?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The purpose of this research is to investigate the effects of financial decision behavior on firm performance of Indonesian public companies using panel data. The dynamic generalized method of moment is utilized in this study. The results show that firm performance is dynamic in nature, which indicates that last year performance affects current performance significantly. Empirical result of financial decision behavior shows that investment, leverage, and dividend per share (DPS) have significant impact on firm performance. Specifically, investment has negative impact on firm performance. Meanwhile leverage has negative effects on return on assets (ROA), but positively affects Tobin’s Q. Moreover, DPS positively affects ROA and Tobin’s Q. This finding suggests that investment decision of Indonesian firms is overinvestment, indicated with higher investment affects firm performance negatively. Similarly with leverage, the finding reveals that Indonesian public companies borrowed external fund more than they required (overleverage). The positive effect of DPS on firm performance implies that dividends payout to shareholders create good signal to the market, in which managers uses dividend to deliver private information to the market. However, based on the coefficient of financial decision variables, the impact is more on the market performance and less on the accounting performance.

Public Interest Statement

Firm management has an important role to increase firm profitability and maximize shareholders’ wealth. Hence, managers should act on behalf of shareholders’ interest to enhance firm performance. Generally, the financial performance measures are categorized into the accounting-based and the market-based measures. Firm performance is determined by various factors, of which that the internal and external factors play an important role in determining firm performance. Thus, financial decision behavior; such as investment, financing decision, and dividend policy becomes important role for managers in allocating fund resources. Firms with higher internal fund tend to overinvest in unprofitable investment instead of paying dividend to shareholders. The results of this research show that firm performance is dynamic in nature, indicates that last year performance has impact on current performance. Investment, leverage, and dividend policy become important factors that determine firm performance. However, the impacts are more on the market performance and less on the accounting performance.

1. Introduction

This study deals with an important issue in corporate finance, in which we investigate the dynamic firm performance and financial decision behavior. Even though most of prior studies of firm performance and financial decision have been done, but still interesting to be analyzed and discussed, in fact that a firm periodically makes three major important financial policies that determine the value of firm. Firm performance is associated with the concepts of productivity, efficiency, and effectiveness of corporate management in utilizing resources optimally (Tan & Wang, Citation2010). These concepts correlated to the size of the firm: A small firm is more efficient than a large firm due to the former’s absence of agency problems, flexibility, and nonhierarchical structure (Halkos & Tzeremes, Citation2007). Past studies proposed that Indonesia firms had good market performance, which recoded the average of Tobin’s Q was valued at 1.13% for period 2009 to 2013 (Nikolaus, Citation2015), and the profitability (return on assets -ROA) of manufacturing firm was valued at 12.69% (Bambang Sudiyatno, Puspitasari, & Kartika, Citation2012). Hence, financial decision policy plays an important role to enhance firm performance.

The value of firm is determined by investment decision (Fama, Citation1978), although in perfect capital market investment decision is independent of the financial structure. This is because external funds serve as a perfect replacement for internal capital (Modigliani & Miller, Citation1958). In contrast, empirical research shows that internal and external capitals do not perfectly substitute each other in the short run, meaning that investment should be dependent on financial factors, so that both investment and financing decisions are interdependent in imperfect capital market, and the debt financing influences value of the firms (Modigliani & Miller, Citation1963). Additionally, several earlier studies on investment decisions have been widely discussed in relation of the cash flow and investment level to analyze the problems of over- and underinvestment (Fazzari, Hubbard, & Petersen, Citation1988; Hubbard, Citation1998; Kaplan & Zingales, Citation1997), the overinvestment occurs when firms have excess internal funds (Jensen, Citation1986). Empirical studies of Indonesian firms found that investment has negative effect on firm performance but not significant (Bambang Sudiyatno et al., Citation2012). Another issue is the global financial crisis impacted the economic and manufacturing firms turn to lower investment and capital market confidence plunged significantly (Djaja, Citation2009).

Regarding financing decision, the issues occur when companies assess their financial needs, their borrowing capacity and their ability to generate shareholder returns and maximize the firm value. Therefore, financing decision and policy to raise financial resources are among very important considerations. The consequence of higher leverage, firm may suffer agency cost and bankruptcy. Therefore, financial leverage and firm performance have negative relationship (Jensen & Meckling, Citation1976; Myers, Citation1977). However, some researchers argue that financial leverage and firm performance have positive relation because debt financing implies a commitment on managers to payout more cash, and discipline managers by restricting the amount of free cash flow (FCF) under their control (Jensen, Citation1986). In Indonesia, the level of leverage is highest for the period 2005–2011, which shows the average debt-to-equity ratio has valued at 57% in various industry sector (Hardiyanto, Achsani, Sembel, & Maulana, Citation2014).

Lastly, dividend policy issue of firm performance, in which dividend itself having implicit private information and is a signaling device to influence stock price (Bhattacharya, Citation1979; John & Williams, Citation1985; Miller & Rock, Citation1985). Thus, when a firm announces an increasing dividend, it is a sign of good news in the capital market with positive reaction of share price. Therefore, only good performance firms can send signals to the market using dividends. However, dividend policy appears to have a matter in firm behavior, in this case, the issue of why the firm should pay dividends or hold dividend payout is still unresolved. This is due to the fact that many listed companies in Indonesia do not pay dividends regularly. One explanation is that the firm is deferring dividend payments because the firm needs more funds to finance its investment specifically during the financial crisis. In Indonesia, the propensity of the firm to pay dividend has decline over time and dividend life cycle explains well the dividend policy (Leo Indra Wardhana, Tandelilin, Wayan Nuka Lantara, & Junarsin, Citation2014).

Accordingly, we argue corporate financial decision as important factors affect firm performance. Although most studies have been conducted in many perspectives, phenomena and empirical evidence, such as studies of corporate finance behavior, equity, leverage, total market share, investment ratio, growth, profitability, size, and corporate governance (Babatunde & Olaniran, Citation2009; Burca & Batrinca, Citation2014; Fauzias Mat Nor, Azlan, & Hasimi, Citation2011; Liow, Citation2010; Mirza & Javed, Citation2013; Nikolaus, Citation2015). These findings provided the mixed results and still inconclusive, possibly because they used different measurements, time dimension, and firm effect. Therefore, this study aims to close the gap in the existing literature by analysis the issue of corporate financial decision behavior and firm performance. Hence, this study proposes to investigate the impact of investment, leverage, and dividend per share (DPS) on firm performance.

This study apply the dynamic panel model uses generalized method of moment (GMM)-first difference estimator for the advanced statistical analysis to overcome the endogeneity issue in corporate finance. The first lagged of firm performance are likely to be endogenous or highly correlated with the dependent variables, so that they are correlated with the error term. Therefore, the ordinary least square (OLS) or static panel model estimation method (fixed effect model and random effect model) would not be an appropriate method or would be bias for estimating the model parameters. Thus, it can be used to control for the dynamic nature of relationship between firm performance and financial decision behavior while accounting for other sources of endogeneity in corporate finance research (Wintoki, Linck, & Netter, Citation2012).

Therefore, to provide additional evidence on the impact of financial decision on firm performance, the present study contributes to the existing literature by providing economic justification for use of dynamic panel GMM estimation for both accounting and market performance. The rest of this paper is organized as follows. Section 2 reviews the literature and hypotheses are developed. Sections 3 and 4 describe the methodology and empirical results, respectively whereas Section 5 concludes.

2. Literature review

2.1. Investment and firm performance

The relationship between investment and firm performance has been examined by several prominent researchers from underpinning theories of investment (Fama, Citation1978; Modigliani & Miller, Citation1958; Tobin, Citation1969). The Tobin’s Q becomes a central theoretical model of investment and provides an empirical framework for analyzing individual firm’s financial decisions. It is also a popular proxy for the unobservable investment opportunities based on market value. Fama and Miller (Citation1972) proposed that the market value of a firm is the discounted value of expected future cash flows from all its investment in the present and future; that is, an increase in capital expenditure will have a positive impact on a firm’s market performance. Earlier on, Del Brio, De Miguel, and Pindado (Citation2003) study on investment and firm value, the result suggests that the positive or negative market reactions to investment (divestment) announcement persist over time. This implies that the increase in firm value is greater for the firm with valuable investment opportunities and when firms divesting is a sign of decrease in value for the firms with valuable investment opportunities. However, Investment in stock market has been studied by Ahmar et al. (Citation2017) the results found that Sutte indicators are better in predicting stock price movement.

According to overinvestment theory, it proposes that firm with higher FCF tend to invest in negative NPV project (Jensen, Citation1986), and it is more serious to occur for rich firm and firm with higher concentrate ownership (Yu & Li, Citation2011). Previous several empirical studies indicate a significant and negative relationship between investment and firm performance but insignificant (Sudiyatno & Puspitasari, Citation2010). Similarly Loof and Heshmati (Citation2008), also found negative and insignificant. Moreover, other studies focused on the effect of investment and firm performance with different measurements. For instance several studies found a positive relationship and significant between firm performance and investment (Grazzi, Jacoby, & Treibich, Citation2016; Kaplan & Zingales, Citation1997; Riachi & Schwienbacher, Citation2015), and others also found investment have positive impact on firm performance, but its insignificant (Ruzita, Hasimi, Yaacob, & Fauzias, Citation2010; Ye & Yuan, Citation2008). Recently, Hashmi, Mirza, and Us Sehar (Citation2016), investigated the effect of investment measures by the capital expenditure on Tobin’s Q, and they found that investment positively affects investment opportunities (Tobin’s Q) for the manufacturing sectors of Pakistan companies in 2000–2008. Accordingly, increase in the capital expenditure would lead a positive impact on market performance. Hence, this study posits the following hypotheses:

H1a: There is a positive and significant impact of investment on accounting performance (ROA).

H1b: There is a positive and significant impact of investment on market performance (TOBIN’S Q).

2.2. Leverage and firm performance

The studies of the effect of leverage on firm performance has been developed by numerous prominent scholars from a broad range of underpinning theory (Miller, Citation1977; Modigliani & Miller, Citation1958, Citation1963), and three others major theories of financial structure decision (Harris & Raviv, Citation1991; Jensen & Meckling, Citation1976; Kraus & Litzenberger, Citation1973; Myers & Majluf, Citation1984). Modigliani and Miller (Citation1958) posited that in a perfect capital market, firm value is independent of its capital structure, and implies that the total value of the firm is not affected by ratio of debt. A number of researchers conducted empirical work to show the changes in level of debt that have impact on the total market value of the firm. So that, the firm value reflects a valuation by shareholders, including the value perquisites consumed by manager as the agent of shareholders (Jensen & Meckling, Citation1976). However, the trade-off theory stated that when the firm has a higher profitability rate, the expected cost of distress would decrease, and the firms will prefer to use debt financing because of their raised leverage, even if it increases the risk of bankruptcy and financial distress (Scott, Citation1977). The pecking order theory explained the firms are more likely to use the internal funds and prefer debt to equity when external financing is needed, then therefore, the pecking order theory concluded that issuing debt is not for companies with more funds and liquid (Myers & Majluf, Citation1984).

The relationship between capital structure and firm performance has been investigated by many researchers with mixed results. Earlier empirical studies supported the capital structure theory proposed by Modigliani and Miller (Citation1963), which argued that firm using debt to finance their investment, may increase firm value. Moreover, profitable firm use more debt to solve agency problem between manager and shareholders (Jensen, Citation1986). Thus, some studies found a positive relationship between financial leverage and firm performance (Abu-Rub, Citation2012; Bassey & Inah, Citation2012; San & Heng, Citation2011; Zeitun & G.Tian, Citation2007). In contrast, other studies indicated a significant and negative relationship between firm performance and financial leverage (Onaolapo & Kajola, Citation2010; Saeedi & Mahmoodi, Citation2011; Vithessonthi & Tongurai, Citation2015; Zeitun & Saleh, Citation2015). Furthermore, similarly with studies proposed by Shahzad, Ali, Ahmad, and Ali (Citation2015), found that leverage negatively affect accounting performance (ROA), and short-term debt has positive effect on market performance (Tobin’s Q). Therefore, based on the pecking order theory and the trade-off theory, this study posits the following hypotheses:

H2a: There is a negative and significant impact of leverage on accounting performance (ROA).

H2b: There is a positive and significant impact of leverage on market performance (TOBIN’S Q).

2.3. Dividend policy and firm performance

The relationship between dividend policy and firm performance has received a lot of attention in past studies. Various theories have been proposed by academicians on the principles of dividend policies that have been described as either irrelevant or relevant theory in making financial decision (Deangelo, Deangelo, & Stulz, Citation2006; Miller & Modigliani, Citation1961; Stulz, Citation2000). Miller and Modigliani (Citation1961) stated that dividend policy is irrelevant for the cost of capital, and that the value of the firm is determined by its earning power and risk. The agency theory explained about dividend payment increases firm value (Easterbrook, Citation1984). He argued that dividend payments may act as one form of bonding cost. The transaction cost theory implies that dividend payment reduces in value because they lead to rising external financial costs. Moreover, firms with insufficient cash flow have greater dependency on external finance, and should maximize shareholders wealth by accepting lower payout policies (Rozeff, Citation1982). The empirical evidence proposed that firms with a higher FCF should pay more dividends to decrease agency cost (Holder, Langrehr, & Hexter, Citation1998; Mollah, Keasey, & Short, Citation2002). In addition, relating to dividend payment the firms paying dividend are significantly having greater cash flows (Berk, Citation2006).

The signaling hypothesis is consistent with Lintner (Citation1956), suggests that managers are typically concerned with dividend stability and believe that the market has a good response to a stable dividend policy. Therefore, by paying dividend, the level of dividend changes; thus, the information is released to the market as a good signal and the price volatility reduced, and it influences the share price. The relationship between dividend policy and firm performance have been addressed (Amidu, Citation2007; Charles, Joseph, & Sang, Citation2014; Murekefu & Ouma, 2012; Uwuigbe, Jafaru, & Ajayi, Citation2012) found that dividend policy has positive relation on firm performance. In addition, the value of the signal depends on the level of information asymmetries in the market. In conclusion, it can be argued that information is important to reveal whether the dividend signal should be sent, and its effect on prices as well as on firm value. Thus, this study posits the following hypotheses:

H3a: There is a positive and significant impact of DPS on accounting performance (ROA).

H3b: There is a positive and significant impact of DPS on market performance (TOBIN’S Q).

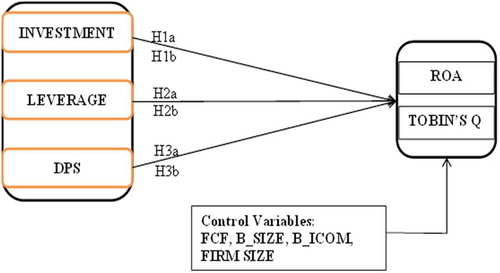

3. Conceptual framework

This study aims to investigate the impact of financial decision behavior on firm performance of Indonesia public companies. There are three important financial decision that determine firm performance, namely, investment, leverage, and dividend policy. Various theories that support the relationship between financial decision factors (investment, leverage, and dividend policy) have been described in Section 2, such as investment theory, agency theory, pecking order theory, trade-off theory, and signaling theory. Financial performance is an important key indicator for the firm survival and an essential indicator for measuring the overall corporate performance; thus firm performance measurements are commonly classified into the accounting-based and market-based measures (Abu-Rub, Citation2012; Bhagat & Black, Citation2002; Fauzias Mat Nor et al., Citation2011; Khan, Nadeem, Islam, Salman, & Gill, Citation2016; Suta, 2006). Thus, this study focuses on ROA as the accounting performance and TOBIN’S Q as the market performance.

The conceptual framework of this study develops to linking the independent and dependent variable. Thus, the investment, leverage, and DPS uses as independent variables, then FCF, board size (B_SIZE), board independent commissioners (B_ICOM) and firm size as control variables. Furthermore, the hypotheses are developed based on the theoretical background and empirical studies discussed in the literature review. Therefore, this study proposes three sets of the hypotheses towards achieving the research objectives. Based on the theoretical underpinnings, the research framework is derived, indicating the direction of the hypothesized relationships between the main constructs (financial decision and firm performance). The research framework of this study is presented in Figure

Figure 1. Research framework.

4. Methodology

To investigate the impact of financial decision behavior on firm performance, this study uses yearly of 212 nonfinancial listed firms for the period from 2003 to 2013. The data are gathered from the annual report of companies include book value of total assets and total debt, net income, market value of equity, DPS, and other financial data used in this study also corporate board structure. The data are retrieved from the latest version 2.1 of Datastream and annual report of companies. Therefore, this study has annual observation of over than 11 years period per company, producing a balanced panel data of 2332 unit observations for data analysis.

This study used numerical variables to measures dependent and independent variables. Firm performance defined as a bivariate dependent variable by two measurements, namely accounting-base performance and market-based performance (ROA and TOBIN’S Q). ROA is defined as the ratio of net profit divided by total assets. TOBIN’S Q is the ratio of market value of equity plus book value of the total debt divided by the book value of total assets each firm and years (Fauzias Mat Nor et al., Citation2011; Velnampy, Nimalthasan, & Kalaiarasi, Citation2014; Zeitun & Saleh, Citation2015). The independent variables of financial decision behavior are investment, capital structure and dividend policy. Investment is presented as the exponential growth rate of total asset of the firm i, at the time t, calculated as log natural of total asset at the time/year t divided by total assets at previous year (t-1) (Alias et al.; Ruzita et al., Citation2010). Capital structure is a combination of debt and equity and the level of it debt is referred to as leverage ratio. This study defined leverage as the ratio of total debt to total asset (Saeedi & Mahmoodi, Citation2011; Zeitun & Saleh, Citation2015). Meanwhile, the DPS was used to measure dividend policy in this study. DPS is the total amount of dividends paid to the total of share outstanding (Charles et al., Citation2014; Velnampy et al., Citation2014).

Furthermore, the FCF, board size (B_SIZE), board independent commissioners (B_ICOM) and sales are used as control variables. The FCF is the ratio of the total of (EBIT and depreciation) minus the total of (interest, tax, and dividend) divided by book value of total asset (Alias, Rahim, Nor, & Yaacob, Citation2012; Ruzita et al., Citation2010; Wang, Citation2010). Corporate governance measured by board size and board of commissioners independent. Board size (B_SIZE) is total number of directors have been employed by (Guo & Kga, Citation2012; Shahzad et al., Citation2015; Wintoki et al., Citation2012; Zeitun, Citation2014) and BOC Independent (B_ICOM) is measured by calculating the proportion of independent commissioners with respect to the total commissaries as measured by (Jaffar, Mardinah, & Ahmad, Citation2013; Magdalena, Citation2012; Zabri, Ahmad, & Wah, Citation2016). Meanwhile, firm size is the natural logarithms of the total sales (Margaritis & Psillaki, Citation2010; Alias, Yaacob, Rahim, & Nor, Citation2016; Wang, Citation2010).

In order to discover relationship between independent and dependent variable, the dynamic GMM estimator is utilized in this study. The first lagged of firm performance are likely to be endogenous or highly correlated with the dependent variables, so that they are correlated with the error term. Therefore, the OLS or static model estimation method would not be an appropriate method or would be bias for estimating the model parameters. Following the extension of the panel data analysis presented by Baltagi (Citation2008), the multiple regression model applied in this study is the pth order lagged variable model with the following general equation;

where the dependent variable is each of the variables firm performance (ROA and TOBIN’S Q), and the independent variables are all defined determinant variables. So we have the following two general equations, for t > p, where the integer p will be selected so that the lagged variables models fit the data. The empirical equation as follows:

Furthermore, note that the regression of dynamic panel model in Equations (2 and 3) in fact is an additive model of Y, and a single numerical determinant, such as Y(−1) INV, LEV, and DPS as independent variables and FCF B_SIZE, B_ICOM, F_SIZE as control variables.

5. Discussion of results

The summary of descriptive statistical analysis of the variables used in this research is based on the final sample of 212 companies. The descriptive indicators’ result is presented in Table , the results show that the mean of firm performance for both ROA and TOBIN’S Q are 3.8% and 101%, respectively. TOBIN’S Q has greater standard deviation of 62.7% compared to ROA with a standard deviation of 12.7%. This value indicates that the data of return on assets (ROA) has the lowest fluctuation for each company compared to others. TOBIN’S Q has the highest fluctuation compared to financial decision variables. On average, the investment is about 9% with standard deviation is 23.59%. Leverage has average is about 27.52% with standard deviation 20.79% and DPS has average about 968 rupiah and with standard deviation 3.254.

Table 1. Descriptive statistic of the numerical research variables

Table presents the correlation between firm performance (ROA and TOBIN’S Q) and the financial decision (INV, LEV, and DPS) and other variables (B_SIZE, B_ICOM and F_SIZE). In Table 5.2 shows that accounting performance reported to be positive correlation with the investment, DPS, FCF, board size, and firm size but negatively correlated with leverage. Moreover, TOBIN’S Q are reported to be positive correlated with DPS, FCF, board size, and firm size but investment, leverage, and independent commissioner’s shows insignificant correlation.

Table 2. The correlation signs of independent variables with firm performance

The finding of dynamic GMM-Difference models of the impact of financial decision and control variable on firm performance are reported in Table . There are four diagnostic tests that should be addressed in this study to evaluate the most appropriate estimations in dynamic GMM estimation, namely: first- and second-order autocorrelation of residuals (AR(1) and AR(2)), Hansen test (J-statistic) of overidentifying restriction and Wald test. The results of the specification test show that the Hansen J-statistic of overidentifying restriction of the two models has the p values of 0.1519 and 0.054 respectively. So that it can be concluded that both model has a valid instruments or overidentifying restriction are satisfied and appropriate model of ROA and TOBINS_Q, this mean the instruments used in the GMM-Difference models are not correlated with the residuals.

Table 3. Estimation result based on GMM-Difference for Equations (1.1) and (1.2).

The result of the Wald test, which is a test of joint significance, show that all coefficient are jointly equal to zero (H0). Moreover, the Arellano-Bond test suggested that the residual were not affected by the second-order serial autocorrelation for both models, it shows the p values of AR(2) are 0.7666 and 0.0485, respectively. This means that we accept the null hypothesis of no second-order autocorrelation.

The results in Table show that each of the lagged-dependent variables ROA(−1) and ROA(−2) and TOBINS_Q (−1) is positive and significantly impact the current accounting and market performance (ROA and TOBINS_Q). This indicates that the dynamic modeling is a right specification for firm performance. The positive and significant lagged firm performance proposes that the data support the lagged effect, and firm performance is dynamic in nature. This implies that firms produced higher return on asset and firm management has the ability to use its assets efficiently and effectively to generate firm profit in previous year. Similarly, the market performance last year provides information to investors of market value of equity to investors, and encourages them to invest in the company. This study is consistent with the earlier study presented by (Zeitun & Saleh, Citation2015).

Investment has negative and significant impact on firm performance, suggest that Indonesian public companies with higher percentage of investment have lower firm performance (ROA and TOBINS_Q). The result contradicts the theoretical prediction that investment has a positive impact on firm performance. Additionally, based on the theoretical concept of investment, it suggests that when firms have higher investment or increase growth rate of total assets, it would lead firms to increase firm profitability, in which they would use their assets optimally and take only safe investment. However, in this case, this result indicates that increased investment leads to decreased accounting performance, and this implies a symptom of overinvestment problem. This finding is in line with earlier studies (Ruzita et al., Citation2010; Sudiyatno & Puspitasari, Citation2010), who revealed that investment has negative effect on firm performance but insignificant.

Leverage has negative and significant effects on ROA but positive and significantly affects TOBINS_Q. The negative relationship between leverage and ROA suggests that companies with a higher leverage leads to a lower ROA. This implies that firm has overleverage, which in turn affects their performance negatively. This finding supports the theoretical prediction that leverage has negative effect on firm performance. Therefore, profitable firm prefer on internal financing rather than external fund to finance their investment (Myers & Majluf, Citation1984). This findings are consistent with the past studies such as (Abu-Rub, Citation2012; Olokoyo, Citation2013; Ruzita et al., Citation2010; Shahzad et al., Citation2015; Vithessonthi & Tongurai, Citation2015; Zeitun & Saleh, Citation2015) among others, so that this finding supported by pecking order theory.

Moreover, dividend policy (DPS) has positive and significant impact on firm performance (ROA and TOBINS_Q) of Indonesian public companies. The data support the hypothesis that DPS has positive effects on firm performance. This positive relationship indicates that the higher firm performance encourage firms to payout dividends to its shareholders. Nevertheless, firm with higher FCF should pay more dividends to the reduced agency cost as one possible solution to solve it problem of collective actions that tend to lead to undermonitoring of the firm and its management (Easterbrook, Citation1984; Holder et al., Citation1998; Mollah et al., Citation2002). This finding is in line with earlier studies (Imran, Citation2011; Jensen, Citation1986; Ruzita et al., Citation2010).

In addition, FCF has positive and significant effect on ROA but it was insignificant effect on TOBINS_Q. The positive relations suggested that firm with higher FCF lead to increase accounting firm performance specifically for large and profitable firms, in which the firm more stable net earnings as well as firm has ability to pay large dividends to shareholders. With respect to corporate governance structure measured by Board Size (B_SIZE) and Board Independent Commissioners (B_ICOM) have positive effect on ROA but insignificant. However, B_ICOM has positive and significant impact on market performance (TOBINS_Q); this implies that the positive role of independent commissioners is also consistent with theoretical prediction. Since corporate governance of Indonesia firms adopted dual board system (BOD and BOC), so that the ratio of independent commissioners has positive sign to market performance, higher number of independent commissioner leads to increase market performance. Firm size has positive and significant relationship on ROA. The positive relation suggested that higher firm size leads to increase market performance.

6. Conclusion

This study investigates the effect of financial decision behavior on firm performance of 212 Indonesian listed companies using dynamic panel GMM estimation method during the period 2003–2013. The results based on the GMM-difference estimation find that firm performance is dynamic in nature, indicating that the lagged firm performance is significant. This implies that the previous year’s firm performance affects the current year performance. The findings of financial decision behavior indicate that financial decision behavior of Indonesian public companies seems to be important factors in determining firm performance, where the investment, capital structure and dividend policy affect financial firm performance significantly. The negative coefficient of investment suggests that the findings are consistent with the theoretical intuition of over-investment, in which managers overinvest lead to decrease firm performance. Similarly to financing decision, Indonesian firms was overleverage, indicates that the negative impact of leverage on ROA due to agency problem between manager and shareholders, thus leads to the decrease firm performance. However, the interesting finding reveals that leverage is positive and significant on market performance (TOBINS_Q). It indicates that debt improves the Indonesian market performance, which may not reflect on their profitability. Moreover, the positive relation between DPS and TOBINS_Q shows that firm payout dividends to shareholders create good signal to the market, which is manager’s uses dividend to express their private information about firm prospect of the future earning to the market. In term of theoretical explanation, the impact of financial decision variables of financial firm performance for all the period is consistent with the theory. However, based on the coefficient of financial decision variables, the impact is more on the market performance and less on the accounting performance.

Additional information

Funding

Notes on contributors

Darmawati Muchtar

Darmawati Muchtar is a lecturer in Finance at Faculty of Economic and Business, Universitas Malikussaleh (UNIMAL), Aceh-Indonesia. She received her D.B.A (Finance) from the Graduate School of Business, Universiti Kebangsaan Malaysia in 2017.

Fauzias Mat Nor

Fauzias Mat Nor is a professor of finance at Universiti Sains Islam Malaysia. Her research interest is on Islamic Finance with special focus on Corporate Finance and Banking. Prior to joining USIM, in 2015, she has served UKM for more than 29 years as a lecturer, an Associate Professor and Professor in Finance.

Wahyuddin Albra

Wachyuddin Albra is a lecturer in Department of Management at Faculty of Economic and Business, Universitas Malikussaleh (FEB-UNIMAL), Aceh-Indonesia. Now he is a Dean at FEB-UNIMAL, Aceh, Indonesia.

Muhammad Arifai

Muhammad Arifai is a lecturer at Department of Accounting, Lhokseumawe State of Polytechnic, Aceh, Indonesia.

Ansari Saleh Ahmar

Ansari Saleh Ahmar is a lecturer at Department of Statistics, Universitas Negeri Makassar, Makassar, Indonesia.

References

- Abu-Rub, N. (2012). Capital structure and firm performance: Evidence from Palestine stock exchange. Journal of Money, Investment and Banking, 23(1), 109–117.

- Ahmar, A. S., Rahman, A., Arifin, A. N. M., & Ahmar, A. A. (2017). Predicting movement of stock of “Y” using Sutte indicator. Cogent Economics & Finance, 5(1), 1347123

- Alias, N., Rahim, R. A., Nor, F. M., & Yaacob, M. H. (2012). Board structure, capital structure and dividend per share: Do they interact? International Proceedings of Economics Development and Research, 57, 148.

- Alias, N., Rahim, R. A., Nor, F. M., & Yaacob, M. H. (2014). Board structure, capital structure and dividend per share: Is there interaction effect? Indian Journal of Corporate Governance, 7(1),2–13

- Alias, N., Yaacob, M. H., Rahim, R. A., & Nor, F. M. (2016). Board structure, capital structure and dividend per share: Is there interaction effect? Malaysian Journal of Society and Space, 12(2), 58–67.

- Amidu, M. (2007). How does dividend policy affect performance of the firm on Ghana stock exchange? Investment Management and Financial Innovations, 4(2), 103–112.

- Babatunde, M. A., & Olaniran, O. (2009). The effects of internal and external mechanism on governance and performance of corporate firms in Nigeria. Corporate ownership & control, 7(2),330–344

- Baltagi, B. (2008). Econometric analysis of panel data. Chichester, UK: Wiley.

- Bassey, B. E., & Inah, E. U. (2012). Capital structure, corporate financial performance and shareholders’ investment decisions: A survey of selected Nigerian companies. European Journal of Economics, Finance and Administrative Sciences, 54, 128–145.

- Burca, A. M., & Batrinca, G. (2014). The determinants of financial performance in the Romanian insurance market. International Journal of Academic Research in Accounting, Finance and Management Sciences, 4(1),299–308

- Berk, A. (2006). Determinants of leverage in Slovenian blue-chip firms and stock performance following substantial debt increases. Post-Communist Economies, 18(4), 479–494. doi:10.1080/14631370601008621

- Bhagat, S., & Black, B. S. (2002). The non-correlation between board independence and long-term firm performance. As Published in Journal of Corporation Law, 27, 231–273.

- Bhattacharya, S. (1979). Imperfect information, dividend policy, and “the bird in the hand” fallacy.” The Bell Journal of Economics, 10(1), 259–270. doi:10.2307/3003330

- Charles, Y., Joseph, C., & Sang, J. (2014). Effects of dividend policy on firm’s financial performance: Econometric analysis of listed manufacturing firms in Kenya. Research Journal of Finance and Accounting, 5(12), 136–144.

- Deangelo, H., Deangelo, L., & Stulz, R. M. (2006). Dividend policy and the earned/contributed capital mix: A test of the life-cycle theory. Journal of Financial Economics, 81(2), 227–254. doi:10.1016/j.jfineco.2005.07.005

- Del Brio, E., De Miguel, A., & Pindado, J. (2003). Investment and firm value: An analysis using panel data. Applied Financial Economics, 13(12), 913–923. doi:10.1080/0960310032000082079

- Djaja, K. (2009). Impact of the global financial and economic crisis on Indonesia. A rapid assessment. In ILO, Secretary Coordinating Ministry for Economic Affairs, Indonesia.

- Easterbrook, F. H. (1984). Two agency-cost explanations of dividends. The American Economic Review, 74(4), 650–659.

- Fama, E. F. (1978). The effects of a firm’s investment and financing decisions on the welfare of its security holders. The American Economic Review, 68(3), 272–284.

- Fama, E. F., & Miller, M. H. (1972). The theory of finance. New York, NY: Holt, Rinehart, and Winston.

- Fauzias Mat Nor, R. R. A., Azlan, N., & Hasimi, Y. 2011. Corporate finance behavior: Toward key financial performance index (Kfpi) of Malaysian firms. Ministry of Science, Technology and Innovation (MOSTI) Kuala Lumpur.

- Fazzari., S. M., Hubbard., R. G., & Petersen., B. C. (1988). Financing constraints and corporate investment. Broorking Paper on Economic Activity, 1988(1), 141–195. doi:10.2307/2534426

- Grazzi, M., Jacoby, N., & Treibich, T. (2016). Dynamics of investment and firm performance: Comparative evidence from manufacturing industries. Empirical Economics, 51(1), 125–179.

- Guo, Z., & Kga, U. K. (2012). Corporate governance and firm performance of listed firms in Sri Lanka. Procedia - Social and Behavioral Sciences, 40, 664–667. doi:10.1016/j.sbspro.2012.03.246

- Halkos, G. E., & Tzeremes, N. G. (2007). Productivity efficiency and firm size: An empirical analysis of foreign owned companies. International Business Review, 16(6), 713–731. doi:10.1016/j.ibusrev.2007.06.002

- Hardiyanto, A. T., Achsani, N. A., Sembel, R., & Maulana, T. (2014). The difference of capital structure among industry sectors in the Indonesia stock exchange. Business and Management Review, 3(08), 28–35.

- Harris, M., & Raviv, A. (1991). The theory of capital structure. The Journal of Finance, 46(1), 297–355. doi:10.1111/j.1540-6261.1991.tb03753.x

- Hashmi, M. S., Mirza, F. M., & Us Sehar, N. (2016). Political regimes, internal funds and investment behaviour: An empirical analysis of manufacturing sector firms in Pakistan. Pakistan Economic and Social Review, 54(1), 25.

- Holder, M. E., Langrehr, F. W., & Hexter, J. L. (1998). Dividend policy determinants: An investigation of the influences of stakeholder theory. Financial Management, 27, 73–82. doi:10.2307/3666276

- Hubbard, G. (1998). Capital market imperfections and investment. Journal of Economic Literature, 35, 193–225.

- Imran, K. (2011). Determinants of dividend payout policy: A case of Pakistan engineering sector. The Romanian Economic Journal, 4(1):47–60

- Jaffar, R., Mardinah, D., & Ahmad, A. (2013). Corporate governance and voluntary disclosure practices. Jurnal Pengurusan, 39(2013), 8392.

- Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review, 76(2), 323–329.

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3, 305–360. doi:10.1016/0304-405X(76)90026-X

- John, K., & Williams, J. (1985). Dividends, dilution, and taxes: A signalling equilibrium. The Journal of Finance, 40(4), 1053–1070. doi:10.1111/j.1540-6261.1985.tb02363.x

- Kaplan, S. N., & Zingales, L. (1997). Do investment-cash flow sensitivities provide useful measures of financing constraints? The Quarterly Journal of Economics, 112(1), 169–215. doi:10.1162/003355397555163

- Khan, M. N., Nadeem, B., Islam, F., Salman, M., & Gill, H. M. I. S. (2016). Impact of dividend policy on firm performance: An empirical evidence from Pakistan stock exchange. American Journal of Economics, Finance and Management, 2(4), 28–34.

- Kraus, A., & Litzenberger, R. H. (1973). A state preference model of optimal financial leverage. The Journal of Finance, 28(4), 911–922. doi:10.1111/j.1540-6261.1973.tb01415.x

- Lintner, J. (1956). Distributions of incomes of corporations among dividends, retained earnings, and taxes. American Economic Review, 46, 97–113.

- Liow, K. H. (2010). Is real estate an important factor in corporate valuation? Evidence from listed retail firms. Journal of Corporate Real Estate, 12(4),249–278

- Loof, H., & Heshmati, A. (2008). Investment and performance of firms: Correlation or causality? Corporate Ownership & Control, 6(2), 268–282.

- Magdalena, R. (2012). Influence of corporate covernance on capital structure decision: Evidence from Indonesian capital market. World Review of Business Research, 2(4), 37–49.

- Margaritis, D., & Psillaki, M. (2010). Capital structure, equity ownership and firm performance. Journal of Banking & Finance, 34(3), 621–632. doi:10.1016/j.jbankfin.2009.08.023

- Miller, M. H., & Modigliani, F. (1961). Dividend policy, growth, and the valuation of shares. The Journal of Business, 34(4), 411–433. doi:10.1086/jb.1961.34.issue-4

- Miller, E. M. (1977). Risk, uncertainty, and divergence of opinion. The Journal of Finance, 32(4),1151–1168

- Miller, M. H., & Rock, K. (1985). Dividend policy under asymmetric information. The Journal of Finance, 40, 1031–1051. doi:10.1111/j.1540-6261.1985.tb02362.x

- Mirza, S. A., & Javed, A. (2013). Determinants of financial performance of a firm: Case of Pakistani stock market. Journal of economics and International Finance, 5(2),43–52

- Modigliani, F., & Miller, M. (1963, June). Corporate income taxes and the cost of capital: A correction. American Economic Review, 53(June), 433–443.

- Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance and the theory of investment. The American Economic Review, 48(3), 261–297.

- Mollah, S., Keasey, K., & Short, H. 2002. The influence of agency costs on dividend policy in an emerging market: Evidence from the Dhaka stock exchange. Working Paper 10.1044/1059-0889(2002/er01)

- Myers, S. C. (1977). Determinants of corporate borrowing. Journal of Financial Economics, 5(2), 147–175. doi:10.1016/0304-405X(77)90015-0

- Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221. doi:10.1016/0304-405X(84)90023-0

- Nikolaus, V. (2015, July 2). Determinants of Firm financial performance in Indonesia and the Netherlands: A comparison ( 5th IBA Bachelor Thesis Conference). Anjuran Enschede, The Netherlands.

- Olokoyo, F. O. (2013). Capital structure and corporate performance of Nigerian quoted firms: A panel data approach. African Development Review, 25(3),358–369

- Onaolapo, A. A., & Kajola, S. O. (2010). Capital structure and firm performance: Evidence from Nigeria. European Journal of Economics, Finance and Administrative Sciences, 25, 70–82.

- Riachi, I., & Schwienbacher, A. (2015). Investment, firm performance and securitization: Evidence from industrial companies. Finance Research Letters, 13, 17–28. doi:10.1016/j.frl.2015.03.007

- Rozeff, M. S. (1982). Growth, beta and agency cost of determinants of dividend payout ratio. Journal of Financial Research, 5(3), 249–259. doi:10.1111/j.1475-6803.1982.tb00299.x

- Ruzita, A. R., Hasimi, M., Yaacob, N. A., & Fauzias, M. N. (2010). Investment, board governance and firm value: A panel data analysis. International Review of Business Research Papers, 6(5), 293–302.

- Saeedi, A., & Mahmoodi, I. (2011). Capital structure and firm performance: Evidence from Iranian Companies. International Research Journal of Finance and Economics, 70(11), 20–29.

- San, O. T., & Heng, T. B. (2011). Capital structure and corporate performance of Malaysian construction sector. International Journal of Humanities and Social Science, 1(2), 28–36.

- Scott, J. (1977). Bankruptcy, secured debt, and optimal capital structure. The Journal of Finance, 32, 1–19. doi:10.1111/j.1540-6261.1977.tb03237.x

- Shahzad, S. J. H., Ali, P., Ahmad, T., & Ali, S. (2015). Financial leverage and corporate performance: Does financial crisis owe an explanation? Pakistan Journal of Statistics and Operation Research, 11(1), 67–90. doi:10.18187/pjsor.v11i1.781

- Stulz, R. M. (2000). Merton miller and modern finance. Financial Management, 29, 119–131. doi:10.2307/3666371

- Sudiyatno, B., & Puspitasari, E. (2010). Pengaruh Kebijakan Perusahaan Terhadap Nilai Perusahaan Dengan Kinerja Perusahaan Sebagai Variabel Intervening (Studi Pada Perusahaan Manufaktur Di Bursa Efek Indonesia). Dinamika Keuangan Dan Perbankan, 2(1), 1–22.

- Sudiyatno, B., Puspitasari, E., & Kartika, A. (2012). The company’s policy, firm performance, and firm value: An empirical research on Indonesia stock exchange. American International Journal of Contemporary Research, 2(12), 30–40.

- Tan, J., & Wang, L. (2010). Rexibility-efficiency tradeoff and performance implications among Chinese SOEs. Journal of Business Research, 63(4), 356–362. doi:10.1016/j.jbusres.2009.04.016

- Tobin, J. (1969). A general equilibrium approach to monetary theory. Journal of Money, Credit and Banking, 1(1), 15–29. doi:10.2307/1991374

- Uwuigbe, U., Jafaru, J., & Ajayi, A. (2012). Dividend policy and firm performance: A study of listed firms in Nigeria. Accounting and Management Information Systems, 11(3), 442.

- Velnampy, T., Nimalthasan, M. P., & Kalaiarasi, M. K. (2014). Dividend policy and firm performance: Evidence from the manufacturing companies listed on the Colombo stock exchange. Global Journal of Management and Business Research, 14(6), 63–67.

- Vithessonthi, C., & Tongurai, J. (2015). The effect of firm size on the leverage–performance relationship during the financial crisis of 2007–2009. Journal of Multinational Financial Management, 29, 1–29. doi:10.1016/j.mulfin.2014.11.001

- Wang, G. Y. (2010). The impacts of free cash flows and agency costs on firm performance. Service Science & Management, 3(4), 408–418. doi:10.4236/jssm.2010.34047

- Wardhana, L. I., Tandelilin, E., Wayan Nuka Lantara, I., & Junarsin, E. (2014). Dividend policy in Indonesia: A life-cycle explanation. Asian Finance Association (AsianFA) 2014 Conference Paper. Anjuran. Retrieved from https://papers.ssrn.com

- Wintoki, M. B., Linck, J. S., & Netter, J. M. (2012). Endogeneity and the dynamics of internal corporate governance. Journal of Financial Economics, 105(3), 581–606. doi:10.1016/j.jfineco.2012.03.005

- Ye, B., & Yuan, J. (2008). Firm value, managerial confidence, and investments: The case of China. Journal of Leadership Studies, 2(3), 26–36. doi:10.1002/jls.v2:3

- Yu, L., & Li, L. (2011, May). Corporate Governance, free cash flow and over-investment. In Business Management and Electronic Information (BMEI), 2011 International Conference, Guangzhou, China (Vol. 3, pp. 713–717).

- Zabri, S. M., Ahmad, K., & Wah, K. K. (2016). Corporate governance practices and firm performance: Evidence from top 100 public listed companies in Malaysia. Procedia Economics and Finance, 35, 287–296. doi:10.1016/S2212-5671(16)00036-8

- Zeitun, R. (2014). corporate governance, capital structure and corporate performance: Evidence from GCC countries. Review of Middle Eastern Economics and Finance, 10(1), 75–96.

- Zeitun, R., & G. Tian, G. (2007). Capital structure and corporate performance: Evidence from Jordan. Australasian Accounting Business and Finance Journal, 1(4), 40.

- Zeitun, R., & Saleh, A. S. (2015). Dynamic performance, financial leverage and financial crisis: Evidence from GCC countries. EuroMed Journal of Business, 10(2), 147–162. doi:10.1108/EMJB-08-2014-0022