?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The excessive cost of financial intermediation in the Sub-Saharan African banking sectors motivates the investigation of whether competition, regulation and stability matter for efficiency in the banking system. Data from 440 commercial banks for the periods 2006–2015 were collected and analysed by seven-variable panel structural vector autoregressive model. There was evidence to show that efficiency responds positively and significantly to shocks in capital, liquidity and asset quality regulations and competition. However, the results reveal all the variables responding to one standard deviation shock in efficiency, suggesting that while the variables matter for efficiency, they all also require efficiency for their effective operation. Hence, the conclusion is that efficiency is central to the effective running of the banking system.

PUBLIC INTEREST STATEMENT

This article explores the place of efficiency in the banking system of the Sub-Saharan African banking system with a particular interest in the commercial banking sub-sector. The panel structural vector autoregressive was used to analyse the impulse response of efficiency of the banking system to and from regulatory variables, competition and stability of the system using a transformed data of 440 commercial banks from 37 countries. Efficiency was found to be germane to the banking system as there is a transmission from regulation to efficiency via competition and from efficiency to market power. The results suggest that a vicious cycle competition leads to efficiency and efficiency to market power and back to competition.

1. Introduction

The purpose of this article is to analyse the efficiency of the commercial banking system of the Sub-Saharan African (SSA) commercial banks in the context of competition, regulation and stability of the banking system. The SSA financial system is largely bank basedFootnote1 with grossly underdeveloped capital markets (Abdelkader & Mansouri, Citation2013). The financial and banking systems in SSA countries remain underdeveloped and laced with inefficiencies. Banking competition brings about a stable and an efficient banking sector where there is access to finance, low charges and moderate interest rates spread (Ariss, Citation2010; Chirwa, Citation2003; Freixas & Rochet et al., Citation2008; Kouki & Al-Nasser, Citation2014; Mugume, Citation2008). However, service charges and lending rates are extremely high with meagre deposit interest rates in SSA banking sectors (Mlachila, Park, & Yabara, Citation2013). Moreover, high non-performing loans (NPLs) threaten the stability of the banks in the region. Despite some of the efforts to regulate the sector, these problems have persisted. High costs of banking and lending rates are being identified as factors militating against efficient banking sectors’ financial intermediation role. Consequently, service charges are high, financial intermediation is low and high interest rate spreads stifle investment and savings, curtailing the efficient operation of banks in this region, hence their inability to finance SSA countries’ developmental goals. The culmination of the foregoing means a banking system with lowest commercial bank branches compared to other regions of the world, with very low bank credit to private sectors, hence unable to support entrepreneurial drives of the region especially giving the very high cost of banking. These pose enormous challenge to policy-makers of improving efficiency in banking system of the region to facilitate increased financial intermediation that could support the anticipated development in the region. Thus, it requires empirical investigations of ways to improve banking efficiency in the region.

To the best of my knowledge, this is the first research to investigate the implications of regulation (capital, liquidity and asset quality) on efficiency; second, the effect of efficiency on capital and liquidity regulation; and, third, the effects of interest rate spread on the efficiency of banks. This study found evidence to support a direct and significant relationship between the regulation variables and efficiency. Moreover, the results show that competition results in efficiency leading to acquisition of market power which eventually revert to a competitive banking environment. Until now, no study has investigated these issues as suggested by the evidences available and are fundamental extension of literature.

The rest of this article proceeds as follows: literature review, theoretical and empirical, is given in section 2. Section 3 explains the various methods adopted including data source and description of variables employed. In section 4, the results are presented, and section 5 provides the summary and conclusion.

2. Literature review

Efficiency refers to the level of performance of a firm which could be viewed either in relation to output or cost savings. In the former, few inputs are converted to optimal production output, while the later epitomises avoidance of excesses such as waste to achieve a desired outcome. Hence, the classification is as productive (technical) and economic efficiency. Early insight into this field by Koopmans (Citation1951) describes productive efficiency as the point where further output can no longer be achieved without employing more inputs or reducing production of some other outputs. However, economic efficiency aims to achieve a given output at minimum cost or use a given input to maximise revenue or allocate inputs and outputs to maximise profit (Kumbhakar & Lovell, Citation2003). Technical efficiency, hence, emphasises the ability to minimise inputs used in a vector of output production or maximise output from a given input vector. Described by Battese and Coelli (Citation1992), it is the ratio of a firm’s mean production to the corresponding mean production conditioned on the firm’s efficient utilisation of its inputs.

Productivity and efficiency have been used interchangeably but are, however, different. In terms of production, the production frontier is a representation of the maximum attainable output of a firm from a given input, thus reflecting the current state of the firm’s technology. In the case of technical efficiency, when firms in an industry operate on the frontier, they are technically efficient, otherwise inefficient. This implies that firms operating inefficiently have the latitude further to the frontier without altering their inputs. In banking, this is developed to measure an efficient frontier from which banks’ positions are compared. Therefore, competition forces banks to become efficient in their operational activities to maintain a competitive advantage and outperform their rivals. As Hicks (Citation1935) argued, it makes managers to come out of their shelves. By implication, an efficient banking system is characterised by lower costs resulting in a better financial intermediation functions thereby culminating in lower charges to customers.

2.1. Efficiency and competition

The literature that links competition and efficiency relies on the structure of firms pioneered by the Hicks’ (Citation1935) quiet life hypothesis (QLH) which argued that the composition of a firm explains its performance and/or efficiency. This is consistent with the position of the micro market structure theory that stratified firms according to their features in terms of market power ranging from monopoly to pure competition and the go-between as monopolistic competition and oligopoly (Nyong, Citation1999, among others). The more general consensus is that efficient utilisation of inputs for an optimised output is precedent on the relative share of the market a firm control. In other words, firms with market power enjoy quiet life and can afford to be inefficient without consequence for their performance (see Shepherd, Citation1983; Smirlock, Gilligan, & Marshall, Citation1986). This relationship between uncompetitive banking system and its efficiency was also upheld by Pagano (Citation1993) with the argument that inefficiencies increase with market power as managers are under less pressure to minimise cost. However, Demsetz’s (Citation1973) efficiency structure hypothesis (ESH) argued, otherwise, that efficiency determines the structure of firms as more efficient firms can afford more market share, hence more market power, suggesting a reverse causality among competition/market power and efficiency (Vander Vennet, Citation2002). Akande and Kwenda (Citation2017a) empirically investigated the impact of competition on efficiency applying stochastic frontier analysis (SFA) of Battese and Coelli (Citation1992) to a sample SSA commercial bank. The study modelled the efficiency of the banking systems with and without competition and found an increase in efficiency with a competitive banking system as the mean efficiency of the model with competition turned out to be higher than the model without competition. Other empirical works of Fungáčová, Pessarossi, and Weill (Citation2013) and Hussain and Hassan (Citation2012), among others, that also studied the relationship between competition and efficiency found competition to increase efficiency in the banking system.

Meanwhile, Boot and Schmeits (Citation2006) leveraged on the price war in a competitive banking environment to argue that competition results in banking inefficiency as it results in a short-term relationship between the banks and their principal stakeholder, customers. According to Evanoff and Ors (Citation2002), high cost will have to be incurred to sustain customers’ loyalty. Apriadi, Sembel, Santosa and Firdaus (Citation2016) found that efficiency is inversely affected with competition in the Indonesia banking system given that concentration positively Granger causes efficiency in the system. With the foregoing evidences, one could at best conclude that the relationship between competition and efficiency in the banking system is largely inconclusive and has to be further investigated especially in the banking system of SSA region. Specifically, no studies have investigated the nexus between interest rate spread, another good proxy of competition used in the literature,Footnote2 and efficiency, hence providing an opportunity for extending literature in this area.

2.2. Efficiency and regulation

To the best of my knowledge, no existing literatures have been seen to have expressly explored the relationship between regulation and efficiency in the banking system. This study, however, hypothesises a direct relationship between regulation and efficiency as an indirect relationship could be inferred given the relationship between competition and efficiency. It is evident in the literature that one of the fundamental reasons for bank regulation is to stimulate competition of the banking system (Casu & Girardone, Citation2006; Llewellyn, Citation1999). Since competition is necessary for the dynamic efficiency of the banking system (see Casu, Girardone, & Molyneux, Citation2015), it is logical to infer that regulation causes efficiency. However, this study also hypothesises a reverse causality between regulation and efficiency as excessive competition may impair efficiency (Apriadi et al., Citation2016, among others) and thus compels regulatory intervention for remedy. Table outlines some of these gaps in the literature that this study proposes to make some contributions.

Table 1. Research hypothesis for analysis

2.3. Efficiency and stability

The industrial organisation theory alludes to competition–efficiency hypothesis. This relationship provides credence to the competition–stability views widely researched in the literature. The arguments being that a competitive banking environment exudes efficiency which helps to ensure the stability of the system. The literature provides evidences of a relationship between efficiency and stability. On one hand, efficiency has been argued to affect positively on stability. This is true as efficient banks are seen to better manage the asset side of their balance sheet which Williams (Citation2004), Petersen and Rajan (Citation1995) and Berger (Citation1995) argued has helped to reduce incidences of NPLs, hence the stability of the system. On the other hand, Apriadi et al. (Citation2016) considered proxy Z score for stability and found that cost efficiency positively Granger causes stability of banks. At the same time, they found that stability also matters for the efficiency of banks as their results show that improvement in stability also positively affects the efficiency of banks.

Overall, Table summarises the hypothesis that we propose in this study. Specifically, the study contributes to extant literature in the nexus between efficiency and regulation and efficiency and competition by investigating the effects of interest rate spread on efficiency.

3. Methodology

To effectively analyse the impact on efficiency of competition, regulation and stability in the banking system and how efficiency also affects these variables, this study elected to carry out a short-term analysis using the panel structural vector autoregressive (P-SVAR) model. The choice of method is informed by its flexibility to permit the recovery of interesting pattern with little or no theoretical background (see Graeve & Karas, Citation2010), especially in a banking research as in the case of this study. Moreover, the capability of panel vector autoregression (PVAR) to combine past, present and future scenarios in a study (Canova & Ciccarelli, Citation2014) underscores its power over other methods such as ordinary least squares (OLS) and generalised method of moments (GMM), including its ability to accommodate more variables without the loss of degree of freedom (Raghavan & Silvapulle, Citation2008). Furthermore, it is useful in separating shocks as to whether it is permanent or temporary (Ramaswamy & Slœk, Citation1998), while also providing flexibility of dynamic cross section and slope heterogeneity (Canova & Ciccarelli, Citation2014). In fact, it harnessed the merits of vector autoregression (VAR), PVAR and SVAR as it overcomes their limitations individually.

Hence, the reduced form of the P-SVAR can be written as

where is (nxk) vector variable given as

Equation (3.2) is the vector of SSA region commercial bank endogenous variables used in the study, where Z SCORE is the stability measure, IRS is the interest rate spread and LI is the competition index. Others are CAP the regulatory capital, LIQ the liquidity reserve, ASQ the asset quality and EFS the efficiency score estimated with SFA as efficiency measure. From Equation (3.1), is the vector of constants denoting country intercept terms,

is the matrix of polynomial in the lag operator that captures the relationship between the bank endogenous variables and their lags,

and/or

, is a vector of random disturbance. This will be employed to estimate the interaction between regulation, competition and stability of SSA commercial banks.

To enable the recovery of information in the structural model, restrictions were imposed in the matrices Q and K in the system for which the identification scheme follows Davoodi, Dixit and Pinter (Citation2013), whereby structural restrictions are applied to the contemporaneous parameter matrix. This process permits the contemporaneous reactions of the variables to the individual innovations based on their ordering (see Akande & Kwenda, Citation2017b; Kutu & Ngalawa, Citation2016). Hence, the scheme is identified with 70 restrictions on the matrices following, Amisano and Giannini (Citation1997), with maximum of 42 restrictions on the diagonal matrix and the remaining 28 restrictions absorbed by the other matrix for the system to be exactly identified.

3.1. Source of data and variable description

Data were sourced from the BankScope database used in many bank literatures. Our sample comprises 440 commercial banks from 37 SSA countries that excluded South Africa for the level of the financial sector development and others such as Zimbabwe and Sudan, among others, for want of data. Data collected are predominantly bank profile data necessary for the estimation of efficiency (using SFA), competition (based on Lerner index (LERNERI)), capital (using equity capital ratio (ECR; CAP)) and stability (based on Z SCORE). Further details about the data requirement for these surrogates and others considered in this study are given in Table . Regulatory variable selection was informed by CAMEL (see Akins, Li, Ng, & Rusticus, Citation2016; Moyo, Nandwa, Council, Oduor, & Simpasa, Citation2014; among others) and the Basel Accords.

Table 2. Data and variable description

4. Empirical results

The summary statistics of the data for this study is presented in Table for the periods under consideration to provide an insight into the nature of data employed. The hypotheses highlighted in Table are tested using the P-SVAR. Following Kutu and Ngalawa (Citation2016), among others, P-SVAR at levels was implemented giving that the variables are without unit root. The standard final prediction error (FPE), Schwarz’s Bayesian information criterion (SBIC), Akaike’s information criterion (AIC) and Hannan and Quinn information criterion (HQIC) out of the five commonly used information criteria suggest an optimal 5-lag length as the lag selection for the transformed data.Footnote3 The use of an appropriate lag length prevents the equations being potentially mis-specified (see Canova, Citation2007; Stock & Watson, Citation2007) as well as prevents issues of serial correlation in the residuals (see Kutu & Ngalawa, Citation2016). For robustness, other diagnostic tests such as heteroskedasticity, normality test and VAR stability test provided the much-needed confidence for the validity of the results. Besides, Im–Pesaran–Shin (IPS) test was carried out as part of the unit root test which has been argued to account for structural breaks (Glynn, Perera, & Verma, Citation2007). Furthermore, issues of cross-sectional dependence are largely catered for in PVAR, even though Chudik and Pesaran (Citation2013) argued that the assumption could be relaxed for large panel analysis as in the case of this study. Having satisfied the basis for implementing VAR, the results of the impulse response function and the variance decomposition are interpreted and discussed below.

Table 3. Summary statistics

4.1. Impulse response analysis

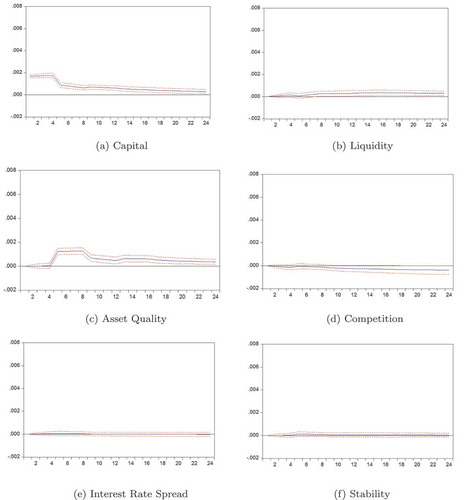

This subsection analyses the response of efficiency to one standard deviation shock in regulation variables (capital, liquidity and asset quality), competition and regulation, as well as the response of these variables to one standard deviation shock in efficiency in the commercial banking sector of SSA region. Impulse response function provides information on the future states of the banking system as it relates to the variables in the system where there are changes in any of the components. Bank efficiency response to capital shock is significant and positive but with a declining trend over the periods. In Figure ), efficiency increases steadily from period 1 to period 4 and declines suddenly with a steep slope up to period 8 and then a steady decline in the rest of the periods. The implication of this is that the level of capital of a bank determines the relative efficiency that the bank can attain and that bank capital has a direct and short-term positive relationship with commercial banks’ efficiency in the SSA region. Figure ) depicts the impulse response graph for liquidity and efficiency. Again, liquidity is positive and significant to explain the efficiency in the banking system of SSA. A standard deviation shock in liquidity causes a positive rise in efficiency with a steady decline between period 4 and period 6. From period 6, efficiency rises, flattened over the periods but declines steadily towards the 24th period. Although issues of liquidity are quite tricky in the banking system, it, however, follows that adequate liquid assets will both support lending and profitable investments without compromising short-term obligations, thus having far-reaching effects on profitability. As for bank’s quality of assets, Figure ) shows a positive and significant relationship between banks’ asset quality and efficiency. As indicated in the graph, a standard deviation asset quality shock triggers quite an interesting pattern of reactions over the next 24 periods. It begins with an insignificant response until the fourth period where it becomes significant and positive with a very sharp increase to become flat and steady between period 5 and period 8. By the ninth period, it declines steadily and rises again with 12th and 14th quarters, respectively, only to decline from there but shows positive responses throughout the periods. This reiterates the fact that efficiency in banks is also directly affected by asset quality regulation and with short-term considerable influence. Overall, this study found all the regulatory variables considered to affirm our expectation as hypothesised in section 2.

Figure 1. Impulse responses of efficiency.

In the other results, competition in Figure ) shows a negative but insignificant relationship with efficiency. This is partly consistent with the study of Fungáčová et al. (Citation2013) who found competition to negatively Granger cause efficiency and Hussain and Hassan (Citation2012) that found a significant negative relationship between competition and efficiency. In the results in this study, efficiency reacts negatively in the short term against expectations to a standard deviation competition innovation, although the response is barely significant over the study period. Efficiency reaction to one standard deviation shock in interest rate spread and Z score, stability measure, is insignificant over the study period implying the absence of short-term response of efficiency to these variables. Although the literature found stability to positively Granger cause efficiency, in Apriadi et al. (Citation2016), this relationship is perhaps more apparent in the long term.

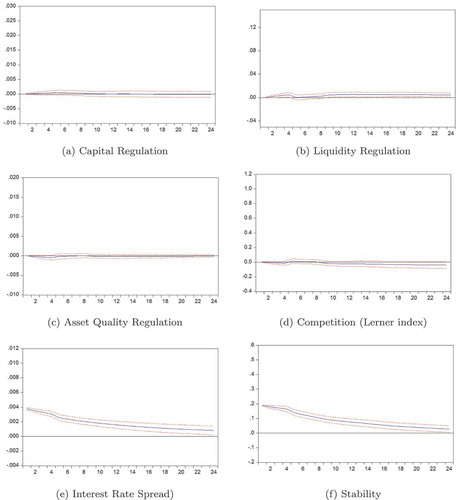

Figure shows the various responses of the variables being considered to a standard deviation efficiency shock. The response of capital regulation to efficiency in the banking system is represented in Figure ). Efficiency is insignificantly related to capital as capital regulation does not significantly respond to a standard deviation shock in efficiency. Between the first and tenth periods, capital response is barely positive and above zero and thereafter declines and tends to fall below zero. In contrast, liquidity responds (Figure )) significantly and positively over substantial periods of the study. This implies that efficiency is positive and significant in explaining liquidity regulation in the banking system. Liquidity rises and falls to zero in period 5, and while the response is not significant in the 4th–8th periods, it reacts with a steady surge with a significant positive rise towards the end of the 24th period. This indicates that changes in efficiency have considerable short-term effects on the liquidity of banks. It is logical that an efficient bank may be able to properly manage its liquid asset in the face of competition. In the case of asset quality, it was found in Figure ) that efficiency is not significantly related to the quality of assets of banks. It shows that asset quality regulation responds not significantly different from zero to a standard deviation efficiency shock for most parts of the periods. Notably, the response is negative up to the fifth period. This is inconsistent with Williams (Citation2004) and Berger and Mester (Citation1997) who argued a better asset management with a more efficient bank. Efficiency as shown in Figure ) is negative but insignificantly related to competition as measured by the Lerner index. It was found that the response of competition to a standard deviation shock in efficiency to be initially negative up to period 5 but rises above zero to be positive between period 5 and period 8 from where it gradually falls back to negative to the end of the period. This result aligns with Fungáčová et al. (Citation2013) who found evidence to show that competition does not increase over time with improvement in banks’ cost efficiency.

Figure 2. Impulse responses to efficiency.

The case is, however, different with competition measured by interest rate spread. Figure ) shows that efficiency is positive and strongly significant to explain interest rate spread as a measure of competition in the banking sector. A downward and gradual decline of interest rate spread in response to a standard deviation efficiency shock was found. This significant and positive relation means that competition increases with efficiency since reduction in net interest margin and/or interest rate spread denotes reduction in market power and increase in competition. This may also speak about changes in lending and deposit rates regulations reacting as efficiency of banks changes. The response steadily declines till period 4 where it experiences a sudden surge that results in a steep slope that becomes normal in period 5 and then the gradual decline continues. This result was found to be consistent with the recent findings of Apriadi et al. (Citation2016) who showed evidence that efficiency negatively Granger causes banking concentration. Thus, it indicates a positive response of competition to an efficient banking system since reduction in concentration is competition. Figure ) again establishes the existence of short-term relationship between bank efficiency and bank stability. Stability responds positively and significantly to a standard deviation efficiency innovation. This is consistent with Apriadi et al. (Citation2016) who found a positive relationship between efficiency and stability. The response as shown in the graph declines steadily over time but positive and significant over the periods. Efficiency has been argued to influence the stability of banks in competition in the efficiency and stability literature (Petersen & Rajan, Citation1995; Williams, Citation2004). Therefore, this provides evidence to underscore the importance of efficiency in banks in relation to stability especially in the short term which will be of tremendous implication for policy development in this area.

4.2. Variance decomposition

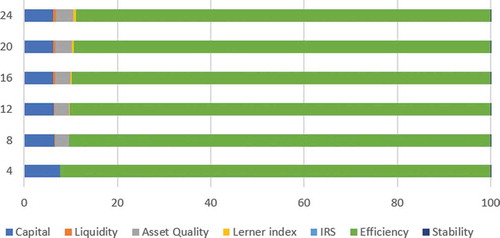

With the variance decomposition, the extent to which regulation, competition and stability variables explain the variation in bank efficiency can be determined (see Ziegel & Enders, Citation1995). The extract is presented in Table . This table reveals the shocks in capital, asset quality, Lerner index and liquidity to have the most direct impacts on the changes in the efficiency of banks. Notably, interest rate spread and stability least affect it and with their effect transmitted through the other variables.

Table 4. Variance decomposition of efficiency

Figure 3. Efficiency variance decomposition bar chart.

Innovation in capital has an average of 6.5% impact on the changes in efficiency over the periods. Specifically, 7.69%, 6.55%, 6.33%, 6.24%, 6.19% and 6.17% by the end of periods 4, 8, 12, 16, 20 and 24. The impact of shocks in asset quality is significant after the 4th period when it is near zero to 2.917%, 3.048%, 3.400%, 3.566% and 3.683% and thereafter to the end of 24th period. Again, the impact of shocks in the Lerner index becomes obvious from the 12th period with 0.116%, 0.233%, 0.392% and 0.583% by the end of period 24 in that order. In like manner, shocks of liquidity to changes in efficiency become pronounced from the end of period 12 at 0.197%, 0.349%, 0.489% and 0.605% by the end of the 16th, 20th and 24th period, respectively. The impact of interest rate spread is almost negligible with an average of 0.005% while stability average about 0.02% beyond the end of period 4. The variations in bank efficiency are, therefore, explained mainly by the shocks in the VAR system rather than variables that are exogenous to it. These are shown pictorally in Figure below.

4.3. Inference discussion of findings

Expectedly, efficiency in Figure ) responds significantly negatively to the measure of competition, the Lerner index, sometimes in the future, suggesting a direct relationship between competition and efficiency. The result suggests a declining efficiency in the future with a standard deviation Lerner index innovation. A competitive banking environment is, therefore, expected to engender an efficient system which according to Petersen and Rajan (Citation1995), among others, should support better loan administration, hence a more responsive and resilient banking system. It also provides an affirmation to the findings of Akande and Kwenda (Citation2017a) of an increase in efficiency with competition, as such could conclude that competition is good for the banking sector of SSA efficiency. But the Lerner index does not respond significantly to shocks in efficiency as shown in Figure ) ruling out the possibility of a reverse causality in the short term. The result, however, differs significantly when competition measured by interest rate spread that reflects the presence of relative market power was considered as shown in Figure ). While efficiency does not respond to interest rate spread, interest rate spread does respond positively and significantly to one standard deviation shock in efficiency as seen in Figure ). Hence, it is consistent with the ESH of Demsetz (Citation1973) who argued efficiency precedes market power in the banking system because a more efficient bank is able to operate at lower cost and better able to acquire more market share resulting in higher market power.

From the foregoing, one can infer a vicious cycle of a market system where competition leads to efficiency and efficiency resulting in market power. The ESH argued that as competitive banks become more efficient, they gain market power which may eventually result in monopoly rent, giving banks the ability to charge high uncompetitive market prices. According to the Austrian school, the monopoly rent is only temporary as new bank entrants that are rent seeking will erode the abnormal profit and/or market power such that the banking system becomes competitive again. However, there is the danger that the presence of entry and exit cost in the banking system may invalidate the Austrian school arguments; therefore, unless policy-makers and regulators alike monitor and moderate the market process, the monopoly rents may continue unabated. This could be exacerbated by the fact that competition does not apply to the banking system as it does in other conventional industries because of certain fundamentals such as information asymmetry, moral hazard and adverse selection that meant that a certain level of market power is desirable within the banking system. The evidence, therefore, should guide regulators in determining the balance between what is a competitive banking and the level of market power desired at least over the next 24 periods in the banking sectors of the SSA region.

In Figures ) and ) are the responses of efficiency to bank stability and stability to efficiency. While efficiency does not significantly respond to stability of the banking system, stability on it part significantly and positively responds to efficiency. Tied to the results of competition and efficiency above, a link among competition, efficiency and stability was found, suggesting a possible mediation by efficiency in competition and stability relationship. Our results show that efficiency responds to competition and stability responds to efficiency. In other words, competition causes efficiency and efficiency causes stability, providing support for these relationships that have been subject of debates in the literature (see Akande & Kwenda, Citation2017a; Schaeck & Cihák, Citation2014; among others).

Finally, efficiency responds positively and significantly to a standard shock in all the regulatory variables, that is, capital, liquidity and asset quality regulation. As hypothesised, this study expects these variables to affect efficiency given their influence on competition and stability of banks. Knowing that efficiency will improve with well-crafted regulations makes our findings unique and a significant contribution to banking literature. The result is consistent with the logic that regulation is not only directly related to efficiency as in this result, but it is also indirectly related via competition. The role of regulation in the banking system is further re-emphasised by these findings. The policy implication for the efficiency of the banking system is that regulation and competition must be closely paid attention to, as both influence efficiency which is germane to the continued stability of the banking system.

4.4. Robustness check

The analysis of the annual data used in this study were carried out with both static (pooled OLS, fixed effect, and random effect models) and dynamic models (GMM) and the results presented in columns 1–4, respectively, of Table . The essence was to help validate the results of the P-SVAR analysis supra and to provide evidence to substantiate the robustness of the results even in the long term. The focus of this analysis was on the GMM, but the static models results were also provided for further robustness purpose. The GMM results based on the robust corrected standard error provide results that are in most cases consistent with P-SVAR results. For instance, Lerner is shown to relate negatively to efficiency (and consistent with the static models), implying that increase in market power will reduce efficiency or increase in competition will increase efficiency. Similarly, the regulatory variables under the GMM model are all significant and with signs consistent with the P-SVAR models apart from capital (ECR) with a negative sign which may be unconnected with the declining responses of efficiency to capital regulation in Figure ). Overall, the diagnostics carried out on the P-SVAR all cumulatively enhanced the robustness of the results.

Table 5. Static and dynamic panel regressions

5. Summary and conclusion

This study analysed efficiency in the SSA region commercial banks in the light of regulation, competition and stability. Based on the theory of the perceived transmissions among these variables, the study fitted a seven-variable P-SVAR to gauge the response of efficiency to and from competition, regulation and stability proxy variables. The essence is finding a way to better enhance an efficient SSA region banking system that could be encouraged to support the right financial intermediation that will drive the much-anticipated development of the region.

The findings reveal that efficiency is central to competition, regulation and stability relationships. Competition was found to cause efficiency, while efficiency causes stability. The result further shows that efficiency causes bank market power suggesting a vicious cycle of competition to efficiency to market power back to competition giving credence to the Austrian school arguments on monopoly rents but with a caution. Furthermore, a direct relationship among capital, liquidity and asset quality regulation variables and efficiency was found, which also infers an indirect relationship between regulation and efficiency via competition. This study, therefore, concludes that competition and regulation matter for efficiency, as efficiency matters for bank market power and bank stability. Hence, to maintain an ongoing efficient banking system in the region, regulation and competition must be adequately enhanced through competition monitoring and moderation as well as continuous review of regulatory frameworks that enhances capital, liquidity and the quality of banks’ assets. One major limitation of this study is that it did not consider regulations that deal with banks ways of doing business, such as activity restrictions, supervision, corporate governance, among others, and so call future research to explore how these affects the efficiency of the banking system.

Additional information

Funding

Notes on contributors

Joseph Olorunfemi Akande

Joseph Olorunfemi Akande is an emerging researcher. He holds a PhD in Finance from the University of KwaZulu-Natal, South Africa, and a member of the Macroeconomic Working Group of the School of Accounting, Economic and Finance of the University. His current research interests, among others, include improving the banking environment in Africa for better management to enable it contribute to the developmental aspirations of the region. He is also exploring the bigger picture of financial stability in the region. His academic experiences span over 10 years lecturing at the Department of Accounting, University of Jos, Nigeria.

Notes

1. A bank-based financial system is one that has dominance of banking system. An economy requires a well-developed capital and money markets for an inclusive financial system.

2. Fu, Lin, and Molyneux (Citation2014).

3. The annual data transformed to higher frequencies of quarterly data following Ngalawa and Viegi (Citation2011) and Borys, Horv´Ath, and Franta (Citation2009), among others.

References

- Abdelkader, I. B., & Mansouri, F. (2013). Competitive conditions of the Tunisian banking industry: An application of the Panzar–Rosse model. African Development Review, 25(4), 526–536. doi:10.1111/afdr.v25.4

- Agoraki, M.-E. K., Delis, M. D., & Pasiouras, F. (2011). Regulations, competition and bank risk-taking in transition countries. Journal of Financial Stability, 7(1), 38–48. doi:10.1016/j.jfs.2009.08.002

- Akande, J. O., & Kwenda, F. (2017a). Does competition cause stability in banks? SFA and GMM application to Sub-Saharan Africa commercial banks. Journal of Economics and Behavioral Studies, 9(4), 173–186. doi: 10.22610/jebs.v9i4.1832

- Akande, J. O., & Kwenda, F. (2017b). P-SVAR analysis of stability in Sub-Saharan African commercial banks. SPOUDAI - Journal of Economics and Business, 67, 3.

- Akins, B., Li, L., Ng, J., & Rusticus, T. O. (2016). Bank competition and financial stability: Evidence from the financial crisis. Journal of Financial and Quantitative Analysis, 51(01), 1–28. doi:10.1017/S0022109016000090

- Amisano, G., & Giannini, C. (1997). Topics in structural VAR econometrics. Berlin Heidelberg: Springer. doi: 10.1007/978-3-642-60623-6

- Apriadi, I., Sembel, R., Santosa, P. W., & Firdaus, M. (2016). Banking fragility in Indonesia: A panel vector autoregression approach. IJABER, 14(14), 10493–10524.

- Ariss, R. T. (2010). On the implications of market power in banking: Evidence from developing countries. Journal of Banking & Finance, 34(4), 765–775. doi:10.1016/j.jbankfin.2009.09.004

- Barro, J., & Barro, R. (1990). Pay, performance, and turnover of bank CEOs (Tech. Rep.). doi: 10.3386/w3262

- Battese, G. E., & Coelli, T. J. (1992). Frontier production functions, technical efficiency and panel data: With application to paddy farmers in India. In International applications of productivity and efficiency analysis (pp. 149–165). Springer.

- Berger, A. N. (1995). The relationship between capital and earnings in banking. Journal of Money, Credit and Banking, 27(2), 432–456. doi:10.2307/2077877

- Berger, A. N., Klapper, L. F., & Turk-Ariss, R. (2009). Bank competition and financial stability. Journal of Financial Services Research, 35(2), 99–118. doi:10.1007/s10693-008-0050-7

- Berger, A. N., & Mester, L. J. (1997). Inside the black box: What explains differences in the efficiencies of financial institutions? Journal of Banking & Finance, 21(7), 895–947. doi:10.1016/S0378-4266(97)00010-1

- Boot, A., & Schmeits, A. (2006). The competitive challenge in banking. Advances in Corporate Finance and Asset Pricing, 133–160. doi:10.1016/b978-044452723-3/50007-3

- Borys, M. M., Horv´Ath, R., & Franta, M. (2009). The effects of monetary policy in the Czech Republic: An empirical study. Empirica, 36(4), 419–443. doi:10.1007/s10663-009-9102-y

- Canova, F. (2007). Methods for applied macroeconomic research (Vol. 13). New Jersey: Princeton University Press.

- Canova, F., & Ciccarelli, M. (2014). Panel vector autoregressive models: A survey. In Var models in macroeconomics - new developments and applications: Essays in honor of Christopher A. Sims (pp. 205–246). Emerald Group Publishing Limited. doi: 10.1108/s0731-905320130000031006

- Casu, B., & Girardone, C. (2006). Bank competition, concentration and efficiency in the single European market. The Manchester School, 74(4), 441–468. doi:10.1111/manc.2006.74.issue-4

- Casu, B., Girardone, C., & Molyneux, P. (2015). Introduction to banking (Vol. 10). UK: Pearson Education.

- Chiou, W.-J. P., & Porter, R. L. (2015). Does banking capital reduce risk? An application of stochastic frontier analysis and GMM approach. In C. -F. Lee & J. Lee (Eds.), Handbook of financial econometrics and statistics (pp. 349–382). New York: Springer Science & Business Media. doi:10.1007/978-1-4614-7750-1_13.

- Chirwa, E. W. (2003). Determinants of commercial banks’ profitability in Malawi: A cointegration approach. Applied Financial Economics, 13(8), 565–571. doi:10.1080/0960310022000020933

- Chudik, A., & Pesaran, M. H. (2013). Large panel data models with cross-sectional dependence: A survey. SSRN Electronic Journal. doi: 10.2139/ssrn.2316333

- Cihak, M., Demirgu¨c¸-Kunt, A., Mart´Inez Per´Ia, M. S., & Mohseni-Cheraghlou, A. (2012). Bank regulation and supervision around the world: A crisis update. World Bank Policy Research Working Paper (6286).

- Coelli, T. J., & Rao, D. (1998). An introduction to efficiency and productivity analysis. New York: Springer-Verlag. doi: 10.1007/b136381

- Coelli, T. J., Rao, D. S. P., O’Donnell, C. J., & Battese, G. E. (2005). An introduction to efficiency and productivity analysis. New York: Springer Science & Business Media.

- Davoodi, H. R., Dixit, S. V. S., & Pinter, G. (2013). Monetary transmission mechanism in the East African Community: An empirical investigation. IMF Working Papers, 13(39), 1. doi: 10.5089/9781475530575.001

- Demirguc-Kunt, A., Laeven, L., & Levine, R. (2003). Regulations, market structure, institutions, and the cost of financial intermediation (Tech. Rep.). National Bureau of Economic Research.

- Demsetz, H. (1973). Industry structure, market rivalry, and public policy. The Journal of Law & Economics, 16(1), 1–9. doi:10.1086/466752

- Evanoff, D., & Ors, E. (2002). Local market consolidation and bank productive efficiency. SSRN Electronic Journal. Elsevier (BV). doi:10.1044/1059-0889(2002/er01)

- Freixas, X., & Rochet, J.-C. (2008). Microeconomics of banking (Vol. 2). Cambridge, MA: MIT press.

- Fu, X. M., Lin, Y. R., & Molyneux, P. (2014). Bank competition and financial stability in Asia Pacific. Journal of Banking & Finance, 38, 64–77. doi:10.1016/j.jbankfin.2013.09.012

- Fungáčová, Z., Pessarossi, P., & Weill, L. (2013). Is bank competition detrimental to efficiency? Evidence from China. China Economic Review, 27, 121–134. doi:10.1016/j.chieco.2013.09.004

- Glynn, J., Perera, N., & Verma, R. (2007). Unit root tests and structural breaks: A survey with applications. Revista de Mtodos Cuantitativos para la Economa y la Empresa, (3), 63–79. Retrieved fromhttp://google.redalyc.org/articulo.oa?id=233117245004

- Graeve, F. D., & Karas, A. (2010). Identifying VARs through heterogeneity: An application to bank runs. SSRN Electronic Journal. doi: 10.2139/ssrn.1710544

- Hicks, J. R. (1935). Annual survey of economic theory: The theory of monopoly. Econometrica: Journal of the Econometric Society, 1–20. doi:10.2307/1907343

- Hussain, M. E., & Hassan, M. K. (2012). Competition, risk taking and efficiency in the US commercial banks prior to 2008 financial crisis. Available at SSRN 2003066.

- Jim´Enez, G., Lopez, J. A., & Saurina, J. (2013). How does competition affect bank risk-taking? Journal of Financial Stability, 9(2), 185–195. doi:10.1016/j.jfs.2013.02.004

- Koopmans, T. C. (1951), An analysis of production as an efficient combination of activities. In T. C. Koopmans (Ed.), Activity analysis of production and allocation, Proceeding of a conference (pp. 33-97). London: John Wiley and Sons Inc.

- Kouki, I., & Al-Nasser, A. (2014). The implication of banking competition: Evidence from African countries. Research in International Business and Finance, 39, 878–895. doi: 10.1016/j.ribaf.2014.09.009

- Kumbhakar, S. C., & Lovell, C. K. (2003). Stochastic frontier analysis. Cambridge: Cambridge University Press.

- Kutu, A. A., & Ngalawa, H. (2016). Monetary policy shocks and industrial output in BRICS countries. SPOUDAI-Journal of Economics and Business, 66(3), 3–24.

- Laeven, L., & Levine, R. (2009). Bank governance, regulation and risk taking. Journal of Financial Economics, 93(2), 259–275. doi:10.1016/j.jfineco.2008.09.003

- Laeven, L., & Majnoni, G. (2005). Does judicial efficiency lower the cost of credit? Journal of Banking & Finance, 29(7), 1791–1812. doi:10.1016/j.jbankfin.2004.06.036

- Lepetit, L., & Strobel, F. (2013). Bank insolvency risk and time-varying z-score measures. Journal of International Financial Markets, Institutions and Money, 25, 73–87. doi:10.1016/j.intfin.2013.01.004

- Liu, H., Molyneux, P., & Wilson, J. O. (2013). Competition and stability in European banking: A regional analysis. The Manchester School, 81(2), 176–201. doi:10.1111/manc.2013.81.issue-2

- Llewellyn, D. (1999). The economic rationale for financial regulation. London: Financial Services Authority.

- Matutes, C., & Vives, X. (2000). Imperfect competition, risk taking, and regulation in banking. European Economic Review, 44(1), 1–34. doi:10.1016/S0014-2921(98)00057-9

- Mlachila, M., Park, S. G., & Yabara, M. (2013). Banking in Sub-Saharan Africa: The macroeconomic context (Vol. 7; Tech. Rep). European Investment Bank (EIB). Retrieved from http://hdl.handle.net/10419/88938

- Moyo, J., Nandwa, B., Council, D. E., Oduor, J., & Simpasa, A. (2014). Financial sector reforms, competition and banking system stability in Sub-Saharan Africa. New Perspectives. Retrieved from academia.edu

- Mugume, A. (2008). Market structure and performance in Uganda’s banking industry. African Econometrics Society. Retrieved from pdfs.semanticscholar.org

- Ngalawa, H., & Viegi, N. (2011). Dynamic effects of monetary policy shocks in Malawi. South African Journal of Economics, 79(3), 224–250. doi:10.1111/j.1813-6982.2011.01284.x

- Nyong, M. (1999). Market structure, conduct and performance in the Nigerian banking industry: New evidence, new insights. Nigeria Deposit Insurance Corporation Quarterly.

- Pagano, M. (1993). Financial markets and growth: An overview. European Economic Review, 37(2–3), 613–622. doi:10.1016/0014-2921(93)90051-B

- Petersen, M. A., & Rajan, R. G. (1995). The effect of credit market competition on lending relationships. The Quarterly Journal of Economics, 110(2), 407–443. doi:10.2307/2118445

- Raghavan, M., & Silvapulle, P. (2008). Structural var approach to Malaysian monetary policy framework: Evidence from the pre-and post-Asian crisis periods. In New Zealand Association of Economics, NZAE Conference (pp. 1–32).

- Ramaswamy, R., & Slœk, T. (1998). The real effects of monetary policy in the European union: What are the differences? Staff Papers, 45(2), 374–396. doi:10.2307/3867394

- Repullo, R. (2004). Capital requirements, market power, and risk-taking in banking. Journal of Financial Intermediation, 13(2), 156–182. doi:10.1016/j.jfi.2003.08.005

- Roy, A. D. (1952). Safety first and the holding of assets. Econometrica: Journal of the Econometric Society, 431–449. doi:10.2307/1907413

- Schaeck, K., & Cihák, M. (2014). Competition, efficiency, and stability in banking. Financial Management, 43(1), 215–241. doi:10.1111/fima.12010

- Shepherd, W. G. (1983). Economies of scale and monopoly profits. In John V. Craven (Ed.), Industrial organization, antitrust, and public policy (pp. 165–204). Springer.

- Smirlock, M., Gilligan, T., & Marshall, W. (1986). Tobin’s q and the structure-performance relationship: Reply. The American Economic Review, 76(5), 1211–1213.

- Soedarmono, W., Machrouh, F., & Tarazi, A. (2013). Bank competition, crisis and risk taking: Evidence from emerging markets in Asia. Journal of International Financial Markets, Institutions and Money, 23, 196–221. doi:10.1016/j.intfin.2012.09.009

- Stock, J. H., & Watson, M. (2007). Introduction to econometrics. Boston: Pearson Education Inc.

- Vander Vennet, R. (2002). Cost and profit efficiency of financial conglomerates and universal banks in Europe. Journal of Money, Credit, and Banking, 34(1), 254–282. doi:10.1353/mcb.2002.0036

- Williams, J. (2004). Determining management behaviour in European banking. Journal of Banking & Finance, 28(10), 2427–2460. doi:10.1016/j.jbankfin.2003.09.010

- Ziegel, E. R., & Enders, W. (1995). Applied econometric time series. Technometrics, 37(4), 469. doi: 10.2307/1269759