area of IR assurance and investment decision-making of corporate firms which has received little attention in Sub-Saharan Africa especially within the South African context.

1. Introduction

Integrated reporting (IR) practice has evolved rapidly since the International Integrated Reporting Council (IIRC) was founded in 2010 (Rinaldi, Unerman & De Villiers, Citation2018). An IR encompasses pertinent information that is both financial and non-financial of an organisation which lead to value creation from short to long term (IIRC, Citation2021). South Africa (SA) was the first country to mandate listed companies to publish integrated reports (IRs) on an annual basis (Ahmed Haji & Anifowose, Citation2016a). Although only listed companies are mandated to publish IRs in SA, unlisted companies are voluntarily adopting the practice of IR (Briem & Wald, Citation2018). The emergence of IR has become a leading form of corporate reporting in SA which has also created a considerable number of benefits, internally and externally, for organisations that have adopted it (Roberts, Citation2017; Qaderi et al., Citation2023). One of the benefits of adopting IR is the improvement in internal incorporation and management. IR has enhanced the way companies think and report on their business (IFAC, Citation2017b).

The rising popularity of IR has increased calls for the assurance of IRs in order to enhance the integrity and reliability of the information reported (Ofoegbu et al., Citation2018; Borgato & Marchini, Citation2021). IR assurance practice in South Africa is not regulated. However, companies are voluntarily assuring their IRs for the benefits that they derive from providing assurance, such as enhancing the integrity and reliability of the information in the IRs, risk minimisation and reputational considerations. However, due to the limitations of the existing professional standards of IR assurance, assurance service providers are currently limited to assuring the financial part of the report (Maroun, Citation2018; Kilic, Citation2018; Briem & Wald, Citation2018). This is a result of the limitations in the existing professional standards and the fact that IR assurance is not yet mandatory. There are steps being taken to address the limitations in the existing professional standards (Maroun, Citation2020). The International Financial Reporting Standards (IFRS) Foundation previously broadcasted the formation of the International Sustainability Standards Board (ISSB) and the consolidation of the Value Reporting Foundation, home to the Framework of IR together with the Sustainability Accounting Standards Board (SASB) Standards. The consolidation of the Value Reporting Foundation was completed into the IFRS Foundation. In light of this, the study sets to assess the IR assurance practices of JSE-listed companies and the relationship between IR assurance and investment decision-making.

There are existing challenges when assuring IRs, specifically, whether IR assurance has any impact on investment decision-making (Miralles-Quiros et al., Citation2021; Simpson, Aboagye-Otchere & Lovi, Citation2016; Briem & Wald, Citation2018). Many IRs are not assured and, if they are, it is only for selected parts and not the entire report (Association of Chartered Certified Accountants (ACCA), Citation2015). Furthermore, this problem is worsened by the limitations of the existing professional standards when dealing specifically with IR assurance (Maroun, Citation2018). Nevertheless, in spite of the existing challenges when assuring IRs, companies are voluntarily assuring their IRs. The study examined the IR assurance practices of JSE-listed companies and whether the IR assurance practices have a relationship with investment decision-making.

Thus, this led to the research question examining whether IR assurance have any relationship with investment decision-making, and the formulation of the three objectives of this study: (i) determine the association between IR assurance of JSE-listed companies and investment decision-making; (ii) evaluate the IR assurance practices of JSE-listed companies; (iii) determine the degree to which the JSE-listed companies assure their IRs. The motivation come from prior studies which suggest the need for a more in-depth analysis of IR assurance and the influence that IR assurance has on investment decision-making (Goicoechea et al. Citation2019; Briem & Wald, Citation2018; Cheng, Green, Conradie, Konishi & Romi, Citation2014).

With the anticipation that IR will become the corporate reporting norm, it is not surprising that the importance placed on IR assurance has increased as IRs become more valuable for decision-making on investments (Miller et al., Citation2017). Nevertheless, the past recent years have seen an increasing demand for IR assurance (Maroun, Citation2018). However, only selected parts of the IRs are still assured. Non-financial assurance is described as one of the possible encouragers of high-quality reporting alongside the company size, industry membership, presence of a sustainability committee, compliance with reporting frameworks and the decision to supplement IRs with independent sustainability reports (Malola & Maroun, Citation2019). Assuring the entire IR will therefore enhance the credibility and reliability of the information as well as the likelihood of investment decisions. Even though IR assurance is not mandatory, the benefits are crucial.

The high costs associated with IR assurance poses a challenge because of the increased complexity of the assurance skills required that might need multidisciplinary teams (Simnett & Huggins, Citation2015). The costs associated with IR assurance are a concern to companies and pose limitations for companies to engage in IR assurance practices to enhance the reliability and credibility of their IRs. However, studies also found that preparers of integrated reports relied on a combination of different methods to demonstrate to users the reliability IRs (Hoang & Phang, Citation2021; Briem & Wald, Citation2018; Maroun, Citation2018).

The purpose of this study was to examine the relationship between IR assurance and investment decision-making. The population was confined to JSE-listed companies only because of the JSE mandatory prerequisite for companies that are listed to prepare and publish IRs annually. The selection was limited to companies from different sectors with five or more companies which published their IRs annually for the period under this research (2018–2020). The selected period was chosen to ensure comparability of the data throughout the study. The selection excluded companies that did not publish their IRs for one year or more during the period of the study. Companies which got delisted during the period of the study were also excluded. The study found that some of the companies conducted compliance reviews in place of independent assurance. In some cases, the management of the companies just verified the processes for measuring the non-financial information rather than providing assurance. The study examined the IRs of the companies only. It was important for the study that details on the assurance of the IRs were readable and easily identifiable.

The study acknowledges the limited scholarly research on the topic of IR assurance and its relationship with investment decision-making, particularly in SA. However, despite these limitations, the study remains valid because of the need to recognise the value of IR assurance and to determine its relationship with investment decision-making. IR assurance places companies that are willingly assuring their IRs in a favourable position (Akisik & Gal, Citation2020). Prior studies show that IRs are perceived credible and reliable when assured. With the need to enhance users’ confidence, the study considered the pertinence of IR assurance practices by JSE-listed companies.

The study contributes to the literature on IR assurance and investment decision making (Reimsbach, Hahn & Gürtürk, Citation2018; Hoang & Phang, Citation2021). It may influence government and regulatory bodies to decide whether to retain the current voluntary practice of IR assurance or to introduce a mandatory regulation to compel listed companies in SA to assure their IRs. Additionally, it may also deliver the basis for the development of a standardised framework that could be utilised for assuring IRs and used by assurance service providers including audit professionals. The study will assist in understanding the nature and extent of IR assurance practices in SA. The study will also provide pertinent insights into IR assurance, such as aspects that influence users’ confidence in the IRs that are assured.

2. Background

IR has become the current frontier in corporate reporting (De Villiers & Hsiao, Citation2018). There has been an increasing emphasis on enhancing the reliability of IRs in recent years (Hoang & Phang, Citation2021). The core objective of IR is to provide an explanation to financial capital providers how organisations create value over a period of time (IIRC, Citation2021). IR improves the quality of information, which contributes to efficient capital allocation, and decision-making processes of investors and shareholders (Sarioglu, Dalkilic & Durak, Citation2019). IR integrates fresh ideas on reporting that has changed the corporate reporting landscape, improved the ability of investors to assess companies’ prospects and provide answers to overcome the criticisms of traditional accounting reporting models (De Villiers et al., Citation2017). The practice of IR has made corporate disclosures an effective means of communication to improve efficiency in management and investment decision-making (De Villiers, Citation2018). IRs are more than just a combination of financial and non-financial information and must also clearly explain how organisations create value in relation to social, economic, environmental and financial factors (Maroun, Citation2018). IR takes a wider view because it considers intellectual and social relationships, as well as human and natural capitals instead of just financial and manufactured capitals that organisations commonly report in financial reports (Dorin, Rosca, Costea & Suciu, Citation2020). The concept of integrated thinking is encouraged by IR (Roberts, Citation2017), which facilitates a better understanding of the impact of decision making on value creation (Dorin et al., Citation2020). The essence of integrated thinking is the management of the six capitals: financial, manufactured, intellectual, human, social and natural, in turn, is applied in the preparation of IRs to show investors that the company’s board and management are mindful of the need to ensure the ongoing viability of the business (Roberts, Citation2017).

Although SA has taken a leading position in promoting IR, Australia is also amongst the early adopters of IR and companies in Japan have contributed to the significant growth in IR (IIRC, Citation2018). IRs have the ability to make companies more cognisant of the impact they have and their dependence on social and environmental capitals (Malola & Maroun, Citation2019). Moreover, IRs have the potential to make companies incorporate and alter their strategy and operations in order to commit to long-term sustainability and stakeholder accountability (Malola & Maroun, Citation2019). For companies to survive and thrive in today’s competitive world, it is critical that they align their decisions and practices with the interests of society and the community (Du Toit et al., Citation2017). Stakeholders depend on high quality relevant information from companies to influence their decision-making (Zhou, Simnett & Green, Citation2017). Thus, the disclosure of non-financial information helps stakeholders to measure, monitor and manage a company’s performance and the impact of the company on society (Barnabe et al., Citation2019). As a result, the adoption of IR has increased globally.

2.1. Integrated reporting assurance

The integrity of non-financial information in IRs are at risk if only the financial part of the report is assured (Kilic, Citation2018). Without mechanisms that enhance credibility, IRs will fail to achieve their objective to give users dependable information for their decision-making purposes (Kilic, Citation2018). If IRs are perceived to lack credibility, their aim will likely not be achieved (IIRC, Citation2018). IR assurance enhances users’ confidence (IFAC, Citation2017a; Erin & Olojede, Citation2024). Assurance clarifies, informs, and enables criticism while making sure the credibility of the information being used to inform management decisions is reliable (Maroun, Citation2020). A study on German companies which publish IRs established that the appreciation of non-financial information together with the validity and reliability of the published information are among the causes for the voluntary assurance of the IRs (Briem & Wald, Citation2018). Assuring financial reports is mandatory whilst assuring IRs is not yet mandatory. Studies addressing the assurance of IRs have recognised the demand and value of IR assurance (Jeriji & Nasfi, Citation2023; Miller et al., Citation2017)

Although the role of audit committee functions have been expanded to incorporate checking organisation processes especially financial reports, there is not much knowledge regarding the actual role of audit committees in non-financial reporting processes, especially in IR practices (Ahmed Haji and Anifowose, Citation2016a). Auditors face multiple challenges when assuring non-financial information, one being the fact that companies have to improve their internal controls over non-financial information flows in order for auditors to have the ability to test and rely on internal controls (Goicoechea et al., Citation2019). Neither the IIRC nor SA’s codes of corporate governance have made it mandatory for IRs to be assured (Maroun, Citation2018). The limitations in the existing professional standards contribute to the challenges when assuring IRs because the existing professional standards were not designed for IR assurance.

There is a paucity of research considering IR assurance and its influence on investment decision-making. Most studies outline the benefits and the challenges associated with the assurance of IRs (Briem & Wald, Citation2018; Maroun, Citation2018). Prior studies concur that investors make reasonable investment-related judgements if the information presented in reports is reliable and credible (Reimsbach et al., Citation2018; Briem & Wald, Citation2018; Kilic, Citation2018; Cheng et al., Citation2014). There is a need for legitimising the role of accounting firms in assuring non-financial information (Briem & Wald, Citation2018). As such, IRs will be most valued by stakeholders if the information being reported is credible, thus, potentially affecting investment (ACCA, Citation2015).

Assurance enhances confidence and provides value to management disclosures (Farewell & Pinsker, Citation2015). There is a significant relationship between the type of assurance and the likelihood of investing as investors are more likely to trust an independent assurance than a management report (Farewell & Pinsker, Citation2015). Investors ascribe value to companies that use high quality financial reporting and are more willing to pay a higher share price for these companies (Elliot, Fanning & Peecher, Citation2020). Nevertheless, there has been little guidance on assuring matters other than financial statements until the International Standard on Assurance Engagement (ISAE) 3000 was issued by the IAASB (Jones & Iwasaki, Citation2011). Audit engagements for selected non-financial information are usually conducted in accordance with ISAEs (Maroun, Citation2018). IRs are still not assured entirely, which may lead to the credibility of the reports being questioned. These standards are designed to provide security for easily identifiable subject matter according to well-defined criteria (AccountAbility, Citation2018). This makes determining the materiality of non-financial information a challenge because professional standards were established in a financial reporting context (Maroun, Citation2018). Overcoming these limitations of the existing professional standards for the assurance of integrated reports will require more research to develop mechanisms that will promote and improve the assurance of IRs. A vital part of IR practices is the development of the normative frameworks and regulations (Jerifi & Nasfi, Citation2023).

3. Theoretical literature review

Studies focusing on integrated reporting and integrated reporting assurance use the following theories, among others: stakeholder theory (Adegboyegun et al., Citation2020; Adhariani and De Villiers, Citation2019; Fernando and Lawrence, Citation2014); legitimacy theory (Ahmed Haji and Anifowose, Citation2016b; Ahmed Haji and Anifowose, Citation2017; Herbert and Graham, Citation2021); agency theory (Briem & Wald, Citation2018); and institutional theory (Briem & Wald, Citation2018; Ntim & Soobaroyen, Citation2013). Stakeholder theory is used to provide an explanation why organisations make certain social responsibility disclosures in their annual reports (Deegan, Citation2014). While stakeholder theory discusses the expectations of a particular group (stakeholders), legitimacy theory discusses what the society in general expect (Deegan, Citation2014). Agency theory provides a discussion on the problems that happen in companies due to the split of owners and managers and stresses the mitigation of these problems (Panda and Leepsa, Citation2017), whilst institutional theory provides a link between the organisation and the social environment in which the organisation operates (Deegan, Citation2014). Legitimacy, stakeholder and institutional theories are complementary and can be linked to non-financial information disclosure practices and to financial information disclosures (Deegan, Citation2014; Fernando and Lawrence, Citation2014). Stakeholder theory was found to be most applicable for this study.

Stakeholder theory describes the relationships between an organisation and its stakeholders, collectively with the overall performance results of the relationships (Fernando and Lawrence, Citation2014; Jones, Harrison & Felps, Citation2018). Under the stakeholder theory, management is required to report information to stakeholders that include employees, customers, suppliers, banks, communities and shareholders (Tanggamani, Amran & Ramayah, Citation2018). Stakeholders require organisations to meet numerous expectations of various stakeholder groups, rather than only the expectations of shareholder (Fernando and Lawrence, Citation2014). Social and environmental disclosures are vital and non-financial information play a vital role when making investment decisions (De Villiers, Citation2018). Nevertheless, the Global Reporting Initiative and the International Integrated Reporting (IIR) Framework require organisations to identify their stakeholders to ensure that key sustainability information is disclosed in their sustainability and IRs (De Villiers, Citation2018). The stakeholder theory requires managers to manage the business in the interests of the stakeholders, although their can sometimes be influenced by the moral and ethical values of society (Kilic et al., Citation2020). Where unethical practices exist, companies should demand sustainability guarantees to remain accountable and transparent to their shareholders and stakeholders (Kilic et al., Citation2020).

3.1. Linking stakeholder theory to IR assurance

This theory addressed the relationship between IR assurance and investment decision-making because management is required by this theory to report information to stakeholders. Thus, IR assurance gives its users the confidence that the information is credible and reliable. The stakeholder theory accentuates an organisation’s accountability and the rights of stakeholders (Fernando and Lawrence, Citation2014). Stakeholder theory was considered more relevant for this study than the other theories described above because it addresses the relationship between IR assurance and investment decision-making. Nevertheless, IR aims to enhance accountability and stewardship (IIRC, Citation2021). The importance of IR stems from the requirement placed on management by the stakeholder theory to report information to stakeholders. IR recognises the importance of reporting on more than just financial information and encourages a long-term sustainable orientation that will benefit corporations and stakeholders (De Villiers, Hsiao & Maroun, Citation2017). Companies are generally more proactive in their decision to provide assurance, especially for powerful and influential stakeholders, thus, their pressure has also led to an increase in the assurance of non-financial information (Martínez-Ferrero & García-Sánchez, Citation2018).

4. Empirical literature review and hypotheses development

Companies have used financial reporting many years to communicate relevant information to stakeholders and investors, and to ensure that they make informed decisions (Abdulla & Runco, 2020). Empirical evidence suggests that higher quality financial reporting is associated with more efficient capital investment (Farewell & Pinsker, Citation2015; Jung, Lee & Weber, Citation2014; Lin, Wang & Pan, Citation2016). However, many companies have now adopted IR to communicate relevant financial and non-financial information to stakeholders and investors. Given that the assurance of IRs is not yet mandatory, this study examined the relationship between integrated reporting assurance and investors’ decision-making. Many companies are responding to calls for the assurance of IRs for different reasons and benefits. Investors make their investment decisions based on the organisation’s transparency along with the accuracy and reliability of the published information in the organisation’s reports. A study on social responsibility reporting and its assurance in China found that the assurance of non-financial information increased credibility and investors’ willingness to invest (Shen et al., Citation2017). Similarly, the study of Steinmeier and Stich (Citation2019) found a positive association between sustainability assurance and sustainability investment. Investors are more likely to invest when assurance is provided on reports (Farewell & Pinsker, Citation2015). Thus, the assurance of IRs will similarly increase investors’ willingness to invest.

The assurance rate for the world’s major 250 companies that publish corporate social responsibility reports reached 63% in 2015 from 30% in 2005 (Shen et al., Citation2017). By 2017, this rate had increased to 67% (KPMG, Citation2017). However, by 2020, the rate declined to 62% due to the rise in the number of Chinese companies in the 250 world’s largest companies since 2017 (KPMG, Citation2020). These assurance numbers are subject to independent assurance (KPMG, Citation2020; KPMG, Citation2017; Maroun, Citation2020). Furthermore, the involvement and domination of the government in China shaped how the assurance of non-financial information was perceived and valued by Chinese investors (Shen et al., Citation2017). The assurance of IRs is a rising area of interest for researchers, companies, assurance professionals and investors (Brown-Liburd et al., Citation2018; Cheng et al., Citation2014; Goicoechea et al., Citation2019; Maroun, Citation2020). Prior studies have shown the importance of IR assurance for investment decision-making (Brown-Liburd et al., Citation2018; Maroun, Citation2020, p. 190; Steinmeier & Stich, Citation2019). However, despite the growing interest in IR assurance, there is not enough empirical studies on how IR assurance influence investors’ decision-making (Cheng et al., Citation2014; Goicoechea et al., Citation2019).

While previous studies focused on the effects of assurance of sustainability information, this study extended its line of research (IR assurance and investment decision-making) by investigating the relationship between IR assurance, specifically of JSE-listed companies, and investment decision-making. To meet the research objectives of this study, the hypotheses below are formulated to test the relationship between integrated reporting assurance and investment decision-making.

H1: Type of assurance has positive influence with investment decision-making.

H2: Level of assurance has a positive influence with investment decision-making.

5. Research design

A quantitative research method using secondary data to measure the relationship between the variables of this research was applied in this study. The variables consist of independent variables (IR assurance), dependent variables (investment decision-making) as well as controlling variables (company size, profitability, leverage, share price and independence of assurance providers), and are described below. Given the focus of this research which was to evaluate the current state of the assurance of IRs of JSE-listed companies and how the current integrated reporting assurance practice associates itself with users’ investment decision-making, a positivist approach using deductive reasoning allowed for an objective measure of the relationship between assurance and investment decision-making. Positivism and realism are the two most common scientific philosophies used in quantitative studies (Coleman, Citation2019; Brown-Liburd et al., Citation2018; Ryan, Citation2018). This study used a positivist approach to find statistical correlations of the two variables (IR assurance and investment decision-making) and to demonstrate the relationships between them. In order to explain the research phenomena, the research approach was applied to gather numerical data that were then analysed using statistical analysis.

The population of this study consist of 297 publicly listed companies on the JSE in 2018 from different sectors to which the provision of the JSE regulation to publish IRs applies. The JSE is amongst the top exchanges worldwide on market capitalisation. JSE-listed companies were used because of the JSE regulation that requires publicly listed companies to publish their IRs annually. JSE-listed companies are amongst those that control a substantial amount of the economy of SA. Therefore, the listed companies were found to be more than likely to deliver a satisfactory picture of IR practices (Ahmed Haji and Anifowose, Citation2016a) and IR assurance practices. JSE-listed companies are amongst those that control a substantial amount of the South African economy and are possibly likely to deliver a clear picture of IR practices (Ahmed Haji and Anifowose, Citation2016a; Erin and Adegboye, Citation2022). Given the probability that JSE-listed companies are likely to assure their IRs because of the availability of resources, the population was limited to JSE-listed companies. Mindful of the regulatory requirement of JSE-listed companies to publish IRs, along with the growing calls for IR assurance (De Villiers, Rinaldi & Unerman, Citation2014; Briem & Wald, Citation2018), this study evaluated the relationship between IR assurance and investment decision-making.

We selected sample from JSE-listed companies over a period of three years from 2018 until 2020. The reason for choosing this period was stirred by the fact that JSE listed companies have been publishing IRs since 2010 as well as the expectation that the companies are likely to have adopted the practice of assuring IRs because they have the financial resources. Secondly, a lot of companies, large and small, were negatively impacted by the effects of the global pandemic of Covid-19 since 2020. This was observed through the data collected during the year 2020. The study included companies from different sectors therefore the sample consisted of five companies per sector. The companies were selected based on the availability of the IRs of the companies for the period of the study (2018–2020).

5.1. Sample selection

The total population of JSE-listed companies as of July 2018 was 297 from various sectors. The list was made available through the iRESS database. Five companies were selected from each sector. Thus, the population was adjusted to remove companies from sectors which did not have at least five companies. The decision to select five companies per sector was because of the need to ensure that the sample size was both manageable and large enough for statistical analysis of the data. Companies that did not publish an IR for any year falling within the period of this study were also excluded. The sample consisted of the remaining companies listed by sector description. Five companies per sector were selected for the sample and this was based on the top five companies with published IRs for the period of this study. A sample of 100 companies from 20 different sectors was selected. A total of 300 IRs, 100 IRs for each year, were downloaded from the JSE website. The study applied a purposive non-probability sampling method to select a manageable sample of 100 JSE-listed companies in 2018. A purposive non-probability sampling method was applied to select the sample intended to achieve a fair distribution of companies in the various industries. This approach was in line with other studies that adopted a similar approach such as Herbert and Graham (Citation2021) and Du Toit et al. (Citation2017). below displays details of the research population and sample selection.

Table 1. Research population and sample selection.

5.2. Variable measurement

5.2.1. Independent variables

This study used quantitative data to test the hypothesis that predicts that the independent variables will positively influence the dependent variable. This study used one independent variable and five control variables to influence the dependent variable. Appendix B shows the operationalisation of the variables. The independent variable used was IR assurance, and it was measured by two proxies, type of assurance and level of assurance. The two proxies of assurance are described below.

There are limited studies that discuss measures of assurance. To determine the relationship of IR assurance with investment decision-making, it was imperative that the assurance in the IR was identifiable. Certain studies used the availability of assurance in IRs as a proxy on an experimental study that investigated the impact of IR assurance on investment related decisions and judgements (Reimsbach et al., Citation2018). Assurance in IRs and the type of assurance provider are the most used proxies of assurance. This study used type of assurance using an indication of the availability of assurance of the six capitals of IRs as well as the level of assurance. Using the level of assurance as a proxy for assurance is informed by the fact that only the financial information is assured in some IRs. In some cases, the financial information and a selection of the non-financial information are assured. It is essential for this study to measure assurance by indicating the type of assurance provided. The level of assurance also links to the level of confidence (Elliot, Fanning & Peecher, Citation2020; Farewell & Pinsker, Citation2015; Martínez-Ferrero & García-Sánchez, Citation2018; Reimsbach et al., Citation2018; Shen et al., Citation2017).

5.2.1.1. Proxy 1 – Type of assurance

The principal role of audit committee functions has expanded to include monitoring processes beyond their financial reporting given the shifting nature of the business environment, the increasing number of corporate failures and the various capitals that companies depend on for their success (Ahmed Haji and Anifowose, Citation2016a; IIRC, Citation2021). The capitals comprise of financial, manufactured, intellectual, human, social and relationship, and natural (Herbert and Graham, Citation2021). This study considered the assurance of the capitals because, similar to the auditing of financial information, prior studies have shown that IR assurance is perceived as the key element of external scrutiny of non-financial information (Maroun, Citation2020; Martínez-Ferrero & García-Sánchez, Citation2018; Reimsbach et al., Citation2018).

5.2.1.2. Proxy 2 – Level of assurance

There are two recognised assurance levels, namely, reasonable assurance and limited assurance (Hoang & Trotman, Citation2021). A third assurance level is a moderate level of assurance that is equivalent to a limited level of assurance (Michelon, Patten & Romi, Citation2019). Both reasonable and limited assurance were found to have resulted in higher reliability estimate than no assurance at all (Hoang & Phang, Citation2021). Limited assurance diminishes engagement risk to a greater level than reasonable assurance (Michelon et al. Citation2019). On the contrary, companies that chose a reasonable or high level of assurance were usually larger and more profitable (Ruiz-Barbadillo and Martínez-Ferrero Citation2020). Higher levels of assurance require a more intensive assurance process to adequately reduce the risk of an assurance engagement (Hummel, Schlick & Fifka, Citation2019). The level of assurance is therefore denoted by the different proxies, namely, limited assurance, reasonable assurance, as well as whether the assurance is combined or is provided for by the internal auditors of the company or external auditors.

5.2.2. Dependent variables

Investment decision-making is used as the dependent variable of this study. Investment decision-making can be measured through various proxies. However, this study used three proxy variables to measure investment decision-making, which are: earnings; the number of shares issued; and dividend yield (Elliot, Fanning & Peecher, Citation2020; Pinsker & Wheeler, Citation2009). These proxies were founded to be associated with investment opportunities (Serafeim, Citation2015).

5.2.2.1. Proxy 1 – Earnings

Earnings is commonly used to measure investment, such as a company’s growth and market value (Gal & Akisik, Citation2020). Investment results in increased earnings, revenue and book value in the future (Hsiao & Li, Citation2012). Thus, IR is expected to improve expectations for future profits and reduce uncertainties brought on by sustainability-related activities (Caglio et al., Citation2020). Findings showed that most investors are particularly susceptible to shifts in business earnings (Moikwatlhai et al. (Citation2019).

5.2.2.2. Proxy 2 – Issued shares

There is a positive influence between IR practice and shares held by long-term investors (Moikwatlhai et al., Citation2019). Findings showed that investors are more likely to invest or hold shares in companies that practice IR (Serafeim, Citation2015). Consequently, investor confidence is therefore more likely to grow when the IR is assured. The study extracted the number of issued shares from the IRs of the listed companies use to measure this variable.

5.2.2.3. Proxy 3 – Dividend yield

Dividend yield states how much income will be received in relation to the share price (Kengatharan & Ford, Citation2021). The study measured the dividend yield derived from the IRs. A dividend yield of less than 2% was considered as low, a dividend yield between 2% and 6% as reasonable and above 6% as high to determine the level of the dividends that the company paid out over the course of the reporting year. The study controls for other variables such as company size, profit margin, leverage, share price and assurance providers as documented in other IR and assurance studies (Erin and Adegboye, Citation2022; Ruiz-Barbadillo and Martínez-Ferrero Citation2020).

5.3. Control variables

The study used company size, profitability, leverage, improved share price and independence of the assurance provider as additional control variables. These variables may have an impact on the data, however, they were not investigated. Studies provide evidence that the incentives for IR assurance may be impacted by control variables (Ruiz-Barbadillo and Martínez-Ferrero Citation2020; Maroun, Citation2020; Steinmeier and Stich Citation2019).

5.4. Model specification

The study aims to explore the relationship between IR assurance and investment decision-making. In order to analyse the data collected from the IRs of the listed companies selected for the study, multiple regression analysis was employed in the study. Hypothesis (H1) is linked to EquationEquations (1)(1)

(1) , Equation(3)

(3)

(3) and Equation(5)

(5)

(5) while hypothesis (H2) is linked to EquationEquations (2)

(2)

(2) , Equation(4)

(4)

(4) and Equation(6)

(6)

(6) . To investigate the relationship between the dependent, independent, and control variables, the following regression formulas were utilised:

5.5. Earnings

5.6. Number of shares issued

5.7. Dividend yield

Where:

b(1), b(2), b(3), b(4), b(5) and b(6) are weights of variables

(Type) = depends on Type of Assurance

(Level) = depends on Level of Assurance

6. Empirical results and discussion

This section presents the findings from the secondary data that was gathered for this study between 2018 and 2020. The results from the analysis aim to address the objectives of this study including the hypotheses of this study.

6.1. The association between IR assurance and investment decision-making

This section addresses the first objective of this study which is to determine the association between IR assurance of JSE-listed companies and investment decision-making. Investment plays a pivotal role in driving the disclosure and assurance of non-financial information, as they deem it pertinent and valuable. Prior research indicates that investment-related decisions increase when IRs are assured (Briem & Wald, Citation2018; Farewell & Pinsker, Citation2015; Miralles-Quiros et al., Citation2021; Maroun, Citation2018; Shen et al., Citation2017). The study of Reimsbach et al. (Citation2018) discovered that decisions pertaining to investments increased when non-financial information was assured. For investors who base their investment decisions on the information included in IRs, IR assurance will therefore be crucial. Using a multiple regression model to analyse the data, the study found no statistical evidence in that ‘Type of Assurance’ and ‘Level of Assurance’ impacted ‘earnings’; however, it could be inferred that the two proxies of assurance had a positive influence with ‘earnings’. It was also inferred that both ‘Type of Assurance’ and ‘Level of Assurance’ had a positive influence with ‘Dividend Yield’ based on the result from . In , the statistical outcomes of the ‘number of shares’ showed that ‘Type of Assurance’ had a negative influence while ‘Level of Assurance’ had a positive influence with ‘number of shares issued’.

Table 2. Regression results of earnings.

Table 3. Regression results of dividend yield.

Table 4. Regression results of number of shares issued.

The degree to which JSE-listed companies assured their IRs is found to be positive as the majority of the companies chose reasonable external audit assurance and reasonable combined assurance for their IRs. Compared to when a limited assurance is given, this is more likely to improve how users of IRs view the report for investments. However, limited assurance is better than no assurance (Hoang & Trotman, Citation2021). The findings of this research are similar to that of other studies with a similar focus area. The results of the studies revealed a favourable correlation between IR assurance and investment decision-making (Hoang & Phang, Citation2021; Reimsbach et al., Citation2018; Shen et al., Citation2017; Steinmeier and Stich Citation2019). The study of Shen et al. (Citation2017) found that investors were more willing to invest when assurance was provided on corporate social responsibility, especially when came from an independent expert rather than a company expert. A positive correlation was also observed between sustainability assurance and sustainability investment, according to the findings of Steinmeier and Stich (Citation2019). To increase the integrity and dependability of IRs, it is necessary to support the valuable practice of reporting on non-financial information and providing independent external assurance.

6.2. Reliability test

The Cronbach’s Alpha coefficients were tested to make certain the variables were reliable. A Cronbach’s Alpha is a measure of internal consistency, that is, how closely connected a set of variables are as a group. It is believed to be a measure of scale reliability. To test the reliability of the variables used, Cronbach’s Alpha coefficients were calculated and reported in . The overall Cronbach’s Alpha is presented in as 0.662. The item-specific alphas are high, which indicates that there is a high level of internal consistency for the scale with this specific sample.

Table 5. Reliability statistics.

A reliability test value of 0.7 is generally accepted as a minimum, while a value as low as 0.6 may also be considered depending on the nature of the data. The value should not be below 0.6 for widely used scales (Dash, Citation2010). As presented in , the variables have Cronbach’s Alpha of 0.662, which is above 0.6.

6.3. Earnings regression model (dependent variable 1)

Based on , ‘Company Size’ is significant at 1% level while ‘Profit Margin’ and ‘Share Price’ are significant at 5% level. The variables of interest, ‘Type of Assurance’ and ‘Level of Assurance’ are not significant, and it can be concluded that there is no statistical evidence that ‘Type of Assurance’ and ‘Level of Assurance’ impact earnings. However, considering the coefficient of 0.138 and 0.024, it can be inferred that ‘Type of Assurance’ and ‘Level of Assurance’ have a positive impact on ‘earnings’. presents statistical evidence that the goodness of fit is satisfied. Thus, the study concludes that the data fits the model developed at a 5% significant level. also explains the power of the variables used in the model in determining earnings. There is statistical evidence that the variables are not strong enough since they are able to explain only a 7.3% variation in ‘earnings’.

6.4. Number of shares issued (dependent variable 2)

Based on , ‘Profit Margin’ and ‘Type of Assurance’ are significant at 1% level while, ‘Company Size’ and ‘Independence of Assurance Providers’ are significant at 5% level. However, in the case of ‘Level of Assurance’, only ‘Company Size’ is significant at 5% level. Considering the variable of interest, ‘Type of Assurance’, it is significant and it can be concluded that there is statistical evidence that ‘Type of Assurance’ has an impact of −0.211 on ‘Number of Shares Issued’. ‘Level of Assurance’ is also significant and it can be concluded that there is statistical evidence that ‘Level of Assurance’ has an impact of 0.131 on ‘Number of Shares Issued’. In other words, ‘Type of Assurance’ has a negative effect on the ‘Number of Shares Issued’ and ‘Level of Assurance’ has a positive effect on ‘Number of Shares Issued’. Based on the presentation in , there is statistical evidence that the goodness of fit is satisfied and it can be concluded that the data fit well the model developed at 1% significant level. also explains the power of the variables used in the model in determining ‘Number of Shares Issued’ and there is statistical evidence that the variables are not strong enough since they are able to explain only 8% and 8.6% variation in ‘Number of Shares Issued’.

6.5. Dividend yield regression model (dependent variable 3)

Based on , ‘Share Price’ is significant at 1% level while ‘Company Size’, ‘Leverage’ and ‘Profit Margin’ are significant at 5% level. Considering the variables of interest, ‘Type of Assurance’ and ‘Level of Assurance’, are not significant and it can be concluded that there is no statistical indication that ‘Type of Assurance’ and ‘Level of Assurance’ have an impact on ‘Dividend Yield’. However, considering the coefficients of 0.013 for ‘Type of Assurance’ and 0.009 for ‘Level of Assurance’, it can be inferred that both ‘Type of Assurance’ and ‘Level of Assurance’ have a positive effect on ‘Dividend Yield’. As presented in , there is statistical evidence that the goodness of fit is satisfied and it is concluded that the data fit well the model developed at 1% significant level. helps to explain the power of the variables used in the model in determining ‘Dividend Yield’ and there is statistical evidence that the variables are not strong enough since they are able to explain only 5.8% variation in ‘Dividend Yield’.

6.6. IR assurance practices of JSE-listed companies

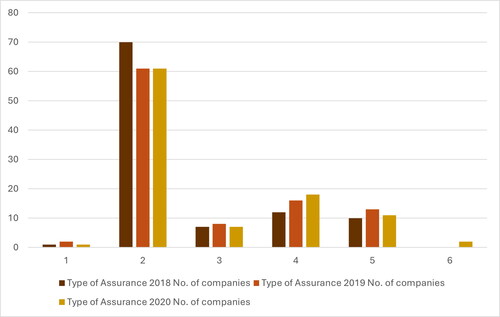

This section addressed the second objective of the study. and below show how the selected 100-listed companies assured their IRs for the periods 2018, 2019 and 2020 using a 6-point Likert Scale (see Appendix A) for ‘Type of Assurance’. ‘Type of Assurance’ is a proxy of assurance and is denoted by the assurance of the six capitals of IR. Companies will provide assurance for financials but are not mandated to assure non-financial information included within the IRs.

Figure 1. Type of assurance by selected 100-listed companies.

Table 6. Assurance practices of selected 100-listed companies.

Based on and , only one company in 2018 and 2020 did not assure the IRs, while two companies did not assure their IRs in 2019. The assurance of IRs is not mandatory. However, only one company, nevertheless, failed to provide IR assurance in 2018 and 2020, and two companies in 2019. The intricacy of IR assurance or the high costs associated with IR assurance could have been among the several factors that prevented the companies from providing assurance. Providing investors with relevant and reliable information can reduce asymmetry and uncertainties (Akisik & Gal, Citation2020). However, the study revealed an increase of companies assuring their IRs.

For the assurance of the financial capital only (Scale 2), 70% of the companies provided assurance in 2018 and 61% in 2019 and 2020. During the research period, most of the companies simply provided assurance for their financial capital, despite the growing need for IR assurance. This is not surprising considering that companies are required to have their financial reports audited but not their IRs. Nevertheless, companies recognise that, for various benefits, it is critical to assure both the financial and non-financial information. As presented in , the benefits of IR assurance have prompted companies to progressively embrace the practice of assuring more than the financial capital. Companies are aware that providing assurance guarantees the integrity of the IRs, which in turn helps view the IRs as trustworthy and dependable. IR assurance is relevant to stakeholders and investors, particularly if they rely on the stock market data and the information they obtain from the companies’ IRs (Miralles-Quiros et al., Citation2021).

Eight companies in 2019 and seven companies in 2018 and 2020 provided assurance of the financial capital and one additional capital (scale 3). For the assurance of financial capital and two extra capitals (scale 4), 12 companies provided assurance 2018, 16 companies in 2019 and 18 companies in 2020. The annual growth in the assurance of financial capital and two other capitals was reasonable. For the assurance of financial capital and three extra capitals (scale 5), 10 companies provided assurance in 2018, 13 companies in 2019 and 11 companies in 2020. From 2018 to 2019, there was a rise of three companies that provided assurance of financial capital and three other capitals, followed by a decline by three companies in 2020. This may have resulted from the difficulties encountered in 2020 due to the Covid-19 pandemic which impacted every country, causing several to go into a lockdown. It also had an impact on the economy, availability of resources and cash flows. The impact of Covid-19 is still lingering on the operations of many businesses in SA, and the residue will remain for a long time as companies scale down on employees or shut their doors permanently. The study also observed the delayed publication of some of the IRs on the JSE website during the period of the lockdown.

The study found that not a single company provided assurance of all six capitals (scale 6) in 2018 and 2019. Reasons for this were not provided in the reported. However, the challenges faced when assuring non-financial information are not overlooked (Goicoechea et al., Citation2019; Maroun, Citation2018). Companies are still limited by determinants such as company size and assurance costs of IRs (Simnett & Huggins, Citation2015). Some companies mentioned in the IRs that they would take independent assurance of the IRs into consideration in future. However, two companies assured all six capitals in 2020, indicating that companies are progressively addressing calls for the assurance of IRs and the potential of having the entire IR assured. Similar to that of other studies, the findings of this study demonstrate that companies recognise the significance of IR assurance and are treating IR assurance with due diligence (Cheng et al., Citation2014; Goicoechea et al., Citation2019; Hoang & Phang, Citation2021; Hassan et al., Citation2020; Kilic et al., Citation2020).

and make it clear that businesses are progressively embracing the practice of assuring both financial and non-financial information in IRs. Investors are somewhat encouraged by this effort on the part of certain companies. While independent assurance adds credibility to IRs (Shen et al., Citation2017), the study found that some companies provided compliance reviews or had management verify the procedures for measuring non-financial information in lieu of giving independent assurance of the non-financial information. This is a result of companies using their discretion to determine whether the IRs should be assured by an external independent assurance provider. Stakeholders, however, view information backed by an independent assurance as credible (Briem and Wald, Citation2018; Hassan et al., Citation2020; Maroun, Citation2018; Simnett and Huggins, Citation2015). The findings of this study thus confirmed the findings of Miralles-Quiros et al. (Citation2021) and offered empirical proof that companies are progressively adopting the practice of assuring both the financial and non-financial information in IRs.

6.7. The degree to which JSE-listed companies assure their IRs

This section addresses the third objective which aimed to examine the degree to which companies, specifically JSE-listed companies assure their IRs. The study employed ‘Type of Assurance’ and ‘Level of Assurance’ as proxies of assurance. ‘Type of Assurance’ was denoted by the assurance of the six capitals of IR using a 6-point Likert Scale. ‘Level of Assurance’ was denoted by the two recognised assurance levels, limited and reasonable assurance, and whether the assurance was combined or provided by the company’s internal auditors or other representatives of the company or external auditors (See Appendix A). below present the degree to which sample assured their IRs for the period of this study. The study sought to identify ‘Level of Assurance’ through a 7-point Likert Scale (See Appendix A).

Table 7. The extent of the assurance of integrated reports by JSE listed companies (2018).

Table 8. The extent of the assurance of IRs by JSE listed companies (2019).

Table 9. The extent of the assurance of IRs by JSE listed companies (2020).

One company did not provide assurance or indicate the type of assurance in the IR in 2018, according to , while 70 companies indicated assurance of the financial capital. Subsequently, seven companies indicated assurance of the financial capital and one capital, 12 companies assured the financial capital and two additional capitals, and 10 companies assured the financial capital and three additional capitals. None of the companies assured all six capitals in 2018. The ‘Level of Assurance’ in 2018 presents: 15 companies did not indicate the level of assurance even though majority of the companies provided assurance for at least one capital or more as presented under ‘Type of Assurance’. Eight companies provided limited external audit assurance while 37 companies provided reasonable external audit assurance. Nine companies provided limited combined assurance and 31 companies provided reasonable combined assurance.

In , ‘Type of Assurance’ in year 2019, two companies did not indicate the type of assurance whilst a majority, 61 companies, indicated an assurance for only the financial capital. Eight companies indicated assurance of the financial capital and one additional capital, 16 companies assured the financial capital and two additional capitals and 13 companies assured the financial capital and three additional capitals. None of the companies assured all six capitals in 2019. The ‘Level of Assurance’ (in 2019) presents: 17 companies did not indicate the level of assurance in the IRs. This was two companies more than 2018. None of the companies provided limited internal audit assurance and reasonable internal audit assurance. The number of companies that provided limited external audit assurance increased by one to nine in 2019. This was followed by 35 companies provided reasonable external audit assurance which is two companies less than in 2018, seven companies provided limited combined assurance which was also two companies less than in 2019 and lastly, 32 companies provided reasonable combined assurance in 2019 compared to 31 companies in 2018.

Based on , ‘Type of Assurance’ (in 2020) demonstrates that only one company did not indicate any assurance in their IR while 61 companies indicated assurance of the financial capital only. Seven companies indicated the assurance of the financial capital and one additional capital whilst 18 companies assured the financial capital and two additional capitals, 11 companies assured the financial capital and three additional capitals, and two companies assured all six capitals. The ‘Level of Assurance’ (in 2020) shows a reduction of companies which did not indicate the level of assurance in their IRs to 14 and one company which indicated a limited internal audit assurance. None of the companies provided reasonable internal audit assurance. The number of companies that provided limited external audit assurance increased from 2019 by one to 10 companies and a reduction by one company to 34 companies which mentioned a reasonable external audit assurance was provided. Seven companies (same as 2019) provided limited combined assurance. The results show a further increase in the number of companies that offered reasonable combined assurance to 34 in 2020.

Evidently from the above tables, companies are progressively adapting to the assurance of non-financial information in IRs and offering reasonable assurance in most cases. Since secondary data were used for this study, the reasons for the selective assurance of non-financial information or the lack of assurance offered by some companies for non-financial information were not examined.

Based on , out of the 100-JSE listed companies selected for this study, 96% of the companies in 2019 reported that the assurance providers were independent of the reporting company compared to 98% in 2018 and 2020. Only 2% of the companies in 2018 and 2020, and 4% in 2019, failed to include information about their assurance providers’ independence in their reports. It is determined that when the assurance provider is independent, the information in the report is more reliable and trustworthy. The aforementioned findings indicate that there is a favourable relationship between IR assurance and investment decision-making. In other words, IR assurance influences investment decision-making in a favourable way. The result is consistent with other studies of a similar nature that discovered a positive relationship between IR assurance and investment decision-making (Akisik & Gal, Citation2020; Briem & Wald, Citation2018; Cheng et al., Citation2014; Reimsbach et al., Citation2018; Shen et al., Citation2017). These studies also revealed that investors base their decisions about investments on the information’s authenticity and reliability as well as the company’s transparency. Assurance is an element that adds certainty in the accuracy and reliability of the published information (Miller et al., Citation2017). Users of IRs can successfully be reassured about the company’s sustainability through assurance (Goicoechea et al., Citation2019). The results also show that more companies are assuring the IRs, indicating that businesses place a high value on IR assurance.

Table 10. Independence of assurance providers.

7. Summary and conclusion

This study explored the relationship between IR assurance and investment decision-making. There is a rising interest amongst stakeholders to have companies assure the entire information in the IRs other than the financial information. Investors make their investment judgements based on the transparency of the company as well as the reliability and integrity of the information. As a result, the study saw a rise of companies assuring their IRs. The degree to which the independent variables have impact on the dependent variables was examined, and a positive influence was found between IR assurance and investment decision-making. The results of this study confirmed that companies were increasingly adopting the assurance of non-financial information in IRs. Furthermore, the results also confirmed the importance placed on IR assurance for enhancing credibility and reputation among stakeholders.

Investors rely on information in IR to make investment decisions and providing assurance on the reports is one way to improve the credibility and reliability of the information. Investors are likely to gain confidence when IRs are assured. However, companies currently exercise their own judgement with regard to the assurance of the IRs. The practice of assuring IRs is not yet mandatory. The study found that not many companies in the sample made use of an external assurance provider because they had a combined assurance model in place. The study considered the following strategies to improve the quality of IR assurance: (i) the use of independent external assurance providers to assure the entire IR make information reported to be value-relevant. (ii) similar to assurance statements of financial reports, the assurance statements of non-financial information in the IRs should be easy to find and read. (iii) there is need to improve the existing professional standards to take into consideration IR assurance and to ensure consistency in the assurance of the IRs.

The findings of this study have important implications for policymakers and practitioners, especially the corporate executives and those charged with governance. The role of external assurance is crucial in enhancing the quality of integrated reporting. External auditors must brace up for this new challenge by ensuring that the content and form of presentation of the integrated report are reliable and credible. Policymakers may also need to consider the costs and benefits of implementing assurance requirements for integrated reporting. While assurance can provide significant benefits in terms of transparency and accountability, it may also impose additional costs on companies and investors. Policymakers would need to weigh these factors carefully to ensure that any regulatory requirements strike the right balance. There is a need for standard-setters and regulators to continue to engage corporate organizations on the best way to deliver high quality integrated reporting that serves the interest of a wide range of stakeholders. The major contribution from this study highlights the effective interconnectivity between integrated reporting assurance and investment decision.

Finally, we discuss the study limitation and other areas for future research. The study was limited to a sample size of 100 firms, which is country-specific; however, it sets the tone for future empirical research on the subject matter. Firstly, future research could extend this by drawing on the entire main board of the JSE instead of a sample to investigate the relationship between IR assurance and investment decision-making. Secondly, future research could look into extending this research beyond 2020 and post the Covid-19 pandemic. This is because many companies were impacted by Covid-19 pandemic and lockdown in 2020 which was the year the study capped its data. However, regardless of the lockdown from the pandemic in 2020, the findings still displayed an increase in companies assuring their IRs. Lastly, future studies could examine a longer period since this study focused only on a three-year period.

Authors contribution

Mushwana conceptualised the research idea, wrote the introduction and literature review. Chikutuma designed the research methods and analysed the data. Erin interpreted the data, wrote the findings and conclusion.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

We confirm that the data is available upon request. For any enquiries concerning the data used in this study, please feel free to contact Phoebe Mushwana, email: [email protected].

Additional information

Funding

Notes on contributors

Phoebe Mushwana

Phoebe Mushwana is a PhD student in Accounting Sciences at the University of South Africa, within the Department of Financial Accounting. Her research focuses on non-financial reporting.

Chisinga Chikutuma

Chisinga Chikutuma holds a Doctor of Philosophy in Accounting Sciences, and is affiliated with the Department of Financial Accounting at the University of South Africa. His research interest is on nonfinancial reporting.

Olayinka Erin

Olayinka Erin completed his PhD in Accounting at Covenant University, Nigeria. He is presently a Postdoctoral Research Fellow at the University of South Africa. His research is centred on corporate governance.

References

- Abdulla, A. M., & Runco, M. A. (2018). Who funds the future? Federal funding support for creativity and 21st Century skills. Business Creativity and the Creative Economy, 4, 1–20. https://doi.org/10.18536/bcce.2018.10.8.1.01

- AccountAbility. (2018). AA1000 assurance standard (AA1000AS, 2008) with 2018 addendum. https://www.accountability.org/static/AA1000AS_Assurance_Standard_(2018)-1bba66c8e1fa05e9e32719b3481d745c.pdf

- Adegboyegun, A. E., Alade, M. E., Ben-Caleb, E., Ademola, A. O., Eluyela, D. F., & Oladipo, O. A. (2020). Integrated reporting and corporate performance in Nigeria: Evidence from the banking industry. Cogent Business & Management, 7(1), 1736866. https://doi.org/10.1080/23311975.2020.1736866

- Adhariani, D., & De Villiers, C. (2019). Integrated reporting: Perspectives of corporate report preparers and other stakeholders. Sustainability Accounting, Management and Policy Journal, 10(1), 126–156. https://doi.org/10.1108/SAMPJ-02-2018-0043

- Ahmed Haji, A., & Anifowose, M. (2016a). Audit committee and integrated reporting practice: Does internal assurance matter? Managerial Auditing Journal, 31(8/9), 915–948. https://doi.org/10.1108/MAJ-12-2015-1293

- Ahmed Haji, A., & Anifowose, M. (2016b). The trend of integrated reporting practice in South Africa: Ceremonial or substantive? Sustainability Accounting, Management and Policy Journal, 7(2), 190–224. https://doi.org/10.1108/SAMPJ-11-2015-0106

- Ahmed Haji, A., & Anifowose, M. (2017). Initial trends in corporate disclosures following the introduction of integrated reporting practice in South Africa. Journal of Intellectual Capital, 18(2), 373–399. https://doi.org/10.1108/JIC-01-2016-0020

- Akisik, O., & Gal, G. (2020). Integrated reports, external assurance and financial performance: An empirical analysis on North American Firms. Sustainability Accounting, Management and Policy Journal, 11(2), 317–350. https://doi.org/10.1108/SAMPJ-02-2019-0072

- Association of Chartered Certified Accountants (ACCA). (2015). Insights into Integrated Reporting: Challenges and best practice responses. https://www.accaglobal.com/content/dam/ACCA_Global/Technical/integrate/pi-insights-into-ir-.pdf

- Barnabe, F., Giorgino, M. C., & Kunc, M. (2019). Visualizing and managing value creation through integrated reporting practices: A dynamic resource-based perspective. Journal of Management and Governance, 23(2), 537–575. https://doi.org/10.1007/s10997-019-09467-z

- Borgato, B., & Marchini, P. L. (2021). Auditors’ perceptions of Integrated Reporting assurance: Insights from Italy. Meditari Accountancy Research, 29(7), 31–53. https://doi.org/10.1108/MEDAR-09-2019-0560

- Briem, C. R., & Wald, A. (2018). Implementing third-party assurance in Integrated Reporting: Companies’ motivation and auditors’ role. Accounting, Auditing & Accountability Journal, 31(5), 1461–1485. https://doi.org/10.1108/AAAJ-03-2016-2447

- Brown-Liburd, H., Cohen, J., & Zamora, V. L. (2018). CSR disclosure items used as fairness heuristics in the investment decision. Journal of Business Ethics, 152(1), 275–289. https://doi.org/10.1007/s10551-016-3307-3

- Caglio, A., Melloni, G., & Perego, P. (2020). Informational content and assurance of textual disclosures: Evidence on Integrated Reporting. European Accounting Review, 29(1), 55–83. https://doi.org/10.1080/09638180.2019.1677486

- Cheng, M., Green, W., Conradie, P., Konishi, N., & Romi, A. (2014). The International Integrated Reporting framework: Key issues and future research opportunities. Journal of International Financial Management & Accounting, 25(1), 90–119. https://doi.org/10.1111/jifm.12015

- Coleman, P. (2019). An examination of positivist and critical realist philosophical approaches to nursing research. International Journal of Caring Sciences, 12(2), 1218–1224.

- Dash, M. K. (2010). Factors influencing investment decision of generations in India: An econometric study. International Journal of Business Management and Economic Research, 1(1), 15–26.

- De Villiers, C. (2018). Stakeholder requirements for sustainability reporting. In C. De Villiers, and W. Maroun (Eds.), Sustainability accounting and integrated reporting. Routledge.

- De Villiers, C., & Hsiao, P. (2018). Integrated reporting. In C. De Villiers, and W. Maroun (Eds.), Sustainability accounting and integrated reporting. Routledge.

- De Villiers, C., Hsiao, P., & Maroun, W. (2017). Developing a conceptual model of influences around integrated reporting: New insights and directions for future research. Meditari Accountancy Research, 25(4), 450–460. https://doi.org/10.1108/MEDAR-07-2017-0183

- De Villiers, C., Rinaldi, L., & Unerman, J. (2014). Integrated reporting: Insights, gaps and an agenda for future research. Accounting, Auditing & Accountability Journal, 27(7), 1042–1067. https://doi.org/10.1108/AAAJ-06-2014-1736

- Deegan, C. (2014). Financial accounting theory (4th ed.). McGraw-Hill Education.

- Dorin, I., Rosca, I., Costea, D., & Suciu, C. (2020). Integrated reporting for public sector in EU: A case study. Academic Journal of Economic Studies, 6(1), 121–126.

- Du Toit, E., van Zyl, R., & Schütte, G. (2017). Integrated reporting by South African Companies: A case study. Meditari Accountancy Research, 25(4), 654–674. https://doi.org/10.1108/MEDAR-03-2016-0052

- Elliot, W. B., Fanning, K., & Peecher, M. E. (2020). Do investors value higher financial reporting quality, and can expanded audit reports unlock this value? The Accounting Review, 95(2), 141–165. https://doi.org/10.2308/accr-52508

- Erin, O., & Adegboye, A. (2022). Do corporate attributes impact integrated reporting quality? An empirical evidence. Journal of Financial Reporting and Accounting, 20(3/4), 416–445. https://doi.org/10.1108/JFRA-04-2020-0117

- Erin, O., & Olojede, P. (2024). Do nonfinancial reporting practices matter in SDG disclosure? An exploratory study. Meditari Accountancy Research, https://doi.org/10.1108/MEDAR-06-2023-2054

- Farewell, S., & Pinsker, R. (2015). Does assurance on XBRL derived financial statements impact the decisions of nonprofessional investors? Management Accounting Quarterly, 16(3), 13–21.

- Fernando, S., & Lawrence, S. (2014). A theoretical framework for CSR practices: Integrating legitimacy theory, stakeholder theory and institutional work. Journal of Theoretical Accounting Research, 10(1), 149–178.

- Gal, G., & Akisik, O. (2020). The impact of internal control, external assurance, and integrated reports on market value. Corporate Social Responsibility and Environmental Management, 27(3), 1227–1240. https://doi.org/10.1002/csr.1878

- Goicoechea, E., Gómez-Bezares, F., & Ugarte, J. (2019). Integrated Reporting assurance: Perceptions of auditors and users in Spain. Sustainability, 11(3), 713. https://doi.org/10.3390/su11030713

- Hassan, A., Elamer, A. A., Fletcher, M., & Sobhan, N. (2020). Voluntary assurance of sustainability reporting: Evidence from an emerging economy. Accounting Research Journal, 33(2), 391–410. https://doi.org/10.1108/ARJ-10-2018-0169

- Herbert, S., & Graham, M. (2021). Application of principles from the International “IR” Framework for including sustainability disclosures within South African integrated reports. South African Journal of Accounting Research, 35(1), 42–68. https://doi.org/10.1080/10291954.2020.1778828

- Hoang, H., & Phang, S. (2021). How does combined assurance affect the reliability of integrated reports and investors’ judgement? European Accounting Review, 30(1), 175–195. https://doi.org/10.1080/09638180.2020.1745659

- Hoang, H., & Trotman, K. T. (2021). The effect of CSR assurance and explicit assessment on investor valuation judgements. Auditing, 40(1), 19–33. https://doi.org/10.2308/AJPT-18-092

- Hsiao, P., & Li, D. (2012). What is a good investment measure? Investment Management and Financial Innovations, 9(1), 34–54.

- Hummel, K., Schlick, C., & Fifka, M. (2019). The role of sustainability performance and accounting assurors in sustainability assurance engagements. Journal of Business Ethics, 154(3), 733–757. https://doi.org/10.1007/s10551-016-3410-5

- Institute of Directors in South Africa (IoDSA). (2016). King IV report on corporate governance for South Africa. https://www.iodsa.co.za/page/king_iv_report

- International Federation of Accountants (IFAC). (2017a). Creating value for SMEs through integrated thinking: The benefits of Integrated Reporting. Retrieved August 5, 2019, from https://www.ifac.org/knowledge-gateway/contributing-global-economy/publications/creating-value-smes-through-integrated-thinking

- International Federation of Accountants (IFAC). (2017b). Enhancing organizational reporting: Integrated reporting key (Policy Position Paper #8). International Federation of Accountants. Retrieved August 28, 2020, from https://www.ifac.org/publications-resources/enhancing-organizational-reporting-integrated-reporting-key

- International Integrated Reporting Council (IIRC). (2018). Integrated report: Building momentum. Retrieved October 24, 2020, from https://integratedreporting.org/integratedreport2018/download/pdf/IIRC_INTEGRATED_REPORT_2018.pdf

- International Integrated Reporting Council (IIRC). (2021). International Integrated Reporting Framework. Retrieved May 4, 2021, from https://www.integratedreporting.org/wp-content/uploads/2021/01/InternationalIntegratedReportingFramework.pdf

- Jeriji, M., & Nasfi, A. (2023). The value relevance of mandatory sustainability reporting assurance. South African Journal of Accounting Research, 37(2), 122–138. https://doi.org/10.1080/10291954.2022.2148887

- Jones, M., & Iwasaki, J. (2011). Governance benefits of new assurance reports. International Journal of Disclosure and Governance, 8(1), 4–15. https://doi.org/10.1057/jdg.2010.30

- Jones, T., Harrison, J., & Felps, W. (2018). How applying instrumental stakeholder theory can provide sustainable competitive advantage. Academy of Management Review, 43(3), 371–391. https://doi.org/10.5465/amr.2016.0111

- Jung, B., Lee, W., & Weber, D. P. (2014). Financial reporting quality and labor investment efficiency. Contemporary Accounting Research, 31(4), 1047–1076. https://doi.org/10.1111/1911-3846.12053

- Kengatharan, L., & Ford, J. (2021). Dividend policy and share price volatility: Evidence from listed non-financial firms in Sri Lanka. International Journal of Business and Society, 22(1), 227–239.

- Kilic, M. (2018). Assurance of integrated reports: Evidence from early adopters. Paper Presented at the Third Integrational Trakya Accounting Finance and Auditing Symposium on October 1-4, 2018, Trakya University.

- Kilic, M., Uyar, A., & Kuzey, C. (2020). The impact of institutional ethics and accountability on voluntary assurance for integrated reporting. Journal of Applied Accounting Research, 21(1), 1–18. https://doi.org/10.1108/JAAR-04-2019-0064

- KPMG. (2017). The road ahead: The KPMG survey of corporate responsibility reporting 2017. Retrieved November 7, 2021, from https://assets.kpmg/content/dam/kpmg/xx/pdf/2017/10/kpmg-survey-of-corporate-responsibility-reporting-2017.pdf

- KPMG. (2020). The time has come: The KPMG survey of sustainability reporting 2020. Retrieved November 7, 2021, from https://assets.kpmg/content/dam/kpmg/uk/pdf/2020/12/the-time-has-come-kpmg-survey-of-sustainability-reporting-2020.pdf

- Lin, C. J., Wang, T., & Pan, C. J. (2016). Financial reporting quality and investment decisions for family firms. Asia Pacific Journal of Management, 33(2), 499–532. https://doi.org/10.1007/s10490-015-9438-8

- Malola, A., & Maroun, W. (2019). The measurement and potential drivers of Integrated Report quality: Evidence from a pioneer in Integrated Reporting. South African Journal of Accounting Research, 33(2), 114–144. https://doi.org/10.1080/10291954.2019.1647937

- Maroun, W. (2018). Modifying assurance practices to meet the needs of Integrated Reporting: The case for Interpretive Assurance. Accounting, Auditing & Accountability Journal, 31(2), 400–427. https://doi.org/10.1108/AAAJ-10-2016-2732

- Maroun, W. (2020). A conceptual model for understanding corporate social responsibility assurance practice. Journal of Business Ethics, 161(1), 187–209. https://doi.org/10.1007/s10551-018-3909-z

- Martínez-Ferrero, J., & García-Sánchez, I. (2018). The level of sustainability assurance: The effects of brand reputation and industry specialisation of assurance providers. Journal of Business Ethics, 150(4), 971–990. https://doi.org/10.1007/s10551-016-3159-x

- Michelon, G., Patten, D. M., & Romi, A. M. (2019). Creating legitimacy for sustainability assurance practices: Evidence from sustainability restatements. European Accounting Review, 28(2), 395–422. https://doi.org/10.1080/09638180.2018.1469424

- Miller, K., Fink, L., & Proctor, T. (2017). Current trends and future expectations in external assurance for integrated corporate sustainability reporting. Journal of Legal, Ethical and Regulatory Issues, 20(1), 56–76.

- Miralles-Quiros, M. M., Miralles-Quiros, J. L., & Daza-Inquierdo, J. (2021). The assurance of Sustainability Reports and their impact on stock market prices. Management Letters, 21(1), 47–60.

- Moikwatlhai, K., Yasseen, Y., & Omarjee, I. (2019). ESG reporting and the institutional shareholder base: A quantitative study of listed companies on the JSE. Southern African Journal of Accountability and Auditing Research, 21, 31–46.

- Musah, A., & Aryeetey, M. (2021). Determinants of share price of listed firms in Ghana. Economic Insights – Trends and Challenges, 2021(1), 57–71. https://doi.org/10.51865/EITC.2021.01.06

- Ncanywa, T., Mongale, I. P., & Mphela, M. P. (2017). Determinants of investment activity in South Africa. Journal of Global Business and Technology, 13(2), 49–57.

- Ntim, C. G., & Soobaroyen, T. (2013). Corporate governance and performance in socially responsible corporations: New empirical insights from a Neo-Institutional framework. Corporate Governance, 21(5), 468–494. https://doi.org/10.1111/corg.12026

- Ofoegbu, G. N., Odoemelam, N., & Okafor, R. G. (2018). Corporate board characteristics and environmental disclosure quantity: Evidence from South Africa (integrated reporting) and Nigeria (traditional reporting). Cogent Business & Management, 5(1), 1551510. https://doi.org/10.1080/23311975.2018.1551510

- Panda, B., & Leepsa, N. (2017). Agency theory: Review of theory and evidence on problems and perspectives. Indian Journal of Corporate Governance, 10(1), 74–95. https://doi.org/10.1177/0974686217701467

- Pinsker, R., & Wheeler, P. (2009). The effects of expanded independent assurance on the use of firm-initiated disclosures by investors with limited business knowledge. Journal of Information Systems, 23(1), 25–49. https://doi.org/10.2308/jis.2009.23.1.25

- Prasetya, R. A., & Yulianto, A. (2019). Determinants of investment decisions with growth opportunities as moderating variable. Accounting Analysis Journal, 8(1), 17–23.