Abstract

This study aims to investigate the factors influencing Responsibility Accounting and its impact on the Management Performance of textile and garment enterprises in Vietnam. Utilizing both qualitative and quantitative research methods, the study surveyed employees and managers from the accounting departments of large-scale textile and garment enterprises in Vietnam. The qualitative research involved summarizing the business conditions of these enterprises, developing research models and hypotheses based on a literature review, and gathering comments from managers and accountants on the questionnaire’s quality. The quantitative research involved using SPSS and AMOS tools to measure, analyze, and interpret the relationships between factors in the model. The results of the linear structural model show that factors including management decentralization, managers’ perspective on Responsibility Accounting, accounting staff qualifications, and information technology application qualifications have the same impact on Responsibility Accounting implementation in textile and garment enterprises in Vietnam. This study also proves that Responsibility Accounting has a positive impact on the Management Performance of the companies. At the same time, research also shows that the higher the effectiveness of Responsibility Accounting, the higher the management skills, financial efficiency and the effectiveness of management activities in these businesses. Based on these discoveries, the author suggests recommendations for both the government and businesses to enhance the effectiveness of Responsibility Accounting, thus boosting their Management Performance.

Reviewing Editor:

1. Introduction

Responsibility Accounting (RA) is a basic component of management accounting and a useful management tool for managers to use to evaluate the business performance of enterprises (Nguyen Manh, Citation2021; Weygandt et al., Citation2020). Since it was first mentioned in the US and then spread to the UK, Australia, and Canada, RA has been researched and developed by many scientists and; applied by managers to the operations of businesses (Harrison & van der Laan Smith, Citation2015). Each center is formed based on the characteristics of the management organization structure and management goals of the manager. Managers empower and assign responsibilities to each specific subject in each center. Normally, there are four responsibility centers: cost, revenue, profit, and investment centers (Biswas, Citation2017; Weygandt et al., Citation2020). Each center performs different tasks according to its assigned responsibilities. The dividing the business into centers will help the center head easily propose methods of operating the center; higher-level managers can control, evaluate, and find shortcomings to overcome and promote the advantages of each center. Thus, businesses can assign specific responsibilities to each object and department. This motivates all departments to implement the assigned requirements (Biswas, Citation2017). RA is also considered a system that creates financial or non-financial information about actual activities while also planning responsibility centers within a unit (Bychkova et al., Citation2021). RA promotes the unity of goals between the board of directors and departments, helps the process of controlling and evaluating the performance of each department to be clear and transparent. This contributes to improving business performance (Alshomaly, Citation2013).

Vietnam has about 7.000 textile and garment enterprises (TGE), of which about 30% are large and foreign-invested enterprises. The garment industry is a key industry in Vietnam, providing jobs for nearly 1,8 million workers. Vietnam’s textile and garment sector has largely sustained its trajectory of recovery. In 2022, export turnover reached 44,4 billion USD, an increase of 10% compared to 2021. However, in 2023, the textile and garment industry must face many challenges because of the impact of the global economic situation and inflation problems in key markets, such as the United States and Europe, increasing interest rates and exchange rates. However, textile and garment exports to international markets such as Japan, Australia, Russia, and India have increased. Textile and garment businesses have also opened several new markets in Africa and the Middle East. This contributes to preventing export turnover in the textile and garment industry from falling deeply in the context of a sharp decline in purchasing power. Thanks to the efforts of businesses, exports in 2023 reached approximately 40,3 billion USD, and the target and expectation that the entire industry’s export turnover in 2024 will reach 44 billion USD, an increase of 9,2% compared to 2023 (VITAS- 2023).

To overcome the difficulties and challenges in the economy during this period and achieve the revenue target in 2024, it is necessary to have a management tool that helps managers evaluate management performance (MP) and operational efficiency, thereby finding solutions to improve the efficiency of business departments. Improving RA, improving the operational efficiency of responsibility centers, and dividing responsibilities in management activities to maximize resources are practical solutions in the current period. However, through practical research in manufacturing enterprises in Vietnam, the application of RA still has many limitations and inadequacies. In general, there is no clear decentralization or management authority in evaluating performance, and evaluation criteria have not been developed at all levels of management. The budgeting system of these enterprises is still general; enterprises have not yet established criteria to evaluate the MP of responsibility centers. The evaluation content only stops at basic indicators, such as revenue, profits, and costs, and does not apply non-financial indicators to evaluate the organization’s performance (Le & Thanh, Citation2023). In addition, managers still wonder whether applying RA really brings better MP to businesses and consider the costs and benefits gained when operating this system (Nguyen Manh, Citation2021).

Although several studies have explored on factors influencing the application of RA in Vietnamese businesses, none have specifically focused on the TGE in Vietnam. Additionally, no research has examined the impact of RA on MP in these businesses, nor how RA affects each aspect of MP. To provide companies with a comprehensive understanding and a foundation for enhancing their RA and MP, this study aimed to investigate the factors affecting RA and its impact on the MP of TGE in Vietnam. Utilizing both qualitative and quantitative research methods, the study surveyed 400 accountants and managers from 200 large – scale companies in Vietnam. The research also assessed the impact of RA on various elements of MP, including management skills, financial performance, and the effectiveness of management activities. Given the unique relationships identified, the author offers recommendations for the government and businesses to enhance the effectiveness of RA, thereby improving their MP.

Besides the introduction and conclusion, the article is divided into five sections: Review of Literature, Theoretical Framework and Research Model, Methodology, Research Findings and Discussion.

2. Literature review

2.1. Research on responsibility accounting

RA appeared relatively early with the initial purpose of motivating employees in different departments of the enterprise, from which the accounting system developed towards decentralization to improve control efficiency (Benston, Citation1963; Higgins, Citation1952). RA is a part of management accounting, introduced in management accounting textbooks around the world, mentioning concepts, roles, functions, methods, and implementation tools. (Drury, Citation2013; Edmonds, Citation2017; Macintosh & Quattrone, Citation2010; Warren et al., Citation2020). Viewpoints on RA have changed significantly since the appearance. Initially, RA merely served to evaluate the results of the established centers. Many studies have introduced the application of RA to evaluate performance and control costs (Mahajan & Kulkarni, Citation2019; Tilt, Citation2010). In practice, the current situation of applying RA in various industries has also been explored in healthcare (Malmmose, Citation2019), hospitality (Altintaş, Citation2008), education (Le & Bui, Citation2020), pharmaceutical (Dawood & Hassoon, Citation2023), garment (Fakir et al., Citation2015), automobile manufacturing enterprises (Huyen, Citation2021), and manufacturing enterprises (Akenbor & Nkem, Citation2013), measuring the implementation of basic principles of RA in Jordanian industrial companies listed on the Amman Stock Exchange (Nawaiseh et al., Citation2014). Some studies have focused on the relationship between RA and socio-economic issues, such as transfer pricing (Cools & Slagmulder, Citation2009), profitability (Festus et al., Citation2020) management decentralization (Demski & Sappington, Citation1989), and internal control (Chima et al., Citation2018). Most studies have pointed out the role and importance of RA, the content of RA, and evaluated the level of application of RA in businesses.

2.2. Research on factors affecting responsibility accounting

Factors affecting RA are among the topics that have received considerable attention in the current period. Most research is conducted using quantitative methods, using primary data in one type of business or businesses in one country. Research on factors affecting RA in joint stock commercial banks in Vietnam (Dien et al., Citation2020), public universities in Vietnam (Nguyen, Citation2020), manufacturing enterprises in Vietnam (Le & Thanh, Citation2023), the TGE listed on the stock market in Vietnam (Tung et al., Citation2022), food processing enterprises (Nguyen et al., Citation2019), beverage enterprises (Trang, Citation2019), small and medium enterprises (Thi, Citation2017), and the impact of organizational structure on RA in enterprises (Safa, Citation2012). The main factors proposed and tested in the research model include Enterprise size, characteristics of production and business activities, management decentralization, accountant qualifications, the level of information technology application, perceptions of managers about RA and the costs of operating RA. Most studies have shown the positive impact of these factors on the effectiveness of the RA system. However, the impact levels are different in industries and geographical locations.

2.3. Research on the impact of responsibility accounting on management performance

Research on the relationship between RA and MP has begun to receive attention in recent years, stemming from the need for managers to innovate management methods. Some studies confirm the role of RA in improving MP, such as research on manufacturing enterprises in Anambra State (Okoye, Citation2009), examining and analyzing the impact of the implementation of responsibility and strategic accounting on the performance of organizations in Indonesia (Sari & Amalia, Citation2019), studying the role of responsibility centers in cost control and business decision making (Bugaian & Technical University of Moldova, Citation2022), testing the role of RA in improving the MP of PT Bumnis in West Java enterprises (Roespinoedji, Citation2020), the impact of the departmental reporting system in implementing governance functions, investors, and credit institutions (Zimnicki, Citation2017); the impact of the responsible cost control system at Han Dan Iron and Steel Company, China on costs and profits (Lin & Yu, Citation2002); and the impact of cost allocation to responsibility centers on cost control effectiveness (Ocansey & Enahoro, Citation2012). Most studies have shown the positive impact of RA on the MP of businesses. The main research method is quantitative research based on designing a questionnaire, designing a scale to measure factors, and using technical tools to determine the relationship between factors and, at the same time, based on practical data from a number of specific businesses to illustrate and clarify the relationship. However, no research has explored the influence of RA on each factor that constitutes corporate governance efficiency, to help us see that RA has the strongest impact on financial performance, the effectiveness of management activities, or the skills of leaders.

3. Theoretical basis and research model

3.1. Theoretical basis

3.1.1. Responsibility accounting

Since its inception, RA has been understood as a tool to control costs and evaluate the performance of each individual, determining the responsibilities of the organization’s head (Higgins, Citation1952). Subsequently the RA system was designed for all management level in the unit. RA is closely related to cost accounting, providing cost accounting information to managers and, helping businesses manage costs from the lowest to the highest level (Benston, Citation1963). To do that, it is necessary to build responsibility centers in the enterprise - department or function whose achievements are directly responsible for a specific manager and prepare revenue and cost budgets for each responsibility center. RA also collects, synthesizes, and reports accounting data related to each responsible center to evaluate the achievements of each manager (Macintosh & Quattrone, Citation2010). RA provides information about realized costs and income, controllable and uncontrollable costs, and income to department managers. In addition, the RA provides information about the profits of each department (Festus et al., Citation2020). RA uses a combination of cost accounting, realized income, and performance evaluation methods to measure and evaluate achievements to provide information about the financial situation and performance. Non-financial for managers, thereby controlling production and business activities to achieve the set goals (Chi, Citation2018). From general research and concepts of RA from different perspectives, the content of RA in the current period includes the following basic issues: (1) Identifying responsibility centers; (2) Budgeting; (3) Collecting and processing incurred information; (4) Preparing RA reports; (3) Evaluating performance at responsibility centers (Edmonds, Citation2017; Warren et al., Citation2020). To evaluate the effectiveness of RA in TGE in Vietnam, we used these five components.

Responsibility center, identify the responsibility center

A responsibility center is a department in an enterprise, and the head of each responsibility center is a manager who is fully responsible for the results of the activities taking place there. Managers in each department have the right to make decisions on how to use resources to perform set tasks (Atu et al., Citation2014). Each responsibility center should be controlled by at least one manager (Macintosh & Quattrone, Citation2010). To establish a responsibility center, each part of the organization must be separable and identifiable for operational purposes and have measurable achievements. Each center must have its own operating characteristics, responsibilities, and authority (Bhandari & Kaur, Citation2018). However, to ensure business operations, responsibility centers must have a relationship and combination with each other (Mahajan & Kulkarni, Citation2019; Mahmud et al., Citation2018). The basis for determining the scope of responsibility centers is the organizational structure, operating cycle of each business, and short and long-term goals of the business (Atu et al., Citation2014). Basically, there are four responsibility centers: cost, profit, revenue and investment centers (Mahajan & Kulkarni, Citation2019; Patel, Citation2013; Ritika, Citation2015; Tilt, Citation2010; Zimnicki, Citation2017).

Budgeting

After determining the responsibilities of the centers, for these centers to carry out their assigned tasks, each center must balance its own resources within the scope of decentralization. Balancing resources with assigned goals or tasks constitutes the budget. Estimating must be based on the operating goals of each department, towards the common goals of the entire enterprise (Jones & Thompson, Citation2000). Managers at each responsibility center must be responsible for budgeting. Estimates are the basis for superiors to allocate resources, and are also the basis for subordinates to carry out their tasks to achieve set goals (Huyen, Citation2021; Jones & Thompson, Citation2000; Citation2002; Le & Thanh, Citation2023). Budgeting information at each responsibility center is the basis for controlling, measuring, and evaluating the center’s performance (Huyen, Citation2021; Jones & Thompson, Citation2002). To evaluate budgeting at responsibility centers, it is necessary to consider whether the estimation methods are appropriate, modern, and meet the requirements of managers. Commonly used budgeting methods include net present value, profitability index, internal rate of return, payback period, accounting rate of return accounting (Nurullah & Kengatharan, Citation2015), weighted average cost of capital, and cost of debt (Vonasek, Citation2011).

Collecting and processing incurred information

Performance information provided by RA emphasizes the responsibilities of stakeholders, usually focusing on low-level management such as teams, production workshops, or management departments where the costs are directly incurred. Incurred information shows the responsibilities and results of implementing the goals of the centers, associated with the responsibilities of managers (Hameed, Citation2023; Mahajan & Kulkarni, Citation2019). To obtain the information incurred at responsibility centers, businesses need to apply accounting methods such as document methods, account methods, price calculation methods, balance synthesis, and cost accounting methods tailored to each center (Warren et al., Citation2020, Hameed, Citation2023). The implementation information that needs to be collected and processed includes both financial information (costs, revenue, profits, and investment results) and non-financial information (product and service quality, customer satisfaction level, information related to training and human resource development process, and relationships with investors). To collect this information, responsibility accountants will collect from different related departments in the enterprise, such as production, product quality inspection, and human resources departments (Hameed, Citation2023; Huyen, Citation2021; Le & Thanh, Citation2023).

Responsibility Accounting reporting system

RA reports are an important means of providing information and determining the specific responsibilities of managers in the departments they manage. RA reports are the operating results of each responsibility center according to the enterprise’s management organization chart. This reporting system records goal implementation and compares it to each department’s assigned goals (Warren et al., Citation2020; Zimnicki, Citation2017). The difference between the realized and estimated information will help managers evaluate performance (Hung, Citation2022; Le & Thanh, Citation2023; Zimnicki, Citation2017). RA reports motivate managers to take action to improve results (Hung, Citation2022; Le & Thanh, Citation2023; Zimnicki, Citation2017). To evaluate the quality of RA reports, it is necessary to consider whether the information provided is complete and useful for evaluating the management responsibilities at each center: cost center, center revenue, profit center, and investment center (Huyen, Citation2021; Le & Thanh, Citation2023).

Evaluating performance in responsibility centers

After each period, the RA will determine indicators to evaluate responsibility for the center to find core reasons and support managers in making decisions (Warren et al., Citation2020). To evaluate responsibility centers, an enterprise’s indicator system includes estimated indicators, indicators reflecting the results of task implementation, and criteria for evaluating responsibility centers. This target must be clearly defined as financial or non - financial target (Viet, Citation2018). During this period, RA will assess managers’ accomplishments and responsibilities within responsibility centers by comparing actual and projected outcomes. Evaluation within these centers should be aligned with the tasks delegated by the enterprise to each respective center. The indicator system must be determined by combining the resources, functions, and tasks of each responsibility center so that the evaluation can improve the performance of the responsibility centers (Ibrahim & Tursun, Citation2021). To evaluate investment management responsibility, responsibility centers use main indicators, including actual ROI, RI, EVA, and ROCE, compared with estimates (Drobyazko et al., Citation2019).

3.1.2. Management performance

MP is the level of success of managers for the efforts they spend in implementing set programs and goals (Yuniarsih & Suwatno, Citation2013). MP is also understood as the performance of each member of the organization in management activities, including planning, investigation, coordination, evaluation, monitoring, and decision-making (Lubis & Dan Suzan, Citation2016). MP is also related to the ability of each level of management to build a company and increase its performance in terms of both human resource quality and financial performance (Wulandari & Riharjo, Citation2016).

MP can be measured using many other factors. Managers are primarily responsible for leading subordinates and making decisions so that the entire department works effectively. To do so, they must possess several management skills, including communication, decision-making, leadership, co - ordination with subordinate units, and innovation in management (Gregory, Citation2000). The financial measures of MP include profitability, efficiency, market position, and financial results. Organizations use different accounting tools to evaluate the financial performance of different responsibility centers. Cost centers are evaluated by meeting the established cost standards. Profit centers are measured by income, sales, and cost targets. Investment centers are also evaluated by means of reported income, but usually in terms of the rate of return that can generate investment funds (Garrison, Citation2000, Kaplan & Norton, Citation1996; Neely, Citation2005).

3.2. Research model and hypothesis

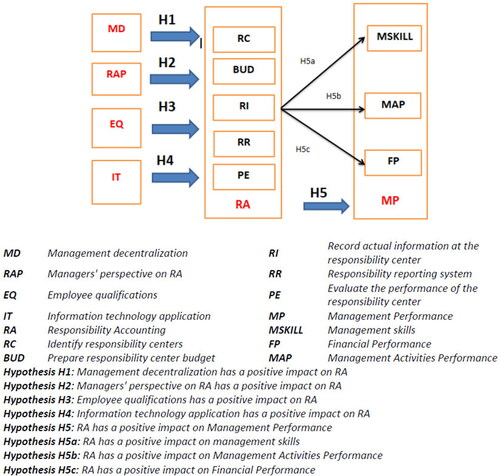

This study relies on contingency theory to develop its hypotheses. Contingency theory is commonly used in management accounting (Abba et al., Citation2018; Otley, Citation2016). Contingency theory underscores the significance of situational elements in shaping business operations. It elucidates the interplay between influential factors and outcomes through an analysis of business behavior and activities. Moreover, it elucidates how particular situational elements, such as the environment, technology, experience, and scale, can impact this relationship. According to this theory, there isn’t a universally optimal method applicable to all business scenarios; rather, processes and structures must align with the specific environment of each business. Ensuring harmony between internal (organizational structure) and external (environmental characteristics) dynamics is crucial for effective operation. Businesses are poised to function more efficiently when equipped with a management framework tailored to the requirements and context of each group and the particular environmental conditions (Lawrence & Lorsch, Citation1967). There is no optimal organizational structure for all businesses; however the specific context of each business must be considered when designing an appropriate organizational structure (Zheng et al., Citation2010). In this study, organizational structure is implemented in the form of an accounting system, specifically an RA system. Therefore, the author believes that there is a relationship between the RA system and the specific business context such as (1) Management decentralization; (2) Staff qualifications; (3) Application of information technology; (4) Managers’ awareness. These factors have been suggested and tested in previous studies and have been tested (Dien et al., Citation2020; Le & Thanh, Citation2023; Nguyen, Citation2020; Tung et al., Citation2022). Some studies also suggest factors such as business size, business operation characteristics (Hung, Citation2022; Thi, Citation2017; Trang, Citation2019). However, the author believes that these are intrinsic factors of the business that are difficult to change in a short time. At the same time, the application of RA in businesses of different sizes and production processes is completely different; therefore, assessing the impact of these essential factors on RA is unnecessary and does not provide policy implications for TGE in Vietnam in general.

3.2.1. The impact of management decentralization on responsibility accounting

Management decentralization includes delegating authority to subordinates to make decisions, allowing lower-level managers to have more autonomy in planning and controlling activities and attaching their responsibilities to the activities of the organization (Meyer & Hammerschmid, Citation2010). Some studies approached management decentralization at the macro level and examined decentralization in national governments. A study of 37 countries from 2000-2009 provides a scale to measure management decentralization, including politics, administration, and economics (Hanson, Citation2022; Morozov, Citation2016). Management decentralization is the basis for identifying responsibility centers, which has a strong impact on management accounting organizations in general, and RA in particular (Kesumawati et al., Citation2019). To achieve this management decentralization must be unified throughout the enterprise to implement enterprise goals (Chia, Citation1995). Management decentralization must clearly indicate the appropriate powers and responsibilities of each department in the enterprise. Management decentralization contributes to improving the feasibility of decisions made at management levels. Management decentralization must be publicly announced in an enterprise (Chen & Eriksson, Citation2019). Most studies showed the same directional impact of management decentralization on RA (Dien et al., Citation2020; Le & Thanh, Citation2023; Nguyen, Citation2020; Tung et al., Citation2022, Ramadan, 2016) with varying levels of impact. Administrators at all levels are given more authority in the enterprise, so they also have more responsibility for planning and controlling related activities. Therefore, managers at all levels must use more management tools, including RA tools. However, there are also studies showing a negative relationship between management decentralization and management accounting work in enterprises, stating that the higher the level of decentralization, the higher the complexity of management accounting implementation (Chia, Citation1995; Williams & Seaman, Citation2001). Based on the above analysis, the author builds Hypothesis H1: Management decentralization has a positive impact on RA at the TGE in Vietnam.

3.2.2. The impact of managers’ perspective on responsibility accounting

Managers’ perspectives include their level of education, understanding, perspective evaluation, and acceptance of an issue they are considering before making a decision. Managers’ perspectives play a decisive role in corporate governance effectiveness (Thompson & Martin, Citation2005). Regarding management accounting, businesses will have better conditions for applying management accounting if managers have a greater understanding of management accounting (Nyakuwanika et al., Citation2012), as the usefulness of RA (Mohammad, 2014; Nguyen, Citation2020; Tung et al., Citation2022). Managers clearly understand the concepts and functions of RA, appreciate the usefulness of RA, are aware of the urgency of applying RA in businesses, and are willing to accept the costs incurred to carry out RA. This helps RA be quickly applied and implemented more effectively (Le & Thanh, Citation2023, Nguyen, Citation2020; Trang, Citation2019). Based on the above analysis, the author builds Hypothesis H2: Managers’ awareness of RA has a positive impact on RA in the TGE in Vietnam and a scale to evaluate its level.

3.2.3. The impact of employee qualifications on responsibility accounting

Accountants are the core forces in implementing and applying RA and effectively exploiting this management tool. If the level of accounting expertise does not meet these requirements, the application of RA in businesses cannot be implemented ineffectively (Ishola et al., Citation2018; Slapničar et al., Citation2014). Employee qualifications are measured by their abilities, skills, and experience in performing work. They are also measured by workers’ coordination with other departments in business and professional ethics. Previous studies have also shown that employee qualifications are related to the application of RA in businesses (Dien et al., Citation2020; Le & Thanh, Citation2023; Nguyen, Citation2020; Nguyen et al., Citation2019; Thi, Citation2017; Trang, Citation2019; Tung et al., Citation2022). The more qualified an accountant, the more positively it will affect the application of RA in businesses. Based on the above analysis, the author builds Hypothesis H3: The qualifications of accounting staff have a positive impact on RA at TGE in Vietnam.

3.2.4. The impact of information technology applications on responsibility accounting

Information technology facilitates data processing on computers, enables data sharing across sources, and expedites the simultaneous handling of large volumes of economic transactions. Consequently, integrating information technology into management and accounting practices is poised to yield favorable outcomes for RA within businesses (Dahal, Citation2019; Taipaleenmäki & Ikäheimo, Citation2013). The level of information technology application is shown through the quality of hardware (computers, links, hard drives); software (accounting, business administration, manufacturing software) has full features and works well (Lim, Citation2013); and a stable and high-speed network and database management system, and the relationship between software, hardware, and network systems is unified (Ghasemi et al., Citation2011). In addition, information technology must be invested, used, and updated regularly (Le & Thanh, Citation2023; Nguyen, Citation2020). Recent research has shown that the application of information technology has a positive impact on the application of management accounting in general and RA in businesses in particular (Le & Thanh, Citation2023; Lim, Citation2013, Ghasemi et al., Citation2011; Nguyen, Citation2020; Talha et al., Citation2022; Trang, Citation2019; Tung et al., Citation2022). Based on the above analysis, the author builds Hypothesis H4: The level of information technology application has a positive impact on RA at TGE in Vietnam.

3.2.5. The impact of responsibility accounting on management performance

Some studies have confirmed the role of RA in improving MP, such as research on manufacturing enterprises in Anambra State, and the results showed that RA helps promote MP and control (Okoye, Citation2009). Another study examined and analyzed the impact of implementing strategies and RA on the performance of organizations in Indonesia, and the results showed a positive impact, suggesting recommendations for businesses. Businesses should focus on RA to improve their competitiveness and contribute to achieving their business goals (Sari & Amalia, Citation2019). Responsibility centers are a tool for decentralizing responsibility through management hierarchies, supporting managers in controlling costs, and making right business decisions (Bugaian & Technical University of Moldova, Citation2022). With the impact of modern information technology and, good human resources, effective RA helps improve the MP of PT Bumnis in West Java enterprises (Roespinoedji, Citation2020). The departmental reporting system created by the RA is an effective management tool for large businesses and corporations with many branches, helping managers obtain complete information about their operations and business activities. The reporting system helps investors and credit institutions to have more reliable sources of information (Zimnicki, Citation2017). The responsible cost control system installed at the Han Dan Iron and Steel Company, China, has significantly reduced production costs and improved profits, making it an effective tool for controlling costs in a changing economic environment (Lin & Yu, Citation2002). In addition, allocating costs to specific responsibility centers helps managers implement better control principles (Ocansey & Enahoro, Citation2012). Most studies have shown the positive impact of RA on the MP of businesses. Based on the above analysis, the author builds Hypothesis H5: RA has a positive impact on MP in TGE in Vietnam. At the same time, to explore the impact of RA on each factor of management effectiveness, including management skills, management activities performance, and financial performance, the author proposes several hypotheses. Hypothesis H5a: RA has a positive impact on the management skills of managers at TGE in Vietnam; Hypothesis H5b: RA has a positive impact on management activities performance at TGE in Vietnam; and Hypothesis H5c: RA has a positive impact on financial performance in Vietnam’s TGE. On theoretical basis, the author proposes a research model with eight hypotheses, as shown in the :

Figure 1. Research model. (Source: Compiled by the author).

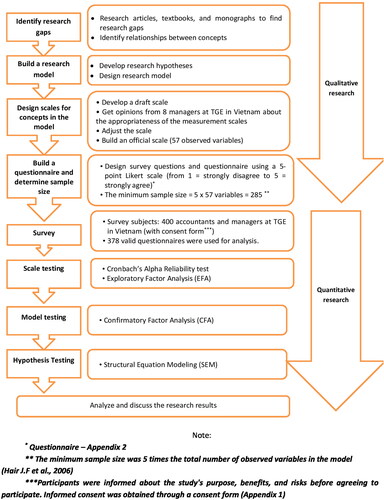

4. Research methodology

The research was conducted in two phases: qualitative research and quantitative research, described in . All procedures performed in this study involving human participants were in accordance with the ethical standards of the institutional and national research committee and with the 1975 Helsinki Declaration and its later amendments in 2013 (World Medical Association, Citation2013).

Figure 2. Research process. (Source: Hair et al., Citation2006; Phi Ho et al., Citation2018; Dang, Citation2024b).

The author has followed best practice in due diligence when human participants are involved. The survey subjects were managers and accountants in the TGE in Vietnam. The participants knew that the research was not dangerous and they were completely voluntary to fulfill the questionnaire (Appendix B). Their consent was obtained by a consent form (Appendix A). The author conceals their personally identifiable data and the research data is used for research purposes only.

Although there was no ethics or institutional committee in the author’s institution which is Hong Duc University at the time the study was conducted; however, before conducting the interview and survey, the authors received a waiver for human research ethics by the Department of Science Technology & International Cooperation, Hong Duc University. The confirmation letter of the waiver stated that the research was not dangerous, low risk and the participants were completely voluntary.

5. Research results

5.1. Qualitative research result

Drawing from the definitions and measurement scales of the factor in prior research and considering the real-world conditions of TGE in Vietnam, the author chose 57 observed variables to form 4 independent factors and 2 independent factor groups in the model. These concepts and measurement scales are detailed in .

Table 1. Measurement scales.

The experts participating in the interviews generally agreed on the number of observed variables for each factor. However, to improve the quality of the questionnaire, the experts all have a common opinion that to answer the survey reliably, the questions must be easy to understand, and in some explanations must be added for difficult and complex questions to avoid misunderstanding the questionnaire content. The author has synthesized the opinions of experts participating in the qualitative research program to complete, supplement and produce results of the set of observed variables used for official quantitative research (Questionnaire – See Appendix)

5.2. Quantitative research result

5.2.1. Cronbach’s alpha reliability test

Each observed variable demonstrates Corrected Item-Total Correlations surpassing 0,3, and all Cronbach’s Alpha coefficients are 0,6 or greater. Consequently, all 57 variables (comprising 18 independent variables and 39 dependent variables) are retained. The results of the scale testing are shown in .

Table 2. Results of the scale testing.

5.2.2. Exploratory factor analysis (EFA)

The principal axis coefficient is employed in conjunction with Promax Rotation, utilizing a Factor Loading criterion of ≥ 0,5 to incorporate the remaining variables into the FEA model for scale validation. The Kaiser-Meyer-Olkin (KMO) coefficient obtained was 0,876, exceeding the threshold of 0,5. Bartlett’s test statistic yielded a value of 27777,067, with a significance level of 0,000, which is below 0,05. Moreover, the Cumulative Variance reached 83,780%, surpassing 50%. These findings affirm the thorough consistency of the analyzed data (Dang, Citation2024a; Phi Ho et al., Citation2018). Consequently, all factor loadings exceed 0,5, and the explained variance exceeds 50%, indicating that the remaining 57 observed variables are grouped as in the original scale ().

Table 3. KMO and Bartlett’s test result.

After conducting the EFA, it is clear that the model aligns with the research framework, with no variables being eliminated from the original set. displays the new factor groups.

Table 4. Exploratory factor analysis matrix.

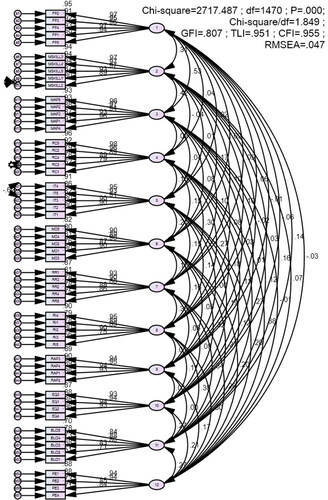

5.2.3. Confirmatory factor analysis (CFA)

Using the findings from the EFA, the research model identified 12 core concepts. Various metrics were employed to evaluate the model’s adequacy, including the Chi-square statistic (CMIN), chi-square adjusted for degrees of freedom (CMIN/df), GFI index, TLI, CFI, and RMSEA index. The model is considered suitable for market data if it satisfies the following criteria: GFI = 0,807 > 0,8, TLI = 0,951 > 0,9, CFI = 0,955 > 0,9 (Baumgartner & Homburg, Citation1996; Doll et al., Citation1994), CMIN/df ≤ 3, and RMSEA = 0,047 ≤ 0,08 (Steiger, Citation1990).

The outcomes of Confirmatory Factor Analysis (CFA) affirmed the suitability of the research model (). The observed variables corresponding to the factors exhibited a significant value of 0,00, suggesting they fully represent the CFA model factor. Furthermore, the statistical measures of normalized weights showed substantial values and statistical significance (P-value = 0,000), validating the attainment of discriminant validity for the concepts (Hoyle, Citation1995).

Figure 3. CFA normalization diagram of research model. Source: Author’s processing data by Amos.

The standardized weights were above 0,5, and the unstandardized weights were significant (sig. < 0,000), indicating that the concepts were convergent. This measurement model is suitable for the research data, with no correlation among the measurement errors, thus achieving unidimensionality. (Hoyle, Citation1995).

5.2.4. Structural equation modeling (SEM)

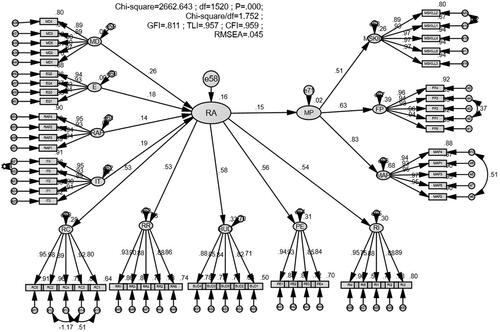

5.2.4.1. Structural equation modeling (SEM 1) for H1, H2, H3, H4, H5

The study used SEM to evaluate the fit of the research model and test the relationships within the initial model. The SEM analysis result of the model with df = 1520, Chi-square = 2662,643 with a p-value = 0,000 < 0,05, Chi-square/df = 1,752 < 3, GFI = 0,811, TLI = 0,957, CFI = 0,959; RMSEA = 0,045 < 0,08 confirms that the model is suitable for market data () (Cheung, Citation2015; Hoyle, Citation1995).

Figure 4. Linear structural model 1 (SEM 1). Source: Author’s processing data by Amos.

The regression coefficient results of the model show that all P-values are below 0,05, leading to the acceptance of all hypotheses H1-5 ().

Table 5. Hypothesis testing result (SEM 1).

5.2.4.2. Structural equation modeling (SEM 2) for H5a, H5b, H5c

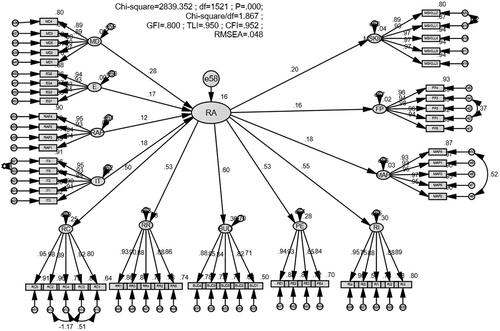

Another test was conducted to examine the relationship between RA and each MP component in businesses. The second SEM analysis result of the model with df = 1521, Chi-square = 2839,352 with a p-value = 0,000 < 0,05, Chi-square/df = 1,867 < 3, GFI = 0,800, TLI = 0,950, CFI = 0,952; RMSEA = 0,048 < 0,08, confirms that the model is suitable for market data ().

Figure 5. Linear structural model 2 (SEM 2). Source: Author’s processing data by Amos.

The model’s regression coefficient outcomes indicate that the P- values are all less than 0,05; Therefore, all hypotheses H1, H2, H3, H4, H5a, H5b, and H5c are accepted ().

Table 6. Hypothesis Testing Result (SEM 2).

6. Discussion

6.1. Findings

This study offers an empirical analysis of the factors influencing the application of RA and its impact on the MP of TGE in Vietnam. Unlike previous research, this study specifically evaluates the effect of RA on each component of MP within the textile and garment industry. Most other studies have either focused on different industries or conducted general research across companies within a country. Nonetheless, the findings of this investigation are consistent with earlier empirical studies.

The research results show that factors including management decentralization, manager awareness, human resource level, and information technology application level all have a positive impact on RA at TGE in Vietnam. Specifically, management decentralization has the strongest impact on RA, with an estimate of 0,262, which is contrary to the research results of Chia (Citation1995) and Williams and Seaman (Citation2001) but similar to most studies (Chen & Eriksson, Citation2019; Chia, Citation1995; Dien et al., Citation2020; Hanson, Citation2022; Kesumawati et al., Citation2019; Le & Thanh, Citation2023; Meyer & Hammerschmid, Citation2010; Morozov, Citation2016; Nguyen, Citation2020; Tung et al., Citation2022, Ramadan, 2016). The next factor is the IT application level, with an estimate of 0.191, consistent with previous findings (Ghasemi et al., Citation2011; Le & Thanh, Citation2023; Lim, Citation2013; Nguyen, Citation2020; Talha et al., Citation2022). The employee qualification factor is as follows with an estimate of 0,177, it also has a positive impact on RA, consistent with previous research (Dien et al., Citation2020; Ishola et al., Citation2018; Le & Thanh, Citation2023; Nguyen, 2019; Citation2020; Slapničar et al., Citation2014; Thi, Citation2017; Trang, Citation2019; Tung et al., Citation2022). The factor that has the least impact on RA is the manager’s perspective of RA, with an estimate of 0,136; although it has been confirmed in previous studies as an extremely important factor in decision-making to use RA (Le & Thanh, Citation2023; Nguyen, Citation2020; Thompson & Martin, Citation2005; Trang, Citation2019; Tung et al., Citation2022). This result is consistent with the actual situation and specific production and business activities of TGE, which are complex production processes, mass production and production according to orders that require proper management decentralization. Most managers in large TGE in Vietnam are clearly aware of the importance of RA and wish to invest in modern management accounting methods to optimize the production efficiency of departments within the company; therefore, managers’ cognitive factors have the least impact on RA.

The research findings also reveal a favorable correlation between RA and MP within Vietnamese TGE. This is validated by the acceptance of H5 in the SEM model, with an estimate of 0,150. Hence, when RA effectiveness increases, MP improves, and vice versa. Despite the modest level of impact, this outcome aligns with prior research findings and mirrors the real circumstances within Vietnamese TGE. (Bugaian & Technical University of Moldova, Citation2022; Okoye, Citation2009; Roespinoedji, Citation2020; Sari & Amalia, Citation2019).

The SEM framework also illustrates how RA influences each factor contributing to effective management within TGE. Specifically, RA has a positive impact on management skills, financial efficiency, and effectiveness of administrative activities. Among them, RA has the greatest impact on management skills with an estimate of 0,204; the next is the effectiveness of administrative activities that managers perform with an estimate of 0,181; finally, financial performance with an estimate of 0,157. However, the impact of RA on these factors was not significantly different. This shows that the more effective the RA, the better the management skills, the higher the financial efficiency, and the better the efficiency of management activities. This result is consistent with previous research (Bugaian & Technical University of Moldova, Citation2022; Ocansey & Enahoro, Citation2012; Roespinoedji, Citation2020; Sari & Amalia, Citation2019; Zimnicki, Citation2017).

6.2. Policy implication

The research results confirm the significant influence of these factors on the effectiveness of the RA system in PGE in Vietnam, and the impact of RA on MP in these units. Management decentralization, information technology application level, human resource level, and managers’ awareness of RA all have a positive impact on RA. This discovery underscores various suggestions for the Vietnamese government. It’s imperative for the government to prioritize establishing legal frameworks that facilitate the adoption of modern management accounting practices within business operations, particularly delving into the realms of financial and management accounting. For TGE in Vietnam, it is necessary to focus on establishing and perfecting the management hierarchy within the company because this is the decisive factor for the success of RA. Enterprises need to establish decentralization towards the goal of development and unity throughout the unit, ensuring the appropriateness of the powers and responsibilities of each department. In addition, businesses need to focus on investing in improving the level of information technology applications, investing in hardware, software, network systems, data management, and regularly investing and developing information technology. Businesses also need to pay attention to human resource training, so that employees in responsibility centers have sufficient knowledge, skills, capacity, responsibility, and ethics to perform assigned tasks. Managers must regularly update their knowledge, become more aware of the importance of RA, promotes decision - making to apply RA, and implement this system well, contributing to improving MP.

Once RA is more effective, the MP is also improved. Therefore, TGE in Vietnam need to implement solutions to improve RA, thereby contributing to improving MP.

To improve identifying responsibility centers: Based on the business’s strategy and vision, short-term and long-term goals; characteristics of the business; managers at TGE in Vietnam need to divide the organizational structure into different responsibility centers. The companies should empower managers in responsibility centers. They must make decisions at the center and are responsible for the results and performance of their center. In the TGE, cost centers can be garment factories; revenue centers can be sales branches, sales offices, stores, representative offices; profit centers can be at the enterprise level or at the branch or factory level; and investment center can be the board of directors.

To improve budgeting: After responsibility centers are established, TGE in Vietnam need to perform budgeting for each center properly. Budgeting must be based on the operating goals of each responsibility center as well as the overall goals of the entire enterprise. For TGE in Vietnam, the system of cost budget is also the basis for evaluating the effectiveness of responsibility centers.

To improve collecting and processing implementation information: Implementation information provided by RA often focuses on lower management levels such as groups, teams, production line or management departments - where costs directly arise. For garment businesses, the main places where costs arise are garment factories, management departments, and sales departments. Businesses need to choose a cost determination method suitable for the process. Some modern cost determination methods suitable for garment businesses are the Activity-Based Costing method and Target costing. The collection and processing of incurred information should be carried out in accordance with the goals of each center and entire company.

To improve RA reporting system: TGE in Vietnam needs to pay attention to perfecting the responsibility reporting system of the centers. Information on the reports must be useful for assessing management responsibilities in terms of costs, revenue, investment and finances of the enterprise. To do that, businesses need to design a responsibility reporting system for each responsibility center.

To improve evaluating performance in responsibility centers: At cost centers, it is necessary to prepare reports on the difference between estimated costs and implemented costs, controllable costs and uncontrollable costs; reports summarizing costs by item, by garment factory, or by department within the enterprise. The reporting system at the revenue center must show the difference between actual and budgeted revenue to evaluate revenue management responsibilities. The reporting system at the profit center must show the difference between actual profit and budgeted profit. The responsibility reporting system at the investment center must show a comparison between actual investment performance indicators and estimates to evaluate investment management responsibility.

7. Conclusion

This study explores the factors affecting RA and the relationship between RA and MP, as well as the factors that constitute MP in the TGE in Vietnam. This study analyzes data from accounting department employees and managers at all levels of a large-scale PGE in Vietnam. The results show a positive relationship between the factors of management decentralization, information technology application level, human resource level, and managers’ awareness of RA and the effectiveness of RA. The research also highlights how RA affects managerial competencies, financial outcomes, and the efficiency of management practices within Vietnam’s TGE, marking a novel contribution compared to prior studies. Furthermore, it offers recommendations for both the government and the TGE in Vietnam to enhance the adoption and efficacy of RA, thereby aiding in the enhancement of MP.

Although this study makes noteworthy theoretical and practical contributions, it has certain limitations. Firstly, this research on TGE in Vietnam tends to focus on the same industry, business sector, and scale. Consequently, this study did not differentiate between large enterprises and medium or small ones. Future research should adopt a broader scope to offer more comprehensive insights. Secondly, the study did not examine the effects of the factors on each component comprising RA within businesses. This could be a suggestion for future research.

Author contribution

Dr. Lan Anh Dang was the sole contributor involved in conceptualization and design, data analysis and interpretation, drafting the manuscript, critically revising it for intellectual content, and granting final approval for publication.

Ethical approval

This study is approved to waive Ethics from the Department of Science Technology & International Cooperation, Hong Duc University, Thanh Hoa, Vietnam.

Acknowledgement

The research presented in this article, was conducted without any external funding, no specific grants or financial support were received or available for this research. I acknowledge the absence of financial contributions while affirming the dedication of my effort to conduct this research independently.

Disclosure statement

The author has no conflicts of interest to disclose. I affirm that the research was conducted in an unbiased and impartial manner, without any financial or personal interests that could influence the research, analysis, or the reporting of its findings

Data availability statement

The data that support the findings of this study are openly available in ‘figshare’ at https://doi.org/10.6084/m9.figshare.25855480.v1 (Dang, Citation2024a). This dataset includes SPSS data, CFA and SEM result – anonymous results.

Additional information

Funding

Notes on contributors

Lan Anh Dang

Lan Anh Dang as the senior lecturer at the Faculty of Economics and Business Administration, Hong Duc University, Thanh Hoa, Vietnam. Her research and teaching interests are in the areas of management accounting, accounting information system, and internal control.

References

- Abba, M., Yahaya, L., & Suleiman, N. (2018). Explored and critique of contingency theory for management accounting research. Journal of Accounting and Financial Management, 4(5), 1.

- Akenbor, C. O., & Nkem, N. J. (2013). The effectiveness of responsibility accounting in evaluating segment performance of manufacturing firms. Journal of Accounting Research and Practices, 2(2), 103–26. https://www.researchgate.net/publication/275658110

- Alshomaly, I. Q. (2013). Performance evaluation and responsibility accounting. Journal of Management Research, 5(1), 291–301. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2461159

- Altintaş, N. N. (2008). Responsibility accounting: A useful management tool for the hotel industry in tourism, hospitality and leisure [Paper presentation]. The 4th world conference for graduate research in tourism, hospitality and leisure, Antalya (pp. 391–398). https://www.researchgate.net/profile/nalan-yakar/publation/280574346_responsibility_accounting_a_useful_management_Tool_the_hotel_Indry/links/5B1D15334585151581F214F41 -For-the-hotel-dustry.pdf

- Atu, O., Endurance, O., Sunny, A. I., & Ozele, C. E, Lecturer – Department Of Accounting Igbinedion University, Okada. Edo State, Nigeria-West Africa. (2014). Responsibility accounting: an overview. IOSR Journal of Business and Management, 16(1), 73–79. http://www.iosrjournals.org/iosr-jbm/papers/Vol16-issue1/Version-4/J016147379.pdf https://doi.org/10.9790/487X-16147379

- Bannink, D., & Ossewaarde, R. (2012). Decentralization: New modes of governance and administrative responsibility. Administration & Society, 44(5), 595–624. https://journals.sagepub.com/doi/10.1177/0095399711419096 https://doi.org/10.1177/0095399711419096

- Baumgartner, H., & Homburg, C. (1996). Applications of Structural Equation Modeling in Marketing and Consumer Research: a review. International Journal of Research in Marketing, 13(2), 139–161. https://doi.org/10.1016/0167-8116(95)00038-0

- Benston, G. J. (1963). The role of the firm’s accounting system for motivation. The Accounting Review, 38(2), 347–354. https://www.jstor.org/stable/242925

- Bhandari, A. S., & Kaur, S. J. (2018). Responsibility accounting: An innovative technique of accounting system. International Journal of Management, Technology And Engineering, 8(12), 6193–6200. https://ijamtes.org/gallery/705.%20dec%20ijmte%20-cw.pdf

- Biswas, T. (2017). Responsibility accounting: A review of related literature. International Journal of Multidisciplinary Research and Development, 4(8), 202–206. https://www.researchgate.net/profile/Tanmay-Biswas/publication/339302404_Responsibility_accounting_A_review_of_related_literature/links/5e4a5f38458515072da4678d/Responsibility-accounting-A-review-of-related-literature.pdf

- Bugaian, L, Technical University of Moldova. (2022). Responsibility center-managerial accounting instrument. Journal of Social Sciences, 5(2), 173–186. https://ibn.idsi.md/sites/default/files/j_nr_file/JSS-2-2022.pdf#page=173 https://doi.org/10.52326/jss.utm.2022.5(2).16

- Bychkova, S. M., Karelskaia, S. N., Abdalova, E. B., & Zhidkova, E. A. (2021). Social responsibility as the dominant driver of the evolution of reporting from financial to non-financial: Theory and methodology. Foods and Raw Materials, 9(1), 135–145. https://naukaru.ru/temp/990229c427ce60cb88ec0850bb22dad8.pdf https://doi.org/10.21603/2308-4057-2021-1-135-145

- Chen, Q., & Eriksson, T. (2019). The mediating role of decentralization between strategy and performance: Evidence from Danish firms. Journal of Organizational Change Management, 32(4), 409–425. https://doi.org/10.1108/JOCM-05-2018-0128

- Cheung, M. W. L. (2015). Meta-analysis: A structural equation modeling approach. John Wiley & Sons.

- Chi, N. T. (2018). Responsibility accounting in businesses [Paper presentation]. International conference on sustainable economic development and business management in the context of globalization, academy of finance.

- Chia, Y. M. (1995). Decentralization, management accounting system (MAS) information characteristics and their interaction effects on managerial performance: a Singapore study. Journal of Business Finance & Accounting, 22(6), 811–830. https://doi.org/10.1111/j.1468-5957.1995.tb00390.x

- Chima, C. C., Obiah, M. E., & Linda, O. N. (2018). Internal control and Responsibility Accounting in corporate governance of Nigerian organizations. Journal of Accounting and Financial Management, 4(8), 32–42. https://www.iiardjournals.org/get/JAFM/VOL.%204%20NO.%208%202018/INTERNAL%20CONTROL.pdf

- Cools, M., & Slagmulder, R. (2009). Tax-compliant transfer pricing and responsibility accounting. Journal of Management Accounting Research, 21(1), 151–178. https://doi.org/10.2308/jmar.2009.21.1.151

- Dahal, R. K. (2019). Changing role of management accounting in 21st Century. Review of Public Administration and Management, 7(3), 1–8. https://doi.org/10.24105/2315-7844.7.264

- Dang, L. A. (2024a). Factors affecting responsibility accounting and its impact on management performance of textile and garment enterprises in vietnam - DATA. figshare. Dataset. https://doi.org/10.6084/m9.figshare.25855480.v1

- Dang, L. A. (2024b). The impact of cost management accounting techniques on supply chain performance using the balanced scorecard approach: A case of logistics companies in Vietnam. Uncertain Supply Chain Management, 12(3), 1493–1510. https://doi.org/10.5267/j.uscm.2024.4.002

- Dawood, Y. A., & Hassoon, L. N. (2023). Evaluating Responsibility Accounting effectiveness under resource consumption accounting method-a case study in the state company for the pharmaceutical industry and medical appliances/Samarra. American Journal of Business Management, Economics and Banking, 18, 81–99.

- Demski, J. S., & Sappington, D. E. (1989). Hierarchical structure and responsibility accounting. Journal of Accounting Research, 27(1), 40–58. https://doi.org/10.2307/2491206

- Dien, N. T., Le Doan Minh Duc, V. H., Thuy, N., & Tien, N. H. (2020). Factors affecting responsibility accounting at joint stock commercial banks in Vietnam. Journal of Southwest Jiaotong University, 55(4), 1-10. https://doi.org/10.35741/issn.0258-2724.55.4.22

- Doll, W. J., Xia, W., & Torkzadeh, G. (1994). A confirmatory factor analysis of the end-user computing satisfaction instrument. MIS Quarterly, 18(4), 453. https://doi.org/10.2307/249524

- Drobyazko, S., Shapovalova, A., Bielova, O., Nazarenko, O., & Yunatskyi, M. (2019). Evaluation of effectiveness of responsibility centers in the management accounting system. Academy of Accounting and Financial Studies Journal, 23(6), 1–6. https://www.abacademies.org/articles/Evaluation-of-Effectiveness-of-Responsibility-Centers-in-the-Management-Accounting-System-1528-2635-23-6-490.pdf

- Drury, C. M. (2013). Management and cost accounting. Springer.

- Edmonds, T. P. (2017). Fundamental management accounting concepts. McGraw-Hill Education. http://librodigital.sangregorio.edu.ec/librosusgp/06450.pdf

- Fakir, A. A., Islam, M. Z., & Miah, M. S. (2015). The use of responsibility accounting in garments industry in Bangladesh. XXXV(2), 1–15. https://doi.org/10.13140/RG.2.1.3430.8568

- Festus, A. F., Ochai-Adejoh, U., & Ayodeji, O. B. (2020). Responsibility accounting and profitability of listed companies in Nigeria. International Journal of Accounting, Finance and Risk Management, 5(2), 101–117. https://doi.org/10.11648/j.ijafrm.20200502.15

- Garrison, R. H. (2000). Management accounting: Concept for planning control and decision-making. Texas Business Publications.

- Ghasemi, M., Shafeiepour, V., Aslani, M., & Barvayeh, E. (2011). The impact of Information Technology (IT) on modern accounting systems. Procedia - Social and Behavioral Sciences, 28, 112–116. https://doi.org/10.1016/j.sbspro.2011.11.023

- Gregory, P. (2000). Managerial performance. http://www.paperinorg/system/file/downloads/student on 1st July, 2009.

- Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E., & Tatham, R. L. (2006). Multivariate data analysis (Vol. 6). Pearson Prentice Hall.

- Hameed, L. A. M. (2023). Accounting based on responsibility centers and their role in reducing costs. World Economics and Finance Bulletin, 27, 113–125. https://scholarexpress.net/index.php/wefb/article/view/3323/2831

- Hanson, A. H. (2022). Decentralization In Planning and the Politicians (pp. 104–126). Routledge.

- Harrison, J. S., & van der Laan Smith, J. (2015). Responsible accounting for stakeholders. Journal of Management Studies, 52(7), 935–960. https://doi.org/10.1111/joms.12141

- Higgins, J. A. (1952). Responsible accounting. The Arthur Andersen Chronicle.

- Hoyle, R. H. (1995). The structural equation modeling approach: Basic concepts and fundamental issues. In: Hoyle, R.H. (Ed.), Structural Equation Modeling: Concepts, Issues, and Applications (pp. 1-15).Thousand Oaks: Sage Publications.

- Hung, P. H. (2022). Influence of factors on responsible accounting organization in enterprises: evidence from Vietnam. Journal of Positive School Psychology, 6(7), 4112–4130. https://www.journalppw.com/index.php/jpsp/article/view/12100

- Huyen, C. T. (2021). Responsibility accounting at automobile manufacturing enterprises in Vietnam [Doctor Thesis].

- Ibrahim, A. K. S. U., & Tursun, M. (2021). Analysis of responsibility centers performance in businesses by system dynamics method. Muhasebe ve Vergi Uygulamaları Dergisi, 14(3), 949–966. https://doi.org/10.29067/muvu.901635

- Ishola, A. A., Adeleye, S. T., & Tanimola, F. A. (2018). Impact of educational, professional qualification and years of experience on accountant job performance. Journal of Accounting and Financial Management ISSN, 4(1), 32–44. https://doi.org/10.5281/zenodo.1210796

- Jones, L. R., & Thompson, F. (2000). Responsible budgeting and accounting. International Public Management Journal, 3(2), 205–227. https://core.ac.uk/download/pdf/36740092.pdf https://doi.org/10.1016/S1096-7494(00)00036-2

- Jones, L. R., & Thompson, F. (2002). Responsible budgeting and accounting reform. Budget Theory in the Public Sector.

- Kaplan, R. S., & Norton, D. P. (1996). The balanced scorecard: Translating strategy into action. Harvard Business School Press.

- Kesumawati, N. K. A., Putri, I. M. A. D., & Dwirandra, A. A. N. B. (2019). The role of business strategies, environmental uncertainty and decentralization as moderating the effect of management accounting systems on managerial performance. International Research Journal of Management, IT and Social Sciences, 6(3), 37–45. https://doi.org/10.21744/irjmis.v6n3.627

- Lawrence, P. R., & Lorsch, J. W. (1967). Differentiation and integration in complex organizations. Administrative Science Quarterly, 12(1), 1–47. https://doi.org/10.2307/2391211

- Le, O. T. T., & Bui, N. T, Department, University of Labour and Social Affairs. (2020). Responsibility Accounting in public universities: A case in Vietnam. The Journal of Asian Finance, Economics and Business, 7(7), 169–178. https://doi.org/10.13106/jafeb.2020.vol7.no7.169

- Le, T. Y. O., & Thanh, H. H. (2023). Factors affecting responsibility accounting: Evidence from Vietnamese manufacturing enterprises. International Journal of Professional Business Review, 8(6), e02188. https://doi.org/10.26668/businessreview/2023.v8i6.2188

- Lim, F. P. C. (2013). Impact of information technology on accounting systems. Asia-Pacific Journal of Multimedia Services Convergent with Art, Humanities, and Sociology, 3(2), 93–106. https://doi.org/10.14257/AJMSCAHS.2013.12.02

- Lin, Z. J., & Yu, Z. (2002). Responsible cost control system in China: a case of management accounting application. Management Accounting Research, 13(4), 447–467. https://doi.org/10.1006/mare.2002.0200

- Lubis, H. F., & Dan Suzan, L. (2016). The Effect of implementing responsibility accounting on managerial performance - case study at PT. North Sumatra plantations. Eproceeding of Management, 3(2), 15–23.

- Macintosh, N. B., & Quattrone, P. (2010). Management accounting and control systems: An organizational and sociological approach. John Wiley & Sons.

- Mahajan, S., & Kulkarni, M. (2019). Costing techniques and Responsibility Accounting. Nirali Prakhashan.

- Mahmud, I., Anitsal, I., & Meral Anitsal, M. (2018). Revisiting responsibility accounting: What are the relationships among responsibility centers? Global Journal of Accounting & Finance, 2(1) https://www.igbr.org/wp-content/uploads/articles/GJAF_Vol_2_No_1_2018-pgs-84-98.pdf

- Malmmose, M. (2019). Accounting research on health care–Trends and gaps. Financial Accountability & Management, 35(1), 90–114. https://doi.org/10.1111/faam.12183

- Meyer, R. E., & Hammerschmid, G. (2010). The degree of decentralization and individual decision making in central government human resource management: A European comparative perspective. Public Administration, 88(2), 455–478. https://doi.org/10.1111/j.1467-9299.2009.01798.x

- Morozov, B. (2016). Decentralization: Operationalization and measurement model. International Journal of Organization Theory & Behavior, 19(3), 275–307. https://doi.org/10.1108/IJOTB-19-03-2016-B001

- Nawaiseh, M. E., Zeidan, A. R., Falahat, M., & Qtish, A. (2014). An empirical assessment of measuring the extent of implementing Responsibility Accounting rudiments in Jordanian industrial companies listed at Amman stock exchange. Advances in Management and Applied Economics, 4(3), 123. https://www.zuj.edu.jo/wp-content/staff-research/economic/dr.mahmoud-falahat/2.pdf

- Neely, A. D. (2005). The evolution of performance measurement research: developments in the last decade and a research agenda for the next. International Journal of Operations & Production Management, 25(12), 1264–1277. https://doi.org/10.1108/01443570510633648

- Nguyen Manh, T. (2021). The impact of responsible accounting on organizational performance: a case study of pharmaceutical enterprises in Vietnam. The Journal of Asian Finance, Economics and Business, 8(3), 1065–1071. https://doi.org/10.13106/jafeb.2021.vol8.no3.1065

- Nguyen, N., Nguyen, T., & Pham, D. (2019). Factors affecting the Responsibility Accounting in Vietnamese firms: A case study for livestock food processing enterprises. Management Science Letters, 9(9), 1349–1360. https://doi.org/10.5267/j.msl.2019.5.015

- Nguyen, N. T. (2020). Factors affecting responsibility accounting at public universities: evidence from Vietnam. The Journal of Asian Finance, Economics and Business, 7(4), 275–286. https://doi.org/10.13106/jafeb.2020.vol7.no4.275

- Nurullah, M., & Kengatharan, L. (2015). Capital budgeting practices: Evidence from Sri Lanka. Journal of Advances in Management Research, 12(1), 55–82. https://doi.org/10.1108/JAMR-01-2014-0004

- Nyakuwanika, M., Gutu, G. J., Zhou, S., Tagwireyi, F., & Chidoko, C. (2012). An analysis of effective responsibility accounting system strategies in the Zimbabwean Health Sector. Research Journal of Finance and Accounting, 3(8), 86–92. https://www.academia.edu/53251898/An_Analysis_of_Effective_Responsibility_Accounting_System_Strategies_in_the_Zimbabwean_Health_Sector_2003_2011_

- Ocansey, E. O. N. D., & Enahoro, J. A. (2012). Determinant controllability of responsibility accounting in profit planning. Canadian Social Science, 8(6), 91–95. https://doi.org/10.3968/j.css.1923669720120806.7676

- Okoye, E. I. (2009). Improvement of Managerial performance in manufacturing organizations-an application of responsibility accounting. Journal of the Management Sciences, 9(1) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1788827

- Otley, D. (2016). The contingency theory of management accounting and control: 1980–2014. Management Accounting Research, 31, 45–62. https://doi.org/10.1016/j.mar.2016.02.001

- Patel, A. T, Professor, S.D. Arts & B.R. Commerce College, Mansa, Dist. Gandhinagar. (2013). Responsible accounting: A study in theory and practice. Indian Journal of Applied Research, 3(3), 1–2. https://www.worldwidejournals.com/indian-journal-of-applied-research-(IJAR)/ https://doi.org/10.15373/2249555X/APR2013/1

- Phi Ho, D., Van Nhi, V., & Phuoc, T. (2018). Quantitative research in accounting and auditing., Finance Publisher.

- Ritika, R. M. (2015). The role of responsible accounting in organizational structure. International Journal of Science, Technology & Management, 4(1), 185–190. https://www.researchgate.net/publication/338225440_Role_of_Responsibility_Accounting_in_Organization_Structure

- Roespinoedji, R. (2020). The effect of participatory budgeting, managerial competence and utilization of information technology on the implementation of Responsibility Accounting, and its implications on managerial performance (a survey of pt bumnis in west java). PalArch’s Journal of Archeology of Egypt/Egyptology, 17(10), 1378–1393. https://archives.palarch.nl/index.php/jae/article/view/4835

- Safa, M. (2012). Examining the role of responsibility accounting in organizational structure. American Academic & Scholarly Research Journal, 4(5) http://aasrc.org/aasrj/index.php/aasrj/article/view/571

- Sari, I. A., & Amalia, M. M. (2019). The effect of responsibility accounting and strategy implementation on organizational performance. Sustainable Business Accounting and Management Review, 1(1), 9–18. https://doi.org/10.61656/sbamr.v1i1.24

- Slapničar, S., Groff, M. Z., & Štumberger, N. (2014). Does professional accounting qualification matter for the provision of accounting services? In Accounting in central and eastern Europe (pp. 255–277). Emerald Group Publishing Limited.

- Steiger, J. H. (1990). Structural model evaluation and modification: An interval estimation approach. Multivariate Behavioral Research, 25(2), 173–180. https://doi.org/10.1207/s15327906mbr2502_4

- Taipaleenmäki, J., & Ikäheimo, S. (2013). On the convergence of management accounting and financial accounting–the role of information technology in accounting change. International Journal of Accounting Information Systems, 14(4), 321–348. https://doi.org/10.1016/j.accinf.2013.09.003

- Talha, M., Wang, F., Maia, D., & Marra, G. (2022). Impact of information technology on accounting and finance in the digital health sector.Journal of Commercial Biotechnology, 27 (2). https://doi.org/10.5912/jcb1299

- Thi, K. N. N. (2017). Responsible accounting organizations in small and medium enterprises. Scientific Journal of Tan Trao University, 3(5), 84–90.

- Thompson, J. L., & Martin, F. (2005). Strategic management: Awareness, analysis and change. Cengage Learning (formerly Thomson Learning).

- Tilt, C. A. (2010). Corporate responsibility, accounting and accountants (pp. 11–32). Springer.

- Trang, C. T. H. (2019). Factors affecting Responsibility Accounting in enterprises: data from the subsidiary of Saigon beer alcohol beverage Corporation. Journal of Science & Technology, 55, 149–156. https://tapchikhcn.haui.edu.vn/media/30/uffile-upload-no-title30213.pdf

- Tung, T. V., Phat, C. L., Ngoc, N. T. N., Phuong, H. T., & Chien, N. V. (2022). Factor affecting the implementation of Responsibility Accounting on firm performance – Empirical analysis of listed textile firms. Cogent Business & Management, 9(1), 1–32. https://doi.org/10.1080/23311975.2022.2032912

- Viet, L. T. T. (2018). Building a system of indicators to evaluate management responsibility centers in enterprises in the Vietnam Rubber industry [Doctoral thesis]. National Economics University.

- Vonasek, J. (2011). Implementing responsibility center budgeting. Journal of Higher Education Policy and Management, 33(5), 497–508. https://doi.org/10.1080/1360080X.2011.605224

- Warren, C. S., Jones, J. P., & Tayler, W. B. (2020). Financial and managerial accounting. Cengage Learning, Inc.

- Weygandt, J. J., Kimmel, P. D., & Aly, I. M. (2020). Chapter 11. In Managerial accounting: Tools for business decision-making. John Wiley & Sons.

- Williams, J. J., & Seaman, A. E. (2001). Predicting change in accounting management systems: national culture and industry effects. Accounting, Organizations and Society, 26(4-5), 443–460. https://www.academia.edu/31317869/Predicting_change_in_management_accounting_systems_national_culture_and_industry_e_ects https://doi.org/10.1016/S0361-3682(01)00002-2

- World Medical Association. (2013). World medical association declaration of helsinki ethical principles for medical research involving human subjects. JAMA: Journal of the American Medical Association, 310(20), 2191–2194. https://doi.org/10.1001/jama.2013.281053

- Wulandari, D. Edan., & Riharjo, I. B. (2016). The influence of participative budgeting on managerial performance with organizational commitment and leadership style. Journal of Accounting Science and Research, 5(4) https://doi.org/10.31949/jcp.v8i3.2754

- Yuniarsih, T Suwatno. (2013). Human resource management. Alfabeta Zwell.

- Zheng, W., Yang, B., & McLean, G. N. (2010). Linking organizational culture, structure, strategy, and organizational effectiveness: Mediating role of knowledge management. Journal of Business Research, 63(7), 763–771. https://doi.org/10.1016/j.jbusres.2009.06.005

- Zimnicki, T. (2017). Responsible accounting inspiration for segment reporting, Copernican Journal of Finance & Accounting, 5(2), 219–232. https://doi.org/10.12775/CJFA.2016.024

Appendix A.

Consent Form

“Factors affecting responsibility accounting and its impact on management performance of textile and garment enterprises in Vietnam”

I ……………………….(participant name), agree to participate in the research project titled Factors affecting responsibility accounting and its impact on management performance of textile and garment enterprises in Vietnam, conducted by Dr. Anh, Dang who has discussed the research project with me.

I have received this form in plain, easy-to-understand language. I had the opportunity to ask questions about this study and received satisfactory answers from the author. I understand the general purpose, risks, and methods of this study through the author’s discussions. I consent to participate in the research project and the following has been explained to me:

The research may not be of direct benefit to me

My participation is completely voluntary

My right to withdraw from the study at any time without any implications to me

The risks including any possible inconvenience, discomfort or harm as a consequence of my participation in the research project

The steps that have been taken to minimise any possible risks

Public liability insurance arrangements

What I am expected and required to do

Whom I should contact for any complaints with the research or the conduct of the research

I am able to request a copy of the research findings and reports

Security and confidentiality of my personal information.

In addition, I consent to:

Audio-visual recording of any part of or all research activities (if applicable)

Publication of results from this study on the condition that my identity will not be revealed.

Name:

Signature:

Date:

Appendix B.

Questionnaire

My name is Anh, Dang, I am currently conducting a research: “Factors affecting Responsibility Accounting and its impact on Management Performance of textile and garment enterprises in Vietnam”. I’m so grateful to having a support by answering the questions below. Your opinion will help me a lot in assessing factors affecting responsibility accounting and its impact and management performance at your business. The information you provide is only for scientific research purposes, is confidential and is not used for any other purpose.

Thank you very much for your help and cooperation!

A – GENERAL INFORMATION ABOUT PARTICIPANTS AND BUSINESSES

Name of the company: ………………………………………………………… …….

Company’s address: ……………………………………………………………………

Your Full name: ………………………………………………………………………

Your gender □ Male □ Female

Your age □ Under 35 □ From 36 to 50 □ Over 50

Your department:

□ Enterprise management □ Accounting/Finance □ Other.

Your education qualification:

□ Bachelor Degree □ Master Degree □ Other.

B – Assessing factors affecting your company’s Responsibility Accounting (RA) and management performance (MP)

Please answer the question by marking a cross (X) in the box according to the levels: Level 1, Level 2, Level 3, Level 4, Level 5. For each question, mark a single box according to the level that you choose.

Completely disagree

Disagree

Moderately agree

Agree

Completely agree

- The end -