?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examined how female leadership, board communication, independent third-party assurance, and sustainability disclosure quality are interconnected in Nigerian listed firms. Using data from the top 100 firms on the Nigerian Exchange (NGX) Group from 2013 to 2022, comprising 1000 observations, the study evaluates its hypotheses. Employing a panel regression analysis with the Random Effect (RE) robust estimation technique, the findings demonstrate that female leadership, board communication, and external assurance positively and significantly impact sustainability disclosure quality. This suggests that having women in leadership roles, fostering effective board communication through shared membership, and obtaining independent (external) assurance for sustainability disclosures enhance the quality of such reports. The robustness of the results is confirmed by the One-Year Lag Effect, which aligns with the outcomes of the main model. This positive correlation signifies an enhancement in the quality of sustainability disclosures within Nigeria. However, there is room for improvement, as indicated by descriptive statistics revealing a 20% level of sustainability disclosure quality. This study underscores the need for regulators, firm management, and stakeholders to bolster compliance with sustainability reporting standards and guidelines, exerting pressure to elevate disclosure quality. In addition, the research fills gaps in the literature by providing fresh empirical evidence and insights regarding the significance of female leadership, board communication, and external assurance in shaping sustainability disclosure quality among Nigerian listed firms.

1. Introduction

Corporate entities typically seek to maximize profit and shareholder wealth at the expense of people and the environment (Tiamiyu et al., Citation2021). This is because the urge to generate and maximize profit appears to trump sustainability (i.e., economic, environmental, and social [EES]) repercussions of firms’ operational actions (Tiamiyu et al., Citation2021). Financial information focuses on the economic performance of reporting firms, with little or no attention paid to non-financial activities that affect the host community and society as a whole (Wang, Citation2017). The absence of a focus on sustainability performance and information disclosure causes financial information to lose credibility and is perceived as incomplete (Tiamiyu et al., Citation2021). As a result, Elkington (Citation2013) emphasized that business performance should not be judged solely by financial reporting content but should also include companies’ sustainability performance.

Consequently, the purpose of sustainability reporting is to strike a balance between financial and non-financial performance in terms of economic and sustainable development (Elaigwu et al., Citation2020). For example, in a situation in which firms strive to maximize shareholder wealth, they should not take the negative impact of their business activities on the environment, people, and society at large for granted (Gherghina & Simionescu, Citation2015; World Commission on Environment & Development, Citation1987). Consequently, sustainability reporting has become a global phenomenon in corporate practices, which emerging economies cannot afford to ignore if sustainable development is to be accomplished (Elaigwu et al., Citation2024). This is because the world is threatened by sustainability challenges, and the existence of man on the planet has become a source of concern in many emerging economies.

For example, increased global sustainability threats, as enshrined in the United Nations Sustainable Development Goals in terms of negative effects of firm operations, are a source of concern for various stakeholders who request more comprehensive corporate information outside financial reporting (Abdulsalam & Babangida, Citation2020; Anazonwu et al., Citation2018; Sanusi & Sanusi, Citation2019). These sustainability issues concern climate change, ozone layer depletion, pollution, desertification, various types of emissions, biodiversity loss, and an increase in poverty, inequality, hunger, and a slew of others that are detrimental to survival (AbdulKareem et al., Citation2021; Al-Dhamari et al., Citation2022; Talab et al., Citation2023). Meanwhile, firms’ active sustainability performance disclosure of the aforementioned sustainability issues is insufficient, as the quality of such disclosures is critical to sustainable development.

Therefore, analyzing the Sustainability Disclosure Quality (SDQ) of Nigerian listed firms reveals an evolving landscape in corporate transparency and responsibility (Erin et al., Citation2022). While Nigeria’s regulatory framework emphasizes sustainability reporting, the quality and depth of disclosures vary significantly among companies. Adeyemi et al. (Citation2020) noted that, although there is an increasing trend in the number of firms disclosing sustainability information, the quality of these disclosures remains a concern. Several factors contribute to the varied quality of sustainability disclosure among Nigerian listed firms. For instance, inadequate regulatory enforcement and reporting standards play a pivotal role. Despite the Securities and Exchange Commission (SEC) Nigeria’s efforts to mandate sustainability reporting through the Nigerian Code of Corporate Governance (2018), compliance lacks uniformity across industries and firms (Okoye, Citation2021).

Moreover, the lack of standardized reporting frameworks tailored to Nigeria exacerbates this issue. Although global standards such as the Global Reporting Initiative (GRI) and the Sustainability Accounting Standards Board (SASB) exist, their alignment with local needs and priorities remains a challenge (Uadiale & Fagbemi, Citation2019). The lack of stakeholder engagement is another critical factor in sustainability disclosure quality. Firms often struggle to identify and prioritize stakeholders’ interests and concerns, leading to superficial or generic disclosures that lack substance (Akinbode et al., Citation2021). In addition, sustainability reporting quality research has received less attention in the Nigerian context and remains a gray area for investigation (Anazonwu et al., Citation2018; Odoemelam & Okafor, Citation2018; N. P. Osazuwa et al., Citation2017; Sanusi & Sanusi, Citation2019).

Given the aforementioned concerns and deficiencies in governance, ethical practices in business, and regulatory frameworks, sustainability disclosures in emerging economies have often been perceived as lacking quality (Elaigwu et al., Citation2024; Katmon et al., Citation2019). This observation prompted an investigation of the SDQ in Nigeria. Therefore, this study aims to assess the SDQ of listed firms in Nigeria, with a specific focus on significant governance attributes, such as female leadership, board communication, and external assurance, which, to the best of our knowledge, have not been analyzed together in our context. We chose to analyze these variables, as they are believed to be fundamental determinants of Sustainability Disclosure Quality (SDQ).

This study examines female leadership roles as opposed to gender diversity in the spirit of tokenism and critical mass assumptions (Rao & Tilt, Citation2016; Zhuang et al., Citation2018), focusing on women in positions such as CEO, board chairs, board committee chairs, and other strategic positions that are uncommon in the sustainability reporting literature on emerging economies. This is because the female leadership role in corporate organizations requires attention to showcasing female talent in strategic positions (Aluwong & Fodio, Citation2019; Moreno-Gómez et al., Citation2018), which could lead to more effective decisions based on the cognitive variety of the teams, which could improve the SDQ (Al-Shaer & Zaman, Citation2016; Klein, Citation2017). Similarly, board communication is explored in this study through the lens of overlapping membership, which may lead to successful information management (Moreno-Gómez et al., Citation2018). Such information management is especially important when the board’s makeup is substantially diversified as it reduces knowledge asymmetry (Samuel et al., Citation2019). Furthermore, board communication (overlapping membership) has received the least attention in sustainability reporting research as it is primarily focused on firm value and financial reporting quality (Kalelkar, Citation2017; Sassen et al., Citation2018; Velte, Citation2017). Furthermore, the Global Reporting Initiative (GRI-G4) emphasizes the importance of the external assurance of sustainability reporting, although it is not mandatory. Meanwhile, there has been little research on the external assurance of sustainability disclosures in Nigeria, as in many other emerging nations. Therefore, because of the importance of external assurance for sustainability reporting regarding the quality of disclosures, the current study felt it was timely to evaluate the Nigerian scenario.

The study employed panel regression (Random Effect) using content analysis and found a significantly positive association between female leadership, board communication, external assurance, and SDQ. The study has practical and theoretical implications for listed firms, stakeholders of firms, government, and future sustainability research. The remainder of this paper is structured as follows: Section 2 covers the literature review and theoretical background, Section 3 presents the development of hypotheses, and Section 4 discusses the methodology. Sections 5 and 6 present the results and conclusions, respectively, while Section 7 presents the limitations of the study.

2. Regulatory background of the Code of Corporate Governance in Nigeria

It is obvious that the rise in industries such as refineries and breweries, as well as the increase in environmental impacts, has created serious sustainability issues. Consequently, the urgent regulation of these activities without extinguishing the prospects of these sectors is therefore required (Osazuwa et al., Citation2015, Citation2017). The Nigerian government has put in place policies via the revised Nigerian Code of Corporate Governance (NCCG) 2018 and its emphasis on sustainability and enacted laws (Federal Ministry of Environment, Environmental Impact Assessment Act, and other Acts) that are supposed to address in totality sustainability issues (Financial Reporting Council of Nigeria (FRC),), Citation2018). The issue of whether this policy is being adhered to is a subject of debate (Ozili, Citation2021). There are indeed legislations and strategies in place to protect the existing facilities ensure they meet international standards and requirements, and ensure the citizens have the best possible conditions for optimum health and wellbeing (Osazuwa et al., Citation2015). The policies for environmental management range from enactments in the constitution, and international treaties to environment and resource protection laws (Osazuwa et al., Citation2017).

The background of the code for corporate governance in Nigeria can be traced to the 1990s when several corporate governance issues such as overvaluation and concealment of indebtedness level by some companies and the collapse of some banks led to the need for a code of corporate governance (Osazuwa, Citation2016). In 2003, the Securities and Exchange Commission (SEC) under the chairmanship of Atedo Peterside set up a committee to address the issue of corporate governance known as the Peterside commission on corporate governance of companies (Osazuwa, Citation2016). The committee came up with its report in 2003. However, despite the code of 2003, several companies still experienced weak governance systems which led to a series of corporate failures and distorted the economy (Aina, Citation2013). In 2008, with the dawning of the global financial meltdown that rocked the world economy and the lessons learned, the commission set up another committee to review the 2003 code and cater to its perceived weakness, and also inculcate ways of ensuring compliance following the international best practices (Osazuwa, Citation2016). This was a timely intervention as many companies were facing collapse due to weak governance and risk structures at the time. This led to the establishment of the revised code of corporate governance for listed companies in 2011 (Securities and Exchange Commission (SEC); Citation2011) and 2018 (Financial Reporting Council of Nigeria (FRC),), Citation2018).

Therefore, corporate governance regulations play a pivotal role in shaping the business landscape of any country, ensuring transparency, accountability, and responsible decision-making within corporations. In Nigeria, the regulatory framework governing corporate governance has undergone significant evolution, particularly concerning board gender diversity and corporate social responsibility (CSR) practices. The CAMA 2020Footnote1 represents a landmark overhaul of Nigeria’s corporate governance framework. It introduces provisions aimed at enhancing board diversity and accountability. Section 849 mandates public companies to have a minimum of 30% female representation on their boards. Non-compliance may result in penalties or fines. Besides, the Nigerian Code of Corporate Governance (NCCG) 2018 provides guidelines for corporate governance practices in Nigeria. It emphasizes the importance of gender diversity on boards as a means to improve decision-making and corporate performance. The code recommends that companies strive for gender balance in their board composition, encouraging diversity in skills, experience, and perspectives (Financial Reporting Council of Nigeria (FRC),), Citation2018). Moreover, the SECFootnote2 plays a crucial role in regulating corporate governance practices in Nigeria’s capital market. It requires listed companies to disclose their board diversity policies and report on their compliance with gender diversity objectives. Additionally, SEC guidelines encourage companies to integrate CSR initiatives into their business strategies, ensuring sustainable development and stakeholder value creation.

3. Theoretical background and hypotheses development

3.1. Theoretical background

The concept of sustainable development, spearheaded by the United Nations, gained prominence in 1987 with the publication of the Brundtland report at the United Nations conference known as "Agenda 21" in Rio de Janeiro (Tiamiyu et al., Citation2021). By 1992, within a span of fewer than five years, 178 countries had embraced a comprehensive action plan labeled "Agenda 21" during the UN Conference on Environment and Development (Tiamiyu et al., Citation2021). The impetus for sustainability reporting arose from societal concerns regarding the sustainability of the human economic system, where the exponential growth of the population poses significant threats to the biophysical carrying capacity of the planetary ecosystem, as underscored by the American Accounting Association (Tiamiyu et al., Citation2021).

At times, the term "sustainability reporting" is used interchangeably with "corporate social responsibility" (Aziz & Rosmiza, Citation2017; Elaigwu et al., Citation2020). Nevertheless, research indicates that while companies in advanced economies often utilize corporate social responsibility to safeguard their reputation, sustainability reporting offers burgeoning economies boundless growth opportunities (Tiamiyu et al., Citation2021). For instance, Dyduch and Krasodomska (Citation2017) suggest that the global financial crisis of 2008 led to an upsurge in demand for more comprehensive and detailed reports, either in the form of sustainability or corporate social responsibility concepts, to rebuild confidence among investors and consumers in the market. In contrast, Lys et al. (Citation2015) argue that corporate sustainability transcends environmental concerns, corporate social responsibility, and strategic philanthropy. Instead, it embodies an awareness of stakeholders’ interests, aiming to ensure economic viability, while upholding social responsibility and environmental sustainability.

The discussion of the World Commission on Environment and Development (WCED) in 1987 emphasized the relevance of sustainability practices and indicated that the future is as important as the present regarding the preservation of resources (World Commission on Environment & Development, Citation1987). The importance of the future is portrayed in the definition of sustainable development provided by the WCED. The report officially states that sustainable development (sustainability) “is the development that meets the present needs without denying the future generations the opportunity to meet their own needs” (World Commission on Environment & Development, Citation1987). Sustainability, as defined by the WCED, has gained acceptance in several previous studies on sustainability practices. Sustainability is defined as the calculation of sustainable development that brings forth the idea of sustainability reporting (Deegan, Citation2013; Guenther et al., Citation2006; Guthrie & Abeysekera, Citation2006). Following the above definition of sustainability, a non-profit organization, the Global Reporting Initiative (GRI) defined sustainability reporting as “reporting on how an organization contributes or aims to contribute in the future, to the improvement or deterioration of economic, environmental, and social conditions, developments, and trends at the local, regional, or global level” (Global Reporting Initiative (GRI), Citation2015, p. 17). The GRI emphatically suggests that the sustainability concept is widely presented in such a way that “it involves discussing the performance of the organization in the context of the limits and demands placed on environmental or social resources at the sector, local, regional, or global level” (Global Reporting Initiative (GRI), Citation2015).

Based on the relevance of sustainability, as shown by the various definitions and the UN Sustainable Development Goals (SDGs), stakeholders have communicated sustainability information through the sustainability reporting medium as a newly formalized mode of communication (Fernandez-Feijoo et al., Citation2018; Gnanaweera & Kunori, Citation2018; Schaltegger & Wagner, Citation2006). The essence of communicating sustainability information is to enhance stakeholders’ investment decisions by meeting their information needs, thereby legitimizing firms’ operations (Deegan, Citation2013; Lock & Seele, Citation2016). However, achieving impactful sustainability reporting practices left the board of directors with huge responsibility via the board’s governance mechanisms. This portrays the idea of using governance elements to encourage firms to engage in sustainable practices to enhance the green environment through resource conservation (Cooke, Citation2015). Following previous Nigerian sustainability reporting literature (e.g. Abdulsalam & Babangida, Citation2020; Odoemelam & Okafor, Citation2018; Ofoegbu, Odoemelam & Okafor, Citation2018; Osazuwa et al., Citation2017) the present study employs salient board governance elements, such as board independence and board size, to examine the sustainability disclosure quantity of the top 100 listed companies in Nigeria. The study is premised on a theoretical framework based on agency, stakeholder, and legitimacy theories to explain the link between the variables of interest and the SDQ.

Agency theory focuses on information asymmetry between a firm and its various stakeholders and posits that such asymmetry can be reduced by monitoring and controlling the responsibility of the board (Fama & Jensen, Citation1983; Jensen & Meckling, Citation1976). The theory has been well operationalized in sustainability reporting literature and documented that asymmetric information could be ameliorated through firms’ sustainability disclosures (Clarkson et al., Citation2008; Martínez-Ferrero et al., Citation2015). Sustainability disclosure is a communication tool that ameliorates the information asymmetry that may exist between company management and stakeholders (Fama & Jensen, Citation1983; Reverte, Citation2012).

Therefore, agency theory provides a lens through which we can understand the dynamics between principals (shareholders) and agents (management) within organizations, particularly in the context of decision-making and governance. In the realm of sustainability disclosure, agency theory helps illuminate how female leadership, overlapping membership, and external assurance intersect to influence the quality of disclosures. The theory posits that the presence of female leaders may enhance board monitoring and governance effectiveness, leading to improved transparency and disclosure quality (Adams, Citation2015). From an agency theory perspective, overlapping membership can either enhance or diminish governance effectiveness. On one hand, it can facilitate information sharing, coordination, and collective decision-making across different organizational entities, thereby improving oversight and accountability. On the other hand, it may raise concerns about conflicts of interest, divided loyalties, and the potential for managerial entrenchment (Fama & Jensen, Citation1983). Also, agency theory suggests that external assurance can mitigate information asymmetry between principals and agents by enhancing the credibility, reliability, and objectivity of disclosed information (Deegan, Citation2002). By providing an external check on management assertions, assurance mechanisms strengthen the monitoring and control functions of corporate governance systems, thereby reducing agency costs and enhancing disclosure quality.

However, the main limitation of agency theory is that it focuses more on monetary values, with less consideration for other potential users of non-financial (economic, environmental, and social) information. Therefore, this study integrates other theories to address this gap.

Stakeholder theory suggests that firms have responsibilities not only to their shareholders but also to other parties affected by their operations (Freeman, Citation1984). This theory has been predominantly used in previous research to elucidate why firms disclose information related to sustainability practices (Şener et al., Citation2016). This emphasizes the importance of firms in effectively managing their relationships with various stakeholders to ensure their continued existence (Freeman et al., Citation2004). In essence, stakeholder theory underscores the significance of prioritizing the needs and interests of stakeholders recognized by the company’s management. Previous studies have shown that a stakeholder-oriented approach can positively impact organizational performance (Şener et al., Citation2016). Freeman (Citation1984) defines a stakeholder as ‘any group or individual who can influence or is influenced by the organization’s objectives’ (p. 46). He emphasized that responding to stakeholders’ expectations and maintaining positive relationships can provide companies with a competitive advantage for survival.

Consequently, stakeholder theory provides a robust framework for understanding the interconnectedness between female leadership, overlapping membership, external assurance, and sustainability disclosure quality within organizations. This theoretical lens emphasizes the significance of various stakeholders, including employees, customers, communities, and investors, in shaping organizational behavior and decision-making processes (Freeman, Citation1984). The presence of female leadership within an organization has been shown to positively influence sustainability practices and disclosure quality. Research suggests that female leaders often exhibit a more inclusive and collaborative leadership style, which aligns with the principles of stakeholder theory (R. B. Adams & Ferreira, Citation2009). Moreover, the concept of overlapping membership, wherein individuals serve on multiple boards or hold various positions across organizations, plays a crucial role in enhancing sustainability disclosure quality (Kusnadi et al., Citation2016). When board members or executives are involved in multiple entities, they bring diverse perspectives and experiences to the decision-making process, enabling a more comprehensive consideration of stakeholder interests (Freeman et al., Citation2004). External assurance further strengthens the link between stakeholder theory and sustainability disclosure quality. By subjecting sustainability reports to independent verification, organizations demonstrate their commitment to transparency and accountability, thereby enhancing stakeholder trust (Deegan, Citation2002).

Aligned with the principles of stakeholder theory, which posits that companies should acknowledge and address the interests of all relevant stakeholders, numerous investigations have been conducted to explore the advantages derived from meeting these stakeholder demands. One documented benefit is the financial gain experienced by shareholders when the management responds to various stakeholder demands (Ruf et al., Citation2001). Moreover, firms that commit to sustainability and disclose their efforts foster trust among stakeholders and gain a competitive edge, enabling them to thrive and remain viable (Jones, Citation1995). Chiu and Wang (Citation2015) examined the factors influencing sustainability disclosure quality and found that stakeholder influence leads to enhancements in disclosure quality. Similarly, Wang (Citation2017) observed that sustainability disclosures increased with improved board governance, in line with the stakeholder theory. Consequently, sustainability reporting practices predominantly reflect companies’ concerns for stakeholders, as they endeavor to sustain themselves. Thus, stakeholder theory serves as a fundamental framework for this study, elucidating why corporate boards prioritize sustainability reporting.

Legitimacy theory suggests that organizations consistently strive to align their operations with the norms and expectations of the societies they function in Suchman (Citation1995). From this perspective, a company would choose to disclose its activities if its management believes that such actions are anticipated by the communities it serves (Cormier & Gordon, Citation2001; Deegan, Citation2002; Rankin, Citation2012). Given the potentially severe consequences of perceived breaches in the social contract for an organization’s survival, it becomes crucial to explore the remedial measures that organizations may undertake (Elaigwu et al., Citation2024). In this context, legitimacy theory introduces the concepts of the ‘legitimacy gap’ and ‘legitimacy strategies’, which play pivotal roles in corporate sustainability practices.

Therefore, legitimacy theory provides a framework for understanding how organizations strive to maintain their legitimacy in the eyes of stakeholders by conforming to societal norms, values, and expectations. In the context of sustainability disclosure, legitimacy theory suggests that organizations disclose information about their sustainability practices to demonstrate their commitment to responsible business conduct and to maintain legitimacy in the eyes of stakeholders (Elaigwu et al., Citation2024; Suchman, Citation1995).

Female leadership has been increasingly recognized as a factor that can influence organizational behavior, including sustainability practices. Research suggests that female leaders may bring different perspectives and values to decision-making processes, leading to a greater emphasis on issues such as corporate social responsibility (CSR) and sustainability. For example, studies have shown that companies with female CEOs are more likely to prioritize sustainability initiatives and disclose more comprehensive sustainability information (R. B. Adams & Ferreira, Citation2009). The link between female leadership, overlapping membership, and external assurance to sustainability disclosure quality lies in the way these factors collectively contribute to organizational legitimacy. Female leaders, by prioritizing sustainability, set the tone for the organization’s commitment to responsible practices. Overlapping board memberships facilitate the exchange of ideas and best practices, fostering a culture of sustainability across organizations. External assurance mechanisms provide independent validation of sustainability disclosures, enhancing their credibility and reinforcing organizational legitimacy.

Upper echelon theory concerns the role of female leadership. This study uses the upper echelon theory to describe the leadership position of women in corporate hierarchies, as opposed to the critical mass theory (CMT), which has been used in most sustainability studies. The current study employs the upper-echelon theory to address the limits of critical mass by looking beyond the minimum of three women on the board to gender diversity in leadership roles (Moreno-Gómez et al., Citation2018). According to the upper-echelon theory, an organization’s performance is mostly determined by its leaders. Thus, the theory provides an empirical foundation for correlating specific aspects and diversity of corporate hierarchy with business success (Jeong & Harrison, Citation2017; Moreno-Gómez et al., Citation2018). This minimizes bias in terms of the lower outgroup for women on boards based only on critical mass (Torchia et al., Citation2011; Wiley & Monllor-Tormos, Citation2018). Furthermore, the upper echelon believes that gender is an important factor to consider when assessing the personal characteristics of executives (i.e., the top management team) that may affect organizational performance (Nishii et al., Citation2007).

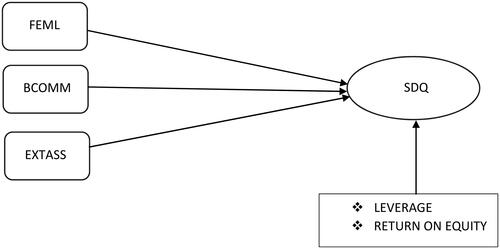

The existing body of literature on corporate governance frameworks and strategic management underscores the pivotal role of top management in shaping business conduct and outcomes (R. B. Adams et al., Citation2010). Moreno-Gómez et al. (Citation2018) found that gender diversity at the uppermost levels of the organizational hierarchy correlates with enhanced company performance. Furthermore, they noted that a greater presence of women in leadership roles contributed positively to performance, as documented by The New York Times on December 6, 2014. Similarly, research conducted in Latin America has revealed that integrating a critical mass of women into top-tier business positions yields substantial and advantageous effects on performance (Delloite, Citation2015, Citation2017). Palvia et al. (Citation2015) conveyed in their examination titled "The CEOs and Chairwomen in the USA Banking Industry" that banks led by female CEOs and/or Board Chairs exhibit lower failure rates. Liu et al. (Citation2014) identified a constructive association between female CEOs and the economic performance of publicly listed Chinese enterprises. Consequently, this study adopts the upper-echelon theory to elucidate how leadership by female directors can engender high-quality sustainability reporting. The theoretical framework is illustrated in .

Figure 1. Theoretical framework.

3.2. Development of hypotheses

3.2.1. Female leadership and SDQ

Friedman (Citation2007) argues that participation in sustainability reporting could reveal an agency problem. In other words, the agent’s interests conflict with those of the principal. In such a case, agents may use sustainability reporting to benefit themselves at the expense of shareholders (Friedman, Citation2007; Jensen & Meckling, Citation1976). According to agency theory, board effectiveness in terms of control is critical, because it pushes corporations to be more accountable for sustainability policies (Jo & Harjoto, Citation2011). Meanwhile, this study examines gender leadership diversity in the corporate hierarchy (executive roles–the boardroom or top management) as opposed to the token or critical mass of female participation on the board of directors (Moreno-Gómez et al., Citation2018; Wiley & Monllor-Tormos, Citation2018). This is because women’s leadership roles in corporations highlight their talent in executive positions (Kota, Citation2019; Moreno-Gómez et al., Citation2018). Consequently, women in corporate high echelons contribute to team diversity in terms of both human capital and social structure. This viewpoint is consistent with the upper-echelon theory proposed by Hambrick and Mason (Citation1984) and Kanter (Citation1977). According to upper-echelon theory, the presence of women in leadership roles contributes to the success of companies, as the organization reflects the qualities of its leaders (Hambrick & Mason, Citation1984; Hambrick, Citation2007; Moreno-Gómez et al., Citation2018). This is supported by previous research indicating that women tend to be more risk-averse than men (Palvia et al., Citation2015), possess superior monitoring skills (R. B. Adams & Ferreira, Citation2009), and exhibit strategic and long-term orientations (Reguera-Alvarado et al., Citation2017). These characteristics contribute to the exchange of information, foster effective business operations, and ultimately improve organizational performance (Moreno-Gómez et al., Citation2018; Van Knippenberg et al., Citation2004). It is noteworthy that women’s leadership style has a direct impact on strategic processes, corporate culture, and consequently, business performance (Moreno-Gómez et al., Citation2018; Tang et al., Citation2011).

Additionally, Rosener (Citation1996) highlighted that women’s leadership approaches tend to be more participative, fostering encouragement and inclusivity, thereby promoting the exchange of input and information among team members. The author emphasizes that women in leadership roles are recognized as maintaining open lines of communication with stakeholders, displaying a collaborative and democratic approach to business management compared to their male counterparts (Ravasi & Schultz, Citation2006; Tang et al., Citation2011). Palvia et al. (Citation2015) observed that companies led by female CEOs and board chairs have a lower likelihood of failure, while Liu et al. (Citation2014) identified a positive correlation between female CEOs and Chairwomen and firm performance. Furthermore, Moreno-Gómez et al. (Citation2018) established a positive and significant connection between gender diversity in top corporate positions and overall firm performance. Moreover, legitimacy theory suggests that a proficient board contributes to sustainability disclosures, legitimizing the existence and survival of firms. The presence of women in roles such as board Chairs, CEOs, and board committee chairs may contribute to this legitimization and enhance the chances of organizational survival.

Hence, agency theory, upper echelon theory, and empirical findings collectively suggest a correlation between female leadership roles and the success of companies. Building on this premise, the current study proposes the following proposition.

H1: There is a positive and significant relationship between female leadership and SDQ in Nigeria.

3.2.2. Board communication and SDQ

Effective board communication is vital when there is an overlap in membership, especially on diverse boards (Samuel et al., Citation2019). This research aligns with agency theory, asserting that the quality of corporate reporting improves through effective communication facilitated by overlapping board memberships, addressing information asymmetry (Jensen & Meckling, Citation1976). Additionally, from a stakeholder theory perspective, which is intricately tied to non-financial firm performance, boards with effective communication and information management contribute to the legitimacy and long-term survival of firms through sustainability disclosures (Freeman et al., Citation2004; Freeman, Citation1984). Stakeholder theory emphasizes that organizations should consider the interests of all relevant stakeholders, extending beyond shareholder decision-making. This theory advocates accountability to a broader range of stakeholders, including employees, customers, communities, and the environment (Freeman, Citation1984) which is also in tandem with assumptions of the legitimacy theory with regard to social contract (Suchman, Citation1995). Sustainability reporting, which involves disclosing a company’s economic, social, and environmental performance, serves as a crucial mechanism for demonstrating accountability to stakeholders. Therefore, companies with overlapping directorships may opt for sustainability reporting to enhance their legitimacy by showcasing commitment to environmental, social, and governance (ESG) issues in the eyes of stakeholders.

The empirical data indicate a correlation between board communication and corporate disclosure. Fernández Méndez et al. (Citation2017) demonstrated the positive impact of overlapping directorships on financial reporting quality. Habib and Bhuiyan (Citation2016) observed that companies with overlapping committee members exhibit superior financial reporting quality compared to those without such an overlap. Similarly, Velte (Citation2017) concludes that shared membership in audit and compensation committees enhances the overall quality of corporate reporting. The favorable connection highlighted in the existing literature is attributed to the positive effects of overlapping memberships on expertise, knowledge sharing, and enhanced monitoring capabilities of the board (Habib & Bhuiyan, Citation2014, Citation2016).

Hence, considering the earlier discourse on the correlation between board communication (overlapping directorship) and the quality of firms’ financial reporting, this study opts to similarly explore its connection with sustainability reporting. It asserts that:

H2: There is a positive and significant relationship between board communication and sustainability reporting quality.

3.2.3. External assurance and SDQ

The focal point of sustainability reporting practice lies in the revelation of trustworthy and credible information regarding sustainability performance, as advocated by Braam et al. (Citation2016) and Braam and Peeters (Citation2018), aligned with the principles of agency theory. According to agency theory, conflicts of interest arise between principals (owners) and agents (management) within organizations. The principal-agent relationship necessitates mechanisms to align interests and minimize information asymmetry (Jensen & Meckling, Citation1976). In the realm of sustainability reporting, shareholders (principals) depend on management (agents) to accurately communicate a company’s ESG performance. External assurance functions as a mechanism for addressing the agency problem by offering an independent evaluation of the reliability of sustainability disclosures. Serving as a monitoring tool, external assurance ensures that the reported sustainability information adheres to relevant standards and frameworks, is accurate, and comprehensive. Companies, by engaging external assurance providers, demonstrate their dedication to transparency and accountability, thereby addressing agency concerns.

Moreover, there is a growing demand for transparency and accountability in stakeholders’ organizational activities. External assurance aligns with these expectations by independently evaluating the reliability of the sustainability information. This alignment is crucial for building positive relationships with stakeholders and reducing the risk of skepticism or distrust, consistent with stakeholder theory principles. According to Adams (Citation2015), external assurance has a positive impact on stakeholders’ perceptions of the credibility and reliability of sustainability reports. Consequently, the presence of external assurance signifies a shared commitment to the accuracy of sustainability disclosure. This alignment narrows the information gap and decreases the likelihood of opportunistic behavior by management, in line with the agency theory framework (Deegan, Citation2013). Deegan (Citation2002) found that external assurance enhances the credibility and reliability of disclosed information and positively influences the quality of sustainability reporting. Earlier investigations, such as those conducted by Erin et al. (Citation2022), Hsueh (Citation2018), Manning et al. (Citation2019), Fernandez-Feijoo et al. (Citation2018), Braam et al. (Citation2016), and Junior et al. (Citation2014), have recognized the significance of independent third-party assurance in enhancing transparency and the quality of information in corporate sustainability reports. Drawing on agency theory, stakeholder theory, and prior scholarly works, this study proposes the following hypotheses:

H5: There is a positive and significant relationship between external assurance and sustainability reporting quality in Nigeria.

4. Methodology

4.1. Population, sample, and data

The population of the study is the entire companies (161) listed on the NGX between 2013 and 2022, which includes all sectors of the economy. The sample size constitutes the top 100 firms listed on the NGX from 2013 to 2022 making 1000 firm-year observations, as shown in . This period was chosen to enable the researcher to observe how the dispensation of President Muhammadu Buhari has shown concern for the issue of sustainability practices and to observe the effect of the Nigerian Code of Corporate Governance (NCCG) reform in 2018, which has the issue of sustainability on its top list (Ozili, Citation2021). The selection of larger firms (top 100) is determined by their market capitalization, consistent with previous studies that commonly focus on larger firms in sustainability reporting research (Talab et al., Citation2023; Kühn et al., Citation2018; Teoh & Thong, Citation1984; Zainal, Citation2017). In addition, larger firms tend to have greater public visibility, which impacts society more significantly and necessitates the legitimization of their business operations (Elaigwu et al., Citation2023; Kühn et al., Citation2018). Furthermore, larger firms are more inclined to adopt sustainability practices in response to public pressure form the public (Al-Dhamari et al., Citation2022), a trend supported by Hahn and Kühnen (Citation2013) and Haniffa and Cooke (Citation2005), who assert that a company’s size is a key determinant of extensive sustainability reporting.

Table 1. Sample selection procedure and distribution.

This study utilized secondary data spanning 2013 to 2022, primarily sourced from the annual reports of listed companies available on the NGX website. Content analysis served as the data collection method, in agreement with previous research (e.g. Al-Dhamari et al., Citation2022; Elaigwu et al., Citation2024). The annual report, recognized as a statutory report by various stakeholders (Vergoossen, Citation1993) and a vehicle for sustainability disclosure (Harte & Owen, Citation1991), was chosen for its accessibility and regular publication (Suttipun & Stanton, Citation2012). Sustainability disclosure quality data were manually extracted from the sustainability reporting section of the annual reports, consistent with the content analysis approach. Similarly, data pertaining to board governance variables, including female leadership, board communication, external assurance, and financial variables, were collected manually from various sections of annual reports, such as corporate governance statements, chairman’s statements, director’s reports, board profiles, and financial statements.

4.2. Estimation technique

This research utilized a panel regression estimation methodology to examine the relationships among female leadership, board communication, external assurance, and SDQ. We chose this approach because of its advantages, as detailed by Baltagi (Citation2005) and Asteriou and Hall (Citation2007). The measurement and description of these variables are shown in below.

Table 2. Description and measurement of variables.

4.3. Measurement of variables

4.3.1. Sustainability disclosure quality

This study developed a checklist adapted from the work of Ahmad (Citation2017) and Katmon et al. (Citation2019) following the NCCG and sustainability reporting frameworks of the Global Reporting Initiatives (GRI), see Appendix A. While Katmon et al. (Citation2019) and Ahmad (Citation2017) employed a CSR Framework, this study used a Sustainability Framework that considers three dimensions or themes (i.e., Economic, Environmental, and Social) of sustainability disclosure which is in tandem with the sustainability framework of Global Reporting Initiatives (GRI) (Global Reporting Initiative (GRI), Citation2015). The evaluation of Sustainability Disclosure Quality (SDQ) utilized an index ranging from 0 to 3, consistent with prior research (e.g., Ahmed Haji, Citation2013; Elaigwu et al., Citation2023; Erin et al., Citation2022). “A score of 3 was assigned for reports presenting both quantitative and qualitative disclosures, 2 for either quantitative or monetary disclosures, and 1 for qualitative or general statements. Reports without disclosure received a score of 0, with a maximum attainable score of 126 (42 × 3)” (Elaigwu et al., Citation2024). Consequently, in assessing the SRQ, a quality index was formulated by dividing the total scores by the number of items using the following formula:

where

is the sustainability reporting quality index for j the firm j,

is the SDQ on a scale of 0 to 3, and

is the total number of items estimated for the jth firm (

).

4.3.2. Female leadership

This study considered the Female Leadership (FEML) dimension of corporate gender diversity. This study defines gender leadership diversity based on the upper-echelon perspective theory from the perspective of female leadership roles in top executive positions. Therefore, gender leadership diversity is defined as the role of female leadership in the board or top executive position. The study measured FEML as the number of leadership positions occupied by females in a company. For example, the board Chairman, CEO, and board committee chair are against mere membership in the board or any of the board committees, as adopted in previous studies. If females occupied leadership positions (e.g. board Chair, board committee Chair, and CEO), the study scored three or more based on the number of leadership positions occupied. This accounts for the leadership effect of women in corporate management, which is in line with extant literature (Bandi, Citation2017; Moreno-Gómez et al., Citation2018; Palvia et al., Citation2015).

4.3.3. Board communication

Board communication (BCOMM) was measured by audit committee overlap, which is defined in this study as a board member serving simultaneously on more than one committee, such as compensation, audit, and nomination committees. It is measured as a percentage of overlap among committees. This agrees with prior research (Chandar et al., Citation2012; Kalelkar, Citation2017; Velte, Citation2017), which examines overlapping membership between the audit committee and the compensation committee. Board members who serve on more than one committee were first identified, and subsequently, an indication that members of the board serve concurrently on audit, compensation, and nomination committees was scored accordingly. The percentage is the total overlap divided by the total of the three board committee members, multiplied by a hundred.

4.3.4. External assurance

External assurance (EXTASS) refers to the assurance of the sampled firms’ sustainability disclosures by an independent assurer, either by an audit professional or sustainability expert. A dummy variable is measured with a score of 1 if the sustainability report of the company is assured; otherwise, it is 0. This aligns with the extant literature, such as Erin et al. (Citation2022), Elaigwu et al. (Citation2024), and Fernandez-Feijoo et al. (Citation2018).

5. Presentation of results

5.1. Descriptive statistics

illustrates the descriptive statistics for the SDQ model from 2013 to 2022. The findings reveal that the mean value for SDQ is 24%, with a range from 0 as the minimum to 65% as the maximum. Despite being relatively low, this indicates an enhancement in the sustainability disclosure level among listed firms in Nigeria, which is consistent with previous research (Erin et al., Citation2022; Ofoegbu et al., Citation2018; Sanusi & Sanusi, Citation2019). Low SDQ is also evident across various sustainability disclosure themes, with Economic Sustainability Disclosure Quality (ESDQ) at 0.06, Environmental Sustainability Disclosure Quality (ENSDQ) at 0.07, and Social Sustainability Disclosure Quality (SSDQ) at 0.11. Regarding Female Leadership (FDL), the scores ranged from 0 (minimum) to 4 (maximum), with an average value of 30%. This suggests variability in the presence of female leaders within the sampled companies, with some lacking female leaders, while others have up to four females in leadership roles during the specified period. On average, 30% of the leadership positions in the sampled companies were held by females. Board communication, as indicated by overlapping directorships, ranged from 8% to 87%, with a mean of 49%. This suggests varying degrees of overlap among board committees, similar to the patterns observed in the United States and Germany. For instance, in the United States, approximately 7% of audit committee members also serve on compensation committees (Kalelkar, Citation2017), whereas in Germany, the overlap averages around 34.5% (Velte, Citation2017). External assurance (EXTASS) has an average value of 9%, indicating that only nine percent of sustainability reports from the sampled firms underwent independent external assurance. This finding underscores the limited emphasis on external assurance among firms, contributing to the perceived low quality of sustainability disclosures.

Table 3. Descriptive statistics.

5.2. Correlation matrix

A correlation below 0.8 indicates a lack of multicollinearity (Gujarati, Citation1995). The correlation coefficient reported in falls within the range of -0.115 to 0.219, which is considered acceptable as it does not exceed 0.80 (Gujarati & Porter, Citation2004). Overall, these findings suggest the absence of multicollinearity. This conclusion is further supported by the Variance Inflation Factor (VIF) results presented in , where the mean VIF value is 1.02, which is well below the threshold of 10 commonly used for detecting multicollinearity.

Table 4. Pearson correlation.

Table 5. Results of Random Effect (RE) robust estimation technique for SDQ model.

5.3. Regression results

The relationship between FEML, BCOMM, EXTASS, and SDQ was examined using panel regression analysis. Before conducting the regression analysis, several diagnostic tests were performed to address potential issues concerning the data. A VIF of 1.02 indicates that multicollinearity is not an issue. However, the presence of first-order autocorrelation was detected through the Wooldridge test, which showed 1% significance. This result implies that a correlation exists between the error terms in the regression model. Heteroscedasticity, which refers to the unusual variance of the error terms, was also detected using the Breusch-Pagan test, which showed a significance of 1%. In addition, the study followed the panel regression rule of selecting the best estimator among the pooled, random, and fixed-effect models. The result of the Lagrangian Multiplier test (Breusch & Pagan, Citation1980) for the SDQ Model is significant at the 0.0000 level, indicating that the RE Estimation technique is more appropriate. Meanwhile, the Hausman specification test (Hausman, Citation1978) is insignificant at 0.136, indicating that the Random Effect (RE) estimation technique is more appropriate. RE Robust was used for the panel regression to address the issues of serial correlation and heteroscedasticity.

The results of the multiple regression employing RE Robust estimation techniques from 2013 to 2022 are presented in and . The regression model included three themes (i.e., economic, environmental, and social) of SDQ. The R-squared value for the SDQ model, as indicated by the main Model in , reveals that 20% of the variation in the SDQ is explained by the independent variables. The relationship between FEML and SDQ showed a highly significant and positive effect of 1%, as shown by M5, M4, and M1. This result supports Hypothesis 1, suggesting that the FEML role increases SDQ. These results indicate that BCOMM has a positive significant effect on SDQ at 5% in M5, with similar results in M2 and M1, revealing that BCOMM (overlapping directorship) enhances the quality of sustainability disclosures, which supports Hypothesis 2. Similarly, EXTASS has a significant and positive effect on SDQ at 1% in all models, showing that verifying sustainability reports by external assurers enhances the quality of disclosure, thereby confirming Hypothesis 3. We analyzed M1, M2, M3, M4, and M5 to test the individual effect of the independent variables, the combined effect of independent variables, and the whole effect of the independent and control variables which constitute the main model following the work of Nguyen et al. (Citation2021).

Table 6. Results of Random Effect (RE) robust estimation technique for ESDQ, ENSDQ, and SSDQ models.

The results of the control variables show that leverage and return on equity have a significant and positive relationship with SDQ. This indicates that larger companies with higher leverage and higher returns on equity tend to have higher-quality sustainability disclosures.

5.4. Robustness check

5.4.1. Analysis of the separate themes of SDQ

We carried out additional analysis to investigate the separate dimensions of the SDQ, specifically economic sustainability disclosure quality (ESDQ), environmental sustainability disclosure quality (ENSDQ), and social sustainability disclosure quality (SSDQ). This analysis aims to equally check the robustness of the findings obtained from the main model, as shown in . The results of the separate themes are shown in , indicating that the outcomes are similar to those of the main model, thereby demonstrating the robustness of the results of the main model.

5.4.2. One-year lag effect of independent variables on SDQ

The research delved deeper into assessing the lag effect of the independent variables on the SDQ, taking into consideration factors such as reverse causality, endogeneity, and indirect effects, which are consistent with previous studies (Setiawan et al. (Citation2021); Kontesa et al. (Citation2020). Setiawan et al. (Citation2021) highlighted that endogeneity can stem from various sources, including "unobserved errors, simultaneity, measurement bias, and reverse causality," a view also supported by Masaki et al. (Citation2017). Setiawan et al. (Citation2021) proposed that addressing simultaneity can be achieved by re-evaluating the model using one-year-lagged explanatory variables instead of contemporaneous values. Additional findings, detailed in using Random effects robust analysis, examine the one-year lag effect. These lag results are consistent with the non-lag results in , reinforcing the robustness of the primary model.

Table 7. Results of Random Effect (RE) robust estimation technique for SDQ (One-year lag).

6. Discussion and implications

6.1. Discussion

This study examined the relationship between female leadership, board communication, external assurance, and SDQ. The results indicate a positive and significant relationship between the variables of interest and the SDQ. The positive relationship between female leadership and SDQ supports the assumptions of the upper echelon theory, which links female representation in corporate hierarchies to the success of firms (Hambrick & Mason, Citation1984; Jeong & Harrison, Citation2017; Post & Byron, Citation2015). The positive result also supports the premise of the agency, stakeholder, and legitimacy theories in terms of ameliorating information asymmetry enhancing firm survival, and legitimizing firms’ operations via sustainability reporting practice as a tool for stakeholder management (Cho, Lee, & Pfeiffer Jr., 2013; Freeman, Citation1984; Jensen & Meckling, Citation1976; Suchman, Citation1995). This positive relationship is consistent with previous literature that views organizations as a reflection of their leaders (Moreno-Gómez et al., Citation2018). This is because the female gender is known to be risk-averse, has better monitoring skills, strategic, and long-term orientation (Palvia et al., Citation2015; Reguera-Alvarado et al., Citation2017); as it promotes the sharing of information for efficient business functioning and corporate performance (Moreno-Gómez et al., Citation2018) which coincides with the focus of sustainability practices. For instance, Moreno-Gómez et al. (Citation2018) found a positive and significant association between gender diversity in the top corporate hierarchy and firm performance. He argued that the female leadership style directly affects strategic processes, corporate culture, and, consequently, the financial and non-financial performance of firms. Similarly, Palvia et al. (Citation2015) find that companies with female CEOs and board chairs are less likely to fail. The author argues that gender-based behavioral differences have a positive influence on corporate decisions.

The findings also demonstrate a significant and positive correlation between board communication, characterized by overlapping directorships, and SDQ. This suggests that having directors serving on more than one committee enhances SDQ. This affirmative outcome resonates with the principles of agency and stakeholder theories, which argue that an effective board of directors mitigates the information asymmetry between management and shareholders (Chen & Jaggi, Citation2000), thereby improving the quality of sustainability disclosures (Freeman, Citation1984; Jensen & Meckling, Citation1976). Moreover, these results corroborate the descriptive analysis of board communication, which reveals that approximately 49% of board committees overlap. This underscores that overlapping directorships are a beneficial practice that bolsters the SDQ within this context.

The result of the association between board communication and SDQ is in line with prior studies that mostly looked into the association between overlapping directorships and financial reporting quality (Fernández Méndez et al., Citation2017; Habib & Bhuiyan, Citation2016; Kalelkar, Citation2017; Velte, Citation2017). These studies found a positive relationship from which Hypothesis 2 of the present study was replicated to test for sustainability reporting quality. One plausible reason could be that effective communication on a diverse board via overlapping membership is crucial for the success of the board of directors (Samuel et al., Citation2019). This is because overlapping memberships are said to have a connection with an improvement in terms of expertise and knowledge spillovers and increase the monitoring quality of the board (Habib & Bhuiyan, Citation2014, Citation2016). Moreover, board communication is said to be an essential tool for diverse board effectiveness; hence, a diverse board can only succeed if there is effective communication to ameliorate the negative impacts of diversity (Samuel et al., Citation2019). Malenko (Citation2013) observed that directors’ independence is effective, and members of the board are most likely to be properly and adequately informed in the process of board discussions only if there is an avenue for effective communication among them. Such an avenue could be overlapping membership. To this effect, Samuel et al. (Citation2019) posit that overlapping directorships enhance board communication, as overlapping directors have homophily and a tendency for collaboration. Similarly, Liao and Hsu (Citation2013) concluded that approximately 67% of sampled firms have at least one member of the audit committee serving on the compensation committee. Further, the consistency of the present result with the extant literature is evidenced by Fernández Méndez et al. (Citation2017), who found that overlapping directorships positively contribute to financial reporting quality. Similarly, Habib and Bhuiyan (Citation2016) document that companies with overlapping committee members have better financial reporting quality than those without.

The findings also indicate a positive correlation between external assurance and the SDQ, suggesting that when companies enlist independent third-party assurance providers to review their sustainability reports, it enhances the quality of sustainability disclosures. This positive correlation supports both agency and stakeholder theories, aiming to mitigate information asymmetry and ensure firm survival by improving sustainability performance and providing credible sustainability information to stakeholders (Fama & Jensen, Citation1983; Freeman et al., Citation2004). These results are in line with those of previous studies (e.g. Braam & Peeters, Citation2018; Hsueh, Citation2018; Manning et al., Citation2019). One plausible explanation is that merely publishing sustainability reports may not meet stakeholders’ expectations regarding information quality unless assurance services are employed (Junior et al., Citation2014). However, the descriptive statistics indicate a low level of assurance practices (9%) among the sampled firms, possibly contributing to the observed low disclosure quality (24%). This finding underscores the importance of external assurance for the SDQ, consistent with the standards set by the Global Reporting Initiative (GRI) and the Sustainable Development Goals of the United Nations (Abdul Latif et al., Citation2023; Weber, Citation2018).

The positive correlation between external assurance and the SDQ aligns with prior research findings. For instance, Fernandez-Feijoo et al. (Citation2018) observed a link between the enhanced quality of sustainability information disclosure and third-party (external) assurance. Junior et al. (Citation2014) suggested that both the disclosure and assurance of sustainability practices are globally recognized methods for enhancing the SDQ. Braam et al. (Citation2016) found that environmentally conscious companies utilize external assurance to enhance the quality of sustainability disclosures, aiming to bolster public confidence, foster trust among stakeholders, and gain organizational legitimacy. These scholars further theorized that, in the absence of regulations, sustainability reports may not accurately reflect a firm’s genuine commitment to addressing the adverse impacts of its operations on society. Similarly, Hsueh (Citation2018) found that independent external assurance services can help alleviate credibility gaps in sustainability reporting practices. Furthermore, Manning et al. (Citation2019) documented a positive association between third-party assurance and the SRQ.

Based on the theories and extant literature, the present study found that female leadership, board communication, and external assurance are key determinants of the SDQ.

6.2. Implications

6.2.1. Practical and policy implications

This research contributes to the existing body of knowledge by adapting a sustainability index aligned with both the Global Reporting Initiative (GRI) and the sustainability framework of the Nigerian Code of Corporate Governance (NCCG). This index assesses the economic, environmental, and social aspects of sustainability reporting by examining how the sampled firms align with the United Nations’ Sustainable Development Goals. Moreover, this study offers practical insights to listed companies, regulators, and practitioners on the significance of female leadership, board communication, and external assurance in determining the caliber of sustainability disclosures in Nigeria. Therefore, implementing policies or regulations mandating external assurance, promoting greater representation of women in leadership roles, and fostering board communication through shared directorships would significantly improve the quality of sustainability disclosures among Nigerian listed companies.

6.2.2. Theoretical implication

This research has significantly enhanced the understanding of sustainability within the context of a developing nation, such as Nigeria, where companies often prioritize shareholders over stakeholders. By scrutinizing the assumptions of the upper echelon, stakeholder, legitimacy, and agency theories, this study addresses a critical theoretical gap and provides empirical support for these theories. According to upper echelon theory, organizational behavior mirrors the characteristics of leaders. The presence of women in leadership roles, as observed in Nigeria, is positively correlated with the SDQ. Moreover, the findings align with stakeholder, agency, and legitimacy theories, which emphasize the importance of firms meeting stakeholders’ information needs through transparent sustainability disclosures to mitigate information asymmetry and legitimize firm operations. By examining the combined impact of these variables and theories, this study makes a valuable contribution to the existing knowledge, particularly as one of the few investigations to do so comprehensively.

7. Limitations and suggestions for future investigations

This study has certain limitations. It underscores its quantitative nature, attributing this to the subjective nature of assigning scores (3, 2, 1, and 0) to the SDQ Index. While acknowledging that subjectivity in quantitative scoring is common in research concerning SDQ, this study recognizes that relying solely on quantitative data can pose challenges that may hinder sustainability performance. Moreover, this study exclusively employs quantitative methods. Despite these limitations, we assert the relevance and timeliness of our research in Nigeria, where sustainability reporting plays a crucial role in the public interest. Future research should address these limitations identified in this study.

Authors’ contribution

Moses Elaigwu and Ugwu, James Ike – conception, drafting of the paper, critical revision for intellectual content; Abdelkader Alghorbany and Ogechukwu Maria Ngwoke – Design, data cleaning, data analysis, and interpretation. Alexander Onyebuchi Ude, Obani Chimaobi Desmond, and Peter Audu – Data collection.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

I utilized data from companies’ annual reports listed on the Nigerian Exchange Group (NGX) between 2013 and 2022. The authors confirm that the data of this study are available from Listed Companies - Nigerian Exchange Limited (nxggroup.com)

Additional information

Notes on contributors

Moses Elaigwu

Moses Elaigwu is a Senior Lecturer at the Department of Accounting, Kogi State University, Anyigba, Kogi State, Nigeria. His research area focuses on corporate governance and corporate sustainability reporting.

James Ike Ugwu

James Ike Ugwu is a Senior Lecturer at the Department of Accounting, Faculty of Management Sciences, Prince Abubakar Audu University, Nigeria. His area of specialization Public Sector Accounting and Finance and corporate governance.

Abdelkader Alghorbany

Abdelkader Alghorbany is an Assistant Professor at the Department of Management, University of Oran 1, Oran, Algeria. The research area focuses on corporate governance and auditing.

Ogechukwu Maria Ngwoke

Ogechukwu Maria Ngwoke is a Postgraduate Student University of Canada, West British Columbia, Canada. His research area focuses on Taxation and Corporate governance

Alexander Onyebuchi Ude

Alexander Onyebuchi Ude is an Associate Professor at Dept of Accounting, Faculty of Management Sciences, Prince Abubakar Audu University, Nigeria. His area of specialization: Corporate governance, oil and gas, public sector accounting.

Obani Chimaobi Desmond

Obani Chimaobi Desmond is a lecturer at the Department Of Accountancy, Caritas University, Amorji Nike, Enugu, Nigeria, area of specialization: performance Management (Management Accounting)

Peter Audu

Peter Audu Lecturer at the Department of Business Administration, Faculty of Management Sciences, Prince Abubakar Audu University, Nigeria. His research area focuses on Human resources management and corporate governance

Notes

1 Companies and Allied Matters Act 2020. Nigeria: Federal Republic of Nigeria Official Gazette, 2020.

2 Nigerian Code of Corporate Governance 2018. Securities and Exchange Commission, Nigeria.

References

- Abdul Latif, R., Taufil Mohd, K. N., Kamardin, H., & Mohd Ariff, A. H. (2023). Determinants of sustainability disclosure quality among plantation companies in Malaysia. Sustainability (Switzerland), 15(4), 1. https://doi.org/10.3390/su15043799

- AbdulKareem, I. A., Elaigwu, M., & Ismail Shola, A.-T. (2021). The role of risk management, sustainability disclosure practices, and Islamic finance in Nigeria business environment. The Journal of Management Theory and Practice (JMTP), 2(4), 89–23. https://doi.org/10.37231/jmtp.2021.2.4.160

- Abdullah, S. N., Mohamad, N. R., & Mokhtar, M. Z. (2011). Board independence, ownership and CSR of Malaysian large firms. Corporate Ownership and Control, 8(2), 467–483. https://doi.org/10.22495/cocv8i2c4p5

- Abdulsalam, N., & Babangida, M. A. (2020). Effect of sales and firm size on sustainability reporting practice of oil and gas companies in Nigeria. Quest Journal of Research in Business and Management, 8(1), 1–8. https://www.questjournals.org/jrbm/v8-i1.html

- Adams, R. (2015). Myths and facts about female directors. International Finance Corporation.

- Adams, R. B., & Ferreira, D. (2009). Women in the boardroom and their impact on governance and performance. Journal of Financial Economics, 94(2), 291–309. https://doi.org/10.1016/j.jfineco.2008.10.007

- Adams, R. B., Hermalin, B. E., & Weisbach, M. S. (2010). The role of boards of directors in corporate governance: A conceptual framework and survey. Journal of Economic Literature, 48(1), 58–107. https://doi.org/10.1257/jel.48.1.58

- Adeyemi, S. B., Ogbechie, C., & Ibidunni, A. S. (2020). Corporate sustainability reporting in Nigeria: A study of listed firms. Heliyon, 6(6), e04201.

- Ahmed Haji, A. (2013). Corporate social responsibility disclosures over time: Evidence from Malaysia. Managerial Auditing Journal, 28(7), 647–676. https://doi.org/10.1108/MAJ-07-2012-0729

- Ahmad, N. (2017). Board independence and corporate social responsibility (CSR) reporting in Malaysia. Australasian Accounting, Business and Finance Journal, 11(2), 61–85. https://doi.org/10.14453/aabfj.v11i2.5

- Aina, K. (2013). Board of directors and corporate governance. International Journal of Business and Finance Management Research, 1, 21–34.

- Akinbode, S., Adegbite, E., & El Omari, S. (2021). Stakeholder engagement and corporate social responsibility disclosure: Evidence from Nigeria. Journal of Business Ethics, 170(3), 591–613.

- Al-Dhamari, R., Al-Gamrh, B., Farooque, O. A., & Elaigwu, M. (2022). Corporate social responsibility and firm market performance: the role of product market competition and firm life cycle. Asian Review of Accounting, 30(5), 713–745. https://doi.org/10.1108/ARA-07-2022-0179

- Alghorbany, A., Salau Olarinoye, A., Elaigwu, M., & Che-Ahmad, A. (2024). Does institutional investor influence information technology investment decisions and corporate performance? Cogent Business & Management, 11(1), 1–13. https://doi.org/10.1080/23311975.2024.2316280

- Al-Shaer, H., & Zaman, M. (2016). Board gender diversity and sustainability reporting quality. Journal of Contemporary Accounting & Economics, 12(3), 210–222. https://doi.org/10.1016/j.jcae.2016.09.001

- Aluwong, D. B., & Fodio, M. I. (2019). Effect of corporate attributes on environmental disclosure of listed oil and gas companies in Nigeria. European Journal of Accounting, Auditing and Finance Research, 7(10), 32–47.

- Anazonwu, H. O., Egbunike, F. C., & Gunardi, A. (2018). Corporate board diversity and sustainability reporting: A study of selected listed manufacturing firms in Nigeria. Indonesian Journal of Sustainability Accounting and Management, 2(1), 65. https://doi.org/10.28992/ijsam.v2i1.52

- Asteriou, D., & Hall, S. G. (2007). Applied econometrics (2nd ed.). Palgrave Macmillan UK.

- Aziz, N. S. A., & Rosmiza, H. B. (2017). A Review of the indicators disclosed in sustainability reporting of public listed companies in Malaysia. Journal of Human Capital Development, 10(2), 1–14.

- Baltagi, B. (2005). Econometric analysis of panel data (Chicheste (Ed.), 3rd ed.). John Wiley and Sons.

- Bandi, R. P. (2017). Leadership role for women a national survey on gender. https://doi.org/10.13140/RG.2.2.26106.08643

- Braam, G. J. M., Uit de Weerd, L., Hauck, M., & Huijbregts, M. A. J. (2016). Determinants of corporate environmental reporting: the importance of environmental performance and assurance. Journal of Cleaner Production, 129, 724–734. https://doi.org/10.1016/j.jclepro.2016.03.039

- Braam, G., & Peeters, R. (2018). Corporate sustainability performance and assurance on sustainability reports: Diffusion of accounting practices in the realm of sustainable development. Corporate Social Responsibility and Environmental Management, 25(2), 164–181. https://doi.org/10.1002/csr.1447

- Breusch, T. S., & Pagan, A. R. (1980). The Lagrange multiplier test and its applications to model specification in econometrics. The Review of Economic Studies, 47(1), 239–253. https://doi.org/10.2307/2297111

- Chandar, N., Chang, H., & Zheng, X. (2012). Does overlapping membership on audit and compensation committees improve a firm’s financial reporting quality? Review of Accounting and Finance, 11(2), 141–165. https://doi.org/10.1108/14757701211228192

- Chen, C. J. P., & Jaggi, B. (2000). Association between independent non-executive directors, family control and financial disclosures in Hong Kong. Journal of Accounting and Public Policy, 19(4–5), 285–310. https://doi.org/10.1016/S0278-4254(00)00015-6

- Chiu, T. K., & Wang, Y. H. (2015). Determinants of social disclosure quality in Taiwan: An application of stakeholder theory. Journal of Business Ethics, 129(2), 379–398. https://doi.org/10.1007/s10551-014-2160-5

- Cho, S. Y., Lee, C., & Pfeiffer, Jr., R. J. (2013). Corporate social responsibility performance and information asymmetry. Journal of Accounting and Public Policy, 32(1), 71–83. https://doi.org/10.1016/j.jaccpubpol.2012.10.005

- Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2008). Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organizations and Society, 33(4–5), 303–327. https://doi.org/10.1016/j.aos.2007.05.003

- Cooke, P. (2015). Green governance and green clusters: regional & national policies for the climate change challenge of Central & Eastern Europe. Journal of Open Innovation: Technology, Market, and Complexity, 1(1), 1–17. https://doi.org/10.1186/s40852-015-0002-z

- Cormier, D., & Gordon, I. M. (2001). An examination of social and environmental reporting strategies. Accounting, Auditing & Accountability Journal, 14(5), 587–617. https://doi.org/10.1108/EUM0000000006264

- Deegan, C. (2002). Introduction: The legitimising effect of social and environmental disclosures – a theoretical foundation. Accounting, Auditing & Accountability Journal, 15(3), 282–311. https://doi.org/10.1108/09513570210435852

- Deegan, C. (2013). Financial accounting theory (N. S. North Ryde (Ed.), 4th ed.). McGraw-Hill Education.

- Delloite. (2015). Diversidad en los Consejos de Administraci?on, Boletín de Gobierno Corporativo. Invierno. 2(Enero de 2015).

- Delloite. (2017). Mujeres en los Consejos de Administraci?on: Una Perspectiva Global. https://www2.deloitte.com/content/dam/Deloitte/mx/Documents/risk/Gobierno-Corporativo/2017/Mujeres-en-Consejos-Administracion-2017.pdf

- Dyduch, J., & Krasodomska, J. (2017). Determinants of corporate social responsibility disclosure: An empirical study of Polish listed companies. Sustainability, 9(11), 1934. https://doi.org/10.3390/su9111934

- Elaigwu, M., Abdulmalik, S. O., & Talab, H. R. (2024). Corporate integrity, external assurance and sustainability reporting quality: evidence from the Malaysian public listed companies. Asia-Pacific Journal of Business Administration, 16(2), 410–440. https://doi.org/10.1108/APJBA-07-2021-0307

- Elaigwu, M., Abdulmalik, S. O., Alghorbany, A., & Che-Ahmad, A. (2024). Sustainability reporting quality in Malaysia: The intricacy of family controlled and politically connected firms. Corporate Social Responsibility and Environmental Management, 1–21. https://doi.org/10.1002/csr.2799

- Elaigwu, M., Che-Ahmad, A., & Abdulmalik, S. O. (2020). Board governance mechanisms and sustainability reporting quality: A theoretical framework. Cogent Business & Management, 7(1), 1771075. https://doi.org/10.1080/23311975.2020.1771075

- Elaigwu, M., Che-Ahmad, A., & Abdulmalik, S. O. (2023). Auditor choice, audit partner busyness, and sustainability reporting quality. Afro-Asian Journal of Finance and Accounting, 13(6), 735–758. https://doi.org/10.1504/AAJFA.2023.134699

- Elkington, J. (2013). Enter the triple bottom line. In The triple bottom line (pp. 23–38).

- Erin, O., Adegboye, A., & Bamigboye, O. A. (2022). Corporate governance and sustainability reporting quality: evidence from Nigeria. Sustainability Accounting, Management and Policy Journal, 13(3), 680–707. https://doi.org/10.1108/SAMPJ-06-2020-0185

- Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. The Journal of Law and Economics, 26(2), 301–325. https://doi.org/10.1086/467037

- Fernández Méndez, C., Arrondo García, R., & Pathan, S. (2017). Monitoring by busy and overlap directors: an examination of executive remuneration and financial reporting quality. Spanish Journal of Finance and Accounting / Revista Española de Financiación y Contabilidad, 46(1), 28–62. https://doi.org/10.1080/02102412.2016.1250345