?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This research delves into the adoption dynamics of International Financial Reporting Standards for Small and Medium-sized Entities (IFRS for SMEs) in Morocco, a nation yet to embrace these standards, presenting a distinctive opportunity to scrutinize the challenges of implementation within a developing, pre-adoption milieu. While existing studies have primarily scrutinized post-adoption scenarios through a macroeconomic lens, often neglecting individual and firm-level intricacies, this investigation employs qualitative methodologies such as semi-structured interviews and content analysis to unearth fresh determinants of accounting standards adoption. Insights gleaned from discussions with 12 accounting professionals unveil novel factors like Implementation Modality and Industry Sector, contributing to a more nuanced comprehension of the adoption process at both individual and organizational levels. By shedding light on these micro-level dynamics, this study addresses a notable gap in the literature, augmenting the predominantly country-level analyses of IFRS for SMEs adoption.

1. Introduction

In today’s rapidly evolving global business environment, firms increasingly seek international opportunities, necessitating accounting standards that transcend national boundaries and accommodate diverse economic landscapes (Barth et al., Citation2008; Kılıç et al., Citation2014). Consequently, there is a pressing need for harmonized accounting standards applicable not only to publicly listed companies but also to non-listed entities, addressing the diverse stakeholder needs within the global market (Bonito & Pais, Citation2018). To meet this need, the IFRS Foundation introduced the IFRS for SMEs in July 2009, offering a streamlined framework with approximately 300 disclosures, significantly fewer than the full IFRS’s 3,000 disclosures, thereby enhancing accessibility and applicability across a broader range of entities (Perera & Chand, Citation2015).

The adoption of IFRS for SMEs has gained momentum globally, with nearly one hundred jurisdictions considering or implementing these standards. Unlike full IFRS, which targets publicly listed companies with public accountability, IFRS for SMEs caters to entities without public accountability, reflecting diverse economic ecosystems’ needs. Despite its name, IFRS for SMEs is not limited to small and medium-sized enterprises, as it lacks specific quantitative criteria, making it relevant to larger non-listed companies seeking international exposure.

Previous studies highlight the benefits of adopting IFRS, such as improved communication, reduced agency costs, decreased capital expenditures, enhanced comparability, lower transaction costs, and increased international openness (Beuselinck et al., Citation2009; Brüggemann et al., Citation2013). Additionally, literature affirms that adopting IFRS can reduce corruption, increase value relevance, bolster capital market efficiency, and stimulate foreign investment (Leykun Fisseha, Citation2023). However, there is professional reluctance to fully embrace IFRS despite its advantages (DeFond et al., Citation2011).

Countries with greater international openness often prefer full IFRS over IFRS for SMEs, as observed by Irvine (Citation2008), and Neu and Ocampo (Citation2007). This preference suggests that implementing IFRS, whether complex or simplified, poses significant challenges for individual jurisdictions. While developed economies deliberate convergence at their pace, developing economies, particularly in Africa, face institutional pressures to embrace convergence, extending to adopting international accounting standards like IFRS for SMEs (Boolaky et al., Citation2020).

In the African context, Sappor et al. (Citation2023) found that coercive isomorphism and environmental factors positively influence IFRS for SMEs adoption in Ghana, moderated by compliance levels. Similarly, Muda et al. (Citation2024) indicated that coercive and mimetic pressures significantly influence IFRS for SMEs adoption, while normative pressures did not. Environmental factors either moderate or enhance the relationship between normative pressures and IFRS for SMEs adoption.

These studies illustrate the intricate landscape of IFRS for SMEs adoption in sub-Saharan Africa, primarily driven by coercive isomorphism from formal and informal external pressures, including regulatory frameworks (DiMaggio & Powell, Citation1983). While sub-Saharan countries share commonalities with IFRS for SMEs’ principles, the Moroccan context presents a unique case. Morocco’s accounting framework, influenced by French colonialism, is characterized by a de-jure code-law system focused on legal compliance. Thus, adopting IFRS for SMEs in Morocco poses unique challenges for accounting professionals accustomed to tax compliance and legal adherence, similar to other North African French-speaking countries like Algeria and Tunisia.

Extensive research has examined IFRS for SMEs adoption at the national level (Aboagye-Otchere & Agbeibor, Citation2012; Hussain et al., Citation2012; Samujh & Devi, Citation2015; Sellami & Gafsi, Citation2018; Zeghal & Mhedhbi, Citation2006), but individual and firm-level determinants remain underexplored (van Wyk & Rossouw, Citation2009). Our study addresses this gap by exploring IFRS for SMEs adoption within Morocco’s unique context, aiming to uncover specific adoption variables relevant to this setting.

Moreover, our research is motivated by the scarcity of literature on ex-ante adoption determinants. Utilizing the Diffusion of Innovations (DOI) theory, we examine variables influencing adoption based on constructs facilitating or hindering the process. This approach mitigates the recall problem in adoption studies, ensuring that variables influencing the adoption decision are accurately measured.

By integrating DOI theory, our study comprehensively explores IFRS for SMEs adoption in a pre-adoption framework, addressing literature gaps. We emphasize individual and firm-level determinants among Moroccan accounting professionals and potentially similar contexts. Employing a qualitative methodology, we use semi-structured interviews and Morin Chartier’s content analysis technique, involving 12 accounting professionals from diverse companies.

Our findings indicate that IFRS for SMEs adoption by Moroccan professionals depends on various variables, some previously unexplored. These include organizational factors, external influences, IFRS for SMEs attributes, and individual considerations, with new determinants such as implementation modality and industry sector.

This study contributes to understanding individual and firm-level factors shaping IFRS for SMEs adoption in emerging nations. It highlights the interplay between Morocco’s unique context and IFRS for SMEs adoption, offering crucial insights for stakeholders in the adoption process. Additionally, it expands adoption and diffusion studies by introducing new variables relevant to this context and methodologically enriches content analysis techniques.

Given the inconclusive evidence in this field, our study addresses the research question: How do Moroccan accounting professionals perceive various factors, including potential new variables, influencing their intention to adopt IFRS for SMEs? This approach may uncover overlooked variables, expanding the literature’s breadth.

The study begins with a comprehensive background and literature review on IFRS for SMEs adoption, followed by the research design, empirical findings, discussion, and a summary conclusion.

2. Background

Before 1992, Morocco lacked an official accounting framework, leading to inadequate economic and financial information from corporate accounting. To address this, the ‘National Committee for the Accounting Chart of Accounts’ was established in 1983 and began its substantive work in 1986. Within this committee, the Minister of Finance formed a technical commission known as the ‘Accounting Standardization Commission’, tasked with drafting the General Code of Accounting Standards (CGNC) – the first official Moroccan accounting framework.

Implementation of the CGNC occurred through various legislative measures, including Decree No. 2.89.61 in 1989 and Opinions No. 1 and 2 of the National Accounting Council (CNC) in 1993, following the enactment of Law No. 9.88 in 1992 – The Moroccan accounting law. This transition marked a shift from a simplistic to a more sophisticated accounting system, emphasizing a new philosophy and principles aimed at portraying a true and fair view of enterprises.

Subsequently, the global economic landscape has undergone significant transformations, presenting institutions and entities with a myriad of new challenges that necessitate the adoption of updated practices and consequently up-to-date accounting standards. Regrettably, Morocco has not kept pace with these changes, as the CGNC has remained stagnant since 1992 leading to its obsolescence in light of contemporary economic dynamics. For instance, this outdated accounting framework fails to incorporate recognition and measurement principles pertaining to certain basic items of the entity’s assets like websites or softwares, highlighting its inadequacy in addressing contemporary economic issues. Instructions in this regard (and on similar items) are provided by tax regulations.

In this context, the imperative for revising the Moroccan accounting framework has become evident, constituting a prerequisite for the nation’s strategic alignment with international standards and its commitment to economic globalization. However, while the decision in 2007 ostensibly aligns with this trajectory as it mandates the use of full IFRS for the consolidated financial statements, its scope remains delimited, exclusively encompassing entities listed on the Casablanca Stock Exchange (BVC) and financial institutions (e.g. banks, insurance companies …etc.). This selective approach overlooks a substantial swath of the Moroccan economic landscape (Benhayoun, Citation2022, p. 5), comprising predominantly small and medium-sized enterprises (SMEs) and non-publicly traded large enterprises, which collectively constitute the cornerstone of the nation’s economic architecture as they alongside constitute 99% of the Moroccan industrial fabric.

Consequently, there arises a compelling need to examine the viability of implementing a standard tailored to this context, exemplified by the IFRS for SMEs’ framework. Gélard (Citation2013) – a former member of the IASB - underscores the pivotal role of such adoption initiatives, particularly within the Moroccan context, characterized by a paucity of listed entities. Indeed, the adoption of simplified standards assumes heightened significance, representing a critical imperative for the Moroccan business milieu. Nevertheless, notwithstanding the perceived importance of this transition, Moroccan enterprises evince a notable hesitance, citing an asymmetrical cost-benefit calculus favoring the status quo (El Haddad & Amzile, Citation2015). Hence, the Moroccan context emerges as a linchpin for evaluating the feasibility of integrating IFRS for SMEs.

The 2007’s decision aiming to bolster the openness of Morocco’s financial market by furnishing foreign investors with clear, standardized financial statements (Benhayoun & Marghich, Citation2018) was followed by events and occasions in which Moroccan accounting officials expressed their intention to converge with IFRS. At the 2013 and 2019’s national accounting symposium, the National Accounting Council (CNC) and the Institute of Chartered Accountants (OEC), the principal bodies governing accounting in Morocco, underscored the importance of aligning Moroccan GAAP (CGNC) with IFRS (El Quortobi, Citation2013).

Furthermore, the nature of the existing Moroccan accounting framework constitutes a challenging opportunity as it pervades a spirit of legalistic adherence, tax compliance and low levels of accounting judgements. The inherited accounting framework from French colonialism is characterized by an inflexion towards a macro-uniform, de-jure code-law system. Consequently, the unique case of rooted code-law based accounting tradition constitute an opportunity for exploring the adoption of IFRS for SMEs. Moroccan accounting professionals, accustomed to a culture of tax compliance and legal adherence in their daily practices, now confront the challenge of embracing accounting standards that diverge from their accustomed norms and introduce new challenges.

While Moroccan authorities and official institutions have shown a commitment to further adherence of Moroccan GAAP to IFRS standards (e.g. Opinion No. 26 regarding the irreversibility of IFRS mandatory application starting from July 24, 2023), Morocco has yet to adopt IFRS for SMEs as of 2024. This unique situation offers an ideal pre-adoption context for our study.

3. Literature review

3.1. IFRS for SMEs adoption

Following the retrieval of 106 papers from Scopus and WoS databases, it became apparent that both the publication and citation rates of IFRS for SMEs’ adoption experienced a notable surge starting in 2009, coinciding with the issuance of the standard. Prior to this year, only one article (Samujh, Citation2007) was identified, which examined the prerequisites for adopting this standard through a documentary study of its Exposure Draft, the implementation guide, and the adoption context within New Zealand. However, no empirical research has been undertaken thus far.

Out of the 106 papers, 60 addressed the adoption phenomenon, constituting approximately 56%, which aligns with earlier findings (Benhayoun & Marghich, Citation2017) emphasizing the primary focus on the adoption of IFRS for SMEs. Furthermore, it was observed that over 30% of the retrieved papers examined the acceptability of the standard, with these papers garnering 47% of the total citations. This observation is supported by other studies within the field (Aboagye-Otchere & Agbeibor, Citation2012; Adetula & Owolabi, Citation2014; Albu et al., 2013; Kılıç et al., Citation2014; Masca et al., Citation2010; Schutte & Buys, Citation2011; Strouhal, Citation2012)

While acceptability could be observed as a topic to be tackled in a pre-adoption context, in reality, this has not been the case for most research. Atik (Citation2010, p. 29) found that Turkish SMEs’ willingness to adopt IFRS is expressed when the standard is elective and not compulsory because most of them tend to use tax-based accounting because they satisfy their current accounting practices. The findings of Uyar and Güngörmüş’s study (2013, p. 86) indicate that while most of their Turkish accountants’ respondents stated that they have little knowledge of IFRS for SMEs, they also consider many major advantages of the adoption of the standard (e.g. ease in reaching financing sources, comparability of financial statements of SMEs, increase in reliability of financial statements of SMEs, efficiency in auditing, ease of rating SMEs by credit rating agencies, ease in transition to full IFRS, and increase in efficiency of cross-border activities), except for accounting professionals who are trained on IFRS for SMEs and are the employees of Big4. This finding indicates that SMEs do not objectively assess and evaluate the advantages and disadvantages of the standard. Based on the neo-institutional accounting theory, Albu et al. (Citation2013) tackled stakeholder perceptions regarding the implementation of IFRS for SMEs in emerging economies by studying four countries – the Czech Republic, Hungary, Romania, and Turkey. They suggested three scenarios for implementing the standard, using interviews and a qualitative approach.

Our study focuses on adoption determinants; therefore, papers on adoption factors should be highlighted. As mentioned in , only seven studies covered IFRS for SMEs’ adoption factors. After careful reading, we noticed that all the studies tackled the country-level determinants of IFRS adoption for SMEs.

Table 1. Analysis of IFRS for SMEs adoption subjects in the literature.

The findings of Rudzani and Manda (Citation2016) regarding the adoption of IFRS by SMEs in South Africa are significant for firm-level determinants. However, the theoretical background needs to be addressed to better understand the adoption process of this standard. They observed that most SMEs in the Vhembe District have adopted IFRS for SMEs despite the existing challenges that they face, and even though they do not see it as serving the main goal of business growth. They also provided some obstacles to be considered - low level of awareness, lack of accounting education, training, and inability to acquire relevant resources – when it comes to SMEs adopting this standard.

While Samujh (Citation2007) concluded that IFRS for SMEs does not present significant advantages to New Zealand’s SMEs because it does not address any issues pertaining to their context, and ironically quoting in the epilogue of his paper (2007, p. 19) that: ‘If ain’t broke don’t fix it, ‘ Ezaaz et al. (Citation2014) see that the standard has benefited SMEs in Fiji since its adoption, even though it presents some difficulties in the interpretation of some technical matters.

The results of Oyewo’s survey (Citation2015) of 136 SME proprietors in Lagos, South Africa, show the necessity to take into account factors such as short timeframe and high cost of acquiring requisite technological infrastructures that support IFRS-compliant accounting systems and internal business processes, as well as other perceptual factors such as necessity for adoption, perceived benefits, and personal qualities such as work experience, level of education, and age of SME proprietors. To the best of our knowledge, this is the only study highlighting individual-and/or firm-level determinants relating to IFRS for SMEs adoption.

Kaya and Koch (Citation2015) studied a sample of 128 countries and concluded that countries that do not have the capability to develop their own local GAAP- generally developing non-EU countries – are more likely to adopt IFRS for SMEs. Prior application of full IFRS by SMEs seems to help the adoption of IFRS for SMEs compared to local GAAP, and lower governance quality is positively associated with IFRS adoption. However, Kaya and Koch (Citation2015, p. 33) stressed the necessity of further research at the firm level to better understand the adoption process.

Additionally, authors as Damak-Ayadi et al. (Citation2020) and Bonito and Pais (Citation2018) delved into the adoption of IFRS by SMEs at the national level. Damak-Ayadi et al. (Citation2020) for instance suggest that future research should investigate the factors influencing firms’ adoption of IFRS for SMEs, given the significance of SMEs in the economy. Therefore, it is crucial to explore firm-level determinants, especially in developing contexts where adoption has not yet taken place.

Furthermore, Sappor et al. (Citation2023) investigated the factors driving companies’ adoption behavior in Ghana, using Structural Equation Modeling within the framework of neo-institutional accounting theory. They found that coercive isomorphism and environmental factors directly and positively impact the adoption of IFRS for SMEs, with the latter being indirectly influenced by the level of awareness. In a separate study by Muda et al. (Citation2024), it was revealed that coercive and mimetic isomorphic pressures significantly promote the adoption of IFRS for SMEs in Ghana, while normative isomorphic pressure does not exert a significant effect. Moreover, environmental factors were shown to moderate or amplify the non-significant relationship between normative isomorphic pressure and the adoption of IFRS for SMEs.

Nevertheless, it noteworthy that such studies showcase the necessity of considering additional variables that might strengthen the explaining capacity of their models. In fact, it is crucial to diligently unravel the intricate and hidden variables that potentially contribute and may significantly heighten our understanding of the adoption dynamics of IFRS for SMEs in similar social and economic settings (See ).

3.2. Diffusion of innovations’ theory

Accounting research typically revolves around a select few theories (Benhayoun, Citation2020), notably focusing on positive accounting theory (Watts & Zimmerman, Citation1986) and the neo-institutional theory of accounting (DiMaggio & Powell, Citation1983). Despite their utility, these theories exhibit limitations in addressing the adoption of IFRS for SMEs (Benhayoun & Zejjari, Citation2022), prompting the inquiry into why previous studies have not primarily relied on theories related to the adoption and diffusion of innovations.

This inquiry led us to explore the DOI theory as the framework for our study. Upon reviewing 131 papers retrieved from Scopus on the DOI theory, it becomes evident that administrative innovations have received comparatively less attention than technical innovations. Becker et al. (Citation2015, p. 108) point out that while early innovation research has predominantly focused on technical innovations, there is a paucity of literature on administrative innovations, which includes accounting systems in general.

While the DOI theory originally emerged from the realm of technological advancements and initially focused on individual-level dynamics rather than broader organizational or systemic contexts, its versatility has led researchers to apply it across various domains, regardless of the nature of the innovation or the population under study. Nonetheless, comprehending the intricacies of studying innovation diffusion from organizational or systemic perspectives is crucial. Wisdom et al. (Citation2013, p. 3) emphasize the multifaceted nature of the adoption process at these levels, while Rogers (Citation2003, p. 355) sheds light on the oversight in early diffusion studies, which failed to consider the organizational context of decision-makers.

The DOI theory holds significant promise for examining the adoption of IFRS for SMEs. Not only does it provide a robust framework for analyzing such phenomena, but it also enables researchers to anticipate events before their occurrence, offering a forward-looking perspective on their emergence. This stands in contrast to the retrospective nature of positive accounting theory, which typically explains events after they have transpired, potentially introducing methodological biases, such as the ‘time-order criticism’ highlighted by Rogers (Citation2003). In essence, this criticism underscores the importance of measuring explanatory variables at the time of the phenomenon’s occurrence rather than afterward.

Furthermore, applying an accounting framework rooted in the Anglo-Saxon tradition within a de jure accounting system can engender conflicts with existing accounting practices. Surveys conducted by El haddad and Amzile (Citation2015) among Moroccan companies reveal a reluctance to adopt IFRS for SMEs due to perceived disadvantages outweighing benefits, prompting a preference for aligning Moroccan GAAP with the new standard. Similarly, studies in the French context by Delvaille et al. (Citation2005) underscore similar reservations among professionals, highlighting the challenges associated with international standards adoption in contexts characterized by established accounting traditions.

Additionnaly, prior studies mobilised the DOI theory on the country-level using the bell shaped curve of categories of adopters tenet (early adopters, early majority, late majority and laggards) to study full IFRS adoption from a macro standpoint.

Consequently, adopting IFRS for SMEs does not necessarily entail a prior evaluation, both at the national and organizational levels, of the pros and cons of such a strategic decision. Therefore, assessing the conditions for adopting such a framework is of paramount importance, particularly given that adopting a common set of standards has become a priority if not a necessity.

Rogers (Citation2003, pp. 115-116) succinctly states: ‘Most past diffusion research has studied ‘what is,’ rather than ‘what could be’ […]. It is obviously impossible for an individual’s attitudes or personal characteristics, formed and measured now, to have caused his adoption of an innovation three years or five years previously’. Hence, it becomes evident that the factors influencing innovation adoption remain the most appropriate perspective for studying such a phenomenon within an ex-ante study context, especially when it helps avoid the recall problem.

These factors significantly influence adoption decisions. According to (Wisdom et al. (Citation2013), innovation adoption effectiveness hinges on the presence or absence of specific adoption constructs, which either facilitate or hinder adoption. These constructs operate diversely across various levels (external, organizational, innovation, or individual) and contexts. Consequently, these factors can be classified into four main categories: those pertaining to the external system, organization, individual, and innovation (See ).

4. Research design

The primary objective of our exploratory study is to formulate conjectures concerning the individual determinants of adopting IFRS for SMEs within the Moroccan context, with the aim of comparing them with existing literature and associating them with factors derived from the diffusion of innovation theory (Benhayoun & Marghich, Citation2020).

Given the pre-adoption status of IFRS for SMEs in Morocco, our study adopts an ex-ante approach, focusing on the examination of a pre-adoption context. This decision is informed by the complexity of the issue, which involves multiple stakeholders, and the constructive nature of this phase, which seeks to generate empirically testable hypotheses rather than validating pre-existing research hypotheses. Hence, qualitative methods are deemed appropriate for this exploratory endeavor.

Therefore, we chose to conduct individual interviews as our preferred technique, as they are deemed suitable by Gavard-Perret et al. (Citation2008, p. 90) for exploring intricate individual processes such as understanding, evaluation, decision-making, and mental imagery, as well as sensitive topics related to privacy or taboos. Furthermore, to mitigate researcher subjectivity, we employed content analysis, a method known for its objective procedures, as described by its pioneer (Berelson, Citation1952) as ‘a research technique for objective description’.

Typically, three types of individual interviews are distinguished based on the structuring of interaction levels between the interviewer and the interviewee: directive, non-directive, and semi-structured.(Gavard-Perret et al., Citation2008, p. 90) In fact, we utilized semi-structured interviews as our primary data collection method because it is an appropriate technique to: a) obtain diverse responses and understand various opinions (Glaum & Friedrich, Citation2006), targeting multiple stakeholders involved in the adoption of IFRS for SMEs, namely preparers, auditors, tax specialists, managers, government representatives, and users; (Albu et al., 2013, p. 151) and b) the ex-ante nature of our study, which aims to explore in-depth insights regarding our topic.

According to Cooper and Schindler (Citation2006, p. 205), semi-structured interviews are characterized by the following points:

They rely on developing a dialogue between the researcher and the interviewee.

They require imagination and creativity on the part of the researcher.

They use the researcher’s skills to elicit a quality and variety of information.

They leveraged the experience and skills of the researcher to achieve clear and structured responses.

Since we used semi-structured interviews in our methodological setting, approval was provided by the Scientific and Ethics Committee of our Research Laboratory of Entrepreneurship, Management and Organizations’ Control [LEREMCE] belonging to the Moulay Ismail University in Meknes with ethics approval reference QSSSI-22-0009.

However, it is essential to prepare an interview guide in advance, considering all of these elements, whose main purpose is to achieve the predetermined objectives of the interview.

4.1. Interviewees

Our study focuses on a target group comprising 12 accounting professionals drawn from diverse companies in terms of size, geographical location, workforce composition, accounting practices, and direct involvement in financial reporting within the Moroccan context. We assert that these 12 interviewees are representative of eligible companies for applying IFRS for SMEs, a belief supported by several research studies in this domain (Albu et al., Citation2014). This selection is justified for the following reasons:

The interviewees hold key positions in the process of adopting IFRS for SMEs.

The interviewees held diverse positions, including accountants, certified accountants, auditors, top managers, and executives, representing various levels of the accounting process.

The interviewees had diverse profiles, including different backgrounds, levels of education, and knowledge of IFRS for SMEs.

The selection of these companies, which have opted for anonymity, is justified for several reasons:

Their legal status aligns with the criteria for applying the IFRS for SMEs (IFRS Foundation, Citation2015, p. 11).

In fact, these companies do not have public accountability under IFRS for SMEs, because

Their borrowing or equity instruments are not traded in an organized market, and they are not in the process of issuing them for trading in an organized market.

These companies do not hold assets in fiduciary capacity for a broad group of third parties during their primary activities, such as banks, credit cooperatives, insurance companies, securities brokers/stockbroking companies, mutual funds, and investment banks.

However, these companies publish their general-purpose financial statements for external users, for example, owners who do not participate in business management (the state) and existing and potential creditors (international funders).

These companies have undergone significant accounting changes, transitioning from public and budgetary accounting to the General Accounting Standard Code and from manual to computerized accounting. This unique history has equipped them, and particularly their accounting teams, with extensive technical expertise and experience in adapting to accounting changes, further supporting their selection for the study.

The broad geographical spread and diverse organizational structures of these companies, encompassing various sizes, workforce compositions, executive backgrounds, and accounting practices, make them an ideal target group. Their heterogeneity provides a rich source of diverse information.

The cooperative attitude displayed by the interviewees facilitated easy access to information. Their close professional relationship with the researcher encouraged open expression of concerns and opinions regarding the research problem, contributing to the richness of data gathered.

4.2. The interview guide

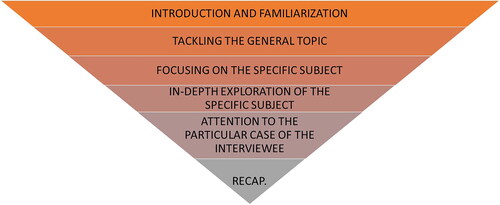

Effective preparation lays the foundation for conducting interviews that delve deeply into the intricate determinants influencing the adoption of IFRS for SMEs. Recognizing the need for both structure and adaptability in our approach (), we constructed an interview guide to steer our discussions. Serving as a compass for the exchange between researcher and interviewee, this guide is designed to navigate through the complexities of the research subject and extract nuanced insights. This process involves not only identifying the key areas of inquiry but also formulating questions that elicit meaningful responses (Gavard-Perret et al., Citation2008, p. 96). While there’s no universal blueprint for crafting an interview guide, we adhere to general principles outlined by Cooper and Schindler (Citation2006, p. 207), which delineate the interview process into four distinct stages resembling a funnel. This systematic framework ensures that our interviews are conducted with precision, guiding the flow of conversation from broad topics to specific details, thus maximizing the depth and richness of the data collected.

Figure 1. The structure and hierarchy’s interview according to Cooper and Schindler (Citation2006) and Gavard-Perret et al. (Citation2008). Source: Elaborated by authors.

Prior to commencing each interview, our foremost responsibility was to establish a comfortable atmosphere for the interviewee, emphasizing the significance of their participation in our research endeavor. We began the discussion with a broad overview, gradually honing in on specific topics to gain comprehensive insights. However, this approach did not entail a rigid adherence to a linear progression; rather, it ensured that essential points were addressed while allowing for organic conversation flow. As noted by Loufrani-Fedida (Citation2006, p. 207), our interview guide served as a valuable tool to maintain focus and prevent oversight of key aspects.

Drawing upon insights from our literature review, we initially developed a draft of the interview guide. This draft underwent rigorous scrutiny and refinement in collaboration with another researcher to ensure its structural integrity and coherence, culminating in the final version presented in Appendix 1.

The interview guide is structured around three overarching themes pertaining to the adoption of IFRS by SMEs. The pre-adoption phase delves into the interviewees’ perspectives on various aspects, including their opinions on the revision of the Moroccan GAAP (CGNC), their insights into the adoption process of international standards, and the prerequisites for such adoption. The subsequent theme explores issues related to the adoption process itself, encompassing discussions on required resources, associated costs, additional considerations beyond financial implications, and potential obstacles to transitioning from the Moroccan GAAP. Finally, the post-adoption theme delves into the ramifications of implementing IFRS for SMEs by Moroccan companies.

4.3. During the interview

This stage holds significant importance, warranting careful attention to the interview process. At the outset of each interview, we ensured to obtain informed verbal consent from every participant. Throughout the interviews, we prioritized allowing the interviewees ample space to express their thoughts without interruption, ensuring a seamless transition between topics outlined in the interview guide to maintain a fluid conversation flow.

Furthermore, we adopted a flexible approach during the interviews, aiming to delve deeper into the subject matter while fostering an atmosphere of trust, active listening, and open exchange to ensure the comfort of the interviewees.

Acknowledging the potential for bias, as highlighted in the literature (Bunea et al., Citation2012; Uyar & Güngörmüş, Citation2013), we refrained from immediately framing the discussion around IFRS for SMEs. Instead, we initially emphasized our focus on changes within the Moroccan GAAP to solicit insights. Gradually, we introduced IFRS for SMEs as one potential solution, among others, that might be pertinent in the Moroccan context.

At the conclusion of each interview, we proposed sending the transcripts to the interviewees and expressed sincere gratitude for their time and invaluable contributions to the research.

4.4. After the interview

The concluding phase of this exploratory stage holds comparable significance to its antecedent steps, as it encompasses the synthesis and establishment of the foundational framework for data analysis. Following each interview, we promptly compiled interview summary sheets, which were succeeded by transcription and data coding processes.

4.4.1. Interview summary sheet

The rationale behind generating interview summary sheets (refer to Appendix 2) was to document all interview comments immediately after each session while the researcher’s impressions were still vivid. These sheets, in accordance with recommendations from researchers like Miles and Huberman (Citation2003, pp. 104-105), are designed as straightforward documents featuring a series of questions intended to summarize or clarify field interactions. The researcher provided concise responses to each question based on their field note transcriptions, thereby offering a comprehensive recapitulation of the primary topics addressed during the interview.

4.4.2. Data coding

Data coding was conducted using a codebook developed from the findings of a literature review, with the model outlined in Appendix 3 serving as a guide. Additionally, the Morin Chartier’s method of content analysis was employed due to its recognized validity and reliability levels (Leray, Citation2008), as well as its qualitative-quantitative combinatory approach, which facilitates a thorough examination of underlying meanings and trends across various content types.

Our coding framework encompassed two primary measures, which were deemed as key strengths of the analysis:

Firstly, the framework allowed for the assessment of the unit of analysis by determining whether statements regarding a particular subject were favourable (+), unfavourable (-), or neutral (0) towards the adoption of IFRS for SMEs in Morocco. This facilitated the generation of indices useful for further quantitative exploration of qualitative analysis.

Secondly, the framework enabled the identification of the underlying variables that explain each unit of analysis. In other words, it sought to ascertain whether evaluations about a particular subject could be explained by variables contained within the unit of analysis. To this end, we asked an additional question Can the evaluation made about this subject be explained by a variable contained within the unit of analysis?’. This provided insights into the factors influencing the evaluations made for each unit.

For instance, if an interviewee expressed, ‘I am in favor of converging towards IFRS for SMEs’ the response to the first question would evaluate the statement as favorable towards the adoption of IFRS for SMEs. However, if the interviewee did not initially provide variables explaining their position, probing further would be necessary to elicit additional information. Subsequently, if the interviewee offered an explanation such as, ‘Because converging towards this framework will allow my company to perform better in terms of financial results’ the variable explaining the favorable evaluation would be the financial performance of their company.

Following transcription of the recordings, we engaged in a thorough review of the corpus to categorize the data, and subsequently proceeded with coding based on the established framework. For data analysis, thematic analysis (Bardin, Citation1993) was chosen as the method to uncover the underlying units of meaning, aligning with the study’s objective to explore and analyze the phenomenon at hand.

5. Empirical results and discussion

Previous research has extensively explored the adoption of IFRS for SMEs at the country level, covering various macroeconomic factors influencing its adoption. However, this leaves a gap in the literature, particularly regarding individual and firm-level determinants (Sellami & Gafsi, Citation2018; van Wyk & Rossouw, Citation2009). Additionally, there is a lack of literature on the determinants of IFRS for SMEs adoption in an ex-ante (Damak-Ayadi et al., Citation2020; Sappor et al., Citation2023) and francophone contexts (Benhayoun & Zejjari, Citation2023). Morocco is consequently well suited as the existing accounting framework is inherited from French colonialism that is typically tainted with a legalistic orientation. Therefore, the adoption of IFRS for SMEs by Moroccan companies serves as a distinctive case for investigation. Moroccan accounting professionals – mainly oriented towards tax compliance and legal adherence in their practices – must now adhere to a new spirit of accounting standards that deviate from their conventional norms and introduce new complexities. This situation is also pertinent to other North African French-speaking countries, such as Algeria and Tunisia.

Our study aims to fill this gap by investigating the adoption of IFRS for SMEs within Morocco’s unique context. By doing so, we seek to identify specific adoption variables relevant to this setting, providing insights that broader analyses may overlook. The DOI theory enriches our examination of IFRS for SMEs adoption within a pre-adoption framework. Its comprehensive analysis of various factors and stakeholders fills a significant gap in the literature, offering a nuanced approach that extends beyond existing research paradigms. By considering organizational, individual, and firm-level factors, our study provides a deeper understanding of the adoption process. Consequently, we emphasize the importance of individual and firm-level determinants in the adoption of IFRS for SMEs by Moroccan accounting professionals, and potentially in similar contexts. Our research addresses critical gaps in previous studies, including the specific nature of IFRS for SMEs and the quality of respondents, which previous studies often overlooked by focusing on full IFRS adoption determinants and broader country-level analyses

5.1. Data

We conducted 12 semi-structured interviews with a diverse group of accounting professionals hailing from various Moroccan companies, as detailed in . Our interviewees, specialized in the broad field of accounting, held pivotal roles in financial reporting within their respective organizations, encompassing positions such as Auditors, Chief Financial Officers, and Division Managers. They boasted extensive professional experience, averaging 11 years, and possessed diverse educational backgrounds, ranging from Undergraduate to CPA qualifications. Furthermore, the majority exhibited intermediate to expert-level knowledge pertaining to IFRS.

Table 2. Summary of the findings related to IFRS for SMEs adoption.

Interview durations varied between 44 minutes and 1 hour 22 minutes, with an average duration of one hour per interview. Collectively, the interviews spanned a total of 762 minutes, equivalent to 12 hours and 42 minutes.

To ensure the reliability of the collected information, twelve interviews were recorded and transcribed within a week. Transcription is known to be a time-intensive task, often necessitating six hours of work for every hour of recording, as highlighted by Loufrani-Fedida (Citation2006, p. 209). Consequently, for this study, the transcription process amounted to nearly seventy hours of work to build the 164 qualitative units of analysis that constitute our corpus. The latter (our dataset) is available from the corresponding author on reasonable request.

The content analysis encompassed eight key themes pertaining to the adoption of IFRS for SMEs in Morocco, spanning topics such as the ramifications of adoption, the procedural aspects of adoption, the motivations driving adoption, the essential resources for implementation, the associated efforts, incurred costs, prerequisites, and potential hindrances. Through the aggregation of data, statistics were derived in the form of totals, averages, and percentages. This analytical approach facilitated objective interpretations and fostered a comprehensive understanding of the studied phenomenon, surpassing the insights attainable through alternative analytical methodologies.

5.2. Index analysis

The index analysis of our content is divided into the following components:

Frequency Analysis or ‘Visibility’: This analysis quantifies the appearance of each subject in the overall corpus. This value was calculated using the following formula:

Equation 1: Calculation of the visibility of units of analysis in the corpus.

Weight-Trend Analysis: This analysis measures the weight that a subject or any other type of code represents compared to the overall trend observed in the corpus. The index was calculated as follows:

Equation 2: Calculation of the weight-trend of units of analysis in the corpus.

The cumulative weight-trend calculation allowed for the determination of the overall trend-impact of all codes. These indices are valuable as they measure general orientation, excluding neutral elements that could bias the study if neutrality was significant.

Bias Analysis: This analysis measures the degree of neutrality in the corpus of the study. The bias index calculates the levels of favorable and unfavorable orientations using the following formula:

Equation 3: Calculation of the bias of units of analysis in the corpus.

In our case, .

Orientation Index: This index provides the overall orientation of the research subject through the documents analyzed in the corpus. It also calculates the favorability index using the following formula:

Equation 4: Calculation of the orientation of units of analysis in the corpus.

The interviewees demonstrated a high bias index of 75.61%. However, in our context, this index should ideally reflect a high level of engagement from the interviewees, given that the subject matter relates closely to their core profession and influences their daily professional activities. This high level of involvement is crucial for ensuring that the study is not biased, as it indicates that the interviewees treated the subject with interest and sensitivity. Conversely, only 24.39% of the statements in our corpus were deemed neutral, which aligns more closely with the interviewees’ actual level of engagement.

The most frequently discussed topic, as indicated in , was the Consequences of adoption, which accounted for 19% of the total subjects addressed. It exhibited a bias of 84% and a weight trend of +9.68. This was closely followed by the Adoption Process, comprising 17% of the overall corpus, with a relatively lower bias of 61% and a weight trend of approximately +10.48.

Table 3. Summary of the findings related to DOI theory.

Additionally, it is worth noting that the topics Resources and Interest both hold a shared third position, each comprising 13% in terms of frequency. However, favorability significantly influences their ranking, with trend-weights of +11.29 and +15.32, respectively. Notably, the topic Interest maintains a neutrality score of 100%, indicating a complete absence of neutral expressions within the corpus concerning this subject. In contrast, the subject of Resources registers a neutrality rate of 73%. Finally, Conditions ranked fourth, representing a frequency of 12%. It exhibited a bias of 85% and a weight-trend of +10.48, positioning it as one of the most significant subjects of our analysis.

Consequently, it can be inferred that our interviewees exhibit a favorable inclination towards the adoption of IFRS for SMEs, particularly when the consequences are positive, the adoption process is encouraging, resources are favorable, conditions are met, and there exists an underlying interest driving this decision.

In terms of professional status (as depicted in ), CPAs exhibited the highest level of impartiality, indicated by an index score of 65%. However, they hold a relatively cautious stance towards the adoption of IFRS for SMEs, as evidenced by a modest weight-trend of +8.78. In contrast, consultants displayed the lowest level of impartiality, with an index score of 94%. Interestingly, consultants’ position on the adoption of the standard closely mirrors that of CPAs, as indicated by a weight trend of +8.06.

Table 4. Profiles of interviewees.

Furthermore, individuals operating within companies demonstrated a partiality index of 75%, placing them in an intermediary position compared to CPAs and consultants. However, their favorability towards adoption was particularly pronounced, reflected in a substantial total weight trend of +41.13. This strongly indicates their inclination towards adopting IFRS.

5.3. Detecting new adoption determinants

As previously stated, the objective of the second question in our content analysis is to ascertain whether it is probable that the unit of analysis could be elucidated by a particular variable. This inquiry yields variables that have the potential to elucidate the positions held by our interviewees.

The results, as depicted in , reveal previously unaddressed determinants in the literature. Initial observations indicate that out of the 164 units of information analyzed, 128 pertain to potential determinants for the adoption of IFRS, indicating a comprehensive analysis with a detection rate of 78%. Among these, a company’s international openness emerges as the most frequently discussed determinant in the corpus, representing 13% of the total variables analyzed. Notably, there is unanimous favorability towards this determinant, with no expressions of neutrality and a bias index of 100%. The weight impact index of +16.19 underscores the significance of this variable in the adoption of IFRS by SMEs in Morocco. It is important to highlight that this determinant is viewed not as an individual factor but rather as part of the determinants of external systems.

Table 5. Index table related to the code “Subject”.

Table 6. Index table related to the code “Status”.

Table 7. Analysis of detected determinants of our corpus.

The second most significant determinant pertains to the training plans of the stakeholders involved in the adoption process of IFRS for SMEs, addressed in 12% of the total variables. The corpus exhibits a non-neutral stance towards this determinant, with a bias index of 73% and a weight-trend index of +8.57, underscoring its importance for our interviewees. Despite a relatively lower weight-trend index of +3.81, the size of the company ranks third in terms of frequency, accounting for 10% of the total units of analysis with variables and a bias rate of 77%.

Additionally, the implementation modality emerges as the fourth determinant identified in our analysis, alongside the incentive offers from the organization and the benefits provided by the standard compared to current practice. This determinant, absent in both the literature specific to IFRS for SMEs adoption and that addressing factors of diffusion innovations, holds considerable importance, discussed in 9% of cases, with only 8% of the corpus expressing neutrality. It ranks third in terms of weight trend after international openness and training plans, at +6.67, underscoring its significance among the interviewees.

Moreover, our analysis detected another previously unaddressed determinant: the Industry Sector. The corpus exhibits no favorable position towards it, with a frequency of approximately 1%, a weight-trend of -0.95, and 100% impartiality.

However, it is crucial to note that the objective of this study is not to determine which variable is more favorable or unfavorable for the adoption of IFRS. Rather, the aim is solely to identify determinants that could potentially play a role in explaining the adoption of IFRS by SMEs at the individual and firm levels.

6. Summary and conclusion

This study delves into unexplored determinants of IFRS for SMEs adoption at both firm and individual levels within the unique Moroccan legalistic macro-based code-law system, situated in a pre-adoption, ex-ante, and developing context. As previous research predominantly focuses on macroeconomic factors in a post-adoption context, often utilizing theories unrelated to adoption phenomena, our study addresses a gap in the literature as we utilize the DOI theory lenses to help grasp the dynamics at play (Benhayoun & Zejjari, Citation2023).

We have employed a qualitative approach via semi-structured interviews with twelve accounting professionals from Moroccan companies directly involved in potential adoption of IFRS for SMEs, and utilized a content-analysis method inspired by Morin Chartier’s technique to explore the variables that could be linked to the adoption of IFRS for SMEs by Moroccan accounting professionals.

The main findings reveal that the adoption of IFRS for SMEs by Moroccan accounting professionals hinges on a variety of factors that either facilitate or impede the adoption process. While some of these factors have been previously studied in the literature, our research uncovers novel determinants previously overlooked. Our interviewees’ responses suggest that understanding the adoption of IFRS for SMEs requires a sequential analysis of organizational factors, external systemic influences, specific attributes of IFRS for SMEs, and individual considerations, alongside newly identified variables. Notably, our study reveals previously unexplored determinants such as the implementation modality of IFRS for SMEs and the industry sector.

This study has several contributions. Firstly, it empirically enhances understanding regarding the individual and firm-level factors shaping the adoption of IFRS for SMEs within an emerging nation and a pre-adoption context. Secondly, it sheds light on the interplay between the unique features of the Moroccan and North African context and the adoption of IFRS for SMEs. Thirdly, it provides stakeholders involved in the adoption process of accounting standards with vital considerations to consider before decision-making. Fourthly, it theoretically expands the scope of adoption and diffusion studies by introducing new variables that could explain the adoption of IFRS for SMEs in this specific context. Finally, it contributes methodologically to content analysis by incorporating an additional question to Morin Chartier’s technique, enhancing its analytical depth.

The implications of this study extend across various domains, offering valuable insights for policymakers, accounting professionals, researchers, and methodologists alike. Policymakers, standard-setters, and regulators in Morocco should carefully consider the identified determinants, such as the implementation modality of IFRS for SMEs and industry-specific dynamics, when formulating policies and regulations related to accounting standards adoption. This consideration can facilitate a smoother transition to IFRS for SMEs and address unique challenges faced by Moroccan companies. Concurrently, accounting professionals and firms should integrate these determinants into their decision-making processes to navigate IFRS adoption effectively. Targeted training initiatives focusing on organizational readiness and individual considerations can enhance professionals’ understanding and facilitate informed choices. The study’s identification of previously unexplored determinants also offers fertile ground for future research endeavors, enabling scholars to delve deeper into the causal relationships between these determinants and adoption outcomes in emerging economies. Moreover, the methodological contribution of integrating content analysis with supplementary questions enhances analytical depth and scope, providing researchers with a robust framework for investigating complex accounting phenomena.

However, our study acknowledges its limitations and does not claim exhaustiveness. Particularly, the absence of external validity measurement restricts the generalizability of results, typical of qualitative studies. Future research should aim to elucidate these determinants further, incorporating adoption factors derived from the tenets of DOI theory.

Author contributions

IB: Conceptualization; Data curation; data collection; original draft; and review & editing. IZ: conceptualization, literature review, methodology, data analysis. Both authors read and approved this manuscript.

Acknowledgements

We extend our sincere gratitude to the professionals who generously participated in this study, sharing their expertise and insights, which enriched our research endeavor. Their contributions have been invaluable in shaping the findings of this work. We also wish to express our heartfelt appreciation to Dr. Collins G. Ntim, Cogent Business and Management’s editor of the Accounting, Corporate Governance & Business Ethics’ section, as well as the anonymous reviewers for their diligent efforts in critically evaluating our manuscript. Their constructive feedback and valuable suggestions have significantly contributed to improving the clarity and rigor of our research.

Disclosure statement

No potential conflict of interest was reported by the author(s)

Availability of data and materials

The dataset used and/or analysed during the current study are available from the corresponding author on reasonable request.

Additional information

Funding

Notes on contributors

Issam Benhayoun

Issam Benhayoun is a specialist in accounting and finance, with a particular focus on financial reporting, International Financial Reporting Standards (IFRS), and small and medium-sized enterprises (SMEs). He applies his expertise in both academic and professional contexts. Dr. Benhayoun is a full-time Associate Professor of Accounting and Finance at the National School of Business and Management (ENCG) of Meknes at Moulay Ismail University. He also contributes as a part-time faculty member in Accounting and Finance at the School of Business Administration (SBA) of Al Akhawayn University. With a solid professional background, including roles as a former Senior Executive in Finance and Accounting and the former Head of the Management Control Division, Dr. Benhayoun combines practical experience with extensive research in the field of accounting. This unique blend of practical and scholarly expertise enables him to effectively bridge the gap between practice, research, and academia.

Ibtissam Zejjari

Ibtissam Zejjari is a researcher and Professor of Marketing and Management with a focus on consumer behavior in the Moroccan market. Her research interests lie particularly in the field of consumer behavior and the factors influencing purchasing decisions within this segment. Dr. Zejjari’s research explores the impact of factors like country of origin on consumer attitudes and purchase intentions. Her work contributes to a deeper understanding of the Moroccan context in particular and emerging markets in a broader aspect. Dr. Zejjari is passionate about advancing interdisciplinary research through many of her co-authored publications including bibliometric analyses as well as a deep understanding of adoption decisions in sustainability, supply chain management and financial reporting.

References

- Aboagye-Otchere, F., & Agbeibor, J. (2012). The international financial reporting standard for small and medium-sized entities (IFRS for SMES): Suitability for small businesses in Ghana. Journal of Financial Reporting and Accounting, 10(2), 1–21. https://doi.org/10.1108/19852511211273723

- Adetula, D., & Owolabi, F. (2014). International financial reporting standards (IFRS) for SMES adoption process in Nigeria. European Journal of Accounting Auditing and Finance Research, 2(4), 33–38.

- Albu, C., Albu, N., & Alexander, D. (2014). When global accounting standards meet the local context – Insights from an emerging economy. Critical Perspectives on Accounting, 25(6), 489–510. https://doi.org/10.1016/j.cpa.2013.03.005

- Albu, C. N., Albu, N., Pali-Pista, S. F., Gîrbină, M. M., Selimoglu, S. K., Kovács, D. M., Lukács, J., Mohl, G., Müllerová, L., Paseková, M., Arsoy, A. P., Sipahi, B., & Strouhal, J. (2013). Implementation of IFRS for SMEs in emerging economies: Stakeholder perceptions in the Czech Republic, Hungary, Romania and Turkey. Journal of International Financial Management & Accounting, 24(2), 140–175. https://doi.org/10.1111/jifm.12008

- Atik, A. (2010). SME’s views on the adoption and application of “IFRS for SMEs” in Turkey. European Research Studies Journal, XIII(Issue 4), 19–32. https://doi.org/10.35808/ersj/297

- Bardin, L. (1993). L’analyse de contenu (9th ed.). Puf le psychologue.

- Barth, E., Landsman, W., & Lang, M. H. (2008). International accounting standards and accounting quality. Journal of Accounting Research, 46(3), 467–498. https://doi.org/10.1111/j.1475-679X.2008.00287.x

- Becker, S., Wald, A., Gessner, C., & Gleich, R. (2015). Le rôle des attributs perçus pour la diffusion des innovations dans la comptabilité analytique. Le cas de la comptabilité par activités. Comptabilité Contrôle Audit, Tome 21(1), 105–137. https://doi.org/10.3917/cca.204.0105

- Benhayoun, I. (2020). L’isomorphisme mimétique, cette maladie chronique des dirigeants marocains. Challenge, 1(2024), 167036.

- Benhayoun, I. (2022). Pratique de la comptabilité des sociétés au Maroc [Practices of corporate accounting in Morocco]. Auto.

- Benhayoun, I., & Marghich, A. (2017). IFRS for SMEs: A structured literature review. International Journal of Accounting and Financial Reporting, 7(2), 538–561. https://doi.org/10.5296/ijafr.v7i2.12390

- Benhayoun, I., & Marghich, A. (2018). Moroccan GAAP and IFRS for SMES: A comparative study of the principles, concepts, financial statements and their components. Revue du Contrôle, de la Comptabilité et de L’audit, 2(2), 571–592.

- Benhayoun, I., & Marghich, A. (2020). L’influence des marchés financiers sur la normalisation comptable: Une lecture historique. International Journal of Innovation and Applied Studies, 29(4), 1189–1198.

- Benhayoun, I., & Zejjari, I. (2022). The diffusion of innovations’ theory shortfall in accounting standardization research: The case of IFRS for SMEs. Revue Marocaine de Gestion et de Société, 1, 22–57.

- Benhayoun, I., & Zejjari, I. (2023). Determinants of IFRS for SMEs adoption worldwide. International Journal of Accounting and Finance Studies, 6(2), 12–39. https://doi.org/10.22158/ijafs.v6n2p12

- Berelson, B. (1952). Content analysis in communication research. Free Press.

- Beuselinck, C., Deloof, M., & Manigart, S. (2009). Private equity involvement and earnings quality. Journal of Business Finance & Accounting, 36(5-6), 587–615. https://doi.org/10.2139/ssrn.1381242

- Bonito, A., & Pais, C. (2018). The macroeconomic determinants of the adoption of IFRS for SMEs. Revista de Contabilidad, 21(2), 116–127. https://doi.org/10.1016/j.rcsar.2018.03.01

- Boolaky, P., Tawiah, V., & Soobaroyen, T. (2020). Why do African countries adopt IFRS? An institutional perspective. The International Journal of Accounting, 55(01), 2050005. https://doi.org/10.1142/S1094406020500055

- Brüggemann, U., Jörg-Markus, H., & Sellhorn, T. (2013). Intended and unintended consequences of mandatory IFRS adoption: A review of extant evidence and suggestions for future research. European Accounting Review, 22(1), 1–37. https://doi.org/10.1080/09638180.2012.71

- Bunea, S., Săcărin, M., & Minu, M. (2012). Romanian professional accountants’ perception on the differential financial reporting for small and medium-size enterprises. Accounting and Management Information Systems, 11(1), 27–43.

- Cooper, D., & Schindler, P. (2006). Business research methods (9th ed.). McGraw-Hill.

- Damak-Ayadi, S., Sassi, N., & Bahri, M. (2020). Cross-country determinants of IFRS for SMEs adoption. Journal of Financial Reporting and Accounting, 18(1), 147–168. https://doi.org/10.1108/JFRA-12-2018-0118

- DeFond, M., Hu, X., Hung, M., & Li, S. (2011). The impact of mandatory IFRS adoption on foreign mutual fund ownership: The role of comparability. Journal of Accounting and Economics, 51(3), 240–258. https://doi.org/10.1016/j.jacceco.2011.02.001

- Delvaille, P., Ebbers, G., & Saccon, C. (2005). International financial reporting convergence: Evidence from three continental European countries. Accounting in Europe, 2(1), 137–164. https://doi.org/10.1080/09638180500379103

- DiMaggio, P. T., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101

- El Haddad, M., & Amzile, R. (2015). The IFRS for SMEs accounting standard: survey on their applicability to Moroccan SMEs. International Journal of Innovation and Applied Studies, 11(2), 429–436.

- El Quortobi, A. (. (2013 Référentiel IFRS: quel modèle de convergence pour le Maroc? Paper presentation]. 2nd Édition of "Les Assises Nationales de la Profession Comptable, Skhirat.

- Ezaaz, H., Sheetal, M., Glen, F., & Prena, R. (2014). The 2012 review of IFRS for SMES: possible responses from the Fiji Institute of Accountants. Accounting & Taxation, The Institute for Business and Finance Research, 6(2), 71–83.

- Gavard-Perret, M., Gotteland, D., Haon, C., & Jolibert, A. (2008). Méthodologie de la Recherche, Réussir son mémoire ou sa thèse en sciences de gestion. Pearson.

- Gélard, G. ((2013). IFRS: Une priorité pour les PMEs. Finances News, p. 200.

- Glaum, M., & Friedrich, N. (2006). After the bubble: Valuation of telecommunications companies by financial analysts. Journal of International Financial Management & Accounting, 17(2), 160–174. https://doi.org/10.1111/j.1467-646X.2006.00125.x

- Hussain, F. F., Chand, P. V., & Rani, P. (2012). The impact of IFRS for SMEs on the accounting profession: Evidence from Fiji. Accounting & Taxation, 4(2), 107–118.

- IFRS Foundation. (2015). IFRS for SMEs. IASB.

- Irvine, H. (2008). The global institutionalization of financial reporting: The case of the United Arab Emirates. Accounting Forum, 32(2), 125–142. https://doi.org/10.1016/j.accfor.2007.12.003

- Kaya, D., & Koch, M. (2015). Countries’ adoption of the international financial reporting standard for small and medium-sized entities (IFRS for SMEs) - early empirical evidence. Accounting and Business Research, 45(1), 93–120. https://doi.org/10.1080/00014788.2014.9

- Kılıç, M., Uyar, A., & Ataman, B. (2014). Preparedness for and perception of IFRS for SMEs: Evidence from Turkey. Accounting and Management Information Systems, 13(3), 492–519.

- Leray, C. (2008). L’analyse de contenu: De la théorie à la pratique: la méthode Morin-Chartier. Presses de l’Université du Québec.

- Leykun Fisseha, F. (2023). IFRS adoption and foreign direct investment in Sub-Saharan African countries: Does the levels of Adoption Matter? Cogent Business & Management, 10(1), 2175441. https://doi.org/10.1080/23311975.2023.2175441

- Loufrani-Fedida, S. (2006). Management des compétences et organisation par projets: une mise en valeur de leur articulation. Analyse qualitative de quatre cas multi-sectoriels [Doctorate thesis]. Sophia Antipoli University.

- Masca, E., Moldovan-Teselios, C., & Batrancea, L. (2010). Financial information presented under IFRS for SMEs in Romania. Applied Economics, Business and Development, 1(1), 192–197.

- Miles, M., & Huberman, M. (2003). Analyse des données qualitatives (2nd ed.). De Boeck.

- Muda, P., Tornyeva, K., & MacCarthy, J. (2024). The moderating role of environmental factors between institutional isomorphic pressures and the adoption of IFRS for SMEs: Application of SEM. Cogent Business & Management, 11(1), 2330012. https://doi.org/10.1080/23311975.2024.2330012

- Neu, D., & Ocampo, E. (2007). Doing missionary work: The World Bank and the diffusion of financial practices. Critical Perspectives on Accounting, 18(3), 363–389. https://doi.org/10.1016/j.cpa.2006.01.007

- Oyewo, B. (2015). How prepared are Nigerian small and medium scale enterprises (SMES) for the adoption of international financial reporting standards (IFRS)? Evidence from a survey. Academic Journal of Economic Studies, 1(1), 45–64.

- Perera, D., & Chand, P. (2015). Issues in the adoption of international financial reporting standards (IFRS) for small and medium-sized enterprises (SMES). Advances in Accounting, 31(1), 165–178. https://doi.org/10.1016/j.adiac.2015.03.012

- Rogers, E. M. (2003). Diffusion of innovations. Free Press.

- Rudzani, S., & Manda, D. C. (2016). An assessment of the challenges of adopting and implementing IFRSS for SMEs in South Africa. Problems and Perspectives in Management, 14(2), 212–221. https://doi.org/10.21511/ppm.14(2-1).2016.10

- Samujh, (2007). IFRS for SMEs: A New Zealand perspective. Department of Accounting Working Paper Series (p. 96). University of Waikato.

- Samujh, H., & Devi, S. S. (2015). Implementing IFRS for SMEs: Challenges for developing economies. International Journal of Management and Sustainability, 4(3), 39–59. https://doi.org/10.18488/journal.11/2015.4.3/11.3.39.59

- Sappor, P., Sarpong, F., & Seini, R. (2023). The adoption of IFRS for SMEs in the northern sector of Ghana: A case of structural equation modeling. Cogent Business & Management, 10(1), 2180840. https://doi.org/10.1080/23311975.2023.2180840

- Schutte, D., & Buys, P. (2011). A critical analysis of the contents of the IFRS for SMEs - a South African perspective. South African Journal of Economic and Management Sciences, 14(2), 188–209. https://doi.org/10.4102/jef.v12i1.393

- Sellami, Y., & Gafsi, Y. (2018). What drives developing and transitional countries to adopt the IFRS for SMEs? An institutional perspective. Journal of Corporate Accounting & Finance, (2)29, 34–56. https://doi.org/10.1002/jcaf.22331

- Strouhal, J. (2012). Applicability of IFRS for SMEs in the Czech Republic. Economics and Management, 17(2), 452–458. https://doi.org/10.5755/j01.em.17.2.2166

- Uyar, A., & Güngörmüş, A. (2013). Perceptions and knowledge of accounting professionals on IFRS for SMEs: Evidence from Turkey. Research in Accounting Regulation, 25(1), 77–87. https://doi.org/10.1016/j.racreg.2012.11.001

- van Wyk, H., & Rossouw, J. (2009). IFRS for SMEs in South Africa: a giant leap for accounting, but too big for smaller entities in general. Meditari Accountancy Research, 17(1), 99–116. https://doi.org/10.1108/10222529200900007

- Watts, R., & Zimmerman, J. (1986). Positive accounting theory. Prentice-Hall.

- Wisdom, J., Ka Ho, B., Hoagwood, K., & Horwitz, S. (2013). Innovation adoption: A review of theories and constructs. Administration and Policy in Mental Health, 41(4), 480–502. https://doi.org/10.1007/s10488-013-0486-4

- Zeghal, D., & Mhedhbi, K. (2006). An analysis of the factors affecting the adoption of international accounting standards by developing countries. The International Journal of Accounting, 41(4), 373–386. https://doi.org/10.1016/j.intacc.2006.09.009

AppendixAppendix 1:

The interview guide

Interviewer: BENHAYOUN ISSAM Date: ../…/2022

Acknowledgment for the interest shown in this study and Verification of the time allocated to the researcher.

Permission to reference the company? Authorization for recording? Alternatively, note-taking.

Introduction of the researcher:

An Assistant Professor of Accounting and Taxation in ENCG- Moulay Ismail University of Meknes and Part-Time Faculty of Accounting and Finance in The School of Business Administration of Al Akhawayn University of Ifrane.

Demonstrating interest in IFRS for SMEs research and particularly focusing on their adoption in Morocco.

Morocco is currently in its preliminary phase of amending its GAAP with the aim of aligning it with new international economic and financial developments. Indeed, during the 2nd Accounting Symposium held in June 2013 in Skhirat, the Moroccan authorities notably expressed their intention to converge it with international standards.