?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The research examines how Environmental, Social, and Governance (ESG) performance influences firm performance in the ASEAN region, focusing on how country regulatory quality and government effectiveness affect this relationship. The study uses a comprehensive dataset and finds that environmental and social performances do not directly impact firm performance significantly. However, governance performance has a notably positive effect on firm performance, highlighting the importance of sound governance practices. The study also identifies that the connections between environmental and social performance and firm performance are notably affected by country regulatory quality and government effectiveness. This suggests that the benefits of environmental and social initiatives on firm performance depend on the regulatory and governance environments in which firms operate. Similarly, the link between governance performance and firm performance is also influenced by these factors. These findings underscore the essential role of supportive regulatory structures and effective government practices in enhancing the positive effects of ESG initiatives on firm performance. Overall, this study enhances our understanding of ESG impacts within the ASEAN context and emphasizes the need to integrate ESG efforts with broader institutional support to achieve optimal firm performance.

1. Introduction

In recent years, there has been a significant transformation in the global business landscape, with a growing emphasis on Environmental, Social, and Governance (ESG) criteria (Chopra et al., Citation2024). This shift is vital for fostering sustainable development and corporate accountability, encouraging enterprises to make informed decisions considering the consequences of their actions on ESG factors (Baratta et al., Citation2023). The diverse economies, dynamic growth trajectories, and mounting sustainability challenges within the Association of Southeast Asian Nations (ASEAN) region present both opportunities and challenges that necessitate a balanced approach to sustainable growth and development (Suriyankietkaew & Nimsai, Citation2021). This study aims to offer theoretical insights and practical implications by investigating the relationship between ESG practices and firm performance in the ASEAN context. The goal is to enhance our understanding of how ESG practices impact firm performance and to identify strategies that encourage businesses to adopt more sustainable practices.

Incorporating ESG factors into business strategies is crucial in today’s landscape, where sustainability has become a focal point of business discussions (Friede et al., Citation2015). Historically, companies often overlooked the importance of ESG aspects, considering them only in the context of philanthropy or ethics. However, there has been a noticeable shift as businesses now recognize the fundamental connection between their ESG efforts and potential financial benefits. While ESG research has gained popularity, it predominantly focuses on single-country analyses, leaving regional analyses relatively neglected despite the global importance of sustainability and ethical practices. This gap in understanding, particularly in emerging markets like ASEAN, may hinder investors’ ability to make informed decisions that account for ESG risks and opportunities in these markets.

This study aims to investigate the relationship between ESG practices and firm performance in ASEAN economies. The research will address two main questions: first, how much ESG practices impact the financial performance of firms in the ASEAN region; second, whether the influence of ESG on firm performance is affected by country-specific factors like government effectiveness and regulatory quality. The goal is to provide insights into the connection between sustainable business practices and economic outcomes in ASEAN, contributing to the broader discussion on corporate sustainability. Additionally, the research aims to offer valuable guidance to policymakers and business leaders who are working to balance economic growth with sustainable development.

The study focuses on understanding the impact of ESG practices on company performance, particularly in the context of ASEAN. While there is a general belief that strong ESG practices lead to better business performance, empirical data is inconclusive, especially in emerging markets. This research aims to address this gap by examining the specific economic landscape of ASEAN, which includes a mix of emerging markets and varying degrees of regulatory maturity. The objective is to gain a better understanding of how ESG practices influence firm performance in this region and to provide guidance for policymakers considering the unique economic characteristics of ASEAN.

This study aims to fill significant research gaps on the effects of ESG practices on firm performance within ASEAN countries. The research will provide an in-depth analysis of the correlation between ESG dimensions and firm performance in the diverse economies of ASEAN. One notable gap is the lack of empirical research on the individual and collective impacts of ESG dimensions on firm performance in ASEAN. Given the diversity of ASEAN economies, it is likely that the effects of ESG practices vary across the region. This study will explore the varying impacts of ESG practices on firm performance in different ASEAN countries. Additionally, sustainability studies have been largely guided by a single theoretical perspective. To address this limitation, this study will adopt multiple theoretical perspectives to examine the complex relationship between ESG performance and firm performance.

This research makes a significant contribution to the existing literature by examining the intricate relationship between ESG practices and firm performance in the ASEAN context. By taking into account the moderating effects of country regulatory quality and government effectiveness, the study provides a comprehensive understanding of how these institutional factors influence the effectiveness of ESG initiatives. It enhances the theoretical framework by establishing a link between ESG performance and institutional quality and provides practical insights for policymakers and corporate leaders in the ASEAN region. The study emphasizes the critical importance of strong regulatory environments and effective governance in maximizing the positive impacts of ESG practices on firm performance, thereby contributing to sustainable development and strengthening economic resilience in the region.

2. Background

The connection between ESG factors and firm performance has attracted significant attention from academia and the corporate world. This topic is becoming increasingly relevant in the ASEAN region as sustainability is seen as crucial for long-term business success. With the diverse economies, development levels, and governance practices in ASEAN, it is an ideal setting to study how ESG factors influence firm performance. This study aims to contribute to existing literature by examining the real effects of ESG considerations on firm performance within ASEAN. Specifically, we will investigate the potential moderating roles of country regulatory quality and government effectiveness. By analyzing these factors, we hope to deepen our understanding of the importance of ESG in ASEAN corporate performance. The findings will provide valuable insights into the relationship between ESG criteria and firm performance, highlighting the moderating impact of regulatory quality and government effectiveness.

The quality of public governance has a significant impact on the relationship between ESG practices and firm performance in ASEAN. Two important aspects of public governance are regulatory quality and government effectiveness. Regulatory quality refers to the government’s ability to create and enforce policies and regulations that promote private sector development while maintaining ethical business practices (Handoyo, Citation2023). The way businesses include ESG issues in their strategies is impacted by this. Better regulatory quality makes it easier for businesses to integrate ESG practices into their models. Government effectiveness, on the other hand, refers to the quality of public services, the competence of the civil service, and its independence from political pressures (Handoyo, Citation2023). Government effectiveness impacts the enforcement of ESG regulations and the protection of stakeholder interests. Greater government effectiveness leads to better enforcement of ESG regulations and enhanced stakeholder protection.

As businesses increasingly recognize the importance of sustainable practices for long-term viability, the quality of public governance becomes a critical factor that can either aid or impede this process. Public governance includes regulatory policies and government services, which significantly impact the integration of sustainability into business models. To understand the link between ESG practices and firm performance in ASEAN, it is essential to assess public governance quality comprehensively. This evaluation helps identify how public governance influences the effectiveness of ESG practices in promoting business sustainability. Insights gained from this relationship can assist policymakers and strategists in developing policies and strategies to enhance public governance in the region, fostering a sustainable business culture. Ultimately, this contributes to a more prosperous and sustainable future.

ASEAN has shown a strong commitment to promoting sustainability through initiatives aimed at enhancing regulatory frameworks and governance mechanisms. Notable examples of these regional efforts include the ASEAN Corporate Governance Scorecard and the ASEAN Green Bond Standards, both of which aim to encourage sustainable finance and investment. These initiatives demonstrate a deep understanding of the crucial role of governance in sustainable development and the integration of ESG criteria into business practices. The ASEAN Corporate Governance Scorecard assesses the corporate governance practices of publicly listed companies, while the ASEAN Green Bond Standards provide guidelines for green bond issuers to ensure compliance with environmental sustainability standards. By promoting good governance practices and encouraging sustainable investments, these initiatives make significant contributions to the region’s sustainable development goals.

The varying levels of regulatory quality and government effectiveness across ASEAN countries provide a unique opportunity to study how these factors influence the relationship between ESG (Environmental, Social, and Governance) practices and firm performance. In countries with effective governance and high regulatory quality, businesses are likely to operate in environments that support ESG initiatives, leading to better performance. On the other hand, in countries with lower regulatory quality and government effectiveness, businesses may face obstacles in adopting ESG practices, which can negatively impact their performance. This highlights the importance of creating an ecosystem that supports ESG practices to promote social and financial sustainability. Therefore, businesses are encouraged to adopt ESG practices and operate in socially responsible and financially viable ways.

In light of the varying levels of development and unique characteristics in ASEAN's public governance, this study aims to provide a comprehensive analysis of the challenges in implementing ESG practices in emerging markets and their impact on sustainable business success. The study will explore the moderating roles of regulatory quality and government effectiveness to gain a thorough understanding of how ESG practices influence businesses in the region with different public governance performances. Ultimately, the goal is to guide businesses in navigating the changing landscape of emerging markets using ESG strategies and addressing specific factors such as government effectiveness and regulatory quality to achieve sustainable success.

3. Theoretical literature review

3.1. Stakeholder theory

Stakeholder theory suggests that an organization’s success depends on how effectively it manages and balances the interests of different stakeholder groups, such as employees, customers, suppliers, communities, and investors (Freeman, Citation1984). An organization can create lasting value that benefits everyone by addressing the needs and desires of all stakeholders. This theory challenges the traditional shareholder-centric model by advocating for a more inclusive approach to value creation and ethical responsibility. It suggests that organizations have a duty to make decisions that benefit not only shareholders but all stakeholders (Goswami & Bhaduri, Citation2023). This inclusive approach is vital for achieving long-term sustainability and success, as stakeholder support and approval are crucial for maintaining operations and fostering growth.

Stakeholders’ perceptions significantly impact a firm’s ESG efforts. Positive perceptions can improve a firm’s reputation, attract and retain customers, and boost investor confidence, all of which are crucial for financial performance and competitive edge (Razak et al., Citation2023). Conversely, negative perceptions can lead to boycotts, divestments, and a damaged reputation, which can have long-term adverse effects on the firm’s success (Razak et al., Citation2023). Stakeholders’ opinions can affect their engagement with the firm, their loyalty, and their advocacy (Bellucci et al., Citation2019). Therefore, companies must actively engage with their stakeholders to comprehend their expectations and principles, allowing them to better customize their ESG strategies.

Companies that prioritize ESG initiatives can achieve significant benefits in overall performance. The link between ESG performance and firm performance is mediated by how the company’s ESG efforts influence stakeholders’ perceptions and behaviors. For customers, a company’s ESG initiatives can result in greater loyalty and satisfaction (Puriwat & Tripopsakul, Citation2023). Customers prefer to associate with firms whose values align with their own, leading to increased sales and a stronger brand. Customers view ESG initiatives as a sign of a company’s commitment to social responsibility and sustainability. For employees, a company’s ESG commitment can positively impact engagement and morale (Koeswayo et al., Citation2024). The belief that a company is making a positive impact on society and the environment can lead to more productive, innovative, and committed employees. This, in turn, can result in higher retention rates and create a more sustainable and efficient workplace. For investors, a company’s performance in the areas of ESG signals its long-term viability and ethical standing (Khandelwal et al., Citation2023). Investors consider a company’s ESG performance as proof of its dedication to sustainability and social responsibility, impacting investment choices and potentially lowering capital expenses

Empirical evidence indicates a positive correlation between ESG adherence and firm performance. Stakeholder theory elucidates this relationship by underscoring the importance of building trust, loyalty, and cooperation among diverse stakeholders (Minoja, Citation2012). Implementing ESG can drive innovation, mitigate risks, enhance operational efficiencies, and ultimately improve firm performance (Narula et al., Citation2023). Stakeholder theory highlights the necessity of addressing all stakeholders’ interests and concerns in today’s global business environment. ESG factors reflect a company’s social responsibility toward these stakeholders, and strong ESG performance can strengthen relationships with them, leading to improved financial performance. Beyond shareholders, businesses are accountable to a wider array of stakeholders, including communities and the environment. By addressing multiple stakeholders’ concerns, companies can garner greater support and achieve better firm performance.

3.2. Institutional theory

Institutional Theory provides a strong basis for studying the influence of ESG on company performance, especially in the ASEAN region. This theory emphasizes how the institutional environment, including regulatory frameworks, cultural norms, and societal expectations, significantly influences the behaviors, strategies, and overall performance of firms (Huang & Sternquist, Citation2007). According to Institutional Theory, organizations conform to external rules and norms in order to gain legitimacy, secure resources, and ensure their survival (David et al., Citation2019). When it comes to ESG, this theory emphasizes that companies are motivated by both internal goals and external pressures to embrace sustainable and socially responsible practices.

Studies on ESG and firm performance, viewed through the lens of Institutional Theory, suggest that firms are influenced by external institutional pressures in addition to internal motivations and market forces (Iatridis & Kesidou, Citation2018). These pressures include formal regulations, standards, and policies, as well as informal norms and stakeholder expectations. High-quality regulation and effective governance are crucial elements of the institutional environment that can either support or hinder the adoption and effectiveness of ESG practices. Firms operating in environments with stringent regulatory frameworks are more likely to engage in ESG activities due to higher compliance requirements and the elevated costs of non-compliance. Furthermore, strong governance mechanisms ensure transparency and accountability, prompting firms to integrate ESG considerations into their strategic planning.

The theoretical literature indicates that in countries with strong regulatory frameworks and effective governance, firms are more inclined to adopt comprehensive ESG practices due to stringent compliance requirements and increased accountability (Singhania & Saini, Citation2022). These institutional conditions foster a supportive environment that underscores the importance of ESG initiatives, thereby amplifying their positive effects on firm performance. Effective regulations and governance systems mitigate uncertainties and risks associated with ESG investments (Singhania & Saini, Citation2022), facilitating firms’ resource allocation towards sustainable practices. Additionally, robust institutional frameworks often offer incentives like tax benefits, subsidies, or access to green financing, which further motivate firms to pursue ESG goals. Consequently, firms in such environments can achieve better operational efficiencies, improved reputations, and enhanced financial performance through their ESG efforts.

In contrast, firms in countries with weaker regulatory quality and governance may encounter difficulties in effectively implementing ESG practices (Mooneeapen et al., Citation2022), leading to inconsistent impacts on performance. Weak regulatory environments may lack proper enforcement mechanisms, allowing firms to bypass ESG practices without facing substantial penalties (Yee et al., Citation2014). This can create a competitive disadvantage for firms that voluntarily invest in ESG initiatives, as they may incur higher costs without corresponding benefits. Moreover, ineffective governance can lead to issues such as corruption, lack of transparency, and inadequate stakeholder engagement, undermining the potential positive impacts of ESG practices. In these contexts, firms might adopt superficial ESG measures mainly for symbolic purposes rather than to achieve substantive environmental and social outcomes, thus limiting the overall effectiveness of their ESG strategies.

Institutional Theory also introduces the concept of institutional isomorphism. This suggests that firms within the same institutional context tend to adopt similar practices to gain legitimacy and conform to societal expectations (Pal & Ojha, Citation2017). In ASEAN countries, where regulatory and governance structures can vary significantly, this study’s focus on these moderating factors provides valuable insights into how differences in institutional environments influence the relationship between ESG practices and firm performance. Institutional isomorphism can occur through coercive, mimetic, or normative mechanisms. Coercive isomorphism arises from legal and regulatory pressures, mimetic isomorphism results from firms imitating successful peers, and normative isomorphism stems from professional standards and norms (Liu et al., Citation2018). Understanding these mechanisms helps explain why firms in different ASEAN countries may display varying levels of ESG commitment and performance, shaped by their specific institutional contexts.

Institutional Theory provides a comprehensive framework for understanding the important role of external institutional factors in shaping the effectiveness of ESG practices. This study adds to the theoretical literature by examining how regulatory quality and government effectiveness moderate the influence of institutional dimensions on the extent to which ESG practices can enhance firm performance in the ASEAN context. This theoretical perspective underscores the importance of creating supportive institutional environments that encourage and incentivize sustainable business practices. Policymakers and corporate leaders can use these insights to design and implement policies and strategies that promote stronger ESG engagement, ultimately fostering sustainable development and economic growth in the ASEAN region.

4. Literature review and hypothesis development

4.1. Environmental performance and firm performance

Companies that embrace environmentally sustainable practices fulfill their ethical and legal obligations, while also improving their competitiveness and stakeholder relationships. Focusing on environmental sustainability allows firms to enhance their overall performance and reputation, leading to long-term success and profitability (Valentinov, Citation2023). The connection between environmental practices and performance is intricate and multifaceted. Investments in sustainability can initially strain financial resources, and not all stakeholders place equal importance on environmental stewardship (Ye & Dela, Citation2023). Nevertheless, most literature supports that strategically aligning environmental performance with stakeholder expectations can yield numerous benefits. This strategic approach can help companies mitigate risks, drive innovation, and create value, ultimately providing a sustainable competitive edge over their peers (Tan et al., Citation2022). Moreover, environmental performance significantly influences a firm’s speed of adjustment (SOA) to target leverage more so than social and governance performance (Adeneye et al., Citation2023). Therefore, firms should adopt a stakeholder-oriented approach, aligning their strategies with stakeholder demands to achieve positive environmental and financial outcomes. This highlights the necessity of considering stakeholders’ needs when designing and implementing environmental initiatives.

The environmental aspect of ESG relates to how a company affects the natural world. This involves managing waste, reducing carbon footprint, conserving resources, and taking action to address climate change. In recent years, businesses have realized the significance of environmental sustainability because of pressure from stakeholders and the understanding that good environmental management can result in positive financial performance. Several studies have found a positive connection between environmental and financial success. For instance, Hart and Ahuja (Citation1996) and Ramanathan (Citation2018) found that firms with proactive environmental strategies often experience better financial performance, potentially due to waste reduction and increased innovation efficiency. Similarly, research by King and Lenox (Citation2002) and Naseer et al. (Citation2023) suggests that strong environmental performance can enhance competitive advantage and financial outcomes. Good environmental performance can protect against reputational risks, especially in environmentally sensitive industries (Pineiro-Chousa et al., Citation2017). Firms that actively manage and improve their environmental impact can benefit from cost savings, innovation, and new market opportunities (Vasileiou et al., Citation2022). For example, reducing energy consumption can lead to lower operational costs.

On the other hand, poor environmental performance can result in significant reputational and financial damage (Ventouri et al., Citation2023). Companies with poor environmental records may face penalties, fines, and regulatory actions, adversely affecting their financial performance (Matozza et al., Citation2019). Additionally, poor environmental practices can damage a company’s reputation, leading to long-term negative effects on sales, profitability, and share value (Kumar, Citation2018). Companies are increasingly recognizing the importance of sustainable practices in their supply chains. Implementing green supply chains often leads to reduced costs and risks, enhancing financial performance (Zeng et al., Citation2022). Environmentally responsible firms often enjoy higher customer loyalty, translating into better sales and profits (Godefroit-Winkel et al., Citation2022). Research by Sen and Bhattacharya (Citation2001) indicates that corporate social responsibility, including environmental efforts, significantly influences customer reactions. Additionally, investors are increasingly considering ESG factors when making investment decisions (Park & Jang, Citation2021).

Hypothesis 1: Environmental performance is positively associated with firm performance.

4.2. Social performance and firm performance

Using the stakeholder theory framework, firms that effectively engage with their stakeholders and invest in socially responsible initiatives can achieve superior financial performance, enhanced reputation, and a competitive edge (Pedrini & Ferri, Citation2019). This positive relationship is due to the social capital and goodwill generated by ethical and socially responsible practices, which foster stakeholder trust and loyalty, potentially reducing risks and improving operational efficiencies (Ting et al., Citation2019). However, this association is complex, and its impact can depend on factors such as firm size, industry, country, and specific aspects of social performance being measured (Elmghaamez et al., Citation2023)

The body of empirical research on the relationship between social and firm performance reveals a mix of supportive and nuanced findings. Studies like those by Licandro et al. (Citation2024), Kim and Li (Citation2021), and Maqbool and Bakr (Citation2019) generally indicate a positive relationship, suggesting that higher social performance correlates with better financial outcomes, possibly due to enhanced corporate reputation and stakeholder satisfaction. However, the strength and direction of this relationship may vary significantly across different industries and regions. For example, Arian et al. (Citation2023) and Zaiane and Ellouze (Citation2023) found that the positive impact of social performance on firm performance is more noticeable in consumer-facing industries, where consumer perceptions have a direct effect on sales and profitability. Conversely, studies such as Cristina and Rita (Citation2020) and Alshehhi et al. (Citation2018) offer a critical perspective, suggesting that the relationship may show diminishing returns, where the cost of social initiatives eventually outweighs the financial benefits.

The social aspect of ESG concentrates on how a company handles its interactions with employees, suppliers, customers, and the broader community (Becchetti et al., Citation2022). This includes labor standards, health and safety, community development, and customer relations (Boufounou et al., Citation2023). Companies with strong social practices often see benefits like increased employee morale, reduced turnover, and stronger customer loyalty (Chang et al., Citation2021). Positive community relations can also enhance a company’s reputation, potentially driving sales and profitability (Malik, Citation2015). Conversely, poor labor practices can lead to strikes, lawsuits, and reduced productivity (Dahan et al., Citation2023). Ignoring customer and community concerns can damage a brand’s image, leading to lost sales and reduced market share (Werther & Chandler, Citation2005). Socially responsible business practices can lead to better operational efficiency, improved stakeholder relationships, and enhanced reputation, which can, in turn, boost financial outcomes.

Some researchers argue that social responsibility does not always translate into better financial results. McWilliams and Siegel (Citation2000) suggest that firms might engage in socially responsible activities for reasons other than financial returns, such as responding to stakeholder pressure or complying with regulations. Barnett and Salomon (Citation2006) propose a U-shaped relationship, indicating that there might not be significant financial gains at moderate levels of social performance. However, as firms increase their commitment to social performance, they can achieve better financial results by developing superior stakeholder relationships and gaining reputational benefits.

Hypothesis 2: Social performance is positively associated with firm performance.

4.3. Governance performance and firm performance

Corporate governance encompasses a company’s structure and management, including the makeup of the board, executive compensation, and shareholder rights. Effective corporate governance can result in improved decision-making, a decreased risk of scandals, and enhanced trust among shareholders and other stakeholders (de Villiers & Dimes, Citation2021). Firms with strong governance structures often benefit from improved access to capital markets and reduced capital costs (Huo et al., Citation2021). Conversely, poor governance can result in mismanagement, financial irregularities, and a loss of shareholder trust (Velte, Citation2023). Scandals stemming from inadequate governance can harm shareholder value and cause lasting damage to the organization’s reputation.

Stakeholder-oriented governance structures and practices, such as implementing ethical guidelines, stakeholder engagement policies, and transparency measures, can significantly enhance firm performance. These practices build trust, reduce agency costs, and facilitate efficient resource allocation (Dao & Phan, Citation2023). Moreover, diverse and strategically composed boards can better address stakeholder needs and expectations, thereby positively impacting firm performance (Simionescu et al., Citation2021). However, the relationship between governance practices and firm performance is complex and context-dependent, varying across different organizational, cultural, and regulatory environments (Handoyo, Citation2023; Handoyo et al., Citation2023)

Empirical evidence from Alsayegh et al. (Citation2020) supports the notion that firms with higher governance standards make more efficient investment decisions, achieve better operational performance and engage in strategic activities aligned with long-term value creation for stakeholders. However, the literature also notes that the governance-performance relationship varies across different contexts. Factors like firm size, industry sector, and the legal and regulatory environment play mediating roles. For example, Ghabri (Citation2022) suggests that the impact of governance on firm performance is more pronounced in environments with stronger investor protections. Additionally, studies by Baatour and Ben Saada (Citation2022) and Kabir et al. (Citation2023) emphasize the global diversity in governance practices, indicating that cultural and institutional differences significantly influence the effectiveness of governance mechanisms in enhancing firm performance.

Good corporate governance is linked to better financial performance. For instance, Arora and Sharma (Citation2016) and Achim et al. (Citation2015) found that overall corporate performance positively affects firm performance. Specific governance structures, such as board independence, board quality, and shareholder accountability, significantly impact firm performance (Stanwick & Stanwick, Citation2002). Another study found that implementing effective corporate governance improves a company’s financial performance (Affes & Jarboui, Citation2023). Additionally, there is a connection between corporate governance and corporate sustainability performance, leading to improved financial outcomes (Goel, Citation2018). Research by Ntim and Soobaroyen (Citation2013) indicates that better-governed companies tend to pursue more socially responsible agendas through increased CSR practices. Furthermore, a combination of CSR and governance practices has a stronger positive effect on corporate financial performance than CSR alone.

Hypothesis 3: Governance performance is positively associated with firm performance.

4.4. Moderating role of regulation quality

Using an institutional theory framework, this study suggests that the quality of a country’s regulations plays a crucial moderating role, either enhancing or reducing the impact of ESG initiatives on firm performance metrics such as profitability, market value, and sustainability outcomes. For firms operating in countries with stringent regulations and robust enforcement, the positive effects of strong ESG practices on firm performance are more pronounced, highlighting the synergistic relationship between regulatory quality and corporate ESG efforts (Maji & Lohia, Citation2023). Conversely, in countries with less developed or poorly enforced regulatory frameworks, the benefits of ESG engagement to firm performance are often reduced, illustrating the conditional nature of ESG outcomes within different regulatory environments (Rahmaniati & Ekawati, Citation2024).

The empirical literature on the moderating role of regulatory quality in the relationship between ESG performance and firm performance provides a nuanced perspective. Studies by Tang (Citation2023) and Singhania and Saini (Citation2023) have highlighted the significant impact of stringent regulatory frameworks in enhancing the positive effects of ESG practices on firm performance. These studies suggest that in countries with higher regulatory quality, firms engaging in ESG practices tend to show superior financial performance, likely due to the alignment of sustainability practices with regulatory standards and stakeholder expectations. Conversely, in less regulated environments, ESG initiatives may also lead to improved firm performance as these practices can help firms stand out and gain a competitive advantage in markets where stakeholders’ sustainability concerns are not fully addressed by regulations (Tahmid et al., Citation2022).

The influence of ESG factors on firm performance has garnered significant academic and business attention, revealing that companies with strong ESG practices often exhibit better financial and non-financial outcomes (Friede et al., Citation2015). However, the relationship between ESG and firm performance is dynamic and can be influenced by the regulatory framework of the country in which the firm operates. Regulatory quality refers to the government’s ability to implement policies that support the development of private-sector businesses (Kaufmann et al., Citation2011). In countries with high regulatory quality, firms are more likely to adhere to strict ESG standards. This can improve performance, as non-compliance can be costly, and adherence can enhance a company’s reputation (Dhaliwal et al., Citation2011). Conversely, in regions where regulatory quality is low, voluntarily adopting ESG practices can serve as a differentiation strategy, potentially providing a competitive edge (Flammer, Citation2015).

Each ASEAN country has its own set of regulations and legal frameworks for ESG. These country-specific regulations determine the standards for corporate governance, environmental sustainability, and social responsibility, significantly impacting business operations, stakeholder expectations, and firm performance. The level of enforcement of these regulations varies from country to country. In countries with stricter enforcement, there may be a more direct relationship between ESG initiatives and firm performance. This is because these countries require companies to be more transparent and follow best practices. In countries with rigorous regulations and high compliance, ESG can be seen as a measure of corporate excellence, influencing investor perceptions and, consequently, the firm’s valuation (Amran et al., Citation2014). Complying with country-specific regulations can introduce additional costs (Dhaliwal et al., Citation2011). A firm’s ability to offset these costs through increased market appeal or operational efficiency can moderate the relationship between ESG and firm performance (Dhaliwal et al., Citation2011).

Hypothesis 4: The relationship between environmental performance and firm performance is moderated by regulatory quality

Hypothesis 5: The relationship between social performance and firm performance is moderated by regulatory quality

Hypothesis 6: The relationship between governance performance and firm performance is moderated by regulatory quality

4.5. Moderating role of government effectiveness

Literature indicates that in countries with high government effectiveness—characterized by efficient, transparent, and accountable governance—the positive impacts of ESG performance on firm outcomes, such as financial performance, operational efficiency, and competitive advantage, are more significant (Mendiratta et al., Citation2023). Effective government mechanisms enhance the benefits derived from ESG initiatives by ensuring stringent enforcement of environmental regulations, promoting social welfare, and fostering a stable economic environment conducive to sustainable business practices (Bruno & Lagasio, Citation2021). Conversely, in settings where government effectiveness is low, the potential for ESG initiatives to improve firm performance is greatly diminished due to factors such as regulatory unpredictability, lack of enforcement, and political instability (Makhdalena et al., Citation2023)

A study by Zhou et al. (Citation2020) suggests that government effectiveness significantly boosts the positive relationship between ESG practices and firm performance. This enhancement is attributed to effective governments being better at implementing policies that encourage or mandate sustainable practices, thereby creating an environment where ESG initiatives are more likely to be rewarded by the market. Additionally, research by Eliwa et al. (Citation2021) and Wang et al. (Citation2022) supports the view that in countries with high government effectiveness, firms engaging in robust ESG practices benefit from stronger institutional support, better access to capital, and a more favorable public perception, leading to improved financial performance. On the other hand, in environments where government effectiveness is low, the impact of ESG on firm performance is diluted due to weaker policy enforcement, less transparency, and greater uncertainty (Mendiratta et al., Citation2023).

ESG factors encompass a company’s efforts towards environmental protection, social responsibility, and effective governance. These practices align with global sustainability objectives and have been linked to improved financial outcomes. However, their impact on firm performance varies globally, largely due to the differing effectiveness of governance at the national level. Countries with strong governance not only demonstrate efficient and effective public service but also uphold transparency in their policies (Handoyo, Citation2017). These nations create an environment in which ESG practices are integrated into regulatory mandates, ensuring businesses and organizations adhere to ethical and sustainable guidelines (Kaufmann et al., Citation2011).

Governments committed to promoting ESG initiatives often allocate substantial resources to support them, including funding for research and development and strengthening infrastructure. In these regions, consumers, suppliers, and the workforce have higher expectations of corporate responsibility, leading to greater trust, loyalty, and benefits for firms that comply with ESG standards. This creates a virtuous cycle, as companies prioritizing ESG initiatives tend to perform better in the long run, attracting more investment and earning greater recognition as responsible corporate citizens. Empirical research by Deng et al. (Citation2013) implies that the correlation between a company’s adherence to corporate social responsibility (CSR), a crucial component of ESG, and its market value heavily relies on the nation’s institutional infrastructure. While the intrinsic value of ESG is universally acknowledged, its potential as a performance determinant is modulated by the effectiveness of a country’s governance framework. Consequently, companies in nations with robust governance structures are likely to experience a more significant impact on their valuation from their CSR and ESG efforts than those in nations with weaker governance systems.

Hypothesis 7: The relationship between environmental performance and firm performance is moderated by government effectiveness

Hypothesis 8: The relationship between social performance and firm performance is moderated by government effectiveness

Hypothesis 9: The relationship between governance performance and firm performance is moderated by government effectiveness

5. Research design

5.1. Population and sample

The population of this study is all the publicly traded companies in five ASEAN countries, namely Indonesia (IDX), Malaysia (Bursa Malaysia), Philippines (PSE), Singapore (SGX), and Thailand (SET). The study’s focus was on the firms that have disclosed their ESG scores over 10 years (2018–2022) using the Refinitiv Eikon database. Refinitiv Eikon is a comprehensive database and analytics platform widely utilized by professionals in finance, investment, and economics to access real-time and historical financial data, market insights, and analytical tools. It offers a deep and broad range of data across global markets, including ASEAN. We excluded the financial sector due to the types of risks that financial institutions face, including credit risk, market risk, and liquidity risk, which differ from the operational and market risks faced by non-financial companies. These distinct risk profiles necessitate different ESG considerations and strategies, making direct comparisons with non-financial firms potentially misleading. Additionally, we also excluded datasets with outlier negative financial performance to maintain the homogeneity characteristics of the firms under investigation. Especially during the pandemic COVID 19 (2020–2021), the extraordinary conditions affected business organizations and led to financial loss.

provides a detailed and comprehensive overview of the sample selection process used in this study. The data population used for this research encompasses the data of firms listed in the capital stock market of five Southeast Asian countries: Indonesia, Malaysia, Singapore, the Philippines, and Thailand. It is worth noting that only firms with available ESG scores in the Refinitiv database are included in the analysis. Any incomplete data or firms that do not disclose their ESG scores are excluded from the sample selection process.

Table 1. Sample selection.

5.2. Model analysis

The study proposes that firm performance (PERF) is a function of environmental performance (ENVI), social performance (SOC), governance performance (CG), and the control variable, firm size (SIZE). This study utilizes panel data for analysis, which refers to data collected over time from a sample of firms. The model analysis for this study is constructed as Model 1, which takes into account the panel data structure.

Model 1

Model 1

In addition to proposing model analysis as stated in Model 1, the study also proposes model analysis that involves interaction with moderating variables, namely country regulation quality (REQUAL), as presented in Model 2.

Model 2

Model 2

Model analysis that includes interactions with moderating variables of government effectiveness (GOVEC) is formulated in Model 3.

Model 3

Model 3

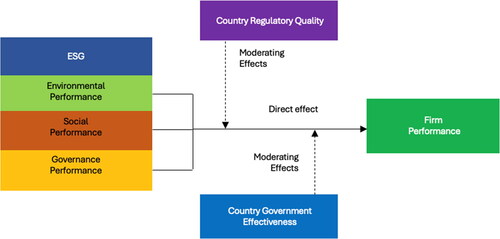

In order to facilitate a better comprehension of the research model, we have incorporated a graphical depiction of the associations among the variables under study. This visual representation is included in , which provides a comprehensive overview of the interrelationships between various variables.

Figure 1. Research model.

5.3. Variable operationalization and measurement

This study aims to explore the relationship between ESG performance and firm performance. The dependent variable in this research is the firm performance (PERF). The study considers three independent variables, namely environmental performance (ENVI), social performance (SOC), and governance performance (CG). Additionally, control variables, namely Firm size (SIZE) and the moderating variables of country regulation quality (REQUAL) and country government effectiveness (GOVEC), are also taken into account. To better understand the included variables and to get a clear picture of the study’s scope, provides detailed descriptions of each variable.

Table 2. Variable operationalization.

6. Results and discussion

6.1. Direct effect analysis

presents the results of the fixed effect regression analysis examining the effect of environmental, social, and governance (ESG) performance on firm performance, with and without fixed effect categorical variables. The dependent variables considered are Net Profit Margin (NPM), Operating Profit Margin (OPM), and Return on Assets (ROA), while the independent variables include Environmental Performance, Social Performance, and Governance Performance. Firm Size is used as a control variable, and categorical variables include country, industry, and year effects.

Table 3. Fixed effect regression analysis.

In the regression model without fixed effect categorical variables, the environmental performance variable shows negative but statistically insignificant coefficients for Net Profit Margin (NPM) (-0.00180, p = 0.489), Operating Profit Margin (OPM) (-0.00075, p = 0.855), and Return on Assets (ROA) (-0.00025, p = 0.110). Similarly, the social performance presents negative coefficients for NPM (-0.00180, p = 0.538) and positive but insignificant coefficients for OPM (0.00706, p = 0.127) and ROA (0.00022, p = 0.200). On the other hand, governance performance shows a positive and statistically significant coefficient for NPM (0.00502, p = 0.015), a negative but marginally significant coefficient for OPM (-0.00553, p = 0.091), and an insignificant effect on ROA (0.00009, p = 0.452). Firm size exhibits positive but statistically insignificant coefficients for NPM (0.02839, p = 0.846), OPM (0.00927, p = 0.968), and ROA (0.01160, p = 0.193).

In the regression model that includes fixed effect categorical variables (country, industry, and year), the environmental performance variable continues to show negative but statistically insignificant coefficients for NPM (-0.00145, p = 0.598) and OPM (-0.00047, p = 0.914), and a positive but insignificant coefficient for ROA (0.00008, p = 0.619). Social performance coefficients remain positive but statistically insignificant for NPM (0.00237, p = 0.443) and OPM (0.00769, p = 0.116), with a minor positive and insignificant effect on ROA (0.00017, p = 0.348). Governance performance continues to exhibit a positive and statistically significant coefficient for NPM (0.00498, p = 0.018), while the negative coefficient for OPM is no longer significant (-0.00502, p = 0.132). The effect on ROA remains insignificant (0.00012, p = 0.326). Firm size coefficients remain statistically insignificant for NPM (0.04631, p = 0.781), OPM (-0.00502, p = 0.722), and ROA (0.00507, p = 0.607).

Overall, reveals that incorporating fixed effect categorical variables (country, industry, and year) slightly enhances the model’s explanatory power, as shown by the higher R-square values. Governance performance consistently has a positive impact on firm performance, especially on Net Profit Margin, which is statistically significant in both models. However, environmental and social performance do not show statistically significant effects on firm performance metrics in either model. Additionally, firm size does not significantly impact any of the performance metrics in the models.

6.2. Moderating effect analysis

6.2.1. Moderating effect of regulatory quality

of the study presents a detailed analysis of the moderating effect of regulatory quality on the relationship between environmental, social, and governance (ESG) factors and firm performance, measured by net profit margin (NPM), operating profit margin (OPM), and return on assets (ROA). The coefficients and p-values provide insights into both the main effects of ESG components and the interaction effects between these components and regulatory quality.

Table 4. Moderating effect of regulatory quality.

The findings regarding the interaction effects present a nuanced picture. For environmental performance, the interaction with regulatory quality is positive but not statistically significant for Net Profit Margin (NPM) (β = 0.00016, p = 0.265) and Operating Profit Margin (OPM) (β = 0.00008, p = 0.733). However, a significant positive interaction effect is noted for Return on Assets (ROA), with a coefficient of β = 0.00002 and a p-value of 0.006. This suggests that higher regulatory quality enhances the positive impact of environmental initiatives on asset efficiency.

Regarding social performance, the interaction effect with regulatory quality shows a positive but statistically insignificant relationship for NPM (β = 0.01242, p = 0.360). For OPM, the interaction is negative and also not statistically significant (β = -0.00041, p = 0.114). For ROA, however, the interaction reveals a significantly negative relationship (β = -0.00002, p = 0.025), indicating that improved regulatory quality may diminish the positive impact of social initiatives on asset efficiency.

The correlation between governance performance and regulatory quality is positive but statistically insignificant for NPM (β = 0.01709, p = 0.141). Conversely, it shows a notable and statistically significant positive influence on OPM (β = 0.00042, p = 0.025) and an insignificant effect on ROA (β = 0.00000, p = 0.398). This suggests that governance practices are particularly effective in improving operating margins in environments with high regulatory quality.

provides a detailed view of the complex relationships between environmental, social, and governance (ESG) factors, regulatory quality, and firm performance within the ASEAN context. The analysis highlights the crucial role of regulatory quality as a moderator, significantly affecting the outcomes of ESG initiatives across various performance metrics. These findings emphasize the importance of considering the regulatory landscape when assessing the effectiveness of ESG practices in enhancing firm performance.

6.2.2. Moderating effect of government effectiveness

shows the moderating effect of government effectiveness on the relationship between environmental, social, and governance (ESG) factors and firm performance in the ASEAN region. Government effectiveness has a positive impact on Net Profit Margin (NPM) (0.02877, p = 0.006), indicating that firms in countries with effective governance structures achieve better net profit margins. The interaction between environmental factors and government effectiveness is positive but not statistically significant (0.00025, p = 0.100). Similarly, the interactions between social factors and government effectiveness (-0.00019, p = 0.241) and governance factors and government effectiveness (-0.00019, p = 0.114) are not significant. This suggests that government effectiveness does not significantly moderate the impact of social and governance factors on NPM.

Table 5. Moderating effect of government effectiveness.

Regarding Operating Profit Margin (OPM), environmental factors have a negative but insignificant effect (-0.00980, p = 0.592). Social factors, however, show a positive and significant impact (0.05461, p = 0.005), suggesting that better social practices are linked to higher operating profit margins. Governance factors have a significant negative effect on OPM (-0.050361, p = 0.001), indicating that implementing governance practices might be costly, thus lowering operating profit margins.

Government effectiveness has a positive but statistically insignificant effect on OPM (0.020149, p = 0.218). The interaction between environmental factors and government effectiveness is not significant (0.000126, p = 0.602). Similarly, the interaction between social factors and government effectiveness is not significant (-0.00062, p = 0.019). However, the interaction between governance factors and government effectiveness is significant and positive (0.00060, p = 0.019), suggesting that the positive impact of governance on OPM is amplified in countries with higher government effectiveness.

For Return on Assets (ROA), environmental factors have a significant negative effect (-0.00209, p = 0.002). Conversely, social factors have a significant positive impact (0.00207, p = 0.005), indicating that better social practices lead to higher returns on assets. Governance factors have a negative effect on ROA, although this effect is not statistically significant (-0.00045, p = 0.407).

Government effectiveness has a positive and significant effect on ROA (0.00171, p = 0.005), highlighting the importance of effective governance for better firm performance. The interaction between environmental factors and government effectiveness is positive and significant (0.00002, p = 0.001), suggesting that the negative impact of environmental factors on ROA is lessened in countries with higher government effectiveness. Conversely, the interaction between social factors and government effectiveness is negative and significant (-0.00002, p = 0.011), indicating that the positive impact of social factors on ROA is slightly reduced in such countries. The interaction between governance factors and government effectiveness is not significant (0.0000, p = 0.341).

Overall, illustrates the complex relationships between ESG factors and firm performance, with government effectiveness playing a significant moderating role in several instances. Effective governance generally enhances the positive impacts of ESG factors on firm performance, particularly for governance and social factors. However, the specific effects vary across different performance metrics, indicating that the influence of ESG factors and government effectiveness is multifaceted and context-dependent.

6.3. Endogeneity test

To determine if the model is endogenous, we must examine the results of the endogeneity test shown in . This table includes data from baseline regressions and instrumental variable (IV) regressions with different endogeneity specifications. The independent variables are environmental performance, social performance, governance performance, and firm size, while the dependent variable is the Net Profit Margin (NPM). The instrumental variables account for the effects of country, industry, and year.

Table 6. Endogeneity test.

In the baseline regression, the coefficient for environmental performance is -0.0014 with a p-value of 0.598, indicating it is not statistically significant. Similarly, in the IV regression, where environmental performance is treated as an endogenous variable, the coefficient is -0.0079 with a p-value of 0.351, also showing no statistical significance. This lack of significance in both the baseline and IV regressions suggests that environmental performance does not significantly impact NPM in this model.

When social performance is treated as an endogenous variable, the baseline regression shows a coefficient of 0.0023 with a p-value of 0.443, indicating no statistical significance. In the IV regression, the coefficient for social performance is 0.0062 with a p-value of 0.341, which is also not statistically significant. This consistency between the baseline and IV regression results suggests that social performance does not significantly influence NPM, and endogeneity might not be a major concern for this variable either.

Governance performance consistently demonstrates a significant impact. In both the standard and IV regressions, the coefficients are statistically significant, with p-values of 0.018, 0.011, and 0.012, indicating a notable positive influence on NPM. This consistency in findings suggests that governance performance has a robust and reliable effect on NPM across various model specifications.

Based on the results in , endogeneity does not appear to be a significant issue for environmental and social performance in these models. The similar results between the baseline and IV regressions imply that the instruments (country effect, industry effect, year effect) effectively control for potential endogeneity. However, the low R-squared values suggest the need for further investigation into other factors that might influence NPM. In conclusion, while governance performance shows a consistent and significant impact on NPM, environmental and social performance do not appear to be substantially endogenous in this context.

6.4. Discussion

6.4.1. The direct effect of environmental performance on firm performance

The common belief is that there is a positive correlation between a company’s environmental performance and its financial performance. The Stakeholder Theory framework suggests that investing in environmental practices can enhance a company’s reputation, meet stakeholder demands, and provide a competitive advantage, ultimately leading to better financial performance. However, the negative relationship observed between environmental performance and financial firm performance could indicate that there are underlying factors, such as the trade-off theory, that are not fully understood. The trade-off theory posits that the costs associated with improving environmental performance may outweigh the financial benefits in the short term (Cordeiro & Sarkis, Citation1997; Deng et al., Citation2016). Therefore, companies should consider the long-term impact of their environmental practices on their financial performance more carefully. The relationship between environmental and financial performance is more complex than previously believed.

Extensive research has examined the relationship between environmental performance and financial outcomes, but the findings are mixed. Some studies suggest that sustainable practices can lead to financial benefits (Kim & Li, Citation2021; Licandro et al., Citation2024). In contrast, others, like this study, indicate that implementing such measures can involve significant costs and investments that may not be offset by revenue increases in the short term, resulting in a negative financial impact (Liu & Wu, Citation2023; Ye & Dela, Citation2023). This implies the necessity for a thorough analysis that considers various factors such as the specific industry sector, geographical location, and strategic orientation (Handoyo et al., Citation2023). Such an analysis is crucial for fully understanding the financial consequences of environmental efforts.

In examining the ASEAN region, it becomes clear that rapid economic growth has led to a surge in industrial activities, not all of which are eco-friendly. Consequently, businesses in the region may view environmentally sustainable practices as potential impediments to their expansion. Switching to cleaner and more sustainable processes often requires significant investment and may result in short-term financial losses.

The study conducted in this specific context provides valuable insights into why environmental performance may negatively impact financial outcomes. The study indicates that various factors, such as regulatory requirements, market dynamics, consumer preferences, and competitive pressures, can all influence this relationship (Iraldo et al., Citation2011). In regions or sectors with strict environmental regulations, complying with these requirements can become a significant financial burden that affects financial performance (Earnhart, Citation2018). Similarly, in markets with minimal demand for environmentally sustainable products, investing in environmental sustainability may not yield the expected financial returns due to a lack of market differentiation (Hunt et al., Citation2004). A study by Orazalin et al. (Citation2024) indicates that firms may adopt sustainability initiatives symbolically to create positive impressions among stakeholders and protect their legitimacy. By understanding these factors, businesses can make well-informed decisions about balancing their environmental and financial goals.

Findings from this study suggest that firms prioritizing environmental performance may experience a slight drop in their immediate financial returns. This could be due to the initial costs of implementing eco-friendly practices, which may not be immediately offset by financial gains. However, in the long run, firms that prioritize environmental performance may enjoy greater financial benefits, such as improved brand reputation, increased customer loyalty, and reduced operating costs. Even though this finding is not consistent with the initial prediction, it aligns with previous studies conducted by Hassel et al. (Citation2005) and Walker and Wan (Citation2012). Elsayed and Paton (Citation2005) also found that environmental performance has a neutral impact on firm performance. This can be attributed to the high upfront investment in implementing environmentally friendly initiatives and technologies. While some environmental initiatives might impose short-term costs on businesses, they could lead to long-term financial benefits by mitigating potential environmental risks and tapping into green market opportunities.

6.4.2. The direct effect of social performance on firm performance

The study found not significant correlation between social performance and financial firm performance, although this was not statistically significant. This result contrasts with the principles of stakeholder theory, which posits that companies can achieve better outcomes by effectively managing relationships with key stakeholders. A firm’s social performance, which reflects its ethical and responsible behavior toward stakeholders, can significantly influence its overall success and financial viability. Building strong relationships with stakeholders can lead to benefits such as increased customer loyalty, improved employee morale and productivity, and better supplier relations (Bridges & Harrison, Citation2003; Koeswayo et al., Citation2024). Although these benefits may not be immediately quantifiable in financial terms, they contribute to the firm’s long-term financial performance. The study’s non-significant finding suggests that while social performance may not yield immediate financial gains, it has the potential for long-term financial benefits by fostering strong stakeholder relationships (Ruf et al., Citation2001)

The findings indicate that social performance does not significantly influence firm performance, which is surprising given that numerous studies, such as those by Eccles et al. (Citation2014) and Shakil et al. (Citation2019), have shown a positive correlation between corporate social responsibility (CSR) and financial performance. One plausible explanation for this finding is that the ASEAN region has unique sociocultural dynamics, making the benefits of social initiatives more intangible and long-term, and thus not immediately reflected in ROA. However, this result is consistent with previous studies by Makni et al. (Citation2009) and Kong et al. (Citation2020). The cultural diversity within ASEAN, including varying ethnicities, religions, and socioeconomic conditions, may affect how well social performance translates into financial performance for firms. Unlike Western contexts, where social responsibility may directly influence firm outcomes, ASEAN companies operate in a more complex environment that requires a nuanced approach to social performance. Therefore, the return on investment (ROI) from social initiatives should be measured not only financially but also by non-financial parameters such as community trust, employee morale, or brand reputation.

Another explanation for the lack of a significant association between social performance and firm performance could be the motivation behind engaging in the social pillars of ESG. Compliance with the social pillars of ESG may be driven by moral motives or external pressures McWilliams and Siegel (Citation2000). In such cases, firms might engage in socially responsible activities due to stakeholder pressure or regulatory compliance rather than purely financial motives. Additionally, Barnett and Salomon (Citation2006) proposed a U-shaped relationship between social performance and financial gains. They suggest that there might be no significant financial gains at moderate levels of social performance, implying that firms could see financial benefits only when they significantly invest in social initiatives. This perspective can help businesses make informed decisions regarding resource allocation toward social performance initiatives.

Empirical studies examining the relationship between social performance and financial outcomes report a wide range of results, highlighting the complexity of measuring the impact of CSR initiatives. The mixed results in the literature are due to differences in methodologies, time frames, and contexts, making it challenging to capture the nuanced effects of social performance on financial outcomes (Oduro et al., Citation2022). The success of a company’s social initiatives heavily depends on its operating environment. Factors such as industry norms, regulatory expectations, and societal values significantly influence how stakeholders perceive a company’s social behavior. These factors shape stakeholder expectations and perceptions, determining the importance they place on a company’s social performance. In contexts where stakeholders highly value social performance, companies are more likely to see significant benefits from their CSR activities. However, in contexts where such expectations are low or where the financial implications of CSR are less direct, the benefits may not be immediately visible in financial metrics.

6.4.3. The direct effect of governance performance on firm performance

Stakeholder theory emphasizes the importance of considering the interests of all stakeholders to achieve organizational success (Freeman, Citation1984). The research findings indicate that ethical and comprehensive governance practices significantly contribute to better financial outcomes. When financial firms prioritize the well-being of a broad range of stakeholders, including employees, customers, suppliers, and the community, they can enhance their reputation, manage risks more effectively, and ultimately achieve superior financial performance. This underscores the critical need for integrating stakeholder considerations into the governance frameworks of financial institutions, aligning with global trends towards corporate social responsibility and ethical business conduct. Prioritizing stakeholder welfare is essential for financial firms to achieve long-term success while fostering a positive societal impact.

These findings align with previous studies by Arora and Sharma (Citation2016) and Achim et al. (Citation2015), which found that companies with robust governance mechanisms generally exhibit higher financial performance. Empirically, this study adds to the growing body of literature examining the impact of governance on firm performance, particularly within financial institutions. By demonstrating a positive and significant relationship, the study reinforces the notion that effective governance is a key driver of financial success. This contribution is vital for both theoretical development and practical application, suggesting areas for further research, such as identifying specific governance practices that are most effective in enhancing firm performance. Moreover, it provides empirical support for the argument that adopting robust governance frameworks can lead to better financial outcomes, offering a concrete basis for firms to prioritize governance reforms as part of their strategic planning processes.

The study’s findings are based on the unique and diverse context of ASEAN, a region that encompasses a wide range of economic, political, and cultural environments. Despite the varying regulatory frameworks and corporate governance models within the region, the study clearly demonstrates the undeniable advantages of effective governance in driving financial firm success. The study’s conclusions have significant implications for policymakers and regulators in ASEAN, who face the challenge of harmonizing governance standards to promote economic integration and enhance the region’s competitiveness. By doing so, ASEAN can unlock its full potential, maximize economic growth, and pave the way for a brighter and more prosperous economic future.

The implications of this study’s findings are significant and far-reaching. From an economic perspective, they highlight the critical importance of good governance in strengthening firm value and contributing to broader economic stability and growth, particularly in the financial sector, where sound governance can act as a safeguard against financial crises. The study also enriches academic discourse on corporate governance, offering fresh insights into governance’s varied impacts, which could inspire further research in this area. There are abundant opportunities for researchers to explore the effects of governance across different industries and regions and to address emerging governance challenges. On the policy front, the study emphasizes the need for policymakers to develop and enforce stringent governance standards. In the ASEAN region, this presents a unique opportunity to adopt and implement governance best practices that can enhance the region’s global economic competitiveness. Policymakers can leverage these insights to push for governance reforms that not only enhance the transparency and accountability of financial firms but also attract more global investors to ASEAN markets.

6.4.4. The moderating effect of regulatory quality

The strength of a country’s regulatory framework significantly impacts the relationship between environmental performance and firm performance. This supports the theory that external environmental factors, such as regulatory frameworks, are crucial in determining the success of organizational strategies. It suggests that the regulatory environment can either enhance or diminish the impact of environmental performance on firm success, highlighting the importance of aligning firm strategies with external conditions. Conversely, the lack of moderating effects on social and governance performance implies that these dimensions might be influenced by a broader set of factors beyond regulatory quality, inviting further investigation into the variables affecting these relationships. Our findings reveal a significant moderating role of regulatory quality in the positive relationship between environmental and firm performance. This aligns with the assertion by Clark et al. (Citation2015), who found that firms with robust ESG practices, especially in stringent regulatory environments, tend to outperform their counterparts in the long run. Effective regulatory environments compel firms to adopt proactive environmental strategies that mitigate risks and create competitive advantages, leading to enhanced financial performance (Porter & van der Linde, Citation1995). This study highlights the strong link between environmental and firm performance, especially when effective regulation is present. This aligns with the global emphasis on sustainability as both a moral and business imperative. Eccles et al. (Citation2014) argued that firms embedding robust sustainability practices, particularly in regions with strong regulatory oversight, often have an edge over their peers regarding long-term value creation. Such regulatory environments are likely to incentivize companies in ASEAN to adopt strategic environmental practices, facilitate risk mitigation, and foster innovative approaches that lead to sustainable growth (Hart, Citation1995).

The study found that country regulatory quality negatively moderates the relationship between social performance and firm performance. Previous studies have highlighted that social performance is multifaceted, and its impact on firms varies based on regional differences (Margolis & Walsh, Citation2003). When considering regulatory quality, the relationship between social and firm performance is complex. Social performance often intertwines with regional sociocultural nuances (Aguilera et al., Citation2007). In the ASEAN context, alignment with broader societal or cultural imperatives may impact financial outcomes more than strict regulations. Social performance, which includes activities like environmental stewardship and fair labor practices, typically aims to enhance a firm’s reputation and financial outcomes. However, in countries with high regulatory quality, stringent regulations, and higher compliance costs can offset the financial benefits of social performance. Firms in these environments may not gain significant additional legitimacy from social performance due to existing pressures to conform to high standards, and resources may be diverted to mandatory compliance rather than discretionary social initiatives. This results in a weaker positive impact of social performance on firm performance.

Regulatory quality denotes the effectiveness of a country’s policies and regulations in supporting private sector development, characterized by clear, transparent, and consistently enforced regulations that create a stable business environment. In countries with high regulatory quality, strong corporate governance practices are more credible and trustworthy due to transparent and enforceable legal frameworks, enhancing investor confidence and leading to increased investment and improved firm performance. High regulatory quality ensures rigorous enforcement of governance standards, reducing agency problems and enhancing decision-making and operational efficiency, contributing positively to firm performance. Firms in countries with high regulatory quality and strong corporate governance are often viewed more favorably by investors and financial institutions, leading to easier access to capital at lower costs, thereby improving financial performance. Additionally, strong corporate governance in a high regulatory quality environment helps mitigate risks associated with corruption, fraud, and mismanagement, protecting firm assets and enhancing reputation and stability. Investors and stakeholders in high regulatory quality environments place significant value on strong corporate governance, leading to more favorable market reactions and boosting stock prices and overall firm valuation.

Findings in this study indicate that the relationship between corporate governance and firm performance is moderated by country regulatory quality. This finding is in line with previous studies such as those by Klapper and Love (Citation2004) and Tan and Chintakananda (Citation2016), which found that firms in countries with strong legal environments exhibit better financial performance due to effective governance practices. Additionally, the benefits of good corporate governance are more pronounced in countries with strong regulatory frameworks. Firms should prioritize robust corporate governance practices in high-regulatory quality countries to leverage these enhanced benefits, integrating strong governance into core strategies to improve financial performance and investor confidence. Policymakers should continue to strengthen regulatory frameworks to ensure consistent enforcement of corporate governance standards, creating a conducive environment for businesses to thrive and enhancing overall economic performance. The moderating effect of country regulatory quality on the relationship between corporate governance and financial performance highlights the significant role that a strong regulatory environment plays in enhancing the benefits of good corporate governance, ensuring that governance practices are credible, reducing risks, and improving access to capital, leading to better financial performance. Understanding this dynamic is crucial for firms aiming to optimize their governance and financial outcomes in various regulatory contexts.

6.4.5. The moderating effect of government effectiveness