?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The International Accounting Standard (IAS) 27 should be used in the preparation of separate financial statements (SFS) for entities with securities traded on regulated markets within the European Union (EU) that adopt International Financial Reporting Standards (IFRS). This research aims to assess the value relevance of SFS. Additionally, it also analyses the value relevance of the interests under IAS 27 reported therein. It uses documental analysis as a technique and researches archival as a method, with entities from the major indices of EU countries as a research sample. Linear regression models are used for data analysis. The findings indicate that both the SFS and those interests influence the entities’ share prices. As far as the authors’ knowledge, this research solves a gap in the literature by assessing the value relevance of interests reported in the SFS and the SFS itself, which have not been reaching the same attention by researchers compared to studies with similar purposes but focusing on the consolidated financial statements. As a contribution, this study can benefit standard-setter bodies and local regulators in understanding the usefulness of SFS for stakeholders’ decision-making by stressing the relevance of those accounts, and the material items reported therein.

IMPACT STATEMENT

The relevance of separate financial statements has already been subject to some investigation, but there is no consensus on those results. This research contributes to the discussion about this, and a significant item reported therein, namely the interests in subsidiaries, associates, and joint ventures. Thus, this research is useful to standard-setter bodies, local regulators, auditors, and local regulators since the findings enable the identification of the relevance of this information, highlighting that the profusion of accounting choices in those accounts may not produce the benefits from the financial information usefulness to investors and other stakeholders.

1. Introduction

As a result of the diversity of accounting systems and in response to the globalization of the economy and markets, international accounting harmonization emerges with the primary objective of contributing to the standardization of practices, transparency and comparability of financial information reported by entities from different jurisdictions (Bhimani, Citation2008; Lopes & Camões, Citation2021; Pathiranage & Jubb, Citation2018). Accordingly, the International Accounting Standards Committee (IASC), firstly, and then the International Accounting Standards Board (IASB) after the restructuring of the former, developed a set of accounting and reporting standards, namely the International Accounting Standards (IAS) and the International Financial Reporting Standards (IFRS), aiming to minimise accounting differences and contribute to improving the quality and comparability of financial information disclosed worldwide (Ashbaugh & Pincus, Citation2001; Cairns et al., Citation2011; Callao et al., Citation2007; O Cualain & Tawiah, Citation2023).

In the European Union (EU) context, Regulation (EC) No 1606/2002 of the European Parliament and of the Council of 19 July 2002 was responsible for the introduction of those standards in this territory, with mandatory and optional requirements to be adopted by the Member States depending on some entities’ specific characteristics and type of accounts. That Regulation thus determined that entities with securities admitted to trading on any regulated market in the EU should mandatorily adopt the IAS and IFRS in their consolidated accounts, as endorsed by the EU (hereinafter only referred to as IAS for simplification purposes), from 2005 onwards. In addition, it established the optional or mandatory use of such standards for those entities when preparing their so-called annual accounts.

The usefulness of financial information can be seen as intrinsically associated with its relevance in influencing the users’ judgments and decision-making of current and potential investors (Badu & Appiah, Citation2018; IFRS Foundation, Citation2018; Imhanzenobe, Citation2022; Kargin, Citation2013; Müller, Citation2011). Furthermore, to provide useful information for users’ decision-making (Al-Refiay et al., Citation2022; Kargin, Citation2013), financial information must be comparable, transparent, understandable, and reliable (Tarca, Citation2020). The current version of the IASB’s framework precisely reinforces this understanding by defining relevance and faithful representation as key qualitative characteristics and comparability and understandability, as well as verifiability and timeliness, as reinforcing qualitative characteristics (IFRS Foundation, Citation2018). As a practical mechanism to measure the relevance of different matters related to entities’ financial and non-financial information, researchers have been using value relevance models (e.g. Alnodel, Citation2018; Badu & Appiah, Citation2018; Busari & Bagudo, Citation2021; Lo, Citation2012; Müller, Citation2011; Sotti, Citation2018).

Despite the IASB’s aim of achieving a global level of comparability, some flexibility still underlies its standards, which have been leading the IASB to the development of projects to improve them, namely by dropping alternative treatments for the same subject (Souza et al., Citation2015). Furthermore, practical expedients have also been used to reduce the level of some complexity requirements, despite some criticisms regarding, for instance, the IASB’s intention to increase its legitimacy by introducing inconsistencies and theoretical flaws that weaken the comparability and relevance of financial statements (Moscariello & Pizzo, Citation2022). This exemplifies the complexity of the standardisation process and the balance to achieve comparability, considering that some authors argue that if, on the one hand, flexibility can lead to opportunistic behaviour, it can also result in more relevant information, as it can be adapted to the specific circumstances and entities’ characteristics (e.g. Souza et al., Citation2015; Tarca Citation2020).

Regardless of those considerations, in what concerns the IAS 27 – Separate Financial Statements (SFS), which is the object of this research, alternative treatments remain. Under IAS 27, interests in subsidiaries, associates and joint ventures can be accounted for by the cost method, by the Equity Method (EM) or even under IFRS 9 – Financial instruments, which results in the possible use of fair value through profit or loss (FVTPL) or fair value through other comprehensive income (FVTOCI). Due to the alternatives available under IAS 27, entities that need to apply them when preparing their separate accounts are faced with the need to make accounting choices, which may result in a lack of comparability and, therefore, of the relevance (usefulness) of those accounts from their users’ perspective when making their decisions.

Thus, this research aims to assess the relevance of SFS in the light of IAS 27, by measuring the value relevance of those accounts, as well as the interests in subsidiaries, associates and joint ventures under that IAS. Therefore, the subject matter of the investigation comprises the SFS for the year 2021 and those interests reported therein. The study sample covers the entities that make up the main capital markets indices of the stock exchanges of EU countries that use IAS when preparing these accounts, whether mandatorily or optionally.

For this purpose, Ohlson’s (Citation1995) value relevance model is used, which assesses the possible influence of entities’ financial and non-financial information on their share prices and is commonly applied in accounting research (Alnodel, Citation2018; Badu & Appiah, Citation2018; Busari & Bagudo, Citation2021; Lo, Citation2012; Müller, Citation2011; Sotti, Citation2018). The findings indicate that both the SFS and the interests in subsidiaries, associates and joint ventures influence the entities’ share price and, consequently, are value-relevant.

The literature on matters related to SFS is substantially lacking, primarily due to the non-mandatory nature of these accounts in some jurisdictions, in contrast to consolidated accounts, which are usually mandatory. In this regard, few studies have been dedicated to assessing the value relevance of SFS, either individually (Lopes & Camões, Citation2021), or in comparison with consolidated accounts (Busari & Bagudo, Citation2021; Müller, Citation2011; Citation2014; Palea, Citation2014; Sotti, Citation2018). Divergent conclusions have, however, been drawn from these studies.

Besides, the SFS seems to be also neglected by IASB concerning the achievement of its objective of providing financial information highly comparable among entities, which is evidenced by the profusion of accounting choices under IAS 27. The use of different accounting methods for the accounting of interests in the SFS can potentially lead to different impacts on the entities’ financial position and performance, and, as previously discussed, possibly affect the relevance of financial information.

Also, and interestingly, the matter of entities’ interests is a relevant audit matter usually highlighted in auditors’ reports, thus assuming itself as a pertinent research topic in this area (Neukirchen & Bonotto, Citation2017; Pereira, Citation2019). Moreover, the relevance of the study is further reinforced by the fact that the interests held by the parent company of groups listed on EU stock exchanges represented 51.5% of the Gross Domestic Product generated in the region in 2018 (The World Bank, Citationn.d.).

Therefore, the financial information reported in the SFS may prove to be further necessary and useful (Busari & Bagudo, Citation2021; Lopes & Camões, Citation2021; Palea, Citation2014; Sotti, Citation2018), justifying the objective underlying this research by its focus on the need of assessing whether the SFS are value-relevant. This is corroborated by the findings of this study on the value-relevance of the SFS and the method for accounting interests in subsidiaries, associates and joint ventures.

Hence, considering the lack of research covering this topic, this research fills important gaps in the literature. Furthermore, no previous research included all listed entities from European Union countries as its sample. Finally, no studies have been found that assess the value relevance of interests under IAS 27, making it another element of innovation proposed for this study.

As likely contributions, this research has the potential to benefit multiple stakeholders by reinforcing the relevance of the presentation of SFS by entities within the scope of IAS 27. Despite some findings from the literature on this topic, standard-setters’ bodies and local regulators have not considered this since there is no consensus or significant research specifically dedicated to this issue. As a result, those entities can potentially benefit from this study, as they can draw attention to accounting choices as an element that mitigates the comparability of relevant financial accounts.

Therefore, by shedding light on the need for more comparable and relevant accounts, auditors and supervisors can be particularly involved in this process, by ensuring that users of financial reporting may have access to more reliable information. Then, by reinforcing the qualitative characteristics of financial information, such as comparability, relevance and faithful representation, investors and other stakeholders of those accounts can have access to a useful piece of financial information for their decision-making process.

This paper is divided into six sections, including this introduction. The background is provided in the next section. In the third section, the literature review and hypotheses are presented. The fourth section deals with the materials and methods, while the fifth presents the empirical results and discussion of them. The sixth section concludes the research with a summary and conclusions.

2. Background on IAS 27 - Separate Financial Statements

This section is divided into two subsections, intending to present the legal framework of the SFS and the accounting options envisaged for interests under IAS 27.

2.1. Legal framework for separate financial statements

The concept of annual accounts is not clearly defined in Regulation (EC) No 1606/2002 of the European Parliament and of the Council of 19 July 2002, nor in Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013. However, it appears to encompass the accounts of most entities, whether they are parent companies (non-consolidated accounts) or not, as established in the national law of an EU Member State.

The SFS, as defined within the IAS 27 and adopted in the EU by Commission Regulation (EC) No. 2023/1803, of 13 August 2023, are prepared as a complement to the consolidated accounts of a parent company with subsidiaries or to the accounts of an investor who, despite not having subsidiaries and thus not preparing consolidated accounts, holds interests in associates or joint ventures for which the EM is applied under IAS 28 - Investments in associates and joint ventures (§6 of IAS 27). Consequently, accounts prepared by entities without subsidiaries, associates, or joint ventures are not considered SFS (§7 of IAS 27).

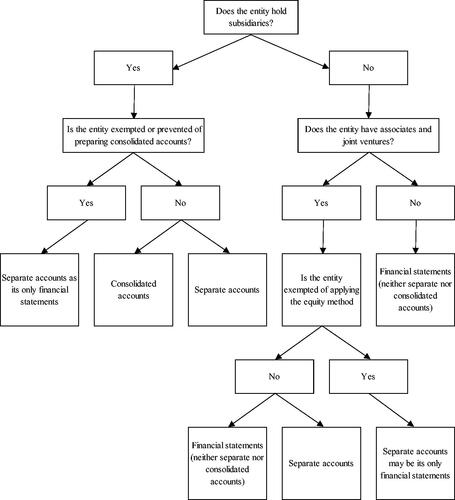

Exceptionally, entities may only present SFS when, despite having subsidiaries, they are exempt or prevented from consolidation per §§4(a) and 31 of IFRS 10 - Consolidated Financial Statements, or are exempted from applying EM, although holding interests on associates or jointly controlled entities, per §17 of IAS 28 (§§8 and 8 A of IAS 27).

illustrates the financial statements applied to several situations, under IAS.

Figure 1. Entities’ financial statements under IAS. Source: Adapted from Santos et al. (Citation2023, p. 54).

shows that entities can present three types of accounts under IAS: consolidated accounts, SFS, and accounts (neither separate nor consolidated accounts). The latter are prepared by entities that do not hold interests in subsidiaries and apply the EM to the interests in associates or joint ventures, and by entities that do not hold none of those interests.

The following subsection provides the accounting options for interests under IAS 27.

2.2. The accounting options provided for in IAS 27

IAS 27 prescribes that when an entity prepares SFS, the interests in subsidiaries, associates, and joint ventures may be accounted for either at cost, using the EM or under IFRS 9 (i.e. at FVTPL or FVTOCI). These accounting options impact differently either on the interests carrying amount, or on the entities’ profit or loss (P&L) and other comprehensive income (OCI).

presents the characteristics of each accounting method, summarizing their potential impacts on the entities’ financial position and performance.

Table 1. Characteristics of the cost method, EM and fair value methods.

Regarding the cost method, there isn’t a specific IFRS relating to this method, as it is not a model covered in IFRS 9, the standard that replaced the IAS 39 which addressed the cost model for interests when fair value was not reliable. Yet, by drawing on parallels with requirements outlined in that standard for financial instruments measurement, and considering its applicability to other assets, it seems plausible to assume that under this model those interests are initially recognised at fair value, usually corresponding to the transaction price (§B5.1.1, IFRS 9), with transaction costs also considered in the cost (§B5.1.1, IFRS 9, a contrario sensu). Additionally, the interests are subject to impairment loss, notwithstanding the IAS 39 did not allow this impairment reversal. Also, dividends are recognised in the entity’s P&L when is established their right to receive it (§12, IAS 27).

Under the EM, the investment is initially recognised at cost. The carrying amount is subsequently adjusted to recognise the changes in the investor’s share in the investee’s net assets (§3, IAS 28). Although IAS 28 doesn’t address transaction costs, they are usually added to the asset (EY, Citation2022; PwC, Citation2020), following the cost model for other assets (a contrario sensu of §B5.1.1, IFRS 9). Goodwill is recognised if the cost exceeds the investor’s share in the investee’s net assets fair value at the acquisition date, as part of the investment carrying amount, being recorded directly in the P&L otherwise (§32, IAS 28). The interest’s carrying amount is subsequently adjusted based on the investor’s share in the investee’s P&L or OCI, affecting the investor’s P&L or OCI, respectively (§§3 and 10, IAS 28). When an entity discontinues the use of the EM, all amounts previously recognised in OCI related to that investment should be accounted for as if the investee had directly disposed of the related assets or liabilities (§§22 and 23, IAS 28). Dividends are recognised as a reduction from the carrying amount of the investment (§12, IAS 27). The latter may also be adjusted through impairment losses (§40, IAS 28) or their reversals (§42, IAS 28). Other adjustments may include harmonisation of accounting policies (§35, IAS 28), adjustments for transactions between the investor and investee (§28, IAS 28), and differences between the reporting dates of their accounts (§34, IAS 28).

Lastly, IAS 27 also allows to account for those investments under IFRS 9, resulting in two possible accounting methods for interests: FVPL or FVOCI. Under FVPL, interests are initially recognised at fair value, with transaction costs recognised in P&L (§5.1.1, IFRS 9). Subsequently, interests are adjusted to reflect fair value changes in the P&L (§5.7.1, IFRS 9). Under FVOCI, interests are also recognised at fair value, but transaction costs are added to the investment (§5.1.1, IFRS 9, a contrario sensu). Also, the interests will be subsequently adjusted for fair value changes, now recognised in the OCI (§B5.7.1, IFRS 9), which are not reclassified to P&L upon derecognition or reclassification of the interest (§B5.7.1, IFRS 9). In both methods based on fair value, the right to receive dividends does not affect the carrying amount of the interest, being recognised directly in P&L (§12, IAS 27), as with the cost model, differing from the EM.

The following section presents the literature review and the hypotheses proposed.

3. Literature review and hypotheses development

The main goal of financial information is to provide useful information for users’ decision-making (Al-Refiay et al., Citation2022; Kargin, Citation2013; Lo, Citation2012). To be useful, the information needs to influence users’ decision-making and faithfully represent the entity’s financial position and performance (IFRS Foundation, Citation2018). According to the IASB (IFRS Foundation, Citation2018), the usefulness of financial information is enhanced by its relevance and reliability. Besides faithful representation, relevance is one of the fundamental qualitative characteristics of financial information, being defined by its capability to influence users’ decisions and have predictive or confirmatory value (IFRS Foundation, Citation2018). Therefore, relevant information reinforces and contributes to the overall quality of the users’ decisions (Albuquerque et al., Citation2023).

The literature traditionally measures the extent to which investors consider accounting information relevant for decision-making as value relevance models (Imhanzenobe, Citation2022). Thereby, the information’s ability to influence users’ decisions (its relevance) is measured by its likely association with the entity’s market value (Albuquerque et al., Citation2023; Barth et al., Citation2000; Imhanzenobe, Citation2022; Kabir, Citation2021; Kargin, Citation2013; Lopes & Camões, Citation2021).

In decision-making, investors often lack a variety of information available both in the capital markets and in the financial information disclosed by entities (Pratiwi et al., Citation2022). The significant relationship between accounting information and market value suggests that financial information significantly influences investor valuations, being reflected in the entities’ share prices (Albuquerque et al., Citation2023; Barth et al., Citation2022; Hossain, Citation2021; Lopes & Camões, Citation2021).

On this matter, Ohlson (Citation1995) developed a flexible model that highlights the value relevance of certain items of financial information, through their relationship with the entities’ market value. This model seeks to identify and assess how financial information influences the market and contributes to identifying elements of accounting information that affect investors’ decisions (Albuquerque et al., Citation2023). It is one of the first models developed in this field and remains widely used in several studies, as it is an easily measurable tool with different applications (Sotti, Citation2018).

Specifically, Ohlson (Citation1995) suggested that accounting information such as earnings per share (EPS) and book value per share (BVPS) influence the entities’ share prices, explaining the possible association between the entities’ market value and diverse information (variables) that can be gathered from financial statements. Thus, EPS and BVPS have been the elements commonly suggested as fundamental variables to explain the value of shares (Bhatia & Mulenga, Citation2019; Khader & Shanak, Citation2023; Vázquez et al., Citation2007), being considered as references in the entity analysis process and decision-making (Srivastava & Muharam, Citation2021). By extending it, however, information from other related sources has also been proposed in this model, including non-financial information (Almujamed & Alfraih, Citation2019), which makes it highly adaptable.

Through the inclusion of those seminal variables (EPS and BVPS), together with additional ones, it is possible to identify the likely relationship between the item(s) under assessment and the entities’ share prices and, consequently, to measure the specific relevance of a given matter. Following this procedures, the value relevance model has given rise to a vast literature in several areas of analysis, such as non-controlling interests (So & Smith, Citation2009a), investment properties (Kadri et al., Citation2020; So & Smith, Citation2009b), intangible assets (Al-Ani & Tawfik, Citation2021; Chalmers et al., Citation2008; Oliveira et al., Citation2010), property, plant and equipment (Diantimala & Sofyani, Citation2020; Sabino, Citation2010), biological assets (Gonçalves et al., Citation2017; Kadri et al., Citation2023), financial assets (Gomes, Citation2009; Zeng et al., Citation2012), cash flows (Albuquerque et al., Citation2023; Burke & Wieland, Citation2017), inventories (Badenhorst & Von Well, Citation2023), and goodwill (AbuGhazaleh et al., Citation2012; Hamberg & Beisland, Citation2014; Xu et al., Citation2011).

More recently, the relevance of non-financial information and sustainability matters has also been the subject of investigations, including their comparative analysis of the relevance of financial information (namely, Amir & Lev, Citation1996; Boodhun & Jugurnath, Citation2023; E-Vahdati et al., Citation2023; Honggowati et al., Citation2015; Jorion & Talmor, Citation2001; Migliavacca, Citation2023; Okechukwu & Jimba, Citation2023).

However, the literature on matters related to SFS is substantially lacking, primarily due to the non-mandatory nature of these accounts in some jurisdictions, in contrast to consolidated accounts, which are usually mandatory. Specifically regarding the relevance of the information in SFS, some studies have addressed this topic, either using these accounts solely (Lopes & Camões, Citation2021) or by comparing with the consolidated accounts relevance (Busari & Bagudo, Citation2021; Goncharov et al., Citation2009; Müller, Citation2011, Citation2014; Palea, Citation2014; Sotti, Citation2018). Nonetheless, the literature presents divergent conclusions. Then, from the studies on this field, despite SFS have been generally considered relevant, they are less relevant than consolidated accounts and have a smaller impact on market information (Busari & Bagudo, Citation2021; Müller, Citation2014; Sotti, Citation2018).

On the other hand, Lopes and Camões (Citation2021) confirmed the relevance of SFS, showing that both the EPS and the BVPS were relevant. Palea (Citation2014) also argues for the relevance of SFS and that they provide useful information for investors, in addition to consolidated accounts. However, this usefulness may be linked to the potential relationship between share prices and expected dividends, as these dividends are often based on SFS in the Italian context. Conversely, other studies concluded that the SFS are not useful for investors and not relevant to assess the entities’ market value (Goncharov et al., Citation2009; Müller, Citation2011).

Despite the divergent conclusions in the literature, SFS are expected to be useful for European entities that present them and, consequently, relevant for several users of financial information, as suggested by most of the literature. Thus, the following hypothesis was formulated:

H1: SFS are value relevant.

This indicates that these interests constitute one of the most relevant assets, being a potential target for analysis by investors in their investment decisions and, consequently, influencing the value of the shares in each period. Thus, the following hypothesis was additionally formulated in this research, based on the value relevance model.

H2: Interests in subsidiaries, associates and joint ventures in the SFS are value-relevant.

The next section presents the material and methods used for this research.

4. Materials and methods

This research is eminently based on a quantitative methodology. It primarily resorted to the method of archival research and the technique of documental analysis.

The main capital markets index of the stock exchanges for all the European Union countries were initially identified, mostly through the investing.com website. Then, the data were mainly extracted from the entities’ SFS included in the sample. The entities’ identification was carried out through the Refinitive Eikon database, with the end of January 2023 as the reference period, based on the market indices they are included. The entities of the FTSE MIB and the MSE are exceptions in this context since the information was obtained from the Amadeus database and the annual report released on that stock exchange, respectively.

Through the entities’ website, SFS for the 2021 period were collected, except for those where the reporting date differs significantly from the calendar year, i.e. where the reporting period covers a greater number of months for the year 2020. In such circumstances, the SFS for 2022 were used, with this figure consisting of six entities. In addition, for the three entities where SFS for the period 2021 were not available at the time of data collection, those for 2020 were exceptionally used.

Further elements necessary information for the study were gathered from financial websites commonly used in other investigations, such as investing.com (Alves et al., Citation2020; D’Orazio & Dirks, Citation2020; Helseth et al., Citation2020) and The Wall Street Journal (Alves et al., Citation2020; Cui et al., Citation2021), namely the data on the entities’ share prices.

The initial empirical field corresponded to the entities that are part of the main capital markets indices of the stock exchanges of the EU countries, for which the use of IAS in SFS is mandatory or optional. Such information was initially obtained through the IFRS Foundation website, based on the positive answers to the following question ‘For example, are IFRS accounting standards required or permitted in the entities’ SFS whose securities are traded on a public market?’ (IFRS Foundation, Citationn.d.). Therefore, twenty-one countries were initially considered since IAS application is not permitted in six cases (Austria, France, Germany, Hungary, Spain, and Sweden).

shows the indices in which the entities included in the sample are inserted, also detailing the type of IAS adoption (mandatory or optional) for preparing their SFS. In certain countries, this type of adoption also depends on specific criteria, as additionally explained in the column ‘observations’.

Table 2. Sample description.

Finally, seventy-two entities that did not provide the SFS, or for which this information could not be found, were excluded, as well as ten entities that are silent on the accounting method adopted for interests within the scope of IAS 27. Due to the availability of these reports in a language other than Portuguese or English and in formats that are incompatible with machine translation, six entities were additionally excluded from the scope of this investigation.

summarizes the process that led to the exclusion of entities from the initial to the final sample.

Table 3. Sample selection.

It should be stressed that, at the end of this process, all three entities from Belgium and twenty-four from Finland were also excluded, as none of these entities met the sample selection criteria, namely by not disclosing key elements for analysis and the use of standards other than IAS, respectively.

Thus, at the end of the selection process, 267 entities met the criteria defined for analysis, being distributed among the indices of the capital markets representing different countries. Thus, after excluding all entities from Belgium and Finland, the final sample consists of 19 countries.

shows the distribution of the sampled entities by their respective countries.

Table 4. Final sample research by country.

To achieve the objective proposed in this study, two hypotheses (H1 and H2) were developed as previously proposed, which will be tested through distinct linear regression models. Within those models, a set of independent and control variables are proposed. In turn, the dependent variable corresponds to the entities’ share price (SP) at the date of publication of the SFS or, in the absence of this, to the date of reporting. For cases where the SP was not available on any of these dates, the value for the immediately closest date was used.

identifies the independent and control variables used in the models proposed, as well as the literature that served as a reference for these options.

Table 5. Independent and control variables and their proxies.

Then, for the analysis of the value relevance of the SFS and the interests reported therein, the model developed by Ohlson (Citation1995) was followed, as well as the variables proposed by him (EPS and BVPS). In turn, the interests under assessment in this research (subsidiaries, associates, and joint ventures reported in SFS) were also defined as independent variables, being calculated as the ratio between the accounting value found for this item and the entities’ total shares (IPS). Then, whenever this variable was included, the variable BPVS excluded the latter (being mentioned as BVPS’) to eliminate the duplication effect since those interests are comprised in the entities’ book value. Following, the sector of activity (SECTOR), indebtedness (IND) and the size of the auditing entity (AUDIT) were classified as control variables.

The economic activity sectors were based on the Industry Classification Benchmark (ICB) classification. provides the distribution of entities by their main economic activity sectors, also providing these sector codifications for analysis purposes.

Table 6. Final sample research by main economic activity sectors.

It should be noted that the inclusion of the categorical variable sector requires the prior transformation of each of the five sectors into distinct dichotomous variables (sector 1 to sector 5), in which ‘1’ indicates, for each of these variables, the sector concerned and ‘0’ if otherwise (entities from other sectors). In addition, the inclusion of these variables necessarily leads to the elimination of one of the existing variables, used as a reference variable for the analysis. Thus, as usually adopted in similar research, this study excluded sector 6 (health), which corresponds to the last variable and is the least representative.

Following, the remaining dichotomous variables were classified as follows. The variable AUDIT intends to identify if the audit firm that reported the KAM is a Big Four, being those cases classified as ‘1’ and ‘0’ otherwise. The variable MET consists of the identification of the method of accounting for interests in subsidiaries, associates, and joint ventures (MET), with the value ‘1’ being assigned if the entities exclusively adopt the cost method in the accounting of those interests and ‘0’ otherwise. The dichotomous variable related to KAM (KAM_IAS27) corresponds to the identification of matters related to interests in subsidiaries, associates, and joint ventures in the audit reports, where the value ‘1’ is assigned in cases where this is the case and ‘0’ otherwise. Finally, for the variable relating to the type of IAS adoption (TYPE), the value ‘1’ was assigned in the case of entities in which the Member States require the adoption of IAS 27 for entities presenting their SFS and ‘0’ otherwise.

Different analyses and statistical metrics were used as preliminary analyses, as well as to verify the assumptions underlying the linear regression models under study, such as the adjusted R2, the Durbin-Watson test and the analysis of variance (ANOVA) test.

The adjusted R2 is used to evaluate the validation and explanatory power of the models, and the closer to 1, the better it translates the explanatory power of the independent variables concerning the dependent variable (Bento et al., Citation2021). Based on the Durbin-Watson test, it is possible to assess the adequacy of the model through the level of autocorrelation between residuals, which varies between 0 and 4 (Ringo & Lyimo, Citation2023), while values between 1.5 and 2.5 indicate no autocorrelation between variables (Magoma et al., Citation2022). The overall significance of the linear regression models is based on ANOVA, which indicates the explanatory capacity of the models to be used for statistical inference.

Multicollinearity analyses between the independent variables were also performed, based on the Variance Inflation Factor (VIF) analysis. To this end, correlation levels were considered high for values greater than 0.7 and the existence of multicollinearity when the VIF was greater than 10, also considering what is commonly accepted for value-relevance models (Albuquerque et al, Citation2023; Bayman & Dexter, Citation2021; Kargin, Citation2013; Saputra, Citation2020). Such analyses make it possible to prevent possible errors in the analysis models when independent variables are highly correlated (Daoud, Citation2017).

Within the scope of this study, two baseline models and an additional model were developed, to compare different variables and observe the impacts they have on the value relevance of the information in the SFS.

The first baseline model (M1) was developed to identify the overall relevance of SFS through the influence of EPS and BVPS on SP, as proposed in H1 and shown in EquationEquation 1(1)

(1) .

(1)

(1)

With a similar purpose, the second baseline model (M2) was developed to test the influence of IPS on SP and to evaluate the impact of the interests provided for in IAS 27 on the relevance of the information, as proposed in H2 shown in EquationEquation 2(2)

(2) .

(2)

(2)

By comparing it with M1, it will be possible to determine whether these interests specifically influence the value relevance of the SFS. As such, and as already mentioned, the BVPS had to be replaced by the ‘BVPS’, as the IPS is already implicitly integrated into that variable.

Furthermore, an additional model (M3) based on M2 but, incorporating, however, specific variables related to the SFS and interests provided for in IAS 27, for a combined and more comprehensive analysis, as presented in Equationequation 3(3)

(3) .

(3)

(3)

Through M3, it will be possible to evaluate the impact that certain variables specifically associated with the SFS reported by entities, along with the interests in the scope of IAS 27, have on the relevance of that information.

The following section provides the results of the regression models proposed and also discusses those findings.

5. Empirical results and discussion

This section is divided into two subsections, with the first being dedicated to the presentation of results and the second one to their discussion.

5.1. Presentation of results

This subsection intends to provide the results obtained, through the initial descriptive analyses and, subsequently, the regression models performed.

shows the descriptive statistics, namely the mean, median and standard deviation for the continuous variables, as well as the frequency for the dichotomous variables also included in the value relevance models proposed.

Table 7. Descriptive statistics.

Except for the IND, shows a significant range in the values of the variables under investigation. The cost is more common than other accounting methods (MET), with a lower spread of methods other than that used by the entities. The audit entities selected by the listed European entities were also the major four audit ones (AUDIT). Most of the entities’ SFS presentations are required. Lastly, even if the interests recorded in the entities’ SFS have material relevance, the auditors only report these assets as a KAM in about 30% of the cases they have audited.

Following, correlation analyses using Pearson’s correlation and multi-correlation through VIF analysis were carried out for the variables under assessment, to detect potential collinearity or multicollinearity issues, respectively.

shows the correlation between the variables included in the proposed models.

Table 8. Correlation between the variables of the regression models.

Since the correlations shown in are strong, with values higher than 0.7 found for some cases, the figures highlights certain instances of notable collinearity issues. There is a requirement to rule out one of the variables based on these relations, which include the EPS and the BVPS (and likewise the BVPS’). Considering this, it was decided to omit the variable EPS from the models.

Following, the VIF analysis was performed. Because the maximum acceptable threshold was not exceeded and the maximum VIF matched a value that was rather close to 0.6, no multicollinearity issues were found, and the analysis can be conducted with no restrictions. Again, the previously mentioned relation between the variables BVPS or BVPS’, and EPS are exceptions in this context, aligned with the findings of the Pearson correlation analysis performed before.

Finally, based on the Durbin-Watson test, the adequacy of all developed models was also observed.

5.1.1. Baseline models

shows the results of the baseline regression models (M1 and M2) proposed for the value relevance analysis. M1 determines the overall relevance of the data in the SFS based solely on the inclusion of the BVPS and control variables. In turn, the M2 was developed to determine the significance of the weight of the interests (IPS) under IAS 27 reported in the entities’ SFS. In this model, the BVPS was replaced by the BVPS’, a variable that does not include the IPS, to avoid redundancies since the IPS is identified separately. The dependent variable in both models is the entities’ share prices (SP).

Table 9. Regression models (M1 and M2).

shows that both models have a high explanatory capacity for statistical inference. However, there was a residual improvement in the fit of data in M2, with the addition of the variable IPS in this model, being, therefore, the one with the greatest explanatory capacity. Both the BVPS (included in M1) and the BVPS’ (included in M2), as well as the IPS (included in M2), are significant and present a positive influence on the level of the dependent variable. On the other hand, the control variables (SECTOR, IND and AUDIT) do not present any statistical significance.

5.1.2. Additional analysis

The results for M3 are shown in , which was developed as an additional model. In this model, three further variables were integrated into it, as follows: MET, KAM_IAS27 and TYPE. Therefore, M3 can be considered the most complete model since it incorporates all the independent variables proposed in this research for the value relevance analysis.

Table 10. Regression model (M3).

indicates that M3 can explain 98.5% of the variation of the dependent variable, demonstrating to be effective in explaining the associations with no decrease in its explanatory power in comparison to the previous models. Regarding the further variables included in this model, MET and KAM_IAS27 present a significant and negative influence on the dependent variable. Concerning the variable TYPE, in turn, it does not present any statistical significance.

The next subsection is dedicated to the discussion of the findings.

5.2. Findings discussion

To achieve the objective proposed for this research, which aims to assess the value relevance of SFS and the interests reported therein, the Ohlson (Citation1995) model was used. This model uses accounting information to assess its likely influence on the entities’ share prices, intending to measure the impact and relevance of that information on the entities’ market value.

Through the first model (M1), a significant and positive statistical influence was observed between the BVPS and the entities’ share prices, thus validating the H1, associated with the overall value relevance of the SFS. Thus, although not fully consensual in the literature, it corroborates what was evidenced in several previous studies (namely, Busari & Bagudo, Citation2021; Lopes & Camões, Citation2021; Müller, Citation2014; Palea, Citation2014; Sotti, Citation2018).

Regarding the relevance of the interests provided for in IAS 27, the results also confirm H2 as a positive association was identified between these interests and the entities’ share prices, which underscores the value relevance of the SFS. The material relevance (weight) of those interests in the entities’ SFS may represent the main explanation for the relevance of this information, despite the absence of previous studies on this particular matter, since it constitutes a novelty of this research.

In addition, the findings also provided evidence that the cost method for accounting for those interests has a negative influence on the share prices, which interestingly highlights, conversely, a positive association between the relevance of the entities’ adoption of either the EM and fair value models. This association is strengthened, for instance, by the studies developed by Benyasrisawat et al. (Citation2015), Garg and Hanlon (Citation2012) and Tutticci (Citation2002), being explained for the higher alignment with those methods with the entities’ market value, which increase their relevance (usefulness) for stakeholders in general and, more particularly, for the investors.

KAM, as per International Standard on Auditing 701 issued by the International Auditing and Assurance Standards Board (IAASB, Citation2021), have been identified as having a negative influence on the entities’ share prices, meaning that the presence of such matters may adversely affect the investors’ decisions. The material relevance of those interests allied with being appointed as KAM, i.e. having a higher assessed risk of material misstatement (IAASB, Citation2021), may explain this effect. Altawalbeh and Alhajaya (Citation2019) also observed that the presence of KAM has a significant impact on investors’ decisions.

According to Prasad and Chand (Citation2017), investors, analysts and other stakeholders supported that the presence of KAM increases the informative value of the entities’ data reported. Thus, and based on the findings, it is possible to conclude that the presence of KAM associated with the interests provided for in IAS 27 also increases the value relevance of SFS provided by the entities to their stakeholders.

Finally, the type of IAS adoption has not revealed any influence on the entities’ share prices because it did not present statistical significance. In this follow-up, the SFS seems to be relevant in their presentation itself since the mandatory or voluntary requirements in this regard do not influence their value relevance.

The next section discusses the main conclusions, as well as the research limitations and future avenues.

6. Summary and conclusions

The empirical study carried out has the SFS in the light of IAS 27 as a research object for assessing the value relevance of this accounting information reported by listed European Union entities. Besides, the value relevance of the interests in subsidiaries, associates and joint ventures reported in those accounts is also assessed since it represents the particular assets within the scope of that standard.

This research proved the existence of value relevance concerning both the overall SFS and the weight of the interests reported therein, by the likely influence of those elements on the entities’ share prices. It is also important to highlight the high explanatory capacity of the models proposed. In addition, it was confirmed that the accounting method and the presence of interests as a KAM are also relevant in this context, increasing the value relevance of the information reported. Among the accounting methods available to entities whenever they use the IAS 27, the EM and fair value models seem to be the ones that positively influence the value relevance of the SFS, aligned with a highly consensual doctrine in the accounting area.

As a limitation of this research, it is important to highlight the difficulty of obtaining clear information from the entities’ reports since, sometimes, it is not easily available and is subject to judgment by the researcher. The research was also restrained to data availability for listed European entities, which is also dependent on the local requirements regarding the mandatory and optional SFS presentation. Therefore, the number of observations was restricted to the information publicly reported, which did not permit the use of further analysis. This would permit the inclusion of additional variables for a more in-depth analysis of explanatory factors that may explain the value relevance of the SFS, namely with a breakdown by country for a cross-country comparison. Furthermore, the use of dependent variables other than the entities’ share prices, as a proxy of the entities’ market value, would possibly mitigate the volatility effects that naturally underlie that, also providing distinct perspectives of analysis of the relevance of the entities’ SFS.

Even though the study is limited to listed European Union entities, since IASB’s standards are widely adopted worldwide, future researchers can replicate the analysis to a significant number of other countries or capital markets that have accepted those standards to determine if the findings are similar. Therefore, as a suggestion for future investigations, it is proposed a possible extension of the sample to other indices or markets outside Europe. This analysis can identify whether the profile of European entities is similar to entities from other continents, considering the different cultures and local regulations, which may be a significant research opportunity to extend the analysis proposed, as previously suggested.

The exploration of further independent variables related to corporate governance can also be assessed, namely the weight of shares held by members of the board of directors and its independence and gender composition. Other matters underlying the value relevance of the SFS, and the interests disclosed therein, or even those compared to similar assets within the consolidated accounts, are also identified as potential proposals for future investigations. Other opportunities for future investigations may include extending the analysis period or comparing recessionary with growth periods. Finally, the analysis of further dependent variables that can be used as proxies for the relevance of SFS would add novelty to the literature since it would avoid the constraints behind the classical use of the entities’ share price that underlies Ohlson’s model.

As far as the authors’ knowledge, this is the first research that assesses the value relevance of interests reported in the SFS, which have not been reaching the same attention by researchers compared to studies with similar purposes but focusing on the consolidated accounts. Therefore, by stressing the relevance of those accounts, and the items reported therein, this study can benefit standard-setter bodies and local regulators in understanding the usefulness of SFS for stakeholders’ decision-making. This seems to be controversial, as it can be exemplified by the issue of accounting choices under IAS 27 to measure the interests in subsidiaries, associates, and joint ventures, which indicates a low level of relevance attributed by IASB to those accounts.

Author contributions

Maria Ribeiro, Fábio Albuquerque and Paula Gomes dos Santos equally contributed to the conception and design of the work, to the analysis and interpretation of the data, to review it critically for intellectual content, and to the final approval of the version to be published. Additionally, Maria Ribeiro provided the first draft of the paper and data collection. All authors agree to be accountable for all aspects of the work and they assume to be accountable for all aspects of the work, regardless of the duties the authors were involved in. Finally, no artificial intelligence (AI)-assisted technologies were used in the production of the submitted work.

Acknowledgement

The authors thank the Instituto Politécnico de Lisboa for supporting this research. This study was conducted at the Research Center on Accounting and Taxation (CICF) and was funded by the Portuguese Foundation for Science and Technology (FCT) through national funds (UIDB/04043/2020 and UIDP/04043/2020).

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

All data for this study were directly collected from the entities’ consolidated non-financial reports included in this research sample, which are publicly available. Notwithstanding, the authors are available to share the data collected for this purpose upon reasonable request, namely for research purposes. If you are interested in this data, please contact the corresponding author.

Additional information

Funding

Notes on contributors

Maria Carolina Ribeiro

Maria Carolina Ribeiro has a master’s in Auditing at ISCAL/IPL.

Fábio Albuquerque

Fábio Albuquerque has a PhD in Financial Economy and Accounting. He is a coordinator professor and director of the master’s degree in accounting at Lisbon Accounting and Business School (ISCAL) of Instituto Politécnico de Lisboa (IPL) and professor of the practice at NOVA Information Management School (NOVA IMS). He is also an integrated member of the Research Centre on Accounting and Taxation (CICF) at IPCA.

Paula Gomes Dos Santos

Paula Gomes Dos Santos has a PhD in Management with specialization in Accounting. She is a coordinator professor at ISCAL/IP L and an integrated member of the Center for Research in Organizations, Markets and Industrial Management (COMEGI) at Universidade Lusíada.

References

- AbuGhazaleh, N., Al-Hares, O., & Haddad, A. (2012). The value relevance of goodwill impairments: UK evidence. International Journal of Economics and Finance, 4(4), 206–216. https://doi.org/10.5539/ijef.v4n4p206

- Al-Ani, M., & Tawfik, O. (2021). Effect of intangible assets on the value relevance of accounting information: Evidence from emerging markets. Journal of Asian Finance, Economics and Business, 8(2), 387–399. https://doi.org/10.13106/jafeb.2021.vol8.no2.0387

- Albuquerque, F., Velez, A., & Pinto, V. (2023). What is more relevant? A comparison of cash flows indicators versus profit or loss from listed European companies. Cogent Business & Management, 10(3), 1–32. https://doi.org/10.1080/23311975.2023.2251214

- Almujamed, H., & Alfraih, M. (2019). Value relevance of earnings and book values in the Qatari Stock Exchange. EuroMed Journal of Business, 14(1), 62–75. https://doi.org/10.1108/EMJB-02-2018-0009

- Alnodel, A. (2018). The impact of IFRS adoption on the value relevance of accounting information: Evidence from the insurance sector. International Journal of Business and Management, 13(4), 138–148. https://doi.org/10.5539/ijbm.v13n4p138

- Al-Refiay, H., Abdulhussein, A., & Al-Shaikh, S. (2022). The impact of financial accounting in decision-making processes in business. International Journal of Professional Business Review, 7(4), e0627. https://doi.org/10.26668/businessreview/2022.v7i4.e627

- Altawalbeh, M., & Alhajaya, M. (2019). The investors’ reaction to the disclosure of key audit matters: Empirical evidence from Jordan. International Business Research, 12(3), 50–57. https://doi.org/10.5539/ibr.v12n3p50

- Alves, L., Sigaki, H., Perc, M., & Ribeiro, H. (2020). Collective dynamics of stock market efficiency. Scientific Reports, 10(1), 21992. https://doi.org/10.1038/s41598-020-78707-2

- Amir, E., & Lev, B. (1996). Value-relevance of nonfinancial information: The wireless communications industry. Journal of Accounting and Economics, 22(1-3), 3–30. https://doi.org/10.1016/S0165-4101(96)00430-2

- Ashbaugh, H., & Pincus, M. (2001). Domestic accounting standards, international accounting standards, and the predictability of earnings. Journal of Accounting Research, 39(3), 417–434. https://doi.org/10.1111/1475-679X.00020

- Badenhorst, W., & Von Well, R. (2023). The value‐relevance of fair value measurement for inventories. Australian Accounting Review, 33(2), 135–159. https://doi.org/10.1111/auar.12382

- Badu, B., & Appiah, K. (2018). Value relevance of accounting information: An emerging country perspective. Journal of Accounting & Organizational Change, 14(4), 473–491. https://doi.org/10.1108/JAOC-07-2017-0064

- Barth, M. E., Beaver, W., & Landsman, W. (2000, October). The relevance of value relevance research. Journal of Accounting and Finance Conference at Stanford University in October, https://cs.trinity.edu/rjensen/readings/barth.pdf

- Barth, M., Li, K., & McClure, C. (2022). Evolution in value relevance of accounting information. The Accounting Review, 98(1), 1–28. https://doi.org/10.2308/TAR-2019-0521

- Bayman, E., & Dexter, F. (2021). Multicollinearity in logistic regression models. Anesthesia and Analgesia, 133(2), 362–365. https://doi.org/10.1213/ANE.0000000000005593

- Bento, F., Galvão, L., & Nobre, F. (2021). The level of indebtedness and the determinants of the capital structure of companies in the textile industry listed in B3 [Paper presentation]. ADM International Management Congress 2021. https://admpg.com.br/2022/anais/arquivos/07202022_110735_62d80d8f3a223.pdf

- Benyasrisawat, P., Dixon, R., Kaewphap, K., & Virunjanya, U. (2015). Equity and cost methods in reported earnings: the case of Thai listed firms. Asian Journal of Business and Accounting, 8(1), 95–114. https://www.researchgate.net/publication/282071706_Equity_and_cost_methods_in_reported_earnings_The_case_of_Thai_listed_firms

- Bhatia, M., & Mulenga, M. (2019). Value relevance of accounting information: A review of empirical evidence across continents. Jindal Journal of Business Research, 8(2), 179–193. https://doi.org/10.1177/2278682118823307

- Bhimani, A. (2008). The role of a crisis in reshaping the role of accounting. Journal of Accounting and Public Policy, 27(6), 444–454. https://doi.org/10.1016/j.jaccpubpol.2008.09.002

- Boodhun, Y., & Jugurnath, B. (2023). Value relevance and integrated reporting sustainability approach: Evidence from listed non-financial companies in Australia. The Eurasia Proceedings of Educational and Social Sciences, 29, 10–23. http://www.epess.net/en/pub/issue/79582/1351964 https://doi.org/10.55549/epess.1351964

- Burke, Q., & Wieland, M. (2017). Value relevance of banks’ cash flows from operations. Advances in Accounting, 39, 60–78. https://doi.org/10.1016/j.adiac.2017.08.002

- Busari, K., & Bagudo, M. (2021). Comparing the value relevance of selected accounting information in consolidated and separate financial statements: The case of Nigerian listed financial service firms. Journal of Economics and Sustainability, 3(Number 2), 16–32. https://doi.org/10.32890/jes2021.3.2.2

- Cairns, D., Massoudi, D., Taplin, R., & Tarca, A. (2011). IFRS fair value measurement and accounting policy choice in the United Kingdom and Australia. The British Accounting Review, 43(1), 1–21. https://doi.org/10.1016/j.bar.2010.10.003

- Callao, S., Jarne, J., & Laínez, J. (2007). Adoption of IFRS in Spain: Effect on the comparability and relevance of financial reporting. Journal of International Accounting, Auditing and Taxation, 16(2), 148–178. https://doi.org/10.1016/j.intaccaudtax.2007.06.002

- Chalmers, K., Clinch, G., & Godfrey, J. (2008). Adoption of international financial reporting standards: impact on the value relevance of intangible assets. Australian Accounting Review, 18(3), 237–247. https://doi.org/10.1111/j.1835-2561.2008.0028

- Cui, L., Kent, P., Kim, S., & Li, S. (2021). Accounting conservatism and firm performance during the COVID‐19 pandemic. Accounting & Finance, 61(4), 5543–5579. https://doi.org/10.1111/acfi.12767

- D’Orazio, P., & Dirks, M. (2020). COVID-19 and financial markets: Assessing the impact of the coronavirus on the eurozone. Ruhr Economic Papers, 859. https://doi.org/10.4419/86788995

- Daoud, J. (2017). Multicollinearity and regression analysis. Journal of Physics: Conference Series, 949(1), 012009. https://doi.org/10.1088/1742-6596/949/1/012009

- Diantimala, Y., & Sofyani, H. (2020). Value relevance of asset revaluation disclosure. Journal of Accounting and Investment, 21(3), 555–569. https://doi.org/10.18196/jai.2103164

- Ernest, O., & Oscar, M. (2014). The comparative study of value relevance of financial information in the Nigeria banking and petroleum sectors. Journal of Business Studies Quarterly, 6(1), 42–54. https://www.proquest.com/docview/1566313130

- E-Vahdati, S., Wan-Hussin, W., & Ariffin, M. (2023). The value relevance of ESG practices in Japan and Malaysia: Moderating roles of CSR award, and former CEO as a board chair. Sustainability, 15(3), 2728. https://doi.org/10.3390/su15032728

- EY. (2022). Financial reporting developments- Equity method investments and joint ventures. https://assets.ey.com/content/dam/ey-sites/ey-com/en_us/topics/assurance/accountinglink/ey-frd02230-161us-06-28-2022.pdf?download

- Garg, M., & Hanlon, D. (2012). The value relevance of fair value accounting: Evidence from the real estate industry. Corporate Ownership and Control, 9(4-4), 408–417. http://www.virtusinterpress.org/IMG/pdf/COC___Volume_9_Issue_4_Summer_2012_Continued4_.pdf#page=33 https://doi.org/10.22495/cocv9i4c4art4

- Gomes, D. (2009). Value relevance of financial assets. Faculty of Economics of the New University of Lisbon. (Work project, presented within the scope of the requirements for obtaining the Master’s Degree in Finance) http://hdl.handle.net/10362/9481

- Gonçalves, R., Lopes, P., & Craig, R. (2017). Value relevance of biological assets under IFRS. Journal of International Accounting, Auditing and Taxation, 29, 118–126. https://doi.org/10.1016/j.intaccaudtax.2017.10.001

- Goncharov, I., Werner, J., & Zimmermann, J. (2009). Legislative demands and economic realities: Company and group accounts compared. The International Journal of Accounting, 44(4), 334–362. https://doi.org/10.1016/j.intacc.2009.09.006

- Hamberg, M., & Beisland, L. A. (2014). Changes in the value relevance of goodwill accounting following the adoption of IFRS 3. Journal of International Accounting, Auditing and Taxation, 23(2), 59–73. https://doi.org/10.1016/j.intaccaudtax.2014.07.002

- Helseth, M., Krakstad, S., Molnár, P., & Norlin, K. (2020). Can policy and financial risk predict stock markets? Journal of Economic Behavior & Organization, 176, 701–719. https://doi.org/10.1016/j.jebo.2020.04.001

- Honggowati, S., Aryani., & Y., Rahmawati. (2015). Value relevance of financial and non-financial information to investor decision. Global Business Finance Review, 20(2), 95–104. https://doi.org/10.17549/gbfr.2015.20.2.95

- Hossain, T. (2021). The value relevance of accounting information and its impact on stock prices: A study on listed pharmaceutical companies at Dhaka Stock Exchange of Bangladesh. Journal of Asian Business Strategy, 11(1), 1–9. https://doi.org/10.18488/journal.1006.2021.111.1.9

- IAASB. (2021). Handbook of international quality control, auditing, review, other assurance, and related services pronouncements (Vol. I). https://www.ifac.org/_flysystem/azure-private/publications/files/IAASB-2021-Handbook-Volume-1.pdf

- Ibanichuka, E., & Briggs, A. (2018). Audit reports and value relevance of accounting information: evidence from commercial banks in Nigeria. Indian Journal of Finance and Banking, 2(1), 44–62. https://doi.org/10.46281/ijfb.v2i1.92

- IFRS Foundation. (2018). Conceptual framework for financial reporting. https://www.ifrs.org/issued-standards/list-of-standards/conceptual-framework/

- IFRS Foundation. (n.d). Who uses IFRS accounting standards? [Website]. https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction/

- Imhanzenobe, J. (2022). Value relevance and changes in accounting standards: A review of the IFRS adoption literature. Cogent Business & Management, 9(1), 1–13. https://doi.org/10.1080/23311975.2022.2039057

- Isaboke, C., & Chen, Y. (2019). IFRS adoption, value relevance and conditional conservatism: evidence from China. International Journal of Accounting & Information Management, 27(4), 529–546. https://doi.org/10.1108/IJAIM-09-2018-0101

- Javed, F., Akhtar, N., Sheikh, M., & Rasheed, M. (2023). Value relevance of accounting information in an emerging stock market: The case of Pakistan. Journal of Policy Research, 9(1), 28–37. https://doi.org/10.5281/zenodo.7726265

- Jorion, P., & Talmor, E. (2001). Value relevance of financial and non-financial information in emerging industries: The changing role of web traffic data. SSRN Electronic Journal, 1-26. https://doi.org/10.2139/ssrn.258869

- Kabir, N. (2021). The value relevance of accounting information on share price: evidence from Nigerian listed companies. UMYU Journal of Accounting and Finance Research, 1(2), 56–69. https://doi.org/10.61143/umyu-jafr.1(2)2021.004

- Kadri, M. H., Amin, J. M., & Bakar, Z. A. (2020). Investment property, cost model, fair value model and value relevance: Evidence from Malaysia. International Journal of Financial Research, 11(3), 115–124. https://doi.org/10.5430/ijfr.v11n3p115

- Kadri, M. H., Mohd Amin, J., & Abu Bakar, Z. (2023). Examining the value relevance of biological assets and their fair value change in Malaysia. International Journal of Academic Research in Accounting, Finance and Management Sciences, 13(1), 562–571. https://doi.org/10.6007/IJARAFMS/v13-i1/16574

- Kargin, S. (2013). The impact of IFRS on the value relevance of accounting information: Evidence from Turkish firms. International Journal of Economics and Finance, 5(4), 71–80. https://doi.org/10.5539/ijef.v5n4p71

- Khader, O., & Shanak, H. (2023). The value relevance of accounting information: empirical evidence from Jordan. International Journal of Law and Management, 65(4), 354–367. https://doi.org/10.1108/IJLMA-11-2022-0247

- Lee, H., & Lee, H. (2013). Do Big 4 audit firms improve the value relevance of earnings and equity? Managerial Auditing Journal, 28(7), 628–646. https://doi.org/10.1108/MAJ-07-2012-0728

- Lo, E. (2012). The value relevance of accounting information in transition to IAS/IFRS: the case of Indonesia. Jurnal Akuntansi Dan Manajemen, 23(2), 139–151. https://www.stieykpn.ac.id/journal/index.php/jam/issue/viewFile/96/159

- Lopes, A., & Camões, R. (2021 About the material value of the separate financial statements [Paper presentation].21.° USP International Conference in Accounting,. https://congressousp.fipecafi.org/anais/21UspInternational/ArtigosDownload/3142.pdf

- Magoma, A., Mbwambo, H., Sallwa, A., & Mwasha, N. (2022). Financial performance of listed commercial banks in Tanzania: A camel model approach. African Journal of Applied Research, 8(1), 228–239. https://doi.org/10.26437/azar.03.2022.16

- Migliavacca, A. (2023). Value relevance of accounting numbers and sustainability information in Europe: Empirical evidence from nonfinancial companies. Forthcoming on Journal of International Accounting, Auditing and Taxation, 55, 100620. https://ssrn.com/abstract=4498581 https://doi.org/10.1016/j.intaccaudtax.2024.100620

- Moscariello, N., & Pizzo, M. (2022). Practical expedients and theoretical flaws: the IASB’s legitimacy strategy during the COVID-19 pandemic. Accounting, Auditing & Accountability Journal, 35(1), 158–168. https://doi.org/10.1108/AAAJ-08-2020-4876

- Müller, V. (2011). Value relevance of consolidated versus parent company financial statements: Evidence from the largest three European capital markets. Accounting and Management Information Systems, 10(3), 326–350. https://doi.org/10.1016/j.intaccaudtax.2005.01.001

- Müller, V. (2014). The impact of IFRS adoption on the quality of consolidated financial reporting. Procedia - Social and Behavioral Sciences, 109, 976–982. https://doi.org/10.1016/j.sbspro.2013.12.574

- Neukirchen, L., & Bonotto, M. (2017). Analysis of the main audit matters (PAA) disclosed by the big four in the first adoption of the new auditor’s report of companies listed in the "new market" level of corporate governance on Bm&F Bovespa. https://lume.ufrgs.br/bitstream/handle/10183/182991/001073110.pdf?sequence=1&isAllowed

- O Cualain, G., & Tawiah, V. (2023). Review of IFRS consequences in Europe: An enforcement perspective. Cogent Business & Management, 10(1), 1–19. https://doi.org/10.1080/23311975.2022.2148869

- Ohlson, J. (1995). Earnings, book values, and dividends in equity valuation. Contemporary Accounting Research, 11(2), 661–687. https://doi.org/10.1111/j.1911-3846.1995.tb00461.x

- Okechukwu, O., & Jimba, I. (2023). Value relevance of sustainability reporting of listed industrial and consumer goods companies in Nigeria [Paper presentation]. 8th Annual International Academic Conference on Accounting and Finance (p. 262). https://icanig.org/documents/ACAF%208%20P16.pdf

- Oliveira, L., Rodrigues, L., & Craig, R. (2010). Intangible assets and value relevance: Evidence from the Portuguese stock exchange. The British Accounting Review, 42(4), 241–252. https://doi.org/10.1016/j.bar.2010.08.00

- Palea, V. (2014). Are IFRS value-relevant for separate financial statements? Evidence from the Italian stock market. Journal of International Accounting, Auditing and Taxation, 23(1), 1–17. https://doi.org/10.1016/j.intaccaudtax.2014.02.002

- Pathiranage, N., & Jubb, A. (2018). Does IFRS make analysts more efficient in using fundamental information included in financial statements? Journal of Contemporary Accounting & Economics, 14(3), 373–385. https://doi.org/10.1016/j.jcae.2018.10.004

- Pereira, A. (2019). Relevant audit matters reported by companies listed on Euronext Lisbon (Master’s Thesis in Auditing and Taxation). Católica Porto Business School. https://repositorio.ucp.pt/bitstream/10400.14/28779/1/TFM_AngelaPereira.pdf

- Prasad, P., & Chand, P. (2017). The changing face of the auditor’s report: Implications for suppliers and users of financial statements. Australian Accounting Review, 27(4), 348–367. https://doi.org/10.1111/auar.12137

- Pratiwi, A., Sumual, F., & Tanor, L. A. (2022). The value relevance of fair value on non-financial assets. Journal of International Conference Proceedings, 5(2), 52–63. https://doi.org/10.32535/jicp.v5i2.1670

- PwC. (2020). Initial measurement of equity method investment. [Website]. https://viewpoint.pwc.com/dt/us/en/pwc/accounting_guides/equity_method_of_accounting/Equity_Method_account/chapter_3/32_initial_measure.html

- Ringo, N., & Lyimo, B. (2023). The interplay of research and development spending, foreign direct investment, and economic growth: A moderation analysis. Olva Academy – School of Researchers, 5(1), 96–107. https://www.researchgate.net/publication/372195800_The_Interplay_of_Research_and_Development_Spending_Foreign_Direct_Investment_and_Economic_Growth_A_Moderation_Analysis

- Robu, I., Carp, M., Istrate, C., Popescu, C., & Robu, M. A. (2016). The value relevance of financial information under the influence of country risks. The case of the Indian listed companies. Review of Economic and Business Studies, 9(2), 77–93. https://doi.org/10.1515/rebs-2016-0035

- Sabino, J. (2010). The value relevance of tangible fixed assets. (Work project, presented within the scope of the requirements for obtaining the Master’s Degree in Finance). Faculty of Economics of the New University of Lisbon. https://run.unl.pt/handle/10362/10333

- Santos, P., Albuquerque, F., & Ribeiro, M. (2023). Notes on separate accounts in the light of International Accounting Standards. Reviewers and Auditors, 101, 52–59. https://www.oroc.pt/uploads/publicacoes/revista/2023/Revista101.pdf

- Saputra, K. (2020). The performance of the internal auditors of the village rural institution. International Journal of Environmental, Sustainability, and Social Science, 1(2), 28–35. https://journalkeberlanjutan.com/Index.php/ijesss https://doi.org/10.38142/ijesss.v1i2.24

- So, S., & Smith, M. (2009a). Value relevance of IAS 27 (2003) revision on presentation of non‐controlling interest: evidence from Hong Kong. Journal of International Financial Management & Accounting, 20(2), 166–198. https://doi.org/10.1111/j.1467-646X.2009.01029.x

- So, S., & Smith, M. (2009b). Value‐relevance of presenting changes in fair value of investment properties in the income statement: Evidence from Hong Kong. Accounting and Business Research, 39(2), 103–118. https://doi.org/10.1080/00014788.2009.9663352

- Sotti, F. (2018). The value relevance of consolidated and separate financial statements: Are non-controlling interests relevant? African Journal of Business Management, 12(11), 329–337. https://doi.org/10.5897/AJBM2017.8335

- Souza, F., Botinha, R., Silva, P., & Lemes, S. (2015). The comparability of accounting choices in the subsequent valuation of investment properties: An analysis of Brazilian and Portuguese publicly-held companies. Revista Contabilidade & Finanças, 26(68), 154–166. https://doi.org/10.1590/1808-057x201500580

- Srivastava, A., & Muharam, H. (2021). Value relevance of earnings and book values during the IFRS convergence period in India. Journal of Financial Reporting and Accounting, 19(5), 885–900. https://doi.org/10.1108/JFRA-11-2020-0321

- Tarca, A. (2020). The IASB and comparability of international financial reporting: Research evidence and implications. Australian Accounting Review, 30(4), 231–242. https://doi.org/10.1111/auar.12326

- The World Bank. (n.d). Market capitalization of listed domestic companies (% of GDP) - European Union. [Website]. https://data.worldbank.org/Indicator/CM.MKT.LCAP.GD.ZS?End=2018&locations=EU&start=1975&view=chart

- Tutticci, I. (2002). The value relevance of equity accounting in Australia during the pre-recognition regulatory period. Asia-Pacific Journal of Accounting & Economics, 9(2), 209–233. https://doi.org/10.1080/16081625.2002.10510609

- Umoren, A., & Enang, E. (2015). IFRS adoption and value relevance of financial statements of nigerian listed banks. International Journal of Finance and Accounting, 4(1), 1–7. https://doi.org/10.5923/j.ijfa.20150401.01

- Vázquez, R., Valdés, A., & Herrera, H. (2007). Value relevance of the Ohlson model with Mexican data. Contaduría y Administración, 223, 33–52. https://www.scielo.org.mx/scielo.php?pid=S0186-10422007000300003&script=sci_arttext&tlng=en

- Xu, W., Anandarajan, A., & Curatola, A. (2011). The value relevance of goodwill impairment. Research in Accounting Regulation, 23(2), 145–148. https://doi.org/10.1016/j.racreg.2011.06.007

- Zeng, X., Guo, X., Yang, C., & Xiong, Y. (2012). Value relevance of financial assets’ fair values: Evidence from Chinese listed companies. African Journal of Business Management, 6(12), 4445–4453. https://doi.org/10.5897/AJBM11.275